Category: News

Trump Signs Pipeline Permits To Boost US–Canada Oil Flow

Trump Signs Pipeline Permits To Boost US–Canada Oil Flow

Authored by Kimberley Hayek via The Epoch Times,

President Donald Trump issued several pipeline permits on April 15, including one for the construction of a new pipeline to facilitate the transportation of crude oil and petroleum products between the United States and Canada, according to documents released by the White House.

The action covers four permits in total. The permit authorizing construction was issued to the Bakken Pipeline Company LP for pipeline facilities in Burke County, North Dakota. Other permits were issued for the maintenance and operation of existing pipelines at border locations in North Dakota and Michigan. The recipients of those operational permits are “Enbridge Energy, Limited Partnership” and “Enbridge Pipelines (Southern Lights) L.L.C.”—both indirect subsidiaries of Canadian pipeline giant Enbridge Inc.

According to the White House documents, the permits cover transport of crude oil and petroleum products of every description—refined and unrefined—including naphtha, liquefied petroleum gas, natural gas liquids, jet fuel, gasoline, kerosene, and diesel. The permits explicitly exclude natural gas subject to the Natural Gas Act.

Wednesday’s permits reflect the administration’s sweeping effort to expand America’s domestic and cross-border energy infrastructure.

At the CERAWeek energy conference March 2025 in Houston, Energy Secretary Chris Wright had said that Trump’s pledge to lower energy costs by boosting oil and natural gas production would require a corresponding increase in infrastructure investment.

“If ‘Drill, baby, drill’ is to [lower energy costs], we’re going to have to ‘Build, baby, build,’” Wright told reporters.

The Enbridge permits issued Wednesday supersede authorizations dating to 1991, 1994, and 2008, effectively reissuing and consolidating federal approval under the current administration. The cross-border pipeline landscape has grown increasingly complex in recent years—there are more than 2.6 million miles of oil and gas pipelines crisscrossing the United States, with 71 networks spanning the border with Canada, meaning they are primarily regulated under federal law and by treaties between the two countries.

Enbridge has long been a central player in that network, though not without controversy: The company confirmed in late 2024 that it had cleaned up roughly 60 percent of a nearly 70,000-gallon oil spill from one of its lines in Wisconsin.

The U.S.–Canada energy relationship has also been shadowed by tariff tensions. Trump threatened to impose 25 percent tariffs on Canada over border security concerns, along with a reduced levy of 10 percent on Canadian oil and gas. Wednesday’s permits signal continued bilateral energy cooperation even as trade negotiations between the two countries remain active.

The permits arrive against a backdrop of years of pipeline battles between Washington and Ottawa.

Trump has pushed for the revival of the Keystone XL pipeline, which would transport crude oil from Canada to the United States.

“The company building the Keystone XL Pipeline that was viciously jettisoned by the incompetent Biden Administration should come back to America, and get it built—NOW!” Trump wrote on Truth Social in February 2025.

The Keystone XL project was ultimately suspended on Jan. 20, 2021, when then-President Joe Biden revoked its presidential permit, citing the need to “advance environmental justice.” Biden argued the project would “not serve the U.S. national interest” based on an analysis conducted under the Obama administration citing climate risk.

Canada has been eager to expand its access to U.S. markets. Calgary-based Enbridge Inc. has been in talks with customers about expanding its Mainline pipeline network—the largest pipeline system in North America—to handle growing volumes of Canadian oil output. Canada currently sends 97 percent of its oil exports and 100 percent of its natural gas exports to the United States, leaving it with limited leverage in any trade dispute.

Wednesday’s permits are the latest step in Trump’s strategy to make North America self-sufficient in energy and a dominant exporter.

Tyler Durden

Thu, 04/16/2026 – 11:05

https://www.zerohedge.com/energy/trump-signs-pipeline-permits-boost-us-canada-oil-flow

Can You Price In No Longer Pricing Things In?

Can You Price In No Longer Pricing Things In?

By Michael Every of Rabobank

At this point it isn’t a random walk but a determined march: markets have decided the Iran war and the Hormuz blockades are over, and everything is going to be better than normal imminently: the Nasdaq and S&P are at all-time highs and even worries over private credit are receding. In the real world, there are signs that back that stance and ones that say otherwise.

Iran warned it could sink US ships in Hormuz if they police the waterway and the Houthis could blockade the Red Sea. The FT reports Iran used a Chinese spy satellite to target US bases. Note the subtext to Trump’s subsequent Truth Social post: “China is very happy that I am permanently opening the Strait of Hormuz. I am doing it for them, also – And the World. This situation will never happen again. They have agreed not to send weapons to Iran. President Xi will give me a big, fat, hug when I get there in a few weeks. We are working together smartly, and very well! Doesn’t that beat fighting??? BUT REMEMBER, we are very good at fighting, if we have to – far better than anyone else!!!”

Yet the US and Iran are reportedly weighing a two-week truce extension and inching towards a framework deal, as the latter feels the economic pressure; crucially, China is seen pressing Iran to open Hormuz; and Tehran has offered a proposal allowing ships to exit the Oman side of the Strait free of attack, if a wider deal with the US can be struck. That looks like the face-saving way for the regime to re-open the Strait… if there can be a “grand bargain” on the nuclear issue, missiles, and its regional proxies. Matching that trend, Israel is close to a one-week ceasefire with Hezbollah in Lebanon, even if there is no clear way to rid the country of the terror group despite the Israeli and Lebanese authorities now seeming united in wanting to do so.

Potentially, we could still see this war end in line with what has been our base case for a while now: a broad –if naturally disputed– US win vs Iran by the second to third week of April, giving it de facto control of a new Middle East (or, less likely, a belated TACO). Yet the downside is longer blockades, with tail risks of any new escalation deepening and/or widening the war. The latter scenario might only be priced into the physical market, not the oil futures markets.

Meanwhile, the US Beige Book noted “The conflict in the Middle East was cited as a major source of uncertainty that complicated decision-making around hiring, pricing, and capital investment, with many firms adopting a wait-and-see posture… Many Districts continued to report signs of consumer financial strain, increased price sensitivity, and rising demand at food banks and other social service organizations, while spending among higher-income consumers was resilient… several Districts reported that rising crop prices helped offset steep price increases of fertilizer and fuel.”

Australia needs more energy imports as a fire rages at one of its two oil refineries, the latest in a series of such accidents at the few western facilities still operating. An accident, sabotage, or just the result of over-working the facility in a crisis? Regardless, the founder of Ivanhoe Mines states that: “The Australian mining industry is now on the verge of collapse due to diesel shortages… the fuel supply chain that powers every drill, truck, and haul is about to snap.” Who drove that decline in refineries, one may ask? Markets and their uncanny ability to ‘price things in.’

China’s Canton Fair is clouded by higher costs hitting its exporters due to the Iran war.

Brussels warned EU countries not to hoard fuel within their borders weeks after telling everyone there was no risk of an energy crisis. Reportedly, the European Commission also wants to see fossil fuels taxed higher than electricity to drive the EU towards renewable energy in the long term – as member states are doing the opposite in the face of this crisis so far; and, from a broader geopolitical perspective, as we see the warning that ‘Fuel scarcity is European armies’ ‘Achilles’ heel.’ No military, and no mine, currently runs on electricity.

But let’s look to the ‘all-time highs’ post-war period and see if that’s really priced in or not.

Lots of scores will be settled in lots of places. As just one example of many, Trump has warned that the US-UK trade deal “can always be changed” with bilateral relations in a “sad state” after Britain was “not there when we needed them” on Iran.

There will be major structural shifts. For example, the IMF warns the war threatens to turbocharge a looming government debt crisis. The longer the blockade goes on, the more this is true. Defence spending is going to soar even higher even faster in even more places.

Specifically, the US is pushing for a staggering $1.5 trillion defense budget, up nearly 50%, and it’s using Iran and the ‘China threat’ to convince Congress to spend (read: borrow) much more. Very significantly, the Pentagon has also approached US automakers and manufacturers to ask if they can boost weapons production, e.g., GM or Ford shifting capacity from civilian to military. I’ve long argued neo-mercantilism and the US WW2 heuristic underlined ‘resilience’ requires a broad manufacturing base that can be adapted for military purposes in a crisis; that requires commodities and energy; and, in the face of others’ neo-mercantilism, it also means tariffs, subsidies, price controls, and a stronger state hand.

Indeed, alongside the farcical disconnect between the oil screen price –where investigations are underway into potential insider trading before Trump policy pivots– and the physical price of a barrel, that Pentagon request is a clear ‘Reverse Perestroika’: a shift from markets and consumption to state-led military-industrial production, which requires other key components to succeed, including the Fed.

Notably, Trump is refusing to allow to halt the criminal probe of Fed Chair Powell –the DOJ made a surprise visit to the Fed’s under-renovation headquarters, where they were turned away: a blockade?– while threatening to fire him if he won’t step down from the FOMC when his term ends on May 15. Powell says he won’t step down from the Committee until Warsh is appointed as Chair by the Senate; the Senate won’t appoint Warsh until the criminal prosecution of Powell is dropped. Does somebody need both sides to go to Pakistan to sort this out? But seriously, explain the logic of the Fed remaining untouched while epic shifts in geopolitics and political economy are underway; and do it without saying, “because markets.”

On which note, New York Mayor Mamdani also announced ‘Happy Tax Day’ aimed at raising $500m by taxing billionaires’ pied-a-terres in Manhattan: how much are their equivalents in Miami, one wonders?

Happy Tax Day, New York. We’re taxing the rich. pic.twitter.com/Wky2LFXC9W

— Mayor Zohran Kwame Mamdani (@NYCMayor) April 15, 2026

Pulling this all together, it’s not just that the market has priced in only one possible geopolitical scenario ahead: it’s not pricing that geopolitics suggests a future when things aren’t priced in as the norm. At which point, what are markets for? Try answering that without answering what GDP is for.

I conclude by noting that a social media meme going round yesterday had two dinosaurs looking at a huge meteor approaching to impact the earth. The first says, “That doesn’t look good for us.” The second replies, “Don’t worry, it’s priced in.”

Tyler Durden

Thu, 04/16/2026 – 10:25

https://www.zerohedge.com/markets/can-you-price-no-longer-pricing-things

Former Virginia Lt. Gov. Justin Fairfax And Wife Found Dead In Apparent Murder-Suicide

Former Virginia Lt. Gov. Justin Fairfax And Wife Found Dead In Apparent Murder-Suicide

Justin Fairfax, the former lieutenant governor of Virginia, and his wife, Cerina Fairfax, a dentist, were found dead in an apparent murder-suicide at their home shortly after midnight on Thursday, according to Fairfax County police.

Fairfax, 47, shot and killed his wife before turning the gun on himself, Police Chief Kevin Davis said. The couple’s teenage children were home at the time of the shootings.

Davis described the deaths as the result of an “ongoing domestic dispute surrounding a complicated or messy divorce.” Court records show that the Fairfaxes had been engaged in divorce proceedings this year.

Fairfax, a Democrat, served as Virginia’s lieutenant governor from 2018 to 2022 after winning election in 2017 alongside Gov. Ralph Northam. He largely remained out of the spotlight until 2019, when a series of scandals engulfed the state’s Democratic leadership.

The crisis began when old medical school yearbook photos surfaced appearing to show Governor Northam in blackface. As calls mounted for Northam’s resignation, two women came forward to accuse Mr. Fairfax, who would have been next in line for the governorship, of sexual assault. One alleged the assault occurred in 2000 at Duke University; the other said it took place in 2004 at the Democratic National Convention, the NY Times reports.

Fairfax denied both allegations – but the accusations effectively stalled momentum to force Northam from office. The situation grew more chaotic when the state attorney general, the third-ranking Democrat in Virginia’s executive branch, admitted he too had worn blackface as a college student. All three men ultimately served out their full terms.

Insisting he had done nothing wrong, Fairfax launched a bid for governor in the 2021 Democratic primary. In one televised debate, he accused his rival, former Gov. Terry McAuliffe, of “treating me like Emmett Till” for calling on him to resign over the sexual assault allegations.

With minimal institutional support and limited fundraising, Fairfax finished fourth in the primary, receiving just 3.6 percent of the vote. Mr. McAuliffe won the nomination but lost the general election to Republican Glenn Youngkin.

You’re never going to believe what happened next. https://t.co/pvwGEeQald

— Stephen L. Miller (@redsteeze) April 16, 2026

Fairfax had kept a low public profile since leaving office. Thursday’s tragedy marks a grim end to a once-promising political career that was repeatedly overshadowed by scandal and personal turmoil.

Tyler Durden

Thu, 04/16/2026 – 10:05

DOJ Petitions Court To Toss Convictions Of Unpardoned Jan. 6 Defendants

DOJ Petitions Court To Toss Convictions Of Unpardoned Jan. 6 Defendants

Authored by Janice Hisle via The Epoch Times,

The Justice Department is petitioning an appeals court to throw out the convictions of unpardoned defendants who were charged in connection with the U.S. Capitol breach on Jan. 6, 2021.

“The United States has determined … that dismissal of this criminal case is in the interests of justice,” read a motion filed April 14 in the case of Elmer Stewart Rhodes III, Kelly Meggs, Kenneth Harrelson, and Jessica Watkins.

All four defendants belonged to the Oath Keepers, a group that says its members are mostly former military, police, and medics who are dedicated to upholding Constitutional rights. Rhodes, the group’s founder, had been one of the most high-profile Jan. 6 defendants; he was sentenced to 18 years in prison for seditious conspiracy and other charges.

In their motion filed in the U.S. District Court for the District of Columbia, federal prosecutors said they would file separate motions-to-vacate in “similar” Jan. 6 cases.

Those cases involve four other Oath Keepers—Roberto Minuta, Edward Vallejo, David Moerschel, and Joseph Hackett—along with Proud Boys members Ethan Nordean, Joseph Biggs, Zachary Rehl, and Dominic Pezzola.

The Proud Boys group has said it is open to men who are “gay or straight,” and of all races and religions who support Western values that created the modern world.

After being sworn in as the 47th president in 2025, President Donald Trump granted full pardons to about 1,500 people who faced Jan. 6 charges.

However, he stopped short of pardoning 14 defendants who were Oath Keepers and Proud Boys.

He instead commuted their sentences, leaving their convictions still standing.

Cases involving 12 of those defendants are part of the motion that U.S. Attorney Jeanine Pirro signed on April 14.

The remaining two defendants who had not received pardons include Oath Keeper associate Thomas Caldwell, who received a delayed presidential pardon in March 2025. The other is former Proud Boy Jeremy Bertino, who admitted guilt and served as a prosecution witness against other Proud Boys.

If the Washington appeals court vacates the convictions as requested, prosecutors then would move to dismiss the cases “with prejudice,” Pirro wrote.

That specification would permanently bar prosecutors from refiling the charges.

Since 1977, the U.S. Supreme Court has “recognized that appellate courts have authority” to take the action Pirro has requested, the filing said.

Some members of the Oath Keepers and Proud Boys did receive pardons, including former Proud Boys national chairman Henry “Enrique” Tarrio. He had been convicted of seditious conspiracy and other charges that brought a 22-year sentence—the longest meted out to any Jan. 6 defendant.

Last year, Tarrio, Biggs, Rehl, Nordean, and Pezzola filed a $100 million civil lawsuit against the federal government, alleging prosecutors violated their constitutional rights.

Nicholas Smith, an attorney who represents Nordean, expressed gratitude to the Justice Department for its “wise decision” in seeking dismissal of the convictions.

“We don’t want a precedent that says that any physical confrontation between protesters and law enforcement means a crime akin to treason, such as seditious conspiracy,” Smith said.

However, former Metropolitan Police Officer Michael Fanone, who suffered a heart attack after a rioter shocked him with a stun gun on Jan. 6, spoke out against the Justice Department’s motion to throw out the convictions.

“I would remind Americans that these were traitors to this country,” Fanone said. “They planned, incited, and carried out an insurrection.”

In a post on X, John Strand, a Jan. 6 defendant and conservative activist, said the government’s move constituted “exoneration” for defendants who were “entrapped and crushed by an evil, weaponized government.”

Tyler Durden

Thu, 04/16/2026 – 09:45

https://www.zerohedge.com/political/doj-petitions-court-toss-convictions-unpardoned-jan-6-defendants

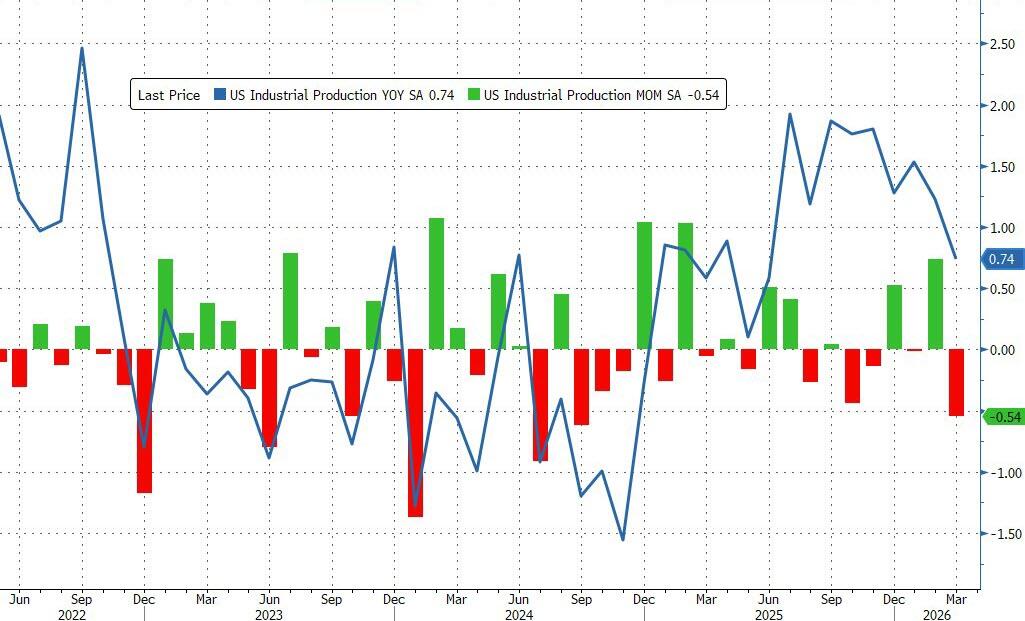

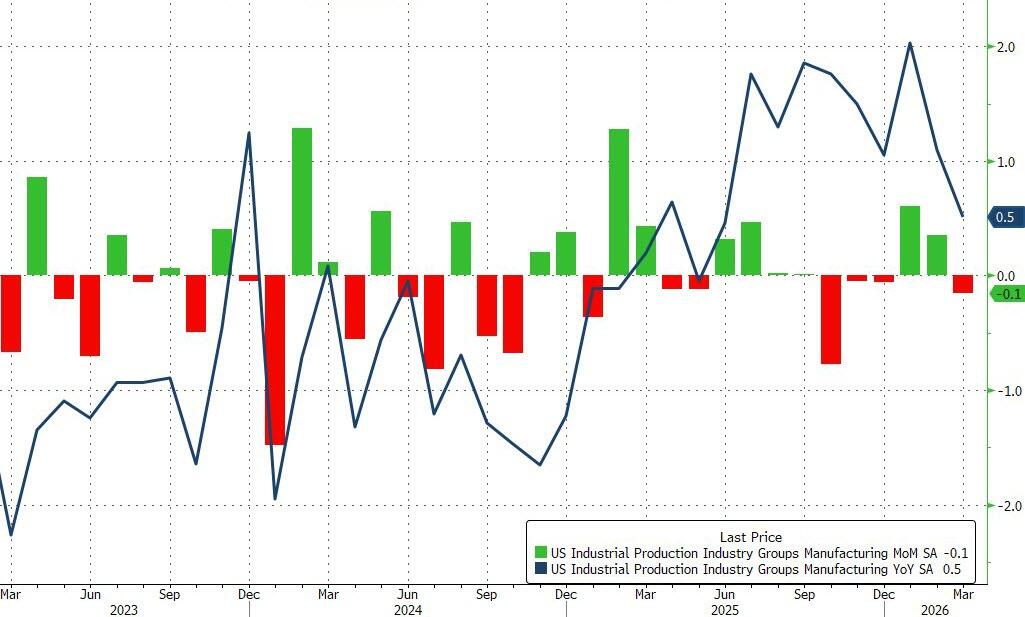

US Industrial Production Unexpectedly Drops In March (After Huge Upward Revision For Feb)

US Industrial Production Unexpectedly Drops In March (After Huge Upward Revision For Feb)

At first glance the 0.5% MoM decline in US Industrial production (considerably worse than than the 0.1% MoM rise expected – and dragging YoY growth in IP down to +0.74%) is bad news… suggesting immediate impacts from the war are being felt and sparking headlines decrying President Trump’s actions.

Source: Bloomberg

However, while we agree that the decline is notable, the fact that February’s data was revised drastically higher, from +0.2% to +0.7% MoM, means that over the two months, industrial production overall is actually higher (and up 0.2% since the end of the war)…

Source: Bloomberg

Energy was behind the slowdown:

March oil and gas drilling posted a decline of 2.4% m/m after rising 0.6% in Feb., Federal Reserve data show.

March consumer energy products was decline of 2.1% m/m after rising 2.3% in Feb.

March commercial energy products declined 0.3% m/m after increasing 0.8% in Feb.

A similar picture evolves for Manufacturing production which fell 0.1% MoM in March (worse than the 0.1% MoM rise expected) after February’s 0.2% MoM rise was revised up 2x to a 0.4% MoM rise. Nevertheless, Manufacturing production YoY slowed to just 0.5%…

Source: Bloomberg

Bottom Line: it’s not great news that industrial production is slowing… but it’s not as dire as it looks at first glance (and remember Manufacturing PMIs were strong)…

…and energy production is unpredictable at best in the current environment.

Tyler Durden

Thu, 04/16/2026 – 09:35

Sotomayor Apologizes After Criticizing Kavanaugh Over Immigration Case

Sotomayor Apologizes After Criticizing Kavanaugh Over Immigration Case

Authored by Tom Gantert via The Epoch Times,

U.S. Supreme Court Associate Justice Sonia Sotomayor apologized in a statement for comments she recently made about Associate Justice Brett Kavanaugh.

“At a recent appearance at the University of Kansas School of Law, I referred to a disagreement with one of my colleagues in a prior case, but I made remarks that were inappropriate,” Sotomayor said in the statement released by the Supreme Court.

“I regret my hurtful comments. I have apologized to my colleague.”

Sotomayor was at an event April 7 at the University of Kansas School of Law when she criticized Kavanaugh over his stance involving U.S. Immigration and Customs Enforcement agents stopping individuals to question them about their immigration status.

Her remarks appeared to reference the Supreme Court’s Sept. 8, 2025, emergency order in Noem v. Vasquez Perdomo, which allowed immigration enforcement to continue while legal challenges proceed.

The Supreme Court issued a temporary order allowing the practice to continue while the case moves through the courts.

In a concurring opinion, Brett Kavanaugh wrote that such encounters are typically brief and that individuals are generally released quickly.

“I had a colleague in that case who wrote, you know, these are only temporary stops,” Sotomayor said, referencing Kavanaugh, according to Bloomberg.

“This is from a man whose parents were professionals. And probably doesn’t really know any person who works by the hour.”

Kavanaugh’s parents were Martha Kavanaugh, an associate judge in Maryland, and Everett Kavanaugh Jr., a Washington lobbyist.

Sotomayor’s parents were Juan Sotomayor, a tool worker with a third-grade education, and Celina Baez, a nurse.

Jonathan Turley, a law professor at George Washington University Law School, said Sotomayor’s criticism of Kavanaugh suggested “that he is an out-of-touch elitist.”

“The suggestion is that Kavanaugh has avoided—and continues to avoid—interactions with people who get paid on an hourly basis—while she is more inclusive in her circle of friends. It is obviously false, but more importantly, petty and unfair,” Turley posted April 12 on X.

David French, a former attorney and columnist for The New York Times, said Sotomayor’s comments were “inappropriate.”

“This gets a little personal feeling to me,” French said on The Dispatch podcast on April 14.

“Maybe they know each other well enough to where she can make assumptions or make educated guesses about what his parents experienced or their broader experience. I don’t know. To me, it’s not even a close call. It was over the line in its personal nature.”

The Epoch Times reached out to Sotomayor and Kavanaugh for comment.

Tyler Durden

Thu, 04/16/2026 – 09:10

Hegseth: Hormuz Blockade Stays “As Long As It Takes” – Ships Now Fair Game For Search & Seizure

Hegseth: Hormuz Blockade Stays “As Long As It Takes” – Ships Now Fair Game For Search & Seizure

Summary

US Navy: vessels seeking entry into Hormuz Strait now fair game for boarding, search, and outright seizure – including for suspicion of ‘contraband’.

Hegseth: US forces are ready to restart combat if Iran doesn’t agree to a deal & strait blockade to continue for as long as it takes. Already 13 ships have been turned around.

Iran’s parliament speaker Mohammad Bagher Qalibaf calls ceasefire in Lebanon “as important as a ceasefire in Iran.”

Heavy Israeli bombardment of southern Lebanon, including targeting of infrastructure and bridges.

Trump announces end of military operations against Iran by May 31st?

Yes 70% · No 31%

View full market & trade on Polymarket

* * *

Boarding, Search, & Outright Seizure

Ships seeking to enter the Hormuz Strait already sanctioned by the US just got a lot more vulnerable: under Washington’s blockade of Iranian ports, they’re now fair game for boarding, search, and outright seizure, per US Naval Forces Central Command.

“In addition to enforcing the blockade, all Iranian vessels, vessels with active OFAC sanctions, and vessels suspected of carrying contraband, are subject to belligerent right to visit and search,” the notice said, referring to the Office of Foreign Assets Control. “These vessels, regardless of location, are subject to visit, board, search, and seizure.”

The definition of “contraband” is broad and expansive. It spans weapons, ammunition, combat aircraft, and military electronics, WSJ has described. “Petroleum products and lubricants are conditional contraband due to their essential role in military operations and their contribution to Iran’s war-sustaining economy,” the advisory also said. “Contraband is defined as goods that are destined for an enemy and that may be susceptible to use in armed conflict.”

Up until now, the blockade – initially rolled out Monday – was limited to ships moving in and out of Iranian ports, but the definition who can be targeted just widened. Meanwhile, US Central Command (CENTCOM) said Wednesday that in the first 48 hours, not a single ship made it past the blockade.

Hormuz Blockade: ‘As Long As It Takes’

The US will maintain a naval blockade of Iran for as long as it takes, Pentagon chief Pete Hegseth has stated in a press briefing Thursday. He and Joint Chiefs Chairman Gen. Dan Caine say that US forces are ready to resume major combat operations at a moment’s notice, which suggests the initial two-week ceasefire could get extended, as was widely reported the day prior. But this also suggests that Washington likely has no appetite for resuming major aerial operations directly against Iran anytime soon.

On the question of resumption of major combat operations, Hegseth warned: “To Iran, choose wisely. I pray you choose a deal which is within your grasp for the betterment of your people and the betterment of the world.” He followed with, “In the meantime, the War Department is locked and loaded.” Additional main highlights to the Hegseth/Caine update and presser:

Iran likes to say it controls Strait of Hormuz but it has no navy

Energy industry not destroyed ‘yet’, US blockade shutting down exports

For as long as it takes, we will maintain blockade

Launching operation ‘economic fury’

Iran is digging out bombed out launchers

I hope you choose a deal which is within your grasp

But again, the chief takeaway is that the Pentagon and Trump administration are making clear that US forces are ready to restart combat if Iran doesn’t agree to a deal. On that front, US officials say future talks are likely to be held again in Pakistan’s capital, Islamabad. Prior reports have indicated both sides have “agreed in principle” to engage in another round of talks.

Iran’s PressTV touting ability to inflict global economic pain…

International Monetary Fund’s chief economist says that growth is expected to slow this year amid repercussions from the war against Iran and disruptions to global oil and gas trade.

Follow Press TV on Telegram: https://t.co/LWoNSpkc2J pic.twitter.com/ZAty9htTov

— Press TV 🔻 (@PressTV) April 15, 2026

Pentagon: 13 Ships Turned Around

Since the blockade went live, US forces have already turned around 13 ships, according to Gen. Caine in the same briefing. He underscored how far this reach extends, saying operations will take place “inside Iran’s territorial seas and in international waters.”

Officially, the Pentagon claims the blockade is limited – targeting Iran’s ports and coastal areas while sparing vessels simply passing through the Strait of Hormuz. In practice, however, the net is touted as much wider, as US forces “will actively pursue any Iranian-flagged vessel or any vessel attempting to provide material support to Iran,” including so-called “dark fleet vessels carrying Iranian oil,” Caine added.

He confirmed that more than 10,000 service members are now involved in the blockade, but with more US servicemembers en route to the region.

Lebanon Still Bombed Heavily by Israel amid US Ceasefire Efforts

Israeli jets pounded Nabatiyeh in southern Lebanon Thursday, unleashing one of the heaviest barrages there since the war began and sending black smoke billowing over the region. Strikes hit near the industrial zone and a supermarket on Nabih Berri Avenue, with nearby suburbs also taking damage, according to Lebanon’s state-run National News Agency.

Iran has signaled urgency on de-escalation, with parliament speaker Mohammad Bagher Qalibaf calling ceasefire in Lebanon “as important as a ceasefire in Iran.” He described, “In the Islamabad negotiations and afterwards, we have been seriously pursuing efforts to compel the adversaries to establish a permanent ceasefire in all areas of conflict.” Pakistan’s army chief is in Tehran mediating between Washington and Tehran.

⚡#BREAKING Lebanese President Joseph Aoun said in a conversation with US Secretary of State Marco: “I am not willing to talk to Netanyahu”

— War Monitor (@WarMonitors) April 16, 2026

Lebanon’s leadership is in th emeantime framing any truce as a gateway to talks, despite Hezbollah having rejected direct talks with Israel. The ceasefire it is “demanding with Israel” would be a “natural entry point for direct negotiations,” President Aoun said, adding: “Lebanon is keen to halt the escalation… so that the targeting of the innocents ceases, and the destruction of homes” stops.

Destruction of Al-Qasimia Bridge in Southern Lebanon

جسر القاسمية pic.twitter.com/u39LVosxnF

— Lebanon 24 (@Lebanon24) April 16, 2026

He stressed negotiations “are to be undertaken by the Lebanese authorities alone,” and said “the withdrawal of Israeli forces… is an essential step,” alongside redeploying the army “up to the international borders” to “end any manifestation of armed presence.”

And yet Israeli strikes are now hitting infrastructure. A key bridge over the Litani River near Qasmiyeh – linking Tyre and Sidon – was reportedly destroyed, though Israel said it only “struck adjacent to it.” The broader campaign is cutting off southern Lebanon, targeting chiefly Hezbollah positions, Israeli officials have claimed.

Tyler Durden

Thu, 04/16/2026 – 08:55

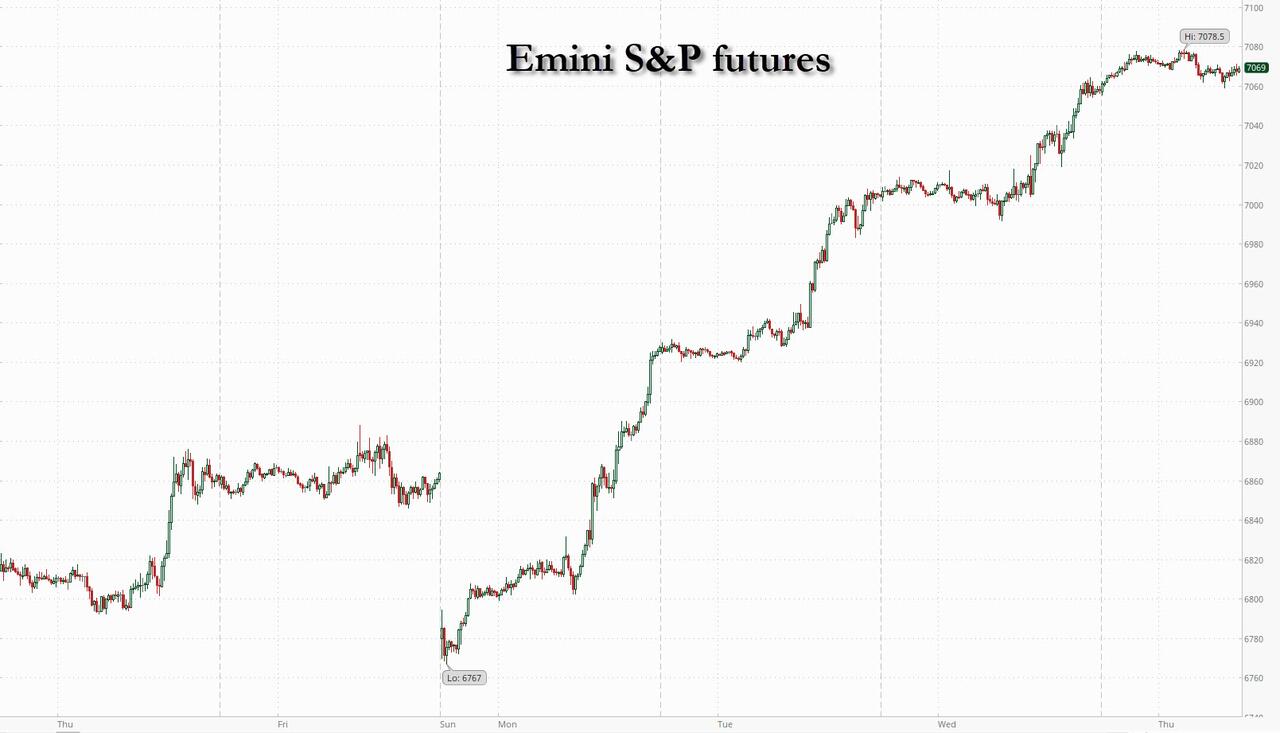

“The Roaring 2020s Are Back”: S&P Futures Hit New Record With Nasdaq Up 12 Straight Days On Iran Truce Optimism

“The Roaring 2020s Are Back”: S&P Futures Hit New Record With Nasdaq Up 12 Straight Days On Iran Truce Optimism

Stock futures are edging higher on continued optimism about an extended truce in the Middle East, while Taiwan Semi’s solid results have sparked another leg higher in AI trade. As of 8:15 am ET, S&P 500 futures rose 0.1%, while Nasdaq 100 contracts +0.2%, and on pace for a 12th day of gains. The early hours of the session saw a sharp rally in technology stocks after TSMC’s upbeat revenue outlook highlighted the resilience of AI chip demand. In premarket trading, Mag 7 stocks were mostly higher led by MSFT +1.8% and TSLA +1.3%. On geopolitical headlines, the White House remains optimistic on the second round of talk (key Pakistani negotiator visits Tehran); Israel’s security cabinet met to discuss a possible ceasefire. Bond yields are 0-2bp lower with a modest gain in the dollar. Brent rose toward $96 a barrel as movements through the Strait of Hormuz remained all but paralyzed. Bonds rose, led by gains in Europe where central bank policymakers signaled they’re in no rush to raise interest rates. The dollar snapped an eight-day losing streak while gold rose above $4,800 an ounce. April’s strong stock rebound is being driven by a new kind of FOMO, according to Ed Yardeni, with Goldman saying that “despite the sharp market rebound, positioning has not fully caught up.” Still, while equities are “definitely pricing” the end of the war, we are “not there yet,” cautioned HSBC’s Patrick George while the IMF and World Bank are also worried that markets are underestimating the war’s economic damage. Today’s US economic data calendar includes April New York Fed services business activity, Philadelphia Fed business outlook, weekly jobless claims (8:30am) and March industrial production (9:15am). Fed speaker slate includes Williams (8:35am) and Miran (10:35am)

In premarket trading, Mag 7 stocks are mixed: Microsoft +1.3%, Tesla +0.7%, Meta Platforms +0.5%, Nvidia -0.4%, Alphabet -0.2%, Apple +0.8%, Amazon -0.1%

Nuclear and uranium companies are set to extend this week’s rally after the White House released rules for establishing a National Initiative for American Space Nuclear Power. Oklo (OKLO) +7%, NuScale Power (SMR) +10%.

Quantum computing shares are on track to extend gains for a third consecutive session after Nvidia unveiled a suite of new open-source AI models aimed at accelerating progress within quantum computing.

Allbirds (BIRD) tumbles 21% as the newly minted AI stock takes a breather after soaring more than 580% on Thursday.

Hims & Hers (HIMS) rises 9%, with shares on track to extend the previous day’s 14% rally, after Health Secretary Robert F. Kennedy Jr. said the FDA is seeking to remove 12 peptides from Category 2 restrictions.

PepsiCo Inc. (PEP) gains 1% after quarterly revenue and earnings beat expectations as the maker of Doritos and Lay’s sees improvement in salty snacks volume following recent price cuts.

PPG Industries (PPG) rises 3% after the supplier of paints and coatings posted preliminary first quarter adjusted earnings per share that topped expectations.

QuidelOrtho Corp. (QDEL) sinks 17% after the health care services provider posted disappointing preliminary first-quarter revenue as US flu-like illness visits fell by about 30% from the year-earlier period.

Travelers (TRV) slips 1.4% after the insurance company posted first quarter results where net premiums written declined 1.7% from the year-ago period.

U.S. Bancorp (USB) rises about 1% after first-quarter profit beat estimates, as Chief Executive Officer Gunjan Kedia rounds out her first year leading the largest regional bank and boosting its stock.

Voyager Technologies (VOYG) gains 6% after the defense and space company signed an order with NASA for the seventh Private Astronaut Mission to the International Space Station.

Elsewhere in AI, Nvidia’s Jensen Huang said the US should seek greater cooperation with China on AI research. Politicians are also weighing in on the global AI race, with House Republicans calling for US sanctions against Chinese entities that improperly extract results from leading US AI models to develop their own competing systems. Today’s Big Take focuses on Anthropic’s race to assess the dangers of Mythos.

Stock markets have rebounded as signs of easing tensions in the Middle East, combined with a fresh burst of AI optimism and corporate earnings, pushed investors to abandon their cautious views. Sentiment was boosted by lack of bad Iran news again: this time, the US and Iran are said to be considering a two-week ceasefire extension to allow more time to negotiate a peace deal; the next meeting between US / Iran may take place later this week with chatter from Pakistani media that Trump is said to be in attendance. April’s strong stock rebound is being driven by a new kind of FOMO, the fear of missing out on peace, according to Ed Yardeni, who said that for stocks, the V-shaped recovery this month makes it feel “like the Roaring 2020s are back.” Still, while equities are “definitely pricing” the end of the war, we are “not there yet,” cautioned HSBC’s Patrick George. The IMF and World Bank are also worried that markets are underestimating the war’s economic damage.

In the latest developments in the conflict, Pakistan stepped up efforts to help the US and Iran prolong a ceasefire that’s set to expire next week.

“Investors have become conditioned to buy every dip,” said Michael Bell, head of market strategy at RBC BlueBay Asset Management. “The outlook is binary, either Hormuz reopens soon or it doesn’t. With equity markets already assuming Hormuz will reopen soon, the upside is perhaps limited.”

The AI narrative is back in focus after TSMC raised its outlook for 2026, forecasting revenue growth of more than 30% and saying that capex is likely to lean toward the upper end of its forecast ($56 billion). Elon Musk’s Terafab project, which aims to reshape the chipmaking landscape dominated by TSMC, is reaching out to chip industry suppliers and asking them to move at ‘light speed’ on his project.

“TSMC describing AI demand as ‘extremely robust,’ pushing capex to the upper end of a $52-56 billion range, and signaling that the next three years of investment will significantly exceed the last three; that is not the language of a cycle nearing its peak,” said Amanda Lyons, information technology sector lead and head of research at Energy Group Capital.

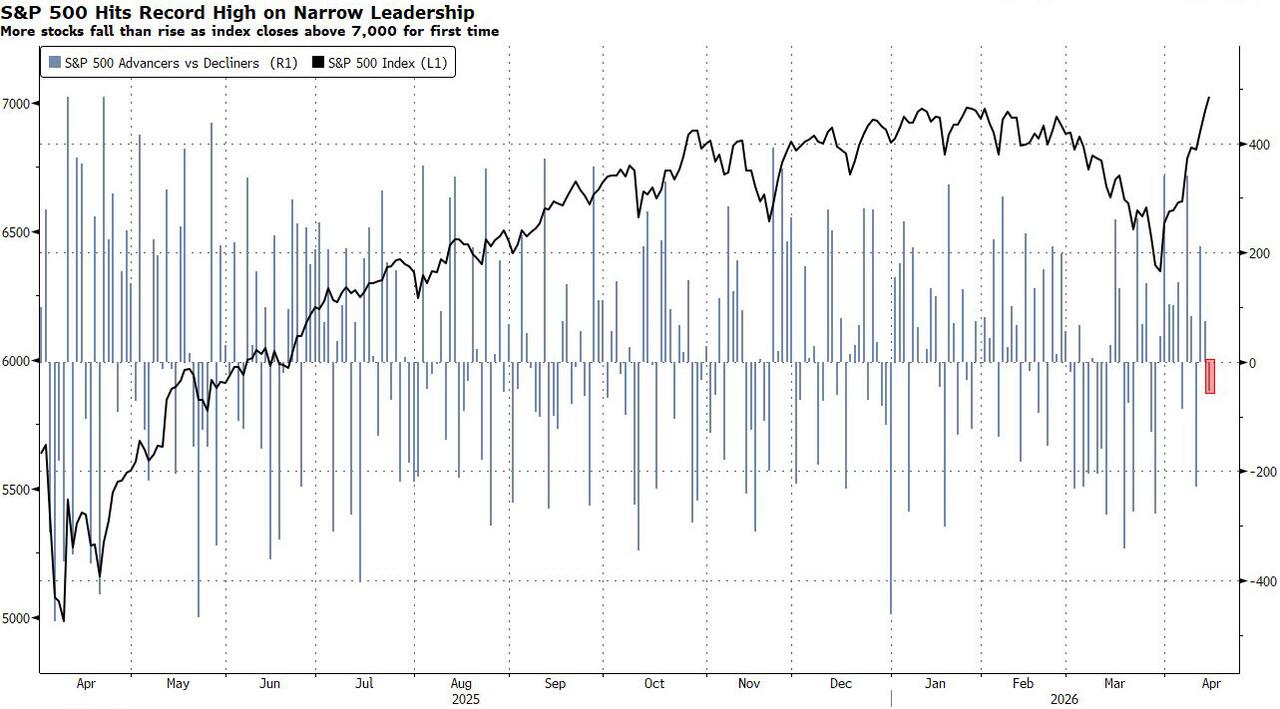

While the S&P 500 hit a new record on Wednesday, valuation ratios are still well below the levels seen in late 2025, indicating that earnings forecasts are moving up faster than stock prices. The current 12-month forward blended PE multiple for the S&P 500 of about 21 times compares to a peak of 23 times in November. The rally is also without breadth, with more decliners than advances as the gauge passed 7,000.

Another concerning fact about the latest record high: it was reach with more decliners than advancers, suggesting the leadership of this meltup is becoming dangerously narrow.

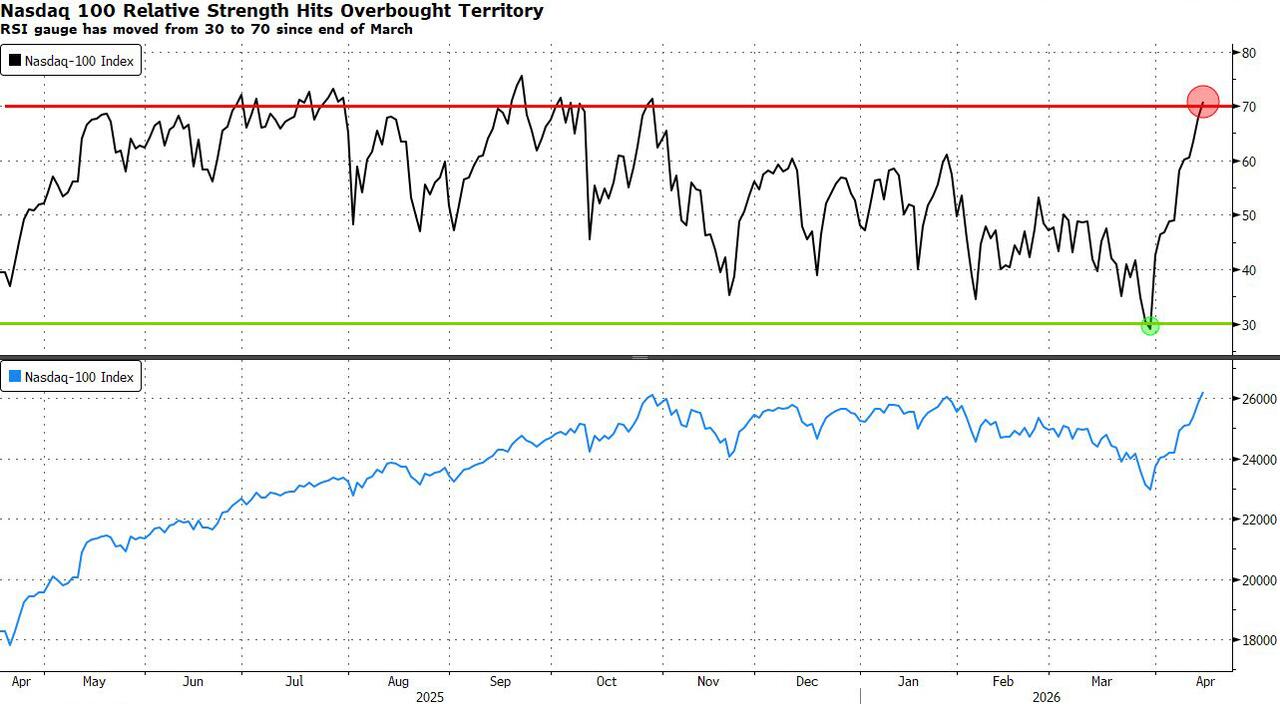

Lack of breadth however hasn’t stopped the Nasdaq from going from oversold to overbought in 2 weeks.

Technology stocks have been snapped up in recent weeks after lagging the market for much of the year, putting the Nasdaq 100 on course for its longest winning streak since 2017 if the gauge extends gains on Thursday.

Claudia Panseri of UBS Wealth Management said her exposure to artificial intelligence stocks is focused on the US and China and is “more selective” than two years ago. “We also prefer companies which are still investing using cash, rather than companies issuing bonds,” Panseri told Bloomberg TV.

Some stocks face a volatile option expiry into Friday, with $3.3 trillion notional of options open interest expiring across US indexes, ETFs and single stocks. Investors are “scrambling” for the “under-owned right tail” according to Nomura’s cross asset desk strategist Charlie McElligott.

Meanwhile, the latest private credit headlines have a more reassuring tone, with Goldman Sachs’ global head of alternatives for wealth saying she expects private credit firms to keep drawing capital despite recent redemption episodes. That follows Blue Owl shares posting their biggest two-day gain since November 2022, and reassurances from US banks that their exposure to private credit is manageable.

Technology stocks fueled gains in Europe where the Stoxx 600 rose 0.4%. Technology and retail shares are leading gains, while telecoms and food beverage stocks are the biggest laggards. Optimism surrounding the sector got a boost after Taiwan Semiconductor Manufacturing Co. raised its revenue outlook for 2026. Here are the biggest movers Thursday:

Entain shares rise as much as 6.6% after its first-quarter online gaming revenue grew faster than expected, offsetting weaker retail and adverse sports results, according to analysts

Tesco shares rise as much as 3.5% after the UK’s largest supermarket chain delivered annual earnings ahead of expectations

Mitie Group rises as much as 4.5%, touching a record high, after the support services provider delivered a trading update

Barry Callebaut shares drop as much as 17%, hitting the lowest level since November, after the Swiss chocolate maker reported first-half earnings that missed estimates and lowered guidance for the year

Kering shares fall as much as 4.6% after the French owner of Gucci outlined financial ambitions at its capital markets day that analysts deemed cautious

EasyJet shares fall as much as 8.7%, the most since June 2022, as the low-cost airline forecasts a 1H26 headline pretax loss of between £540 million ($733 million) and £560 million

Heidelberger Druckmaschinen shares drop as much as 9.2%, pulling back from a two-month high, after the printing press maker issued a profit warning

Earlier in the session, Asian tech stocks also climbed to a record high, while Taiwan’s total market cap topped $4.1 trillion to overtake the UK. Asian markets rose, with a key regional benchmark on course for a third-straight day of gains, on optimism over corporate earnings and a potential US-Iran ceasefire extension. The MSCI Asia Pacific Index advanced as much as 1.5%, with Samsung Electronics and Alibaba among the biggest boosts. Technology stocks led gains, with a sector gauge climbing to a new record high. South Korea’s Kospi, Japan’s Nikkei 225 and Hong Kong’s Hang Seng Tech Index rose more than 2% each, while Taiwan’s total market cap climbed above $4.1 trillion to overtake the UK. Investors are renewing their interest in the artificial intelligence theme with support from resilient earnings at Asian tech hardware makers. At the same time, an outlook for an eventual end to the Middle East conflict and tamer energy prices is gaining traction. Among key moves, EV battery maker CATL climbed more than 10% in Hong Kong after better-than-expected earnings. Meanwhile, chip giant TSMC raised its revenue outlook for 2026, an upbeat forecast that underscores the resilience of AI chip demand.

In FX, the Bloomberg Dollar Spot Index is up 0.2% and on course to snap an eight-day losing streak. The kiwi is the laggard among the G-10’s, falling 0.4% against the greenback. The pound falls 0.2% having derived little support from stronger-than-expected UK GDP data.

In rates, treasuries are slightly richer across the curve with gains led by the front-end and belly, supported by a wider bull steepening move seen across European bonds with oil prices steady. US yields lower by up to 2bp across front-end and belly with 2s10s, 5s30s spreads steeper by around 0.5bp and 1.2bp on the day. US 10-year trades around 4.265%, richer by 1.5bp on the day with bunds and gilts outperforming by 1.5bp and 1bp in the sector. In Europe, both UK and German 2-year yields outperform, richer by over 5bp on an outright basis, follows UK manufacturing data printing lower-than-expected. The US session includes weekly claims and a couple of Fed speakers.

In commodities, brent crude futures climb 1.6% to around $96.40 a barrel. European government bonds gain, led by the short-end as traders pare bets on interest rate hikes by the Bank of England and European Central Bank this year. UK and German 2-year yields fall 4 bps each. Precious metals advance, although are off their best levels.

Today’s US economic data calendar includes April New York Fed services business activity, Philadelphia Fed business outlook, weekly jobless claims (8:30am) and March industrial production (9:15am). Fed speaker slate includes Williams (8:35am) and Miran (10:35am)

Market Snapshot

S&P 500 mini +0.1%

Nasdaq 100 mini +0.3%

Russell 2000 mini little changed

Stoxx Europe 600 little changed

DAX little changed

CAC 40 +0.3%

10-year Treasury yield little changed at 4.28%

VIX little changed at 18.14

Bloomberg Dollar Index little changed at 1193.41

euro -0.2% at $1.178

WTI crude +1.7% at $92.84/barrel

Top Overnight News

Pakistan is stepping up efforts to ensure the US and Iran prolong a ceasefire that’s set to end next week, allowing more time for the warring sides to negotiate a lasting peace deal. The US and Iran are considering a two-week ceasefire extension, according to a person familiar with the matter, with neither side desiring to restart fighting. BBG

The Trump administration wants automakers and other American manufacturers to play a larger role in weapons production, reminiscent of a practice used during World War II: WSJ

Energy Secretary Chris Wright and Interior Secretary Doug Burgum will urge the heads of top U.S. oil and gas companies in a call Thursday to increase drilling in a bid to lower oil prices. Politico

China’s economy picked up speed early in 2026, riding an export surge before the Iran war sent energy costs soaring and put global demand – vital to Beijing’s growth ambitions – at risk. The 5.0% year-on-year pace in the first quarter sits at the top of China’s full-year target range of 4.5%-5.0%, highlighting a resilience that sets it apart from much of Asia, helped by ample strategic oil reserves and a diversified energy mix. RTRS

Australian employment rose by 17,900 in March, missing expectations and driven entirely by full-time roles, while the jobless rate held at 4.3%. BBG

The UK economy grew 0.5% in February, beating estimates to post its strongest monthly reading since January 2024. Activity was boosted by the services sector, though the data predate the Iran war. BBG

Policymakers at the European Central Bank are leaning toward keeping interest rates unchanged this month, postponing their verdict on whether the fallout of the Iran war warrants a response. BBG

Senator Thom Tillis is blocking Trump’s Fed chair nominee, Kevin Warsh, until the Justice Department drops an investigation into Powell. And the stalemate is leaving him in limbo with no clear off-ramp in sight. Politico

Anthropic’s Mythos is so skilled at hacking that access is tightly controlled. The system’s ability to autonomously find and exploit vulnerabilities is forcing banks and governments to rethink cybersecurity. BBG

Foreign holdings of Treasuries soared to a record $9.49 trillion in February. Canada led with a $50.5 billion increase, while Japan remained the largest holder. BBG

Iran Conflict

The Trump admin’s goal is to bring both sides to the brink of an overarching deal to end the conflict that can then be pushed over the finish line in a second face-to-face meeting, according to ABC, citing officials. The officials acknowledge that technical talks to hammer out the fine details and implementation of the arrangement will likely take longer to complete, perhaps eventually necessitating an extension of the initial ceasefire, but that pushing back the truce’s expiration date isn’t a top priority for the administration at the moment.

US President Trump told guests Monday night he wants to bring the war in Iran to a swift end; said only way to get Iran back to negotiating table was to increase the pressure, according to WSJ citing officials at the dinner.

US President Trump posted “Trying to get a little breathing room between Israel and Lebanon. It has been a long time since the two leaders have spoken, like 34 years. It will happen tomorrow. Nice!”.

Pakistani Army Chief is heading to the US on Friday as part of mediation efforts between the US and Iran, Al Jazeera reported citing a Pakistani security source.

Pakistan’s Foreign Ministry said the US and Iran are willing to hold talks and the process is continuing but no date decided for next round of US-Iran talks.

A military advisor to the Islamic Revolution Leader said Iranian Armed Forces’ launchers are ready to hit American warships and sink all of them, Press TV reported.

A senior Iranian official said the fate of Iran’s highly enriched uranium and the duration of its nuclear restrictions remain unresolved, adding that fundamental disagreements persist over nuclear issues. Iranian official said there are greater hopes for extending the ceasefire and holding a second round of talks after the trip, adding that the Pakistani army chief’s visit to Iran helped reduce differences in some areas.

Iranian officials will meet with Pakistan’s army chief on Thursday in Tehran and will discuss US proposals, according to TASS.

Iran and the Pakistani mediator will discuss details of the messages exchanged between Tehran and Washington tomorrow, Thursday; via Al Jazeera citing Iranian TV.

Journalist Abas Aslani posted source said Iran-US talks are far less positive [than reported] due to contradictory US stances & Israeli spoiler efforts, media push hyping success of talks is a PR manoeuvre to calm markets and shield Trump from pressure.

Iran’s ambassador to Pakistan said Islamabad is the sole venue for Iran–US talks.

Diplomatic sources suggest that “Washington is pressing forcefully to cool down the Lebanese front”, via Kan’s Kais; “Second round of negotiations between Israel and Lebanon will take place in Washington soon”. “Second round of negotiations between Israel and Lebanon will take place in Washington soon, and that the current contacts are focused on achieving a temporary ceasefire that will lay the groundwork for ending the war.”

Two Israeli officials said the meeting of the political security cabinet ended without a decision on a ceasefire in Lebanon, according to Axios’s Ravid.

Israeli media citing informed sources state that a ceasefire in Lebanon will not happen soon despite Trump’s statements.

Israeli army has not received any instructions so far to prepare for a ceasefire in Lebanon, via Al Arabiya citing local reported.

Lebanese officials say a ceasefire between Israel and Lebanon is expected ‘soon’, according to FT.

The next meeting between Israel and Lebanon is expected to be held early next week, via Sky news Arabia citing Israel Hayom.

Iran’s Interior Minister has ordered border governors to neutralise the threat of a naval blockade by strengthening and developing border trade by increasing imports of basic goods and exports of goods, utilising all national and regional capacities.

Iranian politician affiliated with Resistance Front of Islamic Iran, Mohsen Rezaei said they will not leave the Strait of Hormuz until the full realisation of Iran’s rights, adds that this time, Iran has set preconditions.

Iranian Parliament Speaker Ghalifbaf said US should withdraw from ‘Israel first’ mistake and must comply with agreement, also said resistance and Iran are one soul both in war and ceasefire.

Hezbollah fires long-range missiles at Tel Aviv, according to Defapress.

Iranian military affiliated outlet Defapress claims that four ships broke the US naval blockade over the past 24 hours, citing satellite data.

Israeli warplanes carried out a strike on the town of Shihabiya in southern Lebanon.

US Central Command said US blockade has turned back 10 vessels in the Strait of Hormuz today.

China’s Foreign Minister Wang Yi stressed to Iran that the Strait of Hormuz needs to reopen and stressed freedom of navigation in Hormuz, while he said Hormuz reopening is a unanimous call from the international community.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly gained following the positive lead from Wall Street, where the S&P 500 and Nasdaq printed fresh all-time highs, amid tech strength and peace talk optimism. ASX 200 bucked the trend and gave back initial gains, and more, as notable outperformance in tech was offset by losses in energy, resources, materials, financials and miners. Nikkei 225 rallied to a fresh record high after reclaiming the 59,000 status amid the hopes for a Middle East resolution and with the index led by the momentum in tech stocks. Hang Seng and Shanghai Comp were higher with further upside seen as the dust settled following the mixed Chinese GDP and activity data, in which GDP growth for Q1 missed expectations, but GDP Y/Y topped forecasts and printed at the high-end of China’s official 2026 GDP growth target. Meanwhile, Industrial Production data for March was better-than-expected, but Retail Sales disappointed.

Top Asian News

Japan’s top FX diplomat Mimura said told US Treasury Secretary Bessent will upgrade FX developments as needed, and both sides agreed to coordinate closely on FX.

Japanese Finance Minister Katayama said regarding exchange rates, agreed to further intensify communication with US Treasury Secretary Bessent.

Japanese Finance Minister Katayama said many central bankers are adopting a wait-and-see stance, as raising interest rates could have a negative impact on the economy, adds it is impossible to predict when the current situation ends and spillover effects.

Senior Japanese Financial Regulator official said Japan sees private credit as potential pillar in new strategy to meet corporate funding demand driven by M&A surge, according to reported.

China NBS said the economy had a good start in Q1, but the external situation is becoming more complex, adds China is to expand domestic demand and optimise supply. China will implement proactive macro policies. Expects a complex, volatile external environment. China will consolidate economic recovery foundation. Sees mixed signs of strong supply and weak demand.

Deutsche Bank upgrades China’s 2026 real GDP growth to 4.9% (prev. 4.5%).

Barclays raises China 2026 GDP growth view to 4.6% (prev. saw 4.0%).

European bourses (STOXX 600 +0.2%) are broadly gaining, albeit only modestly. The CAC 40 is the outperformer, rebounding from Wednesday’s luxury-driven selloff. The FTSE 100 is also slightly higher this morning, after UK GDP came in far stronger than expected in February (0.5% vs exp. 0.1%). Sectors point to a positive bias. Top of the pile lies Technology, supported by strong TSMC earnings, which has lifted peers such ASML. Telecoms is the underperformer, with a downgrade for Telia weighing on the broader sector.

Top European News

EU Inflation Rate MoM Final (Mar) M/M 1.3% vs. Exp. 1.2% (Prev. 0.6%, Low. 1.2%, High. 1.2%).

EU Inflation Rate YoY Final (Mar) Y/Y 2.6% vs. Exp. 2.5% (Prev. 1.9%, Low. 2.5%, High. 2.6%).

EU Core Inflation Rate YoY Final (Mar) Y/Y 2.3% vs. Exp. 2.3% (Prev. 2.4%).

UK Balance of Trade (Feb) -0.720B vs. Exp. -3.6B (Prev. 3.922B).

UK Goods Trade Balance (Feb) -18.79B vs. Exp. -20.2B (Prev. -14.45B, Low. -20.5B, High. -14B).

UK GDP YoY (Feb) Y/Y 1.0% vs. Exp. 1.0% (Prev. 0.8%).

UK GDP MoM (Feb) M/M 0.5% vs. Exp. 0.1% (Prev. 0%, Low. 0.0%, High. 0.3%).

Trade/Tariffs

UK Europe Minister Nick Thomas-Symonds is expected to offer an update on the state of play in negotiations; EU Trade Chief Sefcovic, and European Parliament President Roberta Metsola, will also provide keynotes, reported Politico.

USTR Greer said US-China Board of Investment is to be a government forum, adds there’s no situation where there’s no trade between US and China, also said the Trump admin wants to be pragmatic regarding China.

FX

DXY edged higher throughout the entirety of the European session following punchy Iran rhetoric. The index marked a session high of 98.21, rising from its earlier trough of 97.83 made in Asia. (Full Middle East analysis on the headline feed) As it stands, both US and Iran continue communication, but there is no confirmation yet on second-round talks or a ceasefire extension – not to mention Lebanon, which remains a key point. Aside from geopolitics, POLITICO reported this morning, “a growing chorus of Republicans, eager to install Warsh, are joining the call for the administration to end the probe” into Fed Chair Powell. This comes ahead of Warsh’s hearing next week. The session ahead sees remarks from Fed’s Williams (voter), who will speak at a Federal Home Loan Bank of New York event, while Miran (voter, dovish dissenter) will speak on the global outlook.

GBP knee-jerked higher on a stronger-than-expected UK GDP report from February, but now trades with very mild losses given the Dollar strength this morning. In brief, on a monthly basis, GDP rose 0.5%, while yearly saw an increase of 0.1%. This set of metrics did not encapsulate the US-Iran war and as such, MPC members will likely refer to the second-round effects of the energy shock before opting to adjust rates. Cable continues to trade towards recent highs and is essentially at pre-war levels. The pair attempted to breach 1.36, a rally which faltered at 1.3594.

Antipodeans trade mixed. While Aussie is a touch firmer against a resilient USD following jobs data – Kiwi sits at the bottom of the pile as bets for RBNZ tightening pare a touch with markets implying 77bps of easing by year end (prev. c. 83bps). NZD/USD began falling in Asia, though losses extended throughout the European morning to trade at session lows of 0.5893, the move likely to face support @ 0.5892.

JPY had a choppy overnight session with USD/JPY marking a session low of 158.27 after successful jawboning from Finance Minister Katayama; she told G7 members that Japan was watching FX with a high sense of urgency. She also reiterated close communication with the US Treasury. This, as is typically the case with the Japanese Finance Ministry, indicates officials are uncomfortable with the extent of JPY weakness, with JPY nearing the key 160 mark. Since these comments, JPY pared the entirety of the strength Katayama gave to the haven, pressured by the gains in the USD.

Central Banks

ECB officials are said to be leaning towards an April rate hold.

ECB’s Schnabel said that the memory of high inflation remains fresh, and inflation expectations could be more fragile. Can afford to take time to analyse the Iran shock. We are in a relatively favourable position because we were successful in bringing down inflation to 2% before the war started, have monetary policy stance that is broadly neutral. To carefully consider data that may indicate inflation becoming entrenched or having second-round effects.

ECB’s Demarco said policymakers must be patient on rate decisions, but warns an adverse scenario could materialise; adverse scenario could require two rate hikes; longer-term inflation expectations anchored.

ECB’s Muller said rate move at April meeting still cannot be ruled out, adds may not have all the data this month to determine if interest rates will have to be raised to tame an inflation surge and June meeting will offer greater body of information. No hard evidence of second-round effects of inflation.

Goldman Sachs expects the ECB to deliver 25bp rate hikes in June and September 2026 (prev. saw hikes in April and June). Analysts expect energy prices to remain persistently high through 2026, significant pass-through into inflation is likely in coming months and ECB’s communication has remained largely hawkish on the path ahead.

Fixed Income

Global fixed benchmarks opened the European session with a positive bias, but have gradually edged off best levels as the risk tone deteriorated as the morning progressed. Initial optimism was facilitated by comments from both Israeli and Lebanese officials, who said that a ceasefire is expected soon, and talks are expected to continue in the near-term. On the Iranian front, President Trump said that “he wants to bring the war in Iran to a swift end”. Thereafter, in early morning trade, a military advisor to the Islamic Revolution Leader said Iranian Armed Forces’ launchers are ready to hit American warships and sink all of them – a comment which weighed on the risk tone at the time, leading to upside in the crude complex, which pressured global fixed paper.

USTs are firmer by a couple of ticks and currently trades at the lower end of a 111-11 to 111-17 range. Ultimately, moving at the whim of geopolitical developments, with markets now awaiting clear details on when/if the second round of Iran-US talks will begin. From a domestic perspective, weekly initial jobless claims (215k expected from 219k) and continuing claims (exp. 1.84mln from 1.794mln), NY Fed services activity, Philly Fed manufacturing are all due.

Bunds are firmer by around 15 ticks and currently trade within a 125.32 to 125.62 range. German paper, as above, is off its best levels as the risk tone slipped a bit. Domestic newsflow has been fairly limited this morning, aside from an updated Goldman Sachs call for the ECB; analysts now expect the ECB to deliver 25bps rate hikes in June and September 2026 (prev. saw April and June), citing expectations that energy prices will stay high through 2026, feed through materially into inflation in the coming months and keep ECB communication largely hawkish. As it stands, money markets fully price in a 25bps hike in July. Focus later will be on the ECB Minutes (Mar), where the Bank kept rates steady – traders will be cognizant of any commentary pertaining to the Middle East situation.

Gilts are incrementally lower and trade within an 88.68 to 89.07 range. Slightly underperforming vs peers, given the hawkish impulses from a stronger-than-expected UK GDP report. In brief, on a monthly basis, GDP rose 0.5%, while yearly saw an increase of 0.1%. ING writes “UK output surged in February, but it’s in line with a trend dating back to 2022, where growth is stronger in the first quarter than across the rest of the year. We’re taking this latest data with a pinch of salt”.

Commodities

Regional mediators are actively working to extend the US-Iran ceasefire and secure a second round of talks, with both sides agreeing in principle to reconvene, though no date or venue has been set. The Trump administration is pushing a two-stage strategy: use sustained economic and military pressure to force Iran toward the brink of a broader deal, then finalise it in a follow-up face-to-face meeting, with technical negotiations on implementation likely to extend beyond the current truce. A senior Iranian official said the fate of Iran’s highly enriched uranium and the duration of its nuclear restrictions remain unresolved, adding that fundamental disagreements persist over nuclear issues.

Pakistan has taken a central mediation role, coordinating messages between Tehran and Washington and engaging both politically and militarily, although officials confirm no timeline has been agreed for the next round. Despite publicly downplaying the need for a ceasefire extension, US officials acknowledge it may ultimately be required to keep negotiations alive as talks progress.

Crude prices edged higher following yesterday’s losses as traders feel the ceasefire could be prolonged and negotiations restarted. Brent Jun holds above USD 95/bbl this European morning (in a USD 94.43-96.85/bbl range) while WTI Jun sits in a 87.32-89.82/bbl parameter.

Spot gold trades modestly higher, just above USD 4,800/oz and well within yesterday’s USD 4,786-4,871/oz range. Base metals are flat/positive with 3M LME copper holding above USD 13k/t in a current USD 13,281.00-13,376.58/t range. Overnight data showed China’s Q1 growth accelerated on strong exports (Y/Y printed at the top end of China’s 2026 target of 4.5-5%), while March retail sales rose but slowed from February; analysts said the Iran war still poses risks to the outlook.

Australia said it secures 100mln litres extra of diesel from Brunei and South Korea.

Repsol (REP SM) is set to take back operational control of its Venezuelan oil assets and boost production following an agreement with the country’s government, according to FT.

White House is expected to urge heads of oil and gas companies to increase drilling, according to POLITICO.

Australia’s Energy Minister reported that a fire at Viva Energy’s (VEA AT) refinery is still not under control, while diesel and jet fuel output continues, but refinery fire may hit petrol production more.

Geopolitics (ex Iran)

Ukrainian President Zelensky posted “there can be no normalization of Russia as it is today. Pressure on Russia must work”, following heavy drone attacks, via X.

Explosions reported in Ukraine’s capital, Kyiv, while the Mayor said air defence systems have been activated

US Event Calendar

8:30 am: United States Apr 11 Initial Jobless Claims, est. 213k, prior 219k

8:30 am: United States Apr Philadelphia Fed Business Outlook, est. 10, prior 18.1

8:30 am: United States Apr 4 Continuing Claims, est. 1810k, prior 1794k

9:15 am: United States Mar Industrial Production MoM, est. 0.1%, prior 0.2%

9:15 am: United States Mar Capacity Utilization, est. 76.3%, prior 76.3%

Individual investors are once again snapping up so-called “meme” stocks, an early sign that retail’s animal spirits are returning to the US equity market after the mid-month tax deadline and as geopolitical tensions abate.

Central Bank speakers

8:35 am: United States Fed’s Williams Gives Keynote Remarks

10:35 am: United States Fed’s Miran Speaks in Moderated Discussion

DB’s Jim Reid concludes the overnight wrap

I’m back in the hotseat this morning after a holiday which saw the temperatures on the slopes range from -20 degrees at the start to +25 degrees by the end. It was truly remarkable. Just as I was driving home, I then picked up the most virulent form of man-flu which knocked me out for a few days, including any desire to have early EMR starts this week. All I could do over the weekend was lie on the sofa and watch 30 hours of Masters’ golf coverage. It was brutal. I’ll leave you to assess whether there was sympathy at home or not.

Just as I went on holiday, on March 30th the S&P 500 closed at 6343.7 and at an 8-month low. Fast forward 11 business days and we closed last night above 7,000 (+0.80% at 7,023) for the first time, some +10.71% higher and at record highs. Few would have believed this was possible at the time, but this episode has been a high beta version of the usual geopolitical playbook where the negative impact on average lasts 15 days and the full recovery usually takes another 15-20 days. In this example the decline was slightly beyond the 75th percentile through history and the trough took a week longer to arrive than the average but the recovery took a week or so less. However, the geopolitical playbook has broadly worked.

The rally is continuing in Asia this morning with the Nikkei (+2.06%) leading the gains and hitting fresh all-time highs on the back of technology and chip-related stocks. The KOSPI (+1.64%) is also rising significantly, back to around +47% YTD. Elsewhere the Hang Seng (+1.38%), CSI (+0.90%), and the Shanghai Composite (+0.53%) are all higher after a decent monthly dump of data this morning (details below). The S&P/ASX 200 (-0.34%) is a rare decliner. S&P 500 (+0.15%) and Nasdaq (+0.26%) futures are continuing to edge up.

Coming back to China, GDP grew +5.0% year-on-year in the first quarter, surpassing forecasts of a +4.8% increase and showing an improvement from +4.5% in the preceding quarter. Additional data on economic activity released presented a mixed yet still resilient outlook, as industrial production increased by +5.7% in March compared to the same month last year, exceeding expectations of a +5.3% rise. However, retail sales advanced by +1.7% in March, falling short of the anticipated +1.9% increase, thereby underscoring ongoing weakness in domestic demand. New home prices continued their downward trend, decreasing by -0.21% in March, following a -0.28% decline in the previous month. So the property slump continues.

When it comes to the latest move higher, risk assets took their cue to continue to climb yesterday after the AP reported that the two sides were “in principle” in agreement on extending their April 7 truce, with Bloomberg later reporting that a two-week extension was being considered. So that raised hopes about a more durable ceasefire. White House Press Secretary Leavitt said that the sides remained locked in negotiations but that the US had not “formally requested an extension of the ceasefire.” On the Iranian side there was some optimism for a deal on the back of comments from Iranian Foreign Ministry spokesman Baghaei who told reporters that while the country’s right to peaceful use of nuclear energy “cannot be revoked”, the level and type of enrichment is “negotiable”.

As well as the new record for the S&P 500, the Nasdaq (+1.59%) reached a record of its own as the Mag 7 saw even larger gains (+2.48%). Technology and Consumer-oriented cyclicals drove the S&P gains again, with Autos (+6.59%), Software (+4.29%), Tech Hardware (+1.57%), and Consumer Services (+1.42%) the major outperformers, while commercial-oriented cyclicals lagged such as Cap Goods (-1.73%) and Materials (-1.29%).

Alongside the news from the Middle East, positive earnings helped to support US equities, with both Morgan Stanley (+4.52%) and Bank of America (+0.97%) advancing after their latest results. Coupled with other positive surprises, that’s helped to underscore the narrative of ongoing US economic strength, despite the recent surge in energy prices. Private credit concerns have also seen a couple days of respite as the two-day move in Blue Owl Capital is now over +17%, the biggest two-day rally since late-2022 after the company’s shares fell to its lowest publicly traded level last Friday.

Meanwhile, markets were intrigued by the story that US shoe brand AllBirds surged by +582% after it announced that it would rebrand as an AI compute business. From sneakers to servers, laces to latency, footware to firmware, comfort to compute! Bet you wish I was back on holiday or on the sofa!

In fixed income, treasury yields also rose after officials questioned the case for rate cuts. For instance, Cleveland Fed President Hammack said that her baseline was to keep rates on hold for a good while, and even Treasury Secretary Bessent said that he would “understand if the Fed needs to wait on rate cuts” even if he ultimately saw large cuts beyond that. So that helped yields to rise across the curve, with the 10yr yield (+3.6bps) rising to 4.283%, whilst the 2yr yield (+1.7bps) rose to 3.76%. This comes as Fed futures are again not pricing in a full Fed cut over the next 12 months. The latest data also supported those rate moves, with the Empire state manufacturing index for April up to a 5-month high of 11.0 (vs. 0.0 expected).

Earlier in Europe, equities were more subdued, particularly after some more negative earnings reports came through. That included French companies Kering (-9.29%) and Hermes (-8.22%), which weighed on the CAC 40 (-0.64%). And ASML also fell -4.22%, despite raising its full-year sales forecast. So equities took a hit across the continent, with the STOXX 600 (-0.43%) falling back, despite the more positive headlines about potential US-Iran talks.

Sovereign bonds also lost ground, with yields on 10yr bunds (+2.0bps), OATs (+2.4bps) and gilts (+3.4bps) moving higher. However, expectations for an imminent ECB rate hike continued to decline, with pricing for an April hike down to a one-month low of 23.9% at the close yesterday. 58.3bps of hikes were priced in by year end at yesterday’s close, down from 81bps on March 24th.

Markets generally continue to trade on optimism that the conflict will ultimately be sorted out in weeks even if the current situation in the Strait of Hormuz remains unchanged. The US naval blockade is far from over, with US Central Command posting on X yesterday that no vessels have been able to make it past US forces, with 9 vessels complying with US direction to turn back to Iran.

Trump also announced that President Xi had given him a call, later posting that China is “very happy” that he is “permanently opening up” the Strait of Hormuz, and have agreed to not send their weapons to Iran. His post followed an earlier FT report that Iran had secretly acquired Chinese spy satellite to target US military bases across the Middle East during the conflict.

Finally, Australia’s labour market data showed that the unemployment rate remained unchanged at 4.3% in March. Meanwhile, employment experienced a modest increase of 17,900, compared to the anticipated 20,000, for the month. Firms contributed by adding 52,500 full-time positions, indicating a degree of underlying resilience despite a slight slowdown in hiring. This data emerges as the RBA cautions that it may be necessary to further increase interest rates in the upcoming months to mitigate inflation, which is already significantly above the target and poses a risk of rising even higher.

To the day ahead now, data releases include the US April New York Fed services business activity, Philadelphia Fed business outlook, March industrial production, and initial jobless claims. We’ll also get the ECB’s account of the March meeting, and hear from the Fed’s Williams and Miran, the ECB’s Schnabel, Kazaks, Rehn and Kocher, and the BoE’s Taylor.

Tyler Durden

Thu, 04/16/2026 – 08:45

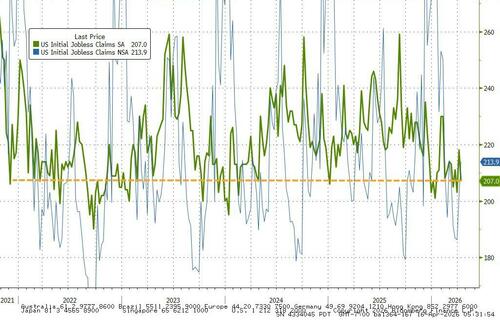

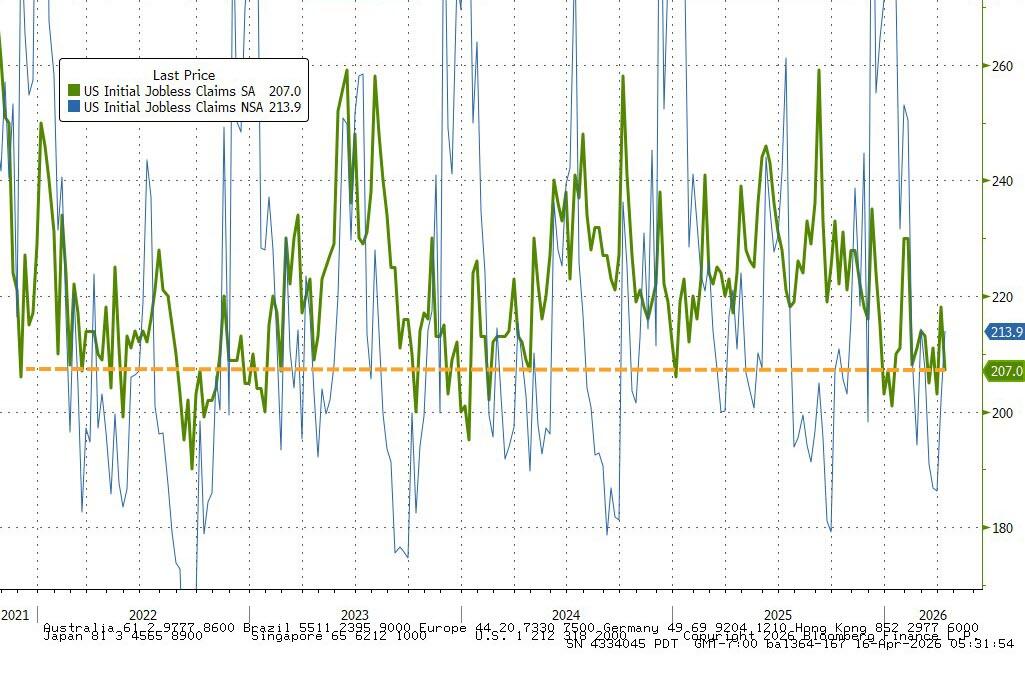

Despite ‘Survey’ Sadness, Jobless Claims Slide Near Historic Lows

Despite ‘Survey’ Sadness, Jobless Claims Slide Near Historic Lows

The number of Americans filing for jobless benefits for the first time fell to just 207k (below the 213k expected and down from the prior 209.25k) – back near its lowest levels in 5 years (and trend towards its lowest level in 50 years)…

Source: Bloomberg

Despite a small pick up last week, Continuing jobless claims have been below the 1.9 million Maginot Line since the start of the year…

Source: Bloomberg

Finally, as the following chart suggests, while it may be “hard to get” a new job, firing remains very low…

Source: Bloomberg

The ‘no hire, no fire’ economy is alive and kicking.

Tyler Durden

Thu, 04/16/2026 – 08:37

https://www.zerohedge.com/markets/despite-survey-sadness-jobless-claims-slide-near-historic-lows

Fire Erupts At Major Australian Refinery, Amplifying Fuel Shock As “Green” Killed Refining Buffer

Fire Erupts At Major Australian Refinery, Amplifying Fuel Shock As “Green” Killed Refining Buffer

Australia’s failed “green” domestic energy policies had already sparked a fuel-supply shock shortly after the U.S.-Iran conflict disrupted tankers at the Hormuz chokepoint. Now, a fire has broken out at the larger of Australia’s two remaining oil refineries, adding even more fuel supply woes.

Victoria state fire authorities said the blaze erupted at Viva Energy’s 120,000-barrel-per-day Geelong refinery, one of only two operating oil refineries left in Australia. The refinery accounts for roughly 10% to 12% of Australia’s fuel supply while covering about half of Victoria’s fuel demand.

Reported Viva Energy’s Corio refinery in Geelong is ablaze

Source: Geelong Community FB pic.twitter.com/oRsI10fVr3

— Timjbo 🇦🇺 (@TimjboAU) April 15, 2026

Reuters cited authorities early Thursday saying the fire at the refinery is now “under control.”

In a separate report, Al Jazeera noted that flames were reported to be as high as 200 feet and that a “gas leak” was potentially the source of the fire.

An oil refinery is engulfed in flames after an explosion in Victoria on Wednesday morning.

Viva Energy in Corio, near Geelong, is one of Australia’s last two oil refineries, and the blaze which engulfed it comes amid a global fuel crisis.

The refinery supplies over 50 per cent… pic.twitter.com/ovPkuIGO73

— 7NEWS Australia (@7NewsAustralia) April 15, 2026

“This is not a positive development, but obviously there’s a long way to go in terms of working out just what the impact is,” Energy Minister Chris Bowen told local outlet Channel Nine.

The incident has once again exposed how thin Australia’s refining buffer has become after “green” was prioritized over common-sense domestic energy policies, including the import of a vast share of its fuel needs from the Gulf.

Viva Energy said the incident is set to affect petrol and aviation gasoline. The good news is that the plant is still producing jet fuel and diesel.

Australian Strategic Policy Institute analyst John Coyne warned, “I would expect we’d see a price hike depending on the scale of the damage, and secondly, it reinforces the challenges we have in terms of sovereign and resilient capabilities here.”

There was no indication from Viva Energy of the specific damage or a repair timeline.

Australia’s decision to prioritize “green” policies while allowing its fossil-fuel complex and refining capacity to deteriorate looks absolutely reckless and now nation-killing.

Let’s not forget there has been a wave of high-value energy assets damaged in conflicts across Eurasia or mysterious industrial accidents elsewhere.

Tyler Durden

Thu, 04/16/2026 – 08:20

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}