Category: News

Ex-Goldman Commodity King Warns ‘No Policy Response Can Meaningfully Reverse Oil Prices’

Ex-Goldman Commodity King Warns ‘No Policy Response Can Meaningfully Reverse Oil Prices’

“There is NO policy response that will stop this ascent in crude in the near term,” warns Goldman’s former head of commodity research, Jeff Currie.

In an interview on Bloomberg TV (watch here), Currie warned that the broader crisis goes beyond just oil:

This isn’t solely an oil issue; the Strait disruption affects multiple commodities and global trade.

The system “simply cannot accommodate” such a shock, leading to extreme hoarding, upward price pressure, and potential inflation spillovers.

Oil

Crude’s ascent is unstoppable in the near term: No effective policy response (e.g., from governments, SPR releases, or other interventions) can halt or meaningfully reverse the upward trajectory of oil prices while the Strait of Hormuz remains disrupted/blocked.

He emphasizes that policy options are “unlikely to break crude’s ascent” under current conditions.

Severe supply chain risks and disruptions: Risks to global energy supply chains are at unprecedented highs. A prolonged closure of the Strait (which carries 18.5 million b/d of oil, plus gas, fertilizers, and metals) would represent massive lost flows—e.g., 31 days could equate to over 575 million barrels stopped, far exceeding the entire US Strategic Petroleum Reserve (411-415M barrels historically, with no major releases confirmed recently).

Market optimism vs. reality: Financial markets appear “wildly optimistic” if betting against prolonged disruption (e.g., Polymarket odds cited in related Carlyle analysis put high probability on continued closure). Physical constraints and underinvestment in supply are “biting,” with no real glut despite past narratives.

Hard Assets

Currie has repeatedly emphasized the “revenge of the old economy” theme.

This frames hard assets—particularly energy (oil, natural gas), metals (copper, base/precious metals), agriculture, and other real/physical commodities—as entering or reasserting a commodity supercycle driven by:

Chronic underinvestment in traditional supply chains (e.g., oil and metals have been “substantially underinvested” for years, with no major non-OPEC supply surge ahead after 2026).

Structural demand shifts (e.g., AI/data center energy needs boosting power demand, electrification increasing metals use like copper/silver, geopolitical fragmentation leading to higher “security premiums” on commodities).

Capital rotation from tech/financial assets (e.g., massive MAG7 market caps) into real assets (smaller mining/energy sectors), which could trigger explosive price moves due to limited free float and supply constraints.

Hoarding and strategic stockpiling by nations like China/India amid risks, amplifying upside in physical commodities.

Geopolitical/security factors overriding efficiency (e.g., “just-in-case” stockpiling vs. just-in-time, leading to higher cyclicality and premiums on energy/metals).

HALO

Jeff Currie’s thinking on the HALO portfolio centers on Heavy Asset Low Obsolescence (HALO) assets – tangible, physical, “old economy” companies and sectors with durable infrastructure that resist rapid technological disruption or obsolescence.

Jeff argues that amid geopolitical shocks like disruptions in the Strait of Hormuz, every major inflection point over the past 50 years has triggered a capital rotation from asset-light sectors (e.g., tech, now ~53% of the S&P) to asset-heavy sectors.

Energy’s weight has shrunk to just ~3% (from 25% in the 1970s, when it provided a natural inflation hedge), leaving portfolios exposed as markets wrongly priced energy as declining and tech as perpetual.

HALO assets, including commodities, energy, metals, mining, infrastructure (e.g., pipelines, railroads, utilities), and other real-asset plays, position investors to weather anticipated and unanticipated inflation, supply chain risks, hoarding, and the “revenge of the old economy” supercycle—driving potential explosive upside from underinvestment and capital shifts.

This isn’t a rigid ticker list but a strategic overweight toward resilient hard assets for hedging and growth in the current volatile environment.

Tyler Durden

Wed, 03/11/2026 – 11:00

Supreme Court Justices Kavanaugh, Jackson Publicly Disagree Over Emergency Docket

Supreme Court Justices Kavanaugh, Jackson Publicly Disagree Over Emergency Docket

Authored by Matthew Vadum via The Epoch Times,

U.S. Supreme Court Justices Brett Kavanaugh and Ketanji Brown Jackson clashed on March 9 over the court’s various emergency orders that have allowed President Donald Trump to pursue his policy agenda.

The setting was a federal courtroom in the nation’s capital, at an annual lecture honoring former federal judge and prosecutor Thomas Aquinas Flannery, who died in 2007.

Kavanaugh, who was appointed by Trump in 2018, and Jackson, who was appointed by President Joe Biden in 2022, discussed the high court’s emergency docket, also known as the interim relief docket and the shadow docket, which refers to applications that seek immediate action from the justices.

Such cases are handled on an expedited basis, with limited briefing and generally without oral argument.

Often, the orders that follow are unsigned and provide little or no reasoning, though sometimes justices will file concurring or dissenting opinions.

The issue in emergency appeals is often whether a policy being challenged in court should be allowed to take effect while litigation that could take years to complete plays out.

Lower courts have stifled Trump’s policy agenda, issuing order after order blocking aspects of it. The second Trump administration has increasingly turned to the Supreme Court for emergency relief, and that court has often provided it by lifting those orders.

For example, in U.S. Department of State v. AIDS Vaccine Advocacy Coalition, on Sept. 9, 2025, the court granted a Trump administration request to temporarily withhold about $4 billion in foreign aid funding previously authorized by Congress.

On Nov. 6, 2025, in Trump v. Orr, the court allowed the Trump administration to enforce its policy requiring the sex designation on a U.S. passport to be consistent with the passport holder’s sex at birth.

The court has also issued emergency rulings upholding redrawn congressional maps in Texas and California.

On Dec. 4, 2025, in League of United Latin American Citizens v. Abbott, the court allowed a new election map that is expected to increase Republican representation in Texas’s U.S. House delegation.

On Feb. 4, in Tangipa v. Newsom, the court allowed California to use its newly redrawn congressional map that aims to give Democrats five extra seats in the upcoming midterm elections.

Public Debate

Jackson, who often dissents from the emergency orders, said at the March 9 event that Kavanaugh and other conservatives on the high court who repeatedly sided with Trump in emergency rulings last year were doing a disservice both to the court and the country.

U.S. Supreme Court Justice Ketanji Brown Jackson poses for an official portrait in Washington on Oct. 7, 2022. Alex Wong/Getty Images

“The administration is making new policy … and then insisting the new policy take effect immediately, before the challenge is decided,” Jackson said.

“This uptick in the court’s willingness to get involved in cases on the emergency docket is a real unfortunate problem.”

The Supreme Court is “creating a kind of warped” legal process by intervening at an early stage of a case and basically predicting the outcome before the arguments are developed fully, she said.

Kavanaugh said the Supreme Court is only doing its job by addressing the emergency applications filed.

The Department of Justice’s rush to the Supreme Court didn’t begin during the Trump administration, the justice said. He said that as it becomes more difficult to enact legislation through Congress, administrations “push the envelope in regulations. Some are lawful, some are not.”

Kavanaugh added that some critics of recent orders did not object when the justices allowed Biden administration policies that were being challenged to take effect even as cases about them were pending in lower courts.

Jackson reiterated a complaint that the liberal justices have made in their dissenting opinions.

“Should the Supreme Court be superintending the lower courts when they are hearing and deciding the issues?” Jackson said.

Kavanaugh, who concurred with a majority opinion criticizing lower court judges for ignoring Supreme Court rulings, said the issues for the justices are often complicated, and the cases are close.

“None of us enjoys this,” he added.

Associate Supreme Court Justice Brett Kavanaugh poses for his official photo at the Supreme Court in Washington on Oct. 7, 2022. Olivier Douliery/AFP via Getty Images

In that Aug. 21, 2025, ruling in National Institutes of Health v. American Public Health Association, the court held that the institutes could cancel hundreds of millions of dollars in research grants linked to diversity, equity, and inclusion (DEI) initiatives.

Jackson dissented in the case, arguing the ruling was arbitrary and criticizing the court majority for what she called “lawmaking on the emergency docket.”

Other justices have also criticized what they consider an abuse of the emergency docket.

Justice Sonia Sotomayor dissented in the Sept. 8, 2025, ruling in Noem v. Perdomo, which lifted a lower court order preventing U.S. Immigration and Customs Enforcement from using “apparent race or ethnicity” when deciding whether to detain a person suspected of violating federal immigration laws.

Sotomayor said the federal government engaged in “yet another grave misuse of our emergency docket.”

“We should not have to live in a country where the Government can seize anyone who looks Latino, speaks Spanish, and appears to work a low wage job,” she said.

Justice Elena Kagan dissented in the Sept. 22, 2025, ruling that temporarily upheld Trump’s authority to fire Federal Trade Commission (FTC) member Rebecca Slaughter.

Kagan said the FTC statute bars the president from removing members except for “inefficiency, neglect of duty, or malfeasance in office,” adding that the “emergency docket should never be used, as it has been this year, to permit what our own precedent bars.”

Justice Samuel Alito dissented from the April 19, 2025, order that temporarily blocked the Trump administration from deporting alleged members of the Venezuelan criminal gang Tren de Aragua.

“Literally in the middle of the night, the Court issued unprecedented and legally questionable relief without giving the lower courts a chance to rule, without hearing from the opposing party, within eight hours of receiving the application, with dubious factual support for its order, and without providing any explanation for its order,” Alito wrote.

The justices acted even though “it is not clear the Court had jurisdiction,” or authority to hear the case, he wrote.

Tyler Durden

Wed, 03/11/2026 – 10:45

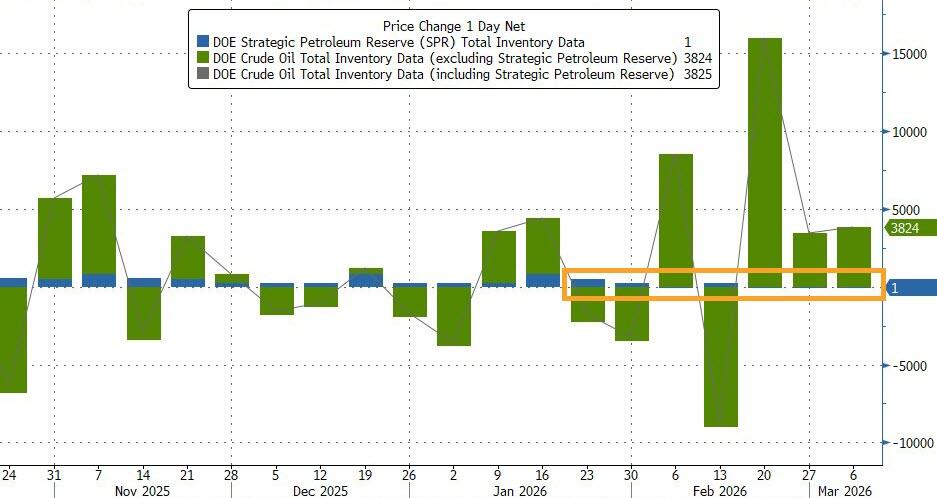

WTI Extends Gains, Shrugs Off SPR Release Amid Crude Build, Dip In US Production

WTI Extends Gains, Shrugs Off SPR Release Amid Crude Build, Dip In US Production

Oil prices are higher this morning, shrugging off the well-telegraphed (and practically useless) SPR release.

“Oil prices remain volatile and risk sentiment fragile and trading is on the headlines and rapidly evolving conflict in the Middle East,” noted Neil Wilson, Saxo UK investor strategist.

And while, the main drivers of crude prices remain more global, the domestic supply and demand situation remains noteworthy based on its impact on gasoline (pump) prices.

API

Crude -1.7mm (+1.1mm exp)

Cushing

Gasoline -1.8mm

Distillates -2.3mm

DOE

Crude +3.82mm (+1.1mm exp)

Cushing +117k

Gasoline -3.65mm – biggest draw since Oct 2025

Distillates -1.35mm

Crude stocks rose more than expected last week (third week in a row) while gasoline stocks saw sizable draws (for the fourth week in a row)…

Source: Bloomberg

For the third week in a row, the Strategic Petroleum Reserve (which is now once again making headlines) saw no change…

Source: Bloomberg

US Crude production dipped modestly last week as the rig count stabilized…

Source: Bloomberg

Oil prices extended gains…

“Markets are likely to grow increasingly fearful over the long-term implications with each day that passes,” said Joshua Mahony, chief market analyst at Scope Markets.

“Oil prices remain the main driver of market sentiment,” he added.

Finally, the International Energy Agency is proposing a release of 400 million barrels with Birol stating that “each member will release oil at a time frame appropriate for each member state” – a slippery way of saying the release won’t come nearly as fast as it is required.

Of course, what really matters (for Trump and the Republicans) is the price of gas, which at this rate is set to soar above $4/gallon imminently…

…and it may already be too late to avoid it.

Tyler Durden

Wed, 03/11/2026 – 10:39

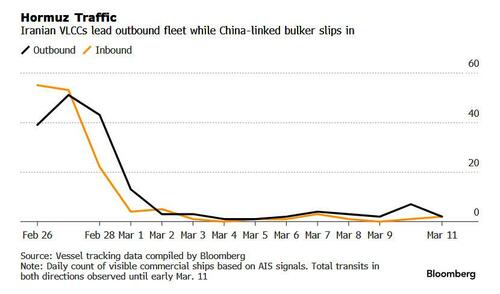

Most Ships Transit Strait Of Hormuz Since War Started Led By Iranian, China-Linked Tankers

Most Ships Transit Strait Of Hormuz Since War Started Led By Iranian, China-Linked Tankers

Yesterday we pointed out that contrary to conventional wisdom of a full Gulf blockade, more ships are now transiting the Strait of Hormuz…

Strait ship traffic starting to move (chart GS) pic.twitter.com/VJ0M9ET3yi

— zerohedge (@zerohedge) March 10, 2026

… with the caveat that most are turning off their transponders not to attract undue attention, whether by Iran or the US.

Strait ship traffic starting to move (chart GS) pic.twitter.com/VJ0M9ET3yi

— zerohedge (@zerohedge) March 10, 2026

This morning, Bloomberg confirms that while mainstream Western shipping remains largely suspended through the Strait of Hormuz, recent 24-hour observations reveal a jump in Iran-linked traffic, specifically involving two sanctioned (read China-focused) VLCCs.

There were eight commercial transits on Tuesday and four more were identified early Wednesday, most of which have ties to Iran or have Chinese commercial links, according to vessel-tracking data compiled by Bloomberg.

Two sanctioned Iranian VLCCs, were seen exiting the Persian Gulf for Asia early Wednesday. Their drafts suggest both supertankers are fully laden, and since they saw no pushback from Iran, are headed toward China. As much as 13.7 million barrels of Iranian crude has been shipped through the strait since the war began on Feb. 28, according to Tankertrackers.com, a company that specializes in the use of satellite imagery to track vessels.

According to Bloomberg, one Iran-affiliated container-ships entered the Persian Gulf on Tuesday and another on Wednesday. In addition, a bulk carrier also entered the Gulf Wednesday signaling ‘China Owner All Chinese.’

This increase in activity comes amid an escalation in hostilities in the region. The cargo ship Mayuree Naree was hit by an unknown projectile, while transiting the Strait of Hormuz.

BREAKING:

Iran strikes a Thai ship attempting to pass through the Strait of Hormuz.

Thai authorities said the bulk carrier Mayuree Naree, sailing under the Thailand flag, was struck by projectiles while travelling about 18km north of Oman.

— Visegrád 24 (@visegrad24) March 11, 2026

Another bulk carrier signaling ‘China Owner&Crew’ u-turned away from the strait following the incident, underscoring the heightened security risks.

As we reported previously, widespread electronic warfare tactics, including spoofing and signal jamming, have made real-time monitoring of traffic increasingly difficult. With several vessels opting to deactivate AIS transponders in high-risk areas, data accuracy is expected to lag, leading to an eventual upward revision of historical transit numbers.

Still, despite the occasional successful crossing, the bulk of the industry’s tonnage remains stuck on either side of the strait until maritime security is restored. Traffic through the channel was effectively halted following several attacks on merchant ships as Iran retaliated against US and Israeli strikes. Missile and drone activity continues to pose a critical risk to all vessels in the vicinity.

Tyler Durden

Wed, 03/11/2026 – 10:20

Microsoft Backs Anthropic’s Bid To Block Pentagon’s ‘Supply-Chain Risk’ Label

Microsoft Backs Anthropic’s Bid To Block Pentagon’s ‘Supply-Chain Risk’ Label

Authored by Aldgra Fredly via The Epoch Times,

Microsoft on March 10 filed an amicus brief backing Anthropic’s lawsuit against the Department of War, seeking a court order to temporarily stop the Pentagon from labeling Anthropic as a supply-chain risk.

Anthropic filed the suit on March 9 after the Pentagon designated it a supply chain risk to national security, a label that would hinder the Pentagon and its contractors from using Anthropic’s artificial intelligence technology in their work for the U.S. military.

The designation stemmed from Anthropic’s rejection of the Pentagon’s request for unrestricted access to its Claude models over concerns that the technology could be used for mass domestic surveillance or fully autonomous weapons. The Pentagon has denied that it planned to use Claude for such purposes.

In its amicus brief filed March 10, Microsoft said it was directly affected by the Pentagon’s designation of Anthropic because it uses Anthropic’s technologies in products made available to the Pentagon.

The tech giant said that a temporary block on the designation would “enable a more orderly transition and avoid disrupting the American military’s ongoing use of advanced AI.”

Microsoft warned that U.S. warfighters could be hampered “at a critical point in time” if companies are required to immediately alter existing product and contract configurations used by the Pentagon.

It also warned that putting the Pentagon’s designation of Anthropic into immediate effect will have “broad negative ramifications for the entire technology sector and the American business community.”

Microsoft said the Pentagon gave itself a six-month period to transition services away from Anthropic’s technologies but did not provide the same transition timeline for contractors that use Anthropic products.

“Should this action proceed without the entry of a temporary restraining order, Microsoft and other government contractors with expertise in developing solutions to support U.S. government missions will be forced to account for a new risk in their business planning,” it stated.

“Should companies choose to forgo the opportunity to work with the U.S. government due to the attendant risks, the U.S. government, its missions, and the people it serves would lose access to state-of-the-art technological solutions,” Microsoft said.

The Pentagon said it does not comment on ongoing litigation.

Anthropic alleged in its lawsuit that the federal government designated the company in retaliation for its viewpoint protected under the First Amendment.

Secretary of War Pete Hegseth on Feb. 27 accused Anthropic of trying to dictate military operations by denying the Pentagon permission to use its Claude models for all lawful purposes.

“Their true objective is unmistakable: to seize veto power over the operational decisions of the United States military. That is unacceptable,” Hegseth said in a post on X.

The Pentagon used the Claude AI system for mission-critical functions, including intelligence analysis, modeling and simulation, operational planning, and cyber operations.

Tyler Durden

Wed, 03/11/2026 – 09:45

https://www.zerohedge.com/ai/microsoft-backs-anthropics-bid-block-pentagons-supply-chain-risk-label

JPMorgan Limits Lending To Private Credit Groups After Marking Down Loan Collateral

JPMorgan Limits Lending To Private Credit Groups After Marking Down Loan Collateral

The barrage of negative private credit news, now that the $1.8 trillion bubble has burst, is coming hot and heavy.

Following last night’s report that Cliffwater, a private credit interval fund which according to Rubric Capital “is the canary in the coal mine and will be the first domino in the bank run” was the latest fund to be hit with 7% in investor redemptions (and unlike BlackRock, interval funds can not gate investors), this morning the FT reported that JPMorgan has “clamped down on its lending to private credit groups, with bankers looking to cut risk as concerns mount over the credit quality of companies in their stables.”

According to the report, the bank informed private credit lenders that it had marked down the value of certain loans in their portfolios, which serve as the collateral the funds use to borrow from the bank. The loans that have been devalued are to software companies, which are seen as particularly vulnerable to the onset of AI and which account for the bulk of private credit loans made in recent years.

The news, which hit just around 1am ET, hit S&P futures which until that point were trading at session highs.

JPMorgan’s decision will limit how much money the bank lends to private credit groups against those loans going forward, a sign traditional Wall Street banks are becoming increasingly nervous about the $1.8 trillion industry that has grown rapidly as non-bank lenders became top creditors to higher-risk borrowers.

The move was to be expected: JPM CEO Jamie Dimon has expressed an increasingly negative view of the private credit space, and told investors at the bank’s leveraged finance conference last week that it was being more prudent in lending against software assets. Troy Rohrbaugh, co-chief executive of JPMorgan’s commercial and investment business, told analysts at a February company update that the bank was becoming more conservative compared to its peers on the risks in private credit.

“As the world gets more volatile . . . this outcome should be expected,” he said, adding: “I’m shocked that people are shocked.”

One person briefed on the bank’s decision said the valuation haircuts did not trigger margin calls at funds but were done to pre-emptively reduce the amount of credit available to the funds.

“They have been more difficult the past three months,” the head of one fund said of JPMorgan’s willingness to provide back leverage. He added JPMorgan rarely got “rattled and this is the first time we’ve had a little issue”.

As we explained at the start of February, investors are concerned AI will heavily disrupt enterprise software businesses, with scrutiny centred on the companies and their private capital financiers who poured hundreds of billions of dollars into the space. Publicly traded software stocks and debt have all plummeted this year. Private credit lenders, by contrast, tend to hold loans for the entire term and have not marked down their portfolios in lockstep. Private lenders have said enterprise software companies are still growing and expect their loans to continue performing, as investors backstop the borrowers.

The growth of the private credit industry has been supplemented by leverage from regulated banks, debt that is critical in bolstering returns above high-yield bond or leveraged loan funds. Banks including JPMorgan, Wells Fargo and Bank of America have all lent heavily to the industry, in part because regulations allow them to reserve less capital than if they were lending to borrowers directly.

As the FT notes, the fundraising ability of private credit firms, which took in $400BN from wealthy individuals and hundreds of billions more from institutions since the end of 2020, has allowed the funds to provide larger loans and compete directly with banks on multibillion-dollar leveraged buyouts.

That included financing mega takeovers when software businesses were fetching high valuations given work-from-home trends, including Thoma Bravo’s $6.4bn takeover of customer service software company Medallia, and Permira and Hellman & Friedman’s $10.2bn buyout of Zendesk.

The problem is that much of the new issuance was rubberstamped by captured rating agencies at artificially inflated ratings, and as the new reality of reduced cash flows emerges, some banks are repricing their loans – carried until now at par – sharply lower and in some cases all the way to zero.

Additionally, that debt is maturing in the coming years and much of it faces a dramatically different outlook.

JPMorgan is an outlier in the private credit financing business as it reserves the right to revalue assets at any time. Most other banks require triggers such as missed interest payments. Private credit funds can dispute the marks, according to a sample credit financing agreement reviewed by the FT. That could take months and require a third-party valuation. In the meantime, the bank’s determination remains.

The FT writes that the bank considers individual analysis and macroeconomic factors when valuing loans, according to another person familiar with the bank’s thinking. It also looks to public proxies, such as investment vehicles that buy private credit loans, and occasional private trades it can evaluate.

“The point is to do it as needed, not only when there’s a crisis,” one person said

The good news for now is that private credit executives said they had not seen other banks take a similar view as JPMorgan. However, once more sources of funding to the private credit industry read the apocalyptic report by Rubric Capital, (available here to pro subscribers) we are confident that will change.

Tyler Durden

Wed, 03/11/2026 – 09:30

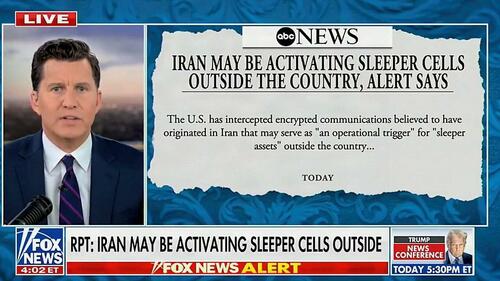

Iran Sleeper Cells ‘Activated’; Threaten To “Eliminate” Trump

Iran Sleeper Cells ‘Activated’; Threaten To “Eliminate” Trump

Authored by Steve Watson via Modernity.news,

US intelligence intercepts reveal Iran may be triggering covert operatives abroad, as Tehran issues direct warnings to President Trump following the airstrike death of its former supreme leader.

U.S. intelligence has intercepted an encrypted message from Iran that appears to be an “operational trigger” for sleeper cells embedded in foreign countries, raising alarms about potential attacks.

This development comes amid ongoing conflict, with Iran’s new supreme leader, Mojtaba Khamenei, facing threats from multiple fronts after his father’s death in a U.S.-Israeli airstrike.

🚨 ABC News reported that Iran may be activating sleeper cells.

— Breaking911 (@Breaking911) March 9, 2026

The intercepted communication, reported by ABC News, was flagged shortly after Ayatollah Ali Khamenei’s death on February 28. Analysts believe it originated in Iran and was directed at “clandestine recipients” using passcodes, with characteristics suggesting it was meant for operatives outside the country.

The alert describes the signal as resembling historical methods used to activate covert assets without internet reliance. “The signals could be intended to activate or provide instructions to prepositioned sleeper assets operating outside the originating country,” the alert stated.

Concerns are heightened by reports of Iranian-linked operatives using routes like Venezuela to enter Western nations, potentially establishing networks near the U.S.

Security experts warn of threats from both organized cells and lone actors. Former DHS adviser Charles Marino told the Daily Mail that simultaneous attacks by 10-20 people in a cell are possible, targeting soft spots like concerts or sporting events. The upcoming World Cup, a National Special Security Event, is a particular worry.

Tensions escalated further with Iran’s defiant response to President Trump’s comments on the new supreme leader. Trump stated on Fox that Mojtaba Khamenei would be unable to “live in peace” and expressed dissatisfaction with the appointment, warning Iran to brace for “death, fire and fury” if it shuts the Strait of Hormuz.

Iran’s security chief Ali Larijani dismissed these as “empty threats,” adding, “Even those greater than you could not eliminate the Iranian nation. Take care of yourself not to be eliminated!”

Iran tells Trump ‘be careful not to be eliminated’ and hits back at ’empty’ threats after US President said he does not believe new Supreme Leader can ‘live in peace’ https://t.co/CJYC7iGxIT

— Daily Mail (@DailyMail) March 10, 2026

This exchange follows the conviction of Asif Merchant, a Pakistani national trained by Iran’s IRGC, for plotting to assassinate Trump during the 2024 race. Merchant was found guilty days ago, with the plot linked to revenge for Qasem Soleimani’s 2020 killing.

In a related development, Merchant told FBI agents he suspected Iran was behind the July 13, 2024, Butler assassination attempt on Trump. He claimed it mirrored his own scheme, orchestrated under IRGC coercion with threats to his family.

Prosecutors allege Merchant recruited hitmen targeting U.S. politicians, including Trump, Biden, and Haley. During his trial, he handed $5,000 to undercover agents. U.S. strikes have since killed the IRGC leader behind the plot, as announced by Defense Secretary Pete Hegseth.

Hegseth described it as the “most intense day” of attacks on Iran, with refined intelligence leading to more strikes. Iran has fired fewer missiles in recent hours, he noted.

Iran’s IRGC announced that countries expelling U.S. and Israeli ambassadors would gain passage through the Strait of Hormuz, amid warnings from Saudi Arabia’s oil company of market “catastrophe” due to disruptions.

Israeli Prime Minister Benjamin Netanyahu stated Israel is “not done yet” in Iran, while warning Lebanese residents ahead of strikes on Hezbollah. French President Emmanuel Macron assured Cyprus of support amid regional strains.

Tehran saw massive airstrikes with “unusually large” explosions, as Trump vowed to end the war “very soon” but indicated further actions. Smoke billowed over the capital, and Iran’s Foreign Minister Abbas Araghchi ruled out resuming U.S. negotiations, citing past betrayals.

Mojtaba Khamenei, reportedly wounded in the conflict and dubbed “vengeful” by some, has ties to the IRGC and is seen as more extremist. Protests in Iran include chants of “death to Mojtaba,” while state media rallies support.

Trump reiterated warnings on Truth Social, promising to hit Iran “twenty times harder” if oil flow is blocked. Iran insists it will determine the war’s end and continue missile attacks as needed.

The Strait of Hormuz remains effectively shut, halting oil tankers and filling storage, spiking global prices and raising economic crisis fears.

These intercepts and threats underscore the precarious security landscape, with potential implications for U.S. safety and international stability as the conflict persists.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Wed, 03/11/2026 – 09:10

https://www.zerohedge.com/geopolitical/iran-sleeper-cells-activated-threaten-eliminate-trump

Lloyd’s Of London Says Gulf Tanker Coverage Available As Strait Chaos Erupts Again

Lloyd’s Of London Says Gulf Tanker Coverage Available As Strait Chaos Erupts Again

What caught the attention of one UBS analyst earlier this morning was a Financial Times report stating that Lloyd’s of London is pushing back against claims that insurers are choking off traffic through the Strait of Hormuz. As we have outlined, tanker flows are beginning to creep higher in the strait by midweek, with some tankers switching off their transponders while transiting the narrow waterway.

Lloyd’s head of underwriting, Patrick Davison, told the FT that the insurance market is “still providing cover to basically anyone who asks,” but stressed that the slowdown in Strait traffic is “not an insurance issue – it’s a question of vessel and crew safety.”

“All the insurers at Lloyd’s are still quoting business, and will still provide cover to basically anyone who asks,” Davison said.

War-risk insurance premiums for any commercial ship transiting the world’s most important energy chokepoint surged well before the conflict and then skyrocketed, with rates now up twelvefold.

Therefore, the real constraint is not so much the insurance as the extreme danger facing tankers, bulk carriers, and container ships, as Tehran threatens vessels with drones, missiles, and water-based mines.

Related:

Insurance As A Weapon: How The Strait Of Hormuz Shapes Global Power And Energy Markets

The US is in the early stages of preparing a potential $20 billion reinsurance backstop to help restart transits through the strait. Underwriters in London learned of the US plan only recently and question whether it will ever be launched.

Last week, an FT report said the US Development Finance Corporation will create a $20 billion reinsurance facility to restart maritime cargo and oil commerce. There are other reports that the US could use its naval power to shadow commercial vessels in the waterway.

However, a Reuters report states that those military escorts are not yet ready, and that near-daily US military requests from tankers have been denied this week.

Chaos in the Strait continued in the overnight hours, with a Reuters report saying three vessels had been hit by unknown projectiles.

BREAKING:

Iran strikes a Thai ship attempting to pass through the Strait of Hormuz.

Thai authorities said the bulk carrier Mayuree Naree, sailing under the Thailand flag, was struck by projectiles while travelling about 18km north of Oman.

— Visegrád 24 (@visegrad24) March 11, 2026

That explains that.

*IRAN WON’T ALLOW A SINGLE LITER OF ‘HOSTILE OIL’ TO PASS HORMUZ

*IRAN SAYS STRIKES TO BE CONTINUOUS FROM NOW ON: FARS

*IRAN MILITARY SAYS POLICY OF RECIPROCAL STRIKES IS OVER: FARS

— zerohedge (@zerohedge) March 11, 2026

By now, readers understand how critical the Hormuz chokepoint is, as it serves as a key energy artery for about 20% of global oil and gas supply. Since Operation Epic Fury, energy supplies across the Gulf area have dramatically slowed, prompting panic among G-7 leaders and the IEA, who are set to release their plan to release the “largest ever” SPR dump onto markets to cap Brent and WTI prices.

Tyler Durden

Wed, 03/11/2026 – 08:50

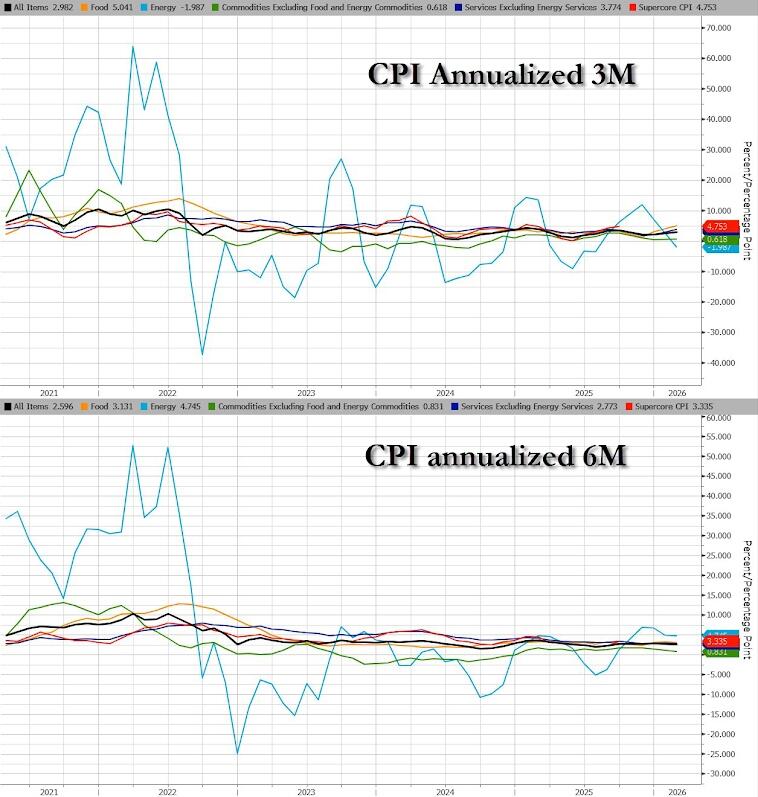

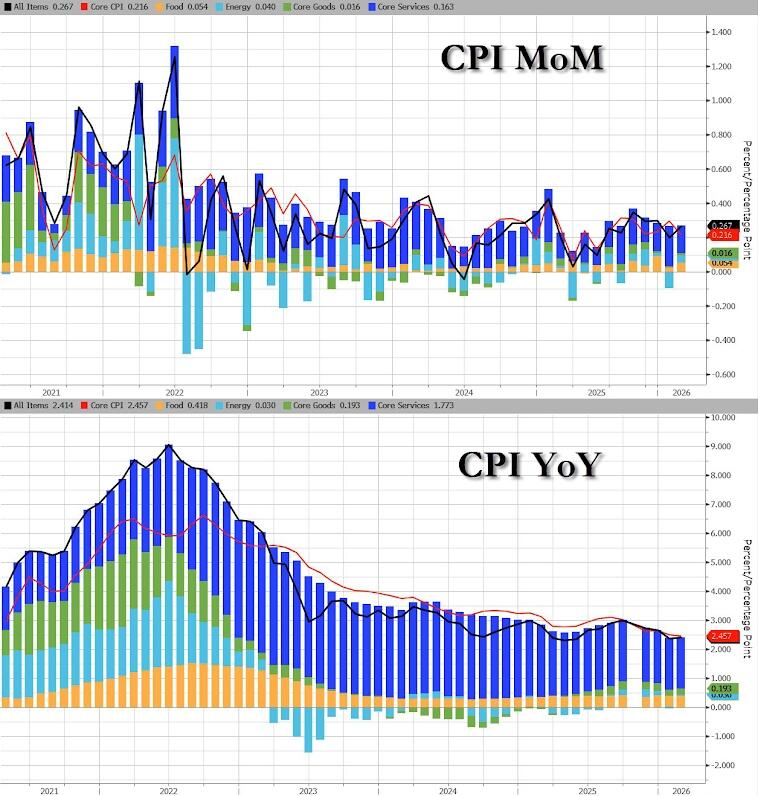

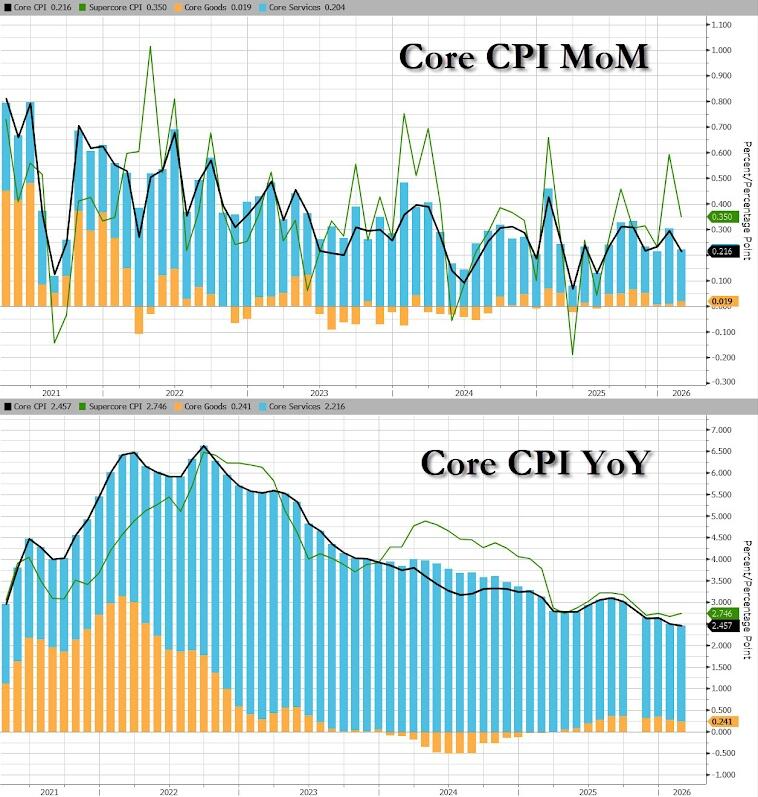

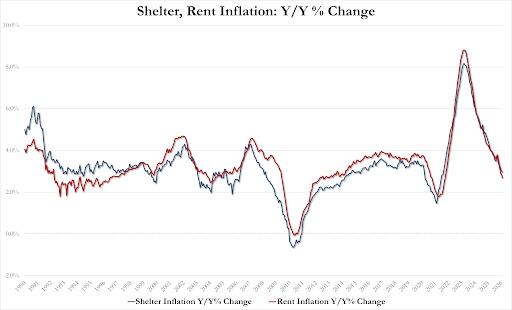

US Core CPI Tumbles To Slowest In 4 Years (Before Iran-Triggered Oil Spike)

US Core CPI Tumbles To Slowest In 4 Years (Before Iran-Triggered Oil Spike)

While all attention is currently on Iran (and the energy impact of actions overseas), today’s CPI (for February) should not be affected by the recent surge in WTI (but March’s data definitely will be)…

Source: Bloomberg

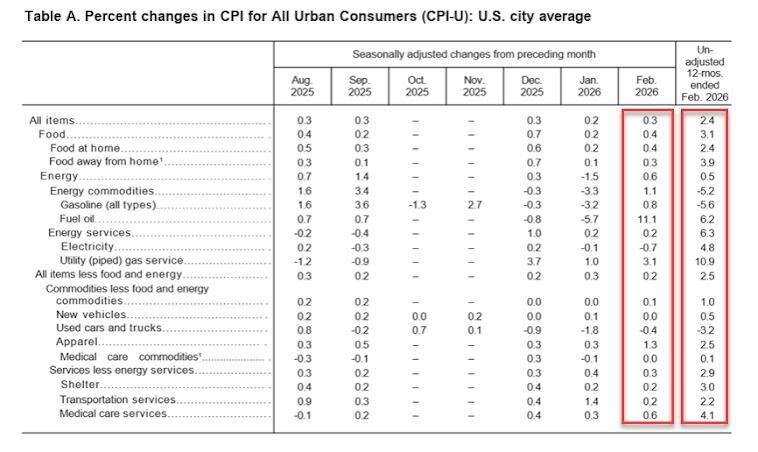

Headline CPI rose 0.3% MoM (as expected), lifting prices by 2.4% YoY (unchanged from the prior month at the lowest since May 2025)…

Source: Bloomberg

The disinflation trend is still your friend as the terrors of tariff-flation remain non-evident, much to the disappointment of establishment economists.

Core Services remain the biggest driver of CPI with Core Goods relatvely unmoved (and Energy starting to pick up)…

CPI rose 0.3% MoM after rising 0.2% MoM in January, and in line with estimates. Over the last 12 months, CPI rose 2.4%, also in line with estimates and unchanged from January.

The index for shelter rose 0.2 percent in February and was the largest factor in the all items monthly increase. The food index increased 0.4% over the month as did the food at home index, while the food away from home index rose 0.3% . The index for energy also increased in February, rising 0.6 percent.

Core CPI also met expectations with a +0.2% MoM move, leaving prices up 2.45% YoY – the lowest since March 2021

Source: Bloomberg

Core CPI Services are also the main driver of Core CPI (but are seeing significant disinflation)…

Core CPI rose 0.2% MoM in February; Over the last 12 months, core CPI rose 2.5%, also in line with estimates and unchanged from January.

Indexes that increased over the month include medical care, apparel, household furnishings and operations, airline fares, and education. Conversely, the indexes for communication, used cars and trucks, motor vehicle insurance, and personal care were among the major indexes that decreased in February.

The energy index increased 0.5% for the 12 months ending February. The food index increased 3.1% over the last year.

Some more details on the core print

The index for all items less food and energy rose 0.2% in February, following a 0.3% increase in January.

The shelter index increased 0.2% over the month as did the owners’ equivalent rent index.

The index for rent increased 0.1% in February, the smallest 1-month increase in that index since January 2021.

The lodging away from home index rose 1.0% over the month. The medical care index increased 0.5% in February, after rising 0.3% in January.

The index for hospital services increased 0.6% over the month and the index for physicians’ services rose 0.3%.

Conversely, the prescription drugs index decreased 0.2% in February

The index for apparel increased 1.3% over the month, after rising 0.3% in January. The household furnishings and operations index rose 0.3% in February and the airline fares index rose 1.4%.

The index for education rose 0.2% over the month.

The new vehicles index was unchanged in February.

The communication index declined 0.5% in February and the used cars and trucks index decreased 0.4% over the month.

The index for motor vehicle insurance decreased 0.3% in February and the index for personal care fell 0.2%

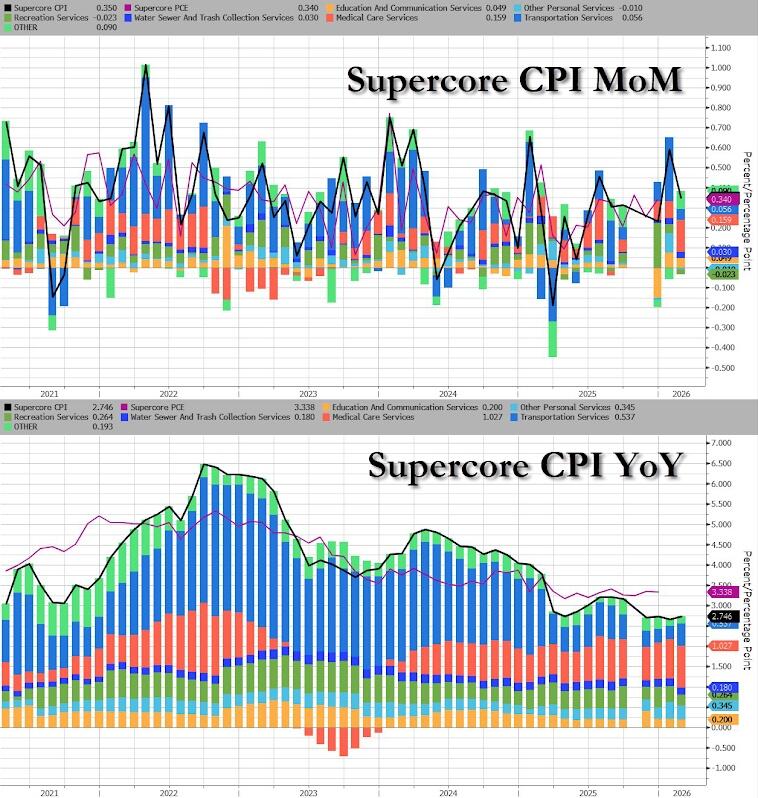

SuperCore CPI (Services ex-Shelter) lifted very modestly on a YoY basis with Medical Care Services the biggest driver…

While typically, a hot (or cold) CPI would drive stocks and bonds dramatically, we remain beholden to the slings and arrows of outrageous crude oil price fortune (for now) with rate-cut odds remaining near recent (hawkish) cycle lows.

Interestingly Fuel Oil costs soared MoM…

Both Goods and Services costs are signaling disinflation (ahead of March’s potentially explosive moves)…

The question is – how long will the impact of soaring energy costs impact CPI?

Is it different this time?

The policy sensitive two-year yield was around 1.5 basis points higher at 3.605% after the report, while swaps linked to Fed meeting dates implied traders see 34 basis points of easing this year, versus around 35 basis points earlier in the session. The market continues to price the first full quarter-point reduction arriving in September or October.

Longer-dated Treasuries were under more pressure, with the yield on 10-year notes two basis points higher at 4.18%. Later in New York, Treasury will sell $39 billion of the current 10-year issue.

Tyler Durden

Wed, 03/11/2026 – 08:39

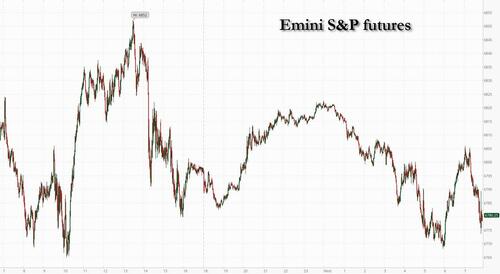

Stocks Drop As Oil Rebounds Over $90 On Escalating War, Ignoring Looming SPR Release

Stocks Drop As Oil Rebounds Over $90 On Escalating War, Ignoring Looming SPR Release

US equity futures remain extremely illiquid, jittery and volatile, and are down 10bps near the morning lows, erasing a 0.5% gain after earlier rebounding on hopes the upcoming SPR release will keep oil lower (it has so far failed to do that). Global equities saw a leg lower during APAC hours following an FT report that JPMorgan is marking down private credit portfolios. Mixed messaging from the Trump administration has helped fuel sharp swings in volatility gauges, with the VVIX jumping 10 points on Tuesday. As of 8:10am ET, S&P and Nasdaq futures are down 0.1%, as Oracle’s 10% climb in the pre-market offers support to the AI trade, while inflation is back in focus with today’s CPI print. The ORCL print supports optimism across the secular AI data center trade with focus on raised FY27 rev guidance on management’s expectations for continued expansion in AI and advanced compute demand. Asia is leading overseas with TWSE up 410bps, NKY up 143bps, Europe flat to lower led on the downside by Germany down 67bps. In commodities, crude up 300bps feels like a non-event vs. intra day swings over the last seven trading days. Oil does, however, remain in focus as strikes continued across the Middle East overnight, with the UK Navy noting three vessels were hit in the Strait of Hormuz and the Persian Gulf. The IEA is proposing a record release of up to 400 million barrels of emergency oil reserves — more than double the amount deployed after Russia’s invasion of Ukraine. However, as explained here, it is unlikely the release will do much for a sustained drop in prices. Moves elsewhere in commodities benign. Yields elevated ahead of CPI with 10-year at 4.17%, dollar bid back with DXY at $99 and Bitcoin lower down 1% just below $70k. German CPI in line at +1.9%. We’ll get US CPI at 8:30am ET this morning.

In premarket trading, Magnificent Seven stocks are mixed (Alphabet -0.1%, Amazon +0.1%, Meta -0.01%, Nvidia +0.2%, Apple +0.1%, Microsoft +0.1%). Tesla rises 0.2% after Business Insider reported that the company is ramping up an AI agent project

AeroVironment (AVAV) falls 10% after the drone maker cut its revenue guidance for the full year. Analysts trim their price targets, while Citizens noted that some of the weakness stems from defense deals getting delayed.

Campbell’s Co. (CPB) falls 5% after the food company cut its adjusted earnings per share guidance for the full year.

Domo (DOMO) rises 38% after the enterprise software company’s fourth-quarter results beat expectations.

Nike (NKE) gains 2% after Barclays upgraded the sportswear retailer to overweight, citing recent operational progress, financial inflections and management’s disciplined actions.

Oracle (ORCL) rises 9% after the company posted strong results and gave an outlook that suggested there is little letup in demand for AI computing.

Serve Robotics Inc. (SERV) climbs 12% after the developer of AI-powered delivery robots posted fourth quarter results. Also, the company and White Castle launched a delivery pact via Uber Eats.

UniFirst Corp. (UNF) rises 8% after Cintas Corp. agreed to buy the uniform maker in a cash-and-stock deal valued at $5.5 billion

Upstart (UPST) rises 2% as the firm plans to apply for a US national bank charter, aiming to reduce costs and streamline its AI-based lending platform

In other AI news, the Chinese government moved to curb the usage of OpenClaw for banks and state agencies amid a user rush to adopt the AI agent. Amazon is making its debut in the euro bond market with a record eight-part sale, with maturities ranging from two to 38 years, following the 11-part dollar sale on Tuesday to fund AI investments. Elsewhere, Nintendo surged due to the surprise success of its new Pokémon game.

US futures are struggling for direction and Brent climbed back above $90 a barrel as an expected record release of crude stockpiles failed to lift sentiment amid attacks on vessels in the Middle East, simply because it will do little to offset the daily supply taken out by the Strait blockade. Volatility continued to grip equities, with S&P 500 contracts erasing a 0.5% advance, and it’s nowhere near over: equities are “set for days of upcoming volatility, as the conflict in the Middle East is far from being resolved,” according to Roland Kaloyan, head of European equity strategy at Societe Generale adding that “Moving forward, there are high chances of seeing alternating risk‑on and risk‑off days.” The “markets’ starting point from when the conflict began was quite high so it’s also some excess optimism being cut to risk premiums which appears closer to what we perceive as the fundamentals.”

Sentiment was also dented as JPMorgan restricted some lending to private credit funds after marking down the value of certain loans in their portfolios, the latest sign of stress in the $1.8 trillion industry.

As the Iranian conflict rages on with no sign of de-escalation, the UK Navy said three ships were attacked in the Strait of Hormuz and the Persian Gulf. Governments are seeking to contain the spike in energy prices, with the International Energy Agency proposing a release of emergency oil reserves of as much as 400 million barrels, according to a person familiar.

“It’s helpful, but it’s more a short-term fix,” said Richard Saldanha, global equity fund manager at Aviva Investors. “The reality is, the way we’re going to avoid any kind of long-term shock is the Strait of Hormuz re-opening again.”

In the latest oil news, the IEA will propose the biggest-ever release of oil reserves. The potential 400 million barrels would cover days of global demand. OPEC’s monthly deep-dive analysis on the global crude market will likely draw more attention than usual.

The US CPI print will be closely watched as stagflation concerns resurface. Bloomberg Chief US Economist Anna Wong expects the reading to be “unseasonally tame,” citing disinflationary effects from several heavily weighted components, while two new supply shocks – in metals and memory chips – were building pre-Iran. Derivatives strategists at Barclays say the S&P 500’s implied move for Wednesday is materially higher than recent history with the forward volatility term structure having shifted higher amid market stress.

The consumer price index report is projected to show a core inflation measure, which strips out volatile food and energy costs, rising 0.2% last month. That would suggest some easing in price pressures before the outbreak of the war. Money markets are leaning toward a Federal Reserve rate cut in July and the possibility of a second move in December.

“Even with geopolitics in the foreground, investors still want CPI to validate the ‘disinflation-with-room-for-cuts’ narrative rather than re‑ignite a sticky‑inflation scare,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg.

Inflation expectations are building in international markets with European assets facing challenges because cost pressures concerns have soared rapidly, and an ECB rate hike is potentially closer than thought, according to Governing Council member Peter Kazimir.

The Stoxx 600 fell 0.4% to 603.44 with 417 members down, 171 up. The upside in energy prices and mounting bets that the ECB will hike rates have knocked European stocks lower with the Stoxx 600 down 0.8%, although off the lows of the day as oil trimmed gains; retail and automotive stocks outperforming, while industrial goods and real estate underperforming. Here are the biggest movers Wednesday:

Balfour Beatty shares surge as much 13% to a record high after the construction group announced better profits and a larger buyback than expected

Inditex shares gain 5.2%, outperforming European peers, after the Zara parent reported strong results for 2025 and gave a trading update for 1Q that analysts called “reassuring.” Shares are 2.8% lower YTD

Orlen gains as much as 4.2% to the highest since Nov. 2017 after PKO and Santander both raised the Polish energy group to buy, expecting higher refining and gas margins from disruptions in the Middle East

Avolta shares climb as much as 4.6% after the travel retailer reported solid results, announced a buyback and confirmed its 2026 outlook, despite uncertainty caused by conflict in the Middle East

Wacker Chemie shares rise as much as 10% after the German chemicals firm posted better-than-expected guidance for 2026 on the back of its semiconductor polysilicon unit and cost savings

Elis shares rise as much as 7.7%, the biggest jump in 11 months, after the workwear specialist delivered in-line results and outlined a bigger buyback for this year than expected

CVC Capital shares fall as much as 7.4% to a new low as the private equity and investment advisory company cuts guidance for performance-related earnings again

Legal & General shares fall as much as 6.2%, the most in 11 months, as the insurer and asset manager’s solvency ratio, an indication of financial strength, proves lower than expected

Rheinmetall shares fall as much as 6.3% after the German defense company’s sales outlook fell short of analyst expectations. Oddo BHF says the print is slightly disappointing when it comes both to results and 2026 guidance

Canal+ shares drop as much as 21%, the sharpest fall on record, as challenges at newly-acquired MultiChoice Group weigh on sentiment and detract from positive trends in the rest of the business

Galenica shares fall as much as 5.3% after UBS lowers earnings per share expectations for the Swiss pharmacy operator through 2028, citing a weak flu season and the strong franc

BW LPG falls as much as 10%, the most in almost nine months, after DNB Carnegie gives the maritime gas transportation company its only sell rating and sets a new Street-low PT to reflect an uncertain near-term outlook

Earlier, Asian stocks – which are now due for a painful catch down – rose as oil prices cooled, easing concerns about a major inflation shock for the region’s energy-import-dependent economies. The MSCI Asia Pacific Index gained as much as 2%, adding to Tuesday’s 3.2% advance. Shares of chip giants such as TSMC, Samsung and SK Hynix were among the biggest contributors to the rally after better-than-expected earnings from Oracle Corp., which pushed the cloud infrastructure company’s stock up nearly 10% in extended US trading. Oil climbed back near $90 a barrel after the close of trading in several Asian markets, paring the previous session’s 11% plunge, as vessels in the Middle East came under fire amid ongoing military strikes. Volatility across financial markets continued to be high as mixed messages from the Trump administration over the war in Iran kept investors on edge.

In FX, the Bloomberg Dollar Spot index faded losses as the risk tone deteriorated and is now flat. Aussie dollar is the clear outperformer across the majors as traders expect the RBA to deliver another rate hike next week.

In rates, treasury yields nudged higher ahead of the February inflation print; long-end yields are about 2bps higher as oil advance weighs globally. US front-end yields are little changed, slightly extending Tuesday’s curve-steepening move; 10-year near 4.17% is higher by less than 2bps with German and UK counterparts cheaper by 5bp and 7bp. European bonds plunged as a central bank official warned the Iranian war could force an earlier-than-expected interest-rate hike. Front-end bonds in Europe remain under pressure with German and UK two-year yields adding 8bps and 10bps respectively. Focal points of US session include February CPI report and $39 billion 10-year auction. Corporate new-issue slate may include Salesforce with a jumbo offering following Tuesday’s single-day volume record.

In commodities, brent crude futures are up 3.4% and largely shrugging off news that the IEA has proposed a 300-400 million barrel reserve release. Spot gold is flat, while silver declines 1.8%. Bitcoin is down 1%.

US economic data slate includes February CPI (8:30am) and federal budget balance (2pm)

Market Snapshot

S&P 500 mini -0.1%,

Nasdaq 100 mini -0.1%,

Russell 2000 mini -0.5%

Stoxx Europe 600 -1%,

DAX -1.6%,

CAC 40 -1%

10-year Treasury yield +1 basis point at 4.17%

VIX +0.8 points at 25.73

Bloomberg Dollar Index little changed at 1200.97,

euro -0.1% at $1.1596

WTI crude +5.2% at $87.79/barrel

Top Overnight News

Iran has begun laying mines in the Strait of Hormuz, the world’s most important energy chokepoint that carries about one-fifth of all crude oil, according to two people familiar with US intelligence reporting on the issue. The mining is not extensive yet, with a few dozen having been laid in recent days. CNN

The IEA is proposing a record release of up to 400 million barrels of emergency oil reserves — more than double the amount deployed after Russia’s invasion of Ukraine, a person familiar said. Japan is set to release oil reserves by itself as early as Monday, NHK reported, citing PM Sanae Takaichi. BBG

The Trump administration believes it can withstand a brief spike in oil prices — for as many as four weeks, as one person close to the White House suggested — before the political hit does lasting damage. Politico

JPMorgan Chase has clamped down on its lending to private credit groups, with bankers looking to cut risks as concerns mount over the credit quality of companies in their stables.

Global bonds face more declines as traders bet inflation fallout from the Iran war will push central banks to raise rates. Markets are pricing two hikes in Australia and see the BOJ and ECB among candidates to also tighten. BBG

Lebanon’s Hezbollah is applying lessons from its last war with Israel as it braces for a possible full-scale Israeli invasion and protracted conflict, returning to its roots in guerrilla warfare in south Lebanon, four Lebanese sources said. RTRS

The UK Navy said three vessels were hit in the Strait of Hormuz and the Persian Gulf. BBG

China moved to restrict government agencies and state firms from running OpenClaw AI apps on office computers. BBG

ECB’s Christine Lagarde said policy makers will ensure the Iran war doesn’t cause the same inflation surge as Russia’s Ukraine invasion did. BBG

Senators Warner (D) and Rounds (R) are to introduce new legislation focused on AI and the workforce: Axios

CPI Preview from Goldman: Expect a 0.17% increase in February core CPI (vs. +0.2% consensus), corresponding to a year-over-year rate of 2.42% (vs. +2.5% consensus). Expect a 0.18% increase in headline CPI (vs. +0.3% consensus), reflecting higher food (+0.1%) and energy (+0.5%) prices. GS forecast is consistent with a 0.24% increase in core PCE in February.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher as the recent easing of oil prices helped the region shrug off the lacklustre lead from Wall Street and reports of Iran beginning to lay mines in the Strait of Hormuz. ASX 200 gained with strength in mining, resources, materials and financials, front-running the advances, but with upside capped amid increased bets for the RBA to hike rates at next week’s meeting following recent central bank rhetoric and calls by some of Australia’s largest banks for consecutive rate increases in March and May. Nikkei 225 rallied following the recent easing of oil price pressures and as softer-than-expected PPI data, which showed a surprise monthly deflation, supports the case for a delay in BoJ policy normalisation. Hang Seng and Shanghai Comp lagged amid quiet catalysts and with Chinese officials said to be frustrated by what they see as insufficient US preparation for the Trump-Xi summit later this month, while China also moved to curb the use of OpenClaw AI by banks and state agencies.

Top Asian News

Japan’s government is considering measures amid Middle East tensions and will announce gas and utility price measures at an appropriate time, according to Nikkei.

European bourses (STOXX 600 -1.0%) are entirely in the red, as the Iran conflict intensifies. Losses in the IBEX 35 (-0.4%) have been limited after positive Inditex (+0.8%) earnings, which beat Q4 EBIT estimates and boosted capex following a strong start to 2026. The DAX 40 (-1.2%) underperforms after Rheinmetall (-6.2%) missed FY net income and guided softer 2026 revenue than analysts expected. European sectors are broadly weaker across the board, as Energy (+0.3%) continues to gain. Real Estate (-1.3%) and Financial Services (-1.3%), alongside Industrial Goods and Services (-1.8%), sit at the bottom of the pile, with higher yields and risk tone weighing on the sectors.

Top European News

European Commission draft Citizens’ Energy Package recommends concrete measures to lower household energy prices, Handelsblatt reported; aim is to lower electricity taxes to a minimum.

Central Banks

ECB’s de Guindos said risks are tilted to the downside, macroeconomic projections will be much more complicated now.

ECB’s Kazaks said the ECB could act if war raises inflation expectations.

ECB’s Kazimir said a rate hike on Iran may be closer than thought; no reason to act at next week’s meeting.

ECB’s Villeroy said he does not expect a rate hike at next week’s ECB meeting, said energy costs are a minor part of consumer spending, said banks should stay calm amid the Iran crisis.

ECB’s Nagel said the ECB will act decisively if an energy spike feeds into durably higher inflation; the risk of higher inflation has risen, economic outlook has deteriorated; the latest US statements on Iran war offer cause for hope.

Westpac and National Australia Bank now expect the RBA to hike rates in March and May.

FX

DXY is choppy this morning; currently trading around the unchanged mark, within a narrow 96.69-99.07 range. Little fresh from a European perspective, as focus remains on newsflow out of Iran. As it stands, the current conflict is showing few signs of ending, with reports now suggesting that Iran is taking steps to lay mines in the Strait of Hormuz. On the energy front, the IEA Governing Board is meeting today, whilst a separate G7 discussion on energy coordination is also scheduled for 14:00 GMT today. It was recently reported that the IEA proposed a 300-400mln barrel release of stockpiles – sources suggest that, should there be no objections, it could be announced as soon as today. Focus later will also be on US CPI, though it may lack signalling capacity given the current geopolitical situation.

The Aussie extends on recent outperformance, as more banks now expect the RBA to hike rates at next week’s meeting. NAB and Westpac are the latest banks seen supporting a hike, joining the likes of Goldman Sachs and Bank of America. Delving into Westpac briefly, the bank previously forecast a hike in May, but the analysts now believe that the RBA will be “compelled to react” to the recent strength in oil prices. AUD/USD currently trades towards the upper end of a 0.71154 to 0.7185 range.

Other G10s are trading modestly on either side of the unchanged mark vs the USD. The Loonie posts mild gains, given today’s strength in oil prices, whilst the JPY is the slight laggard, joined by the EUR. USD/JPY is venturing back into the touted “intervention zone”, beyond the 158.00 mark – though desks question the efficacy of intervening as the Iran war continues. GBP is essentially flat, awaiting cues from the Treasury Committee, which will question the Chancellor Reeves on the Spring Statement. BoE’s Breeden is also set to speak.

For the EUR, currently trades just above the 1.1600 mark, within a 1.15904-1.1645 range. Today, there was a slew of ECB speakers, with particular focus on Kazimir who suggested that a rate hike on Iran may be closer than thought. This spurred some very modest upside in the EUR at the time, but was ultimately short-lived, given that he stated there is no reason to move rates at the next meeting.

Fixed Income

APAC trade for fixed income was for the most part rangebound, with USTs and Bunds holding a handful of ticks in the red. JGBs also opened under pressure, with downside of 20 ticks at most. However, the move proved short lived as strong demand at the 5yr JGB tap underpinned the benchmark and lifted it to a 131.98 high, just shy of yesterday’s 132.01 best.

While relatively contained at first, EGBs came under renewed pressure early doors following ECB speak and a further uptick in energy benchmarks. Sending Bunds to a 126.55 trough over the course of the morning. On the former, Kazimir said an Iran-related rate hike could be closer than thought, though clarified that there is no reason to act in March. Near term market pricing has seen a very slight hawkish move this morning, but more pertinently end-2026 pricing implies around 25bps of tightening.

In geopols, the UKMTO update seemingly spurred another leg higher in the crude space, with additional impetus potentially coming from the ongoing reporting around but lack of action on a reserve release.

Moving to Gilts, the benchmark opened lower by over 50 ticks and has since slipped another 30 or so to a 90.27 base. Currently lagging, posting downside of 78 ticks vs 63 for Bunds. Action is very much occurring in tandem with the EGB move. Additionally, the UK has a packed agenda with Chancellor Reeves discussing her Spring Statement with the TSC, the release of Mandelson-related files by the government (around 12:30GMT) and then an appearance from BoE’s Breeden, however this is scheduled to be on stablecoins.

Vnet (VNET) , China’s largest data centre operator, is considering a dollar bond sale to fund expansion, Bloomberg reported citing sources.

Amazon (AMZN) opens books on eight-part EUR denominated bond offering.

Japan sold JPY 1.9tln 5yr JGBs; b/c 3.69x (prev. 3.10x), average yield 1.633% (prev. 1.640%).

Australia sold AUD 1bln 4.25% October 2036 bonds, b/c 3.87, avg. yield 4.9002%.

Commodities

WTI and Brent front-month futures have been grinding higher since early European hours following a choppy APAC session and the declines seen during the prior session. Yesterday, there was a bout of selling pressure after US Energy Secretary Wright mistakenly posted that the US Navy escorted an oil tanker through the Strait of Hormuz, although oil then pared some of the losses as the post was deleted shortly after, and the White House confirmed that this was false.

Note, the IEA Governing Board is meeting today, whilst a separate G7 discussion on energy coordination is also scheduled for 14:00 GMT today. It was recently reported that the IEA proposed a 300-400mln barrel release of stockpiles – sources suggest that, should there be no objections, it could be announced as soon as later today.

Spot gold holds an upward bias on either side of the USD 5,200/oz level, with the precious metal kept afloat alongside the recent easing in oil price pressures, although DXY has clambered off worst levels as eyes remain on flows in the Strait of Hormuz. A deterioration in sentiment in early European hours cushions downside for the yellow metal for now, which resides in a narrow USD 5,175.35-5,223.38/oz at the time of writing.

Copper futures traded rangebound overnight but then slipped in early European hours amid a broader deterioration of sentiment as the Iranian war shows no signs of ending despite recent commentary from US President Trump. 3M LME copper is back under USD 13,000/t and resides towards the bottom end of a USD 12,993.00-13,151.53/t at the time of writing.

G7 statement said the group is vigilantly monitoring the energy market, and G7 supports in principle the use of strategic oil reserve.

IEA to recommend the release of strategic reserves, according to sources; volume in the first month would reportedly exceed 100mln barrels.

IEA reportedly proposed oil stockpile release of around 300-400mln barrels, according to Bloomberg; decision is possible later on Wednesday, said a source.

IEA has proposed the largest ever release of oil from strategic reserves to bring down the price of crude, according to WSJ. “Countries would decide Wednesday whether to release oil stocks in an attempt to tame crude prices”. “The release would exceed the 182 million barrels of oil that IEA member countries put onto the market in two releases in 2022 when Russia launched its full-scale invasion of Ukraine”.

As part of a potential 400mln barrel IEA crude release, Germany would release around 19.5mln barrels, Handelsblatt reports citing sources; equating to around 20% of Germany’s reserves

Black Sea CPC blend oil exports were reportedly revised down to around 1.4-1.5mln BPD for March (prev. 1.7mln BPD)

White House reportedly believes it can “withstand a brief spike in oil prices — for as many as four weeks… before the political hit does lasting damage”, according to Politico citing sources.

Iraq’s oil ministry has sent a letter to the Kurdistan regional government for the export of at least 100k BPD via the Kurdistan pipeline to Turkey’s Ceyhan, according to oil officials.

EU Commission President von der Leyen said Europe’s dependency on fossil fuels have cost it EUR 3bln in extra costs in the first 10 days of the Iran war, returning to Russian fossil fuels in the current crisis would be a strategic blunder. EU is preparing options to lower energy prices, which include better use of purchase power agreements and CFDs, state aid measures, gas price subsidies or caps.

Maersk (MAERSKB DC) CEO tells the WSJ that 10 ships are trapped in the Persian Gulf and would need at least 10 days to resume normal operations if a ceasefire was to occur.

Glencore (GLEN LN) workers reportedly set to conduct a strike at Australian copper refinery, according to Bloomberg.

Geopolitics

Iran’s Joint Command Spox said US and Israeli banks will be hit after an attack on an Iranian bank, via IRNA.

Iran’s IRGC said it carried out its heaviest and most intense attacks since the start of the war, targeting US and Israeli assets across the region, according to WSJ.

IRGC said it launched missiles carrying 2-ton warheads in a new wave of heavy, multi-warhead strikes targeting US bases in Iraq and Bahrain as well as Israel.

Iran’s police chief said anyone taking to the streets at the enemy’s request will be confronted as an enemy and not a protester, adds security forces are prepared to respond and have their fingers on the trigger.

Iran launches new wave of missiles on occupied territories.

Iranian armed forces spokesperson vows retaliation for Israeli and US strikes on residential areas.

US officials said Iran has laid less than 10 mines in the Strait of Hormuz and it is unclear if it intends to lay more in the near term, according to WSJ.

Drone reportedly hits a US diplomatic facility in Iraq, according to Washington Post.

US Central Command said US forces eliminated multiple Iranian naval vessels on March 10th, including 16 mine layers near the Strait of Hormuz.

Air defenses shoot down a drone targeting a US military base near Erbil Airport in Iraqi Kurdistan.

Israeli army announces massive wave of raids on Tehran, targeting Iranian regime infrastructure.

UAE Defence Ministry reported air defences are currently intercepting missiles and drones from Iran.

Israel rejects Lebanon’s request for a halt in fighting to allow for talks, according to FT.

UKMTO said it has received a report of an incident 50NM north-west of Dubai, with a bulk carrier hit by an unknown projectile.

Russia’s Kremlin said Istanbul is an possible location for talks next week but there is no specific clarity yet.

North Korea conducted strategic cruise missile tests on Tuesday for a naval destroyer, while Leader Kim said destroyers must be equipped with supersonic weapons, according to KCNA.

US event calendar

7:00 am: United States Mar 6 MBA Mortgage Applications, prior 11%

8:30 am: United States Feb CPI MoM, est. 0.29%, prior 0.2%

8:30 am: United States Feb Core CPI MoM, est. 0.23%, prior 0.3%

8:30 am: United States Feb CPI YoY, est. 2.4%, prior 2.4%

8:30 am: United States Feb Core CPI YoY, est. 2.5%, prior 2.5%

2:00 pm: United States Feb Federal Budget Balance, est. -310b, prior -94.62b

DB’s Jim Reid concludes the overnight wrap

After an extraordinary start to 2026, a small – and possibly brief – pocket of relative calm has returned to markets. I’d stress the emphasis on the word relative. The year has already delivered Venezuela, Greenland, an early year JGB slump, a surge and subsequent slump in gold and silver, IEEPA tariffs being overturned, sharp falls in software and other AI sensitive stocks, private credit fears, major breakthroughs from Claude and Anthropic, and viral, vibe-driven commentary from Matt Shumer and Citrini Research that wiped more than a trillion dollars off global equity markets amid fears of disruption and millions of imminent job losses. We have also seen the KOSPI rise more than 50% in the first handful of weeks of the year, only to fall into a bear market before rebounding. And now we find ourselves in the middle of the Iranian conflict. Have I missed anything? In nearly 31 years of doing this job, I’ve experienced many years dominated by huge headlines and crises, but I don’t think I’ve ever seen the narrative shift so rapidly over such a short period. What is equally impressive is that most asset markets remain healthily positive for the year.

Until we move onto the next big event, markets continue to be driven by volatile news flow around Iran and the outlook for oil flows. Overall, the narrative has shifted towards a cautiously more optimistic tone, even as there’s little sign of an imminent end to the conflict. The improved optimism helped drive a dramatic fall in oil prices, with Brent crude down -11.28% from Monday’s European close to $87.80/bbl, marking its largest one-day decline since March 2022. The 12-month Brent future also fell by -1.93% to $72.05/bbl. After some volatility late yesterday, Brent is slightly lower again this morning and is around -27% below Monday’s intra-day highs but still about +20% above where it was before the US and Israeli strikes against Iran.

While much of the oil decline had come after Trump comments late on Monday, the move extended on Tuesday, notably after Saudi Aramco said it will ramp up crude flows via its pipeline to the Red Sea to 7mb/day within a few days, which would allow it to resume 70% of its usual oil shipments. While redirection of crude via this route was expected, it was still seen as good news as questions remained over its exact capacity. And while reporting over potential mining of the Strait of Hormuz saw oil prices bounce late in the US session, they moved lower again overnight after the Wall Street Journal reported that the IEA (International Energy Agency) has proposed the largest release of oil reserves in history to combat rising prices. IEA member countries are expected to decide on the proposal today, while G7 leaders will also today discuss the response to the crisis, according to Canada’s Mark Carney.

Brent even moved as low as $81/bbl shortly after the European close yesterday as US Energy Secretary Chris Wright posted that the US had successfully escorted an oil tanker through the Strait of Hormuz. However, this post was soon deleted and the White House confirmed that no such operation took place. And not long after, President Trump posted that Iran would face consequences “at a level never seen before” if it placed any mines in the Strait of Hormuz. That came as CNN reported that Iran was beginning to lay mines in the straits. Those headlines saw Brent move back towards $92/bbl, before declining again following the WSJ report on the planned oil reserve release.

Easing oil market stress sparked a strong rally in risk assets yesterday, with the STOXX 600 (+1.88%) recording its best day since last April. And while more concerning headlines late in the US session saw the S&P 500 (-0.21%) erase its gains, futures on the S&P 500 are +0.32% higher overnight. As I started typing this, they were +0.5% higher but an FT story has just been released suggesting JP Morgan have “clamped down on its lending to private credit groups” and have “marked down the value of certain loans in their portfolios”. Asian markets are also off their highs but still up strongly with the Nikkei (+1.99%) and Kospi (+2.52%) leading the gains in Asia this morning.

The volatility late in the US session did mean that the S&P 500 (-0.21%) closed nearly a percentage point off intra-day highs, with the equal-weight S&P 500 seeing a larger -0.82% decline. And the VIX index closed at 24.93, a modest -0.57pts lower on the day and notably above its intra-day low of 22.19. Still, while there remains plenty of caution, financial stress has eased materially since the start of the week when the VIX reached 35 at Monday’s open. And despite the recent volatility, the S&P 500 is still less than 3% from its record high on January 27. Some of the risk premium was also stripped out of other assets, with US high yield spreads tightening by -9bps while the dollar index (-0.35%) recorded its largest daily fall in the past month.

The Mag-7 have played a big role in supporting the relative resilience of US equities, with the index now +1.15% above its levels before the strikes after a +0.38% gain yesterday. The tech mood was also helped by Oracle’s results after the US close last night, with a strong sales forecast sending its stock +8% higher in after-hours trading.

Although developments in the Middle East remained the dominant driver, the latest US economic data also reinforced the picture of resilience. ADP’s weekly private payrolls report showed a four-week average of 15.5k for the period up to February 21, equivalent to around 62k on a monthly basis. Meanwhile, US existing home sales surprised to the upside in February, rising to an annualised pace of 4.09mn (vs 3.88mn expected). These releases helped mitigate concerns following the weakness in last Friday’s jobs report and pushed yields higher. A surge in corporate bonds sales added some upward pressure on yields, with a soft 3yr auction and volatile oil headlines leaving 10yr yields (+6.0bps to 4.16%) at the session’s highs by the close. Treasuries are reversing some of this move overnight, with the 10yr yield down -1.6bps.

US data remains firmly in focus today with the release of the February CPI report. This is a key print, as the recent oil shock has pushed back market expectations for the next Fed rate cut. While the Fed is widely expected to hold rates steady at next week’s meeting, today’s data will help shape expectations for subsequent decisions. Our US economists are watching for tariff related strength in core goods, particularly apparel, alongside recent gains in wholesale used car prices. Overall, they expect headline CPI to rise by +0.27%, boosted by a +1.0% increase in energy prices, keeping the year-on-year rate at +2.4%. Core CPI is forecast at +0.24% month on month, leaving the annual rate unchanged at +2.5%. For more detail, see their full preview here.

In Europe, markets rallied sharply as investors finally had the chance to react to Trump’s comments made after the previous day’s close. All major equity indices surged, including the DAX (+2.39%), FTSE 100 (+1.59%) and CAC 40 (+1.79%). Fixed income markets also saw large moves, as the fall in oil prices prompted investors to rapidly scale back expectations for rate hikes this year. Overnight index swaps are now pricing just 17bps of ECB tightening in 2026, down from 30bps at Monday’s close, while BoE pricing for December moved from pricing 1-2bps of hikes to 16bps of cuts by the close. As a result, 10 year gilt yields dropped by -9.3bps, their biggest daily fall since the reaction to the 90 day tariff delay after Liberation Day last year, while 2 year gilt yields fell -12.3bps. Moves in German bunds were more muted, with the 10 year yield down only -2.0bps to 2.83%, although the 2 year yield declined by a larger -6.4bps. Overall, the backdrop now looks much closer to the scenario outlined by our European economists here, which envisages a moderate and transitory shock rather than one that would prompt ECB tightening.

Early morning data showed that Japan’s wholesale inflation (PPI) slowed for a third consecutive month in February (+2.0% y/y) down from +2.3% in January and coming in slightly below the 2.2% forecast. This moderation was largely facilitated by government fuel subsidies, providing a temporary buffer against rising commodity costs. Nevertheless, economists warn that the benefits may be short-lived due to the escalating oil prices.

Looking ahead, today brings the US February CPI and the federal budget balance. Central bank speakers include the Fed’s Bowman and the ECB’s Guindos and Schnabel. Notable earnings include Telecom Italia, and there is also a 10-year US Treasury auction.

Tyler Durden

Wed, 03/11/2026 – 08:28

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}