Category: News

Senate Parliamentarian Rejects White House Ballroom Funding In Reconciliation Bill

Senate Parliamentarian Rejects White House Ballroom Funding In Reconciliation Bill

Authored by Joseph Lord via The Epoch Times,

The Senate’s nonpartisan referee has rejected a bid by Republicans to fund $1 billion for the White House ballroom expansion and other White House security upgrades.

According to Senate Parliamentarian Elizabeth MacDonough, the $1 billion proposal breaks the rules of the reconciliation process. As parliamentarian, MacDonough’s go-ahead is traditionally required to approve individual items passed under the partisan process.

Republicans are seeking to use the reconciliation process—which is not subject to the filibuster—to pass $72 billion in funding for Immigration and Customs Enforcement (ICE) and Customs and Border Protection, which has been blocked by Democrats in the wake of fatal shootings of U.S. citizens by immigration agents. The GOP bill would fund the agencies through 2029, the end of President Donald Trump’s second term.

Trump has long pushed for the addition of a major ballroom to the East Wing of the White House, particularly in the wake of an alleged assassination attempt while attending an event away from the executive mansion.

The Secret Service had requested the money after the incident at the White House Correspondents’ Association dinner last month.

Republicans had pursued including this funding in an immigration enforcement funding package.

According to Democrats, MacDonough’s ruling holds that funding for a project as large as the proposed White House expansion is too broad to be included in the filibuster-proof bill.

It’s unclear which, if any, segments of the GOP proposal can be included in the final funding bill.

The parliamentarian left the bulk of the bill’s immigration language intact, barring some minor provisions such as the one providing funding for Customs and Border Protection to hire, train, and pay agents. Republicans have indicated that these sections can be revised and retained in the legislation.

A model of the White House and proposed ballroom (R) is displayed during a ballroom fundraising dinner with President Donald Trump in the East Room of the White House on Oct. 15, 2025. Kevin Dietsch/Getty Images

Technically, Republicans can ignore MacDonough’s rulings, which are ultimately considered advisory; however, respect for the parliamentarian’s authority is so deeply embedded in the upper chamber’s culture that this rarely happens.

Ignoring or overriding a ruling on a budget reconciliation bill would set a precedent that could deeply weaken the filibuster, an eventuality that members of both parties have long wished to avoid.

In 2021, after the Senate parliamentarian rejected a bid by Democrats to include a $15 minimum wage in a reconciliation package, some Democrats called for the ruling to be overturned; however, these calls were ultimately rejected.

Senate Majority Leader John Thune (R-S.D.) speaks to members of the press in Washington on April 14, 2026. Madalina Kilroy/The Epoch Times

A spokesman for Senate Majority Leader John Thune (R-S.D.) wrote in a post on X that “none of this is abnormal” during the complicated budget process that Republicans are using to try to pass the immigration enforcement and White House security money on a partisan basis.

“Redraft. Refine. Resubmit,” Wrasse said in the post.

Senate Minority Leader Chuck Schumer (D-N.Y.) framed the ruling as a win for Democrats.

“Republicans tried to make taxpayers foot the bill for Trump’s billion-dollar ballroom. Senate Democrats fought back — and blew up their first attempt,” Schumer wrote in a May 17 post on X.

“Americans don’t want a ballroom. They don’t need a ballroom. And they sure as hell should not be forced to pay for one,” Schumer added, vowing that Democrats would continue to seek to block funding for the White House expansion.

Tyler Durden

Mon, 05/18/2026 – 14:15

Judge Dismisses Musk’s OpenAI Lawsuit After Jury Reaches Verdict

Judge Dismisses Musk’s OpenAI Lawsuit After Jury Reaches Verdict

A nine-person federal jury has sided with OpenAI, Sam Altman, Greg Brockman, and Microsoft, determining that Elon Musk filed his high-profile lawsuit too late under the statute of limitations. The verdict effectively ends Musk’s claims that OpenAI abandoned its founding nonprofit mission to benefit humanity.

The jury unanimously concluded that Musk knew or should have known about OpenAI’s shift toward a for-profit model and major Microsoft partnerships years earlier – potentially as far back as 2019–2021, making his August 2024 filing untimely. U.S. District Judge Yvonne Gonzalez Rogers in turn accepted the advisory jury’s finding on this threshold issue and dismissed the case.

Musk, a co-founder who contributed roughly $38–44 million in OpenAI’s early days, alleged that the company betrayed its original charitable trust by pursuing massive profits and commercial deals, particularly with Microsoft. He sought up to $150 billion in damages or “ill-gotten gains,” the removal of Altman and Brockman from leadership, and a restructuring to restore the nonprofit focus on safe, humanity-benefiting AI.

OpenAI countered that Musk was fully aware of the company’s evolving plans (including for-profit elements he himself had once advocated), waited until after launching his competing xAI venture in 2023, and was motivated by competitive rivalry rather than genuine concern for the mission. They described the suit as “sour grapes.”

Developing…

Tyler Durden

Mon, 05/18/2026 – 13:38

https://www.zerohedge.com/technology/jury-rules-against-musk-openai-lawsuit

Judge Tosses Key Evidence In Luigi Mangione Case Over Warrantless Backpack Search

Judge Tosses Key Evidence In Luigi Mangione Case Over Warrantless Backpack Search

A judge just handed Luigi Mangione some big wins in his high-profile murder case. On Monday, New York Supreme Court Justice Gregory Carro issued a mixed ruling on evidence seized during the suspect’s dramatic arrest at a Pennsylvania McDonald’s. The decision represents a partial victory for the defense on constitutional grounds while delivering a significant boost to prosecutors by preserving the most damning pieces of physical evidence linking Mangione to the assassination of UnitedHealthcare CEO Brian Thompson.

Mangione, 28, appeared in court for the hearing, dressed sharply as he has throughout proceedings. He has pleaded not guilty to second-degree murder and other charges in the Dec. 4, 2024, killing that shocked the nation and ignited fierce public debate over corporate greed in the American healthcare system.

The Arrest and the Evidence at Stake

The ruling stems from Mangione’s arrest on Dec. 9, 2024, in Altoona, Pennsylvania – roughly 280 miles from the Manhattan crime scene. Police responded to a tip after Mangione was recognized while eating breakfast. Officers approached him, and what followed became the focal point of lengthy suppression hearings held late last year.

During the initial encounter at the McDonald’s, officers conducted a warrantless search of Mangione’s backpack in a public setting, visible to restaurant employees and patrons. They discovered a loaded gun magazine wrapped in underwear and other items. The search was paused, and Mangione was taken to the Altoona police station, where a more formal inventory search occurred.

Justice Carro ruled that the initial McDonald’s search was improper – an unconstitutional warrantless intrusion because the backpack was not within Mangione’s immediate control or reach at the time. As a result, several items recovered during that phase are now suppressed and inadmissible in the state trial.

The Ditched Evidence Includes:

Loaded handgun magazine

Cellphone

Passport

Wallet

Computer chip

Certain initial statements made by Mangione to officers at the scene

However, the judge found the subsequent search at the police station valid, allowing prosecutors to use critical items recovered there.

Admissible Key Evidence:

The alleged murder weapon: A 3D-printed “ghost gun” with a silencer, which ballistics reportedly match to shell casings found at the crime scene.

A red notebook containing handwritten notes expressing deep frustration with the health insurance industry—often described in media as a “manifesto.”

USB drive and related items from the station search.

This split decision mirrors similar outcomes in Mangione’s separate federal case and underscores the complexities of Fourth Amendment jurisprudence in high-stakes arrests.

The Crime That Captivated America

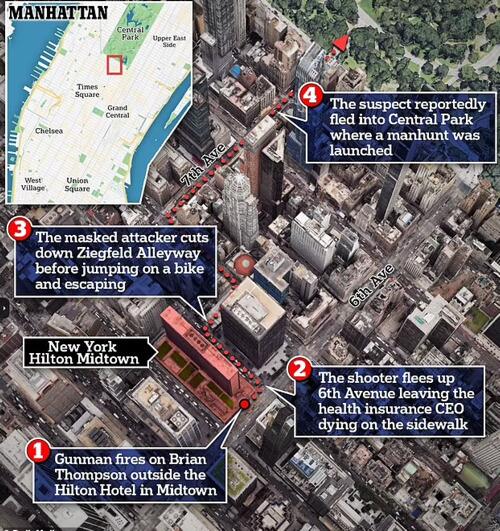

To understand the ruling’s weight, one must revisit the events of December 2024. On the morning of Dec. 4, Brian Thompson, 50, a father of two and CEO of UnitedHealthcare, was gunned down in cold blood outside the New York Hilton Midtown. He was heading to an investors’ conference when a masked assailant approached from behind and fired multiple shots. Thompson was struck in the back and leg; he died shortly after.

The killer fled on a bicycle, leaving behind shell casings engraved with the words “delay,” “deny,” and “depose” – phrases widely interpreted as a pointed critique of insurance industry practices that deny claims and delay care. Surveillance video, fingerprints, DNA, and other forensic links quickly pointed investigators toward Mangione, a 26-year-old University of Pennsylvania graduate from a well-to-do Maryland family with a background in engineering.

Mangione’s arrest five days later, with a fake ID and a backpack full of incriminating items, ended a intense manhunt. His Ivy League education, handsome appearance, and apparent grievances against corporate America turned him into an unlikely folk hero for some. Protests, “Free Luigi” chants, and online memes have accompanied the case from the start, reflecting broader societal anger over healthcare costs, claim denials, and corporate profiteering.

Legal Strategy and Implications

For the defense, led by prominent attorneys, the suppression motion was a cornerstone of their strategy. By challenging the backpack search, they hoped to dismantle much of the prosecution’s physical case. While they secured wins on peripheral items, the admission of the gun and notebook is a heavy blow. The notebook, in particular, could allow prosecutors to argue motive and premeditation before a jury.

Manhattan District Attorney Alvin Bragg’s office hailed the ruling as preserving justice for a “premeditated, targeted” killing. Bragg has emphasized that additional evidence – beyond the backpack – ties Mangione to the scene, including video footage, ballistics, and witness identifications.

Legal experts describe the outcome as a classic “partial win” scenario. Defense attorneys may appeal the admissible evidence or challenge statements under Miranda rules (the judge also addressed Huntley issues regarding voluntariness of statements). However, with the weapon and writings intact, the state’s case remains formidable.

The state trial is scheduled to begin September 8, 2026, in Manhattan Criminal Court. A separate federal case, charging stalking and other counts, carries potential life sentences but no death penalty following an earlier federal ruling. Mangione remains detained at the Metropolitan Detention Center in Brooklyn.

Tyler Durden

Mon, 05/18/2026 – 13:30

The Lines We Thought Machines Wouldn’t Cross

The Lines We Thought Machines Wouldn’t Cross

Authored by George Ford Smith via The Mises Institute,

In 2000, the world braced for Y2K. It came with a date and a remedy. There was panic about doomsday but as I and other programmers stretched the year field from two to four characters, apart from scattered hiccups, the lights stayed on. Everything about Y2K was known – the problem, the solution, and the deadline.

Q-Day is something else entirely.

Q-Day is shorthand for the moment when quantum computing crosses a line we assumed would hold—when the mathematics that secures modern life can be broken, and broken quickly. On Q-Day the locks will be quietly and rapidly picked. And the unsettling part is that the thief may already have your safe, waiting for the day the combination becomes trivial to compute.

Today’s encryption is a lock that would take an ordinary zeros-and-ones computer longer than the age of the universe—26.7 billion years—to pick. The most widely-used system—RSA with a 2,048-bit key—relies on the virtual impossibility of factoring “the product of two very large prime numbers.”

A sufficiently advanced quantum computer, however, would not try every possible combination. It would use a fundamentally different method—one discovered by MIT mathematician Peter Shor—to solve the problem efficiently. What is impossible today would become routine. The world’s assumption of security would no longer hold.

Data stolen today—bank records, corporate secrets, medical files, state communications—can be stored until the day it becomes readable, what analysts call “harvest now, decrypt later.” It gives today’s thieves a speculative claim on tomorrow’s knowledge. But, like all speculative claims, its value depends on time, uncertainty, and the actions of others. The longer the delay, the more likely the data is obsolete, replaced, or secured in a different manner or place.

There is no agreement about when Q-Day will likely arrive. “Google thinks it could happen by 2029, while Adi Shamir—one of the cryptography experts behind the development of RSA encryption—believes it’s at least 30 years away.”

Meanwhile, something else is headed our way:

The technological singularity, the point where artificial intelligence surpasses human intelligence and begins improving itself in an unstoppable loop, is most commonly predicted to arrive between 2035 and 2045. That window has been shrinking. A few years ago, most experts placed it decades away. Now, some of the most prominent voices in AI believe the precursor step, artificial general intelligence (AGI), could arrive before 2030.

Singularity futurists might be overlooking technical obstacles in their projections, such as the failure of intelligence to scale at the projected magnitude, but Q-Day’s arrival seems fairly certain. It brings into view several themes familiar to students of Austrian School economics.

First, the knowledge problem. As Hayek emphasized, the information required to coordinate complex systems is dispersed, qualitative, and often tacit. No central planner can know when Q-Day will arrive or which systems are most exposed in real time. Mandates that assume a timetable risk misallocating resources. By contrast, decentralized actors—banks, firms, developers—can respond to price signals, insurance costs, vendor competition, and evolving threat intelligence.

Second, incentives and time preference. Security spending is the classic case of a present cost for a future benefit. The payoff is the loss you never incur. In a world of quarterly reports and countless distractions, the temptation is to defer. Yet the nature of Q-Day flips the calculus: the cost of delay compounds because the exposure window is long and the fix is slow. Systems are not swapped overnight. Keys must be rotated, protocols updated, hardware replaced, staff retrained. The discipline required here is precisely what Austrian analysis highlights: aligning incentives so that long-term preservation of capital is not sacrificed to short-term appearance.

Third, capital structure. Information systems are capital goods with long lives and complex interdependencies. When firms procrastinate and then rush, investment bunches up under pressure—an IT version of malinvestment. By contrast, building crypto-agility—the ability to swap cryptographic components without tearing down the whole system—is a form of sound capital planning. It spreads costs over time and reduces the risk of a frantic, error-prone scramble later.

Fourth, property rights and trust. In a digital economy, encryption is not a luxury; it is part of the institutional framework that makes exchange possible. If signatures can be forged and identities spoofed, claims to ownership—of accounts, contracts, even money—are weakened. The invisible infrastructure of trust becomes visible precisely when it fails. Q-Day, if mishandled, would not merely be a technical glitch; it could turn the reliability of exchange itself into a disaster.

Fifth, competition. If a single, mandated solution fails, it fails system-wide. A free-market approach—multiple implementations, open standards, independent audits, competing vendors—reduces single points of failure and encourages faster discovery of weaknesses.

One more point. We often draw comfort from lines we believe machines will not cross, but occasionally those lines move. Q-Day is one such movement. It does not herald the end of privacy or the collapse of commerce, any more than Y2K heralded the end of computing. But it does force us to confront a truth Austrians have long emphasized: Complex orders endure not because they are guaranteed, but because they are maintained—by incentives, by institutions, and by continual adaptation to changing knowledge.

And, as long as we still have the power to act purposely, the singularity, if it comes about, will represent a higher level of human intelligence and human life generally. It will not be something we will passively accept. Cost-benefit considerations will always apply, as will our moral sense of what is right. As Ray Kurzweil has written,

Since AI is emerging from a deeply integrated economic infrastructure, it will reflect our values because in an important sense it will be us. We are already a human-machine civilization. Ultimately, the most important approach we can take to keep AI safe is to protect and improve on our human governance and social institutions.

And as I have argued elsewhere, our human governance institution is in need of radical revision.

Tyler Durden

Mon, 05/18/2026 – 13:15

https://www.zerohedge.com/technology/lines-we-thought-machines-wouldnt-cross

Buffett Cash Hoard: Why $397 Billion Sits On The Sidelines

Buffett Cash Hoard: Why $397 Billion Sits On The Sidelines

Authored by Lance Roberts via RealInvestmentAdvice.com,

$397 billion. That’s how much “Buffett cash” now sits on Berkshire Hathaway’s balance sheet after Greg Abel’s first quarter as CEO. Warren Buffett left $373 billion behind when he stepped down at the end of 2025. Three months later, after Abel’s debut earnings report on Saturday, the hoard had grown by another $24 billion. The figure is bigger than the GDP of Hong Kong or Norway. It exceeds the market value of every American corporation except a tiny handful of mega-cap names. And it earned roughly four to five percent in Treasury bills while the S&P 500 ripped through three of its best consecutive years in modern history.

That Buffett cash hoard has also created a lot of speculation, innuendo, and assumptions, which is what I want to walk through in today’s discussion. Primarily, what that cash hoard actually represents, the popular theories explaining it, and what it really costs shareholders to hold.

The headline cash hoard number is striking on its own. Berkshire Hathaway ended Q1 2026 with a record $397.4 billion in cash and short-term Treasury bills, surpassing the prior $381.7 billion peak set in Q3 2025 and adding another $24 billion to what Buffett left behind. Of that, roughly $52 billion sits in plain cash and equivalents, with the bulk parked in Treasury bills earning short-term yields. By the time Abel released his first quarterly print on May 2, Berkshire was one of the largest holders of US Treasury debt in the world.

This wasn’t an accident. Between 2022 and 2024, Berkshire sold a net $172.93 billion in equities, with $134.1 billion of that coming in 2024 alone. Buffett trimmed his Apple position from nearly 50% of the equity portfolio down to roughly 22%. He cut Bank of America by more than half. Berkshire stopped repurchasing its own shares for nearly two years, sitting out twenty-one consecutive months as the stock traded above what Buffett considered its intrinsic value. Buybacks finally resumed under Abel on March 4, 2026, but only at $234 million in Q1, a token figure against a balance sheet of this size. In Q1 alone, Berkshire sold another $24.1 billion in equities against $16 billion in purchases, a net $8.1 billion reduction that pushed the cash pile to its new record.

The selling was deliberate, sustained, and almost entirely contrary to the prevailing market mood. While CNBC anchors debated whether the AI revolution was just getting started, the world’s most patient investor was quietly heading for the exits. Abel, in his first quarter, did exactly the same thing.

The History Of Buffett’s Cash Hoard

Berkshire’s cash position has always been countercyclical. When markets get cheap, the pile shrinks. When markets get expensive, it grows. That pattern has held for decades, but the magnitude in this cycle is unlike anything we’ve seen before.

In 2014, Berkshire’s cash and Treasury position hovered around $63 billion. By 2019, it had grown to $128 billion as bull market valuations stretched higher. The pandemic crash in early 2020 drew Buffett out for a brief window, when he deployed capital into Occidental Petroleum and Chevron. Those deployments barely dented the larger trend, and by the end of 2022, Buffett’s cash hoard had only modestly receded to roughly $109 billion despite the bear market that year.

Then came 2023 and 2024. As the S&P 500 ripped through gains of roughly 26 percent and 25 percent in consecutive years, Buffett didn’t chase. He sold. The cash hoard nearly doubled in 2024 alone, climbing from $168 billion to over $325 billion. By Q3 2025, it crested at $381.7 billion before a slight deployment trimmed it to $373.3 billion at year-end. Then in Abel’s first quarter at the helm, the hoard climbed to a fresh record of $397.4 billion as Berkshire kept selling, kept compounding T-bill yield, and continued to find few large-scale opportunities at acceptable prices.

The shape of that chart isn’t a coincidence. It’s the visual representation of a value investor’s discipline meeting a market that increasingly didn’t offer value. And the bar that matters most now is the one on the right: the discipline didn’t end with Buffett’s retirement.

Theory Versus Reality

The financial press has spent the past two years generating theories about Buffett’s cash position, and Saturday’s record Q1 print has reignited every one of them. Some are reasonable. Most miss the structural drivers entirely. Let’s separate the popular narratives from the actual mechanics.

Theory: Buffett Was Calling A Crash

This is the most viral interpretation. The Oracle of Omaha sees a bubble. He’s positioning Berkshire to scoop up bargains when the market collapses. The Buffett Indicator, which compares total US market capitalization to GDP, reached its highest level in history at the end of Q1 2026.

The math behind the indicator is straightforward. Take the total market value of all US publicly traded equities, divide by US nominal GDP, and you get a single ratio that Buffett himself called in a 2001 Fortune interview “probably the best single measure of where valuations stand at any given moment.” With Q1 2026 nominal GDP at $31.86 trillion (BEA advance estimate, released April 30, 2026) and total market capitalization near record highs, the ratio has surpassed every prior peak in the data series.

Two readings matter at this moment. The Federal Reserve’s broader corporate equities measure, divided by GDP, is roughly 232%, the highest level on record. The narrower Wilshire 5000 measure divided by GDP comes in at approximately 215%. Both versions are in record territory. Both are roughly two standard deviations above their long-term trend lines.

There’s some truth in the crash-call interpretation. Buffett has openly cited valuation discipline in his shareholder letters, and Abel echoed that language Saturday when he told shareholders Berkshire “can move it from insurance to non-insurance, into equities, or if we so choose, to hold it in cash.” But framing either of them as a market timer misreads the process. They don’t sell because they predict a crash. They sell because they can no longer find prices that justify the underlying business economics. Those are different statements that happen to look identical from the outside. The indicator above is consistent with the decision to stop buying. It’s not the same as a forecast that the market will fall next quarter.

Theory: Buffett Lost His Edge

The narrative that Buffett, at 95, simply couldn’t keep up with a bull market led by technology gained traction during 2023 and 2024. Berkshire trailed the S&P 500 in both years. Berkshire has now trailed the index by more than 30 percentage points since Buffett signaled his plan to step down last May. The Magnificent Seven were running, AI was the dominant story, and Berkshire’s portfolio looked stodgy by comparison.

However, I’ve heard this critique my entire career. It was wrong every previous time, and I’d argue it’s wrong now. Buffett’s framework is the same one he used in 1969, 1999, and 2007. The framework doesn’t fail. The market environments that cause its short-term underperformance are themselves brief and mean-reverting. And Abel’s decision to keep selling in his first quarter signals the framework isn’t going anywhere.

Reality: Berkshire Is Too Big For Its Own Process

Here’s the part that doesn’t make headlines but matters most. Berkshire’s market cap is now approaching $1 trillion. Buffett has said for years that “there remain only a handful of companies in this country capable of truly moving the needle at Berkshire.” When you need to put $50 billion or more to work in a single position to move the dial on a balance sheet that size, your universe of investable opportunities shrinks dramatically.

Add in the 20% takeover premium that Berkshire would have to pay to acquire any meaningful target, and the math gets brutal. A potential acquisition trading at 22x forward earnings quickly becomes 26x or 27x after the premium. That’s not a value investment, but rather a momentum trade dressed up in a board resolution.

Reality: Treasury Bills Were Paying You To Wait

The single most overlooked factor in this entire conversation is yield. From 2023 through most of 2025, short-term Treasury bills paid roughly 4-5%. That’s nothing. Berkshire generated about $8 billion in interest and other investment income in just the first three quarters of 2024, compared to $4.2 billion in the same period of 2023. Q1 2026 operating earnings just printed at $11.35 billion, up 18% year over year, with insurance underwriting profits up 28%. Net income more than doubled to $10.1 billion. The cash isn’t just sitting there. It’s compounding while it waits.

When cash itself produces a real return, the opportunity cost of waiting collapses. That’s a structural change from the 2010 to 2021 environment, when zero-rate cash was a guaranteed loss relative to any positive-return asset. The hoard wasn’t growing only because Buffett was selling and Abel kept selling; it had been compounding all along.

What The Cash Hoard Cost Shareholders

This is the part of the analysis no one wants to do, honestly. So let’s do it.

If we take the cash position averaged across 2023, 2024, and 2025, roughly $250 billion blended over the three years, and ask what that capital would have earned in the S&P 500 versus what it actually earned in Treasuries, we get a meaningful number. The S&P 500 returned approximately 26% in 2023, 25% in 2024, and 16% in 2025. Compounded against the average cash position, a hypothetical S&P 500 deployment would have produced roughly $155 billion in gains over the three years. The actual Treasury bill earnings on that cash came to about $34 billion. The forgone gain was approximately $125 billion.

That’s a real number. By any reasonable measure, holding that much cash during a sustained bull run costs Berkshire shareholders meaningful upside relative to a hypothetical fully invested alternative. The trailing 12 months tell the same story. Berkshire’s Class A shares have lagged the S&P 500 by a meaningful margin over the past year as the index has continued to grind higher, and Saturday’s earnings reaction was muted despite the operating beat.

Comparing Berkshire to the S&P 500 understates what a strict value framework actually missed during this cycle. The S&P is a blended benchmark. The basket Buffett genuinely sat out was the mega-cap growth complex. The cleanest investable proxy for that basket is the Vanguard Mega Cap Growth ETF (MGK), a fund built around the largest US growth names. It captures the Magnificent Seven and the broader leadership in AI names that drove the bulk of index returns from 2020 forward.

Looking at the ten-year price-return comparison anchors the cost differently. Over the period from May 2016 through April 2026, BRK.B delivered approximately 237% in cumulative price appreciation, while MGK returned roughly 398%. That’s a CAGR gap of about 4.5 percentage points per year, compounded across a full decade.

The chart above isn’t an indictment of Buffett, but rather a mirror. The companies that drove the spread, Nvidia, Microsoft, Apple at peak weighting, Alphabet, Meta, and Amazon, are precisely the ones Buffett either never owned in size or began trimming aggressively. The same discipline that has produced his long-term track record kept Berkshire underweight the very basket that won the decade. Whether that discipline is vindicated by an extended period of mean reversion or whether the mega-cap growth basket continues to compound at premium rates is the open question. The answer matters more for Abel’s first three years than almost any other variable he inherits.

Here’s where the analysis usually stops. It shouldn’t.

The calculation of the opportunity cost of Buffett’s cash assumes Berkshire could have deployed $397 billion into the S&P 500 at index returns. That’s a fantasy. Berkshire doesn’t allocate to index funds, even though Buffett often recommends that individual investors do. The mandate is to buy entire businesses or substantial equity stakes in great companies at fair prices. By 2024, those opportunities at Buffett’s required hurdle rate had effectively disappeared. Q1 2026 confirmed that Abel inherited the same problem.

The chart above isn’t an indictment of Buffett, but rather a mirror. The companies that drove the spread, Nvidia, Microsoft, Apple, at peak weighting, Alphabet, Meta, and Amazon, are precisely the ones Buffett either never owned in size or began trimming aggressively. The same discipline that has produced his long-term track record kept Berkshire underweight the very basket that won the decade. Whether that discipline is vindicated by an extended period of mean reversion or whether the mega-cap growth basket continues to compound at premium rates is the open question. The answer matters more for Abel’s first three years than almost any other variable he inherits.

Here’s where the analysis usually stops. It shouldn’t.

The calculation of the opportunity cost of Buffett’s cash assumes Berkshire could have deployed $397 billion into the S&P 500 at index returns. That’s a fantasy. Berkshire doesn’t allocate to index funds, even though Buffett often recommends that individual investors do. The mandate is to buy entire businesses or substantial equity stakes in great companies at fair prices. By 2024, those opportunities at Buffett’s required hurdle rate had effectively disappeared. Q1 2026 confirmed that Abel inherited the same problem.

The relevant counterfactual isn’t “S&P 500 returns minus Treasury yields.” The relevant counterfactual is what equities Berkshire could have actually bought, in the size it needed, at prices the team would defend in an annual letter. That set was very nearly empty in 2024. It remains nearly empty today.

There’s a second issue. Buffett’s actual track record requires you to measure performance over full cycles, not just the rising part of one. In 2022, when the S&P 500 fell 18%, Berkshire gained 4%. The cash looks like a drag in a bull market. However, it becomes the most valuable asset in the conglomerate’s portfolio when the cycle turns. Abel inherits that firepower at a moment of historically extreme valuations across the S&P 500. He used his first quarter to grow it rather than spend it. The full accounting will require seeing what he does with the dry powder over the next two to three years.

What This Means For Your Portfolio

If you’re managing your own money, the temptation is to map Buffett’s actions directly onto your situation. That’s a mistake. You’re not Berkshire or Warren Buffett. You don’t have a $1 trillion balance sheet, a 100+ year portfolio duration, and you don’t need to deploy $50 billion to move the needle. However, you can buy a $10,000 position in a great company without distorting the price of that company’s stock.

What you can take from this is more philosophical.

Yes, valuation matters. The S&P 500 entered 2026 at one of the most expensive starting points in history, with a CAPE ratio above 40 and a forward P/E that historically correlates with poor 10-year forward returns. Buffett’s cash position was a market signal even if it wasn’t a market call.

Sequence-of-returns risk is also real, especially for retirees or those approaching retirement. A market correction in the early years of retirement does permanent damage to a portfolio that a 30-year-old can absorb without consequence. Building a cash buffer when valuations are extreme is sound risk management, not market timing.

And finally, discipline beats fear of missing out. Every cycle produces a chorus of voices arguing that valuation no longer matters because of some structural innovation. In 1999, it was the internet. In 2007, it was the new financial alchemy of structured credit. In 2024, it was AI. The names change. The discipline that protects capital across cycles does not.

Regardless of where you align, the next two years will tell us whether the $397 billion cash hoard was the most prescient capital allocation decision of the cycle, or whether Abel will eventually validate the critics by paying up for assets Buffett refused to chase. His first quarter answered the immediate question. He kept selling, kept the discipline, and he let the cash hoard grow. I have my view on what comes next. The data, the discipline, and the sixty years of history all point in the same direction.

But I’ve been wrong before, and so has Buffett. We’ll find out together.

Tyler Durden

Mon, 05/18/2026 – 12:40

https://www.zerohedge.com/markets/buffett-cash-hoard-why-397-billion-sits-sidelines

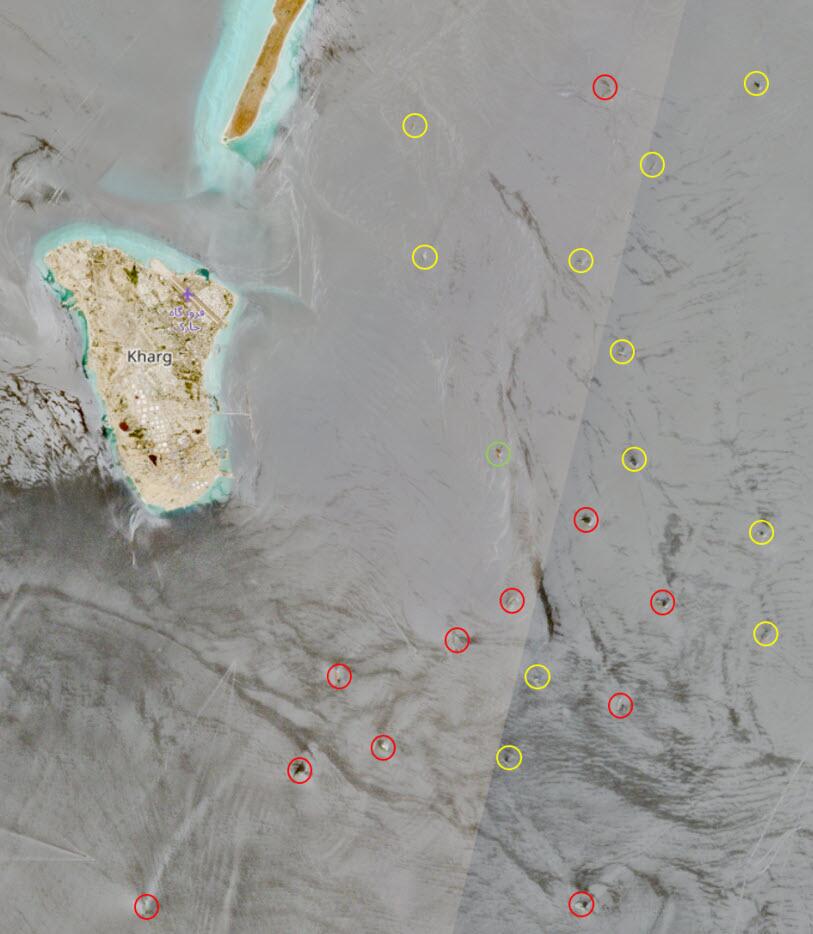

Iran Counter-Blockade Bites As No Tankers Load At Kharg For 10th Day

Iran Counter-Blockade Bites As No Tankers Load At Kharg For 10th Day

Earlier today, in response to news that the number of tankers anchored at Iran’s Kharg Island oil terminal had hit a post-blockade peak, we wondered if this means that Iran is running out of tankers to store oil, i.e., Trump’ blockade of the blockade is working. In any case, it certainly means that Iran is no longer able to sell any of the oil, depriving it of much needed oil export revenues which it has found itself forced to shut in as there is no open downstream path for the product.

Tanker Tally at Iran’s Kharg Island Hits Post-Blockade Peak: BBG

Running out of tankers to store oil.

— zerohedge (@zerohedge) May 18, 2026

A few hours later, Bloomberg echoed question, writing that Iran’s main oil export facility in the Persian Gulf stayed devoid of tankers for at least a 10th day, underscoring the growing strain on Tehran from a US naval blockade.

Using Sentinel satellite data of Kharg Islan, Bloomberg found that since May 8, no loadings of large ocean-going tankers are visible at the facility’s crude-export berths.

The counter blockade is depriving Tehran of critical petroleum revenue and the market of millions of barrels of supply. Prior to the US blockade, Iran was by far the largest – if not only – country exporting its crude because the Islamic Republic had blocked other countries’ ships from using the strait.

With no loaded tankers departing Kharg even as oil keeps arriving at the country’s largest oil terminal, it remains unclear how much of a factor lack of spare capacity has become as Trump hopes to cripple Iran’s oil production with lenghty shut-ins. Bloomberg’ Julian Lee writes that it’s hard to say the speed at which Kharg’ remaining capacity might fill given that Iran has curbed its output in response to the American blockade.

One possibility is that it’s cheaper for Tehran to use on-land facilities rather than filling ships, something that might help to explain the absence of loadings and a simultaneous buildup of tankers in nearby anchorage areas.

Here, Bloomberg’s other energy analyst Javier Blas chimes in, and notes that Iran is still loading crude into tankers (although not in Kharg Island). Instead, it’s loading a tanker at Jask, an alternative terminal outside the Strait of Hormuz. But since it is inside the US Navy blockade line, those tankers are likely only being used for storage purposes.

An image on Monday from the European Union’s Sentinel 1 satellite, examined by Bloomberg, shows a ship moored at Jask’s loading buoy. A separate image from the Sentinel 2 orbiter from Sunday shows an Aframax-sized vessel heading toward the mooring.

Iran is still loading crude into tankers — although (not right now) in Kharg Island. Instead, it’s loading a tanker at Jask, an alternative terminal outside the Strait of Hormuz (but inside the US Navy blockade line).

Left May 17 🛰️Sentinel-2; right, May 18 🛰️Sentinel-1 pic.twitter.com/iU2o6YXAmD

— Javier Blas (@JavierBlas) May 18, 2026

Vessel-tracking data compiled by Bloomberg identify the tanker as the Vernon, a ship that has been sanctioned by the US for its involvement in Iran’s oil trade. It remains to be seen if the ship will attempt to get through the American cordon.

There were no telephone or email contact details for the Panama-based company listed as the ship’s beneficial owner and manager on the Equasis maritime database, while emails to the ISM manager, based in Hong Kong, were returned as undeliverable

While Tehran appears to have shifted its primary loading terminal from Kharg to Jask, loading at Jask remains uncommon. The port has seen only nine carriers filled since the terminal was officially opened in 2021. Of those, five have taken place since the war began at the end of February.

Up to Friday, the US Navy had redirected 75 Iran-linked commercial vessels and disabled a further four since it imposed its blockade on April 13, US Central Command said in posts on X last week.

Tyler Durden

Mon, 05/18/2026 – 12:20

https://www.zerohedge.com/energy/iran-counter-blockade-bites-no-tankers-load-kharg-10th-day

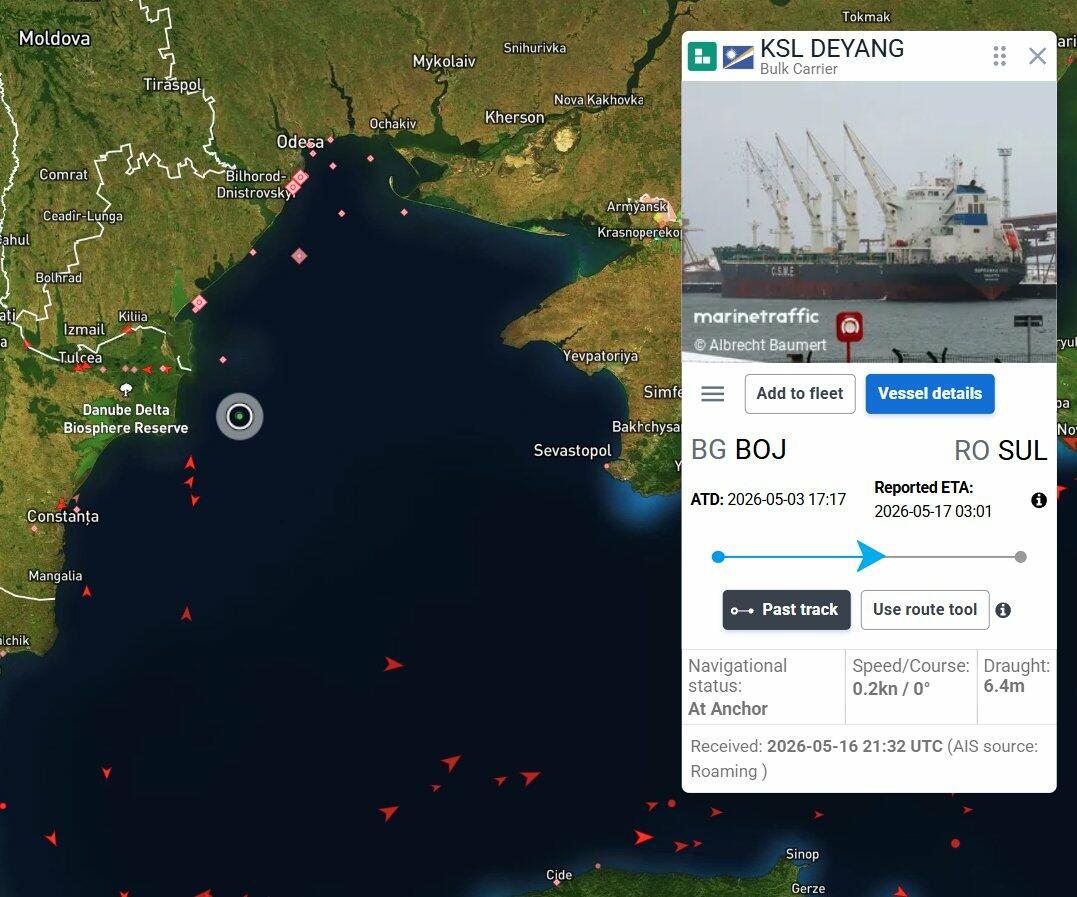

Russian Drone Hits Chinese Ship In Black Sea, Less Than 24-Hours Before Xi-Putin Summit

Russian Drone Hits Chinese Ship In Black Sea, Less Than 24-Hours Before Xi-Putin Summit

Just 24 hours before Presidents Vladimir Putin and Xi Jinping are set to meet for their planned summit in Beijing, soon on the heels of Trump’s visit, and a geopolitical wrench may have just been thrown into the works.

According to Ukrainian President Volodymyr Zelensky, Russian forces have attacked a Chinese ship heading toward a Ukrainian port – a provocative move that threatens to seriously anger Beijing at the worst possible diplomatic moment.

Early Monday morning, a Russian drone reportedly struck the KSL Deyang, a vessel flying under the Marshall Islands flag, just off the coast of Ukraine, Reuters also confirms.

The ship was reportedly empty at the time while en route to Ukraine’s Pivdennyi port in the Odesa region to load up on iron ore concentrate.

A fire was observed on board, but it was quickly brought under control and extinguished, with the vessel escaping severe damage.

The Ukrainian government is alleging this wasn’t some kind of accidental fog-of-war blunder, with President Zelensky immediately calling out Moscow:

“Drones struck Odesa … and one of the UAVs hit a vessel owned by China. The Russians could not have been unaware of what vessel was at sea,” Zelensky said.

A Ukrainian navy spokesman told AFP that none of the crew members, all Chinese nationals, were injured. He added that the vessel continued on its journey.

“The ship was entering for loading. After it was hit at night by a Shahed, the crew coped with the consequences on their own. Fortunately, no one was injured, and the vessel continued on its way to its port of destination,” navy spokesman Dmytro Pletenchuk said.

The incident went down just after on Sunday Xi and Putin had just exchanged “congratulatory letters” to set the stage for Putin’s upcoming arrival in Beijing.

The China-owned vessel wasn’t the only ship attacked within that span of time. According to The Independent:

Russia attacked a Panama-flagged civilian vessel heading to Ukraine’s Chornomorsk port in the southern Odesa region on the Black Sea early on Monday, the regional governor said.

It is one of several ships destined for Ukrainian ports that have been struck by Russian forces in the past day.

The vessel was damaged in the attack, which caused a fire, Governor Oleh Kiper said on the Telegram messaging app, adding that no one had been injured in the incident and that the crew had extinguished the fire. The vessel has continued on its way, the governor added.

TradeWinds is also suggesting a third ship was struck, but few details have been given. Black Sea transit continues to be a dangerous prospect, also with naval mines long being a feature of the 4+ year long war.

Tyler Durden

Mon, 05/18/2026 – 12:00

DoJ Establishes “Anti-Weaponization” Fund After Trump Drops $10 Billion Lawsuit Against IRS

DoJ Establishes “Anti-Weaponization” Fund After Trump Drops $10 Billion Lawsuit Against IRS

Update (1130ET): The DOJ announces that as a part of the settlement agreement in President Donald Trump v. the IRS, the Attorney General established “The Anti-Weaponization Fund” to provide a systematic process to hear and redress claims of others who suffered weaponization and lawfare.

“The machinery of government should never be weaponized against any American, and it is this Department’s intention to make right the wrongs that were previously done while ensuring this never happens again,” said Acting Attorney General Todd Blanche. “As part of this settlement, we are setting up a lawful process for victims of lawfare and weaponization to be heard and seek redress.”

“The use of government power to target individuals or entities for improper and unlawful political, personal, or ideological reasons should not be tolerated by any Administration,” said Principal Associate Deputy Attorney General Trent McCotter.

Bloomberg reports that the fund will receive $1.776 billion and will come from the judgment fund, which is a perpetual appropriation allowing DOJ to settle and pay cases.

The fund will have the power to issue formal apologies and monetary relief owed to claimants.

The Fund will consist of a Commission of five members appointed by the Attorney General. One Member will be chosen in consultation with congressional leadership. The President can remove any member, but a replacement must be chosen the same way as the replaced member was selected.

* * *

As Tom Ozimek detailed earlier via The Epoch Times, President Trump’s attorneys on Monday filed a court notice voluntarily dismissing his $10 billion lawsuit against the IRS and the U.S. Treasury Department, in a case that accused the agencies of failing to prevent a former contractor from leaking Trump’s tax returns to the media.

No reason was stated in the May 18 motion, which asks the court to dismiss the case with prejudice, meaning Trump and the other plaintiffs cannot bring the same claims again in the future. A court filing in April indicated that talks were underway to settle the case, with the parties stating at the time that discussions were taking place “productively to avoid protracted ligitation.”

Monday’s filing said the IRS and Treasury Department had neither filed an answer nor moved for summary judgment, allowing the plaintiffs to dismiss the action unilaterally without requiring court approval or government consent.

Trump, along with two of his sons and the Trump family business, sued the IRS and the Treasury Department in January, accusing both agencies of failing to take mandatory precautions to prevent former IRS contractor Charles “Chaz” Littlejohn from illegally obtaining access to their tax records and disclosing that information to The New York Times and ProPublica.

The lawsuit alleged that Littlejohn had “staff-like access” to confidential tax return information and exploited weaknesses in IRS safeguards to obtain and leak the records between 2019 and 2020.

Lawsuit Details

The lawsuit, filed in the U.S. District Court for the Southern District of Florida, sought at least $10 billion in damages and accused the IRS and THE Treasury of violating federal privacy laws governing taxpayer information.

Trump brought the suit in his personal capacity, while Donald Trump Jr., Eric Trump, and the Trump Organization were also named as plaintiffs.

Littlejohn, who at the time was employed by defense contractor Booz Allen Hamilton, was accused of having improperly accessed and disclosed tax information related to Trump and affiliated entities, including business holdings.

The plaintiffs claimed Littlejohn’s actions caused “reputational and financial harm, public embarrassment, unfairly tarnished their business reputations, portrayed them in a false light, and negatively affected President Trump, and the other plaintiffs’ public standing.”

The lawsuit argued that IRS and Treasury safeguards were so inadequate that the agency took roughly 3 years to detect the breach.

“Defendants had a duty to safeguard and protect Plaintiffs’ confidential tax returns and related tax return information from such unauthorized inspection and public disclosure,” the complaint alleged, pointing to the need for the agencies to have in place appropriate technical, employee screening, and monitoring systems to prevent Littlejohn’s actions.

“Defendants failed to take such mandatory precautions.”

Littlejohn pleaded guilty in October 2023 to one count of unauthorized disclosure of tax return information.

Prosecutors said he used broad search parameters to conceal his activities, uploaded stolen data to a private website to avoid IRS monitoring systems, and stored records on personal devices before providing them to media outlets.

In January 2024, U.S. District Judge Ana Reyes sentenced Littlejohn to five years in prison, the maximum sentence permitted under the statute. Reyes described the breach as the “biggest heist” in IRS history.

“It cannot be open season on our elected officials,” Reyes said, noting that Littlejohn purposefully sought his job at least in part to obtain and leak tax information.

Before Monday’s voluntary dismissal, the case had appeared to be moving toward a possible resolution in recent weeks.

In an April 17 filing, attorneys for Trump and the Justice Department jointly requested a 90-day pause in proceedings to allow settlement negotiations to continue.

The IRS and THE Treasury Department did not immediately respond to requests for comment on the dismissal filing.

Tyler Durden

Mon, 05/18/2026 – 11:40

https://www.zerohedge.com/political/trump-drops-10-billion-lawsuit-against-irs

Cuban Foreign Minister Says US Is Building ‘Fraudulent Case’ For Military Action

Cuban Foreign Minister Says US Is Building ‘Fraudulent Case’ For Military Action

Authored by Chris Summers via The Epoch Times (emphasis ours),

Cuban Foreign Minister Bruno Rodríguez on May 17 said the United States is building a “fraudulent case” to justify economic war and eventual military intervention against the Caribbean island nation.

His comments were a direct response to a report by Axios, which cited classified U.S. intelligence reports saying Cuba had obtained more than 300 military drones and had discussed using them against the U.S. military base at Guantanamo Bay, which is at the eastern end of the island. The Epoch Times is unable to verify the Axios report.

“Without any legitimate excuse, the #US government is building, day after day, a fraudulent case to justify a ruthless economic war against the Cuban people and eventual military aggression,” Rodriguez said in a post on X. “Specific media outlets are playing along, promoting slander and leaking insinuations from the U.S. government itself.”

The minister did not specifically mention the Axios report about military drones, and he did not formally deny that Cuba possessed such weapons, which have been used by both Russia and Iran, and Tehran’s proxies, in conflicts in recent years.

“Cuba does not threaten or desire war,” Rodriguez added. “It defends peace and is willing and preparing to confront external aggression in exercise of the right to legitimate self-defense recognized by the UN Charter.”

In a May 18 email to The Epoch Times, a U.S. State Department spokesperson said the U.S. president will always act “to protect Americans, our interests and our homeland from any threat.”

“President Trump … has taken historic action to rid our backyard of uncontrolled migration, dangerous narco trafficking, organized crime, and hostile foreign military presence,” the department said.

“Cuba, a failed Communist state which has long hosted hostile foreign military, intelligence and terror groups, presents a significant threat to our national security that President Trump will not allow to devolve into a greater crisis to the safety and security of Americans.”

In a May 17 post on X, Monroe County Sheriff’s office, which covers the Florida Keys, said, “Monroe County Sheriff Rick Ramsay has not been contacted by any federal or state authorities regarding news reports Sunday of any possible military action taken by Cuba against the U.S. military base in Cuba at Guantanamo Bay using drones.”

The post quoted Ramsay as saying he did not believe there was any reason to be concerned.

“I am confident I will be notified if anything does change and I will alert the public,” Ramsay added.

The Cuban ambassador to the United Nations, Ernesto Soberón, said in a May 17 post on X that the people of Cuba “stand ready to defend their territory, their sovereignty, and their independence.”

“Cuba would never initiate an attack on any country, let alone the United States,” Eva Golinger, an attorney and writer based in New York, said in a May 17 post on X. “They do, however, have the right to self defense under international law, as all countries do, if they are attacked.”

U.S. President Donald Trump has previously said Cuba persecutes and tortures political opponents, provides a safe haven for terrorist groups such as Hezbollah and Hamas, and constitutes an “extraordinary threat to U.S. national security and foreign policy.”

Last week, Cuba said it poses no threat to U.S. national security and that there are no legitimate grounds for it to remain on the list of state sponsors of terrorism.

CIA Director John Ratcliffe and other officials visited Cuba on May 14, at the invitation of the communist regime in Havana. At the time, the U.S. Embassy in Cuba referred The Epoch Times to the White House for comment, which in turn referred it to the CIA. The CIA didn’t respond to an email seeking comment on that meeting.

Fuel Crisis

Cuban Energy and Mines Minister Vicente de la O Levy said on May 13 that the country has completely run out of diesel and heavy fuel oil, and its power grid has entered a critical state.

O Levy said Cuba had not received any oil imports since December, until Russia sent 100,000 tons (about 700,000 barrels) of crude last month.

Trump said on Truth Social last week that Cuba was asking for help and that the two countries were going to talk.

The regime in Cuba was founded in 1959 after rebels led by Fidel Castro ousted U.S.-backed leader Fulgencio Batista. Under Castro’s leadership, the regime moved toward Marxism-Leninism and consolidated one-party communist rule in the years that followed. Cuba was closely allied with the Soviet Union until the bloc’s collapse in the early 1990s.

Cuba was heavily reliant on Venezuelan oil, supplied by former Venezuelan leader Nicolás Maduro’s socialist regime, but that supply was stopped after he was ousted in January and replaced by interim leader Delcy Rodríguez.

Mexico also stopped sending oil, under pressure from the United States.

The U.S. State Department said in a May 13 post on X that it “is publicly restating the United States’ generous offer to provide additional direct humanitarian assistance to the Cuban people.”

“The Cuban regime must decide whether to accept our offer or deny life-saving help for the Cuban people, who desperately need it,” the State Department said.

Tyler Durden

Mon, 05/18/2026 – 11:20

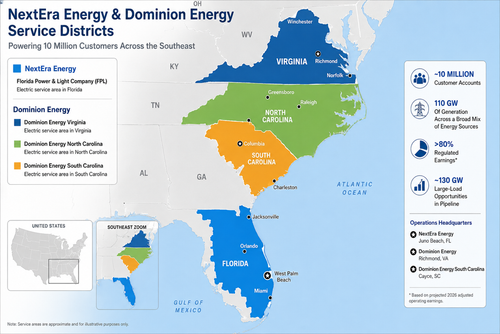

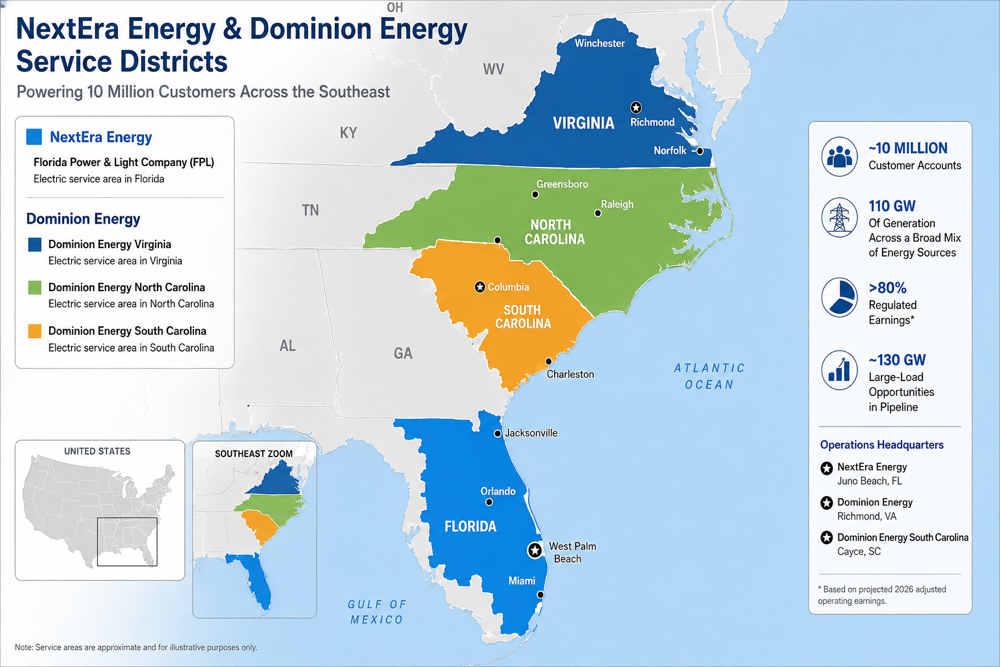

“Scale Matters”: NextEra, Dominion To Merge In Utility Megadeal Aimed At Grid Expansion To Power AI Boom

“Scale Matters”: NextEra, Dominion To Merge In Utility Megadeal Aimed At Grid Expansion To Power AI Boom

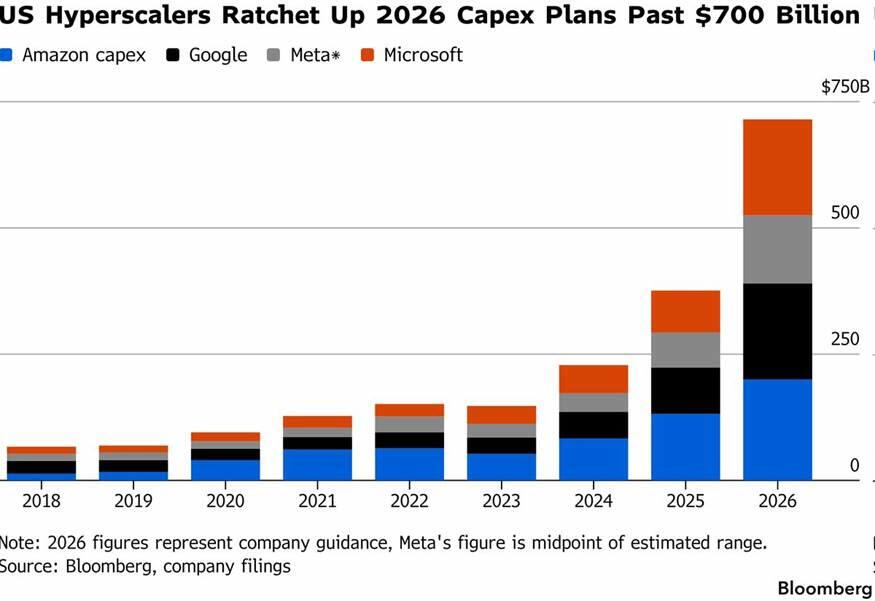

As power demand surges on the back of data-center buildouts, with hyperscalers expected to unleash about $700 billion in capex this year to expand AI infrastructure and maintain an edge over China in the AI compute race, NextEra Energy and Dominion Energy are moving to scale up. The utilities agreed to a $67 billion all-stock merger that would create the world’s largest regulated electric utility network.

Dominion shareholders will receive .8138 NextEra shares for each Dominion share, leaving NextEra investors with about 74.5% of the combined company and Dominion holders with 25.5%. The merged utility would be more than 80% regulated, serve 10 million customer accounts, and control about 110 gigawatts of generation capacity across the U.S. East Coast, from Florida to a cluster of data centers in Northern Virginia.

NextEra positioned the merger with Dominion as a way to quickly scale power grids along the East Coast while lowering power bills, as the era of AI data center buildouts only begins to accelerate:

With growth drivers evenly balanced between regulated and long-term contracted businesses and more than 130 GW of large-load opportunities in its pipeline, the combined company will have a broader opportunity set, more ways to grow and the scale, balance sheet and best-in-class operating, supply chain, construction and technology capabilities to deliver the generation, transmission and grid investments needed to serve customers, support economic growth and cost-effectively meet surging power demand while keeping bills affordable.

“The transaction is structured as a 100% stock-for-stock transaction and is expected to be tax-free to shareholders. The combined company will operate under the NextEra Energy name and trade on the New York Stock Exchange under the ticker symbol NEE,” NextEra wrote in the press release.

NextEra CEO John Ketchum said the merger is a “historic moment” and comes as “electricity demand is rising faster than it has in decades.”

Ketchum continued:

We are bringing NextEra Energy and Dominion Energy together because scale matters more than ever— not for the sake of size, but because scale translates into capital and operating efficiencies. It enables us to buy, build, finance and operate more efficiently, which translates into more affordable electricity for our customers in the long run.

The way the merger is framed appears aimed at federal regulators, who have seen growing resistance to data centers at the local level amid soaring power bills. It is worth noting that on some grids, especially in the Mid-Atlantic, backfiring green policies have collided with data-center buildouts and surging demand, sending power prices sky-high.

This earnings season was an eye-opener, as we noted that hyperscalers will deploy $700 billion in capex this year to support AI infrastructure.

In markets, shares of Dominion Energy soared 15%, while shares of NextEra remained flat.

Evercore ISI analyst Nicholas Amicucci noted that the merger will “likely face a significant amount of regulatory scrutiny.”

The way the merger is framed, as a means of scaling grids and supporting data-center buildouts while pitching affordable household power prices, is music to the ears of federal regulators.

Tyler Durden

Mon, 05/18/2026 – 10:45

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}