Category: News

The Democrats Are About To Destroy John Fetterman

The Democrats Are About To Destroy John Fetterman

John Fetterman has become the most interesting politician in America, and the Democratic Party’s most uncomfortable mirror. His willingness to speak honestly, vote his conscience, and refuse to define himself purely in opposition to President Donald Trump has made him a hero to some and a traitor to others.

Back in March, he declared the party had no real leader except Trump Derangement Syndrome. Democrats, according to Fetterman, are so consumed with opposing President Donald Trump that they’ve failed to construct a coherent agenda of their own. That’s not a fringe critique. It’s a fairly accurate description of where the opposition party stands as we head toward the 2026 midterms.

Last week, Sen. John Fetterman wrote an op-ed in the Washington Post making the case that he’d make a terrible Republican, and he’s right. He’s pro-choice, firmly behind legal marijuana, a committed supporter of LGBT rights, a staunch defender of SNAP benefits, and a reliable friend to organized labor. His overall voting record is overwhelmingly aligned with the Democratic caucus.

“It wasn’t long ago when Democrats wanted a secure border. I voted on an immigration bill in 2024 to make sure an influx the size of Pittsburgh doesn’t come through the border like it did under the previous administration,” he wrote. “I have co-sponsored legislation to stop the flow of fentanyl. I was the lead Democrat on the Laken Riley Act, and I strongly believe that someone who comes here illegally and commits a violent crime should be deported. Full stop.”

He noted how his party used to oppose government shutdowns because they put “American livelihoods at risk” and held workers “hostage.” Yet, he stood alone as a Democrat when he voted to end his party’s recent shutdowns, saying he “took no pleasure in voting against my party” but felt that keeping “the lights on” for TSA, homeland security, airports, and “everyday Americans” mattered more than “partisan games.”

As far as he’s concerned, his occasional departures on border security, crime, and Israel are a sign of his party becoming more extreme, not him becoming more conservative.

In a recent conversation on Reason’s Reason Interview podcast with Nick Gillespie, Fetterman was asked to reflect on how his politics had changed since he backed Bernie Sanders in 2016. His answer cut to the heart of the Democratic Party’s ongoing identity crisis. “Well, I mean, you know, in 2016, it was much more about the minimum wage and some other very basic kinds of things,” he said. “And now that’s just turned into much more standing with Cuba, standing with Venezuela, standing with the Iranian regime, and turned that into much more becoming more increasingly anti-American for me. So my views really haven’t changed that much.” The punchline came shortly after: “What’s really changed is the party.“

That is a sitting Democratic senator describing his own party’s base as “increasingly anti-American,” and describes himself as lonely inside the party he still agrees with over 90 percent of the time. And how has the party responded to one of its more prominent voices offering this kind of candid self-assessment?

By quietly beginning to show him the door.

A report from Punchbowl News last month made it quite clear how his party sees him. Pennsylvania Democrats on Capitol Hill wouldn’t commit to supporting a Fetterman reelection bid, and none would explicitly endorse him. Rep. Brendan Boyle, who is rumored to be eyeing a 2028 Senate run himself, said he’d “be very surprised if [Fetterman] ran in the Democratic primary.” Rep. Chris Deluzio, also said to be interested in the seat, acknowledged “serious disagreements” with Fetterman over the war in Iran, before adding a diplomatic “we’ll see what comes after ’26.” Rep. Summer Lee simply said of Fetterman seeking reelection, “Up to him. At his own peril.”

That’s the kind of language you use for someone the party has already written off. And clearly they have. He still votes with Democrats more than 90 percent of the time. And yet Pennsylvania Democrats won’t even give him a courtesy endorsement for a future Senate bid.

Democratic voters in Pennsylvania aren’t any more forgiving.

A February Quinnipiac poll found that Fetterman sits at 46 percent approval among Pennsylvania voters overall. This isn’t great, but the partisan breakdown is most interesting: he’s underwater 62%–22% among Democrats, while running 74%–18% among Republicans.

As far as the party’s progressive base goes, anything less than 100% compliance isn’t enough, especially when you break with the party on issues like Israel, immigration, or anything that can be characterized as insufficiently hostile to the right. Fetterman’s independent streak might help him win a general election, but it won’t help him win a Democratic primary.

That’s the trap, and he appears to know it.

He’s made it quite clear he won’t become a Republican. His op-ed was practically a manifesto on the subject. But a man who describes himself as “lonely” inside his own party, who watches that party signal it won’t back him for reelection, has a big decision to make. Will he try to win reelection as a Democrat, become an independent, or not run at all? One thing is for sure: his future inside the Democratic Party is already closed.

Tyler Durden

Tue, 05/19/2026 – 14:40

https://www.zerohedge.com/political/democrats-are-about-destroy-john-fetterman

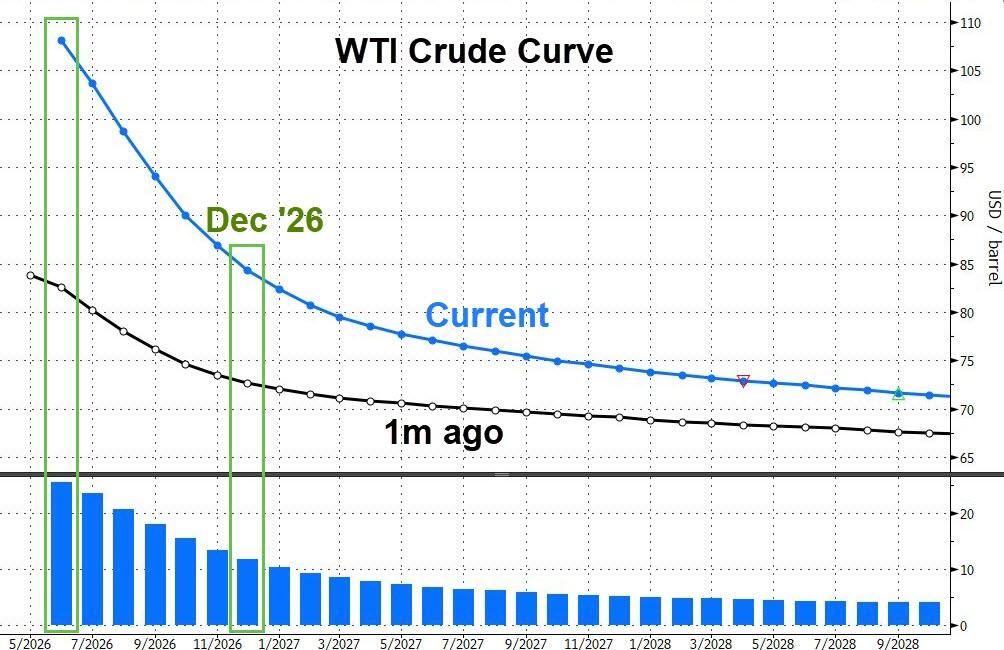

Iran’s Floating Oil Stockpile Jumps 65% As U.S. Naval Blockade Bites

Iran’s Floating Oil Stockpile Jumps 65% As U.S. Naval Blockade Bites

By Charles Kennedy of OilPrice.com

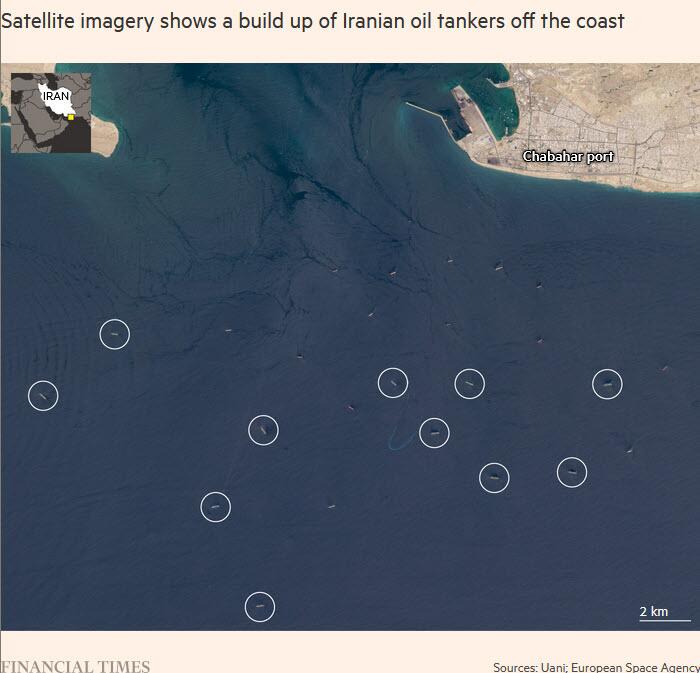

The volumes of Iranian oil stored at tankers in and around the Strait of Hormuz have jumped in recent weeks as Iran considers ways to circumvent the U.S. blockade in the Gulf of Oman aimed at choking Iranian oil exports.

The number of tankers laden with crude but sitting in the Persian Gulf and near the Strait of Hormuz has jumped since the U.S. initiated in the middle of April a naval blockade to prevent Iranian oil exports and force Tehran into a deal, a Financial Times analysis of shipping and satellite imagery data showed on Tuesday.

Data from the U.S.-based non-profit United Against Nuclear Iran (UANI) showed that the number of tankers in the Gulf laden with Iranian crude and petrochemicals has now jumped to 49, up from 29 before the U.S. blockade began on April 13.

Separately, UANI and FT have identified more than a dozen tankers clustered near the Iranian port Chabahar outside the Strait of Hormuz but within the line of the U.S. blockade.

Ship-tracking and maritime intelligence analyses pointed three weeks ago that Iranian tankers laden with oil were loitering in a cluster near the port of Chabahar. The cluster signals that Iran continues to load oil on Iranian tankers that are trying to leave the Middle East region. On the other hand, the piling up of ships outside the Strait of Hormuz but inside the U.S. blockade line suggests that the American interception of vessels is working.

Tanker Tally at Iran’s Kharg Island Hits Post-Blockade Peak: BBG

Running out of tankers to store oil.

— zerohedge (@zerohedge) May 18, 2026

About 42 million barrels of Iranian crude are now sitting on Iranian tankers, many of these old vessels, in the Middle East, a 65% surge compared to the beginning of the war, per Kpler estimates cited by FT.

Loadings at Kharg Island, Iran’s key export port, have come to a standstill, maritime intelligence firm Windward said in a report last week.

“At the same time, dark tanker concentrations across northern Hormuz, eastern Hormuz, and Chabahar indicate that Iran is increasingly relying on protected holding zones to buffer export capacity and manage outbound flows,” Windward’s analysts said.

“Persistent ship-to-ship transfer activity, bunkering operations, and prolonged dark anchorage behavior reinforce indications that covert cargo-transfer and sanctions evasion operations are expanding inside Iranian territorial waters.”

Tyler Durden

Tue, 05/19/2026 – 14:20

https://www.zerohedge.com/markets/irans-floating-oil-stockpile-jumps-65-us-naval-blockade-bites

Iran Now Has More Incentive To Resist US Demands, Even If War Restarts: Israeli Think Tank

Iran Now Has More Incentive To Resist US Demands, Even If War Restarts: Israeli Think Tank

At this point even hawkish Israeli think tank pundits are increasingly admitting that Iran currently has certain leverage and an edge when it comes to dealing with the United States, and the so far stalled and failed peace talks to end the war.

President Trump has just described that he called off planned renewed airstrikes on Iran, at the request of Gulf allies – who claim efforts toward getting back to the table and reaching a deal are close, despite that Iran’s position on its nuclear program has not budged.

When the White House first initiated Operation Epic Fury, it was hyped as presenting the opportunity for a clean tactical victory likely to result in swift regime change (Venezuela-style); however, it has officially morphed into yet another classic, grinding Washington Mideast dilemma – just as critics loudly warned would happen.

President Trump now finds himself boxed into a high-stakes corner with no easy exit ramp in sight – he can appear ‘weak’ through inaction, or pursue escalation and potential quagmire with likely disastrous economic and political consequences at home. In such situations each new and ‘next’ military action which gets presented as a ‘way forward’ actually often serves to make a conflict more unpredictable, sinking the US into a deeper escalation trap.

And now enter aforementioned Israeli think tank hawks. Raz Zimmt, the Director of the Iran and the Shiite Axis program at the Israel-based Institute for National Security Studies (INSS), has pointed out that Trump’s pull-back from ‘planned’ new airstrikes will leave Tehran leaders with some clear conclusions. It should be remembered that the INSS, which is affiliated with Tel Aviv University, is Israel’s most premier defense establishment think tank.

“Whether or not it was indeed requested to do so by the rulers of the Gulf states, Tehran draws two main conclusions this morning from the president’s statement,” Zimmt, whose work is often promoted by Axios Barak Ravid, began in a thread on X (machine translated).

Here’s how the Israel-based pundit lays it out (emphasis ZH):

A. It has once again been proven that Trump is not interested in war. From Tehran’s perspective, this does not mean there will be no war, and therefore it is preparing for a resumption of hostilities. However, this strengthens its perception that the fear in the US and the Gulf of the consequences of renewing the campaign outweighs the fear in Iran.

B. It is impossible (and this too, of course, is not a new insight in Tehran) to rely on any word coming from Trump’s mouth or keyboard in his endless frenzy. Therefore, not only must it refrain from agreeing to concessions that amount to capitulation to US demands—for example, forgoing nuclear capabilities, such as enrichment infrastructure, and not just the products of the program, such as uranium enriched to 60%—but it must continue to insist, already in the first stage, on security and economic guarantees: a complete end to the war, easing of sanctions or unfreezing of frozen Iranian assets, and management arrangements in the Strait of Hormuz that express recognition of Iran’s control over the strait. And the problem is that it is doubtful whether this perception will change even in a scenario of renewed hostilities, unless a way is found to incorporate within its framework an action or actions that succeed in denying or significantly weakening one of the two cards in Iran’s hand: control of Hormuz and the nuclear assets.

President Trump on Monday actually said “hopefully, maybe forever” when asked about the decision to delay the Iran attack. This was certainly not missed in Tehran.

A Trump-Iran pattern?

• Wed: Iran wants a deal. They called us

• Thu: We are looking at proposals

• Fri: We might be close. Very close

• Sat.: Iran knows what to do

• Sun: OBLITERATION. TOTAL. COMPLETE. They have 24 hrs.

• Mon. : The storm is coming

• Tue.: I’m giving it…

— Joyce Karam (@Joyce_Karam) May 18, 2026

Meanwhile, as of Tuesday Reuters is reporting that the five key elements of Iran’s new proposal to the US to end the war include the following:

US troops leaving areas close to Iran

The US paying war reparations

Lifting sanctions on Iran

Release Iran’s frozen assets

Ending the US blockade

And so both sides continue to insist on not moving away from their initial demands and conditions, with barely any compromise visible, in a perpetuation of the zero sum game and standoff, also as the Hormuz Strait continues to be de facto blocked to the vast majority of maritime transit.

* * *

Latest Tuesday developments via Newsquawk…

US President Trump posted on Truth that he instructed Secretary of War Hegseth, Joint Chiefs of Staff Chairman Caine and the US military to hold off on the Iran attack that was initially planned for Tuesday after Saudi Arabia, UAE and Qatar requested him to do so, as serious talks are now taking place. Trump added that in their opinion, a deal will be made that is very acceptable to the US and the Middle East, while a deal will include no nuclear weapons for Iran, but he also instructed the US to be prepared to go forward with a full, large-scale assault of Iran on a moment’s notice, in the event an acceptable deal is not reached.

US President Trump said ‘hopefully, maybe forever’ regarding the decision to delay the Iran attack, while he added that they will probably be satisfied if they can make a deal where Iran doesn’t get a nuclear weapon. Trump also stated that countries requested to put off the attack on Iran briefly and asked if an attack on Iran could be delayed 2-3 days.

US President Trump told The Post on Monday that he is “not open” to any concessions for Tehran after receiving the latest disappointing Iranian response on peace deal talks, while he said Iran knows “what’s going to be happening soon.”

US State Department spokesperson said President Trump prefers the diplomatic path and has kept this door open from the start, according to Al Jazeera.

Iran’s Deputy Foreign Minister said ending the war on all fronts, including Lebanon, and US forces exiting areas close to Iran are also included in the proposal.

Iranian Parliament spokesperson said Tehran is working on a legal framework for managing the Strait of Hormuz, Al Araby reported.

US officials told the NYT that Iran has taken advantage of the ceasefire to re-expose dozens of bombed ballistic missile sites, move mobile missile launchers, and adjust its tactics in anticipation of a possible resumption of attacks, according to Amichai Stein.

Iran’s Khatam al-Anbiya headquarters commander warned the US and its allies against strategic mistakes, while he said Iran’s forces have become ready and will respond quickly and firmly to any new aggression from the enemies.

Iranian Supreme Leader’s military advisor Rezaei said the iron fist of Iran’s armed forces and nation will force America to retreat and surrender.

Israeli media said the main reason US President Trump postponed attacks on Iran is the Pentagon’s warning that Iran is strengthening its air defenses, while senior Pentagon officials warned that Iran is enhancing its warplane detection capabilities and bolstering its air defences, according to Al Mayadeen. It was also reported that air defences were activated in Isfahan, according to Mehr News.

Unknown explosions last night in Bab al-Mandeb Strait halted vessel traffic for two hours, Far News reported. Sources cited note of “unusual silence” from global maritime and insurance authorities.

Israeli drone strike was reported in Al-Qarara, Khan Yunis, in the southern Gaza Strip. It was separately reported that Hezbollah announced it attacked Israeli soldiers in the town of Rashaf, southern Lebanon with drones, while the Israeli army issued an evacuation warning for a building in the city of Tyre, southern Lebanon.

Tyler Durden

Tue, 05/19/2026 – 13:20

New York Governor Signs Bills To Preserve Mandatory Vaccines

New York Governor Signs Bills To Preserve Mandatory Vaccines

Authored by Zachary Stieber via The Epoch Times,

New York Gov. Kathy Hochul has signed legislation to preserve vaccine requirements for children.

Hochul, on May 15, signed two bills that decouple New York’s vaccine requirements from the federal government, after the Trump administration rolled back recommendations for hepatitis B and other vaccines.

“When public health comes under attack by an anti-science administration, New York fights back,” Hochul, a Democrat, said in a statement.

She added that the legislation “protects access to lifesaving vaccines for New Yorkers of all ages.”

One bill, Assembly Bill 10711, removes language about vaccines needing to be approved by federal regulators. Instead, it says that children must receive vaccines against measles, hepatitis B, and other diseases “in accordance with regulations issued by the commissioner of health of New York.”

Assembly Bill 10710, the other piece of legislation, requires health insurers to cover vaccines recommended by New York’s health commissioner, even if the shots are not recommended by the federal Centers for Disease Control and Prevention.

New York has, in the past, only mandated vaccines approved and recommended by federal health agencies.

“Vaccines remain one of the greatest public health tools in history, protecting individuals, families, and entire communities from serious and preventable diseases,” New York Health Commissioner Dr. James McDonald said in a statement.

“At a time when misinformation is undermining confidence in science, this legislation reinforces New York State’s commitment to following trusted medical guidance and keeping New Yorkers healthy.”

The Trump administration has narrowed its recommendations for vaccines against several diseases, including COVID-19, hepatitis B, and rotavirus.

The biggest changes came after President Donald Trump issued an order directing officials to review recommendations from other countries and update U.S. recommendations as appropriate in light of the results of the review.

A federal judge in mid-March blocked the updates, concluding that officials did not follow proper procedure when altering the vaccine recommendations.

The Trump administration has appealed.

New York Democratic lawmakers who authored or voted for the bills Hochul signed hailed the development.

“In an era where federal health officials are undermining scientific integrity and sowing skepticism about lifesaving vaccines, New York is making the conscious choice to champion our medical professionals and reaffirm this state’s commitment to the evidence-based practices that have safeguarded communities for generations,” New York Senate Majority Leader Andrea Stewart-Cousins said in a statement.

Children’s Health Defense, an organization founded by Health Secretary Robert F. Kennedy Jr., was among the groups that opposed the legislation.

Michael Kane, director of advocacy for Children’s Health Defense, told The Epoch Times previously that one of the bills would enable the state to require experimental vaccines, as it removed language stating that vaccines needed federal approval.

“It would also allow for foreign entities to determine what vaccines our children must take,” Kane said.

Tyler Durden

Tue, 05/19/2026 – 13:00

https://www.zerohedge.com/political/new-york-governor-signs-bills-preserve-mandatory-vaccines

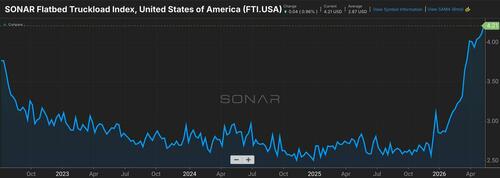

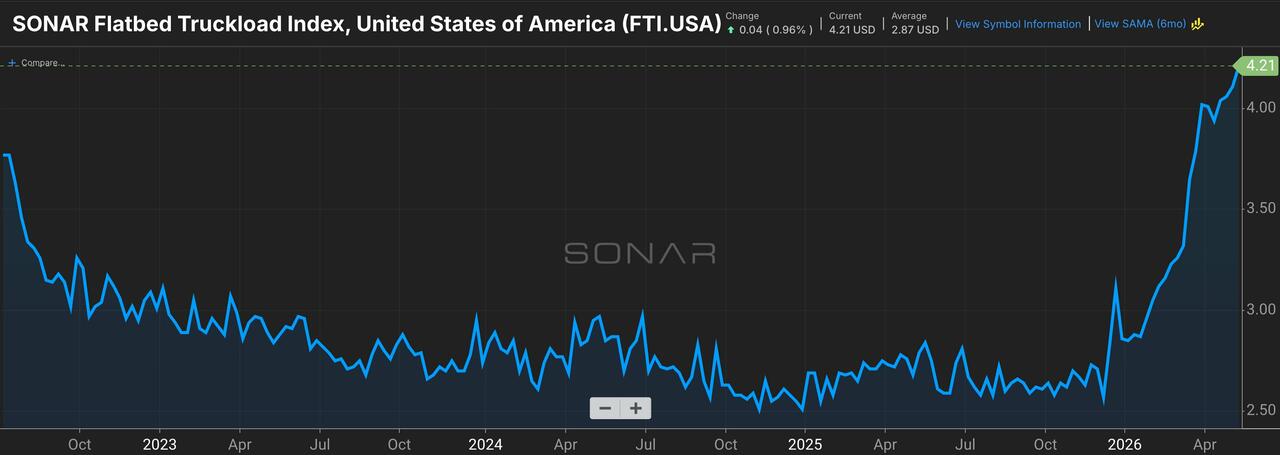

Flatbed Truck Rates Hit New Highs As These Drivers Fuel Boom

Flatbed Truck Rates Hit New Highs As These Drivers Fuel Boom

Flatbed trucking conditions have never looked stronger, with spot rates surging to record highs amid a mix of tightening capacity and rising industrial freight demand.

“Flatbed trucking rates have hit a new all-time high as industrial demand and a crackdown on bad actors continue to shape trucking economics,” said FreightWaves founder Craig Fuller.

Fuller added, “It is a great time to be a compliant trucker in America.”

There are two drivers behind why U.S. flatbed spot trucking rates (via SONAR Flatbed Truckload Index) have surged to $4.21 per mile, well above the index’s $2.87 average and to record highs:

Data center and AI infrastructure boom, which is driving higher volumes of steel, transformers, generators, construction materials, and other open-deck freight;

And the crackdown on foreign truck drivers, which is shrinking the available labor pool and tightening capacity further, is creating a more favorable pricing backdrop for American owner-operators.

Last week, the U.S. Supreme Court ruled that freight brokers now face state-law negligent hiring claims when they hire unsafe trucking firms that later cause crashes. This came after a series of deadly crashes nationwide, with some of these drivers being illegal aliens who were unable to read English.

BREAKING: 3 kiIIed in California by an illegal alien truck driver, Jashanpreet Singh. Singh entered in 2022, was released by Biden.

— End Wokeness (@EndWokeness) October 23, 2025

There are reports that freight brokers are no longer hiring foreign truck drivers.

It took less than 24 hours for brokers to tighten the belt after the Supreme Court ruled that brokers could be held liable for carrier accidents WOW!

#Truckers #trucking #truckinglife @topfans pic.twitter.com/MEnvzcKkar

— GRANDPA’s FREE ADVICE (@GOP_is_Gutless) May 16, 2026

The combination of surging industrial demand and the reduction in foreign drivers is finally driving higher rates after mom-and-pop American truckers endured years of overcapacity that pushed rates to nearly unaffordable levels.

Tyler Durden

Tue, 05/19/2026 – 12:40

https://www.zerohedge.com/markets/flatbed-truck-rates-hit-new-highs-these-drivers-fuel-boom

US Dept Of War Suspends Permanent Joint Board On Defense With Canada

US Dept Of War Suspends Permanent Joint Board On Defense With Canada

Authored by ‘sundance’ via The Last Refuge,

Remarkably, many news articles are citing confusion in trying to understand why U.S. Undersecretary of War, Elbridge Colby, announced the suspension of U.S. participation in the Permanent Joint Board on Defense with Canada.

However, the announcement comes immediately after his meeting with U.S. ambassador to Canada, Pete Hoekstra, at the Pentagon and the comment, “we’re working closely to ensure every NATO partner, including Canada, reaches the Hague Summit’s 3.5% GDP defense spending target, a vital investment for North American and Arctic defense.”

The issue, as outlined by Undersecretary Colby, centers around Prime Minister Mark Carney’s recent statements in antagonism toward the U.S., a public announcement that Canada would not be purchasing U.S. military equipment and the biggest issue of all, that Canada is not living up to the NATO defense spending agreements.

It was in December of 2024, immediately after the November election where Donald Trump won, when then Prime Minister Justin Trudeau flew to Mar-a-Lago for dinner with President Trump and told him there’s no way that Canada could meet their NATO obligations.

Canada had relied on the USA to provide all national defense and was 16th in defense spending at 1.1% of GDP. {CITATION}

The issue of NATO compliance was part of a larger discussion around trade imbalances, non-tariff barriers, intellectual property conflicts and legislative hurdles that Canada used as a crutch to retain economic benefit without reciprocity.

Trudeau was arguing that Canada could not change all the points of conflict, drop their non-tariff barriers, comply with NATO demands and simultaneously get into total alignment with the USMCA trade compact (CUSMA to Canada), because their climate policies did not support or match the heavy industrial processing capabilities of both the United States and Mexico.

This triggered President Trump to respond with the 51st state, notation.

Essentially, if you cannot be a partner with equal capabilities; and if you need to retain structural economic dependency; then Canada should just become a 51st state of the USA.

Since that time, things went downhill quickly. Instead of trying to find ways to eliminate points of conflict, Prime Minister Mark Carney began a campaign of aggressive anti-Trump narrative distribution in order to maximize domestic political benefits.

President Trump then turned toward Mexico and began working with USTR Jamieson Greer to construct what is essentially a bilateral trade agreement between the U.S. and Mexico.

The administration began ignoring Canada, planning instead to announce the upcoming dissolution of the USMCA and then force Canada to negotiate a bilateral. A jilted Canada then began doubling and tripling down on the anti-Trumpism, with Carney saying the era of trade between the USA and Canada is over.

Carney then reached out to Europe and China for trade replacement value and began making announcements about no longer purchasing U.S. manufactured fighter jets and military hardware.

U.S. Undersecretary of War, Elbridge Colby meets with U.S. Ambassador to Canada, Pete Hoekstra, and obviously the NATO stuff is just the straw that ended the U.S. participation in the Permanent Joint Board on Defense with Canada. Not a complicated timeline to figure out.

WASHINGTON – […] “A strong Canada that prioritizes hard power over rhetoric benefits us all,” Colby said.

“Unfortunately, Canada has failed to make credible progress on its defense commitments. DoW is pausing the Permanent Joint Board on Defense to reassess how this forum benefits shared North American defense.

“We can no longer avoid the gaps between rhetoric and reality. Real powers must sustain our rhetoric with shared defense and security responsibilities,” he continued. “Delivering on shared continental defense begins by recognizing our shared geography. Only by investing in our own defense capabilities will Americans and Canadians be safe, secure, and prosperous.”

It’s unclear why Colby made the announcement on Monday, given that Carney’s Davos speech was months ago.

Minutes before the announcement, Colby posted a photograph of himself meeting with the U.S. ambassador to Canada, Pete Hoekstra, at the Pentagon, though he did not specify when the meeting took place.

“We’re working closely to ensure every NATO partner, including Canada, reaches the Hague Summit’s 3.5% GDP defense spending target, a vital investment for North American and Arctic defense,” he wrote along with the photo.

Carney’s relationship with President Donald Trump has fractured in recent months over several different issues, including the former’s address at Davos. (read more)

Every trade and economic associated agency within the Trump administration is in alignment, and the elimination of the USMCA with Canada is clearly at the end of this path.

However, if you can find one in one-hundred Canadians who understand or accept this destination, I would be surprised.

A mass formation psychosis has fallen upon the land of Canada, and the overwhelming majority of Canadians just repeat, “Trump bad.”

It’s weird.

Tyler Durden

Tue, 05/19/2026 – 12:20

https://www.zerohedge.com/geopolitical/us-dept-war-suspends-permanent-joint-board-defense-canada

Nickel Jumps As Indonesian Output Cut Stokes Supply Fears

Nickel Jumps As Indonesian Output Cut Stokes Supply Fears

Nickel prices on the London Metal Exchange surged as much as 2.6% to $19,050 a ton after Shanghai Metals Market said upwards of 15% of high-grade nickel pig iron capacity at Indonesia’s Weda Bay Industrial Park will undergo rotational maintenance in the coming months, according to Bloomberg.

Indonesia’s Weda Bay Industrial Park is one of the most important nickel-processing hubs in the world and serves a large cluster of smelters that produce nickel pig iron, a key input for stainless steel production.

Indonesia dominates global nickel supply, producing 2.6 million metric tons of nickel in 2025 out of a global total of 3.9 million tons, accounting for roughly two-thirds of global mine production.

So, the earlier news from SMM indicating a 10% to 15% reduction in NPI output from Weda Bay Industrial Park in the coming months, building on existing NPI reductions in March and April due to lower ore supplies and high costs, has easily sparked supply concerns on the LME …

Nickel is extremely valuable and a critical industrial metal in the era of electrification and data center buildouts:

Stainless steel, by far the largest demand center, where nickel improves corrosion resistance, strength, and heat tolerance.

EV and energy-storage batteries, especially nickel-rich lithium-ion chemistries that increase energy density and driving range.

Aerospace and military superalloys, including jet-engine turbine blades and high-temperature gas turbines.

Industrial alloys, plating, and catalysts, used across machinery, chemicals, and corrosion-resistant equipment.

Let’s not forget that sulfuric acid prices have surged amid the Hormuz disruption. This industrial chemical is used in nickel production, especially in Indonesia’s battery-grade nickel supply chain.

The line in the sand for LME nickel futures is $20,000.

Tyler Durden

Tue, 05/19/2026 – 12:05

https://www.zerohedge.com/commodities/nickel-jumps-indonesian-output-cut-stokes-supply-fears

Supreme Court Directs Lower Courts To Reexamine Decisions In Voting Rights Act Cases

Supreme Court Directs Lower Courts To Reexamine Decisions In Voting Rights Act Cases

Authored by Matthew Vadum via The Epoch Times,

The U.S. Supreme Court on May 18 ordered lower courts to reconsider rulings in two redistricting cases that concern whether private individuals may sue to enforce a federal law that bans discriminatory voting practices.

The court directed the lower courts to take another look at the cases from Mississippi and North Dakota in light of its recent landmark ruling limiting the use of race in redistricting efforts.

Justice Ketanji Brown Jackson dissented from both new rulings.

In Louisiana v. Callais, a majority of the court had said April 29 that race may not be the predominant, overriding reason for how congressional district lines are drawn. The case focused on the Pelican State’s decision to add a majority-black district after a lower court said omitting the district would violate the Section 2 nondiscrimination provisions of the federal Voting Rights Act.

On Monday, the nation’s highest court summarily disposed of the two cases, State Board of Election Commissioners v. Mississippi State Conference of the National Association for the Advancement of Colored People (NAACP), and Turtle Mountain Band of Chippewa Indians v. Howe, in unsigned orders. The court did not explain its decisions.

Lawyers call this process, which disposes of cases without holding an oral argument, GVR, which stands for grant, vacate, and remand.

The Supreme Court follows this procedure when it wants lower courts to reconsider their rulings using a new legal framework from a recent decision without delving deeply into the specifics of the cases.

North Dakota

In the North Dakota case, the Turtle Mountain Band, the Spirit Lake Tribe, and three Native American voters sued the state’s secretary of state after the state legislature redrew the boundaries of state legislative districts in 2021. The move took the number of majority-Indian districts in the northeastern section of the state from three down to one, and this, the tribes’ petition argued, constituted illegal dilution of Indian voting power.

They filed what’s called a private enforcement lawsuit against the secretary of state to enforce Section 2. They brought their legal action under 42 U.S.C. Section 1983, a federal law that allows individuals to sue the government for civil rights violations.

Secretary of State Michael Howe urged the federal district court to dismiss the case, arguing that there was no implied right of action allowing enforcement of Section 2. The court did not rule on the issue because the plaintiffs also pleaded their case under Section 1983, which the court found yielded a cause of action to enforce Section 2. A cause of action is a set of facts that provides a legal basis for suing someone, the petition said.

The district court ruled in favor of the plaintiffs, finding that Section 2 created individual rights and that nothing in the section’s enforcement provisions was “incompatible with private enforcement.”

Howe appealed, and the U.S. Court of Appeals for the Eighth Circuit found for the state and reversed the district court. The appeals court found that Section 2 does not make provisions for an implied private right of action, and that private plaintiffs may not “instead maintain a private right of action for alleged violations of [Section] 2 through 42 U.S.C. [Section] 1983.”

In his brief, Howe urged the Supreme Court to reject the case, arguing that the Eighth Circuit ruled correctly.

Section 2 “did not unambiguously create an individual right against collective vote dilution,” and the section’s prohibition against dilution is not privately enforceable under Section 1983, he said.

The tribes said in their petition that the Eighth Circuit erred in finding that Section 2 was not privately enforceable and urged the Supreme Court to grant their petition.

The Supreme Court held in Morse v. Republican Party of Virginia (1996) that Section 2 and other sections of the Voting Rights Act are privately enforceable, the petition said.

Mississippi

In the Mississippi case, the NAACP challenged a map for state legislative districts drawn by the Mississippi Legislature after the 2020 census, the NAACP said in its brief.

The group argued that some of the new districts in the 2022 redistricting plan violated Section 2 and the U.S. Constitution, by cracking “large, cohesive Black populations.” Cracking is drawing districts that divide a population or constituency across several districts.

The NAACP argued that four Senate districts and three House districts violated Section 2. The plaintiffs cited Section 1983 and the implied right of action under Section 2 as bolstering their right to privately enforce Section 2, the brief said.

A district court panel of three Mississippi federal judges ruled that the redistricting plan violated Section 2. The court gave the legislature an opportunity to fix its legislative map and ordered special elections in specific districts.

The state said in its brief, which asked the Supreme Court not to take up the case, that the panel erred when it found that the private parties in the case may sue to enforce section 2 of the Voting Rights Act.

That issue regarding private enforcement action is “unsettled and profoundly important” and has divided the regional courts of appeals. Section 2 does not, in “clear and unambiguous” terms, create a federal right to enforce the law under either an implied right of action or Section 1983.

The NAACP urged the Supreme Court to affirm the panel’s ruling.

Jackson’s Dissent

Jackson wrote a nearly identical dissent to both Supreme Court rulings.

“This case presents only the question of Section 2’s private enforceability, which our decision in Louisiana v. Callais … did not address,“ she said. ”Thus I see no basis for vacating the lower court’s judgment.”

Citing the Morse precedent from 1996, Jackson said she would affirm the lower court’s ruling in the Mississippi case, and reverse the lower court’s ruling in the North Dakota case.

Tyler Durden

Tue, 05/19/2026 – 11:45

Berkshire Trolls The AI Bubble By Buying Macy’s

Berkshire Trolls The AI Bubble By Buying Macy’s

Submitted by QTR’s Fringe Finance

For the better part of the last year, Wall Street has behaved like a teenager who just discovered Red Bull and leverage at the same time. Anything remotely tied to artificial intelligence has soared into the financial stratosphere.

Startups with no revenue, no profits, and occasionally no actual product are raising millions or billions because their founders can say the words “large language model”. Public company CEOs now jam “AI” into earnings calls with the same shamelessness that “trendy” gastropubs have when being the 4th “new” place on the block to not just offer a good ole’ fashioned cheeseburger, but the breathtaking innovation of a truffle aioli smashburger.

Meanwhile, looming over all of this market hysteria was Berkshire Hathaway and its absurd cash pile. More than $390 billion sitting on the sidelines while markets rocketed higher. The question became an obsession. What were Warren Buffett and his successor Greg Abel waiting for?

Surely this cash hoard was being preserved for some grand masterstroke. Maybe Berkshire would make a massive AI acquisition. Maybe it would take a huge stake in some futuristic robotics company whose product sounds vaguely dystopian. Maybe Buffett would emerge from Omaha wearing a black turtleneck and announce BerkshireGPT.

Nope. None of these. The filing arrived yesterday and Wall Street discovered that the answer was Macy’s: a company most people associate with buying last minute wedding gifts and wandering through perfume fog thick enough to qualify as weather.

In an era when investors are paying breathtaking multiples for companies promising that AI will revolutionize enterprise workflows, Berkshire appears to have strolled calmly into a department store hoping to get harassed by the Vancome lady.

It is notable to write about because it feels so aggressively out of sync with the cultural moment.

Right now entire hedge funds are building investment theses around the possibility that artificial intelligence may someday help your refrigerator compose emails and then there is Berkshire, quietly behaving like an investor that ignores market spectacle and focuses instead on underlying value. While others chase whatever appears most exciting in the moment, Berkshire tends to concentrate on businesses and assets that are durable, understandable, and often overlooked.

Berkshire likely was attracted to Macy’s because it combined several characteristics long associated with Buffett-style investing: a deeply discounted valuation trading near book value and at a low forward earnings multiple, substantial underlying real estate assets including the flagship Herald Square property, strong cash generation and shareholder returns through free cash flow and dividends, and a credible turnaround strategy focused on closing weaker stores while reinvesting in stronger locations.

Berkshire also likely recognized the enduring value of Macy’s higher-performing brands, particularly Bloomingdale’s and Bluemercury, which provide growth and profitability beyond the traditional department store business. In fact, a lot of the reasons Berkshire bought Macy’s remind me of another retail stock that I think is similarly as attractive to own right now.

And this isn’t to say Berkshire is anti-technology. The company increased its stake in Alphabet and clearly understands where the economy is headed. But Berkshire has spent decades avoiding one of the central mistakes in modern investing: confusing a compelling narrative with a compelling investment. A transformative future does not automatically justify any price. Investors learned that during the dot-com bubble, when companies with weak earnings and questionable business models were treated as inevitable paths to wealth. Many eventually discovered that enthusiasm alone is not a substitute for sustainable economics. They will learn this again with the AI bubble.

That is what makes the Macy’s move so interesting. It suggests that Berkshire still sees value in businesses the market has largely dismissed as boring, outdated, or finished. Macy’s possesses valuable real estate, broad brand recognition, and consistent cash generation — qualities that can become easy to overlook in markets dominated by growth narratives. Perhaps most importantly, expectations surrounding the company have become so low that stability itself can exceed investor assumptions.

That may be the broader lesson for investors. Markets often become fixated on whatever appears revolutionary while overlooking companies that quietly generate profits in less glamorous industries. Investors naturally want exposure to the future, but there can also be opportunity in businesses that continue to serve enduring consumer needs and produce reliable cash flow.

Investors should also be careful about dismissing Berkshire Hathaway simply because it appears old-fashioned in an era defined by speed and disruption. Yet Berkshire has continued to compound wealth across market cycles while many trend-driven strategies have struggled to deliver lasting results.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

The lesson is not that investors should rush to buy Macy’s. It is that when disciplined long-term investors begin allocating capital to areas the broader market has written off, it is worth paying attention. Wall Street is often drawn to what is new and exciting. Berkshire has historically succeeded by identifying value where others stopped looking.

Another lesson is that patience remains one of the most underappreciated advantages in investing. Modern markets reward constant activity, rapid reactions, and short-term narratives, but Buffett’s track record has repeatedly demonstrated the power of allowing investments time to mature. Companies facing temporary pessimism or cyclical weakness are often abandoned long before their underlying economics can recover. Berkshire’s approach suggests that long-term value is frequently created not through constant trading, but through disciplined conviction and the willingness to endure periods of unpopularity.

There is also a lesson about temperament. Successful investing is often less about predicting the future perfectly and more about avoiding emotional decision-making when sentiment becomes extreme. During periods of market excitement, investors can feel pressure to chase momentum and follow consensus thinking. Conversely, when industries fall out of favor, fear and pessimism can create opportunities for investors willing to evaluate businesses on fundamentals rather than headlines. Berkshire’s history reflects an investment philosophy grounded in rationality and discipline rather than market emotion.

Finally, Berkshire’s strategy highlights the importance of understanding the difference between a good company and a good stock at a particular price. Even strong businesses can become poor investments when expectations become unrealistic, while unpopular companies can sometimes offer attractive risk-reward profiles if expectations fall too far. The broader lesson is not that every overlooked stock represents hidden value, but that investors benefit from questioning consensus assumptions. Markets are highly efficient much of the time, but periods of excessive optimism and excessive pessimism continue to create opportunities for patient, disciplined capital allocators.

Now read:

Under The Chaos, One Stock Still Looks Cheap

The Fed Will Invent New Inflation Numbers Out Of Thin Air

Your Retirement Is Being Used To Buy Wall Street’s Toxic Sludge…Again

Bonds Are Screaming “Something’s Wrong”

This Rally Ends In Panic

Time For Rate Hikes

—

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Tue, 05/19/2026 – 11:25

https://www.zerohedge.com/markets/berkshire-trolls-ai-bubble-buying-macys

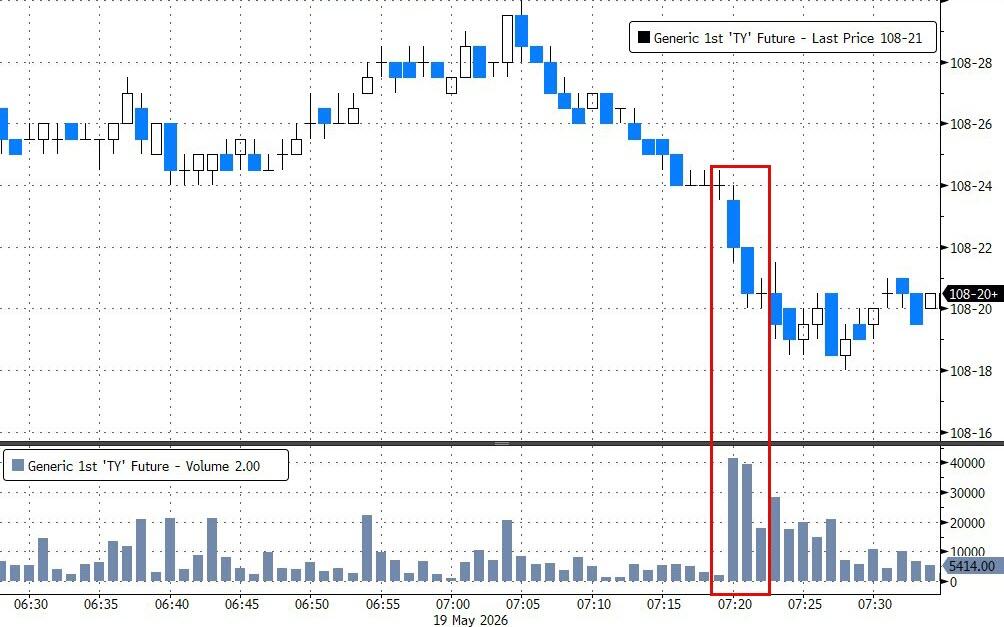

“Door Of Doom” Looms As 30 Year Yield Soars To 19 Year High After Two Huge Treasury Block Sales

“Door Of Doom” Looms As 30 Year Yield Soars To 19 Year High After Two Huge Treasury Block Sales

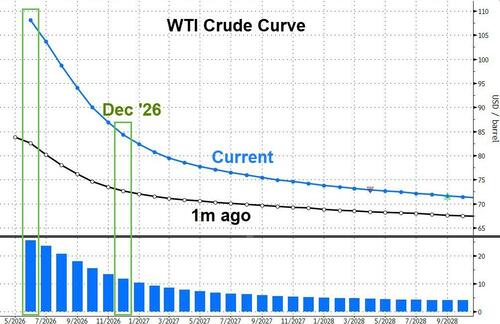

Bond yields continued to move sharply higher today, driven in large part by the aggressive repricing in the oil strip as markets (finally) price in a lengthy disruption to Hormuz traffic which has pushed year-end prices higher by about $12 in the past month.

The result has been a spike across virtually all tenors:

*US 2-YEAR YIELD RISES TO 4.11%, HIGHEST SINCE FEBRUARY 2025

*TREASURY 5- AND 7-YEAR YIELDS RISE 10 BASIS POINTS ON DAY

*US 30-YEAR YIELD RISES TO 5.195%, HIGHEST SINCE JULY 2007

… as can be seen below, with the 30Y yield rising above 5.19% and the highest since 2007

According to Bloomberg, the latest spike higher in 10Y yields which is reverberating across the curve…

… is due to a block of 23,000 contracts in 10-year bond June futures traded at a price of 108-25+ on CBOT.

A total of 1.34 million contracts traded so far in this session.

Two minutes later 20,000 was also blocked at 108-24+ with price action around the two trades consistent with sellers.

The combined amount of risk weighting over the two trades equates to $2.8m/DV01.

On May 13, there were identical size block buyers at levels of 110-00 (20,000) and 109-30 (23,000).

The two sales Tuesday point to the unwind/loss liquidation of these long positions established May 13.

As Nomura’s Charlie McElligott notes, the resumption of investor focus on reaccelerating inflation (both due to 1–the obvious lack of progress with Iran and the Energy / Petrochem “supply shock” as emergency inventories are depleting rapidly, plus 2—signals of an “overheating” US economic risk ironically from the “demand” / FCI -side) have repriced the global central bank policy path “hawkish-ly” while FOMC outlook at the very least is “less dovish-ly” with high pricing of “No Fed Cuts” -scenario through YE and real Delta of the dreaded “Fed Hikes” -potential by YE too.

Bloomberg technical analysts note that the 30-year Treasury yield is right at a key technical level, a break of which targets 5.44% unless liability-driven investors step in to arrest the selloff. The 10-year yield may make a new range if the 4.66% level holds.

But more importantly, the 30Y is about to rise above 5.20%, some 20bps higher than what Michael Hartnett warned in his last two Flow Shows is the “door of doom” red line for the bond market.

And stocks are starting to notice.

Tyler Durden

Tue, 05/19/2026 – 10:45

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}