Category: News

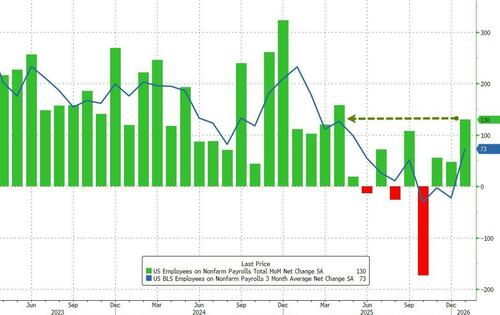

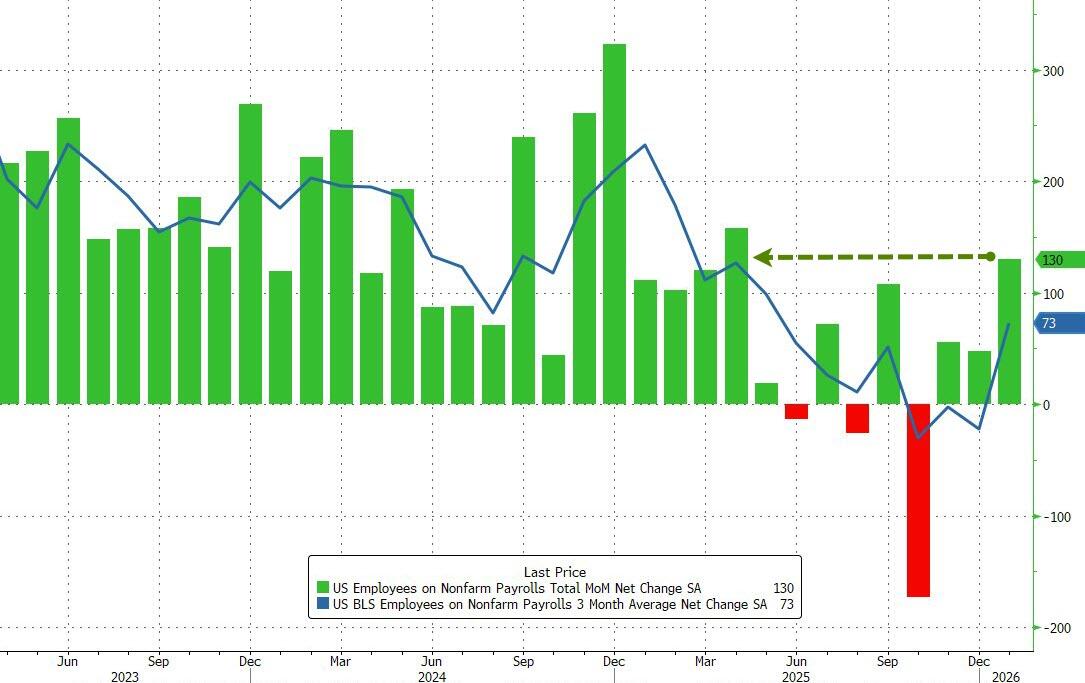

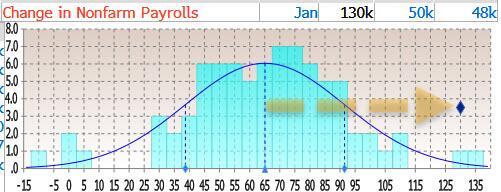

US Unexpectedly Adds 130K Jobs In January, Most Since 2024, Amid Massive Negative Revisions

US Unexpectedly Adds 130K Jobs In January, Most Since 2024, Amid Massive Negative Revisions

Ahead of today’s jobs report, the Trump admin unleashed a full court press to warn markets about what was expected to be a very weak numbers, with Peter Navarro saying “we have to revise our expectations down significantly for what a monthly job number should look like” and Kevin Hassett told CNBC on Monday to “expect slightly smaller job numbers” and that “one shouldn’t panic” if the labor data comes in weak. That’s also why the whisper number ahead of today’s jobs print was well below the consensus, at 35K vs 65K median consensus.

And so with markets and traders fully expecting a ugly print – with Bloomberg’s chief economist looking for a 0 January print – the BLS decided to shock everyone, and reported than in January the US added 130K jobs, double the 65K median estimate and up from a downward revised December print of 48K (vs 50K previously). This was also the highest monthly jobs increase since December 2024.

While today’s number was double the median consensus, here is some additional color: at 130K, the forecast was higher than 79 out of 80 forecasts, with just Citigroup’s 135K forecast higher.

That said, expect today’s number to be revised sharply lower last month: that’s because the November report was revised down by 15,000, from +56,000 to +41,000, and the change for December was revised down by 2,000, from +50,000 to +48,000. With these revisions, employment in November and December combined is 17,000 lower than previously reported. It gets worse though, with 25 of the past 26 jobs reports revised lower.

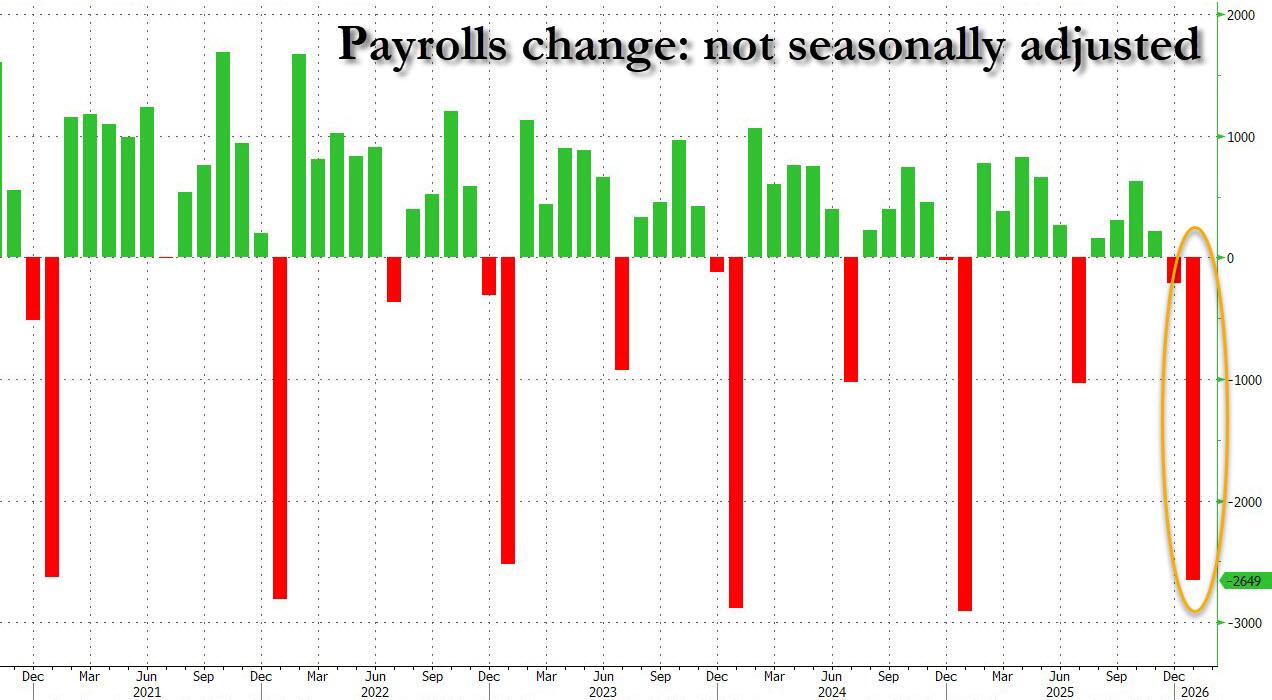

There is another reason why today’s report will be revised away: while the seasonally adjusted change was a stronger than expected 130K, the unadjusted was a negative 2.649 million. That means that the entire delta in today’s “surprise beat” was due to seasonal adjustments.

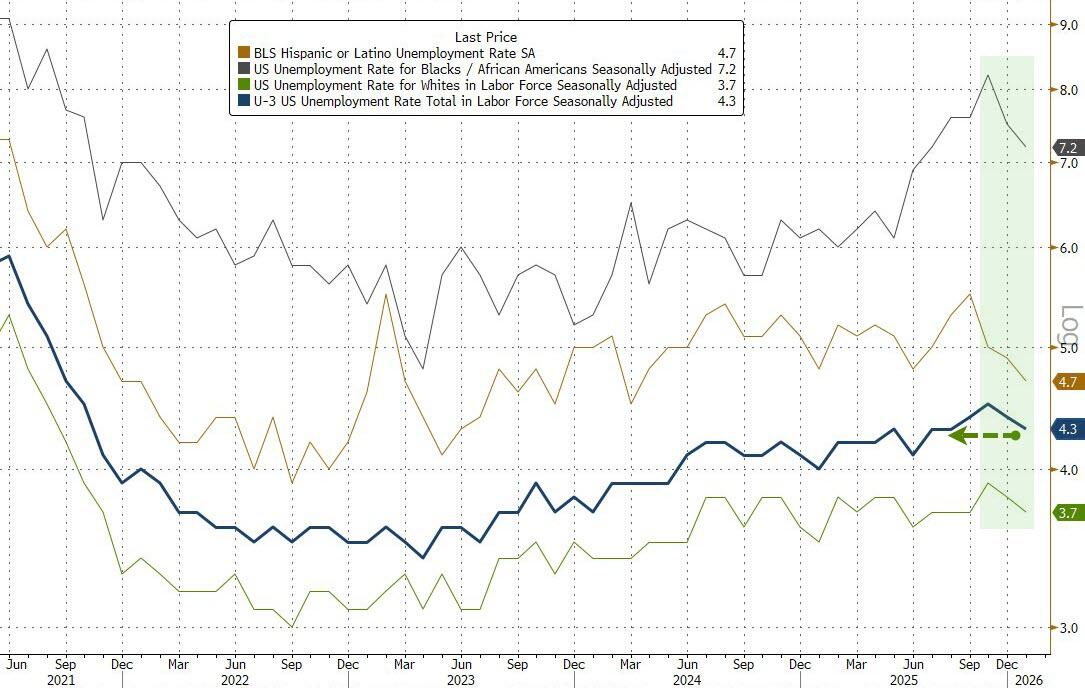

The positive surprise in the payrolls number also translated into improvement in the unemployment rate, which unexpectedly dropped to 4.3%, down from 4.4% in December where it was expected to stay. Among the major worker groups, the unemployment rate for teenagers declined to 13.6 percent in January. The jobless rates for adult men (3.8 percent), adult women (4.0 percent), and people who are White (3.7 percent), Black (7.2 percent), Asian (4.1 percent), or Hispanic (4.7 percent) all posted modest improvements in recent months.

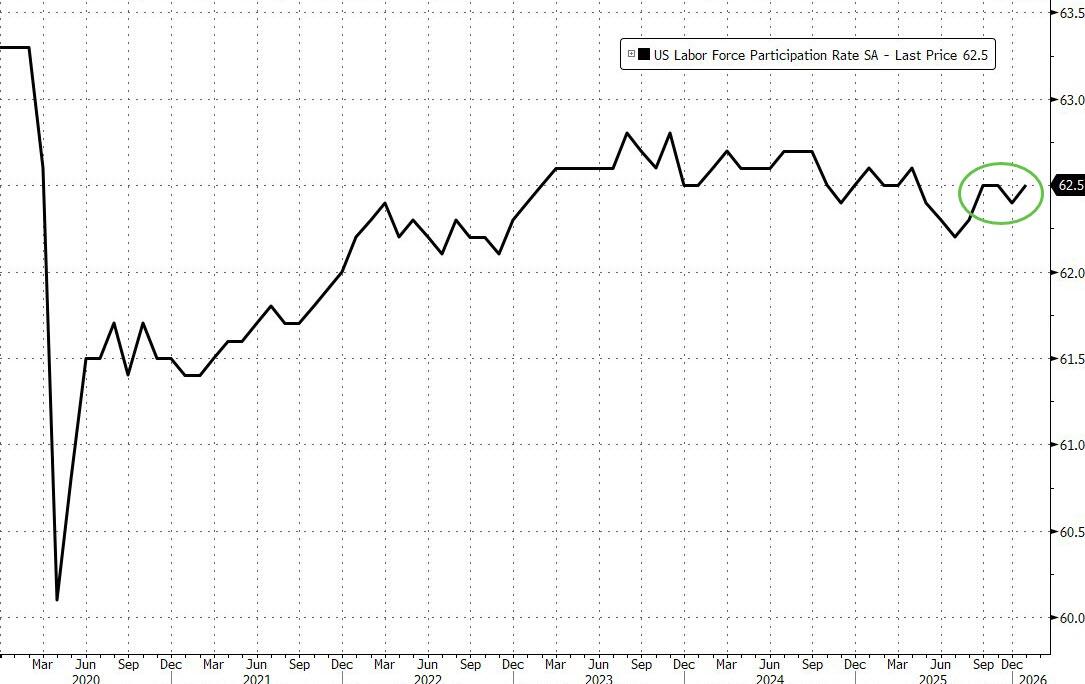

Tied to this, the labor force participation rate rose to 62.5%, up from 62.4% and fractionally better than the expected unchanged print.

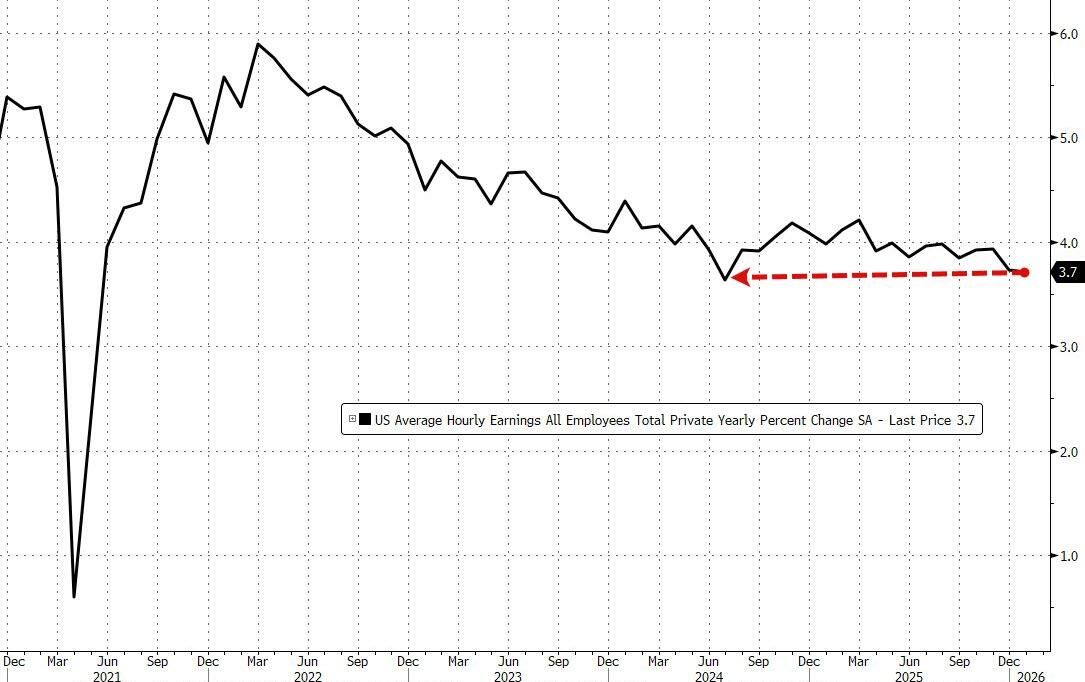

There was more positive surprises: in January, hourly earnings rose 0.4% MoM, up from a downward revised (of course) 0.1% in January and above the 0.3% estimate. On a YoY basis, this translated to a 3.7% increase in average hourly earnings, in line with estimates and unchanged from the previous month.

Some more details from the report:

The number of people employed part time for economic reasons decreased by 453,000 to 4.9 million in January but is up by 410,000 over the year. These individuals would have preferred full-time employment but were working part time because their hours had been reduced or they were unable to find full-time jobs.

In January, the number of people not in the labor force who currently want a job decreased by 399,000 to 5.8 million. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

Among those not in the labor force who wanted a job, the number of people marginally attached to the labor force changed little at 1.7 million in January. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, also changed little at 475,000 in January.

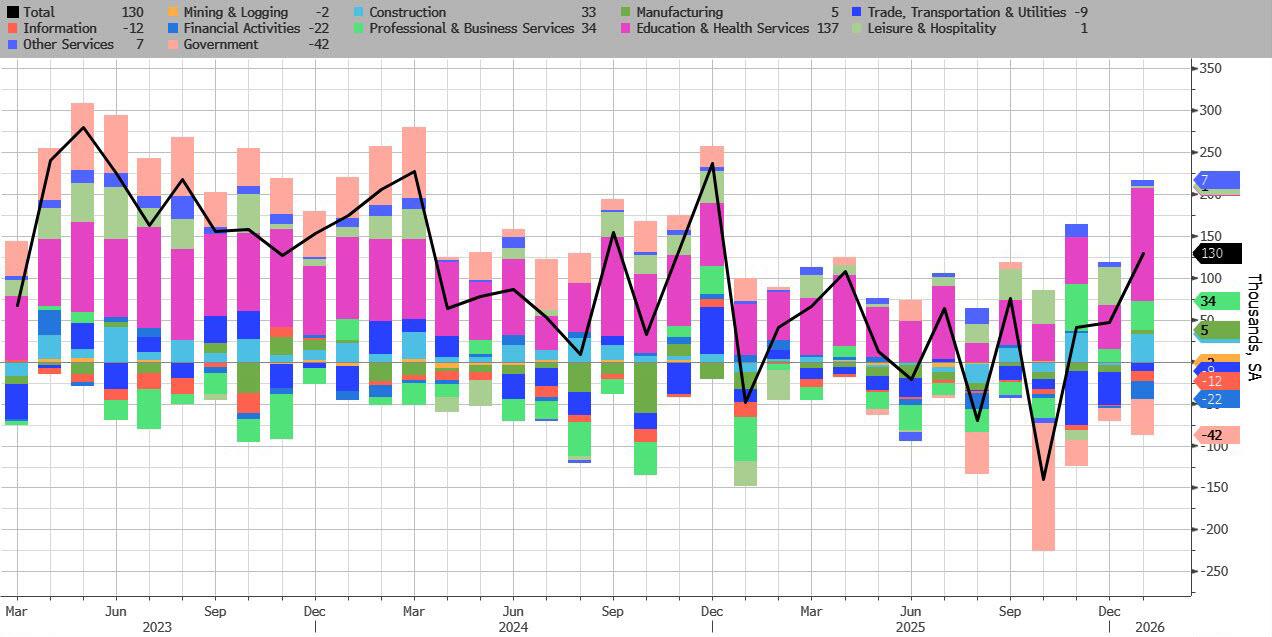

Taking a closer look at the Establishment survey, we find that job gains occurred in health care, social assistance, and construction, while federal government and financial activities lost jobs. Payroll employment changed little in 2025 (+15,000 per month on average).Here is the breakdown:

Health care added 82,000 jobs in January, with gains in ambulatory health care services (+50,000), hospitals (+18,000), and nursing and residential care facilities (+13,000). Job growth in health care averaged 33,000 per month in 2025.

Employment in social assistance increased by 42,000 in January, primarily in individual and family services (+38,000).

Construction added 33,000 jobs in January, reflecting an employment gain in nonresidential specialty trade contractors (+25,000). Employment in construction was essentially flat in 2025.

In January, federal government employment continued to decline (-34,000) as some federal employees who accepted a deferred resignation offer in 2025 came off federal payrolls. Since reaching a peak in October 2024, federal government employment is down by 327,000, or 10.9

percent.

Financial activities employment declined by 22,000 in January and is down by 49,000 since reaching a recent peak in May 2025. Within the industry, insurance carriers and related activities lost 11,000 jobs over the month.

And visually:

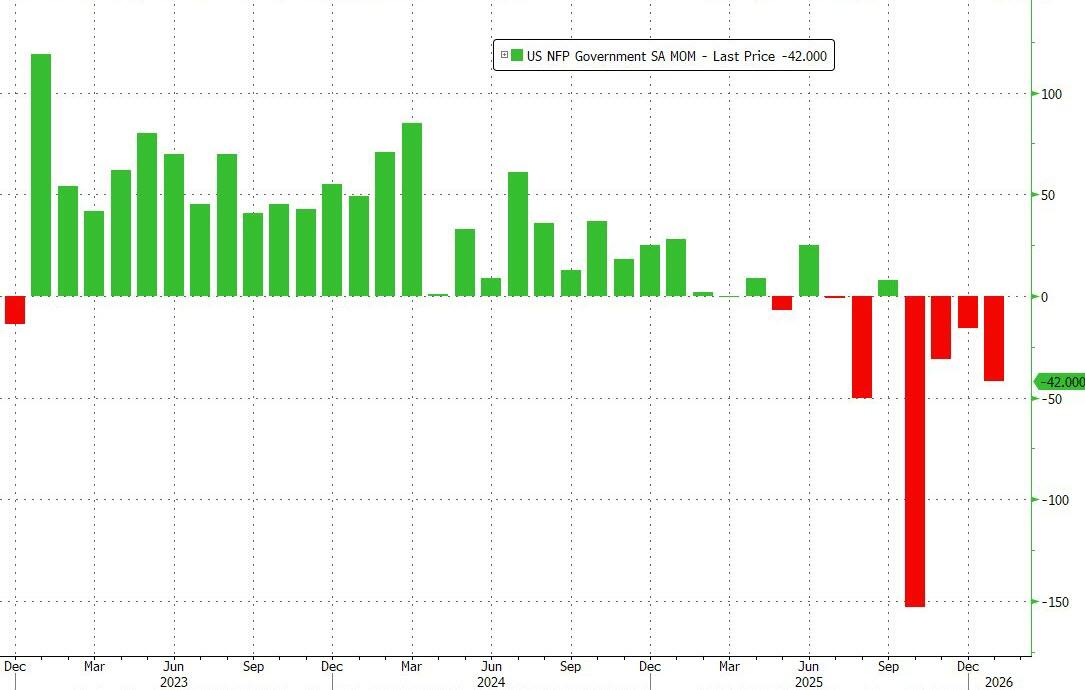

Of these, the most notable is was the ongoing sharp decline in government workers, which tumbled by 42K, and are down 5 of the past 6 months.

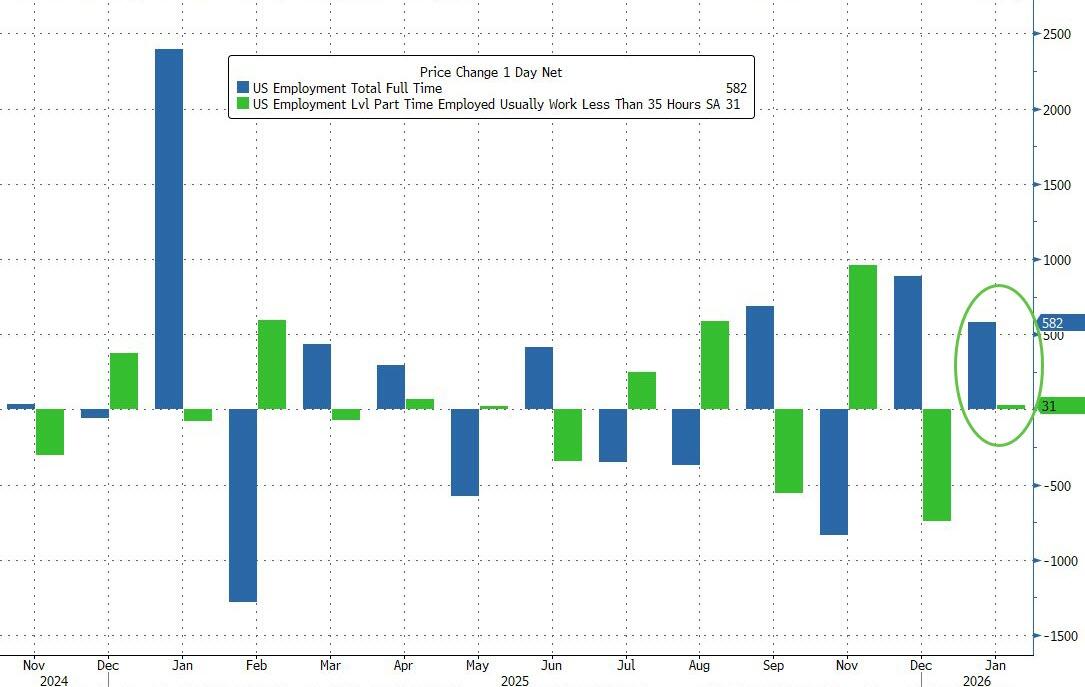

Last but not least, extending last month’s move, in January the bulk of job creation was full time jobs which increased by 582K, while part-time jobs rose by only 31K.

And while the January numbers was stellar (at least until it is revised much lower in coming months), the much uglier part to today’s jobs report was the dramatic negative benchmark revisions which we highlighted yesterday.

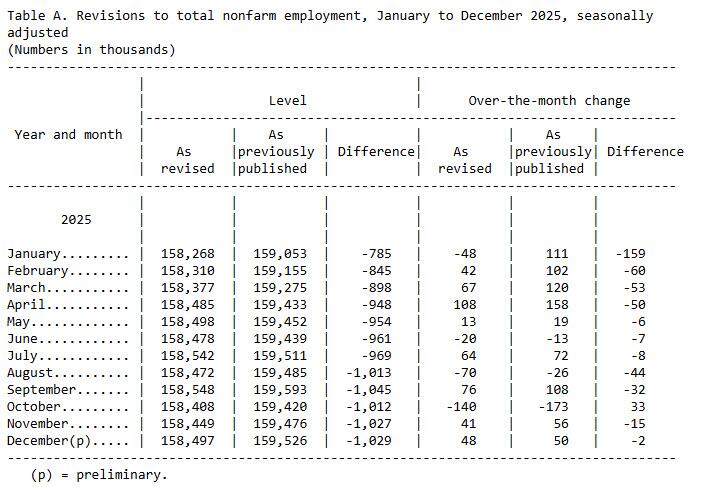

As we noted, the establishment survey data released today was re-benchmarked to reflect comprehensive counts of payroll jobs for March 2025. These counts are derived principally from the Quarterly Census of Employment and Wages (QCEW), which counts jobs covered by the Unemployment Insurance (UI) tax system. The benchmark process results in revisions to not seasonally adjusted data from April 2024 forward. Seasonally adjusted data from January 2021 forward are subject to revision. In addition, data for some series prior to 2021, both seasonally adjusted and unadjusted, incorporate other revisions.

The seasonally adjusted total nonfarm employment level for March 2025 was revised downward by 898,000. On a not seasonally adjusted basis, the total nonfarm employment level for March 2025 was revised downward by 862,000, or -0.5 percent.

AS a result, the change in total nonfarm employment for 2025 was revised from +584,000 to +181,000 (seasonally adjusted), which means that the US barely generated any jobs in 2025, and that instead of creating 49K average jobs per month, the US only added 15K jobs.

We will have more to say on the historic negative revisions shortly, but for now suffice to say, the picture is one of a much weaker jobs market, and the January bounce notwithstanding – and it won’t stand once it is revised lower – the Fed will have no choice but to slash rates aggressively to prevent the already precarious labor market from rolling over into contraction.

Tyler Durden

Wed, 02/11/2026 – 09:04

AI ‘Disruption’ Fears Go Global: France’s Dassault Crashes Most On Record After ‘Weak Guide’

AI ‘Disruption’ Fears Go Global: France’s Dassault Crashes Most On Record After ‘Weak Guide’

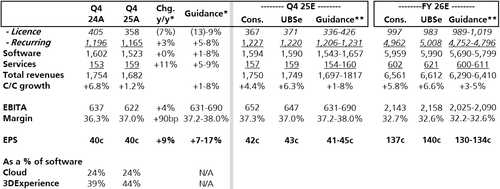

Dassault Systemes, which Nvidia has recently described as being at the epicenter of the “next frontier of artificial intelligence,” suffered its largest intraday decline on record in Paris trading after issuing weaker-than-expected guidance. The miss reinforced the latest market narrative that some software firms are vulnerable to AI-driven disruption, a fear that has crushed software stocks in recent weeks.

Paris-based Dassault reported unaudited estimated financial results for the fourth quarter and guidance for the new year.

The focus among traders was on the company’s guidance for 2026 sales growth of 3% to 5%, well below the 5.9% consensus among Wall Street analysts tracked by Bloomberg. The downgraded outlook was attributed to a softening automotive sector and shrinking life sciences activity.

Dassault also disclosed its annual run rate for the first time, a financial metric used in the software industry, but said growth was about 6% since the fourth quarter of 2023.

“In a software industry that has been accelerating to subscription/ recurring revenues, this is likely to be seen as underwhelming,” Jefferies analyst Charles Brennan wrote in a note.

UBS analyst Michael Briest flagged in a note what he characterized as a “weak finish and a weak guide” for the software company.

Briest wrote:

How did the results compare vs expectations?

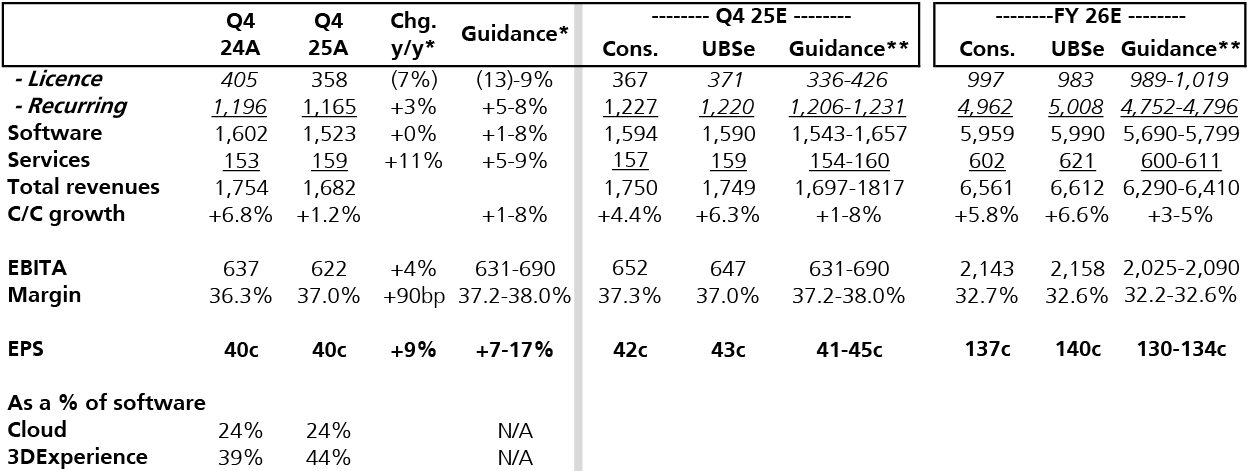

A: Q4 revenues of €1,682m (cons. €1,750m) grew by 1.2% c/c (guidance 1-8%) and just 0.6% organically to €1,682m, with a weak Auto sector in Europe called out. Within this, total Software was flat at €1,523m (guidance 1-8%) with licences down 7% y/y to €358m and at the lower-end of guidance for (13)-9%, while recurring software grew by just 3% to €1,165m (guidance: +5-8%) with subscription up just 4% (guidance 8-12%) and support 2%. Q4 cloud revenues grew by 9% (Q3 25: +8%) but were up 38% for 3DX as Life Sciences fell by 4% y/y with Medidata impacted by lower study volumes. For the year, Medidata reported 1% growth in Direct Enterprise sales (70% of the total) – and would have been +6% excl. Moderna – but CRO volumes (30% of the total) fell by 5%. Q4’s EBIT of €622m/37.0% was 5% below cons. of €652m/37.3% and light of guidance for 37.2-38.0%.

What were the most noteworthy areas in the results?

A: While Asia grew by 6% and the Americas 3%, Europe declined by 5% y/y in Q4. Life Sciences fell by 4% y/y (Q3: -3%). Mainstream 3D grew by 1% (Q3: +4%) despite “good growth” at Solidworks as CentricPLM weighed. 3DExperience revenues fell by 3% y/y (Q3: +16%). FCF for the year grew by 2% to €1,380m but would have been 5% excl. French tax effects albeit overall taxes paid were €32m lower y/y and DSOs rose to 117 vs 109 last year. Contract liabilities movements were also a slight outflow in the year we note. Headcount was down 0.2% y/y at 25,967. In a new KPI, ARR grew 6% y/y to €4,497 in Q4.

Has the company’s outlook/guidance changed?

A: 2026 guidance is introduced for 3-5% c/c growth to €6,410m revenues at the high-end (VA cons. +5.8% to €6,561m) and assumes a $1.18 FX rate. This includes Software at 3-5% (cons. +5.5% c/c) and licences at (1)-2% (FY25: -6%). A margin of 32.2-32.6% is expected vs cons. at 32.7% and FY25’s 32.0%. EPS should grow just 3-6% c/c to €1.30-1.34 (cons. €1.37). For Q1, total sales are expected to grow 1-5% to €1,541m at the high end (cons. €1,590m), with total software growing 1-5% (Q1 25: +5%), including licences at 0-8% y/y (Q1 25: -10%). Guidance is for a Q1 margin of 29.2-30.7% (cons. 31.9%). DS talks of “aligning the organisation to focus” on execution and a CMD is planned in November. Having set a goal to grow at least 7%pa from 2024-29, the guidance means DS now needs to grow 8.2-8.9% in 2027-29.

Via the UBS analyst: Figure 1: Dassault Q4 25 results summary (€m)

Shares in Paris posted their steepest decline on record, plunging 22%. The bull market peaked in 2021, and the liquidation phase has been ongoing since 2024. The next technical level to watch is the 76.4% Fibonacci retracement, around 15 euros.

Traders are sorting “AI winners vs. losers,” pressuring companies seen as highly exposed, including peers such as Autodesk and Synopsys.

Dassault creates “virtual twins” using Nvidia models of complex machines, a field increasingly threatened by other AI “world models” that help systems navigate the physical world.

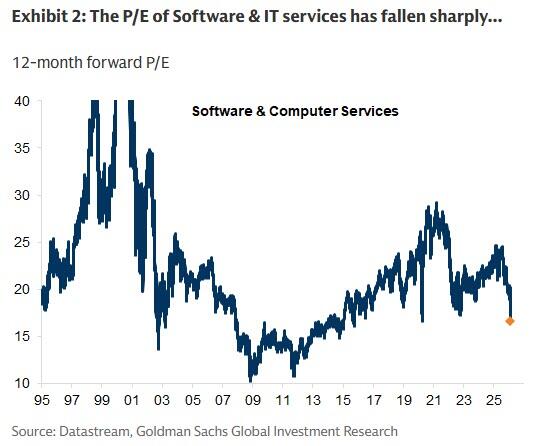

Software valuations have crashed.

But as we note in recent trading sessions:

Software Pops, Financials Flop As ‘Bad’ Data Sparks Bond Bid, Rate-Cut Hopes

‘Off The Charts’: Retail Is Buying-The-Dip In Software Stocks Like Never Before

Our Market Ear technicians say:

Everybody Hates Software — And That’s the Setup

“Our vision is built on decades of industrial and scientific knowledge and know-how, and we are now building the capabilities to turn that vision into reality,” CEO Pascal Daloz said in a statement, adding, “True transformation takes time, for our customers and for ourselves.”

Tyler Durden

Wed, 02/11/2026 – 09:00

https://www.zerohedge.com/markets/dassault-systemes-crashes-most-record-over-ai-fears

Tottenham despide al técnico Thomas Frank tras mala racha en la Premier

Por JAMES ROBSON

El técnico Thomas Frank fue despedido el miércoles por Tottenham tras una efímera etapa de ocho meses al mando y con su equipo apenas cinco puntos por encima de la zona de descenso en la Liga Premier.

A pesar de llevar a los Spurs a los octavos de final de la Liga de Campeones, los resultados de Tottenham en el plano doméstico han sido decepcionantes. La derrota 2-1 ante Newcastle el martes fue recibida con silbidos de los hinchas locales. El equipo sigue sin conocer la victoria en la liga en lo que va de 2026.

“El club tomó la decisión de hacer un cambio en la posición de técnico del equipo masculino y Thomas Frank dejará el cargo hoy”, anunció Tottenham en un comunicado. “Thomas fue nombrado en junio de 2025, y estuvimos decididos en darle el tiempo y el apoyo necesarios para construir juntos para el futuro”.

“Sin embargo, los resultados y las actuaciones han llevado a la junta directiva a concluir que un cambio en este punto de la temporada es necesario”, agregó.

Desfile de técnicos

Los Spurs iniciarán la búsqueda del sexto entrenador en menos de siete años desde que el argentino Mauricio Pochettino se marchó en 2019.

El danés Frank fue nombrado al final de la temporada pasada cuando Ange Postecoglou fue despedido a pesar de llevar al Tottenham a su primer trofeo en 17 años al conquistar la Liga Europa y asegurar la clasificación para la Liga de Campeones.

Frank se ganó una impresionante reputación por su trabajo durante un período de nueve años al mando de Brentford cuando estableció al modesto club londinense como un rival de cuidado en la Premier. Pero no pudo repetir ese éxito en Tottenham, donde apenas logró siete victorias en 26 partidos de la liga inglesa.

La última victoria en la liga de los Spurs se remonta al 28 de diciembre y la derrota en casa ante Newcastle les dejó con apenas una victoria en 11 partidos en la máxima categoría de Inglaterra.

Los Spurs cayeron al puesto 16 en la clasificación, dos lugares por encima de la zona de descenso.

Las lesiones resultaron costosas

Frank no fue ayudado por una extensa lista de lesiones que incluía a figuras clave como James Maddison, Dejan Kulusevski, Rodrigo Bentancur, Mohammed Kudus y Lucas Bergvall.

El capitán Cristian Romero también estuvo ausente contra Newcastle después de que el defensor argentino fue expulsado en el partido anterior contra ell Manchester United.

Frank dijo después de la derrota ante el Newcastle que estaba “convencido” de que seguiría a cargo para el próximo clásico contra Arsenal más adelante este mes.

“Si haces algo bien, construyes algo que puede durar”, dijo. “Por supuesto, no estamos en una posición superior ahora. Todos saben —directores, propietarios, yo mismo— en qué posición estamos, qué necesitamos mejorar y qué necesitamos hacer mejor. Eso es en lo que estamos trabajando muy duro”.

Borrón y cuenta nueva

Frank se una amplia lista de técnicos que no han logrado revivir a Tottenham. Siguió los pasos de algunos renombrados estrategas, como Antonio Conte y José Mourinho, quienes no pudieron sacar adelante al club del norte de Londres.

E incluso cuando Postecoglou logró alzar un trofeo importante y el boleto a la lucrativa Liga de Campeones, no fue suficiente para salvar su trabajo.

Postecoglou pagó el precio por una nefasta campaña doméstica que dejó a los Spurs terminar en el puesto 17, su más bajo desde que se fundó la Premier en 1992.

El desempeño en la liga también le pasó factura a Frank, cuyo equipo sacó menos que el de Postecoglou en esta etapa el año pasado.

___

Deportes AP: https://apnews.com/hub/deportes

Rusia afirma que respetará los límites nucleares del Nuevo START siempre que EEUU lo haga

Por VLADIMIR ISACHENKOV

MOSCÚ (AP) — Moscú observará los límites del más reciente pacto de armas nucleares con Estados Unidos, que expiró la semana pasada, siempre que vea que Washington hace lo mismo, dijo el miércoles el principal diplomático de Rusia.

El tratado Nuevo START expiró el 5 de febrero, dejando sin restricciones a los dos mayores arsenales atómicos por primera vez en más de medio siglo y alimentando temores de una carrera armamentista nuclear sin control.

El presidente ruso Vladímir Putin declaró el año pasado su disposición a adherirse a los límites del tratado por un año más si Washington hacía lo mismo, pero el presidente de Estados Unidos, Donald Trump, ha argumentado que quiere que China sea parte de un nuevo pacto, algo que Beijing ha rechazado.

Comentarios a los legisladores rusos

El miércoles, ante la cámara baja del Parlamento, el ministro de Relaciones Exteriores de Rusia, Serguéi Lavrov, dijo que, aunque Estados Unidos no ha respondido a la oferta de Putin, Rusia respetará los límites del Nuevo START mientras vea que Estados Unidos también los observa.

“La moratoria declarada por el presidente se mantendrá mientras Estados Unidos no exceda estos límites”, dijo Lavrov a los legisladores. “Actuaremos de manera responsable y equilibrada con base en el análisis de las políticas militares de Estados Unidos”.

Agregó que “tenemos razones para creer que Estados Unidos no tiene prisa por abandonar estos límites y que serán observados en el futuro previsible”.

“Vigilaremos de cerca cómo se desarrollan realmente las cosas”, dijo Lavrov. “Si se confirma la intención de nuestros colegas estadounidenses de mantener algún tipo de cooperación en esto, trabajaremos activamente en un nuevo acuerdo y consideraremos los temas que han quedado fuera de los acuerdos de estabilidad estratégica”.

Conversaciones entre Estados Unidos y Rusia en Abu Dabi

La declaración de Lavrov se produjo tras la divulgación de un informe de Axios donde se afirma que negociadores rusos y estadounidenses analizaron un posible acuerdo informal para observar los límites del pacto durante al menos seis meses en conversaciones sostenidas la semana pasada en Abu Dabi. Al ser consultado sobre el informe, el portavoz del Kremlin, Dmitry Peskov, dijo el viernes que cualquier extensión de este tipo solo podría ser formal, agregando que “es difícil imaginar cualquier extensión informal en esta esfera”.

Al mismo tiempo, Peskov confirmó que negociadores rusos y estadounidenses hablaron sobre el futuro control de armas nucleares en Abu Dabi, donde delegaciones de Moscú, Kiev y Washington mantuvieron dos días de conversaciones sobre un acuerdo de paz en Ucrania.

“Hay un entendimiento, y hablaron de ello en Abu Dabi, de que ambas partes tomarán posiciones responsables y ambas partes se dan cuenta de la necesidad de iniciar conversaciones sobre el tema lo antes posible”, dijo Peskov.

Los límites del Nuevo START

El Nuevo START, firmado en 2010 por el entonces presidente Barack Obama y su homólogo ruso, Dmitry Medvedev, ha sido el más reciente de una larga serie de acuerdos entre Moscú y Washington para limitar sus arsenales nucleares, que comenzó con el SALT I en 1972.

El Nuevo START restringía a cada una de las partes a poseer no más de 1.550 ojivas nucleares en no más de 700 misiles y bombarderos desplegados y listos para su uso. Originalmente, su expiración estaba prevista para 2021, pero el pacto fue extendido por cinco años.

El acuerdo preveía amplias inspecciones in situ para verificar el cumplimiento, aunque se detuvieron en 2020 debido a la pandemia de COVID-19 y nunca se reanudaron.

En febrero de 2023, Putin suspendió la participación de Moscú, diciendo que Rusia no podía permitir inspecciones estadounidenses de sus sitios nucleares en un momento en que Washington y sus aliados de la OTAN declararon abiertamente que querían la derrota de Moscú en Ucrania. Pero el Kremlin también enfatizó que no se retiraba del pacto por completo, comprometiéndose a respetar sus límites sobre armas nucleares.

En septiembre, Putin ofreció mantener los límites del Nuevo START por un año más para ganar tiempo y lograr que ambas partes negocien un acuerdo sucesor.

Aun cuando el Nuevo START expiró, Estados Unidos y Rusia acordaron el 5 de febrero restablecer un diálogo de alto nivel, de ejército a ejército, tras una reunión entre altos funcionarios de ambas partes en Abu Dabi, dijo el comando militar de Estados Unidos en Europa. El enlace fue suspendido en 2021 debido a que las relaciones se volvieron cada vez más tensas antes de que Rusia enviara tropas a Ucrania en febrero de 2022.

——

The Associated Press recibe apoyo para la cobertura de seguridad nuclear de la Carnegie Corporation de Nueva York y la Outrider Foundation. La AP es la única responsable de todo el contenido.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

EEUU añadió 130.000 empleos el mes pasado, pero cifras revelan baja para 2024-2025

Por PAUL WISEMAN

WASHINGTON (AP) — Los empleadores en Estados Unidos añadieron la cifra sólida 130.000 empleos el mes pasado, pero las revisiones gubernamentales redujeron las nóminas de 2024-2025 en cientos de miles.

La tasa de desempleo cayó al 4,3%, informó el Departamento de Trabajo el miércoles.

El informe incluyó revisiones importantes que redujeron el número de empleos creados el año pasado a solo 181.000, la cifra más débil desde el año de la pandemia de 2020, y menos de la mitad de los 584.000 reportados anteriormente.

El mercado laboral ha estado lento durante meses, aunque la economía está registrando un crecimiento sólido.

La débil contratación refleja el impacto persistente de las altas tasas de interés, la purga de la fuerza laboral federal realizada por el multimillonario Elon Musk el año pasado y la incertidumbre derivada de las erráticas políticas comerciales del presidente Donald Trump, que han dejado a las empresas inseguras sobre la contratación.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

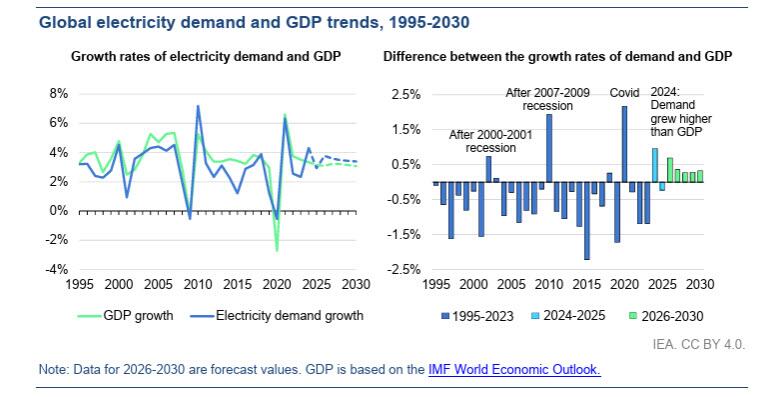

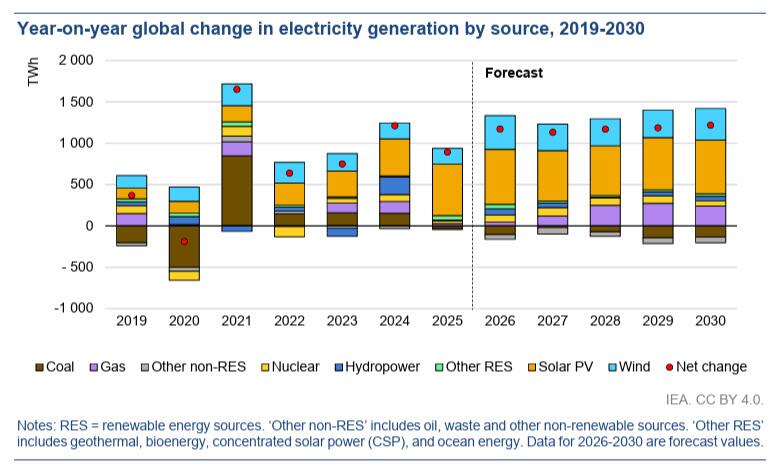

Electricity Demand Is Surging, The Grid Isn’t Ready: IEA

Electricity Demand Is Surging, The Grid Isn’t Ready: IEA

By Tsvetana Paraskova of OilPrice.com

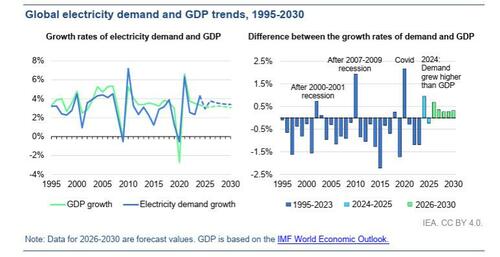

International Energy Agency says global electricity demand is growing at its fastest pace in 15 years, set to rise more than 3.5% annually through 2030.

While renewables, nuclear, and natural gas are expanding rapidly, grid infrastructure is becoming the key bottleneck, with over 2,500 GW of power and load projects stuck in connection queues worldwide.

Grid investment must rise about 50% above current levels to keep pace, with BloombergNEF and Goldman Sachs warning that persistent grid constraints could trigger power shortages and even undermine the U.S. position in the global AI race

Global electricity demand is rising at the fastest pace in 15 years and will continue to do so at least until the end of the decade as AI infrastructure, advanced manufacturing, and electrification have ushered in The Age of Electricity, the International Energy Agency (IEA) says.

Global power demand is expected to grow by more than 3.5% per year on average through the end of the decade, the agency said in its new Electricity 2026 report.

Renewables, nuclear, and natural gas are the big winners of the electricity demand boom, but the rise in all these power-generating sources would not mean anything if they struggle to connect to the grid.

Power Demand Surge

Global electricity demand increased by 3% annually in 2025, following growth of 4.4% in 2024, the IEA said in the report.

Between 2026 and 2030, the annual average growth rate would be 3.6%, driven by higher consumption from industry, electric vehicles (EVs), air conditioning, and data centers, according to the agency.

While emerging economies, including China, India, and the Southeast Asian region, will drive 80% of the additional power demand by 2030, advanced economies see growth in electricity demand after 15 years of stagnation, the IEA said. Artificial intelligence, data centers, and advanced manufacturing support the return to growth in power demand in advanced economies.

U.S. electricity demand rose by 2.1% in 2025 and is expected to grow by nearly 2% annually through 2030. The rapid expansion of data centers will drive half of the increase, the agency noted.

EU demand is forecast to increase by around 2% per year through 2030, and many other advanced economies – such as Australia, Canada, Japan, and South Korea – are also expected to see faster electricity demand growth through 2030.

Grid Investment Lagging Behind Power Generation Boom

As demand grows, developers of new capacity, especially renewables and natural gas, face constraints in connecting to the grids. Regional and country-specific trends are not the same, but the need for rapid and efficient expansion of grids is a pressing global issue. Without increased system flexibility and rapid grid expansion, the Age of Electricity could roll out slower than expected.

Today, global investments in grids are about $400 billion per year. If the world is to meet the expected growth in power demand through 2030, it would need to boost annual grid investment by about 50% from $400 billion, according to the IEA.

The Age of Electricity will also need “a significant scaling up of grid-related supply chains,” the IEA said.

Currently, more than 2,500 gigawatts (GW) worth of projects – renewables, storage, and projects with large loads such as data centers – are stalled in connection queues worldwide.

A total of 1,600 GW of queued projects could be integrated in the near term through grid-enhancing technologies and regulatory reforms that enable more flexible grid connections and usage, the agency reckons.

But increased flexibility and grid expansion need more investment than the current spending.

Last year, grid investment was on track to top $470 billion for the first time, up by 16% from 2024, a December analysis from BloombergNEF found.

The U.S. accounted for a quarter of global grid spending with the highest investment level in 2025, at $115 billion. China and the EU/UK followed as other major contributors, each with around 20% of the global sum, according to the report.

However, rising equipment costs compounded by high inflation have started to affect overall spending figures, BNEF said, adding that increased spending “will not fully eliminate ongoing grid-infrastructure bottlenecks, meaning delays to new generation and demand connections are likely to continue in the coming years.”

“We’ve seen that even with increased investment, there are significant barriers to meeting the needs of new generation and power demand on time,” Peter Wall, Head of Grids Research at BloombergNEF, said.

“With data centers and industrial electrification driving sharp increases in power demand, investors need to factor in how essential timely grid expansion is for not only connecting new demand but also connecting all of the generation we will need to ensure a secure and reliable supply to this demand after over a decade of stagnation.”

Additional grid investment is hampered by supply chain and labor constraints, BloombergNEF notes.

In the U.S. specifically, the aging grid infrastructure in key regional U.S. markets cannot cope with all requests, with grid investments lagging behind soaring power demand.

At the current rate of interconnection requests and grid capacity, the U.S. could face a power crunch by 2030, Samantha Dart, Goldman Sachs’ co-head of global commodities research, said at a conference last month.

“We aren’t adding enough capacity,” Dart said in January at the Goldman Sachs Energy, CleanTech and Utilities Conference in Miami.

Nearly all power grids in the U.S. may lack critical spare capacity by the end of the decade. If the issue with grid constraints remains unaddressed, China could pull ahead of the U.S. in the AI race, Dart noted.

Tyler Durden

Wed, 02/11/2026 – 08:40

https://www.zerohedge.com/markets/electricity-demand-surging-grid-isnt-ready-iea

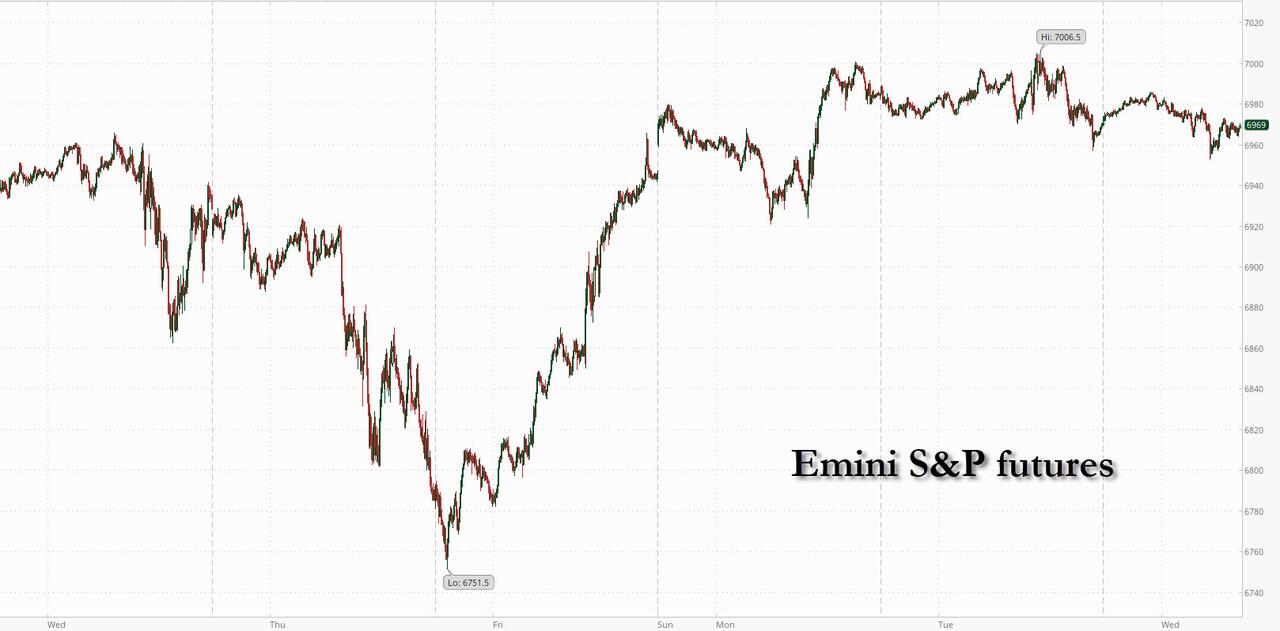

Futures Rise Ahead Of Today’s Delayed Jobs Report

Futures Rise Ahead Of Today’s Delayed Jobs Report

US equity futures are flat ahead of today’s delayed January payrolls (full preview here) with the market now expecting a weaker print after the Retail Sales miss and weaker high-frequency data. As of 8:00am ET, S&P and Nasdaq 100 futures are both up 0.1%. Pre-market, Mag7 names are mostly lower; Discretionary, Energy, Industrials and Materials are all higher pointing to a potential broad-based cyclical rally while TMT is muted; AI ex-Mag7 is seeing a bid. JPMorgan’s trading desk expects the delayed January data to give a small boost to stocks — something much-needed amid the indiscriminate selling of those on the wrong side of AI. International markets are mixed with trends similar – Japan closed, KOSPI strong up 100bps, HSI not far behind up 30bps. Europe more flat to down with CAC down 13bps and DAX off 24bps. Australia leads the downside off 172bps. 10 TSY yields are at lows 4.13%, while the USD is weaker for the 4th consecutive session, the DXY down below $97 to $96.58 and Bitcoin trades down to $67k. FT reports Ukraine planning presidential elections and a referendum on any peace deal, potentially by mid-May, under US pressure. Timing uncertain given Donbas, Zaporizhzhia and escalation risks. China CPI soft +0.2% vs. 0.4%. Commodities moving higher this morning led by silver but Comex copper back above $6 to $6.07 up 3%, crude quietly moving up with WTI at $65. Today’s macro data focus is on the NFP release but watch the drop in Mortgage Approvals given the strength of the recent Homebuilders bid. McDonald’s and Cisco are due to report.

In premarket trading, Mag 7 stocks are mixed (Nvidia +0.6%, Amazon +0.2%, Microsoft +0.2%, Alphabet +0.07%, Apple -0.04%, Meta -0.4%, Tesla -0.2%)

Astera Labs (ALAB) falls 11% after the semiconductor manufacturing company reported its fourth-quarter results. It also announced that its chief financial officer would retire.

Beta Technologies (BETA) climbs 18% after Amazon.com Inc. disclosed a stake in the electric-powered aircraft manufacturer.

Centrus Energy (LEU) falls 8% after the uranium company’s fourth-quarter earnings per share fell short of analyst estimates, with Citi pointing to higher-than-expected capex spending.

Cloudflare (NET) gains 14% after the software company’s fourth-quarter results beat expectations and it gave a bullish revenue forecast.

Humana (HUM) falls 6% after forecasting full-year profit that fell short of Wall Street’s expectations, adding to investor concerns about the challenges facing the US health-insurance industry.

Kraft Heinz (KHC) falls 6% after pausing work on its planned separation as new Chief Executive Officer Steve Cahillane works to improve results.

Lattice Semiconductor (LSCC) rises 11% after the semiconductor device company gave a first-quarter revenue forecast that was much stronger than expected.

Lyft (LYFT) falls 17% after issuing a disappointing forecast that missed Wall Street expectations, a sign that its global expansion and new product offerings are not performing as quickly and as well as anticipated.

Mattel (MAT) slumps 26% after the toymaker’s 2026 adjusted earnings-per-share forecast missed the average analyst estimate, triggering a downgrade at JPMorgan.

Moderna (MRNA) falls 10% after US regulators refused to review its novel mRNA flu vaccine, dealing a major blow to the company as it seeks to expand beyond its Covid shot.

Rapid7 (RPD) falls 22% after the software company’s outlook was seen as disappointing. Analysts cited weakness in annual recurring revenue as a concern.

Robinhood (HOOD) declines 7% after the fintech company reported net revenue for the fourth quarter that missed the average analyst estimate.

Teradata (TDC) gains 15% after the database management company reported fourth-quarter results that beat expectations and gave an outlook for adjusted earnings that is stronger than expected.

Vertiv Holdings (VRT) rises 13% after the power equipment company forecast adjusted earnings per share for the first quarter; the guidance beat the average analyst estimate.

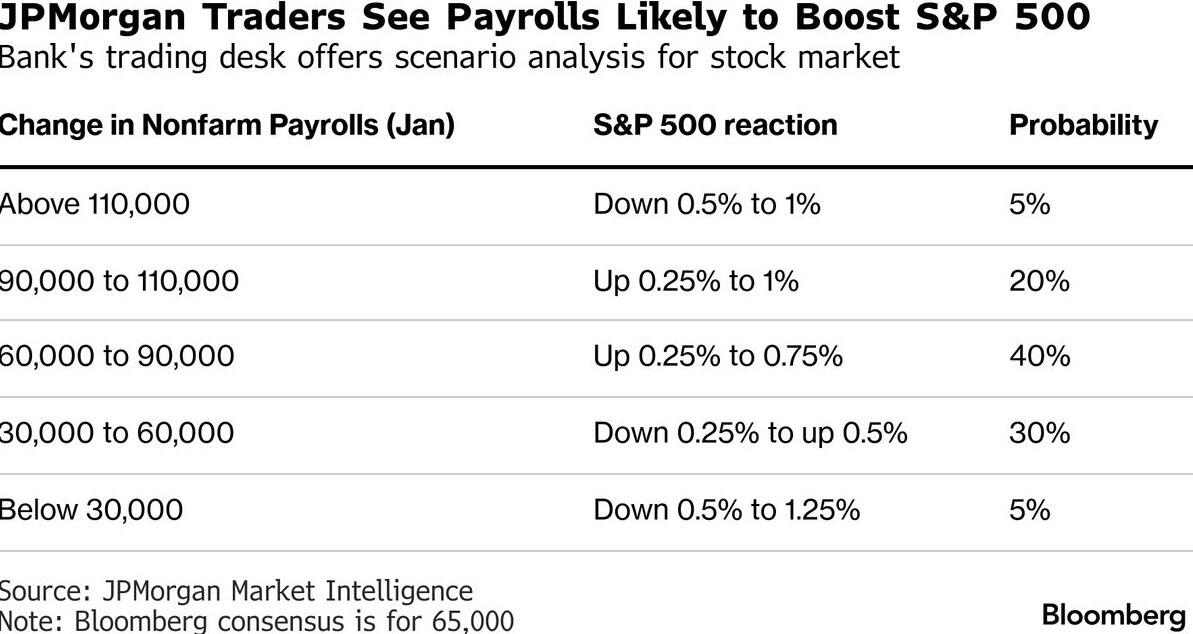

January’s payrolls report (full preview here) is due after several Trump admin officials, including National Economic Council Director Kevin Hassett and Peter Navarro, recently warned that investors should expect lower jobs numbers going forward. Analysts are also anticipating an annual revision to the jobs count, which is expected to reveal a huge markdown in the year through March 2025, to the tune of 750-900K jobs. Bloomberg’s consensus is for 65k job additions in January vs 50k in December, with a crowd-sourced whisper number of 35k, while scenarios laid out by JPMorgan Market Intelligence suggest a sweet spot between 60k and 110k to boost stocks. With the job market in the midst of a “low-hire, low-fire” environment, expectations are low, which could act as a potential catalyst for equities.

JPMorgan strategists also note that the S&P 500 options market is underpricing payrolls compared to historical swings, with past moves nearly double what is currently being priced. Meanwhile, interest-rate traders are betting on two or three Fed rate cuts this year, becoming slightly more conservative than the dovish bets seen after Warsh’s nomination earlier in the month.

“We’re still in this sort of, not-really-hiring, not-really-firing mode. But we haven’t seen a clear breakout in either direction,” said Graham Secker, head of equity strategy at Pictet Wealth Management. “Everyone’s very aware of the kind of the K-shape dynamic within the US economy, and the US consumer in particular.”

For Nicolas Bickel, group head of investment private banking at Edmond de Rothschild, the jobs report and Friday’s inflation data will offer insight into the impact of January’s extreme weather. A strong jobs report would instill confidence in the consumer outlook and help fuel a broadening of the stock rally.

“I really like that rotation personally, because it’s for me the lifeblood of a bull market,” Bickel said. Investors “are just choosing another horse, and means that they have money to be invested, or are confident in the economy.”

The selloff in software stocks has been overblown, creating buying opportunities for investors, according to Nannette Hechler-Fayd’Herbe, head of investment strategy for EMEA at Lombard Odier.

“There have been a lot of concerns that AI might be disrupting software companies, but we have held the view that actually, it is empowering them, it is shortening the time for coding, it is enabling efficiencies of workflows,” she told Bloomberg TV. “For us it’s actually been an opportunity to take exposure.”

In other assets, Bitcoin fell to its lowest level since last Friday’s selloff, despite support from its largest holders, so-called whale wallets, in their biggest buying spree since November. The dollar also fell for a fourth straight day. In Europe, shares in software firms and wealth managers continued to slide on AI disruption fears.

In politics, House lawmakers are set to vote today on whether to reject some of Trump’s tariff policies, starting with a resolution opposing levies on Canada. Trump is expected to unveil plans to use government funding and Pentagon contracts to sustain coal-fired power plants.

A quick look at earnings: Out of the 326 S&P 500 companies that have reported so far in the earnings season, 78% have managed to beat analyst forecasts, while 17% have missed. T-Mobile, Shopify and Kraft Heinz are among companies expected to report before the market open. T-Mobile’s new CEO is likely to maintain a strategy of promoting aggressively to sustain industry-leading postpaid phone net additions and service growth, according to Bloomberg Intelligence. Earnings from Cisco and McDonald’s follow later.

Stocks in Europe are mixed, the Stoxx 600 is up 0.1%. The FTSE 100 outperforms peers, boosted by energy and materials stocks. European wealth managers tracked their US peers lower amid fears over the disruptive impact of a new AI tool designed to create tax strategies. St James’s Place Plc slumped 12% in London, while investment platforms such as AJ Bell Plc and IntegraFin Holdings Plc were sliding as well. Weak guidance by Dassault Systemes SE played into fears that the French software firm may be vulnerable to AI, sending the stock lower by the most in three decades. Here are some of the biggest movers on Wednesday:

Ahold Delhaize shares gain as much as 9.9%, the most since 2020, as the Dutch retail store operator reported margin beats across the board.

Siemens Energy shares rally as much as 6.5% to its highest intraday level on record after first-quarter earnings surpassed the average analyst estimate, driven by strong order growth in gas turbines.

Heineken shares rise as much as 5.5%, the most in nearly a year, after the Dutch brewer exited 2025 with what analysts consider an uptick in momentum, boosted by a cost-saving program that sees it cut up to 6,000 jobs.

Renishaw shares rise as much as 6.4%, the most in five months, as the engineering firm’s order book grows.

B&M shares climb as much as 5.4% after Peel Hunt upgraded its recommendation on the discount retailer, arguing that the shares appear undervalued given the prospects for stronger sales and earnings.

Gerresheimer shares plunge as much as 35%, hitting their lowest level since 2009, after the German maker of packaging for medicines and cosmetics delayed the publication of its 2025 earnings.

Dassault Systemes shares sink as much as 22% the most on record, after the software company gave a weaker-than-expected sales growth guidance for 2026, on top of 4Q results that missed estimates.

St James’s Place shares fall as much as 11%, the most in nearly two years, leading a drop in European wealth managers over worries that artificial intelligence will disrupt their businesses.

Randstad shares fall as much as 9.3%, touching the lowest level since March 2020, after the staffing and HR services provider reported organic revenue for the fourth quarter that missed the average analyst estimate.

Barratt Redrow shares fall as much as 8.4%, the most since July, as pressure increases on the UK homebuilder’s margins.

Earlier in the session, Asian equities climbed to a fresh record, led by technology shares, as investors continued to rotate away from US assets amid a weaker dollar. The MSCI Asia Pacific ex-Japan Index rose as much as 1.3%, set for a third straight daily gain. TSMC, Commonwealth Bank of Australia and Samsung Electronics were among the major contributors. Benchmarks in South Korea, Hong Kong and Australia advanced, while those in mainland China slipped. Japanese markets were shut for a holiday. The strength in Asia’s technology shares and weakness in the greenback continue to drive investors into the developing world. The 30-day correlation between the dollar and MSCI Asia is minus 0.5, around the most severe level since April, Bloomberg-compiled data show. Bucking the trend, SK Hynix was among the major drags on the index following a report China’s CXMT plans to allocate a chunk of its DRAM capacity to produce superfast HBM3 chips that are used in AI. Samsung reversed earlier losses after a top executive said that the company is back at the top of the memory industry with its new HBM4 technology. Taiwan’s benchmark Taiex index jumped 1.6% to an all-time high on its last trading day before Lunar New Year holiday. Tech optimism rose after TSMC’s solid January sales data showed a sign of sustained global AI spending. The island’s stock market will resume trading from Feb. 23.

In FX, the yen has continued its climb against the dollar with USD/JPY briefly slipping below the 153 level. Accordingly the Bloomberg Dollar index is down 0.3%, also hampered by gains in NOK and AUD, with the latter bolstered by hawkish RBA remarks.

In rates, treasury yields are slightly lower on the day ahead of the rescheduled January employment report at 8:30am New York time. Overnight trading bands were narrow amid similarly muted price action European bonds, while S&P 500 futures hold small gain. US session also includes new-issue 10-year note auction for $42 billion, following good demand for 3-year notes Tuesday. US intermediate yields are richer by about 1bp with 10-year steady around 4.135% and curve spreads within 1bp of Tuesday’s close. German and UK peers are equally contained. For the 1pm auction, 10-year notes have when-issued yield near 4.142%, about 3bp richer than last month’s sale, a second and final reopening that stopped through by 0.7bp. IG dollar issuance slate empty so far. Eight names priced $11.3b Tuesday, led by Walt Disney Co. and pharmaceutical distributor Cencora’s multi—tranche trades. Issuers paid about 2bps in new issue concessions on deals that were 4.3 times covered

In commodities, metals prices are broadly firmer, with spot gold and silver up 1.4% and 6.2% respectively. Oil futures have continued to rise amid tensions in the Middle East. Bitcoin has extended this week’s declines, down 2.9%. Nickel has also been boosted by Indonesian output curbs. Gold hovered above $5,000 an ounce. Bitcoin slid under $67,000, with last week’s reprieve proving short-lived and highlighting investors’ lack of confidence in a sustained recovery.

Today’s calendar includes the nonfarm payrolls for January are due at 8.30 a.m., followed by Fed budget balance at 2 p.m. Fed’s Bowman (10:15am), Schmid (10:00am) and Hammack (4pm) are scheduled to speak at events.

Market Snapshot

S&P 500 mini little changed

Nasdaq 100 mini -0.2%

Russell 2000 mini little changed

Stoxx Europe 600 -0.2%

DAX -0.3%

CAC 40 -0.5%

10-year Treasury yield -1 basis point at 4.13%

VIX +0.5 points at 18.26

Bloomberg Dollar Index -0.3% at 1179.03

euro +0.2% at $1.1917

WTI crude +1.3% at $64.8/barrel

Top Overnight News

Top White House officials have started trying to downplay a highly anticipated jobs report set for release on Wednesday, insisting that the US economy remains strong even if the data may ultimately show a fresh slowdown in hiring. WSJ

Negotiations between US Democrats and the White House are ongoing, but right now, a deal on a stopgap funding measure seems unlikely: Punchbowl

Iran wants to make a deal with the US, Donald Trump told Fox. On the Fed, the president reiterated his call for lower rates, saying employment numbers are “really good.” BBG

House lawmakers are set to vote today on whether to reject some of Trump’s tariff policies, starting with a resolution opposing levies on Canada. BBG

The White House revised its fact sheet on the US-India trade agreement to adjust language around agricultural goods, adding to confusion about the deal already raised by farmer groups. BBG

Ukraine has begun planning presidential elections alongside a referendum on any peace deal with Russia, after the Trump administration pressed Kyiv to hold both votes by May 15 or risk losing proposed US security guarantees. FT

China’s consumer inflation eased at the start of 2026 after reaching a near three-year high in December, as food prices declined. China’s PPI for Jan came in at -1.4% (vs. the Street -1.5% and down from -1.9% in Dec) while the CPI was +0.2% (down from +0.8% in Dec and below the Street’s +0.4% forecast). WSJ

Euro-area wage growth is poised to pick up in the second half, ECB predictions showed, supporting officials’ view that interest rates can remain steady. BBG

The Reserve Bank of Australia sees the country’s inflation rate as too high and will take all necessary measures to bring it under control, a top central bank official said. WSJ

China’s latest call to curb Treasuries in its holdings is stoking fear that Trump’s unpredictable policies may encourage traditional lenders like Europe and Japan to follow in its footsteps. BBG

Trade/Tariffs

China is reportedly considering probing wine from France; could consider launching anti-dumping duty to French wine, and potentially take counter measures against the EU if it adopt duties.

China plans to extend import VAT breaks on cancer and rare disease drugs until the end of 2027.

White House revised Fact Sheet on US-India trade deal with reference to pulses dropped and it changed the wording around India’s proposed USD 500bln purchase from a firm “commitment” to an “intent”.

US House Speaker Johnson fails in an effort to block votes on measures to rescind Trump’s tariff policies, according to CNN’s Manu Raju.

US Treasury Secretary Bessent said US-China ties are stable but competitive, aiming for fair competition and de-risking, not decoupling, while he adds China must rebalance amid persistent USD 1tln trade imbalance.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher but with some of the gains in the region capped after the weak handover from the US and with the NFP report on the horizon, while participants also digested earnings and data in thinned conditions, with Japanese markets shut for a holiday. ASX 200 outperformed with the index led higher by the top-weighted financial sector after shares in Australia’s largest lender and company by market cap, CBA, rallied following a 5% increase in H1 profits. Hang Seng and Shanghai Comp were kept afloat following the PBoC’s liquidity operations and recent pledge to continue implementing an appropriately loose monetary policy in its quarterly implementation report. However, the upside was limited as participants also reflected on the mixed Chinese inflation data in which CPI printed softer-than-expected, while PPI was slightly better-than-feared but remained in deep deflationary territory.

Top Asian News

Goldman Sachs revised its 2026 China PPI forecast to -0.5% Y/Y.

ByteDance reportedly plans to produce 100k-300k units of AI chips this year, while it is developing the AI chip and is in talks with Samsung (005930 KS) to manufacture it, according to sources.

Tencent Cloud (0700 HK) partners with Tesla (TSLA) to upgrade its cockpit experience.

NetEase (9999 HK / NTES) Q4 (USD): EPS 1.58 (exp. 2.03), Revenue 3.90bln (exp. 4.10bln).

European Bourses (STOXX 600 -0.3%) opened mixed, but now display a mostly negative picture (ex-FTSE 100, buoyed by strength in oil/mining names). Sectors hold a negative bias. Energy and Basic Resources are towards the top of the pile, whilst Tech lags. Movers today include; Siemens Energy (+5%, strong Q1 results), Dassault Systemes (-17%, poor results and weak outlook), Lufthansa (-4%, pilots threaten to strike). Elsewhere, some modest pressure was seen in Pernod Ricard (+0.5%) following reports that China could consider an anti-dumping duty on French wine.

Top European News

EU’s von der Leyen said the EU needs one large, deep and liquid capital market, adding that its currently too fragmented. Completing their own single market also means completing their own energy union, which is crucial when it comes to bringing prices down even further.

FX

DXY is slightly lower this morning and trades towards the lower end of a 96.49-96.91 range. Focus for the day lies solely on the US NFP report in the afternoon. The delayed January jobs data is expected to show 70k nonfarm payrolls added in the month (vs a prev. 50k; with the range of forecasts between -10k to +108k); the unemployment rate is expected to remain steady at 4.4%. Recent labour metrics are painting a subdued picture for the labour market, and commentary via WH Economic Adviser Hassett also dampened expectations ahead of the report today. Following his remarks, Bloomberg’s NFP whisper number dropped to 37k (prev. 50k).

JPY remains at the top of the pile, continuing to extend on the recent strength seen following PM Takaichi’s landslide victory. As mentioned in the coverage since the election, there are numerous factors helping buoy the JPY; a) BoJ potentially to normalise faster, b) less friction for Japanese officials to conduct intervention, c) hefty flows to Japanese equities, d) FinMin Katayama suggesting that surplus foreign reserves could help to fund the food tax suspension. USD/JPY briefly dipped below the 153.00 mark, and currently holds within a 152.79-154.51 band. The pair is now approaching the touted rate check/intervention lows seen late Jan (152.09).

G10s are firmer against the USD to varying degrees. JPY outperforms (mentioned above), whilst the Aussie follows closely behind. AUD/USD has now breached above the 0.70 mark, to now trade at levels not seen since Feb’23. The pair currently trades around 0.7113, and further upside could see a test of the high from 2nd Feb 2023 at 0.7157. Recent strength comes amidst the continued strength in underlying metals prices, and after commentary from RBA’s Hauser. He noted that inflation is too high, which they can’t let persist and will do what is needed to bring inflation back to the target band.

Elsewhere, EUR is slightly firmer and trades around the 1.19 mark, and off recent highs which saw the single currency top 1.2000 in late January. A weak US jobs report could see another bid higher for EUR/USD, which may lead to ECB doves to push for an FX-led rate cut. No move was seen after the ECB Wage Tracker, where the 2026 annual estimate was increased to 2.388% (prev. 2.316%).

The NOK continues to strengthen against the EUR in the aftermath of Tuesday’s hotter-than-expected Norwegian inflation data; a report which led some banks to push back calls for Spring cuts. EUR/NOK is currently at session lows, in a 11.2638-11.3300 range.

Fixed Income

In brief, benchmarks are contained into today’s NFP report (delayed due to the brief shutdown), which includes benchmark revisions. US labour data during the window has been on the softer side of things, with claims steady, continuing easing, ADP weak and Revelio posting job losses. Furthermore, Challenger cuts were the highest for January since 2009, and JOLTS were at the lowest since September 2020.

USTs approach this, and then data and Fed speak afterwards, firmer by a tick or two in a thin 112-15 to 112-18 band; note, trade was quiet overnight with no cash trade due to Japan’s market holiday. For the Fed, markets currently fully price a cut in June (-25.2bps implied), with around a 20% chance of one occurring earlier in March and c. 40% in April.

EGBs in-fitting with the above, Bunds firmer but only marginally so in a 128.60-74 band. ECB speak this morning once again sticking to the script. Interestingly, the latest ECB wage tracker was hot across the board and factors in favour of those who think the next move will be a hike rather than a cut. Adding to the hawkish narrative from/affecting some global central banks in recent sessions, i.e. the RBA and Norges Bank.

Gilts are contained in a 90.71-90 band. UK specifics are much quieter thus far vs the last few sessions, with a busy docket of data scheduled for next week. Much of the UK press is focused on Angela Rayner after it was revealed that a “Rayner for leader” site briefly went live in January; a Bloomberg write-up on the subject characterises the discussion/view of insiders neatly as “Buy Rayner and Sell Streeting”.

Germany sells EUR 750mln vs exp. EUR 1bln 2.90% 2056 and EUR 1.16bln vs exp. EUR 1.5bln 2.50% 2054 Bund.

UK sells GBP 300mln 4.25% 2049 Gilt via Tender: b/c 4.32x, average yield 5.256%.

China’s Ministry of Finance issues CNY 14 bln of treasury bonds in Hong Kong.

Australia sold AUD 700mln 3.75% April 2037 bonds, b/c 4.14, avg. yield 4.8342%.

JPMorgan launches USD 1.5bln tender offer for EA bonds ahead of USD 20bln buyout financing; buyback includes USD 750mln each of 2031 and 2051 maturities, expiring March 11th.

Commodities

Crude benchmarks have steadily moved higher as the European session gets underway, with traders digesting a report by Axios quoting President Trump saying that he might send a second carrier to strike Iran if talks fail, pushing aside the larger-than-expected US private inventory build. WTI and Brent rebounded from a trough of USD 63.65/bbl and USD 68.49/bbl respectively in the later hours of Tuesday’s trading session, and oscillated in a tight c. USD 0.50/bbl range during the APAC session, with WTI nearing USD 65/bbl to the upside.

Spot gold remains contained in a USD 4965-5086/oz band that has been formed so far this week, ahead of a busy week of tier-1 US data.

Base metals have been steadily bidding higher with 3M LME Copper reaching USD 13.25k/t. The broad-based move seems to have been driven by nickel prices. Weda Bay, the world’s largest nickel mine, has been told by Indonesian authorities to cut its output by 70% in an effort to boost global prices. Indeed, LME nickel futures prices did lift higher following the report, rising from USD 17.75k/t to USD 17.95k/t, but have since pared back slightly.

Indian state-owned refiners are to consider buying more US and Venezuelan crude after the trade deal with the US, Bloomberg reported.

SHFE is adjusting the automatic conversion standard for hedging position limits in silver futures. “…starting from the last trading day of February 2026, the hedging transaction position limits for all silver contracts that have not obtained hedging transaction position limits for the near-delivery month will be temporarily adjusted to 0 lots for both buy and sell hedging transactions in the near-delivery month (the month preceding the delivery month and the delivery month itself).”.

Russia to complete building two ice-class LNG tankers in 2026, according to IFX.

World’s biggest nickel mine in Indonesia, Weda Bay, has been told to slash output by 70% to 12mln tonnes, Bloomberg reported.

Syria taps energy majors to explore for trillions of cubic meters of gas with the state oil chief noting that Chevron (CVX) , ConocoPhillips (COP) and TotalEnergies (TTE FP) and Eni (ENI IM) are interested in exploration, according to FT.

US Private Energy Inventory Data (bbls): Crude +13.4mln (exp. +0.8mln), Distillates -2.0mln (exp. -1.3mln), Gasoline +3.3mln (exp. -0.4mln), Cushing +1.4mln.

US issues Venezuela related license authorizing certain transactions necessary to ports and airport operations, also authorising certain activities involving Venezuelan-origin oil.

Wells Fargo raises its 2026 gold target to USD 6,100-6,300/oz citing geopolitical risks, market volatility, and strong central-bank demand.

Central Banks

ECB Wage Tracker: 2026 Annual 2.388% (prev. 2.316%).

ECB’s Makhlouf said uncertainty means the ECB should take a meeting-by-meeting approach.

RBA Deputy Governor Hauser said Australia’s economy is not just ‘dig it and ship it’, many parts of the economy are doing quite well, adds inflation is too high which they can’t let persist and will do what is needed to return it to the band.

Westpac anticipates RBNZ hiking rates more quickly in 2027.

Geopolitics: Ukraine

Russia’s Kremlin said that the US has prohibited Russia and China from dealing with Venezuelan oil and are looking to discuss with the US about the restriction.

Russia to complete building two ice-class LNG tankers in 2026, according to IFX.

Ukrainian President Zelensky plans spring elections alongside a referendum on the peace deal after US push, according to FT.

Geopolitics: Middle East

Iranian Supreme leader Khamenei’s advisor says that Iranian negotiators have no authority to discuss missiles.

Iran’s Foreign Minister Araqchi said the date for the next round of US negotiations have not been set.

Iranian Foreign Ministry said they are ready to negotiate on the percentage of uranium enrichment and the size of its enriched stockpile.

Iran’s President said that the country is not seeking nuclear weapons and are ready for any kind of verification.

US President Trump said Iran wants to make a deal and it would be foolish if they didn’t.

Geopolitics: Others

Australia charges two Chinese nationals with foreign interference.

Taiwan’s President Lai said Indo-Pacific nations are raising defense budgets and Taiwan must do the same, while he thanks US for its support of Taiwan’s defence.

UK expands settlement visa for Hong Kongers following Jimmy Lai’s sentence.

US Event Calendar

7:00 am: United States Feb 6 MBA Mortgage Applications, prior -8.9%

8:30 am: United States Jan Change in Nonfarm Payrolls, est. 65k, prior 50k

8:30 am: United States Jan Change in Manufact. Payrolls, est. -6.8k, prior -8k

8:30 am: United States Jan Unemployment Rate, est. 4.4%, prior 4.4%

2:00 pm: United States Jan Federal Budget Balance, est. -94.35b, prior -144.7b

10:00 am: United States Fed’s Schmid Speaks on Monetary Policy and Economic Outlook

10:15 am: United States Fed’s Bowman in Moderated Conversation

4:00 pm: United States Fed’s Hammack Speaks on Leadership at Ohio State University

DB’s Jim Reid concludes the overnight wrap

The last 24 hours have seen a modest risk-off move in markets, with the S&P 500 (-0.33%) and STOXX 600 (-0.07%) both falling back. In part, that was thanks to a weak batch of US data, which added a little bit more doubt on the near-term growth outlook, and pushed Treasury yields down across the curve. So in turn, that cemented expectations the Fed would keep cutting rates under a new Chair this year, and the 10yr Treasury yield (-5.9bps) fell back to 4.14%. But matters also weren’t helped by ongoing concerns in the tech space, whilst fresh geopolitical risks around Iran have seen Brent crude oil move up to a 1-week high this morning of $69.17/bbl. To be fair, US equity futures are back up again this morning, with those on the S&P 500 up +0.29%, but so far the index has been unable to get back up to its record high from a couple of weeks ago.

That weak US data was the biggest market driver yesterday, with a succession of prints that all leant on the softer side. Most notably, retail sales were unchanged in December (vs. +0.4% expected), which added to the sense the economy had stumbled into year-end, particularly after last week’s data where job openings were at their weakest since 2020. Meanwhile, the dovish narrative got even more fuel from the latest Employment Cost Index for Q4, which came in at just +0.7%. That’s a measure of labour costs that’s closely followed by the Fed, and it was the weakest it’s been since the current inflation surge got going in Q2 2021. Moreover, with the data coming in a bit weaker than expected, the Atlanta Fed’s GDPNow estimate for Q4 also came down, now showing an annualised growth rate of +3.7%.

Collectively, those releases helped to validate the dovish arguments pushing for more rate cuts this year. So investors priced in more Fed easing in 2026, and there was even a growing sense that Powell might deliver another cut before departing as Chair if the data continued in that direction. For instance, the probability of a cut by the April FOMC (Powell’s last as Chair) was up to 47% by the close. And looking further out, the amount of cuts priced in by December was up +3.3bps on the day to 60bps. In turn, that brought Treasury yields down across the curve, with the 2yr yield (-3.3bps) closing at 3.45%, whilst the 10yr yield (-5.9bps) fell to 4.14%.

That dovish repricing came as Trump continued to call for lower rates, saying in an interview with Fox Business that the US “should have the lowest interest rates in the world”, and that interest rates should be 2 points lower right now. However, commentary from Fed officials was more cautious, with Cleveland Fed President Hammack saying that “we could be on hold for quite some time”, whilst Dallas Fed President Logan said that it would take “further material cooling” in the labour market for more rate cuts to be appropriate.

Over on the geopolitical side, we also had some fresh headlines on Iran yesterday which put upward pressure on oil prices. First, President Trump told Axios in an interview that he was “thinking” about sending a second aircraft carrier strike group to the Middle East, and said that “Either we will make a deal or we will have to do something very tough like last time”. Separately, the WSJ reported that Trump administration officials had considered whether to seize tankers transporting Iranian oil, but have held off because of concerns about retaliation and the oil market impact. So oil prices moved higher after those headlines, and this morning Brent crude is currently around a 1-week high of $69.17/bbl.

Looking forward, US data will stay in the spotlight today, as we’ll get the January jobs report that was delayed from last Friday because of the partial government shutdown. In terms of what to expect, our US economists see nonfarm payrolls coming in at +75k, with the unemployment rate staying at 4.4%. Remember as well that today’s report will include the annual benchmark revisions to payrolls, which could rewrite some of the trends over recent history. We already got the preliminary number in September, which said that payrolls were -911k lower as of March 2025. However, that number can be different from the preliminary release, and last year’s preliminary benchmark revision was -818k but the final number was a smaller -589k, so not as negative as first thought. For more details, click here for our US econ team’s preview and their subsequent webinar.

Ahead of that, US equities fell back, with the S&P 500 (-0.33%) initially on course for a new record before reversing course later in the session. That came amidst a turnaround in software stocks, which were up over 2% in early trading, before paring that back to close just +0.09% higher. That tech drag was seen more broadly, with the Mag 7 (-0.60%) falling back as every member except Tesla lost ground, whilst the small-cap Russell 2000 (-0.34%) performed in-line with large caps as investors grew more cautious ahead of today’s jobs report.

Earlier in Europe, markets had also put in a steady performance, with sovereign bonds rallying after the US data. So that meant yields on 10yr bunds (-3.2bps), OATs (-3.7bps) and BTPs (-3.8bps) all moved lower. And similarly, 10yr gilt yields (-2.1bps) were also subdued as the political uncertainty over Prime Minister Starmer’s position eased back again. Meanwhile for equities, it was a quiet day as well, with the STOXX 600 (-0.07%) modestly declining from its record high the previous day.

Staying on Europe, tomorrow will also see EU leaders gather for a meeting on how to strengthen the single market and reduce their economic dependencies. They’ll also be joined by former ECB President Mario Draghi, who wrote a report on boosting EU competitiveness back in 2024. Our European economists have a preview of that summit (link here), where they also look at the progress so far in implementing Draghi’s recommendations.

Overnight in Asia, most equity markets have put in a decent performance, with gains for the KOSPI (+0.9%), the Hang Seng (+0.41%) and the Shanghai Comp (+0.20%), although the CSI 300 (-0.08%) is down slightly. Meanwhile in Japan, markets are closed for a public holiday, but futures on the Nikkei (+0.68%) are also pointing higher this morning, with those on the S&P 500 (+0.24%) rising as well. Otherwise, we also have the latest Chinese inflation data overnight, which showed that CPI decelerated by more than expected to +0.2% in January (vs. +0.4% expected). By contrast however, the PPI reading rose by more than expected, with a deflation rate of -1.4% (vs. -1.5% expected). So that’s actually the highest PPI reading in 18 months, even though it’s still in deflationary territory.

Looking at the day ahead, data releases include the US jobs report for January, and Italy’s industrial production for December. Central bank speakers include the Fed’s Schmid, Bowman and Hammack, along with the ECB’s Cipollone and Schnabel.

Tyler Durden

Wed, 02/11/2026 – 08:29

https://www.zerohedge.com/markets/futures-rise-ahead-todays-delayed-jobs-report

Incertidumbre en San Francisco mientras huelga de maestros deja a 50.000 alumnos sin clases

Por OLGA R. RODRIGUEZ

SAN FRANCISCO (AP) — Connor Haught ha estado equilibrando reuniones de trabajo virtuales y proyectos de manualidades para sus dos hijas mientras su familia intenta navegar por una huelga de maestros en San Francisco sin una fecha de finalización a la vista.

El trabajo de Haught en la industria de la construcción le permite trabajar desde casa, pero, como muchos padres en la ciudad, él y su esposa estaban luchando por planificar actividades para sus hijos en medio de la incertidumbre de una huelga que ha dejado a casi 50.000 estudiantes fuera del aula.

“La gran preocupación para los padres es realmente el cronograma de todo esto y tratar de prepararse para cuánto tiempo podría durar”, expresó Haught.

Las 120 escuelas del Distrito Escolar Unificado de San Francisco estaban programadas para permanecer cerradas por tercer día el miércoles, después de que unos 6.000 maestros de escuelas públicas se declararan en huelga por salarios más altos, beneficios de salud y más recursos para estudiantes con necesidades especiales.

Algunos padres están aprovechando los programas extracurriculares que ofrecen programación de día completo durante la huelga, mientras que otros dependen de familiares y entre ellos para obtener ayuda con el cuidado de los niños.

Haught dijo que él y su esposa, quien trabaja por las noches en un restaurante, planearon tener a sus hijas de 8 y 9 años en casa la primera semana de la huelga. Esperan organizar citas de juego y excursiones locales con otras familias. Aún no han decidido qué harán si la huelga se extiende a una segunda semana.

“No intentamos inscribirnos en todos los campamentos y cosas de inmediato porque pueden ser costosos, y puede que seamos un poco más afortunados con nuestro horario que algunas de las otras personas que están siendo afectadas”, comentó Haught.

Los Educadores Unidos de San Francisco y el distrito han estado negociando durante casi un año, con los maestros exigiendo atención médica familiar completamente financiada, aumentos salariales y la cobertura de vacantes que afectan la educación especial y los servicios.

Los maestros en huelga dijeron que saben que la medida es difícil para los estudiantes, pero que lo hacen para ofrecerles estabilidad a largo plazo.

“Esto es para el mejoramiento de nuestros estudiantes. Creemos que nuestros estudiantes merecen aprender de manera segura en las escuelas y eso significa tener escuelas completamente dotadas de personal. Eso significa retener a los maestros ofreciéndoles paquetes salariales competitivos y atención médica y significa financiar completamente todos los programas que sabemos que los estudiantes necesitan más”, afirmó Lily Perales, profesora de historia en Mission High School.

La superintendente Maria Su declaró el martes que hubo algunos avances en las negociaciones del lunes, incluyendo apoyo para familias sin hogar, capacitación en IA para maestros y el establecimiento de mejores prácticas para el uso de herramientas de IA.

Pero las dos partes aún no han llegado a un acuerdo sobre un aumento salarial y beneficios de salud familiar. El sindicato inicialmente pidió un aumento del 9% en dos años, lo que dijeron podría ayudar a compensar el costo de vida en San Francisco, una de las ciudades más caras del país. El distrito, que enfrenta un déficit de 100 millones de dólares y está bajo supervisión estatal debido a una crisis financiera, rechazó la idea. Los funcionarios propusieron con un aumento salarial del 6% pagado en tres años.

El martes, Sonia Sanabria llevó a su hija de 5 años y a su sobrino de 11 a una iglesia en el vecindario de Mission District que ofrecía almuerzo gratis a los niños fuera de la escuela.

Sanabria, quien trabaja como cocinera en un restaurante, indicó que no fue a trabajar para cuidar a los niños.

“Si la huelga continúa, tendré que pedir a mi trabajo una licencia, pero me afectará porque si no trabajo, no gano”, manifestó Sanabria.

Dijo que su madre anciana ayuda con la llevada y recogida de la escuela, pero dejar a los niños con ella todo el día no es una opción. Relató que les ha dado tareas de lectura y escritura y ha trabajado con ellos en problemas de matemáticas, y que está haciendo planes para los niños día a día. Expresó su apoyo a los maestros en huelga.

“Están pidiendo mejores salarios y mejor seguro de salud, y creo que lo merecen porque enseñan a nuestros hijos, los cuidan y los están ayudando a tener un mejor futuro”, apuntó, agregando, “Solo espero que lleguen a un acuerdo pronto”.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

Egipto reorganiza su gabinete en medio de crisis económica y conflictos regionales

EL CAIRO (AP) — Egipto nombró y tomó juramento a un nuevo ministro de Defensa el miércoles, junto con otros 13 nuevos ministros, en la más reciente reorganización del gabinete mientras el país enfrenta una débil economía y una creciente presión ejercida por los conflictos regionales.

El presidente Abdel-Fattah el-Sissi supervisó la ceremonia de juramentación en el Palacio Presidencial, donde el recién nombrado ministro de Defensa, Ashraf Salem, prestó juramento, junto con los otros ministros aprobados el martes por el Parlamento. La reorganización ha afectado áreas como vivienda, educación superior, comunicaciones, juventud y deportes. La reorganización anterior del gabinete se realizó en julio de 2024.

Ahmed Rostom, economista de alto nivel del Banco Mundial, fue nombrado ministro de Planificación, mientras que Mohamed Farid Saleh, presidente de la Autoridad Reguladora Financiera, ahora encabeza el Ministerio de Inversión.

El ministerio de Información fue restaurado después de haber sido disuelto en 2021, y Diaa Rashwan, presidente de la agencia gubernamental conocida como Servicio de Información del Estado, fue nombrado ministro de Estado de Información.

Todos los nuevos nombramientos fueron propuestos por el-Sissi, quien se reunió el martes con el primer ministro Mustafa Madbouly antes de la sesión de votación del Parlamento sobre la reorganización.

Egipto ha sido golpeado fuertemente por años de medidas de austeridad tras un programa del Fondo Monetario Internacional adoptado en 2016, la pandemia de coronavirus, las repercusiones de la invasión a gran escala de Ucrania por parte de Rusia y, más recientemente, la guerra entre Israel y Hamás en Gaza.

Los ataques de los rebeldes hutíes de Yemen, respaldados por Irán, contra las rutas de navegación en el mar Rojo también han reducido los ingresos que Egipto recibe por el Canal de Suez, una fuente importante de divisas, debido a que los ataques obligaron a desviar el tráfico del canal hacia el extremo de África.

La tasa de inflación anual fue del 10,1% en enero, en comparación con el 10,3% del mes anterior, según un informe presentado el martes por la agencia de estadísticas del país.

En 2025, el gobierno aumentó el salario mínimo mensual para los trabajadores del sector público y privado a 7.000 libras (138 dólares), frente a las 6.000 libras (118,58 dólares) anteriores.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

Fiscalía de Ecuador pide prisión preventiva para alcalde de Guayaquil en caso de lavado de activos

Associated Press

QUITO (AP) — La Fiscalía ecuatoriana pidió el miércoles la prisión preventiva para el alcalde de la ciudad portuaria de Guayaquil, detenido junto a otras 10 personas por presunta delincuencia organizada, lavado de activos y defraudación al Estado.

En su cuenta de X la institución indicó que con base a 20 pruebas “solicitó –de forma motivada– la prisión preventiva de 10 de los procesados” y para uno más la prisión domiciliaria atendiendo al hecho de que es una persona de la tercera edad.

Añadió que el pedido de prisión preventiva se justifica en la necesidad de neutralizar riesgos procesales, pues se investiga un “entramado societario complejo que ha corrompido a funcionarios y evadido el control de instituciones estatales” en torno a la comercialización de combustible.

Horas antes de su apresamiento, el alcalde Aquiles Álvarez había solicitado 15 días de permiso laboral al municipio de Guayaquil.

En caso de que el juez de la causa acepte el pedido de la Fiscalía, Álvarez no podrá ejercer sus funciones y si su ausencia se prolonga por más de 30 días perderá su cargo y tendrá que ser reemplazado por la vicealcaldesa Tatiana Coronel.

Durante los allanamientos de la víspera se levantaron indicios relacionados con el caso como teléfonos celulares, computadoras, dinero en efectivo y documentos, entre otros. En la publicación de la Fiscalía se difundieron fotografías de muchos fajos de billetes.

Entre los acusados están dos hermanos del burgomaestre, Xavier y Antonio Álvarez, quienes fueron detenidos durante un operativo realizado la madrugada del martes por el Ministerio Público y la policía en Guayaquil, 270 kilómetros al suroeste de la capital.

Antonio y Xavier Álvarez son empresarios. El primero es además presidente del popular equipo ecuatoriano de fútbol Barcelona y el segundo es integrante de la comisión directiva.

AP solicitó pidió un comentario a la alcaldía de Guayaquil, pero no hubo una respuesta.

Álvarez llegó a la alcaldía guayaquileña de la mano del partido Revolución Ciudadana del expresidente Rafael Correa (2007-2017), quien se encuentra prófugo de la justicia y tiene pendiente varias sentencias por corrupción. El exmandatario ha dicho que se trata de una persecución política de sus adversarios.

El burgomaestre, junto a otras 15 personas, enfrenta desde mediados de 2024 un proceso judicial por la presunta comercialización ilegal de combustible, lo que Álvarez ha negado.

Guayaquil es una de las ciudades más pobladas de Ecuador y epicentro del comercio y la industria.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}