Category: News

Housing Market’s Crucial “Spring Selling Season” Is In Tatters

Housing Market’s Crucial “Spring Selling Season” Is In Tatters

Authored by Wolf Richter via Wolf Street,

Late last year and early this year, the story was that dropping mortgage rates, powered by big rate cuts from the Fed, would unleash demand in the housing market in the spring – the key spring selling season – and that sales volume would take off and that Realtors’ commissions would rocket to the moon.

And so that didn’t happen. Inflation has been reheating for months before the war and before the energy price spike. The energy price spike in March and April then added to that resurgence of inflation. The Fed is now talking about a possibility of rate hikes as next move. And longer-term Treasury yields, such as the 10-year Treasury yield, rose in March and April in response to inflation fears. Mortgage rates, which track those Treasury yields but are higher, rose back to the 6.5% range. And the housing market remained in the same-old-same-old frozen pattern that it has been in for four years after the price explosion from mid-2020 through mid-2022. And it continued in the latest week.

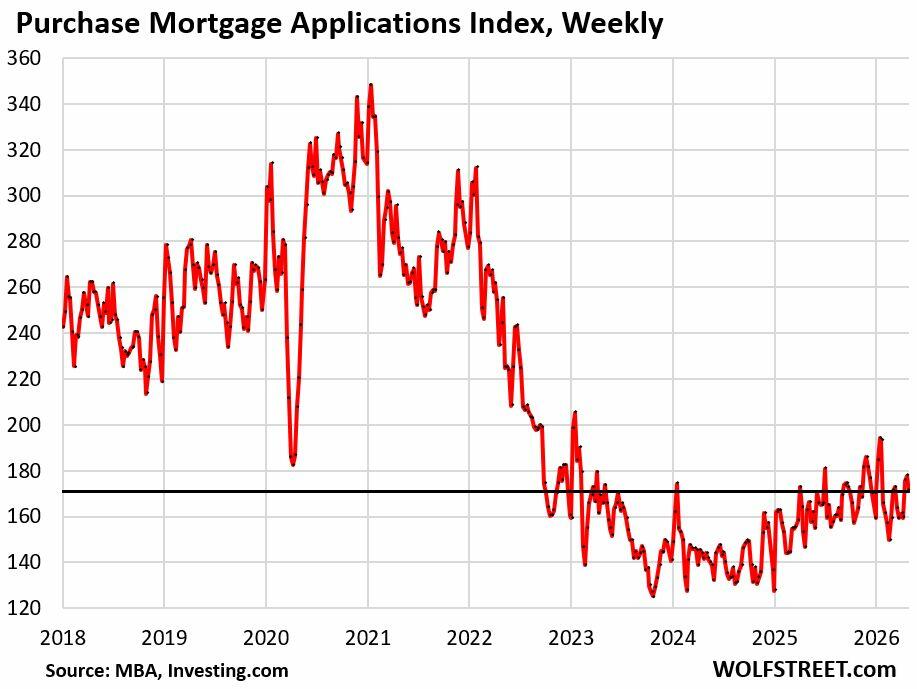

Mortgage applications to purchase a home – a measure of demand that may become actual home sales in the future, so a forward-looking indicator of home sales – dipped in the current survey week and remained near rock-bottom levels, down by 34% from the same week in 2019, according to data by the Mortgage Bankers Association today. That level of mortgage applications is below even the collapse of mortgage applications during the lockdown in the spring of 2020.

The average weekly mortgage rate for conforming 30-year fixed mortgages rose to 6.45% in the latest reporting week, according to the Mortgage Bankers Association today.

For the past 7 weeks, this measure of mortgage rates has been back in the middle of the 6-7% range, the range it has been in since September 2022, except for some breakouts to the upside.

These mortgage rates are not high in a historical context; they’re only high in the context of the Fed’s QE which started in 2009 and took on mega-proportions during the pandemic.

Under its QE programs, the Fed bought trillions of dollars of securities, including mortgage-backed securities (MBS), which repressed mortgage rates below 3%. But this massive amount of reckless money printing was part of the toxic mix at the time that triggered the worst inflation in 40 years. With mortgage rates below 3% and inflation at 9% – negative “real” mortgage rates, better than free money – home prices exploded and are now too high. And that inflation has refused to go back into the bottle.

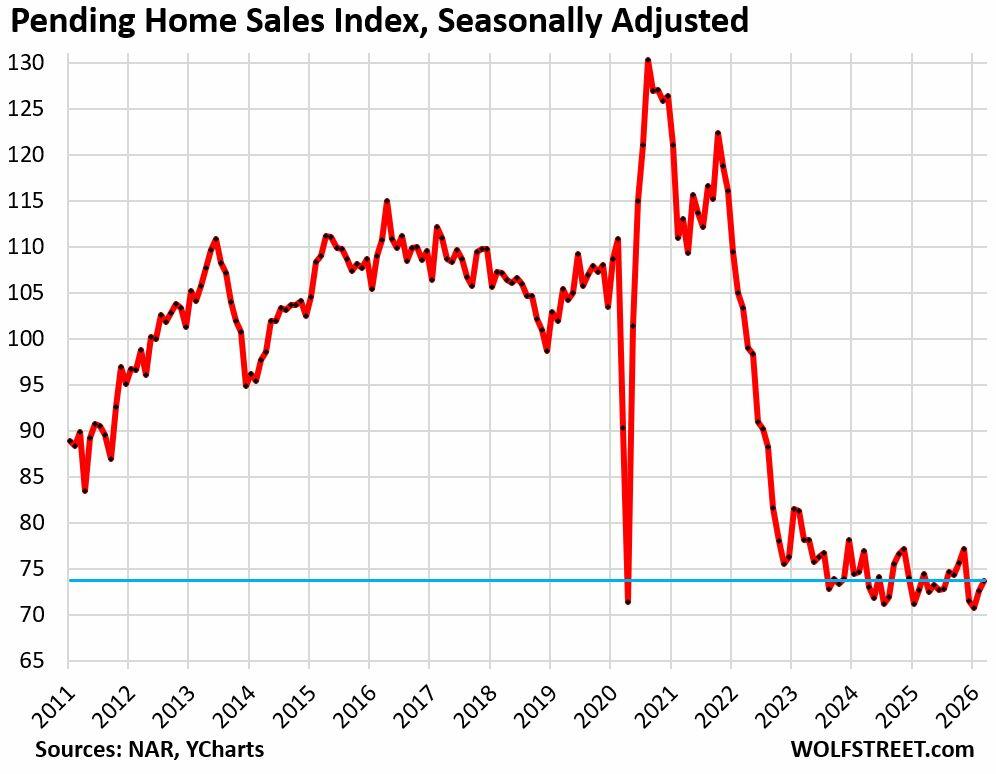

Pending home sales for March – deals that were signed in March but haven’t closed yet – also remained at rock bottom, down by 30% from March 2019. In January, they’d dropped to a record low in the data by the National Association of Realtors going back to mid-2010, and in February and March, they inched up from that record low.

And the much-hyped spring selling season has turned into the fourth dud in a row: 2023, 2024, 2025, and 2026.

Mortgage applications to refinance a home instantly react to even small changes in mortgage rates. A dip in mortgage rates unleashes homeowners like a coiled spring to refinance a mortgage at even a slightly lower rate. And when mortgage rates rise after that dip, demand re-fizzles. These dynamics have been repeated several times since mid-2024.

Refis do nothing for the housing market, though they’re crucial for the income of mortgage brokers and lenders. But they may have a positive impact on consumer spending when they lower the mortgage payments and leave borrowers more money to spend on other stuff; or when they’re cash-out refis, the proceeds of which might then be used to pay down more expensive debts, or might be used for spending projects.

The up-front fees to be paid by homeowners when they refinance a mortgage – typically 1% of the mortgage balance – are generally added to the loan amount where they’re largely out of sight but increase the payment, which reduces the advantage of lower mortgage rates.

Homeowners can do a breakeven analysis with online calculators or through brokers and mortgage lenders, to see if refinancing a mortgage is worth it. When mortgage rates briefly drop and the breakeven analysis tilts their way, they pull the trigger, thereby creating these curious spikes in refis.

But even these spikes in refis since mid-2024 were relatively low compared to the two-year refi boom from early 2020 through 2021 when the Fed’s QE repressed mortgage rates below 3%, and everyone and their dog refinanced into these low-rate mortgages.

And now they’re part of the “lock-in effect,” when these homeowners avoid buying a new home, and thereby selling their current home, because the new home’s much higher price would have to be financed at a much higher mortgage rate, and that math doesn’t work very well for many people. But life does happen. My analysis: Update on the “Lock-in Effect” in the Housing Market: Below-3% & 4% Mortgages Fade Very Slowly

This longer view demonstrates the inverse relationship between mortgage rates (blue) and applications to refinance a mortgage (red):

In case you missed it: New Single-Family Home Prices Drop Further amid Inventory Glut. But Lower Prices Beget Higher Sales

Tyler Durden

Sun, 05/10/2026 – 12:15

https://www.zerohedge.com/economics/housing-markets-crucial-spring-selling-season-tatters

Soaring Death Toll In Lebanon Toll As Full-Fledged Israel, Hezbollah Fighting Returns

Soaring Death Toll In Lebanon Toll As Full-Fledged Israel, Hezbollah Fighting Returns

Full-fledged war has returned to Lebanon as the government has announced that at least 23 people have been killed by Israeli airstrikes on Saturday alone.

Stretching back into Friday, this brings the total death count to at least 50 killed over the past 24 hours of Israeli bombings, also as Lebanon’s National News Agency (NNA) late on Saturday said rescue operations were still ongoing for bystanders missing underneath the rubble.

Illustrative prior image: Getty

Heavy bombing has not ceased in southern Lebanon, as the Israeli military says it’s trying to root out and destroy Hezbollah, including raids on the districts of Nabatieh, Bint Jbeil and Sidon, among others. Several were also killed in Tyre on Friday.

But Israeli forces have also absorbed casualties, with The Times of Israel describing the following serious drone strikes launched from Lebanon:

On Saturday, the terror group launched several salvos of explosive-laden drones and rockets at Israeli forces. One drone struck Israeli territory, close to the border with Lebanon, seriously injuring a reservist soldier and moderately wounding a reservist officer and another reservist soldier.

The troops were taken to Galilee Medical Center, which said the seriously wounded soldier underwent surgery and was now stable in the intensive care unit. The moderately wounded troops were scheduled for surgery later.

In another incident, the military said an explosive drone struck an unmanned engineering vehicle in southern Lebanon, causing damage. No injuries were caused.

There are reports of the IDF issuing evacuation orders for various areas, only to attack the so-called safe zones. For example the below comes via Israeli sources:

“In light of the Hezbollah terror organization’s violations of the ceasefire agreement, the IDF is forced to act against it with force and does not intend to harm you,” warned army spokesman Col. Avichay Adraee.

Meanwhile, Lebanese media reported that Israeli airstrikes on Saturday killed at least 12 people, including in areas where no evacuation orders were issued.

Starting in late April a 10-day ceasefire brokered by Washington took effect, even as Israeli forces remain deployed in a strip of Lebanese territory several miles deep along the border. That appears to be effectively collapsed, also as Israel has been upping its targeting of Beirut suburbs of late.

Israel calls the Lebanese strip of land now occupied by IDF troops a ‘buffer zone’ – but Lebanon sees it as a land grab. Lebanese Parliament Speaker Nabih Berri, a Hezbollah ally and leader of the Amal Movement – which is the other big Shia organization in Lebanon – has recently stated that if Israel “maintains its occupation, whether of areas, positions, or by drawing yellow lines, it will smell the scent of resistance every day.” He added: “If they insist on remaining, they will face resistance, and our history bears witness to that.”

Israeli airstrikes on vehicles south of Beirut killed 4 people, while strikes in southern Lebanon killed at least 13, state media and the Health Ministry said.

Iran war: https://t.co/GEBscM5Zz2 pic.twitter.com/6mHpjCkVis

— Sky News (@SkyNews) May 9, 2026

Lebanese officials have also charged Israel with trying to erase the Lebanese presence in southern Lebanon in a genocidal act, or ‘cultural genocide’.

This after Israeli forces have carried out demolitions in southern villages, targeting what they describe as Hezbollah infrastructure embedded in civilian areas.

Tyler Durden

Sun, 05/10/2026 – 11:40

Winning? Do We Need To Understand UBI

Winning? Do We Need To Understand UBI

Submitted by Peter Tchir of Academy Securities

Winning? Do We Need To Understand UBI

Iran (and the potential for a deal) has continued to move markets. As the 30-year bond rose above 5% earlier this week, we got news that we have a new approach to resolving the conflict – a one-page MOU. Markets (ex-oil) rallied around various “deal” headlines all week.

Spider, Bret, and I spent some time discussing this on Friday’s Podcast – The U.S. Proposal to End the War (also available on Spotify and iTunes).

Information continues to leak out in dribs and drabs about how those negotiations are doing. There continue to be conflicting messages. In the back of my mind, I’m increasingly forced to remember what we mentioned at the start of the conflict – Iran has never won a war but has never lost a negotiation.

There was a time when that statement didn’t seem likely to be reflective of this conflict. From “unconditional surrender” to various other metrics (especially surrounding nuclear weapons capabilities) we seem to be drifting to – let’s open the Strait and figure out the rest later?

The U.S. has displayed exceptionalism on every military task that it has been asked to undertake during this conflict. While we have had a limited presence in the Strait, our maritime efforts have been successful in accomplishing the missions that have been defined. Yes, Project Freedom was short lived. Not so much because the U.S. couldn’t deal with the threat (we successfully defended ourselves against Iranian missiles, drones, and small boats), but because it became pretty clear that not many commercial vessels were ready, under current circumstances, to risk challenging Iran.

We did argue, earlier in the week, that the admin’s assertion that Iran only has a few weeks before its economy collapsed, was underestimating the Iranians. They in all likelihood have prepared for this economic pressure and likely have significant IOUs with countries like China (and possibly even crypto holdings) to survive months not weeks. A regime that will shoot 40,000 or more citizens in a week for protesting is not going to be overly concerned with “standard of living” issues. Finally, all the “hype” around the fact that Iran’s ability to store oil is running out and this is causing them to shut the pumps (resulting in long-lasting damages) seemed “optimistic” at best. Iran has been decreasing the pressure, reducing the flow, and giving more leeway to when their reservoirs fill up. They also have the ability to just pump oil back onto the sand (and there are some reports of oil slicks in the Gulf). So, yes, if they left their facilities on full pressure, and were worried about “dumping” oil, it might be a week or two before irreparable damage is done. But they aren’t doing that. Also, according to many in the oil industry, other countries in the region are employing the same tactics. It isn’t just Iran that faces an inability to load oil onto transportation systems (pipelines or tankers). Much of the region faces similar challenges from the inability/unwillingness to transit the Strait.

A deal would be good, but a good deal would be better.

We discuss our views, options, and even highlight a couple of possibly great outcomes in the podcast (linked above), but we do seem to be drifting towards expediency rather than something more comprehensive.

I am still in the camp that the U.S. will once again become frustrated with Iran and launch another set of attacks, to truly push this conflict to a conclusion that leaves the world much safer.

Do We Need to Understand UBI?

With the release of some formerly classified information, I probably should be talking about UFOs, but somehow I’m here thinking about UBI. UBI or Universal Basic Income is a topic I haven’t paid much attention to.

It reminds me a bit of some other economic theories that I paid little attention to, without doing much damage to my work.

Mint the Coin was a movement “predicting” or “encouraging” the government to mint a trillion dollar coin to avert the debt ceiling. It would get some traction periodically and every once in a while made me wish I spent some time even thinking about this “absurd” (in my opinion) “solution” to our debt ceiling.

Brexit. Yes, Brexit eventually happened, but it took so long to play out (as does everything in Europe including their “inevitable” adoption of ProSec ) that it was at best an undercurrent of markets, and I would argue (as someone who largely ignored it), not an undercurrent to the global economy. Important for the U.K. for sure, but I think I saved myself a lot of time and effort by largely ignoring it.

The point here is that I’ve been “dismissive” of any conversation around UBI. The concept has seemed anti-capitalist and almost “un-American.” The U.S. has “safety nets” of all sorts. Every “capitalist” country has their own version of “safety nets” – some more robust than others. UBI always seemed “a step too far,” especially in the U.S., but I cannot help thinking about it, as I struggle to digest the data this week – the “hard” data as well as the anecdotal data.

For the second month in a row, we had (at least on the surface) very strong job growth – Back to Back Dingers.

If the only piece of economic data I had was the Establishment survey of jobs, I’d be pretty pumped for the economy.

But that is NOT the only piece of data we have. There are so many ways I could express concern, that it would take too long to write, and would become repetitive, so I will stick to what some other people said recently. Here are “paraphrased” comments that caught my attention:

Recession-level demand slump in North America. (Whirlpool)

Consumer sentiment is certainly not improving, and it may be getting a little bit worse. (McDonald’s)

Consumers are literally running out of money toward the end of the month. (Kraft Heinz)

There are many stocks we can look to, in order to gauge the state of the consumer. HD (Home Depot), for example, is almost 25% off of its high from last October. LOW (Lowe’s) is off 20% from its high set in February. That tells me there is something off with the consumer (rather than something company specific). If people are not spending money on home improvement, that indicates a lack of optimism from consumers.

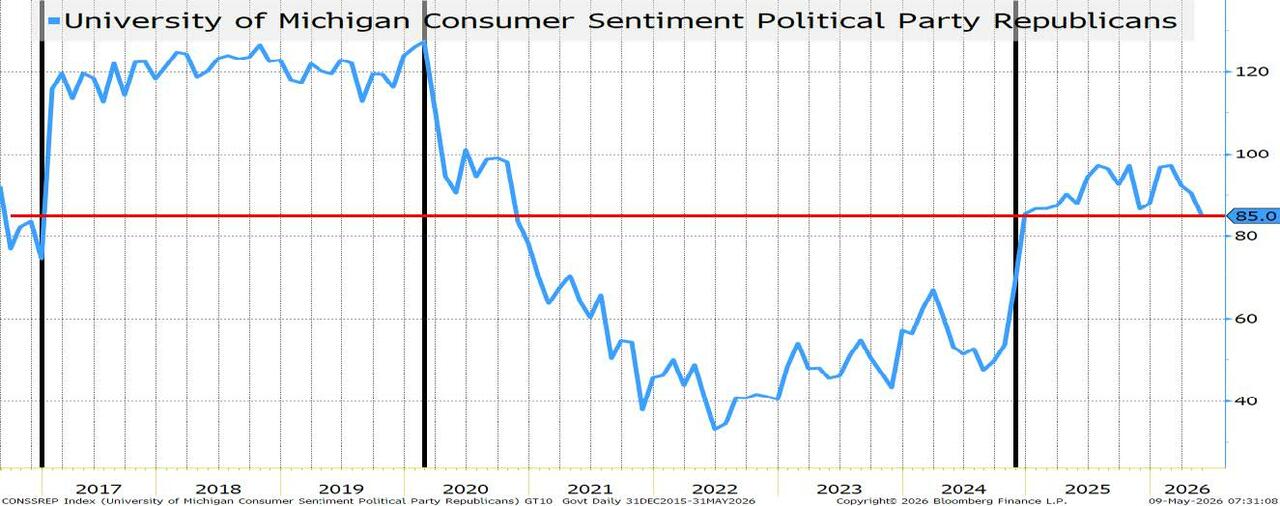

Since I’m not a huge fan (or even a small fan) of the various CONsumer CONfidence surveys, I feel almost bad referencing it for the 2nd month in a row. Yes, it hit all-time lows, but that isn’t what caught my eye. Okay, it caught my eye, but everyone saw that. This is the chart from that survey that I find most interesting.

Here we get the responses from the Republicans for the University of Michigan Survey. It is 85. Far above the 48.2 headline number (which is the one that set a new record low). At 85 it is well above the lows during the Biden administration.

But this is the lowest Republican sentiment while President Trump has been in office.

That, to me, is important.

I have never understood how or why Republicans and Democrats would have such a different view of the economy. Maybe, if somehow, it was picking up differences in regional economies (areas where Republicans reside are booming, and vice versa), but it seems counterintuitive that the difference on economic outlook is so tied to party. Which is why I largely ignore this entire CONsumer CONfidence set of data, but the recent erosion in the chart makes me think twice.

AI versus Affordability

I really, really, want to bring up the line from Apocalypse Now – “Charlie Don’t Surf.” Maybe I’ve been spending too much time fixated on the war.

But I really want to write something along the lines of “AI Don’t Spend.” Or “one person’s expense, is another person’s revenue.”

So far any concerns about job losses due to AI don’t seem to be showing up in the jobs data. This is likely because:

The buildout of AI requires a lot of hiring. Not just making the components necessary to run a data center (chips, cooling, electricity, etc.) but also the actual construction of the data centers and all the “picks and shovels” around data center construction.

AI, in most cases, seems to have slowed hiring, rather accelerated the firing of employees. Attrition is playing the biggest role in adjusting headcount to offset AI spending (and productivity, to the extent it is being productive).

I’m stuck believing that the pressure on the consumer, so far, is primarily due to affordability, rather than job losses.

Concern about the future of jobs or pay may be influencing consumer sentiment and spending (I’m going to keep making T-Reports so confusing that AI cannot replicate them any time soon), but the bulk of the issue is affordability right now. What the heck will happen if job losses, especially due to AI, increase?

Let’s use some “water” analogies here (to try to link into the surf comment).

A rising tide lifts all boats. This is the sort of economic growth we are all used to. Everything does better. It doesn’t really matter what you do, or where you are, you do better. This economy does not currently have that “vibe” to me.

We see who is swimming naked when the tide goes out. Always a good one, but not sure how relevant it is to today’s economy. I think we are more about all boats not lifting, than we are about a tide going out.

If the water is rising and you are anchored to the ground, you are in trouble. Okay, I just made that one up. But we’ve all seen it in movies.

The water level is rising in a room, where the “hero” cannot get out. There is real fear. If there wasn’t some fear of this, Harry Houdini probably wouldn’t be as famous as he is.

I think this latter analogy may be the most apt:

The water is rising (affordability). More and more people are getting sucked into the daily, weekly, monthly, and annual struggle of making ends meet. If we want to go down the “k”- shaped analogy, more and more of the k is underwater. Maybe it was only the lower leg of the k that was struggling, but as the water rises (affordability), more of the k is being covered. We may well be into the upper leg of the k. I guess we better hope that is a K rather than a k where the upper leg is long and goes high, but I’m concerned it is not (I still stick with the i-shaped economy, where a handful is doing extremely well and the rest of us are seeing the water rise).

On that pleasant note…

Bottom Line

Anyone with a job that can be disrupted by AI should own AI stocks as a “hedge.” I cannot tell if I’m being facetious or serious, but it is something to think about.

It is too early to spend a lot of time trying to understand how UBI would work, but I suspect we will start hearing more about this rather than less as affordability remains an issue. The issue will decline once we get a deal with Iran, but the affordability issue is not going away (I restrained myself from calling it a crisis, but…).

On credit, I continue to think credit will do fine and like owning private credit as marks seem to be adjusting to a new reality. More for a “trade” than being married to the position. I will get a detailed report out this week, as I am actually not on the road this week!

On rates, our more detailed analysis from last weekend’s Living in an AI World stands. Largely rangebound, with 4.35% to 4.4% as the middle of the range on 10s.

Continue to focus on ProSec themes, here and in Europe. If we get a deal, expect the admin to turn more attention to things like electricity production and the processing, refining, and smelting of commodities (as well as their extraction). A lot is being done in the background, but the President remains a key driver and while his attention has been diverted, we haven’t seen as much progress on ProSec as we’d like (away from domestic-focused chip manufacturing). That should change!

Thanks for everything and best wishes to all the moms out there! Hope you and your family and friends have an amazing day today! (Hopefully, every day is amazing, but today everyone should focus on the importance of family, more than the average day, where things like “work” get in the way).

Tyler Durden

Sun, 05/10/2026 – 11:05

https://www.zerohedge.com/markets/winning-do-we-need-understand-ubi

Iran Responds To US Peace Proposal, As Ayatollah Meets With Top General To Discuss ‘Readiness’

Iran Responds To US Peace Proposal, As Ayatollah Meets With Top General To Discuss ‘Readiness’

Summary

Iran responds Sunday to US peace proposal, finally submitting something official to Pakistan. Details not initially disclosed.

IRGC new warning: will unleash “heavy attack” on US bases in region if more Hormuz aggression persists.

The still not publicly seen Supreme Leader has met with a top Iranian military commander to talk ‘readiness’ against US-Israeli aggression.

US x Iran permanent peace deal by June 30, 2026?

Yes 52% · No 49%

View full market & trade on Polymarket

* * *

Iran Finally Responds To US

After days of waiting, Iran has submitted its response to the latest US peace proposal to mediator Pakistan, despite the recent flare-up in renewed exchanges of fire in the contested Strait of Hormuz this past week.

“Iran has submitted its response to the latest US proposal to end 10 weeks of war, the state-run Islamic Republic News Agency reported on Sunday, without providing any further details,” Bloomberg confirms in a fresh headline. “Tehran hasn’t yet given any public indication it would accept President Donald Trump’s plan that stipulates Iran permits passage through the Strait of Hormuz and Washington ends its blockade on Iranian ports in the next month.”

IRAN REPLY TO US PROPOSAL INCLUDES ENDING WAR ON ALL FRONTS: TV

This comes as Qatar’s PM has warned Iran that using the Strait of Hormuz as a pressure card, to choke the global economy, “would only lead to deepening the crisis” – and amid reports there could still be sporadic attacks on Gulf countries like the UAE. According to more of the limited details:

Sources in both camps have told Reuters the latest peace efforts are aimed at a temporary memorandum of understanding to halt the war and allow traffic through the Strait of Hormuz while they discuss a fuller deal, which would have to address intractable disputes such as Iran’s nuclear program.

The latest from Iran’s president:

President Trump told Fox News days ago, “They want to make a deal. We’ve had very good talks over the last 24 hours, and it’s very possible that we’ll make a deal.” He had said if this happens “it’ll be over quickly” and oil prices will plummet.

IRGC Fresh Warning on US Bases

Iran’s Islamic Revolutionary Guard Corps (IRGC) has warned any attack on Iranian oil tankers and commercial ships will be met with assaults on US bases and “enemy ships” in the region, Al Jazeera reports.

“Warning! Any aggression against the oil tankers and commercial vessels of the Islamic Republic of Iran will be met with a heavy attack on one of the American centers in the region and the enemy’s ships,” the IRGC Navy said in the statement.

“Iran will no longer allow passages that are harmful to its interests”

Brigadier General Akrami Nia, the spokesman of the Iranian army, says countries that comply with US sanctions against Iran will surely have problems crossing the Strait of Hormuz. pic.twitter.com/6EZ6NWsZse

— Press TV 🔻 (@PressTV) May 10, 2026

Tehran is accusing the US side of severely violating the ceasefire earlier this week, by firing on and disabling two Iranian-flagged tankers trying to reach Iranian ports. State media reviewed of these hostile incidents:

In a statement, the spokesman for Iran’s Khatam al-Anbiya Central Headquarters said the “aggressive, terrorist and marauding US military” had targeted an Iranian oil tanker sailing from Iran’s coastal waters near Jask toward the Strait of Hormuz, as well as another vessel entering the strategic waterway near the UAE port of Fujairah.

The spokesman also said civilian areas along the coasts of Bandar Khamir, Sirik and Qeshm Island came under aerial attacks carried out “with the cooperation of some regional countries.”

The IRGC further said it will respond “powerfully and without the slightest hesitation” to any aggression or attack. Indeed there are reports that during the past week’s skirmishes Iran fired on three US warships seeking to exit waters of Iran’s coast.

Ayatollah Meets With Military Commander

We reported earlier that in an official update Iran said that Supreme Leader Mojtaba Khamenei had been ‘moderately injured’ but is recovering, and he had met with the president of the Islamic Republic. On Sunday he also met with a top military commader, per state Mehr, which writes: “In a meeting with Leader of the Islamic Revolution Ayatollah Seyyed Mojtaba Khamenei, Commander of Khatam al-Anbiya Central Headquarters Major General Ali Abdollahi presented a comprehensive report on the preparedness of the powerful Armed Forces of the country to confront enemies’ strategic mistake.”

According to more of the state readout:

Abdollahi said “all fighters of Islam” possess high readiness in terms of morale, defensive and offensive preparedness, strategic plans, and the equipment and weaponry required to confront hostile actions by the “American-Zionist enemies.”

He warned that if the enemies commit any “strategic mistake, aggression, or invasion,” Iranian forces would respond “swiftly, intensely, and powerfully.”

The commander also assured the Leader that the armed forces would, “with full obedience” to his orders, defend “the ideals of the Islamic Revolution, our beloved land Iran, sovereignty, national interests, and the brave Iranian nation until the last breath and to the death.”

During the meeting, Ayatollah Khamenei praised the country’s armed forces and issued new directives for continuing action and confronting enemies decisively following the 40-day US-Israeli war against the country.

The Wall Street Journal wrote Saturday of the Ayatollah, “A government official claimed Khamenei, who hasn’t been seen in public since that attack, is now in good health.” However, there’s still a lot of speculation on his role in national decision-making, and over whether he will ever make a public appearance.

Tyler Durden

Sun, 05/10/2026 – 10:30

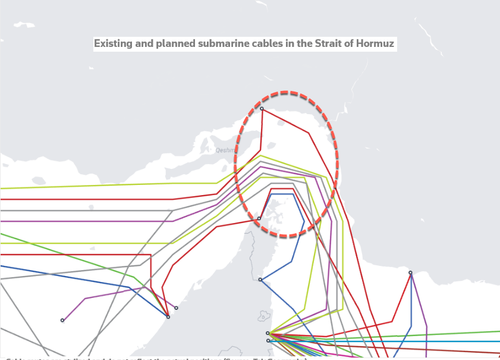

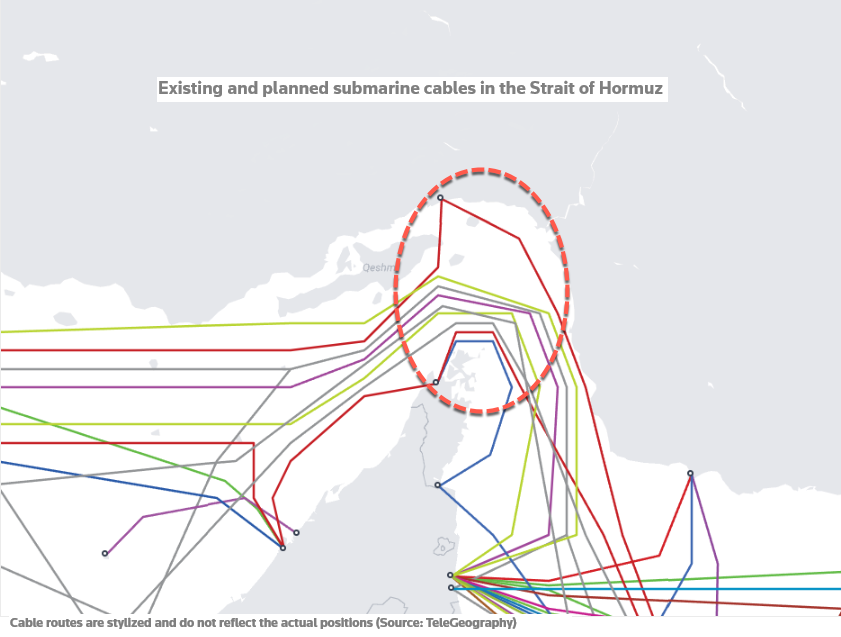

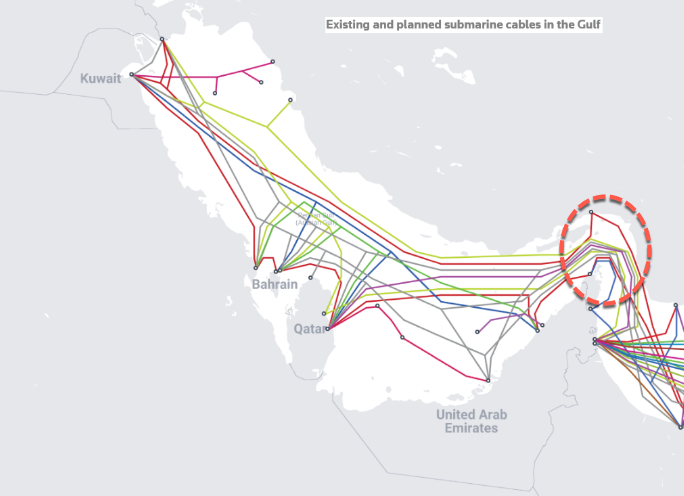

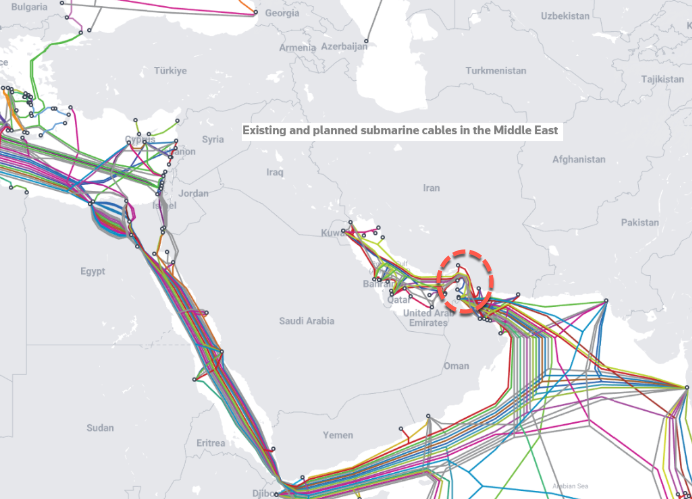

Iran-Linked Media Floats Data Tax On Hormuz Undersea Internet Cables

Iran-Linked Media Floats Data Tax On Hormuz Undersea Internet Cables

An Islamic Revolutionary Guard Corps-linked media outlet has signaled that submarine fiber-optic cables running through the Strait of Hormuz remain in Tehran’s crosshairs.

Tehran views Hormuz not only as an energy chokepoint but also as a digital chokepoint, with undersea cables beaming internet across the Gulf and into the global network.

Tasnim published an article titled “Three Practical Steps for Generating Revenue from Strait of Hormuz Internet Cables,” pointing out that Tehran must reassess how it exercises sovereignty over the strategic maritime chokepoint.

The IRGC-linked outlet said that submarine fiber-optic cables in the critical waterway facilitate more than $10 trillion in financial transactions each day, and claimed that Iran has been deprived of the economic and sovereign benefits tied to the digital economy.

Tasnim warned that any disruption, cut, or damage to these cables, whether from natural causes or ship anchors, could impose heavy losses on the world’s economy.

“These cables, which are laid on the seabed using advanced technologies such as DWDM and double-armored standards, carry the bulk of international internet traffic, cloud synchronization, enterprise virtual private networks, voice traffic, and financial-payment networks. From the perspective of the digital economy, any disruption, outage, or damage to these communications highways, whether from natural incidents or ship anchors, can cause irreparable losses,” the outlet stated.

Tasnim lists three steps for how Iran should begin imposing fees on internet traffic routed through Hormuz:

Licensing and tolls: Iran should require telecom consortia and cable operators to obtain permits for laying and operating cables through the strait, with initial licensing fees and annual renewal payments.

Iranian legal jurisdiction over tech firms: Major technology companies using the cables, including Google, Microsoft, Amazon, and Meta, should be required to operate officially under Iranian law and cooperate with Iranian technology firms, knowledge-based companies, and media entities.

Iranian control over maintenance and repair: Iran should develop the technical infrastructure to control or participate in the maintenance and repair of the cables, turning cable servicing into both a revenue stream and a sovereignty tool.

Beyond the quest to charge data fees, Tehran has already imposed fees or tolls on vessels passing through the strait.

Last week, Iran’s newly created Persian Gulf Strait Authority pushed forward with a new protocol for commercial vessels transiting the strait. It’s unclear whether the protocol will incur a fee.

However, Iranians have made “demands for payments, payments for toll fees, as we say, for those vessels to be granted permission to sail,” Dimitris Maniatis, CEO of maritime risk consultancy Marisks, told CNN.

The direct result of Tehran’s attempt to position itself as the gatekeeper of the Hormuz chokepoint, across energy, freight, and potentially digital traffic, will be to accelerate global efforts to bypass the strait. That means rerouting pipelines, tanker traffic, commercial shipping, and eventually undersea cable infrastructure away from Iran’s strait.

That effort has already started:

. . .

Tyler Durden

Sun, 05/10/2026 – 09:55

What Would Be Truly Bullish? Actually Fixing What’s Broken

What Would Be Truly Bullish? Actually Fixing What’s Broken

Authored by Charles Hugh Smith via Of Two Minds,

We’ve come to an interesting juncture in history, interesting because while we’re being assured that AI will solve all problems, including any it creates, back in the real world, AI is incapable of fixing what’s broken because too many people are getting rich off the status quo, and since the status quo is the problem, those who own / control AI will use it to maintain the status quo, guaranteeing that what’s broken spirals into irreversible breakdown.

Richard Bonugli and I discuss what’s fatally broken in a new podcast on what it will take to become Bullish (32 min).

Let’s start with what’s “obvious”: letting what’s broken fester until it implodes the status quo is not bullish, and neither is substituting delusion and denial for a realistic appraisal of what’s actually broken–the essential observe and orient steps in the OODA loop (observe, orient, decide, act).

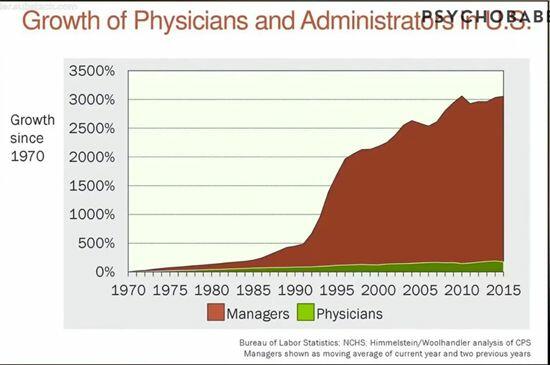

I’ve often described the two dynamics that are broken that AI can’t fix because those who own / control AI are using it to increase the asymmetrical distribution of wealth and income that are the source of breakdown. Consider healthcare. Everyone except the managers / owners / shareholders of healthcare / pharma cartels agrees healthcare is fundamentally broken and is bankrupting households, employers and the government / nation.

Those profiteering off the status quo healthcare system claim AI is going to reduce costs. They fail to mention this won’t reduce the price, it will only serve to increase their profits. Cut costs by replacing human labor with AI tools, yea, we reap even higher profits. Nobody is claiming healthcare will magically become affordable because a truly affordable healthcare system wouldn’t be as profitable because it wouldn’t be as open to exploitation, fraud, profiteering, extraction and parasitic pricing.

In the same way, AI can’t solve the other fatal dynamic–widening wealth and income asymmetry–because it’s widening the asymmetry to new extremes. The owners of AI are reaping vast fortunes while stripmining resources to run their AI data centers and laying off wage earners. Rather than fixing what’s broken in America, AI is accelerating the endgame of what’s broken.

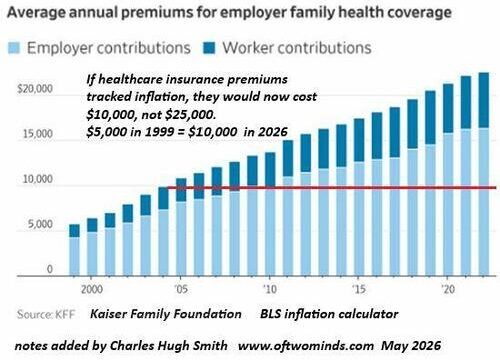

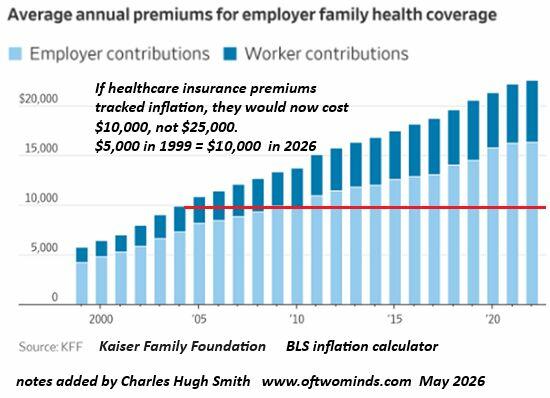

Let’s run through why increasing numbers of online comments suggest burning the whole rotten healthcare system down and starting over. Healthcare insurance–which often turn out to be a profitable facsimile of actual insurance–has more than doubled beyond the official rate of inflation. If healthcare insurance had tracked inflation, it would cost $10,000 a year for family coverage in 2026. Instead, it costs $25,000+ annually.

Diagnosis: broken.

Regardless of how you toy with statistics, the reality is administrative costs / bloat / profiteering have soared. Diagnosis: broken.

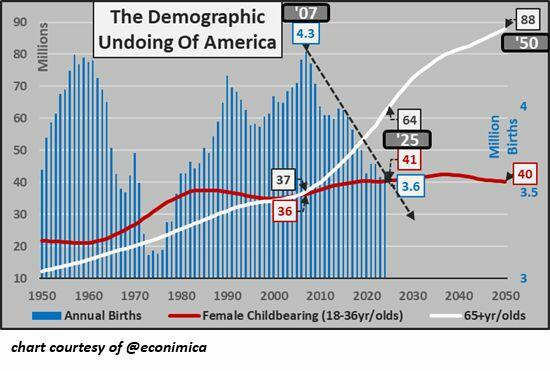

Meanwhile, back in reality, rapidly aging populations are far from their peak demand for healthcare services. Check out the white line on this chart (courtesy of @econimica) of those aged 65+. While births collapse and the workforce is pressured by AI and the soaring cost of living, millions of elderly retirees are being added to the Medicare beneficiary pool. Diagnosis: broken.

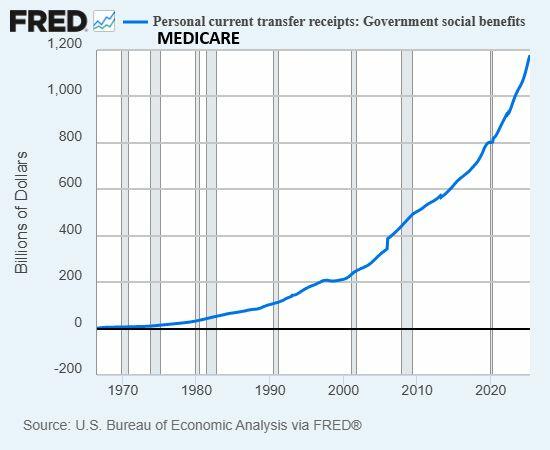

Here is the chart of Medicare costs: parabolic. It’s nice we can borrow a few trillion every year, but can we borrow $5 trillion or more every year with no consequence? Diagnosis: broken.

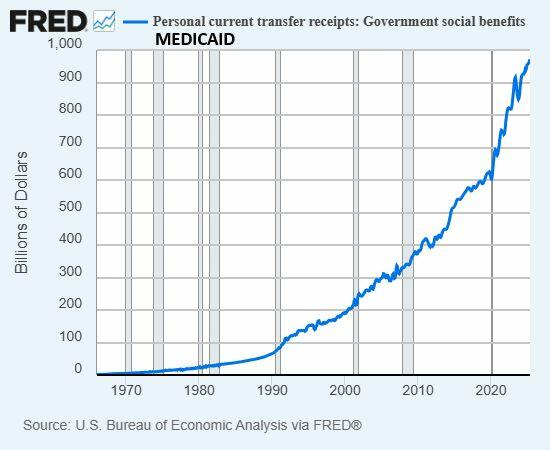

Here is the chart of Medicaid costs: parabolic. Diagnosis: broken.

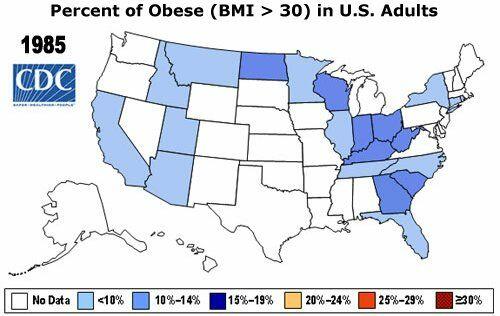

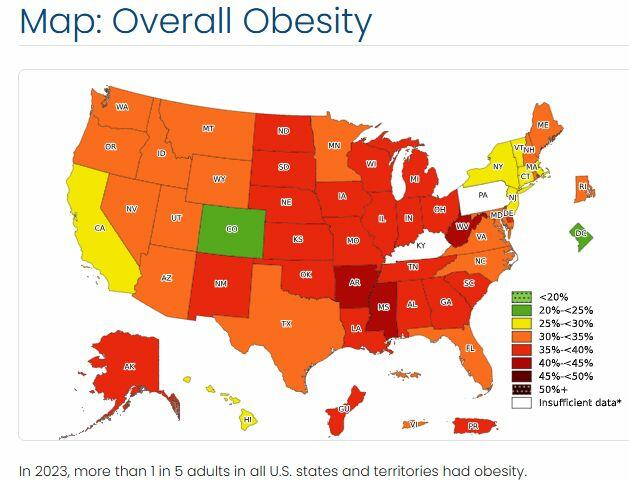

As for the health of the general populace: it’s been declining for two generations as our diet has shifted from real food made at home to ultra-processed goo and fitness has bifurcated into a thin layer of extreme fitness and a majority of the populace burdened with the complex ill health of poor diets, poor fitness and metabolic disorders.

Weight of the populace in 1985:

Weight of the populace in 2023:

Yes, now we have GLP-1 drugs that reduce weight and the diseases related to weight, but these drugs have side effects in many patients and they must be taken for life. Once the patient stops taking them, the weight returns.

Drugs that must be taken for life are not a substitute for being healthy. Healthy = not needing any medications.

Diagnosis of the healthcare system: broken. Prognosis: bifurcation: the rich will get “the finest care in the world,” and everyone else will be in a queue or denied care–basically the same result–or offered extraordinarily profitable meds and a spectrum of side effects.

What’s broken is the entire financial-economic system that distributes the pain and the gain: the pain of sharply higher costs of living and increasing financial precarity is distributed to the bottom 80% while the gains are distributed to the top 10%, with a dribble going to the cohort between 81% and 90% who own enough capital to support their claim to being “middle class.”

Note to America’s elites: when only the top 15% just below the top 5% qualifies as “middle class,” that’s not a middle class. I know, you don’t concern yourselves with such trivia: there are trillions of dollars to be reaped “solving problems” with AI.

The “problem” you can’t solve with AI is AI only “solves” the “problem” you see, which is how to increase your wealth and income before the bottom 80% awaken from the 24/7-hyped delusion that credit-asset bubbles (AI!) raise all boats and will continue to do so forever and ever.

Real life has diverged from that delusion, and the radioactive power of AI to extend that delusion has a short half-life. Refusing to recognize, much less actually fix, what’s broken hurries our collective rendezvous with consequences.

What would be bullish is actually fixing what’s broken. Promoting self-serving illusory “solutions” that only widen the asymmetries stretching the socio-economic fabric to the breaking point is not bullish.

New podcast: what it will take to become Bullish (32 min).

My book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition). Introduction (free)

Tyler Durden

Sun, 05/10/2026 – 09:20

https://www.zerohedge.com/political/what-would-be-truly-bullish-actually-fixing-whats-broken

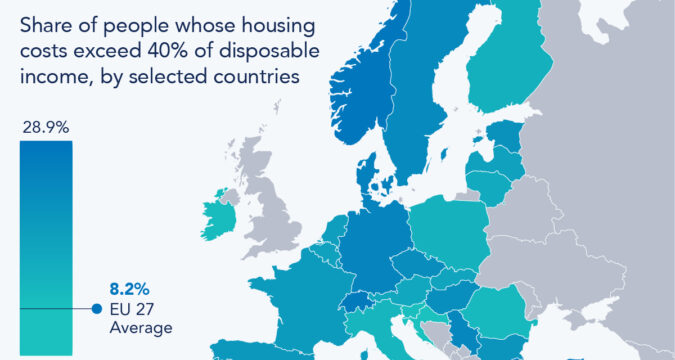

Housing Cost Pressure Varies Widely Across The EU

Housing Cost Pressure Varies Widely Across The EU

Housing affordability in the EU has an uneven spread across the continent according to data from Eurostat.

As Statista’s Jack Lillis details below, the share of people whose housing costs exceed 40% of disposable income ranges from as low as 2.4% in Cyprus to as high as 28.9% in Greece.

The EU 27 average stands at 8.2%, but this figure masks significant disparities between countries.

You will find more infographics at Statista

After Greece, Turkey appears among the most heavily burdened, while countries like Finland, Sweden, and France sit at the lighter end of the scale, suggesting considerably lower housing cost pressure on their populations.

The disparities carry real implications for labor mobility and quality of life.

In countries where housing consumes a disproportionate share of income workers in lower-wage sectors, such as the hospitality industry, could face particularly acute pressure.

Tyler Durden

Sun, 05/10/2026 – 08:45

https://www.zerohedge.com/personal-finance/housing-cost-pressure-varies-widely-across-eu

The Most Direct Social Engineering Propaganda You’ll Ever See

The Most Direct Social Engineering Propaganda You’ll Ever See

Authored by Steve Watson via modernity.news,

A new Channel 5 drama series has delivered what many are calling peak social conditioning: a classroom scene where a teacher is berated by students for failing to instantly adopt preferred pronouns and for daring to stage Shakespeare’s A Midsummer Night’s Dream.

A clip, shared widely on social media, shows an old-school drama teacher clashing with pupils over basic biology, literature, and “respecting identities.”

In the footage, a student corrects the teacher when she uses the wrong name for a student who has decided to swap genders and adopt new pronouns: “Their name is Dee now actually,” one student explains, adding “you just deadnamed them Miss.”

Channel 5 has always been wank and only MASSIVE wankers watch it!

But I think I’ve found the most Wanktarded woke TV show ever!

This wank even out wanks the BBC!

Not only is it woke wank!

It tries to shit on Shakespeare’s legacy!

This is what commie wankers do! pic.twitter.com/AUR07lfSVb

— Wanker Finder (@IfindWankers) May 5, 2026

The teacher responds: “I’m sorry. I’ve known you as Daphne for two years and can’t click a switch. I am trying.”

Another insufferable student fires back: “You shouldn’t have to try. You either see them or you don’t. I think you should apologise.”

The teacher then puts her foot in it again and states: “I just did, and am sure she can fight her own battles!”

“It’s they not she… It’s about respecting other people’s identity,” the student lectures.

Later, students challenge the Shakespeare choice, with one suggesting “There’s a consent issue. Titania is drugged before sleeping with Bottom… It’s also anti-feminist portraying women as submissive and dependent on men… to a modern audience it could be quite triggering.”

The scene perfectly captures the absurdity: instant language policing, classic literature deemed harmful for not meeting 2020s standards, and virtue-signalling students demanding deference.

This isn’t subtle. It’s overt social engineering dressed as entertainment.

This fits a well-established pattern and has been ongoing for years, as documented in the videos below:

Freedom of Information releases have confirmed the extent. UK ministers met with BBC and ITV bosses to insert pro-vaccine storylines into EastEnders, Coronation Street, and more during the pandemic, using “entertainment” to nudge compliance and shape opinion.

The BBC also used its Doctors soap to normalize the “furry” subculture, complete with lines like “You accepted their gender so why not this?”

Channel 5’s The Teacher takes it further by framing resistance to this ideology as outdated and problematic, while portraying demanding students as enlightened.

The drama reduces complex cultural heritage and language to potential “harm,” training audiences — especially younger ones — to view traditional education and biological reality as suspect. It’s not storytelling; it’s a masterclass in cultural reprogramming.

British broadcasters, taxpayer-supported or not, continue embedding these agendas. FOI documents prove coordination between government and media to “nudge” perceptions on everything from vaccines to identity. What starts as classroom lectures in fiction becomes pressure in real schools and workplaces.

This latest effort on Channel 5 strips away any pretense. It’s propaganda in plain sight — mocking Shakespeare, enforcing pronouns on demand, and shaming anyone who can’t “just flip a switch.”

Viewers are noticing. The pushback is growing as more see these shows not as harmless drama, but as tools to reshape society one scripted confrontation at a time.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Sun, 05/10/2026 – 08:10

https://www.zerohedge.com/political/most-direct-social-engineering-propaganda-youll-ever-see

Maersk CEO Warns Iran War Is A “New Wake-Up Call” For Global Trade

Maersk CEO Warns Iran War Is A “New Wake-Up Call” For Global Trade

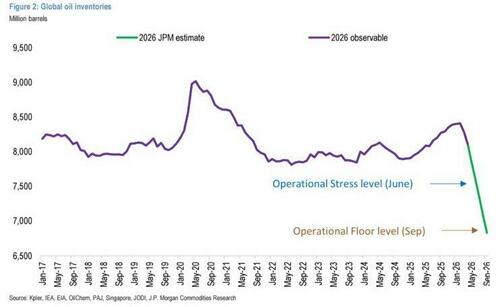

It is becoming increasingly clear that reopening the Strait of Hormuz has become a top U.S. priority (really a global priority) , as oil executives and industry insiders warn that the clock is ticking toward an energy and global trade shock if the maritime chokepoint remains closed for another month.

Frederic Lasserre, head of research at Gunvor, one of the world’s largest oil traders, warned earlier this week: “The tipping point is clearly June. This is the point at which something has to give.”

JPMorgan analysts warned that the world is spiraling toward a catastrophic cliff-edge shortage of crude oil if the maritime chokepoint is blocked for another four weeks.

Speaking to CNBC’s “Squawk Box Europe” earlier this morning, Maersk CEO Vincent Clerc warned that a “new wake-up call” has emerged beyond energy markets and that if the Hormuz chokepoint remains shuttered, it could severely impact global trade in the coming months.

Clerc was speaking to CNBC after Maersk reported a plunge in profitability and kept its guidance unchanged, but warned that the US-Iran war and the resulting Gulf energy shock are “dominant forces shaping the macroeconomic outlook, as well as the trade and logistics environment.”

Maersk wrote in its earnings report that the Iran war had introduced an “additional layer of uncertainty.”

“Currently, fragile ceasefires are in place in both Iran and Lebanon, negotiations proceed slowly, and traffic at the Strait of Hormuz remains at a near-standstill. The conflict has already weighed on sentiment. Consumer confidence deteriorated,” the shipper said.

Maersk warned that crude oil prices in the $90 to $100 per barrel range and continued Hormuz chokepoint disruption would soon begin hitting global container demand, which is still expected to grow between 2% and 4%.

It noted that the balance of risks is “on the downside and more adverse outcomes cannot be ruled out.”

“Energy and shipping disruptions in the Strait of Hormuz are rapidly reshaping global supply chains,” Maersk said in the earnings report. “After the recent tariffs on U.S. imports, the conflict represents another wake-up call to deploy new tools to make supply chains more resilient and develop new strategies to mitigate future disruptions.”

We pointed out earlier this week:

Trump’s Project Freedom Likely Triggered By Oil Market’s One-Month Countdown To Chaos

Latest as of Thursday morning:

It is increasingly evident that another month of Hormuz disruption represents a critical tipping point for energy markets and the global economy. If the conflict extends through June and the chokepoint remains shuttered, first-order impacts would likely worsen across Asia and Europe, where dependence on Gulf crude, refined products, LNG, and container flows is highest. From there, the shock could spread into fuel shortages, factory disruptions, higher shipping costs, and broader economic turmoil.

The clock is ticking.

Tyler Durden

Sun, 05/10/2026 – 07:35

https://www.zerohedge.com/geopolitical/maersk-ceo-warns-iran-war-new-wake-call-global-trade

AI Is Losing The PR Battle And The Consequences Could Be Huge

AI Is Losing The PR Battle And The Consequences Could Be Huge

Authored by Donald Kendal via The Epoch Times,

Lately, when watching high-profile sporting events like the NBA Playoffs, you may have noticed a rash of commercials for artificial intelligence (AI) companies. While average commercials strive to show off new products or services or recruit new customers, these AI commercials seem to have a different primary objective. They seem to target goodwill.

Heartwarming commercials show families bonding over AI-generated memories, where AI brings life to old family photos. Emotional voice-overs promise connection, creativity, and even nostalgia. These AI companies are trying to sell people a good reputation.

This strategy should tell us something. Companies don’t often spend millions trying to make you feel good about their brand unless they know, deep down, that you don’t trust it.

Despite hundreds of billions of dollars pouring into AI development, the industry is quietly losing the battle for hearts and minds. And sentimental advertising is not doing much to fix this problem.

Rare Bipartisan Agreement on AI

A new national survey from Marquette University Law School should give the AI industry serious pause. According to the poll, roughly 70 percent of Americans believe artificial intelligence will do more harm than good for society. Even more striking, the skepticism cuts across party lines.

Poll Director Charles Franklin put it bluntly: “It really is striking … there’s pretty much bipartisan skepticism … That’s an awful lot of partisan agreement, where we normally see Republicans and Democrats on opposite ends.”

In today’s political climate, bipartisan agreement on anything is rare. On AI, however, Americans seem united, just not in the way Silicon Valley might hope.

Worse yet is the fact that this poll supports similar findings on AI skepticism from numerous other surveys. A particularly damning NBC News poll from last month showed that AI’s net favorability rating ranked lower than nearly every other topic.

Why the Left and Right Don’t Trust AI

The industry is up against stiff headwinds in its battle for public trust.

For every story about the potential for AI curing diseases or boosting productivity, there are headlines about job displacement, algorithmic bias, and systems behaving in ways even their creators don’t fully understand.

We’ve seen AI tools generate historically inaccurate content in the name of ideological goals. We’ve seen concerns about “woke AI,” where outputs appear shaped by political preferences rather than objective reality. We’ve seen warnings from industry leaders themselves that these systems could eventually escape human control.

At the same time, public trust in the institutions building AI is already fragile.

Progressives have long been skeptical of massive corporations wielding outsized economic power. They also raise concerns about the environmental footprint of massive data centers and the risk that AI-driven productivity gains will further concentrate wealth among a small group of industry elites.

Conservatives, meanwhile, have grown increasingly wary of Big Tech after years of content moderation controversies and corporate activism tied to ESG-style frameworks.

In other words, both sides of the political spectrum are looking at the same handful of companies building the most powerful technology in human history while wondering if they can be trusted.

The Political Winds

AI companies should understand that this skepticism won’t stay confined to opinion polls. These poor poll results and negative stories in the media are giving bountiful ammunition to policymakers who are looking to target the burgeoning AI industry.

Lawmakers are beginning to float a wide range of proposals aimed at regulating artificial intelligence, some narrowly tailored, others sweeping in scope. Certain efforts are understandable, particularly those designed to prevent abuses similar to what we saw during the height of the Big Tech censorship debate.

Some proposals go further.

Some policymakers seek to impose heavy restrictions on AI, computational infrastructure, or model development. In New York, legislative proposals aim to restrict AI models from offering guidance on medical, legal, or professional issues.

A major threat to the industry is a proposal from the likes of Sen. Bernie Sanders (I-Vt.) and Rep. Alexandria Ocasio-Cortez (D-N.Y.) to impose a moratorium on the construction of AI data centers. This would essentially slow AI development in the United States to a crawl, potentially giving adversarial countries like China a great advantage in the AI race. In this scenario, the future of AI could then be left in the hands of governments that care far less about individual liberty and personal autonomy.

Earning Public Trust

If the AI industry wants to win back public confidence, it will need to do more than produce emotionally manipulative advertisements. It will need to address the concerns driving that skepticism in the first place.

Americans don’t want AI systems that nudge them toward preferred political outcomes, filter information through ideological lenses, or act as invisible referees of acceptable thought. They want assurance that these tools of the future act on objective truth rather than political ideology.

That means committing to principles that protect individual liberty and personal autonomy. It means transparency in how systems are trained and deployed. It means resisting pressure from governments, activist groups, or corporate interests to embed subjective values into systems that increasingly shape public life.

This route is possible. Elon Musk, for example, has acknowledged the importance of free expression and open inquiry in AI development. But this course needs to be fleshed out, fully implemented, and become an industry standard.

Without clear, consistent standards, suspicion will remain that there is a political agenda behind the interface.

The Fate of AI Is Not Set

The trajectory of artificial intelligence development may be inevitable, but there are many questions that need to be answered.

The best way forward for the AI industry is not through carefully crafted marketing campaigns, but a deliberate effort to earn public trust. That trust must be built on transparency, commitment to truth, and clear respect for individual liberty and personal autonomy.

If these companies want to usher in a new era of prosperity powered by AI, they must show the public that this technology will serve people, not shape or control them.

Tyler Durden

Sun, 05/10/2026 – 07:00

https://www.zerohedge.com/ai/ai-losing-pr-battle-and-consequences-could-be-huge

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}