Category: News

Bond Markets Are Beginning To Panic Over Inflation

Bond Markets Are Beginning To Panic Over Inflation

By Benjamin Picton, Senior Market Strategist at Rabobank

Look To America

US equity indices closed lower yesterday but were comparative outperformers against European and Asian counterparts, which were roundly brutalized. The relative performance of equity markets reflects what is happening in oil markets, where the law of one price is being strained by a complete dearth of oil in Asia, a shortage of oil in Europe, and relative abundance in North America. The spread between West Texas crude and the more international Brent crude is now at its widest level since the Covid demand shock of 2020.

The oil market has fragmented: Oil is now trading for $150/bbl in Asia (except the occasional sanctioned Iranian tanker) where demand destruction has started. China and India most pressured.

Meanwhile it is still $100 in the US https://t.co/QweAyzEN0a pic.twitter.com/YyvgAMdMwl

— zerohedge (@zerohedge) March 17, 2026

At the risk of stating the obvious, the oil market is experiencing unprecedented tightness; the Brent prompt spread is current 4.55 sigma from the long-run mean. Dramatic as this is, it probably understates the severity of the situation in Asian markets where the loss of Gulf cargoes is being felt most acutely. The Wall Street Journal is today reporting warnings from Saudi Arabia that oil prices could spike as high as $180/bbl if disruptions persist into late April, and Reuters reported yesterday that Australia – a net energy exporter, but not of oil – is buying record volumes of products from ExxonMobil, BP and Vitol shipped from the United States.

Usually, Australia buys most of its oil products from Asian countries – especially Singapore. There’s a neat historical parallel here because 75 years ago Australian PM Curtin announced that “Australia looks to America” after the fall of Singapore to the Japanese. This time Australia is looking to America after the fall of the Singapore refining industry and confirmation overnight that the US will not be imposing export bans on oil. This will suit Donald Trump’s trade agenda and his efforts to corral tremulous allies just fine.

Speaking of which, it seems we are once again seeing signs that US allies may soon be doing things that only days ago they were indicating they would not do. Britain, France, Germany, Italy, the Netherlands and Japan have issued a joint statement condemning Iranian attacks on oil and gas infrastructure and the de factor closure of the Strait of Hormuz, while also saying that they are ready to “contribute to appropriate efforts to ensure safe passage through the Strait”.

It’s not immediately clear what this means. Presumably this is not declaring an intention to surrender and acquiesce to Iranian demands to pay a toll on commercial transits, so the most plausible interpretation seems to be that we are witnessing the formation of an international coalition backing American efforts re-open the Strait to shipping. This as news also emerged yesterday that a second US amphibious assault group is now headed to the Middle East, the Pentagon has asked Congress for $200m to fund the war, and as Benjamin Netanyahu said that “there has to be a ground component” to ensure the fall of the Islamic regime.

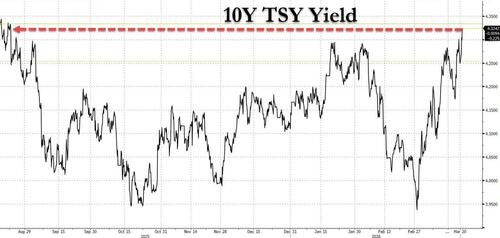

This all sounds like escalation, and bond markets are beginning to fret over the outlook for inflation as predictions over the duration and severity of the supply shock slide further towards the severe end. The Australian 10-year yield rose to its highest level since 2011 but the largest moves are happening at the short end of the curve where the two year yield is now up to 4.69%. Overnight index swaps currently imply a further 70bps worth of policy rate tightening in Australia this year, on top of the 50bps already delivered in February and March. UK 10-year gilt yields rose 11bps yesterday to 4.84% and 2-year gilt yields lifted by an astonishing 30bps.

The Bank of England and the European Central Bank both left policy rates unchanged yesterday, but were clearly hawkish in tone. The BoE said that it was “ready to act” if inflation pressures intensify, while also pointing out that existing slack in the economy means that the starting point for this energy shock is different to 2022. The ECB dropped references to being “in a good place” and reiterated its determination to ensure that inflation stabilises at 2% over the medium term, while making stagflationary updates to its economic projections. RaboResearch has now incorporated a rate hike as early as April in our BoE forecast, and a hike in April with the potential for a summer follow-up for the ECB.

In a meeting with Japanese PM Takaichi at the White House yesterday Donald Trump said that Japan had offered “tremendous support” in the war and reportedly indicated that he would be singing Japan’s praises when he meets with Xi Jinping in Beijing later this month. This is likely to be interpreted as a bolstering of the US-Japan partnership, coming as it does in the context of recent tensions between China and Japan over Taiwan.

Indeed, the China subtext behind recent U.S. policy actions is clear to anyone paying attention. Yesterday, the co‑founder of Supermicro and two other employees were indicted in New York for allegedly violating U.S. export controls by smuggling NVIDIA chip servers into China. On the same day, Trump and Takaichi announced a joint action plan on critical minerals aimed at reducing China’s dominance in global supply chains.

Meanwhile, U.S. Treasury Secretary Scott Bessent suggested that the United States may “un‑sanction” Iranian oil currently on the water that would have otherwise been destined for China, arguing that Beijing has been effectively funding a leading state sponsor of terrorism by purchasing discounted Iranian crude. According to Bessent, removing sanctions would lift Iranian oil prices to market levels and redirect flows away from China and toward other Asian countries who have been “good actors”. That’s as Netanyahu says that oil pipelines from the Arabian Peninsula to Israeli ports should be built in the future to prevent the world from being held hostage by a Hormuz blockade ever again. Needless to say, such a move would be an enormous re-alignment in favour of Washington and its allies.

So, while markets understandably continue to trade based on the day’s headlines, the bigger picture is that the global order is shifting under our feet and ultimately determining the price action. Oil is scarce, alliances are hardening, and central banks are preparing for a world where supply shocks might be structural rather than temporary. Hard power is being used alongside economic statecraft to achieve strategic aims. As our Global Strategist Michael Every is fond of asking: “if lines on a map can move, how much more can lines on a Bloomberg screen move?”

Tyler Durden

Fri, 03/20/2026 – 10:40

https://www.zerohedge.com/markets/bond-markets-are-beginning-panic-over-inflation

IEA Chief Warns Gulf Flows May Take Six Months To Restore After Biggest-Ever Energy Shock

IEA Chief Warns Gulf Flows May Take Six Months To Restore After Biggest-Ever Energy Shock

The head of the International Energy Agency told the Financial Times on Friday that the world is severely underestimating the scale of the Gulf energy shock, and that it may take at least six months to restore disrupted oil and gas flows.

Fatih Birol described the conflict, now in its third week, as “the greatest global energy security threat in history”, and said it would take time “to have oil and gas rehabilitated”.

“It will be six months for some [sites] to be operational, others much longer,” Birol warned.

Attacks on energy facilities in the Middle East continued this week, with Israel unleashing a firestorm by striking Iran’s South Pars gas facility, which led Iranian forces to launch attacks on Qatar’s LNG facilities that may take three to five years to return to full capacity.

Both attacks signaled that upstream energy assets were no longer off-limits, though Israel has since promised not to hit any more Iranian energy assets.

Goldman commodities expert Daan Struyven said his oil team’s near-term view remains as follows:

1) oil prices will likely continue to trend higher while Hormuz flows very remain low,

2) Brent is likely to exceed its 2008 all time high if depressed flows keep the market focused on the risk of lengthier disruptions, and

3) any rise in market perceived risks of US export restrictions is likely to widen the Brent-WTI price gap further. (denied today… for now)

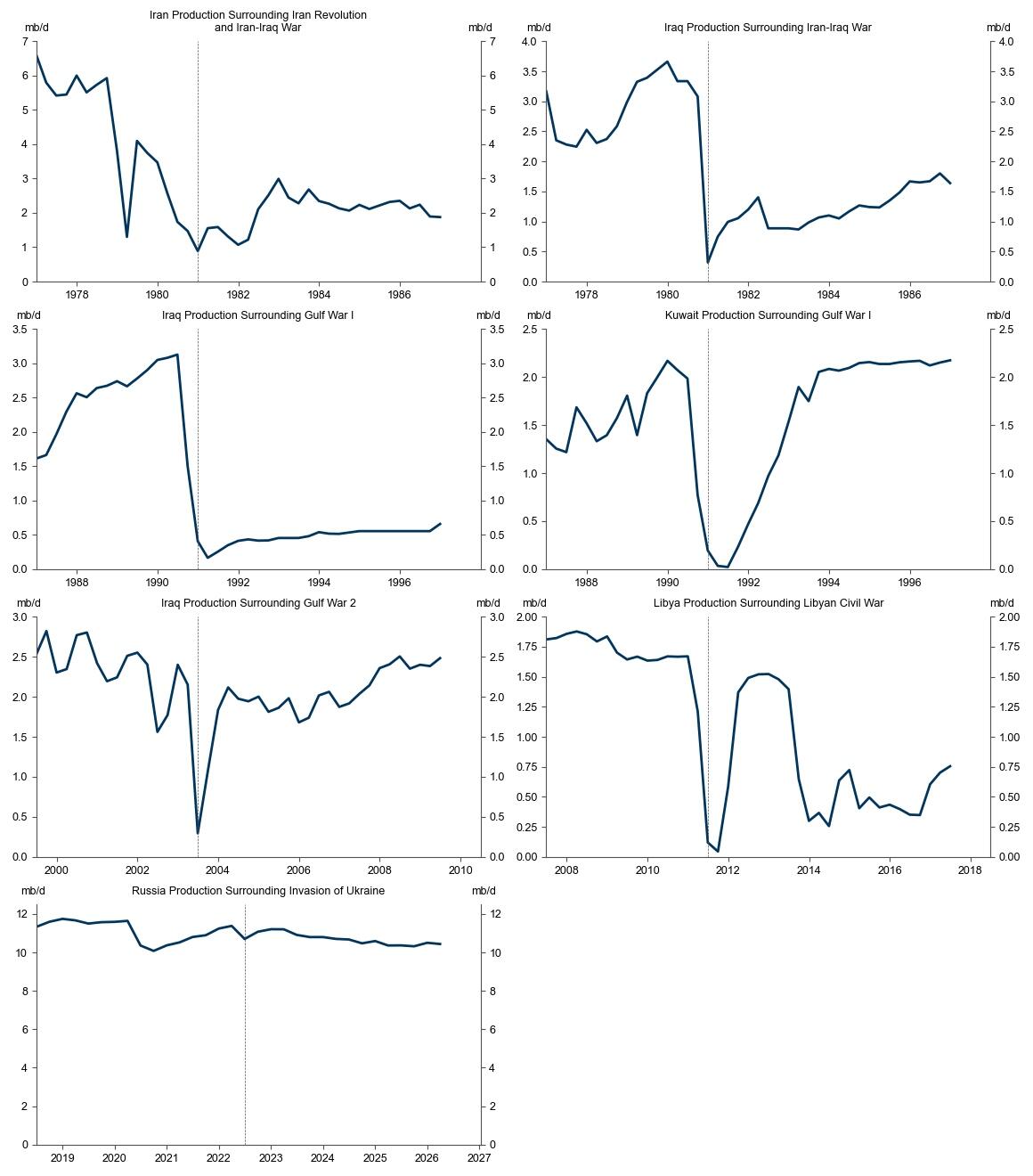

5 of the 7 Largest Historical Oil Supply Shocks in the Past 50 Years Were Persistent

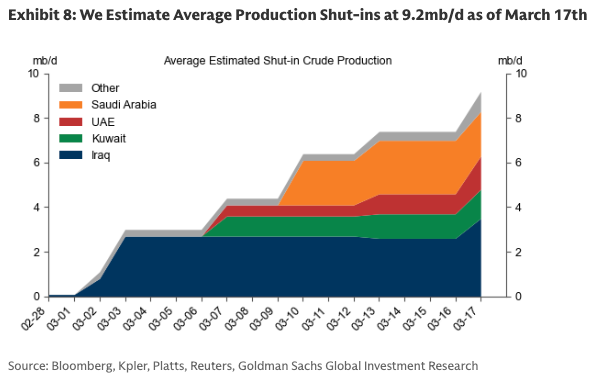

In a separate note, Goldman analyst Yulia Zhestkova Grigsby estimates that total crude production shut-ins (primarily due to precautionary curtailments and storage management) have reached 9.2 mb/d.

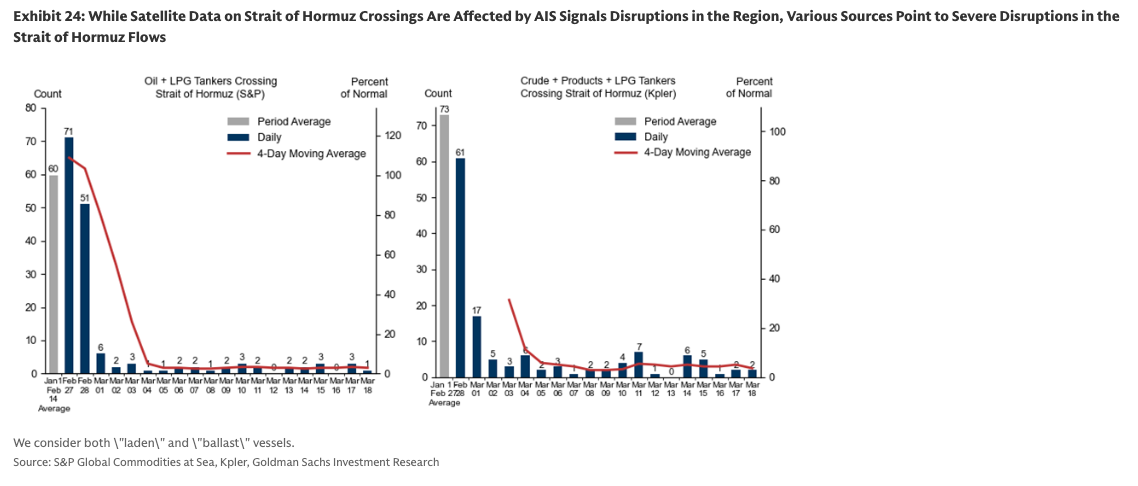

Strait of Hormuz tanker crossings by the end of the week show muted activity.

Commodity chaos has already arrived:

JPMorgan’s New Hormuz Closure Math: Just 3 Days Until Commodity Chaos

The Most Important Number For The Market: “25 Days”

Iran’s Attack On Qatar’s LNG Plant Is Bad; The Math Behind The Global LNG Fleet Is Far Worse

Brent Likely To Exceed 2008 All-Time-High, Goldman Sees ‘Higher Oil Prices For Longer’

The hardest-hit regions from the energy shock are in Asia at the moment because of their heavy reliance on imported Gulf energy. Let’s not forget that diesel prices in the US have jumped above $5/gallon.

“The countries that are exposed to that supply disruption are not so much in Europe, or in the Americas, they’re actually really in the Asia region,” Michael Williamson of the United Nations Economic and Social Commission for Asia and the Pacific, told AP News.

And now we have three oil markets: Asia (Oman oil at $167), Brent ($113) and US (WTI $97) https://t.co/uHmMD24E9G pic.twitter.com/41a4BhKOIA

— zerohedge (@zerohedge) March 19, 2026

Asia should prepare for “cascading impacts into all economic activities,” according to Ramnath Iyer of the U.S.-based Institute for Energy Economics and Financial Analysis.

Is it only a matter of time before the energy shock in Asia spreads to the region’s financial markets? There are already signs of credit market cracks (read here).

Tyler Durden

Fri, 03/20/2026 – 10:20

California Moves To Rename Cesar Chavez Day Before March 31 Holiday

California Moves To Rename Cesar Chavez Day Before March 31 Holiday

Authored by Jill McLaughlin via The Epoch Times,

California state lawmakers took steps on March 19 to remove Cesar Chavez’s name from a state holiday this year and replace it with “Farmworkers Day” after accusations against the civil rights icon of sexual assault involving children and women surfaced the day before.

The state became the latest to take action to change or cancel plans to celebrate Chavez as fallout over the accusations continued.

Cesar Chavez Day has been celebrated each year on March 31 in California, where Chavez first founded the National Farm Workers Association in 1962, which later became the United Farm Workers of America (UFW).

California was the first state to designate the labor leader’s birthday a legal holiday, celebrating Cesar Chavez Day as an official state-paid holiday in 2000, after former Gov. Gray Davis signed related legislation into law.

State Assembly Speaker Robert Rivas, son of a farmworker, introduced the name change in the state Capitol.

“As someone who grew up in the farmworker movement … I am shocked,” Rivas said. “The fact that many of these women were children when they were abused makes this even more heartbreaking.”

The New York Times published an article on March 18 stating that Chavez allegedly sexually abused and groomed minors as young as 13 who worked in the labor movement.

Labor leader and UFW co-founder Dolores Huerta came forward with her own allegations later in the day, claiming she secretly gave birth to two of Chavez’s children and gave them up after suffering sexual abuse.

Rivas said Huerta worked alongside his father to secure the first labor contract at Almaden Vineyards in the 1960s, and he respected her resilience.

“But let me be clear about something: The farmworker movement was never about one man,” Rivas said. “It was built by thousands—tens of thousands—of workers … Their legacy is not defined by one individual. It is defined by a movement—a movement for dignity, a movement for justice, a movement that still lives on today.

“And now we have a responsibility not just to remember that movement, but to carry it forward with integrity,” Rivas said.

California Gov. Gavin Newsom echoed Rivas’s sentiments about the name change.

“The farmworkers’ movement was always bigger than just one man or one person,” Newsom posted on X.

“Given the horrendous allegations that were made public for the first time yesterday, this is a welcomed change.”

Seven states have recognized a day on or near Chavez’s birthday as an official state holiday, including Arizona, California, Colorado, Minnesota, Texas, Utah, and Washington state.

President Barack Obama also signed a national proclamation designating March 31 as Cesar Chavez Day, but the federal day isn’t a paid holiday.

Texas canceled the holiday this year, hours after the allegations were made public.

Gov. Greg Abbott announced he would work with state lawmakers to permanently remove the holiday from state law this year.

Arizona Gov. Katie Hobbs has decided to decline to recognize March 31 as Cesar Chavez Day this year, according to her spokeswoman. The state recognizes the day but has not made it an official state holiday.

In Colorado, city leaders in Denver announced they would begin renaming and removing property, and would rename the city’s official holiday honoring Chavez.

The annual March 31 march will be renamed “Si Se Puede Day,” which is a Spanish term meaning “Yes, it can be done.” The term was coined by Huerta and popularized by Chavez in the 1970s and became a rallying cry for worker empowerment. The city passed legislation in 2001 making the day an official holiday and paid day off for city workers to replace Christopher Columbus Day.

National unions have also acted, withdrawing from celebrating Chavez this year.

The AFL-CIO said the allegations came as a shock and condemned the alleged actions.

The unions decided not to participate or endorse any activities for Cesar Chavez Day this year.

The UFW Foundation also announced it had canceled all Cesar Chavez Day activities.

In Washington, Rep. Tim Burchett (R-Tenn.) said he was preparing a letter to ask the secretary of War to remove the name of Cesar Chavez from the USNS Cesar Chavez.

The vessel was launched on May 5, 2012, and named in honor of Chavez, who served in the Navy from 1946 to 1948.

Last year, Rep. Gil Cisneros (D-Calif.) and 22 other Democratic congressional members sent a letter to Secretary of War Pete Hegseth asking him to retain Chavez’s name on the ship when the secretary decided to “take politics out of ship naming.”

They said renaming the vessel would dishonor his legacy. Hegseth retained the vessel’s name.

Tyler Durden

Fri, 03/20/2026 – 10:00

https://www.zerohedge.com/political/california-moves-rename-cesar-chavez-day-march-31-holiday

“Our Employees & Guests Were Uncomfortable”: Arkansas Gov. Sanders Told To Leave Restaurant

“Our Employees & Guests Were Uncomfortable”: Arkansas Gov. Sanders Told To Leave Restaurant

Republican Arkansas Gov. Sarah Huckabee Sanders was kicked out of another restaurant this week. Years ago, I wrote about how Sanders, then the Trump White House spokesperson, was told to leave the Red Hen restaurant in Lexington, Virginia. Now, the Croissanterie Restaurant in Little Rock, Arkansas, has told the governor to leave because employees said they felt uncomfortable having her in the restaurant. One person yelled at her and flipped her off as she left with her friends and security.

Sanders went to the restaurant with three other moms for a quick meal. She recounted how she and the other moms were then told to leave:

“Last week I was having lunch with two other moms at a restaurant when the owner approached a member of the State Police Executive Protection Detail and said my presence made their employees feel threatened and told us to leave.”

She added:

“Arkansans are known for their warm hospitality, and while that restaurant certainly doesn’t meet that standard, my administration will continue to focus on lifting Arkansans up, not tearing others down with discrimination and hate.”

Sanders had already started to eat when the restaurant’s owner approached a member of the security detail and requested that the governor leave.

The Croissanterie released a lengthy statement and admitted that they told the governor and her party to leave. While offering a hand-ringing explanation about being “surprised and uncertain how best to respond,” it admitted that it “ultimately made the decision” to “support our employees and guests who expressed they were uncomfortable.”

It added, “We regret being placed in this position and having to make a difficult decision. However, we stand by our choice to support our employees and guests.”

The restaurant is founded and owned by Jill McDonald, executive chef, and Wendy Schay, pastry chef.

We have seen various restaurants refusing to serve Trump supporters, conservatives, and even those deemed allies. Democratic members of Congress have defended such actions and even encouraged liberals to disrupt meals of conservatives.

Liberals went to social media to celebrate the move by the restaurant. One posting from an employee declared:

“Good Morning! Sarah Huckabee Sanders no amount of evil you send our way can ever take our smiles away!!! I’m proud af to work here! I’m proud af to be gay and I’m proud af to be an Arkansan. My voice matters. Try again.”

There have been virtually no condemnations from leading Democrats, who either fear or support such mob actions.

In my book, The Indispensable Right: Free Speech in an Age of Rage,” and my new book, Rage and the Republic, I discuss what I called this “age of rage.”

Rage is a curious emotion. It is the ultimate release. It allows you to do things and say things that you would not otherwise do or say. That is why it is addictive and contagious. What people will not admit is that they like it. It allows them to hate completely; to dispense with notions of decency or civility.

This restaurant yielded to hate and intolerance to appease not only its employees but the radical left.

This action occurs the same week as a poll showing that a majority of Americans now view those with opposing views as “morally bad.”

The rage addiction is obvious in these postings, as shown most recently by James Carville.

Democratic leaders believe that they can fuel this rage addiction and lead the mob to victory in the midterm elections. The cost is also to fuel the product of rage, including political violence.

The most recent targeting of Sanders presents a moral choice for the left. If you rationalize this action or continue to patronize restaurants like the Croissanterie Restaurant, you have made a choice. You have embraced the intolerance and hatred sweeping over this nation.

For all of their superficial expressions of reluctance, Jill McDonald and Wendy Schay chose hate over tolerance. While claiming to be “uncertain how best to respond,” the answer was obvious for anyone with a sense of decency: you serve everyone regardless of your political differences. Food like music allows people to come together; share common experiences and environments.

I truly believe that this age of rage will end as prior such ages ended. Eventually, the rage burns off and people recognize that their hatred had twisted them into grotesque figures. To reach that point, however, we must learn to again speak to each other and tolerate those who disagree with us. To put it simply, we have to break bread with one another and consider what we have in common.

Jill McDonald and Wendy Schay appear to want to cater to the rage and make their food exclusively available to those with whom they and their employees agree politically. We will have to see if that is a winning business strategy, but most of us have little appetite for their type of culinary-based hate.

Tyler Durden

Fri, 03/20/2026 – 09:25

Hormuz Showdown Begins: US Warplanes, Apaches Launch Sea Lane Offensive As Trump Eyes Kharg Takeover, Marines En Route

Hormuz Showdown Begins: US Warplanes, Apaches Launch Sea Lane Offensive As Trump Eyes Kharg Takeover, Marines En Route

Summary

IRGC contradicts Bibi: says missile production is ongoing, is of “no concern” – even as IRGC spokesman Ali Mohammad Naeini is reported killed.

Energy war ongoing: Major sites damaged across the region – Haifa refinery hit, Qatar LNG output cut 17%, Kuwait facilities ablaze.

Kharg Island escalation looms: Trump admin weighing seizure of Kharg Island to reopen Hormuz; Thousands of Marines in route, reports of low US jet strafing runs over strait.

Signal of zero restraint from Ayatollah & FM: Iran sends warning if energy sites are hit again, leadership structure grows opaque; supreme leader says enemies will be denied security.

* * *

IRGC Says Missile Production Intact, Contradicting Netanyahu

On day 21, the Iran war shows no signs of abating. Iran’s IRGC spokesperson Ali Mohammad Naeini was reportedly killed in an Israeli overnight strike, another high-level hit as the decapitation campaign grinds on.

However, Iran’s Revolutionary Guards said on Friday that the Islamic republic has continued to produce missiles despite the war with Israel and the United States. This directly contradicts Israeli PM Netanyahu’s assertions from the day prior, where he said both missile production capacity and uranium enrichment capability have been destroyed. Netanyahu had claimed, “Iran no longer has the capacity to enrich uranium and manufacture ballistic missiles.”

“Our missile industry deserves a perfect score…and there is no concern in this regard, because even under wartime conditions we continue missile production,” IRGC spokesman Ali Mohammad Naini said according to Fars.

⚡️Massive airstrikes in Iran this morning pic.twitter.com/5FBlymJ5V4

— War Monitor (@WarMonitors) March 20, 2026

Energy Complexes From Gulf to Israel Burning; Casualties Mount

The energy war continues to be front and center. Israel confirmed major Thursday Iranian strikes hit its Haifa refining complex, damaging critical infrastructure, and leaving many in the area without power. Also, the attack on Qatar’s Ras Laffan facility is expected to slash LNG export capacity by roughly 17%. Kuwait hasn’t been spared either, with its massive Mina al-Ahmadi refinery hit for a second straight day, with fires ripping through processing units.

Elsewhere, Bahrain says it has faced over 140 missiles and 240 drones since the war began, underscoring the scale of Iran’s regional barrage.

Across the region, escalation is bleeding into civilian life even in countries not directly part of the conflict. The biggest Muslim holiday of the year, Eid, is being celebrated, and in Iran the Persian New Year “Nowruz” – are unfolding under air raid sirens, also with fresh Israeli strikes in Lebanon and Syria. Currently Palestinians are being barred from Al-Aqsa during Eid. Casualties continue to mount with over 1,400 reported dead in Iran, including 204 children per the Red Crescent – and more than 1,000 killed in Lebanon.

Signs of US Plans to Take Kharg Island

But the real escalation risk surrounds what Washington’s next move may be, as the Trump administration is actively weighing seizing Kharg Island, Iran’s key export hub, in a desperate effort to force Hormuz back open. One source put it bluntly to Axios: “We need about a month to weaken the Iranians more with strikes, take the island, and then get them by the balls and use it for negotiations.” For all the bravado and rhetoric, some analysts see the situation as a classic escalation trap.

But the report says no final decision has been made, but the direction of travel is clear. “He wants Hormuz open… If he has to take Kharg Island… that’s going to happen,” one senior official said, while acknowledging a coastal invasion remains on the table.

The Wall Street Journal in fresh reporting sees signs that an operation is already underway: “The U.S. and its allies have intensified the battle to reopen the Strait of Hormuz, sending low-flying attack jets over the sea lanes to blast Iranian naval vessels and Apache helicopters to shoot down Iran’s deadly drones, American military officials said.” it writes.

Iran Vows ‘Zero Restraint’ If Its Energy Sites Attacked Again

Here’s what Iranian Foreign Minister Abbas Araghchi posted to X on Thursday: “Our response to Israel’s attack on our infrastructure employed FRACTION of our power. The ONLY reason for restraint was respect for requested de-escalation. ZERO restraint if our infrastructures are struck again. Any end to this war must address damage to our civilian sites.”

And CNN reports Friday: “Mojtaba Khamenei, who has made no public appearance since being chosen to succeed his father, said in a written statement security must be denied to all Iran’s enemies.”

Things are meanwhile getting more opaque in terms of leadership structure inside Iran: “Iran has not named replacements for the vast majority of senior officials killed by Israeli strikes since the conflict began on February 28,” CNN reports.

Iran’s strategy appears to be to survive while imposing severe high costs:

Every single day that this war goes on, the more the economic damage just compounds. This is the key line right here from @tracyalloway https://t.co/T6hrWxL1Op pic.twitter.com/t8Qos0vB1A

— Joe Weisenthal (@TheStalwart) March 19, 2026

Intense Attacks on Israel Continue

There has remained heavy censorship in Israel amid the war, but various overnight reports suggested another past 12 hours of heavy Iranian missile bombardment of Israel. Times of Israel confirmed, though without much in the way of details that sirens have been constant around central and northern Israel.

There were at least half a dozen missile salvos on Israel since late last night. “A home in the central city of Rehovot is burning following an apparent cluster munition impact, rescue services say,” TOI writes. “There are no immediate reports of injuries after Iran launched a ballistic missile carrying a cluster bomb warhead at central Israel.”

Flash90/TOI: The site of an Iranian missile impact in Rehovot, central Israel.

One war observer who has regional contacts wrote on X the following account: “Israel has been pummeled all night. Based on my counts of alerts and reports of landings from open sources the number increased tonight, though there are no reports of casualties.”

The journalist continues, “My Whatsapp groups are filled with people having breakdowns after not sleeping for two weeks. In Jerusalem 4 alerts were heard in a 90 minute span. Iran has been able to increase the number of launches daily. Everyone seems angry at the IDF and Netanyahu for lying about the destruction of Iranian capabilities.”

Tyler Durden

Fri, 03/20/2026 – 09:00

Futures Slide Ahead Of Massive $5.7 Trillion OpEx As Iran War Shows No Signs Of Easing

Futures Slide Ahead Of Massive $5.7 Trillion OpEx As Iran War Shows No Signs Of Easing

Futures are weaker heading into the weekend after US equities finished lower yesterday despite Netanyahu headlines leading to a late day bounceback into EOD. Geopolitical headlines remain the focus overnight with Brent rising as much as 90bps before reversing, as Iran pressed ahead with hitting energy assets & headlines that the US is considering plans to occupy Iran’s Kharg Island to press for the reopening of the Strait of Hormuz. As of 8:15am, S&P 500 futures fell 0.4% after finishing on Thursday under its 200-day moving average which could trigger even more forced selling; Nasdaq 100 futures declined 0.6%. US stocks are on course for a fourth week of losses, the longest losing streak in a year. Brent crude oil prices reversed earlier gains to decline 0.7% to around $108. The VIX rose to around 25. Elsewhere, it was a relatively quiet overnight with upward pressure on yields still the focus (USGG10YR +4bps @ 4.29%) amid concerns about hawkish central bank reaction functions. Metals are mostly lower: Aluminum -4.4%, Silver -1.0%. The US Dollar is up 0.2% as markets price in less than 5bp of Fed rate cuts this year, down from 60bp last month. There is no macro on today’s calendar.

In premarket trading, Mag 7 stocks are all lower (Alphabet -0.7%, Amazon -0.6%, Tesla -0.4%, Nvidia -0.5%, Meta -0.4%, Microsoft -0.5%, Apple -0.4%)

FedEx (FDX) climbs 7% after raising its full-year profit forecast, signaling that the courier’s plan to restructure its delivery network is gaining traction despite geopolitical conflict and economic volatility.

Figs Inc. (FIGS) rises 6% after Oppenheimer upgraded the seller of medical scrubs to outperform, saying a sustained recovery is underway.

Firefly Aerospace (FLY) gains 7% after the spacecraft maker reported revenue for the fourth quarter that beat the average analyst estimate

Planet Labs (PL) gains 14% after the satellite imaging firm reported revenue for the fourth quarter that beat the average analyst estimate.

Rhythm Pharmaceuticals (RYTM) rises 6% after the drugmaker said it received expanded indication approval from the FDA for its drug Imcivree (setmelanotide) to treat patients four years and older with acquired hypothalamic obesity.

Super Micro Computer Inc. (SMCI) tumbles 26% after the US charged a co-founder with illegally diverting billions of dollars in Nvidia Corp.-powered servers to China.

York Space Systems (YSS) rises 9% after the space and defense company gave revenue guidance in its first report as a public company that JPMorgan called “solid.” The firm also saw revenue grow and its losses narrow in the fourth quarter.

In other corporate news, at least a dozen large drugmakers are set to roll out copies of Novo Nordisk’s blockbuster weight-loss drugs in India, crashing prices as soon as the patent expires Friday. JPMorgan started a monitoring program to guard against overwork by its junior investment bankers, according to the Financial Times. Alibaba and Tencent lost $66 billion of market value in 24 hours after failing to lay out clear visions for how to profit off AI. Meanwhile, investors overwhelmed by Iran news are turning to AI tools – mining history for insights and context to assist work-flows and time management.

“Investors are stuck in geopolitical pinball right now,” said Max Gokhman, deputy CIO at Franklin Templeton Investment Solutions, as “literally and figuratively explosive developments are bouncing global market sentiment.” Confidence is being tested, and different schools of thought on the length of conflict are emerging.

An ugly, rollercoaster week is set to end with the Iran war – about to enter its third week – showing no signs of easing as Tehran keeps up attacks on Arab states in the Persian Gulf even after Israel signaled it would spare the country’s energy infrastructure. Axios reported the US is considering plans to take over Iran’s key oil-export site Kharg Island to add pressure on Tehran to reopen the Strait of Hormuz. Iran’s Revolutionary Guard insists it’s still building missiles and vowed the war will continue. Oil is headed for another weekly surge.

“I think that the market is right now coming to grips with the reality that higher energy prices are going to persist longer than expected,” said Mark Malek, chief investment officer at Siebert Financial. “It is clear that the Iran regime turned to the last page in its playbook: MAD, mutually assured destruction.”

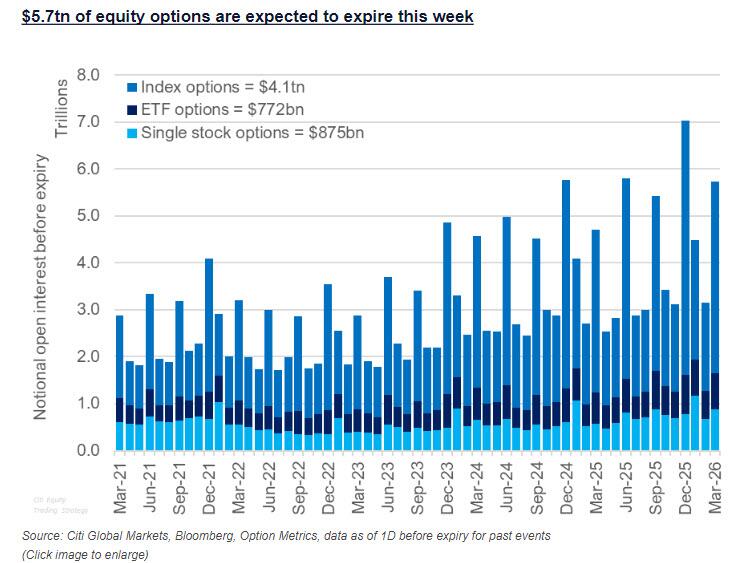

Meanwhile, traders braced for a historic amount of March options expiry. Roughly $5.7 trillion in notional options tied to individual US stocks, indexes and exchange-traded funds are set to expire on Friday in the quarterly event that traders have dubbed the “triple-witching”, the largest March expiry in 30 years and one the 4th largest ever. That includes $4.1 trillion in index contracts, $772 billion in exchange-traded funds and $875 billion in single-stock options. The event has a reputation for triggering abrupt price swings as large pools of derivatives exposure suddenly vanish. It also tends to reset dealer gamma sharply lower, unleashing an “unclenching” that lead to higher volatility in subsequent days. The scale of this week’s expiration is also notable relative to the broader market. At 8.4% of Russell 3000 Index market capitalization, it’s well above historical norms, amplifying the potential for positioning-driven flows.

Trading activity in options markets has surged in recent weeks, particularly in index and ETF contracts, both of which hit record notional volumes in March, about 9% above their year-to-date averages, according to Citi’s Vishal Vivek. In contrast, single-stock options volumes are roughly 3% below the level, a move partly attributed to waning retail participation and worries around geopolitical risks.

Stocks including Regeneron Pharmaceuticals Inc., PDD Holdings Inc. and T. Rowe Price Group Inc. are among those seen as vulnerable to outsized moves during the session as they have large open interest in options that expire near the current prices, according to Citi.

“Given recent volatility, today could almost be described as unchanged but clearly the bias has been lower,” said Sameer Samana, head of global equities and real assets at Wells Fargo Investment Institute. “I think the true test of today will be what investors decide to do at the close, before the weekend.”

Crude oil prices continued to be traders’ main concern as it affects inflation and consumer sentiment. The latest oil future curves showed “markets are beginning to price a more persistent ‘higher for longer’ oil backdrop,” Barclays strategists including Emmanuel Cau said in a note. “This dynamic is reinforcing stagflation concerns.”

On Wednesday, Jerome Powell said the Fed will not lower interest rates until inflation cools, as it was too early to determine the impact of rising oil prices on the US economy. The central bank left rates steady for a second straight meeting.

“We think the Fed staying on hold remains the most appropriate positioning,” said Deborah Cunningham, chief investment officer for global liquidity markets at Federated Hermes. “The current conflict with Iran is nowhere near the magnitude of the disruptions seen during COVID, nor the 2008 global financial crisis, so there is no justification for cutting rates by hundreds of basis points.”

Stocks have unwound earlier gains too, with the Stoxx 600 now flat. The construction sector outperforms while energy stocks lag. Here are some of the biggest movers on Friday:

CD Projekt’s share gain as much as 8.1%, the most since June, after it indicated it may release new gaming content to meet net income targets.

Spire Healthcare shares jump as much as 11% after Sky News reported buyout firm Bridgepoint is drawing up proposals for a formal offer worth £1b for the UK operator of private hospitals.

Elmos shares climb as much as 11% after Reuters reported the chip-equipment company is exploring a sale.

Zabka shares rise as much as 2.7% after the convenience store chain said it saw a rebound in sales since mid-February.

Inwit shares slide for a second day, as much as 9.7%, after the Italian tower company said Telecom Italia and Swisscom’s joint initiative to co-develop mobile towers will weigh on its growth.

J D Wetherspoon shares drop as much as 11%, the most in a year, after the pub chain warned rising costs and pressure on consumer finances “may result in profits that are slightly below current market expectations” this year.

Smiths Group shares fall as much as 5.5% to their lowest since July, after the UK manufacturing equipment group reported a somewhat light outlook.

Fuchs shares fall as much as 4.7% to the lowest since November 2022 after the German manufacturer of automotive and industrial lubricants forecast profits for the year that missed the average analyst estimate.

Earlier, Asian stocks dropped as tech companies like Alibaba Group Holding and Taiwan Semiconductor retreated. The MSCI Asia Pacific ex-Japan Index swung between gains and losses before breaking lower as the session wore on, dropping as much as 0.6%. Markets in Japan, Indonesia, Malaysia and the Philippines were closed for a holiday. Tech giants Alibaba and Tencent lost $66 billion of market value in roughly 24 hours, after the market punished the twin leaders of China’s tech arena for failing to lay out clear visions for how to profit off artificial intelligence.

In FX, the Bloomberg Dollar Spot Index is rising though mixed against major currencies, with the yen lagging.

USD/JPY rose 0.7% to 158.68, trimming weekly drop to 0.7%; Japanese markets were closed for a holiday on Friday. Tensions between the US and Japan over the Iran war remained evident as Trump hosted Prime Minister Sanae Takaichi, even as he said Tokyo was answering his call for support in the effort

EUR/USD slipped 0.3% to 1.1555; European government bonds edged lower as money markets continued to price in a high chance of three rate hikes through 2026. During a summit in Brussels on Thursday, EU leaders expressed anxiety at the economic situation and called for a “moratorium” on strikes against energy facilities

GBP/USD fell 0.2% to ~$1.34, while gilts extended Thursday’s drop triggered by a hawkish Bank of England stance; traders are betting on three hikes this year

In rates, yields rising across the curve in the US and Europe are being led by the short-end, with the UK underperforming for a second day, as bond markets extend their selloff as an initial paring in central bank rate hike bets in Europe reverses, as Brent crude edges toward new multiyear high close and Iran struck Arab states in the Persian Gulf. With US long-end yields only about 3bp higher, 2s10s and 5s30s spreads resume flattening, by 2bp and 3bp respectively. US 10-year is 4.5bp higher near 4.3% vs 9bp for UK counterpart, which reached 4.95%, highest level since 2008. A deeper selloff is gripping UK bonds as traders price in BOE rate hikes, while US short-term rate markets no longer see any chance of a Fed rate cut before next year. Fed-dated OIS contracts price in around 4bp of tightening for the April policy meeting; ECB swaps price in almost three 25bp rate hikes this year, while BOE swaps price in a combined 85bp of tightening by the December policy meeting.

In commodities, Brent crude futures have pared a gain of 2.4% to less than 0.2%, while US benchmark WTI crude is up 0.3%. Brent declined from its highest closing level since July 2022 to trade around $108 per barrel after Israel’s Prime Minister said the nation will no longer target energy infrastructure, and added that the war will end a lot faster than people think. Gold is fluctuating and now back below $4,700/oz. The precious metal is headed for the biggest weekly loss in six years, as war in the Middle East boosted energy and reduced expectations for rate cuts

There is no US economic data releases are scheduled, and Fed’s Bowman (8am) and Waller (8:30am) are slated to speak

Market Snapshot

S&P 500 mini -0.4%

Nasdaq 100 mini -0.5%

Russell 2000 mini -0.5%

Stoxx Europe 600 +0.2%

DAX +0.4%

CAC 40 +0.2%

10-year Treasury yield +4 basis points at 4.29%

VIX +0.5 points at 24.55

Bloomberg Dollar Index +0.2% at 1207.36

euro -0.2% at $1.1567

WTI crude little changed at $96.2/barrel

Top Overnight News

The U.S. and its allies have intensified the battle to reopen the Strait of Hormuz, sending low-flying attack jets over the sea lanes to blast Iranian naval vessels and Apache helicopters to shoot down Iran’s deadly drones, American military officials said. WSJ

Oil prices’ climb saw no letup as Iran pressed ahead with hitting energy assets. The country’s Revolutionary Guard insisted it is still building missiles and vowed the war will continue. Kuwait’s Mina Al-Ahmadi oil refinery shut down some units after a drone attack caused a fire. BBG

Saudi Arabia’s oil officials are working frantically to project how high oil prices might go if the Iran war and its disruption of energy supplies doesn’t end soon—and they don’t like what they are seeing. The base case, several oil officials in the Gulf’s biggest producer said, is that prices could soar past $180 a barrel if the disruptions persist until late April. WSJ

China is throttling exports of jet fuel, diesel and fertilisers, adding to fears in some of Asia’s biggest resource, manufacturing and agricultural nations that supplies could run short because of the war in the Middle East. FT

Wall Street braced for $5.7 trillion in options set to expire in today’s triple-witching, which risks injecting yet more volatility into a market that’s seen weeks of turbulence. BBG

In dollar terms, China’s GDP as a share of the global economy, peaked in 2021 at around 18.5%, when it grew to be around three quarters of the size of the U.S. economy. Many economists predicted China’s explosive growth would eventually make its economy bigger than that of the U.S. Instead China’s share of the pie has decreased, ending 2025 at around 16.5% of the global economy. It is now less than two-thirds the size of the U.S. economy, according to International Monetary Fund data. WSJ

Australia’s 10-year bond yields rose to an almost 15-year high as mounting inflation concerns drove traders to ramp up bets on RBA rate hikes. BBG

The ECB will need to consider hiking rates as soon as next month if price pressures build further due to the Iran war, Governing Council member Joachim Nagel said. Traders fully priced three rate hikes this year. BBG

Trump is dialing back his mass deportation push, shifting focus toward targeting criminals on political and voter concerns. WSJ

The Trump administration has delayed an executive order that could have required banks to collect and report more information on the immigration status of their customers, after Wall Street push-back: WaPo

US President Trump said at dinner with Japanese PM Takaichi that the US is encouraged to see Japan buying US defence equipment.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued but with downside limited as the region reacted to the recent oil swings, deluge of central bank meetings and mixed geopolitical headlines, while conditions were thinned – with the absence of Japanese participants due to the Vernal Equinox holiday. ASX 200 was dragged lower by weakness in the materials and commodity-related sectors, but with losses cushioned by strength in telecoms and defensives, while there were few fresh drivers overnight. Hang Seng and Shanghai Comp were following disappointing earnings results from the likes of Alibaba and CK Hutchison, with the former posting a 67% drop in Q3 net, which also weighed on other tech names. Furthermore, the PBoC’s reiteration to continue implementing a moderately accommodative monetary policy and to use RRR and MLF to ensure sufficient stability did little to inspire, while China’s Loan Prime Rate were unsurprisingly kept unchanged for the 10th consecutive month.

Top Asian News

Chinese Commerce Ministry releases measures to boost travel services, CCTV reported; announces measures to expand inbound consumption.

China’s government is said to be urged to reform consumption tax in order to boost local income, according to China’s Securities Journal.

European bourses kicked off cash trade on the front foot, rebounding from Thursday’s losses. The IBEX 35 is currently bouncing the most, closely followed by the DAX 40. The FTSE 100 lags, weighed on by losses in oil majors and Smiths Group, as the Co. cuts its 2026 organic revenue growth to between 3-4% from 4-6%. Futures however dipped following reports the Trump Administration is reportedly considering plans to occupy or blockade Iran’s Kharg Island to pressure Iran to reopen the Strait of Hormuz, according to Axios citing sources. Sectors point to a cyclical bias, with Construction and Materials and Banks sitting at the top of the pile. Energy and Media are the only sectors in the red.

Top European News

UK Public Sector Net Borrowing Ex Banks (Feb) 14.3B vs. Exp. 8.5B (Prev. -30.4B).

German PPI MoM (Feb) M/M -0.5% vs. Exp. 0.3% (Prev. -0.6%, Low. -0.1%, High. 0.7%).

German PPI YoY (Feb) Y/Y -3.3% vs. Exp. -2.7% (Prev. -3%, Low. -3.1%, High. -2.1%).

FX

DXY initial traded in a narrow range for most of the European morning before edging higher alongside crude following reports the Trump Administration is reportedly considering plans to occupy or blockade Iran’s Kharg Island to pressure Iran to reopen the Strait of Hormuz, Axios reported citing sources. The index edged higher to a 99.60 peak from a 99.25 low, still a way off yesterday’s 100.23 peak.

EUR/USD mildly pulled back overnight but trades relatively steady in a narrow range during the European morning. There have been several ECB speakers on the wires this morning, with Nagel suggesting that the ECB would need to hike in April if the price outlook sours, and will act with necessary resolve. The broad message by speakers suggested a meeting-by-meeting approach, echoing President Lagarde from her post-policy press conference. Pressure seen in recent trade on the aforementioned USD strength.

GBP/USD trickled lower overnight after strengthening in the aftermath of the BoE decision. GBP clambered off its worst levels briefly at the start of the European session but is now trading at session lows as energy prices grind higher. Pressure seen in recent trade on the aforementioned USD strength.

USD/JPY partially rebounds after slumping briefly below the 158.00 handle, while the mild recovery was facilitated by improved risk appetite, but with further momentum contained amid the absence of Japanese participants. JPY pressure was seen in recent trade on the aforementioned USD strength.

Antipodeans initially tilted higher on a positive risk mood but has turned lower since as tone begins to sour, with added pressure following the Axios report on the Kharg islands.

FX

ECB’s Nagel said the ECB would need a hike in April if the price outlook sours, will act with necessary resolve.

ECB’s Makhlouf says the ECB is currently managing extreme uncertainty, adds that action will be taken if facts point to action. Every meeting is a live meeting.

ECB’s Rehn said no decision has been locked in ahead of time.

ECB’s Villeroy said rate hikes will be decided meeting by meeting and are totally determined to bring inflation back to 2%.

ECB’s Villeroy said ECB will remain vigilant and has the ability to act as needed.

ECB’s Muller said duration of high energy prices is key for ECB.

ECB’s Kazak said we know that inflation will go up and economy will slow, and will take stock in April.

European Council appoints ECB’s Vujcic as the central bank’s Vice President to replace de Guindos as of June 1st.

Barclays now forecasts ECB will raise rates by 25bps each in April and June vs. previous hold outlook.

JP Morgan now expects ECB to hike interest rates in April and July, versus a previous forecast of holding rates unchanged throughout the year.

Goldman Sachs now expects BoE to remain on hold throughout 2026 vs. prior forecast of quarterly cuts from July.

Fixed Income

UST futures were initially on a firmer footing but are down some 3 ticks, largely moving in tandem with oil prices, with pressure seen across fixed income following reports that the Trump Administration is reportedly considering plans to occupy or blockade Iran’s Kharg Island to pressure Iran to reopen the Strait of Hormuz. Earlier gains were limited after the recent choppy performance and curve flattening on hawkish central bank expectations in response to the Iran war.

Bund futures trade lower amid the recent rise in crude prices. Upside has been contained following hawkish ECB reports yesterday, which noted officials see the need for possible rate hike talk to start in April, while ECB’s Nagel stated earlier the ECB would need to hike in April if the price outlook sours.

Gilts underperform, with price action has been driven by the rebound in energy prices following the aforementioned Axios report, while markets are now fully pricing in 3 rate hikes by the BoE in 2026. As a reminder, the Bank kept rates unchanged with all 9 policymakers voting for a hold.

China MOF sold 3-year bonds at 1.29% yield and 10-year bonds at 1.80% yield.

Trade/Tariffs

Chinese media, SCMP, writes that the White Houses’ Section 301 investigations may be less dramatic than war, but they risk retaliation and trade breakdowns.

White House posted Fact Sheet on US-Japan alliance and stated it welcomes a second tranche of Japanese investments and that US and Japan reached a critical minerals action plan.

Commodities

Crude futures initially traded with modest losses as the European session got underway but has steadily reversed higher following an Axios report stating that the Trump administration is considering plans to occupy or blockade Iran’s Kharg Island to pressure Iran to reopen the Strait of Hormuz. WTI regains the USD 96/bbl handle following the report, while Brent extends beyond USD 110/bbl. Comments from US Treasury Secretary Bessent late in Thursday’s session stated that the US could pursue another SPR release to keep prices down and may lift sanctions on Iranian oil but that has since been put in the rear view.

Spot gold stabilises after its recent slide, although remaining on course for its worst weekly loss in six years following a deluge of hawkish-leaning central bank updates amid inflationary pressures driven by the war-related surge in oil prices. Spot gold resides in a USD 4,634-4,736/oz range.

Copper futures have followed on from Thursday’s selloff as the dollar gains following the rebound in energy prices.

SinoChem (600500 CH) reportedly cut throughput at its 300k BPD Quanzhou refinery to ~60%, sources say; also reduces operations at steam cracker to ~60%; seeking prompt delivery crude oil, including Russian oil under waver, to cover the supply gap.

Russia is to limit major foreign container shipping companies from routes involving Russian ports unless they meet strict domestic control requirements.

Spain is to reduce VAT on fuel from 21% to 10% to mitigate the impact of the Iran war, Ser Radio reported.

Saudi officials see the base case for oil to rise to USD 180/bbl if the disruptions persist until late April, according to WSJ.

EU member states to request EU Commission design national temporary and targeted measures to mitigate impacts on energy costs, according to a draft document.

South32 (S32 AT) pauses production at the world’s biggest manganese mine due to cyclone threat.

Geopolitics

The Trump Administration is reportedly considering plans to occupy or blockade Iran’s Kharg Island to pressure Iran to reopen the Strait of Hormuz, Axios reports citing sources.

Iran announces the death of IRGC spokesperson Narini.

Iranian Supreme Leader Khamenei said officials must compensate for the loss of the Iranian Minister of Security, Al Hadath reported.

Iranian President said “the flames of war against us will affect many if the international community does not stand up to the aggression”, Al Jazeera reported.

Iran’s Foreign Minister told his UK counterpart that providing military bases for the US will be considered as participation in aggression.

Iran’s IRGC spokesman, responding to Israeli PM, insists Tehran is still building missiles, AP reported.

Iran’s Revolutionary Guards report that missile manufacturing remains active amid conflict and stockpiles are sufficient.

Iran is said to allow more Indian vessels to pass the Strait of Hormuz.

IDF launches a wave of strikes on infrastructure targets across Iran.

Explosion heard in Iranian city of Isfahan, according to Iran International.

Saudi Arabia’s eastern region saw further drone interceptions, with several threats destroyed.

EU leaders call for de-escalation, civilian protection and full respect of international law by all parties, while they call for moratorium on strikes targeting energy and water infrastructure, also strongly condemned Iran’s indiscriminate strikes.

German Chancellor Merz said EU leaders have asked the European Commission to examine other possible ways of paying out loans to Ukraine.

US Event Calendar

8:00 am: United States Fed’s Bowman Speaks on Fox Business

8:30 am: United States Fed’s Waller Speaks on CNBC

DB’s Jim Reid concludes the overnight wrap

Today will be the 15th trading day of the conflict so far and as I showed in yesterday’s CoTD (link here), that is on average when we bottom out in US equities after a geopolitical shock. However it would be hard to trade on the back of averages at the moment with so much uncertainty so headlines will be more important than history here but if you’re looking for optimism the normal geopolitical playbook would at least give you hope. So far we haven’t deviated from it.

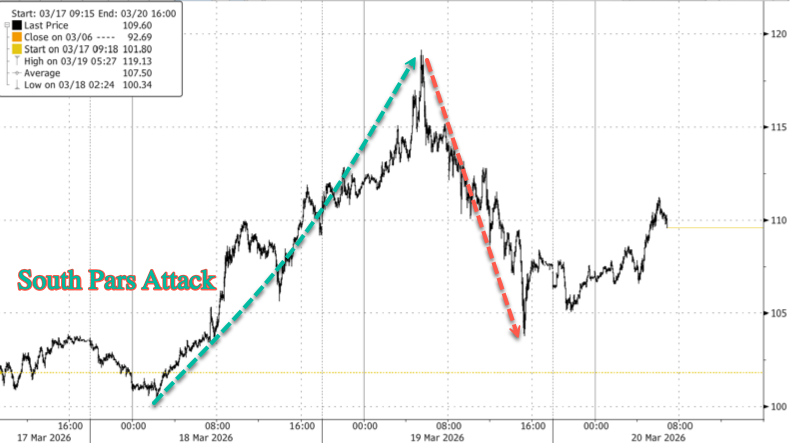

The news flow hasn’t slowed down though, and there’s been so much going on over the last 24 hours, even more over the last 36, that it’s hard to know where to start. The main saving grace after another challenging session was that the price of Brent was well off the $119.13/barrel highs (+10.9% at that point) we reached around 9:30am London time yesterday, a couple hours after European gas futures opened up nearly +35%. They eventually closed +1.18% higher at $108.65/bbl and +13.15% at €61.85/MWh respectively, in turn their highest levels since July 2022 and January 2023. As I type this morning, Brent is at $107.31/bbl, coming off the highs as Israel and the US signaled a desire to avoid further strikes against energy infrastructure that had stoked the market turmoil late on Wednesday and early yesterday. That helped the S&P 500 (-0.27%) recover most of its initial losses, even as the STOXX 600 (-2.39%) earlier posted its worst close of 2026 so far.

Elsewhere, markets also had plenty of other events to react to, with the ECB, BoE, and other central banks across Europe holding policy rates steady in reaction to the ongoing conflict. However, some hawkish interpretations of those on hold decisions, especially that of the BoE, coupled with the energy concerns led to a big global bond sell-off at the front-end. This was most pronounced in Europe, with 2yr gilt yields registering their largest rise (+31bps) since 2022, with about half coming after the BoE meeting. 2yr bund yields rose by +14.5bps to 2.59%, their highest since July 2024. And in the US, 2yr Treasury yields spiked by as much as 15bps though they largely reversed this rise by the close (+1.6bps to 3.79%). At this point, the Fed is the only G10 central bank that is still (albeit very marginally) pricing easing later this year and at one point yesterday, markets no longer priced in cuts for the next few quarters for the first time in the Fed’s post-2024 easing cycle.

Before we delve into yesterday’s central bank decisions, the most recent developments on the Middle East has been an easing of fears that Wednesday’s energy infrastructure attacks would spiral into something worse. That comes as Israel’s Prime Minister Netanyahu said yesterday evening that Israel would no longer target Iran’s energy infrastructure, with Donald Trump also saying that he had told Netanyahu not to attack Iran’s energy fields. Earlier yesterday, Iran’s Foreign Minister Abbas Araghchi posted on X that Iran would show “ZERO restraint if our infrastructure are struck again”, while mentioning the phrase “requested de-escalation”. All that left a sense that we could see a truce when it comes to strikes against energy facilities, even as there’s still little visibility on reopening the Strait of Hormuz or ending the overall war. Indeed, with the Pentagon reportedly asking the White House for a $200bn funding request to Congress, it may be readying for a more protracted conflict.

Some of the peak energy stress earlier yesterday had come as Qatar’s energy officials said that Iran’s attack damaged 2 out of its 14 LNG trains, which represent ~17% of Qatar’s LNG exports and that the damage will take “between three to five years to repair”. While this is likely to lead to lingering stress in the gas market, the easing of the oil market stress through the course of yesterday has brought Brent back to $107.31/bbl this morning. And WTI is down to $94.16/bbl, with the relatively more protected energy position of the US becoming more visible in market pricing.

The S&P 500 erased most of its -1% opening decline but still closed -0.27% lower. However, S&P 500 futures trading are edging +0.10% higher this morning, with those on the STOXX 50 up by a larger +0.64% after yesterday’s slump. Meanwhile, the combination of moderating geopolitical fears and relatively lower US yields saw the dollar index (-0.85%) post its worst day since August yesterday, while gold (-3.50% to $4,650/oz) fell to its lowest level in two months amid the global repricing in front-end rates.

Turning to those central bank meetings, the ECB left their deposit rate on hold at 2%, with President Lagarde exuding calmness in the press conference as she argued that the bank is “well positioned and well equipped” to deal with the energy shock. Lagarde’s comments suggested that the ECB would rather wait for evidence on second-round effects before deciding on any policy change. However, her comment that “we are starting from a good base” pointed to risks now being tilted towards hikes and she did not rule out more imminent action. Our European economists now expect 50bps of risk management hikes to 2.50% in the coming months, penciling June and September as the most likely timing. See their full reaction here. Following the meeting, Bloomberg reported that the ECB would be ready to raise rates as early as April if the Iran war pushed inflation too far above target, though a later hike could be more likely. With this backdrop, market pricing of an April hike rose from 36% to 63% on the day, with about 66bps of ECB hikes priced by year-end.

But it was the BoE that delivered the clearest hawkish surprise versus expectations, even as it held the Bank Rate steady at 3.75%. For the first time since September 2021 the decision was a 9-0 vote, confounding expectations that a couple members would still favour a cut. And the MPC stated that it would “stand ready to act” to contain inflation at the 2% target, removing the earlier easing bias. So while Governor Bailey cautioned later in the day against jumping to “strong conclusions”, investors dialled up expectations of BoE rate hikes in 2026 to +70bps (+49bps on the day), with a 53% chance of a hike priced in for April. Our UK economist has changed his call to no longer expect any rate cuts this year, with the prospect of rate hikes also possible should limited fiscal support to curb inflation materialise, and if the Iran conflict lasts into April and beyond. You can see his full take here.

The hawkish BoE decision, the timing of which coincided with the bond market open in the US, triggered a sharp front-end selloff as discussed at the top. The moves were more modest further out the curve, though 10yr bonds also sold off across the continent, with gilt (+10.8bps), bund (+1.7bps), BTP (+5.0bps) and OAT (+3.6bps) yields all moving higher. The underperformance in BTPs came after Italy announced yesterday that it would make a temporary 20-day tax cut on fuel, becoming the first large European country to use fiscal measures to alleviate surging energy costs. Meanwhile, the energy fears saw many European equity indices fall by more than 2% yesterday, including the STOXX 600 (-2.39%), FTSE 100 (-2.35%), DAX (-2.82%) and CAC 40 (-2.03%), although part of that was due to Europe catching up to Wednesday’s overnight news of Iran’s attack against Qatar’s LNG facility.

In terms of the other central bank decisions, the Riksbank left its policy rate at 1.75%, with the governor saying that it is expected to remain at this level for some time, though alternative scenarios showed a wide range of uncertainty on the rate path ahead. Finally, the SNB left policy rates at zero while incorporating their new, higher willingness to lean against Swiss Franc strength into their policy statement. See more from our FX strategists here.

Asian equity markets are fairly quiet this morning which can only be a positive thing at the moment. Japan is closed for a holiday with the Hang Seng (-0.63%) and the S&P/ASX 200 (-0.82%) lower but with the KOSPI (+0.52%) higher again on the back of tech stocks, and is now up over 5% this week.

In monetary policy action, China’s central bank kept its loan prime rates unchanged for a tenth straight month, with the one-year LPR held at 3.00% and the five-year rate, which influences mortgage pricing, at 3.50%, in line with market expectations.

To the day ahead now, we’ll get the UK’s February public finances, Germany Feb PPI, Italy January trade balance, current account balance, ECB January current account, Eurozone January trade balance, Canada January retail sales. The ECB’s Nagel will also speak today.

Tyler Durden

Fri, 03/20/2026 – 08:37

“Lot Of Questions On Structure:” Goldman Reacts To Old Bay Maker’s Bid For Unilever Food Unit

“Lot Of Questions On Structure:” Goldman Reacts To Old Bay Maker’s Bid For Unilever Food Unit

Bloomberg reported earlier this week that Unilever Plc was in early talks to sell its food business – a move that would end its competition with major packaged-food rivals, including Nestlé, PepsiCo, and Kraft Heinz.

By Friday morning, Unilever stated in a press release that, despite “media speculation regarding a potential transaction involving its Foods business,” it had, in fact, received an “inbound offer” for the unit from Hunt Valley, Maryland-based McCormick & Company.

“Unilever confirms that it has received an inbound offer for its Foods business and is in discussions with McCormick & Company, Inc. There can be no certainty that any transaction will be agreed,” the Anglo-Dutch consumer goods company said.

Bloomberg reported earlier this week that Unilever was in the early stages of offloading all or part of its food business.

Unilever CEO Fernando Fernandez is making a strategic shift to secure at least higher-growth revenue from personal care, wellness, and beauty products, pivoting away from lower-margin food items. Fernandez is now a year into the turnaround plan.

Unilever shares rose nearly 2% in London trading on the news. The stock is down 5% year to date and has traded sideways since 2019. McCormick shares in premarket trading in New York were flat. This year, shares are down 20% and have halved from their 2022 peak above $100.

Goldman analyst Natasha de la Grense offered her first take on a potential deal in which McCormick could acquire Unilever’s food unit.

Has confirmed that it is in talks with McCormick regarding an offer for its Food business. In the context of investor feedback earlier this week revealing limited appetite for a long, messy spin-off, it is encouraging we’ve had two reports of trade buyer interest for this asset (one of which is now confirmed).

Note that there would likely be less of an anti-trust concern for Unilever Food combining with McCormick (than Kraft Heinz). Lots of questions on structure with investors noting Unilever Foods is larger, more profitable and should trade on a higher premium.

WSJ and Reuters mention a 100% equity deal but people view that as an unlikely outcome given aforementioned points. Most investors we spoke with are considering a merged entity in which Unilever retains a majority stake but also receives some cash.

This would enable deconsolidation of Food but participation for Unilever in upside associated with merger synergies (which could potentially offset dissynergies for Unilever group). As mentioned earlier this week, investors see merit in an exit of Food from a long term growth and multiple perspective although are wary of cash/profit dilution.

For McCormick, the deal would accelerate its push beyond spices into condiments and branded foods.

Known for Old Bay seasoning, the company would be building on prior acquisitions such as French’s and Frank’s RedHot.

Tyler Durden

Fri, 03/20/2026 – 08:25

The Debt Can Is Getting Harder To Kick

The Debt Can Is Getting Harder To Kick

Authored by Timothy Nash, Bob Thomas, George Lang, & Tom Rastin via RCP,

In the book When We Are Free, an anthology published by Northwood University Press with a foreword by Milton Friedman, economic historian Dr. Lawrence W. Reed contributed a chapter titled The Fall of Rome and Modern Parallels.Reed examines how the Roman Empire collapsed and draws striking comparisons to the fiscal habits of modern governments.

His warning is worth revisiting today.

In the United States, federal law does not allow states to declare bankruptcy. To prevent fiscal collapse, 49 out of 50 states operate under some form of balanced budget requirement. These rules force policymakers to make difficult decisions each year and prevent deficits from spiraling out of control.

The federal government operates very differently.

Today the U.S. national debt now totals $38.9 trillion, about 125% of GDP, while state and local debt is $3.3 trillion, under 11% of GDP. In 1900, total U.S. debt was just 7.8% of GDP, mostly held by states and local governments. Even in 1981, federal debt was roughly 36% of GDP and barely exceeded $1 trillion.

In other words, the federal government has moved from a relatively small borrower to the dominant source of public debt in the American economy.

Lessons From History

History offers many examples of nations that allowed debt and spending to grow beyond sustainable limits. The Roman Empire collapsed in 476 AD after decades of fiscal strain, inflation, and military spending. Germany’s Weimar Republic unraveled in the early twentieth century after economic instability and runaway inflation destroyed public confidence in the currency and brought Hitler to power. These events did not occur overnight; they were the result of years of postponing hard fiscal choices.

The underlying lesson is this: excessive government borrowing eventually limits economic growth, weakens currency stability, and places heavy burdens on future taxpayers.

According to the U.S. Treasury, federal spending now exceeds $7 trillion annually, with annual deficits surpassing $1.7 trillion. Meanwhile, debt per American citizen is roughly $113,000, and debt per taxpayer exceeds $350,000.

The largest federal expenditures remain familiar: Social Security, Medicare and Medicaid, and national defense. These commitments reflect important national priorities. But when spending rises faster than economic growth, deficits accumulate quickly.

Debt Is Growing at Every Level

The Federal Reserve Bank reports that total U.S. household debt reached $18.8 trillion in late 2025, driven by increases in mortgages, auto loans, credit cards, and student loans.

Even retirement savings, long viewed as a financial safety net, are increasingly being tapped for short-term emergencies. According to a recent Wall Street Journal report, hardship withdrawals from 401(k) accounts increased for six consecutive years. The most common reasons for withdrawals include avoiding eviction or foreclosure and paying medical expenses.

This trend highlights a growing financial fragility among American households. While retirement balances have reached record highs, roughly $168,000, many workers still struggle to maintain financial stability when unexpected costs arise.

At the same time, consumer borrowing continues to expand. Auto loan balances reached $1.67 trillion, credit card balances topped $1.28 trillion, and home equity borrowing has also begun rising again.

These numbers tell a broader story. Americans, like the federal government, are increasingly relying on debt to maintain current spending levels.

New Uncertainty Around Government Revenues

Tariffs were once expected to generate substantial government revenue. However, recent court rulings challenging the legality of certain tariffs have introduced uncertainty about whether those funds, estimated at roughly $130 billion, can ultimately be retained by the federal government.

If repayments are required, the federal deficit could grow even larger.

Meanwhile, geopolitical instability adds another layer of fiscal risk. Military conflicts, including tensions in the Middle East and possible extended operations in the war against Iran, can quickly increase federal defense spending. Wars historically accelerate government borrowing. Combined with rising interest costs on existing debt, these expenditures place additional pressure on federal finances.

At the same time, inflation continues to weigh on Americans. Higher interest rates increase the cost of servicing debt, reducing the financial flexibility of families and businesses alike.

A Sustainable Path Forward

The solution is not simply austerity, nor is it unlimited borrowing. The United States must pursue a balanced approach that combines fiscal restraint with economic growth.

Three steps are essential.

First, Washington must restore spending discipline.

The federal government does not necessarily need to adopt a strict balanced budget amendment tomorrow. However, policymakers should establish credible long-term limits on deficit growth with town hall meetings — a possible useful tool for direct voter input, for all members of Congress and each other. Without fiscal guardrails, spending decisions become increasingly disconnected from economic reality.

Second, the country must prioritize economic growth.

The most effective way to reduce debt relative to GDP is to expand the economy itself. Policies that encourage innovation, entrepreneurship, workforce development, and domestic investment can help generate the productivity gains necessary to grow the tax base without raising tax rates and allowing for sound regulatory reform.

Third, the United States should pursue strategic investment in energy and energy regulatory reform.

Reliable and affordable energy, led by natural gas and nuclear power remains one of the most substantial drivers of economic growth. Expanding domestic energy production can strengthen national security, stabilize prices, and support industrial competitiveness.

Energy development also attracts capital investment, supports manufacturing, and creates high-paying jobs. A strong energy sector therefore plays a direct role in strengthening federal revenues while reducing economic vulnerability to global shocks.

Together, these strategies can help place the country on a more sustainable fiscal trajectory.

The Debt Can Is Becoming Un-kickable

For decades, policymakers have managed the rising federal debt by pushing tough decisions further into the future. But that strategy is becoming increasingly difficult to maintain.

Interest payments on the national debt are rising rapidly. Households are drawing down retirement savings to meet short-term needs. Consumer debt continues to climb as inflation strains family budgets. Underwater trade-ins on new automobiles, light trucks and SUVS hit a record $7,214 in late 2025, with nearly one-third of buyers owing more than their vehicle was worth, according to a recent Automotive News article.

At some point, the can simply cannot be kicked any further down the road.

America’s economic strength has been built on invention, innovation, productivity, and responsible stewardship of resources. Through fiscal discipline, encouraging growth, and investing wisely in strategic industries, the United States can maintain its economic leadership while reducing its debt burden.

The alternative, risks eroding the very economic foundation that made America prosperous in the first place.

The time to confront the debt challenge is not when a crisis leaves you no choice. It is now.

Dr. Timothy G. Nash is director of the Center for the Advancement of Freedom, Free Enterprise and Entrepreneurship at Northwood University. Mr. Bob Thomas is COO of the Michigan Chamber of Commerce. George Lang is an entrepreneur and a member of the Ohio State Senate where he leads the bipartisan Ohio State Business First Caucus. Dr. Tom Rastin is a retired business executive from Ohio.

Tyler Durden

Fri, 03/20/2026 – 08:05

https://www.zerohedge.com/political/debt-can-getting-harder-kick

Israel Vows No More Strikes On Iranian Energy Assets After South Pars Hit Sparks Lasting Shock

Israel Vows No More Strikes On Iranian Energy Assets After South Pars Hit Sparks Lasting Shock

At a Thursday evening press conference, Prime Minister Benjamin Netanyahu attempted to calm energy markets, saying Israel would halt further strikes on energy infrastructure after this week’s attack on Iran’s South Pars gas field triggered Iranian retaliation against Qatar’s Ras Laffan LNG complex. The attacks on upstream oil and gas facilities by both sides sent shockwaves through global energy markets, potentially sparking disruptions for years.

“Israel acted alone,” Netanyahu said at a press conference on Thursday, after Israeli officials previously said they had informed the US about the attack. Netanyahu also said Israeli forces would assist US and allied forces in reopening the paralyzed Strait of Hormuz chokepoint and that the war would be over faster than people think.

“I told him, ‘Don’t do that.’ And he won’t do that,” Trump said Thursday at the White House, referring to Netanyahu’s pledge not to hit Iranian energy assets anymore.

Trump continued, “We get along great. It’s coordinated. But on occasion, he’ll do something, and if I don’t like it, then — so we’re not doing that.”

Shortly after South Pars was hit, Iranian missiles and drones struck the world’s biggest liquefied natural gas plant in Qatar, which will take, according to QatarEnergy, possibly five years and $20 billion to repair. Trump threatened Iran with a complete wipeout of South Pars if Qatar’s energy assets were hit further.

UBS analyst Ed Abraham said the comments from Netanyahu “caused WTI to pull back 7% from Thursday’s highs, along with Brent trading down 3% vs. the close.”

Brent crude futures are still well off the $119/bbl highs seen early Thursday, trading around $110/bbl at 0630 ET. WTI futures traded sub-$100/bbl, currently around $96/bbl.

The Trump administration has taken several steps to combat triple-digit WTI prices, including the release of strategic reserves that must be returned at a later date. This has helped widen the WTI-to-Brent discount to $13 a barrel.

“Price bias for here stays asymmetric, with Brent potentially remaining higher as long as Gulf infrastructure and Hormuz risks are still live,” Saxo Markets analyst Charu Chanana said. “WTI could be choppier and more capped because any spike invites US policy response or direct interventions in the oil markets.”

Beyond Netanyahu trying to calm energy markets by the end of the week, regional tensions are rising, and this week in the three-week conflict, upstream energy assets were targeted on both sides for the first time, which is very concerning.

Goldman analyst Yulia Zhestkova Grigsby provided clients with a full breakdown of the Gulf area energy chaos that unfolded this week:

Attacks on energy facilities in the Middle East continue. Iran’s retaliation following yesterday’s attacks on its South Pars gas field hit several oil facilities, including:

Two Kuwait refineries of 0.8mb/d combined crude processing capacity.

Saudi 0.4mb/d Samref refinery in the Red Sea port of Yanbu (which was also targeted), with Yanbu port briefly halting loadings. UAE Bab oil field, triggering suspension at nearby gas facilities.

We estimate total crude production shut-ins (mostly on precautionary curtailments and storage management) at 9.2mb/d recently (Exhibit 8).

The escalation of the attacks on energy assets implies significant risks for not just near-term oil exports from the region, but longer-term oil production capacity.

For instance, yesterday’s attacks may have cut 17% of Qatar’s LNG capacity for up to 3-5 years, according to QatarEnergy, and threaten gas-dependent oil production in the region.

Our historical analysis of the largest oil supply shocks finds an average hit to production of 42% after 4 years, including from infrastructure damage.

That said, oil prices retreated earlier today after Israel said it will no longer target energy infrastructure.

Policy aims to stabilize tightening oil markets:

The US Treasury confirmed and clarified authorization of Russia oil on water sales, including on “shadow” fleet, through April 11st.

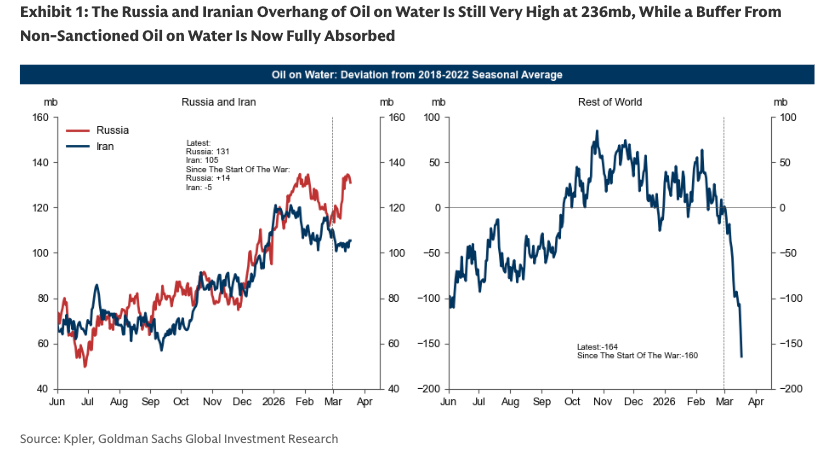

Secretary Bessent also suggested that a similar waver on sanctioned Iranian oil on water is under consideration.

We estimate that the current 131mb of Russian and 105mb of Iranian overhang of oil on water together could eventually offset only about two weeks of Strait of Hormuz disrupted flows (Exhibit 1).

While the US is reportedly not considering a crude export ban, the market remains focused on potential restrictions on US oil flows.

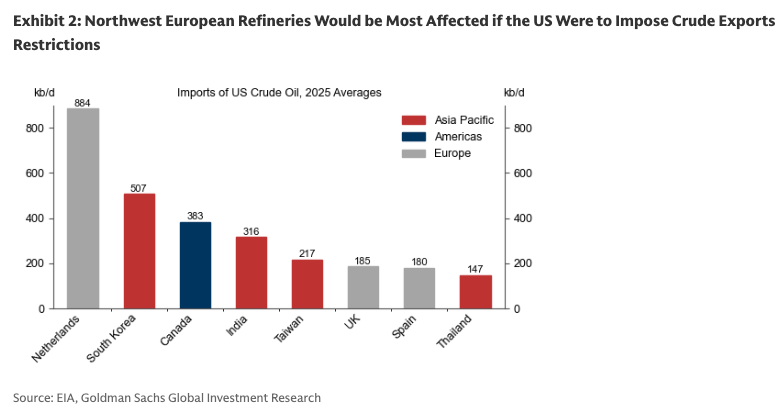

Although not our base case, a hypothetical ban on US oil exports would meaningfully reduce supply of crude in Northwest Europe and South Korea (Exhibit 2) and of diesel and gasoline in Mexico, Northwest Europe, and South Korea (Exhibit 3).

The discount for WTI vs. Brent reached $13/bbl today — the highest level since the removal of the US oil export ban in early 2015.