Category: News

The Fed Is Losing Its Biggest Dove

The Fed Is Losing Its Biggest Dove

Jerome Powell’s term as Fed Chairman expires today, with Kevin Warsh now confirmed by the Senate as his successor.

The transition has implications beyond a change in the Fed’s leadership.

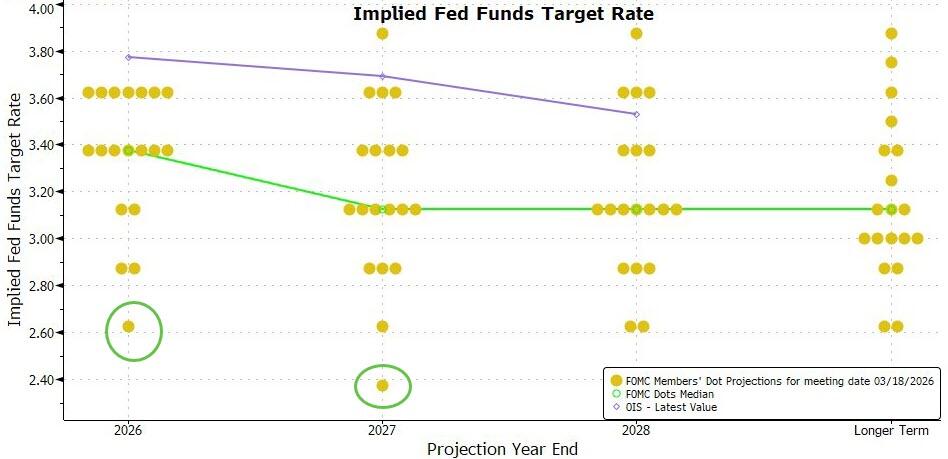

Further, Stephen Miran, who was appointed Fed Governor in September 2025 to fill the vacancy left by Adriana Kugler, is seeing his term come to an end.

Most noteworthy during his term, he dissented at all six FOMC meetings he attended, consistently pushing for 50-basis-point rate cuts.

It’s not a stretch to say he was the Fed’s biggest dove.

In the graphic below, we circle Miran’s year-end Fed Funds projection in the latest Fed’s dot plot.

As shown, Miran projected a year-end 2026 Fed Funds rate of 2.625%, nearly a full percentage point below the current median of 3.42%. That dovish voice is now gone.

Warsh’s arrival shifts the balance. Here are a few considerations worth keeping in mind:

The Fed tilted slightly more hawkishly: Warsh may prove more dovish than his reputation suggests, but it is nearly impossible he will match Miran’s appetite for cuts.

The next FOMC meeting on June 17th is unlikely to produce action. Given recent inflation data, we see little appetite for rate cuts at the next FOMC meeting despite new leadership.

Powell isn’t gone. He has pledged to remain a Fed Governor through January 2028, or until ongoing investigations into the Fed’s construction project and legal challenges against Governor Lisa Cook reach what he calls “transparency and finality.”

The bottom line: The Fed just got incrementally more hawkish, and the June meeting will be the first test of what that actually means. Moreover, Kevin Warsh will now be on the speaking circuit, so we can better ascertain his thoughts on inflation, employment, and how he will lead the Fed going forward.

Tyler Durden

Fri, 05/15/2026 – 12:05

https://www.zerohedge.com/markets/fed-losing-its-biggest-dove

Deadlocked At Square Zero: Very First Line Of Iran’s Latest Proposal ‘Unacceptable,’ Trump Says

Deadlocked At Square Zero: Very First Line Of Iran’s Latest Proposal ‘Unacceptable,’ Trump Says

Tehran and Washington are truly not just back to square one, but it’s as if no rounds of dialogue – direct or indirect – have even taken place. It’s more like being back at square zero – and the US President has just acknowledged it.

President Trump told reporters aboard Air Force One Friday while departing Beijing that even the very first first sentence of Iran’s latest proposal was “unacceptable” and blamed the Iranians for backtracking on the nuclear issue.

The first sentence was an “unacceptable sentence, because they have fully agreed no nuclear, and if they have any nuclear of any form, I don’t read the rest,” he said, stressing that he remains unsatisfied with the “level of guarantee from them.”

Trump’s remarks center on his allegation that Iran agreed to give up its “nuclear dust” but then quickly “then they took it back” – but then stated his view that Tehran will eventually agree to it anyway.

“I looked at it, and I don’t like the first sentence. I just throw it away,” Trump said.

He once again in the comments called for Iran to completely abandon any nuclear capability, insisting there can be “no nuclear of any form.” He described: “You’ve got to get all the fuel out and no more production. You have to get everything.”

Trump has said China’s President Xi Jinping is in full agreement that Iran should not have a nuclear weapon:

According to Trump, Iranian representatives acknowledged only the United States and possibly China possess the specialized equipment necessary to remove radioactive debris from the damaged sites.

“They said the only one that can remove it is China or the U.S.,” Trump said. “They said you were right. It is a complete obliteration.”

The president has said the nuclear material is now “entombed” under ground after nuclear sites were “obliterated” – from bombing operations last June and this latest round of US-Israeli attacks in February through March and early April.

Also this week while in China Trump told Fox News in an interview that he did not underestimate the situation in Iran, despite the constantly shifting and expanding timeline and stated goals within the early weeks of Operation Epic Fury.

TRUMP TO FOX: DIDN’T UNDERESTIMATE ANYTHING ON IRAN

Meanwhile, Iranian Foreign Minister Abbas Araghchi said on Friday that the topic of uranium enrichment “is currently not on the agenda of discussions or negotiations,” but will be addressed in later stages, as cited in Tasnim.

On China and whether President Xi agreed to commit to pressuring the Iranians to reopen the Strait of Hormuz, Trump said Friday “we don’t need favors” but that “we may have to do a little cleanup work.”

“We had a little month-long ceasefire, I guess you’d call it, but we have a blockade that’s so effective, that’s why we did the ceasefire,” he said, after suggesting that the conflict with Iran could continue.

Tyler Durden

Fri, 05/15/2026 – 11:45

Musical Chairs

Musical Chairs

By Molly Schwartz, cross-asset macro strategist at Rabobank

Yesterday, Trump spoke with Xi in Beijing. While markets kept a watchful eye on any headlines about the war in Iran, palates were left dry as only tepid announcements dripped out, such as that China “offered help” on Iran and “pledged not to send weapons.” What they did not manage to evade was a conversation about Taiwan. During the two and a half hour conversation with Trump, Xi underscored that US intervention in Taiwan could trigger a “highly dangerous situation.” While Rubio underscored that the topic of American arms sales to Taiwan wasn’t a major focus of discussion, it likely will be when Congress’ approved USD 14bn arms sale to Taiwan lands on Trump’s desk, and again when Xi visits the White House in September.

While the US and China are stalled in the geopolitical arena, the financial scene seems to be bearing fruit. Treasury secretary Scott Bessent announced that conversations around the creation of a “Board of Investment” were underway, and that tariffs would be reduced or removed for products that the US doesn’t plan on reshoring, like fireworks. China also agreed to buy 200 “big” Boeing planes, according to Trump, which would mark the first significant Chinese purchase of Boeing jets since the last time Trump went to Beijing in 2017. China also hinted that they may intend to buy more US energy to compensate for flows disrupted by the war.

Though Iran didn’t appear to produce much in the way of headlines, the Strait is still closed, and Brent crude oil is still trading above $100/bbl at $106/bbl at the time of writing. According to Reuters, the IRGC announced that some 30 vessels have crossed the Strait since Wednesday (with Tehran’s permission), and transit is being permitted for “some” Chinese vessels.

US Treasury yields closed higher after hotter-than-expected trade price data for April printed, with import prices up 1.9% m/m and export prices up 3.3% m/m. These were the fastest monthly price index increases since early 2022 for both. However, the import price index, excluding petroleum, registered more modest gains of only 0.7% which, while hotter than the expected print of 0.5%, is cooler than levels seen as recently as January and February of this year. USD was the best performing G10 currency yesterday on a one day view. Yesterday afternoon saw a surge in yields across the board, absent a clear driver in sparse news flow, as the 2 year closed 3bp higher, above 4.00%.

Warsh was recently voted in as Fed Chair by the US Senate, but this creates a game of grown up musical chairs for the Board of Governors. There can only be seven Governors on the FOMC, and with Powell not giving his seat up just yet, if no one steps down, we have eight. However, Stephen Miran has announced that he would be stepping down as Governor and has submitted his resignation, effective upon Warsh being sworn in. Miran also assured that while he believes it’s important that the Fed only have one chair, Powell could help Warsh through the transition.

Bloomberg’s Anna Wong hit Powell with an uncomfortable reality check: “if Powell’s Fed had been more active in getting its own house in order following a massive miss on inflation, outsiders would have had less motive and opportunity to attack.” Powell’s Fed was criticized for its slow response to the inflationary pressures which led to “the Great Inflation.” Wong summarizes that “[Powell’s] limited push for accountability, such as a thorough review of Fed’s forecasting framework, opened the door to the nomination of a more aggressive outside like Warsh, who has vowed to ‘break some heads’ at the Fed. The moral of story: Get your own house in order or someone will do it for you.”

Across the pond, UK Health Secretary, Wes Streeting, resigned from his role in an attempt to take over Starmer’s seat. In a statement posted to X, Streeting outlined his accomplishments as Health Secretary, but claimed that he has “lost confidence” in Starmer’s leadership, partially due to the success of the Reform party in elections across the UK last week. Manchester Mayor Andy Burnham has also thrown his hat into the ring after MP Josh Simmons resigned, allowing Burnham to run for Parliament and make a bid for Labour leader as well.

The 30 year gilt yield is down from yesterday’s level of 5.74% to 5.67%, and GBP was the worst performing G10 currency on a one day view, depreciating 0.9% against USD and 0.6% against EUR, and on a month-to-date view, dropped from the fourth worst performing G10 currency to the worst. See Jane Foley’s commentary on GBP here.

Tyler Durden

Fri, 05/15/2026 – 11:30

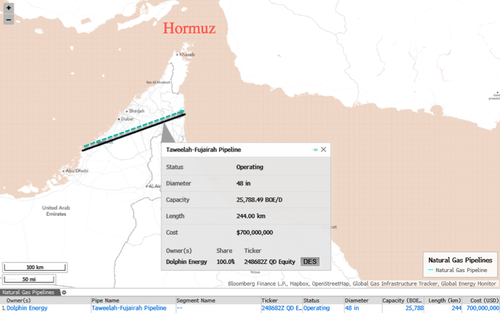

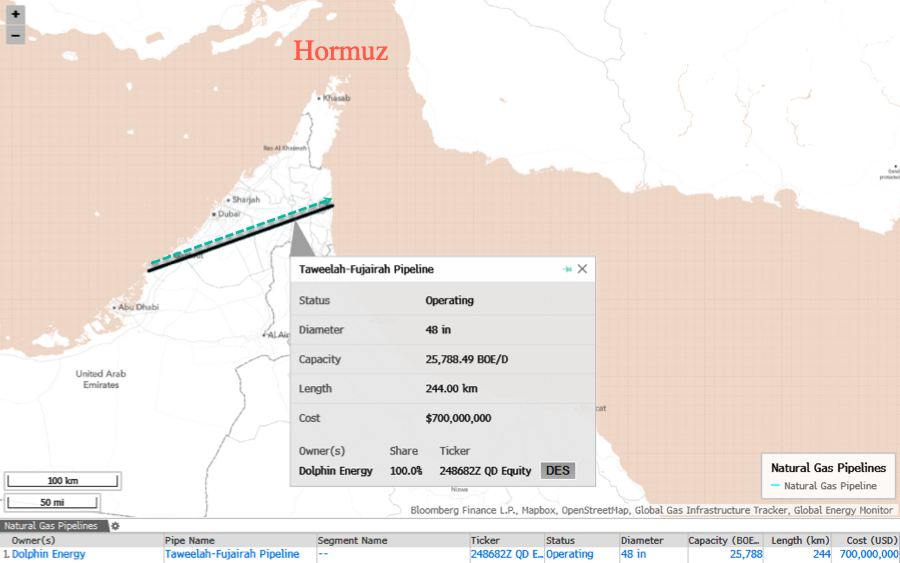

Great Global Energy Rewiring Accelerates: UAE To Double Crude Export Capacity Bypassing Hormuz Chaos

Great Global Energy Rewiring Accelerates: UAE To Double Crude Export Capacity Bypassing Hormuz Chaos

Days after the U.S. bombing campaign against Iran began, we pointed out on March 3 that the conflict was likely to accelerate a major Gulf infrastructure push to bypass the Strait of Hormuz. Saudi Arabia’s East-West pipeline to the Red Sea stood out as the clearest signal that regional producers needed a credible Plan B for moving crude and crude products when the Hormuz chokepoint becomes disrupted. That logic is now coming into sharper focus for the UAE.

March 3:

Surprising Fujairah is not a bigger oil terminal: it bypasses the straits completely.

Expect major infrastructure push here after the war. https://t.co/Do1gK7KBDQ

— zerohedge (@zerohedge) March 3, 2026

Abu Dhabi National Oil Co. (ADNOC) is the UAE’s state-owned energy giant and is set to double its crude-export capacity that bypasses the Hormuz chokepoint next year with the construction of a new pipeline to Fujairah on the Gulf of Oman, according to a new Bloomberg report.

The pipeline project would expand an existing 1.5 million-barrel-a-day pipeline, which has become critical for ADNOC amid the ongoing Hormuz disruption. This allows the UAE to keep about half of its oil exports flowing to the world.

BREAKING: UAE discloses it’s building an additional second pipeline bypassing the Strait of Hormuz.

The new pipeline will be finished in 2027 and will double the country’s export capacity in Fujairah (the current pipeline has a capacity of 1.5-1.8m b/d) pic.twitter.com/adsRgnDbjX

— Javier Blas (@JavierBlas) May 15, 2026

The current bottleneck for the UAE is that ADNOC’s pipeline can handle only about half of its normal export volumes, limiting revenues and proving particularly troubling for the Gulf producer, whose oil-related activity accounted for 22.7% of GDP in Q1 2025.

The urgency to divert flows, or in fact rewire energy flows, will be a top priority for other Gulf producers because oil still matters heavily for public finances and their billionaires.

Perhaps Gulf producers received another memo after President Trump’s comments on Air Force One earlier today, following his China trip, when he said the U.S. does not need to reopen the Hormuz chokepoint. The U.S. still has a naval blockade in place to pressure Iran’s energy complex into collapse, with hopes that Tehran will sign a peace deal.

Tyler Durden

Fri, 05/15/2026 – 11:15

US And China Agree To Establish Trade And Investment Boards As Trump-Xi Summit Delivers Modest Wins

US And China Agree To Establish Trade And Investment Boards As Trump-Xi Summit Delivers Modest Wins

U.S. and Chinese leaders agreed to establish a new “Board of Trade” and a parallel “Board of Investment” during President Donald Trump’s two-day visit to Beijing – a summit that ended much as it began: with significant pageantry, warm personal rapport between the leaders, and modest, incremental progress on trade. The new boards aim to oversee bilateral purchases, manage trade differences, facilitate deals in non-sensitive sectors (with roughly $30 billion in goods identified), and provide a standing channel to prevent future escalations without constant high-level intervention.

The boards were a pre-summit priority pushed by U.S. officials, including Treasury Secretary Scott Bessent and U.S. Trade Representative Jamieson Greer. They build on preparatory talks in South Korea that produced what both sides described as “generally balanced and positive outcomes.” Chinese state media, including Xinhua, highlighted the agreements as part of efforts to expand practical cooperation and maintain stable economic ties.

This development aligns with Xi Jinping’s broader push to reframe the bilateral relationship as one of “constructive strategic stability” – a new guiding vision intended to provide predictability for the next three years and beyond, emphasizing cooperation as the mainstay while allowing for “moderate competition” and “manageable differences.” Xi described it as a positive, sound, constant, and enduring stability that should translate into concrete actions.

Trade and Economic Deliverables

Boeing Aircraft: China committed to purchasing 200 Boeing jets, with Trump indicating the order could potentially grow to 750 based on performance. This was the most visible commercial headline, though it fell short of earlier speculation around larger volumes and drew a muted market reaction.

Agriculture and Energy: Progress on expanded U.S. farm product sales (soybeans, beef, and other goods, with reports of commitments up to $10–50 billion in some readouts) and potential energy deals. Xi told accompanying U.S. CEOs that “China’s door will only open wider” to American businesses, signaling greater market access in mutually beneficial areas.

Investment Outlook: Discussions included pathways for Chinese investment into non-sensitive U.S. sectors, with the Board of Investment intended to provide clearer guidelines and reduce uncertainty from national security reviews.

Trump touted “fantastic trade deals” upon departure, while Xi emphasized win-win outcomes and the importance of sustaining momentum in economic ties.

And hey, America apparently needs 500,000 Chinese students in the US, and China should be able to purchase US farmland so that collages and farm prices don’t collapse, or something.

NOW – Trump says it’s good to have 500,000 foreign Chinese students in the U.S. and for China to purchase U.S. farmland; otherwise, colleges and farm prices would collapse: “I frankly think that it’s good that people come from other countries and they learn our culture.” pic.twitter.com/3vQDXpjchz

— Disclose.tv (@disclosetv) May 15, 2026

Areas Without Breakthroughs

Despite the institutional progress, several high-priority issues saw limited or no resolution:

Nvidia H200 AI Chips: No major summit agreement on advanced AI chip exports. While some U.S. licensing approvals for sales to select Chinese firms occurred around the visit (with Jensen Huang joining the delegation), export controls remained a sticking point and were not centrally resolved in leader-level talks.

Rare Earths: No announced extension of the existing truce or easing of Chinese export controls, which continue to affect U.S. chipmakers and aerospace firms. This remains a lingering vulnerability from prior tariff exchanges.

Iran Conflict: Both leaders expressed a shared desire for stability and reopening the Strait of Hormuz, with Xi showing interest in greater U.S. oil purchases to reduce Middle East dependence. However, China offered no concrete commitments to leverage its influence with Tehran. Beijing’s foreign ministry reiterated support for peace efforts without pledging active intervention.

Taiwan And Competing Narratives

Competing narratives quickly emerged from the summit – highlighting the persistent gap in how Washington and Beijing frame their relationship. Chinese state media, including Xinhua, emphasized Taiwan as “the most important issue” in bilateral ties, with Xi warning Trump that mishandling it could lead to confrontation or even conflict while reiterating opposition to “Taiwan independence.” (U.S. officials, including Secretary of State Marco Rubio, reaffirmed that American policy on Taiwan remains unchanged.) In contrast, the White House readout and Trump’s public comments focused heavily on international issues such as Iran, reopening the Strait of Hormuz, global energy security, and economic cooperation – including Xi’s reported interest in buying more U.S. oil to reduce Middle East dependence, fentanyl precursor controls, and increased agricultural purchases. Trump described the relationship as one that is “going to be better than ever before,” while Xi suggested that “cooperation benefits both, while conflict hurts both.” Analysts noted that Beijing’s spotlight on Taiwan may serve to shape domestic and international perception and divert attention from other sensitive topics like trade imbalances, nuclear issues, and Iran. Meanwhile, the strong U.S. business delegation – including NVIDIA’s Jensen Huang – underscored Washington’s priority of securing concrete commercial wins. These divergent readouts reflect each side’s strategic messaging priorities: China seeking to reinforce red lines and stability on its terms, and the U.S. highlighting transactional progress and geopolitical alignment.

As Rabobank notes;

While markets kept a watchful eye on any headlines about the war in Iran, palates were left dry as only tepid announcements dripped out, such as that China “offered help” on Iran and “pledged not to send weapons.” What they did not manage to evade was a conversation about Taiwan. During the two and a half hour conversation with Trump, Xi underscored that US intervention in Taiwan could trigger a “highly dangerous situation.” While Rubio underscored that the topic of American arms sales to Taiwan wasn’t a major focus of discussion, it likely will be when Congress’ approved USD 14bn arms sale to Taiwan lands on Trump’s desk, and again when Xi visits the White House in September.

* * *

Overall Assessment: The summit went a long way in stabilizing ties through new dialogue mechanisms and modest commercial wins rather than grand bargains. Trump returned with a few modest wins he can highlight domestically ahead of midterms – though the whole ‘Chinese students and farms’ might be a tough pitch to MAGA, while Xi secured a narrative of strategic predictability and time for China to address its economic challenges.

Underlying rivalries in technology, supply chains, Taiwan, and global influence persist, but the relationship now has a more structured channel for management. Future progress is likely to remain incremental and transactional, with the newly agreed boards playing a central role in testing whether this stability proves durable.

Tyler Durden

Fri, 05/15/2026 – 10:45

The Stagflation Narrative: What Doomers Get Wrong

The Stagflation Narrative: What Doomers Get Wrong

Authored by Lance Roberts via RealInvestmentAdvice.com,

The stagflation narrative dominating financial social media isn’t completely wrong. That’s what makes it so dangerous. After more than 30 years of managing client portfolios through actual inflationary cycles, not watching them on YouTube, I’ve learned that the most damaging investment advice isn’t built on outright lies. It’s built on partial truths, stretched past the point where the data still holds.

If you haven’t read Commodity Supercycle: The Enemy Of The Bull Thesis (Part 1), it is an important primer to today’s discussion.

Let’s dig in.

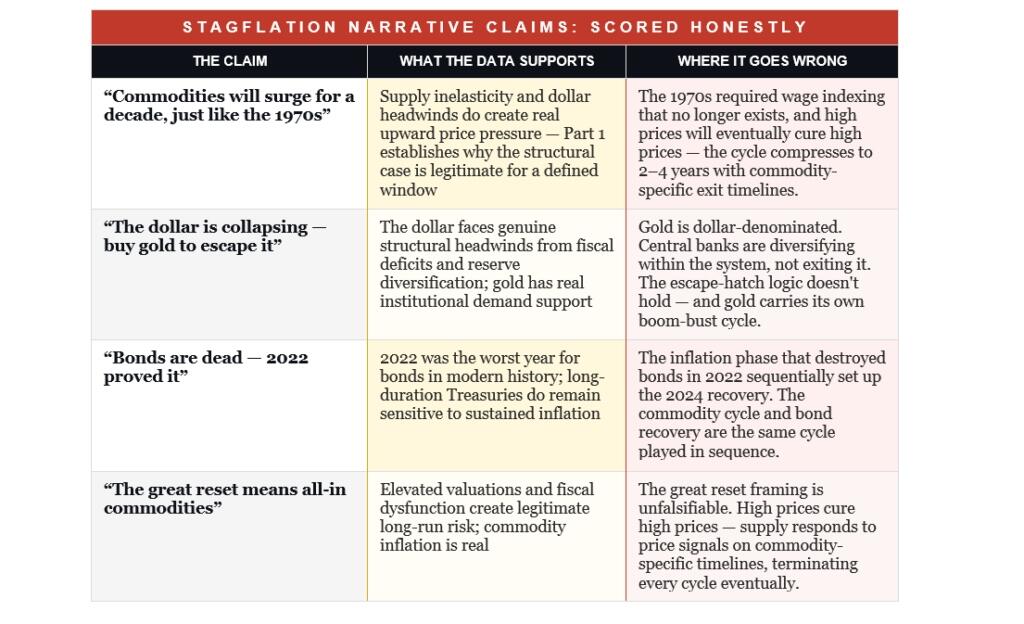

The doomers have legitimate inputs. Supply chains are genuinely under pressure, and the dollar currently faces real structural headwinds. Central banks have been buying gold at a historic pace. Equity valuations in certain segments are stretched, and every one of those observations is defensible. However, the leap from those observations to “sell everything, go all-in on commodities, bonds are dead forever, the great reset is here,” is where the analysis ends and the storytelling begins.

I want to do two things here. First, I’ll score the stagflation narrative claim-by-claim. We will give credit where it’s earned and expose where the logic collapses. I’ll lay out what a sound investment framework actually looks like when the data, not the narrative, drives the decision. Moreover, why the boom-bust nature of commodity markets and the AI-driven capex cycle both fundamentally change where allocations belong.

The Stagflation Narrative Spreading Across Social Media

Spend an hour on X, and you’ll encounter some version of the same script.

The Federal Reserve has destroyed the currency.

The 1970s are back, only worse.

Commodities are going to surge for the next decade.

Gold is the only real money.

Bonds are a guaranteed way to lose purchasing power.

Anyone still holding a diversified portfolio is either naive or not paying attention.

The 1970s comparison is the narrative’s analytical spine. Commodity prices surged for the better part of a decade while equities went nowhere in real terms. Gold went from $35 an ounce to over $800, and the people who held hard assets looked prescient for years. It’s a compelling story, with the added appeal of casting the narrator as the maverick who sees what the establishment refuses to acknowledge.

Here’s the problem.

The 1970s worked the way they did because of structural economic conditions that no longer exist. Both the boom-bust nature of commodity cycles and the emergence of the AI-driven capex boom create dynamics that the doomer framework fails to incorporate.

Before I take this apart, I want to be clear about something. The inputs behind the stagflation narrative deserve serious consideration. As such, dismissing them entirely would be just as intellectually sloppy as swallowing them whole.

As I laid out in Part 1 of this series, supply inelasticity is real. More than a decade of ESG-driven capital discipline, underinvestment in exploration, and production curtailment has left several commodity markets unable to respond quickly when demand rises. That constraint doesn’t vanish because we want it to. It gives the commodity cycle real legs, supporting the bull thesis for select commodities over a meaningful but finite window.

The dollar does face genuine headwinds. Structural fiscal deficits, a Federal Reserve with a long track record of accommodation, and geopolitical pressure on the reserve currency system are all real concerns. JPMorgan projects gold at $5,000 per ounce in 2026, as central bank accumulation runs at roughly 585 tonnes per quarter. There are also pockets of equity valuations that are stretched enough to carry real multiple-compression risk if earnings disappoint.

So the inputs are legitimate. Therefore, there is a version of the commodity trade, sized correctly and timed with discipline, that makes sense right now. The doomer narrative isn’t wrong about the forces in play. It’s wrong about what those forces mean, how long they last, and how to construct a portfolio around them.

Where the Narrative Falls Apart

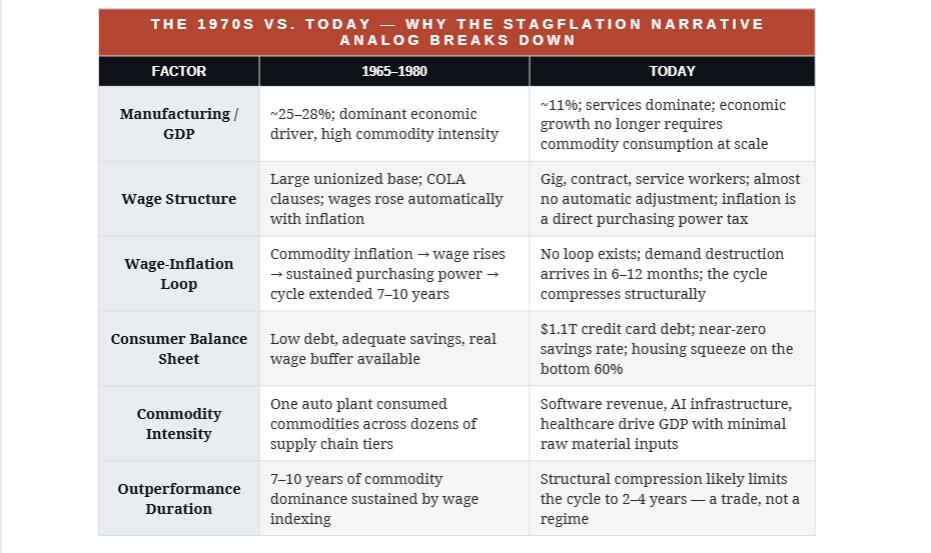

The entire doomer framework rests on one foundational assumption: the 1970s stagflation cycle will repeat itself. Therefore, a 1970s portfolio, heavy on commodities, short on bonds, light on equities, will produce 1970s results. Unfortunately, that assumption doesn’t survive contact with the structural differences between the two economies.

The U.S. economy in the 1970s was built on manufacturing, which accounted for roughly 25% to 28% of GDP. Most crucially, it had a large unionized workforce with cost-of-living clauses written directly into labor contracts. When commodity prices rose, wages rose automatically. In other words, rising costs triggered wage increases, which sustained purchasing power, which kept spending alive even as prices climbed. That feedback loop extended the cycle for years.

The U.S. economy today is roughly 70% to 75% services, and manufacturing accounts for approximately 11% of GDP. The COLA-adjusted workforce is gone. Therefore, when commodity prices rise today, the increase doesn’t trigger wage catch-up. Instead, it functions as a direct tax on purchasing power, and consumers absorb it immediately. What took years to produce meaningful demand destruction in the 1970s now shows up in six to twelve months.

“The 1970s cycle ran on wage indexing. Without it, commodity inflation becomes a demand tax, and demand destruction arrives fast. That is the analytical flaw at the core of the doomer stagflation narrative.”

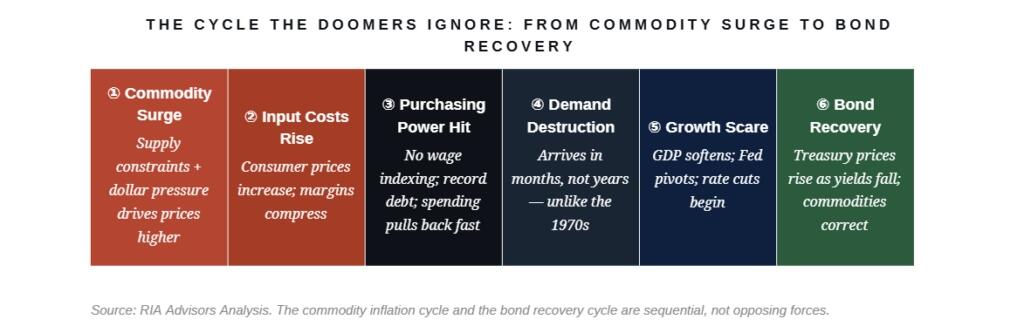

The Inflation Sequence

The doomer version of the stagflation narrative treats the inflation phase as permanent. It isn’t. It’s a phase inside a sequence, and the sequence has a specific ending that the all-in commodity thesis is completely unprepared for.

Commodity prices rise. Input costs surge.

Consumers carrying record debt loads pull back.

Business investment contracts.

Growth slows.

The Fed pivots.

Rate cuts follow.

Bond prices rise.

In other words, the same event that terminates the commodity rally launches the bond recovery.

We saw this exact sequence in compressed form between 2022 and 2024. Commodities surged amid the Russia-Ukraine shock and pandemic-related supply chain disruptions. Bonds had their worst calendar year in modern history. The doomers called it permanent. Then growth wobbled, the Fed pivoted, and by 2024 intermediate Treasuries had recovered sharply while commodity prices corrected from their peaks. The people who abandoned bonds entirely after 2022 missed a significant rally and held concentrated commodity exposure through the drawdown.

The doomer stagflation narrative is built to profit from Phases 1 and 2, but it has no plan, framework, or exit discipline for Phases 3 through 6. That is where the damage happens.

The Gold Logic and the Bond Mistake

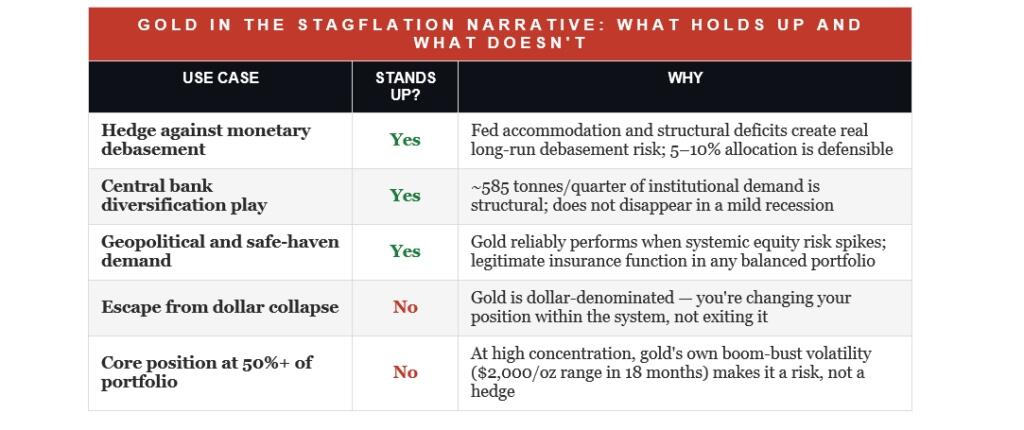

Gold deserves a real discussion, because this is where the doomer stagflation narrative contains its most glaring internal contradiction. Own gold, the argument goes, because the dollar is collapsing and you need to escape a failing monetary system.

Gold is priced in dollars and traded in dollar-denominated markets. Its entire value proposition is measured against the purchasing power of the US dollar. When someone argues that the dollar is collapsing and the solution is a dollar-denominated asset, the argument refutes itself. Central banks buying gold aren’t abandoning the monetary system; they’re diversifying their reserve compositions within it. The Chinese People’s Bank is reducing its concentration in dollar-denominated Treasuries, specifically, but that is a rotation within the system, not an escape from it.

Gold earns a real place in a sound portfolio as a hedge against policy error, inflation (which is what the debasement argument refers to), and geopolitical stress. A 5% weighting of a portfolio allocated to gold, sized appropriately for its volatility, is a defensible position backed by institutional demand data. 50% of a portfolio concentrated in gold because the financial system is “about to collapse” is speculation with an apocalyptic narrative.

The bond mistake is where the most retail damage has been done. The doomers drew a permanent conclusion from 2022’s historically bad bond year. What they missed is that the inflation phase that crushed bonds in 2022 is the same mechanism that eventually forces the Fed to cut rates, which drives bond prices higher. Walking away after the loss and missing the recovery is the most expensive way to be partially right.

I’ve been doing this long enough to know that the most dangerous market narratives are the ones that are right about enough to feel credible all the way through. The stagflation narrative qualifies. Here is every major doomer claim, scored against what the data actually shows.

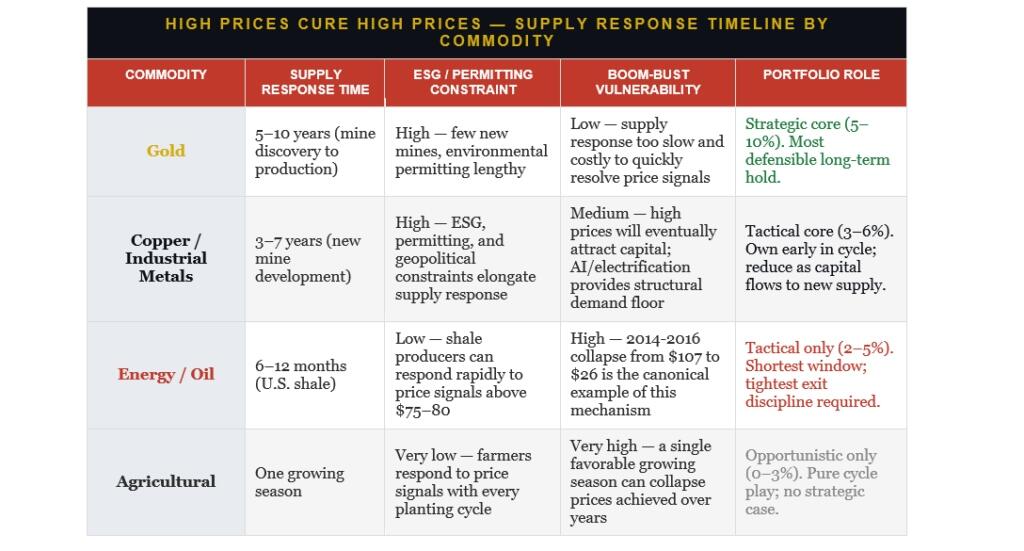

High Prices Cure High Prices

There’s a mechanism the doomer stagflation narrative never seriously models, and it’s the most reliable force in commodity markets: high prices cure high prices. When commodity prices rise far enough, they do three things simultaneously.

They incentivize new supply investment

Activate marginal producers who couldn’t profitably operate at lower price levels (increasing supply)

And they accelerate demand substitution as consumers and businesses find alternatives.

The ESG and underinvestment thesis that Part 1 establishes is real and important, as it delays the supply response and extends the cycle beyond what a typical demand shock would produce. But it doesn’t eliminate the supply response. It sets the clock to a longer timer. The critical insight for portfolio construction is that the timer runs at different speeds for different commodities, and that determines how much of each you should own and how tightly you need to manage the exit.

The 2011 oil market is the canonical example, as West Texas Intermediate Crude traded around $100 per barrel for three consecutive years. During that stretch, the price level didn’t feel unsustainable to the doomers of that era, either, and peak oil narratives were everywhere. Then, oil producers, directly incentivized by those high prices, flooded the market with supply. By early 2016, WTI was trading at $26. The doomers who held concentrated energy positions through that collapse, because the “structural case was intact,” experienced the full arithmetic of boom-bust without a framework for managing it.

CONSISTENCY WITH PART 1 The ESG and underinvestment constraints that Part 1 identifies extend the supply response timeline, but they don’t eliminate it. Gold has the longest clock. Energy has the shortest. That difference in supply response curves should directly determine relative position sizes and exit discipline.

Investment Strategy For Today’s Environment

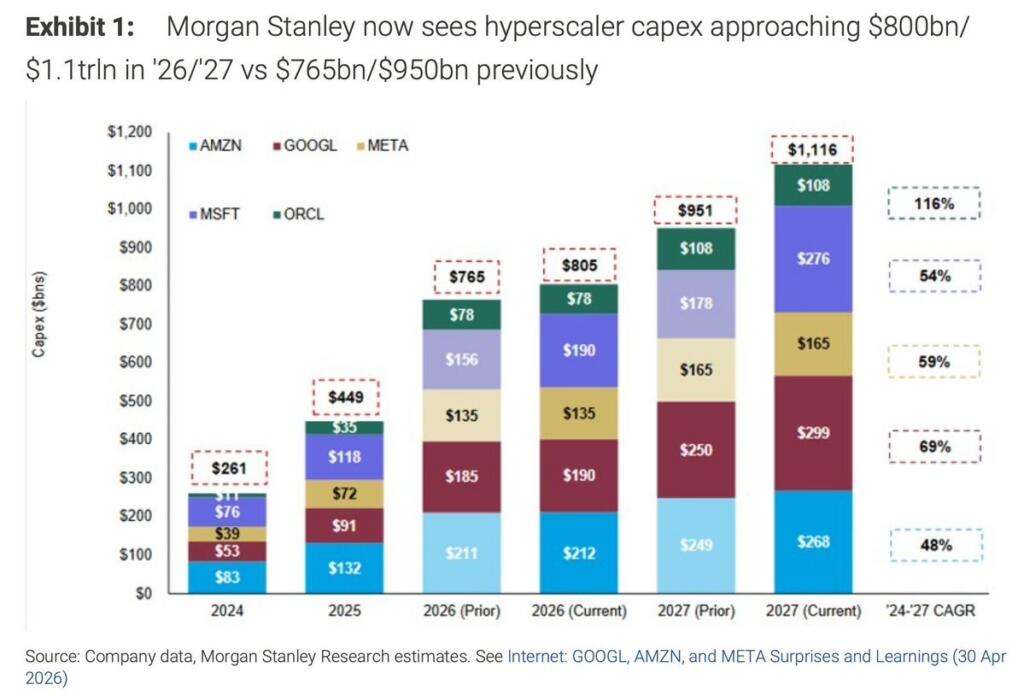

The doomer stagflation narrative misses a second major dynamic entirely: the AI-driven capital expenditure cycle running through the U.S. economy creates a domestic earnings multiplier that didn’t exist in prior stagflation episodes. Microsoft, Oracle, Google, Amazon, and Meta alone are spending hundreds of billions on AI infrastructure that will approach $1.1 trillion by 2027. That capital flows directly into semiconductors, power infrastructure, and data center supply chains, which in turn creates a domestic growth differential with no comparable international analog.

That “multiplier effect” is critical to this story as discussed previously in “The Deficit Narrative May Find Its Cure In AI.”

The American Society of Civil Engineers (ASCE) estimates that every $1 billion in infrastructure investment creates 13,000 jobs and adds $3 billion to GDP over a decade. Therefore, if the U.S. invests $1.8 trillion in AI infrastructure by 2030—plausible given the $500 billion energy need, $300 billion for data centers (150 new centers at $2 billion each), and $200 billion for chip production—GDP could rise by $5 trillion over 10 years, or roughly $300 billion annually. However, that $1.8 trillion is only the beginning. McKinsey & Company expects spending to reach $6 trillion by 2030, just 5 years from now, equating to $18 trillion in economic growth.

That effect was already evident in the Q1-2026 GDP report, where nearly 75% of the 2% annualized growth rate was attributable to business investment in data centers. Currently, the U.S. is projected to grow at roughly 1.8% to 2% in 2026, while Europe struggles to hold 0.5% to 0.8%, and China manages a structural property and debt overhang. That earnings growth differential is real and durable throughout the buildout. The previous case for rotating toward international equities on valuation grounds has also weakened considerably. While European equities ran hard in 2024 and Indian equities now trade at multiples rivaling those of U.S. mid-caps, the broad international valuation discount has compressed.

That said, the AI capex argument carries two important constraints.

First, the earnings are highly concentrated in roughly 8 to 12 companies. The rest of the S&P 500 still faces the same multiple compression risk in a stagflationary environment described in the article. Therefore, owning the broad index is not the same trade as owning the direct beneficiaries.

Second, the capex cycle carries borrowed-demand risk, as these companies pull years of infrastructure investment into a compressed window. When capex growth plateaus, the GDP contribution reverses. The 1990s telecom buildout produced genuine earnings growth in infrastructure, yet ended in a brutal equity cycle when spending decelerated.

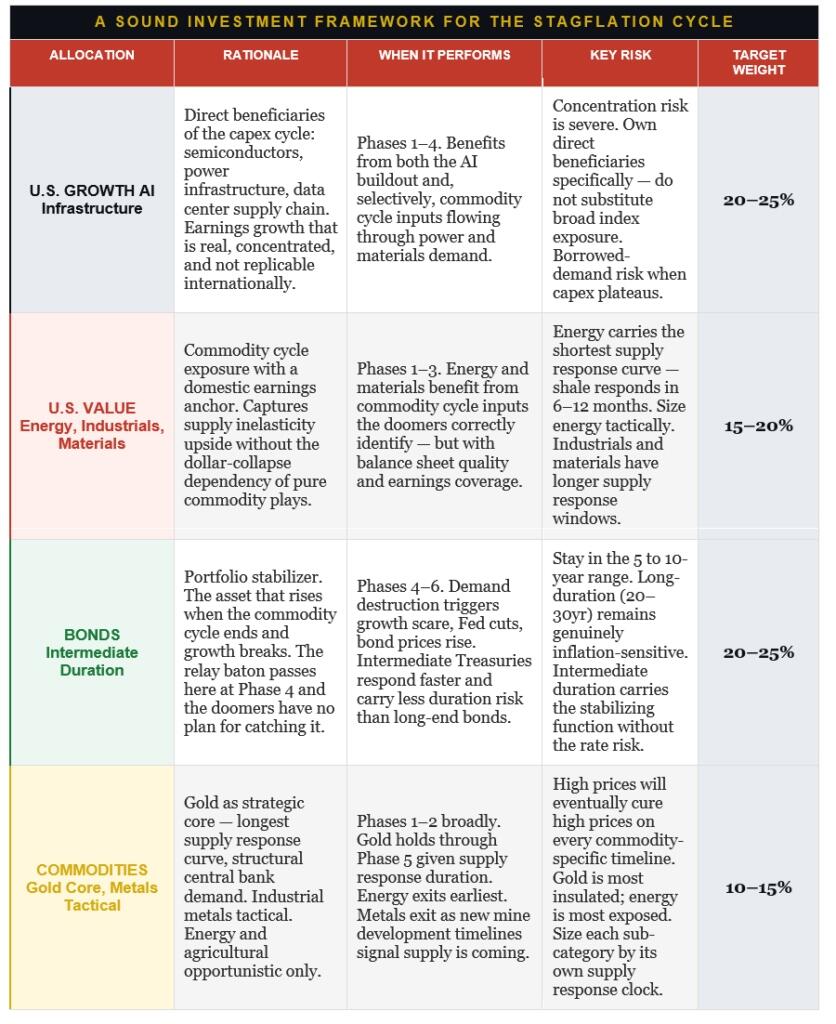

The framework that holds together across all of these dynamics, the commodity boom-bust cycle, the structural compression of demand destruction, the AI capex differential, and the bond recovery sequence, requires four separate allocation legs, each sized for its own cycle duration and exit trigger.

THE REVISED FRAMEWORK The doomer stagflation narrative gets the commodity direction right for the first leg and wrong about the duration, the differentiation by commodity, the bond thesis, and the domestic equity landscape transformed by the AI capex cycle. Own what the data supports. Exit on the supply response clock, not the narrative.

Conclusion

Fear is a durable marketing strategy. The stagflation narrative will keep finding new audiences because it wraps legitimate macro concerns inside an emotionally satisfying story, a villain, a hero, and a clear trade. The people selling it know that partial truths are more persuasive than outright falsehoods. They also know that by the time the cycle turns and the narrative fails, their followers will attribute the losses to bad luck rather than bad analysis.

I’ve watched this play out repeatedly in commodity markets, from the commodity supercycle of 2007 to 2009 to the metals boom of the early 2000s to the oil market in 2011 to 2014. Every time, the same pattern: a legitimate supply constraint, a genuine price move, a narrative that extrapolated the trend into permanence, and then the eventual supply response that high prices had been quietly incentivizing all along. The cycle doesn’t announce its end. It just ends.

The commodity cycle developing now is real, and the AI-driven domestic growth differential is real. However, the bond recovery that follows demand destruction is also real. A portfolio that acknowledges all three, with targeted U.S. growth exposure in the AI infrastructure beneficiaries, U.S. value for the commodity cycle with a domestic earnings anchor, commodity and gold exposure sized by supply response clock rather than apocalyptic conviction, and intermediate bonds providing ballast, is built to survive the full sequence.

That’s the difference between investing in a cycle and betting on a narrative.

Tyler Durden

Fri, 05/15/2026 – 10:30

https://www.zerohedge.com/markets/stagflation-narrative-what-doomers-get-wrong

Iran Says It Has “No Trust” In US, Insists There Is “No Military Solution”

Iran Says It Has “No Trust” In US, Insists There Is “No Military Solution”

Iranian Foreign Minister Abbas Araghchi said on Friday that Tehran has “no trust” in the United States and remains interested in negotiations only if Washington demonstrates seriousness, as talks aimed at ending the war remain stalled. Speaking to Indian media during the second day of the BRICS foreign ministers meeting in New Delhi, Araghchi said military initiatives are ineffective in resolving regional crises, Turkey Today reported.

“There is no military solution, and the U.S. must understand this reality,” Araghchi said, according to a statement shared by Iran’s Foreign Ministry. “They cannot achieve their goals through military action, but the situation would be different if they pursue diplomacy,” he added.

Araghchi also said the United States and Israel had “tested” Iran at least twice during the conflict.

The Iranian foreign minister said one of the main obstacles during negotiations with Washington has been inconsistent messaging from American officials. Araghchi said contradictory statements, interviews and communications from U.S. officials created deep mistrust between the two sides.

Iran has repeatedly accused Washington of pursuing diplomacy publicly while supporting military pressure against Tehran behind the scenes.

Regional tensions escalated after the United States and Israel launched strikes against Iran on Feb. 28, triggering retaliatory attacks by Tehran against Israel and U.S. allies in the Gulf region.

Although a prolonged ceasefire is currently in effect, negotiations aimed at reaching a permanent settlement have largely stalled.

Commenting on the Strait of Hormuz, Araghchi said Iran continues to allow passage for “friendly countries” while imposing restrictions on what he described as “enemy ships.”

“The Strait of Hormuz is not closed to friendly countries. Restrictions are for enemy ships,” he said, although it is unclear why Iran then claims Chinese ships had been blocked until yesterday since China remains Iran’s largest, if not only, oil export client.

“In recent days, many vessels passed through the Strait of Hormuz with the assistance of our naval forces, and this process will continue,” he added.

Araghchi said ships belonging to friendly states and other commercial vessels must coordinate with Iranian armed forces while transiting the strategic waterway.

“The only solution is the complete end of the aggressive war, and afterward we will guarantee the safe passage of every ship,” he said.

He also reiterated Tehran’s position that Iran acted within its right to self-defense following the outbreak of the conflict.

Tyler Durden

Fri, 05/15/2026 – 10:10

Democrats In Illinois Just Lost Hundreds Of Violent Criminals

Democrats In Illinois Just Lost Hundreds Of Violent Criminals

Authored by Steve Watson via Modernity.news,

In yet another glaring example of failed “criminal justice reform” in blue cities, Cook County, Illinois officials have admitted that 243 dangerous criminals have gone completely AWOL from the county’s pretrial electronic monitoring program.

These include individuals charged with murder, attempted murder, and sexual assault — all supposed to be tracked by ankle monitors while awaiting trial instead of sitting in jail.

The revelation comes straight from Cook County Chief Judge Charles Beach II’s new transparency dashboard, which shows roughly 3,048 people currently on the program with 8 percent unaccounted for.

🚨 HOLY CRAP!! Cook County, Illinois Democrats ran a pre-trial program for murders and sexual assaulters so they WOULDN’T BE IN JAIL awaiting trial…

…and 8% OF THEM JUST WENT MISSING! Untraceable.

243 criminals — including murderers, attempted murderers, and sexual… pic.twitter.com/bou1YVobHu

— Eric Daugherty (@EricLDaugh) May 14, 2026

Of the criminals that have gone missing, 21 have been charged with murder, 13 with attempted murder, 103 with sexual assault, and 173 with aggravated battery.

A former Illinois police chief summed it up bluntly: “They have NO idea where they’re at. NONE. ZERO.”

🚨 THIS CANT HAPPEN! Cook County, Illinois just admitted they LOST TRACK of 243 criminals on ankle monitors, including 21 MURDERERS and 13 attempted murderers.

One of them was out on monitoring when he shot and killed a police officer and injured another during an armed robbery… pic.twitter.com/vPbE1ACawK

— Gunther Eagleman™ (@GuntherEagleman) May 14, 2026

The criminals were supposed to be on ankle monitors. Instead, they’re lost, prompting what the report called a “wild goose chase.”

State’s Attorney Eileen O’Neill Burke called the figures alarming and warned of more victims if safeguards aren’t tightened.

Cook County Board President Toni Preckwinkle and Illinois Governor J.B. Pritzker’s justice reforms — including elements of the controversial SAFE-T Act that pushed pretrial release over detention — are now under fresh scrutiny.

As one Illinois lawmaker noted in a follow-up post: “2,450 defendants on ankle monitors. 590 charged with violent crimes. 210 charged with aggravated weapons offenses. 85 felons caught with guns. 21 MURDER defendants. And 8% are just… gone. AWOL. Nobody knows where they are. THIS is Pritzker’s justice system.”

This isn’t some isolated glitch. The same program was ignored by a known career criminal with 72 prior arrests. He violated curfew, boarded a Chicago train, and set a stranger ON FIRE — exactly the kind of preventable horror that keeps repeating under these policies.

Chicago’s Revolving Door Of Doom: 72 PRIOR ARRESTS Revealed For Train Torcher

These repeat offenders keep being enabled in blue cities:

Recent cases like the cop-killing by an EM violator and the train torching show exactly where this leads. Illinois Democrats sold the public on “fairness” and “equity” in pretrial release.

What they delivered is a system where violent offenders roam free until they strike again — or simply vanish. The ankle monitors were meant to be a safeguard. Instead, they’ve become a joke.

Chief Judge Beach says more data and stricter violation reporting are coming. But after years of the same revolving-door failures, residents aren’t holding their breath.

Blue-city leaders keep doubling down on policies that prioritize criminals over victims. The body count — and the missing-persons list — keeps growing.

This is the predictable result of putting ideology over public safety. Until voters demand real accountability and law-and-order leadership, expect more of the same in Chicago and every other city following the same failed blueprint.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Fri, 05/15/2026 – 09:50

https://www.zerohedge.com/political/democrats-illinois-just-lost-hundreds-violent-criminals

US Industrial Production Surged In April

US Industrial Production Surged In April

Despite record low consumer sentiment (if you believe UMich), this morning saw the Empire Fed survey show New York state factory activity expanded in May at the fastest pace in four years, and firms grew more optimistic about the outlook.

That was followed by a much hotter than expected Industrial Production print (up 0.7% MoM vs +0.3% MoM exp and higher than the highest estimate) for April (and March’s decline revised stronger), lifting annual growth up to +1.35% YoY…

Source: Bloomberg

April’s gain for US industrial production was the largest since February 2025.

Manufacturing output rose 0.6 percent in April after edging up 0.1 percent in March.

The production of durables increased 1.2 percent in April, with gains in most categories.

The largest increase was in the output of motor vehicles and parts, which jumped 3.7 percent.

Nondurable manufacturing production edged down 0.1 percent, as declines in several categories – notably the indexes for chemicals and for plastics and rubber products, which both decreased 0.9 percent – were mostly offset by increases in the indexes for food, beverage, and tobacco products, for printing and support, and for petroleum and coal products.

Mining output edged down 0.1 percent in April after falling 1.6 percent in March.

The output of utilities increased 1.9 percent in April, with gains in both electric and natural gas utilities.

Capacity Utilization continued to rise to 76.1% (better than the 75.8% expected)…

So, if Americans are so pissed off (UMich), why is production and factory activity (and retail sales) picking up?

Tyler Durden

Fri, 05/15/2026 – 09:27

https://www.zerohedge.com/economics/us-industrial-production-surged-april

My President Went To Beijing And All I Got Was This Crummy T-Shirt

My President Went To Beijing And All I Got Was This Crummy T-Shirt

Authored by Peter Tchir via Academy Securities,

Stocks rallied after Jensen hopped on AF1 in Alaska. They rallied several times yesterday on Iran/China headlines, on Boeing selling planes headlines, and other soundbites from the much heralded Xi and Trump Summit.

As discussed in Wednesday’s report China and Trade, we did not have high expectations regarding this meeting. We did feel that the President wanted a deal badly enough, that we would get something to help markets, even though it seemed like China had a marginally better/better hand than the U.S.

What we were not expecting was a perfunctory set of meetings and press conferences.

The President is many things, but perfunctory is rarely one of them.

Perfunctory describes an action carried out quickly, superficially, or carelessly, usually as a routine duty rather than out of genuine interest or care.

It implies a lack of enthusiasm, effort, or thoroughness, often done merely to get a task finished. (via AI finding the Merriam Webster definition).

With a truly impressive entourage of politicians, political appointees and business leaders, the stage seemed set for something “bigger” than what we got. We often get more market moving social media posts in the middle of the night than we got as part of this historic meeting.

I did not have high expectations, but I was hoping for more than what we got.

I would rather have seen some confrontation and pushing an agenda, than what seemed quite “perfunctory”.

It leaves me (and possibly markets) a little confused.

Have stocks been pumped as high as they can?

What decision does the President make with Iran over the weekend?

It did not seem like there was any commitment from China to help, and according to at least some comments from the President, China was not asked to help.

Really, not sure what to make of the lack of headlines, but cannot help but think of those souvenir T-Shirts saying My President Went to Beijing and all I got was this Crummy T-Shirt.

It could have been worse.

It could have been a lot better.

But with bonds under pressure, the affordability issue getting more and more attention, and stocks at all time highs, I think markets needed something more than we got.

Maybe there will be a “surprise” statement or two in the coming days, following up on the meeting, but I am disappointed, and suspect markets are too!

Tyler Durden

Fri, 05/15/2026 – 09:15

https://www.zerohedge.com/markets/my-president-went-beijing-and-all-i-got-was-crummy-t-shirt

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}