Category: News

Sony “Temporarily Suspends” Memory Card Orders In Japan As Global Memory Crunch Worsens

Sony “Temporarily Suspends” Memory Card Orders In Japan As Global Memory Crunch Worsens

First, Sony hiked PlayStation console prices, blaming “continued pressures in the global economic landscape.” Now, Sony Japan is warning that the global memory shortage has become severe enough to force a temporary halt to new orders for memory cards, as supply can no longer keep up with production needs.

“Due to the global shortage of semiconductors (memory) and other factors, it is anticipated that supply will not meet demand for CFexpress memory cards and SD memory cards for the foreseeable future,” Sony wrote in a press release.

Sony explained that, due to the memory shortage, it has “decided to temporarily suspend the acceptance of orders from our authorized dealers and from customers at the Sony Store.”

The suspension covers Sony’s CFexpress Type A cards in 240GB, 480GB, 960GB, and 1.92TB sizes, as well as CFexpress Type B cards in 240GB and 480GB. It also affects Sony’s high-end SDXC/SDHC lineup, including 64GB, 128GB, and 256GB TOUGH models, as well as SF-M and SF-E series cards ranging from 64GB to 512GB.

What this suggests is that even some of the largest consumer electronics companies are not immune to the global memory shortage, which is rippling across the world due to surging demand from data centers.

In February, TrendForce raised its Q1 2026 DRAM contract price forecast to 90%-95% quarter-over-quarter, while forecasting NAND flash prices would jump 55%-60% over the same period. Phison’s CEO warned the NAND shortage could force some consumer electronics companies to shutter production lines this year.

Last week, Sony was forced to raise prices on PlayStation consoles, which infuriated some gamers.

“Hot take but I think things should get cheaper the more old that they are, crazy idea,” one X user said.

We told readers in late January: “If you want to buy any consumer goods, PCs, or smartphones … do it now, as it is for sure all the prices will be increased. Take an average PC, for example. The ratio of memory chips in the BoM [bill of materials] cost has increased from some 15% to almost 40%.”

There is hope: We detailed last week that “Google’s DeepSeek Moment,” introducing TurboQuant, sent memory stocks spiraling lower because its compression algorithm for large language models and vector search engines shrinks the amount of memory needed (report here).

* * * With all this creatine malarkey, don’t forget about SURVIVAL

Tyler Durden

Mon, 03/30/2026 – 11:25

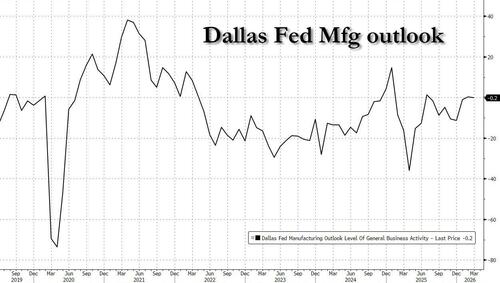

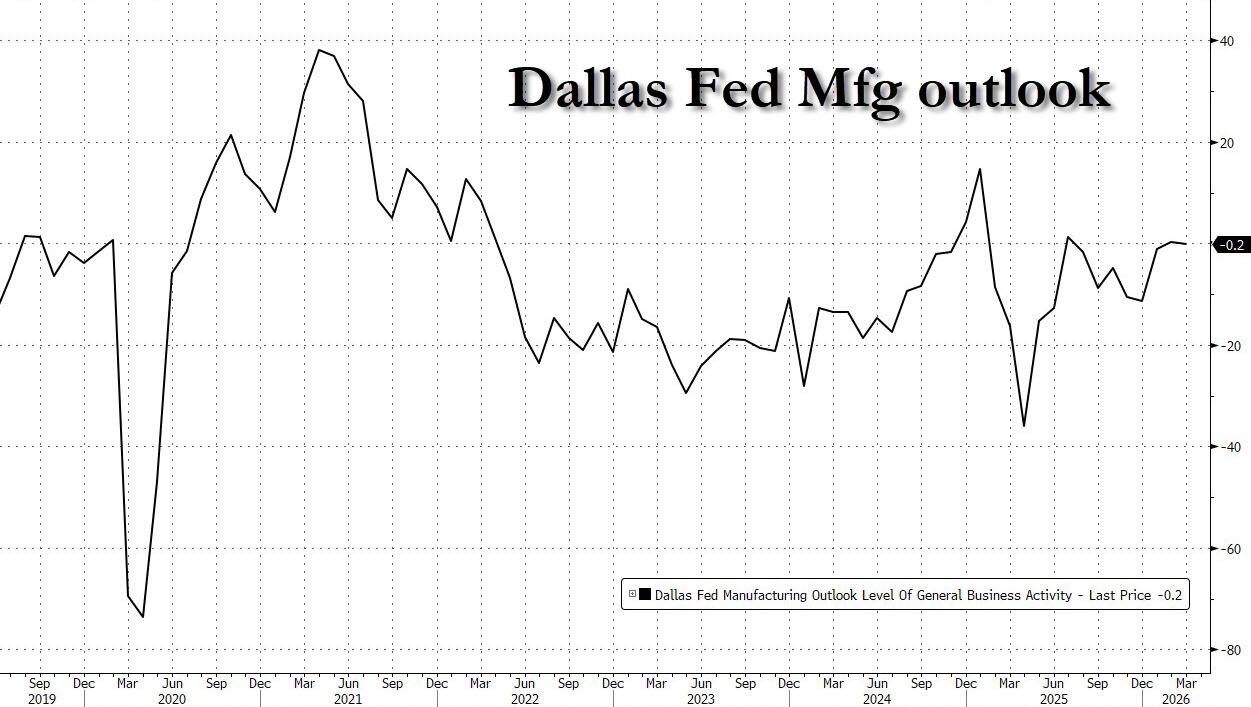

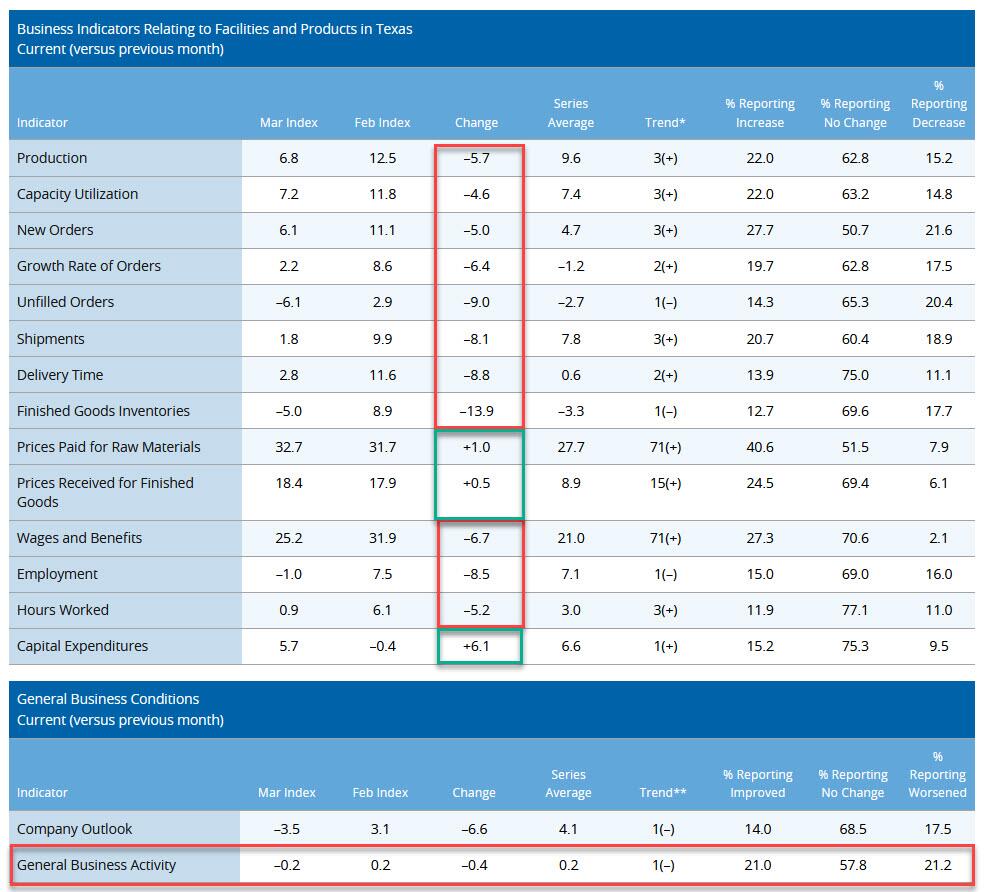

Dallas Fed Mfg Activity Holds Near One Year High Despite Plunge In Respondent Sentiment On Iran War

Dallas Fed Mfg Activity Holds Near One Year High Despite Plunge In Respondent Sentiment On Iran War

The Dallas Fed Manufacturing Index continues to straddle the unchanged line, and despite a tiny dip from 0.2 in February, the highest print since July, to -0.2 in March, just below the 1.5 median estimate, the index remained near the highest level in a year and absent a modest and brief, post-Trump election spike, this remains one of the highest prints since mid-2022.

Curiously, the headline index barely dropped even though most index components (9 out of 12) showed a sharp decline, with just a handful rising fractionally.

But it was the survey responses that showed a decidedly negative view on the economy, except for respondents in Machinery Manufacturing. Below is a snapshot from the latest survey:

Beverage and tobacco product manufacturing

We have seen decreases in some of our costs, in particular agricultural raw materials. We have seen increases in the costs of our packaging materials, some of this related to increase in energy costs. We expect the Iran war to cause increases in energy costs for a period extending at least six months and potentially longer. This has increased our uncertainty for the rest of the year.

Chemical manufacturing

The Iran war and bottleneck in the Strait of Hormuz has caused significant supply chain disruption from China, allowing the U.S. chemicals sector to benefit from the supply bottleneck. We believe this to be short-lived and the situation to return to the lower demand levels in the latter half of 2026.

Computer and electronic product manufacturing

I am thinking about recommending to our board to close the company.

We have seen no impact yet from higher fuel prices. However, we expect to see this very soon, as our vendors will increase raw materials prices to include the increased cost for transportation.

We would like to see lower interest rates throughout this year.

Food manufacturing

Continuing confusion at the federal level, illiquid consumer base and falling federal government spending are not helping the food industry.

High density Hispanic channels are down. Costs are up, and freight is increasing fast. Tariff chaos has wreaked havoc with all of our export customers and seasoning suppliers.

We are worried about costs increasing due to fuel price increases. We are worried about a slowdown in the economy due to geopolitics.

Furniture and related product manufacturing

The Iran war and impact on energy prices are concerns as consumers have to deal with the rapid increase in energy cost. Hopefully it will moderate as the conflict curtails. That said, the more demoralizing impact of the constant circus out of Washington and inability to fund critical infrastructure like TSA is killing the animal spirits of our economy.

Machinery manufacturing

We are beating our competition due to the continued vertical integration plans that we are focused on implementing and improving. This requires a great deal of planning and money, but the payout is very sound.

Spring has sprung. It’s truly like the balm of Gilead. After an extended period of ailment and woe, the healing has occurred and we are on our way to greater things. Our business growth thus far in 2026 is like a sweet fragrance that is healing our loss and hardship from prior years.

We are still seeing strong business activity with our backlog increasing.

Our company is seeing an increase in activity totally unrelated to the current geopolitical conditions. The effect of uncertainty delayed the start of a new manufacturing project in the U.S. (tariffs, capital expenditures) in 2025. Project 2025 is underway with a six-month delay and scaled back to accommodate a less ambitious picture for 2026. We are still recovering from 2025 plus a more conservative outlook for 2026. Things are trending upward in our field but at a much slower pace.

Miscellaneous manufacturing

Many external factors contributing to an unstable market.

If we could get our tariff reimbursement back, that would put us in a position to invest in growth. Without it, though, we don’t have the capital to invest in growth.

Nonmetallic mineral product manufacturing

We are waiting for home building activity to pick up, which is dependent upon interest rates.

Paper manufacturing

Overall business still slow. Have achieved limited price reductions in some raw materials that are in an oversupply condition but not enough to keep up with the decline in selling prices of our products. We still see upward pressure on labor and benefits cost. Margins are reduced from 12 months ago.

Plastics and rubber products manufacturing

Importing from China is precarious. The costs of product and freight are higher and slower. Suppliers are apprehensive. Their costs are increasing, especially a certain raw material plastic impacted by petrochemicals affected by cost of oil.

Printing and related support activities

We have been stupid slow recently, slower than we can recall in many years. We continue to believe it’s from the chaos and confusion coming out of Washington. In addition, now with the Iran war, prices are going to shoot up due to shipping costs, and tariffs are still in effect. So, there is no telling when business will start to improve. We have some nice work coming in soon, but it’s work we knew was coming. We are seeing some improvement in our estimating backlog, which is a good sign of better days to come. The war is causing a disruption of raw materials prices as we are producing plastic-based products, virtually all of our raw materials are hydrocarbon based. Fifteen percent increases are normal.

Tyler Durden

Mon, 03/30/2026 – 11:15

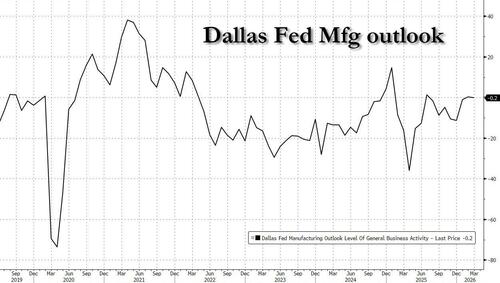

Dallas Fed Mfg Activity Holds Near One Year High Despite Plunge In Respondent Sentiment On Iran War

Dallas Fed Mfg Activity Holds Near One Year High Despite Plunge In Respondent Sentiment On Iran War

The Dallas Fed Manufacturing Index continues to straddle the unchanged line, and despite a tiny dip from 0.2 in February, the highest print since July, to -0.2 in March, just below the 1.5 median estimate, the index remained near the highest level in a year and absent a modest and brief, post-Trump election spike, this remains one of the highest prints since mid-2022.

Curiously, the headline index barely dropped even though most index components (9 out of 12) showed a sharp decline, with just a handful rising fractionally.

But it was the survey responses that showed a decidedly negative view on the economy, except for respondents in Machinery Manufacturing. Below is a snapshot from the latest survey:

Beverage and tobacco product manufacturing

We have seen decreases in some of our costs, in particular agricultural raw materials. We have seen increases in the costs of our packaging materials, some of this related to increase in energy costs. We expect the Iran war to cause increases in energy costs for a period extending at least six months and potentially longer. This has increased our uncertainty for the rest of the year.

Chemical manufacturing

The Iran war and bottleneck in the Strait of Hormuz has caused significant supply chain disruption from China, allowing the U.S. chemicals sector to benefit from the supply bottleneck. We believe this to be short-lived and the situation to return to the lower demand levels in the latter half of 2026.

Computer and electronic product manufacturing

I am thinking about recommending to our board to close the company.

We have seen no impact yet from higher fuel prices. However, we expect to see this very soon, as our vendors will increase raw materials prices to include the increased cost for transportation.

We would like to see lower interest rates throughout this year.

Food manufacturing

Continuing confusion at the federal level, illiquid consumer base and falling federal government spending are not helping the food industry.

High density Hispanic channels are down. Costs are up, and freight is increasing fast. Tariff chaos has wreaked havoc with all of our export customers and seasoning suppliers.

We are worried about costs increasing due to fuel price increases. We are worried about a slowdown in the economy due to geopolitics.

Furniture and related product manufacturing

The Iran war and impact on energy prices are concerns as consumers have to deal with the rapid increase in energy cost. Hopefully it will moderate as the conflict curtails. That said, the more demoralizing impact of the constant circus out of Washington and inability to fund critical infrastructure like TSA is killing the animal spirits of our economy.

Machinery manufacturing

We are beating our competition due to the continued vertical integration plans that we are focused on implementing and improving. This requires a great deal of planning and money, but the payout is very sound.

Spring has sprung. It’s truly like the balm of Gilead. After an extended period of ailment and woe, the healing has occurred and we are on our way to greater things. Our business growth thus far in 2026 is like a sweet fragrance that is healing our loss and hardship from prior years.

We are still seeing strong business activity with our backlog increasing.

Our company is seeing an increase in activity totally unrelated to the current geopolitical conditions. The effect of uncertainty delayed the start of a new manufacturing project in the U.S. (tariffs, capital expenditures) in 2025. Project 2025 is underway with a six-month delay and scaled back to accommodate a less ambitious picture for 2026. We are still recovering from 2025 plus a more conservative outlook for 2026. Things are trending upward in our field but at a much slower pace.

Miscellaneous manufacturing

Many external factors contributing to an unstable market.

If we could get our tariff reimbursement back, that would put us in a position to invest in growth. Without it, though, we don’t have the capital to invest in growth.

Nonmetallic mineral product manufacturing

We are waiting for home building activity to pick up, which is dependent upon interest rates.

Paper manufacturing

Overall business still slow. Have achieved limited price reductions in some raw materials that are in an oversupply condition but not enough to keep up with the decline in selling prices of our products. We still see upward pressure on labor and benefits cost. Margins are reduced from 12 months ago.

Plastics and rubber products manufacturing

Importing from China is precarious. The costs of product and freight are higher and slower. Suppliers are apprehensive. Their costs are increasing, especially a certain raw material plastic impacted by petrochemicals affected by cost of oil.

Printing and related support activities

We have been stupid slow recently, slower than we can recall in many years. We continue to believe it’s from the chaos and confusion coming out of Washington. In addition, now with the Iran war, prices are going to shoot up due to shipping costs, and tariffs are still in effect. So, there is no telling when business will start to improve. We have some nice work coming in soon, but it’s work we knew was coming. We are seeing some improvement in our estimating backlog, which is a good sign of better days to come. The war is causing a disruption of raw materials prices as we are producing plastic-based products, virtually all of our raw materials are hydrocarbon based. Fifteen percent increases are normal.

Tyler Durden

Mon, 03/30/2026 – 11:15

Iran Alleges Series Of ‘False Flags’ – Including On Kuwait Water Plant – Designed To Perpetuate War

Iran Alleges Series Of ‘False Flags’ – Including On Kuwait Water Plant – Designed To Perpetuate War

The Iranian military denied on Monday being behind the recent attack which hit a desalination plant in Kuwait, labeling the strike a US-Israeli false-flag operation aimed at “destabilizing and destroying the region.”

“The brutal aggression by the Zionist regime against the desalination facility in Kuwait, carried out in recent hours under the pretext of accusing the Islamic Republic of Iran, is a sign of the vileness and depravity of the Zionist occupiers,” the Khatam al-Anbiya Central Headquarters of the Iranian army said in a statement.

“We declare that US bases, personnel, and their interests in the region, as well as the military, security, and economic infrastructure of the Zionist regime in the occupied Palestinian territories, remain powerful targets for us,” it added.

The Iranian military went on to urge “countries of West Asia must remain vigilant against the sedition of the US–Zionist axis aimed at destabilizing and destroying the region.”

Regional states “must put an end to the presence of the criminal US army and occupying Zionists in the region,” it stressed. The attack on the desalination plant took place on Sunday.

“A service building at a power and water desalination plant was attacked as part of the Iranian aggression against the State of Kuwait, resulting in the death of an Indian worker and significant material damage to the building,“ said a spokesperson for the Kuwaiti Electricity Ministry.

This is not the first attack Tehran has labeled a false flag. Iran has also denied recent strikes on fuel tankers in Oman and a refinery in Iraq’s Erbil, as well as one that targeted an Aramco facility in Saudi Arabia at the start of the month.

US journalist Tucker Carlson reported earlier in March that Mossad agents were detained in Gulf states for planning bombings.

Iran’s Foreign Minister Abbas Araghchi said on March 15 that the US has been using its new Lucas drone – modeled after the Iranian Shahed – to carry out false-flag attacks in the region and attribute them to the Islamic Republic.

Tehran has said only US and Israeli-linked military and economic assets in the Gulf will be struck by its forces. Iran is warning Gulf governments against allowing Washington to use their bases for attacks on the Islamic Republic.

Iranian drone and missile strikes targeted the Prince Sultan Air Base in Saudi Arabia on March 27, wounding at least 12 US troops and damaging aircraft and buildings.

A senior Iranian intelligence official told The Cradle on March 26 that the Islamic Republic is preparing a “strong response” against the UAE due to the “active role” it has played in the US-Israeli war on it.

Roughly 90% of Kuwait’s drinking water comes from desalination.

“A decision has been made at the leadership level to end the weeks-long tolerance toward this country. In addition to US military barracks and bases in the UAE, which were targeted in Iran’s defensive attacks, the Emiratis also provided some of their own air bases to the US to be used in attacking Iran,” the intelligence officials went on to say, citing security reports.

“The UAE is considered a foothold for Israel in the region,” the source continued, adding that Abu Dhabi has “carried out misleading operations against Oman and other countries” – likely a reference to false-flag operations pinned on Iran.

Tyler Durden

Mon, 03/30/2026 – 11:05

Iran Alleges Series Of ‘False Flags’ – Including On Kuwait Water Plant – Designed To Perpetuate War

Iran Alleges Series Of ‘False Flags’ – Including On Kuwait Water Plant – Designed To Perpetuate War

The Iranian military denied on Monday being behind the recent attack which hit a desalination plant in Kuwait, labeling the strike a US-Israeli false-flag operation aimed at “destabilizing and destroying the region.”

“The brutal aggression by the Zionist regime against the desalination facility in Kuwait, carried out in recent hours under the pretext of accusing the Islamic Republic of Iran, is a sign of the vileness and depravity of the Zionist occupiers,” the Khatam al-Anbiya Central Headquarters of the Iranian army said in a statement.

“We declare that US bases, personnel, and their interests in the region, as well as the military, security, and economic infrastructure of the Zionist regime in the occupied Palestinian territories, remain powerful targets for us,” it added.

The Iranian military went on to urge “countries of West Asia must remain vigilant against the sedition of the US–Zionist axis aimed at destabilizing and destroying the region.”

Regional states “must put an end to the presence of the criminal US army and occupying Zionists in the region,” it stressed. The attack on the desalination plant took place on Sunday.

“A service building at a power and water desalination plant was attacked as part of the Iranian aggression against the State of Kuwait, resulting in the death of an Indian worker and significant material damage to the building,“ said a spokesperson for the Kuwaiti Electricity Ministry.

This is not the first attack Tehran has labeled a false flag. Iran has also denied recent strikes on fuel tankers in Oman and a refinery in Iraq’s Erbil, as well as one that targeted an Aramco facility in Saudi Arabia at the start of the month.

US journalist Tucker Carlson reported earlier in March that Mossad agents were detained in Gulf states for planning bombings.

Iran’s Foreign Minister Abbas Araghchi said on March 15 that the US has been using its new Lucas drone – modeled after the Iranian Shahed – to carry out false-flag attacks in the region and attribute them to the Islamic Republic.

Tehran has said only US and Israeli-linked military and economic assets in the Gulf will be struck by its forces. Iran is warning Gulf governments against allowing Washington to use their bases for attacks on the Islamic Republic.

Iranian drone and missile strikes targeted the Prince Sultan Air Base in Saudi Arabia on March 27, wounding at least 12 US troops and damaging aircraft and buildings.

A senior Iranian intelligence official told The Cradle on March 26 that the Islamic Republic is preparing a “strong response” against the UAE due to the “active role” it has played in the US-Israeli war on it.

Roughly 90% of Kuwait’s drinking water comes from desalination.

“A decision has been made at the leadership level to end the weeks-long tolerance toward this country. In addition to US military barracks and bases in the UAE, which were targeted in Iran’s defensive attacks, the Emiratis also provided some of their own air bases to the US to be used in attacking Iran,” the intelligence officials went on to say, citing security reports.

“The UAE is considered a foothold for Israel in the region,” the source continued, adding that Abu Dhabi has “carried out misleading operations against Oman and other countries” – likely a reference to false-flag operations pinned on Iran.

Tyler Durden

Mon, 03/30/2026 – 11:05

Watch Live: Fed Chair Powell Speaks At Harvard University

Watch Live: Fed Chair Powell Speaks At Harvard University

Fed Chair Jerome Powell, who has just over a month left in his tenure as head of the world’s most important central bank, speaks at 10:30am ET to the Harvard University Principles of Economics class. He is not expected to make monetary policy comments.

As CNBC notes, this will be one of Powell’s final scheduled public appearances before his term ends in May. The discussion comes with markets anticipating the central bank will be on hold regarding interest rates through the end of the year.

In his most recent comments, Powell characterized the economy as growing at “a solid pace” and said he is not concerned with worries of stagflation, low growth with high inflation. However, he noted that policymakers are taking a cautious approach as multiple factors play out this year, including the Iran war, tariffs and a stagnant labor market; he flagged frustration over sticky non-housing services and made clear that, if inflation progress does not resume, cuts will not follow.

On rates, Powell kept optionality but did not open the door to near-term easing. He said policy was in a good place, noting it was around the high end of neutral, or only modestly restrictive. He said the labour market was being watched closely, particularly weak private payroll growth, but stopped short of suggesting employment risks now dominate the Fed’s policy balance.

On his role as Fed Chair, Powell said that if a successor had not been confirmed before his term as Chair ends in May, he would remain in place as Fed Chair “Pro Tern”; on his role as Governor beyond that, he said he has no intention of leaving the Board until the DoJ investigation is over, and he he had not yet decided whether he would stay on.

Powell’s term ends officially on May 15, and there is only one more policy meeting between now and then. However, it’s possible he will stay in the position longer if the Senate does not confirm is designated successor, former Governor Kevin Warsh.

Watch live:

Tyler Durden

Mon, 03/30/2026 – 10:30

https://www.zerohedge.com/markets/watch-live-fed-chair-powell-speaks-harvard-university

Watch Live: Fed Chair Powell Speaks At Harvard University

Watch Live: Fed Chair Powell Speaks At Harvard University

Fed Chair Jerome Powell, who has just over a month left in his tenure as head of the world’s most important central bank, speaks at 10:30am ET to the Harvard University Principles of Economics class. He is not expected to make monetary policy comments.

As CNBC notes, this will be one of Powell’s final scheduled public appearances before his term ends in May. The discussion comes with markets anticipating the central bank will be on hold regarding interest rates through the end of the year.

In his most recent comments, Powell characterized the economy as growing at “a solid pace” and said he is not concerned with worries of stagflation, low growth with high inflation. However, he noted that policymakers are taking a cautious approach as multiple factors play out this year, including the Iran war, tariffs and a stagnant labor market; he flagged frustration over sticky non-housing services and made clear that, if inflation progress does not resume, cuts will not follow.

On rates, Powell kept optionality but did not open the door to near-term easing. He said policy was in a good place, noting it was around the high end of neutral, or only modestly restrictive. He said the labour market was being watched closely, particularly weak private payroll growth, but stopped short of suggesting employment risks now dominate the Fed’s policy balance.

On his role as Fed Chair, Powell said that if a successor had not been confirmed before his term as Chair ends in May, he would remain in place as Fed Chair “Pro Tern”; on his role as Governor beyond that, he said he has no intention of leaving the Board until the DoJ investigation is over, and he he had not yet decided whether he would stay on.

Powell’s term ends officially on May 15, and there is only one more policy meeting between now and then. However, it’s possible he will stay in the position longer if the Senate does not confirm is designated successor, former Governor Kevin Warsh.

Watch live:

Tyler Durden

Mon, 03/30/2026 – 10:30

https://www.zerohedge.com/markets/watch-live-fed-chair-powell-speaks-harvard-university

Vance Tops CPAC Straw Poll For 2028 GOP Presidential Nominee

Vance Tops CPAC Straw Poll For 2028 GOP Presidential Nominee

Authored by Tom Gantert via The Epoch Times (emphasis ours),

Vice President JD Vance is the leading candidate to take the Republican nomination for president in 2028, according to a straw poll taken at the Conservative Political Action Conference (CPAC) on March 28.

Vance received 53 percent of the support of the people who attended the annual conference in Grapevine, Texas. Secretary of State Marco Rubio was in second place at 35 percent. Florida Gov. Ron DeSantis and Donald Trump Jr. came in at 2 percent each. Sen. Ted Cruz (R-Texas), War Secretary Pete Hegseth, Sen. Rand Paul (R-Ky.), Director of National Intelligence Tulsi Gabbard, and Texas Gov. Greg Abbott all had 1 percent support.

The poll was announced at the end of the four-day CPAC conference.

In 2025, Vance won the CPAC straw poll for the 2028 Republican presidential nomination, receiving 61 percent support, and Steve Bannon took second place at 12 percent.

Vance also holds a big lead in the RealClearPolitics average of New Hampshire’s 2028 Republican presidential primary polls conducted in February 2026 and March 2026. Vance leads those polls at 47.3 percent, and Rubio is second at 17.3 percent. They are followed by former U.S. Ambassador to the United Nations Nikki Haley at 6.7 percent and DeSantis at 5.3 percent.

A presidential matchup between President Donald Trump and Haley had overwhelmingly favored Trump in CPAC’s February 2024 straw poll.

According to the poll, 94 percent of respondents said they would support Trump if a Republican primary were held that day, compared with 5 percent for Haley. Only 1 percent said they were undecided.

Trump is not eligible to run for president in 2028. The president did not attend the 2026 CPAC conference.

The recent CPAC straw poll supports earlier polling that had Vance as the leading candidate.

A September 2025 poll from YouGov showed Vance with a commanding early lead in the 2028 Republican presidential field. The survey had Vance as the top choice with 44 percent of Republican respondents, far ahead of any other potential candidate.

The rest of the field trailed in single digits; Trump Jr. drew about 10 percent, followed by DeSantis at roughly 8 percent and Rubio near 4 percent.

Vance talked to Fox News host Sean Hannity in November 2025 about running against Rubio in a presidential election.

In a segment that was aired separately from the full interview, Hannity said Rubio was Vance’s “best friend” in the administration, and Vance agreed.

“People have asked me, ‘Do you see Marco as a rival?’“ Vance said. ”First of all, if either one of us end up running, it’s a long ways in the future and none of us are entitled to it. It would be ridiculous for me to say, ‘Marco is a rival.’ No. No. No. Marco is a colleague.”

Tyler Durden

Mon, 03/30/2026 – 10:25

https://www.zerohedge.com/political/vance-tops-cpac-straw-poll-2028-gop-presidential-nominee

Vance Tops CPAC Straw Poll For 2028 GOP Presidential Nominee

Vance Tops CPAC Straw Poll For 2028 GOP Presidential Nominee

Authored by Tom Gantert via The Epoch Times (emphasis ours),

Vice President JD Vance is the leading candidate to take the Republican nomination for president in 2028, according to a straw poll taken at the Conservative Political Action Conference (CPAC) on March 28.

Vance received 53 percent of the support of the people who attended the annual conference in Grapevine, Texas. Secretary of State Marco Rubio was in second place at 35 percent. Florida Gov. Ron DeSantis and Donald Trump Jr. came in at 2 percent each. Sen. Ted Cruz (R-Texas), War Secretary Pete Hegseth, Sen. Rand Paul (R-Ky.), Director of National Intelligence Tulsi Gabbard, and Texas Gov. Greg Abbott all had 1 percent support.

The poll was announced at the end of the four-day CPAC conference.

In 2025, Vance won the CPAC straw poll for the 2028 Republican presidential nomination, receiving 61 percent support, and Steve Bannon took second place at 12 percent.

Vance also holds a big lead in the RealClearPolitics average of New Hampshire’s 2028 Republican presidential primary polls conducted in February 2026 and March 2026. Vance leads those polls at 47.3 percent, and Rubio is second at 17.3 percent. They are followed by former U.S. Ambassador to the United Nations Nikki Haley at 6.7 percent and DeSantis at 5.3 percent.

A presidential matchup between President Donald Trump and Haley had overwhelmingly favored Trump in CPAC’s February 2024 straw poll.

According to the poll, 94 percent of respondents said they would support Trump if a Republican primary were held that day, compared with 5 percent for Haley. Only 1 percent said they were undecided.

Trump is not eligible to run for president in 2028. The president did not attend the 2026 CPAC conference.

The recent CPAC straw poll supports earlier polling that had Vance as the leading candidate.

A September 2025 poll from YouGov showed Vance with a commanding early lead in the 2028 Republican presidential field. The survey had Vance as the top choice with 44 percent of Republican respondents, far ahead of any other potential candidate.

The rest of the field trailed in single digits; Trump Jr. drew about 10 percent, followed by DeSantis at roughly 8 percent and Rubio near 4 percent.

Vance talked to Fox News host Sean Hannity in November 2025 about running against Rubio in a presidential election.

In a segment that was aired separately from the full interview, Hannity said Rubio was Vance’s “best friend” in the administration, and Vance agreed.

“People have asked me, ‘Do you see Marco as a rival?’“ Vance said. ”First of all, if either one of us end up running, it’s a long ways in the future and none of us are entitled to it. It would be ridiculous for me to say, ‘Marco is a rival.’ No. No. No. Marco is a colleague.”

Tyler Durden

Mon, 03/30/2026 – 10:25

https://www.zerohedge.com/political/vance-tops-cpac-straw-poll-2028-gop-presidential-nominee

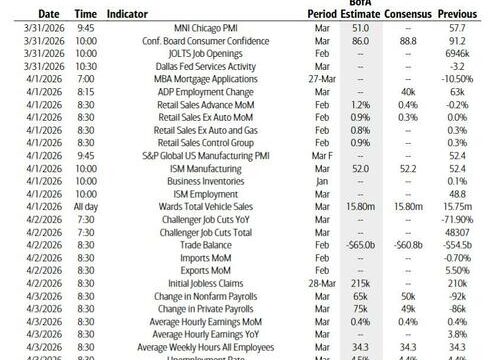

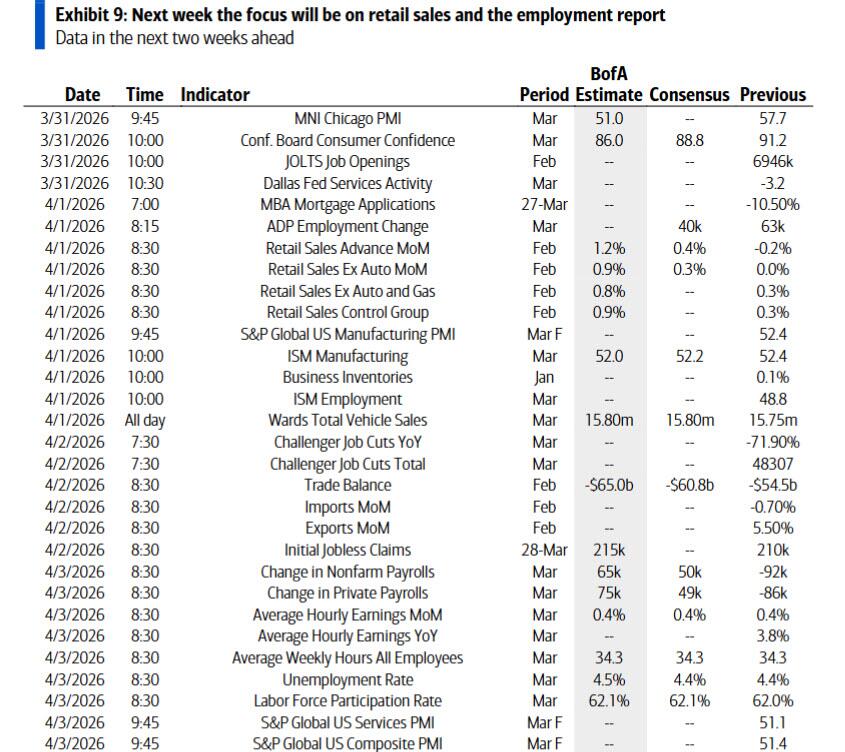

Key Events This Holiday-Shortened Week: Payrolls, PMI, ISM, Retail Sales And Fed Speech

Key Events This Holiday-Shortened Week: Payrolls, PMI, ISM, Retail Sales And Fed Speech

Looking at the week ahead, we should start to learn about the economic consequences of the conflict, as several data releases for March are out which cover the period since the strikes began on February 28.

In the US, that includes the monthly jobs report on Friday – which falls on a Holday when stocks are closed, while bonds are open for half a day – where economists expect nonfarm payrolls to have risen by +60k in March. As a reminder, US payrolls have been pretty choppy in recent months, and on the current series of revisions they’ve been oscillating between positive and negative readings for every month since May. Last month they were down -92k, but some of that weakness was a function of a strike at a major healthcare company that’s since ended, along with severe weather that may have temporarily depressed February’s payrolls. So while DB economists are expecting a positive payrolls print for March, they think the unemployment rate will round up to 4.5% given how close it was last month (4.44%).

Otherwise in the US, the focus will be on whether higher oil prices have started to impact business sentiment and inflation in a meaningful way. So the ISM manufacturing will be in the spotlight, including the prices paid component for whether the inflationary impact has started to filter through. Before that, we’ll also get the Conference Board’s consumer confidence reading tomorrow.

Speaking of inflation, the main highlight in Europe will be tomorrow’s flash CPI print for the Euro Area, which is an important one as the ECB work out what to do. To be fair, the flash print from Spain last Friday was weaker than expected, at +3.3% (vs. +3.8% expected), so that’s slightly eased fears about a very strong print tomorrow. Nevertheless, even with the Spanish number, DB’s European economists are still tracking the Euro Area CPI print at +2.53% year-on-year, up from +1.89% in February, a number which was reinforced with today’s regional German CPI update for March.

Elsewhere this week, there isn’t too much on the calendar of events as we move towards Easter. Indeed, markets will be closed in several countries at the end of the week for Good Friday. However, we will hear from a few central bankers, including Fed Chair Powell later today, who’s speaking in a discussion at Harvard University.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 30

Data: US March Dallas Fed manufacturing activity, February net consumer credit, M4, Germany March CPI, Italy February PPI, Eurozone March economic confidence

Central banks: Fed’s Powell and Williams speak, ECB’s Stournaras speaks

Tuesday March 31

Data: US March Conference Board consumer confidence index, MNI Chicago PMI, Dallas Fed services activity, February JOLTS report, January FHFA house price index, China March official PMIs, UK Q4 current account balance, Japan March Tokyo CPI, February jobless rate, job-to-applicant ratio, retail sales, industrial production, housing starts, Germany March unemployment claims rate, February retail sales, import price index, France March CPI, February PPI, consumer spending, Italy March CPI, January industrial sales, Eurozone March CPI, Canada January GDP

Central banks: Fed’s Goolsbee, Barr and Bowman speak, ECB’s Panetta, Muller, Sleijpen and Kazimir speak, RBA minutes of the March meeting

Earnings: Nike

Other: French President Macron visiting Japan, through April 2

Wednesday April 1

Data: US March ISM index, ADP report, total vehicle sales, February retail sales, January business inventories, China March RatingDog manufacturing PMI, Japan BoJ’s Tankan survey, Italy March manufacturing PMI, new car registrations, February unemployment rate, Eurozone February unemployment rate, Canada March manufacturing PMI

Central banks: Fed’s Musalem and Barr speak, ECB’s Cipollone speaks, BoC’s summary of deliberations

Thursday April 2

Data: US February trade balance, initial jobless claims, Japan March monetary base, France February budget balance, Italy February retail sales, Canada February international merchandise trade, Switzerland March CPI

Central banks: ECB’s economic bulletin, BoE’s DMP survey

Friday April 3

Data: US March jobs report, China March RatingDog services PMI, France February industrial production

Central banks: ECB’s Radev speaks

Other: Good Friday

Looking at just the US, Goldman writes that the key economic data releases this week are the retail sales report on Wednesday and the employment report on Friday. There are several speaking engagements by Fed officials this week, including events with Chair Powell and New York Fed President Williams on Monday.

Monday, March 30

10:30 AM Fed Chair Powell speaks: Fed Chair Jerome Powell will participate in a moderated discussion at Harvard University. Moderated and audience Q&A are expected. On March 18th, Chair Powell said that the risks to employment and inflation are on an equal footing, saying that he would “be hard-pressed to say that one of them is obviously more at risk than the other.” He added that he takes seriously the risk from the oil price shock to inflation expectations against a backdrop where inflation has been high for five years. In light of this, he said, “the framework calls to balance the risks,” and a “mildly restrictive” stance or the “higher borderline of restrictive versus not restrictive” is “the right place to be.”

04:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will speak at the Staten Island Economic Development Corporation. Speech text and moderated Q&A are expected. On March 3rd, President Williams said that “monetary policy is currently well positioned to support the stabilization of the labor market and return inflation to our 2% goal,” adding that “in recent months there have been promising signs of stabilization in the labor market.”

Tuesday, March 31

09:00 AM S&P Case-Shiller 20-city home price index, January (GS +0.3%, consensus +0.4%, last +0.5%)

09:00 AM FHFA house price index, January (consensus +0.1%, last +0.1%)

10:00 AM Conference Board consumer confidence, March (GS 86.5, consensus 88.0, last 91.2)

10:00 AM JOLTS job openings, February (GS 7,000k, consensus 6,890k, last 6,946k): We estimate that JOLTS job openings were roughly unchanged month-over-month in February at 7.0mn based on the signal from online measures of job postings from Indeed and LinkUp. Since the end of February, those measures have declined by roughly 2% on average.

12:00 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will give opening remarks at a Chicago Fed Mobility Project virtual event. On March 24th, President Goolsbee said that “we could be back to the environment with multiple rate cuts for the year, if inflation behaves,” but added that “I could see circumstances where we would need to raise rates if it was going a different way and inflation was getting out of control.”

03:00 PM Fed Governor Barr speaks: Fed Governor Michael Barr will discuss stablecoin regulation at a Federalist Society virtual event. Speech text and moderated and audience Q&A are expected. On March 26th, Governor Barr said that “given the considerable uncertainty about the potential effects of developments in the Middle East on our economy, as well as other factors, it makes sense to take some time to assess conditions,” adding that “our current policy stance puts us in a good place to hold steady while we evaluate the incoming data.”

05:10 PM Fed Vice Chair for Supervision Bowman speaks: Fed Vice Chair for Supervision Michelle Bowman will speak on small businesses at the 2026 Consumer Bankers Association Live conference in San Diego. Speech text and moderated Q&A are expected. On March 20th, Vice Chair for Supervision Bowman said that she has “written three cuts before the end of 2026 to hopefully support the labor market,” and noted that “it is too soon to tell what the impacts of the conflict with Iran will be.”

Wednesday, April 1

08:15 AM ADP employment change, March (GS +40k, consensus +40k, last +63k)

08:30 AM Retail sales, February (GS +0.6%, consensus +0.5%, last -0.2%); Retail sales ex-auto, February (GS +0.5%, consensus +0.3%, last flat); Retail sales ex-auto & gas, February (GS +0.6%, consensus +0.3%, last +0.3%); Core retail sales, February (GS +0.5%, consensus +0.3%, last +0.3%): We estimate core retail sales increased 0.5% in February (ex-autos, gasoline, and building materials; month-over-month SA), reflecting solid alternative data. We estimate headline retail sales increased 0.6%, reflecting a rebound in auto sales.

09:05 AM St. Louis Fed President Musalem (FOMC non-voter) speaks: St. Louis Fed President Alberto Musalem will speak on the economy and monetary policy at the American Enterprise Institute in Washington, DC. Speech text and moderated Q&A are expected.

09:10 AM Fed Governor Barr speaks: Fed Governor Michael Barr will discuss AI and consumer issues at the National Fair Housing Alliance symposium in Washington, DC. Moderated Q&A is expected.

09:45 AM S&P Global US manufacturing PMI, March final (consensus 52.4, last 52.4)

10:00 AM ISM manufacturing index, March (GS 53.0, consensus 52.4, last 52.4): We estimate that the ISM manufacturing index increased by 0.6pt to 53.0 in March, reflecting sequential improvement in regional manufacturing surveys but a slight headwind from potential residual seasonality. Our manufacturing survey tracker increased by 1.1pt to 53.6.

05:00 PM Lightweight motor vehicle sales, March (GS 16.0mn, consensus 15.9mn, last 15.8mn)

Thursday, April 2

08:30 AM Trade balance, February (GS -$50.0bn, consensus -$60.0bn, last -$54.5bn): We forecast that the trade deficit narrowed by $4.5bn to $50.0bn in February, reflecting an increase in gold exports that was partially offset by an increase in goods imports from China.

08:30 AM Initial jobless claims, week ended March 28 (GS 205k, consensus 212k, last 210k): Continuing jobless claims, week ended March 21 (consensus 1,830k, last 1,819k)

Friday, April 3

US equity markets will be closed in observance of Good Friday, while SIFMA recommends an early close at 12 PM for the bond market.

08:30 AM Nonfarm payroll employment, March (GS +70k, consensus +60k, last -92k); Private payroll employment, March (GS +75k, consensus +70k, last -86k); Average hourly earnings (MoM), March (GS +0.3%, consensus +0.3%, last +0.4%); Unemployment rate, March (GS 4.4%, consensus 4.4%, last 4.4%): We estimate nonfarm payrolls increased 70k in March. On the positive side, we expect a 32k boost from the end of worker strikes and a moderate tailwind from sequentially better weather after it likely weighed on February payroll growth. The big data indicators we track were mixed in March. On the negative side, we expect a 5k decline in government payrolls—reflecting a 10k decline in federal government payrolls that is partly offset by a 5k increase in state and local government payrolls. We estimate that the unemployment rate was unchanged on a rounded basis at 4.4% in March, reflecting the stabilization in continuing claims over the last month. That said, the bar for rounding up to 4.5% is not high from an unrounded 4.44% in February. We estimate average hourly earnings rose 0.3% month-over-month in March, reflecting neutral calendar effects.

09:45 AM S&P Global US services PMI, March final (consensus 51.1, last 51.1)

Source: DB, Goldman

Tyler Durden

Mon, 03/30/2026 – 10:15

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}