Category: News

Watch Live: WarSec Hegseth Epic Fury Presser After Trump’s Apparent ‘Off-Ramp’

Watch Live: WarSec Hegseth Epic Fury Presser After Trump’s Apparent ‘Off-Ramp’

There’s been a lot of speculation that the White House is preparing to find a ‘mission accomplished’ declaration moment, as ‘any offramp will do’ as a way to avoid a costly potential quagmire of introducing ground troops, and we may be seeing the start of one.

After comments apparently leaked to The Wall Street Journal overnight that Trump is willing to leave Iran with the Strait unopened, the President has clarified his thinking in his out loud voice this morning.

President Trump has posted on social media this morning, clearly signaling he is further down the road towards an off-ramp:

All of those countries that can’t get jet fuel because of the Strait of Hormuz, like the United Kingdom, which refused to get involved in the decapitation of Iran, I have a suggestion for you:

Number 1, buy from the U.S., we have plenty, and

Number 2, build up some delayed courage, go to the Strait, and just TAKE IT.

You’ll have to start learning how to fight for yourself, the U.S.A. won’t be there to help you anymore, just like you weren’t there for us.

Iran has been, essentially, decimated.

The hard part is done. Go get your own oil!

President DJT

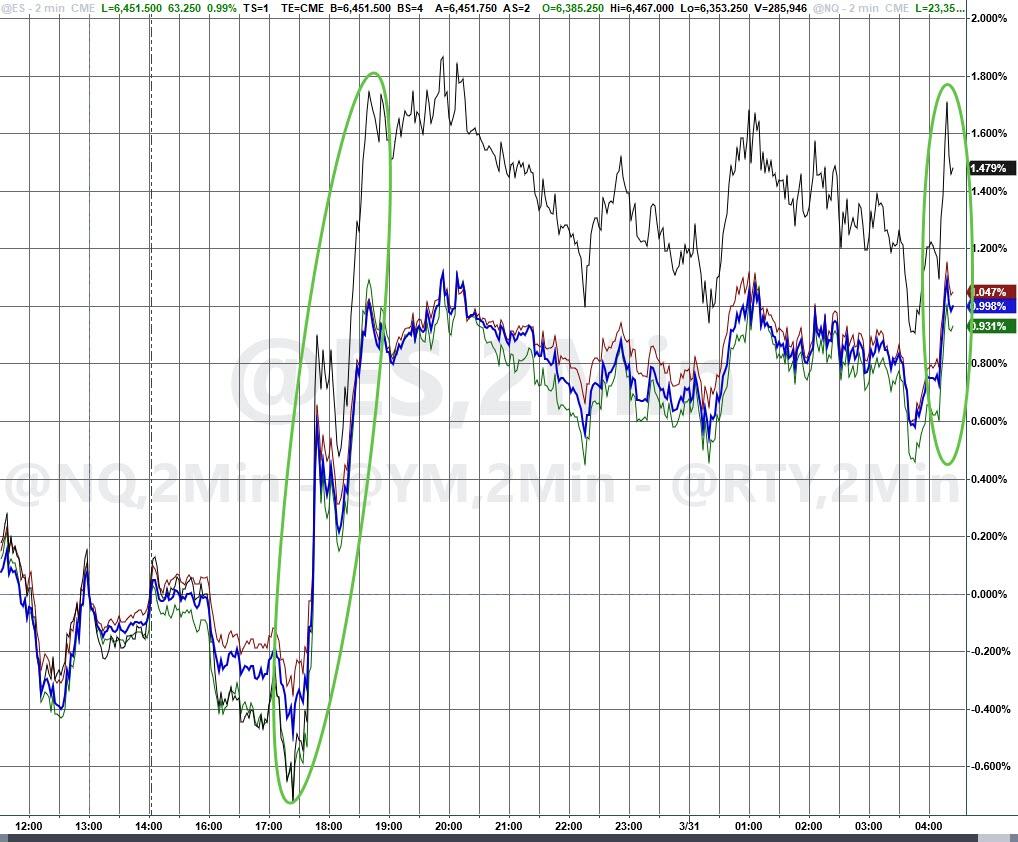

The reaction was a drop in the price of oil…

…and stocks rising…

Nothing dramatic in either – as traders remain nervous of Trump-Talk still – but nevertheless, as Goldman’s Rich Privorotsky noted overnight (in a seemingly precognitive comment before Trump’s tweet), this is shaping up like an off-ramp:

After ~5 weeks of conflict “President Trump told aides he’s willing to end the U.S. military campaign against Iran even if the Strait of Hormuz remains largely closed” (WSJ).

Politically messy (especially in GCC…less so domestically), but probably the least bad short-term pathway (can argue LT worse).

There’s a press conference at 8am EST from the Defense Department.

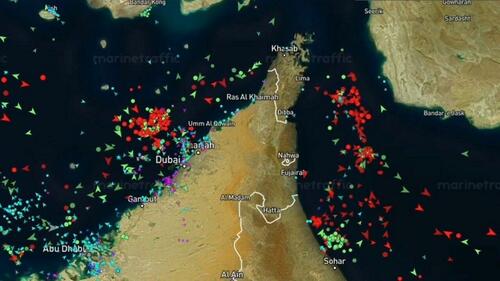

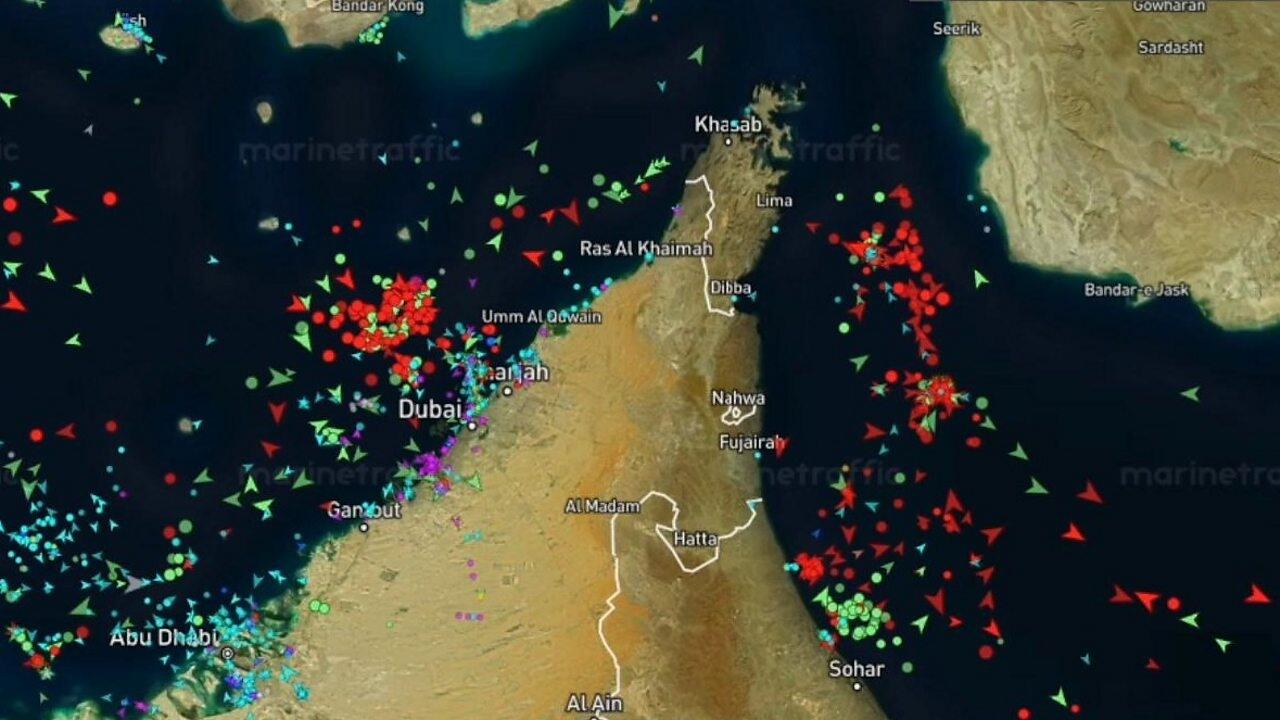

Overnight saw meaningful escalation… Iran struck a heavily laden oil tanker in Dubai port… a very explicit signal around control of shipping.

Likely in response to US actions around nuclear facilities in Isfahan

(Trump on his Truth Social posted uncaptioned video of large explosion 5 hours ago).

BREAKING 🚨: US dropped 2000 lb bomb over #Tehran#Trump and #netanyahu destroying #Iran#IranWar #ısrael pic.twitter.com/7CbrsHtqGu

— Pak-China Today (@PakChinaToday) March 31, 2026

The most bullish near term outcome would be a “mission accomplished” style announcement…

i.e. nuclear capabilities set back materially (say 10–20 years), allowing the US to step away.

No edge here, frankly could be anything but will be watching.

…

The key shift then remains the Strait.

If the US pauses while Iran maintains some level of disruption, the pressure flips… China, Korea, Japan, India, Europe and the GCC all become directly incentivized to force flows back online.

Even partial restrictions (e.g. US/Israeli vessels) are manageable…so a unilateral victory could actually restart flows and shift pressure to ROW to get strait moving.

Watch the live feed here:

Tyler Durden

Tue, 03/31/2026 – 07:37

Unilever In “Advanced Discussions” To Sell Food Unit To Old Bay Maker

Unilever In “Advanced Discussions” To Sell Food Unit To Old Bay Maker

Unilever Plc confirmed it is “now in advanced discussions” with Maryland-based spice maker McCormick & Company to sell its food business unit in a $15.7 billion transaction and said a final deal could be announced as soon as today.

“The Company is now in advanced discussions with McCormick & Company (“McCormick”) regarding a potential transaction,” the Anglo-Dutch consumer goods company wrote in a press release.

Unilever noted, “Work remains ongoing to agree and finalise a transaction and it is possible that an agreement could be concluded today, although there can be no certainty that a transaction will be agreed.”

Unilever explained that if the “transaction were to proceed,” it would combine most of its food business unit, excluding certain assets such as those in India, with the Hunt Valley-based spice company in a transaction valued at $15.7 billion.

After closing, Unilever and its shareholders are expected to own 65% of the combined company. The deal would be structured as a Reverse Morris Trust, making it tax-free for U.S. federal income tax purposes for Unilever and its shareholders.

The transaction is a big move for the spice company, known across the U.S. East Coast for its Old Bay seasoning and other brands such as French’s mustard and Frank’s RedHot.

McCormick is a much smaller company whose business generates about half of Unilever’s food unit. But the proposed transaction comes as Unilever pivots further toward beauty, personal care, and home products – higher margin items – while transforming McCormick into a major food player.

Wall Street analysts are mixed.

“We aren’t overly impressed by what we can see of Unilever’s potential disposal of its food business,” RBC Capital Markets analyst James Edwardes Jones told clients earlier. He added that the current deal means Unilever has full ownership of a division dominated by its own two brands, Hellmann’s mayonnaise and Knorr stock cubes.

Jones added that Unilever will have less ownership of a company with an even bigger brand portfolio. He said, “We are not sure of the justification for introducing partial ownership of a less concentrated business.”

Let’s remind readers that Unilever’s pivot into beauty also comes as blockbuster GLP-1 weight-loss drugs sweep the nation and become more affordable, which means Americans are reducing their caloric intake.

Unilever shares in London are up 1%, while McCormick shares in premarket trading in New York are up 4%.

When the proposed deal first surfaced in financial outlets earlier this month, Goldman analyst Natasha de la Grense had “lots of questions on structure” of the proposed deal (read note).

In addition to the Unilever-McCormick proposed deal that could soon be finalized, there were reports that the Anglo-Dutch consumer goods company will freeze hiring worldwide because of price shocks stemming from the US-Iran conflict.

Tyler Durden

Tue, 03/31/2026 – 07:20

https://www.zerohedge.com/markets/unilever-advanced-discussions-sell-food-unit-old-bay-maker

AI Is “New Front Door To Commerce” As Consumers Ditch Google For Chatbots

AI Is “New Front Door To Commerce” As Consumers Ditch Google For Chatbots

Shoptalk, one of the retail and e-commerce industry’s top U.S. conferences, took place in Las Vegas last week, where Goldman analysts had one key takeaway for clients on Monday morning: AI is beginning to reshape how consumers shop.

Analysts Brooke Roach and Kate McShane, among others, attended the conference and listened to retailers, consumer brands, and technology vendors focus on the evolving consumer space in the era of AI.

Their top takeaway was that AI is emerging as a “new front door to commerce,” and instead of beginning product searches on Google or Amazon, an increasing number of consumers are turning to chatbots to decide what to buy.

“Brands and retailers noted that consumers are increasingly beginning their shopping journey inside AI platforms rather than on brand websites or search engines, with adoption accelerating rapidly over the past several months,” the analyst noted.

Here are more takeaways from Goldman’s analysts after attending Shoptalk:

The front door to commerce is shifting to AI

Brands and retailers noted that consumers are increasingly beginning their shopping journey inside AI platforms rather than on brand websites or search engines, with adoption accelerating rapidly over the past several months.

GAP stated it is seeing stronger purchase intent and higher conversion from customers arriving through agentic channels, and described itself as explicitly not in a wait-and-see mode. The company also noted it is an early partner on Google’s Universal Commerce Protocol, which allows the merchant to bring its own experience including loyalty, promotions, and cart capabilities directly into LLM environments, rather than pushing users to a generic external destination.

Enhancing consumer relevance and enabling product research / purchase decisions

Brands noted that becoming relevant within LLMs is a different challenge from search engine optimization, as LLM crawlers ingest content differently and are blocked more often than classic search crawlers.

Sephora announced the launch of its own app inside ChatGPT, which allows users to connect their Sephora accounts and receive personalized beauty advice (e.g., skin type, shade matching). Management is currently experimenting with their entire ecosystem, and is using AI as another channel to extend their core proposition of being a trusted beauty advisor.

Behr partnered with Google’s Gemini to launch a paint visualizer designed to help DIY customers overcome color paralysis and feel confident in their purchases.

HD has a shopping agent called Magic Apron, designed to help customers find easy answers on home improvement projects.

LOW is using their AI-shopping assistant MyLow to help associates in stores and deliver personalized recommendations to the customers. Management noted that customer expectations are changing, as they now expect comprehensive answers, not just keyword-based results.

Trust and authenticity increasingly important

RDDT noted that consumer trust in online information is declining, as users are rejecting AI-generated content given its tendency to regurgitate information from other sources. Consumers value authentic perspectives and are turning to their platform for experience-based answers.

AEO emphasized the importance of continuously testing marketing creatives with customers and being attentive to what resonates and what doesn’t. They found that AI-generated content must be clearly identifiable on the platform, so customers can trust that the company is not attempting to deceive them.

As consumers shift product searches from traditional Google queries to AI-powered answer engines, the brands and platforms that establish an AI presence first could capture meaningful tailwinds.

Professional subscribers can find the full list of stocks Goldman analysts believe are “well-positioned to benefit” here at our new Marketdesk.ai portal.

Tyler Durden

Tue, 03/31/2026 – 06:55

https://www.zerohedge.com/technology/ai-new-front-door-commerce-consumers-ditch-google-chatbots

China’s Quiet Gains During US-Israel War On Iran

China’s Quiet Gains During US-Israel War On Iran

Authored by Hamza Zaman via RealClearDefense,

The Iran conflict continues to protract despite President Trump’s assumption of a quick and easy victory.

The goals of regime change and the decimation of the Iranian ballistic missile program remain unfulfilled, and the closure of the Strait of Hormuz further adds to the strategic qualms of the Western powers.

The GCC states are also facing significant damage to their services industry, transport infrastructure and energy sector.

While both sides suffer great losses in this protracted conflict, America’s biggest geopolitical rival – China – seems to be gaining palpable economic and strategic benefits from the ongoing conflict in the Middle East.

Challenges to Petrodollar and Yuan’s Rise against U.S. Dollar

Iranian strikes on GCC energy infrastructure, in retaliation for Israeli strikes on Iranian oil refineries and gas infrastructure, sent shockwaves through global energy supply chains. This resulted in supply chain disruptions, shortages, rationing and price hikes. These energy supplies are traded in U.S. dollars and constitute a discernible source of demand for the U.S. dollar. The closure of the Strait of Hormuz further amplifies supply chain disruption, forcing buyers to choose alternative sources, including Russia. Iran’s announcement of a safe passage for oil tankers in exchange for payment in Yuan is being hailed as a direct assault on the primacy of the U.S. dollar and the petrodollar system.

The outcome of these events is the diminution of the U.S. dollar’s hegemony and the rise of the Chinese Yuan. China continues to purchase discounted oil from Iran in Yuan, and the procurement of Russian oil will also be in non-USD denominations. The fall of the U.S. dollar will accentuate China’s rise as a major competitor of the U.S.. China is already vying for a common BRICS currency, and its efforts will intensify in the future, as the U.S. dollar continues to weaken. The war in the Middle East presents an opportunity for the Chinese Yuan to accentuate China’s geoeconomic rise.

Observing and Analyzing American Military Activities

China’s observation of Operation Epic Fury provides its military with an opportunity to gather ample data on American military tactics and strategies. It also provides China with insight into the capabilities and limitations of American weapon systems. The downing of American fighter jets, including F-15E Strike Eagles, KC-135 Stratotanker, F-35A and Q-9 Reapers, as well as the destruction of radars and limitations of American air defense systems in the Middle East, is an opportunity for the Chinese military to evaluate its military arsenal and reassess its own capabilities and limitations vis-à-vis American military prowess.

With the help of artificial intelligence and machine learning, the Chinese military would analyze these weapon systems and military strategies and create real-life war-like simulations for the Chinese military with precise data. The destruction and limitation of the American military assets will also persuade global vendors to pursue Chinese combat-tested alternatives from the May 2025 Pakistan-India War, thus augmenting Chinese defense exports.

Strengthening Rare Earth Leverage against American Military Industrial Complex

The involvement of the U.S. in another war in the Middle East has the American military industrial complex up and running. Given the intense bombardment, fast-paced depletion of its air defence interceptors and the destruction of radars, the U.S. is expected to swiftly replenish its arsenal. However, the U.S. reliance on China for rare earth minerals – essential for the American military industrial complex – indicates that the U.S. strategic autonomy is compromised. In response to the Trump administration’s tariff war and ban on advanced chips exports to China, China meticulously weaponized rare earth minerals, effectively defying the actions of the Trump administration. In the wake of the Iran conflict, the Trump administration’s dependence on China for its rare earth needs magnifies, actively putting China in an advantageous position.

The Chinese government can tactfully play its cards, forcing the U.S. to continue the exports of advanced chips to China as well as completely abolish the exorbitant tariffs on Chinese products.

Strategic Space in the Indo-Pacific

In order to replace the lost batteries and interceptors, the U.S. decided to transfer its Terminal High Altitude Area Defense (THAAD) system from the Korean Peninsula to the Middle East. Additionally, the U.S. moved 2500 marines and USS Tripoli, an amphibious assault ship, stationed in Japan, to the Middle East, with the reported plan of the takeover of Kharg Island – Iran’s predominant energy export hub. This, however, aggravates the security apprehensions of the American allies in the Indo-Pacific, especially South Korea and Japan. Given the Trump administration’s diversion of resources, these states will have to reconfigure their security policies and adopt a more amicable approach towards China. The Chinese government will welcome such developments, perceiving them as a strategic space in the Indo-Pacific. In the wake of reduced American military presence in the region, China will be in a better position to secure its strategic interests along the Strait of Malacca, consolidating its supply chain.

The longer the conflict protracts, the deeper the U.S. will be engulfed in another forever war. This may create temporary energy disruptions for China as well as complications for its BRI program. However, the reoriented focus of the U.S. on military campaigns will allow China to continue its economic rise, backed by innovation and advanced cutting-edge technologies. The stature of China will continue to be amplified as a non-interventionist state, believing in regional connectivity and shared economic growth. This scenario envisages more states swaying to the Chinese camp in the coming years, broadening the scope of BRICS+ and a common BRICS currency.

Hamza Zaman holds an M.Phil. degree in International Relations from Quaid-i-Azam University, Islamabad, Pakistan. He works as an Assistant Research Associate at the Islamabad Policy Research Institute, Pakistan.

Tyler Durden

Tue, 03/31/2026 – 06:30

https://www.zerohedge.com/geopolitical/chinas-quiet-gains-during-us-israel-war-iran

US Must Boost Domestic Uranium Enrichment To Counter Proliferation Risks

US Must Boost Domestic Uranium Enrichment To Counter Proliferation Risks

The Export-Import Bank of the United States recently issued letters of interest supporting up to $4.2 billion in financing for enriched uranium sales by General Matter to utilities in Japan and South Korea. This includes up to $2.4 billion for Japanese operators and $1.8 billion for South Korean ones over the coming decade.

As we reported, the deal advances American energy dominance and reduces allied dependence on adversarial fuel suppliers.

This transaction arrives as the United States, and much of the world, pursues a nuclear renaissance. Surging electricity demand from data centers and industry, combined with policy support for clean baseload power, requires reliable domestic fuel supplies.

With Russian enriched uranium imports facing a full ban by 2028, expanding US enrichment capacity is essential to avoid bottlenecks for both existing reactors and new advanced designs.

Yet the strategic case extends beyond energy security. Nuclear proliferation remains a core concern. Nuclear proliferation is the spread of nuclear weapons, fissile material, and weapons-related nuclear technology and information to additional states. A civilian nuclear power program, though intended for electricity generation, can serve as a foundation for weapons development.

Uranium enrichment technology used to produce low-enriched uranium at 3 to 5 percent U-235 for reactor fuel employs the same centrifuges and processes that can be adjusted to achieve highly enriched uranium above 90 percent, the level needed for nuclear weapons. A facility sized to fuel one reactor can produce material for roughly 20 bombs per year. Once a nation masters enrichment at commercial scale, the leap to weapons-grade material becomes significantly shorter and less detectable.

These risks apply even to close US allies, not just adversarial states. Saudi Arabia has pushed for domestic enrichment rights in ongoing nuclear cooperation talks with Washington, while Crown Prince Mohammed bin Salman has also stated the kingdom would pursue a bomb if Iran does.

South Korea has expressed interest in developing its own enrichment capability. A serious concern there is the potential for the technology to find its way to their northern neighbors.

In contrast, the United Arab Emirates accepted the so-called gold standard, forgoing enrichment and reprocessing in its civil nuclear program.

By building sufficient domestic capacity, the United States can become the preferred supplier of safeguarded enriched uranium to partners. This approach maintains oversight of the fuel cycle, discourages allies from developing independent programs, and limits technology diffusion.

Tyler Durden

Tue, 03/31/2026 – 05:45

Chancellor Merz Admits A “Considerable Proportion” Of Violence In Germany Comes “From Immigrant Groups”

Chancellor Merz Admits A “Considerable Proportion” Of Violence In Germany Comes “From Immigrant Groups”

The debate over violence in German society and schools has reached a boiling point in the Bundestag, pitting Chancellor Friedrich Merz and his supporters against critics who accuse him of racism, including a Left Party politician who published a photo of herself on Instagram giving him the middle finger.

The controversy intensified following a session where Merz addressed the issue of digital and analog violence, particularly against women.

“We have exploding violence in our society, both in the analog and digital space, and we must do something about it together,” said Merz.

However, he said that one must then also talk about where this violence comes from, he said to applause from members of the CDU/CSU and the AfD.

“And then we must also address the fact that a considerable proportion of this violence comes to the Federal Republic of Germany from immigrant groups,” he added.

🇩🇪🔴German Chancellor Friedrich Merz is under fire from the left for tying exploding violence with mass immigration.

“We have an explosion of violence in our society…Then we also need to talk about where this violence comes from. And then we must also address the fact that a… pic.twitter.com/ZPDuI4eHnv

— Remix News & Views (@RMXnews) March 27, 2026

These remarks drew sharp condemnation from the Social Democrats (SPD) and the Left Party. SPD parliamentary group leader Matthias Miersch argued that violence against women should be viewed broadly rather than being reduced to a single population group. Miersch stated, “I don’t think that was an adequate response from the chancellor.”

He added that “violence against women has no origin or religion, it is a problem of society and must be addressed clearly. It is about protecting victims, regardless of who the perpetrator is.”

Data on violence against women and foreigners

However, statistics tell another story from what Miersch asserted. Foreigners commit 65 percent of all sexual crimes on German trains and in train stations despite making up approximately 15 percent of the population. It must be noted that German citizens with a migration background are not included in this 65 percent figure.

As data from North Rhine-Westphalia showed, foreigners commit half of all gang rapes. However, when the first names of gang rape suspects are analyzed, it shows that at least half of the German citizens clearly had names from a foreign background, such as Mohammad. In total, that means 75 percent of all gang rapes are committed by a foreigner or someone with a foreign background.

Data presented by the German government last year shows that 63,977 women were victims of sexual violence in 2024 alone, and the perpetrators were disproportionately foreigners, making up 35 percent of all perpetrators, according to government data released as a result of an inquiry from the Alternative for Germany (AfD) party in the Bundestag.

German government data also shows there were 135,000 crimes by Syrian suspects against Germans since 2015 — one every 39 minutes.

The data, obtained by Freilich magazine, also shows large numbers of victims of crimes committed by suspects from other countries of origin, including 82,960 linked to Afghanistan, 69,946 to Iraq, 39,918 to Morocco, and 32,383 to Algeria. Altogether, more than 460,000 crimes were recorded in a 10-year period involving suspects from the 10 main countries of origin: Syria, Afghanistan, Iraq, Iran, Morocco, Algeria, Nigeria, Pakistan, Somalia, and Eritrea.

The Left says migrants should not be blamed

In the educational sector, Saskia Esken, chairwoman of the parliament’s Education and Family Committee, also raised concerns about school-related crimes. While acknowledging that the number of violent crimes recorded by the police in schools has increased significantly in all federal states, she firmly rejected the migration narrative, despite clear statistical evidence showing there is a serious problem with violence from Germany’s foreign population.

“Migration is not the problem in our schools,” Esken asserted, arguing that violence arises where children neither at home nor at school learn other ways to regulate their feelings and resolve conflicts. She described school as a motley, quasi-forced community where social workers and psychologists are desperately needed to address underlying issues like poverty and lack of prospects.

Again, the data contradicts her, showing that 40 percent of all violent crime suspects in German schools are foreigners. This data shows that there were 4,254 foreign suspects and 7,309 suspects with German citizenship, the German government announced in response to a parliamentary inquiry from Alternative for Germany (AfD) MP Martin Hess.

Of the 11,558 suspects in total, 1,236 had Syrian passports, representing one in ten violent incidents, according to the data, which was provided to Welt newspaper.

It must also be noted that a likely significant number of these suspects are German citizens with a migration background who are only counted as German in the statistics. Researchers, police, and society do not have a clear picture regarding the integration of previous generations of migrants and their role in crime due to this data reporting failure.

Middle finger for Merz

The Left Party member of the Bundestag, Cansin Köktürk, took a more provocative approach by posting a photo of her middle finger directed at Merz on Instagram.

She accused the chancellor of a “hysterical, constant whining” about migrants and suggested that he was serving a racist agenda.

“Hey Merz, I almost think you’d like to be part of us yourself. You’re so obsessed with talking about us,” she wrote.

Köktürk claimed that Merz instrumentalizes specific cases while ignoring the perspectives of those affected, describing his rhetoric as aggressive and hurtful.

Tyler Durden

Tue, 03/31/2026 – 05:00

Liberal MP Labels X A “Massive Problem” For Allowing Brits To Criticize Mass Immigration

Liberal MP Labels X A “Massive Problem” For Allowing Brits To Criticize Mass Immigration

Authored by Steve Watson via Modernity.news,

A British Liberal Democrat MP has openly admitted what the political class really fears about Elon Musk’s X: it lets ordinary Britons speak freely about the disaster of mass immigration.

In a clip that exploded across the platform on Monday, Cheltenham MP Max Wilkinson described X as a “massive problem” precisely because it gives critics of unchecked migration a voice.

“It’s a really easy [way] to get some content out about how you think immigration is too high, or immigration is the big thing that’s tearing the country apart… X is now making sure that you can have your voice heard in a really easy way that you couldn’t in the past,” he complained.

This is not some fringe rant. Wilkinson, the Lib Dems’ Home Office spokesperson, simply said the quiet part out loud. While the establishment lectures the public about “tolerance” and “diversity,” it seethes at the idea that native Brits can now push back online without gatekeepers filtering their concerns.

The backlash was instant and brutal. Toby Young of the Free Speech Union fired back: “Labour MP Max Wilkinson says the quiet part out loud: He doesn’t like X because it enables people who think immigration is too high to have their voices heard.”

Telegraph journalist Allison Pearson was even sharper: “God forbid people should be able to say on X that immigration is far too high. Or that it is causing problems for our way of life. Lib Dem MP Max Wilkinson thinks those opinions should be silenced. How dare he!”

This admission lands at the perfect moment to expose the broader pattern of suppression. It confirms exactly why the government has been so desperate to rein in platforms like X.

As we have highlighted, the UK’s relentless and ongoing push to ban or restrict X has been predicated on protecting children, yet is clearly about narrative control:

The same government that lectures about “hate” has already banned a teacher for the crime of saying migrants should respect our laws or leave:

Samuel Everett’s posts – “If you don’t respect our laws, culture and way of life you should leave, nobody is forcing you to stay” and “deploy the navy” on small boats – earned him an indefinite professional ban even, despite an independent panel clearing him of ‘racism’.

The government has also jailed a man for 18 months over two spicy anti-immigration tweets viewed just 33 times.

Last year alone Britain’s speech gulag saw 10,000 people arrested for social media posts.

The crackdown reaches into schools too. The Green Party wants to teach children radical ideology regarding immigration.

While the current Labour government urges schools to snitch on “anti-Muslim hostility” in an Orwellian dragnet.

It even produced a video game that brands kids “terrorists” for questioning mass migration:

Counter-terror police ran an advert warning teens that sharing “funny content” could be terrorism.

Meanwhile the demographic transformation accelerates. Migrants are set to swallow 40 percent of new UK homes by 2030.

A recent caller to Talk TV perfectly captured how most British people feel about it all:

And the hypocrisy never stops. The same regime is introducing an “anti-Muslim hate” definition while branding the Union Flag a tool of hate in leaked strategy documents.

Wilkinson’s outburst is the clearest proof yet: the real “threat” to the establishment isn’t hate, it’s democracy. They cannot win the argument on open borders, so they attack the platform that lets the public make it.

Britain does not need more speech restrictions. It needs politicians who listen instead of silencing the people they are supposed to serve. X is working exactly as intended – giving a voice to the voiceless. That is why the elites hate it, and why millions of us will keep using it, by hook or by crook.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Tue, 03/31/2026 – 03:30

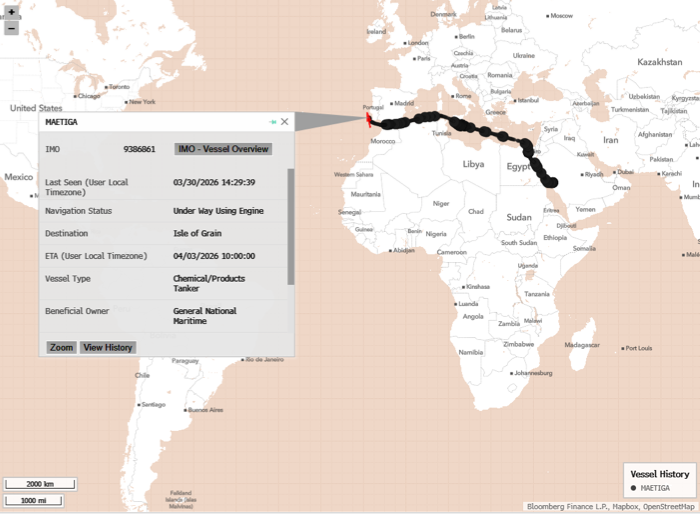

Tracking The Last UK-Bound Jet Fuel Tanker As Shortages Near

Tracking The Last UK-Bound Jet Fuel Tanker As Shortages Near

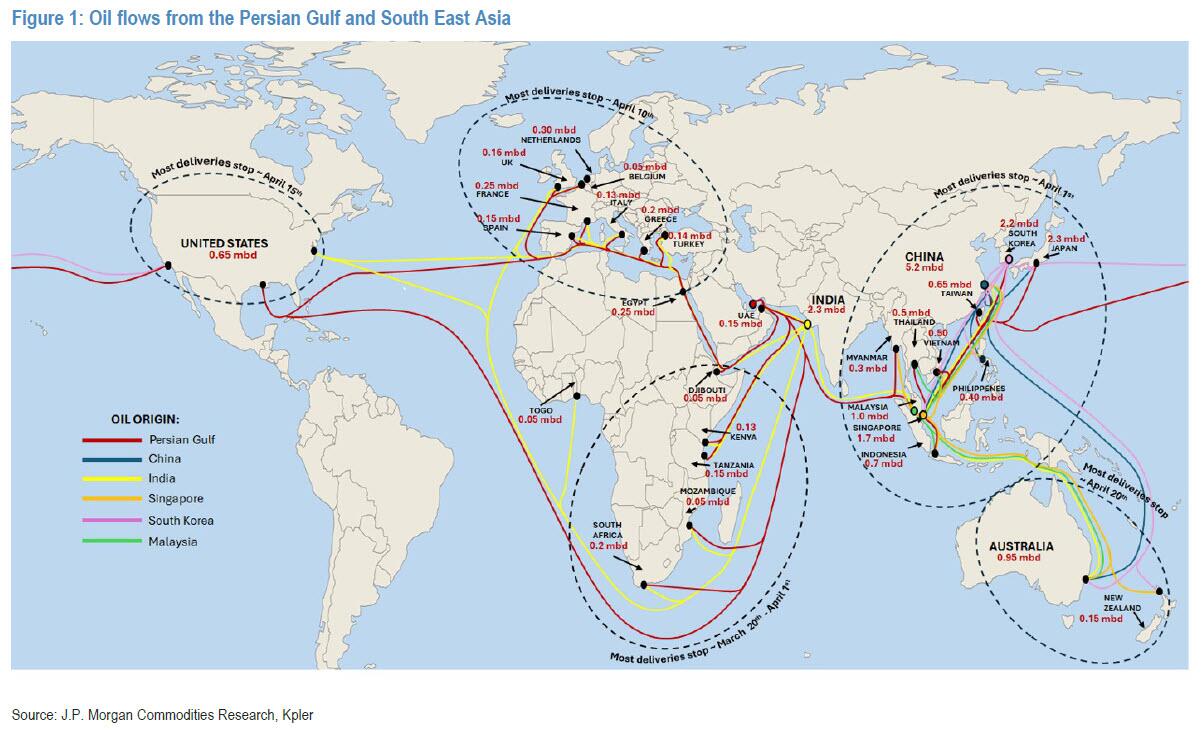

We outlined the early signs of global demand destruction and worsening energy chaos in a note earlier on Monday, mapping the regional dominoes and the order in which they are likely to fall. Turning to the UK, the last known jet fuel shipment from the Middle East is due to arrive later this week, a major warning that aviation disruptions could soon materialize.

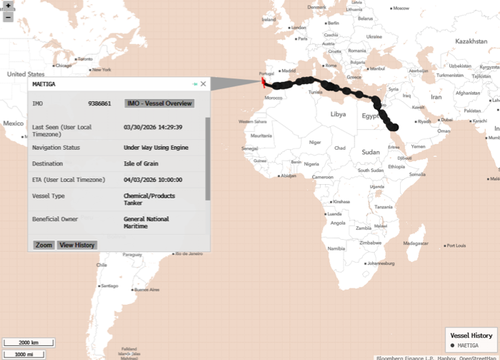

The Financial Times reports that the Libyan-flagged Maetiga vessel, loaded with jet fuel from Saudi Arabia, is set to dock in the UK on Thursday.

Maetiga is currently transiting off the coast of Portugal.

“No other UK-bound cargoes from the region are visible on the water, given the blockage of the Strait of Hormuz,” the FT noted.

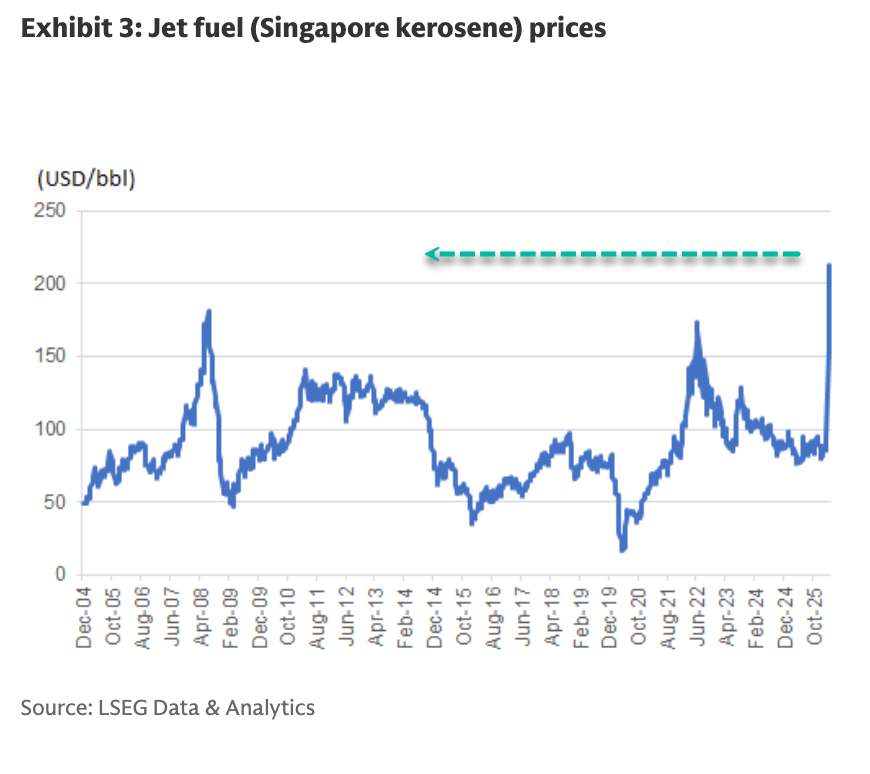

The UK has heavily relied on jet fuel transiting the Hormuz chokepoint for several years after phasing out Russian supplies. Analysts warn that airlines may begin to feel the supply crunch in late April if disruptions in Hormuz persist.

As of Monday, northwest European jet fuel prices were roughly double prewar levels. In Asia, Singapore kerosene is trading at more than $200 a barrel, more than double the level at the start of the year.

“Market understanding is that fuel shortages are not far away in some countries,” and “higher prices are to trickle through the entire supply chain and will be felt by all,” Janiv Shah, vice-president of oil markets at consultancy Rystad Energy, told the outlet.

According to UBS, a shortage of jet fuel in Asia, along with very high prices for what is available, is now leading to more flight cancellations.

As we noted in “Global Demand Destruction: Subsidies, Empty Gas Stations, Rationing, Flight Cancelations, Export Limits, Price Controls,” the regional order in which the energy chaos unfolds is Asia first, then Africa and Europe, before reaching the US, mostly California.

Via JPMorgan:

Europe sources a shocking amount of jet fuel through the Hormuz chokepoint, upwards of 40%, and the UK is especially exposed, both directly and through imports routed via the Netherlands and Belgium.

Lars van Wageningen, research and consultancy manager at data provider Insights Global, pointed out that supply chains are not broken just yet but are being reshuffled, indicating that European buyers will seek additional jet fuel supplies from refineries in West Africa and the US.

Two weeks ago:

Oil is bad. Products are worse pic.twitter.com/rxvlhDNFsv

— zerohedge (@zerohedge) March 19, 2026

Deutsche Bank and UBS have warned for weeks:

U.S. Airlines “Nearly 100% Unhedged” Against Energy Shock

The UK government has told travelers not to worry yet, which is usually the moment to start worrying. Energy shocks do not hit everywhere at once. As we point out, first through Asia, then into Africa, Europe, and eventually onto the US West Coast.

Tyler Durden

Tue, 03/31/2026 – 02:45

https://www.zerohedge.com/energy/tracking-last-uk-bound-jet-fuel-tanker-shortages-near

US Should Start Removing Its Troops From Germany, Proposes AfD Co-Leader Chrupalla

US Should Start Removing Its Troops From Germany, Proposes AfD Co-Leader Chrupalla

Alternative for Germany (AfD) co-chair Tino Chrupalla spoke out in favor of withdrawing American troops from Germany. During a party congress in Saxony, he stressed that, if AfD comes to power, this should be the first step in implementing the party’s program, which calls for the removal of all allied forces from Germany and a withdrawal from NATO’s nuclear weapons sharing system.

“Let’s start implementing this program by withdrawing U.S. troops,” he said, as reported by the Frankfurter Allgemeine Zeitung, cited by Do Rzeczy.

The proposal received loud applause by the audience.

Chrupalla also argued that Germany should not be involved in international military operations, praising Spain for opposing U.S. use of its bases for its conflict with Iran.

“And that is exactly right. Spain is not interfering in this war,” he said.

His criticism of American troops on German soil comes after his sharp criticism of Trump’s decision to launch a war against Iran.

“I am extremely disappointed in Donald Trump when it comes to his campaign promises,” Chrupalla during an appearance on Markus Lanz earlier this month.

“During the election campaign, he also accused Kamala Harris, that she would start World War III. And now we are on the cusp of having probably started the Third World War with Donald Trump. And that’s a breach of his word, which I really resent and which the American people also resent, who incidentally reject this war in Iran at a much higher rate than Germans. So, 70 percent of Americans do not want this war and do not support it.

Chrupalla also stated it was clear the United States was dragged into the war by Israel.

“And I think the Americans, as you can really see now if you look at all the events, were dragged into this war by Israel. There were serious negotiations where Oman, as a peacemaker, came to an agreement with Israel together with the USA, and they basically started bombing Iran on the same day. The Omani Foreign Minister has described this as a huge mistake. The entire Arab world has labeled it a mistake. The Norwegian Foreign Minister has described it as a mistake. It has also been labelled a mistake by Turkey. You can’t ignore all that. These are all countries in this region that are naturally extremely worried that this will escalate into a conflagration. And that’s what we’re seeing now. It’s a huge wildfire.”

In his most recent speech, Chrupalla also addressed Russia’s war against Ukraine. He announced that the AfD would “bring about peace” and that after the conflict ends, Ukrainians in Germany should return to their home country, criticizing the current refugee benefits system.

“This is exactly what must end. All Ukrainians must go back,” he said

Chrupalla’s speech made it clear that the AfD aims to take power in Germany, at both the state and national levels. “We must develop, moving from an opposition party to a governing party,” he said during the party convention in Löbau, as quoted by Deutsche Welle.

Germany’s next federal elections will take place only in March 2029. At that time, Chrupalla plans for the AfD to have a prime minister in Saxony and an AfD chancellor as the leader of Germany. Chrupalla also admitted that this requires further capacity-building and preparing party structures for governance.

Noting that AfD must no longer be perceived as a single-issue party, presumably referring to its focus on implementing mass deportations, and must demonstrate concrete results in government going forward.

“At some point, we will have to present our voters with successes,” he emphasized.

According to Bild reports, the party has already begun organizational preparations to take over the government by establishing a special working group for participation in the government.

Tyler Durden

Tue, 03/31/2026 – 02:00

Global Energy Crisis Or Iranian Surrender In Five Weeks?

Global Energy Crisis Or Iranian Surrender In Five Weeks?

Authored by Brandon Smith via Alt-Market.us

The last time global energy markets witnessed a shock similar to what we might see this year was during the 1973 Arab Oil Embargo. Tensions were escalating in the aftermath of the Yom Kippur War when the Arab Coalition launched a surprise attack against Israel. OPEC nations joined forces to cut off oil to Israeli allies including the US. This froze around 15% of oil exports to America, triggering market speculation, hording and price inflation.

The infection spread to Asian markets long dependent on the Middle East for energy resources. This slowed industrial capacity and many governments imposed rationing and price controls.

Images of long lines of cars at gas stations and people filling up extra containers remain burned into the collective memory of anyone who lived through that era. However, the real threat to the US was not supply shortages; rather, it was the prospect of a market cascade.

Stagflation coupled with supply chain vulnerabilities were exacerbated by public panic. Stock markets also plunged into recession territory in the expectation of an industrial slowdown. The embargo lasted only five months, but the damage was extensive.

Things have changed quite dramatically since the 1970s. The US is far less dependent on energy resources from the Middle East, though, any shocks to the global oil trade have the ability to ripple out and affect American markets. Furthermore, Arab oil producers are now largely allied with the US, which means there’s less risk of a prolonged shutdown due to conflict.

In the case of the Strait of Hormuz, any direct damage to America is minimal. Only 7% of all oil shipments to the US actually travel through the Hormuz, and, Venezuelan oil is helping to fill that gap. The greater danger is rooted in globalism and the interdependent trade system.

For example, US allies like Australia, India, Japan, and the Philippines are heavily exposed to the Hormuz shutdown. Australia is currently one month away from supply shortages and the country has little to no backup. The Philippines has already declared a state of emergency and established ration policies; they have perhaps 2 months of emergency supplies. Japan is currently tapping into strategic oil reserves and they are boosting coal fired power.

China, is facing significant exposure, with 15% of their oil supplies coming directly from Iranian wells and around 35% of their total oil supply traveling through the Hormuz. China has around 4 months of reserves before crisis hits them like a freight train.

Most Asian countries that are reliant on oil and natural gas passing through the Hormuz have around two months before they start to see public panic and long lines at gas stations similar to 1973.

Iran claims that they intend to let “non-hostile ships” pass the strait, but they’ve stopped multiple Chinese ships this week after this announcement was made. It is likely that war conditions will continue for at least another month, and, in the worst case scenario, the Hormuz could remain closed well beyond the cutoff date for many at-risk countries. The longer the war goes on, the greater the chance of a market cascade.

I’ve noticed that there are some bought-and-paid-for “prognosticators” out there adding their own propaganda spin to these events, including the notion that the west is on the verge of collapse because of the Hormuz closure. In reality, the east is far more economically exposed than the west is to this war. That said, there are risks to the US, and they are reliant on how long the conflict lingers.

Energy Crisis, Election Dangers And Global Economic Warfare

As I noted in October of 2024 in my article “The Atlantic Council Has Big Plans For A War Between The US And Iran”, there has been a concerted effort among globalists to lure Americans and Europeans into long term conflicts with Iran and with Russia. As I noted in 2024:

“The establishment media reports that Iran hacked the Trump campaign’s election strategies and gave them to the Harris camp. There are also rumors spread by US intelligence agencies that Iran was working to have Trump assassinated. Are these claims true? There’s little public evidence available to prove it.

Maybe Iran really wants to take Trump down. Or, maybe this is part of a plot to ensure that Trump backs a full blown war with Iran should he win the election. Trump has said repeatedly that he intends to end the war in Ukraine upon his return to the White House. This would ruin over a decade of planning by the Atlantic Council. But what if they can sink the US into a different conflict with the same potential for a world war? That’s what Iran is – Another linchpin…”

I would note that “world war” can take many forms. It could be a war using economic weapons rather than nukes. It could be a series of proxy wars that spiral and spread.

The Ukraine theater serves as a proxy war in which Russia indirectly engages with NATO and Russia is now forced to sustain its military posture for far longer than it expected at a much higher cost. Iran has the potential to become another Ukraine, but one in which the US is trapped into expending military and economic assets while Russia and China drag out the costs.

In my June 2025 article, “The Iran Trap: Everyone Wants Americans To Fight Their Wars For Them”, I predicted:

“Iran will receive ample weaponry and intel from Russian sources, prolonging the conflict….”

The Kremlin has essentially admitted that this is already happening. Iran has shown uncharacteristic precision with some missile strikes exactly because they have access to Russian satellite intel and targeting. The Russians could very well be running Iran’s strategic operations, for all we know. I also argued that:

“On the political front there will be a deep divide between pro-Israel conservatives and anti-war conservatives. Trump will lose a large percentage of his base if the US deploys troops. Americans might hate leftists enough that this won’t matter in 2026, but they’re not going to give Neo-Cons a free pass, either.”

In other words, one of the biggest disasters that could happen for the US as a result of this war is that ideologically deranged Democrats and leftists regain enough political leverage post-midterms to disrupt any practical reforms and eventually bring back the woke nightmare we witnessed under the Biden Administration. If this happens, mass violent unrest in America is inevitable. Not to mention, war with Russia in Ukraine will be back on the table.

For large swaths of Asia, the disaster will be immediately visceral, including economic implosion, rationing and probably civil unrest. And, thanks to globalism, economic crisis in Asia has the ability to spread into western economies.

The BRIC nations have lost much of their leverage over the US Dollar that they had 10 years ago (China’s dollar and treasury holdings have been cut in half and exports from China to the US have dropped significantly), but they can still engage in enough economic warfare through trade disruptions to wreak havoc on US markets.

As I mentioned in recent articles, any disruption to the Yen-Carry trade is perhaps the biggest threat to the US economy right now, and this could be triggered through high energy prices in Japan; not as an attack, but as a basic consequence of market interdependency. All of this depends on the true objectives behind US operations in Iran.

Is the goal an occupation and complete regime change? Well, this is clearly what the Neo-Cons and Israel want. That kind of project could take years to complete and it would require a maximum US ground commitment. However, if Trump intended to pursue an occupation I think he would have committed tens of thousands of troops on day one.

Is the goal to simply destroy the Iranian ability to project military power outside of their country, or take control of the Strait of Hormuz? Walking away is not an option at this stage (the Hormuz cannot be left in the hands of the Iranians without leverage against them). So, this would be the easiest objective to complete with minimal US ground operations, bringing us to our best case scenario…

The Key To Ending The Iran War In Five Weeks

We constantly hear about international exposure to the Hormuz shutdown, but the media rarely mentions that Iran is the MOST exposed economy of all. For now, Iranian oil ships continue to pass through the strait and these vessels are Iran’s economic lifeline. Strategic estimates suggest that without the steady passage of these oil tankers, the Iranian economy would completely collapse within five weeks.

In fact, there is already information leaking out from Iran which suggests that an economic crash is happening right now. This will accelerate the Islamic regime’s willingness to negotiate.

If they don’t, Trump’s strategy will be a ground invasion of Kharg Island along with several other Islands that Iran uses to help secure the Hormuz. Kharg Island handles approximately 96% of Iran’s crude oil exports, making it the single greatest weakness of the regime.

But what if Kharg represents too much risk? The American public abhors even minimal military casualties, which is why we are politically ill equipped to weather a long term war. There is another way, and it’s much safer…

Iranian cargo ships can be targeted for seizure by a US blockade of the Persian Gulf well away from the narrow waters of the Hormuz. The ships could be destroyed, but I suspect the Department of Defense will try to avoid oil spills and ecological disasters. Instead, the best option is to capture Iran’s tankers and then redirect the oil to countries in danger of shortages. Iran has the option of shutting off GPS tracking for their vessels (shadow fleet), but this would not help them maneuver past a comprehensive US blockade.

In other words, I argue that the US could turn the tables on Iran and use their reliance on the Hormuz against them. With Iran’s economy in shambles, they will no longer be able to purchase missiles or drones for resupply from Russia and China. They won’t be able to pay for logistic resources for their military and they won’t be able to contain public unrest.

The Iranians would be forced to negotiate and the war would be over quickly with minimal risk to US troops. It’s the only option I see for returning energy markets to normal operations within a couple months while preventing a global crisis. Trump should treat any calls for long term ground occupation with suspicion; there is no need for this kind of military commitment. The war can be decided quickly through economic means.

Tyler Durden

Mon, 03/30/2026 – 23:30

https://www.zerohedge.com/geopolitical/global-energy-crisis-or-iranian-surrender-five-weeks

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}