Category: News

“Energy Is The Issue” – NANO Nuclear Highlights Reactor And Enrichment Opportunity

“Energy Is The Issue” – NANO Nuclear Highlights Reactor And Enrichment Opportunity

NANO Nuclear’s founder and chairman Jay Yu was on Fox Business to discuss the company’s opportunity with data centers, space, and uranium enrichment.

Yu took the time to review their recent deal with Supermicro. The combination of AI and nuclear is being seen on multiple fronts across both industries. In the past few weeks we’ve also seen Terrestrial Energy partnering with Riot, and Oklo collaborating with Nvidia.

Everyone understands the demand for power coming from the AI data center build out is insatiable. We’ve covered previous comments from Jensen Huang, the CEO of NVIDIA, remarking on how energy is the real bottleneck. He was more recently quoted discussing the scale of the current energy gap with future demand…

🚨 JENSEN HUANG: “The amount of energy that we need for computing is probably 1,000x more than we currently have.” pic.twitter.com/3F2DJ48Ebq

— Chief Nerd (@TheChiefNerd) May 14, 2026

The key requirement of the power, though, is stability above all else. Data centers require nearly 100% uptime, something that cannot be promised by renewable energy sources like wind and solar. The power source of the highest capacity factor, a measure of how often they put out their nameplate power, is required to meet the demand of the ongoing energy revolution.

A massive expansion of nuclear generating capacity is the current goal, but what good is a fancy new car if there’s no gas stations to fill it?

Yu’s other business, LIS Technologies, is working to commercialize a novel laser enrichment method to provide the uranium necessary to fuel the incoming fleet of reactors. The laser technology promises to be significantly cheaper to operate as well as less capital intensive to deploy.

The company is currently working to finance and construct their first major commercial facility in Tennessee. The facility can provide millions of Separative Work Units, the unit of measure for enrichment capacity, that could eventually displace America’s need to import Russian uranium.

Tyler Durden

Fri, 05/15/2026 – 19:40

Woke Judge Admits “Taking A Chance” On Violent Criminal… Who Then Went On Shooting Spree

Woke Judge Admits “Taking A Chance” On Violent Criminal… Who Then Went On Shooting Spree

Authored by Steve Watson via Modernity.news,

A Massachusetts judge openly confessed in court that she knew she was rolling the dice by giving a light sentence to a career criminal with a 20-year rap sheet packed with violence, guns, and assault convictions.

She did it anyway. Now Tyler Brown is back in custody after opening fire with 50 to 60 rounds on a busy Cambridge roadway, critically injuring two innocent drivers.

The shocking audio, released this week, comes straight from Brown’s 2020 sentencing hearing after he fired 13 rounds at Boston police officers. Prosecutors had pushed for 10 to 12 years behind bars. The judge gave him just five. He walked out on parole in March 2025.

In the newly surfaced clip shared on X, the judge tells Brown directly:

“I do realize I’m kind of taking a chance on you — when people stand up, police, experienced police officers, experienced probation officers, and they tell me this guy is a danger to the community.”

She went on to acknowledge she could not predict the future but was still willing to release him, saying she hoped her “intuitions” would prove correct and that Brown would not “endanger other peoples’ lives as you have in the past.”

NEW audio from the judge who released Cambridge gunman Tyler Brown

🚨 This audio is INSANE. The judge says she has been advised by experienced officers how dangerous he is but she’s ignoring them

In 2020, Tyler Brown fired on police officers and only got 5 years. He has a 20… pic.twitter.com/sOlw4IghHP

— Wall Street Apes (@WallStreetApes) May 15, 2026

Brown’s record at the time already spanned two decades and included violence against both police and civilians, firearms offenses, drugs, assault with a dangerous weapon, a 2014 stabbing, and an armed robbery in Michigan. He was on probation when he shot at officers in 2020.

Yet the judge — identified as Janet Sanders — chose leniency over the unanimous warnings from law enforcement professionals on the front lines.

Earlier this week, Brown unleashed chaos on Memorial Drive in Cambridge, spraying vehicles stuck in traffic with heavy gunfire. A state trooper and an armed civilian returned fire, stopping the rampage and wounding Brown before he could kill anyone else.

This is the predictable outcome of a justice system that treats violent repeat offenders as candidates for redemption experiments while law-abiding citizens bear the consequences.

Blue-state judges keep betting against public safety, and Americans keep paying with their lives and security.

Many have responded to call for judges like this to be charged as accessories when they go lenient on violent career criminals.

The pattern is impossible to ignore. Soft-on-crime policies, activist judges, and revolving-door “justice” have turned too many American cities into danger zones.

This is not compassion. It is recklessness with other people’s lives. Real justice means keeping predators off the streets for the full measure of their sentences — no early releases, no “chances,” no crystal-ball prayers from the bench.

Strong leadership has always understood this basic truth: protect the law-abiding first. Until judges face real accountability for endangering the public they swore to serve, these tragedies will keep repeating. The audio makes it crystal clear — the warnings were there. The judge just chose to ignore them.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Fri, 05/15/2026 – 19:15

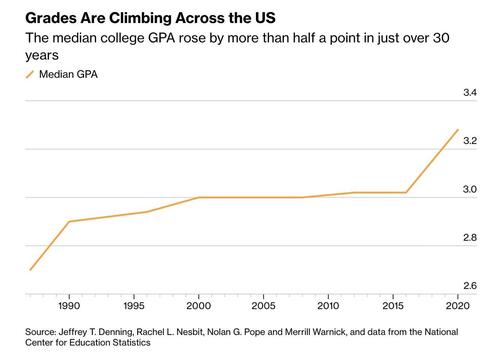

Harvard Weighs Major Crackdown On “Grade Inflation”

Harvard Weighs Major Crackdown On “Grade Inflation”

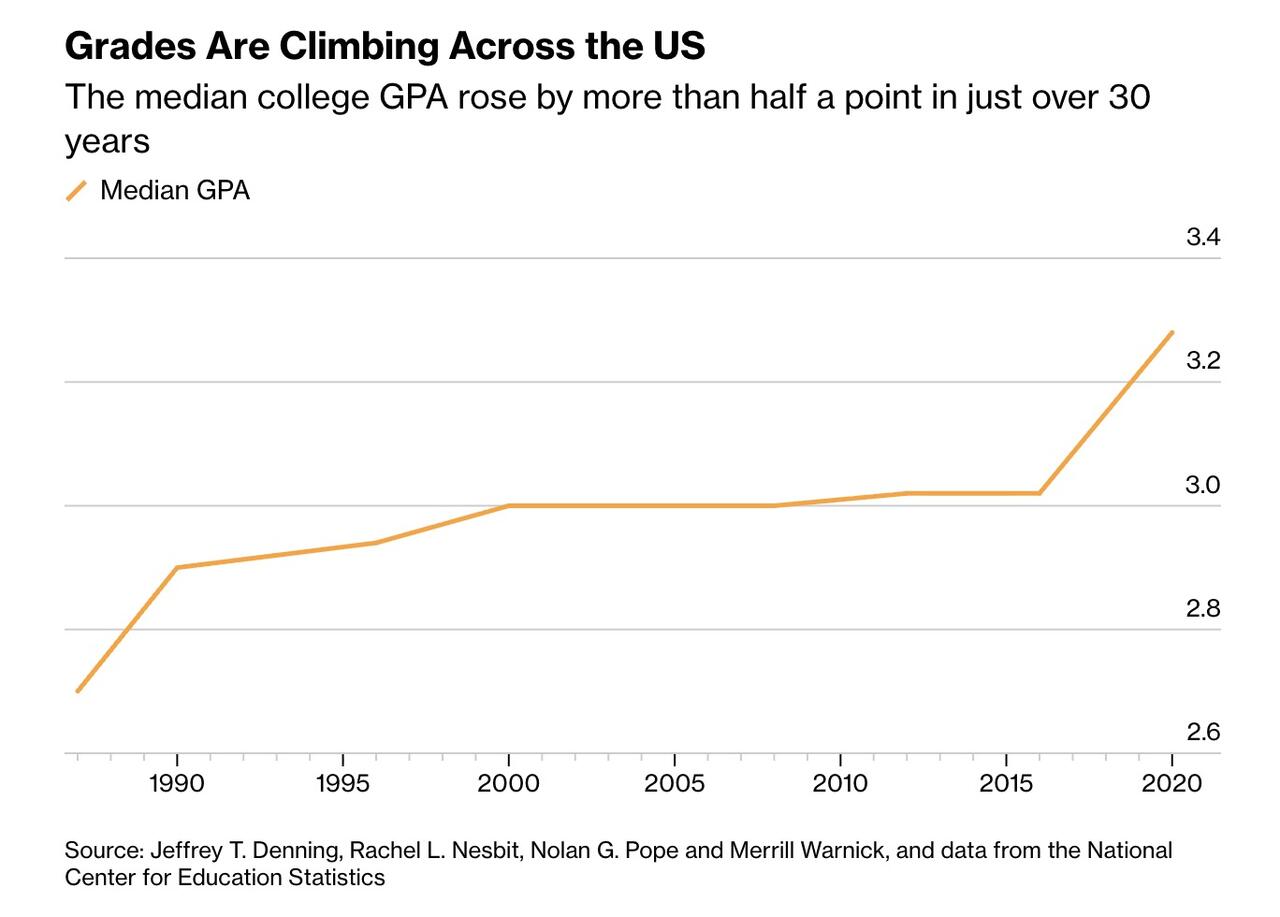

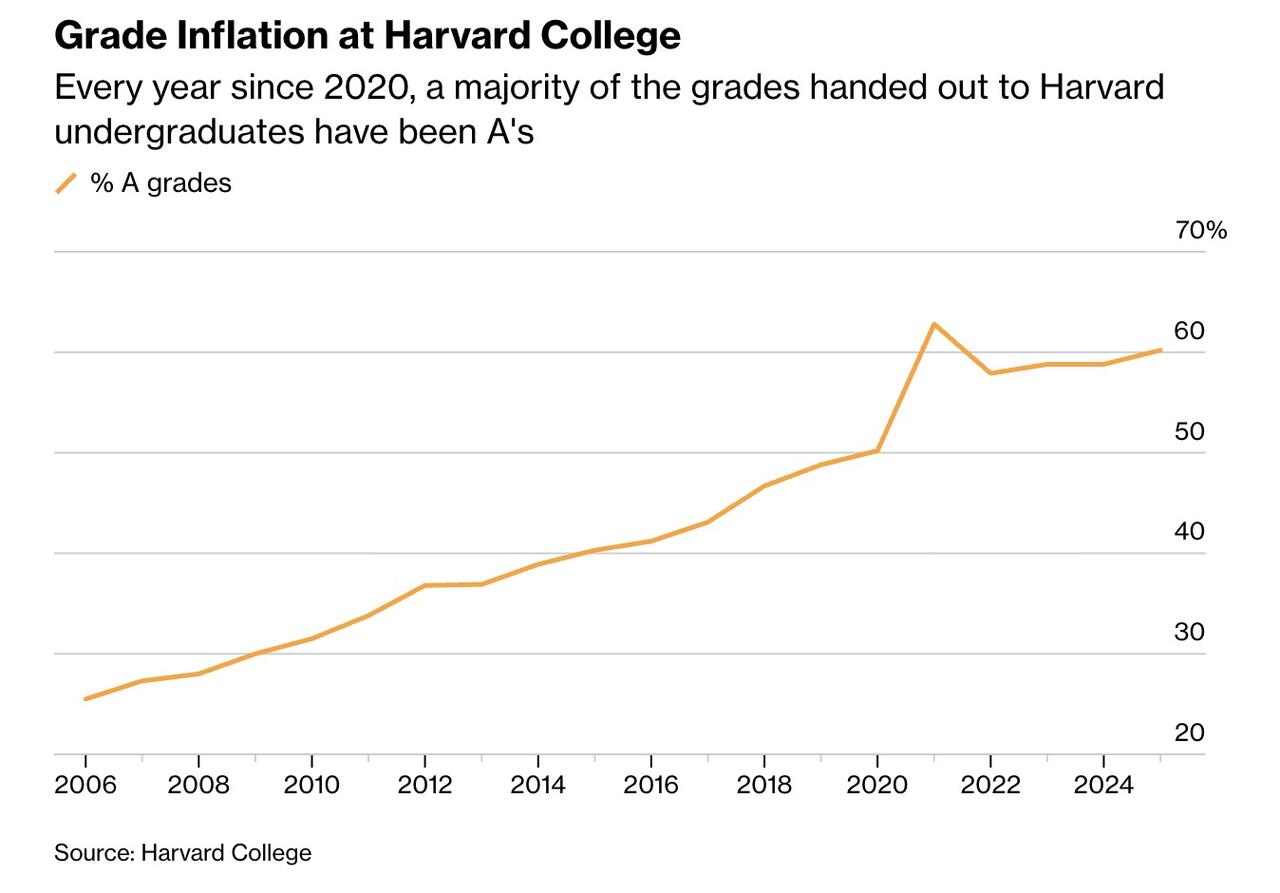

Harvard faculty begin voting Tuesday on what may be the most aggressive effort in decades to curb grade inflation, a long-running issue that has also drawn attention from the White House as it pushes broader higher-ed reforms, according to Bloomberg.

The proposal would cap A grades in undergraduate classes at 20% of students, plus four additional students. The move comes after A grades surged at Harvard: about 60% of grades were A’s in the 2024–25 academic year, more than double the rate in 2006. After administrators pushed for stricter grading last fall, that number dropped to 53%. Faculty have one week to vote, with results expected May 20.

Supporters say grade inflation has made academic distinctions less meaningful. Last year, Harvard seniors needed a 3.989 GPA to earn summa cum laude, and an award traditionally given to one student ended in a 54-way tie. As professor Jason Furman said, “It’s fundamentally dishonest to give the best students in the class the same grade as someone in the bottom half.”

Bloomberg writes that students have strongly opposed the plan, arguing it would increase stress, discourage academic risk-taking, and push students toward easier courses. Nearly 85% of undergraduates surveyed by The Harvard Crimson opposed the proposal. Student leader Caleb Thompson said “people really are against this,” while senior Summer Tan said students are already seeking easier classes instead of more challenging ones.

Some faculty members agree. Scott Duke Kominers warned the policy could discourage ambitious students and make Harvard less attractive to top applicants.

Harvard’s decision could influence other elite schools. Yale recently considered an even stricter proposal for a campus-wide average GPA of 3.0. Earlier efforts at Princeton and Wellesley initially reduced top grades but were eventually reversed after student backlash.

Critics argue schools hesitate to grade more strictly because students could be disadvantaged if peer institutions do not follow. Still, supporters believe Harvard’s prestige could set off broader reform.

If approved, the policy would take effect in fall 2027. Faculty are also voting on allowing some courses to opt out through a satisfactory/unsatisfactory grading system and on replacing GPA with percentile rank for academic honors.

Tyler Durden

Fri, 05/15/2026 – 18:50

https://www.zerohedge.com/markets/harvard-weighs-major-crackdown-grade-inflation

Closing Arguments In High-Stakes OpenAI Trial Focus On Reputation, Character

Closing Arguments In High-Stakes OpenAI Trial Focus On Reputation, Character

Authored by Beige Luciano-Adams via The Epoch Times (emphasis ours),

OAKLAND, Calif.—After nearly three weeks of presented evidence, an Oakland jury on May 14 heard final arguments in a high-stakes legal battle that could have profound impacts on the race for artificial intelligence.

Tech moguls Elon Musk and Sam Altman, once friends and partners in a fledgling AI startup with big dreams and a noble mission, are nearing the climax of a bitter feud over the future of an $852 billion company.

Despite a judicial ban on testimony related to AI-induced “extinction” scenarios, references to speculative risks still surfaced during the Oakland courtroom proceedings, appeared in discussions around “risk” and “safety.” Vague promises about the future benefits of an unrealized technology were also touched upon.

On the stand, Tesla CEO Musk told the court, “We don’t want to have a Terminator outcome,” suggesting humanity would be better off with a “Star Trek” future written by Gene Roddenberry, rather than something from the mind of James Cameron.

Musk cofounded OpenAI in 2015 with Altman, President Greg Brockman, and former chief scientist Ilya Sutskever. At the time, both Musk and Altman expressed grave concerns about the unregulated advancement of Artificial General Intelligence (AGI)—a hypothetical point at which the machines “outsmart” humans and operate autonomously.

Those concerns, Musk testified, were the express motivation for founding OpenAI: open-source to prevent consolidation of power, and philanthropic to offset the profit-driven AI race.

He sued Altman and Brockman in 2024, alleging they bilked him out of $38 million in donations, then restructured as a for-profit corporation by exclusively licensing their flagship product, ChatGPT, to Microsoft—and in doing so, betrayed their founding mission.

OpenAI and Microsoft deny the allegations, arguing Musk abandoned the company in 2018 to start his own for-profit competitor, xAI, when other founders rejected his bid to take full control of the operation.

Alongside the “preponderance” of evidence that both sides say supports their claims, the trial was just as focused on the two men’s reputations and characters.

“Sam Altman’s credibility is directly at issue in this case,” Steven Molo, an attorney for Musk, said in his closing statement. “The defendants absolutely need you to believe Sam Altman. If you cannot trust him … they do not win.”

Molo questioned Altman earlier this week over a list of employees and colleagues who, both on and off the record, have characterized him as dishonest and opportunistic.

OpenAI attorneys dismissed the tactic as “character assassination.”

Sarah Eddy, an attorney for OpenAI, countered, “Mr. Molo says Sam Altman can’t be trusted, but Mr. Musk is the one whose testimony is contradicted by every other witness and all the documents.”

Altman, Brockman, and others cast Musk as a detached outsider who contributed little if any sweat equity, had fraught relationships with colleagues, and attempted to poach OpenAI’s employees for his other companies.

“The claim is that the Midas touch of Elon Musk made OpenAI what it is today,” William Savitt, an attorney for OpenAI, said in closing arguments.

“Elon, Elon, Elon. ‘It was all me.’ Mr. Musk wants all that credit, but he hasn’t earned [it].

“This requires a touch that he doesn’t have. This is not a bulldozer. … To succeed in AI, as it turns out, all Mr. Musk can do is come to court.”

Savitt pointed out Musk wasn’t present for closing arguments, having jetted off to China earlier in the week with President Donald Trump.

Gesturing at Altman and Brockman, he said: “My clients are here because they care a lot about it. Mr. Musk came to this court for exactly one witness—Mr. Musk. Now he’s in parts unknown.”

Musk, according to the Forbes Billionaire Index, is the wealthiest person in the world, with a net worth of around $826 billion. Brockman received equity in the OpenAI corporation worth around $30 billion, and Altman’s net worth is around $3.5 billion.

When Brockman took the stand last week, Molo accused him of plotting to use OpenAI to become a billionaire.

“You had a fiduciary duty [to the nonprofit],” the attorney said. “You took the assets from the nonprofit, you moved them into the for-profit to create this money-making machine that resulted in you having $30 billion.”

Brockman said such was a “deep mischaracterization.” Personal diary entries from late 2017 in which he muses about profits, and about how it would be “morally bankrupt” to “steal the nonprofit” from Musk, he said, were expressions of frustration.

Jurors heard from a parade of Silicon Valley insiders, including all four founders, and from dueling experts on AI safety, nonprofits, business law, and forensic accounting. They watched lawyers pick through reams of internal documents, analyzing complex corporate and financial histories, while private diaries, email, and text threads offered insight on the parties’ underlying motivations and shifting alliances.

“Everyone here has rights, even really rich guys like Elon Musk,” Molo said. “His is a claim that comes from a very deep place inside him, from his passion for this issue.”

During his own testimony, Musk often told the court, “You can’t just steal a charity.”

When his time on the stand came, Altman clapped back, “No, you can’t steal it, but Mr. Musk did try to kill it.”

Altman said on Tuesday that Musk contributed only 28 percent of the nonprofit’s funding from 2015 to 2020, and failed to come through on a $1 billion pledge, leaving the startup with few options.

OpenAI argues its nonprofit foundation is now one of the “best-resourced” in the world, with an equity stake in the company’s for-profit corporation approaching $200 billion—a direct result of $13 billion worth of investments from Microsoft and a 2025 restructure sanctioned by California and Delaware attorneys general.

The details of OpenAI’s journey from a scrappy, underfunded nonprofit to one of the most powerful and valuable AI companies are highly contested. In addition to the power struggle with Musk in 2017 and 2018, it involves a messy 2023 governance shakeup in which Altman and Brockman were briefly ousted and Microsoft was deeply entangled.

By 2017, all parties had agreed they would need vastly more capital and computing power to compete with AI giants such as Google. Various ideas were floated, debated, and discarded—including rolling OpenAI into Tesla and even turning to cryptocurrency. Ultimately, under Altman’s leadership, the company created a for-profit subsidiary in 2018 and, in 2019, partnered with Microsoft. In 2025, OpenAI restructured as a public benefit corporation, which its leaders say remains under the control of the foundation and loyal to the original mission.

The foundation holds an approximately 27 percent equity stake in the corporation; Microsoft owns a 26 percent stake.

Molo argued on Thursday that Microsoft’s investment breached the charitable trust Musk created by enriching its investors and “insiders” at the expense of the nonprofit, and failing to open-source the technology, prioritize AI safety, or follow nonprofit custom and practice.

The $13 billion Microsoft has invested since 2019 dwarfed charitable contributions and weakened OpenAI in its negotiating position with Microsoft, Molo said, resulting in a company focused on commercializing AI, with a gutted charity that does little more than sanitize its reputation.

As for Microsoft, Molo said the company was aware of what OpenAI was doing “every step of the way, they helped them violate their nonprofit mission, that’s aiding and abetting pure and simple.”

OpenAI and Microsoft argued there was never any charitable trust to breach.

Eddy, the OpenAI attorney, argued there were never any strings attached to Musk’s donations to OpenAI, and that he failed to demonstrate that he “properly manifested a specific intent” to devote the trust to a specific purpose, his $38 million in donations going instead to generally further the mission of the nonprofit.

“The specific purposes cannot just be in his head,” Eddy said.

Absent evidence proving this intent and specificity, she said, the plaintiff had resorted to implication and inference.

“It’s all made up,” she said.

As Musk told it, OpenAI’s mission was clear.

“I specifically came up with the idea, the name, recruited key people, taught [them] everything I know, provided the original funding. … It was specifically for a charity that did not benefit any individual person. I could’ve started it as a for-profit, and I chose not to,” Musk said.

He is asking that Altman and Brockman be removed from their leadership positions at OpenAI, and that more than $100 billion be returned to the nonprofit foundation.

In addition to Musk’s three claims—breach of charitable trust, restitution based on unjust enrichment, and, against Microsoft, aiding and abetting a breach of a charitable trust—jurors will decide whether those claims are barred by a statute of limitations.

The jury will begin deliberations on Monday at 8:30 am.

Tyler Durden

Fri, 05/15/2026 – 18:25

https://www.zerohedge.com/ai/closing-arguments-high-stakes-openai-trial-focus-reputation-character

Rep. Steve Cohen Drops Reelection Bid After Tennessee Redistricting

Rep. Steve Cohen Drops Reelection Bid After Tennessee Redistricting

On Friday Democratic Rep. Steve Cohen of Tennessee announced he is ending his bid for reelection to Congress, capping a nearly 20-year career in the U.S. House. The decision comes days after the Republican-controlled Tennessee legislature approved a new congressional map that dramatically reshapes – and effectively dismantles – his longtime majority-Black 9th District in Memphis.

Cohen, 76, described the moment as “by far the most difficult” in his career as an elected official. He formally requested removal from the ballot for the August primary and stated he would retire from public life at the end of his current term. “The 9th District that they have under these new lines is nothing like the 9th District that I’ve represented,” he said, noting that the redrawn district no longer resembles the community he has served since 2007.

Background on the Redistricting

Tennessee Republicans pushed through the new U.S. House map during a special session in early May 2026, following a recent Supreme Court ruling. The changes split the Memphis-based 9th District – long a Democratic stronghold with a majority African American population – across multiple Republican-leaning districts. Critics, including Democrats and civil rights advocates, called it gerrymandering aimed at diluting Black voting power and eliminating the state’s only Democratic congressional seat ahead of the 2026 midterms.

Cohen and others have filed lawsuits challenging the maps. A judge recently denied a temporary restraining order to block them. Cohen has described the process as a “gangster move” influenced by national Republican strategy under President Donald Trump.

Before redistricting, Cohen faced a competitive Democratic primary challenge from progressive state Rep. Justin Pearson. Pearson has indicated he will continue his campaign in the redrawn 9th District. Cohen’s Memphis residence now falls into the 5th District (currently held by Republican Rep. Andy Ogles), which some see as more competitive. Cohen has endorsed Columbia Mayor Chaz Molder, a Democrat running there.

Tyler Durden

Fri, 05/15/2026 – 18:00

Ethanol: Not The Energy Transition We’re Looking For

Ethanol: Not The Energy Transition We’re Looking For

Authored by Ike Kiefer via RealClear Energy,

With current events stirring up global energy prices, corn ethanol is again being dressed up as if it is a domestic energy source and agent of energy security. The truth is that corn ethanol is an energy sump, and that it takes more fossil fuel energy to make a gallon of corn ethanol than a gallon of gasoline. It is time to face this unpleasant truth and the other perverse outcomes achieved by twenty years of misguided policy.

In 2005 and 2007, Congress passed the Energy Policy and Energy Independence and Security Acts that together created the Renewable Fuel Standard (RFS) program. RFS had three stated objectives: to improve U.S. energy security, to reduce greenhouse gas (GHG) emissions, and to support rural economies and agricultural development. Instead, RFS has increased motor fuel prices, increased food prices, put millions of carbon-sequestering acres of land into intensive cultivation, increased GHG emissions and air pollution, and increased water consumption and pollution. As to energy security, the gallons of U.S. gasoline displaced by federal ethanol blending mandates are being exported to Mexico and other nations. The great success of RFS has been the hand of government transferring wealth from motorists to big ag corporations. It’s past time to stop the economic and chemical absurdity of forcing food to be fuel.

The government wanted biofuels bad, and it got them bad. Under Corn Belt lobbying pressure, Congress cynically waived the need for RFS to achieve actual GHG reductions for all existing corn ethanol biorefineries, plus all that could be built by the end of 2010. The bulk of the corn ethanol produced over the past 20 years and still today comes from these waivered plants. The EPA’s specious 2010 prediction that corn ethanol would achieve a 21% GHG reduction by 2022 was immediately challenged by the National Research Council for not properly counting land-use change and not realistically treating food competition and water use. This panel of experts from the National Academy of Sciences even questioned the viability of the entire concept of reducing GHG with biofuels. The most rigorous and honest estimate by a third party in testimony before Congress used the EPA’s own methodology to show that adding corn ethanol to gasoline has increased GHG emissions by 28% over the pure gasoline baseline with no trajectory to ever recover.

As to energy security, the goal was noble, but the method was irrational. Corn ethanol is critically dependent upon fossil fuels at every stage of production—tractor and truck fuel, fertilizer and pesticides, biorefinery energy and chemicals. Biofuels in general are just a way to put a green fig leaf on petroleum by inefficiently re-routing it through a farm field. While corn ethanol production has plateaued at 15-16 billion gallons for the past 10 years—not coincidentally matching the federal subsidy limit—domestic crude oil production has skyrocketed due to technological innovations that have opened up vast new geological formations to economic production. Despite a raft of federal policies and actions as negative for petroleum as they have been favorable for biofuels, the USA is once again energy self-sufficient and the world’s largest producer of crude oil and natural gas. In 2024, the USA exported 100 billion gallons of refined petroleum. Other countries are burning U.S. gasoline in their cars and producing the same CO2 emissions as if Americans were allowed to use it. The energy security objective for RFS is moot, and it was never achievable with fossil-fuel dependent corn ethanol.

On of the great ironies is that RFS was authorized under the Clean Air Act. The EPA’s own 2010 regulatory impact analysis showed it would increase net air pollution and cause up to 245 more U.S. deaths per year. The EPA also granted corn ethanol a perpetual vapor pressure waiver for smog-causing emissions that it has denied to petroleum. Perhaps worse, ethanol in gasoline enables the hydrocarbons to mix with water and thereby increase ground water and surface water contamination from fuel leaks to a far greater degree than the demonized MTBE it replaced as octane booster, yet EPA continues to ignore this risk completely.

A government program that has strayed so far from its objectives should be terminated. The federal agency in charge of protecting the nation’s environment should not be allowed to administer a program that increases air pollution and stresses on water, land, and climate. Fuel should be fuel and food should be food. Surely Congress can find a better way to genuinely promote U.S. energy security and boost rural economies without imposing the highly regressive tax of increased fuel prices, inflicting such harm to the nation’s air and water resources, and promoting global food insecurity.

Ike Kiefer is a Visiting Fellow at the National Center for Energy Analytics and author of the study,Ethanol as Fuel: A Bridge to Nowhere.

Tyler Durden

Fri, 05/15/2026 – 17:40

https://www.zerohedge.com/energy/ethanol-not-energy-transition-were-looking

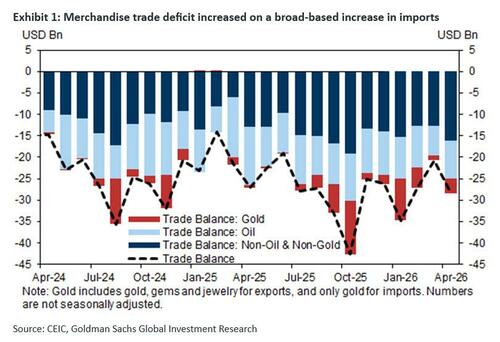

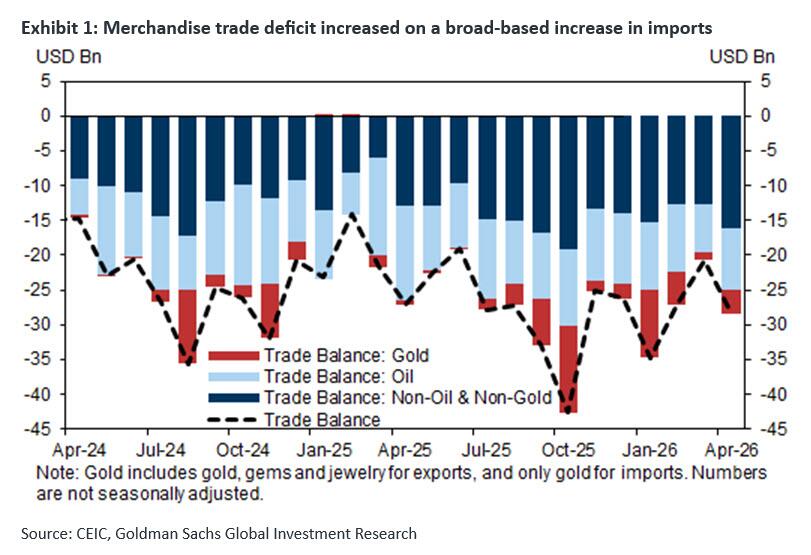

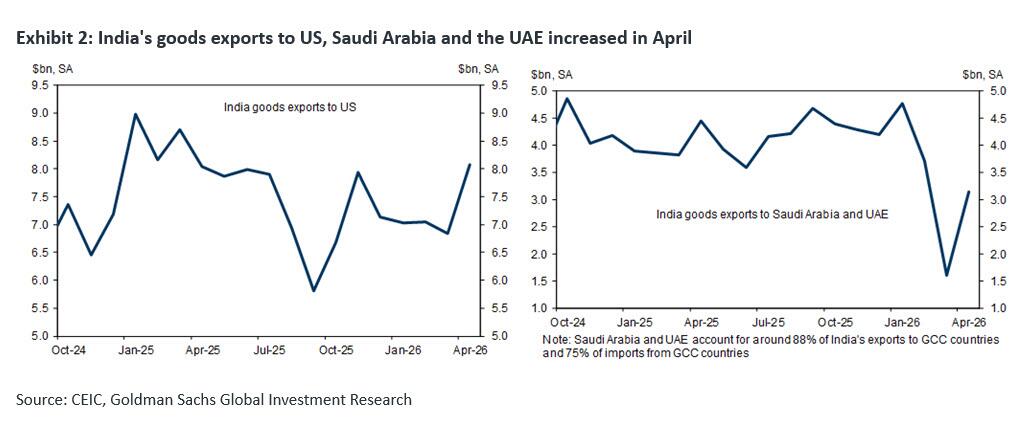

India’s Trade Deficit Surges As Energy Import Prices Soar

India’s Trade Deficit Surges As Energy Import Prices Soar

India’s trade deficit soared in April by more than analysts expected, as the surge in oil and gas prices hiked the Indian energy import bill.

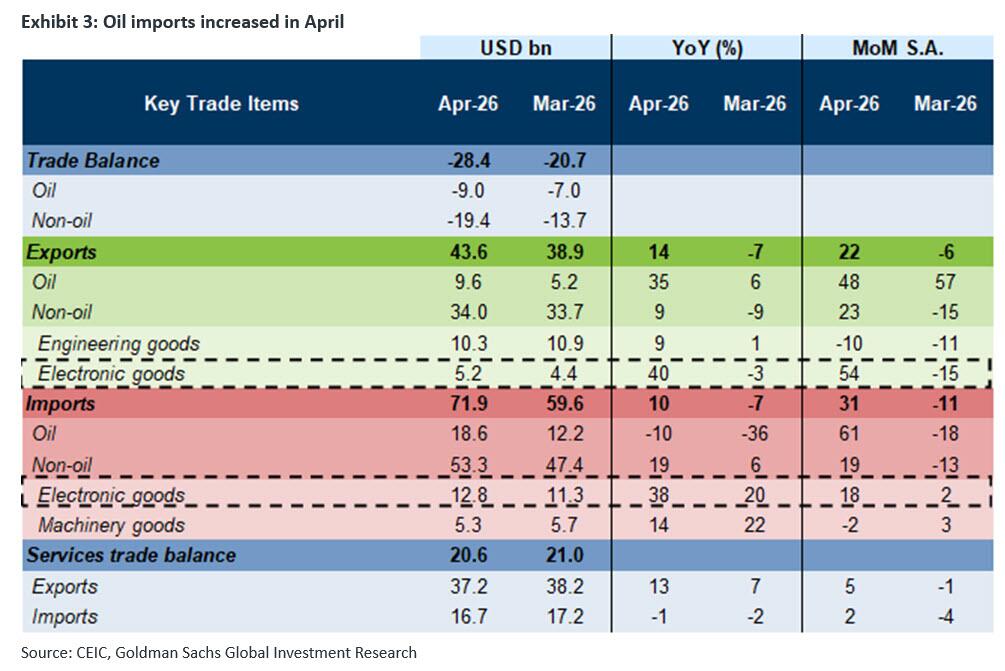

The trade deficit jumped by $8bn from $20.6bn in March to $28.38bn last month, higher than the $26 billion estimate, on a broad-based increase in imports. At the same time, total exports grew by 13.8% in April from a year earlier to hit $43.56 billion.

Oil imports sequentially rose by around 60% MoM likely driven by higher volumes in April (vs. March lows) and higher oil prices.

The value of imports soared as international oil and gas prices jumped amid the Middle East conflict that forced India and every other major crude oil importer to source more expensive supply from producers not dependent on the Strait of Hormuz, which remains closed to most tanker traffic two and a half months after the Iran war began. Meanwhile, petroleum product exports rose by around 48% mom s.a. likely driven by higher exports to Singapore. Gold imports rose sequentially likely driven by higher volume imports of semi-processed gold for refining and higher prices. However, gold imports (in volume terms) may likely decline in May following the government’s import duty hike to 15% from 6%.

Overall non-oil exports remained strong, led by stronger electronics exports. Exports to Saudi Arabia and the UAE recovered in April from its March lows, but remained well below the last year’s levels, while exports to the US increased both sequentially and in year-over-year (yoy) terms. Services trade surplus remained strong at around $21bn, supported by robust services exports.

The widening trade deficit and the soaring energy import bill are pressuring the government’s current account and finances, as the oil supply crisis is already seeping through India’s economy. In the past week, India imposed draconian tariffs on gold imports to defend the currency which has plunged to a record low against the dollar.

Since the war began and cut off over 40% of India’s crude oil flows, those that passed through the Strait of Hormuz, one of the highest-flying economies in Asia has seen its oil import bill soar, investors fleeing the capital market, and the local currency plunging to an all-time low against the U.S. dollar.

Analysts have started to raise inflation estimates and reduce forecasts of this year’s economic growth in India, which is beginning to feel the oil supply shock well beyond the actual disruption of deliveries of oil, LNG, and liquefied petroleum gas (LPG), the primary cooking fuel in the world’s most populous country.

The oil shock that the war has created will weigh on India’s economic growth in the current fiscal year to March 2027. BMI, part of Fitch, expects India’s GDP growth to slow to 6.7% in the 2026/2027 fiscal year, down from 7.7% in 2025/2026, largely due to the oil price shock.

Tyler Durden

Fri, 05/15/2026 – 17:20

https://www.zerohedge.com/markets/indias-trade-deficit-surges-energy-import-prices-soar

Everyone In The Democratic Party Has Money – Except The Democratic Party

Everyone In The Democratic Party Has Money – Except The Democratic Party

Authored by Chase Smith via The Epoch Times (emphasis ours),

On April 30, Maine’s Democratic Gov. Janet Mills dropped out of the race for a U.S. Senate seat.

In a statement about suspending her campaign, Mills was blunt:

“While I have the drive and passion, commitment and experience, and above all else—the fight—to continue on, I very simply do not have the one thing that political campaigns unfortunately require today: the financial resources.”

As Mills said, financial resources matter in today’s political environment as campaigns grow more expensive each cycle.

First-quarter financial reports filed in April with the Federal Election Commission (FEC) show where some of that money is going—and where it is not.

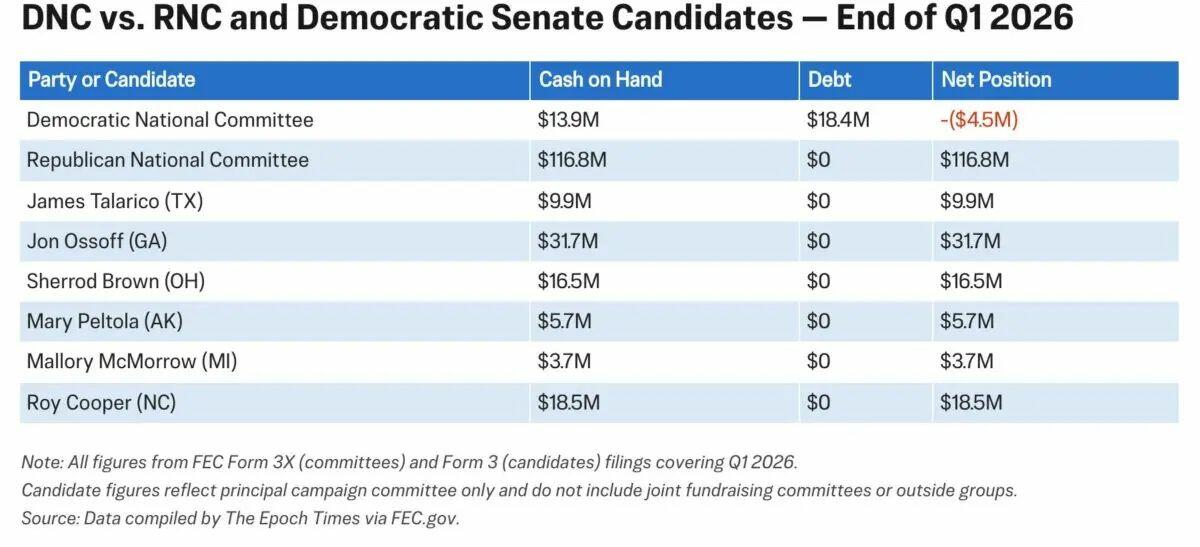

Democratic candidates across the country are raising large sums of money. Democratic Senate candidates, including Georgia Sen. Jon Ossoff, former North Carolina Gov. Roy Cooper, and former Ohio Sen. Sherrod Brown, are sitting on tens of millions of dollars with zero debt.

The party’s congressional campaign arms—the Democratic Senatorial Campaign Committee (DSCC) and the Democratic Congressional Campaign Committee (DCCC)—which work to elect Democrats to each chamber of Congress, carry zero debt and have tens of millions in cash.

On the Republican side, every major committee has a strong cash position.

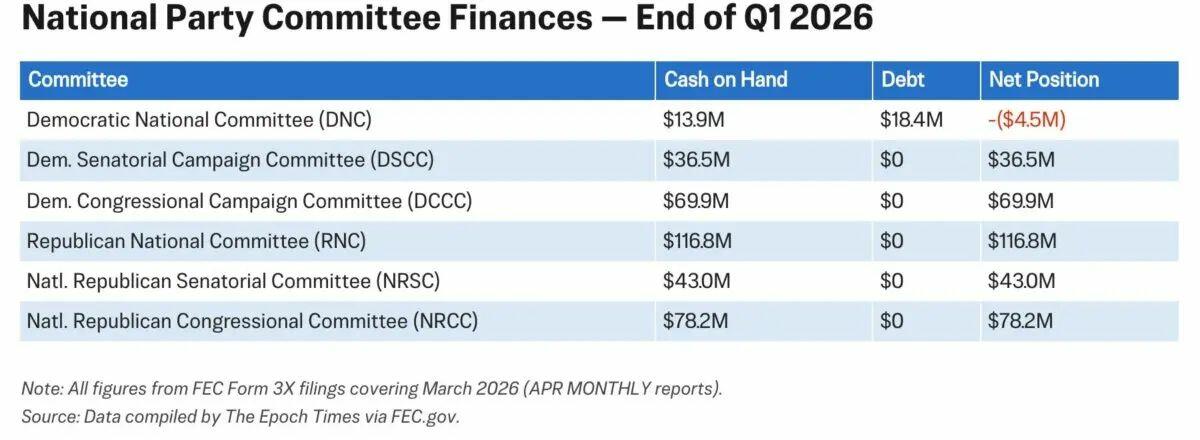

Meanwhile, the Democratic National Committee (DNC) is in debt.

The Numbers

The federal filings lay out the numbers. The DNC reported $13.9 million in cash on hand at the end of March and $18.4 million in debt, putting the committee roughly $4.5 million underwater. It is the only national party committee on either side of the aisle carrying any debt at all.

The Republican National Committee, by contrast, holds $116.8 million in cash with zero debt. The National Republican Senatorial Committee (NRSC) has $43 million, and the National Republican Congressional Committee (NRCC) has $78.2 million. Neither carries debt.

On the Democratic side, the DSCC holds $36.5 million with zero debt. The DCCC holds $69.9 million with zero debt. Both are competitive with or ahead of their Republican counterparts.

The gap widens further when individual candidates enter the picture. Six Democratic Senate candidates—Ossoff, Cooper, Brown, Texas state Rep. James Talarico, former Alaska Rep. Mary Peltola, and Michigan Sen. Mallory McMorrow—hold a combined roughly $86 million in cash on hand. Every one of them carries zero debt.

Ossoff alone has $31.7 million—more than double the DNC’s cash position and more than enough to cover the national committee’s entire debt.

‘A Severe Brand Problem’

Avis Jones-DeWeever, a political scientist and principal of progressive strategic communications firm Nouveaux Strategies, said the pattern points to something deeper than a typical post-election slump.

“The Democratic Party as a national entity has a severe brand problem,” Jones-DeWeever told The Epoch Times in an email. “Even in the midst of a historically unpopular president, they have managed to find a way to consistently garner lower favorability ratings than Donald Trump.

“There is still a sense that the Democratic Party writ large is not rising to this existential moment—that they continue to color within the lines of politics as normal, when we are far away from normal.”

The result, she said, is that donors are making a deliberate choice.

“Donors, it seems, have shifted their funds from supporting an institution they no longer trust to instead investing in individual candidates that have demonstrated strength in this moment,” Jones-DeWeever said.

“It’s not that Democratic donors are tired of giving. It’s just that they are being much more selective and targeted in their spend. They’re willing to fund a fight and are making investments in the specific fighters that they believe have the best chance at carrying them to victory in November.”

The DNC’s Position

DNC Chair Ken Martin has argued the committee’s financial position is the result of a deliberate strategy—not a crisis.

In an April 28 interview on Pod Save America—one of the most listened to Democratic podcasts on all platforms—Martin said the debt traces to a loan the committee took out in 2025 to invest early in organizing, voter registration, and state party infrastructure.

“We do have debt, Jon, and that’s because I took out a loan last year to make sure we can make deep investments,” Martin told host Jon Favreau, a former speechwriter for President Barack Obama and one of the most prominent modern voices in Democratic politics.

The DNC has pointed to those investments in its own public communications. In April 2025, the committee announced what it called the largest monthly investment into state parties in its history: a state partnership program splitting more than $1 million per month between Democratic state and territory parties.

Under the program, each state party receives a baseline of $17,500 per month, with parties in Republican-controlled states receiving an additional $5,000 per month through a “Red State Fund.”

The committee has also launched voter registration programs, a national training initiative for campaign staff, and what it describes as year-round organizing in all 50 states—efforts Martin has summarized with the phrase “organize everywhere, win anywhere.”

Martin pointed to the committee’s track record, saying the DNC raised $105 million in 2025—a record for a first-year chair—with $85 million of that coming from grassroots donors at an average contribution of $51. He said the DNC raised $32 million in the first quarter of 2026 and has more cash on hand than one of his predecessors, former DNC Chair Tom Perez, had at the same point after the party’s 2016 presidential loss.

He described the committee’s debt as manageable and strategically useful, arguing it allowed the party to spend early rather than wait until the final months before an election.

“We can pay that debt off whenever the hell we want,” Martin said. “I could hold that debt until the end of the year. So the reality is, there’s nothing that’s holding me back in terms of the cash I have, the cash on hand I have to spend it on elections.”

Martin pointed out that the committee funds infrastructure that every Democratic campaign depends on, including a voter file that costs more than $10 million a year to maintain.

“Our voter file and our organizing tools and our data, every candidate, whether they’re running for school board or president, relies on that,” he said. “Without the DNC, they would have to do that on their own.”

He also confirmed the DNC purchased the Harris campaign’s fundraising list for $6.5 million after the 2024 election, calling it “a great investment” that has “already paid for itself.”

The DNC did not respond to multiple requests for comment for this report.

‘An Issue Unique to the DNC’

Favreau pressed Martin directly on the contrast between the party’s national committees.

“You’re spending more than you have,” Favreau said. “I know it’s a tough environment for the party out of power, but the DSCC and the DCCC and the Senate candidates have plenty of money. They’re all doing great. So it seems like this is an issue unique to the DNC.”

Favreau pointed to the unreleased 2024 post-election review as a factor in donor reluctance. The review is commonly referred to as the “autopsy” of Kamala Harris’s loss, which Martin said would be made public when he ran for chair but has since said he would not release to instead focus on future races.

Favreau added: “I know the grassroots fundraising has been great. I know that. I concede that for sure. … I’ve talked to plenty of people about this, that a lot of the big donors still have not come off the sidelines, and part of the reason is that there’s a trust issue based partly on the autopsy.”

Martin disagreed. “I’m just not seeing that, Jon,” he said.

Why It Matters

For voters unfamiliar with the mechanics of campaign finance, the distinction between a national party committee and an individual campaign may not be obvious. But the two serve different functions.

National party committees serve a different function than campaigns, at least as the law allows for today. While a Senate candidate raises money to win a single race, as Martin said in the podcast interview, the DNC is responsible for infrastructure that connects all Democratic campaigns together—the voter file that every candidate “from school board to president” relies on, voter registration drives, state party support, legal challenges, and the national get-out-the-vote operation.

Parties are currently restricted to spending only a small fraction of funds in direct coordination with campaigns.

Boris Heersink, an associate professor of political science at Fordham University who has studied national party committees extensively, has argued in his research that these organizations create “national party brands” that are “fundamental to mobilizing voters in elections”—especially “when the party is in the national minority.”

Whether individual candidates can compensate—or even need to—for a national committee carrying more debt than cash is an open question heading into November.

A Pending Supreme Court Case

A pending Supreme Court ruling could change what national party committees are allowed to do with their money.

The court is expected to decide NRSC v. FEC by the end of June, and the case could strike down federal limits on how much national party committees can spend in direct coordination with their candidates.

Under current law, party committees can spend unlimited amounts independently—running ads and organizing without consulting the candidate. But the moment a committee wants to coordinate directly with a campaign—sharing strategy, co-creating ads, directing resources where the campaign wants them—federal law caps that spending.

For Senate races, those caps range from roughly $130,000 to $4 million depending on the state’s voting age population, according to the FEC’s latest coordinated party expenditure limits. For House races, the limits range from about $61,800 to $123,000. While it is a large sum of money, compared to the tens of millions it costs to run campaigns in 2026, it’s only a drop in the larger financial bucket.

The NRSC and NRCC—the Senate and House campaign arms of the Republican Party—are the plaintiffs in the case, arguing the limits violate the First Amendment. The Trump administration’s Department of Justice has declined to defend the law, agreeing the limits should be struck down. The DNC, DSCC, and DCCC have all intervened in the case to defend the existing restrictions.

Read the rest here…

Tyler Durden

Fri, 05/15/2026 – 17:00

https://www.zerohedge.com/political/everyone-democratic-party-has-money-except-democratic-party

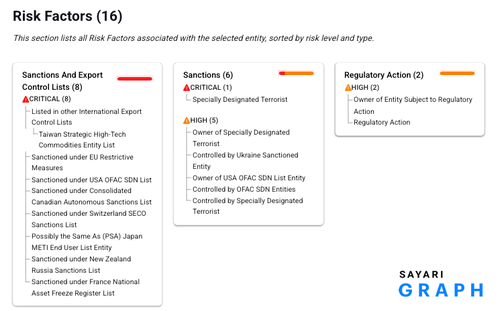

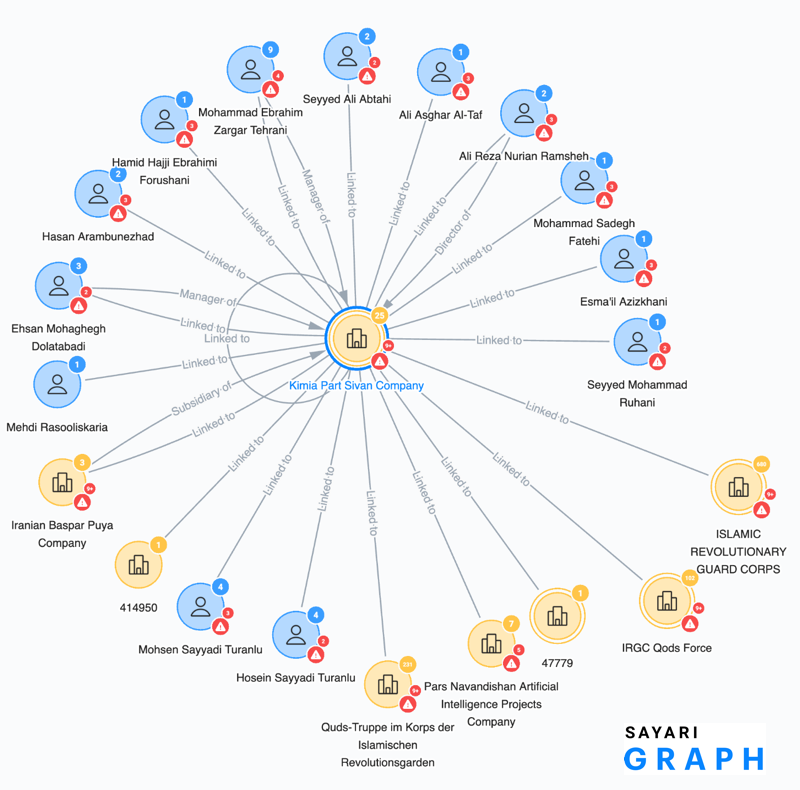

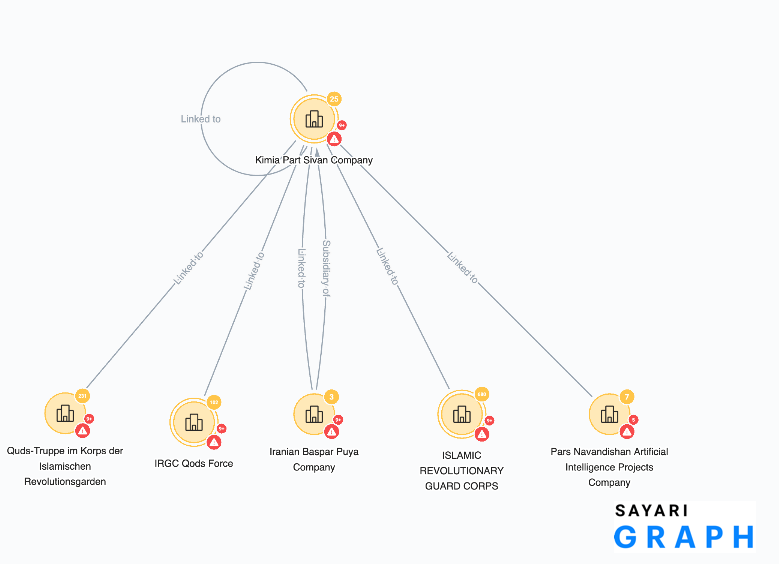

“Send Us A Tip”: U.S. Dangles $15 Million Reward For New Intel On Iran’s Drone Network

“Send Us A Tip”: U.S. Dangles $15 Million Reward For New Intel On Iran’s Drone Network

There is little doubt that Iran’s Shahed drone threat has become a major concern, menacing surrounding Gulf states, commercial tanker traffic in the Strait of Hormuz, and U.S. bases across the region. This backdrop helps explain why the State Department’s Rewards for Justice program has now put up to $15 million for new information in connection with an already sanctioned Iranian drone-production network linked to the IRGC-Qods Force.

Rewards for Justice has named Kimia Part Sivan Company (KIPAS), which the State Department says serves as the drone-production arm of the IRGC-Qods Force. KIPAS has tested drones, supported drone transfers to Iraq, and procured foreign-made components for Iran’s drone program.

“The IRGC has financed numerous terrorist attacks and activities globally, including via its proxies outside Iran, such as Hamas, Hizballah, and Iran-backed militia groups in Iraq. The IRGC funds its international activities – in part – through sales of military equipment, including UAVs. Proceeds from Iran’s sale of weapons and UAVs, including to buyers in Russia, also benefit the Iranian military, including the IRGC-QF,” Rewards for Justice wrote on its website.

Help us put a dent in the IRGC’s revenue stream.

Send us a tip on these bad boys, who manage this drone manufacturer. pic.twitter.com/gwt0jyUqfx

— Rewards for Justice (@RFJ_USA) May 14, 2026

The U.S. Treasury’s OFAC already sanctions KIPAS and appears on the Specially Designated Nationals list. OFAC designated KIPAS on October 29, 2021, for materially assisting the IRGC with its drone program.

According to the State Department, six individuals are involved in the “testing, development, and supply of drones” linked to the IRGC.

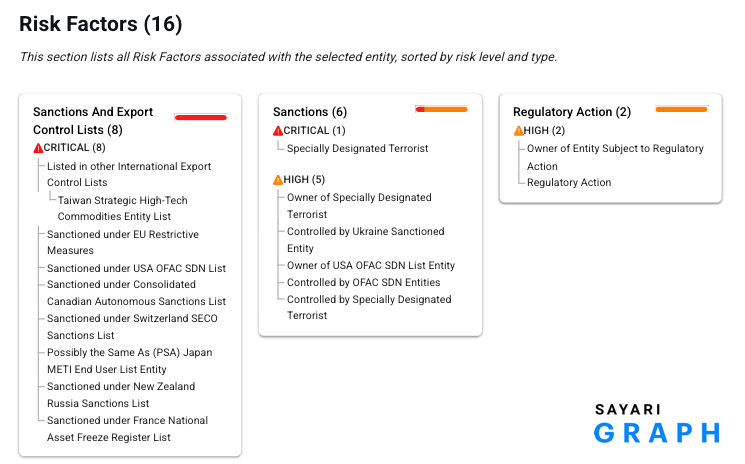

Commercial risk-intelligence and investigations platform Sayari has identified all known managers and links associated with KIPAS:

Further refining:

Follow the money and supply chains, and it appears the State Department wants to disrupt Iran’s drone industry.

Tyler Durden

Fri, 05/15/2026 – 16:40

https://www.zerohedge.com/military/send-us-dangles-15-million-reward-new-intel-irans-drone-network

Re-Arranging The Global Game-Board ‘Bigly’…

Re-Arranging The Global Game-Board ‘Bigly’…

Authored by James Howard Kunstler,

Resource Scramble

“Trump has done so much damage to libtardery that the Democrats will need a decade of uninterrupted power to undo it, which they’re not going to get.”

– Matt Forney on X

If you learned anything from this week’s extravaganza in Beijing, it is that Donald Trump is aggressively re-aligning world relations so that the USA does not end up one of the losers in the global resource scramble that lurks darkly behind all current events.

China does not intend to be an eventual loser, either, though it has lost a lot of traction lately.

The Eurolands are certainly the main losers, embracing loserdom as the old and sick long for death.

India and some of the BRICs countries, are looking a little loser-ish just now.

The primary resource all nations scramble for is oil. Without lavish supplies of oil, you can’t have an advanced techno-industrial economy and, as the feckless Eurolanders learned the hard way, there really isn’t an adequate substitute for oil. The flow of oil depends on economically producible reserves of oil country-by-country, but also on geographic advantage, as we are learning just now in the Hormuz crisis.

“Europe’s crude oil production started its permanent decline in 2001. Asia-Pacific’s production hit a maximum in 2010, and it has been declining since. Africa’s peak oil production took place in 2008, and it has been mostly declining since.”

– Gail Tverberg, OurFiniteWorld.com

Also, turns out, the peak oil story is still real, despite fifteen years of shale oil miracles.

The Persian Gulf states, including Saudi Arabia are probably past peak. American shale oil is in the peaking zone, too — the Permian Basin in Texas is running short of sweet spots. The Arctic National Wildlife Reserve (AMWR) is open for leasing, but it is expensive to drill and produce in the harsh arctic region and the US Geological Survey estimates recoverable reserves there between 7.7 – 10 billion barrels — America consumes roughly 7.5 billion barrels-a-year, so. . . .

There’s Canada, of course, and its tar sands, but the Great White North these days leans rather hostilely towards its neighbor to the south (us). Otherwise, North America is pretty fully explored oil-wise. There can’t be a whole lot of hidden, un-tapped “elephant” fields out there. On the plus side, America enjoys its geographic advantage, comfortably cushioned between the Atlantic and Pacific Oceans, far from the madding crowd of Eurasia.

We have lately trumpeted our supposed acquisition of Venezuela, but projected production of US companies there looking ahead several years would be under a million barrels-a-day while the US uses 20.5-million barrels a day. As for Venezuela’s jungle-bound oil sands, well, for now, fuggeddabowdit.

Russia’s Ministry of Natural Resources puts its commercially recoverable oil resources (with current technology and prices) at around 80-billion barrels, which is a lot, and leaves Russia in a theoretically favorable place for the short term, anyway. China uses about 17-million barrels-a-day and imports about 70-percent of that. Its imports of Iranian oil are substantial but obscured in official statistics due to the evasion of US sanctions. The Hormuz blockade has put a hurt on China.

Here’s how the global resource scramble translates into geopolitical behavior: As has been evident for some time, US interests are increasingly alienated from Euroland’s interests, and better aligned with Russia’s interests. Europe is demonstrably insane these days, roiling with loose talk as it whirls around the drain. Russia, under V. Putin, looks more like the adult in the room. Even Russia’s military operation in Ukraine looks rational if you consider how the EU and the CIA started the damn thing in the first place circa 2014 for the very purpose of provoking Russia.

Mr. Trump has yearned to normalize relations with Russia since he stepped on-stage in 2016, to the great consternation of America’s neocons, CIA shadow-meisters, and the born-again communists running the Democratic Party (who seem to resent Russia ditching Marxism-Leninism thirty-five years ago). This week, the US and China have mutually proposed becoming “partners” rather than rivals on the world scene. We will surely remain mutually wary, but apparently things have changed.

Most urgently, China would like its oil imports from the Persian Gulf restored, and the obvious way to make that happen would be for them to lean on Iran to stop screwing around and come to terms with the US — give up the enriched uranium and stop laying jihad on everybody near and far. We’ll know soon enough if China will do that for us, and we have some goodies promised for them, Nvidia chips, soybeans, and more.

Mr. Trump is rearranging the global game-board bigly, and the net result will be the sorting-out of winners and losers.

Iran is the poster boy for that. It could go either way for them, soon, and rather sharply.

If Iran’s jihad-happy leaders just quit FAFOing, they have the chance to re-enter the global community as an advanced modern economy with a comfortable standard of living.

Or, the US could just blow up what’s left there.

China will probably deliver that message forcefully in the days ahead.

There remains, however, the dirty business of America’s domestic enemies, of whom we learn more and more each week.

This week, it was the testimony of “whistleblower” CIA agent James Erdman that the CIA worked sedulously to conceal the true origins of Covid-19. It looks pretty much like what half of America has suspected all along: that Covid was a trip laid on the nation by its own Deep State (mainly the CIA), in concert with the rogue Democratic Party, for the express purpose of queering the 2020 election.

Related seditious operations apparently continue to this very hour. Former CIA Director John Brennan told MSNBC’s Nicolle Wallace this week: “There’s still a legion of professionals in the law enforcement environment, the Department of Justice, as well as the CIA and other places — the ones who are refusing to follow politically motivated prosecutions, those who are refusing to support any type of political activities on the part of the Trump administration. . . .” Did he just admit that the conspiracy he kicked off in 2016 is still ongoing? And that he is an active party to it? I think so. Do you think Joe DiGenova noticed that down in the DOJ’s Southern District of Florida?

Just as astoundingly, this week former FBI Director James Comey told CNN’s Kasie Hunt that he “still speaks regularly” to current FBI employees. Say, what. . . ? He palavers with the very agency that is investigating him for serious felonies, such as threatening the life of the US president? Sounds a little out-of-order, ya think? Does he long to spend the rest of his life as captain of the ping-pong team at the Lewisburg Federal Penitentiary?

Views expressed in this article are opinions of the author and do not necessarily reflect the views of ZeroHedge.

Tyler Durden

Fri, 05/15/2026 – 16:20

https://www.zerohedge.com/geopolitical/re-arranging-global-game-board-bigly

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}