Category: News

DOJ Probes BlackRock Private Credit Fund Valuations After Dramatic Repricings

DOJ Probes BlackRock Private Credit Fund Valuations After Dramatic Repricings

It all started in late January, just before the Blue Owl debacle and the SAAS-palcypse sparked a historic crash in private credit.

It was then that in a rare off-cycle disclosure, BlackRock TCP Capital Corp., a publicly traded private-credit fund structured as a business development company (BDC), disclosed a 19% markdown in net asset value as troubled loans weighed on performance. The news not only sent shares of the fund plunging 13% on Jan. 26, the most since March 2020 but market one of the first major private credit signal woes of the new year; it certainly wouldn’t be the last.

The credit fund told investors that NAV fell from $8.71 as of Sept. 30 to $7.05 to $7.09, or about a 19% markdown. “This decline is primarily driven by issuer-specific developments during the quarter,” the fund said.

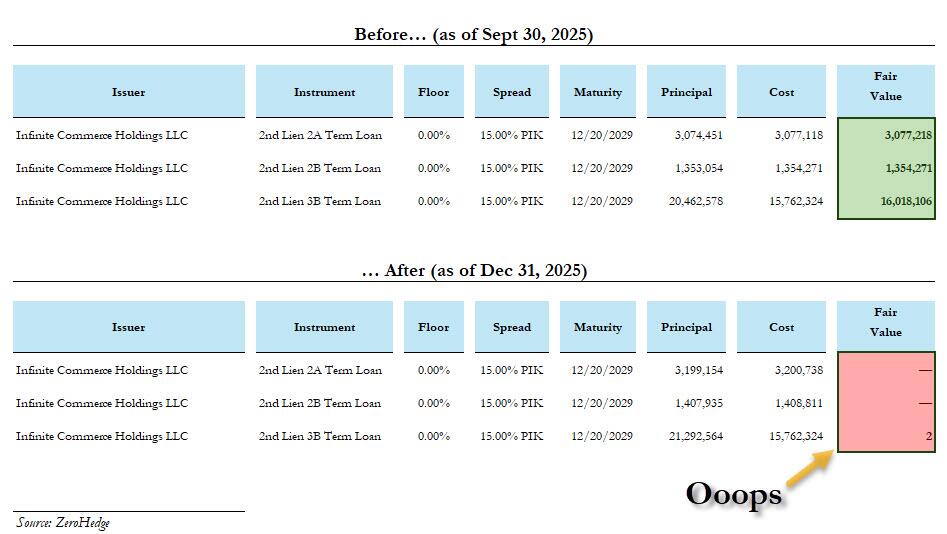

Two months later, in early March, it went from bad to worse for Blackrock’s private credit fund when the asset manager slashed the value of a private loan in its portfolio to zero just three months after assessing it at 100 cents on the dollar, marking the second sudden wipeout to recently hit its private-credit division.

The $25 million loan to Infinite Commerce Holdings, an Amazon aggregator that buys up online sellers of products from spa treatments to light bulbs, was suddenly worthless, BlackRock TCP Capital Corp reported in fourth-quarter filings released last week. The fund had marked the junior debt at 100 cents on the dollar in the third quarter. In other words, total wipeout in 3 months.

The write-off came just months after Infinite Commerce merged with another aggregator (and BlackRock debtor), Razor Group, in August, creating the new debt structure valued at par. Previously, BlackRock had valued loans to Razor at a deeply distressed level. Because financial engineering.

As a result of these bizarre quantized “repricing events” a number of class-action lawsuits were filed on behalf of investors that claim it made “materially false” statements and that Blackrock didn’t properly value its loans.

The final step in this particular lack-of-redemption arc came n Friday when Bloomberg reported that federal prosecutors are scrutinizing valuation practices at a BlackRock’s private credit fund.

The Manhattan US Attorney’s office in recent months has been seeking information about BlackRock TCP Capital Corp., while executives of the BDC have been questioned as part of the probe.

Jay Clayton, who runs the SDNY and was previously SEC commissioner under Trump 1.0, said in November he was concerned about how firms value private assets – and that “people should know that the financial regulators and the department are looking at those.”

Blackrock’s Janauary portfolio markdown was among the starkest examples of how quickly valuations can change in the $1.8 trillion private credit market. Investors in BDCs rely on the values ascribed to the loans, since there is no active market where the assets trade. Marks are therefore a key factor in determining at what price investors can enter or exit the fund, and they also impact the fees managers collect from the vehicles.

Funds like BlackRock’s TCPC typically only report quarterly. That’s what made the January disclosure, stating a preliminary net asset value per share of between $7.05 and $7.09, so unusual. About a month later it officially calculated the fourth-quarter figure at $7.07, sharply down from $8.71 at the end of the prior period.

BlackRock acquired TCP from Tennenbaum Capital Partners in 2018. Since its acquisition of HPS Investment Partners last year, HPS executives have come in to help manage the embattled vehicle, taking three spots on the fund’s seven-member investment committee.

In response to investor outrage over mismarked loans, private equity giant Apollo Global has stepped up efforts to provide liquidity and price transparency in the private-credit market, where assets don’t typically change hands. Two weeks ago, the firm said more than $830 billion of its credit assets will be priced daily by the end of September.

However, that sparked an angry response from other industry players such as PIMCO, whose strategist Lotfi Karoui wrote that more frequently marking assets does little to improve transparency or accuracy in the $1.8 trillion private credit market: “The debate over daily pricing in private credit portfolios has evolved from a narrow accounting question into a proposed remedy for the market’s dispersed — and often stale — valuations.”

“Attempts to increase liquidity — the ability to buy or sell an asset quickly, in size, and at prices reflecting fundamental values — are welcome developments,” Karoui wrote Yet until these efforts address the market’s inherent structural constraints, including a lack of true price discovery, they will only increase the perception of liquidity without truly improving liquidity.”

Pimco, an early critic of the private credit industry, has been vocal about the risks in direct-lending markets and has taken the other side of the bet by hunting for emerging problems in private-credit-backed companies.

“Price-mark dispersion for loans held across multiple business development company portfolios has widened sharply in recent quarters,” Karoui wrote. By the end of last year, “marks for the same instrument were, on average, about five points apart,” he added. “These gaps are difficult to reconcile with the notion of arm’s-length fair value determinations for identical assets.”

And that’s precisely why the DOJ is now involved.

Tyler Durden

Sun, 05/17/2026 – 14:35

The Fed Will Invent New Inflation Numbers Out Of Thin Air

The Fed Will Invent New Inflation Numbers Out Of Thin Air

Submitted by QTR’s Fringe Finance

The Federal Reserve is rapidly approaching the point where every available option becomes politically toxic, economically destructive, or both.

Inflation remains stuck around 3.8% CPI, well above the Fed’s stated 2% target, and that number alone should theoretically eliminate any serious discussion of aggressive easing. Treasury yields are rising as bond investors demand compensation for persistent inflation, uncontrolled fiscal deficits, and the growing realization that Washington’s debt load is becoming increasingly unstable.

The American consumer, meanwhile, is clearly running on fumes. Credit card balances continue hitting records, delinquency rates are rising, savings buffers have been depleted, and wage growth is failing to keep pace with the real cost of living for millions of households. Yet despite all of this stress beneath the surface, equity markets continue trading as if rate cuts are inevitable, growth will remain strong, and the Fed will once again rescue investors the moment volatility appears.

It is a fantasy built on the assumption that policymakers can indefinitely suspend economic consequences.

As I’ve been writing about, the Fed’s dilemma is now impossible to ignore. Raising rates further would intensify pressure on households, corporations, regional banks, commercial real estate, and most importantly the federal government itself, which now faces massive refinancing needs at dramatically higher borrowing costs. Holding rates steady risks allowing weakness to spread until something in credit markets eventually breaks.

Cutting rates, however, presents its own disaster scenario because inflation remains far too elevated to justify meaningful monetary easing. The Fed spent years insisting inflation was transitory before being forced into the most aggressive tightening cycle in decades. Repeating that mistake while inflation remains nearly double target would destroy what little credibility remains. And yet that may not stop them if markets begin unraveling. Remember this Bloomberg Businessweek cover?

As we’re seeing last week, real danger starts in the bond market. Stocks may dominate headlines, but Treasury markets are where systemic pressure becomes impossible to hide. Washington’s fiscal position becomes increasingly unsustainable if yields continue climbing because deficits at current levels only function in a world where debt can be financed cheaply.

If bond investors continue pushing yields higher, policymakers will eventually be forced to intervene directly. As Michael Green noted during this recent interview, that intervention will almost certainly come in the form of yield curve control, where the Fed steps into the Treasury market and effectively caps long-term rates through direct bond purchases. In plain English: money printing returns under a more sophisticated label.

Once that happens, equities likely become the next casualty before ultimately becoming the next rescue target. If yields spike hard enough before intervention arrives, equity valuations face a brutal repricing. Those investors currently paying extreme multiples for growth stocks and not just participating in the massive ongoing gamma squeeze in markets are doing so partially because they assume lower rates are right around the corner. If that assumption fails, stocks can fall hard and fast. And once markets experience enough pain, political pressure on the Fed will become overwhelming. Policymakers will once again be told they must stabilize markets, protect pensions, preserve confidence, and prevent contagion.

That is where things move from reckless, to dangerous, to out of ideas.

If inflation remains stuck around 3.8% but the Fed still wants political cover to print money, suppress yields, and rescue markets, it needs a justification. The easiest way to create that justification is by changing how inflation is measured. A Reuters report recently highlighted comments from Fed Chair Kevin Warsh suggesting that one of his first initiatives could be a major “data project” aimed at better measuring what he called “underlying inflation.”

Rather than relying on traditional inflation readings, Warsh expressed interest in trimmed-mean inflation metrics that remove what policymakers classify as extreme price movements in order to create a supposedly cleaner picture of inflation trends.

That sounds harmless until you understand what it really means. If inflation is running at a very real 3.8% and consumers are already being crushed by rising rent, food, insurance, healthcare, and utility costs, artificially lowering official inflation metrics to justify renewed money printing would be like pouring gasoline onto a house that is already on fire. It would take an inflation problem that is already eroding the middle and lower classes and deliberately intensify it in order to protect asset prices and government financing needs.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

Wealthy asset holders may celebrate easier policy and rising stock prices, but ordinary households would be left paying the real cost through even higher living expenses. Their wages would lag further behind. Their savings would lose more purchasing power. Their path to home ownership would become even narrower. Their ability to absorb everyday price shocks would deteriorate further.

This is what makes the entire idea dangerous. Americans do not live in a world of “trimmed mean inflation.” They live in the real economy. They buy groceries at actual prices. They pay actual rent. They pay insurance premiums that have surged. They deal with medical bills, childcare expenses, utility costs, and tuition payments that continue rising faster than official narratives suggest. Reuters itself noted that similar inflation metrics helped policymakers underestimate the inflation surge in 2021 by filtering out warning signs until inflation became impossible to ignore. Now the same intellectual framework is reappearing at precisely the moment policymakers may need an excuse to restart intervention.

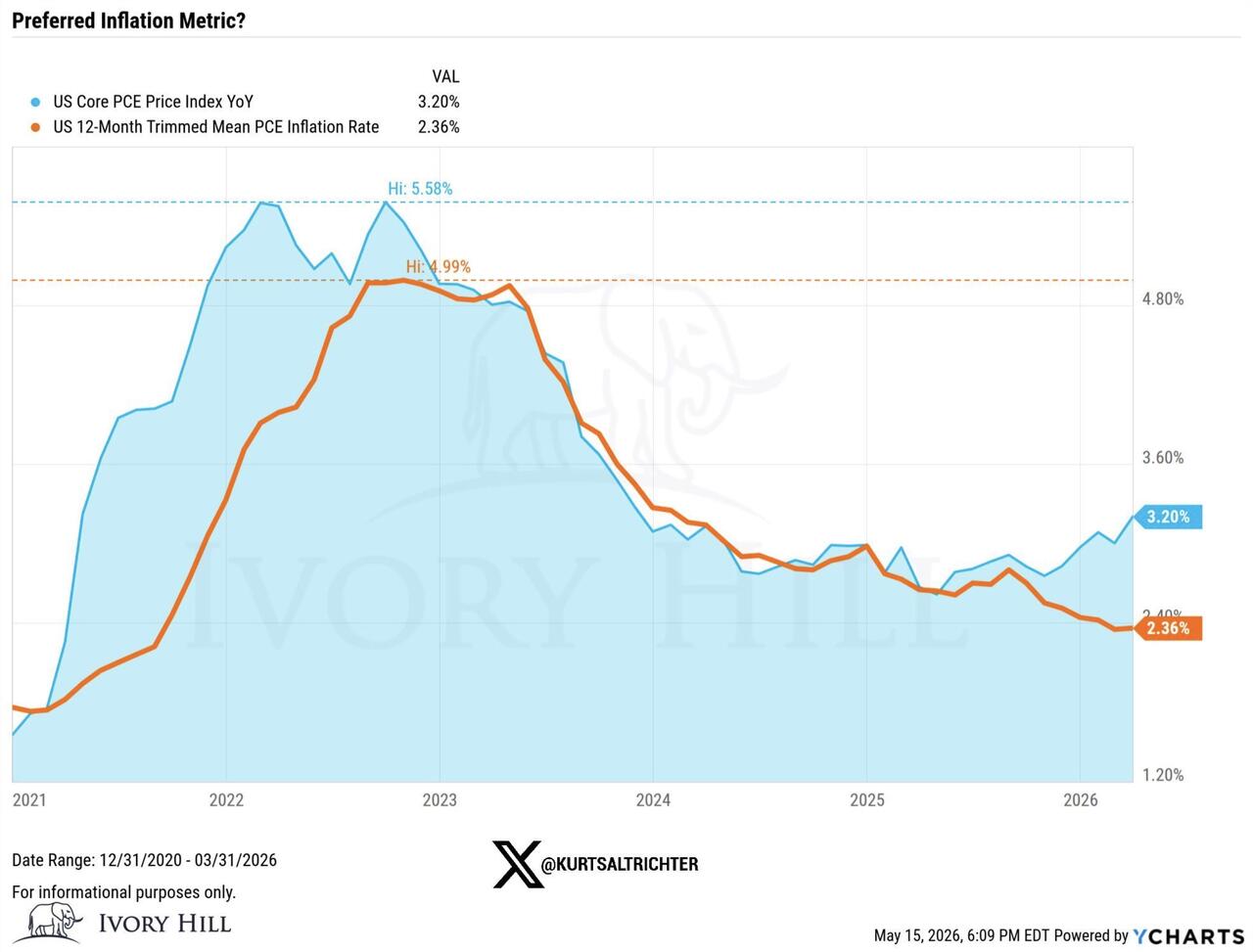

Kurt Altrichter on X noted the potential change: “The Fed has used Core PCE, which excludes food and energy, as its benchmark since 2000. Warsh favors Trimmed Mean PCE, which removes the most extreme price movements each month instead of excluding whole categories.”

He writes: “The practical difference: Trimmed Mean PCE currently reads 2.36%, well below the 3.20% reading on Core PCE. Depending on which measure the Fed follows, the case for rate cuts looks very different. This is not a minor procedural change. The metric the Fed uses to gauge inflation directly determines when it judges the economy to be at target.”

And the purpose of the change: “If Warsh moves the committee toward Trimmed Mean PCE, he is mathematically moving the Fed closer to a declared victory on inflation, which creates runway for rate cuts even as headline readings stay elevated.”

Altrichter concludes: “You’d think with 400+ Ph.D. economists and 500+ researchers on the payroll, the Fed would run the most sophisticated macro forecasting operation on the planet, leaving Bloomberg and every major hedge fund in the dust. Not even close. When the data doesn’t cooperate, just change the data. Same thing I saw in the Army when time or weather worked against higher leadership, and we would quietly move the goalposts rather than admit the standard couldn’t be met. Can you tell why I didn’t stick around for the full 20 years?”

And he’s right. This may be the real endgame. If bonds break, implement yield curve control. If stocks break, flood markets with liquidity. If inflation remains too high to justify either action, simply redefine inflation until the numbers say what policymakers need them to say. First it was hedonic adjustments. Then substitution effects. Then core inflation. Now “underlying inflation.” Every step moves further away from what ordinary people actually experience and closer to whatever statistic allows policymakers to keep the debt machine operating.

Maybe Wall Street celebrates another round of artificial stability. Maybe politicians claim inflation has been defeated because a revised formula says so. But if policymakers print aggressively into what is still a real inflationary environment, they are not solving the problem, they are accelerating it. They would be sacrificing the purchasing power of the middle and lower classes to preserve financial asset prices and government solvency.

And then they will likely stand at podiums explaining that inflation is under control while families wonder why groceries, rent, and insurance somehow keep rising faster than the official numbers suggest. At that point, the only thing more inflated than prices may be the credibility of the people reporting them.

—

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Sun, 05/17/2026 – 14:00

https://www.zerohedge.com/markets/fed-will-invent-new-inflation-numbers-out-thin-air

Massive Mushroom Cloud ‘Test’ Blast Rattles Uninformed Residents Outside Jerusalem

Massive Mushroom Cloud ‘Test’ Blast Rattles Uninformed Residents Outside Jerusalem

Late Saturday night, a massive explosion and a bright fireball illuminated the skies over Israel’s Beit Shemesh, deeply rattling local residents and setting off rampant speculation in local media and online commentary.

The area lies just 19 miles west of Jerusalem, close enough to be located within Jerusalem District. Curiously, the state-owned Tomer rocket propulsion defense ministry-linked firm subsequently sought clarify that the blast was actually a controlled, pre-planned test and that authorities were notified in advance.

However, community members have complained about receiving absolutely no warning, and were shocked at the immensity of the blast which lit up the night sky, visible for many miles.

Tensions were already running high in the city which had been struck multiple times by Iranian missiles during the recent war. The sudden detonation fueled widespread anxiety and anger among residents already on edge, bracing for the potential renew of the Iran war and thus Iranian ballistic missile attacks.

Times of Israel has cited Channel 12, saying that “the test involved propellants for rockets, including those with a range of thousands of kilometers.“

The same report interestingly called it “apocalyptic” in appearance but suggested this was misleading:

On Sunday, Kan reported that in the wake of the panic caused by the blast, a meeting was held at Tomer during which it was decided, in coordination with the Defense Ministry, to warn the public ahead of similar tests.

Tomer sources told the broadcaster that due to operational needs, the company is conducting testing at all hours, including during the night.

According to Kan, the company recently hired dozens of new employees, and the test was scheduled at night due to production constraints. Sources said it was carried out five kilometers from any population areas and that weather conditions had made the blast appear more “apocalyptic” than it actually was.

But it was significant enough to result in the convening of Israeli emergency management and defense officials, who subsequently told the public an investigation would ensue. The Defense Ministry said in the aftermath that “the issue of advance warning to the public will be examined with the company.”

MASSIVE MUSHROOM CLOUD explodes in Israel pic.twitter.com/ZE9WywA1rX

— RT (@RT_com) May 16, 2026

The company in question, Tomer, also separately stated, “A routine and planned test was carried out, conducted according to plan and achieving all its objectives.”

It explained: “All emergency forces were notified in advance, as is customary, and the fact that emergency and rescue forces were not called in attests to this. The videos filmed from a distance amplified the force of the explosion and did not reflect the fact that this was a routine event.”

But longtime resident and Beit Shemesh City Council member David Gozlan shot back, “There were quarries here, there were explosions at the Hartuv quarries, there were quite a few things here – but we have never experienced anything like this.”

The whole incident saw US ‘security experts’ quickly speculate and weigh in, and try and make sense of it on Sunday morning…

ISRAEL SAYS MASSIVE EXPLOSION IS “CONTROLLED DEMOLITION” ; VIDEOS SHOW A DIFFERENT STORY

UAE NUCLEAR POWER PLANT ALSO ATTACKED TODAY!

w/ Fmr. US Navy SCPO Malcolm Nance https://t.co/msIgXcSk74

— Mario Nawfal (@MarioNawfal) May 17, 2026

Naturally the biggest fear among locals was that a final big Iranian attack was underway, also given prior reports of hypersonic missiles launched on Israel during the height of the 38-day Operation Epic Fury bombing campaign on the Islamic Republic.

Israelis across the country spent many anxious and sleepless nights in bomb shelters and hundreds of Iranian projectiles rained down – many of them targeting defense industrial sites in the Israeli countryside.

Tyler Durden

Sun, 05/17/2026 – 13:25

AI vs Affordability And Rates

AI vs Affordability And Rates

By Peter Tchir of Academy Securities

Last week, we contemplated, for the first time, that we might need to Understand Universal Basic Income. The timing was very good as on Monday, South Korea floated the idea of transferring some AI-driven tax revenue to its citizens. As uncertainty around jobs, income, and costs continue to weigh on overall confidence, expect this subject to get more airtime in the political arena. The concept of UBI does go hand in hand with two competing themes: AI and Affordability.

China, Iran, and a Whole Lotta Nothing

Iran took a backseat to the Summit in China. We had relatively low expectations for the Summit. The cards were stacked somewhat in China’s favor as examined in China and Trade. It turns out that even our low expectations seemed to have set the bar too high. Friday’s title pretty much sums it up: My President Went to Beijing and all I got was this Crummy T-Shirt. There may yet be some deals announced, either with Iran or with China, but it looks like we are starting the week roughly where we started the prior week, but with even lower expectations.

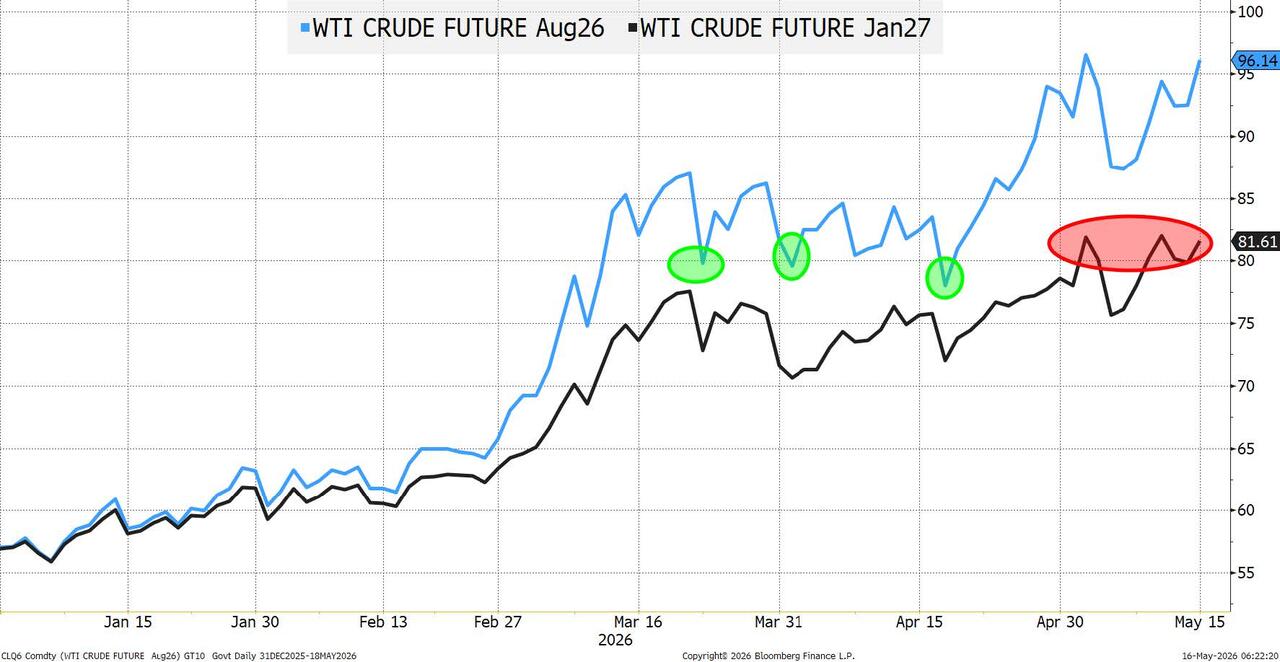

The Oil Curve

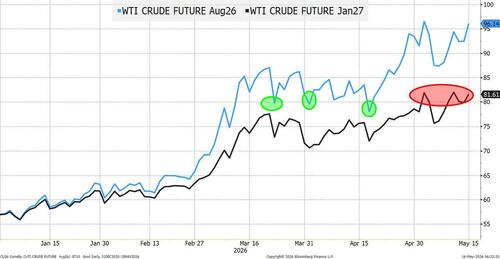

While Brent crude is most impacted by the ongoing problems in the Middle East, we will stick with WTI because that is what affects Americans the most.

One of the talking points for the admin had been that the oil market was predicting a “quick” resolution. Some officials pointed to the August contracts as demonstrating that $100 oil was a blip and things would “normalize” quickly. While $80 was still higher than pre-war, the argument had some legs. But now, the August contract is up to $95, and we are seeing $80 priced in all the way into 2027. This is certainly “higher for longer.” What is increasingly concerning is that it is difficult to tell if this is pricing in a re-opening or not. It was entirely plausible, a month or more ago, to believe that with the Strait of Hormuz getting back to normal levels of transit, global energy prices would “normalize” quickly. It is increasingly unclear what the “new” normal is. How much damage has been done to the “organism” that is energy? How quickly can things be fixed? Is the “new” normal the same as the “old” normal (see “Why One Bank Thinks It’s “Magical Thinking” That Hormuz Reopens In June“)?

Increasingly there are more and more questions about how long the damage will last, and if that damage will continue to elevate not just the price of oil, but also gasoline, diesel, jet fuel, etc.

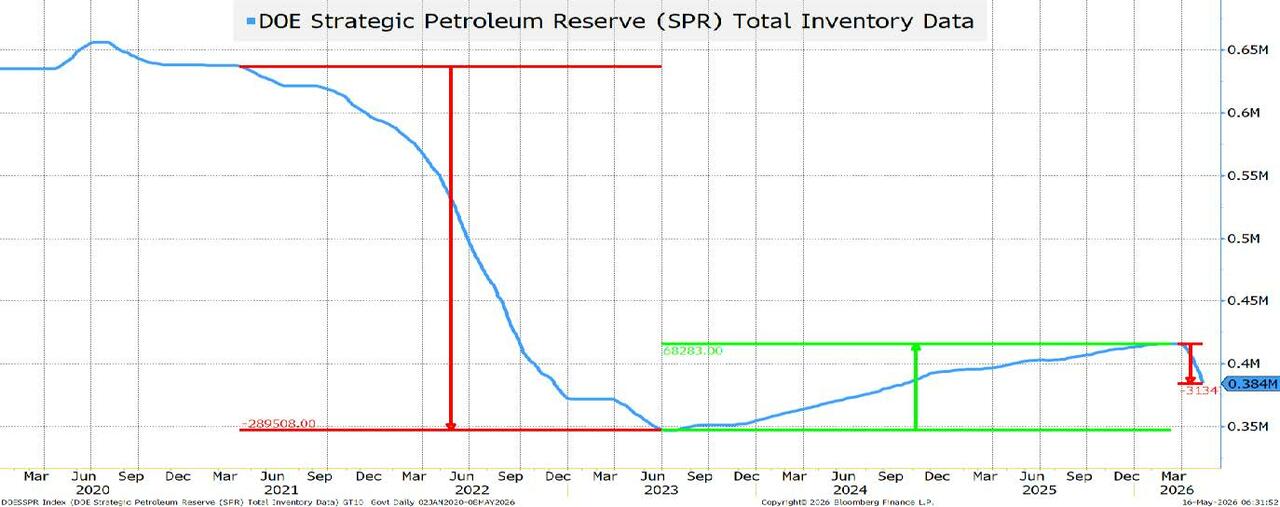

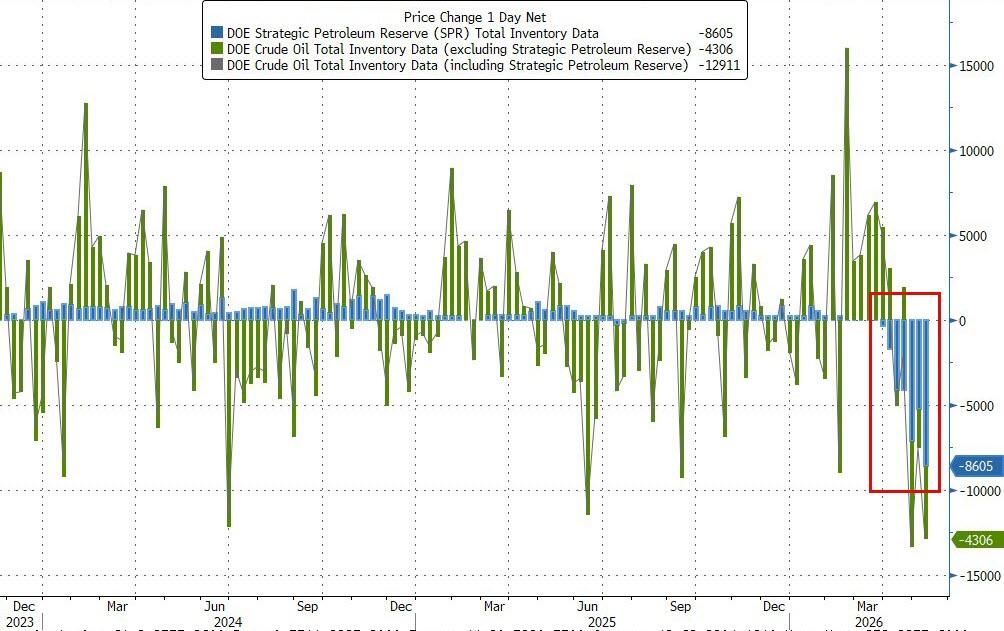

The U.S. can continue to release its Strategic Petroleum Reserves (SPR). It is unclear how low the reserves can go (I’m told that some amount needs to be left in place for structural integrity). We have released about ½ of what was added back to the SPR. Keep an eye on this, as it does limit our options over time. No one is expecting the problems to last that long, yet here we are, 3 months into the conflict, and transit through the Strait remains limited. Higher for longer in the oil market is the single biggest issue for Global Affordability.

AI versus Affordability

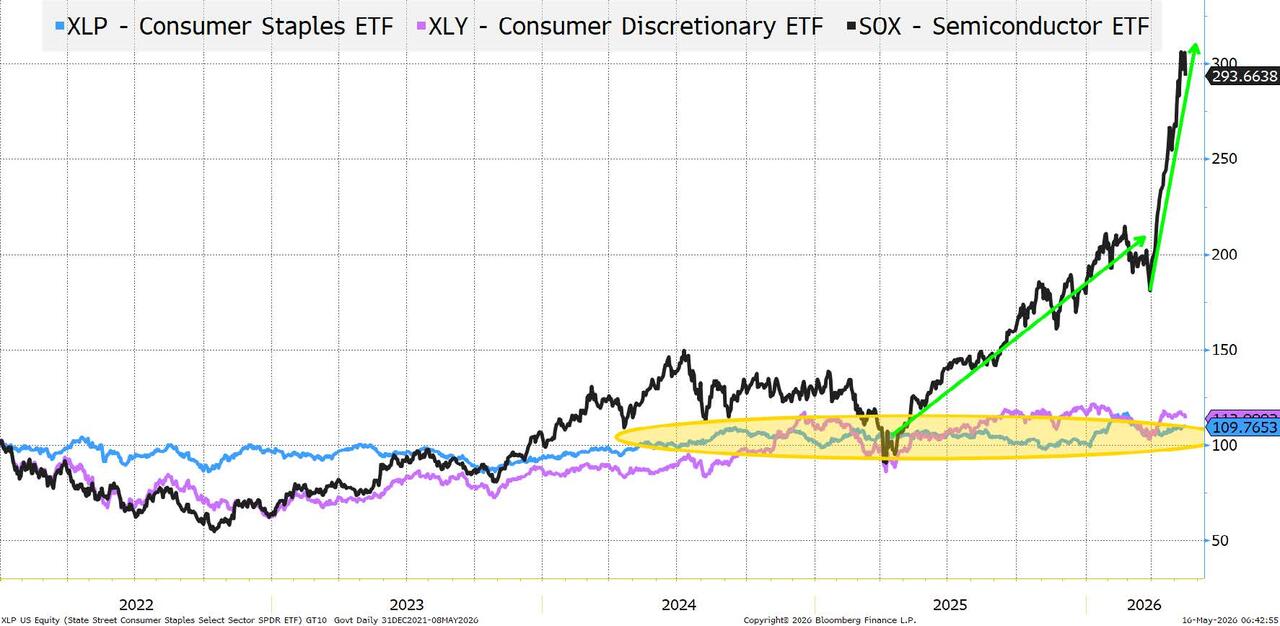

We received some consumer spending data this week which wasn’t too bad. It did seem to highlight, yet again, the problems facing people in the lower income brackets. I’m not convinced it doesn’t obfuscate that we are spending more to get less, but that is for another day. But here is a “simplified” version of a chart I’ve seen in various formats.

Companies servicing the consumer are not seeing much appreciation in their stock price.

Companies making chips are growing like gangbusters!

Is this sustainable? That question is being asked with increased urgency. The “parabolic” rise is raising some concerns. Without a doubt, this is the sector experiencing growth. It does seem to justify not only today’s prices, but also possibly even higher multiples. The earnings engine (and growth) is there, but this market has had a habit of hitting “high-conviction” trades.

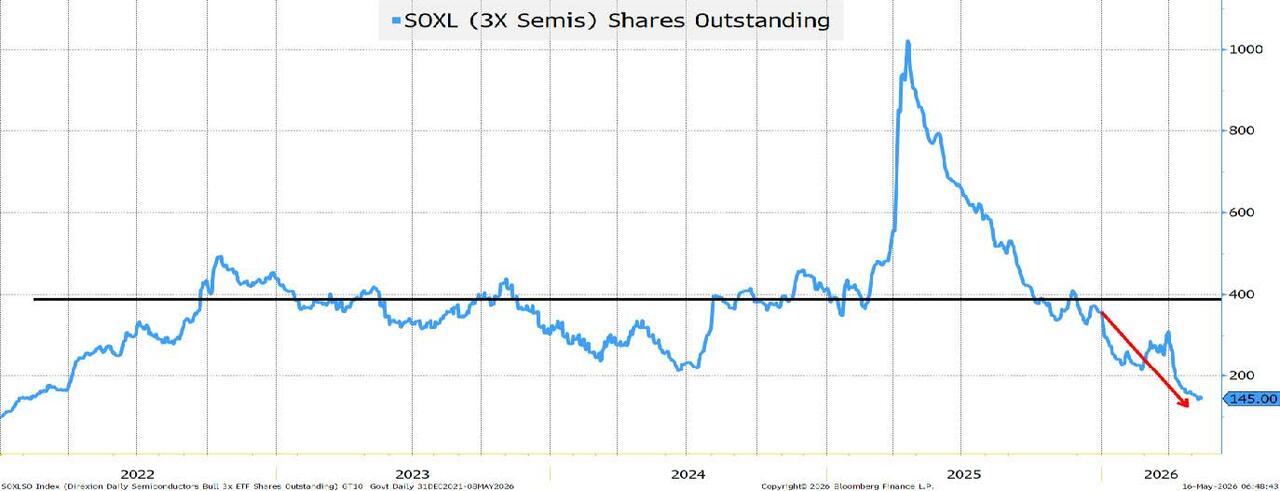

I find this chart extremely weird, but also interesting.

SOXL is a 3x leveraged SOX ETF. The assets in this ETF are about $20 billion, but the shares outstanding have been declining. While it may be inappropriate to label SOXL as a “degen” trade, I’m going to go there. “Degen” is an “affectionate” way of describing a group of very aggressive investors. Whether it is day trading leveraged ETFs, making bets in crypto altcoins, or playing in 0DTE options, there is a crowd of very aggressive traders that I will call “degen” for now (Warren Buffett would probably just call them gamblers).

I do think this crowd represents the “tip of the spear” on retail sentiment. If that assessment is correct, then it might indicate that retail is done (or almost done) fueling this trade.

The SOXX ETF weighs in at $33 billion (I had to do a double take, that it is “only” $33 billion while SOXL is $20 billion). The share count here tends to be more correlated with price. If anything, the last decline in SOXX was possibly telegraphed by a declining share count.

My view is that retail is slowing down on the semi-trade, just as institutions, including hedge funds, are treating it as a “must-have” position.

Retail, unlike funds, don’t have stop losses. Is this setting up for a pullback? Based more on positioning, and who is positioned, rather than the fundamentals?

Without the AI and semi story, market averages would be much lower. That is a fact. Is there anything to indicate that this trade cannot continue? No. But, I am curious what retail is up to here, and whether we are seeing enough of a pullback to create a reasonable pullback?

Which Brings Us To Rates

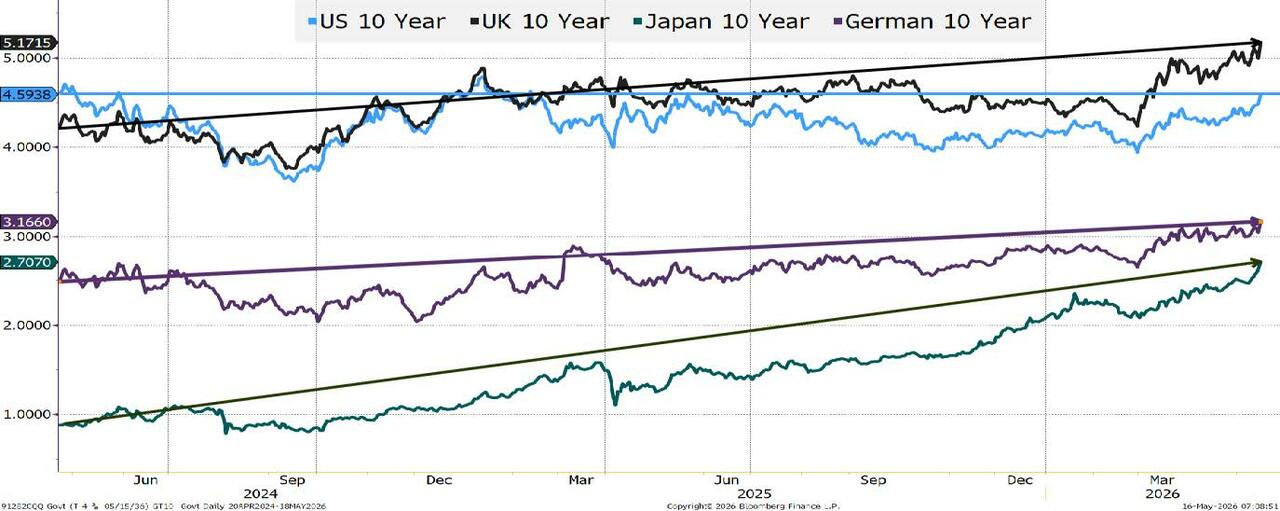

Yes, I “cherry picked” April 2024 as a starting point, because the 10-year U.S. Treasury yield is unchanged, while rates across the globe have risen. Most noticeably for Japan. In 2 years, the 10-year JGB went from yielding less than 1% to almost 3%. This is incredibly important. Japan as a “nation of savers” has been funding much of the world’s debt. I remain convinced that “at or near-zero” bond buyers of all levels of sophistication will take steps to get positive yield. So, when Japan hovered near 0% on rates, many investors would find alternatives to their domestic market to get yield. That has changed.

Globally, U.S. Treasuries, are fairly “generic.”

If you do not need dollar exposure, you have local FX bonds that can serve your needs.

All countries face a variety of risks to their economy. All central banks are trying to navigate the data, their expectations, and their mandate. It is less certain today how the U.S. central bank will respond to data than it was a few months ago – so that uncertainty should have a cost?

It is likely one reason why our agency debt team is seeing agency and super sovereign debt spreads to Treasuries at very low levels.

Defense Spending Requires Money

While ProSec is about far more than defense spending, it certainly incorporates the need to spend more. Japan – spending more. Europe/NATO – spending more and it seems inevitable that they will have to ramp that up.

The AI and Data Center Build Out Competes for Money

The semiconductor valuations depend heavily on data center and AI spending. That is being funded in a large part by debt.

We have been arguing for “range-bound” Treasury trading, while slowly raising the midpoint of the range.

I’m a bit hesitant to be very bearish on bonds here, as 5% or so on 30s (we are well above 5.12% as of Friday’s close) has been a level where this admin has taken steps to drive yields lower.

I could see an “Operation Twist” sort of announcement (the Fed selling shorter-dated bonds they own, to buy longer-dated bonds), but I’m not sure they are prepared to act.

What I find “interesting” is that Bessent no longer seems to be able to do “no wrong.” At the height of Liberation Day fears, Bessent could appear on TV and calm things instantaneously. I heard of the TACO BELL trade. Trump Always Chickens Out. Bessent Explains Longer Later. It was pretty clever (I did not come up with that).

Maybe it is because the Iran conflict is so far removed from what a Treasury Secretary does, that his latest appearances haven’t had the same impact? Maybe I have Bessent Delusion Syndrome? (Anything is possible).

But as many market participants seem to be waiting for some sort of “intervention” to helps bonds, I’m left wondering if they can accomplish that easily now?

Global bond yields are not helping. Higher for Longer on oil is not helping (that seems easier to correct – via peace with Iran, but that doesn’t seem imminent).

Bottom Line

Not “pound the table” bearish on bonds or stocks, but certainly not bullish. Not even really bullish for a trade. With the President likely looking for some “wins” and the admin likely exploring what they can do on the yield front, we could see relief in bond yields and higher stock prices, but I want hedges and would fade any such bounce. Price action in stocks seemed almost “sickly” on Thursday and Friday where every bounce/rally met some serious selling. Maybe all the AI-trained algos have read Sell in May and Go Away? Sorry, had to go there.

Caution into the summer seems warranted. Markets have priced in a lot of good news (China, Iran, and Semis), often multiple times (at some point is an earnings surprise really a surprise when everyone surprises the same way?).

Maybe it is time to “unprice” some of the good news? Affordability remains an issue and it seems to be becoming increasingly entrenched, which is a problem for bonds and stocks as a whole, if not just for the AI/data center spend, where my bigger questions are around positioning, than anything else.

Tyler Durden

Sun, 05/17/2026 – 12:50

https://www.zerohedge.com/markets/ai-vs-affordability-and-rates

Axios Warns Cuba Stockpiled 300 Attack Drones With Crosshairs On U.S. Homeland

Axios Warns Cuba Stockpiled 300 Attack Drones With Crosshairs On U.S. Homeland

Well, well, well.

On Feb. 3, we first asked whether a Cuban Missile Crisis 2.0 was quietly taking shape on the collapsed, communist-run Caribbean island of Cuba.

But instead of Soviet missiles, we warned that Havana may be stockpiling Russian-made Geranium one-way attack drones with the operational range to threaten major U.S. oil and gas refineries in the Gulf of America, key military bases, data centers, power grid infrastructure, and potentially even Washington, D.C.

Nearly three and a half months ago, we laid out the framework for a potential drone threat against the homeland originating from Cuba, using an infographic published by the Russian think tank Rybar.

Rybar is a noteworthy source in this context, and Western officials are not fans. The State Department has offered a $10 million reward for information on the outlet through its Rewards for Justice program, while both the European Union and the United Kingdom have sanctioned it.

At the time, Rybar wrote: “But what would the Cubans do in the event of a conflict? Let us hypothetically imagine that Havana decides to resist the Americans and chooses to fight. In that case, the already world-famous Geran strike drones could come to their aid.”

Fast forward to Sunday: Axios, citing newly obtained U.S. intelligence, reports that Cuba has accumulated roughly 300 military drones from Russia and Iran and has discussed potential wartime strike scenarios targeting Guantanamo Bay, U.S. naval vessels, and possibly Key West.

Axios spoke with a senior US official who said the Cuban drone threat is becoming a growing national security concern because of Cuba’s proximity to the U.S., the presence of Iranian military advisers in Havana, and the rapid proliferation of low-cost drone warfare.

“When we think about those types of technologies being that close, and a range of bad actors from terror groups to drug cartels to Iranians to the Russians, it’s concerning,” the official said.

The official noted that Cuba has been building drone stockpiles of “varying capabilities” from Russia and Iran since 2023.

Late last week, CIA Director John Ratcliffe met with officials in Havana, which appeared to reopen the channel for political dialogue between the two countries.

Ratcliffe and top U.S. officials, some of whose faces were blurred in images released by the CIA on X, held high-level talks with Cuba’s Interior Minister, the head of Cuban intelligence, and Raúl Castro’s grandson, Raulito Rodríguez Castro.

Havana, Cuba pic.twitter.com/7S7TtJPyf5

— CIA (@CIA) May 14, 2026

AP News noted that Cuban officials presented a report to Ratcliffe and his team, claiming to demonstrate that the communist-run island poses no threat to U.S. national security.

Meanwhile, the most glaring vulnerability in U.S. airspace is the absence of a low-cost, layered counter-drone technology capable of detecting and defeating one-way attack drones. That gap spans energy infrastructure, stadiums, data centers, military facilities, power substations, and other high-value civilian assets.

This is precisely why private equity funds have recently rushed into the space. PE firms are increasingly moving to fund, acquire, and import battle-tested Ukrainian drone and counter-drone systems into the U.S. market, positioning for a rapid phase of domestic airspace fortification.

Related:

Micro AI Sentry Guns May Be Next Layer Of Defense For Data Centers Against Kamikaze Drones

We’ve outlined this theme for months, even before it became a national topic. Follow the money, as we’ve mentioned, just watch the parabolic rise of ‘war unicorns‘ in the quarters and years ahead.

Tyler Durden

Sun, 05/17/2026 – 12:15

Uranium Transfer, Nuclear Limits: US Issues 5 Peace Ultimatums To Iran

Uranium Transfer, Nuclear Limits: US Issues 5 Peace Ultimatums To Iran

According to a Sunday report from Iran’s semi-official Fars news agency, the United States has laid down a firm, take-it-or-leave-it ultimatum to Tehran. Both sides are still trying to patiently wait out the Hormuz crisis, hoping to inflict more economic pain on the other until they blink.

At the top of the list, the US is demanding a near-total dismantling of Iran’s atomic ambitions, “allowing only one Iranian nuclear facility to remain operational.”

The list includes direct rejections in response to Iran’s own five conditions from a week ago, which President Trump said were “unacceptable” and “garbage”.

For example the US is refusing to pay compensation for damage caused during strikes on Iranian territory – a ‘maximalist’ sticking point which Tehran had demanded previously.

Washington is also reportedly insists that 400 kilograms of enriched uranium be transferred from Iran to the US, while only one active nuclear facility would remain operational inside the Islamic Republic.

Iran for its part has recently vowed to never transfer its nuclear material out of the Islamic Republic, calling the issue a matter of national sovereignty and energy security which it alone has say over. This after even Russia offered to take it.

The newly reported five conditions by the US side further states that the US does not intend to release more than 25% of frozen Iranian assets. Tehran has demanded the dropping of all US sanctions as a key basis for lasting settlement.

Here are the five newly proposed Washington conditions, which some pundits have called ‘wishful thinking’:

No war compensation from US

Give up 400kg of Highly Enriched Uranium to US

Iran can only have on nuclear facility to remain active

Not more than 25% of frozen assets to be unfreezed

Halting war on all fronts depends on negotiations

So this leaves a huge distance between the Washington list and Tehran’s list, as the seemingly unbridgeable gulf remains, also as Iran is digging in its heels.

As a reminder, the below is the Islamic Republic’s list, which it hasn’t backed down from. It has offered the following as the only basis on which to restart talks:

Ending the war on all fronts, including Lebanon

Lifting all sanctions

Releasing frozen Iranian assets

Compensation for war damages and losses

Recognition of Iran’s sovereign rights over the Strait of Hormuz

US response to #Iran includes zero compensation, not even 25% of frozen assets released, keeping only one #nuclear facility active, handing over 400kg of highly enriched uranium to the US, and ending the war on all fronts dependent on the negotiations. https://t.co/riS7M4fEeF

— Abas Aslani (@AbasAslani) May 17, 2026

While a Pakistani-mediated ceasefire managed to take effect on April 8, subsequent talks in Islamabad completely collapsed, but then President Trump later extended the truce indefinitely, likely to buy time and to figure out “what’s next” – while seeking a complete blockade of Iranian oil exports, and of all vessels entering or exiting Iranian ports.

With Washington demanding total disarmament and Iran demanding control over the world’s most critical oil transit choke point, the stage is set for a likely coming renewal of direct clashes, given the zero sum demands of each side now on the table.

Tyler Durden

Sun, 05/17/2026 – 11:05

Remember: In A Crisis, Everyone Will Consider Themselves ‘The Good Guys’

Remember: In A Crisis, Everyone Will Consider Themselves ‘The Good Guys’

Authored by Charles Hugh Smith via substack,

The state has two monopolies it must protect whatever the cost: the monopoly on decreeing what is legal tender and on force.

We’re entering an era in which push comes to shove will lead to immovable objects encountering irresistible forces. All sorts of verities and vanities will be bulldozed as kicking the can down the road descends into desperation to stave off collapse, a desperation that unleashes second order effects the desperate did not anticipate. The only responses at this late stage are even more desperate, so desperation is self-reinforcing.

The previous eras of institutional-state desperation were 1) The 1930s Great Depression, 2) the 1973-74 Gas Crisis and 3) the inflationary recession of 1980-82. The desperation in the 1930s was truly serious: banning private ownership of gold other than coin-collecting, attempting to remake the Supreme Court, one new federal program after another, slashing the wages of municipal / city employees to keep as many people employed as the shrinking revenues could allow, and so on.

The desperation of the 1970s and 80s were relatively narrow in scope, but felt serious at the time: gas rationing and wage/price controls in the 1970s, and then rocketing bond yields / interest rates in the early 1980s that triggered millions of layoffs in interest-sensitive sectors such as autos and housing.

The strong-arm policies of the 1970s and 1980s worked, and were relatively brief. The crises lasted around two years, and then things normalized.

The strong-arm policies of the 1930s didn’t work, and desperation slid into despair. The official happy-talk continued, but it rang increasingly hollow as the decade ground on.

Given the present-day confluence of disintegrative forces, a.k.a. mutually reinforcing polycrisis, hopes for a brief recession and a quick return to “growth” may be misplaced. If inflation and scarcities intensify, the usual bag of tricks–dropping interest rates to zero, flooding the financial sector with credit / liquidity, increasing federal pork spending, etc.–will not just fail, they will be counter-productive, fueling inflationary forces not in assets that enrich but in real-world goods and services that impoverish.

The footprint of the Central State–and state/county/local government–was relatively modest in the 1930s compared to the footprint of the state now: 36% of GDP in the US (23% federal, 13% state/local) and much higher in many developed nations.

Note that in a recession, GDP drops and state spending tends to rise to compensate for the contraction of private sector spending. so this ratio can climb very quickly.

To a degree few question, the state is the nation. The nation is defined by the state’s legal structure and its ability to enforce that structure. If the state collapses, the nation is in dire straits.

Should the state’s finances enter a self-reinforcing death-spiral, the desperation will quickly reach a level in which nothing is off the table–no extreme is too extreme. The typical self-reinforcing death-spiral is a currency crisis in which the currency loses value so rapidly that everyone holding it wants to convert it into some other form of value. That selling is self-reinforcing.

But that doesn’t exhaust the possibilities of the state’s finances becoming unsustainable, either financially and/or politically. A slow-moving crisis can phase shift into a fast-moving crisis like an avalanche no one is prepared for.

States face an insoluble dilemma: the powerful interests that dominate state decisions find higher taxes on corporations, trusts, foundations and the wealthy unacceptable, while the public living off the state’s largesse finds cuts deep enough to matter unacceptable.

Recency bias kicks in hard: after decades of “growth” and expanding state spending, anything that smacks of discipline or sacrifice is rejected out of hand as needless: why can’t we just go on as we have for the past 17 years, where assets soar in value, and the state spends more every year?

This leads to the illusory “solution” of kicking the can down the road: monetary policy tricks, fiscal sleight of hand, fake policy-tweak fixes presented as “solutions,” and so on. This magic can prop up the illusion of sustainability for years, but since every trick eventually makes the problems worse, this illusory “solution” actually hastens the push comes to shove moment where everyone is seated at the banquet of consequences.

Those tasked with saving the state’s finances from collapsing will view themselves as absolutely The Good Guys, working to saving the nation from greedy leeches on the state, speculators, financiers and those hoarding wealth acquired back when the state could afford to be generous. Now that things are at risk of unraveling, the fun and games are over and we need to do whatever it takes to save the nation–i.e. the state.

The wealthy trying to evade the new taxes will consider themselves The Good Guys: we worked hard for our wealth, created jobs and innovations that benefited the nation. Why should we give our hard-earned wealth to a corrupt, spendthrift state?

In the lower reaches of the economy, those evading taxes will also see themselves as The Good Guys: I’m just trying to support my family, and it’s the rich who should make the sacrifices as they have more than enough.

Those enforcing the expropriations / taxes will develop a unit-cohesion us-vs-them esprit de corps–the ultimate Good Guys who have to put up with both sets of greedy weasels: the weasels sucking off the state and the weasels trying to evade their civic duty to pay what they owe. Their tolerance for the self-serving claims of being “the good guys” by those protesting massive cuts in state spending and massive increases in taxes will be low to start and drop from there.

The state has two monopolies it must protect whatever the cost: the monopoly on decreeing what is legal tender and on force. So when the NSA is tasked with ferreting out miscreants cheating the state, tax-evading millionaires and other federal agencies are tasked with renditioning those who reckon they evaded their responsibilities by fleeing overseas, these are the tip-of-the-spear Good Guys who are trying to save the nation from the terminal rot of a citizenry that has long since lost any sense of civic duty that demands sacrifice and frugality.

Should push come to shove, nothing will be off the table. It will be too late to whine that we’re one of the Good Guys; the money from the state will stop flowing, and the safety deposit boxes and overseas accounts will be opened by force. As the cries of anguish increase, the demands to close down the tax havens of the super-wealthy will reach fever pitch, and whomever is tasked with saving the nation will have an agenda that reverses the order and the priority of wealth and power.

The super-wealthy are safe until they’re understood as the key impediment to saving the state. Right now, nobody thinks push could come to shove to the point that nothing will be off the table in terms of force. States that wait too long to act find their ability to apply force is insufficient to save the state, and this will weigh ever heavier on those tasked with protecting the state from financial collapse.

The irony here is the forces protecting their self-interests by kicking the can down the road are hurrying the collision of immovable objects and irresistible forces. Those who reckon they’ll do fine if the state collapses will find themselves nostalgic for the days when they could whine about a tax on second homes worth in excess of $5 million.

Chaos Unleashed: When “Irrational” Makes Perfect Sense.

I’m not saying I “like” this or that it’s inevitable; I’m saying the longer illusory “solutions” of kicking the can down the road are substituted for real solutions, the more likely a crisis of the state’s financial coherence becomes. Betting on which one wins–immovable objects or irresistible forces–might be a lose-lose proposition.

The only dinosaurs that survived the meteor strike were small birds that didn’t need much to get by, were mobile and were adapted to tough conditions. The descendants of those birds are the ones we see today.

How birds survived the dinosaurs’ doomsday (Scientific American)

Tyler Durden

Sun, 05/17/2026 – 10:30

https://www.zerohedge.com/geopolitical/remember-crisis-everyone-will-consider-themselves-good-guys

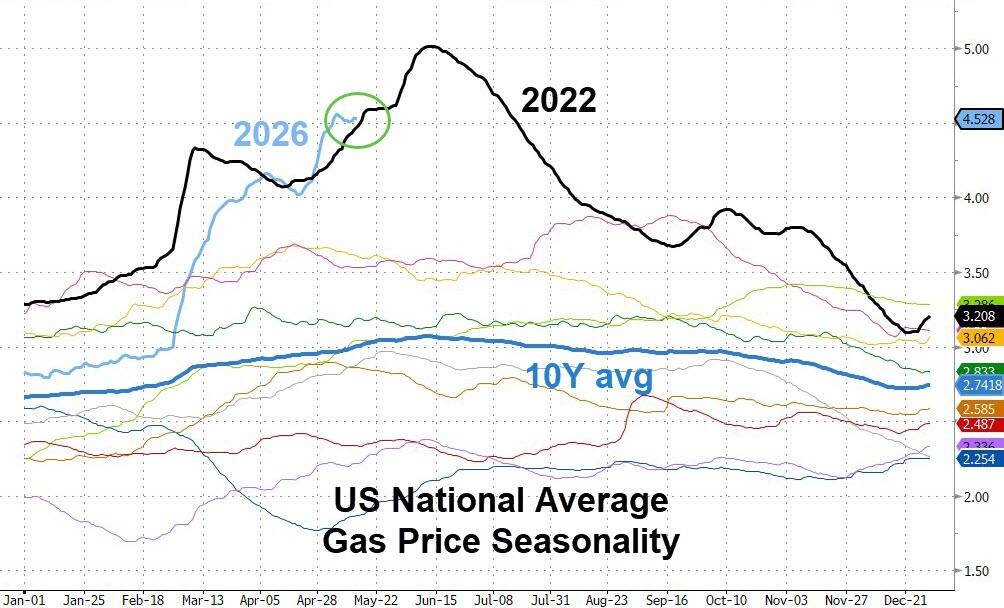

Americans Face The Highest Memorial Day Gas Prices On Record

Americans Face The Highest Memorial Day Gas Prices On Record

The nationwide average price of regular gasoline marginally increased on Thursday, after five straight days of decline, the American Automobile Association (AAA) said in a May 14 statement.

The national average price is “at the same range as it was in 2022, the year gas prices hit record highs. Travelers are preparing to hit the road in record numbers next week, and drivers will be facing the highest Memorial Day gas prices in four years,” AAA said.

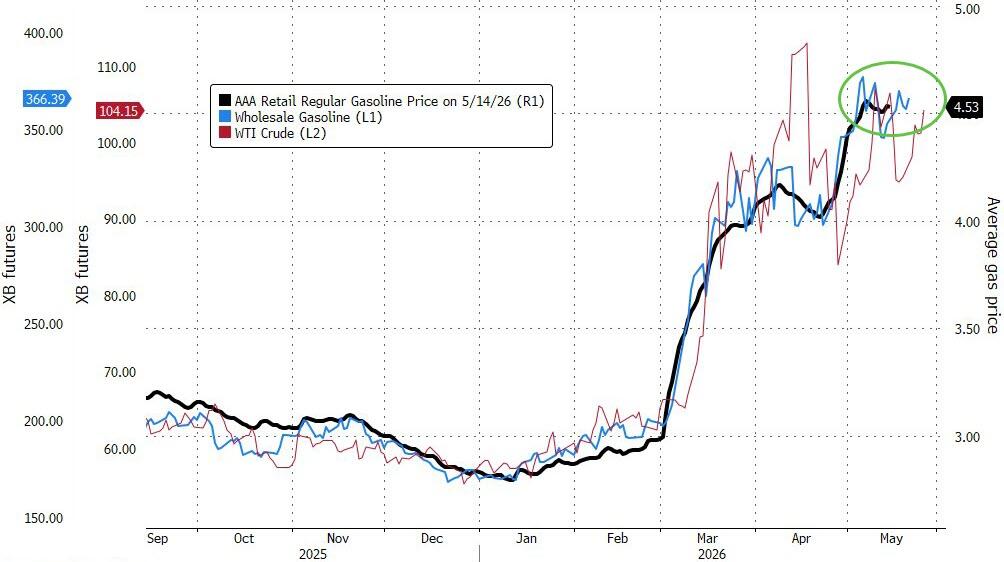

On Friday, prices declined less than a cent to $4.52 per gallon from Thursday’s $4.53. In six states, average gas prices exceeded $5: Illinois, Nevada, Alaska, Oregon, Hawaii, and Washington. Prices exceeded $6 in California. Texas had the lowest price at $3.99 per gallon.

While Thursday’s average gas price was lower than last week’s, prices at the pump continue to remain elevated as crude oil hovers around the $100 per barrel price level.

With prices near record highs as Memorial Day looms, Naveen Athrappully reports for The Epoch Times that the federal government has taken various measures to ease the pressure on gas prices.

On May 11, the Department of Energy (DOE) announced that it would loan 53 million barrels of oil from America’s Strategic Petroleum Reserve to petroleum companies.

“Deliveries will begin immediately as the Department continues to move swiftly to address short-term supply disruptions and strengthen U.S. energy security,” the DOE said.

Earlier, the U.S. government had removed sanctions on Iranian and Russian crude oil stranded at sea to ease the global oil supply shortage.

In late March, the Environmental Protection Agency issued a temporary fuel waiver allowing gasoline with higher ethanol blends to be sold nationwide beginning May 1 to curb rising prices. The waiver will remain in effect until May 20.

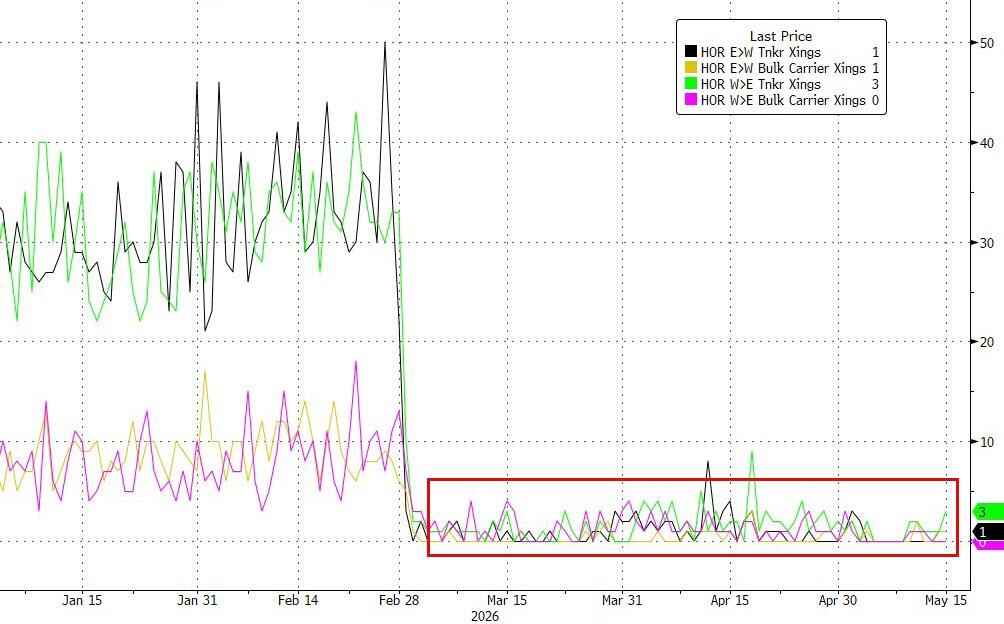

Since the U.S.–Iran war began in late February, Tehran has repeatedly attacked and threatened commercial ships in the critical Strait of Hormuz, a waterway located south of Iran through which over a fifth of global seaborne oil trade is transported. This has disrupted shipments through the strait, pushing oil prices higher.

On Feb. 27, a day before the conflict began, Brent crude oil futures closed the day at around $72 per barrel. On May 15, oil was trading at around $108 as at 9:10 a.m. ET.

Washington and Tehran have yet to negotiate an end to the war, which has kept markets tense and oil prices elevated.

Tight Oil Market

Since the start of the war, crude oil output from OPEC has fallen by more than 30 percent, the group said in a May 13 report.

Current OPEC output is at 18.89 million barrels per day, down from 28.65 million barrels before the conflict broke out. The organization cut its outlook for the year, predicting global crude oil demand would grow by less than 1.2 million barrels per day, down from its previous forecast of 1.4 million barrels per day.

However, “global economic growth continues to show resilience for this year despite geopolitical tensions,” the report said.

In a May 14 post, ING Bank said that the oil market is “eagerly awaiting” the outcome of the meeting between President Donald Trump and Chinese leader Xi Jinping. Trump’s summit in China ended on May 15.

“The market could be pinning too much hope on the US–China talks yielding some positive results on Iran,” ING said.

“Some hope that China could exert pressure on Iran to reach a deal with the US, to end the war and lead to a resumption of energy flows through the Strait of Hormuz.”

Morgan Stanley said in a May 12 report that the risk of prolonged oil supply disruption, especially around the Strait of Hormuz, has now increased.

Prior to the conflict, around 32 ships used to traverse the strait daily between January and March, a number that crashed to roughly two during March–April. There is now a 12 million-barrel-per-day shortage in global oil production.

“While a 12 million barrel-per-day difference may not appear large in a global context, it represents the largest supply shock since the 1970s OPEC oil embargo,” Morgan Stanley said.

“Further, its persistence amplifies the risk of broader economic impacts. Moreover, the timing of this disruption further compounds the issue, with the gasoline-heavy summer driving season (May through August) quickly approaching.”

Tyler Durden

Sun, 05/17/2026 – 09:55

https://www.zerohedge.com/personal-finance/americans-face-highest-memorial-day-gas-prices-record

Market Leadership Is Narrow, Increasing Summer Risk

Market Leadership Is Narrow, Increasing Summer Risk

Authored by Lance Roberts via RealInvestmentAdvice.com,

📈Technical Backdrop – Friday Selloff Tests The Tape

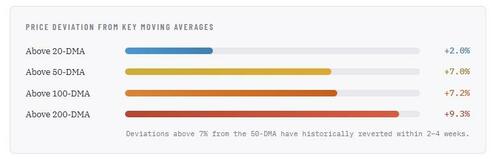

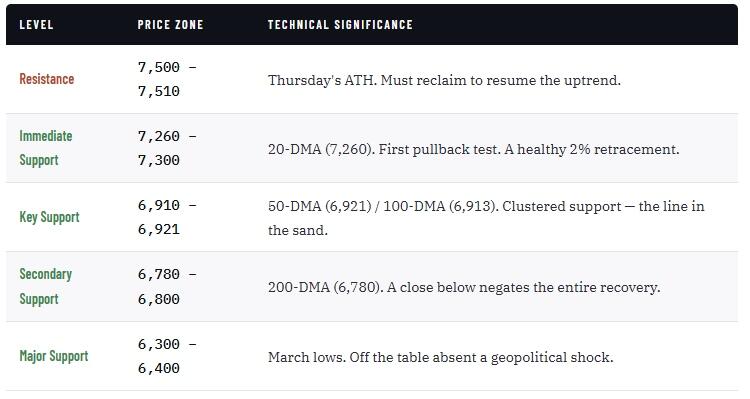

The S&P 500 closed Friday at 7,408.50, surrendering Thursday’s historic first close above 7,500 with a 1.24% decline. The semiconductor names that powered the rally became the source of Friday’s selling. Intel fell 5%, Micron 4%, AMD 3%, and Nvidia 4.4%. From a purely technical standpoint, Friday’s reversal was the first real distribution day in three weeks and the mean-reversion signal we have been flagging.

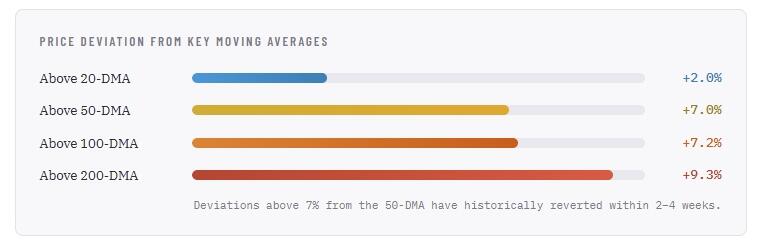

The deviation numbers are the story. At 7.0% above the 50-DMA (6,921) and 9.3% above the 200-DMA (6,780), the index is stretched to a degree that has preceded every meaningful pullback over the past two years. The RSI, however, tells a more nuanced story: at 67.15, it has already pulled back below the 70 overbought threshold. Friday’s selloff did real work in resetting the oscillator. The MACD, while still positive at +1.54, has narrowed significantly from the 40+ readings earlier in the week, with the signal line (148.10) now nearly converging with the MACD line. A bearish crossover is likely on Monday, even if the market stabilizes.

The erratic style rotation we discussed in this week’s Daily Market Commentary, value leading Monday, growth getting slapped Tuesday, then flipping again on Wednesday, intensified into Friday’s close. Single-stock implied volatility is running 2.5x the index VIX, meaning the calm headline masks violent sector-level moves. The gamma feedback loop driving the semiconductor surge works in reverse on the way down: when call flow dries up, market makers sell the underlying to flatten their books. Friday’s action in MU, AMD, INTC, and NVDA is the process beginning.

The bull case: the primary trend is up, the RSI has already pulled back below 70 without breaking any support, and the 20-DMA at 7,260 should attract dip buyers on an initial pullback.

The bear case: the 7% and 9.3% deviations above the 50- and 200-DMAs are extreme, the MACD is on the verge of a bearish crossover, and the gamma unwind in semiconductors has only just begun.

The base case is a pullback toward the 20-DMA (7,260), not a breakdown. A deeper correction to the 50/100-DMA cluster near 6,913–6,921 would represent a 6.6% decline from Friday’s close, painful but technically healthy. Use the 20-DMA as the near-term line: a close below opens 6,921 quickly. Trail stops, take profits in extended names, and use any test of the moving average cluster as an opportunity to add.

💰 Market Leadership Is Narrow

Tech is carrying the tape. Most other sectors aren’t. Here’s what history says about that setup, and how we’re positioning around it.

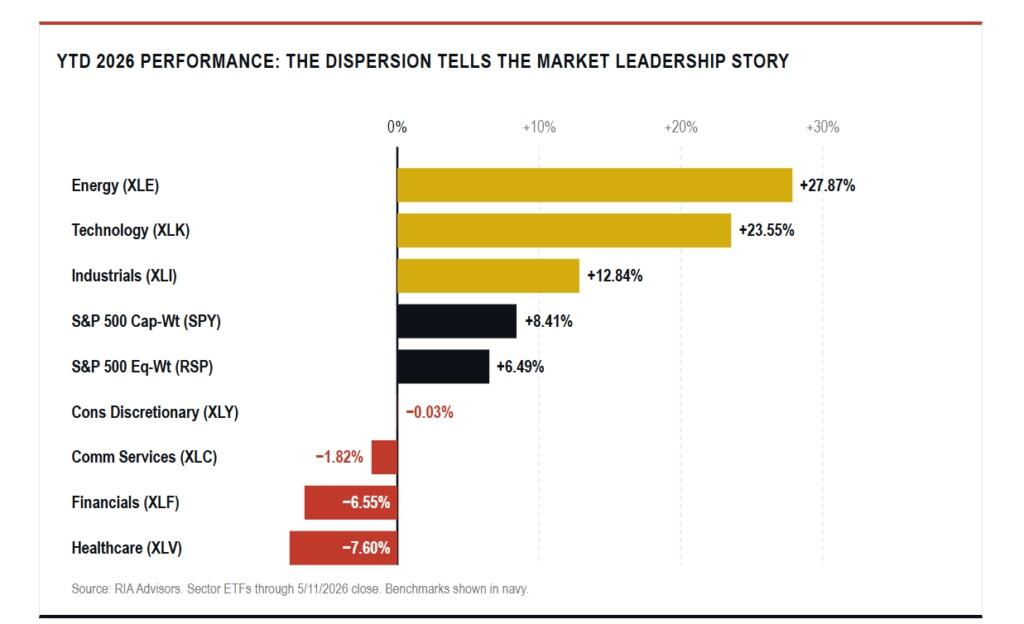

Look under the hood of this year’s rally and the tape isn’t nearly as healthy as the headline number suggests. The S&P 500 sits up roughly 8.4% year-to-date through Friday’s close, but the strength is being carried by a small group of sectors doing all the heavy lifting. Technology is up north of 23%. Healthcare is down almost 8%. Financials have given back more than 6%. Equal-weight, which gives every name an identical vote, has only managed about 6.5%. That gap is the story of 2026 so far, and the story has a name. Narrow market leadership. We’ve seen this movie before, and the ending is rarely as clean as the bulls would like to believe.

Chart of Equal Vs Market Cap Weight

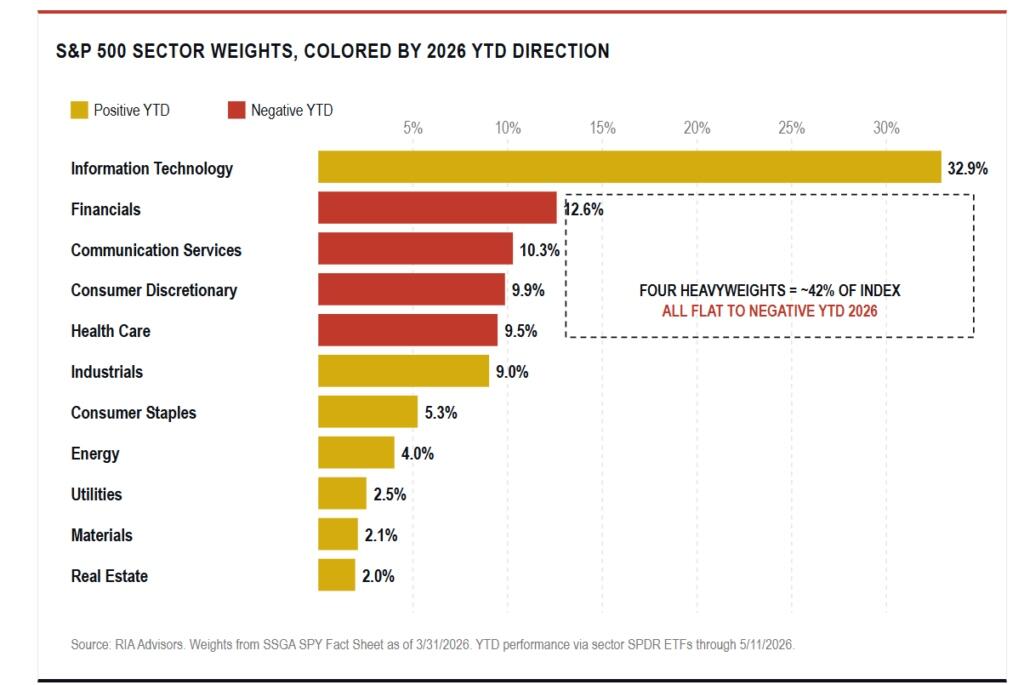

The clearest sign of narrowing market leadership is the spread between the cap-weighted S&P 500 and the equal-weight version. The cap-weighted index, where Apple, Microsoft, Nvidia, and a small group of mega caps carry outsized weight, has outpaced equal-weight by roughly 200 basis points in just over four months. That sounds modest until you remember both indices hold the same 500 companies. The entire performance gap is a weight effect. A handful of names are doing the work for the whole index.

Drill into the table, and the picture sharpens. Technology and Energy are doing the bulk of the index’s heavy lifting, but the way they’re doing it matters. Energy carries just over 4% of the S&P 500 by weight. That’s one of the smallest slots in the index. The sector is the year’s best performer at nearly 28%, but at a 4% weight, even a stellar return only adds about a percentage point to the index. Technology is the opposite story. Tech accounts for roughly a third of the index by weight, and at +23.5% YTD, it alone accounts for the better part of three-quarters of the year’s gain. Strip Tech out, and what’s left of 2026 looks closer to a market in retreat than a market grinding toward new highs.

The bigger problem lies with the heavyweights who aren’t pulling. Financials, the second-largest sector at almost 13% of the index, are down 6.5% year to date. Healthcare, the fifth-largest at 9.5%, has dropped almost 8%. Communication Services at roughly 10% is slightly negative. Consumer Discretionary at nearly 10% is flat. Those four sectors together represent more than 40% of the S&P 500 by weight, and, as a group, they’re a drag rather than a contributor. The bull market isn’t getting help from the heavyweights that should normally be participating, and the dispersion chart above is the visible result.

Here’s why that matters. Sustainable bull markets pass the baton. When Tech gets tired, Financials or Industrials step up. When growth stumbles, value takes over. Right now, the second, third, fourth, and fifth largest sectors of the index aren’t passing the baton. They’re sitting it out. Without those sectors starting to lead, or at minimum starting to participate, this bull market becomes much harder to sustain. The index can ride one sector for a stretch. It can’t ride one sector forever, and that’s exactly what narrow market leadership looks like before it cracks. This isn’t a broad bull market. It’s a Tech-led tape with a thinning bench underneath.

Historical Precedents For Narrow Market Leadership

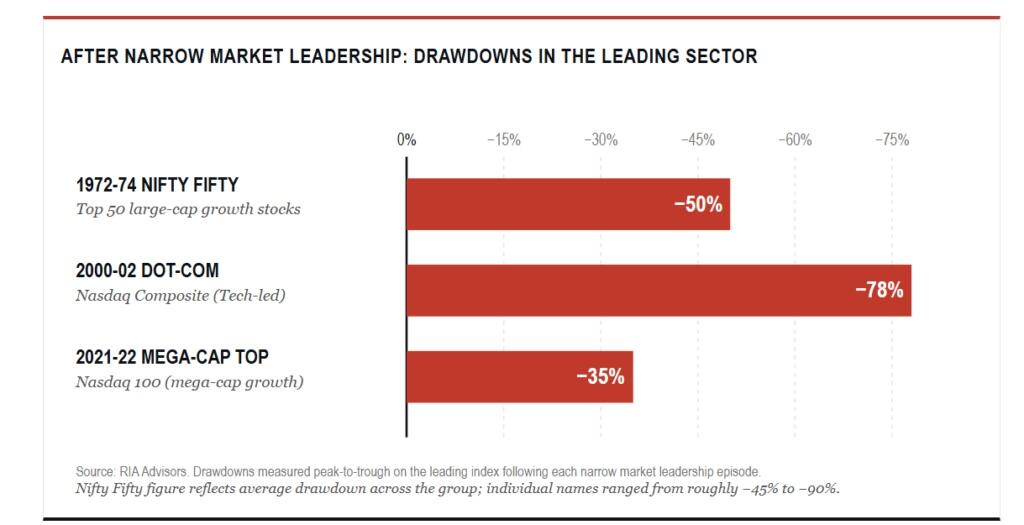

History gives us several clean playbooks for what happens when market leadership concentrates this aggressively into one or two sectors. The first is the Nifty Fifty of the early 1970s. Roughly fifty large-cap growth names carried the index higher into 1972 while the average stock had already started rolling over. When the bear market hit in 1973-74, the Nifty Fifty names lost 45% or more, and the broader index drew down nearly half its value, as participation had been weakening for months beforehand.

The second is the late-1990s dot-com era. By 1999, technology was running away from every other sector. Breadth deteriorated sharply through the back half of that year. The advance-decline line peaked well before the S&P did. When the unwind came in 2000, the Nasdaq lost 78% of its value over the following two and a half years. Importantly, defensive sectors actually outperformed through the worst of it. The third, and the one most relevant for current conditions, is 2021. Mega-cap technology drove the indices to fresh highs while small caps and cyclicals quietly topped out months earlier. The Russell 2000 peaked in November 2021. The S&P 500 didn’t peak until January 2022. The market then spent most of 2022 catching down to what breadth had already been telling investors.

In every one of those cases, narrow market leadership wasn’t the cause of the downturn. However, it was a reliable warning that the underlying participation was thinning out before price followed.

“Investors who own the cap-weighted index right now think they’re diversified across 500 names. In practice, they own a concentrated bet on roughly ten companies with 500 tickers attached.”

What Narrow Market Leadership Tells Us About Risk

Make no mistake, narrow market leadership isn’t an automatic sell signal. Markets can run further than seems reasonable when momentum and passive flows pile into the same names. The 2024-2025 mega-cap run is a recent reminder. But narrow market leadership changes the index’s risk profile in a way most investors don’t appreciate.

Here’s the problem. The same passive flows that drive mega caps higher on the way up reverse on the way down. When the largest weights sell off, they drag the index down, and the already-thin breadth gets even thinner. Drawdowns under narrow market leadership tend to be deeper and faster than drawdowns from broad-based rallies, because there’s no rotation to absorb the selling. Volatility behaves differently, too. When leadership is wide, sector rotation cushions the index. When it isn’t, the index moves with whatever the top five names are doing. Risk goes up. Most investors don’t see it.

The fingerprints of that risk are clear when you look at how far the leading themes have moved from their long-term means. Reversion is mathematical, not optional. Eventually, prices come back to their averages, and when the deviation gets this stretched, the round trip is rarely small. The table below lists the most extended subsectors of the current market leadership rally, the 200-week moving average for each, and the percentage decline required to reset to that average.

Read the right-hand column. These aren’t 10% pullback numbers. Semiconductors and Quantum themes would need declines in the 50% to 60% range just to touch their 4-year means. The broad Technology sector, the heaviest weighting in the S&P 500, would have to give back roughly 40% to do the same. The Momentum factor itself sits 57% above its long-term mean, indicating the entire momentum trade is concentrated in the same overextended names. Energy, despite leading the year, looks comparatively reasonable at 29% above the mean. Mean reversion isn’t a forecast. It’s an arithmetic statement about how much price has been pulled forward into the current market leadership names. The deeper the deviation, the bigger the eventual round trip.

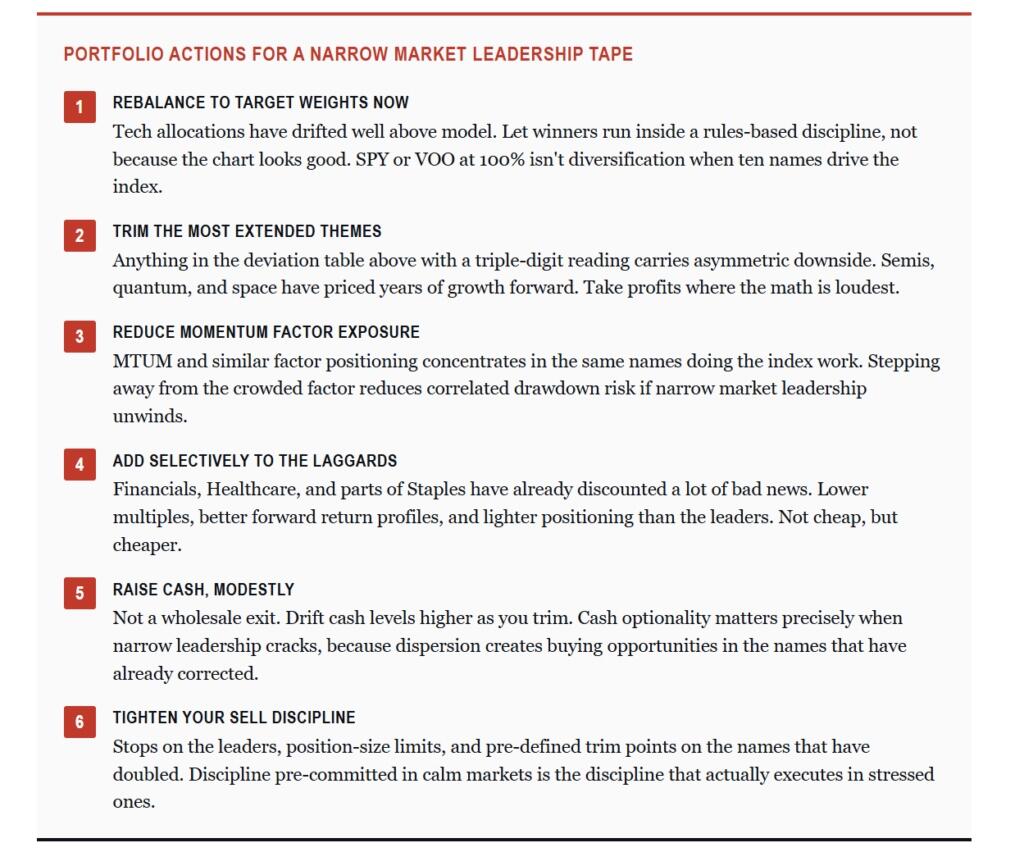

How To Position Around Narrow Market Leadership

What does this mean for portfolios? Pull the threads together. Tech alone accounts for roughly three-quarters of the index’s gain this year. The four heavyweight sectors below, which together account for more than 40% of the S&P 500, aren’t participating. The historical record for narrow market leadership runs to drawdowns of 35% to 78% in the leading sector. And the most extended themes inside this rally sit 50% to 145% above their long-term means. That’s the setup. The setup dictates the response.

This isn’t about predicting the top. It’s about making sure portfolios reflect what’s already been pulled forward. The actions below are what we’re doing in client books right now.

None of this requires calling the top. We aren’t bearish on the bull market. We are bearish on the assumption that this market leadership will remain durable for another 12 to 18 months without a meaningful reset. The arithmetic of mean reversion and the historical record of narrow tapes both point to the same conclusion.

Position accordingly.

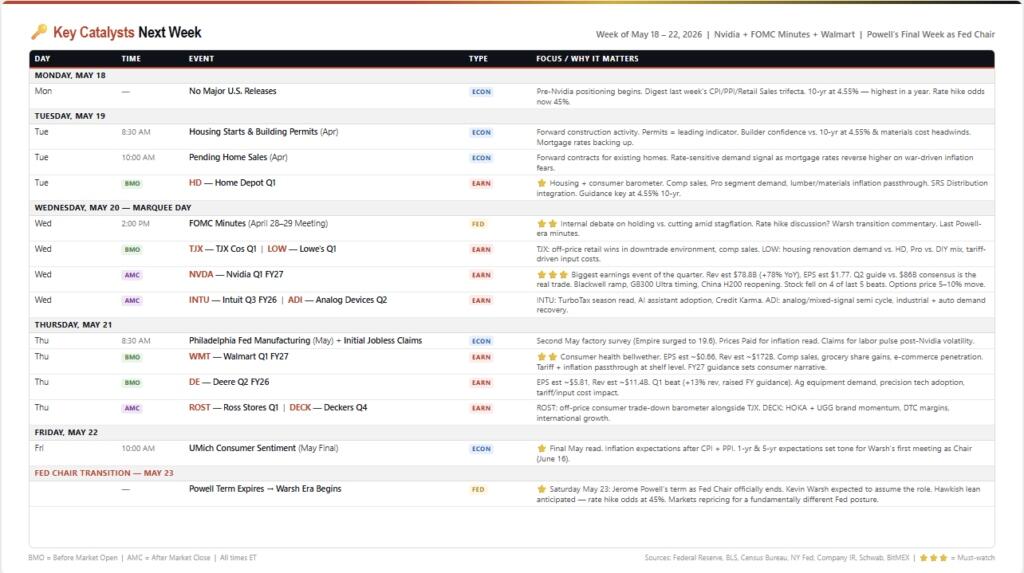

🔑 Key Catalysts Next Week

This is the most important week of Q2 and possibly the year. Nvidia reports Wednesday after the close; the FOMC Minutes land Wednesday afternoon; Walmart opens Thursday morning; and Jerome Powell’s fourteen-year tenure at the Federal Reserve ends Saturday. Each of these events alone would dominate a normal week. Together, they arrive at a moment when the 10-year Treasury yield has surged to 4.55%, the highest in a year, and rate hike probabilities have climbed from 1% a month ago to 45% today. The regime is shifting in real time.

However, Wednesday is a collision day that will define the markets next week. The FOMC Minutes from the April 28–29 meeting drop at 2:00 PM, and they arrive carrying a question the market has never had to ask in this cycle: did anyone on the committee discuss raising rates? With core CPI reaccelerating, oil elevated by the Iran conflict, and the 10-year yield climbing, the minutes will reveal whether the internal conversation has shifted from “when do we cut” to “do we need to hike.” Any hawkish surprise, even a single paragraph acknowledging that hikes were discussed, would detonate the rate-sensitive trade.

Three hours later, Nvidia reports Q1 FY2027. Consensus expects $78.8 billion in revenue, 78% year-over-year growth, and $1.77 in EPS, both above the company’s own $78 billion guidance. But the Q1 number is almost beside the point. The real trade is the Q2 guide versus the $86 billion consensus, Blackwell ramp and GB300 Ultra timing, and any commentary on China H200 reopening after the export restrictions effectively zeroed out Chinese data center revenue. The stock has fallen on four of its last five earnings beats, and options are pricing a 5–10% move, in either direction.

Thursday is the consumer verdict. Walmart before the open is the definitive Main Street read. Estimated revenue is $172 billion, grocery share gains, e-commerce penetration, and critically, how much tariff and inflation costs are being passed through at the shelf level versus absorbed in margin will be key. This is where we learn whether the consumer held up through $100 oil and 4.55% Treasury yields or started to crack. Walmart’s full-year guidance will set the consumer narrative for Q2.

Bottom line: Nvidia tells us whether the AI capex cycle is still accelerating. The FOMC Minutes tell us whether the Fed is considering tightening. Walmart tells us whether consumers are surviving. And Saturday, a new Fed Chair takes over with a fundamentally different worldview. This is the week the narrative for the rest of 2026 gets written. Hedge your book before Wednesday at 2:00 PM.

Trade accordingly.

Tyler Durden

Sun, 05/17/2026 – 09:20

https://www.zerohedge.com/markets/market-leadership-narrow-increasing-summer-risk

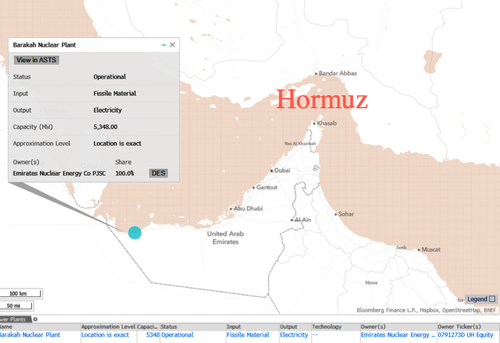

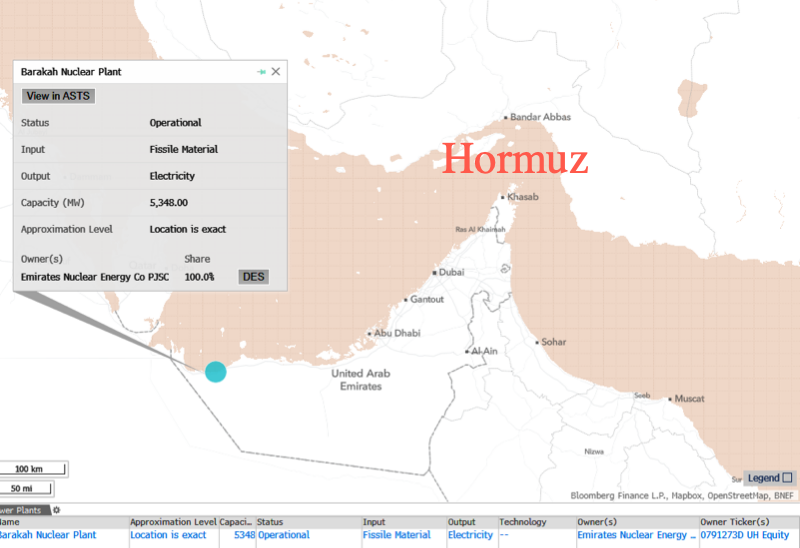

Attack Drone Hits Near UAE Nuclear Power Plant

Attack Drone Hits Near UAE Nuclear Power Plant

Abu Dhabi authorities report that a kamikaze drone struck an electrical generator outside the inner perimeter of the Barakah Nuclear Power Plant in Al Dhafra. Officials said there were no injuries, no impact on radiological safety levels, and no disruption to plant operations.

Dubai-based newspaper Gulf News cited the Federal Authority for Nuclear Regulation, which said the one-way drone attack on the Arab world’s first commercial nuclear facility did not affect the safety of the nuclear power plant or the readiness of its essential systems. FANR added that all systems were operating normally as of late Sunday.

Barakah operates four APR-1400 reactors with a combined capacity of 5.6 gigawatts, generating about 40 terawatt-hours annually, or about 25% of the UAE’s electricity. Any successful attack on Barakah would cripple the UAE’s power grid.

The incident comes as the broader U.S.-Iran truce remains fragile, with President Trump recently describing the ceasefire as being on “life support.”

Trump told reporters on Friday that Iran’s latest proposal was “unacceptable” and blamed the Iranians for backtracking on the nuclear issue.

In response to Iranian demands, the Trump administration has set five conditions of its own for Tehran, according to Iran’s Fars News Agency.

Those conditions include:

No U.S. compensation for damages

Transfer of 400 kg of uranium from Iran to the United States

Limiting Iran’s nuclear activities to only one operating facility

No release of even 25% of frozen Iranian assets

Linking any ceasefire across all fronts to the continuation of negotiations

Here are the latest headlines from the Gulf region (courtesy of Bloomberg):

Peace Talks

The US has set five main conditions for a prospective peace agreement with Iran, including no compensation payments, removal of 400 kilograms of uranium, limiting nuclear infrastructure to a single facility, releasing less than 25% of frozen assets, and suspension of certain activities. [BFW]

Iran’s foreign minister said a lack of trust is the biggest obstacle in negotiations to end the war with the US, citing contradictory messages that have made Tehran reluctant about American intentions. [APW]

Iran would be open to diplomatic help, particularly from China, to help ease tensions. [APW]

Hormuz Chokepoint

Iran said transit through the Strait of Hormuz will flow once the conflict with the US and Israel is over, but the sides are no closer to resolving their differences. [BN]

Commercial shipping through the Strait of Hormuz remains largely frozen, with only limited vessel movements observed and most tied to Iranian-linked shipping. [BN]

A Vietnam-bound supertanker carrying 2 million barrels of Iraqi crude, which was halted by US forces after crossing the Strait of Hormuz, has resumed its journey after getting clearance. [BN]

Gulf Attacks

A drone strike caused a fire at an electrical generator outside Abu Dhabi’s Barakah nuclear power plant on Sunday, with no injuries reported and no impact on radiological safety. [BFW] [APW]

The United Arab Emirates and Saudi Arabia carried out multiple strikes against Iran after their countries were attacked by the regime in the early days of the war. [WSJ]

Iran seized a support vessel owned by a Chinese security firm near the Strait of Hormuz, appearing to signal it is unwilling to permit armed protection even for ships sailing on behalf of its strongest global backer. [WSJ]

Economic Impact

Iraq is currently pumping just 1.4 million barrels a day due to the closure of the Strait of Hormuz and the knock-on impact on production facilities.

Israel’s economy contracted 3.3% in the first quarter in annualized terms, deeper than the expected 2% drop, due to security-related shutdowns from the war with Iran.

The Philippines’ gross gaming revenue fell 16% in the first quarter due to economic headwinds from the Iran war impact. [BFW]

Diplomatic Signals

Iranian Parliament Speaker Mohammad Bagher Ghalibaf has been named Iran’s special envoy for China affairs. [BFW]

President Trump returned from a two-day summit with China’s Xi Jinping, where both agreed the strait should be open but made no apparent progress toward that goal. [BN]

Energy Market

Why One Bank Thinks It’s “Magical Thinking” That Hormuz Reopens In June

Brent Crude

Professional subscribers can read the latest Hormuz reports from Wall Street at our new Marketdesk.ai portal.

Tyler Durden

Sun, 05/17/2026 – 08:59

https://www.zerohedge.com/geopolitical/attack-drone-hits-near-uae-nuclear-power-plant

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}