Category: News

Fewer Universities Require DEI Pledges From Faculty Candidates: Report

Fewer Universities Require DEI Pledges From Faculty Candidates: Report

Authored by Aaron Gifford via The Epoch Times (emphasis ours),

Requests related to diversity, equity, and inclusion (DEI) for faculty job candidates in higher education have decreased dramatically – at least on paper – since President Donald Trump began his second term, a new report from Heterodox Academy says.

This includes the removal of required pledges in cover letters or standalone essays regarding a commitment to DEI. Eleven percent of college and university faculty job listings specified such requirements between August and December of 2025, a decline from 25 percent the previous year, the April 21 report said.

Heterodox Academy, a nonprofit that advocates viewpoint diversity in higher education, analyzed advertisements for more than 20,000 faculty positions posted on HigherEdJobs.com between August and December in the last two years. The website compiles job openings from colleges and universities in every state.

All told, 37 percent of faculty job ads during the fall 2025 semester did not specifically address DEI regarding application materials, but still “signaled that a commitment to DEI will be valued,” the report said.

Additionally, Heterodox Academy researchers found that DEI statements are more likely to be required at schools in the northeast or near the West Coast. The mandate is also more likely at private institutions than public ones, though it has decreased at both since 2024, and is more common found in the humanities disciplines than in STEM (science, technology, engineering, and math) majors, the report said.

Only 13 percent of the faculty job ads reviewed mentioned viewpoint diversity, the report said, “suggesting that universities continue to emphasize demographic diversity rather than other potential dimensions of diversity such as intellectual heterogeneity.”

Heterodox Academy largely attributes the dramatic decline of DEI requirements for faculty candidates to Trump’s policies.

Early last year, the president issued an executive order prohibiting the use of DEI in student admissions and college and university hiring, in accordance with existing Civil Rights laws prohibiting discrimination based on race. The administration initiated investigations into the wealthiest higher education institutions and cautioned that violators could lose federal funding.

In the weeks that followed, the Department of Education sanctioned several schools accused of discriminatory practices in employment, student admissions, and maintaining DEI programs like mandatory training and affinity groups. Several of them paid tens of millions of dollars in penalties and agreed to conditions set by the federal government, while Harvard University pushed back and has litigation ongoing against the Trump administration.

Trump also asked university administrations to certify that they are not violating anti-discrimination laws, and some schools were offered a compact that promised preferred consideration for federal funding if they committed to ending any remaining DEI initiatives, required SAT scores from student applicants, limited undergraduate admission of foreign nationals to 15 percent, and pledged a policy of institutional neutrality.

Seventeen states, meanwhile, passed laws banning the use of diversity statements in hiring, the report said.

Colleges and universities across the country have scrubbed any mention of DEI from their websites, substituting terms like “office of belonging” or “campus culture.”

Peter Wood, president of the National Association of Scholars and a former professor and administrator at Boston University, said he’s skeptical that higher education is ending its deep-rooted commitment to DEI.

He applauded Heterodox Academy for its research, calling this public acknowledgement a step in the right direction, and said the methodology is sound. Still, “counting mentions of DEI in job advertisements is a long way from what universities are actually doing.”

Removing the three letters or words from job ads, much like renaming DEI functions to something like the office of belonging, doesn’t make a dent in a decades-long, entrenched culture in so many university programs where racial preferences in hiring are still considered essential, and administrators and faculty committees presume that most of the applicants share their liberal, progressive ideology, Wood told The Epoch Times.

“There’s certainly a wink and a nudge that if you want a job here, you better make nice on this front,” he said. “I don’t think they’ve changed these jobs one iota. Senior administrators need to be really convinced that it [DEI] was a mistake and it’s time to move beyond it.”

Tyler Durden

Fri, 04/24/2026 – 11:05

https://www.zerohedge.com/political/fewer-universities-require-dei-pledges-faculty-candidates-report

Scramble For AI Compute: Meta Inks Multibillion-Dollar Deal With Amazon For CPU Chips

Scramble For AI Compute: Meta Inks Multibillion-Dollar Deal With Amazon For CPU Chips

Meta Platforms inked a multibillion-dollar agreement with Amazon to deploy tens of millions of AWS Graviton processor cores in support of its next-generation AI buildout. The deal makes Meta one of the largest Graviton customers globally and shows CEO Mark Zuckerberg’s willingness to spend aggressively on compute infrastructure as the AI arms race intensifies with Alphabet, Microsoft, and other tech giants.

The news that the social media giant would deploy hundreds of thousands of Amazon’s general-purpose chips to “support the company’s AI efforts” was first reported by Amazon News.

“The chips will power various workloads at Meta, including supporting the company’s AI efforts. That work requires infrastructure that can handle billions of interactions while coordinating complex, multi-step agent workflows—exactly the kind of CPU-intensive work Graviton is designed for,” the release stated.

The deal also expands Meta’s long-running AWS partnership and builds on its large-scale use of Amazon Bedrock. While GPUs remain essential for training large AI models, Amazon noted in the release that the “rise of agentic AI is creating massive demand for CPU-intensive workloads.”

The press release did not reveal the value of the Meta-Amazon deal on expanding compute. But in recent weeks, Zuckerberg has signed deals totaling $48 billion with CoreWeave and Nebius, both of which rent out access to Nvidia GPUs that run AI models.

To expand computing capacity, Meta has announced a workforce restructuring, with its latest plan calling for layoffs of around 8,000 employees, or about 10% of its workforce. Microsoft has done the same (read report).

“Meta has, as you can imagine, access to so many options from the supply side. But they chose Graviton5, our 3-nanometer chip, for price performance,” Nafea Bshara, an Amazon vice president and distinguished engineer, said, who was quoted by The Wall Street Journal. He said the length of the deal is between three and five years.

Meta shares are marginally higher in premarket trading, while Amazon trades up nearly 2% following the news.

Tyler Durden

Fri, 04/24/2026 – 10:45

Getting More Anxious

Getting More Anxious

By Bas van Geffen, Senior Macro Strategist at Rabobank

We have another potentially eventful weekend ahead of us. A three-week extension of the ceasefire between Israel and Lebanon may ease tensions between the US and Iran somewhat, as Trump wants to avoid that this conflict undermines peace talks with Iran. However, there are still no indications that a new round of talks will be held, as both sides continue to blockade the Strait of Hormuz.

Iran has continued to shoot at commercial ships that tried to navigate the strait, and US President Trump posted that he had “ordered the United States Navy to shoot and kill any boat […] that is putting mines in the waters of the Strait of Hormuz,” after the IRGC reported that the Iranian navy has laid more mines in the strait. So, President Trump may have extended the ceasefire earlier this week, but it remains a relative one. A tanker laden with Iranian oil is reportedly attempting to cross the strait today, perhaps testing the US’ resolve. That’s bound to add to tensions between both sides.

If talks do not happen soon, either side may revert to escalation. Recall that Axios reported earlier this week that the US maintains an unofficial three-to-five-day deadline for Iran to end its internal power struggle and get back to the table. If true, that deadline could expire on Sunday. Israel’s Channel 12 reported that Speaker of the Parliament Ghalibaf has resigned from the negotiating team due to these internal rifts, but Iranian reporters are contradicting these accounts.

It seems that the lack of talks is gradually starting to weigh on energy markets. Oil prices have crept higher over the week, with a barrel of Brent now trading around $106 in the futures market. Still, we remain surprised at the relative tranquillity in the energy space. As our energy strategists underscored in their latest note, “futures markets are still materially underpricing the real supply risk facing both crude oil and natural gas.”

On that same tune, the Bank of England warned that global equity prices may not reflect all the risks that face the global economy. Markets are at, or near, their all-time highs, despite these risks. Deputy Governor Breeden said that the Bank expects “an adjustment [of equity prices] at some point.”

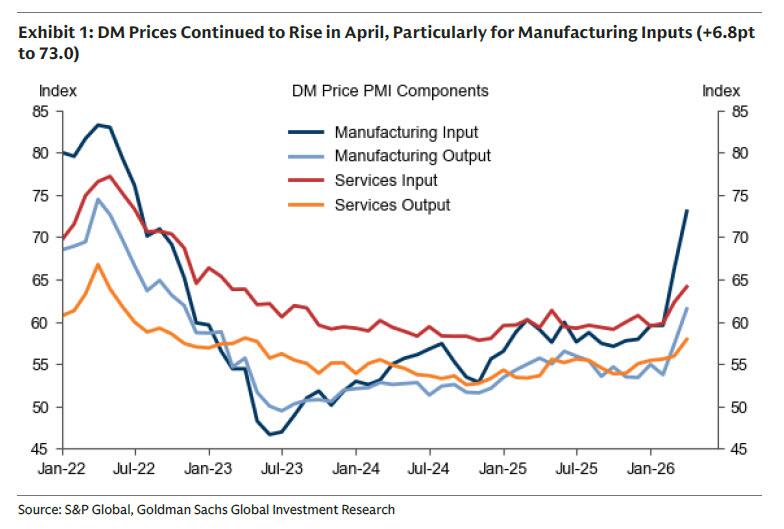

Still, the muted response in markets has lessened the urgency for central banks to act, as policymakers around the world prepare for their next policy decisions. Those policymakers who would prefer to hike will have to convince their peers of the necessity. Just a couple of weeks ago, they might have been able to make a strong case for an April hike. However, the longer the conflict in the Middle East remains unresolved, the bigger the stagflationary impact will be. We have therefore shifted our call for an ECB hike to June, but conviction remains relatively low amidst the fog of war.

An inflation shock seems unavoidable now, and the key question is the intensity and duration. In addition to the anecdotal evidence of ripple effects on various supply chains, data are now starting to flag the economic damage too. The Eurozone PMI data came in mixed yesterday, with the French manufacturing sector above expectations and German manufacturing more-or-less in line. However, these headline prints are overstating the resilience of the sector. Manufacturers reported a large inflow of orders, ahead of expected shortages and price increases. So, this appears to be an attempt at stockpiling before the impact of the war becomes more widespread.

By contrast, the Eurozone services PMI fell to 47.4. Survey respondents reported lower output. We would argue that this services survey better reflects the decline in consumer confidence and business optimism, and their willingness to spend.

The PMIs also indicated that cost pressures continue to build “considerably.” Input prices increased further, particularly in manufacturing. But services providers also noted that higher transportation costs are affecting their business. So far, the passthrough to output prices remains limited. Nonetheless, output prices increased at the fastest rate in three years. And, as margins get squeezed further, companies may be forced to passed on more of the cost pressures in the coming months.

Adding further global inflationary pressures, Chinese exporters have begun to raise their prices on “everything from swimsuits to air conditioners,” as oil and oil-related inputs are causing higher production costs across the globe.

Tyler Durden

Fri, 04/24/2026 – 10:25

DOJ Drops Criminal Probe Of Powell Into Fed Building Costs

DOJ Drops Criminal Probe Of Powell Into Fed Building Costs

The Department of Justice is dropping its criminal investigation into Federal Reserve Chair Jerome Powell, ending a standoff that threatened to delay the confirmation of Powell’s successor at the central bank

In a post on X, US Attorney General for DC Jeanine Pirro said she is directing her office to close its investigation of Federal Reserve Chair Jerome Powell as the inspector general for the agency has been asked to scrutinize its building construction project costs,

This morning the Inspector General for the Federal Reserve has been asked to scrutinize the building costs overruns – in the billions of dollars – that have been borne by taxpayers.

The IG has the authority to hold the Federal Reserve accountable to American taxpayers. I…

— US Attorney Pirro (@USAttyPirro) April 24, 2026

According to ABC, senior DOJ officials had contacted senators in recent days, including Republican Sen. Thom Tillis. who sits on the Senate Banking Committee, informing them of the plan to drop the probe and refer the matter regarding alleged cost overruns at the Fed’s Washington headquarters to the bank’s internal watchdog, the sources said.

The Fed’s independent inspector general conducted an audit of the building renovation costs in 2021 and Powell had already asked the watchdog to take a fresh look at the $2.5 billion project last year.

Powell’s term ends next month, but he said in March that he would stay in the position until President Donald Trump’s pick to lead the Fed, Kevin Warsh, is confirmed. Which is also the reason why the DOJ decided to drop its case as the last thing Trump needed was more confusion over when Warsh would take over.

A spokesperson for the Federal Reserve declined to comment. Reached by ABC News, a spokesperson for Tillis declined to comment.

A Justice Department spokesperson did not immediately respond to a request for comment from ABC News.

Tyler Durden

Fri, 04/24/2026 – 10:19

https://www.zerohedge.com/markets/doj-drops-criminal-probe-powell-fed-building-costs

Kremlin Hails Putin Invite To G20 Summit In Miami, After Trump Said His Presence ‘Very Helpful’

Kremlin Hails Putin Invite To G20 Summit In Miami, After Trump Said His Presence ‘Very Helpful’

The G20 Miami summit is set to take place at Trump National Doral Golf Course and will focus on “unleashing economic prosperity by eliminating burdensome regulations, unlocking affordable energy and pioneering new technologies,” according to President Trump’s words.

Amazingly and quite surprisingly, the Russian Foreign Ministry has announced Russia has been invited to take part “at the highest level” – meaning President Vladimir Putin has been invited, per the Kremlin. The actual date is still far away, slated for Dec. 14-15, 2026.

G20 image, via Atlantic Council

But the fact that this has hit The Washington Post is sure to seriously raise eyebrows among European allies, as well as evoke the ire of Democrats in the US.

“President Trump has been clear that Russia is welcome to attend all G20 meetings as the United States focuses on delivering a successful and productive summit,” a Kremlin spokesperson said in response to the alleged invitation. Here’s what the Washington Post freshly reported:

The United States intends to invite Russian President Vladimir Putin to the Group of 20 leaders’ summit scheduled for December at President Donald Trump’s Doral golf resort in Miami, though the invitation has not yet been sent, administration officials said Thursday.

Moscow’s statements could be in response to what thus far has been only an informal or verbal invite, or in response to the emerging reports this week.

Russia’s Deputy Foreign Minister Alexander Pankin told journalists at the UN Headquarters that Moscow will confirm who it will send at a later date.

Europe would certainly receive it as a shock and surprise, given that Putin is directly banned from entering most European countries, given the International Criminal Court arrest warrant against him.

Trump on Thursday had told reporters that he was unaware of any personal invitation to Putin but did stipulate that it would be “probably very helpful” if the Russian leader attended.

Trump as of Thursday at the Oval Office:

Trump:

I haven’t invited Putin to the G20, but if he came, it would probably be very helpful. pic.twitter.com/Sku1okEP2x

— Clash Report (@clashreport) April 23, 2026

Putin did of course travel to American soil for the Alaska summit at Trump’s personal invitation in August 2025, hoping to forge some kind of breakthrough toward Ukraine peace. But direct negotiations with the Zelensky government proved elusive and is now frozen as a possibility.

Russia remains officially part of the G20, but the last time Putin attended the summit was all the way back in 2019, in Osaka, Japan. Since the Ukraine war started, Putin’s travel has been limited mostly to the Asian continent.

Tyler Durden

Fri, 04/24/2026 – 10:05

JetBlue Sued For Allegedly Using Customers’ Personal Data To Hike Air Fares

JetBlue Sued For Allegedly Using Customers’ Personal Data To Hike Air Fares

Authored by Mary Prenon via The Epoch Times (emphasis ours),

JetBlue Airlines has been sued in a class action lawsuit seeking damages for allegedly using consumers’ personal data to increase airfares.

The case was filed on Wednesday in the U.S. District Court in the Eastern District of New York.

Brought by plaintiff Andrew Phillips of New York, the litigation states that Phillips booked his ticket on JetBlue’s website, which included a flight from New York to Florida. As required, he provided his contact and payment information, as well as desired airfare and accommodations, according to the lawsuit. However, Phillips was unaware that the airline’s tracking code had also collected and provided other information to a third party.

According to the lawsuit, JetBlue has historically used consumer data to make assumptions about the consumer that could impact pricing.

“The ‘Operating System and Platform’ a consumer uses may seem benign—but it is commonly weaponized as a means to tell the socioeconomic status of a consumer, as those who use Apple’s iOS operating system and platforms are often wealthier than those who use an Android operating system and platform,” the lawsuit states.

In addition, the airline allegedly collected information about consumers’ geographic locations that allow them to adjust prices based on someone’s zip code or socioeconomic class based on where they live.

“This is all highly concerning,” the litigation states. “It allows Defendant to manipulate prices in real time in order to make as much money as they can on fares for airline tickets which are priced differently for consumers based on their private information, which they did not consent to surrender for this purpose.”

The lawsuit also cites a conversation between JetBlue’s X account and a customer, arguing that it suggests the company may use customer data in connection with ticket pricing.

In the exchange, the customer wrote, “I love flying @JetBlue but a $230 increase on a ticket after one day is crazy. I’m just trying to make it to a funeral.”

“Try clearing your cache and cookies or booking with an incognito window. We’re sorry for your loss,” the JetBlue account replied.

“The picture becomes clearer considering JetBlue itself admitted to using cookie collected data on its booking pages in order to adjust airfare pricing,” the lawsuit states.

In a statement to The Epoch Times, JetBlue Corporate Communications said the company does not use personal information or web browsing history to set individual pricing.

“Fares are determined by demand and seat availability, and all customers have access to the same fares on jetblue.com and our mobile app,” the statement said.

Regarding the X conversation, JetBlue said, “The recent social media reply was simply a mistake from an individual customer service crewmember. The steps the crewmember suggested would not have changed the airfares available for purchase.”

JetBlue is further accused of sharing this information with other third parties, such as FullStory, a digital intelligence firm that captures user interactions such as website page views and clicks.

The airline is accused of allowing these third parties to use tracking technologies to collect information on consumers and use those same technologies to analyze consumer background and behavior to change prices.

The documents state that JetBlue also uses PROS, an AI-based travel tech firm, which sets prices through algorithms, based on consumer data.

“None of this would have been possible had JetBlue not been collecting this data in the first instance: let alone sharing it with third parties like FullStory, PROS, and others,” the lawsuit states.

While “surveillance pricing”—the use of personal data to determine what a consumer is willing to pay—is not illegal in the United States, secretly collecting consumer data without consent is, the lawsuit states.

According to the litigation, members of Congress have also raised concerns about the allegations. A letter from Sen. Ruben Gallego and Rep. Greg Casar asked JetBlue to clarify whether it uses personal data to set fares.

“We are especially concerned that customers could be charged different prices for the same flight based on their need for travel, such as attending a funeral,” the letter stated, according to the lawsuit.

Among the accusations against JetBlue Airways is a violation of the Electronic Communications Privacy Act, which makes it illegal to intentionally intercept any consumer communication or to disclose or use the contents of an unlawfully intercepted communication.

The airline is also accused of violating New York’s deceptive trade practices and unlawful selling laws.

The plaintiff is requesting a jury trial as soon as possible.

Tyler Durden

Fri, 04/24/2026 – 09:45

China Blacklists EU Defense, Aerospace Firms Over Taiwan Dealings

China Blacklists EU Defense, Aerospace Firms Over Taiwan Dealings

China has newly placed a slew of EU defense and aerospace firms on a control list, or effectively a new blacklist, reportedly with an eye on Taiwan tensions. It has barred its exporters from supplying dual-use items to seven EU firms, including FN Herstal and Omnipol a.s., according to a statement from the Chinese commerce ministry.

The ministry said the measure targets European defense companies that previously sold arms to Taiwan or maintained links with it, and stated the restrictions will not affect normal economic and trade exchanges with the European Union.

Beijing said it will continue working with other countries to safeguard peace and maintain a stable global supply chain, in its usual boilerplate rhetoric directed at the West regarding Taiwan, which China sees as its own.

Other firms named include Hensoldt AG, Excalibur Army, SpaceKnow Inc., VZLU Aerospace, and FN Browning. The companies are mostly based in Czech Republic, Belgium, and Germany.

“The MOFCOM spokesperson emphasized that the legally mandated export control measures target only a small number of EU entities involved in military affairs, entities that have participated in arms sales to Taiwan island or colluded with Taiwan authorities, and the measures only target dual-use items,” state-run Global Times described further, in reference to China’s Ministry of Commerce.

“They will not affect normal trade and economic exchanges between China and the EU, and law-abiding EU entities have absolutely nothing to worry about,” it added, citing the Commerce spokesperson.

All the while, Beijing has kept up its fiery denunciations, making clear there’s “no space” for ambiguity on what China sees as its territory (Taiwan).

Earlier this month, Chinese leader Xi Jinping had welcomed the leader of Taiwan’s main opposition party for a rare direct meeting in the Chinese capital.

The symbolism of the timing couldn’t be missed, as Xi invited Nationalist Party Chairwoman Cheng Li-wun to China ahead of the planned big mid-May summit with President Trump in which the Chinese leader could continue a push to dilute Washington’s support for Taiwan.

However, the Trump-Xi meeting is still anything but assured as moving forward, given the ongoing Iran war and very uneasy ceasefire with little evidence of an offramp in sight.

Also, Washington has suddenly this week charged Beijing with stealing US artificial intelligence labs’ intellectual property on an “industrial scale”.

China’s Foreign Ministry on Taiwan:

There is but one China in the world. Taiwan is an inalienable part of China’s territory.

No one can stop the eventual reunification of China.

Reunification is presented as a matter of inevitability, not possibility.

Separatist attempts… pic.twitter.com/e0Xdz4bRyh

— Open Source Intel (@Osint613) April 22, 2026

The formal memo could upend the May summit before it even gets off the ground: “The US government has information indicating that foreign entities, principally based in China, are engaged in deliberate, industrial-scale campaigns to distil US frontier AI systems,” Michael Kratsios, director of the White House Office of Science and Technology Policy, wrote in a memo shared on social media on Thursday, per Reuters and FT.

Tyler Durden

Fri, 04/24/2026 – 09:25

Lilly Slides After New Obesity Pill Prescription Data Disappoints Wall Street

Lilly Slides After New Obesity Pill Prescription Data Disappoints Wall Street

Shares of Eli Lilly & Co. fell in New York premarket trading after new industry prescription data for the drugmaker’s blockbuster obesity shot Zepbound and recently approved oral weight-loss pill Foundayo disappointed Wall Street analysts.

Foundayo generated 3,707 prescriptions in its second week, according to new prescription-tracking data from IQVIA cited by RBC Capital Markets analysts. That compares with 18,410 prescriptions for Novo’s oral version of Wegovy during its second week after launch, suggesting Lilly’s weight-loss drugs are falling behind in the GLP-1 race.

“While we believe comparisons early into launch should be considered immaterial, Foundayo’s uptake this week is likely to be received negatively,” RBC Capital Markets analyst Trung Huynh wrote in a note to clients earlier.

In a separate note citing the IQVIA data, Cantor analyst Carter Gould said, “We see slower TRx (total prescriptions) growth continuing in the injectable segment across diabetes and obesity, though injectable Wegovy notably grew by 7% week over week.“

Gould noted, “While we are cautious to make definitive claims off of one week of launch data from IQVIA, we acknowledge that investors will be scrutinizing the numbers, and believe that Foundayo scripts totaling just 20% of what oral Wegovy achieved during their first full week could cause the stock to be weak today.”

Shares of Eli Lilly fell as much as 4% in premarket trading. Through Thursday’s close, the stock was down 14.6% for the year.

Danske Bank analysts wrote earlier that Novo might hold the lead in obesity pills because Wegovy is a much better product than competitors.

Tyler Durden

Fri, 04/24/2026 – 09:15

Trump Extends Jones Act Waiver For 90 Days To Counter Fuel Price Pressures

Trump Extends Jones Act Waiver For 90 Days To Counter Fuel Price Pressures

On Friday, President Donald Trump extended a temporary waiver of the century-old Jones Act (Merchant Marine Act of 1920) for an additional 90 days. The move allows foreign-flagged vessels to transport fuel, oil, fertilizer, and other essential goods between U.S. ports, aiming to stabilize domestic supply chains and ease price pressures stemming from the ongoing U.S.-Israeli war with Iran and resulting disruptions in the Strait of Hormuz.

White House Assistant Press Secretary Taylor Rogers announced the extension via social media, stating: “President Trump issued a 90-day extension to the Jones Act waiver. New data compiled since the initial waiver was issued revealed that significantly more supply was able to reach U.S. ports faster. This waiver extension provides both certainty and stability for the U.S. and global economies.” Rogers added that the administration has taken multiple steps to mitigate short-term energy market disruptions and ensure vital products continue flowing.

President Trump issued a 90-day extension to the Jones Act waiver.

New data compiled since the initial waiver was issued revealed that significantly more supply was able to reach U.S. ports faster.

This waiver extension provides both certainty and stability for the U.S. and…

— Taylor Rogers (@TaylorRogers47) April 24, 2026

This builds on the initial 60-day waiver issued on March 17 (effective until mid-May), which White House Press Secretary Karoline Leavitt described at the time as “another step to mitigate the short-term disruptions to the oil market” amid the conflict.

What Is the Jones Act?

The Jones Act requires that goods transported by water between U.S. ports be carried on vessels that are U.S.-built, U.S.-owned, U.S.-flagged, and primarily U.S.-crewed. Enacted in 1920 as Section 27 of the Merchant Marine Act, it was designed to protect and rebuild the American maritime industry following World War I, ensuring a domestic fleet capable of supporting national defense and commerce during emergencies.

Critics argue it limits vessel availability and raises shipping costs, while supporters say it preserves U.S. jobs, shipbuilding capacity, and strategic maritime independence. Waivers are rare and typically granted only for national defense or emergencies, often following requests from the Department of Defense or in response to natural disasters.

Historical precedents include waivers during World War I and II, the Korean War era, Hurricanes Katrina (2005), and other crises like the 2012 Alaska fuel emergency. More recent examples occurred after Hurricanes Harvey, Irma, and Maria in 2017.

The waiver stems directly from the U.S.-Israeli military campaign against Iran that began on February 28, 2026. U.S. and Israeli strikes targeted Iranian leadership, including the assassination of Supreme Leader Ali Khamenei, prompting Iranian retaliation with missile and drone attacks across the Middle East, strikes on U.S. bases and allies, and – critically – the closure (or severe restriction) of the Strait of Hormuz.

The Strait of Hormuz, through which roughly 20-25% of global seaborne oil and significant liquefied natural gas passes, became a major chokepoint. Iran’s actions, combined with a subsequent U.S. naval blockade of Iranian ports starting in mid-April, led to a collapse in tanker traffic (down over 90% at times), global oil price spikes (from ~$70/barrel pre-war to averages above $100 in March), fuel shortages in parts of Asia, and ripple effects on fertilizer and agricultural supply chains worldwide.

These disruptions exacerbated domestic U.S. fuel price pressures, prompting the administration to act on the Jones Act to reroute more Gulf Coast oil and refined products to other U.S. coasts via foreign tankers.

Impacts and Early Data

Early results from the initial 60-day waiver appear positive according to the White House. Officials report that foreign tankers moved approximately 9 million barrels of oil, boosting effective domestic shipping capacity by about 70% and accelerating deliveries to ports and refineries. Rogers and other spokespeople emphasized that “the data reveals more supply has reached U.S. ports faster,” helping mitigate cost increases.

The 90-day extension (expected to run from mid-May into mid-August) aims to provide longer-term certainty as the Iran conflict and Hormuz situation remain fluid, with fragile ceasefires and ongoing diplomatic efforts (including talks in Pakistan) showing limited progress.

The decision has drawn sharp criticism from the U.S. maritime industry. The American Maritime Partnership called the extension of what it termed a “historically long and ineffective” waiver “an affront to U.S. workers,” arguing it undermines domestic shipbuilding and seafarer jobs.

Proponents of the Jones Act maintain that repeated waivers erode the law’s protective intent, while energy and logistics groups see the temporary relief as a pragmatic response to an extraordinary crisis.

Tyler Durden

Fri, 04/24/2026 – 08:55

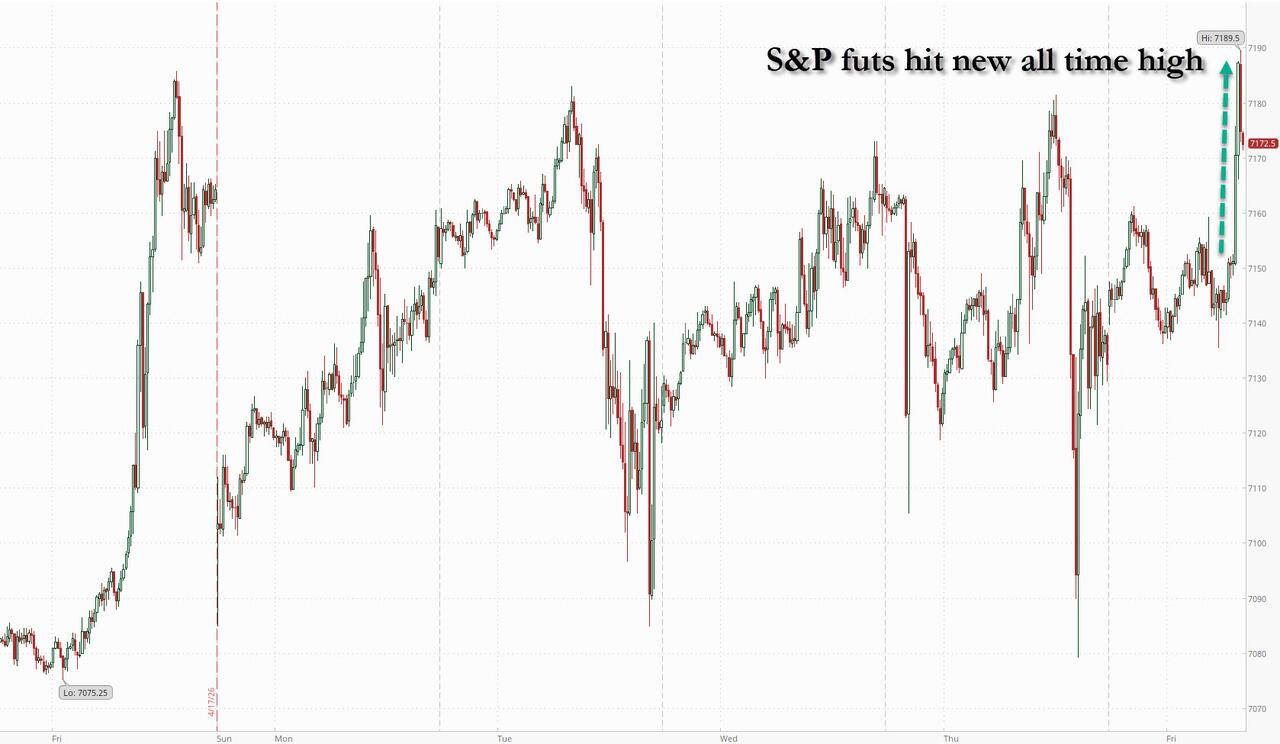

S&P Futures Jump To Record, Oil Tumbles On Report Iran Foreign Minister Going To Pakistan

S&P Futures Jump To Record, Oil Tumbles On Report Iran Foreign Minister Going To Pakistan

US equity futures jumped to a new all time high, reversing modest overnight losses, and oil tumbled to session lows on reports that Iran is sending a delegation to Pakistan today for talks, boosting hopes of ceasefire extension or more. Iranian Foreign Minister Araqchi is expected to arrive in Islamabad at 22:00 local time (1:00pm ET), the NY Post reports. As of 8:00am ET, S&P futures rallied as much a 0.6% to a new all time high of 7,190, reversing a modest loss in overnight trading as Brent tumbled from $107 to around $104 on the report. Tech shares rallied on the back of strong results from Intel and SAP SE, with the Nasdaq 100 up 1.3% and on track for a fourth straight weekly gain with most Mag 7 stocks trading higher. INTC added +29% amid surprises in both earnings and sales across all major businesses; the move will almost certainly extend the gains for semiconductor stocks to 18 straight days. The dollar slid 0.2%. Brent erased gains to fall 1.2% to below $104 a barrel while WTI dropped $1.2 and is now at $94.68 after trading as high as $98 earlier. Treasuries advanced, with the 10-year yield down two basis points at 4.31%. Metals are mixed, gold rebound above $4700; ags are higher. Today’s macro data include the final UMich consumer sentiment survey.

In premarket trading, Mag 7 stocks are mostly higher (Microsoft +1.2%, Amazon +0.9%, Alphabet +0.6%, Meta +0.6%, Apple -0.1%, Tesla +0.9%)

Comfort Systems USA (FIX) climbs 7% after the HVAC company reported revenue that beat estimates.

Coursera (COUR) falls 10% after the online education company’s first-quarter profit missed the average analyst estimate and the midpoint of its full-year revenue forecast also undershot expectations.

Edwards Lifesciences (EW) gains 2% after the medical devices firm reported a first quarter adjusted earnings per share beat, and boosted its sales forecast for the full year.

HCA Healthcare (HCA) falls 7% after the health-care services company reported net income for the first quarter that met the average analyst estimate.

Hims & Hers Health (HIMS) climbs 4% after JPMorgan initiated the stock with an overweight rating, citing improving vitals for the telehealth firm.

Intel (INTC) shares are up 27% — and on track to close at an all-time high if gains hold through regular trading — after the chipmaker delivered a blockbuster sales forecast.

MaxLinear (MXL) jumps 43% after the semiconductor company’s first-quarter results and second-quarter revenue forecast were both better than expected.

Organon & Co. (OGN) climbs 21% after the Economic Times reported that Sun Pharma is planning to submit a binding offer of $13 billion to acquire the US-based pharmaceutical company.

Procter & Gamble (PG) gains 3% after the consumer-products maker reported stronger-than-expected results for its latest quarter, driven by growth in the beauty category.

SLB (SLB) falls 3% after the oilfield services company reported adjusted earnings per share for the first quarter that matched the average analyst estimate. The company also agreed to buy S&P Global Geoscience & Petroleum Engineering portfolio.

World Kinect Corp. (WKC) rises 22% after the fuel-services company reported adjusted earnings per share for the first quarter that beat the average analyst estimate.

In corporate news, DeepSeek rolled out preview versions of a new flagship AI model a year after upending Silicon Valley, calling it the most powerful open-source platform in a challenge to rivals from OpenAI to Anthropic. Cognition AI is said to be in early talks to raise a new round of funding that would more than double its valuation to $25 billion. Mercedes-Benz is assessing potential cybersecurity risks linked to Anthropic’s Mythos model, signaling that concerns over threats from AI bots are spreading beyond the financial sector into the industrial economy. SoftBank plans to transform part of its Osaka factory into a major battery production line to power its AI data centers. President Trump said he is considering having the US purchase Spirit Aviation, saying it could be a potentially good investment for the federal government. United Airlines CEO Scott Kirby on deals, fuel price spikes and turf wars is the subject of today’s

Sentiment was boosted this morning after Pakistani officials familiar with the matter said Iran’s foreign minister was expected in Islamabad on Friday (around 10pm local time), with a second round of talks between Tehran and Washington expected. S&P futures jumped to a record high just under 7,200 as Brent erased gains to fall 1.2% to below $104 a barrel; the dollar slid 0.2%. Treasuries advanced, with the 10-year yield down two basis points at 4.31%. Still, we’ve seen such premature hope fizzle before; meanwhile in the Middle East, a US-sanctioned supertanker laden with Iranian oil appeared to be attempting to cross the Strait of Hormuz on Friday, with traffic through the waterway otherwise at a virtual standstill. As usual, traders will watch for headlines and signals from the US and Iran, along with shipping flows, for clues on energy supply risks, with any Strait of Hormuz escalation likely to keep oil elevated.

Tech shares rallied on the back of strong results from Intel and SAP, with the Nasdaq 100 on track for a fourth straight weekly gain. Intel surged 29% in premarket trading on a blockbuster sales forecast. Taiwan Semiconductor Manufacturing jumped 5% in Taipei after regulators eased limits on single-stock fund holdings.

“Those who called the end of the AI trade made a big mistake, as we can see looking at the semiconductor space,” said Mabrouk Chetouane, head of global market strategy at Natixis Investment Managers. “The earnings growth is just astounding. It’s a sweet spot where the offer for chips can’t meet the demand.”

Barclays strategist Emmanuel Cau notes the “renewed AI frenzy has seen semis stocks surging, widening further the US/Asia vs Europe performance gap.” US equity strength is supported by technical factors, Bloomberg notes as it echoes what we have been saying since late March, adding that gross exposure is high, net exposure isn’t, and there’s still cash that needs to be put to work. Discretionary managers have benchmarks to beat and higher dispersion shows the earning season is leading to a resumption of micro over macro.

Resurgent optimism over the economic potential of artificial intelligence has powered semiconductor manufacturers to an unprecedented 17-day rally. Investors also see the sector as at little risk of spillover from the Iranian war, with corporate profits and outlooks outpacing expectations in most instances.

“One takeaway from this earnings season is that the US leadership is back because of its dominance in tech, and semiconductors notably,” said David Kruk, head of trading at La Financiere de l’Echiquier in Paris. “Investors are now focusing more on earnings than geopolitics and taking the view that eventually a peace deal will occur.”

Equity and bond funds attracted the bulk of inflows this week, with stocks and IG bonds already tracking record annualized inflows, Bank of America says. Equity funds drew $25.9 billion, with US inflows at $18 billion in the week through April 22, according to BofA citing EPFR Global data.

In Europe, SAP climbed 5.5% after reporting cloud backlog growth that reassured investors amid AI disruption concerns. Still, the Stoxx 600 fell 0.1%, with sectors such as autos and retail hit on concern that the war in the Middle East will have a long-lasting impact on consumer sentiment; the energy sector gained. Here are some of the biggest movers on Friday:

SAP shares rise as much as 7.3% after reporting current cloud backlog — a crucial indicator for future revenue to be booked — maintained a 25% growth rate on constant-currency terms in 1Q, beating expectations.

Volvo shares rise as much as 2.6% as the Swedish firm raised its outlook for the European truck market after orders increased. Morgan Stanley calls the results strong and stable.

Telia gains as much as 3.9% after the Swedish telecommunications group reported earnings. Analysts say the mostly in-line print is a good start to the year, noting a slight beat to Ebitda as a key positive.

Siemens Energy rises as much as 4.9%, setting a new record high, after the firm saw significant order beats for both its Gas Services and Grid Technologies divisions in the second quarter and increased its outlook for the full year.

Adyen shares rise as much as 5.3% after agreeing a deal to buy Talon.One in its first ever acquisition. The deal, while small to Adyen’s scale, is a good starting point for the payments firm and should boost its unified commerce offerings, according to analysts.

Coloplast shares extend losing streak into a fifth day, dropping as much as 3.5% to the lowest since February 2014, after issuing a profit warning for the full year.

Electrolux falls as much as 25%, the most on record, after the Swedish home appliances group reported significantly weaker-than-expected 1Q figures, driven by poor performance in its key North American market.

MTU Aero Engines shares fall as much as 4.8% as UBS downgrades the German aircraft engine manufacturer to sell from neutral, citing exposure to a hard landing as the aftermarket cycle turns.

Safran shares fall as much as 3.6% as Oxcap lowers its recommendation on the aerospace and defense firm to equal-weight from overweight, citing concerns around global commercial flight growth.

Mondi shares fall as much as 8.9% as higher costs and lower prices hit the packaging company’s first-quarter earnings.

Asian stocks edged higher as tech stock gains outweighed concerns over the progress of US-Iran peace talks and shipping flows in the Strait of Hormuz. The MSCI Asia Pacific Index rose as much as 0.5% after swinging between gains and losses Friday. The gauge is headed for its third week of gains, the longest streak since the Iran war started. Taiwan’s Taiex index was the best performer in the region, with TSMC leading gains to a fresh record, after the island’s financial regulator eased limits on single-stock fund holdings. Tech stocks were also buoyed by Intel’s stronger-than-expected sales outlook. Meanwhile, equity benchmarks in China, India and Indonesia slipped. Despite mild gains on Friday, risk appetite remains muted into the weekend as investors await further signals from Washington and Tehran for clues on energy supply risks. While elevated oil prices remain a key macro risk, traders are looking for selective opportunities in the artificial intelligence theme. In Japan, investors will be watching out for next week’s Bank of Japan meeting. The BOJ is leaning toward leaving its policy rate unchanged on April 28 amid lingering uncertainty over the war in Iran, according to people familiar with the matter.

Brent erased gains to fall 1.2% to below $104 a barrel. A Pakistani official familiar with the matter said Iran’s foreign minister was expected in Islamabad on Friday, with a second round of talks between Tehran and Washington expected. The dollar slid 0.2%.

In rates, treasuries advanced, with the 10-year yield down two basis points at 4.31%. European bonds underperform over the early London session, led by gilts following stronger-than-expected UK retail sales data. UK yields lead European bond weakness, trading cheaper by up to 5bp across front-end of the curve

US economic data calendar slate includes April University of Michigan sentiment (10am) and Kansas City Fed services activity (11am)

Market Snapshot

S&P 500 mini 0.5%,

Nasdaq 100 mini +1.3%,

Russell 2000 mini 0.4%

Stoxx Europe 600 -0.1%,

DAX -0.1%,

CAC 40 -0.6%

10-year Treasury yield +0.4 basis points at 4.31%

VIX 18.69, -0.70 points

Bloomberg Dollar Index -0.2%

euro little changed at $1.1685

WTI crude -1.4% at $94.5/barrel

Top Overnight News

Iran Foreign Minister to Visit Islamabad Friday, Pakistan Says; Oil Dips After Pakistan Says US-Iran Peace Talks Are Expected: BBG

US President Trump posted that the meeting between Israel and Lebanon went well, the US is to work with Lebanon to protect itself from Hezbollah and that the Israel-Lebanon ceasefire is to be extended by three weeks: RTRS

Israeli media: A limited operation against Iran may be carried out to avoid a prolonged war: Al Arabiya

An Iranian Ship Tried to Slip Past the Blockade. A U.S. Destroyer Chased It Down: WSJ

Tanker Helga arrives at Iraq’s Basra offshore terminal to load 2mln BPD of crude, sources say; Helga is the second tanker to reach Basra terminals since the Hormuz closure.

U.S. Soldier Charged With Using Classified Information to Bet on Maduro’s Ouster: WSJ

Pentagon email floats suspending Spain from NATO, other steps over Iran rift: RTRS

China to Curb US Investment in Tech Companies After Meta Deal: BBG

Intel Shares Set to Eclipse Dot-Com Peak on Sales Forecast

Conservative super PAC threatens to unseat Republicans over immigration bill: RTRS

Hedge Fund at Center of Avis Squeeze Added to Stake Before Rout: BBG

Citadel Sends Warning Shot to NYC After Mamdani Jabs Griffin: WSJ

Meta Signs Multibillion-Dollar Deal With Amazon to Use Its CPU Chips for AI: WSJ

Lilly’s New Obesity Pill Off to Slow Start in Race With Novo: BBG

Oracle’s Deluge of AI Debt Pushes Wall Street to the Limit: WSJ

Orban’s Son-in-Law Waits Out Hungarian Wealth Probe in New York: BBG

Chinese Securities Regulator said that China is to allow qualified foreign investors to trade treasury futures from April 24, 2026, for hedging purposes only.

US official said Russia is to be included in G20 summit invitations

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly in the red, ex. Nikkei 225, as bourses caught up to the selloff seen stateside, as risk-off flows dominated the tape after the reports that Israel is on high alert in anticipation of a possible renewed war this weekend. ASX 200 slipped further below the 8,800 handle, as losses in IT offset the gains made by Energy names. Nikkei 225 outperformed, supported by the tech sector as chips benefitted from Intel’s earnings (see more below). Ibiden, one of Japan’s biggest electronics companies, hit a new ATH while Canon fell after cutting its FY profitability guidance. Hang Seng and Shanghai Comp traded with the biggest losses, albeit just slightly, after a flurry of earnings. China Telecom reported Q1 net that fell by 17% Y/Y while autos underperformed.

Top Asian News

Samsung Electronics (005930 KS) has produced the first working single-digit nanometer DRAM working die, TheLec reported citing sources; Co. intends to adjust processing conditions based on this.

Nomura Holdings (8604 JT) FY25/26 (JPY): Net 362.1bln (prev. 340.7bln Y/Y), Pretax 539.8bln (prev. 432.1bln Y/Y), Revenue 4.76tln (prev. 4.74tln Y/Y). Cuts dividend.

Hyundai Steel (004020 KS) Q1 (KRW) oper. profit 15.7bln (prev. loss 19.0bln Y/Y).

Kia Motor (000270 KS) Q1 2026 (KRW): Net 1.83tln (exp. 1.93tln), Operating Profit 2.21tln (exp. 2.3tln), Revenue 29.5tln (exp. 29.3tln).

Mercuria is to take a 25% stake in an aluminium smelter, as well as hunt for copper mining investments, the FT reported.

Taiwan regulator is to increase the equity exposure limit per stock to 25% from 10% for funds and ETFs.

Renesas (6723 JT) Q1 2026 (JPY): Revenue 380.3bln (prev. 308.8bln Y/Y) , Operating profit 90.6bln (prev. 21.5bln Y/Y).

European bourses started the European session with broad based losses, continuing the downbeat mood seen across APAC trade. From an index perspective, the IBEX 35 (-1.3%) lags peers, whilst the AEX (-0.1%) fares a bit better vs peers. European sectors hold a strong negative bias. Energy leads, buoyed by strength in underlying oil prices. Also for the sector, Siemens Energy (+2.4%) gains post-earnings after it reported a mixed set of results, but raised its FY outlook; elsewhere, Eni (+1%) beat on its Adj. EBIT metric, and announced a 90% increase to its share buyback, citing an upbeat commodities outlook. Tech and Telecoms complete the top three. The Tech sector has been boosted today by post-earnings strength in SAP (+6.4%). The Co. reported better-than-expected operating profit and revenue, with cloud metrics also topping expectations. It also said it will buy back EUR 10bln of shares. To the bottom of the pile resides Autos, Basic Resources and Retail. The autos sector is underperforming this morning with seemingly broad-based losses; Volvo (+1%) reported Q1 metrics today, where its metrics were mixed, but ultimately indicating resilience amidst challenges.

Top European News

German Ifo Current Conditions (Apr) 85.4 vs. Exp. 85.5 (Prev. 86.7, Low. 83, High. 87).

German Ifo Business Climate (Apr) 84.4 vs. Exp. 84.8 (Prev. 86.4, Low. 83.7, High. 87.5).

German Ifo Expectations (Apr) 83.3 vs. Exp. 83.9 (Prev. 86.0, Low. 82, High. 87.3).

Spanish PPI YoY (Mar) Y/Y 3.4% (Prev. -7%).

French Consumer Confidence (Apr) 84 vs. Exp. 88 (Prev. 89, Low. 87, High. 89).

Hungarian Unemployment Rate (Mar) 4.7% (Prev. 4.9%).

UK Retail Sales YoY (Mar) Y/Y 1.7% vs. Exp. 1.3% (Prev. 2.5%, Low. 0.8%, High. 2.2%).

UK Retail Sales ex Fuel YoY (Mar) Y/Y 1.7% vs. Exp. 2.0% (Prev. 3.4%, Low. 1.5%, High. 2.5%).

UK Retail Sales ex Fuel MoM (Mar) M/M 0.2% vs. Exp. 0.2% (Prev. -0.4%, Low. -0.5%, High. 0.6%).

UK Retail Sales MoM (Mar) M/M 0.7% vs. Exp. 0.0% (Prev. -0.4%, Low. -0.8%, High. 1.8%).

Trade/Tariffs

China reportedly to add seven EU companies to export control list, according to reported. Hensoldt (HAG GY) was added.

Canada is reportedly to seek talks with the EU regarding access to ‘Made in Europe’ scheme, according to FT.

China’s Commerce Minister met with the President of European Automotive Manufacturers Association to talk about the China-EU auto industry cooperation and EU trade restrictions. Commerce Minister stated that China will firmly safeguard Chinese firm’s rights.

US President Trump tells the Telegraph that the US will retaliate if the UK continues to target companies such as Apple (AAPL) , Google (GOOGL) and Meta (META) through the digital services tax.

US President Trump said the US will put a tariff on the UK if the digital service tax is not dropped.

FX

FX price action is lacklustre on the final trading day of the week. DXY leads marginally, while CHF and JPY are slightly lower.

DXY trades tentatively and broadly in tandem with oil prices. A light calendar ahead with the Fed on blackout ahead of next week’s meeting and only UoM final data on the docket. USD-specific news light, though the Japanese Finance Minister said overnight there were no plans to change currency swap lines with the US. DXY still remains supported above 100 and 200 DMAs at 98.50; upside resistance is 98.90, which marks the session high.

SNB Chairman Schlegel was on the wires a couple of times. He said they have “unrestricted” room for manoeuvre when it comes to the policy rate and FX intervention – Vice Chair Martin also echoed these remarks. EUR/CHF is unchanged on the session; it attempted to approach 0.92, but the move faltered at 0.9199.

Katayama is also on the wires, she said “will take decisive action on speculative activity”, JPY unchanged, in a signal that markets are becoming comfortable with the Finance Minister’s threats. USD/JPY unchanged, looks at 160 to the upside. BoJ rate decision next week, likely to remain on hold, with all eyes on Governor Ueda’s tone at the presser.

GBP shrugged off strong UK Retail Sales for March, as it does not change the narrative into next week’s BoE, where a hold is the base case. The data showed upside was driven by an increase in fuel sales, with retailers reporting that motorists were filling their tanks when buying following the start of the Middle East conflict. Online sales saw upside and are potentially indicative of a robust spring sale period. However, the core figures were in line/softer-than-expected, and potentially point to some greater-than-expected caution among consumers during the early stages of the Middle East conflict. EUR/GBP and Cable both unchanged, the former on a 0.8670 handle.

Fixed Income

A modestly bearish session for fixed benchmarks, initial action a function of the modest and since increasing energy upside as we count down to and participants position into a potentially risk-packed weekend.

Amidst this, USTs post downside of a handful of ticks in a thin 110-30 to 111-03 band. Ahead, the US docket is light, and we look to next week’s FOMC.

Bunds post slightly larger downside, perhaps as Dutch TTF has been leading oil benchmarks throughout the morning. Currently, in the red by c. 30 ticks but also in a relatively narrow 125.20-44 band. The European docket is light, aside from Italian supply (should be well received, particularly after the sizeable demand at last week’s syndications); as such, price action will likely be dictated by geopolitical developments.

Gilts gapped lower at the open, acknowledging the pressure in fixed peers seen late-Thursday. Opened at 87.10, lower by 41 ticks. Thereafter, slipped another 28 to an 86.82 low and has held there since; the second bout of pressure spurred by further energy upside and a hawkish BoE DMP. The DMP spurred end-2026 BoE pricing to 59bps of tightening from c. 54bps this morning and significantly above the 23bps implied this time last week.

To recap the day’s data. UK Retail Sales were strong on a headline level but in-line/soft on a core basis, with consumer motor fuel purchases driving the headline, no implications for the BoE next week (hold expected, guidance in focus). Thereafter, Germany’s Ifo was soft across the board, with no real follow-through to EGBs.

Italy sold EUR 2.5bln vs exp. EUR 2.25-2.5bln 2.20% 2028 BTP Short Term: b/c 1.63x (prev. 1.78x) & average yield 2.80% (prev. 2.89%).

Australia sold AUD 1bln vs exp. AUD 1bln 2.50% 2030 AGB: b/c 3.82x (prev. 3.44x), average yield 4.6947% (prev. 4.2888%).

Commodities

In geopolitics, fresh updates have been light as focus remains on the state of the US-Iran ceasefire and talks. The week ahead centres on four key watchpoints. First, the Strait of Hormuz “red line”: President Trump has warned the US Navy could actively engage IRGC vessels suspected of laying mines or interfering with traffic, shifting from shadowing to potential direct strikes, particularly after an IRGC-escorted Iranian ship defied the blockade. Second, the nuclear deal standoff: Washington is pushing for a comprehensive deal, while Tehran insists the nuclear file is not part of the current talks, raising the risk that negotiations collapse if neither side compromises on uranium enrichment. Third, internal dynamics in Tehran: reports of leadership friction and IRGC influence over the negotiating team point to possible policy inconsistency or hardline escalation. Fourth, ceasefire fragility: despite the extended Israel-Lebanon truce, sporadic clashes and reported drone activity underline how easily a trigger event could occur.

Oil rose for a fifth day as limited US-Iran progress towards resumed de-escalation talks kept supply concerns elevated; Brent climbed above USD 106/bbl (vs weekly lows of ~ USD 91/bbl) and is set for its biggest weekly gain since the war’s first week. WTI June, however, remains sub-USD 100/bbl. Brent currently trades in a daily range between 105.02-107.40/bbl while WTI resides in a USD 95.55-97.85/bbl range.

Gold edged lower, below USD 4,970/oz, with investors weighing whether higher crude prices from the US-Iran conflict could keep inflation and interest rates elevated. XAU/USD resides in a USD 4,658.03-4,711.23/oz range at the time of writing.

Copper heads for a weekly loss, with the broader base metals complex also mostly under pressure, as uncertainty over the Middle East war clouds the global growth outlook, while the US and Iran show little sign of returning to talks after Trump extended the ceasefire indefinitely, and the Strait of Hormuz remained largely blocked. 3M LME copper resides in a USD 13,215.58- 13,322.33/t. LME aluminium spread experiences the largest backwardation since 2024.

Japanese PM Takaichi said she is urging the cabinet to seek new sources for oil imports.

Union Spokesperson said workers at Australia’s INPEX (1605 JT) LNG plant vote in favour of strikes.

EU leaders have tasked Finance Ministers to come up with new measures to deal with potential energy shortages after assessing that current proposals were not enough, Bloomberg reported, citing sources.

Japan’s METI said Japan is to release 5.8mln kL of national oil reserves, starting May 1st.

Imports of Russian fuel oil to Singapore has jumped with volume in April already more than double the average monthly amount in 2025, according to FT citing Vortexa data.

The fire at Russia’s Tuapse oil terminal is under control.

US President Trump said that the US does not have an oil shortage and are taking millions of barrels of oil from Venezuela. Have a great relationship with Venezuela.

CME cuts initial margin on its Comex 100 gold futures to 6% from 7% and Comex 5000 silver futures to 11% from 14%.

Geopolitics: Middle East

US President Trump posted that the meeting between Israel and Lebanon went well, the US is to work with Lebanon to protect itself from Hezbollah and that the Israel-Lebanon ceasefire is to be extended by three weeks.

US President Trump said nobody is trying to get through the US blockade.

US President Trump said the Israel-Lebanon talks in the Oval Office went well and it would be great to resolve simultaneously with Iran. Looking forward to the next meeting with Israeli PM Netanyahu. Great chance of peace between Israel and Lebanon this year. Everyone seems united against Hezbollah. Israel-Lebanon peace should be an easy one. Israel will have to defend itself if they are shot at. Israel will be surgical in their self-defence. Iran has to cut its Hezbollah funding.

Tanker Helga arrives at Iraq’s Basra offshore terminal to load 2mln BPD of crude, sources say; Helga is the second tanker to reach Basra terminals since the Hormuz closure.

“Israeli media: A limited operation against Iran may be carried out to avoid a prolonged war”, Al Arabiya reported.

Pakistani official noted of a state of uncertainty regarding the second round of talks, “and we await Iran’s response”, Al Arabiya reported.

Israel again attacks southern Lebanon, claiming retaliation for overnight rocket fire, Al Jazeera reported.

Lebanese press Al-Jumhuriya noted of accelerated diplomatic efforts toward a Lebanon–Israel non-aggression agreement, driven by the US–Saudi–Egypt initiative, Journalist Kais reported. Plan revives idea of containing (not dismantling) Hezbollah’s weapons. Key proposed terms:. Israel withdraws to ceasefire line. Lebanese army deploys in south. Hezbollah moves north of Litani River. Start of weapons containment plan. Border disputes (Blue Line) adjusted. Prisoner releases, return of civilians, reconstruction. Deal would have international (especially US) guarantees. Coordination includes Iran to ensure Shiite/Hezbollah involvement. Parallel effort to resolve internal Lebanese political divisions. Saudi envoy pushing for meeting of Lebanon’s top leaders to create a unified position.

“Iranian Foreign Ministry: Araqchi held two called with the Pakistani army chief and foreign minister to discuss a ceasefire.”, Al Araby reported.

Iranian Vice President said any attack on oil wells will be met with strikes on attackers’ oil facilities; said it will be beyond “eye for an eye” response, Mehr News reported.

Senior IRGC Commander said Tehran is secure and its borders are stronger than before, Press TV reported.

The US has put a USD 10mln bounty on the leader of the Iran-backed Shiite militia group in Iraq, CBS reported.

Lebanese media reported that Israel have conducted airstrikes on the town of Al-Qasir in southern Lebanon a few hours after US President Trump announced the 3-week ceasefire extension, IRIB reported.

Israel’s ambassador to the UN said the extension of the Lebanon ceasefire is not 100% certain and that Israel is forced to answer every time a threat is detected, Tasnim reported citing CNN.

US military are developing plans to target Iran’s Hormuz defences if the ceasefire fails, CNN reported.

Israel-Lebanon talks have gotten underway in the White House, according to reported.

Hezbollah said it has launched rockets at Israel’s Shtula region in response to Israel violating ceasefire and targeting towns in southern Lebanon.

Israeli military said several launches crossed from Lebanon towards Israel were intercepted.

An internal Pentagon email explores options to punishing NATO allies that the US believes failed to support the US operations against Iran, according to a US official. Options include:. Suspending Spain from NATO. Reviewing the US position on British claims to the Falkland Islands. Suspending difficult countries from important or prestigious positions at NATO.

Geopolitics: Ukraine

Ukrainian authorities say a foreign-flagged ship bound for Odesa was attacked by Russian drones.

Imports of Russian fuel oil to Singapore has jumped with volume in April already more than double the average monthly amount in 2025, according to FT citing Vortexa data.

The fire at Russia’s Tuapse oil terminal is under control.

US official said Russia is to be included in G20 summit invitations.

US Event Calendar

Markets are entering the final day of the trading week in a cautious mood as US-Iran tensions show no signs of easing while the Strait of Hormuz remains essentially closed. Ahead of the weekend, there have been no signs of further talks, with Trump saying the “I don’t want to rush myself” when it comes to making a deal, while also claiming that “whatever I’m doing, it seems to be working very well”. Meanwhile, we saw Iran’s President, Foreign Minister and Parliamentary Speaker share similar messages of regime “unity” in short succession last night, after Trump posts claimed “infighting” between “Hardliners” and “Moderates” in Iran. The rhetoric had also leant in an escalatory direction earlier yesterday, with Trump posting that he’d ordered the US Navy to shoot boats placing mines in the Strait of Hormuz. So all that has left lingering uncertainty, even as Israel and Lebanon have agreed overnight to extend their ceasefire by three weeks according to the White House.

From a market perspective, that means oil prices continue to grind higher, with Brent crude rising +3.10% yesterday and another +0.97% overnight to $106.09/bbl. Unlike many recent sessions, this also weighed on US equities. The S&P 500 spiked lower just after Europe went home amid headlines that air defences had been activated in Tehran, before partially recovering to -0.41% by the close, with reports that this had been due to small drones rather than signifying a collapse of the ceasefire. Still, with the cacophony of headlines showing no signs of de-escalation, oil prices held onto most of their gains, while both 2yr (+3.6bps) and 10yr (+2.3bps) US Treasury yields closed higher on the day. We have seen some stablisation of these moves overnight, with both S&P 500 futures (-0.06%) and 10yr Treasury yields little changed.

In Asia, the Hang Seng (-0.20%), the CSI (-0.85%), the Shanghai Composite (-0.56%), the S&P/ASX 200 (-0.28%), and the KOSPI (-0.36%) are all in negative territory. In contrast, the Nikkei (+0.61%) is being boosted by tech, even in light of slightly stronger inflation figures from Japan. Core consumer prices increased by +1.8% year-on-year in March, up from +1.6% in February, a tenth ahead of expectations. Headline and core-core were inline. The BOJ is scheduled to convene next week, where it is anticipated that it will maintain current interest rates, while also signaling a potential readiness to raise rates.

Back to yesterday and oil’s gains extended across the futures curve. The 6-month Brent future (+2.34%) reached a 3-week high of $86.74/bbl as investors geared up to facing a more prolonged period of high energy prices. The pressures were even more visible in downstream products with US wholesale gasoline prices (+3.10%) reaching their highest level since 2022. This was echoed in near-term inflation swaps as well, with the 1yr Eurozone inflation swap (+16.2bps) surging up to 3.35%, whilst the 1yr US inflation swap (+8.6bps) rose to 3.32%, with the latter now only 6-7bps below its high on March 20.

The exception to the overall cautious mood were semiconductor stocks. The Philadelphia semiconductor index (+1.71%) posted a record 17th consecutive advance, having now risen by an astonishing +41.1% over that run. See my CoTD yesterday here for more. The positive mood for chipmakers continued overnight after Intel’s Q2 sales guidance came in well above expectations ($13.8-14.8bn vs $13bn expected). Its shares surged by +20% in after-hours trading, helping NASDAQ futures to a +0.39% gain overnight.

The broader tech mood had been more downbeat in yesterday’s session, with the NASDAQ (-0.89%) underperforming and the Mag-7 (-1.56%) posting its biggest decline in four weeks. Meta (-2.31%) lost ground after announcing plans to cut 10% of its workforce, while Microsoft (-3.97%) announced voluntary buyouts that could cover up to 7% of its employees. There is a sense that these job losses are there to offset huge capex spend. Tesla slid by -3.56% after its results the previous evening.

In terms of yesterday’s other news, we saw a notable divergence between the US and European data with the release of the flash April PMIs. Strong US data raised hopes that the economy’s resilience was holding up into Q2. In fact, the flash composite PMI for April moved up to 52.0 (vs. 50.6 expected), with both the manufacturing (54.0) and services prints (51.3) coming in above expectations, while the subindices also pointed to rising price pressures. This saw markets dial down remaining Fed cut pricing, with a cut by year-end now only 20% priced, down from 30% at Wednesday’s close.

Over in Europe, the PMIs told quite a different story, with clear weakness across much of the continent. Most notably, the Euro Area composite PMI fell to 48.6 (vs. 50.1 expected), which was a 17-month low and beneath the 50 mark that separates expansion from contraction. So that confirmed fears that Europe was headed for a more obvious stagflationary hit from the rise in energy prices. Indeed, that showed up in the price components, with input prices rising at their fastest since December 2022, and output prices at their fastest since March 2023.

Given the stagflationary implications of the PMIs, European assets struggled to gain much traction yesterday before the US sell-off. Moreover, investors priced in a growing chance of ECB hikes to deal with the price shock, and the amount of hikes priced by December was up +10.5bps on the day to 59bps. Nevertheless, sovereign bond yields were broadly steady as higher inflation expectations were offset by lower real rates on the back of the growth fears. So 10yr bund yields were unchanged at 3.01%, while 10yr OATs (+0.7bps) and BTPs (+1.3bps) saw slight increases. Otherwise, the STOXX 600 (+0.05%) was basically flat, finally stabilising after three consecutive declines.

Here in the UK, gilts continued to underperform yesterday, with the 10yr yield (+3.0bps) up to 4.94%, whilst the 30yr yield (+3.6bps) hit a 7-month high of 5.61%. In part, that came as the political speculation around PM Starmer’s position continued to swirl. But the UK also saw a clear outperformance in the PMIs, with an unexpected increase that went against the pattern in the Euro Area. For instance, the composite PMI was up to 52.0 (vs. 49.8 expected), with a rise in both manufacturing (53.6) and services (52.0). So that added to expectations that the Bank of England would hike rates this year, with markets now pricing in 55bps of hikes by the December meeting, up +4.3bps on the day.

Looking at the day ahead, data releases include the Ifo Institute’s business climate indicator from Germany, and in the US there’s the University of Michigan’s final consumer sentiment index for April. Central bank speakers include the ECB’s Panetta, whilst today’s earnings include Procter & Gamble.

Tyler Durden

Fri, 04/24/2026 – 08:34

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}