Category: News

Crown Point’s Elle Schara, a Purdue recruit, is the 2025 Post-Tribune Girls Volleyball Player of the Year

Crown Point senior outside hitter Elle Schara has been down this road before.

One year after accumulating a multitude of honors as a junior, the Purdue recruit followed it up with an equally dominant final high school season.

“She never veered off course,” Crown Point coach Alison Duncan said. “She stayed on track and maintained her high level of motivation to be one of Indiana’s best volleyball players. Sometimes when kids receive awards junior year, and they’re recognized so highly, and they’re verbally committed and thinking about the next stage, they kind of flounder in senior year.

“Elle didn’t do that. She came in super focused, ready to go and ready to work — and still ready to become a better volleyball player and not misuse her time during her senior year. She worked on her leadership, tried to be more vocal on court, and I saw her applying different things this year. All of which is good because it means she’s thinking about how to become a better player and is getting ready for the next step.”

That step will come soon for Schara, the 2025 Post-Tribune Girls Volleyball Player of the Year, who will graduate a semester early and join the Boilermakers in January.

It has been a whirlwind for Schara, who recorded 571 kills, 389 digs and 73 aces to lead the Bulldogs (31-4) to a Class 4A regional title. She’s an All-America third-team pick by the American Volleyball Coaches Association, an Indiana Miss Volleyball finalist, an Indiana Senior All-Star, a 4A all-state first-team selection and the Duneland Athletic Conference MVP.

“I’m super proud of myself and my team,” Schara said. “None of this would’ve been possible without them. But I gave myself the week off since everything ended, and I’m just now getting back into it, preparing for college since I’m leaving in January, and trying to stay active.

“I’m super excited, obviously, because it’s an amazing opportunity. But as the time approaches, I’m getting a little more nervous.”

Schara’s teammates are excited for her too.

“She’s going to do amazing things,” Crown Point senior libero Bella Del Real said. “I can’t wait to watch her on TV. Growing up with her, being her teammate and playing next to her, she’s going to be on TV and I’m going to say, ‘That was my best friend I played volleyball with.’ It’s going to be so exciting to watch her be amazing as she always is.”

Crown Point’s Elle Schara spikes the ball against Chesterton during a Duneland Athletic Conference match in Crown Point on Thursday, Sept. 5, 2024. (Kyle Telechan / Post-Tribune)

Del Real said she’ll miss Schara’s personality as much as her play.

“She is a goofy weirdo,” Del Real said. “I don’t know how to explain it. She just does things out of nowhere you would never expect.

“You don’t see it at all when she’s playing, but at practice she was the comedian. She would crack jokes no one else would laugh at, but she would still laugh. She was just so funny, and that brought a lot to our team.”

Duncan, who noted she has coached for “a long time now,” isn’t sure anyone can replicate Schara’s on-court production.

A two-time player of the year, Schara finished her Crown Point career with a program-record 2,051 kills, including a single-season record of 577 in 2024, and also totaled 1,401 digs, 217 aces and 115 blocks. She was the driving force behind four consecutive sectional titles and back-to-back regional titles.

“I don’t know if anybody is going to be able to beat her records,” Duncan said. “Getting over 2,000 kills is a lot. I don’t know if anybody can come in and have the kind of freshman year she had that’s necessary to beat it. She’s a special athlete.”

Noah Poser is a freelance reporter.

OpenAI y Foxconn de Taiwán se asocian para diseñar y fabricar hardware de IA en EEUU

Por CHAN HO-HIM y TAIJING WU

TAIWÁN (AP) — OpenAI y el gigante electrónico taiwanés Foxconn han acordado una asociación para diseñar y fabricar equipos clave para centros de datos de inteligencia artificial en Estados Unidos como parte de planes ambiciosos para fortalecer la infraestructura de IA estadounidense.

Foxconn, que fabrica servidores de IA para Nvidia y ensambla productos de Apple, incluido el iPhone, estará codiseñando y desarrollando racks para centros de datos de inteligencia artificial con OpenAI bajo el acuerdo, dijeron las empresas en comunicados separados el jueves y viernes.

Los productos que Foxconn fabricará en sus instalaciones en Estados Unidos incluyen cableado, redes y sistemas de energía para centros de datos de IA, dijeron las empresas. OpenAI tendrá “acceso anticipado” para evaluarlos y potencialmente comprarlos.

Foxconn tiene fábricas en Estados Unidos, incluidas en Wisconsin, Ohio y Texas. El acuerdo inicial no incluye obligaciones financieras ni compromisos de compra, según los comunicados.

El fabricante por contrato de Taiwán, formalmente conocido como Hon Hai Precision Industry Co., busca diversificar su negocio, desarrollando vehículos eléctricos y adquiriendo otras empresas de electrónica para ampliar su oferta de productos.

Un elegante Model A EV fabricado por la filial automotriz del grupo, Foxtron, estuvo en exhibición en el evento del viernes.

“Este año, Model A. ‘A’, de asequible”, dijo Jun Seki, director de estrategia del negocio de vehículos eléctricos de Foxconn.

La colaboración con OpenAI también puede ayudar a Taiwán, una isla autogobernada reclamada por China, a desarrollar sus propios recursos informáticos, dijo Alexis Bjorlin, vicepresidenta de Nvidia.

“Esto permite que el conocimiento del dominio de Taiwán y los datos de tecnología clave permanezcan locales y aseguren la seguridad de los datos”, dijo.

“Esta asociación es un paso hacia asegurar que las tecnologías centrales de la era de la IA se construyan aquí”, dijo Sam Altman, CEO de OpenAI, con sede en San Francisco, en el comunicado. “Creemos que este trabajo fortalecerá el liderazgo de Estados Unidos y ayudará a asegurar que los beneficios de la IA se compartan ampliamente”.

OpenAI se ha comprometido a invertir 1,4 billones de dólares en la construcción de infraestructura de IA. Recientemente, entró en asociaciones multimillonarias con Nvidia y AMD para expandir la extensa potencia informática necesaria para apoyar sus modelos y servicios de inteligencia artificial. También está colaborando con el fabricante de chips estadounidense Broadcom en el diseño y fabricación de sus propios semiconductores de IA.

Pero sus planes de gasto masivo han preocupado a los inversores, planteando preguntas sobre su capacidad para recuperar sus inversiones y seguir siendo rentable. Altman dijo este mes que se espera que OpenAI, una startup fundada en 2015 y creadora de ChatGPT, alcance más de 20.000 millones de dólares en ingresos anuales este año, creciendo a “cientos de miles de millones para 2030″.

El precio de las acciones de Foxconn, que cotiza en Taiwán, ha aumentado 25% en lo que va del año, junto con el aumento en los precios de muchas empresas tecnológicas que se benefician de la locura por la IA.

La ganancia neta de la empresa taiwanesa en el trimestre de julio a septiembre aumentó 17% respecto del año anterior a poco más de 57.600 millones de nuevos dólares taiwaneses (1.800 millones de dólares), con ingresos de su negocio de nube y redes, incluidos los servidores de IA, contribuyendo con la mayor parte del negocio.

“Creemos que la importancia de la industria de la IA está aumentando significativamente”, dijo Liu durante la llamada de ganancias de Foxconn este mes.

“Soy muy optimista sobre el desarrollo de la IA el próximo año, y espero que nuestra cooperación con clientes y socios importantes se vuelva aún más estrecha”, agregó.

_____

Chan informó desde Hong Kong.

_____

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

The Way We Were: Future Farmers of America a popular Naperville club back in 1942

In 1942, more than three dozen students at Naperville High School were part of the Future Farmers of America. Interestingly, it appears that both Naperville North and Naperville Central high schools continue to have chapters of the club, which is now known as the FFA.

https://www.chicagotribune.com/2025/11/21/naperville-high-1942-future-farmers-america/

Papa modifica ley que permite a mujer liderar Estado de la Ciudad del Vaticano, tras nombrar a monja

Por NICOLE WINFIELD

ROMA (AP) — El papa León XIV solucionó un problema técnico el viernes en una ley del Vaticano que se volvió problemática luego que el papa Francisco nombrara a la primera mujer en dirigir la Gobernación del Estado de la Ciudad del Vaticano.

León enmendó la ley de 2023 para eliminar una referencia que señalaba que el presidente de la Gobernación del Estado de la Ciudad del Vaticano debía ser un cardenal.

En marzo, Francisco nombró a la hermana Raffaella Petrini, una monja italiana de 56 años, como presidenta del Estado de la ciudad. El nombramiento fue uno de los muchos que Francisco realizó durante sus 12 años de papado para elevar a las mujeres a puestos de toma de decisiones en el Vaticano, y marcó la primera vez que una mujer fue nombrada gobernadora del territorio de 44 hectáreas en el corazón de Roma.

Sin embargo, el nombramiento creó inmediatamente problemas técnicos y legales que no habían existido antes porque los predecesores de Petrini habían sido todos cardenales sacerdotes.

Por ejemplo, a Petrini no se le invitó a presentar el informe sobre el estado económico del Estado de la Ciudad del Vaticano en las reuniones a puerta cerrada de cardenales en primavera que precedieron al cónclave de mayo que eligió a León.

Normalmente, el cardenal-presidente del Estado de la Ciudad del Vaticano habría presentado el informe. Pero esas reuniones previas al cónclave, conocidas como congregaciones generales, son sólo entre cardenales.

Al cambiar la ley el viernes para permitir que una figura que no es cardenal presida la Gobernatura del Vaticano, León XIV sugirió que el nombramiento de Petrini no era un caso aislado. Escribió que la gobernación del territorio es una forma de servicio y responsabilidad que debe caracterizar la comunión dentro de la jerarquía de la Iglesia.

“Esta forma de responsabilidad compartida hace apropiado consolidar ciertas soluciones que se han desarrollado hasta ahora en respuesta a las necesidades de gobernación que están resultando cada vez más complejas y urgentes”, escribió León.

La oficina de Petrini es responsable de las principales fuentes de ingresos que financian las arcas de la Santa Sede, incluidos los Museos Vaticanos, pero también maneja la infraestructura, las telecomunicaciones y la atención médica para el Estado de la ciudad. La Comisión Pontificia para el Estado de la Ciudad del Vaticano, que ella dirige, es responsable de aprobar las leyes que rigen el territorio y de aprobar los presupuestos y cuentas anuales.

La Iglesia Católica reserva el sacerdocio para los hombres. Aunque las mujeres avanzaron en alcanzar puestos de alta dirección en el Vaticano durante el pontificado de Francisco, no hubo medida ni indicación de que la jerarquía exclusivamente masculina cambiará las reglas que impiden a las mujeres la ordenación ministerial.

___

La cobertura de religión de The Associated Press recibe apoyo a través de la colaboración de la AP con The Conversation US, con financiación de Lilly Endowment Inc. La AP es la única responsable de este contenido.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

Ukraine & Europe Reject Trump’s Russia Peace Plan, Prepare Emergency Call

Ukraine & Europe Reject Trump’s Russia Peace Plan, Prepare Emergency Call

By all estimates, this is the first ever US-proposed peace plan which actually demands major concessions from Ukraine, but it also seeks to provide assurances for Kiev’s future protection modelled on NATO article five, according to Axios.

Among President Zelensky’s top objectives has long been to obtain a robust US and European security guarantee, and this new 28-point plan appears to give just that:

President Trump’s peace plan for Ukraine includes a security guarantee modeled on NATO’s Article 5, which would commit the U.S. and European allies to treat an attack on Ukraine as an attack on the entire “transatlantic community,” – writes Axios.

Such a pledge could be recipe for future war, however, and that’s precisely how Moscow might see it, especially if other pressing issues of territory or military NATOization on Russia’s doorstep aren’t resolved. The security guarantee would be for up to a decade and could be renewed, according to the draft.

There are also reports that the US is already advancing a very ambitious timeline – that it wants to see the plan signed by Thanksgiving, or as soon as next week.

There are even lines for signatures on the document, indicating places for Ukraine, Russia the US, and even NATO and the EU. It’s unclear just which representatives would sign from each country or bloc, and its as yet unclear whether Putin himself must sign.

A senior Kremlin official cited in Axios said he was “optimistic” about the plan’s prospects, arguing that it aligns more closely with Moscow’s views than previous diplomatic efforts. This is especially as a large portion of the Donbas will be recognized as under Russia’s control, and the size and capability of the Ukrainian army will be scaled back, which a commitment to no foreign troops on Ukrainian soil as well.

And yet, as predicted by many, Ukraine and its European backers stand ready to rejected the plan – though it’s still only in its draft form and hasn’t been seriously negotiated over by the warring sides. Newsweek reports:

European leaders are preparing an emergency call to discuss U.S. President Donald Trump’s controversial proposal to end the war in Ukraine.

German Chancellor Friedrich Merz cancelled a scheduled appearance to join the discussion, which will also include Ukrainian President Volodymyr Zelensky, British Prime Minister Sir Keir Starmer, and French President Emmanuel Macron.

The 28‑point plan caught European capitals off guard. Leaders were not directly involved in the U.S. effort and learned the details only after the document was made public.

Indeed Ukraine wasn’t involved either, and the emerging complaint is that it too closely resembles earlier Russian talking points and proposals for ending the war.

EU High Representative Kaja Kallas said Thursday, “We have always supported a lasting and just peace, and we welcome any efforts to achieve it, but for any plan to work, Ukrainians and Europeans are needed.”

In response to the risk of peace breaking out with the US-Russia peace plan – Germany speaks of supplying long-range fire, Britain wants to send troops, and the EU expresses its opposition. pic.twitter.com/nSfNjTHD0x

— Glenn Diesen (@Glenn_Diesen) November 21, 2025

She went on to indicate her view that nothing fundamental has changed. “In this war there is one aggressor and one victim,” she said. “If Russia really wanted peace, it could have agreed to an unconditional ceasefire some time ago,” she added.

So far Ukraine has only signaled a vague ‘openness’ to examining the US plan: “The President of Ukraine outlined the fundamental principles that matter to our people, and following today’s meeting, the parties agreed to work on the plan’s provisions in a way that would bring about a just end to the war,” the Ukrainian presidential office has said.

In the meantime, European leaders are making their objections known one by one, and roadblocks are fast being erected…

All the decisions concerning Poland will be taken by Poles. Nothing about us without us. When it comes to peace, all the negotiations should include Ukraine. Nothing about Ukraine without Ukraine.

— Donald Tusk (@donaldtusk) November 21, 2025

Below is the US-Russia 28-point plan in full, as has been widely circulated in international reports:

* * *

1. Ukraine’s sovereignty will be confirmed.

2. A comprehensive non-aggression agreement will be concluded between Russia, Ukraine and Europe. All ambiguities of the last 30 years will be considered settled.

3. It is expected that Russia will not invade neighboring countries and NATO will not expand further.

4. A dialogue will be held between Russia and NATO, mediated by the United States, to resolve all security issues and create conditions for de-escalation in order to ensure global security and increase opportunities for cooperation and future economic development.

5. Ukraine will receive reliable security guarantees.

6. The size of the Ukrainian Armed Forces will be limited to 600,000 personnel.

7. Ukraine agrees to enshrine in its constitution that it will not join NATO, and NATO agrees to include in its statutes a provision that Ukraine will not be admitted in the future.

8. NATO agrees not to station troops in Ukraine.

9. European fighter jets will be stationed in Poland.

10. The U.S. guarantee:

The U.S. will receive compensation for the guarantee;

If Ukraine invades Russia, it will lose the guarantee;

If Russia invades Ukraine, in addition to a decisive coordinated military response, all global sanctions will be reinstated, recognition of the new territory and all other benefits of this deal will be revoked;

If Ukraine launches a missile at Moscow or St. Petersburg without cause, the security guarantee will be deemed invalid.

11. Ukraine is eligible for EU membership and will receive short-term preferential access to the European market while this issue is being considered.

12. A powerful global package of measures to rebuild Ukraine, including but not limited to:

The creation of a Ukraine Development Fund to invest in fast-growing industries, including technology, data centers, and artificial intelligence.

The United States will cooperate with Ukraine to jointly rebuild, develop, modernize, and operate Ukraine’s gas infrastructure, including pipelines and storage facilities.

Joint efforts to rehabilitate war-affected areas for the restoration, reconstruction and modernization of cities and residential areas.

Infrastructure development.

Extraction of minerals and natural resources.

The World Bank will develop a special financing package to accelerate these efforts.

13. Russia will be reintegrated into the global economy:

The lifting of sanctions will be discussed and agreed upon in stages and on a case-by-case basis.

The United States will enter into a long-term economic cooperation agreement for mutual development in the areas of energy, natural resources, infrastructure, artificial intelligence, data centers, rare earth metal extraction projects in the Arctic, and other mutually beneficial corporate opportunities.

Russia will be invited to rejoin the G8.

14. Frozen funds will be used as follows:

$100 billion in frozen Russian assets will be invested in US-led efforts to rebuild and invest in Ukraine;

The US will receive 50% of the profits from this venture. Europe will add $100 billion to increase the amount of investment available for Ukraine’s reconstruction. Frozen European funds will be unfrozen. The remainder of the frozen Russian funds will be invested in a separate US-Russian investment vehicle that will implement joint projects in specific areas. This fund will be aimed at strengthening relations and increasing common interests to create a strong incentive not to return to conflict.

15. A joint American-Russian working group on security issues will be established to promote and ensure compliance with all provisions of this agreement.

16. Russia will enshrine in law its policy of non-aggression towards Europe and Ukraine.

17. The United States and Russia will agree to extend the validity of treaties on the non-proliferation and control of nuclear weapons, including the START I Treaty.

18. Ukraine agrees to be a non-nuclear state in accordance with the Treaty on the Non-Proliferation of Nuclear Weapons.

19. The Zaporizhzhia Nuclear Power Plant will be launched under the supervision of the IAEA, and the electricity produced will be distributed equally between Russia and Ukraine — 50:50.

20. Both countries undertake to implement educational programs in schools and society aimed at promoting understanding and tolerance of different cultures and eliminating racism and prejudice:

Ukraine will adopt EU rules on religious tolerance and the protection of linguistic minorities.

Both countries will agree to abolish all discriminatory measures and guarantee the rights of Ukrainian and Russian media and education.

All Nazi ideology and activities must be rejected and prohibited.

21. Territories:

Crimea, Luhansk and Donetsk will be recognized as de facto Russian, including by the United States.

Kherson and Zaporizhzhia will be frozen along the line of contact, which will mean de facto recognition along the line of contact.

Russia will relinquish other agreed territories it controls outside the five regions.

Ukrainian forces will withdraw from the part of Donetsk Oblast that they currently control, and this withdrawal zone will be considered a neutral demilitarized buffer zone, internationally recognized as territory belonging to the Russian Federation. Russian forces will not enter this demilitarized zone.

22. After agreeing on future territorial arrangements, both the Russian Federation and Ukraine undertake not to change these arrangements by force. Any security guarantees will not apply in the event of a breach of this commitment.

23. Russia will not prevent Ukraine from using the Dnieper River for commercial activities, and agreements will be reached on the free transport of grain across the Black Sea.

24. A humanitarian committee will be established to resolve outstanding issues:

All remaining prisoners and bodies will be exchanged on an ‘all for all’ basis.

All civilian detainees and hostages will be returned, including children.

A family reunification program will be implemented.

Measures will be taken to alleviate the suffering of the victims of the conflict.

25. Ukraine will hold elections in 100 days.

26. All parties involved in this conflict will receive full amnesty for their actions during the war and agree not to make any claims or consider any complaints in the future.

27. This agreement will be legally binding. Its implementation will be monitored and guaranteed by the Peace Council, headed by President Donald J. Trump. Sanctions will be imposed for violations.

28. Once all parties agree to this memorandum, the ceasefire will take effect immediately after both sides retreat to agreed points to begin implementation of the agreement.

Tyler Durden

Fri, 11/21/2025 – 08:35

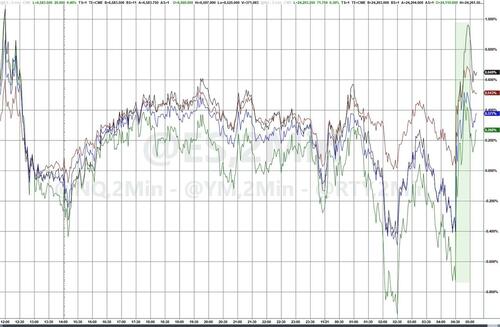

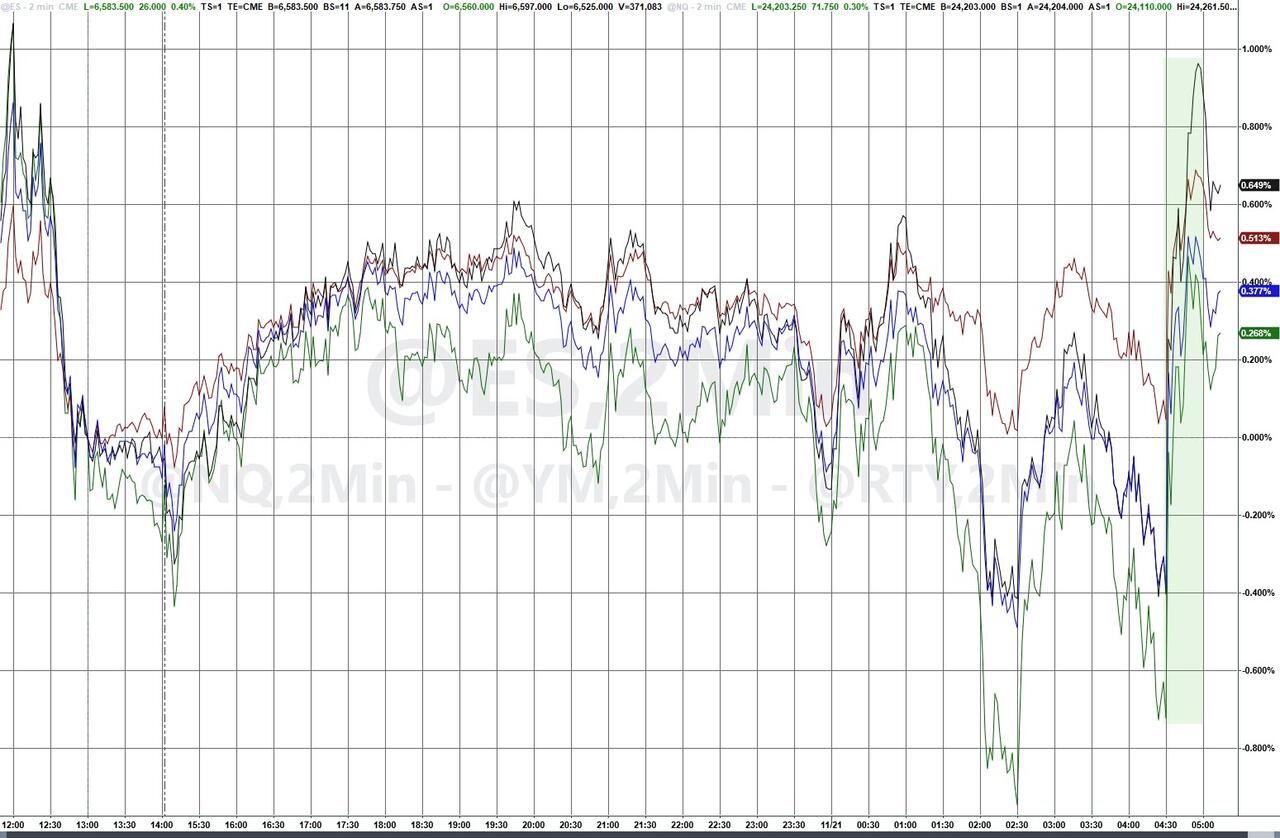

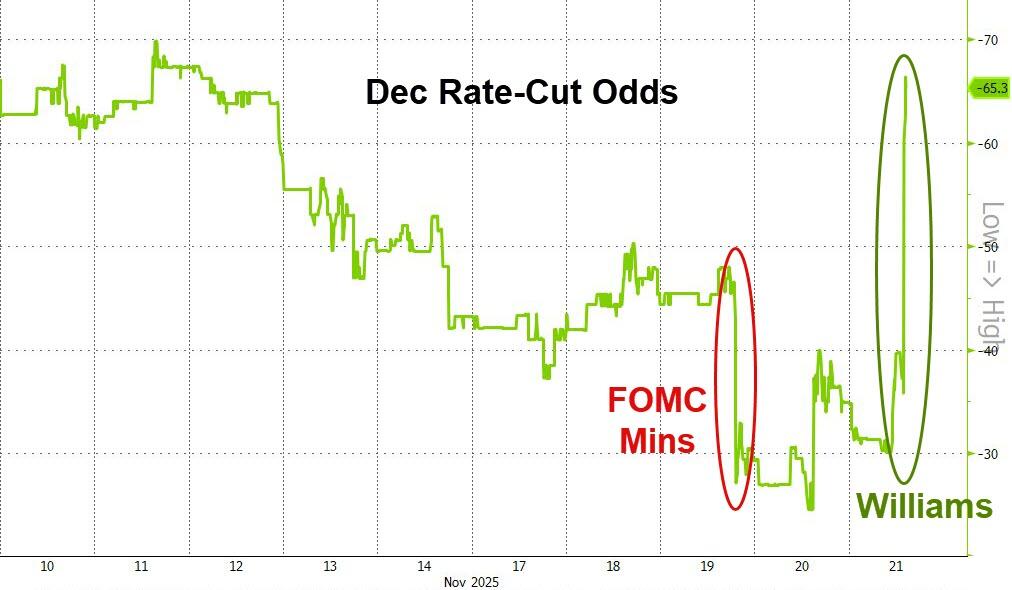

Stocks Rebound As Fed’s Williams Sparks Surge In Rate-Cut Odds

Stocks Rebound As Fed’s Williams Sparks Surge In Rate-Cut Odds

After an ugly overnight session, US equity futures are back in the green this morning following dovish comments from Fed Vice-Chair Williams…

In the text of a speech he delivered Friday in Santiago, Chile, Williams said downside risks to employment have increased while upside risks to inflation have eased.

“I view monetary policy as being modestly restrictive, although somewhat less so than before our recent actions,” he said.

“Therefore, I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral, thereby maintaining the balance between the achievement of our two goals.”

Additionally, Williams noted he was more worried about employment than inflation:

“My assessment is that the downside risks to employment have increased as the labor market has cooled, while the upside risks to inflation have lessened somewhat,” Williams said in his speech.

“Underlying inflation continues to trend downward, absent any evidence of second-round effects emanating from tariffs.”

That sent rate-cut odds soaring higher…

Amid the most fractured Fed we can remember (exposed by the Minutes released this week), we are surprised that one man’s comments can drive such a surge in the market, but then again, we have argued that very recent market pressure has been aimed at forcing The Fed’s hawks back to the table.

Tyler Durden

Fri, 11/21/2025 – 08:21

https://www.zerohedge.com/markets/stocks-rebound-feds-williams-sparks-surge-rate-cut-odds

Perú extiende por 30 días el estado de excepción para enfrentar la delincuencia

Associated Press

LIMA (AP) — Perú extendió el viernes por otros 30 días un estado de excepción para enfrentar la creciente delincuencia, en especial los asesinatos y extorsiones, en la capital y el puerto cercano de El Callao.

La medida restringe derechos constitucionales y permite a la policía ingresar a las viviendas o detener a cualquier persona. También se prohíben las reuniones masivas, aunque desde hace un mes se han producido protestas contra el mandatario interino José Jerí y los mineros informales han tomado las calles para pedir beneficios.

El anuncio en la gaceta oficial El Peruano indica que se prorroga el estado de excepción “para hacer frente a la criminalidad y otras situaciones de violencia”. Los militares apoyarán a la policía y el gobierno destinó 1,8 millones de dólares para financiar sus gastos en esta labor.

La noche del jueves el presidente Jerí presentó de forma adicional al Parlamento un proyecto legislativo para solicitar facultades por 60 días para legislar en temas de seguridad, lucha contra el crimen organizado y crecimiento económico.

El proyecto complementará “las acciones que se vienen ejecutando en la guerra contra la delincuencia. Pedimos al Congreso su pronto debate y votación”, escribió Jerí en su cuenta oficial de X.

El gobierno de Jerí decretó un estado de excepción el 22 de octubre, pero las extorsiones y los asesinatos no se han detenido.

Pese a que los expertos y varias marchas de protesta le han pedido al mandatario que derogue un conjunto de leyes que debilitan la lucha contra el crimen, el presidente no se ha manifestado. Al menos seis de esas leyes fueron aprobadas en el pasado con el voto de apoyo de Jerí cuando era legislador desde 2021.

Jerí sucedió en la presidencia a Dina Boluarte (2022-2025) quien fue destituida el 10 de octubre luego de que la coalición de partidos políticos que la respaldaban le quitaron su apoyo. Jerí, entonces líder del Parlamento, la reemplazó con el apoyo de los mismos partidos que protegían a Boluarte.

Los asesinatos subieron de 676 casos en 2017 a 2.082 en 2024, mientras las denuncias por extorsión aumentaron de 2.305 en 2020 a 21.746 el año pasado, según datos de la fiscalía.

Jaxson Davis is a top-100 prospect. But the ‘best player on the court’ wants Warren to be the best too.

It would be a mistake to assume Warren junior point guard Jaxson Davis can’t aim much higher.

As Davis, the first sophomore to win Mr. Basketball of Illinois, gets back in the driver’s seat for the Blue Devils, staying in neutral isn’t possible.

“I’ve been building confidence the last couple of years, and I would say I’ve been a leader for my team,” he said. “But I feel like I have to lead more and more.

“When I play, I like to think I’m the best player on the court, but now I want to focus on bringing my team with me.”

Davis already led Warren (27-11) to the Class 4A state championship game in March, but he hasn’t forgotten that Benet pulled out a 55-54 win.

“That’s never going to leave my mind,” Davis said. “I’m always going to remember that we were right there at the end.

“For now, I’m just staying in the moment and helping build this team block by block. If we’re able to go and win it this year, that would make me feel much better.”

Davis will be leading a much different team this season. The only other starter returning for the Blue Devils is senior guard Braylon Walker, although senior forward Avonn King and senior guard Javin Griffin played last season.

Of course, the 6-foot-1 Davis is the engine. A consensus top-100 prospect who is ranked No. 1 in the state by 247Sports with offers from DePaul, Illinois, Indiana, Iowa, Marquette, Michigan, Northwestern and Purdue, among others, Davis averaged 19.4 points, 6.1 assists, 4.4 rebounds and 2.8 steals last season.

He had 27 points and seven steals in Warren’s 66-49 win over Rich Township in the state semifinals and nearly recorded a triple-double with 19 points, seven rebounds and eight assists in the state final.

“Already this year, it looks like he has a different focus level,” Warren coach Zack Ryan said. “Every day, he comes in with the same attitude. Some of that comes with maturity.

“But he wins every single sprint. The first week of practice was some of the best practices he’s had. It’s not just how he’s playing, but how he’s communicating with teammates.”

Davis works virtually 365 days each year to ensure he’s at the top of his game, but it’s essential that his teammates are at their best as well.

“His game is more mature, and he’s more of a vocal leader,” Walker said. “You can see him getting guys in the right spots in practice, and he’s like a second coach on the floor, especially with both he and I knowing the offense like the back of our hands.”

Warren’s Jaxson Davis, right, guards Waukegan’s Carter Newsome during the Class 4A Waukegan Sectional championship game on Friday, March 7, 2025. (Mark Ukena / News-Sun)

Davis’ around-the-calendar training also includes AAU tournaments, but even those can’t match the four days he spent at USA Basketball’s men’s junior national team minicamp in Colorado Springs, Colorado, in October.

Davis came away from those sessions feeling better than ever about his game.

“It was amazing being around the top players in the country,” he said. “Everything felt different because everyone was elite. Everything was harder, but the floor was actually more open, and things flowed really easily. I felt like I belonged.”

Being invited to participate in the minicamp is yet another honor for Davis, but he also considers the experience important for his growth.

“The biggest difference between national players and local is that national guys are so athletic,” he said. “You have to be really efficient with every movement, get to the point right away. They know how to use angles, so shot fakes are important. Hopefully, I’ll get asked back.”

Warren’s Jaxson Davis (1) takes the ball to the basket against Lake Forest’s Hudson Scroggins during a North Suburban Conference game in Lake Forest on Friday, Jan. 24, 2025. (Mark Ukena / News-Sun)

The next USA Basketball camp will be held during the NCAA Men’s Final Four. In the meantime, Davis has work to do as he and his teammates tip off the season with two games in Rockford next weekend.

“My voice is big for them, and they believe in me,” Davis said. “So then now it’s my responsibility to lift them up. We’ll see where it leads us.”

Steve Reaven is a freelance reporter.

https://www.chicagotribune.com/2025/11/21/basketball-warren-jaxson-davis/

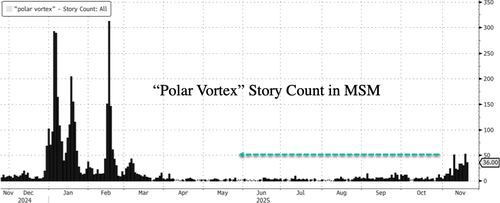

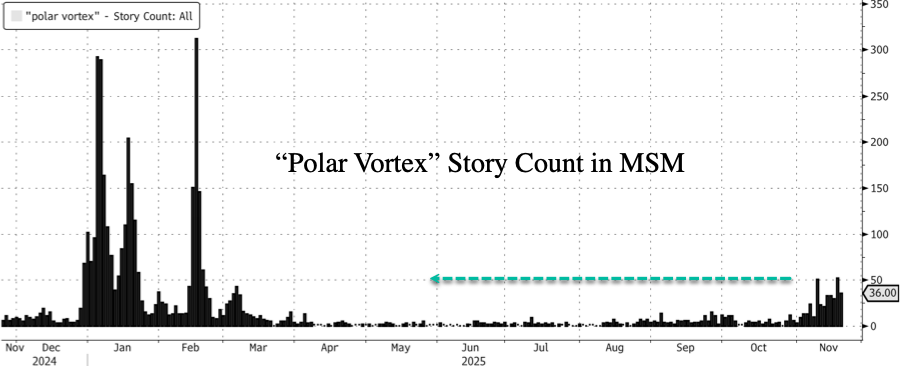

Stratospheric Warming Sparks Goldman Warning Of Looming U.S. Polar Vortex

Stratospheric Warming Sparks Goldman Warning Of Looming U.S. Polar Vortex

We began this week by publishing a weather note on the latest weather models, warning of an incoming winter cold blast that will sweep across parts of the Lower 48 during the holiday Thanksgiving week.

You might have noticed that the term “polar vortex” has been popping up across the news cycle in recent days, with headline volume (via Bloomberg data) surging to its highest level since early March as another cold blast is expected across the eastern U.S.

MSM headlines include:

CNN: The polar vortex is about to bring a wild weather pattern change

The Washington Post: An unusual phenomenon is likely to cause a frigid December in the U.S.

The incoming cold blast has even caught the attention of Goldman analyst Ranald Falconer, who informed clients about the incoming Arctic blast across the eastern and central U.S. for the next two weeks:

On the gas and PMI power front, Henry Hub sold off into the close yesterday but rallying again now; the EIA gas storage numbers showed the first of the winter withdrawals {DOENUSCH Index}. Weather fronts look to be keeping cold air across almost all of the east and central/south U.S. states for the next 14 days. I would expect that to be part of the reason we have seen a $20 move in peak PMI power since mid-October. Interesting note on “severe-weather.eu” about the winter effects of La Nina conditions, where cold Pacific ocean temperature anomalies are being observed. They are confirming the type of stratospheric warming event I mentioned last week, however speaking to my gas traders that breakdown doesn’t appear as severe as previously thought, as the vortex looks to only be disrupted until early December (Strat Observe). Under La Nina conditions, the winter effects can be severe. La Nina acts to redirect the jet stream south, with persistent high pressure over the Northern Atlantic and low pressure over Canada; this in turn brings cold air under the jet stream in western Canada and north west U.S. You can see in the Marquee email note the weather patterns and vortex forecast visuals.

MNI had stated at the close yesterday that the slide in HH might have been on the back of notice from Gulf South Pipeline that pipeline exports for LNG at Freeport might be disrupted, however I can’t see any impact on deliveries on BNEF this morning (Freeport 30d avg 1.63Bcf/day). On the flow side, we have been two way in decent size clips in Jan.

Here’s what the weather community on X is saying:

Very late blog update | Thursday Weather After Dark

November 20, 2025

Canada is slowly but surely getting colder — but it’s going to take 1-2 weeks for major cold pool formation.

Post number 794:https://t.co/PQImD96qYx pic.twitter.com/zfoPxqlPoZ

— Ryan Maue (@RyanMaue) November 21, 2025

I LOVE THIS!!! pic.twitter.com/3VLwqWENmY

— Max Velocity (@MaxVelocityWX) November 20, 2025

🟢🔵 The cold blast we’ve been talking about will arrive just in time for Thanksgiving, but it’ll be relatively short-lived. 🥶

🔴Much warmer than normal temperatures look likely to return for the start of December. 🔥 pic.twitter.com/jqZ7mxcxt4

— Brady Harris (@StormCat5_) November 20, 2025

Change in CFSV2 over the last 10 days of runs for December pic.twitter.com/4eODn449uU

— The American Storm (@BigJoeBastardi) November 21, 2025

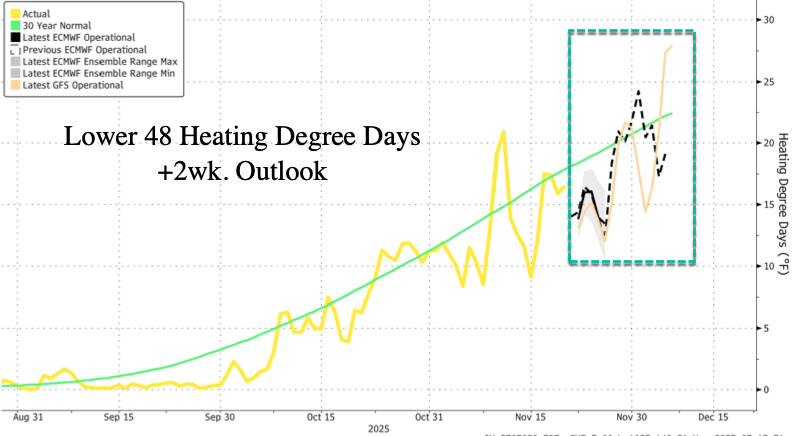

In energy markets, US NatGas futures are up and to the right.

The reason: Lower 48’s Heating Degree Days, a simple weather-based metric used to estimate how much energy people will need to heat homes and buildings, is also up and to the right.

Global warming? Oh, right, that narrative was a big lie by globalists who gave unhinged Democrats talking points and a ‘green’ framework that then pushed climate bills to raid the U.S. Treasury that funneled taxpayer dollars into green companies and climate NGOs.

Tyler Durden

Fri, 11/21/2025 – 08:00

Man struck, killed in Glenview while crossing Milwaukee Avenue

The Glenview police and fire departments responded on Nov. 20, at about 5:35 p.m., to a report of a person struck by a car near the intersection of Milwaukee Avenue and Michael Todd Terrace, they said in a news release.

A 72-year-old man had been struck by a BMW in the southbound lanes of Milwaukee Avenue while trying to cross the street. The man, who was walking westbound, was pronounced dead at the scene, police said.

The driver of the vehicle was uninjured and

remained on scene, said the police department, which is investigating the crash with assistance from the North Regional

Major Crimes Task Force’s Major Crash Assistance Team (NORTAF MCAT).

Police asked anyone with information regarding the crash to call them at 847-901-6055.

https://www.chicagotribune.com/2025/11/21/man-struck-killed-in-glenview/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}