Category: News

India Panics, Further Tightens Gold Flows As Rupee Collapses

India Panics, Further Tightens Gold Flows As Rupee Collapses

Well, that escalated quickly…

With the Rupee accelerating its declines to ever lower record lows against the dollar, Indian authorities have stepped up capital controls, focusing on curbing demand in the gold ‘exit’ route.

4 days ago, there were no signs of import duty hikes as Prime Minister Narendra Modi issued a rare weekend appeal urging citizens to forgo gold purchases as well as unnecessary foreign travel in order to help hold up the currency..

2 days ago, tariffs were more than doubled on gold and silver imports to 15% and 6% respectively.

And today, they are doing even more with India now tightening the advance authorisation route, effectively capping how much gold individual exporters can bring in through that channel.

A government notification stated that imports of bullion exceeding 100 kilograms would be subject to prior authorization, adding that any subsequent imports would only be granted after exports equivalent to 50% had been carried out.

The notification also introduced stricter checks for first-time applicants seeking permission to import gold under the scheme.

The government has also linked future import approvals to export performance.

India, the world’s third-largest oil importer, has been hit hard by the inflationary shock caused by energy disruptions in the Persian Gulf.

Higher import bills have driven sharp foreign-exchange outflows, pushing the rupee down to a record low and prompting the Reserve Bank of India to step in and sell dollars.

And the fact that gold is the country’s largest import item after crude oil does not help, which is why India is doing everything in its power to limit capital outflows.

As UBS explains, the new curbs don’t directly restrict the importing banks, but it does limit how much metal each participant can access, reducing the ability to build larger positions and tightening flows through the system.

The broader backdrop is that India is no longer purely a jewellery-led market.

Demand has become more investment‑driven, with a growing share of imports moving into financial holdings, including ETFs.

A significant part of last year’s import surge appears to have gone into investment rather than fabrication, which changes how the market behaves. During the initial phase of the recent Middle East escalation, Indian ETFs were among the first to react, selling roughly ~20 tonnes in the opening week of the move.

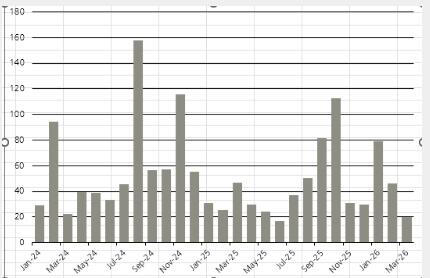

More immediately, demand has already been soft in recent weeks, as reflected in recent import data.

Monthly India Gold Imports below in tonnes, source: UBS

Near‑term uncertainty around fertiliser (urea) supplies also poses a risk to this year’s crop cycle, with the key monsoon period running into August, which could weigh on rural incomes and, by extension, gold buying.

The recent moves underscore policy concerns around curbing import-led dollar outflows from high foreign exchange-draining sectors, Madhavi Arora, economist at Emkay Global Financial Services said.

“We expect gold imports to fall by around 20-25% this year due to these steps.”

New Delhi is weighing several further emergency steps to shore up foreign-exchange reserves and limit the damage from the war in the Middle East.

If demand does recover, however, as seen in previous tightening cycles, attempts by the government to limit capital outflows via precious metals will only encourage activity to re‑route via unofficial channels (with smuggling picking up when the onshore market is constrained), to preserve purchasing power, and it is only a matter of time before India joins the rest of the financially suppressed developing world in actively pursuing such non-fiat alternatives as tether and bitcoin if the traditional gold and silver pathways are limited.

Tyler Durden

Thu, 05/14/2026 – 15:40

https://www.zerohedge.com/precious-metals/india-panics-further-tightens-gold-flows-rupee-collapses

DOJ Sues DC Bar Over Its Prosecution Of Former Trump Lawyer, Calls It “Partisan Arm Of Leftist Causes”

DOJ Sues DC Bar Over Its Prosecution Of Former Trump Lawyer, Calls It “Partisan Arm Of Leftist Causes”

Authored by Troy Myers via The Epoch Times (emphasis ours),

The Department of Justice (DOJ) filed a complaint on May 13 against the D.C. Bar, alleging it has acted as a “partisan arm of leftist causes.”

The U.S. Department of Justice in Washington on April 27, 2026. Madalina Kilroy/The Epoch Times

According to the DOJ, the agency seeks to advance President Donald Trump’s directives to end the weaponization of the federal government while nullifying the D.C. Bar’s prosecution of former Assistant Attorney General Jeff Clark.

D.C. Disciplinary Counsel Hamilton P. Fox III, the D.C. Office of Disciplinary Counsel, the D.C. Court of Appeals, the District of Columbia itself, the D.C. Bar, and others are named as defendants and accused of unlawfully prosecuting Clark based on his internal deliberations of potential fraud in the 2020 presidential election.

The Epoch Times reached out to the D.C. Bar for comment and was referred to the D.C. Board on Professional Responsibility, which did not immediately respond to a request for comment.

Clark wrote a draft letter for his litigation on potential fraud, which was never issued, and the D.C. Court of Appeals’ disciplinary authorities punished him over it, according to the complaint.

The D.C. Bar and others’ investigation and discipline of Clark were improperly based on “their disagreement with Mr. Clark’s performance of his discretionary Executive Branch duties, particularly with respect to a predecisional and deliberative document about potential election fraud in Georgia, which remains the subject of criminal investigation and civil litigation years later,” the complaint said.

Allowing proceedings against Clark to continue would mean state bar authorities can exert control over the executive branch, the DOJ said, adding, “That is not the law.”

The DOJ cited the supremacy clause of the U.S. Constitution, or preemption, as a cause for dismissing proceedings and discipline against Clark. Preemption, the DOJ said, prevents states and the District of Columbia from regulating or interfering with federal officials performing their duties.

In the complaint, the DOJ also argued that a 2024 Supreme Court decision, Trump v. United States, offers protection for Clark.

In that landmark ruling, the justices said the president is entitled to absolute immunity “for conduct within his exclusive sphere of authority” because the president should have the “maximum ability to deal fearlessly and impartially with the duties of his office.”

The president would enjoy little immunity if federal attorneys could be targeted and disciplined for internal deliberations, the complaint said.

In the news release, the DOJ said this filing furthers Trump’s executive order, “Ending the Weaponization of the Federal Government,” and his presidential memorandum, “Preventing Abuses of the Legal System and the Federal Courts.”

“The D.C. Bar will no longer be permitted to probe sensitive Executive Branch deliberations and target Executive Branch officials with whom they happen to politically disagree,” Associate Attorney General Stanley Woodward said. “Federal attorneys will once again be free to share their candid legal advice with their bosses and colleagues.”

In a similar case to Clark’s, the DOJ said it filed a statement in support of former interim U.S. Attorney Ed Martin, who is looking to have the D.C. Bar’s prosecution of him taken up in a neutral federal court.

The DOJ noted in its news release that three former attorneys general have acknowledged that the D.C. Bar’s push to discipline federal attorneys “for making recommendations, factual assertions, and providing legal advice during confidential internal agency deliberations on law enforcement and sensitive public policy” is “improper and constitutionally impermissible.”

“President Trump promised to put an end to the weaponization of the legal process, and today’s lawsuit against the D.C. Bar makes good on that promise,” Woodward said.

Tyler Durden

Thu, 05/14/2026 – 15:20

Zelenskyy’s Former Right-Hand Man Yermak Arrested In $10.5 Million Money Laundering Scheme

Zelenskyy’s Former Right-Hand Man Yermak Arrested In $10.5 Million Money Laundering Scheme

Ukraine’s High Anti-Corruption Court ordered the pre-trial detention of Andriy Yermak, the powerful former head of President Volodymyr Zelenskyy’s Office and once the country’s second-most influential figure, on money-laundering charges tied to a high-profile corruption scheme.

The ruling marks a dramatic fall for Yermak, who served as Zelenskyy’s closest aide from 2020 until his resignation in late 2025 amid earlier raids. He was taken into custody directly from the courtroom following the decision.

Charges and Allegations

Ukraine’s National Anti-Corruption Bureau (NABU) and Specialized Anti-Corruption Prosecutor’s Office (SAPO) named Yermak a suspect on May 11 in a scheme involving the laundering of approximately 460 million hryvnias (about $10.5 million or €9-10 million).

Prosecutors allege he participated in an organized criminal group that funneled illicit funds – originating from kickbacks at the state nuclear energy company Energoatom-through shell companies and fake contracts into the construction of a luxury residential complex (known as “Dynasty”) in the affluent village of Kozyn, south of Kyiv.

The broader “Midas” investigation into Energoatom reportedly uncovered a pattern where contractors paid 10-15% kickbacks to officials to secure or maintain deals. Funds were allegedly laundered between 2021 and 2025 via elite real estate development.

Yermak faces charges under Part 3 of Article 209 of Ukraine’s Criminal Code (legalization of criminally obtained proceeds). A conviction could carry up to 12 years in prison.

After multi-day hearings, the High Anti-Corruption Court (HACC) imposed 60 days of pre-trial detention starting May 14, with an alternative of bail set at 140 million hryvnias (roughly $3.2 million). Prosecutors had requested a higher bail of 180 million hryvnias (about $4 million).

Yermak was remanded in custody immediately, though he could secure release if the full bail is posted while the case proceeds. His legal team plans to appeal the ruling.

Yermak’s Response

Yermak has strongly denied all allegations, calling them “groundless” and “baseless.” He stated he owns only one apartment and one car, and has no involvement in the luxury development.

After the hearing, he told reporters: “I don’t have that kind of money, and my lawyer will now work with friends and acquaintances [to raise the money for bail].” He added that he respects the court, has “nothing to hide,” and is proud of his service to Ukraine during the war. He mentioned visiting the front lines weekly and receiving international support, though he said he would not use it to influence the judiciary.

His defense argues the case lacks merit and may carry political undertones.

Background and Political Impact

Yermak rose from a film producer and diplomat to become Zelenskyy’s chief of staff, wielding immense influence over policy, appointments, judiciary, and even early peace negotiations with Russia before the full-scale invasion. Critics accused him of consolidating power and sidelining longtime allies of the president.

He resigned in November 2025 after NABU raids on his properties linked to the wider Energoatom probe. Zelenskyy has not been implicated, and anti-corruption officials have stressed the president is not a subject of the investigation.

It is no wonder Democrats just love corrupt Ukraine. pic.twitter.com/wqKy6PjzWp

— Marcus Notrealius (@TheLieKeeper) May 14, 2026

The case comes as Ukraine faces intense pressure to combat high-level graft to advance EU membership and sustain Western support amid the ongoing war with Russia. It has sent shockwaves through Kyiv’s political elite and fueled public frustration over wartime corruption.

This remains a developing story. The investigation is ongoing, with potential for more suspects and revelations as the case moves forward.

Tyler Durden

Thu, 05/14/2026 – 15:00

Biden FBI Quietly Hid Trump Prosecution Files For Potential Post-2028 Case

Biden FBI Quietly Hid Trump Prosecution Files For Potential Post-2028 Case

Authored by Luis Cornelio via Headline USA,

Another trove of newly unearthed Biden-era files suggest that the FBI attempted to retain purported evidence related to its prosecution of President Donald Trump until 2030 — when he would presumably be out of office.

The documents, reported Tuesday by Just the News, add to a growing body of records that have detailed the breadth of the aggressive actions targeting Trump, Republican lawmakers and conservative organizations connected to the 2020 election.

According to the report, the retention effort came as part of a broader push to preserve materials gathered by then-Special Counsel Jack Smith following the dismissal of related cases. Such materials are typically handled under DOJ procedures once a case is closed.

The documents in question were reportedly created in 2025, as Trump was preparing to return to office in January, and relate to investigations tied to the certification of the 2020 presidential election.

The decision to retain the evidence has raised questions about whether federal officials were preserving the option to revisit the case after Trump leaves office, when DOJ rules barring the prosecution of a sitting president would no longer apply.

The case itself was closed without prejudice, meaning it could be refiled at a later date.

As reported by Just the News:

“One of the key ‘Case Closing’ documents obtained by Just the News – originating from the FBI’s Washington Field Office’s CR-15 team – was dated a couple of weeks into Trump’s second term, on February 5, 2025, when many holdover FBI agents and leaders were still in place.

The newly-released closing document from early 2025 repeated the extensive claims of criminality against Trump, which had been pursued by Smith and the bureau, and it sought to retain all of the evidence for a half decade until at least February 2030, when Trump would be a former president once more and thus when the DOJ guidance prohibiting the prosecution of a sitting president would no longer be in force.”

According to the outlet, the document — titled “Arctic Frost – Election Law Matters – Sensitive Investigative Matter” — included supporting materials such as a “Deputy Special Counsel Concurrence” and the “Retention of Evidence Approval.”

In response to the findings, FBI Director Kash Patel said he had moved to eliminate the office involved in handling the matter.

“The American people deserve to know how this egregious weaponization of power to target political opponents and President Trump happened inside an institution meant to protect them,” Patel told Just the News.

“We shut down the weaponized CR-15 squad, and we are going to keep following the facts until there is full accountability. The FBI exists to protect the country, not to preserve political prosecutions for a future administration.”

Tyler Durden

Thu, 05/14/2026 – 14:40

With GOP Help, House Dems Force Vote To Give Another $1.3 Billion To Ukraine

With GOP Help, House Dems Force Vote To Give Another $1.3 Billion To Ukraine

In a rebellion defying the priorities of Speaker Mike Johnson, House Democrats have teamed up with two Republicans and an independent in a parliamentary maneuver that will force a vote on a bill that would give another $1.3 billion in military aid and other assistance to Ukraine, as that country continues to lose territory in its war with Russia.

“We look forward to seeing the House pass this bill quickly and encourage the Senate to take it up without delay. The brave men and women of Ukraine are waiting,” said NY Rep. Gregory Meeks, ranking member of the House Foreign Affairs Committee and the author of the bill.

A view, by Zelensky’s former press secretary whose interview went out on Tucker Carlson show last night. https://t.co/kkKP5HxnCQ

— Leonid Ragozin (@leonidragozin) May 12, 2026

All 215 House Democrats signed a discharge petition, a means by which representatives can bypass House leadership’s agenda-setting role and compel a vote on a bill. Seldom used over House history, discharge petitions are showing their potency in a House ruled by a narrow majority, as is the case today. Most famously, Republican Rep. Thomas Massie and Democratic Rep. Ro Khanna used the maneuver last year to compel a vote on forcing the release of the Epstein investigation files. For this Ukraine bill, the Democrats were joined by two Republicans — Pennsylvania Rep. Brian Fitzpatrick and Nebraska Rep. Don Bacon — along with California independent Kevin Kiley, who earlier this year left the GOP.

Kiley’s signature on the petition pushed to the required 218. “Recent Ukrainian gains have created an opportunity for peace, but the collapse of the recent ceasefire shows that leverage is needed for diplomacy to succeed,” he said in a statement. That will force Johnson to bring a vote to the floor on the Ukraine Support Act, which has three major thrusts:

Reaffirming US support for both Ukraine and NATO, and enacting measures for Ukraine’s reconstruction

$1.3 billion in aid and — get this — up to $8 billion more in direct loans that could prove to be LINOs — loans in name only

More sanctions and export controls on Russia, targeting officials, financial institutions, and the oil and mining sectors

The yellow area shows the last part of the Donetsk oblast that Russia has yet to seize control of. The Luhansk oblast is to the northeast, while the next two oblasts moving southwest are Zaporizhzhia and Kherson, with Crimea at the southernmost end (via Russia Matters)

Though the House may pass the bill, the push to give more money to Ukraine will face an uphill climb in the Senate. The discharge-petition development comes as Ukraine and Russia moved on from a brief ceasefire and resumed blasting each other, though — for now — at a reduced tempo. Russia has continued to make gradual progress in taking control of both the Luhansk and Donetsk “oblasts” which together comprise the Donbas region of Eastern Ukraine. Moscow is insisting that Ukraine’s ceding of the last parts of the Donbas is a precondition to resumed peace talks.

Not accounting for another potential $1.3 billion thrown into the Ukraine war — to say nothing of the money pit that is the US-Israeli war on Iran — the US government was in February projected to post a fiscal-year 2026 deficit of $1.9 trillion. Not that anyone in Washington cares.

Tyler Durden

Thu, 05/14/2026 – 14:20

Separate Peace? Saudi Arabia Floats Regional Non-Aggression Pact With Iran

Separate Peace? Saudi Arabia Floats Regional Non-Aggression Pact With Iran

Are regional Gulf countries seeking to forge there own separate peace deals with Iran, apart from the United States? That’s what fresh Thursday reporting in the Financial Times suggests.

The report says Saudi Arabia is supposedly considering a non-aggression pact between the Middle East states and Iran after the military conflict between the United States and Iran ends, the FT indicates.

Citing diplomatic sources, it describes that Riyadh is assessing a model of the Helsinki Process, which helped reduce tensions in Europe during the Cold War, and created an uneasy East-West peace in post-WW2 Europe.

The driving rationale behind the potential diplomatic framework is that while Iran is “weakened,” the reality is that it still “poses a threat to its neighbors.“

An Arab diplomat cited by FT said that a non-aggression pact modelled along the lines of the Helsinki process is something likely to be embraced by most Arab and Muslim states, as well as by Iranian leader.

“It all depends on who is in it – in the current climate, you are not going to be able to get Iran and Israel… Without Israel, it could be counterproductive because after Iran, they are seen as the biggest source of conflict. But Iran is not going anywhere, and this is why the Saudis are pushing it,” the source stated.

The Abraham Accords have theoretically attempted to build a normalization and non-aggression foundation involving Arab states and Israel, but other countries and populations in the region are suspicious of it for the very fact that it is seen fundamentally as a pro-US and pro-Israeli axis of alignment.

As for for Tehran and Riyadh, they recently have experience with direct, good faith talks, given that it was only in 2023 that China made history when it brokered a landmark normalization deal between Iran and Saudi Arabia – after which mutual embassies opened and went into operation.

This week, Reuters and other sources revealed for the first time that at the height of Trump’s Operation Epic Fury which began in late February and endured through March into early April, the UAE directly fired back on Iran as it was under attack by drones and missiles. Also interesting is the fresh revelation that Israeli PM Benjamin Netanyahu made a secret visit to the UAE as the Iran war was in full swing – though UAE has officially denied it, perhaps not wanting to inflame Arab public sentiment.

Kuwait also reportedly directly attacked Iranian interests, and additionally the Saudis attacked Shia Iraqi militias seen as cooperating with Iran.

Highways, railroads and ports in Saudi Arabia, the U.A.E. and Oman have been transformed into an emergency logistics lifeline during the Iran war, bypassing the Strait of Hormuz

With talks between the U.S. and Iran deadlocked, the conflict has devolved into an economic war of… pic.twitter.com/bgnzBmGc6g

— Joshua Landis (@joshua_landis) May 13, 2026

Interestingly, US intelligence and the governments involved kept this under wraps for many weeks, and it suggests just how close the world was to witnessing a broader regional war that could have quickly spun out of control. Before the series of disclosures, it was widely assumed that only the United States military was ‘defending’ the UAE, Kuwait, Qatar, Saudi Arabia, and Bahrain. But clearly some of these countries were hitting back against the Islamic Republic on their own.

Tyler Durden

Thu, 05/14/2026 – 13:40

Did You See Hakeem Jeffries’ Press Conference Tantrum?

Did You See Hakeem Jeffries’ Press Conference Tantrum?

Authored by Matt Margolis via PJMedia.com,

House Minority Leader Hakeem Jeffries is having a rough time right now. For months, the Speaker’s gavel looked to be easily within his reach come November, but recent developments have made it look like it could slip away.

He’s a little touchy about it. During a press conference on Wednesday, Jeffries had a bit of a tantrum, not only invoking the Confederacy but snapping at a CNN reporter who dared to ask him a question.

Last month, the Supreme Court issued a 6-3 ruling in Louisiana v. Callais, striking down Louisiana’s congressional map as an unconstitutional racial gerrymander. The ruling opened the door for several red states to redistrict and eliminate race-based districts.

To say Jeffries isn’t taking it well is an understatement.

“Because we know this unprecedented assault on black political representation, the likes of which we have not seen since the Jim Crow era, the ghost of the Confederacy has afflicted the United States Supreme Court majority and is invading and haunting the nation right now,” Jeffries said.

“And we take that seriously. And we know it’s going to continue, which is why Democrats are committed to launching a decisive and overwhelming response in advance of the 2028 election, to ensure that it’s the American people who are the ones who get to decide who’s in the majority in the House, who’s in the majority in the Senate, and ultimately in 2028, who gets elected as the next president of the United States of America.”

But it was his exchange with CNN’s Manu Raju that got genuinely uncomfortable. Raju pressed Jeffries on Democrats’ failed attempt to gerrymander Virginia’s congressional maps when the Supreme Court of Virginia ruled that the process Democrats used to eliminate four GOP-leaning districts violated the state constitution, invalidating that map as well. Groups aligned with Jeffries had spent over $40 million on the failed effort.

“Mr. Leader, I mean, you ultimately lost this. Do you take personally—” Raju began.

“Who lost?” Jeffries shot back, clearly angry.

“You lost in court—”

“Who lost?”

“Democrats did,” Raju said.

“Do you take personal responsibility for investing so much time and resources, tens of millions of dollars, in an ultimately fruitless effort?”

“We did the right thing,” Jeffries said, “and this effort is not over.”

Hakeem Jeffries loses it when called out for his unconstitutional racist gerrymandering scheme.

JEFFRIES: Who lost?

RAJU: YOU LOST! In court.

JEFFRIES: Did the voters lose?

RAJU: The Democrats did. Do you take personal responsibility for an ultimately foolish effort? pic.twitter.com/2ryGiBVnjP

— RNC Research (@RNCResearch) May 13, 2026

As you can see, Jeffries got a bit undignified there, trying to distance himself from the failed effort that the Democratic Party wasted tens of millions of dollars on. On top of that, multiple red states are now redrawing House districts in the wake of Callais. While some are moving aggressively, others are stalled by legal challenges and political calculations.

Sabato’s Crystal Ball now gives Republicans a slight edge in Safe/Likely/Leans seats, and prediction markets now show the GOP favored to retain the Senate while closing the gap in the House race.

The overall trajectory is clear — and it’s not favorable for Democrats.

The problem for Democrats, of course, isn’t just the short-term implications but the long-term structural problem they face. The 2026 midterms and the 2028 presidential election may be their last chance to win back power before the math and the map become too big a hurdle for them to overcome. Population shifts mean blue states will lose congressional seats after the 2030 census, costing them Electoral College votes as well.

In other words, Jeffries is in full panic mode, and he’s having a hard time hiding it.

Tyler Durden

Thu, 05/14/2026 – 13:20

https://www.zerohedge.com/political/did-you-see-hakeem-jeffries-press-conference-tantrum

Trucking Stocks Tumble As Supreme Court Ruling Risks “Extinction Event” For Freight Brokers

Trucking Stocks Tumble As Supreme Court Ruling Risks “Extinction Event” For Freight Brokers

The US Supreme Court ruled late Thursday morning that freight brokers can face state-law negligent hiring claims when they hire unsafe trucking firms that later cause crashes.

FreightWaves founder Craig Fuller responded to the ruling on X, saying,

OMG, this is the most pivotal moment in trucking history since Deregulation. It could be an extinction event for 30-50% of all freight brokers.

OMG, this is the most pivotal moment in trucking history since Deregulation.

It could be an extinction event for 30-50% of all freight brokers.

Matt Lefler and I will be on the air at 11AM ET to discuss. Live, streaming on X. https://t.co/sc3eKgWV3S

— Craig Fuller 🛩🚛🚂⚓️ (@FreightAlley) May 14, 2026

In other words, this decision will raise liability costs across the freight industry but could force out unsafe trucking firms, some of which have hired illegals.

Landmark win for trucking safety this morning.

The Supreme Court rules UNANIMOUSLY against the broker that helped put the illegal alien who hit Dalilah Coleman on the road.

As a result of this decision, trucking brokers can be liable for negligently giving loads to illegal… https://t.co/0pYntFxiDx

— Senator Jim Banks (@SenatorBanks) May 14, 2026

The case, Shawn Montgomery v. Caribe Transport II, US, No. 24-1238, centers on C.H. Robinson, which arranged a shipment carried by Caribe Transport II. The carrier’s driver struck Shawn Montgomery’s tractor-trailer in Illinois, causing severe and permanent injuries. Montgomery alleged that C.H. Robinson should have known Caribe posed safety risks given its poor federal safety rating.

Justice Amy Coney Barrett, writing for the High Court, said the Federal Aviation Administration Authorization Act does not shield brokers from such claims because states retain authority over safety “with respect to motor vehicles.” The ruling reverses the Seventh Circuit and sends the case back for further proceedings.

Justice Brett Kavanaugh, joined by Justice Samuel Alito, said the case was close but agreed that Congress did not intend to leave brokers in a “black hole” with no meaningful safety accountability. He also acknowledged that the ruling could lead to higher litigation, insurance, and due diligence costs, which may ultimately raise shipping costs.

The Trump administration urged the justices to rule against Montgomery’s claim, saying that allowing liability for freight brokers under state tort law would create regulatory nightmares for the nation’s freight transport industry.

Bloomberg litigation analyst Holly Froum noted:

CH Robinson, Landstar, JB Hunt Dealt Costly Supreme Court Ruling

Trucking brokers including CH Robinson, Landstar along with companies with transportation brokering operations like JB Hunt, Werner Enterprises and others were dealt a setback by the US Supreme Court’s May 14 ruling allowing states to impose personal-injury liability for trucking accidents. A majority of the justices found that state law negligent hiring claims could continue and weren’t preempted by federal law, as we expected they would.

Shares of C.H. Robinson and Landstar fell after the ruling, while JB Hunt moved higher.

Trucking advocacy group American Truckers United stated on X, “A bomb has dropped on the criminal freight brokers!”

Tyler Durden

Thu, 05/14/2026 – 12:40

Are Markets F***ed? Collum And Pomboy To Address Everything Bubble

Are Markets F***ed? Collum And Pomboy To Address Everything Bubble

As the S&P continues to reach new highs in the mid 7000s, leaving the COVID era 3000s as a forgotten fevered dream… and AI euphoria fueling increasingly speculative bets across Wall Street and Main Street, the sane among us need to ask the question: when will reality hit?

In tonight’s ZeroHedge debate, hosted by the legendary Dave Collum, Macro Mavens founder Stephanie Pomboy and Michael Lebowitz will break down the most dangerously overvalued sectors of today’s market. From AI to private credit… and debate how, when, and where the unwind may begin.

Nasdaq is up almost 30% since the end of March. Howbowdah?

— Dave Collum (@DavidBCollum) May 13, 2026

The discussion will examine whether the AI boom has become detached from economic reality, whether Nvidia’s 43 PE ratio makes any sense, and whether private credit gating is the canary in the coal mine. With liquidity tightening beneath the surface and credit conditions deteriorating, Collum and the gang will discuss ways to preserve wealth before the cycle turns.

The conversation will also focus heavily on the Federal Reserve’s next chapter under incoming Fed Chair Kevin Warsh, whose prior statements indicate a hawkish stance… but that’s been true of past chairs before they held the helm. Is Warsh a genuine monetary hawk willing to tolerate market pain to restore credibility to the dollar and contain inflation? Or will he ultimately cave under political and financial pressure like Jerome Powell during COVID?

However, let’s not forget that Warsh voted for QE and bailouts and parroted Bernanke’s nonsense during the GFC.

— Michael Lebowitz, CFA (@michaellebowitz) April 21, 2026

For investors trying to position themselves ahead of what could be the next major repricing event, or for those who just want to hear about how horrible the economy really is… join Collum, Pomboy, and Lebowitz this evening.

The debate will stream live on the ZH X account and homepage at 7pm ET. See you there.

Tyler Durden

Thu, 05/14/2026 – 12:20

https://www.zerohedge.com/markets/are-markets-fed-collum-and-pomboy-address-everything-bubble

Bessent Says US, China To Launch AI Safety Talks After Trump-Xi Meeting In Beijing

Bessent Says US, China To Launch AI Safety Talks After Trump-Xi Meeting In Beijing

Authored by Tom Ozimek via The Epoch Times (emphasis ours),

Treasury Secretary Scott Bessent said on May 14 that Washington and Beijing would begin formal discussions on artificial intelligence (AI) safety protocols following meetings between U.S. President Donald Trump and Chinese leader Xi Jinping in Beijing. Bessent’s comments come as the rival powers sought to stabilize ties strained by trade disputes, the Iran conflict, and AI competition.

Speaking to CNBC from the sidelines of the Trump–Xi summit, Bessent said the United States and China—which he described as the world’s “two AI superpowers”—were preparing to establish a framework on AI best practices and safeguards aimed at preventing advanced models from falling into the wrong hands.

“The two AI superpowers are going to start talking,” Bessent said.

“We’re gonna set up a protocol in terms of how do we go forward with best practices for AI to make sure non-state actors don’t get a hold of these models.”

Bessent said the United States would seek to embed “U.S. values” and American-led best practices into emerging global AI standards, adding that Washington was engaging Beijing from a position of technological strength.

“The reason we are able to have fulsome discussions with the Chinese on AI is because we are in the lead,” he said. “I do not think we would be having the same discussions if they were this far ahead of us.”

The remarks came as Trump and Xi concluded the first major round of meetings during Trump’s two-day visit to Beijing, his first trip to China since returning to office for a second term.

In a White House readout issued after the meeting, Washington said the leaders discussed expanding economic cooperation, increasing Chinese investment in the United States while expanding market access for American businesses into China, boosting Chinese purchases of U.S. agricultural products, and maintaining freedom of navigation through the Strait of Hormuz.

A subsequent White House readout said both countries agreed that the Strait of Hormuz must remain open to “support the free flow of energy.” The strait is a key maritime chokepoint that normally handles around one-fifth of global energy shipments but has been heavily restricted by Iran amid its war with the United States and Israel.

The readout noted that Xi expressed Beijing’s opposition to the militarization of the strait or to Iran charging tolls for use of the critical waterway. Both countries also agreed that Iran “can never have a nuclear weapon.”

AI, Chips, and Investment Talks

AI and semiconductor policy were among the issues discussed at the summit, Bessent told CNBC, with the U.S. delegation’s visit set against a backdrop of intensifying competition between Washington and Beijing over advanced computing technologies with military and economic applications.

Bessent said he expected a major “step-function jump” in upcoming AI model releases from Google and OpenAI. He also addressed the ongoing debate over potential U.S. approvals for Nvidia’s sales of advanced AI chips to Chinese companies.

When asked about reports that Washington had cleared sales of Nvidia’s H200 AI chips to several major Chinese technology companies, Bessent said there had been “a lot of back and forth” on the issue but did not indicate that any finalized agreement had been struck.

Nvidia Chief Executive Jensen Huang joined Trump’s delegation to China alongside a large group of U.S. corporate executives, including leaders from Tesla, Apple, BlackRock, Boeing, and Qualcomm.

The H200 chip, part of Nvidia’s Hopper line of AI processors, is significantly more powerful than the export-restricted H20 chip previously designed for the Chinese market. Critics in Washington have argued that allowing Beijing access to such advanced chips could accelerate China’s military modernization and narrow the U.S. advantage in AI.

“The H200 is one of the most advanced AI chips on the market, and it is currently used to produce frontier AI systems with military applications,” a group of U.S. lawmakers wrote in a December 2025 letter expressing concern about the Trump administration’s decision to permit H200 sales to China, arguing that it “undercuts” national security.

At the same time, administration officials and some technology advisers have argued that controlled sales could preserve U.S. technological dominance while generating revenue for U.S. companies and taxpayers.

“This policy will support American Jobs, strengthen U.S. Manufacturing, and benefit American Taxpayers,” Trump wrote in a December 2025 social media post, noting that sales of the H200 would only go to “approved customers in China.”

David Sacks, chair of the president’s Council of Advisors on Science and Technology, said at the time that he believes sales of the H200 would discourage competitors such as Chinese company Huawei.

Chris McGuire, senior fellow for China and emerging technologies at the Council on Foreign Relations, said in an analysis that H200s could give China’s AI computing power trajectory a threefold boost.

Catherine Yang, Owen Evans, and Troy Myers contributed to this report.

Tyler Durden

Thu, 05/14/2026 – 12:00

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}