Category: News

“Shockingly Bad” Chinese Econ Data Stuns Wall Street, Sparks Hard Landing Concerns

“Shockingly Bad” Chinese Econ Data Stuns Wall Street, Sparks Hard Landing Concerns

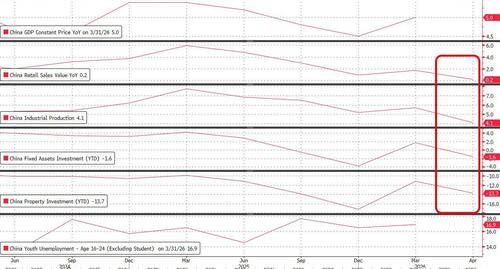

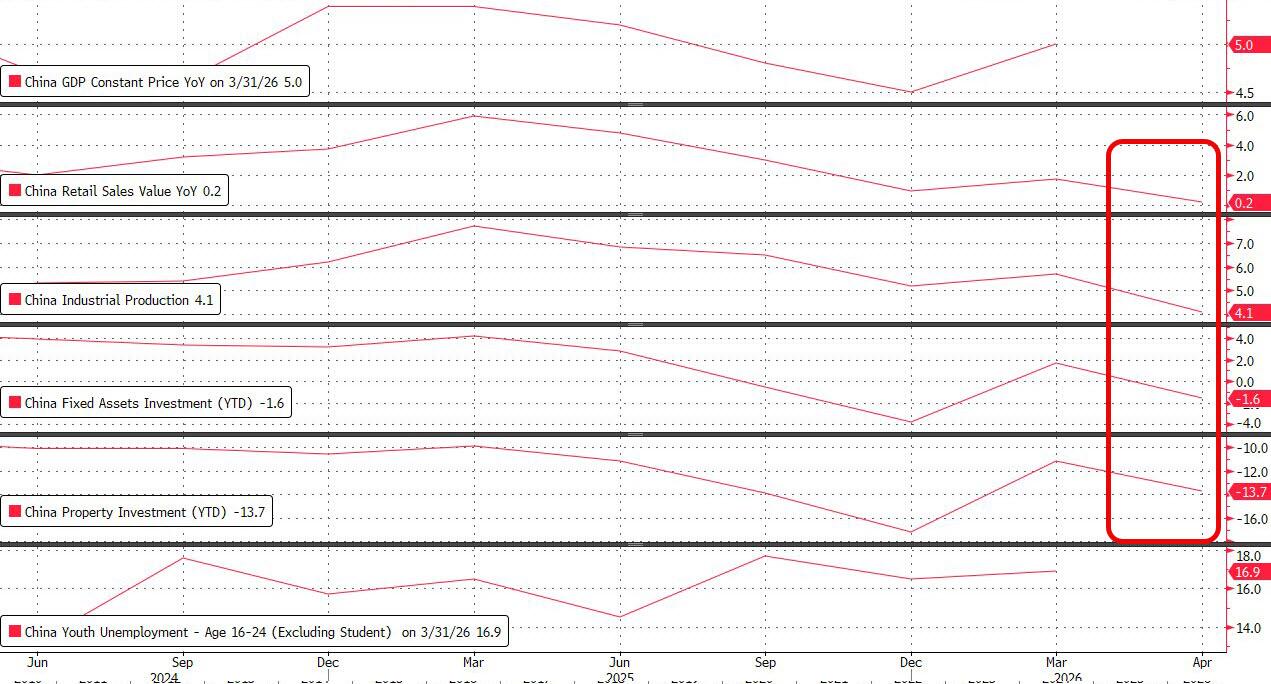

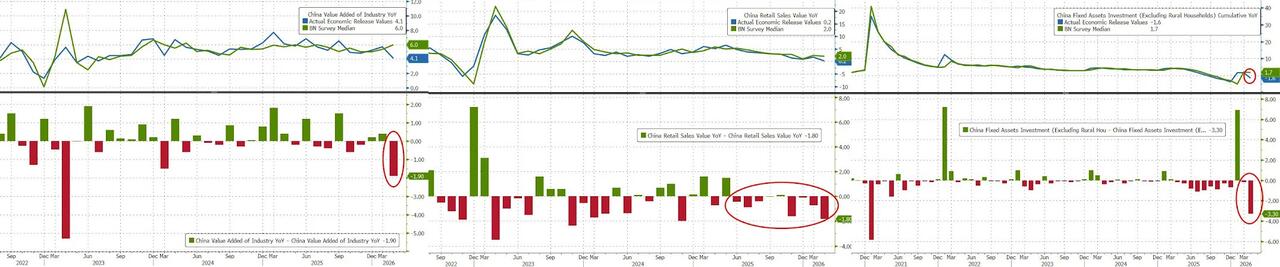

Confirming our Sunday preview, overnight China reported growth data which slowed across the board in April with investment resuming declines, retail sales missing sales and growing at the weakest rate in 4 years while industrial production rose at the slowest pace in three years, calling into question Beijing’s reluctance to add stimulus to the economy as a global energy crisis hits factories and consumers across the world.

China’s Monday data dump of official data on Monday painted a picture of an economy where booming exports no longer offset deteriorating consumption at home, prompting analysts at banks including Nomura and SocGen to urge bolder measures in support of growth.

As shown in the chart below, fixed-asset investment unexpectedly shrank 1.6% in the first four months of 2026 from a year earlier, while industrial production grew just 4.1% last month, the weakest in almost three years. Retail sales also missed forecasts and rose just 0.2% in April, the worst reading since they contracted in December 2022, when China reopened from Covid.

What is shocking is that it is common knowledge that Beijing traditionally massages its economic data to present itself in the rosiest possible light: the fact that it allowed data this ugly would suggest that the picture on the ground is much uglier.

Goldman’s Delta One head Rich Privorotsky captured this sentiment well, writing this morning that “overnight news from China showed economic data materially below expectations. Industrial production, retail sales and fixed asset investment all missed meaningfully. It’s hard to tell whether this reflects genuine demand destruction but perhaps it helps explain how the oil market has managed to balance despite ongoing supply concerns. I genuinely can’t remember a period when Chinese data, which tends to be heavily massaged, missed by anything close to this magnitude. Negative read through for consumption related categories.“

Remarkably, not a single economist surveyed by Bloomberg had predicted as pessimistic a reading for industry, retail sales and investment. The disappointing performance of the world’s second-biggest economy last month is a reminder of its domestic vulnerabilities, after a global artificial intelligence investment boom sent trade soaring.

The breadth of the acute slowdown in April has put the prospect of a more aggressive stimulus back on the agenda after China stood out in its resilience to the fallout from the Iran war. The government pulled back on fiscal spending in March, while the central bank has steered clear of even hinting at any further loosening in policy, amid ample market liquidity and weak demand for credit.

Fu Linghui, spokesman for the National Bureau of Statistics, described the deterioration of economic indicators as “a normal fluctuation from month to month.” But he also highlighted challenges such as a persistent imbalance between supply and demand as well as a complex global environment.

Investment plunged by around 8% in April from a year earlier, according to estimates from Goldman Sachs and Capital Economics, returning to a similar pace of decline seen in the second half of 2025. Manufacturing and infrastructure investment both weakened, while private investment plummeted

In response to the dismal data, Nomura economists wrote that authorities “might need to step up policy support for stabilizing growth,” adding that “Beijing has no room for complacency.”

A rising number of economists has been forecasting the People’s Bank of China won’t lower interest rates this year after the oil shock pushed up inflation expectations, though many still expect a cut to lenders’ reserve requirement ratio. The PBOC last lowered the policy rate and the RRR at the peak of the trade tensions with the US a year ago.

Authorities are still likely to take a patient approach and avoid rushing out response to just one month of data. The Communist Party’s decision-making Politburo will convene in July to review economic growth and policies, making it the next potential window for any adjustment in stimulus.

“The stance still seems to be to play cautiously,” said Jing Liu, chief economist for Greater China at HSBC in an interview on Bloomberg TV. “Our base case is no extra stimulus for the economy for the time being.”

Even though many manufacturers are struggling to cope with higher raw material costs, overall exports soared as Chinese tech products found willing buyers abroad. Greater demand for green energy products is also benefiting China. But a sustained weakening of investment and consumption at home could still bring risks to Beijing’s goal of achieving 4.5% to 5% artificial growth this year.

The April data suggest gross domestic product may expand as little as 4.1% on-year in the second quarter, which could prompt incremental policy easing, according to Macquarie Group Ltd. For now, Goldman is maintaining its forecast for a GDP gain of 4.7% in April-June, compared with 5% in the first three months of the year.

The data “should keep PBOC easing – RRR and even rate cuts – firmly on the table, while fiscal top-up may come later,” SocGen’s head China economist Wei Yao wrote in a note.

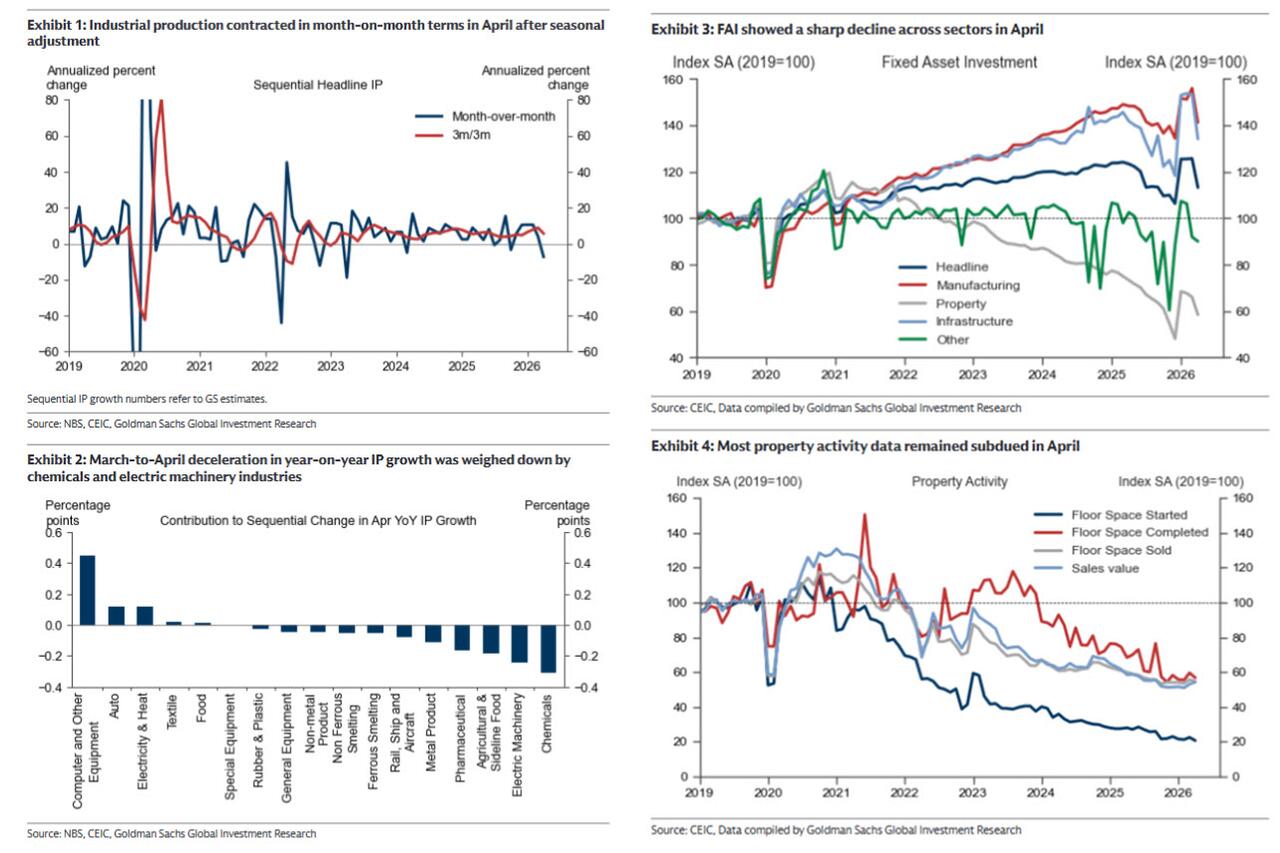

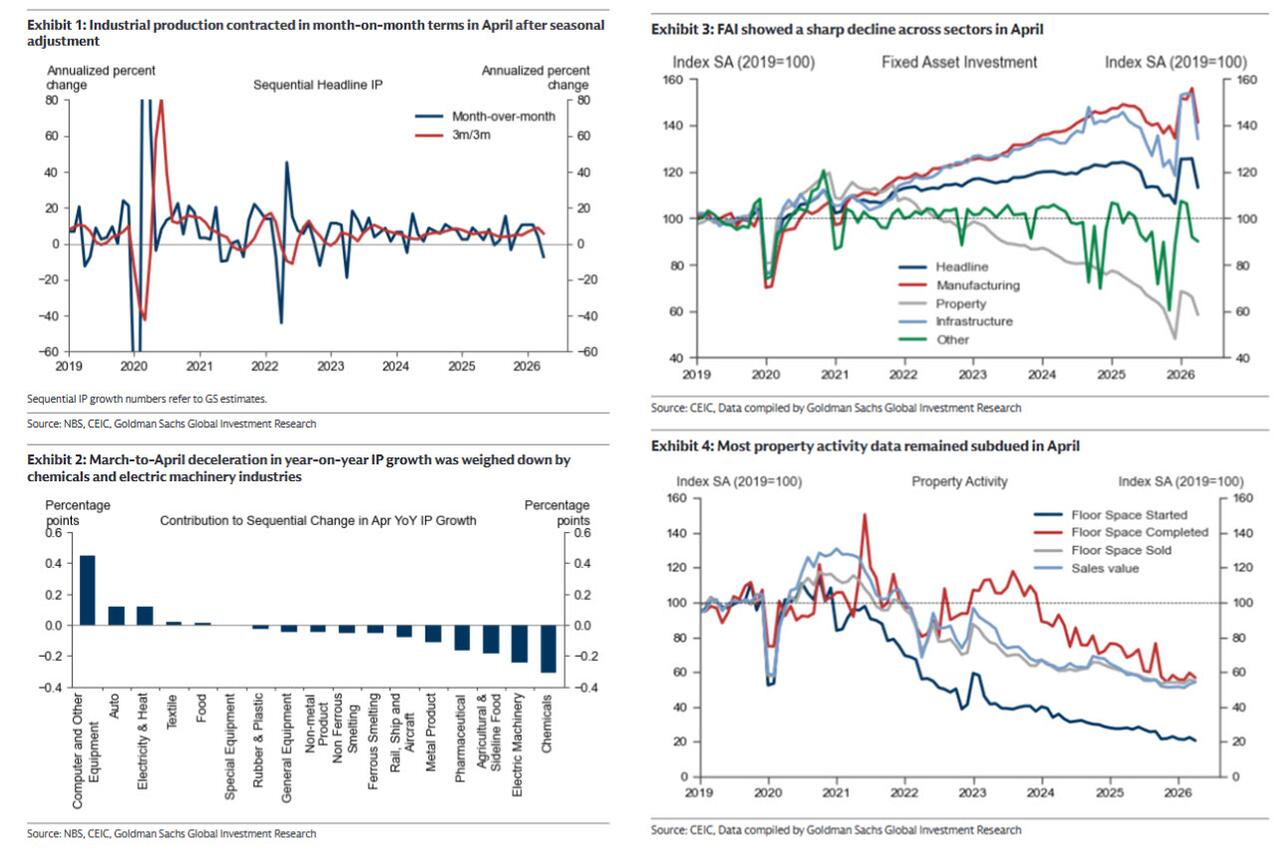

The plunging manufacturing data comes at a time of continued dismal credit demand and heavy rainfall in southern China, which could be behind the sharp fall in capital spending, Goldman economist Lisheng Wang said in a note (available to pro subs here).

Statistical adjustment is another potential factor. Many economists believe authorities took measures to correct over-reporting of the data in late 2025. Such a change may have exaggerated the volatility of the figures recently, as the on-year contraction in steel and cement output narrowed in April, according to Goldman Sachs.

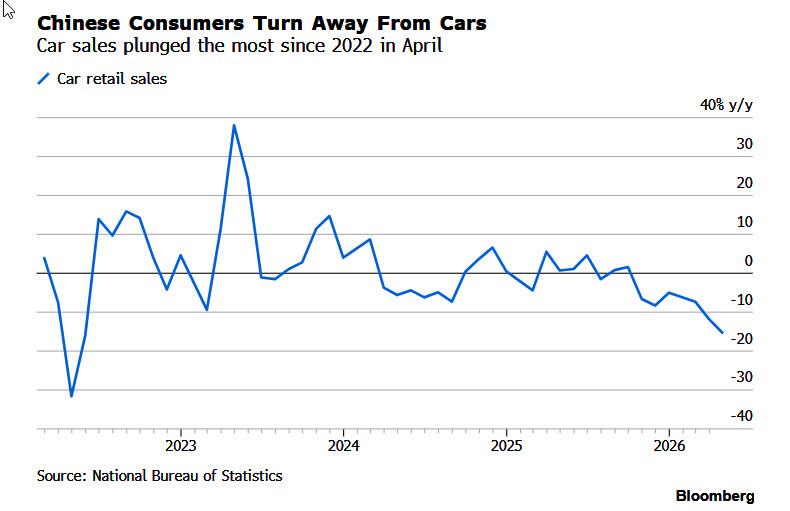

The consumer economy has meanwhile continued to struggle as households spent less on items as varied as autos and furniture. Car sales plunged 15% in April from a year earlier, the worst contraction since mid-2022, when the country was under Covid restrictions. The government has scaled back subsidies for electric vehicle purchases this year, while the Iran oil shock hurt sales of gasoline-powered cars.

Purchases of home appliances and furniture — products that used to be buoyed by government subsidies — declined at a double-digit pace. Gold, silver and jewelry sales plummeted 21% — a huge reversal from earlier this year and 2025, when soaring prices for precious metals led to a speculative investment frenzy.

The industrial sector is also getting more lopsided as export-driven sectors lead the growth while industries that relied on domestic sales lagged. The production of electronics, lifted by soaring global demand for AI chips, expanded 15.6% in April, the fastest pace in two years.

The auto industry also expanded briskly at 9.2%, as overseas EV sales took off. Meanwhile, commodities linked to real estate and construction — such as cement, glass and steel — recorded declines, while crude oil processing volume fell, which ING Bank economist Lynn Song attributed to the war’s impact

Soaring chip prices may partly explain why factory output weakened even as exports surged. While industrial production is reported after an adjustment made for inflation, sales abroad are calculated in nominal terms, making it hard to separate movements in prices versus volumes. Surging costs of chips and electronics accounted for about half of April’s 14% headline export growth, according to Nomura.

“China still looks like a two-speed economy: strong in strategic manufacturing and exports, but weak where household confidence matters most,” said Charu Chanana, chief investment strategist at Saxo Markets in Singapore. “The concern is not just that activity missed, but that the weakness is broadening across the domestic side of the economy.”

There is one silver lining when it comes to the Chinese economy: exports are expected to remain strong after climbing 15% in the first four months from a year ago. Stabilizing trade ties with the US, reinforced by President Donald Trump’s visit to Beijing, further bolster the outlook.

But a turnaround is nowhere in sight for domestic consumption. Chinese households net repaid the most loans in April since comparable data going back to 2010.

“Policy space remains ample,” said Hao Zhou, chief economist at Guotai Junan International Holdings. “The April data are less a sign of deterioration than a trigger for more proactive easing — which should help anchor growth and support a gradual recovery into the second half of the year.”

Tyler Durden

Mon, 05/18/2026 – 10:30

Ukraine’s Odesa Heavily Attacked In ‘Retaliation’ For Deadly Drone Raids On Moscow

Ukraine’s Odesa Heavily Attacked In ‘Retaliation’ For Deadly Drone Raids On Moscow

The Russian Defense Ministry (MoD) announced Monday that its forces executed a massive missile and drone barrage across Ukraine, which is clearly the expected big retaliatory response following Ukraine’s large-scale drone wave attack on Moscow over the weekend.

Kremlin officials specifically described the new assault as indeed direct retaliation for “terrorist attacks” carried out by Kiev, which killed at least three in the Russian capital, injured dozens, hit a refinery, and unleashed havoc and fear among the population. The MoD said it targeted military and defense industrial sites, but Ukraine’s account differed.

Ukrainian forces had deployed at least 130 UAVs during the capital-bound raid, and damaged a major regional airport. Large fires were spotted near major roadways, sometimes in the heart of busy city areas.

Russia’s nighttime into early Monday retaliation has been expectedly fierce, as overnight it specifically targeted Odesa and Dnipro, leaving at least one person dead and over 30 injured. In the port city of Odesa, the drone strikes damaged residential buildings, a school, and a kindergarten, according to Ukrainian officials.

Prior illustrative image: via NBC

Ukrainian media chronicled some of the following:

On Sunday, Russia carried out a combined overnight attack on the city of Dnipro, striking a residential area, sparking multiple fires, and causing casualties.

According to the Ukrainian Air Force, Russian forces began launching drones toward Dnipro at approximately 8 p.m.

On Monday, May 18, at 2:32 a.m., Ukraine was under threat of ballistic missile strikes. Shortly afterward, missiles were detected heading toward Dnipro, including both ballistic and cruise missiles.

According to local authorities, Russian drones struck three residential buildings in Odesa’s Kyivskyi and Prymorskyi districts.

One of the buildings, a single-story house in the Prymorskyi district, was completely destroyed. Other buildings sustained damage to facades, roofs, and windows. Several fires broke out but were quickly extinguished.

But Ukraine’s cross-border drones have also continued unabated, as two people were killed and two more were injured following a a Monday UAV attack on Russia’s southern Belgorod region, local authorities said. Belgorod has come under regular attack since near the start of the war, given its southern-most location, close to the front-lines to the south in Ukraine.

Meanwhile, Kremlin announced Monday that Moscow anticipates an eventual resumption of the Russia-Ukraine peace process, though it noted that negotiations are currently paused.

Kremlin spokesman Dmitry Peskov made the statement in response to comments from President Trump, who on Friday suggested that a Russian missile strike hitting a Kiev residential building had delayed progress toward ending the four-year conflict.

Per the Associated Press, “The death toll from a Russian missile attack that flattened a Kyiv apartment building rose Friday to 24, including three teenagers, Ukrainian President Volodymyr Zelenskyy said as he led the mourning for one of the deadliest attacks on the capital in the 4-year-old war.”

Цієї ночі росія атакувала #Одесу безпілотниками: є постраждалі

Внаслідок влучання виникла пожежі та руйнування в житлових будинках. Попередньо 2 постраждалих, з них – дитина. Пожежі ліквідовані.

Від ДСНС залучалися понад 80 рятувальників pic.twitter.com/hFM1dSqyei

— DSNS.GOV.UA (@SESU_UA) May 18, 2026

“The cruise missile hit the nine-story corner apartment block Thursday during what the Ukrainian air force said was Russia’s biggest barrage on the country of the full-scale invasion. Emergency workers finished digging through the rubble searching for victims after more than a day, Zelenskyy said on X,” the report adds.

But in response, Peskov emphasized that focus should also be directed toward persistent Ukrainian strikes targeting civilian infrastructure inside Russia.

Tyler Durden

Mon, 05/18/2026 – 10:10

Cars Are Fast Becoming Dystopian Prison Pods…

Cars Are Fast Becoming Dystopian Prison Pods…

Authored by Steve Watson via Modernity.news,

The surveillance state has found its newest frontier: your car’s dashboard. What used to be a symbol of American freedom and independence is rapidly morphing into a high-tech cage that watches your every move and can override your decisions at will.

In a widely shared post on X, users detailed complaints pouring in about Subaru’s upgraded AI ‘EyeSight’ system now featured on the latest models.

Drivers report the system pouncing on brief glances away from the road – while Biden-era federal mandates prepare to make this level of surveillance mandatory in every new vehicle by 2027.

Subaru has released a new “EyeSight system” on their new vehicles

Drivers who bought the cars are saying if you glance off the road for a second to look at the mountains, or change a song, the vehicle starts alerting

It will also stop the car by using its ‘Emergency Stop Assist… pic.twitter.com/o0uAgLm58r

— Wall Street Apes (@WallStreetApes) May 16, 2026

As the video highlights, even a momentary glance to change a song or take in the scenery triggers relentless alerts. The technology doesn’t stop there.

Its new Emergency Stop Assist with Safe Lane Selection feature can detect what it calls an “unresponsive” driver, issue escalating warnings through sounds and steering wheel vibrations, and then take full control: automatically braking, slowing the vehicle, steering it to the shoulder, and activating hazard lights.

This isn’t some optional gimmick. It’s being rolled out as standard “safety” tech, but drivers are calling it exactly what it feels like – an overbearing electronic babysitter that treats competent adults like distracted children.

It serves as a chilling preview of where the entire auto industry is headed under government pressure.

This kind of intrusive monitoring is precisely the tool a police state would dream of to exert total control over personal movement. If authorities gain deeper integration with these systems, they could effectively decide when, where, and if you get to drive at all.

The Subaru rollout is just the latest flashpoint in a broader push toward vehicle surveillance that goes far beyond basic safety. A federal mandate buried in the 2021 Infrastructure Investment and Jobs Act requires all new passenger vehicles sold in the U.S. to include advanced impaired-driving prevention technology starting with 2027 models.

As detailed in reporting from the New York Post, this means infrared cameras and sensors constantly monitoring eyes, faces, head position, and behavior to detect distraction, drowsiness, or impairment – with the power to prevent the car from starting or limit its operation. https://nypost.com/2026/04/30/us-news/sinister-in-car-spy-tech-that-can…

Automakers are already patenting and deploying even more aggressive systems, including biometric scans that analyze everything from your gait to your heart rate. Privacy advocates warn the data won’t stay in the car – it could flow to insurers for risk scoring, law enforcement, or worse.

As we also recently highlighted, dystopian technology including AI face scanning, lip reading and emotion monitoring is being deployed in vehicles, as well as cross-checks for drivers against police databases before even allowing the vehicle to move.

And authorities are already signaling their eagerness to weaponize these tools for broader travel restrictions. In Massachusetts, Democrats advanced a bill aimed at reducing statewide vehicle miles traveled to meet climate targets, pushing policies that critics say amount to limiting how far people can drive in their own cars.

X users are reacting with the outrage this deserves, blasting the tech as the thin end of the wedge for total control:

Subaru just turned your car into a fvcking SNITCH. Look away for 2 seconds? BEEP BEEP, vibrate, and then it drives itself off the road like Karen on crack. Government wet dream 1984 Orwellian bullshit. 😒 Boycott these traitors. 🔥

— J. L. Hunter (@JLHunter1984) May 16, 2026

So, this thing will go off if you look into your mirrors or over your shoulder to see if it’s safe to take a turn, or change lane, or to brake. What a GREAT idea. Lets all tunnel vision on what’s in front of us and ignore everything else. What could possibly go wrong?

— sam (@donder172) May 16, 2026

Can only imagine what it would do if it knew you voted for a republican.

— Amos 9 Fifteen (@Amos467253) May 16, 2026

nice.

refuse to purchase a car like this.

simple as.

if they all go bankrupt, they will stop this shit. pic.twitter.com/8N5WQnMVyx

— HumanProbably (@HumanProbably2) May 16, 2026

It must be stopped and waiting for some genius aftermarket design to override. Kill it. Kill all surveillance that’s being rolled out. It must be destroyed.

— L. (@LisaFMRRN) May 16, 2026

Globalist climate agendas, big government overreach, and corporate-government collusion are converging to strip away the last vestiges of personal autonomy on the open road. What starts as “safety features” and “environmental goals” ends with your car deciding whether you’re allowed to leave your driveway.

Americans have always valued the freedom to get behind the wheel and go where they please without Big Brother riding shotgun.

These prison pods represent the opposite vision – one of constant monitoring, automated intervention, and restricted mobility.

The only real answer is rejection: refuse to buy these surveilled vehicles, support politicians who fight the mandates, and preserve the used car market as the last refuge of actual driving freedom.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Mon, 05/18/2026 – 09:50

https://www.zerohedge.com/technology/cars-are-fast-becoming-dystopian-prison-pods

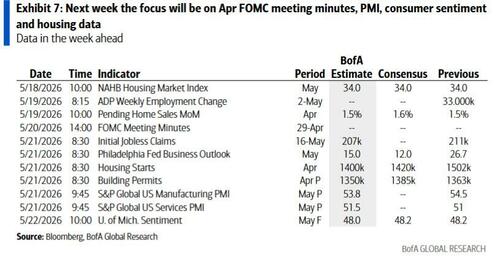

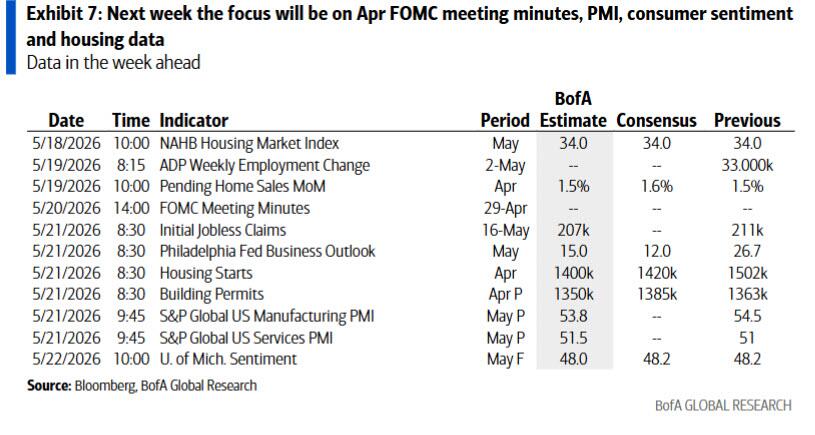

Key Events This Week: Nvidia Earnings, FOMC Minutes And Global PMIs

Key Events This Week: Nvidia Earnings, FOMC Minutes And Global PMIs

Looking at the week ahead, Nvidia’s earnings on Wednesday, with a market capitalisation now of $5.46tn, will be the main event. In economics, we have the global flash PMIs on Thursday, along with inflation data from Canada tomorrow, the UK on Wednesday, and Japan on Friday. From central banks, the highlight will be the FOMC minutes on Wednesday. Those flash PMIs will be important, as they’re one of the first indicators on how the global economy has performed this month, so will be scrutinized for any signs of how the war in Iran is impacting activity and prices.

The US calendar is relatively light, with the NAHB housing market index today expected to remain unchanged at a cyclically low 34, followed by Tuesday’s pending home sales, where a modest +1.0% increase is anticipated (from +1.5% previously). Attention will then turn to Thursday’s April housing activity data, where housing starts are expected to ease to an annualized pace of 1.425mn (from 1.502mn), while permits are projected to tick higher to 1.375mn (from 1.363mn). All estimates are according to our economists.

Beyond housing, Thursday is the key day for macro releases. The weekly initial jobless claims are expected to edge slightly lower to 209k (from 211k). The same day will also bring the Philadelphia Fed manufacturing survey, where our economists expect a pullback to +21.0 (from +26.7), alongside the flash PMIs. In the US, manufacturing is expected to soften marginally to 53.7 (from 54.5), while services are seen ticking up to 51.5 (from 51.0).

In contrast to consumer sentiment—which will see an updated reading of the Michigan survey on Friday (expected at 48.2 versus 49.8 previously)—business surveys have generally remained more resilient despite the energy shock. That said, some indicators have shown rising input costs and lengthening delivery times, developments that could signal renewed inflationary pressure building beneath the surface.

Turning to central bank communications, the Fed speaker slate is relatively limited but still notable. Governor Waller is scheduled to participate in an ECB policy panel tomorrow, alongside comments from Philadelphia Fed President Harker (voter) on the outlook. On Wednesday, Vice Chair Barr will discuss consumer financial health metrics, while the Fed will also publish the minutes from the April FOMC meeting. Richmond Fed President Barkin (non-voter) will follow on Thursday with remarks on the economy, before Governor Waller rounds out the week with a further appearance on Friday.

In Europe, the highlights will include the UK labour market report tomorrow and inflation data on Wednesday. DB’s UK economist expects headline CPI to slow to 2.98% YoY and core CPI to fall to 2.61% YoY. More detail and forecasts are in the full inflation spotlight note here. The UK will also release the GfK May consumer confidence index and April retail sales on Friday. Other notable European releases include Eurozone consumer confidence on Thursday and Germany’s Ifo survey on Friday.

In Asia, Japan faces a busy week, with key data including Q1 GDP tomorrow and April nationwide CPI on Friday. Our Chief Japan economist expects positive real growth of an annualised 1.3% QoQ for the GDP report and sees core CPI inflation, excluding fresh food, holding at 1.8% YoY, alongside a retreat in core-core inflation, excluding fresh food and energy, to 2.2% (from 2.4% in March).

Finally, beyond Nvidia’s earnings on Wednesday, results are also due from major US retailers, including Walmart, Home Depot, and TJX.

Courtesy of DB, here is a day by day calendar of the week’s main events:

Monday May 18

Data: US May New York Fed services business activity, NAHB housing market index, March total net TIC flows, China April retail sales, industrial production, investment, home prices, Italy March trade balance

Central banks: BoE’s Greene and Mann speak

Earnings: Baidu, Ryanair Holdings

Other: G7 meeting of finance ministers and central bank governors (through May 19)

Tuesday May 19

Data: US April pending home sales, UK March average weekly earnings, unemployment rate, April jobless claims change, Japan Q1 GDP, March capacity utilisation, Eurozone March trade balance, Canada April CPI, March building permits

Central banks: Fed’s Waller speaks, ECB’s Lane and Makhlouf speak, BoE’s Breeden speaks

Earnings: Home Depot, Amer Sports

Wednesday May 20

Data: UK April CPI, RPI, PPI, March house price index, Germany April PPI, Denmark Q1 GDP

Central banks: FOMC minutes, Fed’s Paulson and Barr speak, China 1-yr and 5-yr loan prime rates

Earnings: NVIDIA, Analog Devices, TJX, Lowe’s, Intuit, Target, Experian, Marks & Spencer

Auctions: US 20-yr Bonds ($16bn)

Thursday May 21

Data: US, UK, Japan, Germany, France and Eurozone May preliminary PMIs, US May Philadelphia Fed business outlook, Kansas City Fed manufacturing activity, April housing starts, building permits, initial jobless claims, Japan April trade balance, March core machine orders, Italy March current account balance, ECB March current account, Eurozone March construction output, Q1 labour costs, May consumer confidence, Australia April labour force survey

Central banks: ECB’s Villeroy speaks, BoJ’s Koeda speaks, BoE’s Taylor speaks

Earnings: Walmart, Deere, Generali, Ross Stores, Take-Two, BT, Zoom, Workday

Auctions: US 10-yr TIPS (reopening, $19bn)

Friday May 22

Data: US May Kansas City Fed services activity, UK May GfK consumer confidence, April retail sales, public finances, Japan April national CPI, Germany June GfK consumer confidence, May Ifo survey, France May business confidence, Canada March retail sales, April industrial product price index, raw materials price index

Central banks: Fed’s Waller speaks, ECB’s Vujcic, Kazimir, Muller and Lane speak

Earnings: Cie Financiere Richemont, Lenovo

Taking a look at just the US, Goldman writes that the key economic data release this week is the Philadelphia Fed manufacturing index on Thursday. There are several speaking engagements with Fed officials this week, including events with Governors Waller and Barr and Presidents Paulson and Barkin. The minutes to the FOMC’s April meeting will be released on Wednesday.

Monday, May 18

10:00 AM NAHB housing market index, May (consensus 34, last 34)

Tuesday, May 19

08:00 AM Fed Governor Waller speaks: Fed Governor Christopher Waller will participate in a panel at the European Central Bank. Moderated Q&A is expected. On April 17th, Waller cautioned that higher oil prices as a result of the Iran war could lead to a “more lasting increase in inflation.” Waller noted that “if the risks to inflation outweigh those to the labor market,” that could require “maintaining the policy rate at the current target range.”

10:00 AM Pending home sales, April (GS +1.0%, consensus +1.0%, last +1.5%)

07:00 PM Philadelphia Fed President Paulson (FOMC voter) speaks: Philadelphia Fed President Anna Paulson will speak about the economic outlook at the Atlanta Fed’s Financial Markets Conference. Text and audience Q&A are expected. On March 27th, Paulson said that there was “a little bit more of a risk that the transmission of higher fuel prices, higher fertilizer prices, into inflation expectations is faster and maybe a little bit more durable.” That said, Paulson also noted that “for [all these shocks] to turn into sustained inflation, you need a mechanism that keeps that going” and that “on the wage-setting side, it doesn’t seem like there’s a lot of impetus that would make that happen now.”

Wednesday, May 20

09:15 AM Fed Governor Barr speaks: Fed Governor Michael Barr will deliver a speech on consumer financial health at a conference in Atlanta, Georgia. Text is expected. On May 5th, Barr said that “the longer [the Iran war] goes on, the greater the risk that the inflation we’re seeing in these prices becomes embedded in the economy, and then we have to worry more.” Barr noted that “we’re in a situation right now where we really need to wait and see to understand what direction [the conflict] is going.”

02:00 PM FOMC meeting minutes, April 28-29 meeting: At its April meeting, the FOMC left the fed funds rate and the policy guidance in its statement unchanged. Presidents Hammack, Logan, and Kashkari dissented against the implicit easing bias in the standing policy guidance, while Governor Miran dissented in favor of a 25bp cut. Chair Powell said that the number of FOMC participants who could support moving to balanced guidance has increased since March and that the center of the FOMC “is moving toward a more neutral” outlook for future rate changes, but most felt making a change now was unnecessary. We pushed back our expectations for Fed cuts by one quarter to December and March. With energy cost passthrough likely to keep year-over-year core PCE inflation closer to 3% than 2% all year, we think that a combination of lower monthly inflation prints after the oil shock fades and further labor market softening will likely be needed for the FOMC to cut this year. We still expect that bar to be met but now expect it to take a bit longer.

Thursday, May 21

08:30 AM Initial jobless claims, week ended May 16 (GS 210k, consensus 210k, last 211k); Continuing jobless claims, week ended May 9 (consensus 1,785k, last 1,782k)

08:30 AM Philadelphia Fed manufacturing index, May (GS 20.0, consensus 18.0, last 26.7)

08:30 AM Housing starts, April (GS -3.5%, consensus -5.5%, last +10.8%)

09:45 AM S&P Global US manufacturing PMI, May preliminary (consensus 53.7, last 54.5); S&P Global US services PMI, May preliminary (consensus 51.0, last 51.0)

12:20 PM Richmond Fed President Barkin (FOMC non-voter) speaks; Richmond Fed President Tom Barkin will deliver a speech at the Urban Land Institute Triangle in Raleigh, North Carolina. Text and Q&A are expected.

Friday, May 22

10:00 AM University of Michigan consumer sentiment, May final (GS 48.2, consensus 48.3, last 48.2); University of Michigan 5-10-year inflation expectations, May final (GS 3.4%, last 3.4%)

10:00 AM Fed Governor Waller speaks; Fed Governor Christopher Waller will deliver a lecture on the economic outlook at the Frankfurt School of Finance and Management in Germany. Text and moderated Q&A are expected.

Source: Goldman, DB

Tyler Durden

Mon, 05/18/2026 – 09:25

https://www.zerohedge.com/markets/key-events-week-nvidia-earnings-fomc-minutes-and-global-pmis

The Question This Week Is “Does Trump Go Back To The Well On Bombing Iran?”

The Question This Week Is “Does Trump Go Back To The Well On Bombing Iran?”

By Benjamin Picton, Senior Market Strategist at Rabobank

Hormuz diary, day 79. The strait remains functionally closed and global crude and refined product stocks are rapidly drawing down. President Trump has returned from Beijing after much bonhomie with no concrete commitments from China to help get shipping moving again, though the American side has claimed that China wants the strait to re-open with no tolls imposed and has committed to buy at least $17bn of US agricultural products annually.

Trump is running out of patience, and has told Iran that “the clock is ticking” before US strikes resume. Asia is running out of fuel.

Iran has established a new protocol for allowing ships to pass the strait. Araghchi says the strait is “open to all commercial ships”, the IRGC says that Chinese ships are being allowed to pass, Iranian state TV said that “more than 30 ships” had been allowed to pass between Wednesday and Thursday, and that that number is set to accelerate. Nobody seems to know how many of the 30 ships were not Chinese.

George Prokopiou’s Karolos ran the strait with its tracking system switched off, carrying a cargo of 1 million barrels of Iraqi crude bound for India. A Panamanian-flagged vessel managed by Japanese refiner ENEOS snuck through on Friday, and several other ships also passed through Hormuz into the Gulf of Oman.

Bond markets are no longer taking this all in their stride. Yields on US 10s rose 24bps last week, 10-year Gilt yields lifted 26bps. Last week’s hotter-than-expected April US CPI reading of 3.8% conspired with PPI ex food and energy of 5.2%, and strong payrolls data the week before to see the 5y-5y inflation swap creep up to 2.47%. The OIS curve says rate hikes, Kevin Warsh’s ascension as Fed Chair notwithstanding. Gundlach says the Fed can’t possibly cut. Bloomberg says traders are eyeing a tipping point towards a new era of higher yields. A graph of the 10-year says that the tipping point came all the way back in 2022 for those who were paying attention. CPI has now been above target for more than five years. Inflation can-kicking in the 1970s gave us the Volcker Shock later on.

The S&P500 closed down 1.25% on Friday. Futures are -0.7% this morning. Asian stocks are getting battered. The DXY is bid and high beta FX is being offered. Even the hitherto immortal Aussie housing market is beginning to creak as auction clearance rates hit their lowest levels since the pandemic lockdowns of 2020. The headwind of higher rates and lower real incomes is now compounded by tax changes aimed at discouraging investors. Has Australia picked up on the end of neoliberalism zeitgeist to shift from a Thatcherite home-owning democracy to Xi Jinping-style common prosperity where “houses are for living in”? Is there no-one left to buy after government became the liquidity of last resort through first home buyer co-ownership programs last year?

While markets fret over the outlook, the question this week is “does Trump go back to the well on bombing Iran?” Einstein said that doing the same thing over and over again while expecting different results is the definition of insanity; Oscar Wilde said that consistency is the last refuge of the unimaginative. CENTCOM commander Brad Cooper says the Iranian military industrial base is 90% degraded and Scott Bessent says that Iranian crude is going to have to go back to the well as the US blockade brings shut-ins ever closer. The CIA says Iran still has 70% of its pre-war missiles and can hold out under blockade for months. Who is talking their own book? Is the US government as faction-ridden as the Iranian government is supposed to be?

In the meantime, escalation risks mount. A drone struck close to the UAE’s Barakah nuclear plant over the weekend and Saudi Arabia reportedly intercepted three drones directed at its own territory. Ukraine is stepping up attacks on targets deep inside Russia even as Russia pounds Ukrainian territory. Ukraine mounted its largest attack on the Moscow region in more than a year, targeting high-value military assets, oil facilities, Moscow’s main airport, and a sanctioned semiconductor factory. Zelenskyy saying there has been a “shift in the balance” on the battlefield.

As we sit here in 2026 Russia’s ‘Special Military Operation’ originally been planned to conclude within weeks is now in its fifth year. In uncomfortable similarity, the US’s 4-6 week ‘targeted military campaign’ is now in its 12th week. Finding common ground in peace negotiations continues to prove elusive in both cases, making stalemate the path of least resistance. Central banks and many governments continue to base forecasts on a near-term resolution in Iran that sees the Strait of Hormuz fully re-open to shipping. Seemingly everybody has a Schlieffen Plan where they will be home by Christmas.

Financial markets are no different. While markets might be waiting for the restart of a bombing campaign in Iran to send physical crude prices and prompt spreads sharply higher (and stock prices sharply lower), for physical supply chains in Asia getting back to the (oil) well becomes more pressing by the day. Hot war is certainly bad, but a grinding stalemate would be disaster enough.

Tyler Durden

Mon, 05/18/2026 – 09:10

https://www.zerohedge.com/markets/question-week-does-trump-go-back-well-bombing-iran

Space Stocks Take-Off On Musk’s SpaceX IPO Comments

Space Stocks Take-Off On Musk’s SpaceX IPO Comments

AST SpaceMobile, EchoStar, and Rocket Lab moved higher in premarket trading in New York after Elon Musk, speaking by video at the Samson International Smart Mobility Summit on Monday, said a SpaceX IPO is coming “pretty soon,” adding to investor hype around the publicly traded space industry.

“We’ve got to get the SpaceX IPO stuff going here pretty soon,” Musk told the summit, which was taking place in Tel Aviv, via video call.

Elon: “I would be there in person, but we gotta get this @SpaceX IPO going pretty soon.”

👀🚀 https://t.co/6uwiDKS9of pic.twitter.com/yGVMTm7qmg

— Sawyer Merritt (@SawyerMerritt) May 18, 2026

Shares of EchoStar were up about 3.5% in premarket trading. AST SpaceMobile and Rocket Lab also moved higher by about 2.5% after Musk’s comments earlier today.

On Friday, Reuters reported that SpaceX has selected Nasdaq for its long-awaited IPO and is targeting a June 11 pricing date, followed by a June 12 debut under the ticker “SPCX.”

The Polymarket bet on SpaceX’s symbol “SPCX” has hit 93%.

Will SpaceX’s public ticker be another ticker?

Yes 93% · No 7%

View full market & trade on Polymarket.

In April, SpaceX confidentially filed for an IPO with the SEC and is planning to disclose its prospectus as soon as next week, according to CNBC.

SpaceX’s IPO could raise upwards of $75 billion for the rocket company and dwarf Saudi Aramco’s $29 billion debut in 2019. The money raised would be used to fund an “insane flight rate” for the Starship rocket and to push ahead with deploying orbital data centers in low Earth orbit. The company’s valuation stands at around $1.75 trillion.

Other IPOs to watch in the second half include chatbot startups, such as OpenAI and Anthropic.

Tyler Durden

Mon, 05/18/2026 – 08:55

https://www.zerohedge.com/technology/space-stocks-launch-musks-spacex-ipo-comments

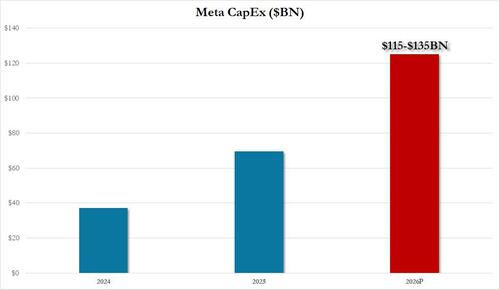

D-Day For “Huuuge” Meta Layoffs Looms As AI Job Apocalypse Accelerates

D-Day For “Huuuge” Meta Layoffs Looms As AI Job Apocalypse Accelerates

‘D-Day’ for Meta layoffs is quickly approaching, as the Facebook and Instagram owner will slash 10% of its global headcount – or about 8,000 employees – in the initial round as it swaps headcount for GPUs.

Former Meta employee Adel Wu described the current situation on X, saying her millennial and Gen Z friends still at the tech company are currently “either just waiting, hoping to get laid off or extremely anxious because the job is their lifeline.”

Welcome to the accelerating AI job apocalypse, affecting white-collar youngsters with lots of student debt.

Wu described the upcoming Wednesday layoff announcement as “huuge” and noted, “I remember the very first big layoff the night before was almost like doomsday, people were stuffing their bags with free snacks and drinks and chargers.”

during my last year at meta there were probably 4-5 layoffs, but this one on 5/20 is huuuge

my friends still there are either just waiting hoping to get laid off or extremely anxious because the job is their lifeline

i remember the very first big layoff the night before was… https://t.co/3fhVNzQjGn

— adel 🌟 (@adelwu_) May 16, 2026

Wu’s X post quoted Emily Dreyfuss of The San Francisco Standard, who provided additional color in a note about the incoming layoffs:

Next week, Meta is expected to lay off 8,000 employees(opens in new tab), roughly 10% of its global workforce, with about 500 of those cuts landing in the Bay Area.

They will join a worldwide tally of more than 100,000 tech workers laid off since January, with more on the horizon.

At Meta, employees are anxiously anticipating a 7 a.m. email Wednesday that will tell them their fate.

To these rank-and-file workers, the AI job apocalypse feels like it’s already here. And even as they fear their own replacement, they are being asked by management to use and train the very products that will soon take their jobs.

Dreyfuss quoted an anonymous Meta employee who said, “This is as anxious and stressed as I have ever been at a job.”

“If you’re on a work machine, you are probably being surveilled. But the framing that we are using this to train AI to do everyone’s job and the sort of unapologetic, ‘we’re training your replacement, and we’re not paying you more for it’ approach is just another signal of how little Meta cares about the humans that it employs,” the employee told Dreyfuss.

We previewed the coming job apocalypse for Meta in recent weeks:

Meta Plans 20% Layoffs To Divert Capital To Data Centers

Meta To Unleash First Wave Of Mass Layoffs May 20 As It Eliminates 10% Of Its Workers

… and this comes as CEO Mark Zuckerberg has been investing hundreds of billions of dollars into AI as he seeks to dramatically reshape his company’s core business around AI after Metaverse failures.

Meta is not alone: Amazon recently trimmed 30,000 corporate employees, representing nearly 10% of its white-collar workers. In February, the fintech company Block fired nearly half of its staff.

Layoffs. fyi, a website tracking tech job cuts worldwide, reported that 73,212 employees have lost their jobs so far this year. For all of 2024, the figure was 153,000.

Goldman laid out in 2023 just how many jobs AI will take. That number is absolutely scary for white-collar America, where many are saturated with student debt.

Tyler Durden

Mon, 05/18/2026 – 08:25

https://www.zerohedge.com/markets/d-day-huuuge-meta-layoffs-next-week-ai-job-apocalypse-accelerates

Oil Slides After Iran Says US Agreed To Lift Oil Sanctions During Negotiation Period

Oil Slides After Iran Says US Agreed To Lift Oil Sanctions During Negotiation Period

Tasnim news agency says Iran has submitted its latest proposal comprising 14 points through Pakistan. State sources say the focus by Iranian leadership is to end the war and build trust. This as Pakistan’s interior minister has extended his Tehran visit for a third day.

In this context a source close to the negotiating team reportedly told Tasnim that, unlike their previous texts, Washington agreed in the new text to lift Iran’s oil sanctions during the negotiation period. This is a first big sign of progress since the White House reportedly sent five ‘counter’ conditions to Tehran, which only offered a partial sanctions reduction.

Per more from Tasnim:

Waiving sanctions means temporarily lifting sanctions.

Iran insists that lifting all sanctions on Iran should be part of the US’s commitments.

However, the US has proposed suspending OFAC until a final understanding is reached.

The headline was enough to push oil down, erasing the gains over the weekend…

According to more of the latest headlines via Al Jazeera:

Iran’s Foreign Ministry spokesperson says talks between Iran and the US are continuing through Pakistan.

He added that Iranian and Omani technical teams met in Oman to negotiate a mechanism for ensuring safe transit in the Strait of Hormuz.

Kuwait and Qatar have condemned drone attacks on Saudi Arabia, which officials say originated from Iraqi airspace.

The Israeli army says it struck more than 30 targets in southern Lebanon, which it claims were used by Hezbollah to attack Israeli forces.

The Israeli navy has seized vessels that were part of the Gaza-bound Global Sumud Flotilla, arresting 100 activists on board.

And more developments via Newsquawk:

US President Trump warned on Truth Social that the clock is ticking for Iran and that they better get moving fast, or there won’t be anything left for them, and that time is of the essence.

US President Trump declined to give a specific deadline for negotiations with Iran and will hold a Situation Room meeting with his national security team on Tuesday to discuss possible options for military action, while he spoke with Israeli PM Netanyahu about the situation in Iran, according to Axios. Trump also stated that he still thinks Iran wants a deal and he is waiting for an updated Iranian proposal, which he hopes will be better than the prior offer. Furthermore, Axios’s Ravid reported that Trump threatened that attacks would resume with greater intensity if the Iranian regime does not come up with a better proposal, while Channel 12’s Kraus posted that President Trump said in a phone call that he thinks the Iranians should be afraid of what’s going on right now.

Pakistan shared revised Iranian proposal to end the war with the US on Sunday night, according to Pakistani sources. The course added that “we don’t have much time”, adding that both countries “keep changing their goalposts”.

Western sources say the new Iranian proposal includes a commitment of unclear value not to produce nuclear weapons but no mention of uranium or Hormuz, according to Journalist Segal.

Iranian Foreign Ministry Spokesperson Baghaei said talks with the US continue through Pakistani mediation. The spokesperson added that they have made great efforts for safe movement and protection of the Strait of Hormuz and are in constant contact with Oman to develop a mechanism. On Uranium, Baghaei said Tehran does not need any party to recognize its right to uranium enrichment and will not discuss during negotiations with the US.

Iranian Defence Ministry spokesman Brigadier General Reza Talaei-Nik warned of a regretful response to enemies and said that Iranian armed forces are fully prepared to confront any potential attack by the US and Israeli regime, according to IRNA.

Iranian Major General Rezaei said Iran is serious about diplomacy and negotiations, but is more serious about dealing with the aggressor, while he added that the US must now prove its good intentions and that Iranian armed forces are on the trigger as diplomatic efforts continue.

Iran said transit through the Strait of Hormuz would flow again once its conflict with the US and Israel is over, although the sides remain far from resolving their differences, according to Bloomberg. In relevant news, three cargo-empty, US-sanctioned tankers reportedly slipped through the US naval blockade in recent days, according to TankerTrackers.com.

Israel said it carried out a Gaza strike targeting the de facto head of Hamas’s armed wing, while Israel also conducted an airstrike on the towns of Froun, Kfar Hounah and Zawtar al-Sharqiya in southern Lebanon. Furthermore, an Israeli air strike targeted Baalbek, Lebanon and killed an Islamic Jihad commander and his daughter.

UAE officials said a drone attack set off a fire near the UAE’s nuclear power station, while it was still investigating the source of the attack.

Saudi Defence Ministry said it intercepted three drones launched from Iraq after entering the kingdom’s airspace.

* * *

While a Pakistani-mediated ceasefire managed to take effect on April 8, subsequent talks in Islamabad completely collapsed, but then President Trump later extended the truce indefinitely, likely to buy time and to figure out “what’s next” – while seeking a complete blockade of Iranian oil exports, and of all vessels entering or exiting Iranian ports. Currently the sides are merely trying to get back to the table.

Tyler Durden

Mon, 05/18/2026 – 08:10

“Please Work Remote”: NYC Braces For Commuter Chaos With Ongoing LIRR Strike

“Please Work Remote”: NYC Braces For Commuter Chaos With Ongoing LIRR Strike

Welcome to day three of the Long Island Rail Road strike, which is set to cause commuter chaos this morning in the New York City area, as more than 3,500 workers across five unions walked off the job Saturday after contract talks with the MTA collapsed.

Negotiations between the MTA and unions resumed Sunday and are set to continue Monday morning.

LIRR service remains suspended due to the strike. Please work from home if you can. If you must travel today, travel alternatives include:

• Limited shuttle bus service to/from six Long Island locations to Queens subway stations, for both the AM and PM rush hour.

• NICE Bus…

— LIRR (@LIRR) May 18, 2026

The MTA has urged riders to work remotely today and is deploying up to 275 free shuttle buses, though that capacity only covers a tiny fraction of the LIRR’s nearly 300,000 weekday riders.

It seems that Socialist NYC Mayor Mandami finally got his promise of free buses, but at the cost of a strike and commuter chaos.

The disruption could also snarl travel to Long Island beach destinations over Memorial Day weekend, including the Hamptons.

Some employers, including JPMorgan and Citigroup, have advised affected workers to consider remote work this week.

The National Mediation Board, a federal agency that oversees labor disputes, summoned both sides late Sunday evening to continue negotiations, but no resolution was found. Talks are expected later today.

A spokesman for the International Brotherhood of Teamsters stated that their wage proposal was reasonable and that two federal review panels had sided with them.

“We remain ready to negotiate a fair agreement at any time and get back to work on behalf of Long Island commuters,” the statement said.

The union wrote on X, “After more than three years with no raises, LIRR’s union workers, including 500 Teamsters locomotive engineers, will not make any more sacrifices to cover for the MTA’s mismanagement.”

Rail Teamsters from the @BLET and their union coalition remain on strike at the MTA-owned Long Island Rail Road.

After more than three years with no raises, LIRR’s union workers, including 500 Teamsters locomotive engineers, will not make any more sacrifices to cover for the… pic.twitter.com/acb6jGY6Fj

— Teamsters (@Teamsters) May 17, 2026

What an absolute mess for commuters this morning.

Tyler Durden

Mon, 05/18/2026 – 07:45

https://www.zerohedge.com/political/please-work-remote-nyc-braces-commuter-chaos-ongoing-lirr-strike

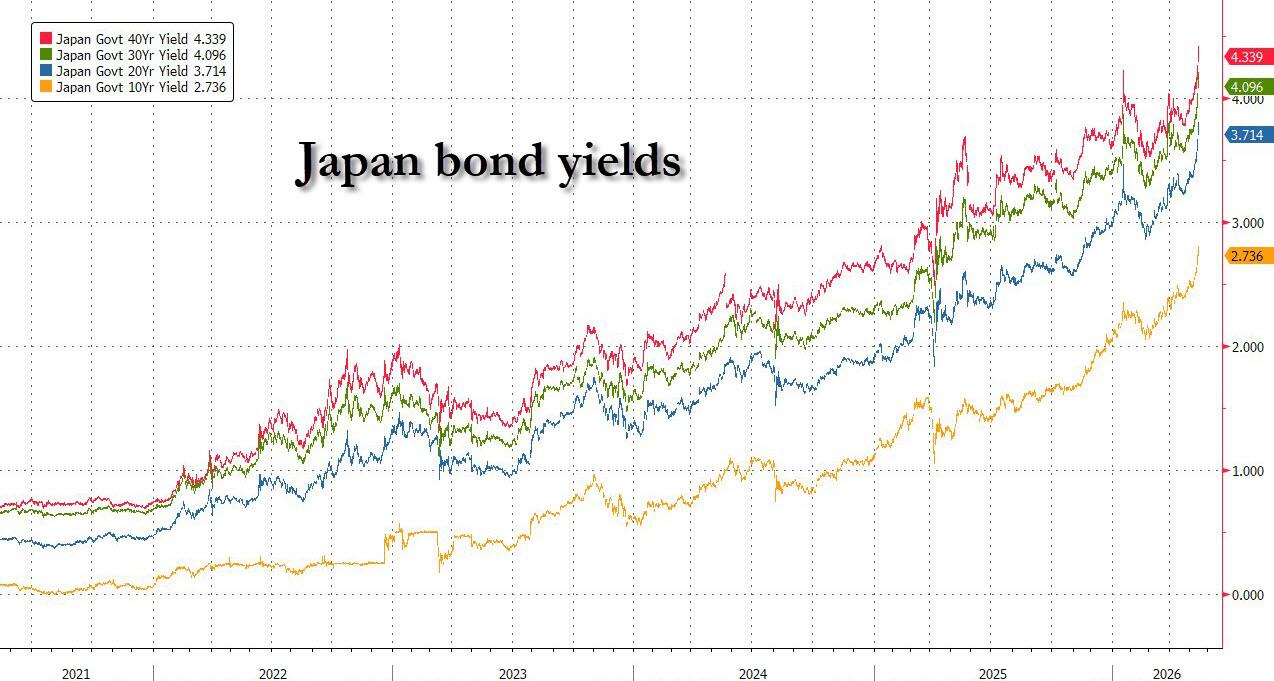

Futures Slide After Bond Yields, Oil Prices Jump Around The Globe

Futures Slide After Bond Yields, Oil Prices Jump Around The Globe

Futures are lower, but off their overnight lows as markets focus on soaring global yields after US/Iran talk progress remains stalled (but at least armed hostilities did not resume contrary to some speculation). Yields also spiked on rising oil prices, concerns of an extra budget in Japan and continued political chaos in the UK. As of 7:00am ET, S&P futures are -0.5%, while Nasdaq futures drop 0.3%; semis are bid, Mag7 are mostly lower ex-NVDA which reports earnings this week. Semis / AI are the bullish story pre-mkt with most names flat to down with the market expressing a slight preference for Defensives over Cyclicals. In other news, US-China will set up a trade/investment board, and China will increase Ag purchases from the US. Bond yields are flat to +1bp with the 10Y at 4.60% after last week’s meltup;Japan’s 30-year yield surged as much as 20 basis points before paring most of the move on what may have been another round of BOJ intervention. Treasuries and European bonds were little changed, while the dollar was set to snap a five-day run of wins as it reverses overnight gains. In commodities, Energy is leading but crude prices have cut their gains: Brent trades around $11 after Trump warned that the “clock is ticking” for Iran to reach a deal that will end the war. Metals are weaker and Ags are bid. Today’s macro data focus is on TIC, housing price index, and NY Fed activity indicator.

In premarket trading, Nvidia is the only Mag 7 member rising: the $6 trillion semiconductor giant is slated to report first quarter results on Wednesday (Nvidia +0.8%, Alphabet -0.6%, Microsoft -0.6%, Apple -0.8%, Meta -0.9%, Amazon -1%, Tesla -1.1%)

Shares in UnitedHealth (UNH) fall 5.3% after Berkshire Hathaway exited its stake in the health insurer. The conglomerate also disclosed that it amassed a $2.6 billion stake in Delta Air Lines (DAL), boosting the carrier’s shares by 2.4%.

EchoStar (SATS), Rocket Lab (RKLB) and AST SpaceMobile (ASTS) rise as billionaire Elon Musk said he’s back in Texas working on plans for an initial public offering of SpaceX.

Regeneron Pharmaceuticals (REGN) falls 10% after the drugmaker’s phase 3 data for fianlimab in metastatic melanoma fell short of expectations. Citi downgraded its rating on the stock following the “disappointing” trial update.

The standoff in the Middle East shows no signs of easing after more than two months, puncturing an AI-driven rally that has pushed global stocks to record highs. Over the weekend, Trump said the “clock is ticking” for Iran to reach a deal, while G7 finance chiefs’ two-day meeting in Paris starts today, focusing on mounting imbalances and rare earths. Meanwhile, bond yields have climbed to levels seen decades ago on fears that central banks will lift interest rates and governments will ramp up borrowing to cushion the blow from rising energy prices. Japan’s 30-year yield surged as much as 20 basis points before paring most of the move.

“Bonds were more nervous about the inflation picture and the equity market was comforted and encouraged by the very strong earnings and AI-led optimism,” said Willem Sels, global chief investment officer at HSBC Private Bank. “What you now have is a bit of a catch-up movement in the equity market, a bit of an exhaustion of the momentum.”

As a fragile ceasefire between the US and Iran extends past 40 days and a deal to reopen the Strait of Hormuz remains elusive, President Donald Trump expressed frustration with Tehran and told it the “clock is ticking.” Earlier, drones targeted a nuclear power plant in the United Arab Emirates.

Elsewhere, at a time when markets expect the Federal Reserve under Kevin Warsh to hike rates as soon as December, minutes from last month’s meeting due for release Wednesday will give investors clues about policymakers’ thinking. “The absence of a near-term bullish catalyst can continue to pressure bonds, with spillover effects to exuberant equities,” said Laura Cooper, global investment strategist and head of macro at Nuveen. “Signs of conflict de-escalation are likely needed to assuage jittery markets.”

Ed Yardeni wrote that the Fed needed to catch up with bond markets or risk losing control of borrowing costs. If the Fed fails to remove its easing bias, “investors will conclude that the central bank is falling behind the inflation curve and will demand a higher inflation risk premium,” Yardeni wrote. “We expect the Fed to hold rates unchanged at the June meeting and shift to a tightening policy stance.”

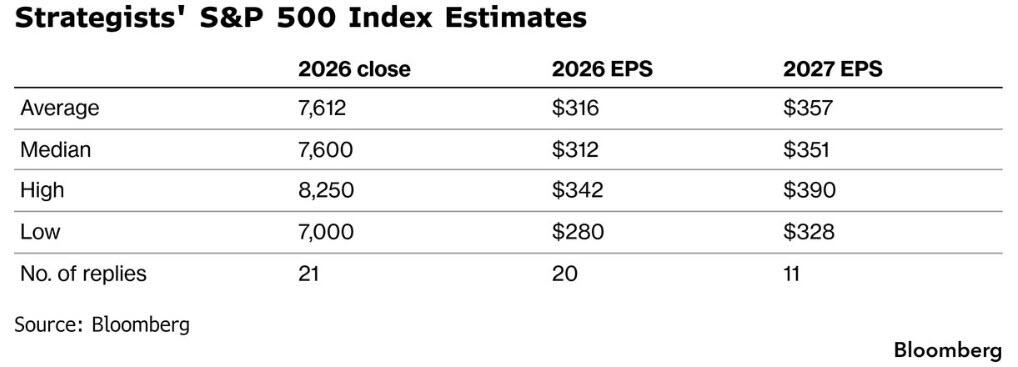

Meanwhile, the higher yields rise, the more bullish Wall Street strategists turn. Six out of the 21 strategists polled by Bloomberg have raised their target for the S&P 500 over the past month. Morgan Stanley’s Mike Wilson retains high conviction of an earnings recovery and broadening thesis, while noting the 10-year yield at the critical 4.50% threshold could be more of a “noticeable headwind” for equity multiples.

Bloomberg News interviewed 32 investment managers across the US, Asia and Europe who were overwhelmingly bullish, with 80% expecting equities to outperform other asset classes over the next three to six months. The top investment choice for about half of these buy-side professionals is megacap tech and AI stocks. Most investors interviewed pointed to the yield on 30-year Treasuries holding sustainably above 5% as the biggest threat to stocks. Perhaps they have been reading Michael Hartnett who has repeatedly said 5% on the 30Y is the “door to doom.”

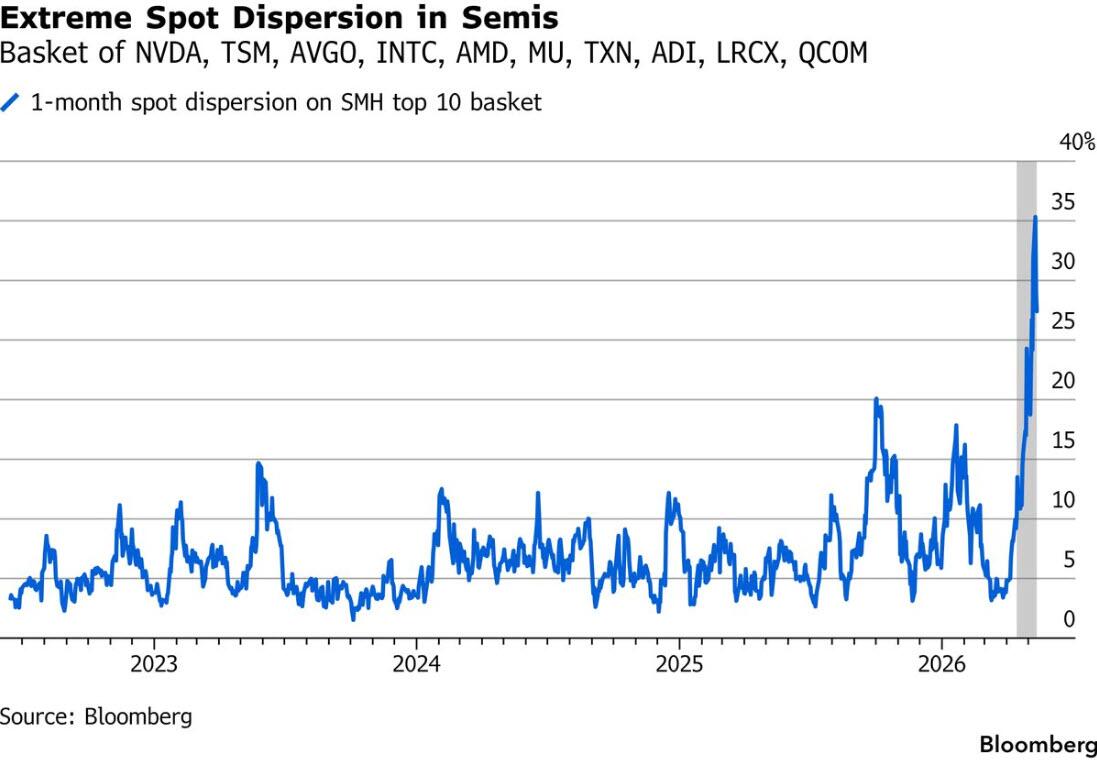

And while the tech-fueled stock rally is looking bubble-like to some investors, timing the pop is tough. Some are turning to exotic options that better protect against an eventual slump. Single-stock volatility — especially in parts of the tech sector such as semiconductors — far outpace relatively mild increases in indexes.

d

In Europe, consumer and auto shares drove a 0.4% decline in the Stoxx 600, although stocks have trimmed some early declines Monday as last week’s selloff in bonds eased and energy shares outperformed. Here are the biggest movers Monday:

Technoprobe shares rise as much as 7.7% to a record high, extending last week’s results-driven gains after an upgrade for the chip-testing equipment maker from Bank of America, which lifted its target price to a Street-high of €38

Sonova shares rise as much as 4.4%, the biggest gainer in the Stoxx 600 Health Care Index, after the Swiss hearing-aid maker’s full-year adjusted Ebita beat the average analyst estimate

FLSmidth gains as much as 5.3%, the most since April 8, after Nordea and Danske Bank upgraded their views on the Danish industrial equipment maker to buy from hold, with Nordea quoting a positive risk/reward profile

Publicis shares climb as much as 5.8% on Monday after the advertising agency increased its earnings growth targets for the next two years, following a $2.2 billion deal to buy US-based data collaboration platform LiveRamp

Draegerwerk shares rise as much as 4.7%, rebounding from a four-month low, after the medical and safety equipment maker was upgraded

Deutsche Boerse shares outperformed Monday after a regulatory filing showed Chris Hohn’s activist hedge fund TCI Fund Management has increased its voting rights in the German market operator to 5.15%

Smart Eye rises as much as 12%, the most since November, after the Swedish eye-tracking technology company reported what DNB Carnegie called a “solid” set of results, with Ebitda showing a “clear improvement”

Ipsen shares drop as much as 5.6%, the most since July last year, following the French biopharma company’s trial data for its experimental frown-lines treatment corabotase

Future shares slide as much as 10% after Stifel downgrades the publisher to hold from buy, saying it will take time for the firm to find new ways to monetize its content, as new AI tools threaten the search market

Alleima falls as much as 7.5%, the most since January, after Swedish business daily Dagens Industri recommended in a column that readers sell shares in the specialty steels group, flagging a weakening order book and rising short interest

Advanced Medical Solutions shares drop as much as 24%, the most since September 2023, after TA Associates confirmed late on Friday that it won’t make an offer for the London-listed firm

Earlier in the session, Asian stocks fell for a second session, as stalled progress on ending the Iran war and higher oil prices intensified concerns about inflation and economic growth. The MSCI Asia Pacific Index dropped as much as 1.4%, before paring losses. Taiwan Semiconductor Manufacturing Co., Toyota Motor Corp. and Mitsubishi Corp. were among the biggest contributors to the losses. Benchmarks in Indonesia, Hong Kong and Australia all fell over 1%. Bucking the trend, South Korean stocks reversed losses of as much as 4.7%, as optimism over progress in Samsung Electronics Co.’s labor talks helped offset pressure from rising bond yields. Behind the global debt selloff and stock market weakness was a third consecutive day of oil price gains, after President Donald Trump renewed pressure on Iran to resolve the war and reopen the Strait of Hormuz. Following the recent rally driven by optimism about artificial intelligence, equities investors are now shifting their attention back to the risk of worsening inflation. Separately, Chinese shares fell after data showed the country’s economic growth slowed across the board in April.

In FX, The Bloomberg Dollar Spot Index is down 0.1%, while the pound takes top spot among G-10 currencies, rising 0.4% against the greenback. The yen is lagging.

In rates, treasuries erased an earlier drop, leaving US 10-year yields flat at 4.60%. US yields are cheaper by 1bp to 2bp across the curve with spreads trading broadly within a basis point of Friday close. US 10-year yields trade around 4.6% with gilts outperforming by around 3bp in the sector. Bunds are steady, while gilts are outperforming, with UK 10-year yields down 3 bps to 5.14% as UK gilts steadied after last week’s sharp selloff. During Asia session, Japan’s 30-year yield surged as much as 20 basis points before paring most of the move as inflation fears continue to ripple through global bond market. IG dollar issuance slate includes a couple of names. Estimates from dealers for this week point to about $40 billion in bond sales. Treasury auctions this week include $16 billion 20-year bonds (Wednesday) and $19 billion 10-year TIPS reopening (Thursday)/

In commodities, Brent crude futures pulled back from their overnight highs to trade around $110 a barrel, helping arrest a selloff in global government bonds.

Economic data slate includes May New York Fed services business activity (8:30am), May NAHB housing market index (10am) and March TIC flows (4pm). Fed speaker slate empty for the session

Market Snapshot

S&P 500 mini -0.4%

Nasdaq 100 mini -0.2%

Russell 2000 mini -0.3%

Stoxx Europe 600 -0.3%

DAX +0.2%

CAC 40 -0.7%

10-year Treasury yield little changed at 4.6%

VIX +0.6 points at 19

Bloomberg Dollar Index -0.1% at 1201.01

euro +0.1% at $1.1639

WTI crude +1.1% at $106.54/barrel

Top Overnight News

President Trump told Axios in a phone call that “the clock is ticking” for Iran and warned that if the Iranian regime doesn’t come with a better offer for a deal, “they are going to get hit much harder.” Axios

Trump declined to give a specific deadline for negotiations with Iran and will hold a Situation Room meeting with his national security team on Tuesday to discuss possible options for military action, while he spoke with Israeli PM Netanyahu about the situation in Iran, according to Axios. Trump also stated that he still thinks Iran wants a deal and he is waiting for an updated Iranian proposal, which he hopes will be better than the prior offer. Furthermore, Axios’s Ravid reported that Trump threatened that attacks would resume with greater intensity if the Iranian regime does not come up with a better proposal, while Channel 12’s Kraus posted that President Trump said in a phone call that he thinks the Iranians should be afraid of what’s going on right now.

China’s industrial output and retail sales growth slowed sharply last month while investment dropped as policymakers warned that geopolitical conflicts were creating a “severe” global economic environment. Industrial production rose 4.1 per cent in April from a year earlier, official data showed on Monday. FT

Chinese artificial intelligence groups have moved ahead of US rivals in video generation, a key battleground in generative AI in which there is rapid uptake across advertising, ecommerce and entertainment. FT

China agreed to buy at least $17 billion of farm products annually through 2028 and establish trade and investment boards, the US announced. Earlier, Beijing said the two countries will also reduce tariffs on certain goods. BBG

Japan’s government is likely to issue fresh debt as part of funding for a planned extra budget to cushion the economic blow from the Middle East war. Any additional debt issuance would further strain Japan’s already worsening finances and may accelerate rises in long-term interest rates. RTRS

Italian Prime Minister Giorgia Meloni asked the European Commission to extend greater latitude within European Union budget rules to measures aimed at tackling rising energy costs. Italy’s government is seeking to include investments and extraordinary measures to address the energy crisis in the so-called national safeguard clause. BBG

NextEra is said to be in talks to buy Dominion in a mostly stock deal valuing the utility at about $66 billion. BBG

Anthropic agreed to brief members of the Financial Stability Board on its AI model Mythos. FT

Over 60 allies of US President Trump have urged him to test and approve the most powerful AI models before its released: Axios

Central banks’ gold purchases are expected to pick up to average 60 tons a month over 2026. We maintain a bullish target for prices to climb to $5,400 an ounce by the end of the year. Goldman

Trump told Fortune he thinks US could sell Intel (INTC) shares slowly over time without tanking the stock market. He added that “Intel should be the biggest company in the world right now… If I had been president when all these companies started sending their chips in from China, I would have put a tariff on that would have protected Intel.”

Iran Headlines

US President Trump warned on Truth Social that the clock is ticking for Iran and that they better get moving fast, or there won’t be anything left for them, and that time is of the essence.

US President Trump declined to give a specific deadline for negotiations with Iran and will hold a Situation Room meeting with his national security team on Tuesday to discuss possible options for military action, while he spoke with Israeli PM Netanyahu about the situation in Iran, according to Axios. Trump also stated that he still thinks Iran wants a deal and he is waiting for an updated Iranian proposal, which he hopes will be better than the prior offer. Furthermore, Axios’s Ravid reported that Trump threatened that attacks would resume with greater intensity if the Iranian regime does not come up with a better proposal, while Channel 12’s Kraus posted that President Trump said in a phone call that he thinks the Iranians should be afraid of what’s going on right now.

Pakistan shared revised Iranian proposal to end the war with the US on Sunday night, according to Pakistani sources. The course added that “we don’t have much time”, adding that both countries “keep changing their goalposts”.

Western sources say the new Iranian proposal includes a commitment of unclear value not to produce nuclear weapons but no mention of uranium or Hormuz, according to Journalist Segal.

Iranian Foreign Ministry Spokesperson Baghaei said talks with the US continue through Pakistani mediation. The spokesperson added that they have made great efforts for safe movement and protection of the Strait of Hormuz and are in constant contact with Oman to develop a mechanism. On Uranium, Baghaei said Tehran does not need any party to recognize its right to uranium enrichment and will not discuss during negotiations with the US.

Iranian Defence Ministry spokesman Brigadier General Reza Talaei-Nik warned of a regretful response to enemies and said that Iranian armed forces are fully prepared to confront any potential attack by the US and Israeli regime, according to IRNA.

Iranian Major General Rezaei said Iran is serious about diplomacy and negotiations, but is more serious about dealing with the aggressor, while he added that the US must now prove its good intentions and that Iranian armed forces are on the trigger as diplomatic efforts continue.

Iran said transit through the Strait of Hormuz would flow again once its conflict with the US and Israel is over, although the sides remain far from resolving their differences, according to Bloomberg. In relevant news, three cargo-empty, US-sanctioned tankers reportedly slipped through the US naval blockade in recent days, according to TankerTrackers.com.

Israel said it carried out a Gaza strike targeting the de facto head of Hamas’s armed wing, while Israel also conducted an airstrike on the towns of Froun, Kfar Hounah and Zawtar al-Sharqiya in southern Lebanon. Furthermore, an Israeli air strike targeted Baalbek, Lebanon and killed an Islamic Jihad commander and his daughter.

UAE officials said a drone attack set off a fire near the UAE’s nuclear power station, while it was still investigating the source of the attack.

Saudi Defence Ministry said it intercepted three drones launched from Iraq after entering the kingdom’s airspace.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly in the red after last Friday’s losses on Wall St, and with risk sentiment sapped as oil prices and yields extended higher after US President Trump warned the clock was ticking on Iran, heading into a meeting on Tuesday with his national security team to discuss possible options for military action, while participants in the region also digest disappointing Chinese activity data. ASX 200 was dragged lower amid losses across nearly all sectors aside from energy, and with sentiment not helped by disappointing data from Australia’s largest trading partner. Nikkei 225 resumed its pullback from last week’s record highs amid higher oil prices and the anticipation of the BoJ to resume rate normalisation next month. KOSPI was volatile as the index initially suffered heavy losses and the Korea Exchange triggered a sidecar after KOSPI 200 futures dropped 5.0% with jitters seen as Samsung Electronics faces an 18-day strike involving nearly 45,000 of Samsung’s unionised workers starting on May 21st. The index then staged a firm rebound alongside Samsung shares after the union said it would engage in government-mediated pay talks, and a court was said to partially accept an injunction request against the union’s planned strike, although the union later announced that it would proceed with the strike as planned. Hang Seng and Shanghai Comp were pressured following the disappointing activity data in which Industrial Production, Retail Sales and Fixed Assets Ex-Rural Investment all missed forecasts, with the latter showing a surprise contraction, while the stats bureau noted the external situation is complex and that China’s economic foundation still needs to be consolidated.

Top Asian news

China State Council said it will leverage national venture capital guidance fund to increase support for entrepreneurship in tech innovation.

Chinese MIIT Minister Li Lecheng said China should upgrade “outdated” industries, and not scrap them, because manufacturing remains the backbone of the economy.

China’s State Administration for Market Regulation set 34 priorities for this year to support private sector growth, with a focus on fair competition, legal protections and efficient regulation.

China’s stats bureau said the external situation is complex and China’s economic foundation still needs to be consolidated, while it added that China is to continue to optimise supply and that the domestic supply-demand imbalance remains prominent. China’s stats bureau said China will continue to expand the domestic demand and should implement more active fiscal policies and moderately loose monetary policies. Furthermore, it said the international situation remains grim and complicated as of April, and the world economic recovery is facing greater headwinds, as well as stated that the will and capacity of people to spend needs improving.

Japan is likely to issue fresh debt as part of funding for a planned extra budget to soften the blow from the Middle East conflict, according to sources cited by Reuters. A separate report confirmed that Japanese PM Takaichi was set to announce an extra Japan budget. However, conflicting comments by Japanese Finance Minister Katayama followed, stating that they are not yet at a stage to talk about the specifics of an extra budget.

Japanese Chief Cabinet Secretary Kihara said they are watching market moves with a high sense of urgency, including long-term rates. No comment on FX intervention.

European bourses (STOXX 600 -0.2%) opened entirely in the red this morning, given the lack of US-Iran progress, and further punchy rhetoric from President Trump. Over the weekend, he stated that the clock is ticking for Iran, though he declined to give a specific deadline. Since then, bourses have clambered off lows amidst positive geopolitical updates; notably, Iran’s Baghaei suggesting that talks with the US continue through Pakistani mediation. Moreover, Pakistani sources suggested that Pakistan shared a revised Iranian proposal to end the war with the US on Sunday night. European sectors opened with a clear negative bias, but this picture is now a little more mixed. Energy takes pole position, benefiting from higher underlying crude prices; Media and Utilities complete the top three. At the bottom of the pile reside cyclical sectors, such as Autos and Travel & Leisure. The latter has been pressured by post-earning losses in Ryanair after reporting in-line metrics, but warned that flat fares may put pressure on profits.

Top European News

UK PM Starmer has decided not to announce a departure timetable unless and until Andy Burnham wins the Makerfield by-election, ITV’s Peston reported.

UK Deputy PM Lammy said PM Starmer will not be announcing a timetable for departure, speaking to Sky News.

UK PM Starmer was reportedly mulling whether he would bring more government stability by announcing a timetable for his departure and a leadership election, according to ITV.

Former UK Health Secretary Streeting vowed to stand in any Labour Party leadership contest to oust UK PM Starmer. In relevant news, Streeting said he would battle Manchester Mayor Burnham for the Labour leadership and called for the UK to rejoin the EU, while Burnham played down rejoining the EU.

UK Chancellor Reeves is reportedly to lay out more details in the week ahead regarding proposals to ease bank regulations that were imposed to prevent a repeat of the 2008 GFC.

Fitch affirmed Germany’s sovereign rating at AAA; Outlook Stable, while DBRS maintained Portugal at A (high), Outlook Raised to Positive.

FX

FX shows a risk-on bias with high-beta outperforming and DXY in the red.

DXY firmed at the Asia reopen and rose to a 99.40 peak as participants digested US President Trump’s remarks over the weekend, “the clock is ticking for Iran.” However, with Brent crude falling from its USD 112/bbl peak (curr. 110/bbl), the index now trades modestly in the red, a touch above 99.00 where its 50 DMA lies. Nothing notable scheduled today, though the rest of the week sees weekly ADP jobs on Tuesday, FOMC Minutes + NVIDIA earnings Wednesday, Jobless Claims and PMIs Thursday and UoM on Friday.

GBP is one of the best G10 performers, likely a factor of technical factors than political reprieve with newsflow light heading into the likely June 18th by-election. EUR/GBP reversed from 0.8730, and Cable bounced from 1.33. On domestic politics, PM potential candidates Streeting and Burnham were on the wires talking up the importance of rejoining the EU. On the Fiscal/Consumer front, the Times reported Chancellor Reeves has plans to retain the cut on fuel duty from September amid fuel price concerns, while separately drawing up plans for a targeted intervention on energy bills – both potentially factors helping the Pound today. The week ahead sees Jobs on Tuesday, CPI on Wednesday and PSNB on Friday, the former which ING says is expected to be mild because of base effects.

JPY is the only G10 currency that trades lower against the buck amid: a) a weak 5yr JGB auction, b) reports that the Japanese government is to start compiling a supplementary budget, c) lack of Iran progress, and d) surging energy prices. (See Fixed Income 09:35 BST for more). USD/JPY +0.1%, up a touch despite earlier gains which were capped by the 159 mark.

Central Banks

BoE’s Greene said some of the global economic resilience to the Iran war is due to inventories while second round effects of the energy price shock will not show up for another year. Should not be looking through negative supply shocks.

BoE’s Breeden said the central bank should not be ‘trigger happy’ on rates, while she warned of a hit to business from political uncertainty, according to FT.

Fixed Income

A bearish start to the week as US President Trump’s escalatory language on Iran and the associated energy move, with Brent peaking at USD 112/bbl overnight.

Amidst this, fixed benchmarks spent the APAC session in the red. Note, JGBs derived pressure from this alongside a weak 5yr outing and reports around the compiling of a supplementary Japanese budget, see 09:35 BST for more details.

USTs hit a 108-30 trough, a fresh contract low, in the early hours. Since, and particularly after remarks from the Iranian Foreign Ministry spokesperson, energy benchmarks have eased off, which has allowed fixed to lift, taking USTs to a 109-08 high with gains of one tick on the session. Today’s US docket is quiet, but the week is busy with Nvidia due before the FOMC Minutes and a 20yr auction. From the Minutes, the last with Powell as Chair, BofA expects the account to “reinforce the Fed’s recent hawkish tone”, showing that Warsh will inherit a Fed with “little appetite to cut”.

Bunds in-fitting with the above, hit a 123.74 base, which is also a new contract low. Given the discussed energy moves, the benchmark has pared much of its 53 ticks of downside and is now lower by a more modest c. 15 ticks, just off a 124.20 peak. Newsflow has been relatively limited, we had remarks from but no move to ECB’s Lagarde, who essentially noted that she is watching the yield space. On yields, the German 10yr hit a 3.19% peak overnight, a new high for the year and the highest since 2011’s 3.49% best. Furthermore, the energy moves continue to be reflected in near-term policy expectations, with 21bps of ECB tightening implied for June and 75bps by end-2026.

Gilts opened near-enough flat, as the bearish leads from overnight had already begun to moderate, in addition to the lack of significant weekend development on the fate of PM Starmer. Furthermore, the complex is perhaps deriving some support from a revival of coverage that contenders Burnham and Streeting would like to rejoin the EU at some point; albeit, Burnham did somewhat distance himself from this over the weekend, concerning the upcoming by-election campaigning at least. As it stands, Gilts are holding at highs of 85.53 with gains of c. 25 ticks. A bounce from the 84.96 base this morning, another contract low.

Japan sells JPY 1.9tln 5yr JGBs; b/c 3.22x (prev. 3.58x), average yield 2.024% (prev. 1.826%), Lowest accepted price 99.85 (prev. 99.84), Weighted average price 99.89 (prev. 99.88), Tail in price 0.05 (prev. 0.04).

Commodities

Crude futures surged at the start of Asia-Pac trade, with WTI making a new contract high of USD 104.37/bbl while Brent peaked at USD 112.00/bbl. Punchy rhetoric over the weekend by US President Trump, warning Iran that the “clock is ticking” and that “they better get moving, fast, or there won’t be anything left of them” initially spurred the upside in energy prices. However, benchmarks have pulled back as European trade gets underway, with WTI and Brent now trading at the lower end of its USD 101.59-104.37/bbl and USD 109.56-112/bbl range, respectively. More recently, according to Pakistani sources, Pakistan shared a revised Iranian proposal to end the war with the US on Sunday night.