Category: News

Punxsutawney Phil is said to have seen his shadow, forecasting 6 more weeks of wintry weather

PUNXSUTAWNEY, Pa. — Punxsutawney Phil predicted six more weeks of wintry weather Monday, a forecast sure to disappoint many after what’s already been a long, cold season across large parts of the United States.

His annual prediction and announcement that he had seen his shadow was translated by his handlers in the Punxsutawney Groundhog Club at Gobbler’s Knob in western Pennsylvania.

The news was greeted with a mix of cheers and boos from the tens of thousands who braved temperatures in the single-digits Fahrenheit to await the annual prognostication. The extreme cold kept the crowd bundled up and helped keep people on the main stage dancing.

Usually guests can come up on stage and take pictures of Phil after his prediction, but this year the announcer said it was too cold for that and his handlers were afraid to keep him out too long. Instead, the audience was asked to come to the stage, turn around and “do a selfie.”

The club says that when Phil is deemed to have not seen his shadow, that means there will be an early spring. When he does see it, it’s six more weeks of winter. Phil tends to predict a longer winter far more often than an early spring.

The annual ritual goes back more than a century, with ties to ancient farming traditions in Europe. Punxsutawney’s festivities have grown considerably since the 1993 movie “Groundhog Day,” starring Bill Murray.

Other Groundhog Day predictions roll in

Phil isn’t the only animal being consulted for long-term weather forecasts Monday. There are formal and informal Groundhog Day events in many places in the U.S., Canada and beyond.

Michael Venos, who tracks Groundhog Day predictions at countdowntogroundhogday.com, said the early results Monday indicated a split verdict.

Agreeing with Punxsutawney Phil that more winter weather is on the way this year have been General Beauregard Lee, a Georgia groundhog, and groundhog mascot Dover Doug in Pennsylvania. Also in the “more winter” camp were That Dog Named Gidget, a Havanese in New York, and opossum Birmingham Jill in Alabama.

Those predicting an early spring include groundhogs Buckeye Chuck in Ohio, Fig Newton in North Carolina and Shubenacadie Sam in Nova Scotia, along with Benny the Bass, a fish in Ohio, and Pennsylvania ferret Jessup Giuseppe.

That’s just the start — Venos expects to tally about 100 events.

Thousands brave cold weather to see Punxsutawney Phil

Lisa Gibson was at her 10th Groundhog Day in Punxsutawney, wearing a lighted hat that resembled the tree stump from which Phil emerged shortly after daybreak.

“Oh man, it just breaks up the doldrums of winter,” said Gibson, accompanied by her husband — dressed up as Elvis Presley — and teenage daughter. “It’s like Halloween and New Year’s Eve all wrapped up into one holiday.”

Gibson, a resident of Pittsburgh, had been rooting for Phil to not see his shadow.

Rick Siger, Pennsylvania’s secretary of community and economic development, said the outdoor thermometer in his vehicle read 4 degrees Fahrenheit (minus 15 degrees Celsius) on his way to Gobbler’s Knob.

“I think it’s just fun — folks having a good time,” said Siger, attending his fourth straight Groundhog Day in Punxsutawney. “It brings people together at a challenging time. It is a unifying force that showcases the best of Pennsylvania, the best of Punxsutawney, this area.”

Last year’s announcement was six more weeks of winter, by far Phil’s more common assessment and not much of a surprise during the first week of February. His top-hatted handlers in the Punxsutawney Groundhog Club insist Phil’s “groundhogese” of winks, purrs, chatters and nods are being interpreted when they relate the meteorological marmot’s muses about the days ahead.

AccuWeather’s chief long-range weather expert, meteorologist Paul Pastelok, said early Monday some clouds moved into Punxsutawney overnight, bringing flurries he called “microflakes.”

Pastelok said the coming week will remain cold, with below-average temperatures in the eastern United States.

Groundhog Day falls on Feb. 2, the midpoint between the shortest, darkest day of the year on the winter solstice and the spring equinox. It’s a time of year that also figures in the Celtic calendar and the Christian holiday of Candlemas.

https://www.chicagotribune.com/2026/02/02/punxsutawney-phil-shadow-winter/

Throwback Waste Of The Day: Monkeys Throw Poop, And $600K

Throwback Waste Of The Day: Monkeys Throw Poop, And $600K

Authored by Jeremy Portnoy via RealClearInvestigations (emphasis ours),

Topline: In 2012, a study published by Agnes Scott College and Emory University concluded that chimpanzees that know how to throw their own feces have stronger communication skills than those that do not.

The National Institutes of Health must have used similarly primitive communication skills when deciding to award the study three federal grants worth $592,000 in 2011. The money would be worth $849,000 today.

That’s according to the “Wastebook” reporting published by the late U.S. Senator Dr. Tom Coburn. For years, these reports shined a white-hot spotlight on federal frauds and taxpayer abuses.

Coburn, the legendary U.S. Senator from Oklahoma, earned the nickname “Dr. No” by stopping thousands of pork-barrel projects using the Senate rules. Projects that he couldn’t stop, Coburn included in his oversight reports.

Coburn’s Wastebook 2011 included 100 examples of outrageous spending worth nearly $7 billion, including the cash wasted on the NIH’s monkey business.

Search all federal, state and local salaries and vendor spending with the world’s largest government spending database at OpenTheBooks.com.

Key facts: Using MRIs of 78 chimpanzees, the study examined the neurological behavior that leads a monkey to “patiently wait” and throw “feces or wet chow” at zoo visitors.

Researchers found that poop-throwing differs from other chimpanzee behaviors because it is not “nutritive in form … It is difficult to imagine that human caretakers would overtly reward a chimpanzee with food immediately after they had just been soiled with feces by the very same ape.”

As lead researcher Bill Hopkins told Wired Magazine, “I’ve never in my life seen a chimp be given a banana for throwing s**t at someone.”

Instead, chimpanzees throw their feces because they enjoy seeing humans’ reaction. Zoo visitors observed by the scientists would “negotiate with the chimpanzees to put down the projectile, or they will try to trick the ape by stopping, then dashing rapidly past the ape enclosure.”

Feces throwing was thus labeled as a form of “successful intraspecies communication” because it caused a reaction from humans. In fact, monkeys that engaged in the behavior were found to have more highly developed left brain hemispheres.

Thanks to taxpayers, the study resurfaced in 2017 to help journalists analyze a viral video of monkeys throwing their poop at a grandmother visiting a zoo in Grand Rapids, Michigan.

Summary: It’s much easier to excuse a monkey’s crude behavior than the money spent on NIH studies with questionable value to taxpayers.

The #WasteOfTheDay is brought to you by the forensic auditors at OpenTheBooks.com

Tyler Durden

Mon, 02/02/2026 – 09:20

https://www.zerohedge.com/political/throwback-waste-day-monkeys-throw-poop-and-600k

Damarrion Smith’s growth is obvious. ‘I look like a different player.’ He’s making Grant better too.

Damarrion Smith made a quick impact in the Grant boys basketball program.

Maybe too quick, at least in one way.

“Earlier in my career, I was just going way too fast,” Smith said. “I was out of control half the time, and that would lead to a lot of turnovers and me having to make split-second decisions. That wasn’t a good feeling to have.

“It took a long time practicing, but now I’m much better at controlling my speed.”

Smith mentioned a couple of in-game scenarios when that comes into play.

“I could tell better when a defender was in position to take a charge, or noticing on fast breaks when we didn’t have numbers and it would be smarter to take the ball back out,” he said.

Grant’s Damarrion Smith (3) drives to the basket during a nonconference game against Clinton, Wisconsin, in Fox Lake on Monday, Jan. 6, 2025. (Rob Dicker / News-Sun)

Entering the final weeks of his high school career, Smith has elevated his game to a higher level, and it’s no coincidence that the Bulldogs (10-10, 6-3) have won four straight Northern Lake County Conference games. The 5-foot-10 senior guard is averaging 13 points this season, but over the past couple of weeks he has also averaged five assists and six rebounds.

“A lot of people expect me to drive, and teams have to respect my teammates, so things open up for me to kick out for an open look,” Smith said. “I wasn’t really rebounding a lot at the start of the season. But going into the paint helps, where I can even get a tap-out, and sometimes it comes down to being physically tougher than everyone else.”

Grant senior guard Noah McMath agreed that Smith’s maturation has helped teammates.

“We’ve definitely benefited from him practicing things like avoiding jump passes and getting to his next move off two feet,” McMath said. “He’s so fast, he gets to his spots, and that allows him to find people.”

Grant coach Wayne Bosworth said Smith has learned to maximize his time on the court.

“If you have the ball in your hands around 8% of the time, what are you going to do in the other 92%?” Grant coach Wayne Bosworth said. “That’s where the emphasis can fall on things like rebounding and assists, and Damarrion has been emphasizing that more than anybody.”

Making changes has been easier for Smith after his experience last season. A role player as a sophomore, Smith emerged as one of the Bulldogs’ primary scoring options after then-senior guard Landon Enters suffered a torn ACL.

Smith rose to the occasion, playing his best basketball to date in the weeks after Enters’ injury. That stretch coincided with the Bulldogs’ first run through the conference.

“I definitely gained a lot of confidence during that time, and my coaches had confidence in me to put the ball in my hands,” Smith said. “But after the first time through (the conference), teams started really forcing me to my left, which I wasn’t totally comfortable doing. It became my main goal to fix that, and I’ve gotten a lot better.”

Grant’s Damarrion Smith (1) takes a jump shot during a Northern Lake County Conference game against Grayslake Central in Grayslake on Saturday, Jan. 10, 2026. (Mark Ukena / News-Sun)

That’s a good way to describe Smith’s career arc in general. He’s always improving. With almost three years of varsity experience, Smith is focused on maximizing the Bulldogs’ potential.

“I know I look like a different player, and I’ve gotten better in a lot of areas,” he said. “I want that to translate to team success.

“We had high expectations, and for the first part of the year, it wasn’t going the way we wanted. Now we’re playing well together and trying to finish on a positive note.”

Steve Reaven is a freelance reporter.

https://www.chicagotribune.com/2026/02/02/grant-high-school-basketball-damarrion-smith/

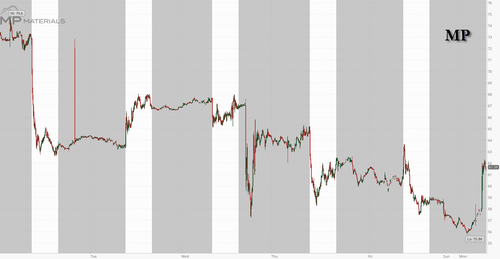

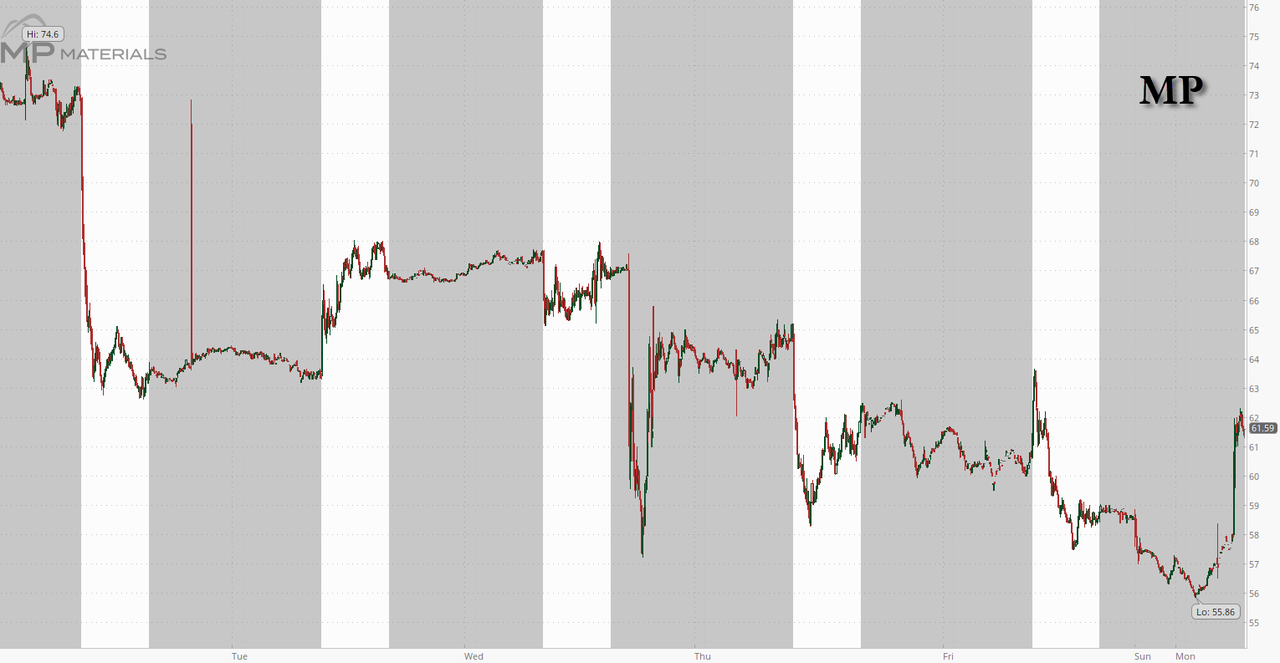

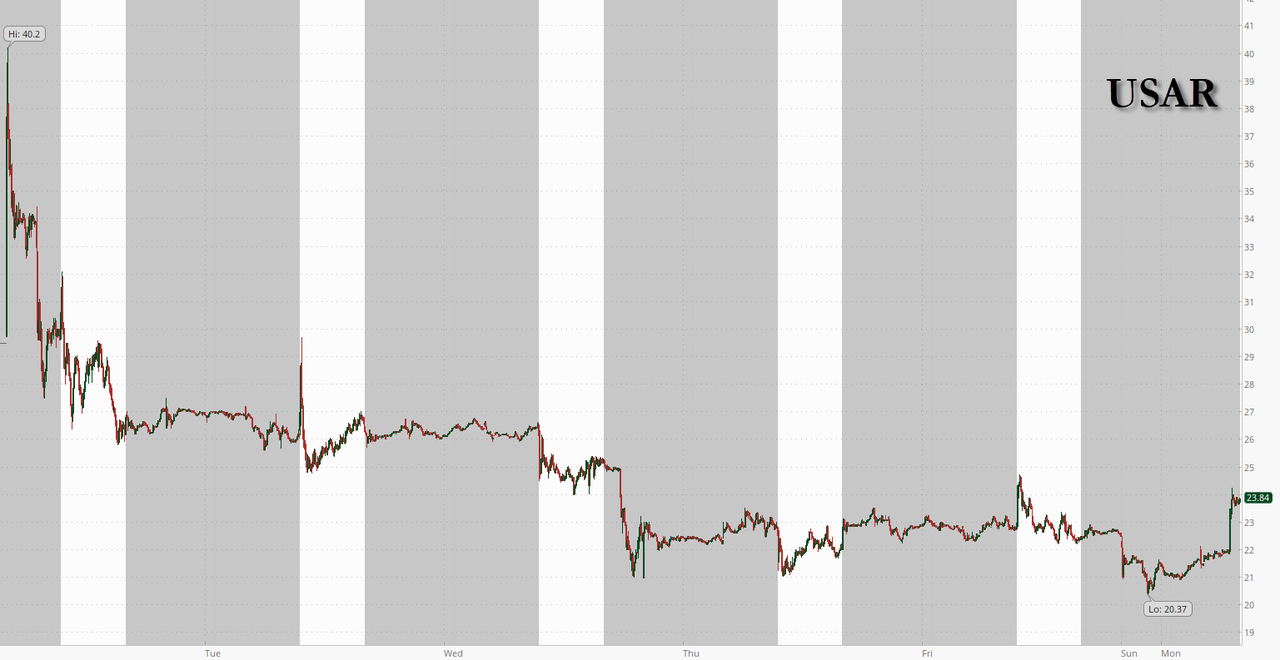

Trump Launches $12 Billion Strategic Mineral Stockpile To Counter China; Rare Earth Stocks Jump

Trump Launches $12 Billion Strategic Mineral Stockpile To Counter China; Rare Earth Stocks Jump

The Trump administration is preparing to launch a major initiative aimed at protecting US manufacturers from disruptions in the supply of critical minerals, committing about $12 billion in initial funding to build a strategic stockpile of essential materials, according to Bloomberg. The project, known as Project Vault, is designed to reduce America’s dependence on China for rare earths and other strategically important metals. By creating a centralized reserve for civilian industries, officials hope to cushion companies against sudden shortages and sharp price swings that can disrupt production and strain finances.

Shares of MP Materials, USA Rare Earth, Critical Metals and other rare earth associated names are higher between 5% and 10% heading into the cash open on Monday on the news.

At this point it’s safe to say last week’s Reuters rare earth hit piece (authored most likely at the behest of a disgruntled short), which sent the sector tumbling on disputed claims the Trump administration was seeking to distance itself from the rare earth space by moving away from a price floor on critical metals and suggesting MP’s deal with the government may be in question, has been thoroughly debunked. Even the MP Materials X account was mocking the grotesque misreporting:

Pathetic

— MP Materials (@MPMaterials) January 29, 2026

Project Vault will be financed through a mix of private and public funding: $1.67 billion is expected to come from private investors, while the US Export-Import Bank is set to provide a $10 billion loan with a 15-year term. The bank’s board is scheduled to vote on the deal, which would be the largest in its history.

More than a dozen major companies have joined Project Vault, including General Motors, Stellantis, Boeing, Corning, GE Vernova, and Google. Three large trading firms – Hartree Partners, Traxys North America, and Mercuria Energy – will handle sourcing and purchasing materials for the stockpile.

Some details about Project Vault’s structure were not immediately known, including the institutional investors providing the $1.67 billion (although JPMorgan will likely be among them). The senior administration officials said the project had been oversubscribed because investors are attracted by a credit-worthy group of manufacturers, their long-term commitments and the involvement of the US export-credit agency.

The specific carrying costs that would be charged to those manufacturers, as well as the fees for the trading firms participating as procurement officers, weren’t disclosed. Under the arrangement, companies that make an initial commitment to purchase materials at a specified inventory price later — and pay some up-front fees — will be able to present Project Vault with a shopping list of preferred materials they need.

The project, in turn, will seek to procure and store the materials, with the manufacturers charged a carrying cost for the expenses associated with interest on the loan and holding the elements. Manufacturers will be allowed to draw down their material stash as long as the firms replenish them. In the case of a major supply disruption, they will be able to access all of it, the officials said.

Project Vault represents the first major public-private partnership under the Trump admin seeking reshoring of a critical supply chain, and blends government-backed financing with private investment and corporate participation. While the plan aims to strengthen domestic supply chains, it comes at a time when rare earth mining stocks such as MP Materials and USA Rare Earth are trading well below their recent highs.

Bloomberg writes that rather than focusing on oil, which naturally is at the basis of the nation’s emergency petroleum reserve, this new effort will concentrate on minerals such as gallium and cobalt.

These materials are used in a wide range of products, including smartphones, electric vehicle batteries, and aircraft engines. The stockpile is expected to cover both rare earth elements and other critical minerals whose prices tend to be unstable.

According to senior administration officials, the initiative would represent the first large-scale mineral reserve designed specifically for private-sector use.

Investor interest has reportedly been strong, with officials saying the project is oversubscribed. They attribute this to the participation of major manufacturers, long-term purchasing commitments, and the backing of a federal credit agency. However, the identities of the main institutional investors and the exact cost structure have not yet been disclosed.

The program is part of a broader push to cut US reliance on China, which dominates much of the critical minerals supply chain. While the US maintains a reserve for defense needs, it has never created a similar system for civilian industries. The government has also expanded domestic investment and international cooperation with partners such as Australia, Japan, and Malaysia.

Momentum increased after China tightened export controls last year, forcing some US manufacturers to reduce output and exposing supply vulnerabilities. Under the system, companies will commit in advance to buy set quantities at agreed prices, pay upfront fees, and submit lists of needed materials, which Project Vault will acquire and store.

A central feature is price stabilization: firms must agree to repurchase the same volumes at the same prices in the future, a structure meant to limit volatility and protect against sudden cost spikes like the post-Ukraine surge in nickel prices. Trump is expected to discuss the plan with GM chief executive Mary Barra and mining entrepreneur Robert Friedland.

Tyler Durden

Mon, 02/02/2026 – 09:02

https://www.zerohedge.com/markets/trump-backs-critical-minerals-12b-stockpile-rare-earth-shares-jump

Bill Maher Torches Virtue-Signaling Lefty Celebs For Ditching Causes Once They’re Not The ‘Current Thing’

Bill Maher Torches Virtue-Signaling Lefty Celebs For Ditching Causes Once They’re Not The ‘Current Thing’

After another awards show shitshow of anti-Trump-ism at The Grammy’s, Bill Maher has had it with Hollywood’s relentless virtue signaling, and during his latest monologue on his HBO show Real Time with Bill Maher.

And he really let the glitterati have it.

Maher, a leftist liberal himself, began with mock enthusiasm for the endless parade of political posturing that now infects every red-carpet event.

“How about everybody drop the politics for a couple of hours,” he quipped, “and just enjoy these happy, dopey celebrations of show business?”

At last month’s Golden Globes awards, a number of celebrities wore small, stylized pins tied to the Renee Good shooting, including vague slogans like “BE GOOD” and “ICE OUT.”

“Of course, this is for the mother who was murdered by an ICE agent, and it’s really sad. I know people are out marching and all today, and we need to speak up,” actress Wanda Sykes told Variety on the red carpet before the award show. “We need to be out there and shut this rogue government down, because it’s just awful what they’re doing to people.”

Maher, who was also at the event, recalled a reporter asking him why he wasn’t wearing a lapel pin at the Golden Globes last month for the shooting of Renee Good in Minneapolis. At the time, he said, “Well, it was a terrible thing that happened, and it shouldn’t have happened, and if they didn’t act like such thugs, it wouldn’t have had to happen. But I don’t need to wear a pin about it.” He then added, “If I had the chance to think about it, my answer would be exactly the same.”

Maher then skewered the hysteria that followed his comments at the Golden Globes, where critics accused him of “refusing to join Golden Globes activism.”

His reply dripped with sarcasm.

“Golden Globes activism? Oh, you mean the activism of fixing a fucking pin to my suit? I’m sorry, it clashed with my keffiyeh.” He mocked the self-congratulation behind Hollywood’s symbolic gestures. “I hope I didn’t spoil the perfect record of pins and ribbons solving all the world’s problems. You can’t name a problem, from guns to AIDS to bullying to breast cancer, that still exists after people wore a ribbon for it—except all of them.”

The old liberal crusaders took a hit next. “You fucking posers. Three years ago, everybody was all into Ukrainian flags. What happened to that? Another cause tossed into the junk drawer with yesterday’s choke collar?” He called virtue signaling “body ornaments” and delivered one of his trademark zingers: “They’re just crucifixes for liberals. Because every time I see one, I think, ‘Jesus Christ.’”

Maher gave a nod to Ricky Gervais’s now-legendary roast of Hollywood’s award show activism during the 2020 Golden Globe awards, when he said, “Don’t use it as a platform to make a political speech. You’re in no position to lecture the public about anything. You know nothing about the real world.”

Maher, of course, agreed with Gervais, adding, “Celebrities absolutely do have a right to speak out. I’m just saying: Don’t. It’s having the opposite effect of what you want.”

Maher then pointed to the 2024 election cycle, where “every big name in show business came out for Kamala Harris, from Oprah to Clooney to Beyoncé, and she lost every swing state.”

Maher highlighted data showing that Taylor Swift’s political endorsement actually drove voters away. “Come on! Read the room, Democrats. Celebrities aren’t helping, and why would they?”

The problem, he argued, is that stars are the least relatable people in the country at a time when affordability dominates public concern, pointing out that “celebrities don’t strike people as relatable or in touch. What their activism mostly activates is eye rolls.”

Celebrities, I know it’s very important to you that you feel that you’re making a difference, and you are, you’re making independents vote Republican. pic.twitter.com/EozEfoF8OZ

— Bill Maher (@billmaher) January 31, 2026

Hollywood’s fake activism has a short shelf life. Stars slap on pins and flags to look good, then ditch the cause when the spotlight moves on because their activism is more about making them look good than about the cause they’re promoting. Maher nailed it—these celebs treat virtue like cheap jewelry, shiny for one night, trash the next. People are sick of it.

Maher ended the tirade with a final swipe at celebrity activism. “Democrats, it’s great you have all the big celebs, but people see them as an arm of the Democratic Party, which they already suspect for lacking common sense. I know celebrities mean well, and we thank them for having their heart in the right place.”

He added, “Just do you. Use your extraordinary talents for the noble cause of bringing relief from the problems that ribbons and pins can’t fix. I know it’s very important to you that you feel that you’re making a difference… so let me assure you, you are. You’re making independents vote Republican.”

Tyler Durden

Mon, 02/02/2026 – 08:55

La policía dice que el hijo de la princesa heredera de Noruega ha sido arrestado antes de su juicio por violación

OSLO (AP) — La policía dice que el hijo de la princesa heredera de Noruega ha sido arrestado antes de su juicio por violación.

Futures Tumble As Plunging Metals And Bitcoin Spark Global Selloff, Margin Calls

Futures Tumble As Plunging Metals And Bitcoin Spark Global Selloff, Margin Calls

Stock futures slide extending Friday’s rout, although are well off session lows, with aggressive unwinds across commodities and a crypto rout adding to the risk-off mood and sparking cross-asset margin calls. As of 8:00am ET, S&P 500 futures are down 0.4%, rebounding from a drop of as much as 1% earlier; Nasdaq futures drop 0.8%, also trimming the drop by half, and lag with focus on AI concerns a key theme for pre-market trading. European stocks were weaker in early trade but have since returned to a positive footing, Stoxx 600 is up 0.2% and just a few points away from its all-time-high. Asian stocks retreated for a second session as risk-off sentiment dominated markets, with high-flying technology names and shares linked to precious metals leading an early selloff in a data-heavy week. The biggest action is in metals, with gold and silver extending sharp declines, though big declines are seen here. Oil fell with other commodities, with easing US-Iran tensions also contributing. Bitcoin plunged to a 10-month low in Asia trading as Korean Kamikaze piled on the short side, before trimming losses. The US economic calendar includes January final S&P Global US manufacturing PMI (9:45am) and January ISM manufacturing (10am). Fed speaker slate includes only Bostic (12:30pm)

In premarket trading, Magnificent Seven stocks were all lower (Tesla -1.9%, Nvidia -1%, Meta -0.9%, Alphabet -0.7%, Amazon -0.6%, Microsoft -0.6%, Apple -0.5%)

US rare-earths stocks are rising as President Donald Trump is set to launch a strategic critical-minerals stockpile with $12 billion in seed money to lower reliance on China.(MP +4%, USAR +7%)

Cryptocurrency-exposed stocks fall after Bitcoin tumbled over the weekend. Decliners include Coinbase (COIN), which is down 3%.

Coterra Energy Inc. (CTRA) and Devon Energy (DVN) are combining to create a US shale producer with an enterprise value of about $58 billion, one of the largest oil and natural gas deals in years. Shares of Coterra are down 3%.

Humana (HUM) falls about 2% after Morgan Stanley downgraded the health insurer to underweight, citing vulnerability in its Medicare Advantage business.

Oracle (ORCL) climbs 4% after Fitch affirmed the company’s long-term issuer default rating at BBB. Oracle plans to raise $45 billion to $50 billion this year through a combination of debt and equity sales to build additional cloud infrastructure capacity.

Walt Disney Co. (DIS) gained about 1% after reporting sales and profit that beat estimates in the first quarter of its fiscal year, boosted by a record $10 billion in revenue from the division that includes parks and cruises.

In corporate news, Oracle fell more than 3% in premarket trading before rebounding and turning green, after outlining plans to raise as much as $50 billion through debt and equity this year to expand cloud infrastructure capacity. As Wall Street braces for a borrowing binge to bankroll AI projects, investors are growing skeptical of the billions of dollars being spent, with little clarity on when returns will materialize. Nvidia CEO Huang said that a proposed $100 billion investment in OpenAI was “never a commitment,” although the company will participate in OpenAI’s latest funding round. Tech Watch looks at how concerns about the huge costs of AI are starting to boil over. Alphabet and Amazon report this week.

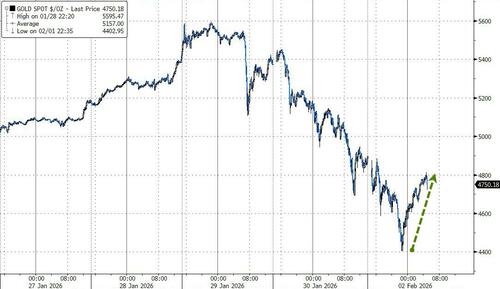

Extreme volatility across commodities continued to be the center of attention in markets. Gold pared losses after falling as much as 10%. At one point, silver sank 16% before reversing most of the retreat. Brent tumbled about 5% after US President Donald Trump said Washington is talking with Iran.

“Markets are nervous,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg. “We see a broad selloff across markets in Asia, Europe and the US. With the volatility increase in gold, but also in silver, investors have to de-risk.”

Monday’s moves are unwinding gains in some of the strongest performers of 2026, including Asian tech, emerging markets and commodities. The reversal was partly triggered by Trump’s pick of Kevin Warsh to lead the Federal Reserve, a move that supported the dollar as traders saw the former Fed governor as tough on inflation and less inclined toward deep interest-rate cuts.

Spot gold and silver remain in the limelight with both extending Friday’s rout, although the metals are well off the worst levels as some Asian buyers make a comeback. Silver is down about 1.9%; earlier it briefly went negative on the year. “The impact of 2x and 3x leveraged longs on assets falling 20-30% is undoubtedly going to trigger margin calls on a lot of other collateral,” said Panmure Liberum’s Mark Taylor.

Bitcoin steadied after shedding nearly 13% since the start of the year, a plunge that briefly pushed it toward levels last seen when Trump retook the White House. The largest cryptocurrency has now fallen for four straight months, with the selloff shaped by an absence of buyers and waning conviction in its value as an alternative asset.

“This pullback looks healthy to me, there was really some excess across gold, silver and some tech stocks too,” said David Kruk, head of trading at La Financiere de l’Echiquier. “My take is that there will be a bounce back in the coming days.”

Equity volatility remains below its average over the past year, while the gold rally has shown a so-called vol-up/spot-up dynamic similar to what’s seen in AI and other frothy parts of the equities world. Retail traders had piled into the iShares Silver Trust (SLV) in the largest one-day net inflow on record last Thursday.

Gold, silver ETF daily notional volume in $ pic.twitter.com/H67ciLuvJW

— zerohedge (@zerohedge) February 2, 2026

Investors continue to parse what a Warsh-led Fed may mean. The selection of the economist known as much for his fierce criticism of the central bank as his changing views on monetary policy has shifted the debate to the Fed’s $6.6 trillion balance sheet and its very role in markets.

Meanwhile, the US government stumbled into a partial shutdown Saturday while waiting for the House to approve a funding deal Trump worked out with Democrats. The funding lapse is likely to be short, with the House returning from a week-long break on Monday.

“It’s typical of the 2026 constant stream of complicated news flow,” wrote Jim Reid, global head of macro research and thematic strategy at Deutsche Bank AG. “This follows a January that managed to both shock and awe in various ways, yet still delivered broad-based gains across all global assets.”

Not everyone is bearish: Robust earnings and well behaved inflation should counter geopolitical and other risks, JPMorgan strategists led by Mislav Matejka write. Traditional growth factors have been among the weakest-performing characteristics in US equities so far in 2026, a development “we view as healthy for the broader bull market,” notes Bloomberg Intelligence analyst Christopher Cain.

With another busy week of earnings on deck, the current market correction isn’t about earnings, Goldman strategists said, pointing to solid guidance from companies so far in the season. Out of the 167 S&P 500 companies that have reported so far, 78% have managed to beat analyst forecasts, while 16% have missed. Disney, Idexx Labs and Tyson are among companies expected to report results before the market open. Disney signaled in November that profitability will take a hit of hundreds of millions of dollars in the quarter, due to marketing expenses tied to the release of the film Avatar: Fire and Ash and the launch of the Destiny cruise ship. Earnings from Palantir and NXP Semi follow later in the day.

European stocks were weaker in early trade but have since returned to a positive footing, Stoxx 600 is up 0.2% and just a few points away from its all-time-high. Here are some of the biggest movers on Monday:

Pandora jumps as much as 9.9% as silver prices extend their slide.

European miners fall as copper extends a slump from a record, while gold and silver fall again.

Julius Baer shares fall as much as 5% after reporting lower profit. KBW said the results were “mixed and messy” and that revenue missed the consensus estimate because of “mild weakness across all key lines.”

European oil stocks fall along with crude prices after OPEC+ kept March output plans unchanged and geopolitical risk eased, with President Donald Trump saying Washington is talking with Iran.

BFF Bank shares slide as much as 33% after the Italian financial services firm cut its 2026 outlook and announced a change in CEO.

European chip stocks fall, tracking declines in Asian and US peers, as momentum trades unwind globally along with gold and silver.

Carl Zeiss Meditec shares slip as much as 2.4% after Barclays downgraded its rating on the stock to equal-weight from overweight, citing continued downside risks which are only “partially priced into the stock.”

Auction Technology Group shares drop as much as 11% as FitzWalter Capital says it will not make another offer for the London-listed firm after its 400p per share bid was rejected last week.

Pharming shares sink as much as 20% after the FDA requested additional data as part of the Dutch biopharmaceutical company’s supplemental new drug application for Joenja in children with a rare primary immunodeficiency known as APDS.

Earlier in the session, Asian stocks retreated for a second session as risk-off sentiment dominated markets, with high-flying technology names and shares linked to precious metals leading an early selloff in a data-heavy week. The MSCI Asia Pacific Index slumped as much as 2.1%, the most since Nov. 18. Tech-heavy benchmarks in South Korea and Taiwan fared worse and the Hang Seng Tech Index lost more than 3% in Hong Kong. An Asian gauge of the materials sector was down 3.6% as gold declined further following Friday’s plunge that was its biggest in more than a decade, and silver whipsawed in choppy trading. Stocks in Indonesia also resumed their selloff Monday, weighed by weaker commodity prices, complicating efforts by regulators to shore up confidence in Southeast Asia’s biggest equities market. Japanese equities outperformed as exporters got a boost from a decline in the yen. Meanwhile, Indian stocks tumbled during Sunday’s special session following a budget proposal to hike taxes on equity derivatives trades. In the week ahead, traders will be watching for central bank decisions in Australia and India, while Indonesia is due to release gross domestic product figures.

In FX, the Bloomberg Dollar Index is down 0.1% after an overnight bid faltered. The euro and pound sit near the top of the G-10 leaderboard but still have some way to go to claw back Friday’s losses versus the greenback.

In rates, Treasuries are off session highs, hold small gains led by long-end tenors, with support from bigger rally in gilts. TSYs are higher by 5 ticks with yields 1-2bps lower across the curve amid a big flight to safety amid cascading margin calls, especially in Korea. Front-end yields are little changed with long-end tenors about 1bp richer, flattening 2s10s spread by around 1bp. US 10-year near 4.23% trails UK counterpart by about 1bp. Bunds are down 7 ticks and gilts up 27 as the slump in commodities helps underpin the latter. US session highlights include manufacturing PMIs and a speech by Atlanta Fed President Bostic. Treasury coupon auctions resume next week with 3-, 10- and 30-year supply, starting Feb. 10; department is scheduled to release quarterly borrowing estimates at 3pm

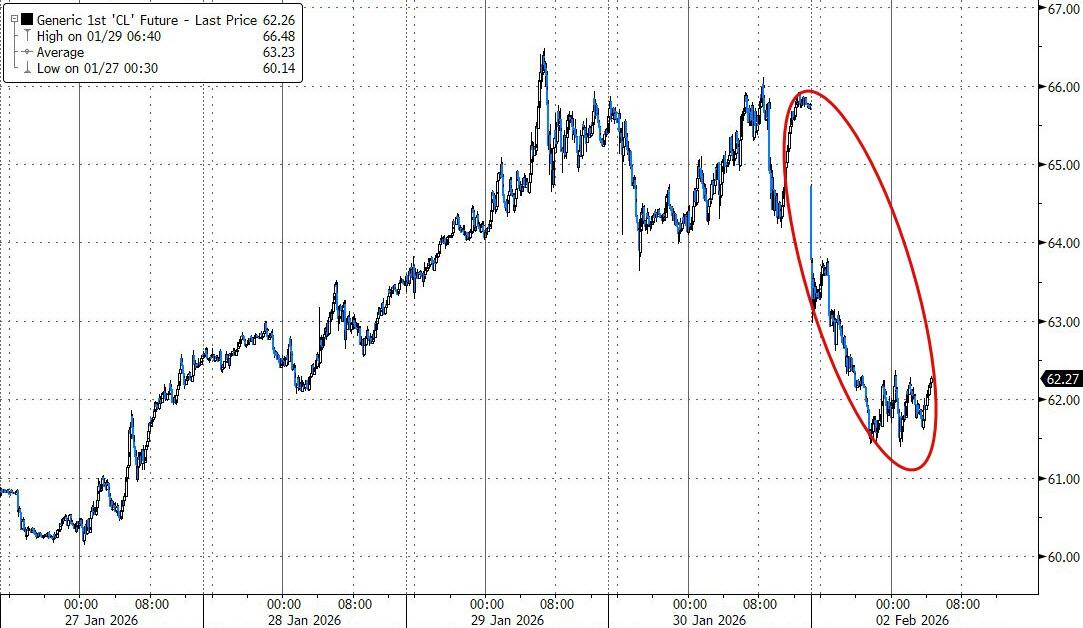

In commodities, WTI oil futures are down around 5% amid positive recent geopolitical developments surrounding Russia/Ukraine and Iran. Bitcoin is now up 1.8%, after looking like at one point it could make a run at the April low.

US economic calendar includes January final S&P Global US manufacturing PMI (9:45am) and January ISM manufacturing (10am). Fed speaker slate includes only Bostic (12:30pm)

Market Snapshot

S&P 500 mini -0.4%

Nasdaq 100 mini -0.8%,

Russell 2000 mini -0.6%

Stoxx Europe 600 little changed,

DAX +0.2%,

CAC 40 little changed

10-year Treasury yield -2 basis points at 4.22%

VIX +1.7 points at 19.11

Bloomberg Dollar Index little changed at 1187.5,

euro +0.1% at $1.1867

WTI crude -4.6% at $62.22/barrel

Top Overnight News

House lawmakers are returning to Washington today to pass a funding deal that Trump worked out with Democrats last week. Approval would fund the Department of Homeland Security for two weeks, and the rest of the government through Sept. 30. BBG

US Senate voted 71-29 to pass the USD 1.2tln government funding deal, and the House is expected to vote as soon as Monday on the plan after a brief government shutdown.

Trump launches a strategic critical-minerals stockpile with $12 billion in seed money to insulate manufacturers from supply shocks.

The venture, dubbed Project Vault, will marry $1.67 billion in private capital with a $10 billion loan from the US Export-Import Bank to procure and store minerals for manufacturers: BBG

Iran signaled it hopes diplomatic efforts to avert a war with the US will bear fruit within days, after Trump said he is hopeful “we’ll make a deal.” BBG

Oracle plans to raise up to $50 billion this year through a mix of debt and equity to expand cloud capacity. BBG

Kevin Warsh’s nomination as Fed chair is reigniting debate over the central bank’s $6.6 trillion balance sheet. White House economic adviser Kevin Hassett told Fox that it should be “as lean as possible.” BBG

Trump said Fed Chair nominee Warsh may get Democrat votes, and he hopes that Warsh will lower interest rates. In relevant news, Trump said on Friday that Warsh did not commit to cutting rates and he will probably talk about cutting rates with Warsh, while Trump also stated that Warsh will cut rates without White House pressure.

China’s manufacturing activity unexpectedly improved in January, with the PMI rising to 50.3 from 50.1 a month earlier, according to a private survey. BBG

Japanese Prime Minister Sanae Takaichi’s party is likely to score a landslide victory in next week’s lower house election, a survey by the Asahi newspaper showed, heightening the chance the country will continue to pursue big spending and tax cuts. RTRS

Narendra Modi unveiled a budget aimed at shielding India’s economy from Trump’s tariffs and providing fresh backing for strategic sectors such as rare earths, critical minerals and chips. Bond yields rose to a one-year high on the government’s record debt-sale plan. BBG

Oil prices fell more than 4% on Monday after U.S. President Donald Trump said Iran was “seriously talking” with Washington, signalling a de-escalation of tensions with an OPEC member, while a stronger dollar also weighed on prices. RTRS

SpaceX is in advanced talks to combine with xAI, people familiar said. The two firms could announce an agreement as soon as this week. BBG

Fed’s Bowman (voter) said on Friday that she supported a rate pause as inflation remains elevated, while she added that downside risks to the labour market have not diminished and that policy is modestly restrictive. Bowman also said that they should not imply that they expect to maintain the current stance of policy for an extended period of time, and noted she projected three rate cuts for 2026 in the December SEPs.

Trump picked Brett Matusmoto to head the BLS: WSJ

Trade/Tariffs

US President Trump warned of a very substantial response if Canada enacts a trade agreement with China, while he added that the US does not want China to take over Canada, which would happen with the deal that they are looking to make.

South Korean Industry Minister Kim said they will speed up the implementation of investment legislation after returning from talks with the US, which he said cleared up misunderstandings regarding tariffs.

EU industry association said on Friday that China proposed final anti-subsidy duties on EU dairy products at lower levels than in provisional duties with the final Chinese anti-subsidy tariffs on EU dairy products to go up to 11.7% vs. a maximum 42.7% in provisional duties.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured amid several recent bearish themes, including the partial US government shutdown and surprise contraction in Chinese official PMIs over the weekend, while sentiment was also not helped by the recent historic collapse in precious metals and with tech-related weakness after reports that NVIDIA’s plan to invest USD 100bln OpenAI stalled. ASX 200 retreated with underperformance in the mining sector after a tumble in metal prices, including last Friday’s biggest intraday drop for gold in four decades, while sentiment was not helped by wide consensus for a looming RBA rate hike. Nikkei 225 initially bucked the trend with early support from a weaker currency and with the Takaichi trade in play after a poll showed that the ruling LDP is likely on course for a landslide victory at the snap election this upcoming Sunday. However, the index gradually wiped out its gains and more alongside the broad risk-off mood across the region. Hang Seng and Shanghai Comp suffered after disappointing PMI data over the weekend, which showed official manufacturing and non-manufacturing PMI unexpectedly slipped into contraction territory, while the private sector RatingDog manufacturing PMI data matched estimates and continued to show an expansion, but failed to inspire risk sentiment. Furthermore, Chinese telecom names were among the worst performers after Beijing notified about raising telecom services VAT to 9% from 6%.

Top Asian News

Japanese PM Takaichi said in a speech on Saturday that the yen’s recent depreciation boosted exporters and returns from the government’s foreign exchange fund, while she failed to address concerns regarding the effect on consumer prices. However, she attempted to clarify on Sunday that she was referring solely to the need to build an economic structure that can withstand currency fluctuations, and not to stress the advantages of a weaker currency.

Japan’s ruling LDP party is likely to win a landslide victory and exceed a majority of 233 seats, while the ruling bloc may win more than 300 seats in the 465-seat parliamentary snap election on February 8th, according to an Asahi survey.

Chinese President Xi called for China’s renminbi to attain global reserve currency status, according to FT.

India increased infrastructure spending in its annual budget with the capital spending target for the upcoming fiscal year lifted by around 9% to INR 12.2tln, while it proposed to boost manufacturing in strategic sectors including rare earths and semiconductors, as well as proposed a tax holiday up to 2047 for foreign cloud companies making data centre investments in India. Furthermore, it strongly emphasised fiscal restraint and targeted reducing the debt-to-GDP ratio to 50% (+/-1%) from 56% by 2030/2031 and estimates the fiscal deficit will decline to 4.3% from 4.4% of GDP, while it is to raise the Securities Transaction Tax on futures and options trading.

European bourses (STOXX 600 -0.1%) opened broadly on the backfoot, but have since gradually moved higher to display a mixed picture. European sectors are mixed. Insurance leads whilst Basic Resources and Energy are the clear laggards, driven by significant pressure across the underlying commodities space.

Top European News

UK PM Starmer said the UK should consider re-entering talks for a defence pact with the EU, while he added that Europe needs to step up and do more to defend itself in certain times, according to The Guardian.

UK and Japan agreed to deepen defence and security cooperation.

Central Banks

BoJ’s Summary of opinions noted that one member said financial conditions remain accommodative even after a rate hike in December. One member said no need to worry too much about impact on corporate profits as long as rate hike pace is not too fast. One member said appropriate to continue raising policy rate if economic and price projections materialise. A member said current financial conditions still significantly accommodative judging from economic strength and fallout from recent weak yen. A member said if overseas rate environments change this year, there is risk BOJ may unintentionally fall behind a curve. A member said that the bank has been examining response of economic activity and prices and financial conditions to each rate hike and has been raising the policy interest rate, while it is appropriate for the bank to continue to do so. One member said BoJ should raise the policy rate at intervals of a few months. One member said some indicators of long-term inflation expectations have already started to show stability.

ECB SAFE: “Inflation expectations were broadly unchanged across horizons, with firms continuing to report upside risks to their long-term inflation outlook.”. Firms reported a net tightening in bank loan interest rates and in other loan conditions related to both price and non-price factors. Financing needs rose modestly, accompanied by a small perceived decline in availability. Inflation expectations were broadly unchanged across horizons, with firms continuing to report upside risks to their long-term inflation outlook. The use of artificial intelligence is widespread among euro area firms, though most firms use it very infrequently or moderately.

FX

The DXY is essentially flat and trades within a very narrow 92.17-97.29 range. Newsflow over the weekend has been light from a Dollar perspective, so attention will be on a data-packed week ahead (incl. ISMs, PMIs & jobs data) and on developments related to the current partial US government shutdown. On the latter point, lawmakers managed to work out a deal on Friday – the House is now set to vote on either Monday or Tuesday; House Speaker Johnson predicts the partial shutdown will end by Tuesday.

G10s are mostly losing vs the USD (ex-GBP & EUR), which are currently incrementally firmer. Nothing is really driving things for the GBP this morning (PMIs were revised a touch higher). In Europe, EZ PMIs were broadly subject to mild upward revisions, and this was reflected in the EZ-wide figure – nonetheless, it still remains in contractionary territory. CHF initially flat, but now underperforms as the risk tone improves.

Focus this morning has also been on the Aussie & Kiwi, which are currently posting mild losses vs the USD. Downside comes amidst the continuation of pressure seen in underlying metals prices; XAU -4.5% this morning. From a central banking perspective, the RBA is set to give a policy announcement on Tuesday. Markets currently price in a 76% chance of a 25bps hike, a recent shift from expectations of a pause – traders cite strong jobs data and inflation remaining above target.

Volatile trade for USD/JPY. Initially gapped higher (154.84) and gradually rose towards a session peak (155.51) within an hour, before paring that move. Since, trade has been rangebound. The earlier bout of weakness in the JPY comes after Japanese press circulated comments via PM Takaichi, where she seemingly talked up the benefits of a weaker JPY – but this was later clarified by the PM. On the subject of Takaichi, recent polls suggest that the ruling LDP is likely on course for a landslide victory at the snap election this upcoming Sunday. In more detail, Asahi reported that the LDP-JIP coalition could “secure more than 300 seats”, far surpassing a simple majority of 233.

Fixed Income

JGBs began the week on the backfoot, down to a 131.32 low, amid the latest election polling. Asahi’s poll has the LDP on track for a standalone majority and, when combined with JIP, to over 300 seats and by extension within reach of the 310 super-majority level in the 465-seat Lower House. However, the pressure proved somewhat fleeting given the global risk-off move and as XAU remains for sale, fixed has benefited. Action that been sufficient to lift JGBs into the green with gains of c. 10 ticks and the 10yr yield below 2.25%; however, the 40yr yield remains firmer and holds at highs of 3.94%.

USTs are being dictated by the risk tone. Just off a 112-02 peak, firmer by c. five ticks as things stand. The tone is driven by the continued pullback in metals, weak Chinese PMIs, NVIDIA reporting, the likely temporary US government shutdown and as we await the first remarks from Trump’s Fed Chair pick and any potential SCOTUS update re. tariffs. While there is no schedule for the latter two points, today’s docket does have the S&P Final Manufacturing PMI and then the ISM figure.

EGBs are contained this morning. Bunds found haven allure overnight and got to a 128.36 peak, with gains of 20 ticks at best. However, the benchmark has gradually come off best into the European morning as the region’s risk tone inches higher, and equities go from being well in the red to somewhat mixed. No move seen to Final Manufacturing PMIs. As it stands, Bunds are near-enough unchanged but around 10 ticks off their 128.04 trough.

Gilts lead this morning. Catching up to the overnight bid seen in peers. Since, in limited newsflow but as the tone continues to recover, Gilts have pulled back from their 91.21 peak to just above the figure, though it continues to outperform with gains of c. 20 ticks. Not driving price action but a narrative to keep an eye on is a piece in The Telegraph that Labour’s Rayner is constructing a war chest and has begun offering Cabinet roles to her supporters, as part of a plot to succeed PM Starmer.

Commodities

Crude benchmarks have slumped at the start of the new week following geopolitical headlines over the weekend that have eased rising tensions in recent weeks. Axios’ Ravid reported that a US-Iran meeting could take place this week, after weeks of potential signs of a strike in Iran. US President Trump also told reporters that Iran was seriously talking with Washington. WTI and Brent began trade just shy of USD 65/bbl and USD 68/bbl, respectively, before steadily falling lower throughout the APAC session to a low of USD 61.44/bbl and USD 65.45/bbl as markets price out the potential of further escalation. Benchmarks have rebounded slightly but remain near session lows.

Nat Gas futures continue to pare back the rise in prices following the Arctic storm, with Dutch TTF now trading below EUR 35/MWh after topping at EUR 43.38/MWh at the peak of the storm worries. Overnight, Russia announced that it will permit gasoline exports for fuel producers through to the end of July to avoid overstocking.

Precious metals continue to slide, with spot gold and silver falling as much as 10% and 16%, respectively. The initial selloff was initiated early last Friday on the possibility (and then confirmation) of Kevin Warsh being announced as the new Fed Chair.

During the APAC session, XAU steadily trended lower as Chinese participants took the opportunity to lock in profits, falling just shy of USD 4400/oz. As the European session continues, the yellow metal continues to rebound and is returning back to USD 4700/oz; but ultimately, remains lower by over 4%. Similarly, after falling to a trough of USD 71.40/oz, silver prices have rebounded to USD 80/oz.

Alongside precious metals, 3M LME Copper gapped below USD 13k/t and drove to a low of USD 12.43k/t, weighed on by the broader risk-off tone and weak Chinese PMIs. Copper prices remain below USD 13k/t but have recently rebounded just shy of session highs of USD 12.95k/t.

Turkey raises lower price limits on some gold and silver funds.

OPEC Secretariat receives updated compensation plans from Iraq, the United Arab Emirates, Kazakhstan, and Oman.

Eight OPEC+ members agreed on Sunday to maintain the pause in oil output hikes in March.

US President Trump said he welcomes investment from China and India in Venezuelan oil, while he announced that they have already made a deal for India to buy Venezuelan oil.

Russia will permit gasoline exports for fuel producers through to end-July to avoid overstocking, although it extended the ban on exports for non-producers, as well as the ban on diesel and other types of fuel for non-producers until end-July.

Geopolitics: Ukraine

Russia’s Kremlin said that they have narrowed their differences on some issues with Ukraine but not on complex issues, next round of trilateral talks on Ukraine will take place in Abu Dubai on Wednesday and Thursday.

Ukrainian President Zelensky said Ukraine is ready for substantive discussions and is interested in results, while he announced the next trilateral peace talks between the US, Russia and Ukraine will take place in Abu Dhabi on Feb. 4th-5th.

US envoy Witkoff said he held constructive talks with Russian special envoy Dmitriev on Saturday in Florida as part of the US effort to end the war in Ukraine.

Russia’s Medvedev said victory will come soon in the Ukraine war, but it is equally important to think about how to prevent new conflicts, while he also commented that US President Trump is an effective leader who seeks peace and that they never found the two nuclear submarines Trump spoke about deploying closer to Russia.

Geopolitics: Middle East

Iranian Supreme Leader Khamenei warned that if the US launches a war, it won’t stay confined to Iran and would likely escalate into a broader regional conflict, according to Iran International. It was separately reported that Iran renewed its threat to strike Israel in which Iranian army chief Major-General Amir Hatami warned that “If the enemy makes a mistake, it will without doubt endanger its own security, the security of the region, and the security of the Zionist regime”.

US officials said a meeting between the US and Iran could take place in Turkey this week, according to Axios’s Ravid.

Iran’s foreign Ministry said US President Trump has not set a deadline for negotiations, via Alhadath on X.

Iran announces it has summoned all the EU ambassadors in the Islamic Republic to protect the bloc’s listing of the paramilitary Revolutionary Guard as a terror group.

Persian Gulf states are warning US officials that Tehran’s missiles program remains capable of inflicting significant damage to US interest in the region, via X.

US Event Calendar

9:45 am: United States Jan F S&P Global US Manufacturing PMI, est. 52, prior 51.9

10:00 am: United States Jan ISM Manufacturing, est. 48.5, prior 47.9

DB’s Jim Reid concludes the overnight wrap

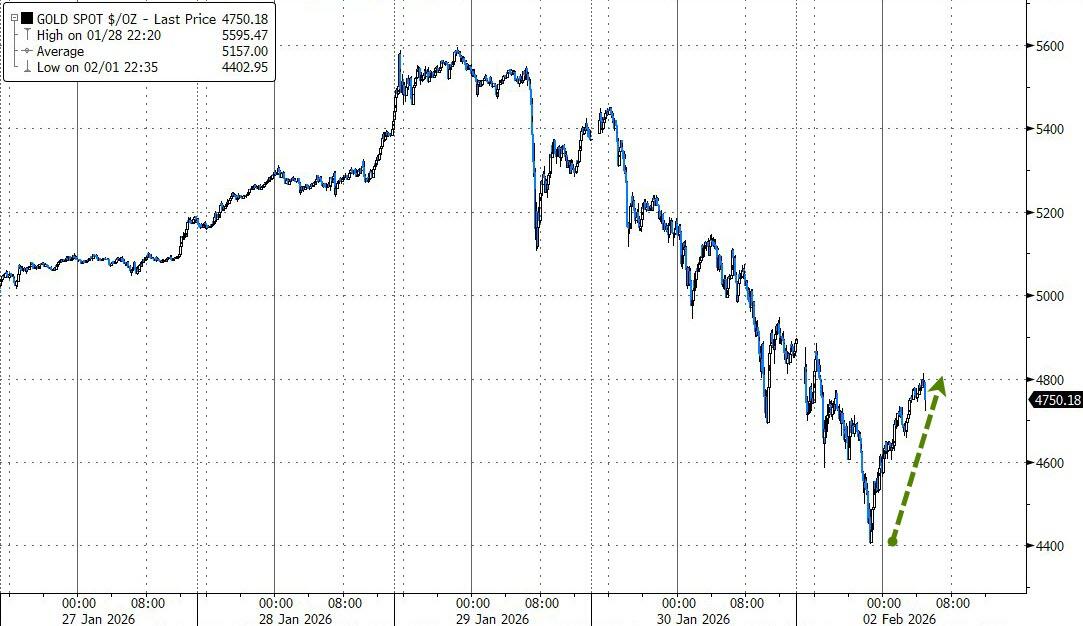

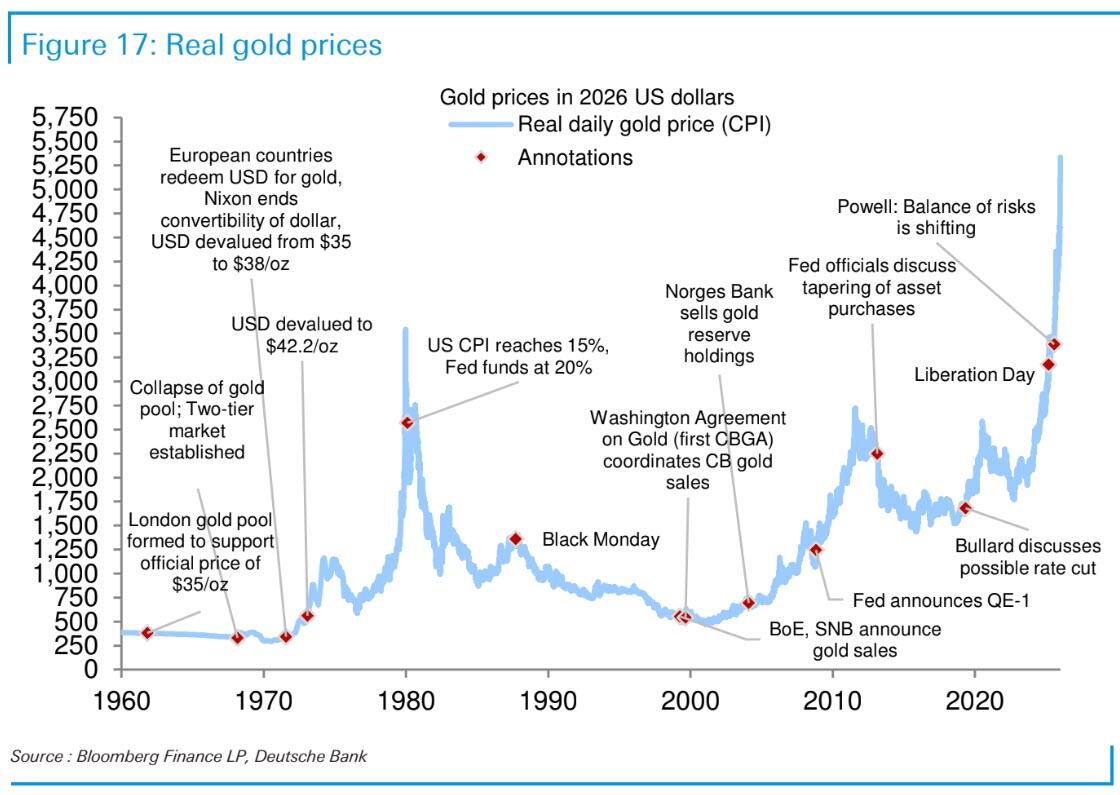

Welcome to February with another big sell-off in Gold (-5%) and Silver (-10%) overnight, and a partial US government shutdown that isn’t as severe as the record one before Xmas, and is expected to get resolved soon. Nevertheless it’s typical of the 2026 constant stream of complicated news flow. This follows a January that managed to both shock and awe in various ways, yet still delivered broad based gains across all global assets in our monthly performance review when measured in USD terms—a genuinely rare occurrence. It was perhaps fitting then, that the month ended with extraordinary volatility: Silver saw its largest daily fall since 1980 (36% at the intraday lows, 26.3% at the close), while Gold recorded its biggest one day decline since 2013 ( 8.95%). With the overnight moves, Silver is now around $5 below its real adjusted level from 1790—something we explored in last Monday’s CoTD here. As we noted, even incorporating the dramatic 1980 boom and bust and the recent surge, Silver has failed to outperform inflation over more than 230 years of data. So while I’ve long been a bit of a gold bug given my strong views on the inflationary consequences of fiat money, the recent run up in precious metals feels to have an enormous speculative element. Friday’s moves, almost certainly driven by positioning and margin dynamics, only reinforced that impression.

Volatility began to build on Thursday, but the clear catalyst for Friday’s sell off appeared to be news in the early UK hours that Kevin Warsh had secured the nomination for Fed Chair. Warsh is known to be more hawkish on the balance sheet than other candidates, pushing back against the prevailing debasement narrative that has supported precious metals. That said, price action had long since detached from any sane discussion on debasement, but it often takes only a small ripple to trigger a broader correction, especially when there is leverage around. Our economics team explored the implications of Warsh’s nomination in detail on Friday here. The Dollar responded to the news with its strongest day since May, while EM assets—after an excellent month—saw sharp reversals across equities and FX.

Henry has just published his usual performance review here, and despite the late month turbulence it was still a very strong January for global assets. Silver (+18.9%) and Gold (+13%) topped the performance tables, joined by oil (+16.2%), which posted its biggest monthly gain in four years. Outside our formal performance review, it’s also worth noting that Bitcoin is currently down about -14% year to date after a difficult few days. It now sits around -40% below its October 2025 peak and back at levels first breached in November 2024. Over that same period, Gold has doubled.

Elsewhere in Asia, Brent crude futures are down by -5.4%, also being impacted by the commodities deleveraging and news that Washington is in talks with Iran. S&P 500 futures are down by -1.21% and NASDAQ 100 (-1.59%) and DAX futures (-1.02%) are also lower. The KOSPI is at the forefront of the regional equity declines, plummeting around -5.0% as major chipmakers, Samsung Electronics and SK Hynix, saw their shares drop between -5.70% and -6.50% respectively. Moreover, the Hang Seng (-2.70%) and the Hang Seng Tech index (-3.87%) are also experiencing significant retreats as an AI-driven sell-off accelerates. In other markets, the Nikkei (-1.02%) is also trading in negative territory, with the CSI (-1.40%) and the Shanghai Composite (-1.64%) also declining amid a broader regional downturn. So a pretty uncomfortable start to February.

The coming week will revolve around a dense run of US macro releases, with the January jobs report set to dominate attention on Friday. We also have the ISM surveys, consumer sentiment and the latest Treasury’s quarterly refunding details. Central banks be in focus with decisions due from the ECB, the BoE (both Thursday) and the RBA (tomorrow). Elsewhere we have the latest global PMIs and inflation in Europe. Corporate earnings include Alphabet (Wednesday), Amazon (Thursday) and AMD (Tuesday). Remember that Meta (+6.56%) and Microsoft (-8.50%) saw big moves in either direction last week with both having a 10% plus intra-day rise and decline respectively.

Looking at more detail into the week ahead, Friday’s employment report is the highlight, with forecasts pointing to another modest payroll gain (consensus at +50k and +37k for headline and private respectively) and no change in either the unemployment rate (4.4%) or the pace of hourly earnings growth. Ahead of that, the JOLTS data tomorrow and the ADP report on Wednesday will give early clues on labour market momentum. The week also brings the manufacturing ISM on Monday and the services ISM mid week, followed by the University of Michigan’s February sentiment survey on Friday. Fixed income investors will also be watching Wednesday’s quarterly refunding announcement and today’s Treasury borrowing estimate closely.

Central banks will remain a major theme as well. The ECB and Bank of England both meet on Thursday, and neither is expected to adjust policy, with the ECB likely extending its on hold stance for a fifth straight meeting and the BoE seen keeping Bank Rate unchanged once again. The Reserve Bank of Australia is also expected to stand pat tomorrow. Additional colour on financial conditions will come from the Fed’s senior loan officer survey today and the ECB’s latest bank lending survey tomorrow.

Across Europe, the flow of flash January inflation reports continues, with France tomorrow and Italy and the broader euro area following on Wednesday. Sweden publishes its CPI on Friday. Several Eurozone economies will also release December retail sales and trade figures, while Germany rounds out the week with its factory orders and industrial production numbers. It’ll be interesting to see if they show continued evidence of the fiscal stimulus.

The corporate earnings calendar remains active, with attention in the US turning to two members of the Mag-7 — Alphabet on Wednesday and Amazon on Thursday — alongside a range of other tech firms such as Palantir, AMD and Qualcomm. Major healthcare names are also reporting, including Eli Lilly and AbbVie in the US and Novartis and Novo Nordisk in Europe. Broader US earnings include updates from PepsiCo, Walt Disney and Uber. In Europe, several banks are scheduled to report, while in Japan, Toyota, Sony and Tokyo Electron will be among the key companies releasing results.

Over the weekend, data revealed that China’s official PMI for January fell back below 50 again at 49.3, down from December’s 50.1, and below expectations. The Manufacturing PMI has been in contraction for nine of the past ten months, reinforcing concerns that December’s data may have been an anomaly rather than the beginning of a sustained recovery.

Simultaneously, the official non-manufacturing PMI decreased to 49.4 in January (compared to the expected 50.3), down from 50.2 the previous month, marking the lowest level since December 2022. This decline was attributed to weak post-holiday demand, cautious consumer spending, and ongoing challenges in the property sector. Conversely, a private survey presented a more positive outlook, indicating that China’s manufacturing activity improved to 50.3 in January (compared to 50.1 in December), and marking the strongest level since October.

Recapping last week, the biggest news happened on Friday when Trump announced Kevin Warsh as his Fed nominee. The confirmation led to a cross-asset sell-off amidst expectations that Warsh would be more hawkish than other candidates – particularly on the balance sheet. So that led to a global risk-off mood and triggered a sharp pullback in precious metals. On Friday gold (-8.95%) posted its largest daily decline since 2013 (-1.87% over the week). And silver registered its largest drop since 1980 at -26.36% (-17.44% over the week). To give some perspective, earlier in the week gold posted its best 8-day run since the GFC, rising to $5,417/oz on Wednesday, while silver also reached a new high of $116.70/oz before ending the week at $85.20. So some remarkable volatility playing out in precious metals.

Equities had also advanced earlier in the week, with the S&P 500 briefly surpassing the 7000 threshold on Wednesday, before ending the week +0.34% higher at 6,939 (-0.43% on Friday). The reversal in equities was partly driven by Microsoft results, which saw the software giant’s shares fall -9.99% on Thursday. Combined with the Warsh news, that left the NASDAQ slightly down on the week (-0.17%, -0.94% on Friday), although the Mag-7 managed to outperform (+1.02%, -0.32% on Friday), supported by Meta’s +10.40% surge on Thursday after its own results suggested AI was boosting ad revenue growth.

In bond markets, Trump’s Warsh nomination added to the steepening in the US Treasuries curve. While 2yr yields fell -3.7bps on Friday (-7.1bps over the week) amid the risk-off mood, 10yr (+0.4bps, +1.1bps over the week) and 30yr (+1.9bps, +4.6bps over the week) moved higher. On Wednesday, the FOMC had held rates steady at 3.50%-3.75% as expected, with Chair Powell offering little near-term guidance but suggesting that the next move is still likely to be a cut.

We also saw sizeable volatility in other asset classes. In FX, the dollar index fell by -0.62% over the week, despite a +0.74% rebound on Friday helped by Trump’s Warsh nomination. Elsewhere, oil prices continued to climb higher, with Brent (+7.30%, -0.03% Friday) rising to its highest level since July amid rising concerns that the US may pursue military action against Iran, with Trump saying that the next US attack would be “far worse” than the strikes last June if Iran did not reach a deal.

Finally in Europe, the mood was more positive with the STOXX 600 ending the week +0.44% higher (+0.64% on Friday), though the DAX (-1.45%, +0.94% Friday) and CAC (-0.20%, +0.68%) retreated after weak results from the likes of SAP and LVMH. We saw mixed economic data, with a soft German IFO expectations reading on Monday (89.5 s 90.3 expected) but a stronger Euro Area Q4 GDP on Friday (+0.3% q/q vs +0.2% q/q expected). We also got stronger than expected German HICP print (+2.1% vs +2.0% expected). Despite this, yields on 10yr bunds (-6.3bps, +0.3bps Friday) and OATs (-5.6bps, +0.6bps Friday) moved lower over the week

Tyler Durden

Mon, 02/02/2026 – 08:37

Día de la Marmota: Phil predice 6 semanas más de clima invernal en EEUU

Associated Press

PUNXSUTAWNEY, Pensilvania, EE.UU. (AP) — La marmota Punxsutawney Phil predijo el lunes seis semanas más de clima invernal, un pronóstico que seguramente decepcionará a muchos después de lo que ya ha sido una temporada larga y fría en gran parte de Estados Unidos.

Su predicción anual y el anuncio de que vio su sombra fueron traducidos por sus cuidadores en el Club de la Marmota de Punxsutawney en Gobbler’s Knob, en el oeste de Pensilvania.

La noticia fue recibida con una mezcla de vítores y abucheos de las miles de personas que desafiaron las bajas temperaturas para esperar la predicción anual. El frío extremo mantuvo a la multitud abrigada y ayudó a que la gente en el escenario principal siguiera bailando.

Usualmente, los invitados pueden subir al escenario y tomar fotos de Phil después de su predicción, pero este año el presentador dijo que hacía demasiado frío para eso y sus cuidadores no querían mantenerlo a la intemperie demasiado tiempo. En su lugar, se pidió a la audiencia que se acercaran al escenario y se tomaran selfies.

El club dice que cuando se considera que Phil no ha visto su sombra, eso significa que la primavera llegará rápido. Cuando la ve, son seis semanas más de invierno. Phil tiende a predecir más inviernos largos que primaveras anticipadas.

El ritual anual se remonta a más de un siglo y tiene vínculos con antiguas tradiciones agrícolas en Europa. Las festividades de Punxsutawney han crecido considerablemente desde la película de 1993 “Groundhog Day” (“El Día de la Marmota”), protagonizada por Bill Murray.

Lisa Gibson estaba en su décimo Día de la Marmota, usando un sombrero con luces que se asemejaba al tocón del árbol del que Phil emerge poco después del amanecer.

“Esto simplemente rompe la monotonía del invierno”, dijo Gibson, acompañada por su esposo, vestido como Elvis Presley, y su hija adolescente. “Es como Halloween y la víspera de Año Nuevo, todo envuelto en un solo feriado”.

Gibson, residente de Pittsburgh, esperaba que Phil no viera su sombra.

Rick Siger, secretario de desarrollo comunitario y económico de Pensilvania, dijo que el termómetro exterior en su vehículo marcaba -15 grados Celsius (4 Fahrenheit) cuando iba rumbo a Gobbler’s Knob.

“Creo que es simplemente divertido: gente pasándola bien”, dijo Siger, quien asistía a su cuarto Día de la Marmota consecutivo. “Reúne a la gente en un momento desafiante. Es una fuerza unificadora que muestra lo mejor de Pensilvania, lo mejor de Punxsutawney, esta área”.

El anuncio del año pasado fue de seis semanas más de invierno, con mucho la evaluación más común de Phil y no una gran sorpresa durante la primera semana de febrero. Sus cuidadores en el Club de la Marmota de Punxsutawney interpretan los guiños, ronroneos, parloteos y asentimientos de la marmota para saber del clima venidero.

El meteorólogo de AccuWeather, Paul Pastelok, dijo el lunes que algunas nubes se movieron anoche hacia Punxsutawney, trayendo “microcopos”.

Pastelok dijo que la próxima semana seguirá fría, con temperaturas por debajo del promedio en el este de Estados Unidos.

Phil no es el único animal consultado para pronósticos meteorológicos de largo plazo. Hay eventos formales e informales por el Día de la Marmota en muchos lugares de Estados Unidos, Canadá y más allá.

El Día de la Marmota cae el 2 de febrero, el punto medio entre el día más corto y oscuro del año en el solsticio de invierno y el equinoccio de primavera. Es una época del año que también figura en el calendario celta y en la festividad cristiana de la Candelaria.

______

Scolforo informó desde Harrisburg, Pensilvania, y McCormack en Concord, Nuevo Hampshire.

______

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

‘Out Of Stock’: As Lunar New Year Looms, AsiaPac Dip-Buyers Emerge In Gold

‘Out Of Stock’: As Lunar New Year Looms, AsiaPac Dip-Buyers Emerge In Gold

“I came to buy because the price of gold dropped today,” said Ng Beng Choo, a 70-something retiree who arrived early in the morning at the headquarters of Singapore‘s United Overseas Bank (UOB), the city-state’s only bank offering physical gold products to retail investors.

Bloomberg reports that clients and walk-in buyers crowded into a dedicated lounge for bullion transactions.

Overnight, after an initial puke (catch-down) in precious metals, gold prices are bouncing back, as it appears retail investors are ‘buying the dip’ across AsiaPac.

The extent to which Asian investors buy the dips will play a key role in determining the direction of the market from here.

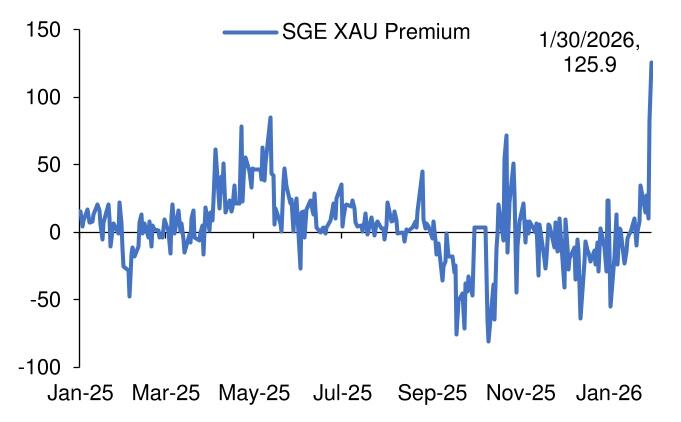

While the Shanghai benchmark price extended losses after the market opened, it was still trading at a premium over the international price.

Over the weekend, buyers flocked to the country’s biggest bullion marketplace in Shenzhen to stock up on gold jewelry and bars ahead of the Chinese New Year.

“The combination of heightened volatility and the proximity of the Lunar New Year will prompt traders to trim positions and reduce risk,” said Zijie Wu, an analyst at Jinrui Futures Co.

At the same time – particularly in peak buying season – the pullback in prices is likely to support retail demand in China, he said.

Rather than seek to sell, many retail investors appeared to be trying to buy the dip in gold, which fell to near $4,400 an ounce on Monday after Friday’s seemingly more technical (ands spectacular) liquidation.

“In my career it’s definitely the wildest that I have seen,” said Dominik Sperzel, the head of trading at Heraeus Precious Metals, a leading bullion refiner.

“Parabolic,” “frenzied” and “untradeable” were all descriptions of the market on Friday, wrote Nicky Shiels, head of metals strategy at MKS PAMP SA.

January 2026, she said, would go down as “the most volatile month in precious metals history.”

But, “fundamental changes played only a minor role in the recent developments,” said Dominik Sperzel, head of trading at Heraeus Precious Metals.

In silver, “limited market liquidity and high leverage significantly amplified the downward momentum,” he said.

“The bottom line is that the trade was way too crowded,” said Robert Gottlieb, a former precious metals trader at JPMorgan Chase & Co. and now an independent market commentator, adding that a reluctance to take further risks would constrain market liquidity.

Bloomberg also reports that in central Sydney, a queue of people snaked out into the street from an ABC Bullion outlet near Martin Place.

“I lost a lot of money” on Friday, but “tomorrow’s a new day,” said Alex, a man in his 20s who was lined up outside the Sydney store to buy bullion, declining to give his full name.

In Thailand, where gold bars and jewelry are popular, people keep their holdings rather than selling off, Thanapisal Koohapremkit, Chief Executive Officer at Thai brokerage Globlex Securities Co. said.

“It’s still a buying trend in here in Thailand,” said Kuhapremkit.

“ They’re holding the old position and then just hold and see.”

Retail buyers may be betting that the main drivers of gold’s ascent – an increasingly unpredictable Trump and the debasement trade where investors avoid currencies and sovereign bonds – are still intact.

That optimism was shared by Michael Hsueh, an analyst at Deutsche Bank AG,, which said in a note on Monday it was sticking with its forecast for gold to get to $6,000 an ounce.

(1) We argue that the adjustment in precious metal prices overshot the significance of its ostensible catalysts. Moreover, investor intentions in precious (official, institutional, individual) have not likely changed for the worse as of yet.

(2) Gold’s thematic drivers remain positive and we believe investors’ rationale for gold (and precious) allocations will not have changed. The conditions do not appear primed for a sustained reversal in gold prices, and we draw some contrasts between today’s circumstance and the context for gold’s weakness in the 1980s and 2013.

(3) We see signs that China has been a prominent driver of precious metal investment flows. Thus, the rise in SGE premiums late last week is an important sign of amplified buying interest in gold. Together these suggest the rationale for a positive outlook has not changed from that described last week (see chart above)

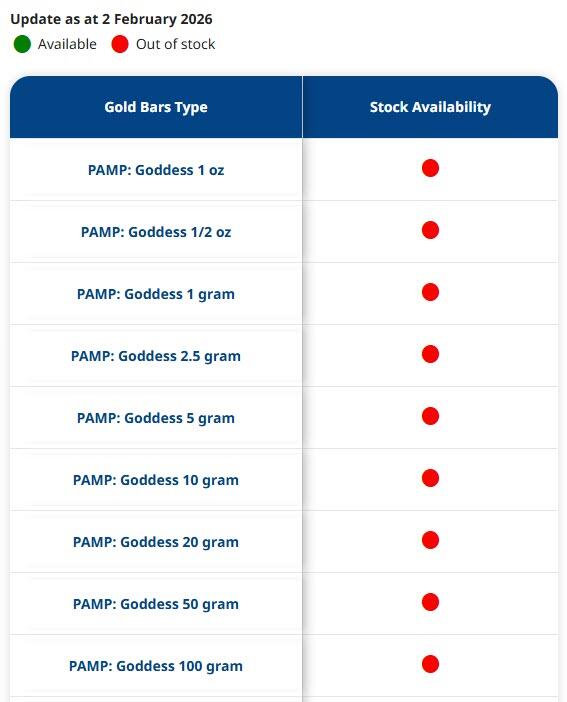

Finally, returning to where we started, Bloomberg reports that at UOB, many customers who hadn’t pre-ordered were disappointed.

All products from MKS PAMP SA, one of the world’s most recognized bullion brands, were sold out, while people who arrived late were out of luck.

“Due to overwhelming response, the buy queue tickets have all been fully issued for the day,” according to notices posted around the UOB headquarters. “Your patience is appreciated.”

Tyler Durden

Mon, 02/02/2026 – 08:25

Oil Prices Tumble 5% Amid Signs Of US-Iran De-escalation

Oil Prices Tumble 5% Amid Signs Of US-Iran De-escalation

Authored by Tsvetana Paraskova via OilPrice.com,

Oil prices dropped by more than 5% on hopes that U.S.–Iran tensions may be easing.

President Trump suggested Iran is engaged in serious talks, dampening fears of military escalation.

Analysts said broader market weakness and election-year politics added to the downward pressure on crude.

Oil prices slumped by 5% early on Monday from a five-month high at the end of last week, after the most recent tensions between the United States and Iran appeared to have eased.

This morning, the Brent Crude international benchmark was back to $65 per barrel, down from $70 it hit last week when U.S. President Donald Trump warned Iran that a “massive armada” of U.S. Navy ships is headed to the Persian Gulf.

Brent Crude prices had slipped by 4.83% to $65.99 on Monday morning, while the U.S. benchmark, WTI Crude, was trading down by 5.11% at $61.92.

Last week, markets reacted to the renewed tension in the world’s most important oil-producing and exporting region, and oil prices soared.

However, this weekend, President Trump said that he believes Iran is “seriously” talking with the U.S., adding he hopes that negotiations could lead to an “acceptable” deal.

President Trump told a reporter aboard Air Force One that he certainly can’t tell them if a military strike is still an option.

“But we do have very big, powerful ships heading in that direction,” President Trump said, but added, “I hope they negotiate something that’s acceptable.”

“They should do that, but I don’t know that they will. But they are talking to us. Seriously talking to us,” the president said, referring to Iran.

Trump says he has quietly imposed a deadline on diplomacy with Iran – just as Turkey, Qatar, and Egypt scramble to keep talks alive. When pressed by reporters, he refused to answer any specifics in terms of planning.

When Israel, followed by the US, attacked Iran last June in the 12-day war, it too was apparently based on an internal timeline only the White House knew about (and presumably Israel) .

Tehran leadership’s working theory seems to be that Iran absorbs heavy blows but responds with unprecedented regional retaliation, including mass-casualty strikes on US forces, to shatter Trump’s apparent belief that war with Iran would look anything like a Venezuela-style operation.

Confronted with that reality, the calculation goes, Trump would be forced to scale back his maximalist demands and reset the parameters.

Whether Iran can actually strike that hard, or survive the scale of US retaliation that would follow, remains an open question.

With the risk premium unwinding, oil prices retreated on Monday from the five-month highs seen last Thursday.

“A broader correction across financial markets has added to the downward momentum,” ING’s commodities strategists Warren Patterson and Ewa Manthey said on Monday.

According to Saxo Bank’s analysts, “With the President facing weak poll numbers, a military escalation that risks pushing gasoline prices sharply higher appears unlikely ahead of the November midterm elections, where affordability and his time in office are set to dominate voter focus.”

Tyler Durden

Mon, 02/02/2026 – 08:05

https://www.zerohedge.com/energy/oil-prices-tumble-5-amid-signs-us-iran-de-escalation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}