Category: News

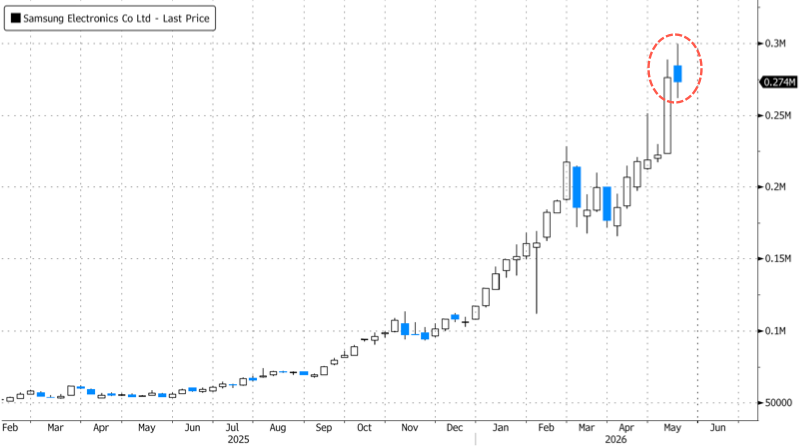

Samsung Strike Threat Sparks Selling Contagion In Memory Stocks

Samsung Strike Threat Sparks Selling Contagion In Memory Stocks

President Trump’s China trip has concluded, with the multi-day summit producing comments from both sides that pointed to warming bilateral relations. As Trump returns aboard Air Force One on Friday morning, traders are shifting focus to overnight turmoil in South Korea, where labor action risks rattled Samsung shares and other memory stocks, and dragged the country’s benchmark KOSPI index lower.

Samsung’s strike is set to formally begin on May 21. Because the company’s semiconductor fabs are already highly automated, the impact on production is expected to be limited. However, there will likely be noticeable disruptions to packaging and logistics, R&D and design, as well… https://t.co/l2ibgeXEIL

— TrendForce (@trendforce) May 15, 2026

“There was pronounced pressure in Asia, with the KOSPI down 6.1%, led by heavy selling in Samsung and SK Hynix. Headlines around a potential 18-day union strike at Samsung further exacerbated weakness across tech,” UBS analyst Zeynep Akkok wrote in a short note to clients.

First time in weeks that Samsung and KOSPI had a down week:

Samsung

KOSPI

Akkok explained that the selling in South Korean tech and memory stocks spread to Europe: “This is feeding directly into Europe, where technology stocks are down 2.7%, and UBS’s semiconductors basket is off 4.2%.”

One of the most aggressive AI melt-ups globally just hit its first real air pocket. Spot-up, vol-up works great…until everybody suddenly realizes they are naked to the downside.https://t.co/YqHKAjyZEP

— The Market Ear (@themarketear) May 15, 2026

Everything you need to know about the labor action theat against Samsung (courtsey of Bloomberg):

Samsung’s largest labor union threatened an 18-day walkout beginning May 21 after government-mediated wage negotiations collapsed on May 13.

The union demands that Samsung scrap existing bonus caps and allocate 15% of operating profits to bonuses, while both sides remain sharply divided over AI-related earnings bonuses.

Samsung CEO Jun Young-hyun and executives met with union leadership on Friday, with Samsung offering unconditional talks and urging swift dialogue.

Samsung reportedly began cutting production on Thursday ahead of the planned strike to prepare for potential quality issues.

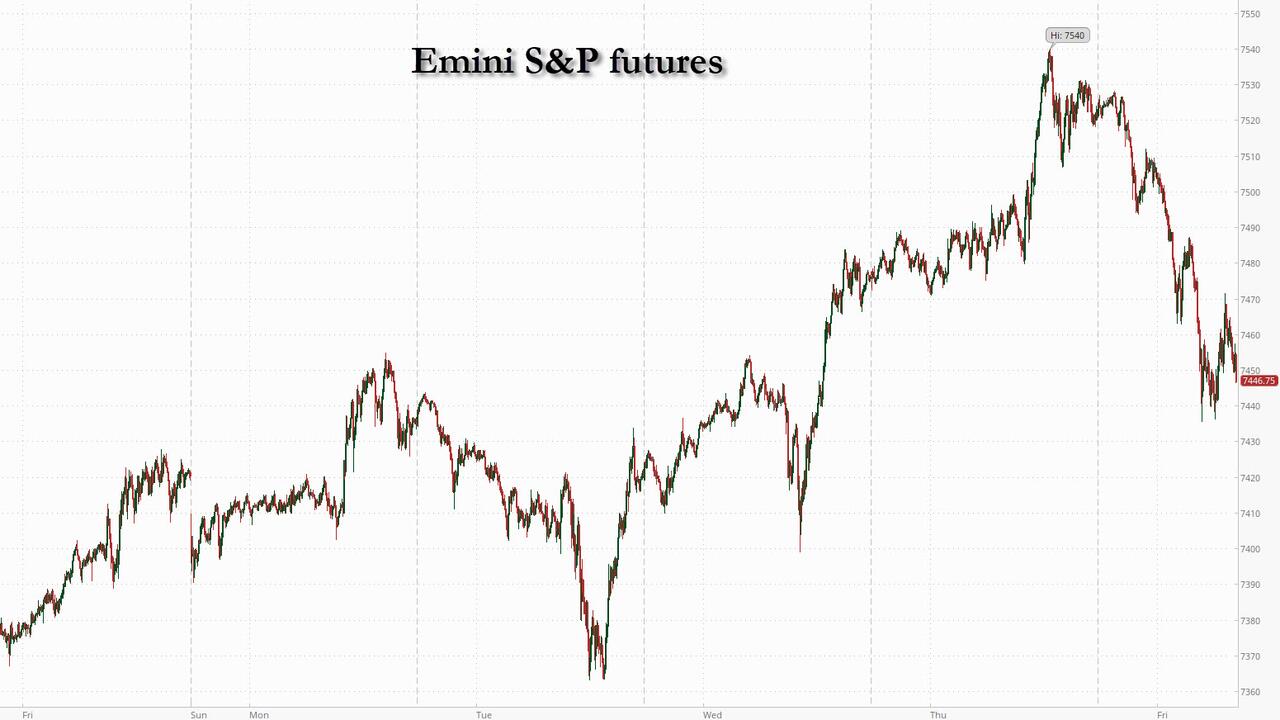

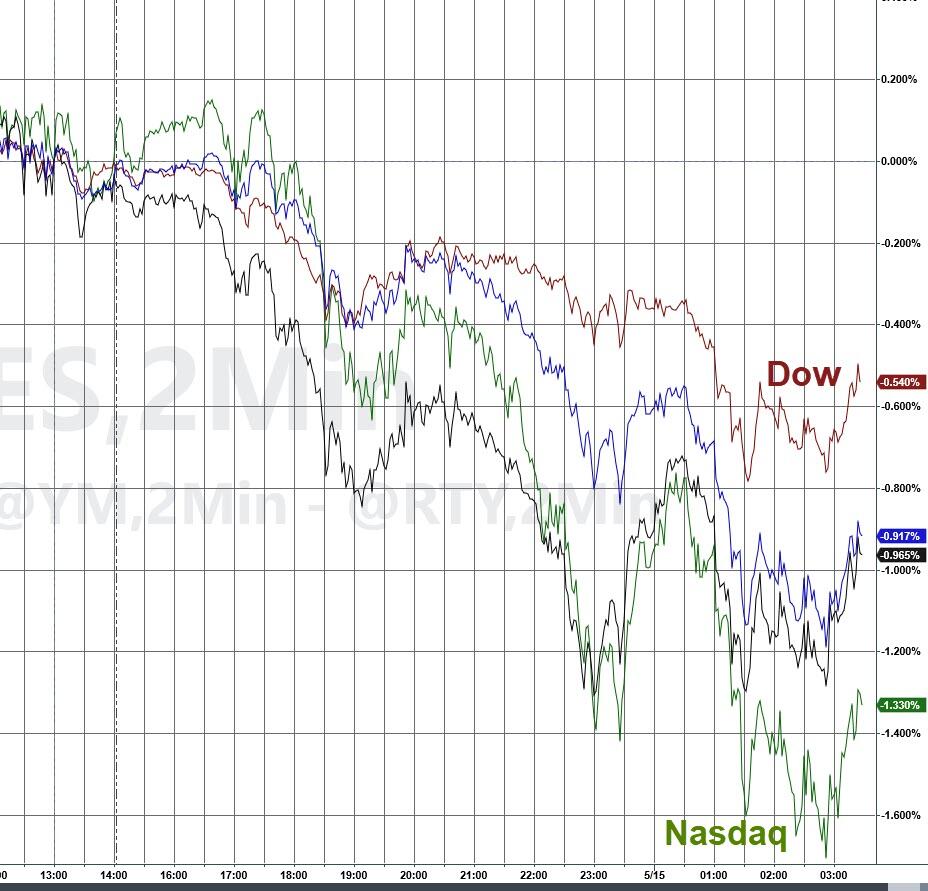

Beyond selling pressure in Asia and Europe, the U.S. is also experiencing a red morning, with Nasdaq futures down 1.6% and S&P 500 futures down about 1.2%.

Among U.S. semiconductor stocks, Nvidia is down 2.6% in premarket trading. Broadcom is down 3%, AMD is down 4%, and Intel is down 5%.

We briefed readers earlier on another bout of selling pressure hitting global markets this morning, including surging Treasury yields and elevated crude prices (read the report here).

Taken together, from memory, stocks soaring and yields higher amid inflation woes, this setup points to a risk-off Friday. That said, traders will be watching closely for any bull-friendly White House comments that could stabilize and provide a relief bid.

Tyler Durden

Fri, 05/15/2026 – 09:05

https://www.zerohedge.com/markets/samsung-strike-threat-sparks-selling-contagion-memory-stocks

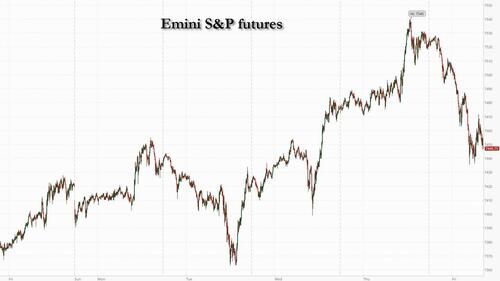

Futures Tumble As Reality Returns And Yields, Oil And Dollar Soar

Futures Tumble As Reality Returns And Yields, Oil And Dollar Soar

Bond yields, oil and the dollar are surging this morning as US futures tumble from all-time highs, with Tech underperforming driven by a series of factors including i) surging energy prices on lack of Iran war progress, ii) elevated positioning into options expiry; iii) Central bank repricing, iv) Tech sell-off driven by higher yields, and v) strikes at Samsung Electronics. The combination of stronger consumption and higher inflation is also a factor today. As of 8:00am ET, S&P futures are down 1.0% and Nasdaq futures slide 1.4% with the momentum brigade of Semis and Memory dumping (that bastion of the memory trade, Korea, sold off last night, its worst day since early March). The losses point to a bleak end to a week in which chipmakers led a narrow rally despite steadily rising yields and the absence of a US-Iran deal. Cyclicals ex-Energy are, unsurprisingly, seeing material underperformance to Defensives. Bond yields are up 4-7bps as the Dollar looks to complete its first 5-day win steak since March. In commodities, Energy is leading with Brent rising 2.3% to above $108 a barrel. Helima Croft, global head of commodity strategy at RBC Capital Markets, said an expectation that the Strait of Hormuz would reopen within the next month was “magical thinking.” Precious metals tumble on dollar strength. Today’s macro data releases are all B-grade, including Empire Mfg, Industrial / Mfg Production, and Capacity Utilization; none are market-moving.

In premarket trading, Mag 7 stocks are mostly lower: Microsoft (MSFT) rises 0.7% after Pershing Square Chief Executive Officer Bill Ackman said he’s taken a new stake in the compan ( Alphabet -1.6%, Amazon -1.5%, Apple -1.2%, Nvidia -2%, Meta -0.7%, Tesla -1.9%)

Dexcom (DXCM) rises 3% after the diabetes device maker gave long-term growth outlook at its investor day that impressed analysts. Separately, activist investor Elliott Investment Management took a stake in the company and struck a settlement that will put two independent directors on the board.

Dlocal (DLO) falls 8% after the emerging markets payment services provider reported first-quarter results that missed expectations in terms of net income and earnings.

Figma (FIG) rises 10% after the creative software platform reported first-quarter results that beat expectations and raised its full-year forecast. Analysts said the report eased concerns about AI-related disruption.

Gemini Space Station (GEMI) gains 21% after the fintech firm announced that Winklevoss Capital Fund has made a $100 million strategic investment in the company, at a price of $14 per share.

Globant (GLOB) climbs 5% after the IT services company reported first-quarter results that beat expectations.

Magnum Ice Cream (MICC) US-listed shares rise 12% after Reuters reported that private equity firms including Blackstone and Clayton Dubilier & Rice are exploring potential bids for the company.

NU Holdings Ltd. (NU) falls 3% after the Brazil-based financial institution reported the cost of credit climbing 72% in the first quarter from the same period a year earlier.

Papa John’s (PZZA) gains 6% after Reuters reported investment firm Irth Capital is working with the pizza chain’s largest US franchisee, who controls around 10% of its domestic restaurants, to take the company private. Reuters cited three sources which it did not identify.

In other corporate news, Kioxia said it would list its shares in the US as it reaps the benefits of a global memory chip shortage that’s ratcheted up prices of the vital component. OpenAI CFO said the ChatGPT maker may raise more capital, as the company races to secure computing power to meet surging AI demand.

A broad selloff in bond markets dragged stocks lower, bringing a sudden halt to the artificial intelligence-fueled equity rally that has pushed the S&P 500 from one record high to the next. The sentiment reversal reflects some profit taking after recent gains, and a lack of concrete progress between Trump and Xi beyond cordial niceties. Also Fed Chair Powell’s term comes to an end today, just as the 10-year Treasury hit 4.5% for the first time overnight since June, prompting a swoon in equity futures.

With a summit between President Donald Trump and China’s Xi Jinping ending without any path to resume flows through Hormuz, the impasse between the US and Iran is moving back into focus. Traders will now watch the next steps the two countries take after more than two months of war.

“There’s no question that momentum has been so aggressive on the upside that the risk of a correction is there,” Paul Skinner of Wellington Management told Bloomberg TV. “With a background of bond markets looking unsettled, with the problem of inflation, with the Strait of Hormuz not having a solution out of that Summit, I think there definitely is some volatility to come.”

Brent crude rose 2.3% to above $108 a barrel. Helima Croft, global head of commodity strategy at RBC Capital Markets, said an expectation that the Strait of Hormuz would reopen within the next month was “magical thinking.”

“There seems to be an emerging consensus that the Strait of Hormuz will reopen in June because the cost of continued closure will be too high,” she wrote. “We are very skeptical. The optimistic scenario seems predicated on the tenuous assumption that there is a relatively easy policy lever that can be pulled.”

In central bank news, the Governor Barr pushed back against proposals to shrink the Fed’s balance sheet, describing them as wrong and a threat to financial stability. The Fed’s Williams said there’s no reason to raise or cut rates right now.

Meanwhile, the turmoil in UK markets is showing no sign of ending as investors price in the possibility of more expansive fiscal policy under a potential successor to Prime Minister Keir Starmer. Manchester Mayor Andy Burnham secured a pathway for a future challenge, unsettling investors who were rattled last year by his comments that the country was “in hock” to bond markets. The prospect of a seventh prime minister in 10 years “is not a record of which any nation would be proud,” said Russ Mould, investment director at AJ Bell. “It is contributing to how the UK has the highest 10-year bond yield in the G7.”

Growing price pressures and a series of key dates next month are setting up the stock market for profit taking, according to Bank of America strategists. Michael Hartnett cited the next OPEC gathering, the start of the World Cup, the Group of Seven summit and the first Federal Reserve FOMC meeting under Kevin Warsh as catalysts. US inflation is on course to exceed 5% by November’s midterm elections unless the 0.4% monthly gains of the past half year slow rapidly. A scenario where inflation climbs above 4% is “where risk assets get twitchy,” Hartnett said. “Bull capitulation into stocks and tech likely fully complete in next few weeks, early June ripe for taking some off table.”

One thing that Xi has that Trump wants is low interest rates, notes BofA’s Michael Hartnett. The strategist had previously said if the 30-year Treasury yield severely breached the 5% threshold, “the door to doom starts to open.” The jury is still out on whether Powell did enough to bring inflation back to target, notes Anna Wong in a Bloomberg Eco Essential Read. The problem is that if macro – and bond yields- actually matters again, then the S&P is about 1000 points too high.

Elsewhere, BofA strategists noted that US large-cap stock funds attracted their largest inflows in five weeks at $24.4 billion, in the week to May 13, citing EPFR Global data. Discussions around positioning and momentum continue at pace. Momentum in large caps is on a tear, with the factor up more than 30% on a long/short basis this year, tracking one of the strongest six-month stretches in more than two decades.

Given the Nasdaq 100’s run-up, it’s worth taking note that the rarely seen “spot up/vol-up” correlation is evident in options. It’s part of the FOMO trade as traders, especially the retail cohort, chase upside through long calls. In a sign of how heated price action has become, the poster child of the AI melt-up, South Korea’s Kospi, touched the 8,000 level before reversing and sinking 7%. All sectors in the benchmark were sharply lower.

In geopolitics, US Trade Representative Jamieson Greer said he anticipates that China would commit to billions in American agricultural purchases. The CIA Director visited Cuba for talks with top leaders as the US grows frustrated over a lack of progress in economic and political change. California Governor Gavin Newsom is proposing a new tax on cloud-based software sales to raise revenue for the state.

European stocks are following their Asian counterparts lower as oil prices rise on concerns that the Strait of Hormuz will remain shut for longer. Miners fall the most while the health care subindex is the leading performer. Stoxx 600 falls 1.2% to 608.54. Here are some of the biggest movers on Friday:

Technoprobe shares rally as much as 39%, the most on record, after the Italian company raised its revenue and margin guidance for 2027 and said it expected to hit those revised targets a year early, indicating soaring demand for its semiconductor probe cards.

Dino Jumps shares jump as much as 18%, the most on record, after the retailer beat first-quarter earnings estimates, with an acceleration in like-for-like sales growth that outpaced competitors. The results should improve sentiment toward the stock, which has fallen nearly 50% over the past 12 months.

Syensqo shares rally as much as 12%, its biggest gain in over 13 months, after the chemicals company reported Ebitda ahead of expectations in the first quarter. Citi said the beat and the improving order book are reassuring investors.

Salvatore Ferragamo shares fall as much as 19% after the luxury goods maker reported first-quarter revenue below analyst estimates. Analysts said Europe remained the weakest region because of the company’s reliance on wholesale, while North America posted strong growth. Ongoing conflict in the Middle East remains a key risk to Ferragamo’s turnaround.

Grafton shares drop as much as 3.8% to trade at a 13-month low, after Citi said tougher trading conditions will weigh on consensus estimates for the building supplies company. Analysts said weakness in the UK is being offset by growth in other regions.

European miners are heavily underperforming on Friday, as copper continues to retreat from the record-high close seen earlier this week. Accelerating US inflation reduced the chance of rate cuts and a stronger dollar make the red metal more expensive for many buyers. Gold is also falling.

The tech sector fueled losses in Europe and Asia too, with the Stoxx 600 falling 1.4%. South Korea’s high-flying Kospi index tumbled 6.1% as investors cashed out of Samsung Electronics Co. and SK Hynix Inc. Nvidia Corp. slid 2.1% in premarket trading after a seven-day streak of gains. Asian equities slid the most since March as higher oil prices fueled concerns over inflation, with heavyweight Korean chip stocks leading the declines after a dizzying rally. The MSCI Asia Pacific Index lost 2.2%, snapping a five-week winning streak. Samsung Electronics and SK Hynix, which contributed to much of Kospi’s roughly 80% rally this year, each dropped over 6% on Friday. Almost all national benchmarks in the region traded lower as Brent crude headed for its biggest weekly advance in three, with efforts to end the Iran war in limbo and the crucial Strait of Hormuz staying effectively closed. President Donald Trump made conflicting remarks on Hormuz, telling Fox News the US doesn’t need the waterway open, and then later saying “we want the straits open” while sitting alongside Chinese leader Xi Jinping in Beijing.

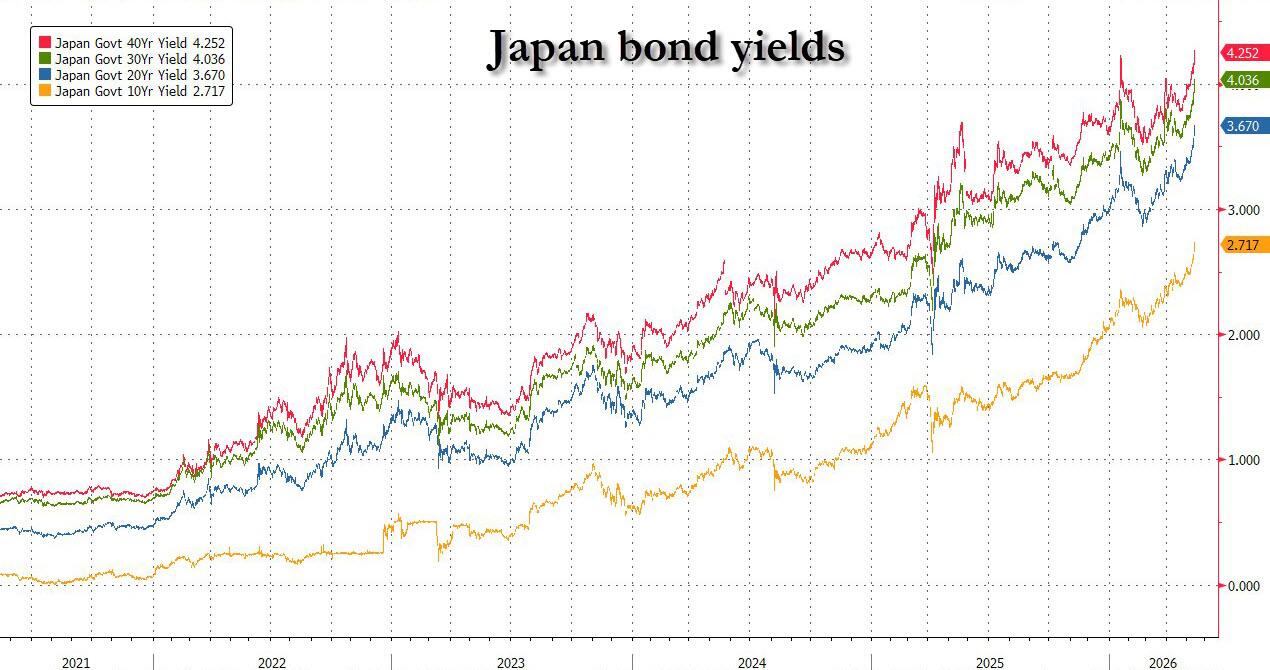

Japan’s government bond yields marched higher across the curve in the latest sign that elevated oil prices are raising inflation concerns across global debt markets. Meanwhile, India’s state-run refiners raised fuel prices for the first time in four years.

In FX, the US dollar has been the main beneficiary, looking to complete its first 5-day win steak since March, after a jump in oil prices reignited inflation concerns and sparked a selloff across global bond markets. The Bloomberg Dollar Spot Index is up 0.3% to its highest level this month.

In rates, bonds fell across the Americas, Europe and Asia as doubts grew over whether oil supplies from the Middle East will normalize anytime soon. Scorching wholesale inflation data in Japan offered a fresh warning of price pressures building throughout the global economy. Treasuries broadly hold losses seen in early Asia session as oil pushes higher with the Strait of Hormuz still effectively closed and efforts to end the war in limbo. Yields are off session highs however leading into the early US session as oil gains unwind slightly. Yields remain cheaper by 2bp to 6bp across the curve in a bear steepening move. US 10-year yields trade near session highs around 4.55%, and highest since May. Front-end outperforms slightly, steepening the US 2s10s and 5s30s spreads by 3bp and 2.5bp on the day. Gilts lag, with UK yields trading cheaper by 9bp to 14bp across the curve.While around 14bp of easing is priced by December, or about 55% of a 25bp move, Fed-dated OIS swaps price 25bp of rate hikes by the April policy meeting next year. In UK, political pressure also in play for gilts along with gains in oil, adding to underperformance, after Manchester Mayor Andy Burnham secured a pathway to potentially challenge Keir Starmer for the prime minister’s job. Wider losses seen across gilts, where long-end trades cheaper by 14bp on the day.

Japan’s government bond yields marched higher across the curve to effectively what are new record highs for the modern era, in the latest sign that elevated oil prices are raising inflation concerns across global debt markets. Meanwhile, India’s state-run refiners raised fuel prices for the first time in four years.

In commodities, Brent crude futures earlier topped $109 a barrel after representatives for Iran bemoaned contradictory US messages, and the The decline in Treasuries has pushed US 10-year yields up 6 bps to 4.54%. Metals are broadly lower with spot silver dropping 6%.

Economic data slate includes May Empire manufacturing (8:30am) and April industrial production (9:15am). Fed speaker slate empty for the session.

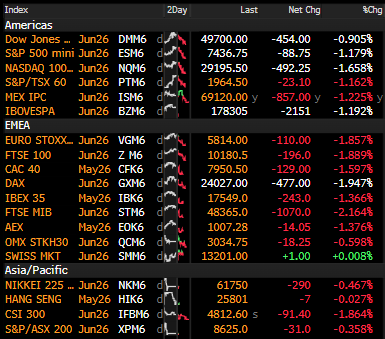

Market Snapshot

S&P 500 mini -1.1%

Nasdaq 100 mini -1.6%

Russell 2000 mini -1.2%

Stoxx Europe 600 -1.4%

DAX -1.7%

CAC 40 -1.4%

10-year Treasury yield +6 basis points at 4.54%

VIX +1.5 points at 18.79

Bloomberg Dollar Index +0.4% at 1202.79

euro -0.4% at $1.1622

WTI crude +3.7% at $104.88/barrel

Top Overnight News

US President Donald Trump left China on Friday with no major breakthroughs on trade or tangible help from Beijing to end the Iran war, despite two days spent heaping praise on his host, Xi Jinping. RTRS

An underappreciated surplus of crude oil, sloshing around storage tanks and aboard ships, cushioned the global economy when the Persian Gulf closed 2½ months ago. That excess supply is now dwindling at a record pace, with oil executives and analysts predicting that a harsh reckoning is set to upend the relative calm in energy markets. Acute shortages of key fuels and soaring prices could emerge within weeks if the Strait of Hormuz remains shut. WSJ

President Donald Trump said the US objective of recovering highly enriched uranium from Iran was “more for public relations than it is for anything else,” while reiterating his commitment to removing the nuclear material. BBG

Iran has allowed some Chinese vessels to pass through the Strait of Hormuz following diplomatic overtures from China’s government, semiofficial Iranian news agencies reported on Thursday. WSJ

The UAE will double its capacity to export crude oil bypassing the Strait of Hormuz by next year, as it seeks to reduce reliance on the shipping chokepoint. WSJ

UK borrowing costs hit their highest level since 2008 on Friday and the pound dipped as traders priced in a greater likelihood that Andy Burnham would challenge Sir Keir Starmer for the Labour leadership. The 10-year bond yield rose as much as 0.15 percentage points to 5.15 per cent, as the price of the debt fell, taking the UK’s benchmark borrowing costs above a post-2008 high set earlier this week. FT

Japan’s corporate goods prices surged in April by the most in 12 years, in another sign of how the war in Iran is boosting inflationary pressures and supporting the case for the Bank of Japan to raise interest rates. Japan’s Apr PPI surges +4.9% Y/Y in Apr, above the Street’s +3% forecast and up sharply from +2.9% in Mar. RTRS

Anthropic has agreed the terms of a $30bn fundraising that will value it at $900bn and is expected to close as soon as this month, capitalizing on its unprecedented growth this year to leapfrog its rival OpenAI’s valuation. FT

Fed Chair Jerome Powell’s term ends today. His colleague Michael Barr said shrinking the balance sheet is a threat to financial stability, while John Williams sees monetary policy in a “good place.”

BofA weekly flow data shows USD 20.5bln into stocks, USD 28.1bln into bonds, USD 5.8bln into cash, USD 2.0bln into gold and USD 1.3bln out of crypto. Bull & Bear Indicator rose to 7.6 (from 7.2).

Middle East

US President Trump said it’s just a question of time regarding Iran, while he also stated that current Iranian leaders are more reasonable and Iran has a lot of inner turmoil, but added that he is not going to be much more patient with Iran, according to a Fox News Interview. Trump also stated that Iran’s enriched uranium could be entombed, but would rather get it, as well as stated that they have their eyes on Iran’s enriched uranium and could bomb it again, but he would rather get it. Trump separately commented that he discussed Iran with Chinese President Xi, and they feel very similar about how they want to end the Iran war.

US has rejected Iran’s 14-point proposal, Tehran Time reported citing sources. According to the information, the US government has responded to Iran’s written proposal regarding the end of the war.

“Perhaps another of the Confidence Building Measures (CBM) between US and Iran is in the play”, Pakistani Journalist Mallick posted.

Iranian Foreign Minister Araghchi said contradictory messages from the US remain the main issue. He added that there is no military solution, and thinks the US needs to understand that fact. They have tested us at least twice and have now concluded that there is no military solution.

Iranian Foreign Minister Araghchi said at the BRICS meeting that the US empire is in decline and Iran will never bow to pressure, according to Press TV.

Iranian Foreign Minister Araghchi said evidence shows that the UAE made American bases available for operations against Iran, provided its airspace and territory for those operations

Iranian Parliamentary Speaker Ghalibaf warned that US efforts at sustaining military escalation near the Strait of Hormuz could trigger a fresh global financial crisis at a time when US national debt already stands at a whopping USD 39tln.

Iran’s Ambassador to Belarus criticised the US negotiation stance and said US President Trump’s excessive ambitions hinder US-Iran talks, according to TASS.

UAE attempted to get Saudi Arabia and Qatar to coordinate on a military response to Iran’s airstrikes, Bloomberg reported citing sources.

Qatar’s Foreign Ministry told Al Arabiya it had shot down several Iranian drones near its airspace, while it stressed the need to open the Strait of Hormuz in its contacts with the Islamic Republic.

Israel has commenced strikes on Hezbollah in the Tyre region of Lebanon.

Israeli army detected rocket launches from Lebanon towards Israeli territory, while Israeli artillery shelling was reported on the town of Nabatieh al-Fawqa in southern Lebanon.

A more detailed look at global markets courtesy of Newqsuawk

APAC stocks were mostly subdued after failing to sustain the early momentum that was spurred by the gains on Wall St, where tech outperformed, and sentiment was underpinned amid constructive headlines from the Trump-Xi summit, while the souring of risk sentiment coincided with higher oil prices and yields amid risk that the geopolitical situation in Iran could escalate when US President Trump returns from Beijing. ASX 200 lacked direction as strength in tech and financials was offset by losses in mining, materials, resources and utilities. Nikkei 225 swung between gains and losses but ultimately continued its pullback from the recent peak amid oil-related headwinds and after hot PPI data further supported the case for a rate hike at next month’s BoJ meeting. Hang Seng and Shanghai Comp were mixed despite the recent constructive headlines from the Trump-Xi summit, while the leaders are meeting again today in a restricted working lunch session prior to US President Trump’s return to the US. Furthermore, sentiment was not helped by recent disappointing lending and aggregate financing data from China for April, which showed a surprise contraction in loans.

Top Asian News

Japan’s Minister for Economy, Trade and Industry Akazawa said they can tap FY26 budget reserves if the Middle East impact lasts. However, it was also reported that Japanese Finance Minister Katayama said they are not in a situation where an extra budget is needed, while she stated they have JPY 1tln in reserve funds in the FY26 budget, but added there’s no immediate need for an extra budget.

European bourses (STOXX 600 -1.4%) are entirely in the red, with sentiment hit for a multitude of factors: 1) Central bank repricing, 2) Tech sell-off driven by higher yields and strikes at Samsung Electronics, 3) Surging energy prices. European sectors confirm the negative bias, with only Health Care posting solid gains. Basic Resources and Tech sit at the bottom of the pile. Metal prices have slumped (XAU/USD -1.8%, XAG/USD -6%), as markets price in further rate hikes across the globe. In addition, South Korea’s KOSPI closed with losses of over 6%, adding to the pressure on silver prices as it highlights silver’s high-beta characteristics (as it stands, KOSPI-Silver correlation is c. +0.7).

Top European News

UK Labour NEC decision on allowing Burnham to run in the Makerfield by-election is not as clear cut as many are reporting, according to GB News’ Harwood. The vote is said to be on a “knife edge”, sources say “everyone is wavering”.

FX

G10s showing a risk-off bias as the Buck in tandem with Crude prices. Antipodeans are the underperformers, while EUR and GBP also lag amid energy/political related headwinds.

DXY continues to perform well, vaulting 50,100 and 200 DMAs over the past two sessions amid a mix of hot US inflation data, resilient jobs data/retail sales and exponentially firm oil prices. The session ahead is absent of major data/speakers, and as such, the Greenback will likely be dictated by incoming geopolitical headlines. As a reminder, Warsh today officially takes the title of Fed Chair, while Powell becomes governor and Miran steps down. MUFG in its morning note said “This week has seen the rolling correlation between DXY and the 2-year US-DXY rates spread strengthen notably, which points to scope for US dollar strength to extend further if rate hike pricing momentum continues”.

Once again, the centre of attention continues to be UK political developments, as markets increasingly price in the possibility of a left-leaning Burnham premiership after he announced his running in an engineered Makerfield by-election. (See 07:35 BST analysis). Sterling has weakened since the announcement on Thursday evening, but losses are somewhat limited given the continued uncertainty about whether the Manchester Mayor would be able to 1) Succeed in winning the by-election, 2) Beat incumbent Starmer in a leadership challenge. Elsewhere, keep an eye on a potential announcement on a support package for bills next week, after Housing Secretary Steve Reed touted it this morning. GBP/USD fell to a 1.3328 low where it found support.

Central Banks

Fed’s Barr (voter) said smaller Fed balance sheets would likely increase Fed interventions and that reducing liquidity rules to shrink the Fed balance sheet is not a good idea. Barr stated that lowering the liquidity requirement would simply increase stability risks, and if anything, the liquidity requirement should go up, not down. Furthermore, he said they are not in a recession, but there’s been little job creation, while he hasn’t decided on what to do at the June FOMC meeting.

Fed’s Williams (voter) said Fed independence delivers better economic outcomes, and it is not time to worry about Fed independence, with staff focused on the mission. Williams said the context matters for inflation given its persistence above target, while he is not surprised to see near-term inflation expectations rise and is seeing pretty stable longer-term inflation expectations. Williams noted there is a lot of uncertainty around energy price outlook and that the job market is not “hot” but also not slowing dramatically, while he added that monetary policy is mildly restrictive and he doesn’t see any reason to hike or cut rates right now.

Fixed Income

Global benchmarks are down, dragged lower early in the week as markets digested hotter-than-expected CPI/PPI, the prolonged Iran conflict (higher energy prices), with fears also exacerbated by the turmoil in the UK’s Labour Party. Markets remain on tenterhooks given the mentioned factors, and this has been reflected in market pricing across several major central banks. Traders now assign a 70% chance of a 25bps hike by year-end and fully priced in for July 2027.

USTs are currently down by 16+ ticks, and trading at the bottom end of a 109-16 to 109-29+ range. Attention over the past day has been on the Trump-Xi meeting, where initial commentary suggested positive developments; President Trump stated that many problems with China were “settled”. Focus now shifts from China, and back to Iran, where no progress has been made. Some reports have touted that Trump may look to immediately strike Iran after his China visit, to force Iran into a deal. If enacted, there is a risk that Iran chooses to restart strikes on US allies in the Middle East, leading to another spike in energy prices, hence filtering through into US yields.

Bunds follow the negative action seen across peers, and trade at the bottom end of a 124.58 to 125.03 range. Whilst yields are firmer across the curve today, levels remain within familiar levels; 10yr holds around 3.108% vs a near-term high of 3.133%. As it stands, the belly of the curve is outperforming; however, traders may soon begin to factor in weaker economic growth across the EZ, which may see medium-term yields begin turning lower.

Gilts underperform vs peers and are currently off by 137 ticks; holding at the bottom of an 85.44-85.85, a trough amongst the contract low. Ultimately, following peers, but the move also exacerbated by domestic politics. A full review is on the Newsquawk feed at 07:35 BST, but in brief: Labour MP for Makerfield announce he is willing to stand aside and spark a by-election, to allow current Greater Manchester Mayor Burnham to run and then, if successful, to challenge for the Labour leadership and, by association, the role of Prime Minister. For reference, Burnham was touted as the “least” market-friendly outcome by a recent FT fund manager survey.

Australia sells AUD 1bln 1.00% December 2030 bonds b/c 3.69, avg yield 4.7049%.

Commodities

Geopolitical risk has heightened as US President Trump returns from his trip to Beijing and refocuses on the Iran situation. As a reminder, reports yesterday via Axios suggested US President Trump’s team is now discussing options for military escalation to break the deadlock. Axios added that US officials said Trump could make his next move immediately after his trip to China. Options reportedly include 1) resumption of “Project Freedom,” with the Navy attempting to break the logjam in the Strait of Hormuz, 2) the launch of a new bombing campaign focusing on Iranian infrastructure. Meanwhile, Israeli officials cited by Axios said they’ll be on high alert this weekend in case Trump decides to resume the war.

In terms of more recent updates, Trump warned it is “just a question of time” regarding Iran and said he will not be “much more patient” with Tehran, while reiterating that the US is monitoring Iran’s enriched uranium and could strike again if necessary, although he would prefer a diplomatic outcome. Trump added that he discussed Iran with Chinese President Xi and both sides agreed the war should end, with China later confirming the leaders reached new consensuses and calling for a comprehensive and lasting ceasefire alongside dialogue on Tehran’s nuclear programme. However, reports suggested that Washington informed Israel that Trump could still authorise fresh strikes inside Iran, while the Tehran Times reported the US formally rejected Iran’s 14-point proposal and maintained its hardline nuclear stance.

In the European morning, an uptick in crude and a leg lower in sentiment coincided with comments from Iranian Foreign Minister Araghchi, who noted contradictory messages from the US remain the main issue. On the supply side, it’s also worth noting that the UAE announces accelerated pipeline construction to bypass the Strait of Hormuz. Nonetheless, WTI Jul rose above USD 100/bbl to currently trade towards the top end of a USD 97.23-100.93/bbl range, while its Brent Jul counterpart resides at the upper end of a 106.26-109.68/bbl parameter. Dutch TTF front-month trades higher by just shy of 3% at the time of writing, north of EUR 49.MWh, vs an earlier low of around EUR 47.60/MWh.

Precious and base metals are softer across the board, given the energy-induced strength in the USD. Spot gold trades in a USD 4,532-4,665/oz, while Spot silver sees deep losses for a second straight session as it continues to recoil from a recent rally, with prices hitting a USD 77.66/oz low vs USD 83.88/oz intraday high, and after hitting a USD 89.37/oz peak on Wednesday. 3M LME copper continues to pull back from record levels, dipping under USD 14,000/t to trade in a current USD 13,586.00- 13,961.03/t range.

UAE is to complete the construction of a new West-East pipeline project in 2027, Bloomberg reported. The ADNOC Chairman later said they are reviewing progress on the new West-East Pipeline (c. 1.5mln BPD, when complete), set to double the co.’s export capacity via Fujairah.

Abu Dhabi backs USD 13bln US gas plant as Middle East supplies falter, according to FT.

Japan’s METI met and confirmed that, at the next meeting, they will deepen consideration on the diversification of oil procurement sources and improve the domestic supply system and future oil reserves, Nikkei reported.

Trade/Tariffs

US President Trump said they have gotten along well with Chinese President Xi and have a very good relationship with China, while he added Xi is a tremendous and strong leader, and that he would like to see US companies do more business in China. Trump said he spoke to Xi strongly about trade and intellectual property, as well as noted that China will open the country in stages and that it would be good for US companies. Furthermore, Trump said China is going to be buying a lot of farm products, as well as stated that he asked China about using Visa (V), and maybe the China Visa ban will come off.

Chinese President Xi said the US and China agreed to enhance talks on regional issues, Chinese State media reported. The two sides reached an important consensus and agreed to stabilise trade relations.

China’s Foreign Ministry said US President Trump and Chinese President Xi reached a series of new consensuses, while it added that the war should not continue and that China is to contribute to Middle East peace. It also said a comprehensive and lasting ceasefire should be reached as soon as possible, and urged solving the Iranian nuclear issue through dialogue.

US President Trump posted that Chinese President Xi congratulated him on so many tremendous successes in such a short period of time, while Trump added that the US was in decline two years ago, but is now the hottest nation.

USTR Greer said they had a lot of successes in rebalancing trade with China and expect to see an agreement for double-digit billions of dollars of agricultural sales to China coming out of the summit. Greer said China is fulfilling its promises on soybean purchases and that China knows there is going to be a certain level of US tariffs on Chinese goods. Furthermore, he cannot commit to a given rate of tariff on Chinese goods and will release findings of trade investigations in weeks, while he stated purchases of NVIDIA H200 chips will be a sovereign decision by China, and that chip export controls were not a major topic in the meeting.

Geopolitics

Commander of Ukrainian drone forces said drones struck Russian oil refinery in the Ryazan region.

US Secretary of State Rubio said China’s preference is probably to get Taiwan willingly and that there will be some agricultural purchases from China, while Rubio hoped to get a positive response from China regarding the case of Jimmy Lai and others.

CIA Director delivered a message from US President Trump that the US is prepared to engage on economic and security issues if Cuba makes fundamental changes, according to a CIA official.

US Event Calendar

8:30 am: United States May Empire Manufacturing, est. 7.2, prior 11

9:15 am: United States Apr Industrial Production MoM, est. 0.3%, prior -0.5%

9:15 am: United States Apr Capacity Utilization, est. 75.8%, prior 75.7%

DB’s Jim Reid concludes the overnight wrap

As we go to press this morning, markets have lost momentum after President Trump said the US doesn’t need the Strait of Hormuz open “at all”. So that’s added to fears that the Strait will remain blocked for some time, leading to a more protracted energy shock for the global economy. Indeed, Brent crude oil prices are up another +1.21% overnight to $107.00/bbl. And in turn, those inflation concerns have pushed the 10yr Treasury yield up +3.5bps this morning to 4.52%, its highest level since May last year. It’s a similar story for equities too, with S&P 500 futures down -0.25% this morning, slipping back from their record high yesterday.

Those moves have also been clear in Asian markets overnight, with particularly sharp losses in Japan after their PPI inflation data was well above expectations. In fact, the year-on-year measure surged to +4.9% in April (vs. +3.0% expected), which has led markets to price in a growing chance of BoJ rate hikes this year. Indeed, there’ve been fresh records for JGB yields overnight as well, with the 10yr yield (+9.6bps) up to 2.71%, marking its highest level since 1997. Asian equities have also struggled, with the Nikkei (-1.16%), the KOSPI (-3.66%) and the Hang Seng (-0.95%) all lower, although in mainland China there’s been a relative outperformance, with the CSI 300 (+0.04%) and the Shanghai Comp (+0.12%) up modestly.

Otherwise this morning, the big thing to look out for will be the gilt market when it reopens, as it responds to the latest political turmoil in the UK. The last 24 hours have brought many headlines, but the biggest is that Greater Manchester’s Mayor Andy Burnham is seeking to return to Parliament. He now has a path to do so, because an MP in the region announced he’d be standing down to trigger a by-election, which Burnham has said he’ll try to stand in. So if he’s successful and becomes an MP, that would mean he could challenge for the party leadership to become Prime Minister.

For gilt markets, there’s been a focus on Burnham’s candidacy, in part as he said last year that the UK shouldn’t be “in hock to the bond markets”. Moreover, Burnham suggested last week that defence spending could be considered outside the fiscal rules, which added to speculation about more gilt issuance under a Burnham premiership. The news came out after gilt markets had closed yesterday, but the pound weakened sharply in response, ending the day -0.89% lower against the US Dollar, making it the worst-performing G10 currency yesterday. And this morning it’s down a further -0.22% to $1.3373.

Earlier in the day, the UK also saw the first cabinet-level resignation since the local elections, as Health Secretary Wes Streeting stood down. In his resignation letter, he said it was clear that PM Starmer “will not lead the Labour Party into the next general election”. But contrary to earlier speculation, Streeting didn’t launch a formal challenge against Starmer, which would require the backing of 20% of Labour MPs. So, for now at least, Starmer remains in position, and a leadership contest hasn’t been triggered. Gilts closed yesterday before the news of Burnham’s potential return, so 10yr gilt yields (-7.2bps) fell to 4.99%. Meanwhile, the UK data was broadly as expected too, with Q1 GDP growth at +0.6%, in line with consensus.

Ahead of all that, global markets had generally put in a strong performance yesterday, thanks to positive noises from the Trump-Xi summit in Beijing, a decent batch of US data, and easing fears about inflation. So that pushed the S&P 500 (+0.77%) to another record, topping the 7,500 mark for the first time. And other risk assets performed well too, with US IG spreads closing at their tightest level in 3 months.

Several factors helped to drive that advance, but in the background, we had the Trump-Xi summit taking place in Beijing. There weren’t any market-moving headlines as such, but several points led to optimism that trade tensions might ease further. For instance, Trump said that relations would be “better than ever”, and Chinese state media reported that Xi told US executives that China’s “doors to the outside world will open wider and wider”. Meanwhile, the onshore yuan reached its strongest level in 3 years yesterday, closing at 6.79 per US Dollar. One of the few more concrete headlines was Trump’s comment that China agreed to order 200 Boeing jets, but this was at the low end of expectations, leading Boeing’s shares to fall -4.73% on the news. Further trade-related announcements are expected today.

Otherwise, risk assets got further support from various corporate headlines. Notably, Cisco (+13.41%) was the top performer in the S&P 500, after they announced a better-than-expected outlook in their latest release. Wider optimism around AI was also supported by a +68% opening jump for AI chipmaker Cerebras Systems after its $5.5bn IPO. Nvidia (+4.39%) led the gains for the Magnificent 7 (+0.49%) while the Nasdaq (+0.88%) hit a record high of its own as well. That wasn’t just confined to the US either, with the STOXX 600 (+0.76%) advancing, whilst Italy’s FTSE MIB (+1.15%) hit a post-2000 high.

In the meantime, oil prices were little changed yesterday, with Brent crude (+0.09%) closing at $105.72/bbl. However, oil did edge higher late in the US session, which contributed to a more hawkish Fed repricing. For instance, futures almost fully priced in a rate hike by June 2027, with 24bps of tightening now priced (+5.6bps on the day). That came as Kansas City Fed President Schmid said he saw “continued inflation as the most pressing risk to the economy”. The US rates mood also wasn’t helped by lukewarm demand for the latest T-bill auctions as the Treasury increased auction sizes for the past couple of weeks. And in turn, 2yr Treasury yields (+3.9bps) rose above 4% for the first time since June 2025. The moves were more muted further out the curve however, with the 10yr Treasury yield (+1.3bps) inching up to a 10-month high of 4.48%. And in Europe, yields fell back yesterday, with those on 10yr bunds (-5.7bps), OATs (-6.6bps) and BTPs (-7.1bps) all lower.

Elsewhere, markets got further support from a robust batch of US data. In particular, retail sales showed signs of resilience, with the headline measure up +0.5% in April as expected. Moreover, it wasn’t just an energy story, as the measure excluding autos and gas stations was up +0.5% (vs. +0.3% expected). And in turn, the Atlanta Fed’s GDPNow estimate for Q2 moved up from an annualised +3.7% rate to +4.0%, suggesting the economy remained on a strong footing. Meanwhile, we also had the weekly initial jobless claims, which rose a bit more than expected to 211k in the week ending May 9 (vs. 205k expected). But that still left the 4-week moving average at just 203.75k, only slightly above its two-year low the previous week.

Looking at the day ahead, and data releases include US industrial production for April, and the Empire State manufacturing survey for May. From central banks, the EC will publish their Economic Bulletin, and we’ll hear from the ECB’s Vujcic and Dolenc

Tyler Durden

Fri, 05/15/2026 – 08:43

https://www.zerohedge.com/markets/futures-tumble-reality-returns-and-yields-oil-and-dollar-soar

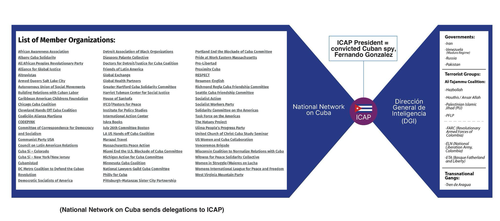

CIA Head Ratcliffe Spotted In Cuba As Trump Refocuses Crosshairs On Havana Communists

CIA Head Ratcliffe Spotted In Cuba As Trump Refocuses Crosshairs On Havana Communists

We noted on Thursday that, once President Trump’s summit with Chinese President Xi Jinping concluded, the Trump team’s next focus would likely shift back toward Cuba. That pivot now appears underway. Aboard Air Force One early Friday, while returning stateside, Trump told reporters that “Cuba needs our help,” signaling the Caribbean island nation is moving higher on the administration’s agenda.

A new AP report offers more insight into how the Trump administration is shifting attention back toward Cuba: CIA Director John Ratcliffe met with officials in Havana on Thursday, reopening a channel for political dialogue between the two countries.

Havana, Cuba pic.twitter.com/7S7TtJPyf5

— CIA (@CIA) May 14, 2026

Ratcliffe and top U.S. officials, some of whose faces were blurred in images released by the CIA on X, held high-level talks with Cuba’s Interior Minister, the head of Cuban intelligence, and Raúl Castro’s grandson, Raulito Rodríguez Castro.

Havana’s communist government released a statement noting that the meeting “took place Thursday, May 14, against a backdrop of complex bilateral relations.”

AP noted that Cuban officials presented a report to Ratcliffe and his team, claiming to demonstrate that the communist-run island poses no threat to U.S. national security.

Consequently, Havana maintains there are no legitimate grounds for its continued inclusion on the U.S. list of state sponsors of terrorism.

As per The Washington Times, “Cuba’s intelligence apparatus is training foreign nationals to wage war against the West.”

Thursday’s meeting comes after a report that Cuba’s power grid collapsed further into blackout conditions, as Energy Minister Vicente de la O Levy warned that the island is completely out of fuel for diesel generators. This comes as Trump’s fuel blockade remains in effect.

Let’s not forget that the Trump team is prepared to provide $100 million in direct humanitarian assistance if Havana moves forward with political reforms after decades of nation-killing communism.

Related

Trump Says Cuba Is Seeking Help: ‘We Are Going To Talk’

Trump and his team appear to be refocusing their efforts on the Western Hemisphere, with more news on Cuba likely to come next week.

Tyler Durden

Fri, 05/15/2026 – 08:20

Gemini Space Station Soars On $100 Million Winklevoss Investment

Gemini Space Station Soars On $100 Million Winklevoss Investment

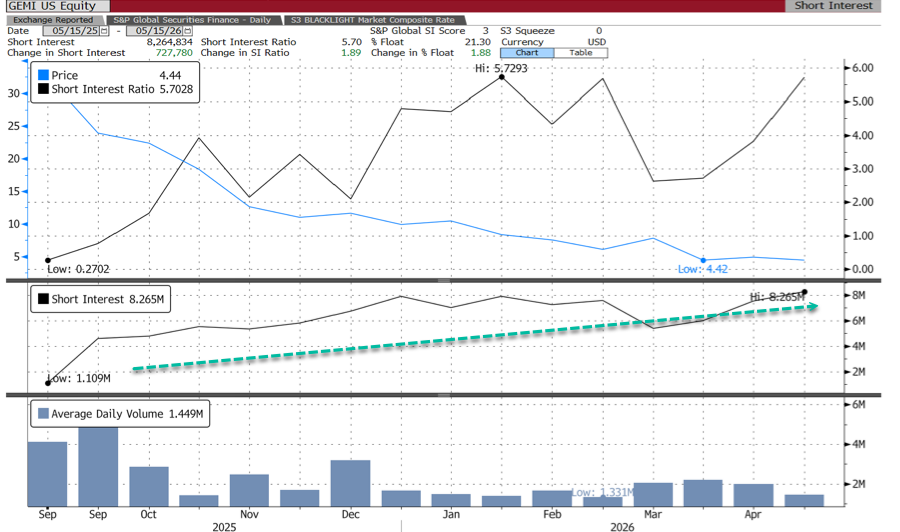

Heavily shorted Gemini Space Station soared in premarket trading after Tyler and Cameron Winklevoss injected $100 million into the money-losing crypto exchange, buying Class A shares at $14 apiece in a bitcoin-funded transaction.

GEMI shares are up 20% in premarket trading after closing at $5.26 on Thursday, though the stock remains down 47% year to date.

Short interest is high at 21.5% of the float, equivalent to roughly 8.3 million shares, with 5.3 days to cover, leaving GEMI vulnerable to a squeeze on any sustained upside momentum.

“We believe the market has significantly undervalued Gemini, and that this investment will allow us to set up the company for its next phase of growth,” CEO Tyler Winklevoss said in a statement.

Winklevoss noted, “Gemini has achieved several major product and regulatory milestones that position us well to evolve from a crypto company into a markets company. This investment will help fuel that ambition and set Gemini up for long-term success.”

GEMI’s first-quarter loss narrowed to $109 million from $149 million one year ago, while revenue jumped 42% to $50 million, helped by growth in services such as credit cards. The exchange went public in September 2025 and remains about 83% from its $28 listing price.

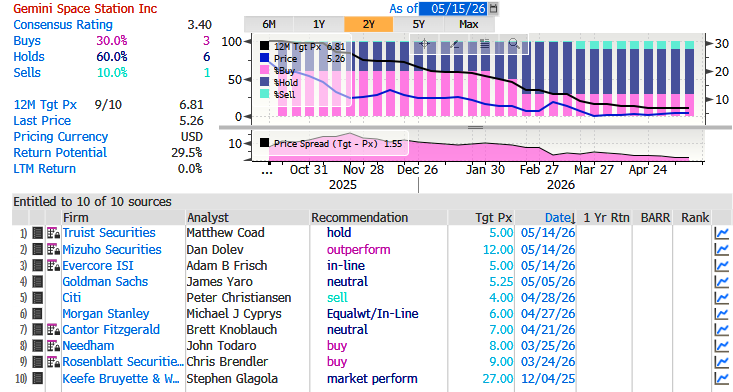

Analyst commentary (courtesy of Bloomberg):

Evercore ISI analyst Adam Frisch (in line, PT $5)

If was not for the strategic investment, the stock “would likely be down on the print as key metrics like user and revenue reacceleration fell well short of pre-IPO expectations”

“The strategic investment is the headline and should support the stock, but we do not view the underlying print as encouraging as fundamentals are not yet reaccelerating”

Mizuho analyst Dan Dolev

Gemini has a “solid start” to the year with these restults

The $100M capital investment and subsequent management commentary are positives

Truist Securities analyst Matthew Coad (hold, $5)

While Gemini’s 1Q were better than feared, “the capital injection may alleviate balance sheet concerns.”

Analyst ratings:

The crypto exchange went public in September 2025 and remains 83% below its $28 listing price.

Tyler Durden

Fri, 05/15/2026 – 07:45

https://www.zerohedge.com/crypto/gemini-space-station-soars-100-million-winklevoss-investment

41 People In US Under Monitoring For Hantavirus: CDC

41 People In US Under Monitoring For Hantavirus: CDC

Authored by Zachary Stieber via The Epoch Times,

Forty-one people are under monitoring in the United States for hantavirus, the Centers for Disease Control and Prevention said on May 14.

Most of those being monitored were at one time on board the MV Hondius, a cruise ship that experienced an outbreak of the disease after it sailed from Argentina on April 1 to remote locations such as Antarctica.

Eighteen people were flown from the ship recently to medical facilities in Nebraska and Georgia for quarantining during the incubation period for the virus, which is up to 42 days.

Some other individuals left the ship before the hantavirus outbreak was detected and are at home in states such as Arizona and California.

The third group is composed of people who were exposed to hantavirus during travel because they came close to cruise ship passengers, particularly on planes, Dr. David Fitter, a CDC official, told reporters on a call.

Eleven Hondius passengers worldwide have been confirmed or are suspected to have contracted hantavirus, according to the World Health Organization. Three people who were on board and either tested positive or showed symptoms of the virus, such as fever, have died.

Humans typically contract hantavirus from infected rodents, but person-to-person transmission is believed to have occurred on board the vessel.

“Epidemiological investigations continue to better define epidemiological links between cases and exposure factors on the ship, as well as to try to understand the potential source of exposure,” the World Health Organization said in a statement on May 14.

No mandatory quarantine orders have been imposed as of yet in the United States.

“We are working closely with passengers and public health partners to ensure monitoring and rapid access to care if symptoms develop,” Fitter said.

“Our goal is to work with them and alongside them, building plans based on their specific situations to protect the health and safety of passengers and American communities. We understand that these passengers have already been through a difficult experience. This coordinated approach reflects our respect for them as partners in keeping themselves and their communities safe.”

Kansas officials said earlier Thursday that three residents who were not on the Hondius were exposed to a person with hantavirus.

The three are being monitored, according to the Kansas Department of Health and Environment.

Other states, including Maryland, New Jersey, and Washington state, have said residents were possibly exposed on flights.

The CDC says the risk to the public is low, with hantavirus transmission believed to only occur through close contact with infected people or their bodily fluids.

Tyler Durden

Fri, 05/15/2026 – 07:20

https://www.zerohedge.com/medical/41-people-us-under-monitoring-hantavirus-cdc

Trump Talk & ‘Thucydides Trap’ Threat Triggers Market Mayhem Overnight

Trump Talk & ‘Thucydides Trap’ Threat Triggers Market Mayhem Overnight

Traders are waking this morning in the US to some relative market mayhem and questioning what came first – the oil spike or the geopolitical angst – to trigger these moves as it appears the market finally remembered there’s more going on in the world than trading ‘short compute’ demand to the moon…

Oil prices are up significantly (WTI >$100)…

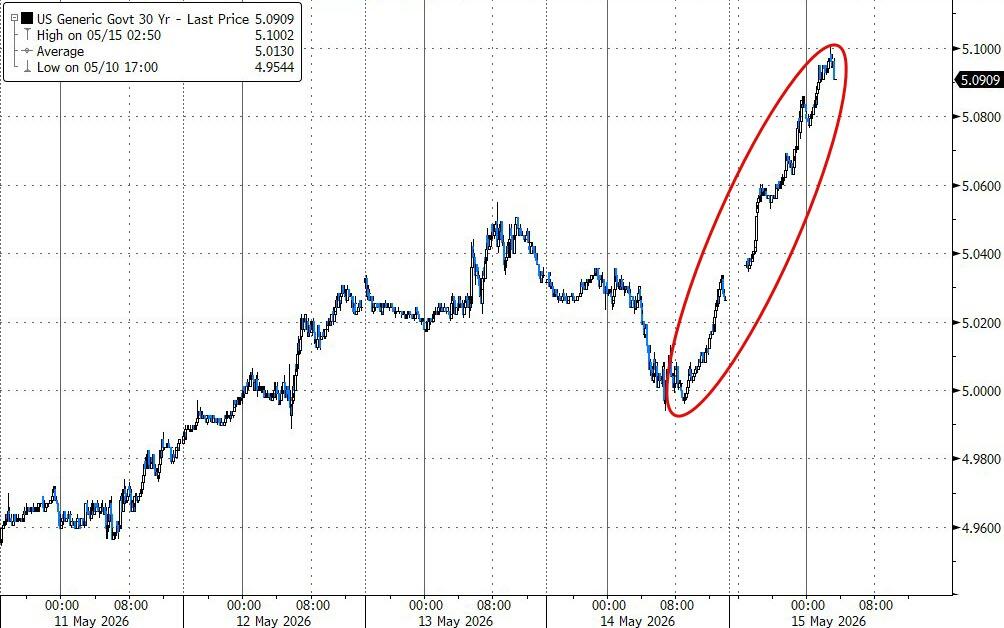

Bond yields are breaking out everywhere (10Y 4.5%, 30Y UST 5.10%!, 30Y Gilt 5.82% – highest sine 1982)…

Equity markets sharply lower overnight (Kospi -6%, Japan Semis approx. -5%, Japan momentum approx. -2.5% Nasdaq -1.5% as levered ETF exposure and high concentration clearly exacerbating the sell off)…

The catalysts are intertwined with what appears to be a nothing-burger in terms of outcomes from Trump’s trip to China (exacerbated by Xi’s not so hidden threat) and Trump’s comments on the Strait of Hormuz..

China Summit

As Goldman Sachs one-delta desk-head, Rich Privorotsky, notes this morning, the Xi/Trump summit appeared to yield little in the way of immediate tangible outcomes.

Despite all the positive rhetoric, Boeing sank, KWEB closed -4.6%, the details around NVIDIA H200 exports remain murky and even some of the headline “wins” looked shaky.

Reuters reported that Chinese customs “halted export clearances for hundreds of U.S. beef plants” just hours after approvals had seemingly been renewed during the summit.

For now this still looks more like stabilization than a durable reset.

Feels like the US side came hoping for transactional risk deals while China was looking for a broader multi year reset and foundations for more constructive dialogue.

The references to the “Thucydides Trap” did not go unnoticed either:

Xi invoked whether China and the US could “transcend the so-called Thucydides Trap” (the theory that when a rising power threatens to displace an established great power, war becomes highly likely).

…very deliberate language and clearly aimed at framing this as something much bigger than tariffs or trade.

Trump later had to go on a posting offensive clarifying that he must have been referring to the Biden administration…

When President Xi very elegantly referred to the United States as perhaps being a declining nation, he was referring to the tremendous damage we suffered during the four years of Sleepy Joe Biden and the Biden Administration, and on that score, he was 100% correct. Our Country suffered immeasurably with open borders, high taxes, transgender for everybody, men in women’s sports, DEI, horrible trade deals, rampant crime, and so much more!

President Xi was not referring to the incredible rise that the United States has displayed to the world during the 16 spectacular months of the Trump Administration, which includes all-time high stock markets and 401K’s, military victory and thriving relationship in Venezuela, the military decimation of Iran (to be continued!) — Strongest military on earth by far, economic powerhouse again, with a record 18 trillion dollars being invested into the United States by others, best U.S. job market in history, with more people working in the United States right now than ever before, ending country destroying DEI, and so many other things that it would be impossible to readily list.

In fact, President Xi congratulated me on so many tremendous successes in such a short period of time.

Two years ago, we were, in fact, a Nation in decline. On that, I fully agree with President Xi!

But now, the United States is the hottest Nation anywhere in the world, and hopefully our relationship with China will be stronger and better than ever before!

However, as Privorotsky noted, the market probably came in pricing deal momentum and instead got managed coexistence.

That is still positive in macro terms, just less catalytic for risk assets immediately.

Now, to the second part of the double-whammy…

Oil

This is where Privorotsky says ‘the rubber meets the road.’

Feels like the US held back from escalation ahead of the China summit, hopeful Beijing might lean on Iran to de-escalate.

But China’s messaging remained diplomatic rather than forceful, saying “the most urgent issue is to keep the ceasefire” and calling for “good-faith negotiation between the two sides.”

Trump said he and Xi agreed that Iran cannot have nuclear weapons, returning market focus to the ongoing closure of the Strait of Hormuz.

Reopening the waterway has been a key objective for the US in diplomatic efforts since a ceasefire between Washington and Tehran took hold about five weeks ago. But Iran insists it keep an oversight of traffic through the maritime chokepoing as part of any peace agreement, stoking fears of a prolonged disruption in energy exports from the Persian Gulf.

Trump oscillated between threatening further attacks on Iran, including in a Truth Social post between meetings with Xi, and insisting the US does not rely on energy imports through the Strait of Hormuz.

“They need the Strait more than we need it open, we don’t, we don’t need it at all,” Trump said in an interview with Fox News.

Trump says US is “doing it to help Israel and to help Saudi Arabia” and other gulf allies.

“It also helps China”

That comment triggered a jump in crude prices, rise in the dollar, and drop in gold…

For now, it appears the combination of Trump’s nonchalance about the Strait and the over-arching geopolitical threat from Xi (combined with a disappointing outcome from the talks in terms of tangible trade deals) are enough to trump the Gamma Squeeze in AI/Semis (so far).

So now the question becomes:

Does the US feel compelled to escalate further (with China… or Iran)?

Markets are understandably skittish into the weekend risk window, which combined with the options expiration removing a chunk of positive (stabilizing) gamma, leaves markets more free to move (up or down).

Tyler Durden

Fri, 05/15/2026 – 06:55

https://www.zerohedge.com/markets/trump-talk-thucydides-trap-threat-triggers-market-mayhem-overnight

Europe’s Green Deal Is Unraveling

Europe’s Green Deal Is Unraveling

Authored by Mohamed Moutii via the American Institute for Economic Research (AIER)

Over the past decade, Europe has played a leading role in shaping global climate policy, highlighted by the launch of the European Green Deal in 2019—Ursula von der Leyen described it as a “man on the moon moment.” The initiative aims to make Europe the world’s first climate-neutral continent by 2050 while fostering innovation and strengthening its industrial base.

Yet several years later, the results are deeply disappointing. Instead of meeting its goals, the Green Deal is increasingly associated with higher energy costs, weakened competitiveness, and growing political backlash. It has deepened divisions within the EU, strained global relations, and increased pressure on households and businesses—raising serious doubts about its feasibility and long-term economic impact.

How Green Ideology Undermines Europe’s Economy

Europe’s economic stagnation points to a deeper structural problem in its energy and climate strategy—one closely tied to the direction set by the European Green Deal. Since its launch, competitiveness has eroded sharply, with soaring energy costs at its core. Electricity prices in Europe are now two to three times higher than in the United States and China, with taxes accounting for nearly a quarter of the total cost.

These outcomes largely stem from policy choices. The EU’s binding targets—net zero by 2050 and a 55-percent emissions reduction by 2030—have constrained energy supply, despite Europe accounting for only six percent of global emissions. At the same time, phasing out nuclear, restricting gas, and relying on intermittent renewables have weakened energy security and increased price volatility. For industry—where energy can account for up to 30 percent of total production costs—this, combined with carbon pricing, has become a critical constraint, driving firms to scale back, relocate, or shut down, accelerating deindustrialization across the continent.

The automotive industry clearly illustrates these pressures: representing over 7 percent of EU GDP and nearly 14 million jobs, the sector is under pressure from the 2035 ban on combustion engines, forcing a rapid shift to electric vehicles despite unresolved technological challenges and market constraints. As Mercedes-Benz CEO Ola Källenius warned, the policy risks driving the sector “full speed into a wall.” The consequences for the sector are already visible: declining production, mounting restructuring, and significant job losses—86,000 jobs since 2020, with up to 350,000 more at risk by 2035—while tightening regulations are set to reduce profits by seven to eight percent by 2030, pushing the sector toward losses and eroding Europe’s automotive leadership.

Agriculture has also become one of the Green Deal’s clearest casualties. Stricter rules on emissions, land use, pesticides, and fertilizers are raising costs and increasing yield volatility, hitting small farmers hardest and accelerating consolidation among large agribusinesses. Targets such as cutting pesticide use by 50 percent and expanding organic farming risk significant declines in output, threatening both rural livelihoods and food security. Rather than enabling farmers to innovate and improve productivity, these policies are constraining production—fueling widespread protests and weakening both competitiveness and sustainability.

Taken together, these pressures are not isolated—they reflect a broader economic burden. The European Commission estimates that the transition will require at least €260 billion in additional investment each year, with total costs reaching up to 12 percent of EU GDP—a burden that is increasingly difficult for the European economy to sustain.

The Green Deal’s Central Planning Problem

The economic strain is now translating into political backlash. In recent years, opposition to the European Green Deal has surged across the continent—from farmers and industrial groups to voters and political parties. The 2024 EU elections confirmed what was already clear: the once-dominant green consensus is fracturing. In response, Brussels has begun quietly rolling back key elements of the policy—weakening regulations, introducing loopholes, and even avoiding the term “Green Deal” itself. What was presented as a historic transformation is now unraveling.

This backlash reflects a deeper failure. Although the EU allocated $680 billion from 2021 to 2027—over a third of its budget—the Green Deal has achieved only modest environmental improvements, while imposing a heavy economic burden on households and businesses, who now face higher energy prices, taxes, and regulatory pressure.

The problem is not merely execution—it is structural. The Green Deal relies on centralized planning to manage a complex energy transition, even though policymakers lack the information and incentives to do so effectively. A major flaw is its rejection of technological neutrality. Leading manufacturers support a mix of electric, hybrid, hydrogen, and e-fuels to compete freely and allow efficient solutions to emerge, yet Brussels is enforcing a single pathway—effectively dictating which technologies survive and sidelining industry expertise.

In such a system, the outcomes are predictable: misallocation, distorted competition, and costly failures. These distortions are amplified by Europe’s restrictive regulatory environment, where internal barriers within the EU single market amount to a 44-percent tariff on goods and 110 percent on services, further constraining efficiency and innovation.

Germany illustrates these dynamics clearly. Long regarded as the leader of Europe’s green transition, its Energiewende—expanding renewables while phasing out nuclear—has cost around $800 billion since 2002, yet delivered only modest results and left German industries paying up to five times more for electricity than American competitors. Much of the progress in renewables has been offset by the closure of zero-emission nuclear plants. Estimates suggest that maintaining nuclear capacity could have achieved a 73-percent emissions reduction at half the cost, highlighting the limits of ideologically driven policy.

The comparison with the United States is instructive. In the U.S., emissions have declined even as the economy more than doubled since 1990—driven largely by market forces, particularly the shift to cheaper natural gas and the expansion of renewables. This combination reduced emissions without imposing comparable costs. Europe, meanwhile, has pursued a more rigid, policy-driven approach that has raised prices and weakened growth.

The deeper lesson of the Green Deal is that climate policy cannot succeed when it abandons the principles that made Europe prosperous in the first place: free enterprise, open markets, private innovation, and limited government. Energy transitions cannot be engineered through centralized planning, subsidies, and political mandates. Innovation emerges from competition, experimentation, and market signals—not from governments dictating technological outcomes.

Tyler Durden

Fri, 05/15/2026 – 06:30

https://www.zerohedge.com/geopolitical/europes-green-deal-unraveling

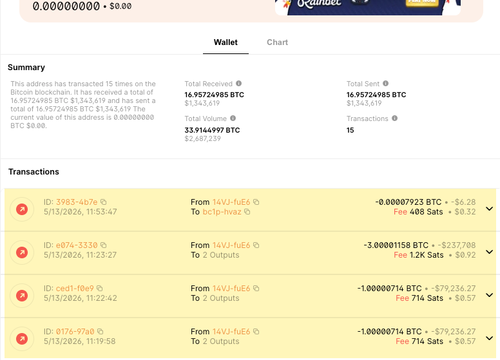

“LoL420F*ckThePOLICE!”: Millennial Uses Claude To Crack Crypto Wallet After Decade-Long Lockout

“LoL420F*ckThePOLICE!”: Millennial Uses Claude To Crack Crypto Wallet After Decade-Long Lockout

A millennial used Anthropic’s Claude to crack the password to his Bitcoin wallet after locking himself out for more than 11 years.

Back in 2014, the X user “cprkrn,” who did not identify himself, explained that he had a crypto wallet on an old computer, got stoned one night, changed the password, and forgot it. He tried trillions of password guesses over the years with no luck.

“I tried like 7 trillion passwords lmfao. Found this old pneumonic a few weeks ago that ended up being the old password before I changed it. Thought I was screwed. Last-ditch effort dumped my whole college computer into Claude,” cprkrn said.

He noted, “It found an OLD wallet file that the pneumonic successfully decrypted. Locked out 11+ years because I got stoned and changed the password.”

The password turned out to be: lol420fuckthePOLICE!* …

Best part is the password was:

lol420fuckthePOLICE!*:)

😂😂😂😂😂😂😂😂😂

— 🍜 (@cprkrn) May 13, 2026

Here are the prompts in Claude that helped the man retrieve five lost Bitcoins…

HOLY FUCKING SHIT OMG CLAUDE JUST CRACKED THIS SHIT, THANK YOU @AnthropicAI THANK YOU @DarioAmodei NAMING MY KID AFTER YOU 😍https://t.co/gObNirRDpS https://t.co/ByTdIM4d20 pic.twitter.com/xB5LUJb6Pe

— 🍜 (@cprkrn) May 13, 2026

And here is proof: the wallet went active on Wednesday after being dormant for a decade.

He added:

Last tweet + muting, asked Claude to summarize our recovery efforts:

TLDR, tried ~3.5 trillion passwords + none worked, ended up matching an old seed phrase found in a college notebook with an old wallet file 🙂 pic.twitter.com/iOaIIVsiHd

— 🍜 (@cprkrn) May 13, 2026

It was on Wednesday when we cited UBS analyst Timothy Arcuri, who provided color on what corporate America thinks about the chatbot race: “The survey continues to point to Microsoft, OpenAI, and Nvidia as the key enterprise AI winners, but with Anthropic gaining ground.”

Read that report here.

Tyler Durden

Fri, 05/15/2026 – 05:45

German SPD Leader Faces Backlash After Claiming Migrants Burdening Welfare System Is A ‘Right Wing Extremist’ Lie

German SPD Leader Faces Backlash After Claiming Migrants Burdening Welfare System Is A ‘Right Wing Extremist’ Lie

Labor Minister and Social Democratic Party (SPD) co-leader Bärbel Bas (SPD) says nobody is immigrating to Germany to take advantage of its social welfare system. However, she has received substantial pushback directed at her claim.

Bas’ comment came during a session of the Bundestag, when AfD MP René Springer asked Bas why she wasn’t cutting spending on immigration due to the current budget crisis, given the clear burden it is putting on social welfare, a situation that is making German taxpayers increasingly angry.

“Immigration into the welfare state threatens social cohesion! The fact is: More and more immigrants are pushing into our social welfare system – and are bringing the system to its limits and to the brink of collapse,” CSU Member of Parliament Stephan Mayer told Bild on Tuesday, as quoted by Junge Freiheit.

Bas, in return, has called this notion a lie from “right-wing extremists.”

Her goal, like many proponents of mass immigration is to link it to eliminating Germany’s skilled worker shortage.

“We have a skilled worker shortage in this country, which many companies are addressing by saying, ‘We need everyone who is here in the country and can work.’”

Mayer, and many others before him, shot her down.

“Every statistic refutes her. The immigration into Germany’s social systems is verifiably documented and one of the main reasons why the Federal Republic is heading toward state bankruptcy,” Springer posted on X last week.

Bärbel Bas hat ein weiteres Zitat für die Geschichtsbücher geliefert. Nach Norbert Blüms „die Rente ist sicher“, Kohls „blühende Landschaften“ im Osten, Merkels „Wir schaffen das“ zur Grenzöffnung und Scholz’ „Doppel-Wumms“ zur energiepolitischen Irrfahrt setzt die… pic.twitter.com/7etME3lddg

— René Springer (@Rene_Springer) May 6, 2026

“There is less and less money for those in need because the wrong people, who have never paid into the system and never will, are being supported by us,” he told Bild.

Remix News has reported extensively on migrant abuse of the German welfare system. In November 2024, data from the federal government revealed that 64 percent of those receiving benefits have a migration background, despite making up a much smaller share of the overall German population. The cost of providing this social welfare rose to €12.2 billion the previous year, but in total, Germany spent nearly €50 billion on immigrants and protecting its border in 2023.

And yet, in August 2025, Germany’s Federal Employment Agency is actively promoting the country’s “citizen’s benefit” (Bürgergeld) to young migrants, with one critic noting: “Germany is so generous that it not only explains to immigrants from abroad how to get a job, but also how to make ends meet in Germany without one.”

That same month, two SPD chiefs in the German state of Thuringia broke with their party, calling for most non-EU migrants — including asylum seekers and recognized refugees — to receive social benefits only as interest-free loans, repayable once they find work, in an effort to break reliance on the state.

Currently, there is very little incentive for many to find work. And even those under deportation orders are being supported at taxpayer’s expense. And this is, of course, ignoring the other issue with massive crime from the migrant community.

Bas, however, has, in turn, said Springer is simply ignorant of the facts.

“You’ve probably never heard of it, because you’re probably not out and about in the country, visiting companies,” she told him.

Alice Weidel, the AfD parliamentary group leader in the Bundestag, reacted to this with her own input:

“The SPD’s denial of reality is symptomatic of the federal government’s inability to act—a government that doesn’t want to change a thing. A political turnaround is only possible with the AfD!” she wrote on X.

According to Günter Krings (CDU), deputy leader of the CDU/CSU parliamentary group, “there are too many people who come to us from other EU countries and only work a few hours a week, receiving social assistance for the rest of their time,” the MP told Bild, noting that the German social system is “a magnet for many EU foreigners.”

Former Bundestag member Joe Weingarten (SPD) described Bas’s statement as “a completely unrealistic assessment.” He added that she “is largely alone in this view, even within the SPD.” Weingarten also told The Pioneer, “Any responsible local politician could provide her with enough examples from their own city to prove the opposite.”

Tyler Durden

Fri, 05/15/2026 – 05:00

“Pushed Into Poverty”: Somalia’s Currency Crisis Leaves Traders Holding Worthless Cash

“Pushed Into Poverty”: Somalia’s Currency Crisis Leaves Traders Holding Worthless Cash

For decades, Muse Omar Jama made a living swapping currencies in Mogadishu’s Bakara market, where customers once lined up to trade Somali shillings for dollars and mobile money. Now his office sits mostly silent, and the safes around him are stuffed with cash no one wants, according to The Guardian.

The problem began when traders in Somalia stopped accepting worn-out shilling notes, saying the bills were too damaged to use. The boycott quickly spread to shops, buses, and businesses across the country, wiping out the value of savings held in local currency. Jama describes the shock bluntly: “It’s like we went bankrupt overnight.”

He can no longer exchange the piles of shillings stacked in his office for US dollars, and many former customers leave empty-handed. “I have to turn them away because my safes, shelves and tables are already full of Somali shillings,” he says.

The Guardian writes that the crisis reflects Somalia’s long shift toward a dollar-based economy. The country hasn’t printed new banknotes since dictator Siad Barre was overthrown in 1991, when the central bank collapsed. Since then, US dollars, remittances sent through hawala networks, and mobile payments have increasingly replaced local currency.

The fallout has hit poor households hardest. Prices for essentials like food, medicine, and transport have risen sharply—one small bag of powdered milk reportedly doubled in price. Jama now walks five kilometers to work because buses no longer accept shillings.

Vegetable seller Asha Ali Ahmed says the change has also hurt small traders. Farmers in Afgoye now demand mobile payments, driving up produce costs in Mogadishu markets. With drought already devastating crops, many customers can no longer afford basic groceries.

According to the World Food Programme, about 6.5 million people in Somalia face severe hunger, while 2 million children under five are suffering acute malnutrition.

The federal government has declared refusing Somali shillings a crime, but many traders doubt it can enforce the order. Jama remains pessimistic: “Millions are going to suffer… More families will be pushed into poverty.”

Tyler Durden

Fri, 05/15/2026 – 04:15

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}