Category: News

The Politicization Of Everything

The Politicization Of Everything

Authored by David Solway via The Epoch Times,

There was a time when politics occupied only a compartment of life.

A citizen might vote, follow public affairs, argue over taxes or foreign policy and then return to the ordinary business of living: work, worship, family, literature, music, sport, conviviality.

This older balance has been upended.

Politics no longer confines itself to government or elections; it increasingly permeates entertainment, education, business, sport, language—even private conscience. As I noted in my recent column about the “apolitical man,” today we inhabit a culture in which nearly every institution demands ideological participation, and where even silence or indifference may be interpreted as a political act.

The issue runs deeper than ordinary political disagreement. We are living through the gradual disappearance of non-political life itself. Today virtually everything arrives freighted with ideological significance. Everything must justify itself politically before it can simply exist.

As the great American political philosopher Harvey Mansfield observed in “The Rise and Fall of Rational Control,” modern society is crowded with instruments of state control “from the most trivial to the most coercive,” apparently to save us the inconvenience of thinking for ourselves. Yet these are also intrusions into privacy, exerting supervision and pressure over life and conduct. The modern political state no longer merely governs society; it increasingly seeks to furnish society’s entire meaning.

Polish philosopher Ryszard Legutko, having lived under both communism and liberal democracy, recognized the unsettling similarities between these ostensibly opposed systems. In “The Demon in Democracy,” Legutko argued that both systems tend toward ideological conformity and both believe themselves liberated from the obligations of history. The civilized past survives largely as maquillage—a decorative paste applied to glamorize a grubby political machine.

The result is what early 19th-century French political philosopher Alexis de Tocqueville foresaw in “Democracy in America”: a “network of small complicated rules, minute and uniform,” through which individuality is gradually softened, bent and guided into conformity.

De Tocqueville understood that democratic societies might drift not toward overt tyranny but toward a condition of permanent tutelage, in which citizens become increasingly dependent upon administrative systems regulating everyday life.

This tendency now permeates nearly every aspect of Western civilization. The quality of feeling itself has become political. Comedy is judged according to ideological criteria before anyone asks whether it is funny. Art becomes activism. Sport becomes moral theatre. Education concerns political formation rather than learning. Even the patent absurdities of wokism often fail to provoke laughter because they arrive stamped with a political brand.

The modern state increasingly treats culture not as an independent civilizational inheritance deserving protection but as raw material to be supervised, corrected, and ideologically aligned. The old pastoral ideal of the fulfilled and self-reliant individual citizen gradually gives way to the therapeutic subject: managed, supervised, controlled, yet perpetually assured of her freedom in “our democracy.”

One recalls the now-scrubbed World Economic Forum slogan: “You will own nothing and you will be happy.” This is the figment of the old apolitical man falsely wedded to the state. Dependency is rebranded as liberation. Administrative management becomes therapeutic care. The happiness of the classical apolitical man has been transformed into the imposed satisfaction of the political man.

The Russian theological philosopher Nikolai Berdyaev warned of this tendency in “The Destiny of Man” when he described the modern state’s willingness to sacrifice freedom—with its innate acceptance of risk and the possibility of failure—for the illusion of perfection. Once politics assumes responsibility for constructing moral meaning itself, there can be no genuine limit to state control. Every sphere of life becomes potentially political because every sphere may contribute either to ideological conformity or ideological dissent.

Meanwhile, the civilized inheritance sustaining the West steadily weakens. Our governing classes inhabit the architectural husk of antiquity while possessing little connection to the civilization that produced it. They have never read Plato or Cicero, scarcely know Virgil exists, and treat history largely as an embarrassment or political inconvenience. The shimmer of potentiality embodied in the classical world has been damped; the larger vista of human achievement increasingly redacted.

Yet not all is lost.

Churches, local associations, independent journals, small enterprises, and serious works of culture still preserve fragments of the civilization that politics alone cannot sustain. These “apolitical forces” remind us that human beings cannot live entirely within ideological systems without becoming spiritually diminished.

A civilization survives only when there remain spheres of life politics cannot wholly absorb. Once politics becomes everything, civilization itself begins to disappear.

Tyler Durden

Mon, 05/18/2026 – 22:35

https://www.zerohedge.com/political/politicization-everything

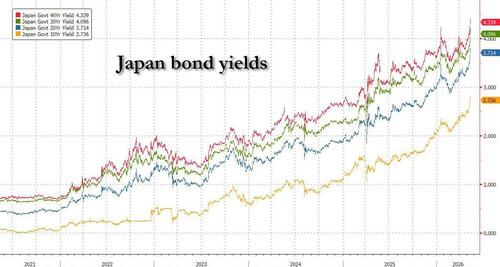

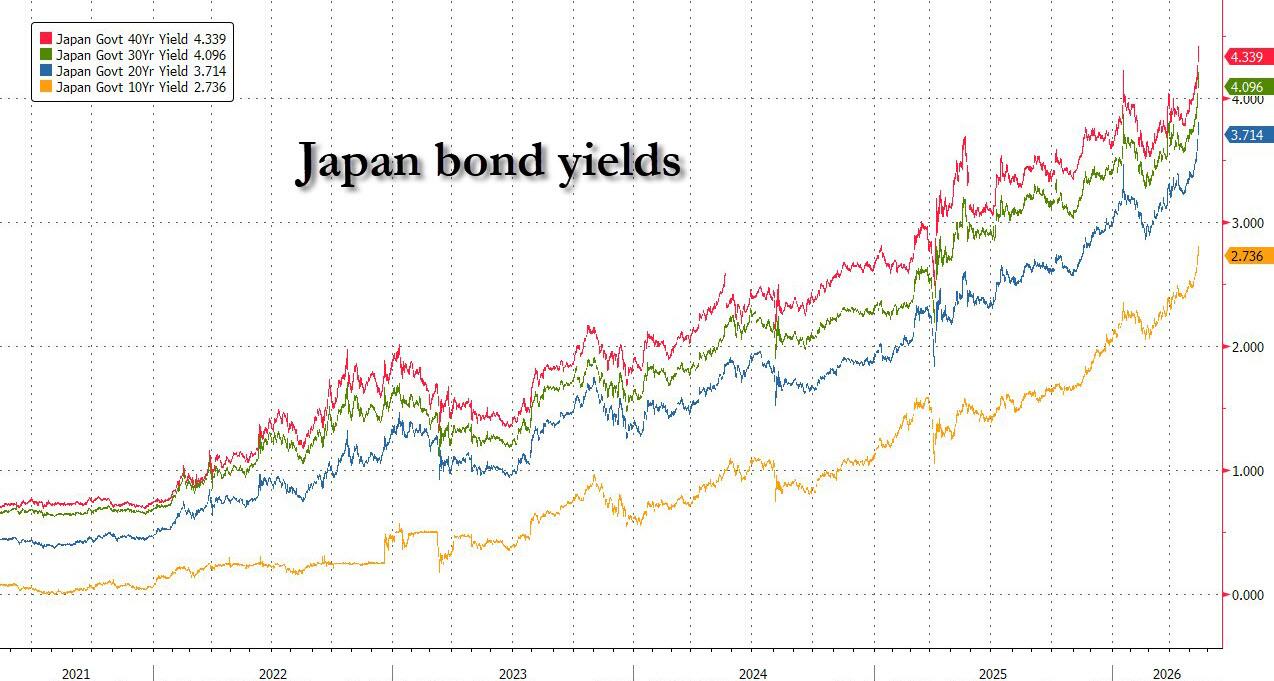

Japanese Bonds Crater After PM Takaichi Prepares To Issue Much More Debt To Pay For Gasoline Subsidies

Japanese Bonds Crater After PM Takaichi Prepares To Issue Much More Debt To Pay For Gasoline Subsidies

While it may seem like every government these days – not just Emerging but certainly all Developing countries too – has become a banana republic in light of the increasingly more idiotic fiscal and monetary policies adopted to kick the can at least until the next election, nobody is quite as cartoonish as Japan, the place where all modern-day central bank experiments started in the late 1980s.

While on one hand the Japanese finance ministry and Bank of Japan have, in recent days and over the years, engaged in aggressive currency day trading, where they try to avoid a collapse in the yen by purchasing the currency in exchange for reserves such as US dollars, on the other hand, the same authorities have been, for the past 3 decades, been engaging in unlimited yen printing through perpetual QE (which despite the country’s soaring inflation and collapsing currency, goes on to this day even though Japan’s Yield Curve Control is taking a short break). End result: between the selling and buying of yen, the only thing Japanese officials have achieved is becoming the laughing stock of the world. Meanwhile, Japanese bond yields have exploded to multi-decade, if not record highs, as we showed last night.

One reason, besides all the other “usual suspects” such as soaring energy import costs, an grotesque inability to hike rates and contain inflation, not to mention relentless capital flight, is that as Reuters reported overnight, Japan’s government is likely to issue even more debt as part of funding for a planned extra budget to cushion the economic blow from the Middle East war.

Of course, any additional debt issuance would further strain Japan’s already worsening finances and may accelerate rises in long-term interest rates. Actually, better make that “will” accelerate: the report pushed the yield on the benchmark 10-year Japanese government bond (JGB) to 2.8% on Monday, its highest since October 1996, and the 30-year yield to a record top.

On Monday, Prime Minister Sanae Takaichi said she had told Finance Minister Satsuki Katayama last week to start work on compiling a supplementary budget, a rather dramatic shift from previous remarks ruling out the chance of an extra budget.

The extra budget will focus on funding government subsidies to curb gasoline and utility bills, as surging oil prices caused by the Middle East conflict cloud the outlook for an economy heavily reliant on fuel imports from the region.

While the size of spending has yet to be worked out, the decision could cast doubt on the administration’s laughable pledge to pursue a “responsible, proactive” fiscal policy. Spoiler alert: there is no “responsible” fiscal policy when your debt/GDP is over 200%. You can only hope for a peaceful death.

And the market was quick to react.

“The about-face by Takaichi, who had been ruling out an extra budget all along, is making markets jittery and triggering a JGB selloff across the curve,” said Katsutoshi Inadome, senior strategist at Sumitomo Mitsui Trust Asset Management.

In a proposal to the finance ministry, opposition party leader Yuichiro Tamaki called on Friday for an extra budget of about 3 trillion yen ($18.9 billion), which may serve as a benchmark for future debates on the size of spending.

“There’s a host of reason to sell JGBs but very few to buy,” Inadome said, adding that markets are starting to price in the chance of an extra budget to the scale of 5 trillion-to-10 trillion yen.

Finance minister Katayama, who is in Paris to attend the Group of Seven finance leaders’ gathering, said on Monday she was instructed by the prime minister to “minimise various risks,” when asked about the rise in long-term interest rates.

“That’s something I’m contemplating,” Katayama said when asked how the government would fund the extra budget. She did not elaborate.

Japan already curbs gasoline prices with subsidies and eyes tapping existing funds to revive subsidies for utility bills (which of course means no demand destruction due to artificially low prices, but instead the massive new debt needed to subsidize said spending, will instead translate into state and sovereign destruction). An extra budget would come on top of a record 122-trillion-yen budget for the fiscal year that began in April, which makes up the core of the dovish premier’s expansionary fiscal policy.

Critics warn that more spending plans, coupled with slow interest rate hikes by the Bank of Japan, could fan inflationary pressure in an economy already seeing rising energy costs from the Middle East war and higher import prices from a weak yen.

Japan’s Nikkei stock average fell on Monday and the yen hit 158.97 per dollar, the weakest level since April 29, and it’s about to explode even higher once the marker realizes the sheer idiocy of selling dollars to buy yen on one hand, and then turning around and doing QE – i.e., printing yen – to absorb all the new massive debt issuance about to hit a bond market where the BOJ has long since become a 50% holder of all JGBs and the marginal price setter.

“When countries like Japan and Britain contemplate fiscal stimulus, there’s a tendency for that to trigger a triple selling of shares, currencies, and bonds because their economic growth is weak and inflationary risks are high,” said Daisuke Uno, chief strategist at Sumitomo Mitsui Banking.

The extra budget will be compiled around June or July, when the administration will lay out plans to boost investment and details for a two-year freeze on an 8% levy on food.

Reuters tongue-in-cheekly adds that “the bond selloff would also complicate the BOJ’s decision on whether to raise its short-term policy rate to 1% from 0.75% at its next meeting in June.” Uhm, no, it wouldn’t complicate it – it would make it an absolute farce as the last thing Japan needs if it is to sell even more debt, is higher rates. But then Tokyo better brace for a yen at 200 vs the dollar, unless the MOF is prepared to liquidate all of its USD-denominated reserves in an absolutely idiotic attempt to keep the yen from collapsing.

At the June meeting, the BOJ will also review its existing bond tapering programme and unveil a new plan for fiscal 2027 onward.

The war-induced spike in energy prices, coupled with rising import costs from the collapsing yen, pushed Japan’s wholesale inflation to a three-year high of 4.9% in April, bolstering the case for the central bank to raise rates as soon as next month.

While the BOJ tends to avoid shifting policy when markets are volatile, delaying rate hikes further could stoke already mounting fears it is behind the curve in addressing the risk of too-high inflation, analysts say. On the other hand, raising rates could spark an even more aggressive selloff across the curve, resulting in both a bond and FX market failure. Oops.

Markets have priced in roughly a 70% chance of a June rate hike after a slew of recent hawkish signals from the BOJ and a split vote to the BOJ’s decision to keep rates steady in April. Nearly two-thirds of economists polled by Reuters expect the BOJ to raise rates in June.

“If inflationary risks heighten, there’s a chance the BOJ could raise short-term rates to 1.5% by the March end of the current fiscal year,” said Mari Iwashita, executive rates strategist at Nomura Securities. The 10-year yield could head towards 3%, she added.

Tyler Durden

Mon, 05/18/2026 – 22:10

UAE Paid New York Firm Millions To Bury Article On Ambassador’s Links To Sex Traffickers: Report

UAE Paid New York Firm Millions To Bury Article On Ambassador’s Links To Sex Traffickers: Report

The UAE paid New York-based reputation management firm Terakeet more than $6 million to bury a 2017 report revealing that the Emirati ambassador to Washington, Yousef al-Otaiba, had ties to sex workers and traffickers, according to a New York Times (NYT) report published on Sunday.

The campaign was designed to push the Intercept report out of public sight on Google search results. According to Foreign Agents Registration Act records cited by the paper, Terakeet’s work for the UAE began in July 2019 and continues today.

Much of the account focused on promoting tourism in the UAE, but NYT reported that Terakeet’s work also extended to suppressing the damaging Otaiba report. Otaiba declined to comment beyond confirming that Terakeet has worked for the UAE.

The effort was kept off paper, with account manager Kenneth Schiefer moving to Washington for more than a year to work directly with Otaiba at the UAE embassy, avoiding a trail of emails or text messages.

The reputation firm had built a personal website for Otaiba, planted favorable leadership profiles on institutional pages tied to him, and fed those profiles links to UAE-friendly blogs written by Terakeet staff. The firm also used an anonymous Wikipedia editor handle, VentureKit, to create a fake sockpuppet account, Quorum816, and add positive material to Otaiba’s page. Wikipedia reversed the edits and suspended both accounts in 2021.

The campaign succeeded, and by 2023, the Intercept story had been pushed to page two of Google results. NYT reported that today, it appears on around page five for most users.

The UAE account formed part of a wider investigation into Terakeet’s reputation-cleaning business for powerful figures and major corporations with damaging public records. The firm’s client list has included MetLife, JPMorgan Chase, Oracle, Target, Walmart, Disney, and Bain Capital, according to NYT.

Terakeet later tried to scrub the online image of Goldman Sachs general counsel Kathryn Ruemmler after her relationship with convicted sex offender Jeffrey Epstein became a public liability.

🇦🇪 The New York Times reports that the UAE paid more than $6 million to the reputation management firm Terakeet between 2020 and 2022 to manipulate Google search results and suppress damaging reporting by Drop Site co-founder Ryan Grim, then at The Intercept, about Emirati… pic.twitter.com/gHRcCZ0HhC

— Drop Site (@DropSiteNews) May 18, 2026

The effort intensified after Justice Department files showed Ruemmler’s name appeared in more than 10,000 Epstein-related documents, including exchanges in which she discussed travel with Epstein, thanked him for lavish gifts, and offered him legal advice.

Terakeet also worked for Vista Equity Partners chief executive Robert F. Smith, who signed a 2020 non-prosecution agreement acknowledging that he had “engaged in an illegal scheme to conceal income and evade taxes” between 2000 and 2015.

Terakeet chief executive Mac Cummings defended the firm’s model, saying “Terakeet’s technology is built on a simple mandate: organizations must tell their own story.”

Drop Site News reported in January that Jeffrey Epstein’s close relationship with DP World chief Sultan Ahmed bin Sulayem helped foster UAE-Israel economic and security ties that later fed into the Abraham Accords.

Here’s the 2017 Intercept report: https://t.co/FV6gBQvDrl

— Drop Site (@DropSiteNews) May 18, 2026

The report says Epstein arranged meetings between Sulayem and former Israeli prime minister Ehud Barak, helped channel Emirati investment into Israeli firms, and maintained contact with Sulayem until his 2019 arrest on sex trafficking charges.

Tyler Durden

Mon, 05/18/2026 – 21:45

Hundreds Of Subpoenas Are Targeting The Russian Collusion Hoax

Hundreds Of Subpoenas Are Targeting The Russian Collusion Hoax

According to Acting Attorney General Todd Blanche, the Justice Department is hunting the architects of the Russia hoax, and they’re leaving no stone unturned.

Blanche sat down with Bartiromo on Sunday Morning Futures to discuss what he says is a sweeping criminal investigation into the origins of one of the most destructive political operations in history.

The Southern District of Florida has an open criminal probe. Hundreds of subpoenas. Hundreds of witnesses. Blanche insists the DOJ is working hard and working efficiently. Bartiromo, who has been covering this story for nearly 10 years, wanted answers on why the process has taken so long.

“What have you done about it?” she asked point-blank.

“Well, look, that’s exactly what we’re investigating right now. And by the way, what is not in dispute is that the whole Russia hoax, there was absolutely nothing to it,” Blanche told Bartiromo.

“And so the question that the American people have to ask is, well, then why did they do it? Why did Comey say what he said? Why did the outgoing Obama administration do what they did?”

Blanche continued.

“And that’s what we’re studying right now, because it did great damage to this country. It did great damage to President Trump’s first term. And we want to understand why that happened, why there are continued to be an effort by operatives in the government to go after President Trump while he was in office, and then, of course, over the past several years as well.”

But Bartiromo wasn’t accepting his statements at face value.

“I’d like to know why it’s taking so long,” Bartiromo pressed.

“Has the statute of limitations run up? Do you have no more wiggle room in terms of zeroing in on things like the Mueller report, the Nunes report, and all the evidence that was clear — that they knew there was no Russia collusion?”

Blanche pushed back on the statute-of-limitations concern, arguing that the conspiracy arguably continued well past its origins (through the Mar-a-Lago raid in 2023), which could extend the legal exposure considerably. He framed the entire thing as potentially one continuous criminal conspiracy, stretching from 2015 through 2023 as part of a singular effort to destroy President Trump. “Whether that’s one conspiracy that continued from 2015, 2016, all the way up to 2023 is what we’re looking at right now,” Blanche said. “We’re finding out some incredibly troubling things. And at some point at the right time, that will be made public.”

“When is the time right?” Bartiromo asked. “When should we expect these charges of conspiracy?”

“Well, I mean, look, as has been publicly reported, the Southern District of Florida has an open criminal investigation,” Blanche explained. “That involves hundreds of subpoenas. It involves hundreds of witnesses. And so, as far as timing and when we can expect it, we are working hard, and we are working efficiently, but we are going to do it right. We are not going to rush something, rush something that shouldn’t, that isn’t ready. We’re not going to reach a conclusion before our investigation is over. But I assure you and I assure the American people that we are completely focused on it.”

With hundreds of subpoenas and hundreds of witnesses, this is clearly no small investigation. And considering the media and Democrats will scrutinize every move, the DOJ knows it can’t afford to cut corners. In a case this explosive, being thorough matters a lot more than moving fast.

Tyler Durden

Mon, 05/18/2026 – 21:20

https://www.zerohedge.com/political/hundreds-subpoenas-are-targeting-russian-collusion-hoax

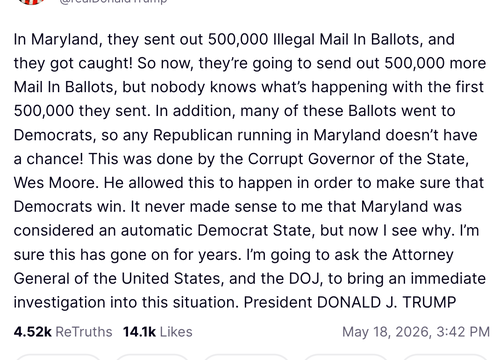

Trump Demands DOJ Probe Of Maryland’s 500,000 “Illegal” Mail-In Ballots

Trump Demands DOJ Probe Of Maryland’s 500,000 “Illegal” Mail-In Ballots

Submitted by Maryland Freedom Caucus,

President Donald Trump is demanding immediate action from the Department of Justice over Maryland’s exploding mail-in ballot scandal, and he’s not mincing words.

In a Truth Social post on Monday, Trump slammed the fiasco:

“In Maryland, they sent out 500,000 Illegal Mail In Ballots, and they got caught! So now, they’re going to send out 500,000 more Mail In Ballots, but nobody knows what’s happening with the first 500,000 they sent. … I’m going to ask the Attorney General of the United States, and the DOJ, to bring an immediate investigation into this situation.”

The Maryland State Board of Elections admitted late last week that a third-party vendor printed and mailed roughly 400,000 ballots for the June 23 gubernatorial primary, with an undetermined number of voters receiving the wrong party’s candidates. Because officials cannot tell exactly who received the flawed ballots, they are re-mailing replacements to every voter who requested one before May 14. However, the original ballots remain in circulation.

The Maryland Freedom Caucus was first out of the gate. On May 16, we issued a press release exposing the crisis, demanding that Jared DeMarinis release Maryland’s voter rolls for a federal audit, and warning that “400,000 double ballots in circulation” threaten the fundamental principle of one vote, one person.

To restore faith in Maryland’s electoral process, decisive action is necessary. We must release the voter rolls to the federal government to allow for a thorough audit into the reported issuance of 400,000 incorrect ballots. pic.twitter.com/39PJlDyKiN

— Maryland Freedom Caucus (@MDFreedomCaucus) May 16, 2026

This is not an isolated glitch. Last fall, the Maryland Freedom Caucus and our partners at Secure the Vote MD blew the lid off the Ian Roberts case — an illegal alien from Guyana who was registered to vote in Maryland for years, requested absentee ballots, and remained on the active rolls even after his arrest. That single case proved what we’ve warned for years: Maryland’s voter rolls are bloated with non-citizens, deceased voters, and people who no longer live here.

Worse, when the DOJ requested Maryland’s full voter registration data last year, the State Board of Elections stonewalled. Administrator DeMarinis specifically asked whether the list would be used for immigration enforcement before providing anything meaningful – a clear admission that transparency threatens their continued subterfuge.

BREAKING: Another Maryland Man controversy!

Have you heard the story of Ian Andre Roberts, the Superintendent for Des Moines Public Schools? He was arrested late last week for a standing deportation order. Turns out, he is actively registered to vote in Maryland, despite being… pic.twitter.com/T7XlAobQ6O

— Maryland Freedom Caucus (@MDFreedomCaucus) September 29, 2025

President Trump’s call for a DOJ investigation is the national spotlight this scandal desperately needs. Permanent, no-excuse mail-in voting was sold as “convenient and secure.” In reality, it has become a black box that erodes public trust and invites chaos, exactly as the Maryland Freedom Caucus has warned.

But calls for investigation without an immediate remedy will not restore Marylanders’ confidence in their elections. Governor Wes Moore must immediately issue an executive order to restore strict chain-of-custody controls: end the use of unmonitored drop boxes, suspend the use of USPS for local delivery, require that all marked ballots be returned directly to a local Board of Elections office, and implement real-time logging so every ballot can be tracked from voter to canvass.

Tyler Durden

Mon, 05/18/2026 – 20:55

https://www.zerohedge.com/political/trump-demands-doj-probe-marylands-500000-illegal-mail-ballots

Wayfair CFO’s Muted Home-Goods Demand Outlook Offers More Bad News For Realtors

Wayfair CFO’s Muted Home-Goods Demand Outlook Offers More Bad News For Realtors

Wayfair CFO Kate Gulliver appeared at JPMorgan’s conference Monday morning in a discussion with the bank’s retail analyst, Christopher Horvers.

What caught our attention in the 35-minute conversation, which ranged from the online home-goods retailer’s financial position to broader consumer trends, was Gulliver’s outlook on home goods and housing markets.

A more active housing market typically drives demand for big-ticket home purchases such as sofas, tables, and other furnishings sold on Wayfair’s online platform.

However, her forecast for the remainder of the year was decidedly muted, a gloomy outlook that may leave realtors and mortgage brokers uneasy.

Horvers asked Gulliver about the home goods and housing markets, including whether she was worried about soaring energy prices, the post-stimulus era, and how those factors could affect consumer demand for home goods over the rest of the year.

Her outlook for the rest of the year was not great. She noted that the home goods category “has not been a tailwind for us.”

“At some point, this cyclical category will recover, but our expectations for 2026 and our guidance for the second quarter do not assume any category recovery. Our operating assumption for 2026 is that the category stays where it is,” Gulliver explained.

Gulliver’s dismal view of the home goods and housing markets for the rest of the year offers valuable insight because Wayfair is one of the largest online home-furnishings platforms in the U.S.

Much of Wayfair’s consumer base consists of millennials and Gen Xers in the household-formation cycle, including raising a family, buying a home, or moving into a larger residence, all of which drive demand for furniture and such.

This muted activity she observes and forecasts also comes as the 30-year mortgage rate is back around 6.5%, up roughly 35 basis points from when the U.S.-Iran conflict began in late February.

Related:

Most Americans Can’t Afford New Homes

Home Prices Register Biggest Annual Increase In More Than A Year: Report

Gulliver’s view serves as a proxy for the housing market. Her comments this morning offer no relief for the struggling realtors and mortgage brokers over the last several years.

Also to note, rate markets are pricing in hikes next year as energy inflation from the Hormuz chokepoint disruption pushes up inflation expectations and TSY yields soar.

Tyler Durden

Mon, 05/18/2026 – 20:30

Combined NextEra-Dominion Would Have 130-GW Large-Load Pipeline

Combined NextEra-Dominion Would Have 130-GW Large-Load Pipeline

By Robert Walton of UtilityDive

Summary

NextEra Energy plans to acquire Dominion Energy in an all-stock transaction announced Monday, potentially creating the largest regulated electric utility in the world — with 10 million customers in four states — if the deal passes muster with three state and two federal regulatory commissions.

The companies have proposed $2.25 billion in bill credits for Dominion customers in Virginia, North Carolina and South Carolina, and they say all customers would see benefits from “enhanced scale in operations, procurement, construction and financing.”

The combined company would have a more than 130-GW large-load pipeline of projects and a rate base of $138 billion, which it expects to grow at approximately 11% through 2032, according to the deal announcement.

Company officials frame the deal as a win for customers by maintaining operating stability and putting downward pressure on rates while allowing the combined utility company to grow faster and more efficiently. Customer advocates, however, warned of the deal’s potential impact on consumers, and analysts say it could signal shifts in the utility operating model and wholesale markets.

“The Dominion Energy name isn’t changing, nor is how we operate locally, serve our customers or engage with the community,” NextEra Chairman, President and CEO John Ketchum said in a statement.

The merger has been approved by the boards of directors of Dominion and NextEra, and the companies say they expect to close the transaction in 12 to 18 months subject to approvals from a host of regulators. The deal must be approved by the Federal Energy Regulatory Commission, Nuclear Regulatory Commission, Virginia State Corporation Commission, North Carolina Utilities Commission and the Public Service Commission of South Carolina.

Customer advocate group Clean Virginia called for state officials to subject the proposed merger “to the most rigorous scrutiny possible.”

“This deal would hand control of Virginia’s electric grid to a company with a deeply troubling track record,” Brennan Gilmore, executive director of Clean Virginia, said in a statement.

“Before Virginia ratepayers are locked into a relationship with NextEra Energy, every policymaker and regulator in the Commonwealth needs to understand what NextEra has done in Florida,” he added, pointing to rate hikes and scandals around dark money political advocacy.

The companies say they plan to maintain dual headquarters in Florida and Virginia. NextEra owns Florida Power & Light, which serves 6 million customer accounts. Dominion serves 3.6 million electric customers in its three-state territory, and about 500,000 gas customers in South Carolina.

The combined entity would have an almost $250 billion market capitalization, which the companies said would make them the “world’s largest regulated electric utility business by market capitalization and one of the world’s largest energy infrastructure companies.”

Consensus data from S&P Global Visible Alpha paints a picture of two growing companies. Analysts expect NextEra to have total operating revenues of $30.6 billion this year, up 11.68% year over year; Dominion is expected to see total operating revenues of $18.4 billion, up 11.5% year over year.

Limited energy capacity remains a vital issue for the broad adoption of AI.

“This deal may support increased scale and efficiency in the space to support the ramp in data center compute,” Melissa Otto, head of research at S&P Global Visible Alpha, said in an email to Utility Dive.

The deal would combine “two well-run utility franchises,” Alex Kania, BTIG managing director and utilities and power analyst, said in a statement. There is some question about how the combination could impact operations in the PJM Interconnection, he noted.

“We believe [the deal] could mark a step to a return to the integrated utility model that has largely been abandoned over the past 10 years — but we think that model may end up being one of the better ways to address PJM resource adequacy. Stay tuned,” Kania said in a research note.

Dominion’s pipeline of contracted data center capacity now stands at about 51 GW, the company said earlier this month in its first-quarter earnings. And in Virginia, its largest utility market, Dominion sold 4% more electricity year over year in the first quarter of 2026.

Dominion’s position in Virginia’s “data center alley” means the utility is “very well situated for large load growth,” Kania said. Its large load pipeline and PJM interconnection portfolio would pair with NextEra’s “vast generation development platform” of gas, renewables and storage.

The combined entity would be “one of just a few players in PJM that could readily offer comprehensive grid and generation solutions to large load,” Kania said.

The deal “makes much sense for NextEra to rebalance its business mix,” Jefferies equity analyst Julien Dumoulin-Smith said in a Monday note. NextEra’s unregulated business has been growing faster than its utilities, “a trend expected to continue,” he said. “Buying a regulated business has been important for years.”

The combined business would be “anchored by a more than 80% regulated business mix, with approximately 11% regulatory capital employed growth across four fast-growing states with constructive regulatory environments,” Dominion and NextEra said.

Officials expressed confidence in getting the merger across the finish line.

“We have some experience getting deals done,” Robert Blue, Dominion chair, president and CEO, said in a call with analysts. “We feel very good about the way the deal has come together, with the focus on customers and communities, and that gives us a high degree of confidence.”

Under terms of the deal, Dominion shareholders will receive 0.8138 shares of NextEra Energy for each share of Dominion they own. The companies say this will result in NextEra and Dominion shareholders owning approximately 74.5% and 25.5% of the combined company, respectively.

Tyler Durden

Mon, 05/18/2026 – 20:05

https://www.zerohedge.com/markets/combined-nextera-dominion-would-have-130-gw-large-load-pipeline

Almost All Non-Iran Tankers That Entered The Persian Gulf During The War, Have Successfully Exited With A Cargo

Almost All Non-Iran Tankers That Entered The Persian Gulf During The War, Have Successfully Exited With A Cargo

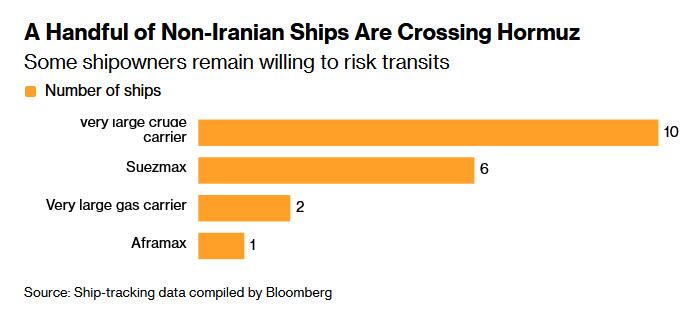

Despite a near-halt in daily Hormuz traffic, Bloomberg reports that almost all large non-Iranian tankers that have entered the Persian Gulf during the war appear to have successfully exited with a cargo, underscoring the emergence of a small group of shipowners willing to risk crossing the Strait of Hormuz.

At least 19 oil- and liquefied petroleum gas-carrying ships without Iranian links have both entered and exited Hormuz since March 1, according to vessel-tracking data compiled by Bloomberg. In contrast, about 100 such tankers that entered the Gulf before the conflict remain stuck for fear of attacks, the data show.

As noted above, merchant shipping through the vital energy chokepoint has – for the most part – ground to a halt since US-Israeli attacks at the end of February triggered a wave of Iranian retaliation and led Tehran to tighten its grip over the waterway. Yet a handful of vessels have been managing to cross under an array of schemes, including deals arranged at a government level (with payment in bitcoin) in some cases (and keep in mind that the numbers, both for ships stranded in the Gulf and those making the crossing, could be higher in reality, given many vessels in the region are switching off their satellite signals to protect against strikes).

Of the 19 ships to cross, seven have been linked to Greece’s Dynacom Tankers Management. The company has been one of the main firms to continue using the strait since the conflict began. In true honey badger form, the company is known to turn off its ship transponders and then to quietly make the Hormuz crossing usually under the cover of night. It is unclear if Dynacom had arranged any special arrangement with Tehran ahead of its crossings.

The cargoes the vessels were carrying have largely been from the United Arab Emirates and Iraq. Of the rest, three were transporting oil from Saudi Arabia or a mix of oil from the kingdom and other Arab Gulf nations.

Only one large tanker that entered the Gulf after the war started hasn’t left, the data show.

The crossings are only a fraction of the typical Hormuz transits before the war, which accounted for about a fifth of the world’s oil supply.

Tyler Durden

Mon, 05/18/2026 – 19:40

The Great American Squeeze Of 2026

The Great American Squeeze Of 2026

Authored by MN Gordon via Economic Prism,

Does your American dream feel like it’s being put through a hydraulic press?

If so, you’re not alone. Between rising rent and gas prices, escalating grocery bills, and sky-high health insurance premiums, Americans are feeling a relentless squeeze from all directions. That’s the painful reality.

Recent economic numbers point to a weary consumer. In fact, consumer sentiment is at a 74-year low. To put that in perspective, Americans feel more pessimistic about the economy today than they did during the 2008 financial crisis, the stagflation of the 1970s, or the height of the 2020 lockdowns.

What’s going on?

Why does it feel like your paycheck is evaporating before it even hits your bank account, while the S&P 500 is hitting record highs over 7,400?

The answer has to do with the K-shaped reality of 2026.

For years, economists have tried to gaslight American workers and consumers. They blamed social media and partisanship. They reasoned that if your preferred politician isn’t occupying the White House, you complain a bit more to a pollster.

Several years ago, Kyla Scanton coined the term “vibecession” to describe a situation where the data looks fine on paper, but people feel bad in their souls. But what about when the data looks bad on paper?

Heather Long, chief economist at Navy Federal Credit Union, recently pointed out today’s reality. The vibes have officially been replaced by cold, hard financial pain. When the University of Michigan sentiment reading drops to 49.8, it’s not just because people are grumpy on Twitter. It’s because the cost of basic survival has outpaced the ability to pay for it.

What’s more, as middleclass families drown in debt, the wealthy flourish. This creates a highly visible divide that presages social instability.

A Tale of Two Americas

The fact is you likely took a pay cut last month. Even if your boss gave you a 3 percent raise this year, you’re still losing ground. With inflation rising at an annual rate of 3.8 percent, per this week’s CPI report for April, your real wages are in the red. Thanks to the U.S.-Israeli war in Iran the energy component of the CPI is increasing at an annual rate of 17.9 percent.

When consumer prices rise faster than your income, that’s not a vibe. That’s the real time erosion of your income. And this is just the beginning…

Joseph Brusuelas, chief economist at RSM, warns that as the supply shocks from the Middle East filter through the system, May is going to be even worse. We are essentially footing the bill for global conflicts through higher prices.

Yet the effects of inflation are felt differently throughout the economy. Those in the higher income brackets are benefiting from an inflating stock market. Retail sales are up 4 percent year over year. So, too, Disney recently confirmed that its domestic park bookings and cruise reservations remain strong through the second half of 2026.

Then there are those in the middle- and lower-income brackets who can’t keep up. They don’t own stocks. They don’t own a house with a 3 percent mortgage. For this group, personal loan applications are spiking. Credit card debt is at an all-time high. They’re also being forced out of their cars and onto the bus because they literally can’t afford the commute.

These diverging stories are both true. This is the tale of the K-shaped economy.

The top line of the K is heading toward the moon. These are the households earning $150,000 or more. For them, the squeeze is a gentle love pat. Their homes have skyrocketed in value, and their stock portfolios are thriving as the S&P 500 bubbles up.

The bottom line of the K, however, is a steep slide downward. This represents the bottom 50 percent of the income distribution. For these families, the resilience everyone has talked about for the last few years has finally hit a wall.

Quiet Desperation

When wages don’t cover the bills, people don’t stop eating. They reach for the plastic. Hence, there’s been a massive increase in people turning to personal loans and credit cards just to make it from one Friday to the next.

This is the latent phase of a recession. It doesn’t show up in the unemployment numbers (which are still a steady 4.3 percent) or the payroll data (115,000 jobs added in April). It shows up in the quiet desperation of an ascending balance on a 24 percent interest credit card.

When people finally get to the end of their credit card rope, we enter the demand destruction phase. This is when people are too broke to buy stuff. Lower-income households are forced to cut back on gasoline and non-essential spending.

There’s also a big picture issue coming into focus that Mohamed El-Erian, chief economic advisor at Allianz, has zoomed in on. Specifically, labor’s share of GDP has hit its lowest level in BLS history.

What that means is that of all the wealth being generated in the USA, a smaller and smaller piece of the pie is going to the people who actually do the work. In other words, more and more of the economy’s capital is being directed to the people who own the stocks, land, and the companies.

This is why the stock market is hitting record highs while the average worker feels like they’re drowning. The market likes muted wage growth because it means companies keep more profit. But for the person trying to pay rent, muted wage growth is a disaster.

Beyond the Siren

Regardless of whether the economy enters a full-blown recession, a large segment of workers and consumers are suffering a painful squeeze. For those being squeezed it adds insult to see people booking luxury cruises when they’re having to choose between buying gas or buying groceries.

As households max out their credit cards, we can expect to see a wave of defaults. If this persists, the banks may get nervous and tighten credit. This will make it even harder for the bottom half to get the loans they need to survive.

Also, with the cost of living so high, middle-class families are raiding their 401(k)s or stopping contributions altogether. People are trading their future security for today’s gas and bread.

The American worker and consumer have proved to be resilient over many years. They persevered through pandemic lockdowns, supply chain meltdowns, and years of inflation. But even the strongest rubber band snaps if you stretch it far enough.

The current sentiment data isn’t a vibe. It’s a warning siren. While the top earners continue to power the retail numbers and fill up the Disney parks, the foundation of the economy – the working and middle class – is being hollowed out by a combination of geopolitical shocks and a declining share of the nation’s wealth.

Until wages outpace the cost of a gallon of gas and a bag of groceries, the American consumer will continue to get squeezed. Alas, there appears to be no relief on the horizon.

With the Strait of Hormuz effectively shuttered, this squeeze will only intensify. As global energy flows cease, surging crude prices will inevitably bleed into your grocery bill. From the diesel powering delivery trucks to the fertilizers growing our crops, the cost of survival is headed for a painful, sustained peak.

* * *

Get a free copy of an important special report called, “Cash Machine – Why You Should Own this Mineral Royalty with a 12% Yield,” when you join the Economic Prism mailing list today. If you want a special trial deal to check out MN Gordon’s Wealth Prism Letter, you can grab that here.]

Tyler Durden

Mon, 05/18/2026 – 19:15

https://www.zerohedge.com/personal-finance/great-american-squeeze-2026

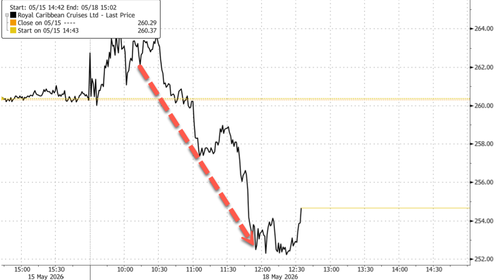

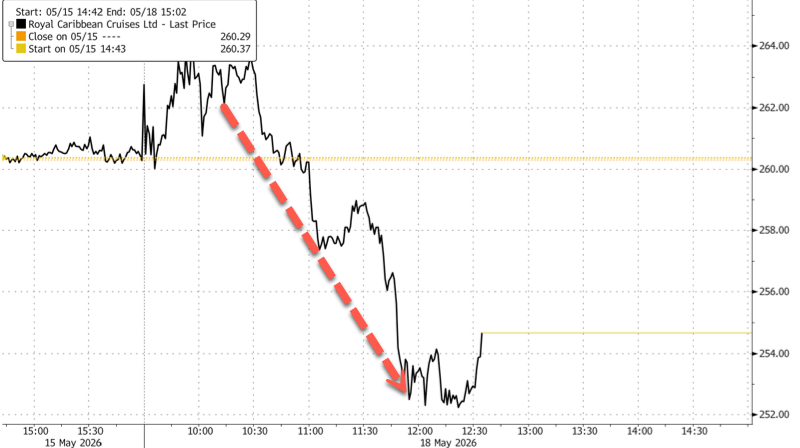

Lawfare? Royal Caribbean Sinks After Mexican President Orders Review Of Resort Project

Lawfare? Royal Caribbean Sinks After Mexican President Orders Review Of Resort Project

Shares of Royal Caribbean Group slid to session lows around midday after Mexican President Claudia Sheinbaum said her environment minister would review the cruise operator’s proposed water park project in Quintana Roo, injecting new regulatory risk into the company’s expansion plans.

President Sheinbaum was speaking at a regular press conference Monday morning, where she addressed a range of topics, from drug traffickers and President Trump to Royal Caribbean.

Sheinbaum said that SEMARNAT México, Mexico’s federal environment ministry – formally the Secretaría de Medio Ambiente y Recursos Naturales – is conducting a very detailed review of Royal Caribbean’s tourism project in Mahahual, Quintana Roo.

She assured that no construction would be permitted if it endangered the area’s ecological balance.

La presidenta Claudia Sheinbaum informó que la @SEMARNAT_mx realiza un análisis muy detallado sobre el proyecto turístico 🌊 de la empresa Royal Caribbean en Mahahual, Quintana Roo. Aseguró que no se permitirá ninguna obra que ponga en riesgo el equilibrio ecológico en la zona. pic.twitter.com/dpMolqYgDk

— IMER Noticias (@IMER_Noticias) May 18, 2026

Shares of Royal Caribbean fell to session lows, down about 3% around 12:45 ET.

The stock is locked in a bear market year to date, down 26%, and appears set to test $250 support. Shares have faced resistance and peaked at around $367 in August 2025.

There was no immediate indication as to why Sheinbaum’s administration singled out Royal Caribbean, or whether the scrutiny was connected in any way to rising tensions with the Trump administration’s war against drug cartels or pressure campaign on Cuba.

Tyler Durden

Mon, 05/18/2026 – 18:50

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}