Category: News

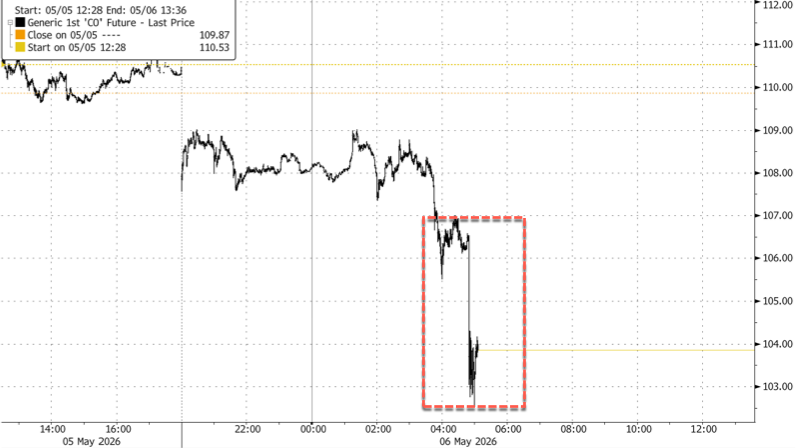

S&P500 Futs Jump, Bonds Rally, Oil Tanks On Axios Report U.S.-Iran Nearing Deal

S&P500 Futs Jump, Bonds Rally, Oil Tanks On Axios Report U.S.-Iran Nearing Deal

Axios reports that the White House is nearing a preliminary deal with Iran to end the war. This is based on a 14-point, one-page memorandum that creates a 30-day negotiating window for a broader nuclear and Strait of Hormuz deal and follows President Trump’s announcement last night of “great progress” and a “complete and final” deal nearing.

“The U.S. expects Iranian responses on several key points in the next 48 hours.

Nothing has been agreed yet, but sources said this was the closest the parties had been to an agreement since the war began,” Axios wrote in the report.

Here are the key points:

Iran would commit to a moratorium on uranium enrichment. The duration is still under negotiation, with the U.S. pushing for 20 years, Iran offering five, and sources suggesting 12 to 15 years may be the likely spot.

Iran would also pledge not to seek nuclear weapons, accept enhanced inspections, potentially halt underground nuclear facility operations, and possibly remove highly enriched uranium from the country.

The U.S. would gradually lift sanctions and release billions of dollars in frozen Iranian funds.

Shipping restrictions through the Hormuz chokepoint and the U.S. naval blockade would be gradually lifted during the 30-day talks. If negotiations fail, U.S. forces could restore the blockade or resume military action.

Axios said talks are being led by Trump envoys Steve Witkoff and Jared Kushner with top Iranian officials, both directly and through mediators.

News of this sparked risk on in U.S. equity index futures, WTI fell to the $95-a-barrel handle, and U.S. Treasury yields dipped.

Market Response:

S&P500 Futs

Brent Futs

WTI Futs

UST10Y

BTC/USD

Polymarket:

US x Iran permanent peace deal by June 30, 2026?

Yes 56% · No 44%

View full market & trade on Polymarket

Strait of Hormuz traffic returns to normal by end of June?

Yes 56% · No 44%

View full market & trade on Polymarket

*Developing…

Tyler Durden

Wed, 05/06/2026 – 05:35

Carbon Neutral, Speech Negative: Amsterdam Bans Ads Featuring Meat & Fossil Fuels

Carbon Neutral, Speech Negative: Amsterdam Bans Ads Featuring Meat & Fossil Fuels

Authored by Jonathan Turley,

In “The Indispensable Right: Free Speech in an Age of Rage,” I write about how censorship often becomes an insatiable appetite once countries go down the road of speech regulation. There is no better example than the Dutch and their recent ban on public ads for meat and fossil fuels. Activists have imposed similar limitations on advertising for products in the United States, from alcohol to tobacco. However, the Dutch law reflects how this tendency can metastasize into shielding citizens from unhealthy choices or influences.

It appears that Dutch painters such as Pieter Aertsen (with his work A Meat Stall with the Holy Family Giving Alms, above) were promoting harmful imagery in their work. As for Rembrandt’s “Slaughtered Ox,” the Dutch master is now little more than a climate change denier.

Starting on May 1, the ban on such images became part of Amsterdam’s push to achieve carbon neutrality by 2050. While purportedly neutral on carbon, it is manifestly negative on free speech.

As with other anti-free speech measures in Europe, this push again came from the left. The GreenLeft Party’s Anneke Veenhoff explained “I mean, if you want to be leading in climate policies and you rent out your walls to exactly the opposite, then what are you doing?”

The answer is engaging in free speech.

This is, of course, commercial speech, which is often subject to a lower level of protection. However, this shows the danger of using the differential standard to target products or industries viewed as unhealthy or ill-advised for consumers.

In Amsterdam, the ban will cover industries such as airlines, including KLM Royal Dutch Airlines, one of the largest employers and revenue generators in the country.

Notably, activists compare this to cigarette advertising bans, confirming the very slippery slope danger that those companies raised when they were targeted.

Hannah Prins, a paralegal at Advocates for the Future, is quoted as saying, “I don’t think it’s normal to see murdered animals on billboards. So I think it’s very good that that’s going to change.”

Other Dutch cities are now following suit, including Haarlem, Utrecht, and Nijmegen.

Of course, prostitutes still advertise live in Amsterdam and marijuana is a major industry for tourists.

If you want drugs, there are ample choices.

However, if you want a steak, you will have to rely on word-of-mouth directions.

Tyler Durden

Wed, 05/06/2026 – 05:00

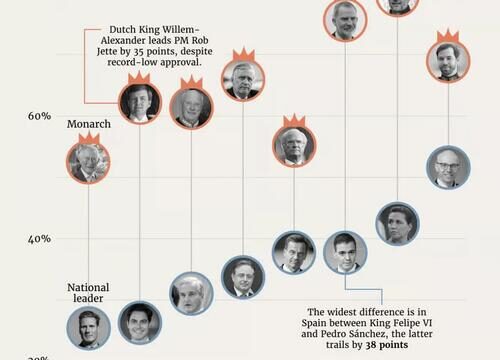

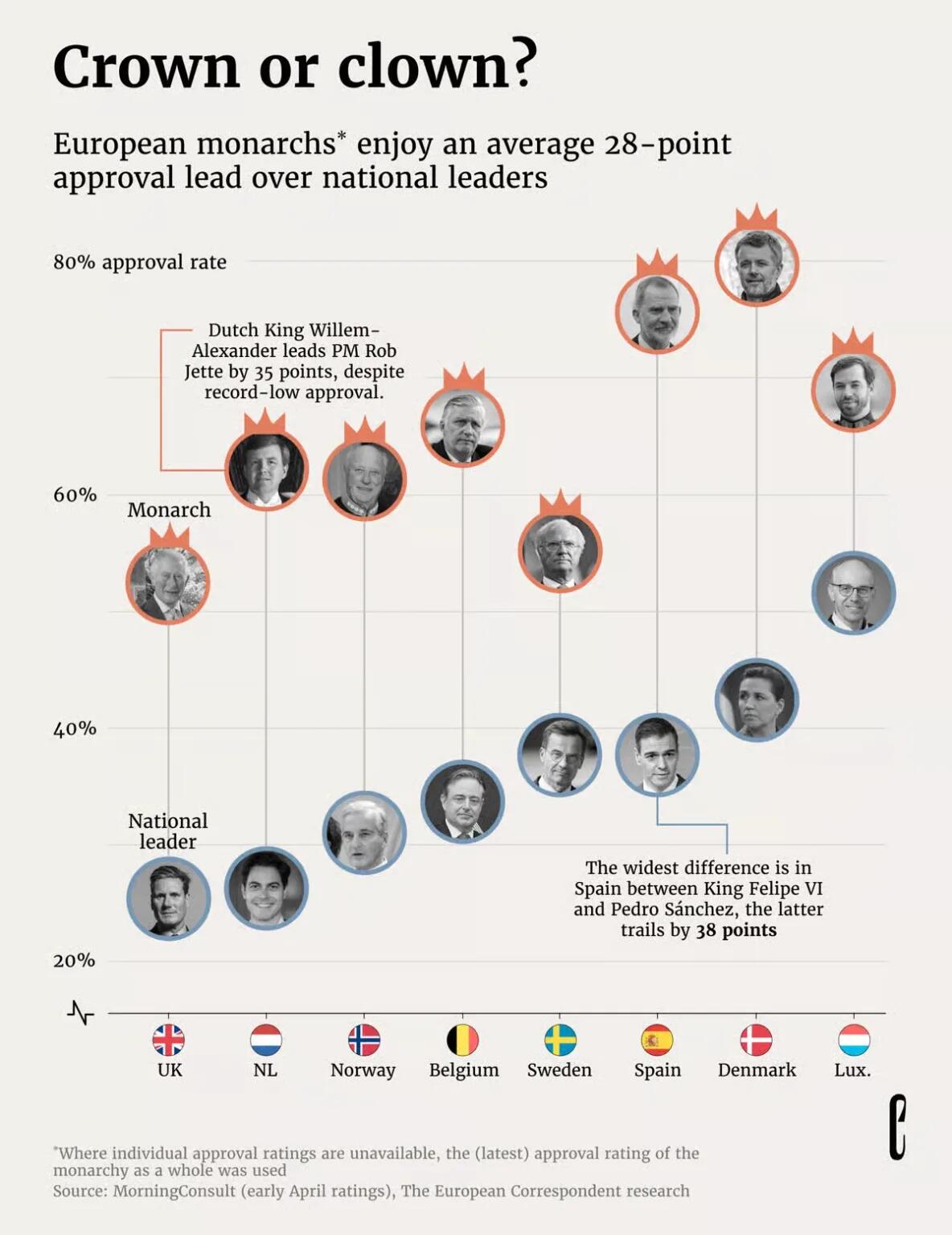

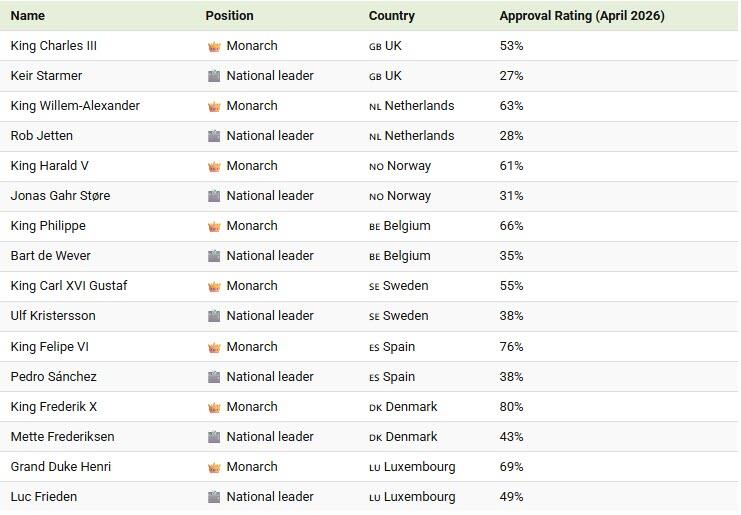

No Kings? In Europe, Monarchs Are Far More Popular Than Politicians

No Kings? In Europe, Monarchs Are Far More Popular Than Politicians

In Europe, monarchs are far more popular than the politicians who govern.

As Visual Capitalist details below, using data from Morning Consult, visualized by The European Correspondent, monarchs hold an approval advantage of nearly 30 points over national leaders. The gap appears in every country analyzed.

The pattern reveals a clear divide: leaders making policy decisions often face public backlash, while ceremonial figures largely avoid it.

Approval Ratings for Elected and Unelected Leaders

Below, we break down approval ratings across eight European countries.

From the UK to Luxembourg, monarchs outperform politicians across the board. Spain stands out with the largest gap, while even the narrowest differences still favor royalty.

Why Do Monarchs Poll Better?

One key explanation lies in the fundamentally different roles these figures play. Monarchs are typically nonpartisan, symbolic heads of state, largely removed from day-to-day political decision-making. This helps them avoid the scrutiny and backlash that elected leaders inevitably face.

By contrast, national leaders are directly responsible for policy decisions on issues like inflation, immigration, and public services. These decisions often divide public opinion, dragging down approval ratings.

Spain and the Netherlands: The Biggest Gaps

Spain has the widest popularity divide, with King Felipe VI outpacing Prime Minister Pedro Sánchez by nearly 40 points. This reflects broader dissatisfaction with political leadership, alongside relatively stable support for the monarchy.

The Netherlands also shows a notable gap, with King Willem-Alexander maintaining a significant lead despite historically low approval ratings for the monarchy itself. This highlights how unpopular political leadership can become by comparison.

Even Lower-Rated Monarchs Still Lead

Even in countries where monarchs have more modest approval ratings, such as the UK, their standing still surpasses that of elected leaders. This underscores a broader trend: monarchy as an institution retains a degree of public goodwill that politicians struggle to match.

As this data shows, in modern Europe, it’s often the figureheads, not the decision-makers, who win the popularity contest.

Tyler Durden

Wed, 05/06/2026 – 04:15

https://www.zerohedge.com/geopolitical/no-kings-europe-monarchs-are-far-more-popular-politicians

UK Faces Summer Flight Disruptions As Jet Fuel Risks Mount

UK Faces Summer Flight Disruptions As Jet Fuel Risks Mount

Ministers are expected to warn Britons that flight cancellations could disrupt summer holiday plans.

Allianz Trade research says the UK is especially exposed to jet fuel shortages because of import dependence.

Airlines are weighing cancellations, surcharges, and ticket price adjustments as fuel supply risks rise.

Ministers are set to warn the British public that flight cancellations will hit summer holiday plans as new research suggested that the UK is more exposed to jet fuel shortages than other European countries.

Heidi Alexander, the transport secretary, is set to tell Brits that there could be flight cancellations this year as she will talk up staycations, according to The Times.

Her warnings will follow a prompt by Sir Keir Starmer that people would have to consider changing “where they go on holiday”.

Trade experts have warned that the supply of kerosene was set to be hit by disruptions across the Strait of Hormuz.

Michael O’Leary, the boss of Ryanair, Europe’s biggest airline, said rivals were “desperately” searching for flights to cancel.

Some airlines have reportedly said that the UK could escape some of the worst effects of jet fuel shortages due to obtaining supplies from other countries.

UK is ‘particularly vulnerable’ to jet fuel shortages

But research by Allianz Trade found the UK had Europe’s “most structurally exposed markets to jet-fuel shortages”.

It said its heavy reliance on imports, albeit from countries outside of the Middle East, would leave the UK “particularly vulnerable” to supply shocks.

“The UK, Germany, France, and Italy show the largest shortfalls, underscoring their reliance on external supply to meet aviation demand,” trade experts said.

“European aviation activity is indirectly exposed not only to global oil price dynamics but also to geopolitical and logistical risks along key supply routes, reinforcing the region’s dependence on external refining hubs for a fuel that is essential to long-haul connectivity.”

The worst effects of flight disruption could come in late June and July, near the peak of summer travel.

Ministers may be looking to discourage Britons from taking long-haul flights in contingency plans being drawn up, according to reports.

Lufthansa Group has announced it will cancel 20,000 flights over the next six months, while Virgin Atlantic added a fuel surcharge and British Airways has warned of “pricing adjustments” to tickets.

Airlines UK, the trade body, said: “UK airlines continue to operate normally and are not experiencing issues with jet fuel supply.”

Tyler Durden

Wed, 05/06/2026 – 03:30

https://www.zerohedge.com/energy/uk-faces-summer-flight-disruptions-jet-fuel-risks-mount

Moscow Targeted By Over 50 Drones, Country’s 2nd Largest Refinery On Fire

Moscow Targeted By Over 50 Drones, Country’s 2nd Largest Refinery On Fire

We’ve been documenting that Ukraine has been demonstrating deeper targeting reach inside Russia, as several key oil sites have come under direct drone attack over several days and weeks, resulting in significant destruction.

Just in the last several days, Russian state media has recorded over 50 Ukrainian drone attacks targeting the country’s capital of Moscow.

Moscow Mayor Sergey Sobyanin on Tuesday confirmed that since the start of this month, Ukrainian efforts to target the capital region have greatly increased.

The distance of Moscow from the Ukrainian border is nearly 300 miles, but lately Ukraine has also demonstrated the ability of its long-range drones to target as far away as Perm and the Ural Mountains.

“The defense ministry’s air defense assets have downed yet another UAV. Emergency relief specialists are working at the scene, where the debris from the UAV landed,” Mayor Sobyanin stated.

And he detailed, per TASS, that “from May 2 to 5, the capital was attacked by 51 drones. In the current 24-hour period, 19 UAVs have been shot down.”

Also, one of Russia’s largest refineries came under fresh attack on Tuesday, with Oil Price reviewing the following:

One of Russia’s largest oil refineries, the 400,000 barrels-per-day Kirishi refinery southeast of St. Petersburg, was on fire early on Tuesday following drone attacks overnight, Bloomberg reports, citing satellite images from NASA.

According to satellite images taken on Tuesday by NASA’s Fire Information for Resource Management System, the Kirishi refinery owned by oil producer Surgutneftegas and nearby areas were detected to emit heating anomalies which signal fires.

Alexander Drozdenko, the governor of the Leningrad region where the refinery is located, posted on Telegram early on Tuesday that the fire at the Kirishi industrial zone has been localized, while the Kirishi refinery was the main target of the drone attacks overnight. The post did not confirm a hit on the refinery, only stating that it was targeted.

Initial footage widely circulating of the overnight attack on Kirishi:

The VNIIR-Progress facility in Cheboksary, Russia, was reportedly hit. It produces secure Kometa navigation modules used in Russian drones, cruise missiles, and ballistic missiles.

The Kirishinefteorgsintez (KINEF) refinery in Kirishi, Russia’s Leningrad region, was also struck.… pic.twitter.com/6Jp31QQCWd

— Anton Gerashchenko (@Gerashchenko_en) May 5, 2026

Currently, the globe’s attention is largely focused on the Iran war and the Hormuz Strait blockade, and with that efforts to reach a political and peace settlement in Ukraine have faded as well. Earlier in the Ukraine war, these major refinery attacks would dominate world headlines, but at the moment they have remained in the background given the constant Iran-related news flow.

President Putin has lately communicated to Trump that he’s open to a ‘Victory Day’ ceasefire, a proposal the Kremlin said Washington has backed. Ukraine is meanwhile offering its own ceasefire, but on a different set of days, and the warring sides haven’t reached agreement.

Tyler Durden

Wed, 05/06/2026 – 02:45

How German Media Became The PR Arm Of The Expanding State

How German Media Became The PR Arm Of The Expanding State

Submitted by Thomas Kolbe

How does economic growth emerge? Let us turn to Ludwig von Mises, one of the defining economists of the 20th century – and paraphrase his idea: growth arises where private capital is guided in a free market by an undistorted price system. Prices signal scarcity and direct scarce resources to where they generate real value. When this system is distorted by ideological intervention, capital is misallocated – potential growth simply evaporates.

That is the theory. And there is no doubt that the reality of emerging economies has repeatedly confirmed the teachings of the Austrian School. Take Argentina, for example: the economic policy shift under President Javier Milei is leading to a rollback of the state and new private investment impulses. That is how it should be: the state as a rule-setting referee, not a player in the economy.

This thesis meets maximum resistance in German editorial offices. There prevails a staunchly statist spirit, a vulgar Hegelianism that regularly loses itself in the labyrinth of economic causality. As a reminder: Milei is the libertarian whom Chancellor Friedrich Merz and German media denounced as a far-right eccentric, accusing him of trampling on his own people. As said: ideologically blinded, intellectually shallow.

On Thursday, Handelsblatt presented its readers with the result of the marriage between green-statist ideology and editorial missionary zeal. In its morning briefing, the author made clear how she interprets the world: at the top, the all-knowing state; far below, the misguided, dependent individual. The piece appeared under the title “When Father State must save German growth” and stands as a case study of the spirit dominating German media. The individual counts for nothing, the state for everything. A hint of Orwell runs through these lines. They are meant to remind us that our economic fate now lies in the hands of an all-knowing federal government. Listening closely, one can still hear the fading odes of the press to former vice chancellor and manager of green chaos Robert Habeck.

Many people find it helpful to embed their existence into the prevailing ideology, thereby relieving themselves of existential responsibility. When this happens on a mass scale, a state within the state emerges – what we call the welfare state. Yet this attitude carries a problem: in journalism it obscures the search for the causes of the current crisis. Editorial work blurs the overregulation of our economy, the destruction of nuclear energy, and clientelist climate policy – together forming the broad delta of deindustrialization.

We are facing a media-historical phenomenon. Magazines such as manager magazin, Handelsblatt, WirtschaftsWoche, and even once-bourgeois papers like FAZ now only vaguely suggest through their names that they were once committed to economic analysis. Condensing tone, imagery, and reporting style, one can hardly escape the impression of a media phalanx of the Green Deal.

The shift in perspective has succeeded. Economic rationality has been replaced by an iron belief in the net-zero cult. For the socialists in editorial offices, a fortunate development – since it is tied to the expansion of a vast state apparatus, conveniently justifying long-term funding of their own activities within the framework of so-called democracy promotion. The state orders – the media deliver: all from a single mold, always in the tone of climate apocalypse.

Manager Magazin confirmed this week the suspicion that even business-oriented outlets operate as a media arm of the green extraction economy. Economics Minister Katherina Reiche, after her cautious criticism of the green subsidy cult, is already depicted on the cover as an oil-soaked fossil-era lobbyist. The rest: a cheer for the energy transition.

The media climax of kneeling before Father State came last year with the presentation of the so-called Draghi Plan. Former Italian prime minister and ECB president Mario Draghi outlined a program intended to lift the eurozone out of stagnation through massive state investment. The plan envisioned around €800 billion annually. Over at least five years, roughly five percent of European GDP would be politically directed. Draghi describes nothing less than a future EU in which economic dynamism is increasingly eroded by state control.

Those who followed media coverage of Draghi’s megalomania rarely encountered dissent. After decades of successful indoctrination – beginning in schools and continuing through universities and media transformed into socialist re-education matrices – this is hardly surprising. Brussels has now largely integrated the plan into the new seven-year budget. Between 2028 and 2034, around €2 trillion will pass through the hands of the Brussels bureaucracy – a remarkable joint success of political elites and their compliant media narrators.

That Draghi, Merz, and von der Leyen are leading us into a new form of socialism under bright daylight is not even up for debate – it is actively reinforced by media work. They pave the ever-widening road into a command economy with rising subsidies and taxes, ultimately resulting in a state quota well above 50 percent – socialism in all but name. The disappearance of market economy is accompanied by massive public-sector expansion: 205,000 new government jobs in just one year – public job creation under state flag.

Meanwhile, the value-creating part of society is bleeding out, while the transformation project coldly smiles at the population. Declining productivity, industrial flight from Germany – a program of impoverishment for the private sector, which was openly mocked by Handelsblatt on Thursday. “Bloodless,” the author called it. Once again, the state must rescue it and pull the chestnuts from the fire – a remarkable worldview given fiscal, regulatory, and energy realities.

You may not notice it – neither at Handelsblatt, manager magazin, Die Zeit, Süddeutsche Zeitung, nor public broadcasting – but their persistent defensive effort, the immunization of the state against criticism, is freezing society in place.

The media form a phalanx shielding government representatives, administration, and the ideological party apparatus from reality. In doing so, they become complicit in enabling the ongoing destruction of the economy. The longer the green transformation unfolds its devastating effects, the more capital and resources are burned – resources needed for rebuilding after the green-statist catastrophe.

Yet nothing happens by chance. Chancellor Merz, like his predecessors Scholz and Merkel, together with the Brussels power cartel, is pursuing a scorched-earth policy. A return to market economy is to be prevented at all costs, despite being the only genuinely democratic and meritocratic form of economic organization. It stands in the way of building green socialism.

Over time, the state apparatus has succeeded in establishing an incentive structure that absorbs people through migration, public employment, or welfare systems into dependency. In such a climate, anyone who raises their voice against the paternal state inevitably stands against the majority – and must expect a storm of outrage.

And as long as Greta Thunberg’s cohorts at Fridays for Future dance in the streets and parts of the population celebrate economic decline as degrowth progress, this children’s party is far from over. A blurred hope remains in the darkest night of the emerging socialism.

* * *

About the author: Thomas Kolbe has worked for over 25 years as a journalist and media producer for clients from various industries and business associations. As a publicist, he focuses on economic processes and observes geopolitical events from the perspective of the capital markets. His publications follow a philosophy that focuses on the individual and their right to self-determination.

Tyler Durden

Wed, 05/06/2026 – 02:00

https://www.zerohedge.com/economics/how-german-media-became-pr-arm-expanding-state

Ramaswamy Wins Ohio GOP Gubernatorial Primary In Landslide

Ramaswamy Wins Ohio GOP Gubernatorial Primary In Landslide

Biotech entrepreneur and former 2024 presidential candidate Vivek Ramaswamy just beat the pants off of political newcomer Casey Putsch (R) by a margin of 82% – 18% (approximately 530,000 votes to 116,000) in the Ohio gubernatorial primary.

The win positions Ramaswamy to face Democrat Amy Acton, the former Ohio health director who led the state’s COVID-19 response and won her party’s nomination unopposed, in the November general election. Acton’s running mate is former Ohio Democratic Party chair David Pepper.

The Republican primary lacked suspense after Ramaswamy, 40, secured early endorsements from President Trump and the state party. Still, the scale of his victory surprised some observers given his relatively recent entry into Ohio politics.

Ramaswamy announced his candidacy in February 2025 after stepping down from his role in the Department of Government Efficiency (DOGE), the Trump administration initiative he co-led with Elon Musk. He has framed his gubernatorial bid as a natural extension of that work – bringing a “startup mindset” to Columbus to make Ohio a national leader in innovation, economic growth, and government efficiency.

His campaign was exceptionally well-funded. Ramaswamy raised more than $25 million from donors and contributed another $25 million of his own money, ending the primary with over $30 million in cash on hand — resources he used for a $10 million television ad blitz in the final weeks. The spending underscored his determination to lock down the nomination early and build momentum for the fall.

Still, the scale of his victory was notable given lingering divisions within the GOP base over one of his signature policy positions: H-1B visas.

Calling the system ‘badly broken,’ Ramaswamy has called for replacing it with a pure merit-based system designed to attract the world’s top STEM and technical talent, insisting this is essential for U.S. competitiveness against China – except he shat on Americans in saying so. In a widely discussed December 2024 post, he attributed American companies’ preference for foreign-born engineers partly to cultural factors, writing that the U.S. has “venerated mediocrity over excellence for way too long” and that immigrant families often prioritize achievement more rigorously than “normal” American households.

Critics, including some Trump supporters and anti-H-1B voices, accused him of wanting to displace American workers and favoring foreign (particularly Indian) talent. His primary opponent Casey Putsch and online influencers amplified claims that Ramaswamy’s companies had previously used the program (filing for 29 H-1B visas historically) while publicly criticizing it. The backlash intensified after Trump’s endorsement, with some MAGA accounts posting comments like “Better work on your H-1B visa.”

His brief tenure at DOGE ended when he resigned to pursue the Ohio governorship, a move some critics viewed as opportunistic but which supporters praised as prioritizing state-level impact. Trump’s enthusiastic endorsement on the night Ramaswamy launched his campaign gave him instant credibility with the GOP base.

Democratic Side and General Election Outlook

Amy Acton, 60, has positioned her campaign around affordability – targeting inflation, gas prices, and housing costs. The fact that she was a lockdown nazi during COVID, however, remains a potential vulnerability in a state that has trended strongly Republican in recent cycles.

Ohio has not elected a Democratic governor in nearly two decades. Yet early polling has suggested the general election could be closer than the state’s partisan lean might indicate, particularly if national headwinds affect Trump-aligned candidates or if Acton successfully mobilizes suburban and independent voters.

The race is already shaping up to be one of the most expensive gubernatorial contests in Ohio history.

Tyler Durden

Tue, 05/05/2026 – 23:53

https://www.zerohedge.com/political/ramaswamy-wins-ohio-gop-gubernatorial-primary-landslide

The Petrogas-Dollar: Symptom Or Strategy?

The Petrogas-Dollar: Symptom Or Strategy?

Authored ‘No1’ via Gold and Geopolitics substack,

Three people sent me Richard Medhurst’s petrogas-dollar piece this week. I read it. Twice even.

There’s a lot in there that I feel is correct.

The chronology of the Levantine Basin deals.

Cheney’s 2001 National Energy Policy.

The roughly $35 billion of Chevron contracts signed across Israel, Syria, Greece, and Cyprus in the past six months.

None of that is in dispute.

The piece is, on the facts, broadly accurate.

What I think though is that the reading of those facts is faulty.

Some history.

In 1944 Bretton Woods pegged the dollar to gold and made it the world’s reserve currency. In 1971 Nixon unpegged it. Three years later, Kissinger negotiated the Saudi arrangement that pegged it to something else – oil. The petrodollar was born. Everyone needed oil, oil was priced in dollars, thus everyone needed dollars.

Medhurst’s thesis is that the same trick is being repeated, with gas as the new anchor.

The Petrogas-Dollar. Same architecture, new commodity.

But gas isn’t oil.

Oil is fungible at planetary scale. One global market, one rough price band with quality differentials. Tankers go anywhere where there’s a port and a refinery. Every country needs it. Every industry uses it. Almost every modality of transport runs on it.

But gas is regional. LNG requires specialised liquefaction terminals on the export side, cryogenic tankers in transit, and regasification infrastructure on the import side. Each piece takes years and billions to build. Pipeline gas is captive to the geography of the pipe. Henry Hub, TTF, and JKM regularly trade at multiples of each other for what is nominally the same molecule. In 2022, European gas hit roughly 25x the US price – that’s the market telling you that there is no single global gas market, just regional ones tethered by expensive bottlenecks.

Anchoring a settlement currency to gas isn’t a step up from oil in my opinion.

It’s a step down.

Less universal demand, less liquid market, more infrastructure dependency, narrower counterparty base. If oil was the commodity that justified the petrodollar’s reach, gas cannot replace it without shrinking the regime it’s supposed to anchor.

Then there’s what’s been happening to the dollar itself. The moment Western powers froze $300 billion of Russian central bank reserves in 2022, every neutral reserve manager on earth received an unscheduled lesson in what “safe” actually meant in practice.

That lesson is still being absorbed, and the absorption is showing up in central bank gold buying at multi-decade highs, parallel payment rails being onboarded, sovereign Treasury holdings declining year over year.

None of it is dramatic. But all of it is compounding.

So the actual picture Medhurst is painting: a fading anchor (oil-and-dollar) being half-replaced by a structurally narrower one (gas-and-dollar), sitting on top of a settlement currency that’s slowly losing the trust required to function as one in the first place.

That’s a regression on two axes at the same time. Not a strategic plan.

The successor isn’t oil-and-dollar. It sure as ain’t a gas-and-dollar. By elimination of every other alternative, it will come back to gold.

Let’s start with Russia.

That’s where his documentary opens.

“The most severe logistical disruption in modern Russian history”. 40% of seaborne export capacity disabled. Production cuts of 300,000 to 400,000 barrels per day in April. (Not an interpretation, those numbers come from OPEC’s monthly report).

The Sirius Report, which tracks vessel movements rather than quotas, has Russian seaborne crude exports flat at 3.5 million barrels per day in April. The Pacific terminals that got hit in the spring strikes are fully recovered by now. The Baltic ports? Kept on loading. Whatever the bombing campaign was supposed to accomplish, it has accidentally functioned as a renovation programme.

The 300-400k figure measures voluntary discipline within the OPEC+ quota framework. It is not a damage assessment. Russia produced slightly less in April because the cartel asked them to, not because there’s a NATO destroyer parked outside Murmansk.

What did happen is that Europe outsourced the demand. They sanctioned Russia. For the 20th time now I guess, because the previous 19 were so successful.

But because even Europe still needs oil, they then turned around and bought the exact same molecules via Indian and Chinese refineries. Who bought it from Russia. At a discount. And mostly in local currencies.

Plus, they sold it at a premium. To Europe. That sanctioned that exact same oil. Great job virtue signaling.

Iran tells a similar story. The piece argues the blockade is starving China of its third-largest oil supplier. TankerTrackers reported on April 24 that Iran exported more oil in the first three weeks of April than in the entire month of March. The blockade has tightened since. WSJ documented loadings dropping in the second half of April, and Project Freedom only formally launched at CENTCOM this morning with 15,000 personnel and over 100 aircraft. The screws are turning, real consequences are landing. (🦗 sidenote: I only hear crickets… 🦗 Still waiting for what news will turn up… 🦗)

But Iran went into this war producing 1.1 million barrels per day at $47 a barrel. Through most of it, production has run around 1.5 million at $110.

I think Trump is pissed right now that he did not receive a “thank you” card yet…

Another argument landed on Saturday – which is after Medhurst’s piece landed. But it doesn’t fit the frame of the article, so I doubt it’ll be added.

US Treasury sanctioned Hengli Petrochemical and four Chinese teapot refineries on Friday over Iranian crude purchases.

Hengli isn’t just a teapot. It’s strategic national infrastructure. 280 billion RMB was invested with a 20 million tons annual refining capacity. It’s one of China’s seven major petrochemical bases. Plus the non-sanctioned parent group is the world’s largest shipbuilder.

Now on Saturday, China’s Ministry of Commerce activated the 2021 Blocking Statute. For the first time ever. Chinese firms and individuals are now legally prohibited from recognizing, implementing, or complying with the US sanctions.

Compliance has been removed as a choice.

“Rock, meet hard place” or something like that?

I doubt this will feature in Medhurst’s 25-year plan any time soon.

To me this looks like a reactive escalation against the Treasury announcement.

And THAT is the recurring shape of this whole thing. Every sanction tightens the parallel system. Every escalation removes another counterparty from the dollar rails. This theory isn’t some 5D strategic genius.

It’s an adaptation. Metabolic. Washington swings at whatever part it wants today… And that system adapts.

Bank of Kunlun was sanctioned by the US Treasury in 2012 for its Iran-related dealings, in what must have seemed like a good idea at the time. The sanctioning was the strategic move. The consequence – as it so often is – was unintended. By cutting Kunlun out of the dollar system, Treasury also cut its remaining dollar exposure to zero, making it the perfect institutional vehicle for yuan-denominated Iran trade.

For thirteen years now, Iranian oil has flowed to Chinese teapot refineries through Kunlun, settled in RMB, entirely outside SWIFT. Iran can’t easily spend the accumulated yuan in dollars, so it likely converts the surplus to physical gold via the Shanghai Gold Exchange.

Iranian oil → yuan → gold. The loop has been running since the year Obama was re-elected. It is now formally protected, on the Chinese side, by a Blocking Statute.

The PBOC has bought gold for seventeen consecutive months. Official reserves are over 74 million troy ounces. The unofficial figure is widely assumed to be substantially higher, given that Chinese domestic mine production since 2000 alone (around 8,150 tonnes) exceeds the entire stated US Treasury holding. China’s US Treasury exposure has fallen from a 2013 peak of $1.32 trillion to $693 billion in February 2026.

Spot is around $4,800 an ounce. Shanghai still trades at consistent premiums to London and COMEX. Chinese banks are rationing 600 kilograms of bullion per bank per day, and every allocation evaporates in under a minute.

While we’re on the subject. The US Treasury carries its own gold holdings on the books at $42.2222 per troy ounce, a statutory price last revised in 1973. Spot is $4,800. The mark-to-market gap is roughly $1.25 trillion. Or said differently: about 3% of its national debt. Or even more differently: if they sell everything, they can run the US government for about a week and a half.

Every $100 that gold rises does add ~$25 billion. I have no idea whether anyone in Treasury has noticed, but I’ve heard a lot of chatter over the years about re-valuating this gold hoard.

The mechanism that I envision instead of a “gas-4-a-dolla’” (not an official US Treasury term… yet) is as I said many times (mainly in comments): internally in a country, the currencies stay fiat. We – the plebs – don’t get to transact in gold and spend 0.03 gram of gold on a gallon of petrol or so. Would be nice, but that’s a pipe-dream in my opinion.

Whatever your local denomination is, be it euro, lira, franc, pound, … Whatever local political pressure or tax laws or domestic monetary systems you have. They’re all localised.

However, cross-border settlement will likely migrate to gold. Not by design. By necessity. By elimination of all worse alternatives.

Every other settlement layer has been politically weaponized over the past six years. The dollar. The euro. SWIFT. CHIPS. Sovereign Treasury holdings. Real estate held in foreign jurisdictions. Central bank reserves. Venezuelan gold seized at the Bank of England in 2019. Russian reserves frozen in 2022. Afghan central bank assets held by the New York Fed since 2021. And Saturday extended the template from sovereign assets to private industrial enterprises.

Gold is the only major asset whose ownership cannot be cancelled by a remote click. It clears bilaterally. It doesn’t care whose face is on the coin. It survives the political weaponisation of every other settlement layer because the weaponisation is the entire reason central banks moved away from it in the first place.

No1 is publishing a roadmap.

There’s no public announcement.

It’s a destination by exclusion – the asset everyone ends up at after the others have been removed.

The petrogas-dollar framing fails on its own terms.

A new monetary regime needs a stable, durable, broadly-accepted anchor. The thesis says the anchor is American gas plus Western Hemisphere oil. The largest LNG producer on earth is already at full export capacity. Henry Hub is at multi-year highs because domestic supply can’t keep up with what’s already been promised. The captured Western Hemisphere reserves require Chevron to actually extract them rather than sign contracts for them. The Levantine Basin gas fields are still in the ground, five months after the deals were inked.

A monetary regime also needs counterparties willing to use it. The petrogas-dollar thesis describes a world where Europe and Asia have no choice but to buy American. In the actual world, the UAE quit OPEC effective May 1 after threatening yuan-denominated oil sales. Saudi Arabia gave 12 million of its citizens access to China’s CIPS payment network the day after that. Iran’s parliament codified yuan and Tether settlement at Hormuz – they’re still deciding on Tether after it got frozen (link). China activated the Blocking Statute on Saturday.

The monetary system is moving.

But it’s not moving to Washington.

The third variable is Trump. The thesis requires you to believe that the same administration that fired its own Navy Secretary three weeks ago for not building ships fast enough is, simultaneously, executing a coherent 25-year plan to reorganize global energy markets and replace fifty years of monetary architecture. Trump and 25-year strategic patience are two phrases that have, to my knowledge, never previously occupied the same sentence before.

Don’t get me wrong. The petrodollar won’t be dying tomorrow.

The US still has the world’s deepest capital markets, the most-traded currency, and the only Treasury market with anywhere near the absorption capacity to hold global savings. Reserve currency status takes decades to erode. The Bank of England held that status for over a century before the dollar took it, and at no point during the slide did anyone in London publish a piece announcing the handover.

Medhurst is right that there’s a transformation under way.

But I strongly believe that he has the direction wrong.

All this chaos ain’t producing a stronger empire.

It’s producing a more fragmented monetary architecture, and gold is starting to fill the gaps the dollar used to fill.

Tyler Durden

Tue, 05/05/2026 – 23:25

https://www.zerohedge.com/geopolitical/petrogas-dollar-symptom-or-strategy

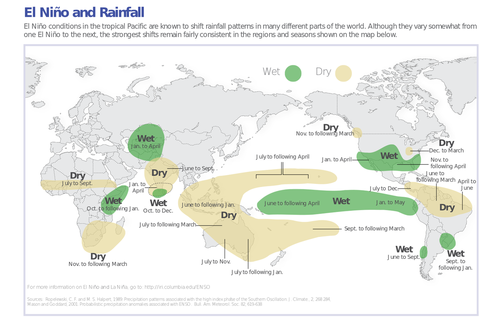

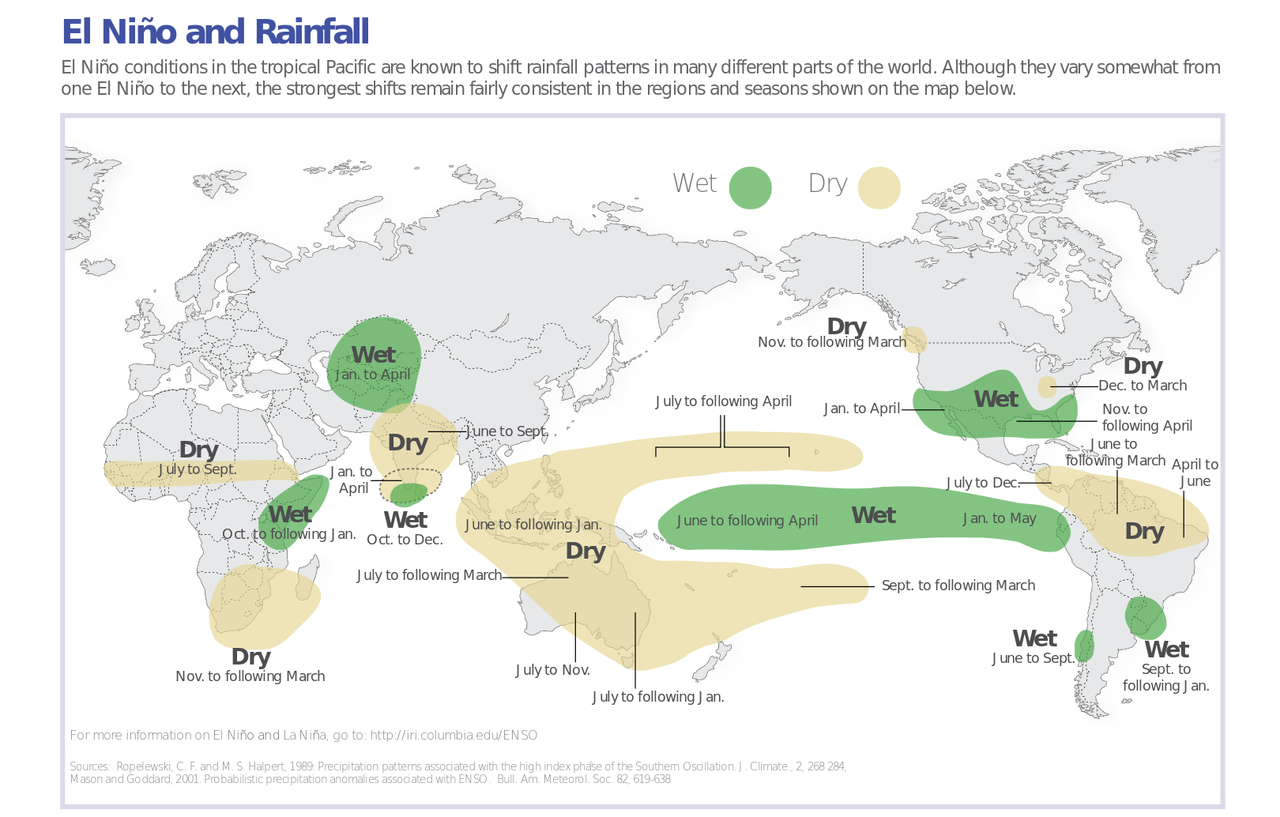

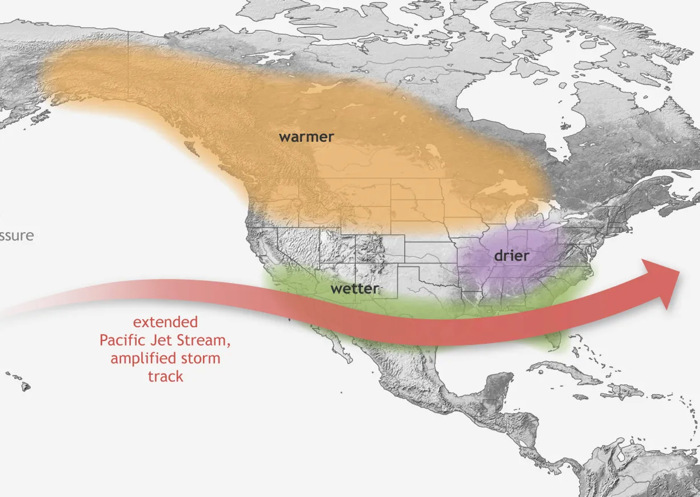

Meteorologists Sound Alarm Over El Nino Plume Racing Across Pacific Like “Freight Train”

Meteorologists Sound Alarm Over El Nino Plume Racing Across Pacific Like “Freight Train”

Meteorologists on X are once again warning about a powerful El Niño, pointing to a new plume of warm subsurface water moving across the Pacific “like a freight train.” The latest water temperature data suggest that El Niño later this year could rank among the strongest on record, with potentially significant implications for the Lower 48.

“Updated El Niño forecast for this summer/autumn is ‘off the charts’ EXTREME with ‘boiling red’ map colors along Equatorial central and eastern Pacific Ocean,” meteorologist Ryan Maue wrote on X. He said this is “code red the Earth’s climate system going into Summer 2026,” which only means “suppressed Atlantic hurricane activity.”

Updated El Niño forecast for this summer/autumn is “off the charts” EXTREME with “boiling red 🔴” map colors along Equatorial central and eastern Pacific Ocean.

This is “Code Red” for the Earth’s climate system going into Summer 2026 –> suppressed Atlantic hurricane activity. pic.twitter.com/NSCJPak6Xt

— Ryan Maue (@RyanWeather) May 5, 2026

Meteorologist Ben Noll said, “A brand new El Niño plume from ECMWF reaches +3˚C in most scenarios by November, which would put this event among the strongest on record.”

Breaking: Brand new El Niño plume from ECMWF reaches +3˚C in most scenarios by November, which would put this event near the strongest on record. pic.twitter.com/m2OOTeXcx8

— Ben Noll (@BenNollWeather) May 5, 2026

Noll continued, “A freight train of warm water continues to chug across the subsurface Pacific Ocean.”

Super El Niño: A freight train of warm water continues to chug across the subsurface Pacific Ocean.

The level of warmth is record-breaking in some areas, peaking around 7˚C (13˚F) above average.

This heat should lead to more intense El Niño projections in May model updates. pic.twitter.com/Y3YKFbgMA7

— Ben Noll (@BenNollWeather) May 4, 2026

If a super El Niño materializes, it could shift weather patterns worldwide, increasing the risk of flooding in some regions, drought and wildfires in others, and further raising global temperatures. An El Niño event typically strengthens the Pacific jet stream and redistributes heat and moisture globally.

Across the U.S., an El Niño influences seasonal rainfall, especially during winter. The stronger, more active jet stream typically shifts southward, bringing wetter-than-average conditions to the southern U.S., including California, the Gulf Coast, and the Mid-South.

The good news is that El Niño reduces Atlantic hurricane activity.

Tyler Durden

Tue, 05/05/2026 – 23:00

Industry Leaders Warn Chinese EV Imports Will Undercut Canada’s Auto Sector, Bring Major Security Risks

Industry Leaders Warn Chinese EV Imports Will Undercut Canada’s Auto Sector, Bring Major Security Risks

Authored by Paul Rowan Brian via The Epoch Times (emphasis ours),

A number of industry leaders and policy experts are warning that the government’s permission of importing Chinese-made electric vehicles (EVs) into Canada at low tariff rates will undermine Canada’s auto sector and cause a number of substantial national security risks.

The warnings came in testimony before the House Committee on Industry and Technology, where the speakers said that Ottawa’s quota-based access to Chinese EV makers will make Canada vulnerable to unfair trade practices from Beijing, hollow out the country’s already-struggling auto industry, and bring along a host of security risks associated with data collection and surveillance.

“Let’s be clear, this is not the approach Canada wanted,” Michael Kovrig, head of the Global Network for Strategic Effects, said while testifying May 4 before the committee.

EV Deal

The import of Chinese-made EVs comes under the terms of an agreement between Ottawa and Beijing signed in January of this year that allows the import of up to 49,000 Chinese-made EVs in the first year at a tariff rate of 6.1 percent, down from 100 percent.

Ottawa has indicated the quota could rise to approximately 70,000 vehicles per year over the next five years.

As part of the agreement, Beijing moved to cut tariffs on Canadian agricultural exports, slashing tariffs from 84–100 percent on Canadian canola products to 15 percent and relaxing restrictions on other products including seafood and peas.

Ottawa also said it expects China will invest in the Canadian auto sector and possibly set up auto manufacturing inside Canada as part of the wider agreement.

Canada opened permits for Chinese-made EVs on March 1, under which 24,500 will be allowed until August under the 6.1 percent tariff rate. Permits are issued by Global Affairs Canada and last 60 days before expiry. Importers are required to be Canada-based automakers or agents of them, and vehicles must comply with Canadian safety standards.

Ottawa said it plans to review and potentially change how the import system works after the first six months.

‘Trifecta of Risks’

Kovrig said that allowing Chinese-made EVs into Canada causes a “trifecta of risks,” which he described as creating “structural dependence” on China, along with “unfair competition [that] erodes industrial capacity” and imposing a “systemic pressure” on government policy going forward.

“The real question is not, ‘don’t we want cheaper EVs?’” Kovrig said. “It’s whether Canada wants to be a producer in the future auto economy, or merely a consumer market for vehicles produced by China’s industrial system.”

Kovrig’s concerns were echoed by Brian Kingston, president and CEO of the Canadian Vehicle Manufacturers’ Association.

“There are no guardrails in this agreement to ensure a level-playing field for manufacturers that have invested in Canada, or to protect Canadians from cybersecurity risks,” Kingston told MPs.

Kingston added that demand for EVs is closely tied to government incentives rather than free-market forces, and that serious harm could be done to the North American auto supply chain.

“Demand for EVs is directly related to rebates, and we saw it when the previous federal government rebate went away, we saw demand for EVs decline quite significantly,” he said, adding that import of Chinese-made EVs “will undermine the auto sector and presents risks to the North American auto supply chain.”

Canada’s auto sector remains a major part of the economy and directly employs roughly 125,000 workers, the majority of whom are employed in Ontario. More than 90 percent of Canadian-made vehicles are exported to the United States.

Kingston also said that keeping access to the U.S. market is crucial for Canada and “there is no industry without U.S. access,” saying that opening up to Chinese imports could undermine North American integration.

In mid-January, U.S. Trade Representative Jamieson Greer said Canada’s deal with China was “problematic.” This was followed on Jan. 24 by U.S. President Donald Trump threatening to put 100 percent tariffs on Canadian goods in response to the deal.

Controls

Several Liberal MPs on the committee asked questions about the economic and security issues related to importing Chinese-made EVs, stating that it could help Canadian consumers access more affordable vehicles and move Canada closer to climate goals.

For her part, Liberal MP Lisa Hepfner asked whether Canada could put conditions on Chinese firms, such as on domestic labour, security, and standards, in order for them to be allowed to import the vehicles.

Kingston said such an approach won’t work.

“If you say that you have to have a local supply chain and use local unionized labour, the response from a Chinese OEM [Original Equipment Manufacturer] is, ’thanks, but no thanks,’” he said.

“The moment they want more access, they will restrict our exports of canola. They’ll come up with other reasons to leverage more access into the market. This is the Chinese trade playbook. You can see it in sector after sector in different countries,” he added.

Kovrig shared this view, saying that Beijing tends to use a quota as a “ratchet” to force more market access.

“What begins as a capped quota becomes a ratchet that only expands. Concentrated sectoral economic dependence also constricts federal policy-making autonomy,” he said.

“The PRC [People’s Republic of China] weaponizes technology, supply chains, and market access to coerce independence to its geopolitical agenda.”

He added that “forced labour” is also part of the Chinese EV supply chain and cited evidence from Sheffield Hallam University linking forced labour of China’s ethnic Uyghur population to key battery and EV production stages.

Kingston added that even if China were to build a factory in Canada, it would likely be a human rights and economic disaster.

“If they build a plant, they bring in labour from China. And as we’ve seen in Hungary, the conditions have been characterized as slave-like conditions,” he said, referring to a Chinese-operated factory in Hungary.

Benefits of EVs

Several industry leaders who testified before the committee said EVs would be a net positive for Canada.

Jeff Turner, director of Mobility at Dunsky Energy and Climate Advisors, said EVs would help Canadians in various ways, including by bringing “almost $2,000 per year in fuel savings per household and reductions of GHG emissions and other emissions that have significant health impacts for Canadians.”

Cherith Sinasac of the Electro-Canada Foundation also emphasized her view of the positive role that EVs could have and said their origin is much less important than infrastructure readiness.

“Canada needs a strong long-term EV charging infrastructure strategy,” she said, adding that there must be a coordinated investment strategy by provinces and economic sectors.

“EVs and their battery storage have the potential to be a national energy asset for our grid,” Sinasac said.

Security Risks

Kingston and Kovrig both said that in addition to economic damage, bringing in Chinese-made EVs could pose security risks, including potential data access concerns and dangers to national security.

“China’s 2017 National Intelligence law compels any Chinese firm, including from overseas operations, to share data with Beijing on demand,” Kovrig said. “There’s no judicial review and no challenge mechanism.”

Kovrig described Chinese-made EVs as “a rolling computer with cameras” that are “state-linked data platforms.”

This echoed similar concerns from Conservative Leader Pierre Poilievre, who stated his opposition to allowing Chinese-made EVs into Canada this past January, writing on X that such vehicles “function like roving surveillance systems on our streets [and] should not be allowed in Canada – collecting data, tracking Canadians and exposing us to a foreign regime.”

Tyler Durden

Tue, 05/05/2026 – 22:35

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}