Category: News

The Return Of History: Deutsche On Gold, The Dollar, & The Monetary Future

The Return Of History: Deutsche On Gold, The Dollar, & The Monetary Future

Authored by Mallika Sachdeva and Michael Hsueh via Deutsche Bank Research Institute,

In 1989, Francis Fukuyama argued that humanity had reached “the end of history”. In the years that followed, the US became the uncontested hegemon, global trade exploded in a US-defined liberal order, developed market central banks sold gold, while emerging markets accumulated vast amounts of US dollar FX reserves. We argue that the end of history has come to an end. The world is back in a superpower struggle; the US is retreating from free trade, alliances, and security provision; the Great Economic Moderation is behind us; and the dollar banking system has been weaponized. The “return of history” has big implications for gold and the dollar.

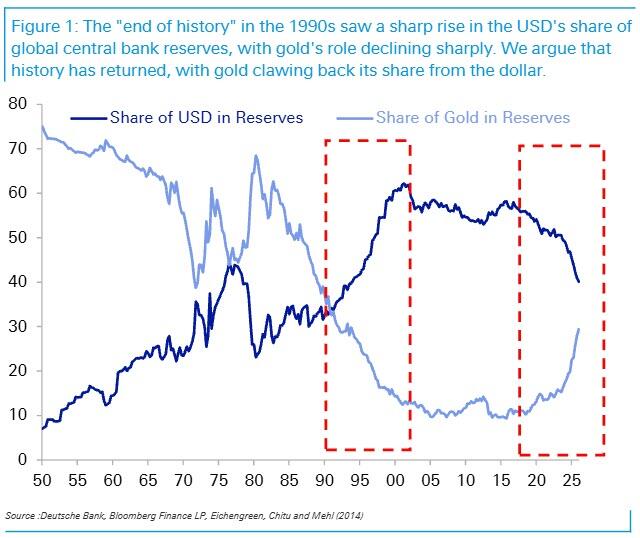

Contrary to conventional thinking, we argue that the share of gold in central bank reserves is not driven by the global monetary system, but by the global geopolitical environment. Gold’s decline as a share of reserves did not happen with the fall of Bretton Woods in the 1970s, but the fall of the Berlin Wall and the assertion of US hegemony in the 1990s. As tectonic geopolitical plates shift again, the share of US dollars in central bank reserves is once more in decline. It has fallen from over 60% to just 40%, while gold’s share has tripled from its lows to 30% today.

We create a framework for the share of gold in central bank reserves as a function of: (1) the volume of gold held by central banks; (2) the price of gold; and (3) the amount of global FX reserves. We see all three pillars on the move, driven by EM. EM central banks have been actively buying gold and driving upward pressure on prices; crucially – their FX reserves may also now begin to structurally decline.

A “return of history” would be consistent with gold getting to at least a 40% share of global reserves. There is significant scope for EM to add towards this. We find that EM countries with closer non-Western defence ties hold more gold. If the world diversifies trade and security dependence away from the US, this would be consistent with less USD and more gold in reserves.

We simulate a range of different outcomes for gold prices depending on the level of FX reserves EM central banks end up with, and the share of gold they target. Even in an environment where EM FX reserves decline to USD5tn, gold prices could still rise to $8000 over the next five years, if EM countries all target a 40% gold share.

For now, EM central bank gold buying likely has to do with preserving the value and accessibility of foreign savings in a changing geopolitical climate. But in the long-run, we consider how gold may one day play a role in anchoring a monetary order that builds independence from the dollar.

All that glitters

The reserves baton is passing back to gold from the dollar

The share of the USD in global central bank reserves has dropped sharply from around 60% at its peak to just 40% today, with attrition accelerating in the past few years. As Figure 1 illustrates, the USD’s share of reserves peaked at the start of this century and sustained those levels for the next two decades before recent losses Importantly, the dollar’s losses as a share of central bank reserves have not gone to other fiat currencies, but to gold.

Gold’s share in global central bank reserves has doubled in the past four years to nearly 30% today. The fact that the gap between the dollar and gold as a share of reserves is now just 10% is extremely notable. As Figure 1 shows, there appears to be a marked reversal underway of the 1990s trend when central banks moved away from gold and towards the USD in their reserves. Before the 1990s, gold had consistently been a larger share of central bank reserves than the fiat dollar. But by the end of the 1990s, the dollar was over four times the share of gold. This seems to now be going in reverse with gold clawing back its share rapidly. What happened in the 1990s and why is this unwinding today? How far can it go and to what end? These are the questions which motivate this paper.

The 1990s began with a declaration by historian Francis Fukuyama that humanity had reached “The End of History.” We argue in this paper that history has returned, but the contest and its leaders will be different. This is the lens through which we think about the resurgence of gold, the decline of the dollar, and the international monetary architecture that may await us this century.

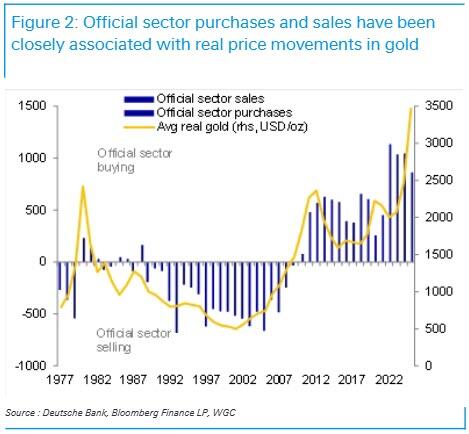

Let’s address the skepticism. Skeptics may say the rising share of gold in central bank reserves is simply reflective of gold price increases. Indeed, around 80% of the rise in gold’s share has been on account of prices. But there is a genuine volume driver underlying this: central bank purchases have arguably themselves been behind significant price momentum. There is indeed a close relationship between official purchases and sales of gold and the change in the real gold price (Figure 2). Volume and prices are thus endogenously related and are both doing the legwork of gold’s rising share.

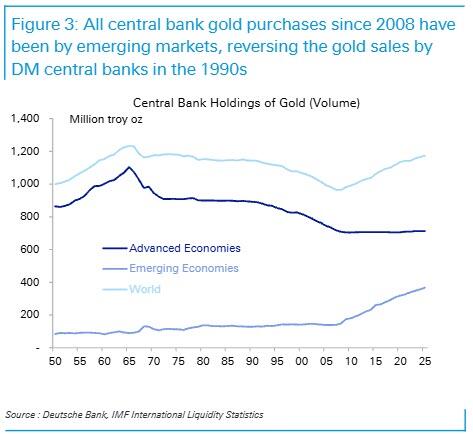

Crucially, all central bank purchases are occurring in emerging markets. As Figure 3 illustrates, it is EM central banks that have been steadily purchasing gold since the 2008 GFC, adding over 225mn troy oz over the past 17 years. Importantly, this is more than advanced economy central banks sold in the 1990s. As we discuss in depth in this paper, we think there could be a long way to go in the trend of EM central bank buying of gold.

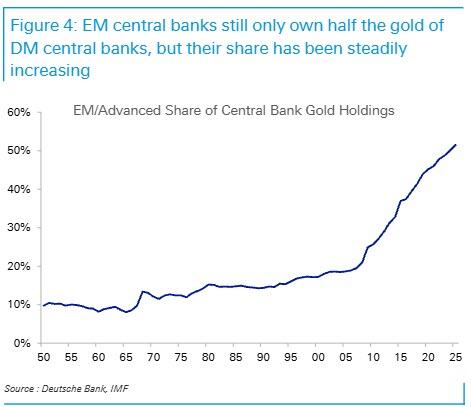

EM central banks still only hold half the amount of physical gold of developed markets. In stock terms, EM central banks held 367mn troy oz at the end of 2025 compared to 712mn troy oz by Advanced Economy central banks, according to IMF classification. This has however been on a steadily rising trend. The ratio of EM/DM central bank gold holding is at around 52%, having risen from just 20% before the 2008 GFC (Figure 4).

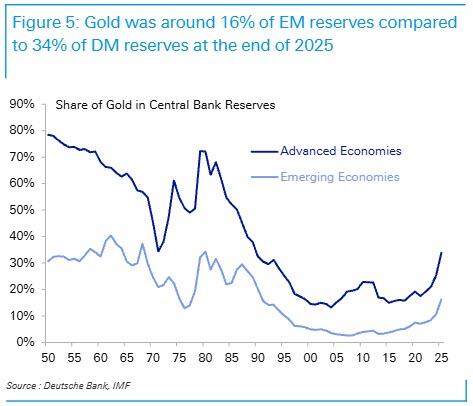

As a share of total reserves (including foreign exchange holdings), which is where our focus in this paper lies, EM central banks had just 16% of total reserves in gold compared to 34% for DM central banks by end-2025. There thus remains a significant gap to close, if not ultimately exceed.

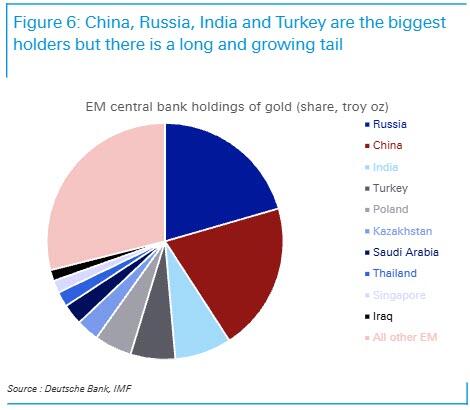

This is not just about the BRICS. Almost half of EM central bank holdings are accounted for by just China, Russia and India. But many middle powers like Turkiye, Kazakhstan, and Saudi Arabia are also significant holders (Figure 6).

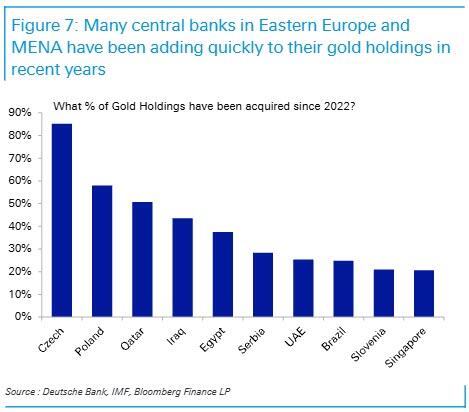

Perhaps most notable in recent years is the momentum of purchases in certain regions. Strikingly, in Eastern Europe, more than half of the gold holdings of Czechia and Poland have been acquired in the past four years alone, after Russia’s invasion of Ukraine (Figure 7).

Many MENA states like Qatar, Egypt and the UAE have acquired between 25- 50% of their total gold holdings in the last few years alone. We will be exploring the motivations for these purchases in more detail later in the paper.

A brief history of gold

Gold was the heart of Bretton Woods but did not fall with it

The US had over 70% of the world’s central bank gold reserves after World War 2, and in constructing the Bretton Woods monetary architecture, it used gold to back a system that centered on the dollar.

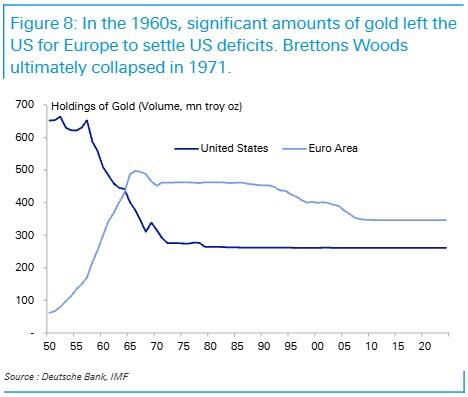

As Monnet and Puy (2019) explain, the Bretton Woods system – which followed WW2 and lasted till 1971 – was not like the gold standard that preceded World War 1, or that was tried unsuccessfully in the interwar period. Under Bretton Woods, gold was not redeemable against bank notes at a fixed rate everywhere in the world. Nor were central banks strictly required to back currency in circulation with gold reserves. Only the US dollar was convertible into gold at $35/oz by other central banks via the Fed. Gold was essentially only a means of settlement between monetary authorities. Foreign countries could choose to hold their claims on the US in US dollars, or exchange them for gold. As the US began to run balance of payments deficits in the 1950s and 60s, some European countries began to make claims on the Fed’s gold. By the mid-1960s, more gold was held at European central banks than in the US (Figure 8). By 1971, the system collapsed with Nixon ending the US dollar’s convertibility to gold.

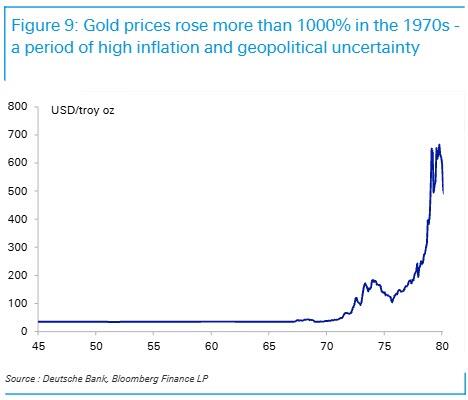

Gold did not however drop as a share of central bank reserves with the fall of Bretton Woods. Even as gold stopped serving a purpose as an official means of international settlement, gold averaged around a 50% share of central bank reserves through the 1970s, albeit with significant gyrations. Notably, it remained more important than the fiat dollar throughout the decade as the earlier Figure 1 depicts. Indeed, the 1970s were a period of enormous price gains for gold which rose more than 1000% in nominal terms through the decade driven by high inflation and geopolitical shocks from the 1973 Arab oil embargo, to the Iranian revolution (Figure 9).

Therefore, even as the global exchange rate system changed in the 1970s, gold’s share in global reserves did not. This points to deeper and different drivers of gold’s role. If central bank gold holdings in reserves were not ultimately only about convertibility of the USD, what were they about? And what brought about the change? We turn to this next.

The end of history

The ultimate decline in gold’s share in global central bank reserves came in the 1990s. As Figure 1 earlier showed, gold fell below the dollar’s share at the start of the 1990s, with the rest of the decade featuring a consistent rise in the dollar and decline of gold. What was behind this crossover?

It was not a transition in the monetary system – which had occurred two decades prior – but a shift in the geopolitical environment that changed the role of gold.

In 1989, Francis Fukuyama questioned whether humanity had reached “the end of history?”. A lot of the 20th century had featured ideological violence, but the ending of the Cold War he believed brought a “triumph of the West, of the Western idea,” “the endpoint of mankind’s ideological evolution” and the “unabashed victory of economic and political liberalism.” The Berlin Wall fell the year of his thesis, and the Soviet Union had fully dissolved by 1991. The US thus became an uncontested hegemon in what appeared to be a geopolitically unipolar world. Japan, which had been the US’ closest economic competitor, was well within the US security and dollar system, and China was still a decade from joining the WTO.

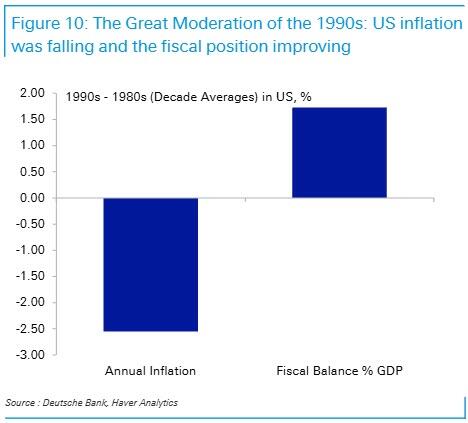

In the economic realm, a lot was changing in the 1990s from the turbulent decades that preceded it. In the US, a “Great Moderation” was underway. Inflation was falling with tight monetary policy having tamed the price instability of the 1970s and 80s. Indeed, average inflation in the 1990s was 2.5% below 1980 averages. The US was running growing fiscal surpluses. The US fiscal position was 1.5% GDP better in the 1990s than in the 1980s on average (Figure 10). The combination of better inflation and fiscal data, and independent central banking raised trust in monetary and fiscal systems, making US Treasuries a more attractive safe asset. Unlike gold, Treasuries paid a positive yield, had a deep and liquid market which made them easy to hold and transact in, and had no storage costs.

Developed world central banks led by Europe thus began to sell gold reserves in the 1990s (see again Figure 2), which came to be seen as a “barbarous relic” (Arslanalp et al, 2023). Countries like Switzerland, UK, Belgium, Netherlands, Austria, Australia, Canada all sold gold. Gold was seen as a vestige of the past, a zero-yielding asset with little role to play, especially in a world where European countries were moving towards a common currency. As gold sales began to impact the price of gold, central banks formalized a Central Bank Gold Agreement to coordinate sales in 1999, a framework that lasted for the next two decades.

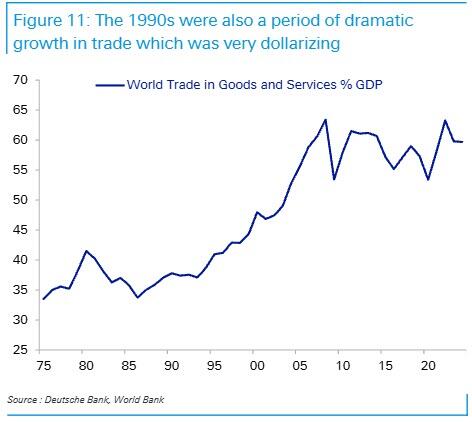

Stabilizing geopolitics, combined with large improvements in technology, communications and transport, led to an explosion in trade and globalization in the 1990s. Trade in goods and services close to doubled as a share of global GDP from 1990 to the 2008 GFC (Figure 11). A rise in global trade contributed to the deepening in dollarization via the channels of invoicing, finance, and the accumulation of dollar surpluses in exporting EM economies. This brings us to arguably the biggest driver of gold’s relative decline against the dollar.

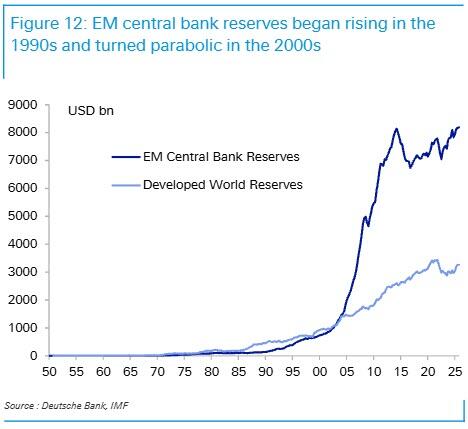

The biggest driver of the decline of gold’s share in global central bank reserves in the 1990s was the meteoric rise of emerging market FX reserves, held in dollars. As Figure 12 illustrates, global reserves began to rise in the 1990s. Japan was the biggest driver in the 1990s, with the baton passing to China in the 2000s alongside a wide swathe of EM countries from Russia, to Saudi Arabia, India, Korea, Taiwan, Brazil and others. The total amount of global FX reserves went up 9 times between 1990-2007. A majority of these reserves were built in USD and saved in US Treasuries given the predominance of the US driven economic and trade order. The Asian Financial Crisis in the late 1990 also led to a deeper preference for self insurance by EM countries and a dramatic shift in favour of building reserves, after the failures of capital account liberalization policies. The IMF itself shifted to encouraging reserves adequacy frameworks that stressed savings in USD liquidity.

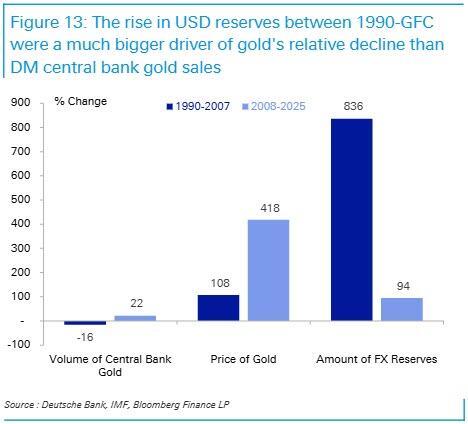

Bringing it all together: one can think of the share of gold in central bank reserves as a function of three things: (1) the volume of gold held by central banks; (2) the price of gold; and (3) the amount of foreign exchange reserves. The former two influence the numerator, while the latter influences the denominator. The decline of gold as a share of global central bank reserves from around 40% on the eve of the 1990s to just 10% by the eve of the GFC was predominantly about the denominator. While developed world central banks were selling gold in the 1990s, this was in fact largely offset by the price increase of gold (Figure 13).

In sum, the biggest driver of gold’s decline in global reserves in the 1990s was the rise of EM FX reserves accumulated in USD. This was in turn a function of dramatic globalization, in a US-driven neo-liberal unipolar order, amidst sound and improving economic fundamentals in the US. By extension, the dollar’s fate as the world’s reserve currency will have a lot to do with how these same countries treat their USD holdings in a de-globalizing world in which the US driven order is fraying: do EM countries still add to USD reserves, diversify away from them into gold, or actively draw them down? The future of the dollar as a reserve currency could well be determined in emerging markets, consistent with our thesis that the Global South will be a much bigger economic and geopolitical force to understand.

The return of history

The drivers of the “end of history” have almost all been going in reverse. The world is back in an ideological struggle between competing economic and political models, this time led by the US and China. Both countries are engaged in growing competition across technology, energy, resources, and influence.The world is no longer unipolar. China is on many metrics a bigger industrial, trade and naval power than the US.

The US is stepping back from free trade and fracturing traditional alliances, with China having positioned itself to step into the fray with years of building trade and investment relationships across the Global South. The provision of global public goods guaranteed by the US – namely freedom of navigation and security for key allied regions – has come into question with the closure of the Straits of Hormuz and the vulnerability of the Gulf in the latest conflict.

If the 1990s was a world where the US was happy to outsource manufacturing and labour to EM, with many EM countries happy to outsource security and savings to the US, this is now reversing. The US is keen to onshore more critical manufacturing, while many EM regions like Asia and the Gulf will be reconsidering their need for strategic autonomy in areas like energy and defence. They may well need the savings they have been investing in the USD to build these capabilities.

On the economic front, the Great Moderation is behind us. US inflation has been above target for over five years, independent central banking has come into question, monetary balance sheets have expanded dramatically under QE, and the US fiscal trajectory is on a worrying path.

Finally, the weaponization of the US dominated banking system with the freezing of Russia’s USD and EUR FX reserves in 2022 has increased the appeal of saving in gold, which can be held physically and locally, away from the arm of sanctions or asset seizures. Indeed, Russia and China hold 100% of their gold locally.

The end of history has itself come to an end, with significant implications for gold and the dollar, which are becoming increasingly apparent.

What the future may hold

EM is not only buying gold, but could soon be selling the dollar too

As discussed earlier, gold’s share in central bank reserves is a function of three main drivers: the volume of gold held, the price of gold, and the stock of FX reserves. For emerging market central banks, all three are on the move.

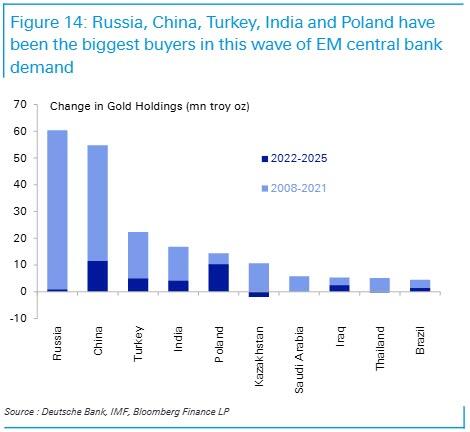

First, EM central banks have been actively buying gold. EM purchases since 2008 exceed the sales made by developed world central bank sales in the 1990s. Figure 14 illustrates the biggest buyers in volume terms since 2008, split between purchases before and after Russia’s invasion of Ukraine (2008-2021 and 2022-25). It is notable that Russia had actively diversified into gold ahead of 2022 (Figure 14).

China has continued to purchase gold at roughly the same pace since 2022, while countries in Eastern Europe, India, and MENA have accelerated gold purchases since then.

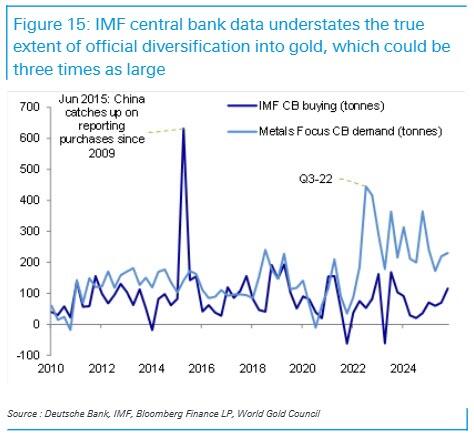

It is important to note that our analysis in this paper focuses on IMF data on central bank reserves, which understates the true accumulation of EM official savings in foreign assets. We have chosen to focus on IMF data for a range of reasons: longer time-series history of the data, comparability to COFER estimates of central bank FX holdings, and availability of country level data series. But there are important caveats to this data. While IMF data shows EM central bank reserves have been stagnant in recent years, EM countries have in fact continued to build and recycle savings abroad via large sovereign wealth funds, state banks, and public pension funds. A significant amount of these savings are held in USD, but often with a riskier, less liquid profile across equities and private markets rather than necessarily US Treasuries. Global SWF pegged sovereign wealth fund holdings in Asia and MENA at over USD12tn in March 2026, greater than the size of their central bank holdings.

If IMF data on central bank reserves is understating the true extent of official foreign savings in EM, it is also understating the full extent of official diversification into gold. Indeed, a series by the World Gold Council (WGC) that tracks quarterly demand by “Central Banks and Other Institutions” and is believed to include sovereign wealth funds and other state-directed flows, shows gold purchases at three times the pace of the IMF series since 2022 (Figure 15). IMF data shows roughly 10 mn troy oz of annual purchases in the past four years by central banks, while the WGC series pegs this at over 30mn troy oz or over 1000 tonnes per year. While this does not change the trend or conclusions of this paper, it does suggest scope to magnify already significant implications.

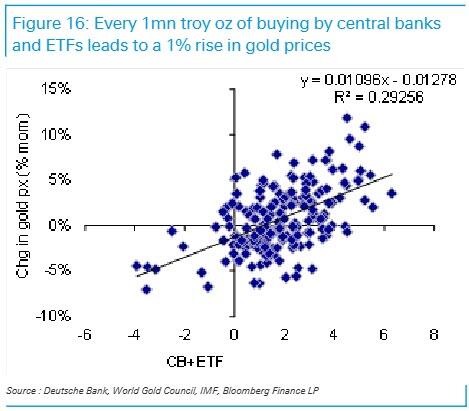

Second, central bank purchases are driving upward pressure on gold prices. Central banks and official institutions as defined by the WGC have accounted for over 40% of the investment demand for gold since 2022, excluding demand for jewelry, technology and industrial purposes. ETF purchases which picked up meaningfully last year may themselves be piggy-backing off the consistent underlying bid from central banks. A simple regression that looks at central bank and ETF demand suggests that every 1 mn troy oz of purchases leads to a 1% increase in the gold price (Figure 16). We adopt this as a simple back-of-the-envelope heuristic, to be used in analysis below.

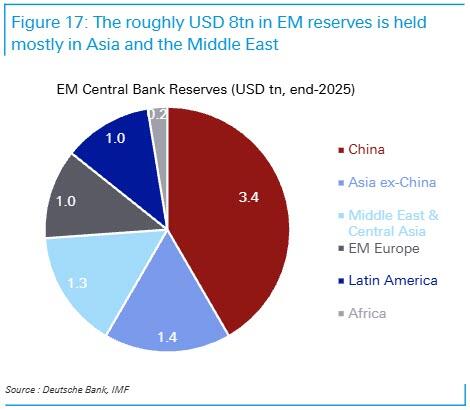

Third, the enormous build of foreign exchange reserves in emerging markets may now go into reverse. As discussed above, the dramatic rise of the dollar’s share in global central bank reserves in the 1990s had almost everything to do with the sharp rise in EM reserves. There is a possibility that EM reserves may begin to decline from here. This would be motivated less by foreign investor capital exits or the need to defend currencies, but as countries in Asia and the Gulf draw on their savings to build strategic autonomy in defence and energy, which will require capital, imports and investment. While a majority of the roughly USD8tn in EM central bank reserves are held in China, a significant share are also in Asia ex-China and Middle East & Central Asia (Figure 17). Recent reports that the UAE has asked the US Treasury for a currency swap, suggests the need for USD liquidity. Indeed, the Gulf may turn to their savings not just to tide over the effects of the ongoing war, but for rebuilding efforts, to address economic scarring and diversification needs, and ultimately to build greater domestic defence resilience.

The first two forces are already underway. EM central banks have been actively buying gold and prices have been rising. The third force of active reduction in US holdings is yet to begin, but could be very significant. All three drivers could be at play together, suggesting there is more to go in gold’s rise and the dollar’s decline as a share of global reserves. Where might they end up?

What share of reserves should gold be?

The combination of gold purchases and price rises has already pushed gold’s share of global central bank reserves to around 30%. Where might we go from here?

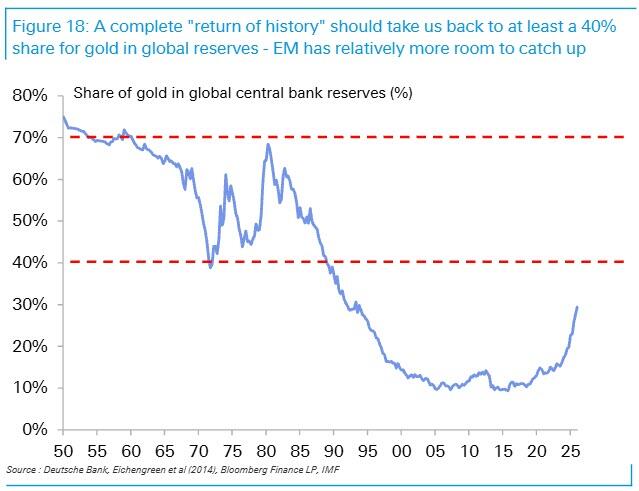

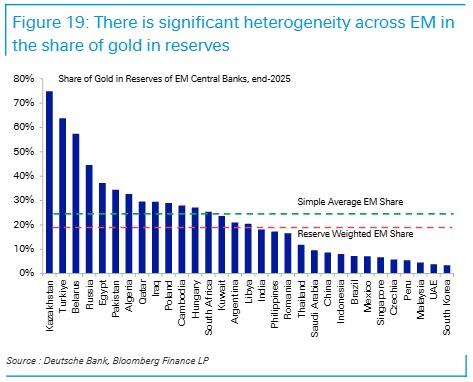

There is likely still a long way to go. We begin with the key observation that before the 1990s, gold’s share of reserves fluctuated between 40-70% of total reserves as illustrated in Figure 18. “The return of history” we described above should make getting to the lower bound of this range – or 40% for gold’s share – a reasonable initial target. If the world is going back to looking like it did before the 1990s – with geopolitical competition between superpowers, high inflation, and less universal support for free trade – then it may make sense to expect gold’s share of reserves to also go back to similar levels. While before the 1990s, emerging market central banks held very little total reserves, today they are the dominant holders of reserves. And whilst the share of gold in advanced economies reached 34% at the end of 2025, or fairly close to the 40% level, it was only 16% in emerging markets. If the dominant trends of central bank purchases and USD reserve sales are taking place in emerging markets, then there could still be a long way to go: from 16% to 40%.

There is a lot of heterogeneity across EM in gold’s share in reserves. While EM central banks as a whole held 16% of reserves in gold (end-2025), this masks large variation. The average has a downward bias driven by the largest reserves holder – China: PBOC holds only 9% of reserves in gold. Clearly, the scope for increase driven by China is huge. Kazakhstan and Turkiye had over 60% of their reserves in gold, Russia and Egypt near 40%, Poland and Hungary had reached nearly 30%, while traditional US allies like South Korea and UAE had under 5% in gold.

Academic literature explains this heterogeneity through both an economic and geopolitical lens. Arslanalp, Eichengreen and Simpson-Bell (2025) argue that “central banks operating floating exchange rates hold more gold, consistent with the presumption that they have less need to use their reserves in foreign exchange market intervention.” Indeed, gold holdings are less effective in helping central banks defend currencies against large scale capital flows. Thus, an increasing share of gold may reflect less concern amongst EM central banks about sudden stops or withdrawals of capital, especially with foreign ownership at lower levels than in the past. More interestingly, they find that “geopolitical alignment with the United States, proxied by the existence of a defence pact, increases dollar reserves. An interpretation is that governments grateful for US military presence encourage their central banks to hold dollars as a show of good faith.”

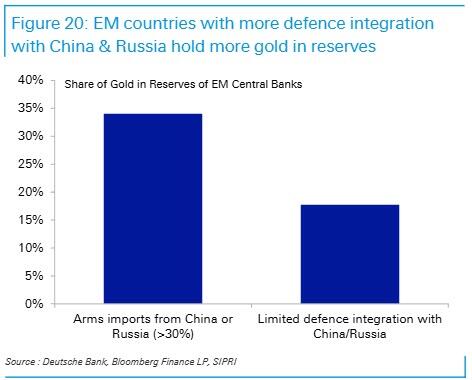

We also find that EM countries with closer defence ties to the Western bloc hold less gold in reserves, while EM countries with closer ties to China and Russia hold more gold. We draw on an analytical metric first used in our Global South framework to measure military alignment. We look at SIPRI data on arms imports for all emerging market countries over the last 10 years and calculate the proportion of arms imports from the “Eastern bloc”, which we define as including China and Russia, versus the “Western bloc” which includes the US, Israel, Europe, and South Korea. We split EM countries into two groups: those that import more than a third of arms from the “Eastern bloc”, and those that have limited defence integration with China and Russia. As Figure 20 illustrates, EM countries in the former group have double the share of gold in reserves than the latter group.

The implication of this analysis is that should more countries diversify defence dependence away from the US, this would be consistent with a reduced share of USD and a greater share of gold in reserves. The US has actively pressured major allies like NATO, South Korea and Japan to take on more ownership for their defence. And we have written about how the US-Iran conflict has challenged the US security umbrella over the Gulf and thereby support for the petrodollar and dollar savings. And while the ultimate geopolitical equilibrium remains to be seen, we think it could lead to some diversification of Gulf ties away from the US, and an acceleration in the localization of defence capabilities.

What might this mean for gold prices?

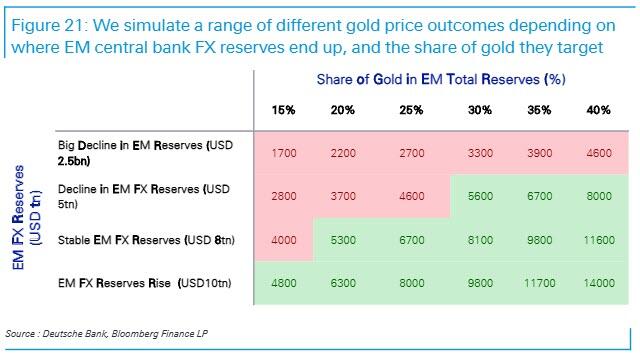

We simulate a range of different outcomes for gold prices depending on the level of FX reserves EM central banks end up with, and the share of gold in reserves they target.

For total FX reserves, we consider four potential scenarios: a steady state for EM FX reserves of USD8tn (similar to current levels); and then three alternatives: a drastic decline in EM FX reserves to USD2.5tn, a decline to USD5tn, or an increase in EM FX reserves to USD10tn.

For the share of gold in reserves, we look at a range of different shares rising from 15% to 40%. As discussed earlier, a 40% gold share could be a reasonable target for a “return to history” scenario, while 15-20% is where EM central banks are as a whole today.

We use our earlier heuristic that every 1mn troy oz of purchases (sales) drives a 1% increase (decrease) in the gold price for our analysis. Our simulation is therefore dynamic, as we assume gold purchases by central banks influence the gold share through their impact on the prices as well. The rise in gold’s share captures the blended impact of both prices and volumes.

The table in Figure 21 shares our simulation results. Prices shaded in green are above current gold prices (at the time of writing), while prices shaded in red are below. The numbers are not intended to be forecasts (found here), but to illustrate the range of potential price impacts from different combinations of EM central bank behaviour.

As intuition would suggest, if EM central banks are targeting a rising share of gold in a steady or growing FX reserves environment, this would be the most bullish outcome for gold. But even in an environment where EM FX reserves decline to USD5tn, if central banks target an increase of gold’s share to 40%, this could still be consistent with gold prices rising to near $8000 over the next five years. We walk through the calculation in the simulation to illustrate. At USD5tn in FX reserves, gold would need to be worth USD3.3tn for gold to be a 40% share. Getting to USD3.3tn in gold would be a function of central banks buying more gold, and that buying driving up prices. Assuming every 1mn troy oz of purchases drives up gold prices by 1%, if EM central banks build gold holdings to 417mn oz, or an additional 52mn oz, this would drive up prices to around $7977, which would put total gold valuations at around USD3.3tn. At the current pace of gold purchases of roughly 10mn troy oz per year by central banks (based on IMF central bank only data series), this would be consistent with five more years of gold buying. In other words, EM central banks could push gold prices to $8000 over the next five years even in a declining FX reserves environment.

In the extreme case of EM FX reserves falling to USD2.5tn, the current volume of gold held by EM central banks at current prices (USD1.7tn), would already give gold a 40% share. There is thus no upside to gold projected in the first row of the table.

This simulation also helps us understand the price action of gold in March 2026 during the Iran war. IMF reserves data for the month of March showed overall EM central banks sold gold, led by Turkiye. These gold sales are likely a function of the fact that Turkiye has a high share of gold in reserves at over 60% which were therefore leveraged for liquidity. As our colleagues note, net FX intervention by the CBT reached USD23bn in the last two weeks of March, and the CBT mobilised around USD 20bn worth of gold — USD 11.1bn via gold-FX swaps and USD 8.2bn through outright gold sales. While acute, this is not likely to be representative of a broader trend in EM. Countries from Poland to Kazakhstan were still buying gold in March according to IMF data, and China’s PBOC data also shows buying at the fastest pace in a year. Most EM countries have gold shares at far lower levels than Turkiye with significant scope to raise them.

If more of the rise of gold’s share for EM central banks is achieved through the drawdown of FX reserves, this will be less bullish for gold. If, however, EM FX reserves are stable or fall more gradually, and central banks engage in active buying of gold to raise their gold shares, this will be more bullish for gold.

What does this suggest about the monetary order to come?

As this paper has discussed, central banks in emerging markets have been actively adding to their gold holdings. The rationale for this is mostly seen as being about diversifying official savings into a physical long-lived asset, that can be held beyond the reach of sanctions, and which is likely to hold value better than fiat currencies amidst greater fiscal and inflation risks.

But it is worth considering whether the build up in physical gold in emerging markets might be a precursor to a potential return of gold as an anchor for an alternative future monetary system. Since the collapse of the Bretton Woods, gold has not had a formal role in international monetary architecture. But history has long alternated between periods of fiat and physical-backed money. It would be consistent with – not counter to – history, to expect gold to return at some stage.

The US backed the dollar with gold when it created the post-war monetary architecture of Bretton Woods. It would thus be intuitive to expect any effort by other countries looking to create a bigger role for their currencies in payments and savings to also turn to gold. Gold has been part of monetary orders for over 2500 years and is not anyone’s liability. And while production does expand supply – with above-ground gold stocks growing at around 2% a year this century – this is less than the growth in most countries’ fiscal deficits. For countries in the Global South, where economic regimes, rule of law, and capital account openness, may be less well understood by global corporates and investors, backing payment currencies with a share of physical gold could be an important trust-building mechanism.

While far from formalized as policy, there are pockets of discussion around gold playing a role in backing a future BRICS currency. A paper from OMFIF, an independent think tank for central banking, economic policy and public investment, noted that the “BRICS are exploring the creation of a common currency that would be pegged partly to gold and partly to a basket of their own currencies.” They noted that “by tokenizing gold reserves, each digital unit would be backed by tangible assets stored in secure vaults, with regular audits ensuring accountability.” They note that a “gold linked alternative BRICS payment system” could again give gold a “distinct role in payments.” Media reports in late 2025 indeed noted the pilot release of a BRICS Unit backed 40% by physical gold and 60% by an equal split of CNY, RUB, INR, ZAR, and BRL fiat currencies. We would stress that the “Unit” does not appear to be formal policy by the BRICS and thus should be considered more a thought experiment at this stage. But the momentum for creating alternative payment rails that facilitate local currency payments in the Global South are well underway. For instance, Project mBridge has already reached minimum viability for payments and involves central banks in China, Saudi Arabia, UAE, Hong Kong, and Thailand settling cross-border trade via wholesale CBDCs over the blockchain.

The economic clout of China and the Global South in PPP-adjusted GDP already exceeds 50% of the world today, and a majority of global trade flow growth is happening down these corridors. Payment innovations in this part of the world should thus be paid heed. We have written in great detail (see here) how competition around payments is heating up and how this is deeply linked with reserve currency status through the linkages between invoicing and savings. The US has opted for stablecoins as its solution to ensuring dollar dominance, namely in the Global South where traditional USD payments mechanisms were at risk. We note that while US stablecoins would be backed by US T-bills, a BRICS currency of the future could well be backed in part by physical gold.

In sum, while EM central bank diversification into gold likely has much to do with preserving the value and accessibility of their foreign savings in a changing geopolitical climate, it may also – in the long-run – play a role in anchoring a monetary order that builds independence from the dollar. There is of course a very long way to go. EM central banks as a whole still only hold half the physical gold of advanced economy central banks. But there is a world where gold returns to the centre of a future monetary system with different leaders.

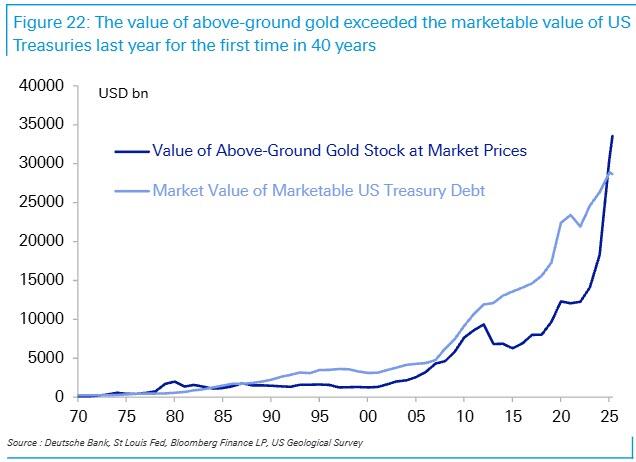

To conclude, we find it notable that the value of above-ground gold exceeded the total value of marketable US Treasury debt last year for the first time in 40 years (Figure 22). In other words, gold is now a bigger asset class than the world’s main safe asset.

The return of history is here.

Professional subscribers can read the full Deutsche Bank note: “The return of history: gold, the dollar, and the monetary future” here at our new Marketdesk.ai portal

Tyler Durden

Sun, 05/10/2026 – 06:33

https://www.zerohedge.com/markets/return-history-deutsche-gold-dollar-monetary-future

How Governments, Corporations, & Technocratic Systems Are Quietly Redefining Ownership In The 21st Century

How Governments, Corporations, & Technocratic Systems Are Quietly Redefining Ownership In The 21st Century

Authored by Milan Adams via PreppGroup,

There are periods in history when societies begin to discover that the liberties they believed to be permanent were, in reality, conditional arrangements tolerated only while they remained politically convenient. Across the Western world, governments are quietly expanding the legal and administrative mechanisms through which private land can be reclassified, restricted, absorbed, or transferred in the name of infrastructure, sustainability, industrial security, climate adaptation, and economic modernization. Entire farming regions are now being surveyed for carbon pipelines. Rural communities are facing unprecedented redevelopment pressure linked to energy transitions and semiconductor expansion. Financial institutions are purchasing strategic agricultural land at historic levels while policymakers openly discuss the restructuring of urban life around centralized digital systems. Officially, these transformations are described as progress. Unofficially, an increasing number of citizens have begun to suspect that the modern definition of ownership itself is being rewritten in real time.

The New Architecture of Property Seizure

The modern citizen has been conditioned to believe that private property represents one of the sacred foundations of liberal democracy. Constitutions defend it, political campaigns celebrate it, and economists routinely describe it as the engine of prosperity and social stability. Yet beneath the ceremonial rhetoric lies a more fragile reality — one in which ownership increasingly resembles a conditional administrative privilege rather than an untouchable natural right. This contradiction becomes impossible to ignore when examining the doctrine of eminent domain, the extraordinary legal authority through which governments may confiscate private property without the owner’s consent.

Supporters of eminent domain insist that such authority is indispensable for the functioning of modern civilization. Roads must be built, railways expanded, energy corridors connected, airports enlarged, water systems modernized, and industrial facilities constructed. In many cases, governments provide financial compensation to displaced owners, presenting the process as a rational exchange carried out for the collective benefit of society. Yet the deeper philosophical problem has never truly revolved around compensation. The more disturbing issue is whether property can genuinely be called “private” if the state ultimately reserves the authority to seize it whenever officials determine that a superior public or economic purpose exists.

Centuries ago, political philosopher John Locke articulated this contradiction with remarkable clarity in his Second Treatise of Civil Government, writing: “For I have truly no Property in that, which another can by right take from me, when he pleases against my Consent.” Locke understood that property rights and liberty are inseparable mechanisms. If ownership exists only so long as political authorities permit it, then freedom itself becomes conditional. A citizen whose property may be overridden by state power is not fully sovereign over the fruits of his labor, his land, or his future.

This philosophical tension has become increasingly visible throughout 2025 and 2026 as eminent domain controversies intensify across the United States and parts of Europe. The issue is no longer confined to highways and traditional public infrastructure. Governments are now invoking compulsory acquisition powers for semiconductor manufacturing facilities, renewable energy grids, carbon capture pipelines, smart-city redevelopment programs, affordable housing mandates, climate resilience projects, and strategic industrial corridors tied to geopolitical competition with China. What once appeared to be an exceptional legal mechanism reserved for rare circumstances is gradually evolving into a normalized instrument of economic planning.

The transformation accelerated dramatically after the controversial Supreme Court decision in Kelo v. City of New London in 2005, which expanded the interpretation of “public use” to include broader economic development objectives. The ruling effectively established that governments could seize private property and transfer it to private developers if officials believed the redevelopment project might generate greater economic productivity or increased tax revenue. Although the decision triggered national outrage, the long-term implications proved even more consequential than many observers initially realized. The ruling fundamentally altered the psychological relationship between citizens and ownership itself. Property was no longer protected solely because it belonged to an individual; it could now be reclassified according to projected economic utility.

Ironically, many of the promises surrounding the original New London redevelopment project collapsed. Large sections of the confiscated land remained undeveloped for years, becoming symbolic monuments to speculative planning failures. Yet rather than causing governments to retreat from expansive eminent domain practices, the ruling instead normalized a new political vocabulary capable of reframing coercive land acquisition in increasingly sophisticated ways. “Urban renewal” evolved into “smart growth.” “Industrial expansion” transformed into “strategic economic resilience.” “Environmental necessity” became “climate adaptation infrastructure.” The language softened while the underlying mechanism remained fundamentally unchanged.

One of the most explosive contemporary examples emerged from the construction of carbon dioxide pipelines across the American Midwest. These projects, promoted as essential components of future climate infrastructure, triggered fierce resistance from farmers and rural landowners who argued that their property rights were being subordinated to corporate and political agendas disguised as environmental policy. Summit Carbon Solutions initiated hundreds of legal actions connected to eminent domain disputes as officials and developers attempted to secure continuous pipeline corridors through privately owned agricultural land. For many rural communities, the issue transcended compensation entirely. Families feared not only environmental consequences involving groundwater and soil stability, but also the broader precedent being established through these forced acquisitions.

The backlash became politically severe enough that South Dakota eventually banned the use of eminent domain for carbon dioxide pipelines in 2025. The significance of this moment extended beyond the pipeline debate itself because it revealed a rapidly expanding distrust toward centralized planning institutions. Citizens increasingly sensed that environmental objectives were being used to justify extraordinary powers capable of overriding local autonomy and long-standing ownership traditions. While governments publicly framed such projects as indispensable for decarbonization and sustainable development, critics argued that the legal infrastructure being constructed around climate policy could eventually extend far beyond pipelines alone.

Many analysts dismiss these fears as exaggerated or conspiratorial. Nevertheless, the broader anxieties persist because governments and international organizations are already openly discussing policies involving managed retreat zones, climate adaptation corridors, AI-assisted urban planning systems, and expanded environmental land-use restrictions. Individually, each proposal appears administratively rational. Collectively, however, they begin to resemble the early architecture of a society in which ownership is increasingly subordinate to centralized optimization models designed around sustainability metrics, industrial planning objectives, and algorithmic governance systems.

The semiconductor industry has provided another revealing example of how geopolitical competition is reshaping the balance between state authority and individual property rights. In New York, a massive semiconductor manufacturing expansion connected to a multibillion-dollar industrial initiative displaced elderly homeowners whose land had been targeted for redevelopment. Officials justified the project as strategically indispensable for national security and technological independence, particularly amid intensifying tensions between the United States and China over advanced chip production. Within such frameworks, resistance from individual landowners becomes politically inconvenient because industrial competitiveness itself is treated as a permanent national emergency requiring extraordinary intervention.

This represents a profound transformation in the logic of democratic governance. Historically, governments expanded coercive authority during visible wars or catastrophic crises. Today, however, economic competition itself increasingly functions as a perpetual justification for exceptional state power. Artificial intelligence infrastructure requires enormous data centers. Data centers require energy corridors and water access. Energy corridors require land consolidation. Strategic manufacturing requires zoning flexibility and rapid acquisition mechanisms. Under these conditions, private property gradually becomes an obstacle to national planning objectives rather than a protected sphere of individual autonomy.

The emotional dimension of this conflict becomes especially visible when examining multigenerational farmland disputes. Across several states, families cultivating the same land for over a century have found themselves confronting eminent domain proceedings connected to rail expansions, renewable energy projects, housing mandates, and transportation corridors. These confrontations reveal a deeper philosophical fracture embedded within modern governance systems. Technocratic institutions increasingly evaluate land through the lens of utility maximization, calculating value according to projected tax revenue, housing density targets, industrial productivity, environmental compliance metrics, or strategic infrastructure potential. Within such frameworks, land ceases to represent permanence, inheritance, or identity and instead becomes a movable economic variable inside a larger administrative equation.

Families, however, tend to perceive property through an entirely different moral architecture. A farm cultivated across generations is not merely acreage measured in market value, just as a family home cannot be reduced to a line inside a municipal redevelopment blueprint. These places often embody continuity, memory, sacrifice, and personal sovereignty in ways financial compensation can never adequately replace. This growing collision between technocratic optimization and emotional permanence is rapidly becoming one of the defining political tensions of the twenty-first century.

What makes the situation particularly volatile is the emergence of a broader economic philosophy that increasingly treats ownership itself as inefficient when compared to centralized management systems. A growing number of political theorists and economic critics have begun describing this transformation as a form of neo-feudalism — not a literal return to medieval structures, but rather the gradual replacement of independent ownership with conditional access controlled by interconnected institutional authorities. Under such systems, citizens may still possess legal titles, mortgages, or deeds, yet ultimate control over property becomes layered beneath zoning commissions, environmental agencies, taxation systems, redevelopment authorities, financial institutions, insurance corporations, and emergency regulatory powers capable of overriding individual autonomy whenever larger policy objectives demand intervention.

The implications of this shift become even more unsettling when viewed alongside the accelerating digitization of governance. Across the Western world, governments and international organizations have proposed integrating land registries with digital identity systems, smart contracts, environmental compliance monitoring, and AI-assisted administrative oversight. Publicly, these innovations are framed as modernization efforts designed to reduce fraud, improve efficiency, and streamline urban planning. Critics, however, fear that such systems could eventually create the infrastructure for unprecedented levels of centralized influence over property rights, particularly if future economic or climate emergencies are used to justify extraordinary intervention measures.

While many of the more apocalyptic theories surrounding these developments remain speculative, the underlying anxieties persist because citizens can already observe partial versions of these dynamics emerging in real time through environmental zoning restrictions, mass institutional acquisition of farmland, algorithmic insurance risk assessments, and increasingly aggressive redevelopment policies carried out under the language of sustainability and economic necessity. Even in the absence of a coordinated conspiracy, the cumulative effect can still produce the same practical outcome: the gradual erosion of truly independent ownership.

Regions Increasingly Targeted by Strategic Redevelopment and Land Acquisition Pressures

Midwest agricultural corridors in Iowa, Nebraska, and South Dakota connected to carbon pipeline expansion projects and renewable infrastructure routes.

Semiconductor development zones in New York, Arizona, and Texas where strategic manufacturing initiatives are accelerating property acquisition and rezoning procedures.

Coastal regions in California, Florida, and parts of the Gulf Coast increasingly affected by climate adaptation planning, insurance withdrawal crises, and managed retreat discussions.

Rural farmland sectors across Illinois, Indiana, and Kansas experiencing rapid institutional investment linked to future food security and energy transition strategies.

Urban redevelopment districts in cities such as Atlanta, Chicago, and Philadelphia where “blight” designations and smart-city modernization programs have intensified displacement concerns.

Transportation and logistics corridors surrounding major inland freight hubs, particularly near Dallas-Fort Worth, Memphis, and Kansas City, where industrial optimization projects continue expanding aggressively.

Water-resource regions in the American Southwest where future scarcity projections are beginning to influence zoning policy, agricultural rights, and long-term land valuation models.

As these pressures intensify, the political meaning of ownership itself may continue evolving in ways previous generations would have considered unthinkable. The central issue is no longer limited to whether governments possess the authority to seize property under extraordinary circumstances. The more consequential question involves how frequently those circumstances are now being redefined and expanded to accommodate increasingly ambitious economic, technological, environmental, and geopolitical objectives.

The modern world increasingly celebrates efficiency as the supreme organizing principle of civilization. Governments pursue efficient transportation systems, efficient energy transitions, efficient housing density models, efficient industrial logistics, and efficient urban management structures powered by predictive algorithms and centralized data analysis. Yet liberty has never been efficient. Genuine freedom often depends upon the existence of friction — the ability of individuals to refuse, resist, delay, negotiate, or preserve spaces outside the reach of centralized planning systems.

The farmer who refuses to sell ancestral land, the homeowner resisting redevelopment pressure, the rancher opposing compulsory easements, and the family preserving generational property despite extraordinary financial offers all represent forms of resistance against the growing belief that economic optimization should supersede personal sovereignty. From a purely technocratic perspective, such resistance appears irrational because it slows development and complicates large-scale planning objectives. From a liberty-centered perspective, however, these acts preserve the final boundary separating ownership from conditional occupancy.

In this sense, the debate surrounding eminent domain extends far beyond legal procedure or infrastructure policy. It touches the deeper philosophical foundation of democratic civilization itself. A society in which property exists only until authorities identify a superior administrative use gradually transforms ownership into permission rather than right. Once that transition occurs, liberty itself begins losing the permanence required for true independence. The danger may not emerge suddenly through overt authoritarianism, but incrementally through layers of regulation, emergency policy, technological integration, and economic planning that slowly redefine the relationship between citizens and the spaces they once believed belonged entirely to them.

The long-term consequences of this transformation may become even more profound as artificial intelligence, predictive governance systems, and centralized economic planning begin converging into a single administrative framework. During previous centuries, governments lacked the technological capacity to monitor property usage, energy consumption, environmental compliance, financial behavior, demographic movement, and land productivity in real time. That limitation functioned as an invisible restraint on centralized authority. Modern states, however, are rapidly acquiring precisely these capabilities through satellite surveillance, digital registries, biometric identification systems, AI-assisted analytics, and integrated financial technologies capable of processing enormous volumes of behavioral data simultaneously.

This technological convergence has introduced a new political phenomenon that many citizens still underestimate: the replacement of reactive governance with anticipatory governance. Traditional democratic systems generally responded to visible crises after they emerged. Contemporary institutions increasingly attempt to predict and preempt future economic, environmental, or infrastructural disruptions before they fully materialize. In theory, such predictive governance promises efficiency and stability. In practice, it creates conditions under which governments may justify extraordinary interventions based not on present realities, but on statistical projections, algorithmic forecasting, and speculative risk assessments.

This distinction is critical because speculative governance dramatically expands the potential scope of eminent domain and administrative land control. A government no longer needs to demonstrate that land is immediately necessary for an existing public project. It may instead argue that future climate migration patterns, projected energy shortages, demographic shifts, industrial competition, water scarcity, or strategic economic vulnerabilities justify preemptive territorial restructuring decades in advance. Under such conditions, ownership becomes vulnerable not only to current policy objectives but also to predictive models generated by institutions whose assumptions may themselves remain politically contested.

The implications become especially significant when examining the emerging relationship between climate policy and territorial governance. Across North America and Europe, policymakers increasingly discuss the concept of “climate resilience corridors,” managed retreat zones, adaptive infrastructure networks, and carbon-neutral urban restructuring. Publicly, these proposals are presented as rational responses to environmental instability. Yet critics argue that the language surrounding climate adaptation is gradually normalizing the idea that governments may eventually redesign entire regions according to sustainability criteria determined by centralized planning authorities rather than local communities.

Several environmental planning documents have already explored scenarios involving the relocation of populations away from vulnerable coastal areas, the consolidation of agricultural production into designated efficiency zones, and the expansion of urban density models designed to reduce transportation emissions. None of these proposals necessarily constitute authoritarian conspiracies in themselves. Nevertheless, they reveal an ideological trajectory in which land is increasingly treated as a strategic administrative asset subject to optimization rather than as a decentralized foundation of individual autonomy.

This broader transformation also intersects with the accelerating financialization of property markets. Over the past decade, institutional investors, multinational asset management firms, pension funds, and corporate real-estate conglomerates have acquired unprecedented quantities of residential housing, farmland, and strategic infrastructure-linked territory throughout the Western world. In many regions, ordinary citizens now compete against entities possessing virtually unlimited liquidity and long-term strategic acquisition models. Critics increasingly fear that this trend is creating a bifurcated society in which large institutions accumulate permanent ownership while ordinary populations transition toward perpetual rental dependency.

The psychological effects of this shift are already visible among younger generations. Homeownership, once considered a realistic milestone of adulthood, has become unattainable for millions due to escalating property prices, speculative investment patterns, and declining purchasing power. As ownership recedes, dependence on institutional landlords, subscription-based living models, and centralized service ecosystems intensifies. What previous generations viewed as temporary economic hardship may actually represent the early stages of a more permanent structural transition away from widespread independent ownership.

Some economic futurists openly defend this transition, arguing that access-based economies are more flexible, sustainable, and technologically compatible with modern urban life. According to this perspective, citizens no longer require permanent ownership because digital platforms can provide transportation, housing, entertainment, labor, and consumption through integrated subscription ecosystems. Yet critics counter that access and ownership are fundamentally different forms of social power. Ownership creates autonomy, while access remains conditional upon continued institutional approval and financial compliance. A citizen who owns nothing substantial becomes increasingly vulnerable to economic disruption, policy changes, financial censorship, algorithmic exclusion, or shifting regulatory standards.

This concern has intensified dramatically following the expansion of digital financial surveillance systems and programmable payment technologies. Several governments and central banks have explored the future implementation of central bank digital currencies capable of integrating transactions into highly centralized financial architectures. Officially, such systems are promoted as tools for efficiency, anti-fraud enforcement, and economic modernization. However, skeptics fear that combining centralized financial control with digitized property systems could eventually create unprecedented leverage over individual autonomy. If property rights, taxation, energy consumption, environmental compliance, banking access, and digital identity become interconnected within unified administrative systems, then ownership itself may become increasingly conditional upon behavioral conformity.

While some of the more apocalyptic narratives surrounding these developments undoubtedly exaggerate the immediacy of such scenarios, the broader structural trajectory remains difficult to ignore. Governments across the world are steadily increasing their reliance on integrated digital oversight mechanisms. Corporations are accumulating strategic physical assets at extraordinary rates. Artificial intelligence systems are becoming embedded within regulatory decision-making processes. Climate policy is expanding into territorial planning. Economic competition is increasingly framed as a permanent emergency requiring centralized coordination. Each development, considered individually, appears manageable. Collectively, however, they form a landscape in which traditional concepts of private ownership may become progressively diluted over time.

The cultural consequences of this evolution could prove as significant as the legal and economic consequences. Property ownership historically functioned not merely as a financial asset, but as a psychological foundation for citizenship itself. Individuals who possessed land, homes, farms, or independent businesses generally maintained stronger incentives to participate in civic life, resist political overreach, and preserve local community structures. Ownership cultivated permanence, and permanence fostered responsibility toward future generations.

By contrast, highly transient populations dependent upon rental systems and centralized infrastructure often develop weaker attachments to local institutions and reduced capacity for long-term independence. A society dominated by temporary access arrangements rather than enduring ownership may gradually become more politically passive, economically fragile, and administratively manageable. In such environments, governments and corporations acquire increasing influence not necessarily through overt coercion, but through structural dependency.

This dynamic helps explain why eminent domain debates provoke such intense emotional reactions even among citizens who never expect their own property to be seized directly. At an instinctive level, many people recognize that the issue transcends infrastructure policy entirely. The struggle concerns whether there remains any sphere of life genuinely insulated from centralized authority. If property can ultimately be overridden whenever sufficient political, economic, environmental, or technological justification emerges, then ownership itself risks becoming symbolic rather than substantive.

The modern political class frequently frames these tensions as conflicts between progress and obstruction. Citizens resisting redevelopment projects are often portrayed as impediments to modernization, sustainability, affordability, or economic growth. Yet this framing deliberately ignores the philosophical role private property has historically played within free societies. Property rights were never designed solely to maximize economic efficiency. They existed partly to limit concentrations of power by ensuring that individuals retained independent zones of autonomy resistant to political centralization.

The erosion of those protections rarely occurs through sudden authoritarian decrees. More often, it unfolds gradually through administrative normalization. Each new exception appears temporary. Each emergency justification appears rational. Each expansion of authority appears narrowly tailored to a specific crisis. Over time, however, the cumulative effect can fundamentally redefine the relationship between citizens and the state without any single revolutionary moment ever occurring.

History repeatedly demonstrates that societies often fail to recognize transformative shifts while they are happening. Citizens adapt incrementally to changes that previous generations would have considered extraordinary. Policies initially introduced during emergencies become permanent. Temporary surveillance becomes normalized infrastructure. Exceptional powers evolve into ordinary administrative procedures. By the time the broader transformation becomes fully visible, institutional momentum may already be deeply entrenched.

This is precisely why contemporary property-rights debates deserve far greater scrutiny than they currently receive. The issue is not simply whether governments occasionally require land for legitimate public projects. Every complex civilization inevitably faces situations involving infrastructure development and competing territorial interests. The deeper concern involves the accelerating expansion of the philosophical categories capable of justifying compulsory acquisition and centralized territorial management.

Today, governments invoke eminent domain and land restrictions for highways, carbon pipelines, renewable energy corridors, semiconductor facilities, affordable housing mandates, environmental adaptation projects, logistics hubs, and industrial modernization zones. Tomorrow, additional categories may emerge involving AI infrastructure, water rationing systems, food-security corridors, demographic redistribution planning, or automated transportation networks. As technological complexity increases, the temptation for centralized optimization will likely intensify alongside it.

Yet civilizations ultimately face a profound choice between efficiency and autonomy. A perfectly optimized society may achieve extraordinary administrative coordination while simultaneously eroding the independent spaces necessary for genuine liberty. Conversely, a society committed to preserving strong property rights inevitably accepts a degree of inefficiency because decentralized ownership creates friction against centralized planning. That friction is not a flaw within free societies; it is often their primary safeguard against excessive concentration of power.

The future of property rights may therefore determine far more than real-estate law or zoning policy. It may shape the very architecture of citizenship in the twenty-first century. Whether individuals remain sovereign owners with meaningful independence or gradually transition into highly managed participants within centralized administrative ecosystems could become one of the defining political questions of the coming era.

And perhaps that is the most unsettling aspect of the entire debate: the possibility that the transformation is not arriving through dramatic revolution, military force, or visible dictatorship, but through a slow and highly sophisticated convergence of technology, economic planning, environmental policy, financial centralization, and administrative normalization that redefines ownership so gradually that many citizens may not fully recognize the implications until the older understanding of liberty has already faded into history.

Tyler Durden

Sat, 05/09/2026 – 23:20

Chinese EVs Absent From U.S. Roads, But Parts Under The Hood Are Alarming

Chinese EVs Absent From U.S. Roads, But Parts Under The Hood Are Alarming

For good reason, U.S. policymakers have resisted opening the domestic auto market to a flood of cheap, gasoline-powered Chinese cars and EVs. Such a move would crush Detroit into even more misery. It would accelerate the hollowing out of the nation’s industrial base (something Europe willingly did), further degrade suppliers, and weaken the country’s ability to convert truck production lines to tank production in wartime.

However, while Chinese-made cars remain absent from U.S. highways, there has been a flood of Chinese auto parts, from airbags to transmissions to starters to steering systems and many other components, according to a new Wall Street Journal report citing data from consulting firm AlixPartners.

According to AlixPartners data, Chinese companies hold ownership stakes in about 10,000 suppliers nationwide. The exposure is an eye-opener for lawmakers, as the urgency to decouple critical supply chains from China remains a national security priority under the Trump administration.

“They’re [China] deeply integrated into the industry,” Michael Dunne, CEO of automotive consulting firm Dunne Insights, told the outlet.

Examples of this alarming deep integration include Ford’s Mustang GT, which uses a six-speed manual transmission from China; Toyota’s Prius plug-in hybrid, with about 15% of parts sourced from China; and GM’s Chevrolet Trax, Blazer EV, and Equinox EV, which contain approximately 20% Chinese parts.

Several automakers have been dialing back their parts exposure to China in recent years. Tesla has required suppliers to remove China-made components from U.S.-built vehicles, while GM says China now accounts for less than 3% of its direct material spending for U.S.-made cars. Still, government data show that at least 40 models for sale in the U.S. have alarmingly high levels of Chinese components.

What’s increasingly clear is that over the last 15 years, Beijing has been taking aggressive market share in the global auto market to become a dominant player. AlixPartners data show that in 2012, only one Chinese company ranked among the world’s top 100 auto suppliers. Now that figure is expected to reach 22 by 2030.

Lawmakers have been briefed about ways to eliminate Chinese auto parts from the U.S. market, which has only put pressure on the domestic supplier network.

In late April, more than 50 House Republicans, led by Rep. Mike Kelly (R., Pa.), penned a letter to Treasury Secretary Scott Bessent, Commerce Secretary Howard Lutnick, and U.S. Trade Representative Jamieson Greer, urging them to block Chinese automotive and battery companies from manufacturing in the U.S.

Juergen Simon, a partner at AlixPartners, told the outlet, “This shows the incredible speed at which the competitive environment has changed.” He noted that Chinese suppliers were once avoided due to concerns about quality and performance, but that is no longer the case.

The race to clean up decades of globalism that crushed America’s industrial core is well underway with the Trump administration. It appears the move to rebuild the nation’s auto supplier network and eliminate China from that ecosystem could be nearing.

Tyler Durden

Sat, 05/09/2026 – 22:45

https://www.zerohedge.com/geopolitical/chinese-evs-absent-us-roads-parts-under-hood-are-alarming

4 Key Points From New White House Counter-Terror Strategy

4 Key Points From New White House Counter-Terror Strategy

Authored by Ryan Morgan via The Epoch Times,

President Donald Trump’s administration rolled out its new counterterrorism strategy overview on May 6, articulating recent policy shifts and new pledges going forward.

The 16-page strategy guide seeks to articulate an “America First” approach to dealing with militants, extremists, and criminal enterprises.

“For the 25th Anniversary of the 9/11 terror attacks, America has returned to a common sense and reality-based Counterterrorism Strategy,” the document states.

“President Trump has [effected] a complete revision of how we defeat threats to America predicated on national sovereignty and civilizational confidence and the objective of destroying the groups who would kill Americans or hurt our interests as a free nation.”

Here are four key points in the new strategy rollout.

Violent Left-Wing Groups Fall Under Expanded Counterterror Scope

The new strategy document articulates a widened aperture for U.S. counterterrorism efforts.

“We face new categories and combinations of violent actors that make the established ways of doing counterterrorism insufficient or obsolete,” the document reads.

Although U.S. counterterror efforts have long focused on threats posed by radical Islamist groups, the new strategy document also lists “violent left-wing extremists” and “narcoterrorists and transnational gangs” among the top three major categories of terror groups.

The Trump administration has already taken steps to apply counterterrorism authorities to violent left-wing groups and ideological movements that oppose the American way of life as outlined in the founding documents.

In November 2025, the U.S. State Department designated four violent transnational left-wing groups as foreign terrorist organizations.

Trump previously issued an executive order declaring Antifa a domestic terrorist organization, although U.S. law currently provides no domestic equivalent to a foreign terrorist organization designation.

Antifa members gather to demonstrate following the announcement of the results of the first round of the presidential election, in Nantes, France, on April 23, 2017. Jean-Sebastien Evrard/AFP via Getty Images

“Our national [counterterrorism] activities will also prioritize the rapid identification and neutralization of violent secular political groups whose ideology is anti-American, radically pro-transgender, and anarchist,” the document states.

“We will use all the tools constitutionally available to us to map them at home, identify their membership, map their ties to international organizations like Antifa, and use law enforcement tools to cripple them operationally before they can maim or kill the innocent.”

The document, at one point, describes a so-called Red-Green alliance of deepening alignment between far-left and Islamist movements.

Focus Shifting to the Western Hemisphere

The move to list cartels and transnational gangs as a leading terror threat category aligns with a broader effort to shift the focus of U.S. counterterror operations to the Western Hemisphere.

“Our Strategy first prioritizes the neutralization of hemispheric terror threats by incapacitating cartel operations until these groups are incapable of bringing their drugs, their members, and their trafficked victims into the United States,” the document reads.

Since the start of Trump’s second term, the State Department has added 15 Latin American and Caribbean cartels and criminal gangs to its list of foreign terrorist organizations.

In September 2025, U.S. military forces began conducting lethal strikes on what officials said were confirmed drug trafficking boats operating in the Caribbean Sea, and later in the Eastern Pacific. Those lethal strikes have continued in the months since.

The U.S. Southern Command reported its most recent strike on a drug boat on May 5. Three people were killed in the strike.

Nicolás Maduro and his wife, Cilia Flores (rear), are escorted by federal agents after landing at a Manhattan helipad, as they make their way into an armored car en route to a federal courthouse in New York City on Jan. 5, 2026. XNY/Star Max/GC Images

U.S. forces also carried out a special operations raid on Venezuela on Jan. 3 to capture Venezuelan leader Nicolás Maduro and bring him to the United States to face criminal prosecution on charges related to drug trafficking and narco-terrorism.

The new strategy document explicitly lists countering leading Islamic extremist groups as its second-highest priority. The document said the top five Islamist groups are al-Qaeda, al-Qaeda in the Arab Peninsula, ISIS, ISIS-Khorasan, which is active in central and south Asia, and the Muslim Brotherhood.

Expanding Resources and Partnerships

Overall, the new strategy document describes an effort to reinvigorate counterterrorism efforts under Trump’s tenure. That includes allocating additional domestic resources and bolstering international partnerships.

The document described the move to designate cartels and other transnational gangs as foreign terrorist organizations as one such step “to make available additional intelligence authorities and deny and disrupt their financial streams and access to the United States.”

Trump is the first U.S. president to apply formal terror designations to such groups and free up counterterrorism authorities to address their activities.

In March, U.S. Secretary of War Pete Hegseth signed a multilateral security cooperation agreement for the Western Hemisphere with 16 counterparts across Latin America and the Caribbean. The agreement included a commitment to join “a coalition to combat narco-terrorism and other shared threats” in the region.

Sonora State Police officers conduct an operation in the deserts of Sonora, Mexico, on April 15, 2025. John Fredricks/The Epoch Times

“President Trump has ushered in a new dawn of burdenshifting, and now is the time to work more aggressively with partners to crush lingering terrorist threats to the United States,” the new counterterrorism strategy document states.

The new document also described the use of diplomatic, financial, cyber, and covert actions to support counterterrorism efforts.

The administration said counterterrorism efforts also include “aggressive information operations to demoralize terror organizations and undermine their anti-American and anti-Western propaganda.”

“We have assets outside the realms of hard security in the informational space that were allowed to atrophy in recent years or were used for partisan political purposes,“ the document states. ”These were previously de-weaponized and must now be reinvigorated to demoralize and delegitimize terror threat groups and their enablers.”

Pledge for Apolitical, Evidence-Based Approach

Although the new counterterrorism guide elevates violent left-wing extremists to one of the three major groups responsible for perpetrating terror against the United States, the strategy document articulates a pledge to guard against counterterrorism authorities being abused for political ends.

“Our counterterrorism operations will be executed apolitically and founded upon reality-based threat assessments,” the document states.

“Our counterterrorism powers will not be used to target our fellow Americans who simply disagree with us. We will not permit the weaponization of America’s unparalleled CT capabilities for partisan purposes and in contravention of every American’s God-given rights.”

Members of the FBI knock on the doors of neighbors of a home associated with the suspected White House Correspondents’ Dinner shooter in Torrance, Calif., on April 26, 2026. Patrick T. Fallon/AFP

The strategy document described U.S. counterterrorism efforts under Trump’s predecessor—President Joe Biden—as being directed against conservatives, Christians, and parents protesting policy changes at school boards.

“Millions of Americans have lost confidence in the rectitude of the most powerful elements of our Federal government; the national security apparatus of the United States,” the document reads.

“That confidence can only be won back when counterterrorism is executed uninfected by politics, and if those who used their counterterrorism powers as a weapon against the innocent pay the full judicial cost for their crimes against the civil rights of innocent Americans.”

Tyler Durden

Sat, 05/09/2026 – 22:10

https://www.zerohedge.com/political/4-key-points-new-white-house-counter-terror-strategy

Cameco Sees As Many As 20 AP1000 Nuclear Reactors On The Horizon

Cameco Sees As Many As 20 AP1000 Nuclear Reactors On The Horizon