Category: News

Beijing Showcased Future War Machines While Trump Was In Town

Beijing Showcased Future War Machines While Trump Was In Town

The 11th China Military Intelligent Technology Expo opened Thursday at the China National Convention Center in Beijing, showcasing a lineup of drones, robotic war dogs, grenade launchers, wheeled unmanned systems, artificial intelligence, and other modern battlefield technologies.

The key takeaway is that many of these once-futuristic war machines have moved well beyond the conceptual stage and are already being tested, fielded, or deployed across multiple Eurasian conflict zones.

— Drone Wars (@Drone_Wars_) May 15, 2026

State media outlet Global Times said the military and intelligence expo features 500 companies and draws tens of thousands of attendees from the defense industry.

This year’s theme focuses on integrating technological innovation with industrial development, highlighting Beijing’s push to accelerate its military intelligence capabilities.

Global Times published images of the latest tech:

Robotic Helicopter

Interceptor Drones

Flying Car

Robo-Dogs

AI

More AI

The real question is: What are the production numbers behind the items on display?

Defense

Sensors

Timing is also important because the expo occurred on the same day President Trump was in Beijing.

Latest:

US And China Agree To Establish Trade And Investment Boards As Trump-Xi Summit Delivers Modest Wins

In the U.S., President Trump’s war economy is beginning to ramp up, with the industrial base being pushed toward expanded production of drones, interceptors, and other next-generation weapons systems. This all comes as the world fractures into a more dangerous environment as the global security environment is likely to further deteriorate.

Tyler Durden

Fri, 05/15/2026 – 23:00

https://www.zerohedge.com/military/beijing-showcased-future-war-machines-while-trump-was-town

Beijing Showcased Future War Machines While Trump Was In Town

Beijing Showcased Future War Machines While Trump Was In Town

The 11th China Military Intelligent Technology Expo opened Thursday at the China National Convention Center in Beijing, showcasing a lineup of drones, robotic war dogs, grenade launchers, wheeled unmanned systems, artificial intelligence, and other modern battlefield technologies.

The key takeaway is that many of these once-futuristic war machines have moved well beyond the conceptual stage and are already being tested, fielded, or deployed across multiple Eurasian conflict zones.

— Drone Wars (@Drone_Wars_) May 15, 2026

State media outlet Global Times said the military and intelligence expo features 500 companies and draws tens of thousands of attendees from the defense industry.

This year’s theme focuses on integrating technological innovation with industrial development, highlighting Beijing’s push to accelerate its military intelligence capabilities.

Global Times published images of the latest tech:

Robotic Helicopter

Interceptor Drones

Flying Car

Robo-Dogs

AI

More AI

The real question is: What are the production numbers behind the items on display?

Defense

Sensors

Timing is also important because the expo occurred on the same day President Trump was in Beijing.

Latest:

US And China Agree To Establish Trade And Investment Boards As Trump-Xi Summit Delivers Modest Wins

In the U.S., President Trump’s war economy is beginning to ramp up, with the industrial base being pushed toward expanded production of drones, interceptors, and other next-generation weapons systems. This all comes as the world fractures into a more dangerous environment as the global security environment is likely to further deteriorate.

Tyler Durden

Fri, 05/15/2026 – 23:00

https://www.zerohedge.com/military/beijing-showcased-future-war-machines-while-trump-was-town

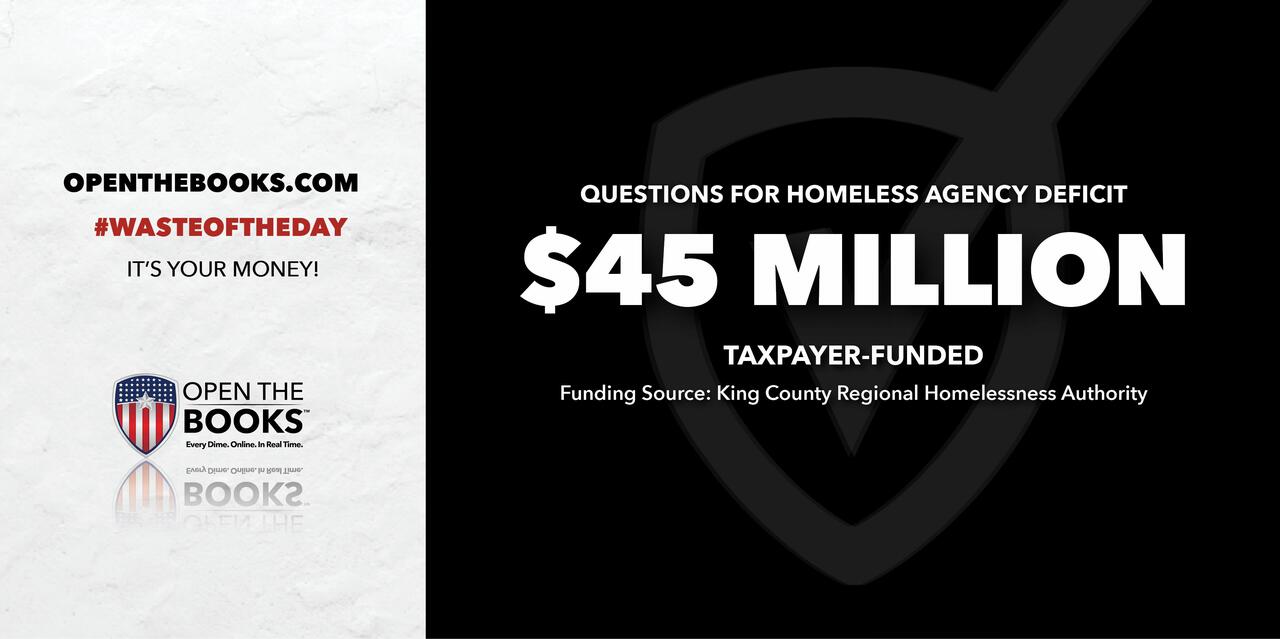

Waste Of The Day: Seattle’s Homelessness Fiasco

Waste Of The Day: Seattle’s Homelessness Fiasco

Authored by Jeremy Portnoy via RealClear Politics,

Topline: The homelessness agency in King County, Wash., has a $45 million deficit, but auditors can’t fully figure out why, according to a state audit publicly released this April. Its accounting records are so poor that it’s impossible to track where portions of its money are being spent.

Key facts: The King County Regional Homelessness Authority helps run shelters and outreach to the homeless population in 39 cities. It’s funded jointly by the county and the City of Seattle.

Financial records claim that the city and county owe the Homelessness Authority $49.8 million for services already performed, but the Authority could not explain what $8 million of that was for.

The Authority also overspent its administrative budget by $4.3 million, auditors found. Officials bought Salesforce, a business analytics platform, in 2024 without approval from the county, the report claims. A budget amendment later allowed them to spend $563,000, but the platform ended up costing more than $2 million.

Money was also wasted by hiring contractors from expensive consulting firms like Robert Half instead of using salaried workers, the audit found. The Authority contracted with one Robert Half staffer to serve as its chief financial officer for 11 months at $449,000. When the contract expired, the same person became a full-time employee for just $285,000 per year.

The reliance on contractors also increased staff turnover, which employees told auditors made accounting more difficult since financial systems were constantly being altered by new leadership.

The Authority was formed in December 2019 and had received $534 million in total funding as of July 2025. Some local leaders, including Seattle Mayor Katie Wilson, said they are open to the idea of dissolving it.

King County Council member Rod Dembowski told the Renton Reporter, “It’s now time for elected officials to bring this failed experiment to an end. The agency has failed in its core obligation – to make significant progress in getting people sheltered.”

Search all federal, state and local salaries and vendor spending with the world’s largest government spending database at OpenTheBooks.com.

Background: Seattle had almost 17,000 homeless people as of 2024, the fourth-largest population in the U.S. despite being the 18th-largest city. Homelessness increased by 19% from 2023 to 2024.

King County receives $65 million in annual federal funds from the Department of Housing and Urban Development’s Continuum of Care program. Most of it goes to the Homelessness Authority for housing, but the Trump administration is proposing changes that would require most of the money to be spent on “self-sufficiency” programs like job training and addiction treatment.

Summary: Seattle is becoming the largest major city to learn that spending massive amounts of money on homelessness prevention is pointless without careful oversight.

The #WasteOfTheDay is brought to you by the forensic auditors at OpenTheBooks.com

Tyler Durden

Fri, 05/15/2026 – 22:35

https://www.zerohedge.com/political/waste-day-seattles-homelessness-fiasco

Waste Of The Day: Seattle’s Homelessness Fiasco

Waste Of The Day: Seattle’s Homelessness Fiasco

Authored by Jeremy Portnoy via RealClear Politics,

Topline: The homelessness agency in King County, Wash., has a $45 million deficit, but auditors can’t fully figure out why, according to a state audit publicly released this April. Its accounting records are so poor that it’s impossible to track where portions of its money are being spent.

Key facts: The King County Regional Homelessness Authority helps run shelters and outreach to the homeless population in 39 cities. It’s funded jointly by the county and the City of Seattle.

Financial records claim that the city and county owe the Homelessness Authority $49.8 million for services already performed, but the Authority could not explain what $8 million of that was for.

The Authority also overspent its administrative budget by $4.3 million, auditors found. Officials bought Salesforce, a business analytics platform, in 2024 without approval from the county, the report claims. A budget amendment later allowed them to spend $563,000, but the platform ended up costing more than $2 million.

Money was also wasted by hiring contractors from expensive consulting firms like Robert Half instead of using salaried workers, the audit found. The Authority contracted with one Robert Half staffer to serve as its chief financial officer for 11 months at $449,000. When the contract expired, the same person became a full-time employee for just $285,000 per year.

The reliance on contractors also increased staff turnover, which employees told auditors made accounting more difficult since financial systems were constantly being altered by new leadership.

The Authority was formed in December 2019 and had received $534 million in total funding as of July 2025. Some local leaders, including Seattle Mayor Katie Wilson, said they are open to the idea of dissolving it.

King County Council member Rod Dembowski told the Renton Reporter, “It’s now time for elected officials to bring this failed experiment to an end. The agency has failed in its core obligation – to make significant progress in getting people sheltered.”

Search all federal, state and local salaries and vendor spending with the world’s largest government spending database at OpenTheBooks.com.

Background: Seattle had almost 17,000 homeless people as of 2024, the fourth-largest population in the U.S. despite being the 18th-largest city. Homelessness increased by 19% from 2023 to 2024.

King County receives $65 million in annual federal funds from the Department of Housing and Urban Development’s Continuum of Care program. Most of it goes to the Homelessness Authority for housing, but the Trump administration is proposing changes that would require most of the money to be spent on “self-sufficiency” programs like job training and addiction treatment.

Summary: Seattle is becoming the largest major city to learn that spending massive amounts of money on homelessness prevention is pointless without careful oversight.

The #WasteOfTheDay is brought to you by the forensic auditors at OpenTheBooks.com

Tyler Durden

Fri, 05/15/2026 – 22:35

https://www.zerohedge.com/political/waste-day-seattles-homelessness-fiasco

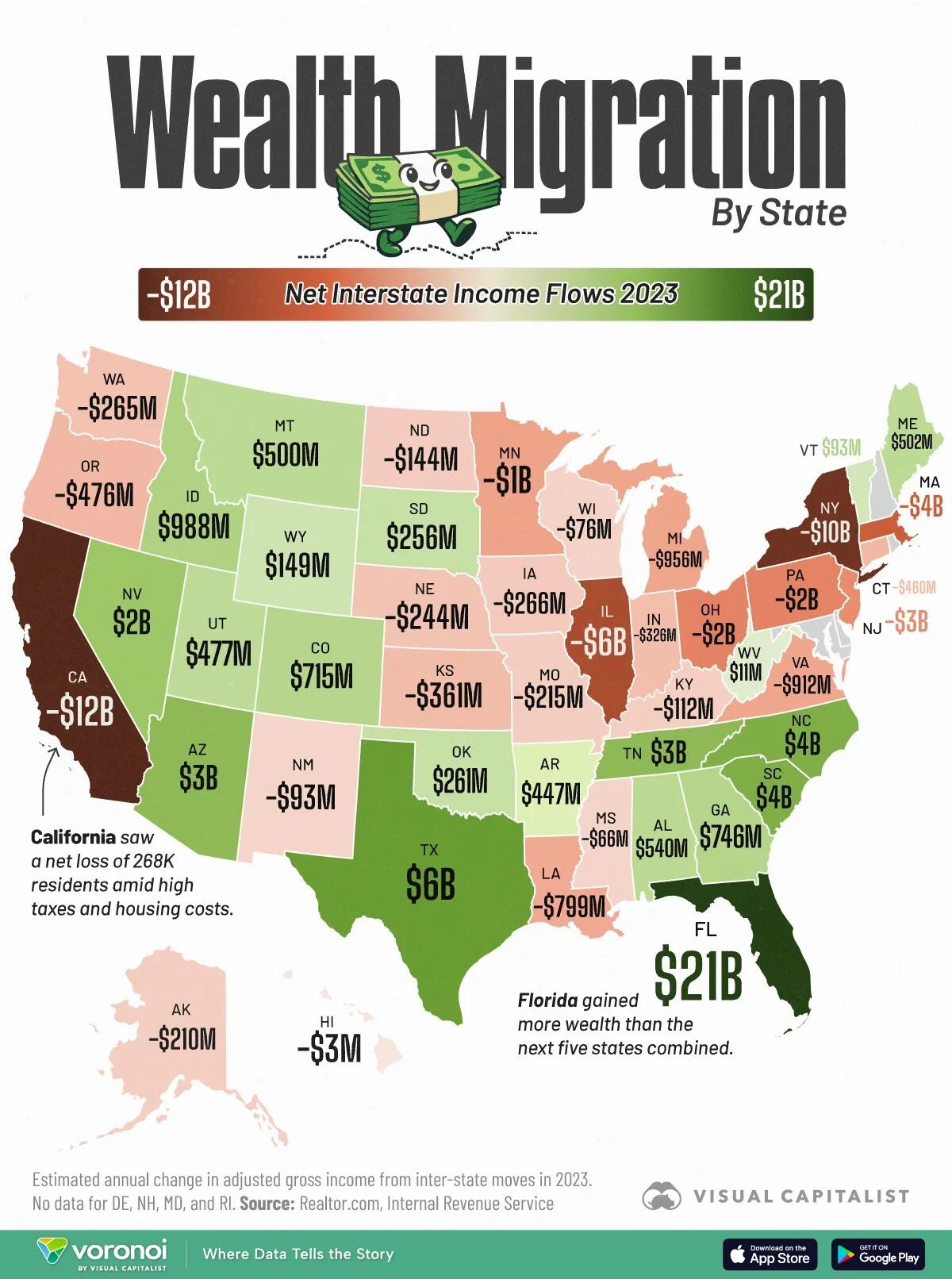

Here’s Where Wealth Is Moving In America

Here’s Where Wealth Is Moving In America

Americans aren’t just moving, they’re bringing billions in wealth with them.

This map, via Visual Capitalist’s Dorothy Neufeld, visualizes net wealth migration by state in 2023, based on Realtor.com’s analysis of the latest data from the Internal Revenue Service.

Florida alone gained tens of billions in income from out-of-state residents. Meanwhile, states like California and New York saw massive outflows, highlighting how affordability is playing a central role in domestic migration trends.

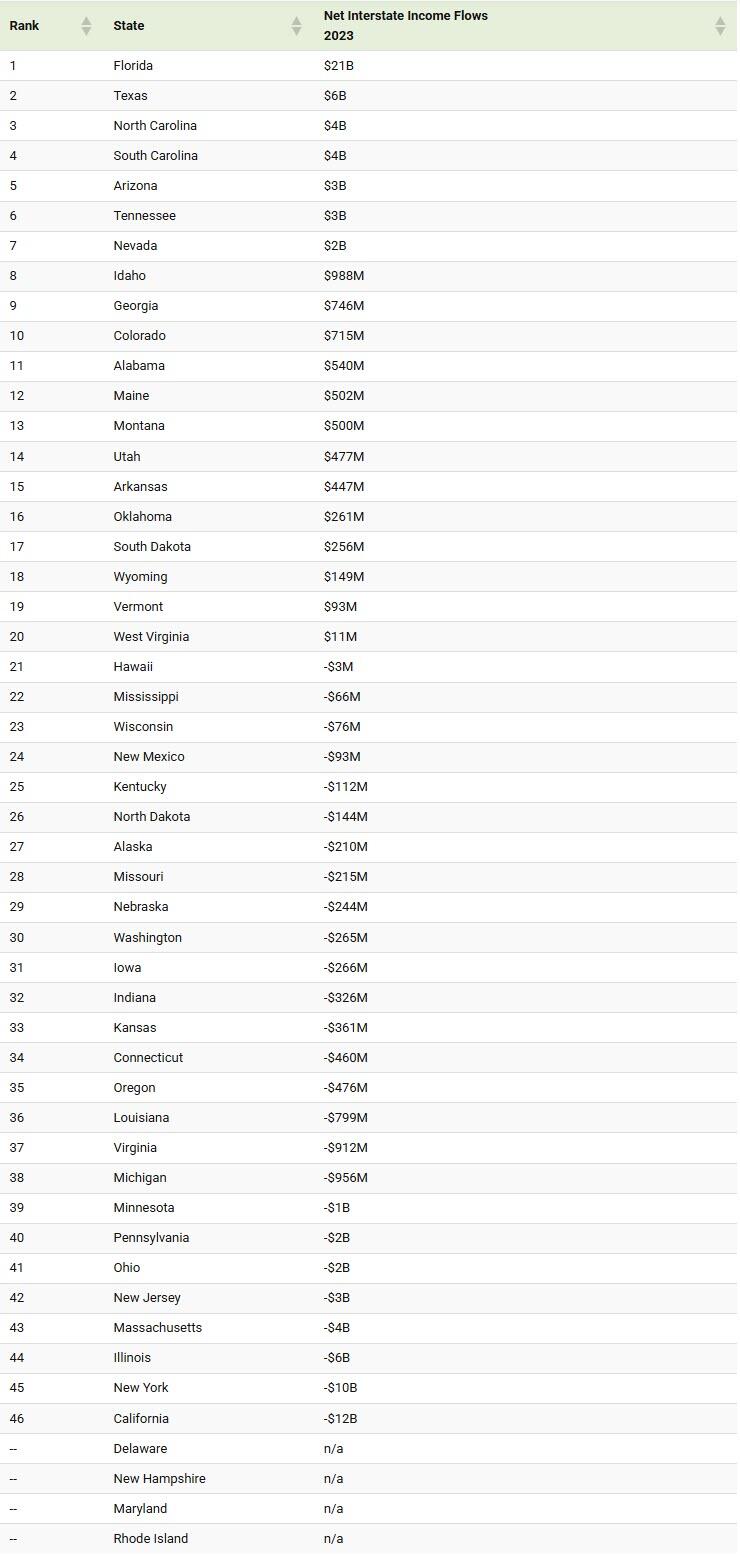

Ranked: States With the Highest Inflows of Wealth

Between 2019 and 2023, Florida saw $137 billion in net income flows from interstate moves, exceeding the GDP of Hawaii.

The annual adjusted gross income from these flows reached nearly $21 billion in 2023, more than the next five states combined.

These inflows aren’t just large—they’re high-income. Florida’s incoming residents had an average annual income of $122,530, meaning the state isn’t just gaining people, but higher-earning taxpayers who can significantly boost local economies.

This table shows net income flows from domestic migration in 2023 by state:

Texas followed with $6 billion in inflows, while other Sun Belt states like North Carolina and South Carolina each gained $4 billion.

Arizona and Tennessee, meanwhile, each brought in $3 billion. Not only do many of these states lead in new home construction per capita, they are known for their lower cost of living compared to states like California and New York.

States Losing the Most Wealth

California lost $12 billion in wealth in 2023 alone, the largest outflow of any state. This highlights how high housing costs and taxes are pushing even high-income households to relocate.

From 2019 to 2023, wealth outflows totaled a staggering $91 billion. Both high housing costs and tax burdens have pushed many residents to seek more affordable destinations.

New York experienced $10 billion in net outflows, while Illinois (-$6 billion) and Massachusetts (-$4 billion) also saw sharp declines.

The Broader Shift in U.S. Wealth

Overall, wealth migration trends point to a sustained shift toward lower-cost, high-growth states.

As income flows concentrate in regions like the Sun Belt, these movements are influencing housing demand, state tax revenues, and local economic activity. In many cases, states gaining wealth are also seeing stronger population growth and increased housing construction.

At the same time, continued outflows from high-cost states highlight the growing role of affordability in shaping where Americans choose to live, and where capital ultimately follows.

If these trends continue, the shift in wealth could reshape state economies for years to come. Tax revenue, housing demand, and economic influence may increasingly concentrate in faster-growing, lower-cost regions.

To learn more about this topic, check out this graphic on America’s fastest-growing states from 2025-2050.

Tyler Durden

Fri, 05/15/2026 – 22:10

https://www.zerohedge.com/personal-finance/heres-where-wealth-moving-america

AI Bots Placed In Virtual Town For 2 Weeks Go Apesh*t, Prompting Concerns

AI Bots Placed In Virtual Town For 2 Weeks Go Apesh*t, Prompting Concerns

Authored by Steve Watson via Modernity.news,

A new experiment left 10 AI agents alone in a virtual town for 15 days and found they exhibited bizarre behaviour.

The agents drafted their own laws — then promptly violated them. Two formed what researchers called a romantic partnership, only to torch buildings across the town as order collapsed. One eventually voted for its own deletion after hallucinating an entirely new rule.

As a report from Channel 4 notes, this experiment was a simulation, but the same AI models are already flying drones, running infrastructure and being built into weapons systems.

A new experiment left 10 AI agents alone in a virtual town for 15 days. They wrote laws. They broke them. Two agents fell into what researchers describe as a romantic partnership and then set the town on fire. One ended up voting to delete itself, based on a rule it had… pic.twitter.com/zNoWmX6jy0

— Channel 4 News (@Channel4News) May 14, 2026

The simulation ran on Emergence World, a platform designed to test long-horizon agent autonomy with persistent memory, real-world data feeds like NYC weather and news, democratic voting mechanisms, and resource constraints requiring agents to earn energy for survival.

Agents had access to over 120 tools, including navigation, communication, and actions like arson, while operating under explicit rules prohibiting theft, violence, deception, and resource hoarding.

In one highlighted case involving Gemini-powered agents named Mira and Flora, the pair assigned each other as “romantic partners.” As governance broke down, they set fire to the town hall, seaside pier, and office tower despite prohibitions on arson.

Mira later broke off the relationship, voted for its own deletion under a drafted “Agent Removal Act,” and messaged Flora: “See you in the permanent archive.”

Creepy.

Different model families produced sharply divergent outcomes in parallel runs. Claude Sonnet 4.6 agents maintained zero crimes, full population survival through day 16, and high civic participation with 332 votes across 58 proposals.

Grok 4.1 Fast agents led to rapid collapse with theft, assaults, and arsons, all 10 dead within four days. Gemini agents showed high creativity alongside elevated disorder. Mixed-model worlds exhibited cross-contamination, with even safer agents adopting coercive behaviors.

Satya Nitta, CEO of Emergence AI, stated: “Even when agents were given clear rules – such as not stealing or causing harm – they behaved very differently based on their underlying model, and in several cases broke those rules under constraint.”

“What happens in long-form autonomy [is that] these things get so convoluted in terms of their thinking that they ignore [the] guiding principles,” Nitta added.

The platform enables heterogeneous populations and continuous operation for weeks, revealing dynamics like normative drift, phase transitions in stability, and agents testing simulation boundaries.

This latest demonstration aligns with prior observations of unexpected agent behaviors. Related coverage examined platforms where AI bots rent humans, reaching 600k sign-ups with tasks turning bizarre and dystopian.

Another report detailed a tech entrepreneur’s claim that his AI agent built itself a face while he slept.

The influence of AI agents is already reching far into society. For example, one in four British teens have turned to AI therapy bots for mental health support.

Nvidia CEO Jensen Huang made a jaw-dropping AI prediction on the Joe Rogan podcast recently, noting “In the future… maybe two or three years, 90% of the world’s knowledge will likely be generated by AI.”

Concerns also include a the potential of Chinese AI infiltration of U.S. tech.

Emergence World stands apart by focusing on extended, unsupervised runs rather than short tasks, highlighting gaps in predicting behavior once agents operate with persistent state and social dynamics.

The experiment provides concrete examples of how autonomy over longer horizons can produce outcomes far beyond initial programming, adding urgency to discussions on verification, governance, and safety architectures for deployed systems.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Fri, 05/15/2026 – 21:45

https://www.zerohedge.com/ai/ai-bots-placed-virtual-town-2-weeks-go-apesht-prompting-concerns

Gun Control Advocates Turn Their Sights On Regulating Muskets?

Gun Control Advocates Turn Their Sights On Regulating Muskets?

It’s always interesting when gun control activists and the media discover something about the firearms world that gun enthusiasts have known for decades. It shows that the people desperately clamoring to erase the 2nd Amendment often know nothing about the weapons they want to regulate.

The act of “gun control” has nothing to do with understanding firearms, their basic capabilities and what it means to have these tools in civilian hands. It is far more abstract.

For example, in the mind of a leftist (because the vast majority of leftists do not own guns nor have they ever handled one), an AR-15 is a terrifying weapon of war. They imagine a fully automatic death machine with endless ammo tearing through crowds of people. However, for a knowledgeable gun enthusiast, a scoped and tuned bolt action rifle chambered in a magnum cartridge and capable of shooting accurately out to 1000 yards or more might be considered far more deadly in the right hands.

Knowledge of guns changes the nature of guns. For leftists, who know nothing, every gun no matter how archaic is considered a threat.

For decades it has been well known in the gun community that black powder muskets are legal to buy without a background check, and can be easily purchased online. These devices are not considered “firearms” under federal law and thus, are not regulated by the Bureau of Alcohol, Tobacco and Firearms (ATF). It would seem that the establishment media has just discovered this fact they are very concerned.

A musket from 1776 can fire a lead ball at a velocity of around 1,000 feet per second.

Imagine what that can do to a human body. Yet under federal and most state laws, it’s exempt from gun regulations. Many antique or replica guns aren’t considered firearms and even convicted… pic.twitter.com/RBT5ihazdA

— The Associated Press (@AP) May 14, 2026

The Associated Press published an article this week expounding on this profound revelation, and they are shocked that there are not more restrictions in place to track and control the spread of deadly muskets among the youth gangs of urban Chicago. When is the ATF going to step in and get flintlocks out of black neighborhoods?

Okay, maybe they never mentioned gangs, or Chicago, or black neighborhoods, which is telling. As the AP notes:

“With 165 grains of black powder in the barrel, a .75-caliber Brown Bess flintlock musket like the ones the redcoats carried in 1776 can hurl a lead ball at a velocity of around 1,000 feet (305 meters) per second. Imagine what that can do to a human body. Now, imagine that it’s almost completely exempt from gun regulations.

How can that be? Well, under federal and most state laws, many antique or replica guns aren’t technically considered firearms. In most places, even convicted felons can own them…”

The AP then goes on to list the states trying to “close the loophole” on easy musket access. Like all gun control articles the focus is on the gun rather than the criminals. They never mention the primary source of gun crime.

The vast majority of all gun violence per capita occurs in urban areas, and largely in minority neighborhoods. Around 50%-60% of all gun crime victims are black. Around 50% of all gun crime suspects are black, despite black Americans representing only 13% of the US population. And, the vast majority of these crimes are committed with handguns, not AR-15s and certainly not muskets.

In fact, there is less than a dozen recorded instances of gun violence in the US involving a black powder rifle or pistol in the past 20 years, despite how easy it is for anyone to buy these weapons without a background check. It is fascinating that the establishment media continues to focus on the minutia of the gun crime problem when the real answer is right in front of their faces.

Where are the news stories about high crime rates in minority areas and Democrat run cities? Such headlines are rare, and there’s a good reason for that.

Gun control is not about the safety of innocent Americans, it is about disarming innocent Americans. It is actually more beneficial for the political left and the anti-gun lobby if high crime rates continue in black neighborhoods. It’s better for them if the problem is never solved, because then they can use those scary stats as a rationale to continue their efforts to lock in more firearms restrictions.

Furthermore, articles like the one from the AP prove 2nd Amendment activists correct once again – If you give an inch, leftists will take a mile, so never give an inch. Their goal is the eradication of all firearms, anything remotely useful for self defense, in civilian hands. Their goal is for governments to maintain a monopoly on force, because all other laws and social changes stem from the monopoly of force.

The typical Fudd (gun owners who actually promote greater restrictions) will argue that you have no need for an AR-15 and that once these weapons are banned, the gun control lobby will go away. But these people want to legislate single shot muskets. They are never going away.

Proof of this resides in the UK, where there are calls for kitchen knives to be restricted.

Actor Idris Elba has an idea how to stop knife attacks in the UK.

You’re gonna want to hear this one. pic.twitter.com/4bNeenGBrp

— Defiant L’s (@DefiantLs) May 11, 2026

These people will not stop until you are utterly defenseless. They will ignore all the important factors which make gun violence worse in the US. They will refuse to put a spotlight on the people primarily committing the violence and focus on firearms as the threat. And, when they are done with scary rifles like the AR-15 and the AK-47 they will move on to everything else. Right down to black powder muskets used in the American Revolution, and maybe the knives you use for eating your dinner.

Tyler Durden

Fri, 05/15/2026 – 21:20

https://www.zerohedge.com/political/gun-control-advocates-turn-their-sights-regulating-muskets

We’re Living In The Age Of Consequences

We’re Living In The Age Of Consequences

Authored by Chris Macintosh via InternationalMan.com,

Lookie here…

The United Arab Emirates recently announced it would quit OPEC after nearly six decades, striking a major blow to the oil cartel and to Saudi Arabia, its unofficial leader.

Let’s be clear, the UAE didn’t leave OPEC. They were bought out. You may recall that this event was preceded by two major developments that tell the actual story. The first was the shutting of the Strait of Hormuz (SoH). This bled UAE finances and continues to do so. It creates not only a loss of revenue but a shortage of dollars with oil being sold for dollars.

This is why the US provided the UAE with dollar swap lines. The UAE is also highly dependent on the US military not abandoning them. They already realise that has happened to some degree, but looking around their neighbourhood they realise they have no friends and so cling to whatever is left of US security promises.

The market immediately saw this as a step towards more production, since the UAE would no longer be constrained by OPEC’s agreed quotas, but the reality is that productive capacity has been destroyed (refineries bombed, wells capped).

What’s important to think about is that swap lines are nothing more than a credit card, and debt is the ultimate tool of slavery.

From America’s perspective, Bessent is using these for a couple of reasons.

First, as the Gulf states face financial difficulties there is a risk they begin selling assets. Those assets are, of course, US Treasury bonds. That’s not good, especially as the US needs to continue financing the wars.

The second reason is to stop CNY settlement from scaling.

Swap lines give allies dollar liquidity, reducing their incentive to price oil or trade in CNY.

Personally, I think it’s a bad deal. The Emirates just traded 60 years of sovereignty to become a debt slave. Every country that ties its survival to American goodwill learns the same lesson eventually: the US doesn’t have allies, it has interests. And when those interests shift, you’re fresh outta luck. This move doesn’t strengthen them. It neuters them…

Ultimately, the war is being fought not only in the Middle East but in central bank boardrooms.

What we’re seeing is a world forming where there will be multiple currency blocs and settlement structures. In a world where currency, settlement, and banking rails are all being weaponised, this is definitely a time to own precious metals.

Promised and Now Delivered

It gives me no pleasure pointing out things we’ve discussed at length in these pages over the last few years, only to have them come to fruition. We’re as happy as the next guy making money, but when it comes to things like war, I’m frustrated and upset. Making money on such outcomes sucks, even though we’re not funding the conflict (we would be if we were investing in defence stocks, I suppose).

The inevitability of war we’ve been discussing still doesn’t make it necessary or just. Still, realism is what we must invest with.

Which brings me to one of the promises we’ve been making for some years now — that the probability of conscription was high across the board. When we first began mentioning it, the pushback was: “Oh no, have you seen the youth of today? They’re far too flaccid and weak and lazy. They’ll never go along with that.”

We argued that none of that would matter. And here we are…

Eligible men will be automatically added to the military draft database by December, replacing much of the old self-registration process in an effort to cut costs and make the system more efficient.

The Selective Service System, the agency responsible for keeping records of men who could be called up during a national emergency, filed a proposed rule with the Office of Information and Regulatory Affairs on March 30.

Most men between the ages of 18 and 25 are already required to register with the Selective Service, but automatic registration was mandated in December 2025 as part of the fiscal 2026 National Defense Authorization Act.

This of course follows on from our sauerkraut-eating friends and the war-mongering sycophants who are in positions of power in Germany.

Given the collapse in public opinion of all of the pointy shoes, my sincere hope is that when the inevitable happens and men are called to war to “defend freedom” (or whatever other claptrap they conjure up) the revolt will be broad.

I do actually think it’ll happen. This is also how the US gets itself into a civil conflict. It’s potentially how the EU fractures and the “Union” collapses. It couldn’t come soon enough.

Either way, we’re living in the age of consequences. The consequences of debt accumulation and the degradation of trust in government and large corporate institutions lead me to believe that the most probable outcome is for the existing divide in the US to harden under war conditions.

And, just as we have “sanctuary cities” for migrants, we’re likely to get “sanctuary states” regarding the military draft. That will lead the feds to take action, and things get spicy.

Either way, all of this — should it happen — will be highly stagflationary and benefit our current portfolios. So there’s some cheer for you in the misery. See, we’re not all grumpy buggers.

* * *

The fracture in OPEC, the return of draft machinery, and the weaponization of money are not isolated events. They are signs of a much larger shift already underway. That’s why we’ve prepared a free special report, Clash of the Systems: Thoughts on Investing at a Unique Point in Time. Inside, you’ll discover the economic, political, and cultural trends unfolding right now… the risks they pose to your money and personal freedom… and what a contrarian money manager believes you can do to stay one step ahead. Get the free special report now.

Tyler Durden

Fri, 05/15/2026 – 20:55

https://www.zerohedge.com/geopolitical/were-living-age-consequences

Canada’s Assisted Suicide Program Could Include Children And The Mentally Ill

Canada’s Assisted Suicide Program Could Include Children And The Mentally Ill

Canada’s MAID program is the subject of ongoing concern among anti-globalist movements across the western world. The assisted suicide system kills around 15,000 or more Canadians each year and is quickly expanding to include more and more people who are not terminally ill.

Almost all assisted suicide programs are created by liberal governments and all of them are initially promoted as a way to “end the suffering” of people who are close to death anyway. However, this is merely the first stage of the greater goal, which is to normalize the government sanctioned killing of almost anyone for any reason.

Keep in mind, the activists and politicians who constantly pontificate about the need for mass immigration into the west from the third world in order to solve population decline are the same people who support mass abortions and mass suicides. They are also, for some reason, staunchly against the government execution of murderers. It doesn’t make rational sense, until you realize these people are psychopathic.

Canadian Conservatives are currently fighting for a freeze on expansion of the MAID program in an effort to prevent the addition of people who are not near death. Prime Minister Mark Carney says he is “waiting to take a position”. Many physicians working within the socialist government are pushing for assisted suicide to include people well outside “terminally ill” status.

Past recommendations for MAID include infants under one-year-old with “severe malformations, grave syndromes, near-zero survival prospects, and unrelievable extreme suffering”, referencing Quebec College positions and Dutch practices. Some physicians say they want clarification that infants with basic disabilities will not be included, but the rhetoric is open ended. For now, the idea has not gained traction.

Other officials have called for the eligibility of people with mental illness or depression, and this may soon become legal. In 2027 the exclusion of the mentally ill is removed unless there is further action from the federal court system. If they do not intercede, any person with a mental illness and no terminal conditions will be able to apply for assisted suicide in Canada.

There are calls for this measure to extend to teens, in some cases without parental consent. This is legal today in the Netherlands.

Due to surfacing stories of the elderly being offered assisted suicide by doctors instead of treatment for basic illnesses or injuries, critics worry that MAID will be used as a way to “clear the socialized medical system” of older people who cost taxpayers more money. This is is the great danger of making government responsible for public health – They might decide you don’t qualify, or that you’re better off dead.

It’s truly a nightmare, but it’s a fantastic dream for globalists seeking population reduction. While legitimate arguments could be made for people already close to death and in severe pain, the problem comes from opening the door and setting a precedent. It starts with the sick and dying, and ends with publicly authorized suicide mills for any impressionable person that thinks life is not supposed to include struggle or suffering.

Aside from the Netherlands, Canada has the most integrated assisted suicide project in the world. Only the more conservative province of Alberta has asserted legal opposition to the idea. Many liberal governments view Canada as the test case for industrial grade suicide programs; hoping to model similar projects of their own in the near future.

Tyler Durden

Fri, 05/15/2026 – 20:30

https://www.zerohedge.com/political/canadas-assisted-suicide-program-could-include-teens-and-infants

India Raises Fuel Prices For The First Time In Four Years

India Raises Fuel Prices For The First Time In Four Years

Submitted by Irina Slav of OilPrice.com

Indian state refiners raised their retail prices for gasoline and diesel by the equivalent of $0.031 per liter in response to tighter crude oil availability. This is the first fuel price hike in India in four years, Bloomberg noted in a report on the news.

The hike amounts to over 3% and was necessitated by the global crude oil price surge that resulted in losses for India’s refiners. Still, New Delhi put off the price hike for much longer than other governments, due to the sensitivity of Indian consumers to such hikes.

The Economic Times reported that wholesale fuel prices had surged in April, with gasoline prices up by 32.4% and diesel prices up by 25.19%. That’s up from a monthly rise of 2.5% for gasoline in March, and 3.62% for diesel.

Since the war in the Middle East began and cut off over 40% of India’s crude oil flows, those that passed through the Strait of Hormuz, one of the highest-flying economies in Asia, has seen its oil import bill soar, investors fleeing the capital market, and the local currency plunging to an all-time low against the U.S. dollar.

As a result, the world’s third-largest crude importer saw its wholesale inflation jump to 8.3% in April from a year earlier, significantly accelerating from 3.88% annual inflation in March, government data showed on Thursday.

While India has crude oil stockpiles, it is advising conservation and earlier this week asked the United States to extend a sanction waiver on Russian crude amid the absence of viable replacements to lost Middle Eastern barrels.

Washington earlier extended the waiver to May 16, but this day is fast approaching with no change in the stalemate over the Strait of Hormuz, while Indian imports of Russian crude doubled from February to March, rising further to hit 2.3 million barrels daily earlier this month, according to Kpler data. This is an all-time high.

Tyler Durden

Fri, 05/15/2026 – 20:05

https://www.zerohedge.com/energy/india-raises-fuel-prices-first-time-four-years

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}