Category: News

Hudson River NJ-NY Rail Tunnel Faces New Halt Without Federal Funds

Hudson River NJ-NY Rail Tunnel Faces New Halt Without Federal Funds

Construction on the planned $16 billion rail tunnel under the Hudson River could halt again within two to three months unless federal funding resumes, the project’s developer warned last week, according to Bloomberg.

The project, led by the Gateway Development Commission, would build a new rail tunnel linking New Jersey and Manhattan for Amtrak and New Jersey Transit trains. It would also allow rehabilitation of the existing tunnel, which opened in 1910 and is in urgent need of repairs. Gateway says the broader project would expand rail capacity between the two states and generate about $19.6 billion in economic activity.

Funding for the project has been in dispute for months. The US Department of Transportation has withheld funds since October, prompting Gateway to sue last month to force the release of the money. New York and New Jersey filed a similar lawsuit.

Bloomberg writes that some payments resumed after a federal judge ordered the Trump administration to release reimbursement funds the agency had requested. Since the ruling last month, Gateway has received about $254 million. The federal government had suspended payments while reviewing whether the project complied with a new administration policy banning contracting requirements tied to race or gender.

Still, Gateway officials say the funding interruptions threaten construction progress. A previous stoppage between Feb. 6 and Feb. 22 temporarily laid off about 1,000 construction workers and added “million of dollars in additional costs,” Gateway chief financial officer Pat McCoy said in a court filing.

“We will have no choice but to stop work again if the federal government does not continue to disburse the funds that are committed to the project,” Gateway Chief Executive Officer Tom Prendergast said in a statement Tuesday. “This project is too important to delay. That’s why we’re doing everything possible to regain consistent and predictable access to all our federal funding so we can keep our workers on the job and deliver the reliable, modern rail transit Americans deserve.”

Congress has already approved funding for the project, including $11 billion in federal support and $4 billion in loans to be repaid by New York, New Jersey and the Port Authority of New York and New Jersey. Amtrak is expected to contribute another $1 billion.

Tyler Durden

Wed, 03/11/2026 – 21:25

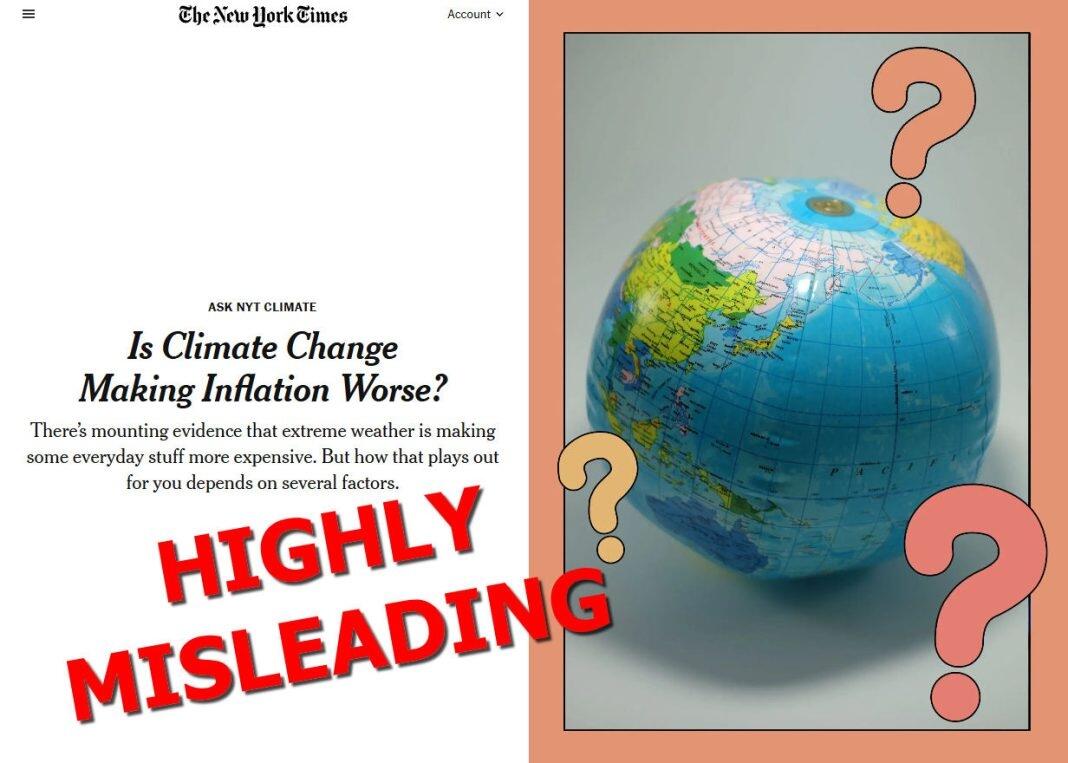

No, New York Times, Climate Change Isn’t Driving Inflation

No, New York Times, Climate Change Isn’t Driving Inflation

Authored by Anthony Watts via ClimateRealism.com,

In The New York Times (NYT) article “Is Climate Change Making Inflation Worse?,” writer Lydia DePillis suggests that extreme weather linked to global warming is quietly raising the price of everyday goods like food, electricity, and insurance.

The framing is, at best, misleading and, at worst, flat-out false. Inflation is a monetary phenomenon driven by fiscal policy, central banking decisions, supply-chain disruptions, and energy policy choices — there is no evidence climate change has altered in a way that impacts any of those factors. The NYT erroneously substitutes weather anecdotes and speculative projections for demonstrated economic causation. However, since instances of extreme weather haven’t become more frequent or severe in recent decades, climate change can’t be causing “inflationary” impacts.

The NYT opens by asserting that there is “mounting evidence that extreme weather is making some everyday stuff more expensive.” That claim is presented as a settled fact. It’s not. The Intergovernmental Panel on Climate Change (IPCC) Sixth Assessment Report (AR6) assigns low confidence to global increases in most types of extreme weather and emphasizes regional variability. The IPCC AR6 does not claim that extreme weather trends are uniformly intensifying in a way that would systematically impact global inflation.

The NYT then turns to food prices, citing drought in Eastern Europe and China, coffee impacts in Brazil, and ranchers culling cattle. Agricultural output, however, fluctuates every year due to natural variability. Long-term production data in the U.N. Food and Agriculture Organization’s FAOSTAT database, shown in the figure below, illustrate that global grain production has generally trended upward, amid modest warming and the recent claims of the “three hottest years ever” from 2022 to 2025.

Commodity markets automatically adjust; when one region underperforms, trade reallocates supply. The NYT acknowledges that tariffs and export controls can amplify price spikes. That is policy-driven inflation, not climate-driven inflation.

When discussing energy, the article points to grid repairs and increased electricity demand during heat waves. U.S. electricity prices have risen sharply in recent years, but that’s not due to a changing climate but rather is primarily due to fuel mix changes, regulatory mandates, and grid reliability challenges tied to rapid renewables integration driven by climate policies. It’s not climate change, but climate policies that have driven higher energy prices. Historical pricing data available through the U.S. Energy Information Administration (EIA) electricity database show that price increases correlate more closely with political decisions that cause fuel supply volatility and shifts to expensive, intermittent, wind, solar, and battery storage power rather than with long-term temperature trends.

The NYT also cites a study projecting that weather-related disruptions could raise electricity infrastructure costs by as much as 25 percent toward the end of the century. That is a modeling projection, not an observed cost trend. The United States has already experienced roughly 1°C of warming since the late nineteenth century, yet official inflation tracking in the Bureau of Labor Statistics (BLS) Consumer Price Index database attributes recent inflation primarily to pandemic-era stimulus, supply chain disruptions, and energy price shocks, not temperature changes.

The article presents insurance costs as the clearest climate-related inflation driver. But insurance markets respond more to litigation environments, construction costs, regulatory frameworks, and development patterns in high-risk areas. Long-term normalized hurricane damage trends discussed at Climate at a Glance Hurricanes show no upward trajectory after population growth and coastal development are accounted for. The same is true for rising wildfire costs. They are due to shifting policies on public lands and increased development in areas historically prone to wildfires, not significant changes in the climate in those regions. Indeed, acreage lost to wildfires has declined significantly over the past two decades. Rising premiums reflect higher rebuilding costs and denser development in vulnerable zones, not necessarily stronger storms.

The article pegs global warming’s impact at “between $400 and $900 per person annually,” but concedes the wide range stems from difficulty separating weather variability from climate change. That uncertainty is not incidental, it is central. Without a clear attribution chain linking long-term warming trends to persistent price acceleration in specific sectors, the NYT claim remains purely speculative; it’s not just that there is no causal link, there isn’t even a correlation between experienced weather trends and inflation related price increases.

The NYT further notes that U.S. commodity crops like corn, soybeans, wheat, and rice “have been less affected by shifting weather patterns.” Those crops form the backbone of global calorie supply. If staple production remains broadly stable, sweeping claims about climate-driven food inflation collapse.

Finally, the article cites mitigation policies, such as emissions trading systems and regulatory mandates, as contributors to rising prices. That is not climate inflation. That is climate policy inflation. When governments impose carbon pricing, trade barriers, or compliance costs, consumers pay more by design. Conflating the cost of political decisions supposedly designed to fight climate change with the cost of climate change itself obscures the true driver.

Inflation over the past five years has been historically elevated across advanced economies, driven primarily by unprecedented fiscal stimulus, monetary expansion, pandemic supply disruptions, and geopolitical energy shocks. None of those are climate variables. Economic research consistently identifies monetary policy as the dominant long-term determinant of inflation.

Weather variability can affect specific commodity prices in specific years. That has always been true. Droughts affected grain markets in the 1930s. Hurricanes disrupted supply chains in the twentieth century, yet sustained inflation requires sustained monetary imbalance.

The New York Times frames climate change as an emerging inflationary force poised to accelerate, but observational economic record refutes any such economy-wide climate-driven inflation trend. Weather anecdotes, modeling projections, and policy cost provide no proof of climate-driven inflation. Inflation is fundamentally a monetary and policy phenomenon. Blaming it on the weather may make compelling click-bait copy, but it does not withstand economic scrutiny.

Tyler Durden

Wed, 03/11/2026 – 21:00

https://www.zerohedge.com/economics/no-new-york-times-climate-change-isnt-driving-inflation

Watch: The Moment LA Street Mob Storms Luxury Apartments

Watch: The Moment LA Street Mob Storms Luxury Apartments

A group linked to a late-night street takeover forced its way into a luxury downtown Los Angeles apartment tower early Sunday, fighting with staff and leaving shattered glass and overturned furniture behind, according to police and video of the incident, according to the NY Post.

The disturbance happened around 3 a.m. at the Circa LA Apartments on South Figueroa Street, the Los Angeles Police Department said.

Authorities told KTLA that a crowd involved in a nearby street takeover moved toward the upscale high-rise and began vandalizing the property.

Video shows a large group gathering outside the building before targeting the lobby. One person is seen throwing an object at a suited employee who appeared to be working near the front desk. The worker initially stood outside but retreated inside as other staff gathered in the lobby.

The crowd soon forced its way into the building. Outside, several people smashed glass doors and windows, while one individual used a metal barricade to ram the entrance.

The Post writes that once inside, members of the group knocked over furniture and ran through the lobby as the scene descended into chaos. At one point, a person appeared to grab a box from the front desk while others rummaged through it before the group dispersed as sirens approached.

Police said the building sustained exterior damage, including broken doors and windows. No injuries were reported, and no victims filed a report with authorities, though video shows at least one punch being thrown. It was not immediately clear whether any arrests had been made.

Tyler Durden

Wed, 03/11/2026 – 20:35

https://www.zerohedge.com/markets/watch-moment-la-street-mob-storms-luxury-apartments

Years After The Pandemic, Younger Students Still Have Far To Go In Reading, Report Says

Years After The Pandemic, Younger Students Still Have Far To Go In Reading, Report Says

Authored by Aaron Gifford via The Epoch Times,

Reading levels in early elementary school grades have remained fairly stagnant since the COVID-19 pandemic, a national education assessment and research organization revealed this week.

A new policy brief from NWEA, formerly the Northwest Evaluation Association, says first- and second-grade reading achievement “remains stalled with little rebounding,” while math achievement in those grades showed modest recovery since 2021, and kindergarten levels in both subject areas have remained mostly steady.

The findings were pulled from NWEA’s ongoing analysis of K-8 students across 30,000 schools dating back to 2017.

For reading, these early grade patterns closely resemble those recently observed in grades 3-8. Current first- and second graders were “day-care age” during the most disruptive periods of the pandemic in 2020 and 2021, yet their achievement mirrors that of older students who experienced those disruptions earlier in their elementary school careers. This suggests broader, longer-lasting system challenges, as opposed to interruptions to a single cohort, said Megan Kuhfeld, NWEA’s data analytics director.

“It is important that we understand the depth and persistence of unfinished learning from the pandemic’s disruptions, but we must also focus on our lens beyond the COVID-19 years,” she said in a news release. “While these youngest elementary students were just infants and toddlers when COVID-19 hit, this stagnation in reading and uneven recovery in math is an indicator of something bigger impacting our education system that extends beyond one cohort or a moment in time.”

The report also notes that while first- and second-grade math scores have steadily improved since 2022, overall achievement remains below pre-pandemic levels. Additionally, gaps have narrowed across various student groups, including those from low-income households, blacks, and Hispanics.

The National Assessment of Educational Progress reports list average state assessment scores in reading and math by grade level and note percentages that are below or above basic and proficiency levels. NWEA’s reports for early grade levels, by contrast, show numbers on a chart that indicate a standardized difference in mean achievement compared to 2019, the pre-COVID reference year. For reading, the 2025 number was -0.13 for second grade, and -0.11 for first. For math, the numbers were -0.15 and -0.05, respectively, but both were still an improvement from 2021.

The math and reading scores for kindergarten achievement both showed positive numbers that were higher than 2019 levels.

NWEA suggests that school leaders should review staffing levels and instructional materials as they consider improvement plans.

In another recent report, NWEA found that only one-third of American K-12 schools have returned to pre-COVID pandemic achievement levels in math or reading.

Standardized tests in every state will take place before March 20. This year’s assessments include math and reading for grades four and eight, and a U.S. history and civics exam for grade eight.

The 2026 reading and math results will be released in early 2027. The U.S. history and civics results will follow, with a summer 2027 release date expected.

Tyler Durden

Wed, 03/11/2026 – 20:10

Years After The Pandemic, Younger Students Still Have Far To Go In Reading, Report Says

Years After The Pandemic, Younger Students Still Have Far To Go In Reading, Report Says

Authored by Aaron Gifford via The Epoch Times,

Reading levels in early elementary school grades have remained fairly stagnant since the COVID-19 pandemic, a national education assessment and research organization revealed this week.

A new policy brief from NWEA, formerly the Northwest Evaluation Association, says first- and second-grade reading achievement “remains stalled with little rebounding,” while math achievement in those grades showed modest recovery since 2021, and kindergarten levels in both subject areas have remained mostly steady.

The findings were pulled from NWEA’s ongoing analysis of K-8 students across 30,000 schools dating back to 2017.

For reading, these early grade patterns closely resemble those recently observed in grades 3-8. Current first- and second graders were “day-care age” during the most disruptive periods of the pandemic in 2020 and 2021, yet their achievement mirrors that of older students who experienced those disruptions earlier in their elementary school careers. This suggests broader, longer-lasting system challenges, as opposed to interruptions to a single cohort, said Megan Kuhfeld, NWEA’s data analytics director.

“It is important that we understand the depth and persistence of unfinished learning from the pandemic’s disruptions, but we must also focus on our lens beyond the COVID-19 years,” she said in a news release. “While these youngest elementary students were just infants and toddlers when COVID-19 hit, this stagnation in reading and uneven recovery in math is an indicator of something bigger impacting our education system that extends beyond one cohort or a moment in time.”

The report also notes that while first- and second-grade math scores have steadily improved since 2022, overall achievement remains below pre-pandemic levels. Additionally, gaps have narrowed across various student groups, including those from low-income households, blacks, and Hispanics.

The National Assessment of Educational Progress reports list average state assessment scores in reading and math by grade level and note percentages that are below or above basic and proficiency levels. NWEA’s reports for early grade levels, by contrast, show numbers on a chart that indicate a standardized difference in mean achievement compared to 2019, the pre-COVID reference year. For reading, the 2025 number was -0.13 for second grade, and -0.11 for first. For math, the numbers were -0.15 and -0.05, respectively, but both were still an improvement from 2021.

The math and reading scores for kindergarten achievement both showed positive numbers that were higher than 2019 levels.

NWEA suggests that school leaders should review staffing levels and instructional materials as they consider improvement plans.

In another recent report, NWEA found that only one-third of American K-12 schools have returned to pre-COVID pandemic achievement levels in math or reading.

Standardized tests in every state will take place before March 20. This year’s assessments include math and reading for grades four and eight, and a U.S. history and civics exam for grade eight.

The 2026 reading and math results will be released in early 2027. The U.S. history and civics results will follow, with a summer 2027 release date expected.

Tyler Durden

Wed, 03/11/2026 – 20:10

February Snapshot Of The Global Nuclear Industry

February Snapshot Of The Global Nuclear Industry

While February saw continued volatility with uranium spot prices after they pulled back from barely breaking into the triple digit range in January, the other metric that remains flat as a board is the number of reactors currently under construction in the U.S. which stands at a solid zero. Reflected against the backdrop of China, as they added one additional reactor for a total of 39 under construction, the frustration for actually launching a nuclear renaissance intensifies for everyone.

In the last month, China started construction on 1 additional nuclear reactor bringing the total to 39. https://t.co/O8lrhcvJJv pic.twitter.com/BXffiftGqN

— zerohedge (@zerohedge) March 10, 2026

TerraPower did recently receive their construction permit for deploying a Natrium reactor in Wyoming, but it will potentially take months for them to meet the actual requirement of getting added to the board. The U.S. should look forward to joining the prestigious ranks alongside Iran for having just one reactor under construction.

Just as we stated in our uranium investment thesis published back in December of 2020 and even more recently in December of last year, we expect uranium to remain a solid choice for the nuclear renaissance.

Goldman Sachs analyst Brian Lee provides a recap for the month of February regarding updates across the uranium and nuclear industries.

New reactor progress and announcements

North America

2/13/2026 – Canada – OPG and Port Hope are collaborating to develop up to 10GW of nuclear capacity at the Wesleyville site, potentially powering 10 million homes. The project includes C$5mn in community funding to support regulatory assessments and local job creation.

2/19/2026 – Canada – Bruce Power has completed the construction phase of the Unit 3 Major Component Replacement, replacing key reactor parts to extend its operating life by up to 35 years. With regulatory approval to begin fuel loading, the unit is on track to return to Ontario’s grid ahead of schedule and on budget.

2/20/2026 – United States – Governor of Illinois, JB Pritzker, has issued an executive order to accelerate the deployment of at least 2GW of new nuclear capacity by 2033. This initiative follows the lifting of a long-standing moratorium and aims to support the state’s goal of 100% carbon-free energy by mid-century.

2/27/2026 – United States – Vistra Corp has secured landmark 20-year PPA with Amazon Web Services and Meta to provide over 3,800 MW of nuclear energy, supporting the long-term relicensing and uprating of its plants through the 2050s and 2060s. While initial power delivery is set to begin in 2026, the planned capacity uprates at the Perry, Davis-Besse, and Beaver Valley facilities are expected to come online between 2031 and 2034.

Europe

2/5/26 – Hungary – Hungary has officially commenced construction of the Paks II nuclear power plant with the first concrete pour for the foundation of Unit 5. The project, featuring two Russian VVER-1200 reactors, aims to provide approximately 70% of the nation’s electricity demand by the early 2030s.

2/10/2026 – Armenia – Armenia and the United States have finalized a “123 Agreement” for nuclear cooperation, enabling up to $9bn in potential US exports and long-term support for projects such as SMRs. This agreement establishes a framework for American technology to compete with Russian and international offers as Armenia prepares to select a new reactor model by 2026 or 2027.

2/13/2026 – France – France’s latest Multiannual Energy Programme for 2026–2035 puts nuclear at the centre of decarbonisation—seeking to extend existing reactors’ lifetimes, build six new reactors (with an option to decide on eight more), and raise decarbonised electricity output while cutting fossil fuel consumption, alongside renewables.

2/18/2026 – Slovenia – Slovenia has officially initiated the National Spatial Plan for a new reactor unit at the Krško Nuclear Power Plant. Prime Minister Robert Golob announced that a referendum is expected by late 2027 or early 2028, at which point the technology, supplier, and final costs will be defined.

2/23/2026 – Serbia – Serbia and Russia have discussed expanding nuclear energy cooperation, with Rosatom offering a full range of technologies from SMRs to large-scale plants to support Serbia’s energy sovereignty. While Serbia is currently working with France’s EDF on its initial nuclear roadmap, the government aims to establish a national implementation organization by the end of March 2026 to prepare for potential grid connection after 2040.

Asia and other

2/3/2026 – Kazakhstan – Kazakhstan has finalized the selection of the Zhambyl district in the Almaty region for its second nuclear power plant, with the China National Nuclear Corporation (CNNC) appointed to lead the construction. This project, alongside the first plant to be built by a Rosatom-led consortium, is part of a strategic plan to diversify the national energy mix and achieve a 5% nuclear power generation share by 2035.

2/9/2026 – Japan – Tepco has restarted Unit 6 of the Kashiwazaki-Kariwa nuclear power plant, marking the first time a reactor owned by the company has operated since the 2011 Fukushima Daiichi accident. The 1,356 MWe ABWR reached criticality on February 17,2026, and is scheduled to return to commercial operation by March 18,2026.

2/11/2026 – India – India’s indigenous 700 MWe Rajasthan Unit 7 has successfully reached its full operating capacity following its initial grid synchronization. This milestone represents a significant step forward in expanding India’s domestic nuclear power generation and clean energy infrastructure.

2/16/2026 – China – Unit 1 of the San’ao nuclear power plant in Zhejiang, China, reached first criticality on 2/14. This Hualong One reactor is the first of 6 units planned for the site and marks the first instance of private capital investment in a Chinese nuclear project.

2/16/2026 – China – Unit 1 of the Taipingling nuclear power plant has successfully connected to the grid, marking the first of six planned Hualong One reactors to supply electricity in Guangdong province. This 1116 MWe reactor is expected to enter commercial operation in the first half of 2026.

2/16/2026 – India – Tarapur Atomic Power Station Unit-1 (TAPS−1), India’s oldest commercial nuclear reactor, has returned to service following an extensive refurbishment and life-extension program. The 160MWe boiling water reactor reached criticality on December 30,2025, and has now been synchronized to the grid with upgraded safety systems and modernized equipment.

2/19/2026 – Russia – Rostekhnadzor has issued a 10-year operating license for Unit 2 of the Zaporizhzhia Nuclear Power Plant, signaling Russia’s intent to bring the facility under its regulatory framework for future power generation. While all six units remain shut down, Rosatom continues to seek licenses for the remaining reactors, including an active application for Unit 6 and plans for the rest by the end of 2026.

3/2/2026 – India – India has officially started construction on Kaiga units 5 and 6 following the first pour of concrete for the two 700 MMe indigenous reactors. This $1.5bn project uses an innovative “mega EPC” strategy to support India’s goal of reaching 100 GW of nuclear capacity by 2047.

3/4/2026 – Turkiye – Candu Energy and Türkiye Nuclear Energy Company signed an MoU to assess deploying Canadian CANDU reactors in Turkiye, covering technical data exchange, site suitability, and regulatory/licensing needs. The review also examines financing and delivery models, localisation, and workforce development as Turkiye expands its nuclear programme beyond Akkuyu.

3/4/2026 – Philippines – KHNP, Korea Eximbank, and Manila Electric Company signed an MoU to support nuclear power plant development in the Philippines, including feasibility work, site selection, and workforce training. Korea Eximbank will also explore financing packages to help fund projects and support participating Korean firms.

SMR announcement tracker

2/12/2026 – Norway – Norway’s Ministry of Energy has officially established the impact assessment program for Norsk Kjernekraft’s proposed SMR plant in the Taftøy industrial park. This regulatory milestone enables the formal evaluation of environmental and safety factors for the project, which aims to generate ~12.5 TWh of electricity annually.

2/13/2026 – Romania – Nuclearelectrica’s shareholders have approved the FID for Romania’s first SMR plant in Doicești, which will utilize NuScale technology to provide 462 MWe of clean capacity by 2033. The project, estimated to cost between $6bn-$7bn, is now transitioning into a financial structuring and pre-engineering phase to secure investors and finalize supply chain logistics. See our report on the news.

2/17/2026 – Philippines – The USTDA has announced $2.7mn in funding for Meralco PowerGen Corp to evaluate American SMR designs and develop an implementation roadmap for the Philippines’ first nuclear plant. This initiative, supported by the bilateral “123 Agreement,” aims to enhance energy security and establish a qualified nuclear workforce through technical assistance, simulators, and university partnerships.

2/17/2026 – Finland – Steady Energy has begun constructing a full-scale, non-nuclear pilot of its LDR-50 reactor in Helsinki to test operational features and establish supply chains for district heating. The $17mn to $23mn project uses an electric heat source to provide 6 MW of thermal output, paving the way for commercial 50 MW underground nuclear heating plants.

2/23/2026 – United States – Kairos Power and DOE’s Oak Ridge National Laboratory signed a $27mn, five‑year partnership to test and validate Kairos’s fluoride salt‑cooled, TRISO‑fueled reactor technology and support the Hermes demonstration program in Oak Ridge, Tennessee.

2/25/2026 – Poland – GE Vernova Hitachi and Orlen Synthos Green Energy (OSGE) have signed an agreement to develop a standardized technical design for the BWRX-300 SMR tailored to Polish regulations and safety standards. This generic design aims to accelerate the deployment of a planned fleet of 24 reactors across Poland, with the first unit in Włocławek targeted for completion by 2032.

2/25/2026 – UAE – NANO Nuclear Energy and EHC Investment LLC have signed an MoU to explore deploying KRONOS MMRs for industrial and data center use in the UAE. These transportable, 15 MWe reactors provide a water-free, scalable clean energy solution to support the region’s decarbonization and energy resilience goals.

2/27/2026 – Lithuania – Lithuania’s Altra and GE Vernova Hitachi have signed an MoU to evaluate the feasibility of deploying BWRX-300 SMRs to meet the country’s projected energy needs. This assessment supports Lithuania’s goal of reaching climate neutrality by 2050, with a formal decision on SMR installation expected by 2028.

3/3/2026 – Singapore – KHNP and Singapore’s Energy Market Authority (EMA) have signed an MoU to jointly study the feasibility of SMRs for Singapore. This collaboration focuses on technical information sharing and human resource development to support Singapore’s long-term decarbonization and energy security goals.

Global reactor critical updates

In the month of February, there have been few changes to new reactor construction

starts, grid connections, shutdowns, or restarts.

Global reactor construction tracker

Global reactors under construction

China only

Fuel announcements

2/6/2026 – United States – BWXT is finalizing TRISO fuel for Antares Nuclear’s pilot reactor, targeting criticality by July 4, 2026, under a DOE acceleration initiative. The Antares R1 is a transportable, sodium heat pipe-cooled microreactor designed to provide up to 1MWe of scalable, carbon-free power.

2/11/2026 – United States – Solstice Advanced Materials is pursuing an expansion to boost UF6 output at its Metropolis Works plant to over 10,000 tonnes in 2026. The company says debottlenecking and further capacity projects are supported by strong demand and a backlog of more than $2bn.

2/13/2026 – Namibia – Bannerman Energy struck a financing and JV deal with CNNC Overseas for Namibia’s Etango uranium project: Bannerman will hold 55% and CNOL 45% of a JV that owns 95% of Etango, with CNOL investing about $294.5mn (plus up to $27mn reimbursement) and receiving 60% life-of-mine offtake, aiming to enable debt-free construction subject to approvals.

2/16/2026 – United States -The U.S. NRC issued TRISO-X a 40-year special nuclear material licence under 10 CFR Part 70 to commercially fabricate TRISO fuel using HALEU at its Tennessee facilities (TX-1 and TX-2), with operations starting after a final NRC pre-startup inspection. TX-1 is expected to produce about 5 tonnes of uranium (about 700,000 TRISO pebbles) per year.

2/17/2026 – Kazakhstan – Kazatomprom said its 2025 uranium output rose about 10–11% yoy to 67.18mn/lb U3O8 (100% basis), mainly from ramp-up at JV Budenovskoye, and guided 2026 production at 27,500–29,000 tU (100% basis), subject to sulphuric acid availability and consistent with its value-over-volume strategy. For more details on CCJ, please see our earnings takeaways note.

2/20/2026 – Denmark – Copenhagen Atomics signed a non-binding Letter of Intent with Rare Earths Norway to secure future access to thorium from Norway’s Fensfeltet deposit to support its containerised molten salt reactor plans, with a first test reactor expected at the Paul Scherrer Institute and commercial deployment targeted in the early 2030s.

2/24/2026 – United States – Orano submitted an Environmental Report for Project IKE to the NRC, moving the project into the next NRC review phase; Orano noted the licensing process can take up to three years, and low-enriched uranium production is scheduled to begin in 2031.

2/24/2026 – Brazil – INB, ENBPar, and Galvani met Ceará’s governor to align licensing and discuss infrastructure for the Santa Quitéria Project at Fazenda Itataia, targeting about 2,300t/year of uranium concentrate for Angra 1, Angra 2, and future Angra 3; it remains in preliminary environmental licensing with IBAMA, accepted for review in March 2022.

2/25/2026 – Russia – Rosatom says its uranium miners hit 2025 production targets and are expanding their resource base, including new licences and added infrastructure to support new deposits. It also highlighted a Krasnokamensk power-plant modernisation to support mining operations and noted growing non-uranium revenue alongside these plans.

2/25/2026 – Canada – Denison Mines says its Board approved building the Phoenix ISR uranium project at Wheeler River in Saskatchewan, with site prep and construction starting next month and first production targeted for mid-2028. The company says Phoenix could be Canada’s first ISR uranium mine.

2/25/2026 – United States – Deep Fission says it has signed a supply agreement to buy LEU from Urenco USA’s enrichment plant in Eunice, New Mexico, to support testing of its 15MWe underground Gravity SMR and early commercial deployment.

3/2/2026 – India – Cameco will supply India’s Department of Atomic Energy nearly 22mn lbs of U3O8 from 2027–2035 on market-linked pricing, a deal estimated at about C$2.6bn, as India ramps up nuclear capacity and other suppliers (e.g., Kazatomprom) also pursue long-term sales; the contract adds to India’s efforts to secure reliable uranium supply for its planned reactor expansion. Please see our note on the deal.

Uranium pricing and volume trackers

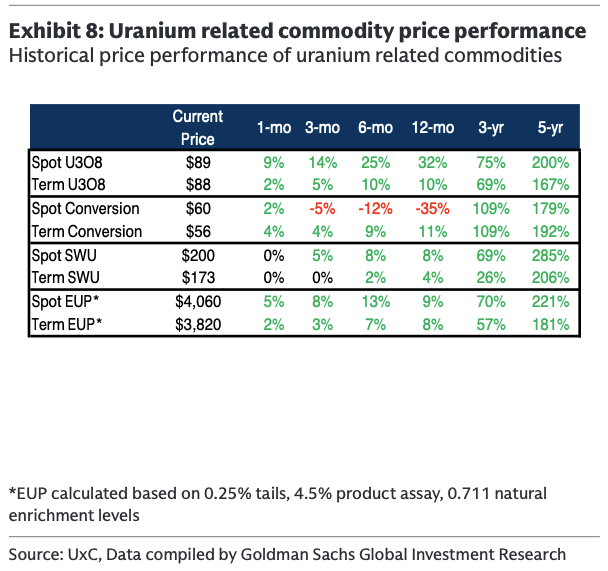

Spot pricing volatile. After a strong start to the year, spot pricing was on a downward trajectory throughout almost all of February. Specifically, spot pricing dropped from ~$94/lb to ~$85/lb in the first week of February, with a slight uptick in the following week with prices climbing back up to ~$90/lb, then followed by a modest decline ever since and currently settling at ~$86/lb. Spot market activity was moderate in the month with a total of 47 transactions involving ~6mn/lbs of uranium, with SPUT being relatively less active this month when compared to the last. Compared to last year, 2026 has started stronger in terms of spot activity.

Term pricing uptick. Term pricing for uranium continued its upward momentum from January, increasing another $2 to reach $90/lb, a level not seen since May 2008. Term market activity remained moderate throughout February, with a total of four utility term contract awards reported: three for uranium (U3O8) and one for conversion services. Additionally, some non-utility mid-term uranium purchases were tracked. Several utilities were actively evaluating offers, including one for nearly 1.2mn/lb of uranium with deliveries starting in 2029, and non-U.S. utilities assessing longer-term requests for uranium and EUP with deliveries extending into the mid-2030s. Offer levels indicated continued upward pressure on term prices, with floor pricing reaching the mid-$70s and ceiling prices pushing into the $125-$130 range, with some even reaching the mid-$150s.

Tyler Durden

Wed, 03/11/2026 – 19:45

https://www.zerohedge.com/markets/goldmans-nuclear-nuggets-february-snapshot-global-nuclear-industry

February Snapshot Of The Global Nuclear Industry

February Snapshot Of The Global Nuclear Industry

While February saw continued volatility with uranium spot prices after they pulled back from barely breaking into the triple digit range in January, the other metric that remains flat as a board is the number of reactors currently under construction in the U.S. which stands at a solid zero. Reflected against the backdrop of China, as they added one additional reactor for a total of 39 under construction, the frustration for actually launching a nuclear renaissance intensifies for everyone.

In the last month, China started construction on 1 additional nuclear reactor bringing the total to 39. https://t.co/O8lrhcvJJv pic.twitter.com/BXffiftGqN

— zerohedge (@zerohedge) March 10, 2026

TerraPower did recently receive their construction permit for deploying a Natrium reactor in Wyoming, but it will potentially take months for them to meet the actual requirement of getting added to the board. The U.S. should look forward to joining the prestigious ranks alongside Iran for having just one reactor under construction.

Just as we stated in our uranium investment thesis published back in December of 2020 and even more recently in December of last year, we expect uranium to remain a solid choice for the nuclear renaissance.

Goldman Sachs analyst Brian Lee provides a recap for the month of February regarding updates across the uranium and nuclear industries.

New reactor progress and announcements

North America

2/13/2026 – Canada – OPG and Port Hope are collaborating to develop up to 10GW of nuclear capacity at the Wesleyville site, potentially powering 10 million homes. The project includes C$5mn in community funding to support regulatory assessments and local job creation.

2/19/2026 – Canada – Bruce Power has completed the construction phase of the Unit 3 Major Component Replacement, replacing key reactor parts to extend its operating life by up to 35 years. With regulatory approval to begin fuel loading, the unit is on track to return to Ontario’s grid ahead of schedule and on budget.

2/20/2026 – United States – Governor of Illinois, JB Pritzker, has issued an executive order to accelerate the deployment of at least 2GW of new nuclear capacity by 2033. This initiative follows the lifting of a long-standing moratorium and aims to support the state’s goal of 100% carbon-free energy by mid-century.

2/27/2026 – United States – Vistra Corp has secured landmark 20-year PPA with Amazon Web Services and Meta to provide over 3,800 MW of nuclear energy, supporting the long-term relicensing and uprating of its plants through the 2050s and 2060s. While initial power delivery is set to begin in 2026, the planned capacity uprates at the Perry, Davis-Besse, and Beaver Valley facilities are expected to come online between 2031 and 2034.

Europe

2/5/26 – Hungary – Hungary has officially commenced construction of the Paks II nuclear power plant with the first concrete pour for the foundation of Unit 5. The project, featuring two Russian VVER-1200 reactors, aims to provide approximately 70% of the nation’s electricity demand by the early 2030s.

2/10/2026 – Armenia – Armenia and the United States have finalized a “123 Agreement” for nuclear cooperation, enabling up to $9bn in potential US exports and long-term support for projects such as SMRs. This agreement establishes a framework for American technology to compete with Russian and international offers as Armenia prepares to select a new reactor model by 2026 or 2027.

2/13/2026 – France – France’s latest Multiannual Energy Programme for 2026–2035 puts nuclear at the centre of decarbonisation—seeking to extend existing reactors’ lifetimes, build six new reactors (with an option to decide on eight more), and raise decarbonised electricity output while cutting fossil fuel consumption, alongside renewables.

2/18/2026 – Slovenia – Slovenia has officially initiated the National Spatial Plan for a new reactor unit at the Krško Nuclear Power Plant. Prime Minister Robert Golob announced that a referendum is expected by late 2027 or early 2028, at which point the technology, supplier, and final costs will be defined.

2/23/2026 – Serbia – Serbia and Russia have discussed expanding nuclear energy cooperation, with Rosatom offering a full range of technologies from SMRs to large-scale plants to support Serbia’s energy sovereignty. While Serbia is currently working with France’s EDF on its initial nuclear roadmap, the government aims to establish a national implementation organization by the end of March 2026 to prepare for potential grid connection after 2040.

Asia and other

2/3/2026 – Kazakhstan – Kazakhstan has finalized the selection of the Zhambyl district in the Almaty region for its second nuclear power plant, with the China National Nuclear Corporation (CNNC) appointed to lead the construction. This project, alongside the first plant to be built by a Rosatom-led consortium, is part of a strategic plan to diversify the national energy mix and achieve a 5% nuclear power generation share by 2035.

2/9/2026 – Japan – Tepco has restarted Unit 6 of the Kashiwazaki-Kariwa nuclear power plant, marking the first time a reactor owned by the company has operated since the 2011 Fukushima Daiichi accident. The 1,356 MWe ABWR reached criticality on February 17,2026, and is scheduled to return to commercial operation by March 18,2026.

2/11/2026 – India – India’s indigenous 700 MWe Rajasthan Unit 7 has successfully reached its full operating capacity following its initial grid synchronization. This milestone represents a significant step forward in expanding India’s domestic nuclear power generation and clean energy infrastructure.

2/16/2026 – China – Unit 1 of the San’ao nuclear power plant in Zhejiang, China, reached first criticality on 2/14. This Hualong One reactor is the first of 6 units planned for the site and marks the first instance of private capital investment in a Chinese nuclear project.

2/16/2026 – China – Unit 1 of the Taipingling nuclear power plant has successfully connected to the grid, marking the first of six planned Hualong One reactors to supply electricity in Guangdong province. This 1116 MWe reactor is expected to enter commercial operation in the first half of 2026.

2/16/2026 – India – Tarapur Atomic Power Station Unit-1 (TAPS−1), India’s oldest commercial nuclear reactor, has returned to service following an extensive refurbishment and life-extension program. The 160MWe boiling water reactor reached criticality on December 30,2025, and has now been synchronized to the grid with upgraded safety systems and modernized equipment.

2/19/2026 – Russia – Rostekhnadzor has issued a 10-year operating license for Unit 2 of the Zaporizhzhia Nuclear Power Plant, signaling Russia’s intent to bring the facility under its regulatory framework for future power generation. While all six units remain shut down, Rosatom continues to seek licenses for the remaining reactors, including an active application for Unit 6 and plans for the rest by the end of 2026.

3/2/2026 – India – India has officially started construction on Kaiga units 5 and 6 following the first pour of concrete for the two 700 MMe indigenous reactors. This $1.5bn project uses an innovative “mega EPC” strategy to support India’s goal of reaching 100 GW of nuclear capacity by 2047.

3/4/2026 – Turkiye – Candu Energy and Türkiye Nuclear Energy Company signed an MoU to assess deploying Canadian CANDU reactors in Turkiye, covering technical data exchange, site suitability, and regulatory/licensing needs. The review also examines financing and delivery models, localisation, and workforce development as Turkiye expands its nuclear programme beyond Akkuyu.

3/4/2026 – Philippines – KHNP, Korea Eximbank, and Manila Electric Company signed an MoU to support nuclear power plant development in the Philippines, including feasibility work, site selection, and workforce training. Korea Eximbank will also explore financing packages to help fund projects and support participating Korean firms.

SMR announcement tracker

2/12/2026 – Norway – Norway’s Ministry of Energy has officially established the impact assessment program for Norsk Kjernekraft’s proposed SMR plant in the Taftøy industrial park. This regulatory milestone enables the formal evaluation of environmental and safety factors for the project, which aims to generate ~12.5 TWh of electricity annually.

2/13/2026 – Romania – Nuclearelectrica’s shareholders have approved the FID for Romania’s first SMR plant in Doicești, which will utilize NuScale technology to provide 462 MWe of clean capacity by 2033. The project, estimated to cost between $6bn-$7bn, is now transitioning into a financial structuring and pre-engineering phase to secure investors and finalize supply chain logistics. See our report on the news.

2/17/2026 – Philippines – The USTDA has announced $2.7mn in funding for Meralco PowerGen Corp to evaluate American SMR designs and develop an implementation roadmap for the Philippines’ first nuclear plant. This initiative, supported by the bilateral “123 Agreement,” aims to enhance energy security and establish a qualified nuclear workforce through technical assistance, simulators, and university partnerships.

2/17/2026 – Finland – Steady Energy has begun constructing a full-scale, non-nuclear pilot of its LDR-50 reactor in Helsinki to test operational features and establish supply chains for district heating. The $17mn to $23mn project uses an electric heat source to provide 6 MW of thermal output, paving the way for commercial 50 MW underground nuclear heating plants.

2/23/2026 – United States – Kairos Power and DOE’s Oak Ridge National Laboratory signed a $27mn, five‑year partnership to test and validate Kairos’s fluoride salt‑cooled, TRISO‑fueled reactor technology and support the Hermes demonstration program in Oak Ridge, Tennessee.

2/25/2026 – Poland – GE Vernova Hitachi and Orlen Synthos Green Energy (OSGE) have signed an agreement to develop a standardized technical design for the BWRX-300 SMR tailored to Polish regulations and safety standards. This generic design aims to accelerate the deployment of a planned fleet of 24 reactors across Poland, with the first unit in Włocławek targeted for completion by 2032.

2/25/2026 – UAE – NANO Nuclear Energy and EHC Investment LLC have signed an MoU to explore deploying KRONOS MMRs for industrial and data center use in the UAE. These transportable, 15 MWe reactors provide a water-free, scalable clean energy solution to support the region’s decarbonization and energy resilience goals.

2/27/2026 – Lithuania – Lithuania’s Altra and GE Vernova Hitachi have signed an MoU to evaluate the feasibility of deploying BWRX-300 SMRs to meet the country’s projected energy needs. This assessment supports Lithuania’s goal of reaching climate neutrality by 2050, with a formal decision on SMR installation expected by 2028.

3/3/2026 – Singapore – KHNP and Singapore’s Energy Market Authority (EMA) have signed an MoU to jointly study the feasibility of SMRs for Singapore. This collaboration focuses on technical information sharing and human resource development to support Singapore’s long-term decarbonization and energy security goals.

Global reactor critical updates

In the month of February, there have been few changes to new reactor construction

starts, grid connections, shutdowns, or restarts.

Global reactor construction tracker

Global reactors under construction

China only

Fuel announcements

2/6/2026 – United States – BWXT is finalizing TRISO fuel for Antares Nuclear’s pilot reactor, targeting criticality by July 4, 2026, under a DOE acceleration initiative. The Antares R1 is a transportable, sodium heat pipe-cooled microreactor designed to provide up to 1MWe of scalable, carbon-free power.

2/11/2026 – United States – Solstice Advanced Materials is pursuing an expansion to boost UF6 output at its Metropolis Works plant to over 10,000 tonnes in 2026. The company says debottlenecking and further capacity projects are supported by strong demand and a backlog of more than $2bn.

2/13/2026 – Namibia – Bannerman Energy struck a financing and JV deal with CNNC Overseas for Namibia’s Etango uranium project: Bannerman will hold 55% and CNOL 45% of a JV that owns 95% of Etango, with CNOL investing about $294.5mn (plus up to $27mn reimbursement) and receiving 60% life-of-mine offtake, aiming to enable debt-free construction subject to approvals.

2/16/2026 – United States -The U.S. NRC issued TRISO-X a 40-year special nuclear material licence under 10 CFR Part 70 to commercially fabricate TRISO fuel using HALEU at its Tennessee facilities (TX-1 and TX-2), with operations starting after a final NRC pre-startup inspection. TX-1 is expected to produce about 5 tonnes of uranium (about 700,000 TRISO pebbles) per year.

2/17/2026 – Kazakhstan – Kazatomprom said its 2025 uranium output rose about 10–11% yoy to 67.18mn/lb U3O8 (100% basis), mainly from ramp-up at JV Budenovskoye, and guided 2026 production at 27,500–29,000 tU (100% basis), subject to sulphuric acid availability and consistent with its value-over-volume strategy. For more details on CCJ, please see our earnings takeaways note.

2/20/2026 – Denmark – Copenhagen Atomics signed a non-binding Letter of Intent with Rare Earths Norway to secure future access to thorium from Norway’s Fensfeltet deposit to support its containerised molten salt reactor plans, with a first test reactor expected at the Paul Scherrer Institute and commercial deployment targeted in the early 2030s.

2/24/2026 – United States – Orano submitted an Environmental Report for Project IKE to the NRC, moving the project into the next NRC review phase; Orano noted the licensing process can take up to three years, and low-enriched uranium production is scheduled to begin in 2031.

2/24/2026 – Brazil – INB, ENBPar, and Galvani met Ceará’s governor to align licensing and discuss infrastructure for the Santa Quitéria Project at Fazenda Itataia, targeting about 2,300t/year of uranium concentrate for Angra 1, Angra 2, and future Angra 3; it remains in preliminary environmental licensing with IBAMA, accepted for review in March 2022.

2/25/2026 – Russia – Rosatom says its uranium miners hit 2025 production targets and are expanding their resource base, including new licences and added infrastructure to support new deposits. It also highlighted a Krasnokamensk power-plant modernisation to support mining operations and noted growing non-uranium revenue alongside these plans.

2/25/2026 – Canada – Denison Mines says its Board approved building the Phoenix ISR uranium project at Wheeler River in Saskatchewan, with site prep and construction starting next month and first production targeted for mid-2028. The company says Phoenix could be Canada’s first ISR uranium mine.

2/25/2026 – United States – Deep Fission says it has signed a supply agreement to buy LEU from Urenco USA’s enrichment plant in Eunice, New Mexico, to support testing of its 15MWe underground Gravity SMR and early commercial deployment.

3/2/2026 – India – Cameco will supply India’s Department of Atomic Energy nearly 22mn lbs of U3O8 from 2027–2035 on market-linked pricing, a deal estimated at about C$2.6bn, as India ramps up nuclear capacity and other suppliers (e.g., Kazatomprom) also pursue long-term sales; the contract adds to India’s efforts to secure reliable uranium supply for its planned reactor expansion. Please see our note on the deal.

Uranium pricing and volume trackers

Spot pricing volatile. After a strong start to the year, spot pricing was on a downward trajectory throughout almost all of February. Specifically, spot pricing dropped from ~$94/lb to ~$85/lb in the first week of February, with a slight uptick in the following week with prices climbing back up to ~$90/lb, then followed by a modest decline ever since and currently settling at ~$86/lb. Spot market activity was moderate in the month with a total of 47 transactions involving ~6mn/lbs of uranium, with SPUT being relatively less active this month when compared to the last. Compared to last year, 2026 has started stronger in terms of spot activity.

Term pricing uptick. Term pricing for uranium continued its upward momentum from January, increasing another $2 to reach $90/lb, a level not seen since May 2008. Term market activity remained moderate throughout February, with a total of four utility term contract awards reported: three for uranium (U3O8) and one for conversion services. Additionally, some non-utility mid-term uranium purchases were tracked. Several utilities were actively evaluating offers, including one for nearly 1.2mn/lb of uranium with deliveries starting in 2029, and non-U.S. utilities assessing longer-term requests for uranium and EUP with deliveries extending into the mid-2030s. Offer levels indicated continued upward pressure on term prices, with floor pricing reaching the mid-$70s and ceiling prices pushing into the $125-$130 range, with some even reaching the mid-$150s.

Tyler Durden

Wed, 03/11/2026 – 19:45

https://www.zerohedge.com/markets/goldmans-nuclear-nuggets-february-snapshot-global-nuclear-industry

Trump–Xi Summit Preview: What’s At Stake

Trump–Xi Summit Preview: What’s At Stake

Authored by Sean Tseng via The Epoch Times (emphasis ours),

President Donald Trump is scheduled to visit China from March 31 to April 2 for a summit with Chinese leader Xi Jinping. What was already shaping up to be a high-stakes meeting on tariffs, trade rules, tech controls, and Taiwan has become more complicated in the past few weeks.

This would mark Trump’s first visit to China since returning to office in January 2025.

Before Trump even boards the plane, two developments have altered the landscape. First, the U.S. Supreme Court struck down a major part of his emergency-tariff program, restricting the broad tariff authority he had used as a negotiating tool.

Then, a U.S.–Israeli military operation against Iran, which killed the Iranian regime’s supreme leader and disrupted oil shipping routes, triggered a new crisis extending beyond the Middle East. The conflict is already intersecting with the broader strategic competition between Washington and Beijing, as China relies heavily on Middle Eastern energy supplies and has cultivated close ties with Tehran.

Analysts told The Epoch Times that the upcoming summit is no longer just about trade. It also focuses on energy security, supply chains, military signals, and how Washington and Beijing handle risk as global tensions rise.

Trump would head to Beijing with one of his simplest tariff tools weakened, they said. Additionally, the Iran war has exposed several economic vulnerabilities for China, especially its reliance on Middle Eastern energy supplies, the vulnerability of key shipping lanes such as the Strait of Hormuz to disruption, and its dependence on discounted crude imports from sanctioned states—factors that could complicate Beijing’s economic planning and its broader strategic posture.

Xi, meanwhile, would use the meeting to project authority and stability amid military turmoil and economic pressure at home, though not at the cost of appearing weak on tariffs or Taiwan, Su Tzu-yun, director of Taiwan’s Institute for National Defense and Security Research, told the publication.

Iran War

Before the Iran war, much of the discussion around the summit centered on whether Trump’s tariff leverage had been weakened and whether Xi might use that opening to press for concessions, especially on Taiwan.

The Iran conflict changed that.

The meeting in Beijing will now take place most likely amid an active war in the Middle East. U.S. and Israeli forces have struck thousands of targets in Iran and hold a clear military advantage, while Beijing’s response on behalf of its close strategic partner has been limited to diplomatic statements rather than military action.

That matters because the war has exposed an area where China is particularly vulnerable: energy, Sun Kuo-hsiang, a professor of international affairs at Taiwan’s Nanhua University, told The Epoch Times.

China is the world’s largest oil importer, and it remains dependent on shipping lanes that pass through the Middle East. Research from Columbia University’s Center on Global Energy Policy estimates that about half of China’s crude oil imports pass through the Strait of Hormuz, one of the world’s most important energy chokepoints.

The same analysis says that about a third of China’s liquefied natural gas (LNG) imports come from Qatar and the United Arab Emirates, shipments that also usually transit the strait.

Qatar alone supplies about 28 percent of China’s LNG imports, according to the analysis. But that flow has come under fresh pressure. On March 4, QatarEnergy said it halted LNG production and related products after attacks on facilities in Ras Laffan Industrial City and later declared force majeure on shipments.

China faces another vulnerability: its reliance on discounted crude from sanctioned states.

Because of U.S. sanctions on Iran, much of Iran’s oil has been sold through opaque channels using shadow shipping, ship-to-ship transfers, and third-country routing. China’s customs data has not shown direct Iranian imports since 2022, but tanker tracking indicates the trade continued.

Using Kpler data, Columbia University’s Center on Global Energy Policy estimated that in 2025, China imported roughly 1.38 million barrels per day (bpd) of Iranian crude and 389,000 bpd from Venezuela. Based on China’s record 11.6 million bpd in total crude imports in 2025, Iranian oil would account for roughly 12 percent of the total.

Sun estimated that a disruption in Iran-related supply would push China’s delivered oil import costs up by 20 to 30 percent.

That poses a clear challenge for Beijing, Sun said. If Iran’s export capacity collapses or tanker insurance and shipping become unavailable, China could lose a steady flow of discounted oil that supports its refiners.

“Put simply, China’s vulnerability is oil and sea lanes access,” he added.

From Trump’s perspective, that creates leverage, said Shen Ming-shih, director at Taiwan’s Institute for National Defense and Security Research.

If a successful U.S. operation in Iran enables Washington, directly or indirectly, to influence Iran’s export routes and nearby sea lanes, including those around the Strait of Hormuz, that could provide the United States with significant leverage on Beijing, Shen told The Epoch Times.

Recent U.S. military actions in Venezuela and Iran, both Chinese strategic partners, also send a broader message: The United States can strike far from home and pressure Beijing-aligned states outside East Asia, Shen said.

The Iran conflict is also serving as an informal test of China’s air defenses and electronic warfare capabilities. Chinese-made air defense systems in Iran have come under scrutiny after they failed to prevent U.S. strikes, he noted.

Key Minerals and Components

The Iran conflict also highlights America’s vulnerability, Shen said.

If China is vulnerable to oil and shipping, the United States remains exposed in parts of the high-end defense supply chain, especially key minerals and components, he said.

“The current U.S. military operation in Iran is consuming large quantities of advanced munitions that require critical minerals controlled by China,” he noted, raising a question about who can actually keep production lines running.

China dominates parts of the supply chain for critical minerals used in semiconductors and modern weapon systems such as precision-guided missiles and fighter aircraft, including the F-22 and F-35, U.S.-based economist Davy J. Wong told The Epoch Times.

According to a July 2025 report by the Center for Strategic and International Studies, for example, China has a near-total monopoly on gallium production, accounting for 98 percent of the world’s supply, and warns of a growing supply crunch that could affect defense production.

Gallium is used in the radar seekers and guidance electronics of many modern missiles.

“The rivalry is not just about tariffs and chips; it is also about industrial endurance,” Shen said. “It is about keeping factories running, producing consumer goods, missile seekers, or the electronics that make advanced weapons work.”

If the United States is burning through expensive interceptors and precision weapons faster than it can replenish them, Beijing may conclude that Washington is limited in its ability to raise pressure in the Indo-Pacific, or at least may be more cautious about opening a second front of escalation on trade, sanctions, or Taiwan amid the Iran war, Shen said.

“That does not mean China gains immediate advantage,” he added. “At present, there is no clear indication that U.S. defense contractors are experiencing shortages of rare-earth materials that would limit production capacity.”

Tariff Issue

The Supreme Court ruling was a setback for Trump, but it did not eliminate all tariffs or trade tools, so the United States retained considerable trade leverage, Wong said.

On Feb. 20, the court struck down most of Trump’s broad “emergency” tariffs, ruling that the 1977 International Emergency Economic Powers Act, or IEEPA, does not give a president the power to impose sweeping tariffs in the way Trump had tried to use it.

The White House responded quickly. On the same day as the ruling, Trump invoked Section 122 of the Trade Act of 1974 to impose a temporary 10 percent duty on imports. Then on Feb. 21, he raised that temporary duty to 15 percent for all countries.

Trump’s tariff is not off the table, Wong said.

“That matters because Trump’s negotiating style has often been simple and direct: threaten tariffs, push for concessions, and claim a win,” he added. “The ruling did not take tariffs off the table. It just made the easiest route slower and more constrained.”

The administration is now leaning more heavily on other trade tools, including Section 232 of the Trade Expansion Act of 1962, which addresses national security risks, and Section 301 of the Trade Act of 1974, which targets unfair trade practices.

U.S. Trade Representative Jamieson Greer said on CBS’s “Face the Nation” on Feb. 22 that although “the Supreme Court struck down tariffs under one authority, tariffs under other national security elements remain in place,” and that the administration can launch “additional investigations” that could lead to more tariffs.

However, Wong stated that U.S. policy has not shifted toward easing trade tensions but has instead moved toward developing a new bargaining strategy.

In late 2025, the Office of the U.S. Trade Representative launched a Section 301 investigation to determine whether China had been fulfilling its commitments under the Phase One trade deal.

Beijing has answered with warnings. China’s Commerce Ministry said on Feb. 25 it would take “all necessary measures” if Washington used that probe as a pretext for new tariffs.

At the same time, Beijing is signaling that it still wants the Trump–Xi summit and aims to keep overall U.S.–China ties manageable. Lou Qinjian, a spokesman for China’s rubber-stamp National People’s Congress, called leader-level diplomacy “irreplaceable” and pointed to regular communication between the two leaders since last year.

Wong said the message is that the Chinese regime does not want to appear weak, but it also wants to avoid another uncontrolled escalation right before a summit.

Why Xi Needs the Summit to Happen

For Xi, Trump’s visit is useful for reasons that go well beyond diplomacy, Su said.

Xi is dealing with unusual domestic turbulence, he told The Epoch Times. An unprecedented purge within the People’s Liberation Army (PLA) has shaken the top ranks of the military.

The Center for Strategic and International Studies (CSIS) has tallied more than 100 senior PLA officers who have been removed or disappeared since 2022, and even top figures in the Central Military Commission have come under investigation or been expelled.

That points to deep disruption inside the institution meant to guarantee Xi’s authority, Su said. The purge also raises practical questions about military readiness.

CSIS said the leadership gaps created by the purge would make it very difficult for China to launch a major operation against Taiwan in the short term, and that the upheaval has already affected military drills around Taiwan.

China’s economy adds to the pressure. Beijing has set a 2026 growth target of 4.5 to 5 percent, its lowest since 1991, while officials have acknowledged a property slump and broader headwinds.

Given that situation, Su said, Xi is incentivized to pursue a more stable external environment, making the summit important.

“A visit by Trump to Beijing is not just diplomacy for Xi; it is also political theater,“ Su said. ”It allows Xi to project authority, stability, and international stature at a time when all three are under pressure.”

For Trump, there are different ways he can frame the visit, according to Su: “as either a demonstration of dealmaking skills or as an assertion of great-power status diplomacy.”

“Xi can use hosting the summit at home to show that Washington still needs to come to him, on his turf, despite economic challenges, military upheaval, and doubts about PLA readiness,” Su continued. “In that sense, the optics may matter more to Xi than to Trump.”

The Taiwan Issue

Taiwan remains the primary issue, according to Shen.

Trump’s February comment that he had been discussing U.S. arms sales to Taiwan with Xi has stirred concern among some Taiwanese lawmakers and experts that cross-strait issues could become a bargaining chip as Washington and Beijing negotiate on trade and security.

“Although the White House later said there is no change to its policy with respect to Taiwan, Beijing’s objective is clear. It wants Washington to reduce visible support for Taiwan and pull back from what it sees as challenging its claims over the island, such as high-level official contacts and military cooperation,” Shen said.

Washington’s incentives are quite clear, he said. Any sign that Trump is trading away U.S. commitments to Taiwan would trigger backlash at home and unsettle U.S. allies in Asia. “And that leaves a narrow and tense path,” he added.

On Feb. 3, Trump signed a sweeping omnibus appropriations bill that includes more than $1.4 billion to support security cooperation with Taiwan.

Those provisions come on top of an arms sale announced last December, which the administration valued at more than $11.1 billion and described at the time as the largest bundled arms sale to Taiwan in U.S. history.

Despite the worries and speculation, U.S. actions suggest otherwise—those arms sales to Taiwan would likely proceed as planned, Shen added.

What Each Side Realistically Wants

Trump will likely push for concrete economic outcomes, Wong said.

“One goal will likely be to extend or reinforce the existing trade truce. Another aims to ensure purchases and market access, including more Chinese purchases of U.S. farm goods such as soybeans,” he said.

At the same time, the Trump administration is covering its bases with measures such as Section 301 investigations and other tariff tools that could take time to develop as potential leverage if Beijing fails to follow through on its promises later, he added.

That indicates the White House is pursuing two strategies at once: negotiating with Xi at the leadership level while preparing legal cases for more targeted tariffs later, Wong said.

Su added that another major goal of the Trump administration is to pressure Beijing into further curbing the production and export of fentanyl precursor chemicals, a key Trump policy priority in combating illicit drugs.

Xi’s goals differ, as he seeks validation of his authority and international stature amid domestic turmoil, Su said. He also wants to reduce the risk of sudden tariff hikes, protect Chinese exporters as growth slows, and seek relief from U.S. export controls on advanced chip equipment and other critical technologies.

“Regarding Taiwan, Xi would hope to secure some symbolic commitments,” Shen said. “But those would likely remain symbolic because the United States would not violate the Taiwan Relations Act or the Six Assurances.”

The Taiwan Relations Act was passed by Congress after Washington switched diplomatic recognition from Taipei to Beijing in 1979. It manages ongoing relations with Taiwan, including security cooperation, arms sales, trade, and cultural exchanges.

The Six Assurances, first conveyed to Taiwan in the 1980s, include commitments that the United States has not agreed to set a date for ending arms sales to Taiwan, will not consult Beijing on those sales, will not mediate between Taipei and Beijing, will not revise the Taiwan Relations Act, has not changed its position on Taiwan’s sovereignty, and will not pressure Taiwan to negotiate with China.

The likeliest outcome, Wong said, is not a fundamental easing of U.S.–China tensions but a temporary effort to manage competition and prevent the relationship from deteriorating further.

Gu Xiaohua contributed to this report.

Tyler Durden

Wed, 03/11/2026 – 19:20

https://www.zerohedge.com/geopolitical/trump-xi-summit-preview-whats-stake

China-Based Copper Scam Leaves Cooling Firm With Fake Metal

China-Based Copper Scam Leaves Cooling Firm With Fake Metal

Thermal Grizzly CEO Roman “Der8auer” Hartung says his company recently fell victim to large-scale materials fraud while trying to source copper and aluminum for its cooling products, according to PC Gamer.

The company needs several tons of metal to machine components such as GPU water blocks. With copper prices rising and European supplies expensive, Hartung turned to suppliers in China’s metal market. After reviewing documentation and conducting supplier checks, Thermal Grizzly placed two orders—one for copper and another for aluminum and copper.

Weeks later, pallets of metal arrived in Germany and the firm began its usual quality inspections. An initial X-ray spectroscopy test on a sample suggested the sheets were pure copper. But a conductivity test produced unexpected results. When the team milled the material to investigate further, it produced sparks—something real copper shouldn’t do.

An engineer then tried a magnet, revealing the truth: the “copper” was actually steel coated with copper. In one shipment, a few genuine sheets had been placed on top of a pallet filled with plated steel underneath.

PC Gamer writes that the aluminum order turned out to be fraudulent as well. The top layers of the pallet contained real aluminum sheets, but below them were steel plates and empty space, allowing the shipment to pass a weight check despite being largely fake.

The orders cost about €40,000. While some value can be recovered as scrap metal, the company still faces a significant loss. Legal options are limited because the suppliers are based in China.

Hartung noted that working with Chinese manufacturers is common and the company had carried out multiple checks before ordering. Fraud like this often appears when the price of key industrial materials spikes, creating incentives for suppliers to pass off lower-value metals as genuine products.

Thermal Grizzly ultimately rejected the materials rather than risk its reputation by using them.

Tyler Durden

Wed, 03/11/2026 – 18:55

https://www.zerohedge.com/markets/china-based-copper-scam-leaves-cooling-firm-fake-metal

The App Store Accountability Act Is A Privacy Nightmare Disguised As Child Protection

The App Store Accountability Act Is A Privacy Nightmare Disguised As Child Protection

Authored by Julio Rivera via American Greatness,

Washington has discovered a familiar political trick: wrap a flawed policy in the language of protecting children and hope nobody reads the fine print. The latest example is the App Store Accountability Act, a bill championed by lawmakers who appear eager to regulate the internet without understanding how it actually works.

Supporters insist the legislation will protect kids online. In reality, it risks undermining privacy, violating constitutional protections, and creating a cybersecurity disaster in the process.

And remarkably, Congress is pushing forward with this even though federal courts have already signaled that this exact regulatory model is unconstitutional.

The App Store Accountability Act would require app stores to verify the ages of every user and share age information with app developers. On paper, that sounds straightforward. In practice, it would force companies to collect massive amounts of sensitive personal data simply to download everyday apps.

Want to download a weather app? Verify your age.

Want to install a calculator? Verify your age.

Want to read the news? Verify your age.

The practical result is obvious: app stores would be compelled to gather highly sensitive identity data on tens of millions of Americans and then distribute that information to countless third-party developers.

This could be one of the largest digital identity honeypots ever conceived.

Security experts have been warning about this for months. In fact, 419 cybersecurity and privacy academics from 30 countries recently signed an open letter warning that large-scale age verification systems are “dangerous and socially unacceptable” because they create enormous new attack surfaces for hackers and data thieves.

The logic is simple. If every app download requires age verification, that means sensitive identity data must be stored, transmitted, and accessed across thousands of services. Instead of limiting the spread of personal information, the bill effectively multiplies it.

For cybercriminals, it would be a dream target.

Equally troubling is the bill’s blatant disregard for recent federal court rulings. Lawmakers promoting the legislation often claim that age-verification mandates have already received judicial approval.

That claim collapses under even basic scrutiny.

Just months ago, a federal judge blocked a nearly identical Texas law modeled on the same concept, ruling that it was “exceedingly overbroad” and failed strict constitutional scrutiny.

The court compared the requirement to a government mandate forcing bookstores to check the ID of every customer before allowing them inside. Such a system, the judge explained, would restrict minors from participating in the “democratic exchange of views online.”

In other words, it violates the First Amendment.

Despite that ruling, Congress now appears ready to repeat the same mistake on a national scale.

Supporters of the bill, including lawmakers like Representatives John James (R-MI), Gus Bilirakis (R-FL), and Erin Houchin (R-IN), argue that forcing app stores to verify the age of every user will protect children online. But critics warn the approach risks creating new privacy and security problems while doing little to address the real harms children face on the internet.

Additionally, the proposal ignores the practical realities of how the modern app ecosystem actually functions.

Most apps are not social media platforms. They are mundane tools: banking apps, airline apps, school apps, fitness trackers, weather alerts, home security dashboards, and so forth. The App Store Accountability Act would force age verification for all of them.

Even worse, the bill requires verification across four distinct age brackets: under 13, 13 to 15, 16 to 17, and adults. That may sound bureaucratically tidy, but in the real world, it creates a massive liability problem for app stores.

If a company guesses wrong about whether someone is 12 or 13, it could face penalties from federal regulators. The only way to avoid that risk is to demand hard identification, such as driver’s licenses, credit cards, or even birth certificates to prove parental relationships.

That is the inevitable outcome of the bill’s legal structure.

And millions of Americans do not even possess the required credentials. More than 45 million Americans are either credit unserved or underserved, meaning the law could effectively force them to hand over government IDs simply to download basic apps.

Ironically, many parents do not even support this approach. Surveys show parents overwhelmingly prefer tools that protect children while they use apps rather than a one-time age verification at the app store level.

In other words, the bill creates a massive bureaucracy that fails to solve the problem it claims to address.

More importantly, it distracts from real solutions that actually help protect kids online.

Digital literacy education, stronger parental control tools, and targeted enforcement against platforms that knowingly facilitate exploitation are all more effective approaches. These strategies address harmful behavior without building a nationwide surveillance system for internet users.

The App Store Accountability Act does the opposite. It places the burden on every user, every developer, and every app store while doing little to target the bad actors responsible for real harm.

That is why critics from across the technology and cybersecurity communities are raising alarms. The legislation threatens to create new privacy risks while inviting years of constitutional litigation that will likely end with the law being blocked in court.

If lawmakers truly want to protect children online, they should start by listening to experts instead of rushing through legislation that ignores both legal precedent and technical reality.

Unfortunately, Washington often prefers symbolic victories to workable solutions.

The App Store Accountability Act is a perfect example of what happens when lawmakers regulate technology they clearly do not understand. It risks undermining privacy, weakening cybersecurity, and violating free speech rights all at the same time.

And if Congress insists on passing it anyway, the courts will almost certainly remind them why the Constitution still matters.

Tyler Durden

Wed, 03/11/2026 – 18:30

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}