Category: News

Futures At New Record High On Tech, Tehran, Trade, Taiwan And Tariffs

Futures At New Record High On Tech, Tehran, Trade, Taiwan And Tariffs

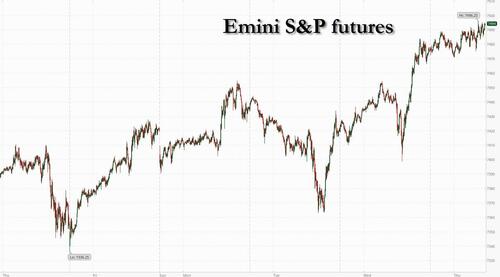

US futures are higher as we await color on the Trump-Xi summit and US- Iran negotiations, which are said to be ongoing, and as the tech meltup continues. What is known so far is that Trump / Xi agree that Iran cannot have a nuclear weapon, Hormuz should reopen without a toll or militarization; the countries will look to increase investment in each other as NVDA H20 chips are approved for a set of Chinese companies. In short, markets are higher on what BBG calls the 4 Ts: Tehran, Trade, Taiwan and Tariffs, to which we can also add Tech. As of 8:00am ET, S&P futures are up 0.3% while Nasdaq futures rise 0.2%. In pre-market trading, Cisco soared 16% after the company reported results that beat expectations and raised its full-year forecast as it laid off thousands to fund capex. Mag7 stocks are higher led by NVDA again; semis are mostly lower despite KOSPI adding 1.7%, while Cyclicals are seeing a bid. Cyclicals, esp Consumer Disc and Fins, would be among the biggest beneficiaries of a reopening of SoH (oil down, yield curve bull steepens, lower inflation expectations). Bond yields are flat to down 1bp, the USD is flat, and commodities are mostly lower. Energy commodities are still rallying but Metals are weaker dragged by the PGMs as Ags come for sale. Today’s macro data focus is on Retail Sales and Jobless Data.

In premarket trading, Magnificent Seven are mostly higher: Nvidia (NVDA) is up 1.5% as the semiconductor giant’s CEO Jensen Huang joined President Donald Trump on his visit to China. Huang told reporters in Beijing that “the meetings went excellent.” (Tesla +1%, Apple +0.4%, Microsoft +0.2%, Meta Platforms +0.1%, Amazon -0.1%, Alphabet -0.2%)

Canada Goose (GOOS) rises 5% after the parka and other apparel maker reported revenue for the fourth quarter that easily beat even the most bullish analyst projection. The stock is down 18% YTD through Wednesday’s close.

Cisco Systems (CSCO) soars 15% after the networking-equipment company delivered a better-than-anticipated sales forecast and announced plans to cut thousands of jobs, an attempt to focus on the fast-growing AI market.

Doximity (DOCS) tumbles 23% after the healthcare software firm gave a full-year forecast that was weaker than expected, with AI investments pressuring the company’s earnings.

EquipmentShare (EQPT) gains 4% after the equipment-rental company reported revenue for the first-quarter that beat the average analyst estimate.

Precigen (PGEN) jumps 17% after the drugmaker reported product revenue for the first quarter that topped the average analyst estimate.

Staar Surgical (STAA) climbs 21% after the healthcare supplies firm reported earnings per share for the first quarter that beat Wall Street analysts’ estimates.

Stubhub (STUB) is up 14% after the ticketing company reported better-than-expected first quarter results and reiterated its annual forecast. Morgan Stanley analyst notes that gross merchandise sales and revenue should improve in the second half of the year.

Viking Holdings (VIK) rises 2% after the cruise line operator posted first quarter revenue that climbed about 17% from the year-ago period.

In corporate news, Cerebras Systems raised $5.55 billion in its US IPO, as the AI chipmaker seizes on the surging demand for semis. The deal, said to be 20x oversubscribed, priced at $185 per share, above an increased, upsized range. It follows Wednesday’s report about Arm and majority owner SoftBank making an approach to acquire Cerebras weeks before the IPO. In other corporate news, Lululemon’s incoming CEO gave her first speech to employees this week, pledging to put the athleisure brand back on track. QVR Advisors is closing its volatility-focused multistrategy hedge fund and looking to sell the management company, following months of losses and investor redemptions.

With the Trump-Xi talks underway, markets may expect a focus on the “four T’s” — Tehran, Trade, Taiwan and Tariffs — with scope for constructive headlines across all four topics. Of course, Tech remains the biggest upside driver of all: Cisco Systems soars in premarket after raising its full-year forecast. Cisco delivered a better-than-anticipated sales outlook and announced plans to cut thousands of jobs to focus on the fast-growing AI market. Analysts highlight the company’s accelerating growth rate. Elsewhere in AI, Alphabet’s bond fundraising continues at pace: the latest sale over four months is for quadruple the amount of bonds Alphabet had sold in its first 26 years in business.

“Ingredients for the big top in markets are still missing, namely multiple Fed hikes, wider credit spreads or an overheating growth pulse,” said Manish Kabra, chief US equity strategist at Societe Generale. “The bull case for the S&P 500 stays intact.”

Trump’s summit with Xi Jinping shifted the spotlight from the war in Iran that has left a key conduit for Middle East oil flows all but closed for more than two months. The Chinese leader signaled that Beijing is moving toward greater openness as traders look out for business deals and purchasing commitments from the world’s second-biggest economy.

“I would expect the summit to matter more for sentiment than for a grand policy reset,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg. “The market is likely looking for a de-escalation tone, fewer tariff threats, and no new restrictions on trade, technology, or geopolitics.”

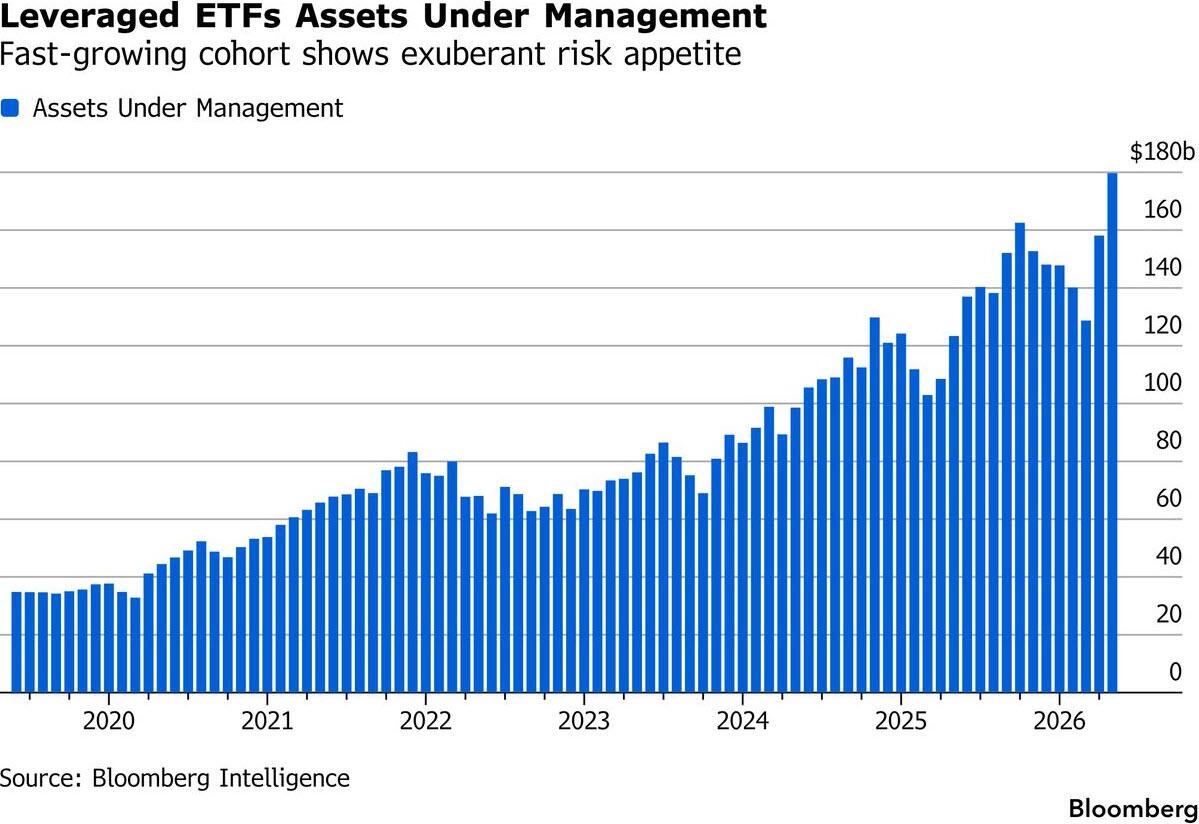

Meanwhile, excessive risk-taking, particularly from the retail crowd, is showing no sign of abating as leveraged ETF assets under management hit a record $180 billion, with growing impact on underlying assets.

In Europe, the Stoxx 600 rose 0.4% as local markets rose for a second day, led by technology shares that were boosted by better-than-expected results from Cisco Systems in the US. Trading volumes were lighter than usual, with markets in Denmark, Finland, Norway, Sweden and Switzerland closed for a holiday. to 614.14 with 164 members down, 407 up, and 29 little changed. Here are some of the biggest movers on Thursday:

Legal & General shares rise as much as 5.2% as the Financial Times reports speculation over whether the financial services firm could be sold or broken up.

Watches of Switzerland shares rise as much as 14%, hitting the highest since early 2024, after the watch retailer said annual adjusted Ebit will be ahead of its previous guidance. Analysts said the confident outlook for the year ahead should also push up consensus. Barclays hiked its price target on the stock to a new Street-high.

Premier Foods shares rise as much as 6.2% after the food company reported profits slightly ahead of expectations and hiked its dividend. Analysts flagged that sales growth improved through the year and that the balance sheet is stronger.

3i Group shares fall as much as 25%, the steepest drop since January 2009, after the private equity group flagged slowing sales growth at its discount retailer Action. RBC analysts said the retailer, 3i’s largest single investment, has left itself much to do in the second half to meet its guidance.

CIE Automotive shares slip as much as 7% after Mahindra Overseas Investment Co. Mauritius sold its stake in the Spanish auto parts firm at €29.37 per share, a 6% discount to the last closing price.

Shurgard shares drop as much as 5.9% after the self-storage company reported a weak set of results, according to analysts. Pricing pressure in the UK was flagged as a key headwind. Guidance was maintained, although Stifel said factors outside its control could weigh on expectations later this year.

Earlier in the session, Asian stocks edged higher as investors poured into the region’s top chipmakers while keeping watch on talks between US President Donald Trump and Chinese counterpart Xi Jinping. The MSCI Asia Pacific Index rose 0.2%, boosted by Samsung, Alibaba and TSMC. Shares advanced in South Korea and Taiwan, while benchmarks in mainland China fell amid the ongoing US-China summit. In their meeting Thursday, Trump said China and the US will have a “fantastic future,” while Xi stressed stability in trade between the world’s top economies. The leaders had discussed expanding market access for US businesses and China’s potential interest in purchasing more US energy and agriculture, among other things.

In rates, treasuries slightly richer across the curve, supported by steady oil prices and marginally bigger gains for bunds and gilts. S&P 500 futures also hold small gains, led by technology stocks. US session includes April retail sales data and several Fed speakers. US 2- to 10-year yields are 1bp-2bp lower on the day, slightly outperforming long-end tenors; 10-year near 4.455% trails German and UK counterparts by about 2bp. IG dollar issuance slate empty so far, with weekly volume $48 billion vs $50 billion predicted. Six names priced $14 billion Wednesday, with issuers paying about 2.7 basis points in new issue concessions on deals that were 3.4 times covered

In FX, Bloomberg’s Dollar Spot Index steadied after three days of gains, while 30-year Treasury yields held above 5%. USD/CNY and USD/CNH fell to the lowest levels since February 2023; Xi Jinping signaled China is moving toward greater openness during his meeting with US business leaders. GBP/USD steadied around 1.3518; Keir Starmer’s efforts to hold back a potential leadership challenge showed new cracks

In rates, treasuries advance, pushing US 10-year yields down 1 bp to 4.46%. European government bonds outperform with UK and German 10-year borrowing costs falling 3 bps each.

In commodities, oil prices are steady with WTI crude near $101/barrel and Brent crude futures near $106 a barrel. Precious metals are mixed.

Economic data slate includes April retail sales and import/export prices and weekly jobless claims (8:30am) and March business inventories (10am). Fed speaker slate includes Miran (8am), Schmid (10:15am), Hammack and Bowman (1pm), Williams (5:45pm) and Barr (7pm)

Market Snapshot

S&P 500 mini +0.2%

Nasdaq 100 mini +0.2%

Russell 2000 mini little changed

Stoxx Europe 600 +0.5%

DAX +1.3%

CAC 40 +0.6%

10-year Treasury yield -1 basis point at 4.46%

VIX little changed at 17.84

Bloomberg Dollar Index little changed at 1193.97

euro little changed at $1.171

WTI crude +0.8% at $101.78/barrel

Top Overnight News

Xi Jinping has told American chief executives travelling with Donald Trump that China’s door to business “will only open wider and wider” as the leaders of the world’s two biggest economies meet in Beijing. FT

Beijing granted permission on Thursday for hundreds of American slaughterhouses to resume beef shipments to China, 15 months after Chinese officials had signaled displeasure with President Trump’s initial tariffs by allowing the industrial facilities’ licenses to expire. WSJ

Scott Bessent said he had no news on additional access for Nvidia chips in China, but said there may be a large Boeing order. BBG

Chinese leader Xi Jinping warned President Trump that any mishandling of Taiwan could lead to “an extremely dangerous situation,” directly raising a point of tension that has loomed over the meeting. Xi’s statement, while in line with China’s longstanding position, threatened to dim the mood of a visit both countries hoped would stabilize ties.

The BoJ should raise interest rates as soon as possible if there are no clear signs of an economic slowdown, board member Kazuyuki Masu said in comments that appear to increase the chances of a June rate hike. RTRS

Data centers in space are gaining traction as an idea to get around constraints limiting expansion on Earth. SpaceX and Blue Origin have both announced plans to build and launch. BBG

Russia pummelled cities across Ukraine with dozens of missiles and more than 1,400 drones on Wednesday into Thursday, as a three-day ceasefire collapsed in a relentless 24-hour bombardment, which killed at least a dozen people. FT

US President Trump’s proposals are reportedly facing opposition in Congress. These include a gas tax holiday and federal funding for a new ballroom in the White House: Semafor

US Pentagon has not signed new contracts to replenish its munitions supplies: NBC

London office leasing bounced back from Covid-era lows, with tenant floor-space expansions reaching a six-year high on rising demand from finance and professional services firms. BBG

India is considering a significant reduction in taxes paid by foreign investors on the nation’s bonds as authorities seek to align policies with global norms and attract inflows, people familiar said. BBG

Trump-Xi Summit

In the White House official statement, it stated that US President Trump had a good meeting with Chinese President Xi, in which the two sides discussed ways to enhance economic cooperation. On the Iran conflict, the two sides agreed that the Strait must remain open and that Iran can never have a nuclear weapon. However, Taiwan was not mentioned.

US President Trump told Chinese President Xi that they’ve had a fantastic relationship, and they are going to have a fantastic future together, while he added that he has such respect for China and that he tells everybody Xi is a great leader. Trump also stated that the relationship between the US and China will be better than before, with trade to be totally reciprocal on their behalf and he looks forward to doing business with China.

Chinese President Xi said to US CEOs that China’s door will only open wider, adds China welcomes US to strengthen reciprocal cooperation in China, according to Xinhua.

Chinese President Xi told US President Trump it is a pleasure to meet him in Beijing, while he has always believed that the common interests between China and the US outweigh the differences. Xi stated that the success of China and the US is an opportunity for each other, and he looks forward to discussions with US President Trump.

Chinese President Xi said talks are the only right way to resolve disputes and that there are no winners in a trade war, while he also commented that the Taiwan issue is the most important in US-China ties, and if the issue is not handled well, the two countries will clash, according to Xinhua.

China People’s Republic Chair Qiang said the US and China should focus on cooperation, and continue to be friends.

Iran War news

US President Trump’s team is now discussing options for military escalation to break the deadlock, Axios reported. US officials don’t expect Trump to take any dramatic steps during his trip but think he could make his next move immediately afterward. One option is to resume “Project Freedom,” while another is to launch a new bombing campaign focusing on Iranian infrastructure.

Pakistan Foreign Ministry said the peace process is intact, its holding on, we remain engaged and hopeful, Journalist Mallick reported.

Iranian Foreign Minister Araghchi said although Iranian forces are ready to “deliver a crushing and devastating response to foreign aggressors, we do not seek war.”

US Secretary of State Rubio said US hopes to convince China to play a more active role in persuading Iran to back down on its actions in the Gulf, according to Reuters.

US intelligence report emphasised that China acted to maximise its advantage and achievements against the US following the war in Iran on the diplomatic, military, economic and intelligence levels, according to WaPo.

UKMTO reports an incident 38NM northeast of Fujairah, UAE. The vessel has been taken by unauthorised personnel whilst at anchor and now bound for Iranian territorial waters.

Israel is to inform the Lebanese delegation that its strategy that it will not be committing to a comprehensive ceasefire, Al Hadath reported citing sources. Israel may offer to avoid bombing northern Bekaa and Beirut

Iraqi sources reported hearing the sound of several explosions in Erbil, Iraq, while a drone strike hit an Iranian opposition camp north of Iraq’s Erbil, according to Fars. It was also reported shortly after that a second drone strike hit an Iranian opposition camp north of Erbil, according to security sources.

Israeli raid was reported on the town of Arnoun in the district of Nabatieh in southern Lebanon, while Hezbollah said it targeted a Merkava tank with a guided missile in Tel Nahas on the outskirts of the town of Kafr Kila and achieved a confirmed hit, according to Al Jazeera. It was also reported that Hezbollah conducted 17 operations against Israeli forces on Wednesday.

Israeli PM Netanyahu reportedly made a secret visit to the UAE in the midst of the Iran operation, where he met with UAE President Mohamed bin Zayed Al Nahyan, while the visit resulted in a historic breakthrough in relations between Israel and the UAE. However, the UAE later denied the report of a visit.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following the mostly positive lead from Wall St, where markets were choppy and gradually brushed aside the firmer-than-expected PPI data amid strength in tech and communications, while the focus turns to the Trump-Xi summit, which has begun in Beijing, although it has provided very little so far to excite markets. ASX 200 was lacklustre as weakness in consumer staples, tech, health care and energy counterbalanced the resilience in the top-weighted financials sector, while a lack of tier-1 data added to the humdrum mood. Nikkei 225 initially climbed to a fresh record high, before fading the gains amid quiet catalysts. Hang Seng and Shanghai Comp were mixed as participants digested earnings releases, including from the likes of Alibaba and Tencent, which both beat on the bottom line but disappointed on sales, while participants now await any concrete outcomes from the Trump-Xi summit.

Top Asian News

Japan considers drafting an extra budget, according to Kyodo. However, Japanese Chief Cabinet Secretary Kihara said no immediate need for a supplementary budget.

A broadly positive start for European bourses (STOXX 600 +0.5%) to begin Thursday’s session. The DAX 40 (+1.4%) is the clear outperformer, supported by Infineon and Rheinmetall while the FTSE 100 (+0.2%) underperforms, as 3i Group slumps after its FY total return missed estimates. European sectors hold a positive bias. Tech tops the sector pile while Financial Services lies at the bottom. Newsflow surrounding European tech has been light, but gains in US-listed Cisco after-hours seem to have passed through to the broader tech area. A Reuters report suggesting that the US approved H200 chip sales to Chinese companies also helped to lift sentiment.

Top European News

Former UK Deputy PM Rayner is prepared to put her herself forward in any leadership race if required, Sky News’ Rigby reported citing sources.

Former UK Deputy PM Rayner said she’s been cleared of any tax wrongdoing by HMRC.

Afzal Khan told Sky News he has no plans to give up his seat for Manchester Mayor Burnham. This is a denial of earlier reports.

Leadership candidates are considering making an early statement that Chancellor Reeves would actually be retained as Chancellor to secure market stability in the event of a longer leadership contest, according to Mail on Sunday’s Hodges citing UK MPs.

BoE is set to water down stablecoin rules after industry pressure, with Deputy Governor Breeden stating that initial plans may have been ‘overly conservative’ and the central bank is ‘looking very hard’ at alternatives, according to FT.

British Chambers of Commerce warned UK manufacturers and construction groups will be hit by significant financial and logistical problems as a result of ministers’ plans to double tariffs on steel imports from July 1st, according to FT.

FX

DXY continues higher into of a packed session of US data and Fed speak. Today’s focus, aside from the scheduled data/speakers, will be on the US/China summit, where we recently saw a positive US readout with no mention of Taiwan and agreement that the Strait of Hormuz must remain open. So far, the Buck has yet to move significantly to the aforementioned updates and resides within narrow 98.41-98.55 parameters.

In terms of notable news overnight, the US Senate confirmed Kevin Warsh to Fed Chair – to remind, Powell’s term officially terminates tomorrow. In terms of some analyst commentary on the Greenback, MUFG wrote this morning that the “Buck could strengthen if there is any indication that the Fed’s tolerance for looking through higher inflation is diminishing”, while ING wrote “face‑to‑face summits involving the US President have tended to generate a slew of conciliatory headlines, which can bolster risk assets”.

USD/JPY continues to chop with a c. 45 pip move lower this morning, seen on hawkish remarks from BoJ’s Masu, who said the central bank needed to raise rates “at the earliest stage possible”. Masu, at the last BoJ confab, was not one of the three hawkish dissenters, meaning the vote split could theoretically be 5-4 should former dissenters maintain their votes. Markets are reluctant to fully price a June meeting hike, with just 15bps of tightening expected. The move seen on Masu’s remarks has since been faded as oil prices remain high.

GBP trades with mild losses, with a strong regional GDP report ultimately overlooked by ongoing political unrest. Latest UK political updates suggest former Deputy PM Rayner may put herself forward in a leadership race after HMRC cleared her tax case. Rayner has indicated she favours supporting Manchester Mayor Burnham, which potentially strengthens his bid. Burnham, however, still needs to find an MP willing to step aside to spark a by-election and give Burnham a route to Parliament; reports and denials on the seat in question continue. Some analysts are circulating a survey from Survation, which indicates that soft-left Burnham is the most popular candidate amongst Labour members by a margin. Cable finds support at the round 1.3500 mark.

Central Banks

BoJ’s Masu said they need to raise the rate at the earliest stage possible, and due attention should be paid to whether inflation triggered by the yen’s depreciation may raise people’s inflation expectations and, in turn, affect underlying inflation. Masu said the BoJ will continue to raise rates in response to economic, price, and financial developments, as well as noted that Japan has clearly entered an inflationary phase. Masu said there were mixed views among policy board members at the April meeting on whether to raise the policy interest rate immediately, while he judged at the April MPM that the situation did not warrant a hasty policy rate hike. Masu also commented that he is convinced the BoJ needs to raise the policy interest rate further, so that it falls solidly within the estimated range of neutral interest rate, and warned that if inflation is not contained at an appropriate level, this could lead to a vicious cycle in which firms have to further raise wages to retain workers. Furthermore, he noted that given Japan is no longer in a deflationary period, negative real rates should be addressed as soon as possible.

Fed’s Collins (2028 voter) said she expected the Federal Reserve would need to maintain restrictive policy for some time but hoped the economy would eventually permit more rate cuts later this year. Collins stated that further rate hikes could become necessary to cool inflation pressures and said current Fed policy remained “well positioned” to address risks. It was later reported by WSJ that Collins said she is watching the extent to which tariffs continue to pass through the price chain and that the Fed may need to raise rates if inflation pressures broaden in the coming months, but sees inflation pressures from the Iran war eventually subsiding.

ECB’s Kazaks said can’t yet see full impact of Iran war on inflation, and the situation is a bit worse than the ECB’s baseline scenario.

Fixed Income

Global fixed benchmarks are firmer this morning, attempting to clamber off recent lows, as energy prices remain stable in today’s session. Geopolitical updates overnight were lacking, but attention this morning was on reports that a vessel off the coast of the UAE has been taken by unauthorised personnel. Later reports by Axios stating that US President Trump’s team is now discussing options for military escalation to break the deadlock failed to move benchmarks.

USTs are firmer by 5 ticks, and currently trading within a 110-02 to 110-06+ range. Strength, which appears to be a bounce-back from the lows seen on Wednesday, following a hotter-than-expected PPI report. Oxford Economics outlined that following both CPI and PPI, its PCE “nowcast points to a 3.8% y/y rise in headline prices.

Bunds are stronger by c. 30 ticks, and trades within a 124.80 to 125.03 range. Price action has followed the above, with a lack of fundamental European drivers this morning. It is also worth noting that today is Ascension Day, celebrated across parts of Europe, so lower volumes are possible. From a policy perspective, ECB’s Chief Economist Lane stated on Wednesday that the surge in energy prices may require the Bank to deliver hikes. He continued his hawkish remarks by suggesting that an increase in selling price expectations suggests input cost pressures will map into higher output prices in the coming months.

Gilts are performing in-line with peers, and trade within an 86.14 to 86.48 range. A strong GDP report this morning is having little follow-through on price action. ING opines that it does not change much for the BoE, which is “singularly focused on the impending inflation spike”. UK traders also eye the domestic political situation, with reports on Wednesday suggesting that Health Minister Streeting is preparing to resign as soon as today. Close allies suggest he has more than the required 81 MPs to launch a leadership contest, though others question these claims. Another growing risk is Former Deputy PM Rayner being cleared of any tax wrongdoing by the HMRC, which gives her better credibility should she decide to launch a challenge.

JGBs underperform vs peers, following hawkish commentary from BoJ’s Masu, who stated that there is a need to raise rates at the earliest stage possible. The 10yr now resides at levels not seen since 1997. Elsewhere, the 30yr auction overnight gave an indication that demand remains strong at these elevated yields, as the b/c rose to 3.49x (prev. 3.12x). However, the wider tail suggests that some buyers are potentially holding out for a 4% yield.

Commodities

In geopolitics, the US and Iran both signalled a preference for diplomacy. US VP Vance said Washington is making progress in talks and remains focused on a diplomatic path “for now”, reiterating that Tehran must not obtain nuclear weapons. Iranian Foreign Minister Araghchi also said Iran does not seek war. However, tensions remain elevated: Tehran warned that new confrontations with the US are possible, said its forces are ready to deliver a “crushing” response if attacked, and confirmed it is preparing new navigation laws for the Strait of Hormuz. Separately, Iran accused Kuwait of unlawfully attacking an Iranian boat and detaining four Iranian citizens near an island allegedly linked to US operations. Shipping risks also rose after UKMTO reported that a vessel northeast of Fujairah was taken by unauthorised personnel and moved toward Iranian waters.

Crude markets are holding a mild positive bias but trade off best levels following the diplomacy-first approach by the US and Iran, whilst the positive US-China commentary could also be underpinning the benchmarks. Some mild pressure was seen in energy benchmarks after a WH statement outlined that the US and China agreed that the Strait of Hormuz must remain open. WTI July resides in a 95.48-98.13/bbl range while Brent July sits in a USD 104.57-107.13/bbl range. Sticking with energy, Dutch TTF meanwhile is choppy but posts mild gains (+0.2%) above EUR 47/MWh at the time of writing.

In terms of metals, spot gold is choppy within a narrow range, and largely within yesterday’s parameters after finding support near yesterday’s trough (4,669.53/oz). Newsflow has remained somewhat light this morning with no real macro drivers. Spot gold resides in a USD 4,669-4,719/oz while spot silver consolidates with modest losses above USD 87/oz after gaining for yet another session yesterday, bringing the win streak to seven straight sessions. HSBC raised its average silver price forecasts to USD 75/oz in 2026 and USD 68/oz in 2027.

Copper futures pulled back from record levels despite the broadly positive risk sentiment, with 3M LME copper briefly dipping under USD 14,000/t to trade in a current USD 13,887.50- 14,132.78/t range.

Trade/Tariffs

China renewed export licenses for more than 400 US beef plants, according to customs data.

EU officials said they are open to collaboration with the UK, but the UK will need to relax its trade and economic integration stance in order to progress towards a more ambitious deal, Politico reported.

US Event Calendar

8:30 am: United States Apr Import Price Index MoM, est. 1%, prior 0.8%

8:30 am: United States May 9 Initial Jobless Claims, est. 205k, prior 200k

8:30 am: United States May 2 Continuing Claims, est. 1780k, prior 1766k

8:30 am: United States Apr Retail Sales Advance MoM, est. 0.5%, prior 1.7%

8:30 am: United States Apr Retail Sales Ex Auto MoM, est. 0.7%, prior 1.9%

Central Bank Speakers

8:00 am: United States Fed’s Miran Appears on Bloomberg TV

10:15 am: United States Fed’s Schmid Speaks on Payments Innovation

1:00 pm: United States Fed’s Hammack Gives Opening Remarks

1:00 pm: United States Fed’s Bowman Delivers Pre-Recorded Remarks

5:45 pm: United States Fed’s Williams in Moderated Discussion

7:00 pm: United States Fed’s Barr speaks on Balance Sheet

DB’s Jim Reid concludes the overnight wrap

This time yesterday I was finishing off the EMR looking across the ocean, thinking that work travel wasn’t actually that bad. Today I’m writing it on a bus in gridlocked LA rush hour traffic. I landed at LAX to find that traffic suggested 1hr 45 minutes to my hotel. However, the maps app suggested a bus and metro route that was slated to take 1 hr 25 mins. I gambled but then waited 30 minutes for a bus and that’s now where you find me. Not moving, along with around 70 other passengers!

Markets have been moving much faster than my bus over the last 24 hours though, with US equities last night surging to new highs, with the S&P 500 advancing +0.58%. That was led by fresh gains for tech stocks, with the NASDAQ (+1.20%) and the Magnificent 7 (+2.00%) reaching record highs of their own. The Mag-7 has now risen by over +27% in just over six weeks, while the Philly semiconductor index (+2.57% yesterday) is up +68% over that period. While there wasn’t a single clear catalyst, positive sentiment around the tech mega caps was a dominant theme as several of the Mag-7 CEOs were among the business leaders joining Trump’s visit to China. This included the Nvidia CEO Jensen Huang who must have been delighted to see his stock up (+2.29%) for a sixth day and to fresh records ahead of earnings next Wednesday. If only the West Coast tech gurus could find an answer to LA traffic.

It’s early in Asia and as long as I’m reading this correctly, while trying to avoid motion sickness, markets continue to be bouyant. The KOSPI is up over a percent and the Nikkei, alongside Nasdaq futures, are up around two-thirds of a percent. European futures are up nearly a percent but it’s still early in the session and perhaps a few hours before you wake up and read this. Obviously the world awaits news from the first Trump/Xi meeting today.

Ahead of that, the market mood was also supported by an easing in oil prices even as the Strait of Hormuz remained blocked with no new signs of progress towards a resolution. Brent crude retreated by -1.99% to $105.63/bbl while WTI was down -1.14% to $101.02/bbl. The drop in oil helped European stocks mostly match US gains, as the STOXX 600 (+0.79%) advanced alongside the DAX (+0.76%), the CAC 40 (+0.35%), and the FTSE MIB (+1.00%).

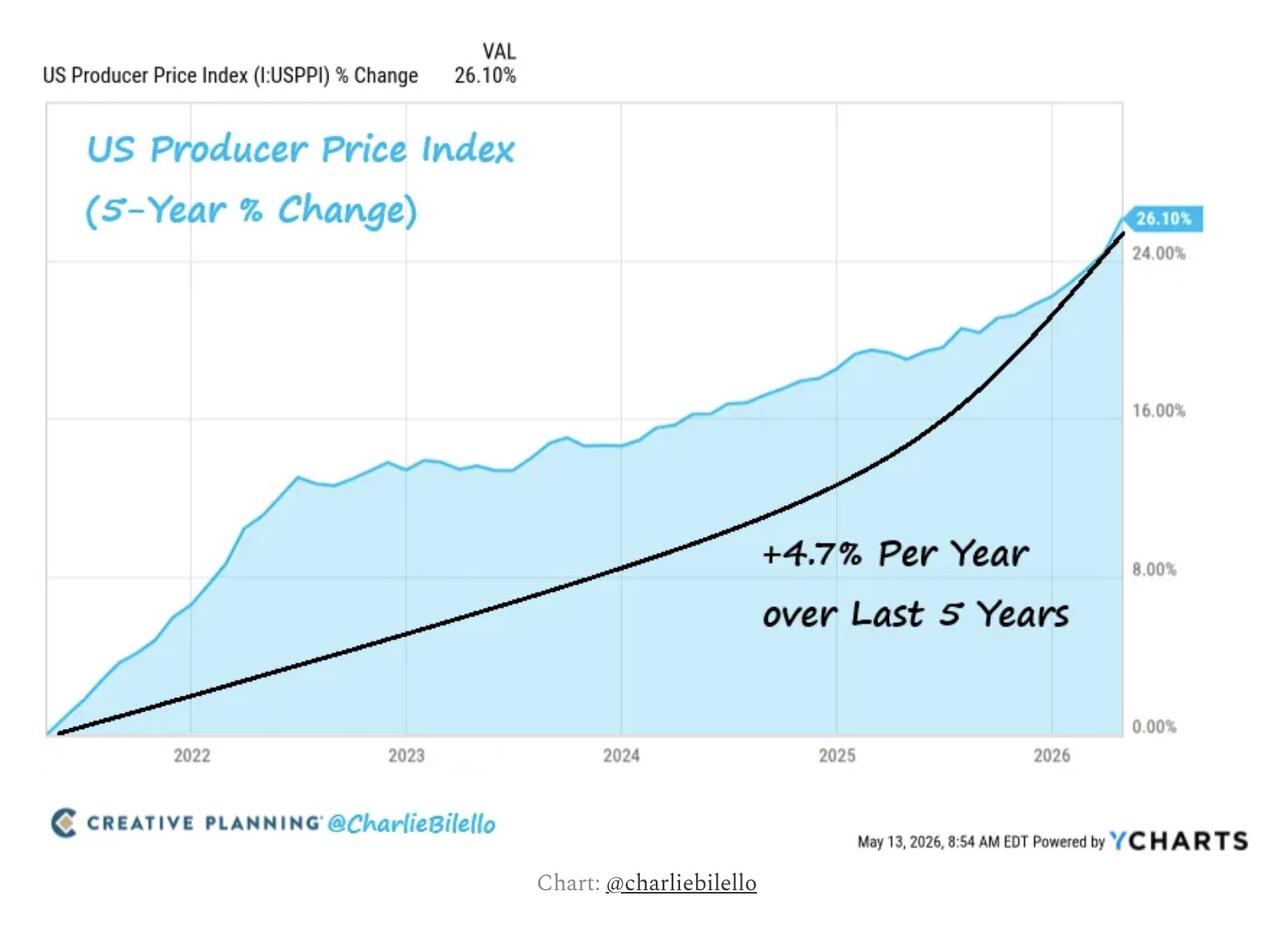

That said, it was not all good news, with nearly two thirds of the S&P 500 actually declining yesterday as blue chip names underperformed. A key challenge was an incredibly strong PPI inflation print, which led markets to price a growing chance of Fed rate hikes. In fact, the monthly PPI reading surged to +1.4% in April (vs. +0.5% expected), marking the biggest monthly surge in producer prices since March 2022. And in turn, that pushed up the year-on-year measure to +6.0% (vs. +4.8% expected), which is the fastest annual pace since December 2022. Moreover, it wasn’t just an energy story, as the core PPI measure excluding food, energy and trade was up +0.6% for the month (vs. +0.3% expected). So for investors, the print pushed back against the idea it was simply a one-time energy shock, and led to growing fears about broader inflation persistence.

That PPI print led to an immediate reaction in rates markets, pushing US Treasury yields to their highest in months, though this reaction then eased as oil prices edged lower. By the close, fed funds futures were little changed, pricing a 40% chance of a hike by year-end, while 2yr yields were down -1.1bps on the day. Yields still inched higher further out the curve, with the 10yr yield (+0.6bps) reaching its highest level since last July at 4.47%, while 30yr yields were up +0.9bps to 5.03%. That came as yesterday’s auction saw 30yr bonds issued at a yield of above 5% for the first time since 2007.

Meanwhile, Kevin Warsh was formally confirmed by the Senate as Fed Chair in a 54-45 vote. He will take over the role as Powell’s term as Chair ends on Friday. Trump’s pick comes in as the FOMC has sounded increasingly doubtful on prospects for further easing. The latest such comments came from Boston Fed President Collins yesterday, who said rates should remain on hold for “some time”, adding that she “could envision a scenario in which some policy tightening is needed” though this was not most likely.

Otherwise in the UK, the political news has shown no sign of letting up, as speculation continues to swirl around PM Keir Starmer’s position. In terms of the latest, it was reported in the Times yesterday, and then in several other outlets, that Health Secretary Wes Streeting might challenge Starmer for the leadership as soon as today. Clearly we’ll have to see what happens, but if Streeting wants to launch a formal challenge, he requires nominations from 20% of Labour MPs, so all eyes on whether he can do that and trigger a contest.

Interestingly, if there is a contest right now, it would also mean that Greater Manchester Mayor Andy Burnham is unable to run as it stands, as he’s not currently an MP in the House of Commons. So that’s led to speculation about whether Energy Secretary and former leader Ed Miliband might run instead although there is some talk overnight of a Labour MP in Manchester prepared to stand down to give Burnham a chance to win a by-election relatively quickly. However, he would still need to be selected as a candidate by the ruling NEC and hold off the strong Green Party in that particular seat.

While this manoeuvring is going on, Starmer himself has made clear that he intends to fight on, so it’s a volatile situation that keeps shifting. Indeed, in the last week alone, the Polymarket odds of a Starmer resignation in 2026 have fluctuated between 47% and 91%, and it’s now back at 70% as we go to press.

When it came to gilt markets, they actually outperformed yesterday, with the 10yr yield down -3.7bps by the close. So that was a larger decline than for yields on 10yr bunds (-0.1bps), OATs (-1.0bps) and BTPs (-2.2bps). Meanwhile, UK equities also traded in line with the rest of Europe, with the FTSE 100 (+0.58%) and the more domestically-focused FTSE 250 (+0.28%) both rising. Moreover, sterling was broadly steady against other major currencies, weakening -0.13% against the US Dollar, but strengthening +0.10% against the Euro.

Looking at the day ahead, a key highlight will be the meeting between President Trump and President Xi in China. Otherwise, data releases include the US weekly initial jobless claims, April retail sales, and the UK’s Q1 GDP reading. Finally, from central banks, we’ll hear from the Fed’s Logan, Schmid, Hammack and Williams, along with the BoE’s Pill. Fingers crossed I won’t be on the same bus by tomorrow’s edition.

Tyler Durden

Thu, 05/14/2026 – 08:30

https://www.zerohedge.com/markets/futures-new-record-high-tech-tehran-trade-taiwan-and-tariffs

‘Lost Confidence In Leadership’: UK PM Starmer ‘Out’ Odds Jump As Wes Streeting Resigns

‘Lost Confidence In Leadership’: UK PM Starmer ‘Out’ Odds Jump As Wes Streeting Resigns

With UK PM Starmer’s leadership under increasing scrutiny, UK Health Secretary, Wes Streeting, has issued a statement via social media that he is resigning his post.

Streeting says that while there are good reasons to remain in post, he has lost confidence in Starmer’s leadership:

“As you know from our conversation earlier this week, having lost confidence in your leadership, I have concluded that it would be dishonourable and unprincipled to [remain in post].”

He went on:

“It is now clear that you will not lead the Labour Party into the next general election and that Labour MPs and Labour unions want the debate about what comes next to be a battle of ideas, not of personalities or petty factionalism.

Setting out the reasons for his resignation, he pointed to last week’s “unprecedented” local elections results, in which the government’s “unpopularity” was “a major and common factor” across Britain, the threat of Reform UK as one of the key reasons for his departure from government, and policy “mistakes”.

“Where we need vision, we have a vacuum. Where we need direction, we have drift. This was underscored by your speech on Monday,” he wrote.

— Wes Streeting (@wesstreeting) May 14, 2026

Streeting is widely thought to be planning to challenge Starmer for the Labour leadership, but he does not announce the start of a formal bid in his letter.

For now there is little to no reaction in GBP or gilts but Polymarket shows the odds of Starmer being gone by the end of May are soaring…

Allies of Mr Streeting, who handed in his resignation as the Health Secretary on Thursday, have made little secret that he is ready to become prime minister and has a comprehensive plan to change the country.

Here is The Telegraph laying out what a Streeting premiership look like?

The economy

Mr Streeting said last year that he was “really uncomfortable with the level of taxation in this country”, suggesting he would resist further increases. Speaking in December, he admitted the Government was “asking a lot” of individuals and businesses with historically high taxes. But he also warned Britain had “a level of indebtedness that we need to take very seriously”, indicating that tax cuts would also be unlikely. He has previously defended Labour’s decision to increase employers’ National Insurance, saying the raise had paid for more NHS appointments. Mr Streeting has previously proposed several radical changes to the tax system. In a 2020 interview, he suggested equalising capital gains tax with income tax, replacing inheritance tax with a “lifetime gifts tax” and increasing corporation tax. He also said all new tax and spending plans should be put through a “progressive impact test” to ensure they helped people on low and middle incomes. But unlike his Left-wing rivals, he has also long advocated that Labour should stick to strict fiscal rules, balancing day-to-day spending with tax revenues.

Defense

Mr Streeting caused a stir in Westminster last month when he suggested that savings should be found from the welfare budget to fund defence. The Health Secretary acknowledged that Britain needed to put more money into the military and that the cash “has to come from somewhere”. While he ruled out taking the money from the NHS budget, he signalled an openness to find it from other areas of spending, such as benefits. Other than on that issue, Mr Streeting has largely backed Sir Keir’s plans to boost defence spending to 3 per cent of GDP by the mid-2030s. Last month, he defended the Government’s handling of the military, insisting that Britain was still “the cornerstone of European defence and security”. Defending the repeated delays to the Government’s defence investment plan, he said Downing Street was taking the time to “get it right”.

Brexit

Mr Streeting is one of the most high-profile Remainers in the Cabinet and was a passionate campaigner for Britain to remain in the EU. Last year, he strongly suggested Labour should consider taking the UK back into a customs union with Europe, saying it would boost growth. But he did insist that the manifesto pledge not to return to freedom of movement with the Continent must stay, ruling out the single market. “The best way for us to get more growth into our economy is a deeper trading relationship with the EU,” he told The Observer in December. “The challenge is any economic partnership we have can’t lead to a return to freedom of movement.” Mr Streeting has long been an advocate of closer EU ties. In 2018, while a backbencher, he rebelled against then leader Jeremy Corbyn, calling for him to commit Labour to keeping Britain in the single market and a customs union.

Immigration

Mr Streeting is naturally a liberal on immigration and has repeatedly signalled his discomfort at the Government’s clampdown on visas and asylum. He criticised Sir Keir’s “island of strangers” speech and has previously said Britain relies on migrants to care for an ageing population. Last November, he admitted he was not comfortable with plans laid out by the Home Secretary to deport families who arrived in the UK illegally. In a 2018 speech, Mr Streeting argued that “we rely on attracting people from overseas, particularly with our ageing population and shrinking working-age population”. But as far back as then, the Health Secretary was stressing the point that Britain needed to increase education and training for its domestic workforce. It is a principle he has taken into government, criticising the health service’s reliance on foreign doctors and admitting voters had “lost confidence in the immigration system”.

The NHS

One of the most notable things Mr Streeting has done in his two years in post is abolishing NHS England, the world’s largest quango. The decision came as a surprise to Westminster and demonstrated that the Health Secretary was unafraid to make significant structural changes to government. It will also put him and his ministers back in direct control of the NHS, hinting at a hands-on approach and a willingness to take on personal responsibility. Waiting lists have fallen on Mr Streeting’s watch and pledges to further improve the health service would be a core part of his premiership. He has also shown himself willing to go to war with the medical unions, warning that their pay demands for junior doctors would “break the country”. But although he has repeatedly spoken of the need to reform the NHS, any change to its funding model would be off the table under Mr Streeting. The Health Secretary has attacked Nigel Farage, the Reform UK leader, for suggesting the UK should consider moving to a French-style public insurance model.

Streeting is only one of the party figures likely to throw their hats into the ring in the event of a formal leadership contest. Former deputy premier Angela Rayner said Thursday morning that she had been cleared of wrongdoing in a probe into her tax affairs, while there is a large faction on the party’s left working to secure a parliamentary seat for Manchester Mayor Andy Burnham, who can’t run without one.

For Starmer to face a formal leadership challenge, a potential successor would have to be nominated by 20% of Labour Members of Parliament. The party currently has 403 MPs, putting that threshold at 81. The ensuing contest would be decided by preferential votes by Labour Party members and affiliates, with precise voting eligibility set by Labour’s governing body.

Tyler Durden

Thu, 05/14/2026 – 08:18

Netflix Sued By Texas For Allegedly Spying On Children

Netflix Sued By Texas For Allegedly Spying On Children

Authored by Mary Prenon via The Epoch Times,

Global video streaming service Netflix has been sued by the Texas attorney general’s office for allegedly collecting consumer data from children and adults without their knowledge or consent.

In a May 11 statement, Texas Attorney General Ken Paxton accused Netflix of spying on consumers by intentionally tracking and logging their viewing habits, preferences, devices, household networks, and other sensitive behavioral data.

The litigation claims that although the mega-entertainment platform purported to refrain from collecting or sharing user data, it, in fact, recorded and monetized “billions of behavioral events.”

According to Paxton, every consumer interaction became a “data point,” which revealed information about the user, and tracking was then applied to both adults’ and children’s accounts and profiles.

“Netflix has built a surveillance program designed to illegally collect and profit from Texans’ personal data without their consent, and my office will do everything in our power to stop it,” Paxton said in the statement.

“Netflix is not the ad-free and kid-friendly platform it claims to be. Instead, it has misled consumers while exploiting their private data to make billions.”

The company argues that the lawsuit lacks merit and is based on inaccurate and distorted information.

“Netflix takes our members’ privacy seriously and complies with privacy and data‑protection laws everywhere we operate,” a Netflix spokesperson told The Epoch Times in an email statement.

“We look forward to addressing the Texas Attorney General’s allegations in court and further explaining our industry-leading, kid‑friendly parental controls and transparent privacy practices.”

Paxton further accused Netflix of disclosing the collected information to commercial data brokers and advertising tech firms to build detailed consumer profiles.

“Netflix users’ data is essentially shopped across Big Ad Tech’s shadowy network,” the statement reads.

In addition, the lawsuit argues that Netflix designs its platform to be addictive, using features that coax users into following certain actions. It cites the autoplay function, which offers a continuous content stream intended to keep users watching for an extended period.

The litigation described Netflix’s actions as a “behavioral-surveillance program of staggering scale.”

“This program requires getting Texans and their children glued to the screen and then extracting every possible piece of data about them while they are there,” it states.

The end game, the lawsuit claims, is for Netflix to earn even more revenue from harvesting and selling consumer data. It notes that between 2018 and 2026, Netflix’s annual revenue grew from nearly $15 billion to more than $50 billion.

“Netflix’s explosive financial growth reflects a deliberate choice to cash in on the trust it spent years cultivating under false pretenses,” the case states.

It also claims that Netflix provided its users’ data to large commercial brokers such as Experian and Acxion, and partnered with ad-tech platforms including Google Display & Video 360 and The Trade Desk, so that its user data could be merged with information collected off the platform.

The lawsuit intends not only to stop the alleged unlawful collection and disclosure of user data, but also to hold Netflix accountable under the Texas Deceptive Trade Practices Act. In addition, the litigation is seeking injunctive relief, civil penalties, and that Netflix be required to disable its autoplay function on children’s profiles.

Paxton is requesting a trial by jury.

Tyler Durden

Thu, 05/14/2026 – 08:05

https://www.zerohedge.com/technology/netflix-sued-texas-allegedly-spying-children

Rate Hikes Are Coming…

Rate Hikes Are Coming…

Submitted by QTR’s Fringe Finance

What a week for macroeconomic data. We got two horrific datapoints this week that, when combined with some key comments from days ago, seem to be pushing the Fed closer to rate hikes than they’ve been in a long while.

The case for rate hikes is no longer some fringe tail risk like it felt it was a year ago as inflation numbers (though still high) appeared to be coming down.

For most of last year, markets were operating under a very clean narrative that inflation would continue cooling, growth would gradually slow, and the Federal Reserve would eventually be in position to cut rates further. That framework is starting to crack.

Regardless of whether investors were focused on a potentially more dovish policy direction under figures like Kevin Warsh or Stephen Miran, the Fed ultimately cannot sidestep hard inflation data. If price pressures are clearly reaccelerating, policymakers risk losing massive credibility if they continue signaling easing while inflation moves in the opposite direction.

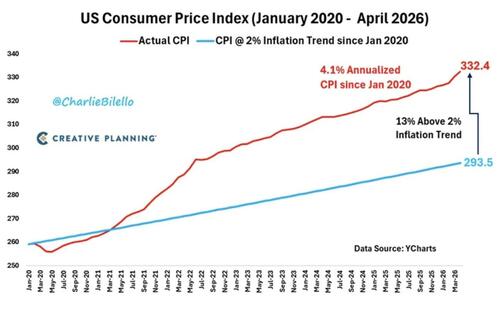

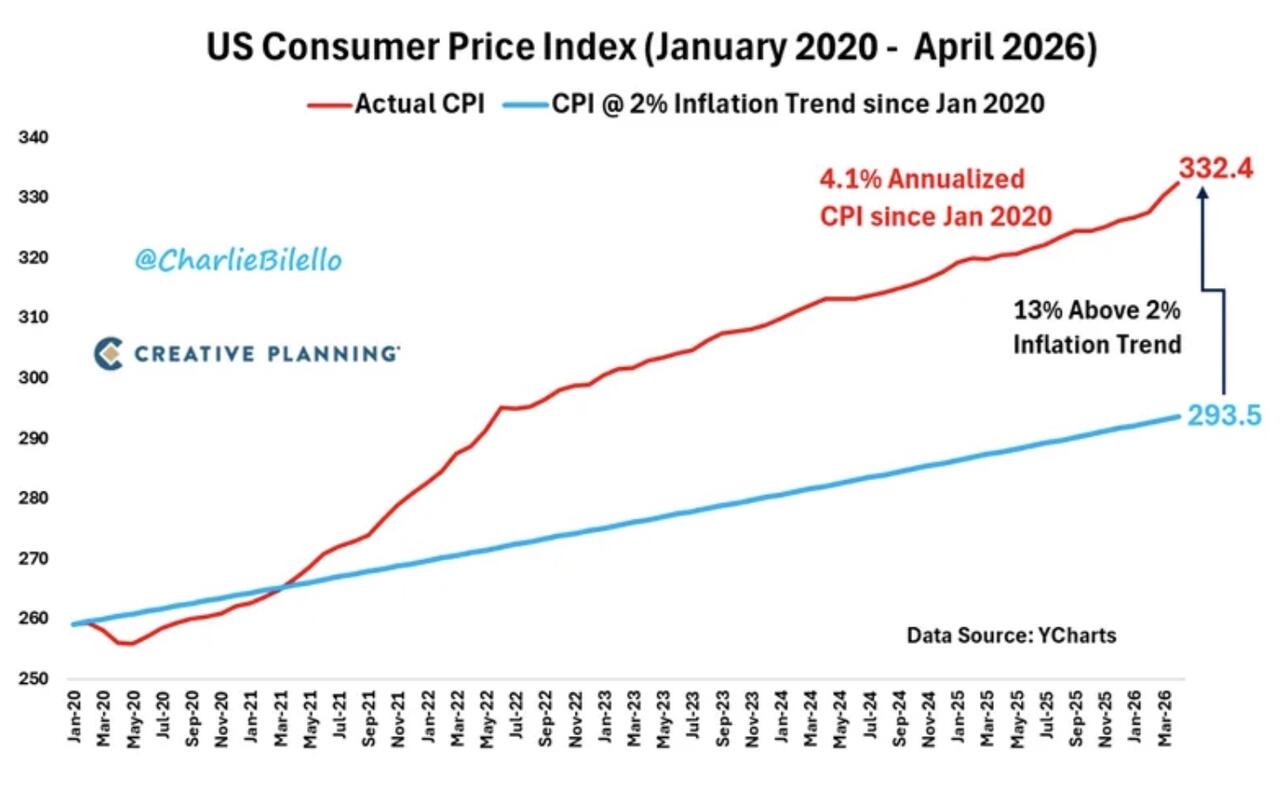

The market is being forced to confront that reality in real time. And this chart from Charlie Bilello yesterday shows exactly what that reality looks like: inflation got away from the Fed in 2020, and we haven’t been anywhere near close to returning it toward the baseline trend we have tried to revert to. In fact, the chart shows the delta between the 2% baseline target and current inflation as widening.

That pressure intensified today after a major upside surprise in wholesale inflation.

The latest producer price index report showed wholesale prices rose 1.4% in April, nearly triple expectations of 0.5% and well above March’s upwardly revised 0.7% increase. On an annual basis, producer prices climbed 6%, marking the biggest increase since December 2022.

This matters because producer prices often serve as an early warning signal for future consumer inflation. Rising input costs eventually work their way through supply chains and show up in prices paid by households. The bigger issue is that this increasingly looks like something broader than a temporary energy spike. Pipeline inflation is building again at a time when the Fed had been hoping for sustained disinflation.

Meanwhile as CNBC noted earlier in the week that the CPI was also still coming in hotter than expected — which was already hot at 3.8%. Don’t lose sight of the fact that the Fed’s target is 2%, so this is nearly double what the Central Bank is gunning for:

The consumer price index rose at a seasonally adjusted 0.6% for the month, putting the one-year pace at 3.8%, the Bureau of Labor Statistics reported Tuesday. The monthly rate was as forecast, but the annual rate was 0.1 percentage point above the Dow Jones consensus.

As CNBC noted, following the hotter consumer inflation report earlier this week, traders sharply reduced expectations for rate cuts and began pricing in the possibility that the Fed’s next move could actually be higher. According to CME FedWatch data cited by CNBC, markets were pricing roughly a 37% probability of a rate hike before year end.

That is a dramatic reversal from the dominant consensus just weeks ago, when the conversation centered almost entirely around when cuts would begin.

What makes this shift even more significant is that Fed officials themselves are no longer trying to shut down the possibility of tighter policy. Austan Goolsbee said last week in an interview with Bloomberg that all options remain on the table and explicitly pushed back on the idea that cuts are the only possible path forward. He said he does not see how anyone can look at current conditions and assume the only conceivable outcome is lower rates.

He also made clear that his concerns extend beyond energy and include broader inflation pressures that could prove more persistent. That is an important signal because central bankers tend to avoid discussing hikes unless they believe the risk is becoming materially more realistic.

🔥 80% OFF FOR LIFE: Using this coupon entitles you to 80% off an annual subscription to Fringe Finance for life: Get 80% off forever

The broader takeaway is that markets may still be underestimating how quickly the macro narrative can shift. The dominant trade had been built around lower inflation, lower rates, and a soft landing. That assumption now faces growing pressure from rising producer prices, elevated inflation expectations, persistent energy shocks, and increasingly hawkish market pricing. If inflation remains hot for another month or two, the conversation may move beyond higher for longer and toward the possibility that the next move from the Federal Reserve is another hike.

That would represent a major regime change for markets that have spent months positioning for the exact opposite outcome.

I’ve been saying for months that the Fed is stuck between a rock and a hard place, and now that reality is getting harder to spin away with carefully worded press conferences and endless “data dependent” talking points. If they raise rates into this inflation reacceleration, they risk detonating the parts of the economy that have only survived because money was essentially free for years. The most speculative and overleveraged corners get hit first. Bitcoin and broader crypto would likely get smoked, subprime auto lending’s implosion accelerates, and the ever growing Private Credit shit officially hits the fan.

But if the Fed backs off because markets throw a tantrum and stocks forget how to go up for three consecutive weeks, they’ll be right back to printing money and flooding the system with liquidity to save everyone from the consequences of their own leverage. And what does more printing solve when inflation is already running hot? Absolutely nothing, except ensuring you get another inflation wave later that’s even harder to contain. That’s the trap. Raise rates and break the economy. Print money and make inflation worse.

Years of kicking the can down the road have left the Fed with two terrible choices, and now the bill is showing up right on schedule. Turns out “we can have permanently elevated asset prices, endless stimulus, and no consequences” was not actually a serious economic strategy. Who would have thought?

Now read:

Why I Avoid Tech Investments…Even During A Tech Boom: Harris Kupperman

The Coming Gamma Nightmare

5 Stocks I’m Still Keeping An Eye On

Do the Rich Pay Their “Fair Share” of Taxes?

Another Real Crisis Hiding Behind Record Highs

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Thu, 05/14/2026 – 07:45

Europe’s Dependence On US LNG Set To Surge

Europe’s Dependence On US LNG Set To Surge

By Irina Slav of OilPrice.com

The European Union’s dependence on liquefied natural gas from the United States is set to rise significantly, reaching 80% of all LNG imports in two years, the Institute for Energy Economics and Financial Analysis has warned.

In a report cited by Reuters, IEEFA noted that the European Union already imports significant volumes of U.S. liquefied gas, creating a potentially risky dependence on a single supplier.

LNG imports from the United States into the EU accounted for 58% of overall LNG imports.

Yet this dependence is only going to increase in the coming years, the outlet said, recommending more wind, solar, and heat pumps as an alternative.

This year, the United States will become the European Union’s biggest supplier of liquefied gas, even as the bloc also gobbles up every ton of Russian LNG it can buy ahead of the 2027 ban on Russian energy imports.

The motivation for that ban, in addition to punishment for the war in Ukraine, has been to avoid overwhelming dependence on a single energy supplier, which is what the EU is currently doing with the U.S.

Energy commodities are a big part of the trade deal signed last year by President Trump and European Commission President Ursula von der Leyen.

The deal featured a commitment on the part of the EU to buy $750 billion worth of U.S. energy commodities over a period of three years.

The European Parliament earlier this year signaled it has problems with the deal, which angered the U.S. president, and he threatened to hike tariffs on EU goods unless the bloc signs the deal as is.

The arrangement elevated American LNG, oil, and refined fuels in Europe’s energy supply mix.

The actual supply of so many energy commodities, however, would be physically – and financially – challenging both for the suppliers and the buyers.

Tyler Durden

Thu, 05/14/2026 – 07:20

https://www.zerohedge.com/commodities/europes-dependence-us-lng-set-surge

Trump, Xi Put Hormuz, Iran, Trade, Taiwan At Center Of Historic Beijing Summit

Trump, Xi Put Hormuz, Iran, Trade, Taiwan At Center Of Historic Beijing Summit

President Trump and Chinese President Xi Jinping are currently seated at the main table at a state banquet. President Xi called the visit historic, and said U.S.-China ties are “stable” amid talks with Trump’s team.

President Xi offers a toast at the state banquet dinner in Beijing: “To the bright future of China-U.S. relations, and the friendship between the two peoples, and to the health of President Trump and all of the friends present.” pic.twitter.com/VmJeU4Xk1f

— Rapid Response 47 (@RapidResponse47) May 14, 2026

According to a White House readout, Trump and Xi agreed that the Strait of Hormuz should remain open to free navigation and that Tehran should not charge a fee to ships using the critical waterway.

Key notes from the White House readout (courtesy of Bloomberg):

Trump Had A Good Meeting With Xi: White House Official

Leaders Discussed Increasing China’s purchases of Agriculture

Trump, Xi Agreed Hormuz Must Remain Open: White House Official

U.S. Says Xi Made Clear China Opposes Militarization of Hormuz

Both Sides Agreed Iran Can Never Have A Nuclear Weapon: U.S.

U.S. Says Xi Expressed Interest in Purchasing More American Oil

From the Bilateral Meeting in Beijing:

President Trump had a good meeting with President Xi of China. pic.twitter.com/WaH8hR1ZV3

— The White House (@WhiteHouse) May 14, 2026

Both countries agreed that Iran can never have a nuclear weapon. pic.twitter.com/7hYMIBoTZY

— The White House (@WhiteHouse) May 14, 2026

Beijing also signaled interest in buying more U.S. oil to reduce China’s reliance on crude and crude products transiting the Hormuz chokepoint. This signifies how the U.S.-Iran conflict is rewiring global energy flows.

Trump-Xi talks also covered fentanyl, securing market access for U.S. companies in the mainland market, and increasing Chinese investment in American industries and purchases of U.S. agricultural products.

“American enterprises are deeply involved in China’s reform and opening up, a process from which both sides have benefited,” Xi told the leaders of U.S. companies accompanying Trump on the trip. Those CEOs include Tesla’s Elon Musk, Apple’s Tim Cook, Boeing’s Kelly Ortberg, and Nvidia’s Jensen Huang.

The two sides discussed ways to enhance economic cooperation between countries, including expanding market access for American businesses into China and increasing Chinese investment.

Leaders from many of the United States’ largest companies joined a portion of the meeting. pic.twitter.com/i3Q1ogde2E

— The White House (@WhiteHouse) May 14, 2026

Xi continued, “China’s door to the outside world will only open wider.”

On the agricultural front, Bloomberg reported that China renewed import licenses for hundreds of U.S. beef plants, reviving trade that will help ranchers and farmers.

Xi was quoted as saying that China and the U.S. agree to build a “constructive and strategically stable relationship” that will serve as a framework for China-U.S. relations over the next three years and beyond.

On the subject of Taiwan, Xi told Trump bluntly that Sino-U.S. relations would enter an “extremely dangerous place” if Trump ignored Beijing’s demands over Taiwan.

Back at the state banquet, Trump invited Xi to Washington on Sept. 24.

Overall, it appears that day one of Trump’s summit with Xi was positive.

.@POTUS delivers remarks at the state banquet dinner at the Great Hall of the People: “It was a fantastic day, and in particular, I want to thank President Xi, my friend, for this magnificent welcome… and for so graciously hosting us on this very historic state visit.” pic.twitter.com/lcFTC7wUY9

— Rapid Response 47 (@RapidResponse47) May 14, 2026

Earlier, Trump and Xi took a walk at an ancient temple in Beijing.

.@POTUS in China: “It’s great — a great place. Incredible. China is beautiful.” pic.twitter.com/Xiu7KSCvpL

— Rapid Response 47 (@RapidResponse47) May 14, 2026

“The China-U.S. Summit is ongoing, with expectations for any breakthroughs low,” UBS analyst Justinus Steinhorst told clients earlier.

UBS analyst Shuo Yang noted, “It has been a subdued Asia session, with markets in wait-and-see mode into the Trump-Xi meeting.”

Treasury Secretary Scott Bessent joined CNBC and said the U.S. and China are seeking to lower tariffs on some trade, starting with $30 billion in non-critical areas. Bessent also noted that Chinese officials are “doing what they can” to reopen Hormuz.

Bessent added that Boeing is nearing a “large” plane order from China, but did not specify whether those orders would be for narrow-body or wide-body jets.

Tyler Durden

Thu, 05/14/2026 – 07:05

Why UBS Is Bullish On Take-Two Ahead Of Grand Theft Auto VI Launch

Why UBS Is Bullish On Take-Two Ahead Of Grand Theft Auto VI Launch

UBS analysts reiterated that Take-Two Interactive is their top U.S. gaming pick, with the highly anticipated release of Grand Theft Auto VI still scheduled for early November.

“We recently framed TTWO as our top pick in the U.S. interactive gaming space,” analyst Christopher Schoell told clients.

Schoell said, “Concerns around AI and the potential for a new wave of content to hit the market/compete for engagement have weighed on the sector,” adding, “We believe the fears for TTWO are overdone and expect new GTA VI announcements, trailers, and gameplay to drive sentiment, while industry consolidation highlights TTWO’s potential strategic value as the remaining publicly traded U.S. AAA developer.”

Schoell expects TTWO to guide to a record fiscal 2027, with $9 billion in bookings, including about $2 billion in GTA VI full-game sales.

Schoell and his team noted, “We build on our conviction that a strong GTA VI launch in the near term, coupled with expanding RCS and in-game monetization, will likely drive more stable long-term economic returns.”

Here’s that bullish framework:

Turning Hits into Recurring Cash Flows: In the mid-2010s with the launch and scaling of GTA Online and NBA 2K RCS, TTWO successfully evolved its CFROI (Cash Flow Return on Investment) profile from extreme volatility to high and stable economic returns. Strong historical execution supports our view of a successful mix shift to higher margin RCS revenues ahead and continued CFROI expansion.

How Big Could GTA VI Be? TTWO’s CFROI Forecast vs Past Blockbusters: Leveraging the breadth of the HOLT framework, we compare TTWO’s forecasted CFROI in the launch year to CFROI levels in other blockbuster game launches. Notably, we believe the launch of GTA VI will push CFROI to one of the highest levels we’ve seen compared to historical game launches.

Framing Long-Term Market Expectations: In HOLT’s default valuation framework, TTWO has around 80% potential upside and market expectations appear muted vs forecasts. TTWO has earned a median CFROI level of 13% the last 10 years in conjunction with a high rate of reinvestment, and the GTA VI launch should increase CFROI to near all-time high levels. Despite this, long-term market expectations imply CFROI will fade to 9%, below its historical median. We see this as a relatively low bar to clear given a bookings mix shift to higher margin RCS revenue, likely supported by a steady cadence of content releases for the established GTA VI player base long-term.

Schoell offered clients his expectations ahead of earnings and guidance next Thursday:

As highlighted in our recent earnings preview, we expect TTWO’s F4Q results to come in at the high-end of guidance (company reporting May 21). The main focus however will be the initial F27 outlook. We expect management to guide to a record year alongside GTA VI’s release, where our prior survey work points to significant pent up demand and pricing power. Similar to precedent, we believe initial guidance could be conservative, setting up for a beat and raise narrative. This was the case for both GTA V (Fiscal 2014) and RDR II (Fiscal 2019), when the company outperformed its initial bookings outlook by several hundred million. We look for $9.0B of bookings in F27, incl. $2.0B of full game sales for GTA VI. Our est. assumes higher amort and S&M alongside GTA’s release, albeit visibility into magnitude is limited and could drive variability to NT EPS (UBSe $6.16/$11.47 of Adj. EPS in F27/F28). We recently published an interactive model which allows investors to input their own unit/pricing assumptions for GTA VI and underlying PC/console/mobile growth.

Shares peaked in late 2025 at around $260 and have since tumbled to $190. Shares are currently clawing back some of those losses.

UBS maintains a Buy rating and a $300 price target, implying about 33% upside from Wednesday’s levels.

Professional subscribers can read the full TTWO/GTA VI note here at our new Marketdesk.ai portal.

Tyler Durden

Thu, 05/14/2026 – 06:55

https://www.zerohedge.com/technology/why-ubs-bullish-take-two-ahead-grand-theft-auto-vi-launch

“It’s Either Us Or Them’: Far-Left French Mayor Calls For Insurrection If Conservatives Win Presidential Election

“It’s Either Us Or Them’: Far-Left French Mayor Calls For Insurrection If Conservatives Win Presidential Election

If the National Rally (RN) candidate wins in the French presidential election next spring, far-left mayor Bally Bagayoko of multi-cultural Saint-Denis has said it will be invalid, calling for a “popular insurrection” if this were to occur.

One social commentator on X, Alain Weber, posted frankly about the reality France is facing: “Contrary to what the Democrats of this country thought, the danger will not come from Jean-Luc Mélenchon but from Bally Bagayoko, who is the calm face of the civil war being prepared in the suburbs.”

Attached to his post was an interview of Bagayoko with Jean-Michel Aphatie on LCI Direct in which he tells the shocked host that if RN wins the election next year, they will never have “popular legitimacy,” only what he calls “institutional legitimacy.”

The mayor also said that those who attempt to “normalize the far right” are “dangerous,” adding that “if the far right comes to power, which we do not want, we will do everything so that it cannot happen.”

During another interview on Oumma.com, a Muslim community media outlet, the mayor of Saint-Denis also attacked President Emmanuel Macron, the Bolloré group’s media outlets, and even certain left-wing parties, according to Le Figaro.

Blaming Macron for the rise of the far right, Bagayoko stated: “Under Macron, the far right has never been so strong. We’re now at almost 140 racist members of parliament,” calling them all “guardians” of RN’s history and doctrine, according to the portal.

Returning to the theme of inevitable insurrection, Bagayoko told the host: “It’s either us or them… that is to say, the far right,” adding later that he was “firmly convinced that the people will rise up” if RN wins next spring, while ignoring the fact that an RN victory would indicate voters exercised their democratic will.

Warned to “be careful” by the host, lest he “be accused of inciting insurrection,” the Saint-Denis mayor doubled down: “All the important reforms in this country have been achieved through popular uprisings,” he said, citing the storming of the Bastille and the Yellow Vest movement.

As noted by Weber, the danger of Bagayoko is real. “He is manufacturing the psychological conditions for a refusal of alternation, that is to say, quite simply, the conditions for a cold civil war, then hot.”

It is shocking to witness the rise of the far-left LFI mayor and the influence he now wields, when, in fact, he received just 13,506 votes out of approximately 64,000 registered voters in Saint-Denis.

However, his voice calling for justice for the wrongs committed against those he sees as having been oppressed by France for centuries has been capturing headlines since his election in March.

In a recent example, Bagayoko drew ire from the local state prefect when it was revealed he had removed a photo of Macron, traditionally on display as a sign of respect, relegating it to a corner of his office and, by some accounts, turning it upside down.

“The portrait will remain in its place until the state fulfils its obligations under the Republican Pact, particularly toward the residents of our territory,” he said, presumably referencing Saint-Denis, a town with a population of some 150,000, as their territory.

Whose territory? That, we can suppose, would be of the Blacks and other minorities, as he has called the city “la ville de Noirs.”

We know that when Bagayoko speaks of “eliminating inequality,” any past colonial oppression and slavery are high up on his list, as he sees these as part of today’s problems. However, as pointed out point-blank by Marion Maréchal, president of Identité Libertés, in a recent interview, “Monsieur Bagayoko has a greater chance of being a descendant of slave traders than I do.”

Her comments came in the wake of the cancellation of an event commemorating the abolition of slavery in Vierzon, an RN stronghold. The town, which has only been holding the event since 2006, says the move is due to budget cuts, while many are predictably calling out RN for refusing to honor the importance of ending slavery.

In fact, the issue for many on the right is more complex. “The memory of slavery must not concern only Europeans. The Arab-Muslim slave trade: 17 million victims. The intra-African slave trade: 14 million victims,” Maréchal noted to viewers. She and many others would prefer a commemoration that addressed all wrongdoers, not simply Whites and Westerners.

In March, the UN General Assembly adopted a resolution that designated the Atlantic slave trade and its involvement in the slavery of Africans as “the most serious crime against humanity.” According to a UN statement, it seeks an order that “confronts historical truth while building mechanisms for equitable futures.”

But many want to know why the issue of African enablers, middlemen, and traders is never called out. “Since the beginnings of the trans-Saharan slave trade in the 7th century, Africans had been selling slaves to Arab Muslims,” and as demand grew from the New World centuries later, ethnic Africans happily met it, wrote Marie-Claude Mosimann-Barbier for Le Figaro last month, in a piece covered by Remix News.

“Long before the arrival of Europeans and the development of the Atlantic slave trade, internal slavery was a structural reality in most African societies,” she wrote.

The question for today is why anyone is welcoming the cries for insurrection from an activist mayor who has shown zero respect for the existing Republic of France — and zero interest in its continuation?

Tyler Durden

Thu, 05/14/2026 – 06:30

The US Has Restarted Jungle Warfare In Panama After 25 Years

The US Has Restarted Jungle Warfare In Panama After 25 Years

For the first time in roughly 25 years, the US has restarted jungle warfare training in Panama, signaling a broader return of American military activity in Latin America, according to a new Bloomberg feature.

At a rainforest training center near Colón, US troops practice survival techniques, patrol operations, casualty evacuations, and combat drills with Panamanian forces. The environment is intentionally unforgiving—thick jungle, venomous snakes, relentless insects—and soldiers often depend on machetes to move through dense terrain. One Panamanian instructor mocked the Americans’ inexperience, joking, “They’re always cutting themselves.”

The renewed training effort reflects a wider shift under President Donald Trump, whose administration has taken a far more aggressive posture toward the region. Officials have discussed military action against drug cartels in Mexico, increased pressure on governments in Cuba and Venezuela, and repeatedly raised the possibility of reclaiming the Panama Canal.

According to historian Alan McPherson, this approach represents a “coercive, multifaceted new imperialism,” combining military threats with trade pressure and diplomatic leverage.

Bloomberg writes that beyond Panama, Washington has deepened military partnerships across the hemisphere. The US has reached new agreements with El Salvador and Paraguay, carried out drone strikes in the Caribbean, and expanded security coordination involving Ecuador. Trump has encouraged regional governments to take a harder line on organized crime, telling leaders they should respond by “unleashing the power of our militaries.”

Inside the Panamanian jungle camp, cooperation between both militaries is highly visible. Troops sleep in the same barracks, eat together, and train side by side. During one exercise, an American soldier explained how a trap designed for animals could also be repurposed in combat: “To trap an enemy, you just use different bait… Maybe some ammo.”

Still, the growing US presence remains politically sensitive in Panama because of the legacy of the 1989 US invasion that ousted Manuel Noriega. While some Panamanians support military cooperation, others see it as a dangerous erosion of sovereignty—especially as Trump continues invoking the canal. Activist José González warned, “We’re ceding national territory, Panamanian territory, to the United States.”

In neighborhoods such as El Chorrillo, where residents still remember the devastation of the invasion, anti-US sentiment remains visible. One mural captures that lingering anger: “We don’t forget or forgive.”

Tyler Durden

Thu, 05/14/2026 – 05:45

https://www.zerohedge.com/markets/us-has-restarted-jungle-warfare-panama-after-25-years

Scientists Intentionally Trigger 8,000 Earthquakes Deep Beneath Swiss Alps

Scientists Intentionally Trigger 8,000 Earthquakes Deep Beneath Swiss Alps

Authored by Steve Watson via Modernity.news,

Scientists at ETH Zurich university in Switzerland have deliberately induced around 8,000 seismic events deep underground in the Swiss Alps as part of an experiment called Fault Activation and Earthquake Rupture (FEAR-2).

The team injected 750,000 litres of water into the ground via two boreholes over approximately 50 hours at the BedrettoLab facility. The quakes were too small to be felt at the surface or cause damage, with magnitudes ranging from -5 to -0.14.

The researcher explained “While some seismic events occurred on the target fault zone, a large number of events took place on neighbouring geological structures activated by the fluid injection.”

Uni researchers are making earthquakes happen under the Alps. Okayyy. https://t.co/EXZIYaGmnm

— m o d e r n i t y (@ModernityNews) May 12, 2026

Professor Domenico Giardini, one of the lead researchers, stated: “If we master how to produce quakes of a certain size, then we know how not to produce them.”