Category: News

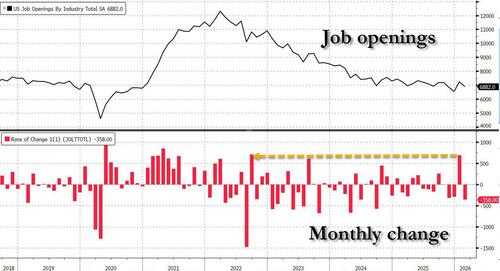

Job Openings Drop After Huge Upward Revision As Hires, Quits Unexpectedly Plunge To Six Year Low

Job Openings Drop After Huge Upward Revision As Hires, Quits Unexpectedly Plunge To Six Year Low

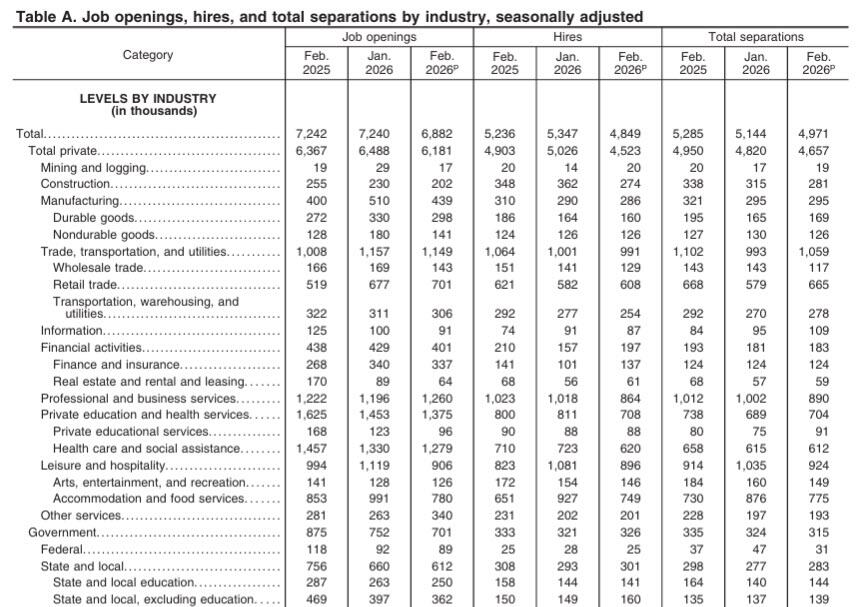

A few weeks ago, the BLS reported that January job openings unexpectedly soared by 400K, the biggest increase since November 2024, to 6.946MM, the highest since last October. Well, it turns out the jump was even higher than that because moments ago, the BLS published the latest February print, and while that number came in line with estimates, at 6.882MM, or just shy of the 6.890MM estimate, it was a big drop from January, which was revised massively higher by another 300K to 7.240MM from 6.946MM. In other words, the January job openings surge after the revision was a massive 690K, the biggest one month increase since Sept 2022!

In this light the February print, while a drop from January, was still a solid improvement from the January five year low of 6.550 million.

According to the BLS, the number of job openings decreased in accommodation and food services (-211,000) and in mining and logging (-12,000). Declines were also observed in Construction, Manufacturing,Information, Finance, Private Education and Government; these were offset by modest increases in Professional and business services as well as Other Services.

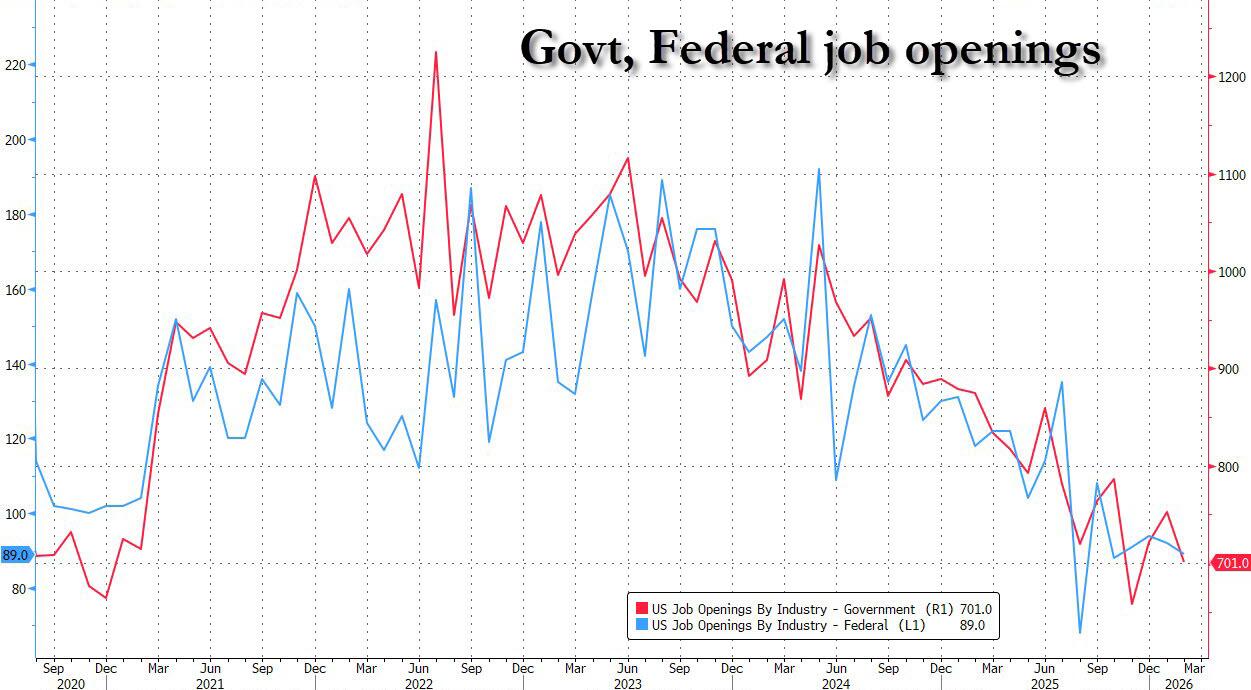

The silver lining: the collapse in government and federal job openings continues.

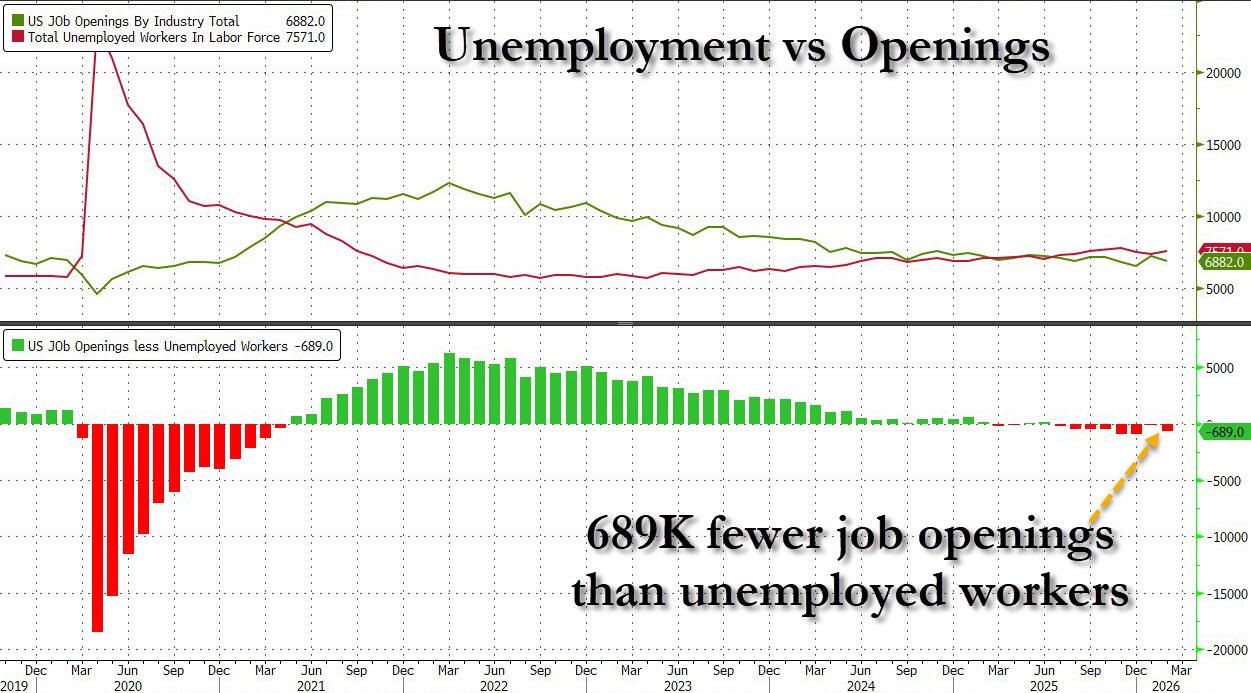

The sharp revision to January and then the extension of job opening declines in February meant that after almost reversing in January (-128K), February saw a surge in labor supply number as there were 689K fewer job openings than unemployed workers.

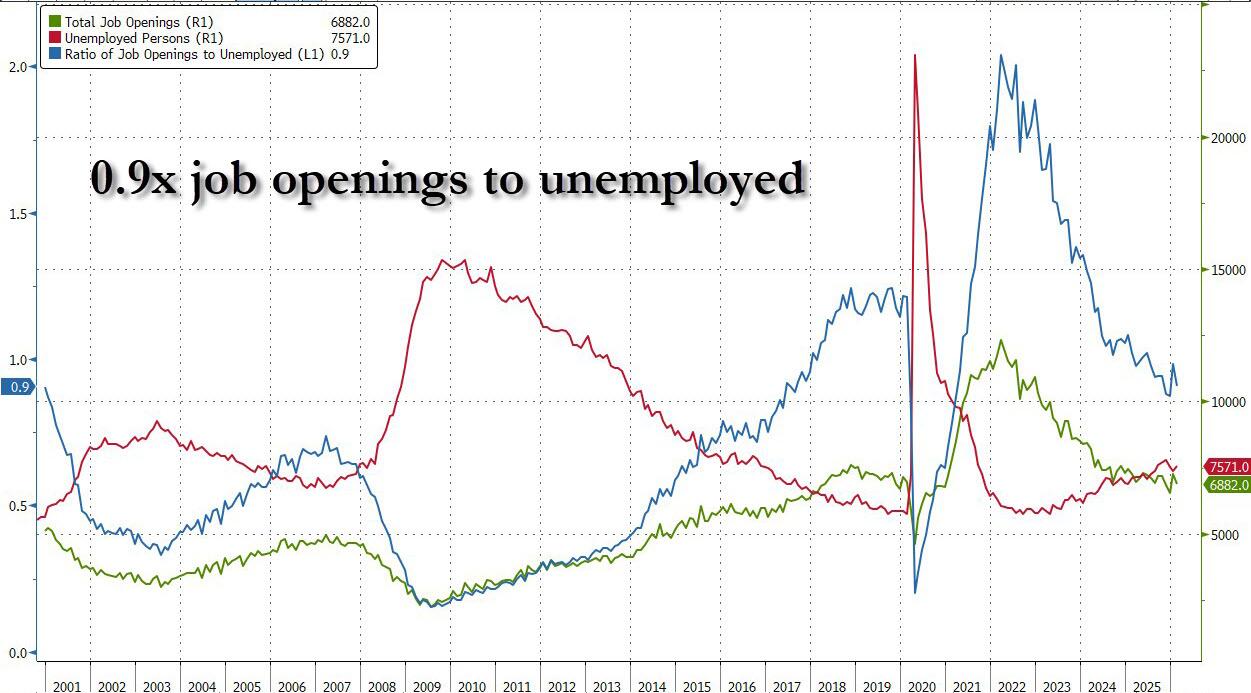

It also means that after rising back to 1.0x in January, in February the ratio of job openings to unemployed dropped back to 0.9x where it has been since last summer.

But while the job openings number was in line, previous month’s revision gimmicks notwithstanding, the real surprise in this month’s print was the number of Quits and Hires, both of which tumbled to 6 year lows.

The number of hires decreased to 4.8 million (-498,000) in February and was down by 387,000 over the year. The hires rate decreased over the month to 3.1 percent. This was the lowest hires rate since April 2020 when it was also 3.1 percent. In February, the number of hires decreased in accommodation and food services (-178,000) and in construction (-88,000).

Since this number feeds directly into the payrolls calculations (after netting out separations) this explains why the March payrolls report was such a total disaster.

As for quits, in February, the number of quits plunged by 157K to 2.974MM, the lowest since 2020, led by decreases in accommodation and food services (-119,000), wholesale trade (-35,000), and federal government (-6,000). Quits increased in nondurable goods manufacturing (+21,000).

Overall, this was a messy JOLTS report and aside from the now revised away January spike, it confirms that the US labor market continues to deteriorate slowly with every passing month.

Tyler Durden

Tue, 03/31/2026 – 10:33

Army Reviews Helicopter Flights Near Kid Rock’s Home, Anti-Trump Protests

Army Reviews Helicopter Flights Near Kid Rock’s Home, Anti-Trump Protests

Authored by Kimberly Hayek via The Epoch Times (emphasis ours),

The U.S. Army has opened an administrative review of two AH-64 Apache helicopters that flew low near musician Kid Rock’s home and above an anti-Trump protest in Nashville over the weekend.

Kid Rock, whose real name is Robert James Ritchie, posted a video on X on March 28 showing the helicopters hovering alongside his outdoor swimming pool. In the clips, he claps, salutes, and raises a fist as the aircraft linger nearby before flying off. The 27,000-square-foot hillside mansion he calls the “Southern White House” sits in the Nashville area.

The Army has launched an “administrative review” into why two Apache attack helicopters performed a low-altitude maneuver in front of the Nashville, Tennessee, home of Kid Rock.

Martha Raddatz reports. pic.twitter.com/oGRtBykO4R

— Good Morning America (@GMA) March 31, 2026

“An administrative review is underway to assess the mission and verify compliance with regulations and airspace requirements,” U.S. Army spokesperson Major Montrell Russell said in a statement sent to media outlets. “Appropriate action will be taken if any violations are found. Until the review is complete, there will be no further comment.”

The U.S. Army did not immediately return a request for comment.

“God Bless America and all those who have made the ultimate sacrifice to defend her,” Rock commented above the video of the helicopters.

The same helicopters had flown earlier over a “No Kings” anti-Trump protest in downtown Nashville that day. Demonstrators had gathered to protest President Donald Trump’s policies.

Fort Campbell leadership initiated the probe after the videos spread online. No injuries or property damage were reported. The Army has not released additional details on the crews or exact mission orders.

Saturday’s “No Kings” rally reflected broader opposition to Trump administration policies, including immigration enforcement and the Iran war. Local authorities said thousands participated in the protest in Nashville. More than 3,200 events had been planned in all 50 states, after the two previous nationwide events attracted millions of participants.

The Army emphasized that Apache crews routinely conduct low-level training in the region to maintain readiness. Such routes are approved in advance through federal aviation channels. Still, the proximity to a high-profile private residence and a political demonstration prompted immediate command-level attention.

Kid Rock has maintained a public friendship with Trump for years, endorsing him in multiple campaigns and performing at related events. His Nashville-area estate has hosted high-profile visitors and become a symbol of the entertainer’s conservative leanings.

Military helicopter operations near civilian areas have drawn scrutiny in the past when they appear to intersect with political activity.

The ongoing administrative review will determine whether any policies were breached. The Army said it will update the public if disciplinary measures or procedural changes follow.

Reuters contributed to this report.

Tyler Durden

Tue, 03/31/2026 – 10:25

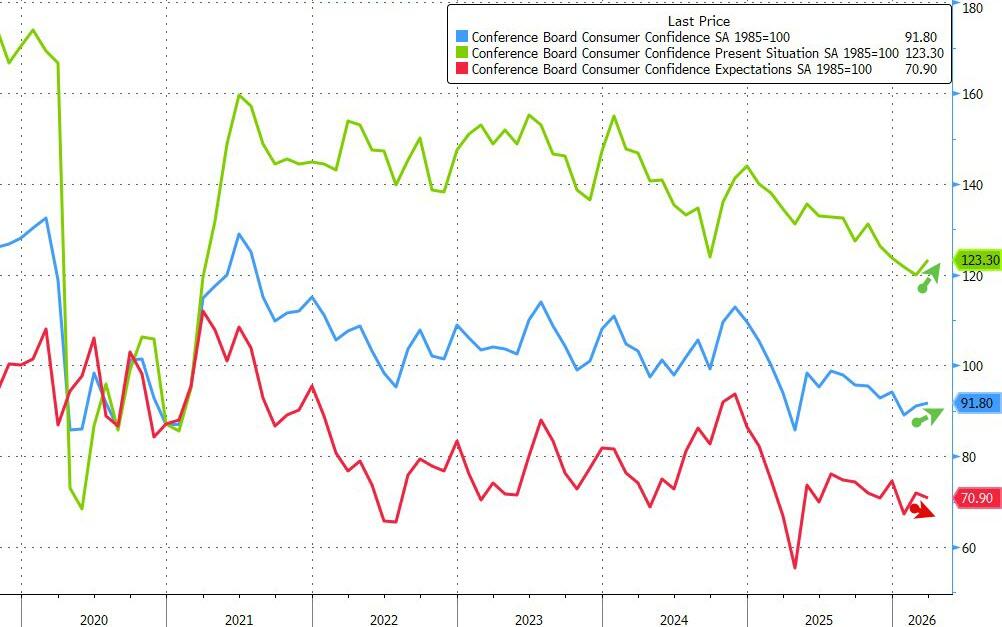

Conference Board Confidence Unexpectedly Jumped Amid War In March

Conference Board Confidence Unexpectedly Jumped Amid War In March

Despite war (and rising gas prices) now on respondents’ minds (the survey period for preliminary results was March 1 to 24), it is perhaps surprising that The Conference Board’s Consumer Confidence rose more than expected in March (from 91.0 to 91.8), considerably better than the 87.9 expected.

Even more intriguing, the Present Situation rose from 120.0 to 123.3 (118 exp) while Expectations fell from 72.0 to 70.9 (68.4 exp)

Source: Bloomberg

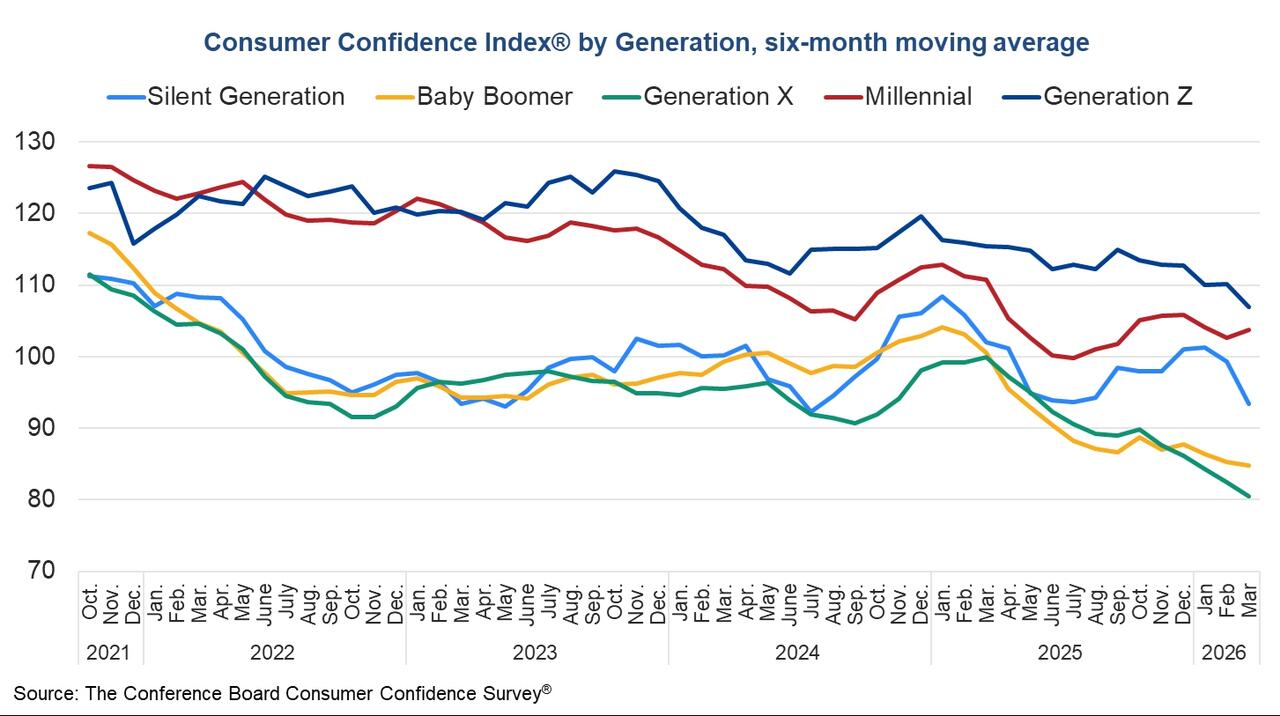

Among demographic groups, confidence on a six-month moving average basis continued to moderate in March for consumers under age 35 and 55 and over, and virtually unchanged after a multi-month decline for those aged 35 to 54.

Respondents under 35 remain the most optimistic and those 55 and over the least.

On a six-month moving average basis, Generation Z remained the most confident among all generations, but their optimism slipped in March along with the Silent Generation, Baby Boomers, and Generation X.

Only Millennials cited improved confidence in the month. By income, confidence on a six-month moving average basis continued to dip in six of eight income groups.

Only consumers earning $25,000-34,999 and $125,000 and over were somewhat more optimistic.

Oddly, with the rise in optimism, inflation expectations surged higher…

Source: Bloomberg

And even more surprising, the weakening labor market trend continued…

Source: Bloomberg

“Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism. Comments about prices and the cost of goods suggest that the cost of living remained at the top of consumers’ minds. As the war in Iran overlapped significantly with the survey sample period, comments about oil/gas and war/conflict spiked, while specific mentions of trade and tariffs decreased notably,” noted Dana M Peterson, Chief Economist, The Conference Board.

Consumer confidence by political affiliation was little changed.

Republicans remained the most optimistic, while confidence was substantially lower among Independents and the lowest among Democrats.

Tyler Durden

Tue, 03/31/2026 – 10:14

https://www.zerohedge.com/markets/conference-board-confidence-unexpectedly-jumped-amid-war-march

No THAC0 Tuesday

No THAC0 Tuesday

By Michael Every of Rabobank

No TACO And No THAC0

The Global Daily yesterday noted lots of reasons to worry about this Gulf War 3 – today there are far more. However, as made clear since the start of this crisis, there is no way to say, “This is silly,” or to ‘go home’ and return to ‘normality’. Everyone in the war except the US *is* at home.

Israel is targeting Iran’s leaders and PM Netanyahu says the country is only “over halfway” to its war goals, with no timeline for ending the conflict. Key Gulf states are urging Trump to intensify the war, even as Trump may bill them for it. Iran’s parliament just passed a bill imposing tolls on Hormuz, seizing that key waterway, and is pressing Yemen’s Houthis to renew attacks on Red Sea shipping, which would massively exacerbate this crisis – Bloomberg warns of $140 oil if so; a disavowed report just said Egypt, who wants the war to end, warned the Houthis it would then attack them. The Iranian ambassador refused to leave Lebanon when ordered to by its government; and Iran just struck Israel’s oil refinery in Haifa, and a fully laden oil Kuwaiti oil tanker in Dubai. In short, the Middle East has its own agency.

The implications for the US in this war are also far beyond oil prices and the mid-terms: Trump’s ‘reverse perestroika’ and 21st century US hegemony may pivot on who wins. If the US wins, it de facto controls Middle East energy and can build a new architecture there. Yet financial press op-eds arguing for a ‘blueprint for Chinese global leadership’ could be right if the US loses – in which case everyone clinging to the flotsam and jetsam of the ‘rules-based order’ loses too.

Only if one starts with that strategic geopolitical imperative is Trump’s potential willingness to climb the escalatory ladder predictable, as is that there can’t be the ‘TACO’ markets want. That thinking underlines our geopolitical base case this war is largely over in 2-3 weeks, on favourable terms to the US – which is what Secretary of State Rubio just told the G7 too: but only after things get much worse first. If they get worse and stay there, so will the economic projections.

Notably, Trump has now warned the faction of the Iranian leadership he’s dealing with –reportedly led by parliamentary speaker Ghalibaf– that if it won’t strike a deal soon that includes reopening Hormuz, the US will destroy Iran’s electricity network and energy before leaving. Yet Trump is also reportedly telling aides that he’s willing to leave Hormuz in the hands of a smashed regime. Either outcome would leave Iran, the Middle East, and probably the global energy system in structural chaos. Meanwhile, thousands of US army paratroopers and marines are close to positions around Iran, offering the US other strategic options: but to what end? Tehran? A uranium hunt? It seems logical. A bridgehead in Hormuz via its smaller islands? Perhaps so. The obvious, but dangerous, target of Kharg island and its oil facilities?

A key complaint, after no TACO, is that the US isn’t clear in its objectives: in the last 24 hours we’ve seen conflicting messages from Bessent, Trump, and Rubio over what the US is trying to do re: Hormuz. Yet here one has to raise another geostrategic point: why does the US have to say exactly what it intends to do? Voters and traders want to know, but the ‘fog of war’ is a critical advantage and Trump is a past master at misdirection. Yes, perhaps there isn’t a US plan, and markets would be wise to price in that uncertainty; but nobody in power is going to tell a journalist or analyst what their war plans are, just what they *want* them to hear and then tell others. For any D&D players reading, there is no THAC0 in war. (But those decision-makers may front-run their actions in markets, so keep your eyes open for those loaded dice.)

In energy, Brent was down at $111 this morning in Asia despite the Kuwaiti oil tanker being hit, with WTI at $102 and 1-month TTF gas at €54.8, while jet fuel in Singapore is at a new high of $233.5, showing more pressure there. European and African oil markets are getting tighter as Asia buys more to fill its supply gaps. Expect that to continue ahead.

In related news, the IMF warned the UK faces one of the biggest energy shocks; Brussels says Europeans should consider traveling less to avoid energy shortages; and a report has it that EU member states’ national fuel price measures are threatening to worsen the energy crisis; China is looking to restart US energy imports as it sees its position in aluminium and EVs strengthened; and Australia’s PM has stated that fuel rationing will only kick in at an “extraordinary” supply hit, without specifying what that is.

Re: uncertainty, Gulf War 3 is exponentially accelerating the evolution/devolution of the global system which was already ongoing.

Spain has closed its airspace to the US military over the war, widening a rift with it. Rubio has just stated that after this is all over, NATO must be “re-examined” – and he’s the US good cop. Don’t think comfortable plans for accelerated European military spending by 2035 will hold up if the US were to make as radical a move vs NATO (and/or Greenland) as it did vs Iran once the Middle East dust has settled. That’s for an EU where, as Politico notes, ‘Europe’s crisis tourism: how the Iran war swallowed the EU’s geopolitical agenda.’

In the US, there is a rush to shift to new defence systems, so cheap drones are not fought with million-dollar missiles. That will entail a major military-industrial structural shake-up, with lessons learned from Ukraine, whose prowess Germany’s Rheinmetall CEO was recently mocking.

The USTR says he now sees only a limited role for the WTO after its recent meeting in Cameroon failed to see any reforms: Politico notes, ‘As the WTO flounders, the world’s middle powers go their own way.’ The US is also pressuring the EU to join its AI chips ‘club’, as the EU is pushing the US to join it in a common 50% steel tariff vs. China. Does the dust eventually settle with EU-US cooperation or separation – and if so at what cost to both?

Meanwhile, in Australia the RBA minutes’ key line was: “it was not possible to predict the future path for the cash rate target with any confidence, given the high degree of uncertainty around the breadth and duration of the current conflict in the Middle East.” It added that the direct effect of oil prices remaining around $100 would on its own lift headline CPI to around 5% in Q2, 0.75% higher than expected in February, and sustained higher oil prices would boost inflation more broadly over time. A majority agreed further tightening in policy would likely be required in the near term, but a minority was already worrying about the ‘stag’ part of stagflation.

The RBA is right about the Middle East – and let’s repeat that one then has to look at that complex region through a broad geopolitical lens, not a narrow “because markets/elections” one that said this war wasn’t going to happen. Oh – and that today saw half a million young Aussie workers get up to 42% pay increase due to changes to minimum wage rates.

Tyler Durden

Tue, 03/31/2026 – 09:55

Negative Equity Leaves 30% Of Car-Buyers Underwater On Trade‑Ins

Negative Equity Leaves 30% Of Car-Buyers Underwater On Trade‑Ins

Authored by Andrew Moran via The Epoch Times,

Almost one-third of American car buyers with a trade-in owe more than the vehicle is worth, new industry data show.

About 30.5 percent of buyers trading in a car toward a new vehicle maintained negative equity, according to a JD Power report released on March 26.

This is up 4.2 percentage points from a year ago and has been steadily rising since 2022, “as consumers who purchased during the peak of inventory shortages 4 years ago return to market,” says Thomas King, president of OEM solutions at JD Power.

“Regarding total consumer spending on new vehicles, the elevated transaction prices in March aren’t enough to offset the inflated sales pace a year ago,” King said. “Consumers are on track to spend $49.4 billion on new vehicles this month, 13.9 percent lower than a year ago.”

Growing auto debt has become a significant challenge in the current car climate, with many motorists enduring the consequences of their pandemic-era financial decisions.

Edmunds, a subsidiary of CarMax, reported in January that the average amount owed on underwater trade-ins during the fourth quarter was a record $7,214. Additionally, 27 percent carried $10,000 or more in negative equity—also an all-time high.

If a buyer trades in a vehicle with negative equity, the remaining balance is typically folded into the financing for their next car. That rollover effect, according to Edmunds data, has pushed the average monthly payment for these borrowers to an all‑time high of $916.

Many underwater trade-ins can be traced back to pandemic‑era loans. At the time, chip shortages slashed inventories and wiped out incentives. Buyers paid close to or above the Manufacturer’s Suggested Retail Price (MSRP)—the sticker price automakers recommend a dealer charge for a new car—and had limited ability to choose cheaper models.

Since leasing was limited, many drivers opted to purchase these vehicles with loans, incurring different financial costs. Years later, the loan balances surpassed the cars’ value.

The auto market—and the typical depreciation—has since stabilized. However, because these loans were originated during a period of elevated prices, they have matured into a market where vehicle values have normalized. That mismatch has widened the gap between purchase prices and current trade‑in values.

But a new threat has emerged in the U.S. auto market: ultra-long car loans.

The Seven-Year Loan

Kelley Blue Book figures reveal that car prices have accelerated over the past year. The average new-vehicle transaction price was firmly above $49,000—hovering near record levels—in February.

“Sales are no longer swinging wildly month to month, but growth is also harder to come by,” Charlie Chesbrough, senior economist at Cox Automotive, said in a March 25 note. “Affordability remains the central challenge for the industry, and that is limiting the market’s ability to expand beyond the mid-15-million range.”

Borrowing costs also remain elevated, with the average auto loan interest rate close to 7 percent.

Current conditions have forced car buyers to take on seven-year loans. An estimated 41 percent of new-car purchases involving negative equity are financed with 84-month loans.

It is unclear whether these numbers will lead to significant pressure on consumers. So far, the data indicate that buyers are not falling behind.

TransUnion says about 1.5 percent of auto loans are 60 days past due. The New York Fed reports that the share of loans in serious delinquency—90 days or more—stands at nearly 3 percent.

In total, Americans owe $1.7 trillion in auto loan debt, soaring 56 percent in the past decade.

While lenders take into account a wide array of factors to price interest rates—credit risk, consumer-loan dynamics, and funding costs—they also loosely track yields on Treasury securities, particularly the five-year government bond.

The five-year Treasury yield has spiked over the past month amid the war in Iran, reaching around 4 percent from its pre-conflict level of 3.5 percent.

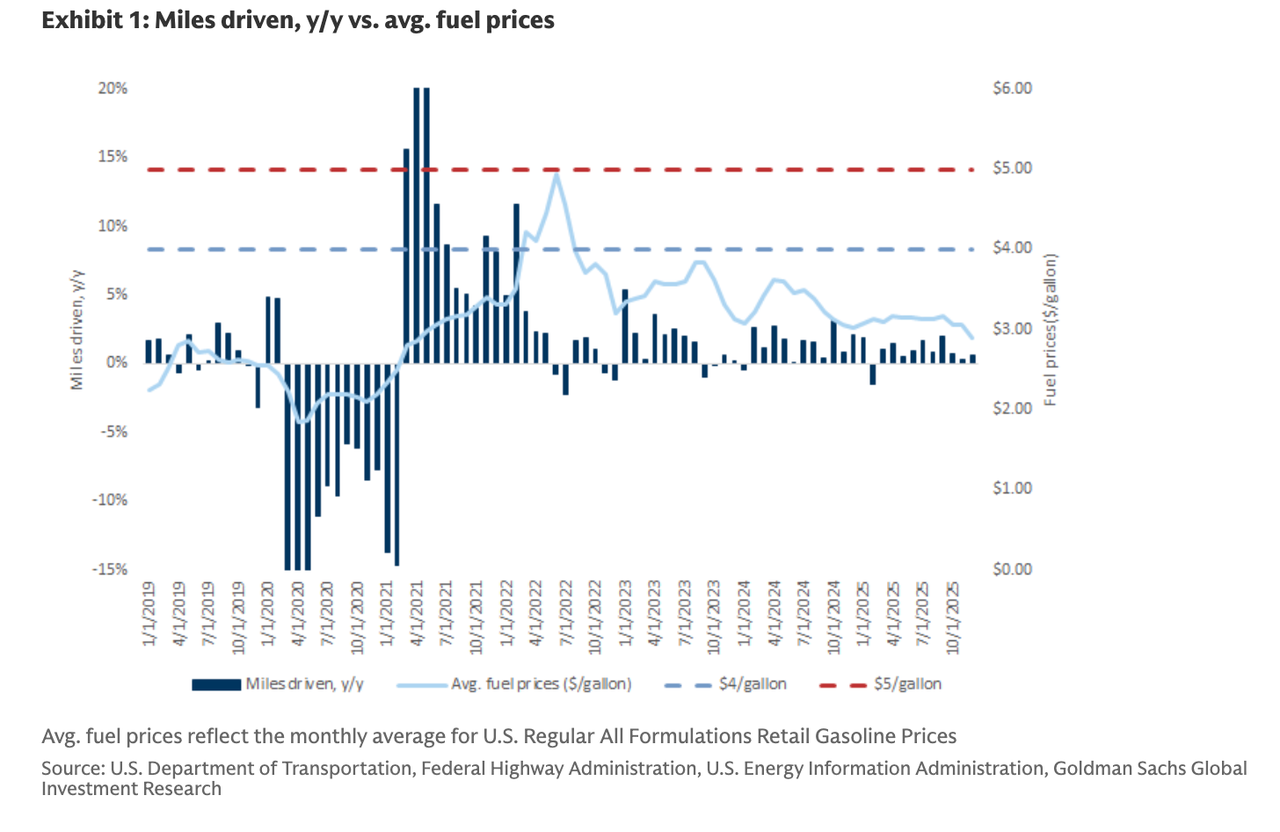

In addition to high car prices and borrowing costs, drivers are also contending with increasing pain at the pump. The national average price for a gallon of gasoline is close to $4, according to the American Automobile Association.

Tyler Durden

Tue, 03/31/2026 – 09:35

https://www.zerohedge.com/personal-finance/negative-equity-leaves-30-car-buyers-underwater-trade-ins

Putin Winning, Ukraine’s Position Weakened, From Prolonged Iran War: Zelensky

Putin Winning, Ukraine’s Position Weakened, From Prolonged Iran War: Zelensky

Ukrainian President Volodymyr Zelensky has warned that a prolonged Iran war will be a net win for Moscow – and a significant setback for Kyiv. Speaking to Axios, he said bluntly: “I am sure Russia wants long war. They have benefits: The US is focusing on the Middle East and may decrease military help to Ukraine.

Further he highlighted that “Sanctions are partially lifted” on Russian energy and so “I see only benefits for Russia from the war with Iran continuing.”

Ukrainian Presidential Press Service, via Agence France-Presse

The logic is simple, he explained: higher oil prices and softer sanctions boost Russia, while US focus shifts away from Ukraine – as well as attention from Western partners – which ultimately results in tightening weapons supply. “I am not just concerned, I am sure we will have such challenges. Absolutely,” he continued.

Zelensky has also been reminding Western audiences that Moscow is actively aiding Iran, including targeting support via intelligence: “I think Russia is supporting Iran directly, 100%… the same format of sharing satellite images like they did in the case of Ukraine,” Zelensky asserted.

This will in the long-run result in a weaker Ukraine, particularly given the surging demand for interceptors in the Middle East. But Zelensky has for weeks been arguing that Ukraine needs these defensive missiles, such as Patriots, the most – repeatedly calling the issue a matter of “life and death”.

Interestingly and somewhat ironically, this has led to Zelensky sounding like a dove and a peacenik:

“Our advice, when they asked us, was to stop the war as soon as possible and sit for negotiations – even if they can’t sit together with Iran – and find a diplomatic way to end the war. But it is up to the sides,” he stressed.

Zelensky himself has at various times throughout the war refused any negotiations with Moscow which hinge on making territorial concessions, while demanding more constant flow of arms and ammo from NATO backers.

Amid waning support from the Trump administration, Zelensky has set his sights on greatly improving ties with the wealthy oil and gas monarchies in the Gulf.

He’s lately been in the Middle East, even as Iran retaliates on Gulf states said to be hosting US forces, while seeking Ukrainian security assistance. In recent days he has met with the leaders of Saudi Arabia, the UAE, Qatar and Jordan. The NY Times gave some background context as follows:

President Volodymyr Zelensky of Ukraine hailed his Middle East tour to promote anti-drone technologies as a success, saying on Saturday that he had negotiated air defense agreements with Saudi Arabia, Qatar and the United Arab Emirates.

In the Mideast conflict, Ukraine has sought to shift its image from a recipient of military aid to a supplier. It sees an opening to export its low-cost, innovative designs created during the war with Russia to compensate for shortages of weapons and ammunition. Ukraine’s military often relies on consumer technologies such as virtual-reality goggles for gamers and off-the-shelf drone components.

This after Trump has indeed signaled willingness to redirect arms meant for Ukraine to the Middle East, where they are urgently needed as part of Operation Epic Fury, and to defend regional allies and increasingly exposed US regional bases.

Tyler Durden

Tue, 03/31/2026 – 09:15

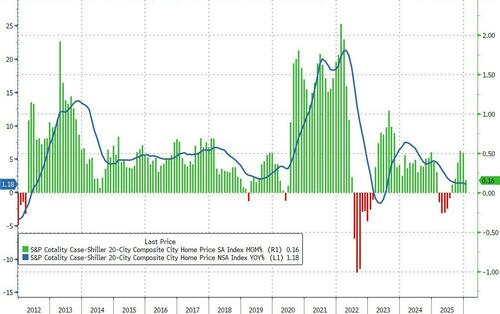

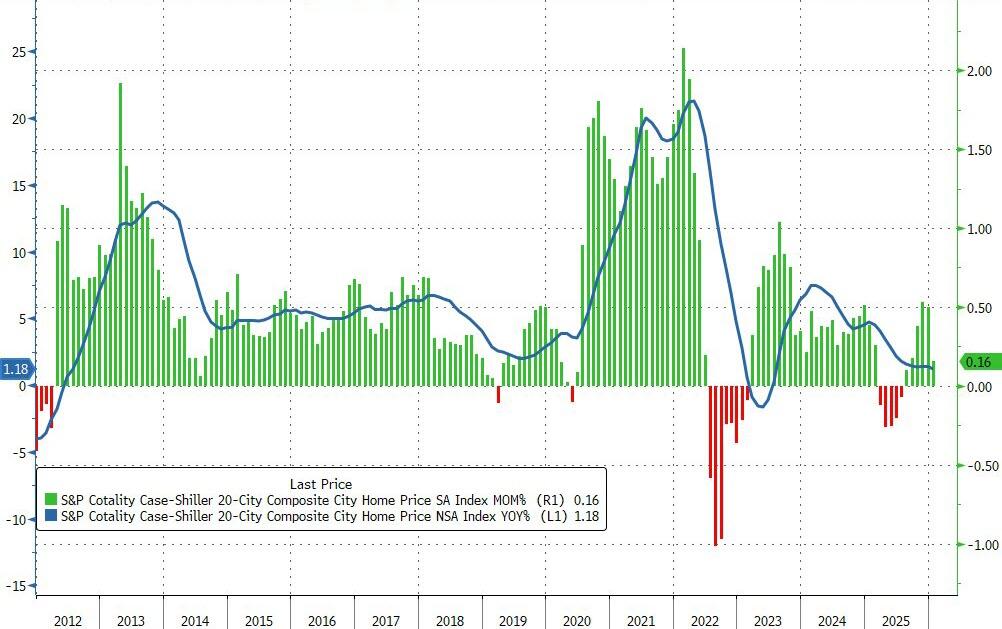

Despite Tumbling Rates, US Home Price Acceleration Slowed In January

Despite Tumbling Rates, US Home Price Acceleration Slowed In January

US home price acceleration slowed significantly in January (according to the always lagged and smoothed Case-Shiller indices).

After rising 0.50% MoM in December, the price of homes in America’s to 20 cities rose just 0.16% MoM in January (the lowest MoM rise since August and well below the 0.35% MoM expected)…

Source: Bloomberg

This left the 20-city composite index up just 1.18% YoY – the lowest since July 2023.

“Price levels remain elevated, but the rate of appreciation has slowed materially,” according to Nicholas Godec, CFA, CAIA, CIPM, Head of Fixed Income Tradables & Commodities at S&P Dow Jones Indices. .

“Splitting the year into two halves sharpens the picture,” Godec continued.

“The National Index rose 2.2% over the first six months of the period, then fell 1.3% over the most recent six – a swing that explains why annual gains have compressed to under 1% despite prices remaining historically elevated.

“Geographic leadership remains narrow,” Godec concluded.

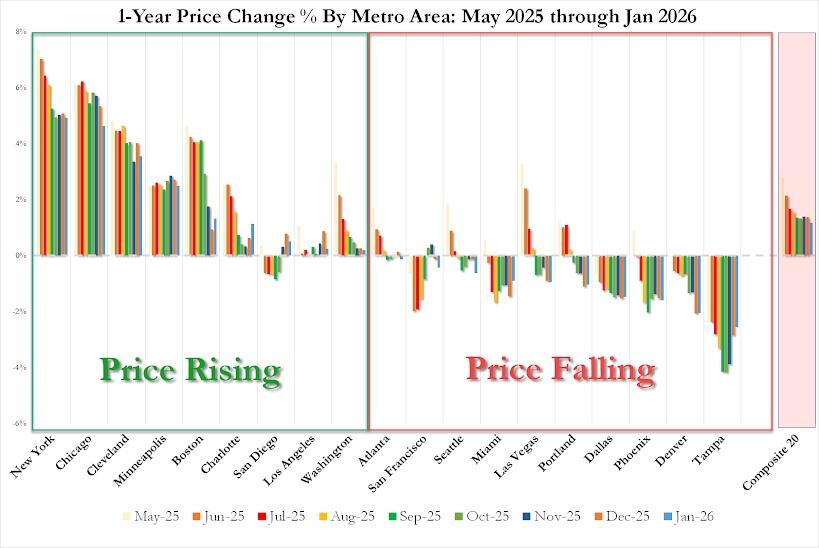

New York leads with a 4.9% annual gain, followed by Chicago at 4.6% and Cleveland at 3.6%, while Tampa fell 2.5%…

However, declining mortgage rates since suggest a rebound in aggregate prices could be about to explode…

…before the recent rise in rates kicks in (remember case-shiller data is very lagged).

Is this what President Trump wants to see? Flat prices and lower mortgage rates means more affordability…

credittrader

Tue, 03/31/2026 – 09:09

https://www.zerohedge.com/markets/despite-tumbling-rates-us-home-price-acceleration-slowed-january

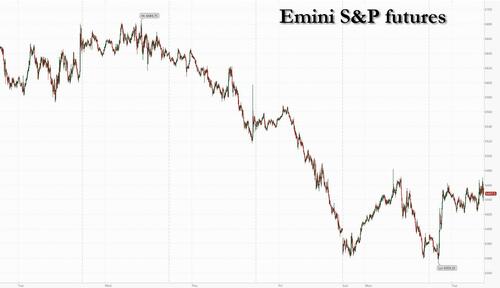

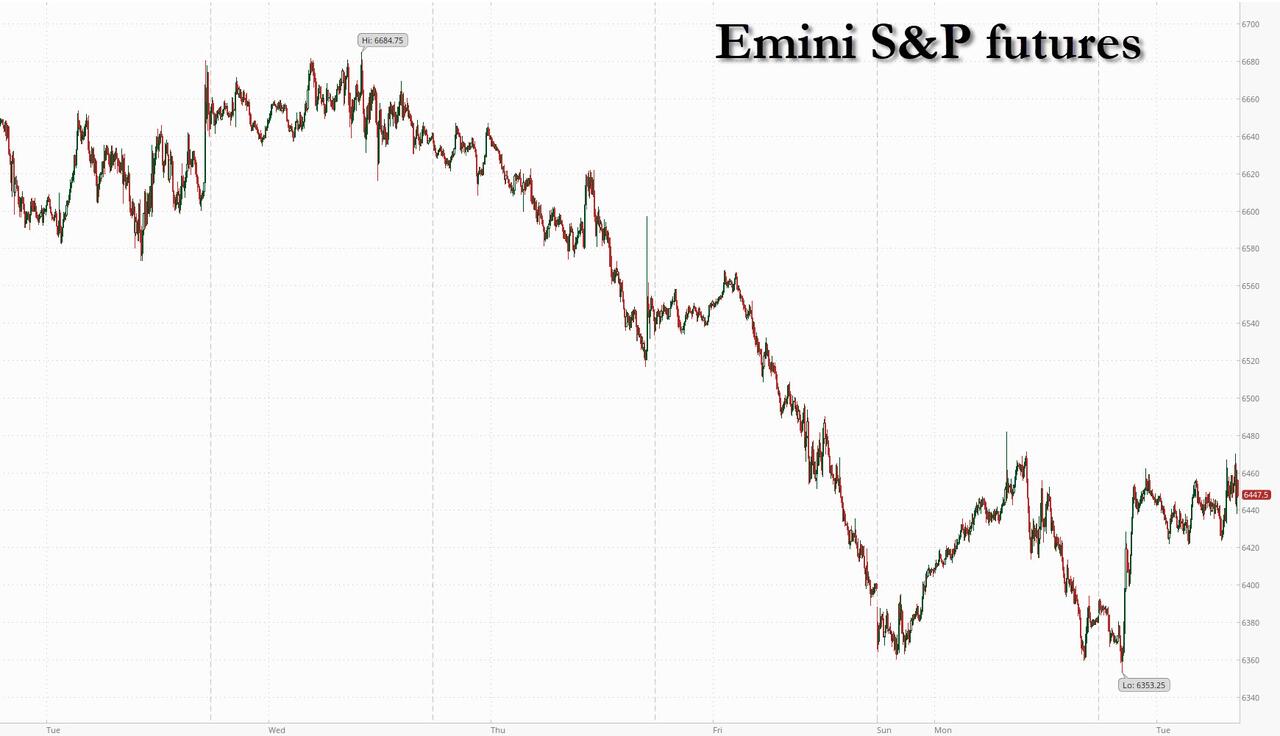

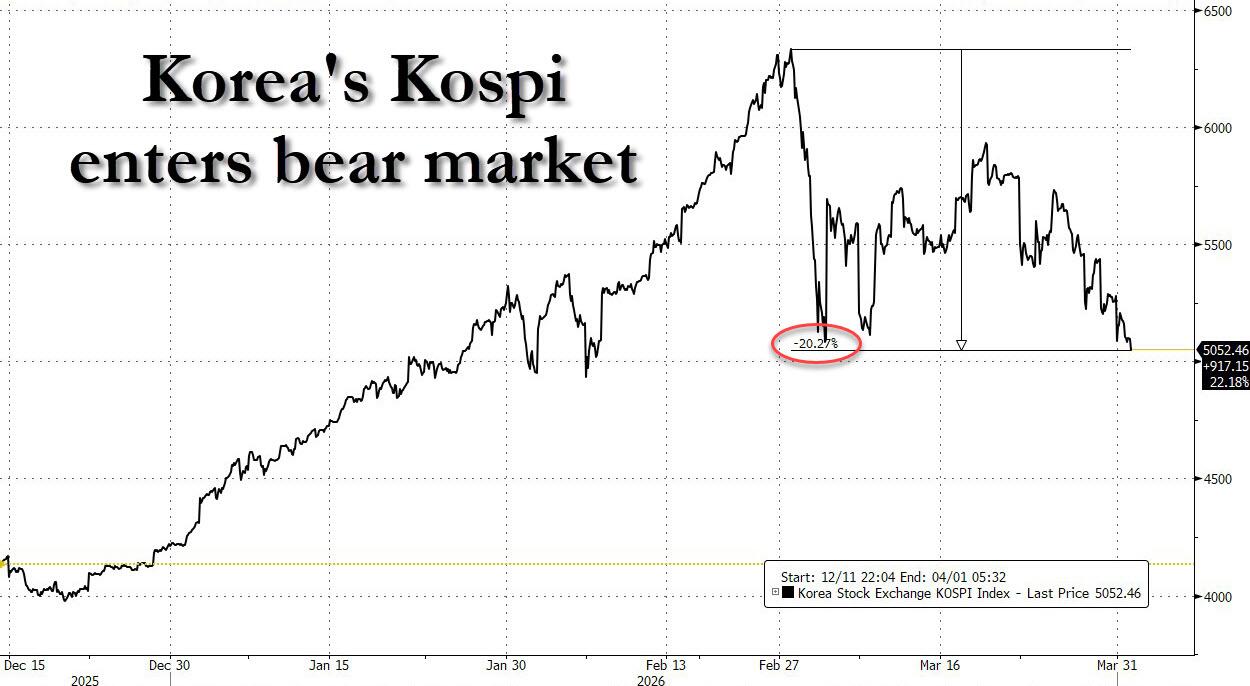

Futures Jump On Hopes Of War De-escalation, Korea Enters Bear Market On Memory Rout

Futures Jump On Hopes Of War De-escalation, Korea Enters Bear Market On Memory Rout

Futures are higher on a WSJ report that Trump is considering exiting the middle east conflict even if the Strait of Hormuz is not reopened; but the market is deciding whether this is a genuine intent to leave or another feint given the previous US attacks during negotiations and that Trump has yet to adjust his Apr 6 deadline. As of 8:00am, S&P futures are 1.1% higher, at session after approaching correction territory yesterday. Nasdaq futures rise 1%, with memory stocks lagging amid reports of DRAM prices plunging as much as 30%. In premarket trading, Mag7 names are higher as part of an ‘Everything Rally’ with bids to both Cyclicals and Defensives. In global markets, South Korea’s Kospi index slid 4.3%, entering a bear market as it extended its drop from a February high to 20%. SK Hynix Inc. slumped more than 7%. Bond yields are down 3-5bp, with the 10Y yield down to 4.30% after nearly hitting 4.50% two days ago; the Dollar is also lower. Commodities are mixed with crude/gasoline mixed (US avg price rises above $4/gal vs. $2.98 one month ago), after fading an earlier bounce, highlighting the paralysis created by the continually shifting White House statements. Precious metals are rallying as base metals are mixed, and Ags are bid. The macro data focus will be on JOLTS and Consumer Confidence.

In premarket trading, Mag 7 stocks are all green (Meta +1.5%, Microsoft +1.6%, Alphabet +1.4%, Amazon +1.5%, Apple +0.8%, Nvidia +1.3%, Tesla +1%)

Apellis Pharmaceuticals Inc. (APLS) soars 138% after Biogen Inc. agreed to acquire the company for $5.6 billion.

Centessa Pharmaceuticals (CNTA) rises 48% after Eli Lilly & Co. agreed to buy the sleep drug maker in a deal worth up to $7.8 billion.

FactSet Research Systems (FDS) gains 6% after the financial data company boosted its adjusted earnings-per-share forecast for the full year. It also reported adjusted EPS and revenue for the second quarter that beat expectations.

McCormick (MCK) rises 1.8% after Unilever said talks to sell most of its food business to the maker of spices are advanced. McCormick reported earnings on Tuesday and made no mention of the Unilever deal.

PepGen (PEPG) plunges 44% after the biotech gave clinical data from a mid-stage trial of its drug candidate for a type of muscle disease. Analysts say the data is mixed and Oppenheimer notes that the selloff might be overdone.

Phreesia (PHR) tumbles 23% after the healthcare software company lowered its full-year revenue forecast far below the analyst consensus. At least four brokerages downgraded their rating on the stock.

Scholar Rock (SRRK) rises 11% after the company resubmitted its biologics license application for apitegromab, a muscle-targeted therapy for children and adults with spinal muscular atrophy, to the US Food and Drug Administration.

T1 Energy (TE) falls 17% after the solar equipment manufacturer reported a wider than expected fourth-quarter loss per share and higher-than-expected expenses.

Stocks are bouncing in the final session of a brutal month as traders welcome a WSJ report that Trump may be willing to end the Iran war even without reopening the Strait of Hormuz (although subsequent comments by Trump suggest that this is merely the latest bluff). Signs of an increased desire for de-escalation from Trump may reduce anxiety over his threats to attack Iranian energy infrastructure. On the other hand, Tehran would be left in control of the key oil shipment chokepoint. Meanwhile, Iran hit a fully laden Kuwaiti oil tanker off Dubai in a drone attack.

Without a ceasefire or tangible progress in negotiations, the market will keep “fading the administration’s ‘everything is going well’ happy talk,” Vital Knowledge’s Adam Crisafulli wrote in a note. Carmignac Gestion’s Kevin Thozet observed that “Trump can’t simply turn an on/off switch on the crisis.” Other observers argue that rhetoric alone about a potential end to the conflict cannot create certainty for the market.

In a social media post, Trump said Iran has “essentially” been decimated and that allies should either buy jet fuel from the US or “take it” from the Strait of Hormuz. Still, an Iranian drone strike on a fully laden Kuwaiti oil tanker off Dubai emphasized the continuing danger. “One can’t exclude a swift resolution, but it won’t mean going back exactly to where we were in February,” said Kevin Thozet, a member of the investment committee at Carmignac. “Investors are seeing the glass half-full. During the past 15 years or so, buying the dip has been absolutely key.”

Trump has repeatedly swung between saying a deal with Iran is close and warning he’s prepared to escalate the US campaign. On Monday, he threatened to target Iran’s energy infrastructure and desalination plants if the strait stays shut. He earlier set Tehran an April 6 deadline to reopen the waterway. “There’s clearly some complacency across the market; there’s no capitulation whatsoever to be found in flows, fundamentals or through a technical analysis,” said Karen Georges, an equity fund manager at Ecofi in Paris. “Despite the rise today, I would say the market is reluctant to take a strong directional bet.”

Equities are, nonetheless, primed to rip higher on positive news about the war following large-scale unwinding of risk by hedge funds and CTAs. The concern is that, post an initial bounce, worries about the economy and the path for interest rates will trigger further volatility episodes, setting up stocks for months of roller-coaster conditions.

European stocks are also higher across the board in the wake of a WSJ report suggesting that US President Trump is willing to end the Iran war even if the Strait of Hormuz remains closed. The Stoxx 600 is set to end 1Q lower by just over 1% and down nearly 8% from February’s record high; mining and financial services stocks leading gains. Meanwhile, energy shares are the biggest laggards. Here are the biggest movers Tuesday:

Demant rises as much as 4.5%, the biggest gainer in the Stoxx 600 Health Care Index on Tuesday morning, after Danske Bank upgraded its rating on the stock to buy from hold

Unilever shares rise as much as 1%, trading only marginally higher than the May 2024 low reached last week, after the company confirmed discussions to sell most of its food business to McCormick

4iG shares rise as much as 15% after the Hungarian telecommunications and defense group says it is selling its 49% stake in Hirtenberger Defence to Czech peer CSG

Borregaard shares rise as much as 4.9% after an upgrade to buy from Kepler Cheuvreux, which makes a series of changes to its ratings to favor what it sees as the more resilient names in the European chemicals sector

Ashmore rose as much as 4.5% in London on Japan Post Insurance Co.’s plans to invest roughly $1 billion more in the British money manager’s emerging markets funds

Pets at Home shares gain as much as 5.2%, the most in two months, after the specialist retailer reported progress in turning around its Retail arm

Raspberry Pi shares rise as much as 30% after the maker of low-cost computers said revenues for 2026 are expected to be materially higher than current market expectations

Future slumps as much as 30%, to the lowest since October 2017, after what JPMorgan describes as a weak first-half trading update

Inventiva shares sink as much as 20% after the French biopharmaceutical company said it expected topline results of its late-stage clinical trial evaluating lanifibranor

Space is also making headlines this week, with Virgin Galactic soaring in late trading after it resumed some sales of commercial space flights. NASA is making final preparations for the Artemis II missions, while what a history-making SpaceX IPO could mean for the space economy is discussed in the Big Take podcast. In other corporate news, Unilever said talks to sell most of its food business to McCormick are advanced and a final deal could be announced later on Tuesday. Boeing will team up with Rheinmetall to offer drones known as the Ghost Bat to Germany’s military.

The Iran war’s impact on prices is beginning to show in economic data. The euro area saw its steepest jump in inflation since 2022 as the Iran war pushed energy costs sharply higher, reinforcing expectations that the European Central Bank will have to raise interest rates. Consumer prices rose 2.5% from a year ago in March – up from 1.9% the previous month and the highest since January 2025. Markets are pricing as many as three quarter-point hikes in the ECB’s deposit rate this year, from its current level of 2%.

“The March rise in inflation is likely the beginning of a sustained pickup,” wrote Bill Diviney, ABN Amro’s senior euro-zone economist. He expects the ECB to raise rates in April and June “in order to pre-empt any de-anchoring of inflation expectations.”

In Asia, a slump in chipmakers fueled stock losses after Monday’s rout in US-listed peers. South Korea’s Kospi index slid 4.3%, extending its drop from a February high to 20%. SK Hynix Inc. slumped more than 7%. US chipmakers such a Micron Technology Inc. and Sandisk Corp., meanwhile, underperformed in premarket trading.

In FX, the Bloomberg Dollar index falls. USD/JPY slips 0.2% to 159.37; Month-end flows make for choppy trading while hedge funds are rolling over short-term options exposure over the next week, Europe-based traders say. EUR/USD drops 2.9% this month, the most since July; it’s little changed on the day at 1.1469. AUD/USD rises as much as 0.3% to 0.6875 before paring gains; it’s up a fifth consecutive quarter, the longest winning streak since 2007.

In rates, treasury futures hold modest gains led belly sectors, with 5-year yields nearly 5bp richer on the day, outperforming European bonds. US session features several economic data points led by consumer confidence and JOLTS job openings, while Treasuries may receive support from month-end index rebalancing at 4pm New York time. US yields are at least 3bp richer across the curve with 5s30s spread wider by around 2bp as belly outperforms. 10-year, about 4bp lower near 4.31%, outperforms bunds and gilts. Continued belly outperformance trims 2s5s30s fly by nearly 3bp, adding to Monday’s 3.5bp drop. The below-expected euro-zone inflation data passed with little market reaction as traders await more evidence on the extent of the Iran war on price pressures.

In commodities, WTI crude oil futures have pared a 3.9% advance to multiyear high to about 0.4% and around $108 per barrel for the June contract following report that US President Trump is willing to end military operation in Iran even if Strait of Hormuz remains closed. Spot gold is up for a third session in a row, higher by 0.8%. Bitcoin is down 0.5% after a brief foray below $66,000.

US economic data calendar includes January FHFA house price index and S&P Cotality home prices (9am), March MNI Chicago PMI (9:45am, several minutes earlier for subscribers), March consumer confidence and February JOLTS job openings (10am) and March Dallas Fed services activity (10:30am). Fed speaker slate includes Goolsbee (12pm), Schmid (1:10pm), Barr (3pm) and Bowman (5:10pm)

Market Snapshot

S&P 500 mini +0.9%

Nasdaq 100 mini +0.8%

Russell 2000 mini +1.4%

Stoxx Europe 600 +0.7%

DAX +0.7%, CAC 40 +0.5%

10-year Treasury yield -3 basis points at 4.32%

VIX -1.7 points at 28.87

Bloomberg Dollar Index little changed at 1221.56

euro little changed at $1.147

WTI crude -0.9% at $101.92/barrel

Top Overnight News

US gasoline prices climbed above an average of $4 a gallon for the first time since August 2022, one of the most visible measures of consumer pain. BBG

President Trump told aides he’s willing to end the U.S. military campaign against Iran even if the Strait of Hormuz remains largely closed, administration officials said, likely extending Tehran’s firm grip on the waterway and leaving a complex operation to reopen it for a later date. WSJ

The IRGC announced that the Strait of Hormuz is fully under the control of its soldiers, and “the slightest movement of the enemies will be hit by missiles and drones”, adding that “the operation continues”, IRGC’s public relations channel reported.

Strait of Hormuz to be run by multinational coalition under White House plan, The Telegraph reported; Second proposal put forward by Pakistan and regional powers. Rubio stressed there would be “no fees, and free circulation” through the key shipping route, according to one interpretation of his intervention.

Houthis in Yemen are monitoring American movements at bases in the Horn of Africa that may signal an imminent American move in the Red Sea, according to Israeli Radio journalist. According to the Yemeni intelligence sources, Washington intends to create a maritime security zone in the Red Sea region and the base in Djibouti will become the center of command and control and rapid intervention. Yemeni officers said that there are American movements in order to bring the Red Sea and the Bab al-Mandab strait into the campaign.

Chinese suppliers say they’re raising prices for their goods because of the recent swings in oil prices resulting from the Iran war and closure of the Strait of Hormuz. A prolonged impasse in the critical waterway also raises the possibility of product shortages. CNBC

A gauge of activity in China’s sprawling manufacturing sector returned to expansion in March in part thanks to seasonal factors, but as the war in the Middle East raises supply shock risks, businesses are starting to feel the pressure. China saw manufacturing (50.4, up from 49 in Feb and ahead of the consensus forecast of 50.1) and non-manufacturing (50.1, up from 49.5 in Feb and ahead of the consensus forecast of 49.9). WSJ

Unilever is in advanced talks to combine its food unit with McCormick, in a deal that may include a $15.7 billion upfront cash component and McCormick shares. The agreement may be announced today. BBG

Euro-area inflation jumped the most since 2022 as the Iran war pushed energy costs sharply higher. It quickened to 2.5% this month, up from 1.9% the previous month. BBG

Iran is pushing the Houthis to prepare for a renewed campaign against Red Sea shipping, contingent upon any further escalation by the US in its war on the Islamic Republic. BBG

Eli Lilly To Acquire Centessa Pharmaceuticals For $38.00 In Cash Per Share Plus One Non-Transferrable Contingent Value Right. BBG

States are pushing ahead with their own AI regulations despite warnings from the White House to allow the federal government to set rules for the industry. NYT

A more detailed look at global markets courtesy of Newqsuawk

APAC stocks were mixed with some indecision seen amid fluctuations in oil and mixed geopolitical headlines, including US President Trump’s threats to obliterate Iran’s energy infrastructure if a deal is not made soon, although he was also reported to have told aides he is willing to end the military operation in Iran without reopening Hormuz. ASX 200 rallied with gains led by strength in tech, telecoms and financials, while there was little impact from the RBA minutes, which stated that board members agreed financial conditions needed to be restrictive and that a further tightening would likely be needed, but disagreed on whether to hike at the meeting. Furthermore, members agreed that it is not possible to predict the future path of the cash rate with any confidence, given the Middle East conflict. Nikkei 225 retreated at the open but is off lows amid mixed data and fluctuations in oil. Hang Seng and Shanghai Comp failed to sustain early gains and dipped into negative territory despite better-than-expected Chinese official PMI data, and with participants reflecting on a deluge of earnings releases.

Top Asian News

Chinese NBS Non-Manufacturing PMI (Mar) 50.1 vs. Exp. 49.9 (Prev. 49.5).

Chinese NBS General PMI (Mar) 50.5 vs. Exp. 50.2 (Prev. 49.5).

Chinese NBS Manufacturing PMI (Mar) 50.4 vs. Exp. 50 (Prev. 49.0, Low. 48.8, High. 50.5).

Japanese Tokyo CPI YoY (Mar) Y/Y 1.4% vs. Exp. 1.7% (Prev. 1.6%).

Japanese Tokyo Core CPI YoY (Mar) Y/Y 1.7% vs. Exp. 1.8% (Prev. 1.8%, Low. 1.6%, High. 2.1%).

Japanese Tokyo CPI Ex Fresh Food and Energy YoY (Mar) Y/Y 2.3% vs. Exp. 2.4% (Prev. 2.5%).

Japanese Retail Sales YoY (Feb) Y/Y -0.2% vs. Exp. 0.8% (Prev. 1.8%, Low. -1.1%, High. 1.3%).

Japanese Retail Sales MoM (Feb) M/M -2.0% vs. Exp. -0.9% (Prev. 4.1%).

European bourses (STOXX 600 +0.9%) continue to rebound, as the STOXX 600 bounces out of correction territory. The IBEX 35 and DAX 40 outperform, while the AEX is the slight laggard due to losses in ASML. European sectors are entirely in the green, ex. Energy. Basic Resources and Financial Services top the sector pile. While a rebound in metals prices supports Basic Resources, UBS is amongst the banks supporting financials after the FT reported that Swiss lawmakers have signalled some compromise on its USD 22bln capital plan.

Top European News

German institutes to cut 2026 economic growth forecasts amid the Iranian war, Reuters sources suggest; 2026 growth outlook seen at 0.6% (prev. 1.2%), 2027 growth seen at 0.9% (prev. 1.4%). CPI is seen at 2.8% for 2026 and 2027. Iranian war and energy costs were cited as the reasons for the cuts.

NOTABLE EUROPEAN DATA RECAP

FX

DXY lacks direction, and holds within a 100.30-100.64 range; the peak for today was made overnight, but then sank from these levels on reports via the WSJ, which suggested that US President Trump told aides he’s willing to end the war without reopening Hormuz. A factor which clearly indicates some early signs of easing tensions, though it raises concerns regarding the future governance of the Strait itself. DXY swung from peaks to troughs within an hour of the report, before then gradually pushing back towards the mid-point of the aforementioned range, as the European session got underway. Focus from a US standpoint now turns to US JOLTS, which are expected to ease to 6.87mln (from 6.946mln). A slew of Fed speakers are also on the docket, including Bowman, Barr, Goolsbee and Schmid.

G10s are mixed against the USD. GBP is the marginal outperformer, potentially benefiting from the lower energy prices, which somewhat alleviates growth-related concerns, at least for now. Sticking on the growth front, Final UK GDP growth in Q4 printed 1% Y/Y (exp. 1%, prev. 1.2%) – a report which spurred no move in Cable. To the bottom of the pile reside the CHF and Kiwi, albeit losses are incremental at this stage.

Elsewhere, EUR is steady, and was little moved to a resilient German jobs report, whilst a cooler-than-expected EZ inflation metric spurred some pressure in the single currency. In a bit more detail, headline Y/Y jumped to 2.5% (prev. 1.9%) and a touch beneath the consensus. As is the case across Europe, the surge in inflation has been attributed to the recent strength in energy prices; for reference, the core figure actually cooled from the prior to 2.3% (prev. 2.4%). EUR/USD fell to 1.1462 post-day before scaling back a touch. The ECB will welcome this report, given that it favours a “wait and see” approach.

JPY is flat this morning, after relative outperformance in the prior session, spurred by jawboning. USD/JPY currently resides within a 159.48-159.97 range, and towards the lower end of the prior day’s session. Overnight, the release of softer-than-expected Retail Sales and slower Tokyo inflation had a limited impact on the JPY – ING opines that the inflation figure will not “deter BoJ’s April hike”; analysts opine that the trifecta of 1) surging oil prices, 2) weak JPY and 3) rising Shunto wage growth, all play in favour of a near-term hike. Attention now turns to the Tankan survey on Wednesday, a report which policy members brought to focus at the last BoJ confab.

Fixed Income

Fixed income on a firmer footing as energy benchmarks initially pulled back, though WTI remains above USD 100/bbl, Brent above USD 105/bbl and Dutch TTF north of USD 50/MWh. The main update came via the WSJ, reporting that US President Trump told his aides that he is willing to end the conflict even without reopening the Strait of Hormuz. The move towards potentially ending the conflict has weighed on energy and, in turn, pressured yields. However, the uncertainty around Hormuz means the energy, and by association, price risks have not meaningfully diminished at this point.

USTs are firmer but off best levels, and within 110-22+ to 111-02 parameters. Ahead, the docket is headlined by Fed speak; however, the events/topics involved somewhat diminish the likelihood of pertinent updates.

Bunds follow global action. Initially stronger, before giving back some of the earlier gains heading into the EZ inflation measures for March – a report which encapsulates the early impact of the Iran war, and the surge in energy prices. In brief, headline Y/Y was cooler-than-expected, and plays in favour of the ECB’s “wait and see approach”. In reaction, Bunds ticked higher by a handful of ticks, though the move proved fleeting.

Gilts in-fitting with peers. Firmer by around 50 ticks at best but have given up around half of that and are below the 88.00 mark in 87.65-88.23 parameters. No reaction to the final Q4 GDP series, or a slight upward revision to the 2025 total.

Germany sells EUR 3.811bln vs exp. EUR 5.0bln 2.10% 2028 Schatz: b/c 1.5x (prev. 1.61x), average yield 2.62% (prev. 2.72%), retention 23.78% (prev. 22.6%).

BoJ said it plans to buy JPY 255bln of 1–3 year JGBs three times a month in April–June (prev. JPY 270bln, three times); JPY 230bln of 3–5 year JGBs three times a month (prev. JPY 245bln, three times). Plans to buy JPY 80bln of 10–25 year JGBs three times a month in April–June (prev. JPY 95bln, three times). Plans to buy JPY 75bln of JGBs 25+ years of maturity two times a month (prev. JPY 75bln, two times).

Commodities

Crude futures are incrementally firmer this morning after reversing earlier losses despite light newsflow. WTI May’26 resides in a USD 100.83-107.15/bbl range, whilst Brent June’26 holds within a USD 104.72-109.99/bbl. Worth noting that in recent trade benchmarks are moving a touch higher, extending further into the green.

Overnight, the complex dipped after the WSJ reported that US President Trump told aides he is willing to end the US military operation in Iran even if the Strait of Hormuz is not reopened. Do note the IRGC continues to provide hardline commentary, with attacks on Gulf countries ongoing. Geopolitics aside, some strength was seen in the crude complex after data showed that Oman’s crude OSP jumped USD 55.90/bbl.

Spot gold rose after comments from Fed Chair Powell and Williams indicated policy remains in a good place, helping to temper rate-hike expectations; the bullion climbed before paring gains to trade near USD 4,555/oz, with the yellow metal currently holding in a USD 4,482.66-4,619.25/oz range at the time of writing. Goldman Sachs said gold could reach USD 5,400/oz by year-end, citing low speculative positioning, expectations for two Fed rate cuts and ongoing central bank demand, with official-sector buying seen at around 60 tonnes per month.

Copper futures marginally benefitted from hopes of an earlier end to the Middle East conflict and after Chinese PMI data topped forecast, but then pared gains given the ongoing uncertainty in the Middle East conflict. 3M LME copper trades in a USD 12,122.00- 12,286.95/t range. Aluminium once again outperforms on the LME amid supply woes from the Middle East after Emirates Global Aluminium and Aluminium Bahrain were both targeted by Iran.

Oman’s crude OSP at USD 124.05/bbl for May (vs USD 68.15/bbl for April), +USD 55.90/bbl, GME data shows.

EU countries should prepare for prolonged disruption to energy markets from the Iran war, the EU energy commissioner said in a letter to EU energy ministers. Immediate impact on EU energy security of supply remains contained. EU countries should delay any non-emergency refinery maintenance. Countries should avoid measures that would increase fuel consumption or curb EU refinery output.

South Africa’s Finance Minister is considering lowering the fuel levy, with the decision to be announced on Tuesday, according to a Government official.

Libya’s National Oil Corporation said full production resumed at the Sharara and El Feel oilfields.

Guyana oil production averaged 915k BPD in January and 918k BPD in February.

Goldman Sachs expects gold to reach USD 5,400/oz by the end of 2026. Low speculative positioning and two Fed rate cuts to support this view. Projects around 60 tonnes of central bank buying per month.

Central Banks

Fed’s Williams (voter) said uncertainty around inflation path is ‘high’ but the economy has been more resilient than expected and the base outlook for the economy has been good. Tariffs and Iran war will push up headline inflation. Expects the unemployment rate to edge down this year and next. Economy facing ‘unusual set of circumstances’. Expects higher headline inflation near term on war and tariffs. War could both push up inflation, and depress growth. Inflation expectations consistent with 2% inflation. Expects US GDP to be 2.5% this year amid help from various factors. Expects inflation to end this year at 2.75%, and back to 2% in 2027. Economy has been resilient among changes. No signs of second round inflation impact from tariffs. Low hiring rate might be boosting economic pessimism. Job market sending out mixed signals.

ECB’s Muller said it is probable that rates will rise in the coming quarters, an April rate hike cannot be ruled out and reiterates that a hike may be needed if energy prices stay high.

ECB’s Panetta warns against second-round wage effects; says monetary policy is better positioned vs 2022.

RBA Minutes from March meeting stated that board members agreed financial conditions needed to be restrictive and that a further tightening would likely be needed but disagreed on whether to hike at the meeting. Agreed it is not possible to predict the future path of the cash rate with any confidence given the Middle East conflict. Rise in oil prices increased risk inflation would remain above target for a prolonged period. Oil prices around USD 100 would lift annual CPI inflation to around 5% in the June quarter. Rate hike could reduce the risk oil shock would flow into inflation expectations.

PBoC is to maintain moderately loose monetary policy with stronger counter-cyclical adjustments, reiterates to make use of various tools in monetary policy control and to maintain ample liquidity and keep CNY stable.

BoK Governor nominee Shin sees Middle East crisis as risk to the Korean economy and said inflationary pressure from extra budgets is limited, adds KRW liquidity is good and external factors affecting KRW have improved considerably.

Geopolitics

US President Trump tells aides he’s willing to end the war without reopening Hormuz, according to the Wall Street Journal.

The IRGC announced that the Strait of Hormuz is fully under the control of its soldiers, and “the slightest movement of the enemies will be hit by missiles and drones”, adding that “the operation continues”, IRGC’s public relations channel reported.

Strait of Hormuz to be run by multinational coalition under White House plan, The Telegraph reported; Second proposal put forward by Pakistan and regional powers. Rubio stressed there would be “no fees, and free circulation” through the key shipping route, according to one interpretation of his intervention.

Israeli PM Netanyahu said it is possible to bypass the Strait of Hormuz issue and that economic interests exist to ensure free flow of oil and gas, while ideas have been proposed for post-war transfer of energy from Persian Gulf to Mediterranean ports.

Israeli PM Netanyahu said Iran’s enriched uranium is Trump’s focus right now and US is leading military options to open Strait of Hormuz. Refuses to set any timeline on ending the Iran war.

Israel Military Spokesperson said “we are prepared to keep operating for weeks to come”.

Houthis in Yemen are monitoring American movements at bases in the Horn of Africa that may signal an imminent American move in the Red Sea, according to Israeli Radio journalist. According to the Yemeni intelligence sources, Washington intends to create a maritime security zone in the Red Sea region and the base in Djibouti will become the center of command and control and rapid intervention. Yemeni officers said that there are American movements in order to bring the Red Sea and the Bab al-Mandab strait into the campaign.

Iran’s Ministry of Foreign Affairs denied US President Trump’s assertions that Washington and Tehran were engaged in talks, according to WSJ.

One of Iran’s desalination plants on Qeshm Island is out of service since the strike and short-term repairs are deemed impossible, Borna reported citing a Health Ministry official.

US reportedly attacks large ammunition depot in Isfahan, Iran, according to WSJ.

Drone crashes in an open area at Iraq’s West Qurna 1 oilfield without exploding, state news reported.

Chinese Foreign Ministry said three Chinese ships recently sailed through the Strait of Hormuz.

Saudi Arabia intercepts 10 drones, Al Jazeera reported.

Power outage hits east of Tehran following explosions.

Explosions heard in Iraq’s Sulaymaniyah province and from US HQ in Baghdad’s Victoria base, according to Tasnim.

Italy denies the US use of its Sigonella naval air station, according to Italian press.

Russia’s Foreign Minister Lavrov says the Middle East crisis may spill over into a wider conflict.

US Event Calendar

9:00 am: Jan FHFA House Price Index MoM, est. 0.1%, prior 0.1%

9:45 am: Mar MNI Chicago PMI, est. 55, prior 57.7

10:00 am: Mar Conf. Board Consumer Confidence, est. 87.9, prior 91.2

10:00 am: Feb JOLTS Job Openings, est. 6890k, prior 6946k

12:00 pm: Fed’s Goolsbee Gives Opening Remarks at Eco Mobility Project

1:10 pm: Fed’s Schmid Speaks on Monetary Policy and Economic Outlook

3:00 pm: Fed’s Barr Discusses Stablecoin Regulation

5:10 pm: Fed’s Bowman Speaks on Small Business

DB’s Jim Reid concludes the overnight wrap

The market tone has become decidedly more positive overnight, with the driver being a Wall Street Journal report saying that President Trump had told aides he was willing to end the US military campaign against Iran, even if the Strait of Hormuz remained largely closed. So that’s raised hopes that the current phase of the conflict will wind down soon, and we’ve seen a clear market reaction in response. Most obviously, Brent crude oil futures have slipped back, coming down above $115/bbl before the article came out, to $113.04/bbl as we go to press. Moreover, equity and bond markets have rallied too, with S&P 500 futures up +0.80% this morning, whilst the 10yr Treasury yield is down another -2.4bps to 4.32%.

According to the WSJ article, Trump and his aides assessed that a mission to open the Strait of Hormuz would push the conflict beyond the four to six week timeline, and Trump had decided that the US should achieve its main goals of degrading Iran’s navy and missile stocks, and continue to pressure Iran diplomatically to resume trade flows. So even though the Strait of Hormuz wouldn’t return to normal in that scenario, markets still took the report positively, because it raised the perceived probability that the conflict might soon end, avoiding the more escalatory scenarios like further damage to energy infrastructure.

That said, the overnight newsflow hasn’t been entirely positive. Notably, oil prices had moved higher before the WSJ article, because Kuwait Petroleum Corp said that an oil tanker was attacked by Iran in a Dubai port. And in Asia, equity markets are down across the board, with losses for the KOSPI (-3.41%), the Nikkei (-1.16%), the Hang Seng (-0.51%), the CSI 300 (-0.58%) and the Shanghai Comp (-0.38%). That’s come despite a modest upside surprise in China’s official PMIs, with the manufacturing PMI at a one-year high of 50.4 (vs. 50.1 expected), whilst the non-manufacturing PMI rose to 50.1 (vs. 49.9 expected).

That overnight newsflow adds to the mixed signals markets have been getting over the last 24 hours. Indeed, Trump posted yesterday that if a deal weren’t reached shortly with Iran, and if the Strait of Hormuz weren’t opened, then the US would target “all of their Electric Generating Plants, Oil Wells and Kharg Island”. But in the same post, he also said that the US was “in serious discussions with a new, and more reasonable, regime to end our military operations in Iran”, which added to hopes for a negotiated settlement. So given there were signs pointing in both directions, markets were fairly steady in response. We also heard that Pakistan’s Foreign Minister will be visiting China today, after his meeting with officials from Egypt, Saudi Arabia and Turkey over the weekend, raising questions whether Beijing might play a role in guaranteeing any possible future ceasefire.

Given the competing headlines, Brent crude ended yesterday broadly flat, although it was still up +0.19% to $112.78/bbl, marking its highest closing level since July 2022. That came alongside a more pronounced rise for WTI (+3.25%), which also closed above $100/bbl for the first time since July 2022, at $102.88/bbl. Indeed, we’re now at the last day of Q1, and despite the overnight stabilisation in oil prices, Brent crude is on track for its biggest quarterly gain since Q3 1990 when the Gulf War began, having risen over +85% this quarter as it stands. So that outpaces the +81% bounce in Q2 2020, when oil prices recovered after more than halving in March 2020 as the pandemic moved into its most serious phase.

Otherwise, rates markets put in a decent performance yesterday, with investors turning their focus towards the dovish implications from a potential growth shock, rather than inflation. In addition, we heard from Fed Chair Powell, whose comments were interpreted dovishly, saying that inflation expectations were “well anchored beyond the short term”. So that eased fears that the Fed would rush to hike, and he also said that “policy is in a good place for us to wait and see”. Later on, we also heard similar comments from New York Fed President Williams who said “policy is well positioned” and that long-term inflation expectations were consistent with the Fed’s 2% goal.

That backdrop meant investors priced out the chance of central bank rate hikes this year. For example, Fed futures were expecting 3bps of rate cuts by December at the close, a change from much of last week when they were pricing in rate hikes this year. Meanwhile at the ECB, the number of hikes this year also fell from 76bps on Friday to 74bps by the close. So even though Brent crude was basically steady yesterday, the market tone became noticeably less hawkish.

With fewer rate hikes priced in, that also helped to bring yields down on both sides of the Atlantic. That was particularly clear for US Treasuries, where the 10yr yield (-8.0bps) saw its biggest decline since the start of the conflict, falling back to 4.35%. It was a similar story in Europe, where 10yr bund yields (-5.8bps) fell back from their post-2011 high to 3.03%, whilst 10yr OATs (-6.5bps) fell from their post-2009 high to 3.77%. Interestingly, there was also a marked decline in real yields, with the US 10yr real yield (-6.9bps) down to 2.04%. But even with yesterday’s rally, 10yr Treasury yields are still on course for their biggest monthly jump since 2024, with the 10yr yield up by +39bps since the end of February.

Despite the bond rally, equities had a more mixed session on Monday. European stocks outperformed, with the STOXX 600 (+0.94%), the FTSE 100 (+1.61%) and the DAX (+1.18%) all seeing solid gains. However, the market mood deteriorated after Europe went home and the S&P 500 ultimately closed -0.39% lower on the day, despite trading +0.92% at the open. So that left the S&P 500 within 1% of technical correction territory, down -9.10% from its late January peak. A large part of yesterday’s decline came due to a slump in chips stocks, with the Philadelphia Semiconductor Index down by -4.23%, even as most S&P 500 constituents closed higher on the day supported by lower nominal and real yields.

Otherwise yesterday, we did get a few data releases. In Germany, the flash CPI print moved up as expected in March, with the EU-harmonised measure rising to +2.8%, having been at +2.0% in February. We’ll get the Euro Area-wide print later this morning, so that’s one to keep an eye on for the ECB, particularly with pricing for a rate hike in the balance currently. Over in the US, we also had the Dallas Fed’s manufacturing index, which fell to -0.2 in March (vs. 2.0 expected).

Looking at the day ahead now, and data releases include the Euro Area flash CPI print for March, German unemployment for March, the US Conference Board’s consumer confidence indicator for March, the JOLTS job openings for February, and the FHFA house price index for January. From central banks, we’ll hear from the Fed’s Goolsbee, Barr and Bowman, and the ECB’s Panetta, Muller, Kazimir and Sleijpen.

Tyler Durden

Tue, 03/31/2026 – 08:41

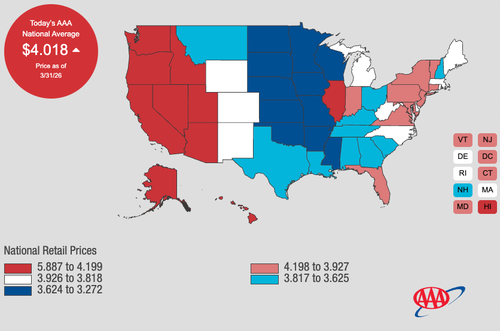

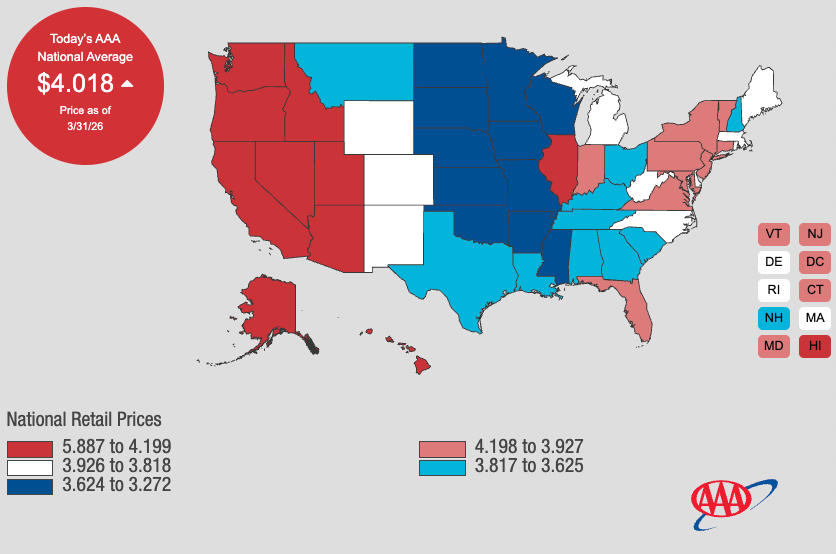

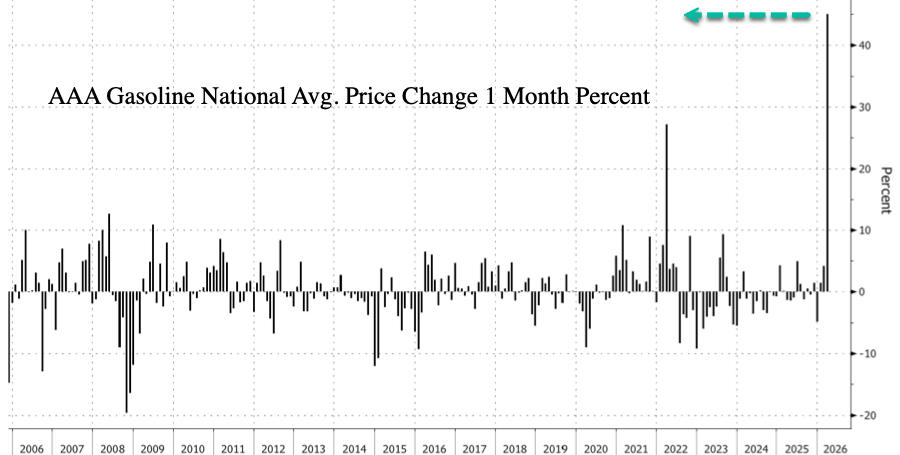

U.S. Gasoline Prices Hit Politically Sensitive $4 Level As Trump Eyes Iran War Off-Ramp

U.S. Gasoline Prices Hit Politically Sensitive $4 Level As Trump Eyes Iran War Off-Ramp

The overnight Wall Street Journal report that President Trump told aides he is willing to wind down the U.S. military campaign against Iran even if the Strait of Hormuz remains disrupted (and appeared to confirm this narrative in a social media post this morning) comes just as the national average gasoline price hit the politically sensitive $4-a-gallon threshold, underscoring the delicate balancing act the administration is facing in managing battlefield objectives and domestic fuel costs.

The latest AAA data shows gasoline prices nationwide topped $4 a gallon on Monday, a 35% increase for Regular 87 at the pump and the largest price shock on record dating back to 2004.

Regular 87 gasoline prices at the pump nationwide have returned to the price shock levels seen during the 2022 Russia-Ukraine crisis.

Largest monthly price shock on record.

Early last week, Bonnie Herzog, managing director and senior consumer analyst at Goldman Sachs, wrote in a note that when fuel prices spike to these “psychological threshold” levels, above $3 and approaching $4 a gallon, consumers tend to drive less and fill up their tanks less frequently.

“Historically, when retail gas prices increase (especially above the $3/gal psychological threshold, although that’s been rebased higher), consumers make the concerted decision to drive less, don’t always fill up their tanks (i.e., lower fill rates),” Herzog told clients.

But Herzog pointed back to history, noting that the real demand destruction for drivers comes when gasoline prices at the pump reach $5 a gallon.

She noted, “Further, we recognize that, in times of a significantly rising fuel-price environment, consumers may opt to trade down the fuel-price spectrum (i.e., from premium to regular).”

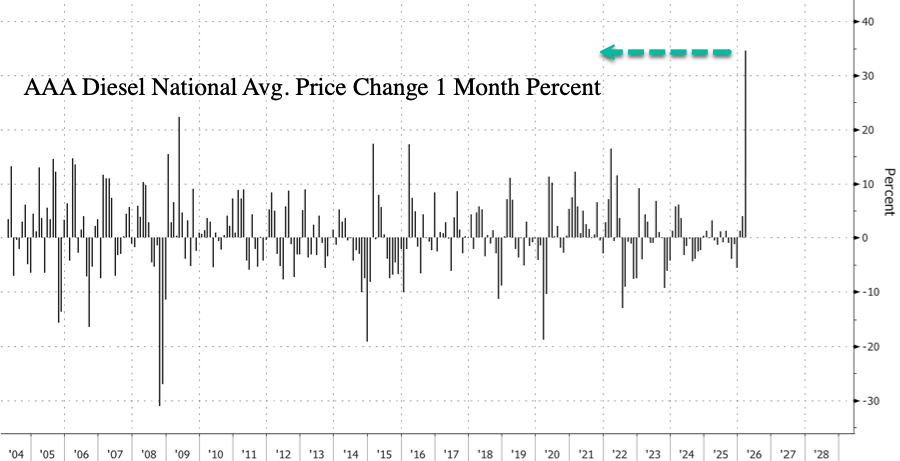

Furthermore, AAA data shows the national average diesel price has surged 45% this month to $5.45 per gallon. That marks the largest spike on record.

The price shock is already sending shockwaves through the real economy. Diesel powers the industrial backbone of the nation: trucking fleets, rail networks, shipping, farm equipment, construction machinery, backup generators, and broad segments of heavy logistics. When diesel prices spike this quickly, cost shock hits companies at the pump, with logistics firms passing fuel surcharges on to customers.

We warned readers on Monday about the unfolding “global demand destruction” and noted that the energy shock was already beginning to ripple outward from Asia.

Tyler Durden

Tue, 03/31/2026 – 08:20

Judge Reassigns Elon Musk Cases After Accusations Of Bias

Judge Reassigns Elon Musk Cases After Accusations Of Bias

Authored by Zachary Stieber via The Epoch Times,

A judge in Delaware on March 30 said she is reassigning cases involving Elon Musk after she was accused of being biased against him.

Delaware Court of Chancery Chancellor Kathaleen McCormick said in a letter to lawyers that she was taking the step because “disproportionate media attention surrounding a judge’s handling of an action is detrimental to the administration of justice.”

Attorneys representing Musk recently filed a motion for recusal or reassignment, pointing to how McCormick on LinkedIn had clicked that she supported a post that celebrated a 2026 ruling against Musk in California. The post, from a jury consultant, said “sorry, Elon,” and congratulated the legal firms that represented the plaintiff in the case as “standing up for the little guy against the richest man in the world.”

“Defendants cannot ignore the recent reaction by this Court to LinkedIn posts attacking Mr. Musk and his chosen counsel, regarding a case with overlapping factual allegations in the consolidated matter, and that bears directly on the appearance of impartiality in these actions,” Musk’s attorneys wrote in their motion.

McCormick had in 2024 ruled that a compensation package for Musk as CEO of Tesla agreed to by the Tesla board of directors was too large, a decision later overturned by the Delaware Supreme Court.

McCormick initially said that she did not click to support the LinkedIn post in question.

“I either did not click the ’support‘ icon at all, or I did so accidentally. I do not believe that I did it accidentally,” the judge wrote in a previous letter to lawyers.

“So, after learning of this issue last night, I logged into LinkedIn, searched for the post based on the screenshot, and tried to make sure that the support icon was not ’clicked on.’ I then reported the suspicious activity to LinkedIn.”

LinkedIn did not respond to a request for comment by time of publication.

The judge said she would review the motion, and on Monday agreed to reassign the cases.

However, McCormick maintained that she was not biased against Musk.

“The motion for recusal rests on a false premise—that I support a LinkedIn post about Mr. Musk, which I do not in fact support,” she wrote.

“I am not biased against the defendants in these actions. In fact, I dismissed a suit against Mr. Musk just last year.”

Lawyers for Musk declined to comment on the development. Musk had not appeared to remark on the reassignment on X, which he owns and on which he frequently posts.

* * * Give this a shot. Full refund if it doesn’t work.

Tyler Durden

Tue, 03/31/2026 – 08:05

https://www.zerohedge.com/political/judge-reassigns-elon-musk-cases-after-accusations-bias

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}