Category: News

Largest Viking Age Coin Hoard Ever Found In Norway Shocks Archaeologists

Largest Viking Age Coin Hoard Ever Found In Norway Shocks Archaeologists

Hailed as a “historic discovery,” metal detectorists led archaeologists to the largest Viking Age hoard of silver coins ever to be found in Norway, reflecting the Vikings’ extensive network and a pivotal turning point in Norway’s history.

The largest coin hoard in Norwegian history.Innlandet County Council

On April 10, metal detectorists Vegard Sørlie and Rune Sætre uncovered 19 silver coins that quickly turned into an astonishing treasure when archaeologists rushed to the site. The number of coins grew exponentially—initially to 70, then to 500, and eventually to over 1,000.

Archaeologist May-Tove Smiseth described the find, named the “Mørstad Hoard,” as “a once-in-a-lifetime” discovery that surpassed all expectations. Currently, the hoard contains between 2,970 and 3,150 pieces, and archaeologists are still on-site, expecting to unearth even more coins.

Beyond their value as currency and historical artifacts, these coins tell the story of a country transitioning between the 980s and the 1040s, a time when foreign currency dominated and Norway would establish its own mint.

On the brink of a national Norwegian mint

Described as “a national and international event,” the discovery has stunned archaeologists, who call it “absolutely fantastic.”

“Few things are as exciting as the Viking Age in Norway.”

The hoard has inspired archaeologists. “This is a truly unique discovery that you may only expect once in your career.” This is it. For archaeologists, this is the Oscar Award of coin hoards.

This coin hoard, “without parallel,” was located in a field near Rena, in Innlandet County. Boasting an “unbelievable” assortment of coins, they provide an exciting snapshot of the country’s economy at a time of deep political shift.

Experts from the Museum of Cultural History in Oslo have examined the coins and found that most are of English and German origin, with some Danish and Norwegian coins among them.

The presence of English and German coins in a Viking hoard raises intriguing questions: why were these foreign coins found in Norway? Principally.

The hoard dates between the 980s and the 1040s. It reflects a peak in Viking power; the “Second Viking Age” encompasses the late 10th and the early 11th centuries. This silver captures this era.

Most of these were minted under Cnut the Great (the height of Viking power), Æthelred II, Otto III, and others. But Harald Hardrada, also represented in this stash, presumably tossed aside as just too much cash, would replace the foreign entities with one currency. He established a national mint.

So the find is exceptional, as a living, breathing, moving history.

How many coins will they find?

Archaeologists continue to beam with excitement, “truly.”

“Being present when something like this comes to light is simply a great experience, both professionally and personally,” says archaeologist and senior advisor at Innlandet County Council, May-Tove Smiseth, in a press release.

They are still conducting investigations onsite, expecting to find more of these “capital stashes,” as iron was minted in this region and then exported to Europe, so they were found in an industrial center.

This hoard doesn’t appear to belong to an individual, also distinguishing it from the hoards that tend to surface. It does not reflect the wealth of an affluent individual but rather the state, government, or ruling body. Iron production was booming.

Speechless and overjoyed, archaeologists are officially guarding the area, having blocked all access until they complete their investigations. They are even singing the praises of the two metal detectorists.

“What makes this even more gratifying is the way the find has been handled.”

These two pioneering enthusiasts had taken the courses that the county offers to detectorists. They followed the necessary protocol to ensure that this priceless history would fall into the right hands.

Tyler Durden

Mon, 05/04/2026 – 13:40

A Property Tax Rebellion Is Emerging In America

A Property Tax Rebellion Is Emerging In America

Authored by Aaron Gifford via The Epoch Times,

At a petition table inside a Cleveland area gun show on a drizzly Saturday afternoon, citizens talk of an American Dream derailed.

There’s the elderly couple who paid off their mortgage decades ago but can’t afford the property taxes on their home. Their local government, theoretically, can seize the property and auction it off to someone else if the annual bills remain unpaid.

Then there’s the recent retiree who took a part-time job at Lowe’s to pay property taxes on his rental property and avoid raising his tenants’ rent.

Add empty nesters who can’t downsize to smaller houses because interest rates are too high, farmers describing an impossible situation, and recent college graduates groaning about moving further away from home to an affordable place.

Show goers, guns and ammo in hand, pause at Beth Blackmarr’s table on their way out and share with her those concerns.

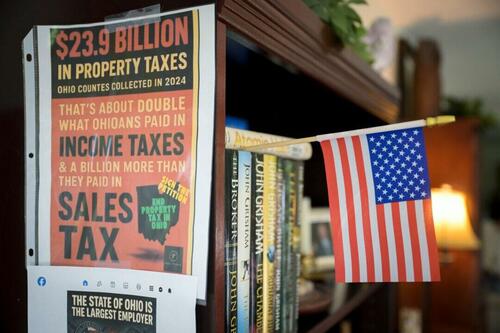

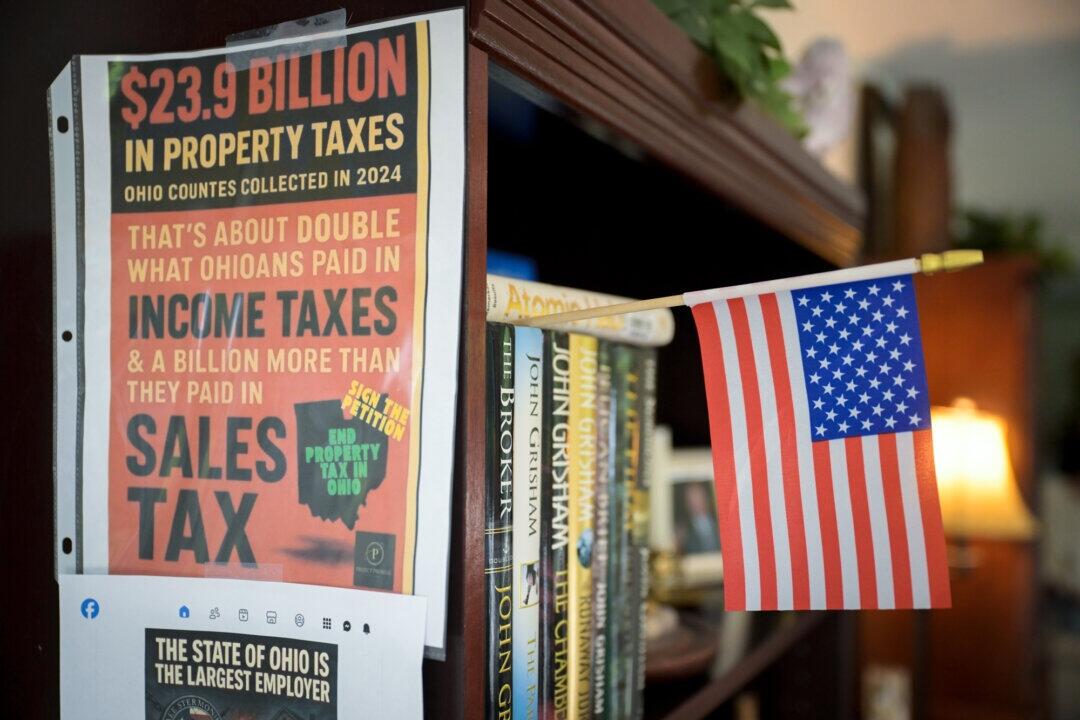

If 413,000 residents throughout the Buckeye State sign a petition before July 1, a public vote to eliminate local property taxes will appear on the November ballot.

If the signature count falls short, whatever is collected can be applied the following year, or however long it takes, said Blackmarr, media coordinator and a main volunteer for the 3,000-plus member Citizens for Property Tax Reform group.

“We are really hurting in Ohio,” she told The Epoch Times. “People never thought they’d be in this situation.”

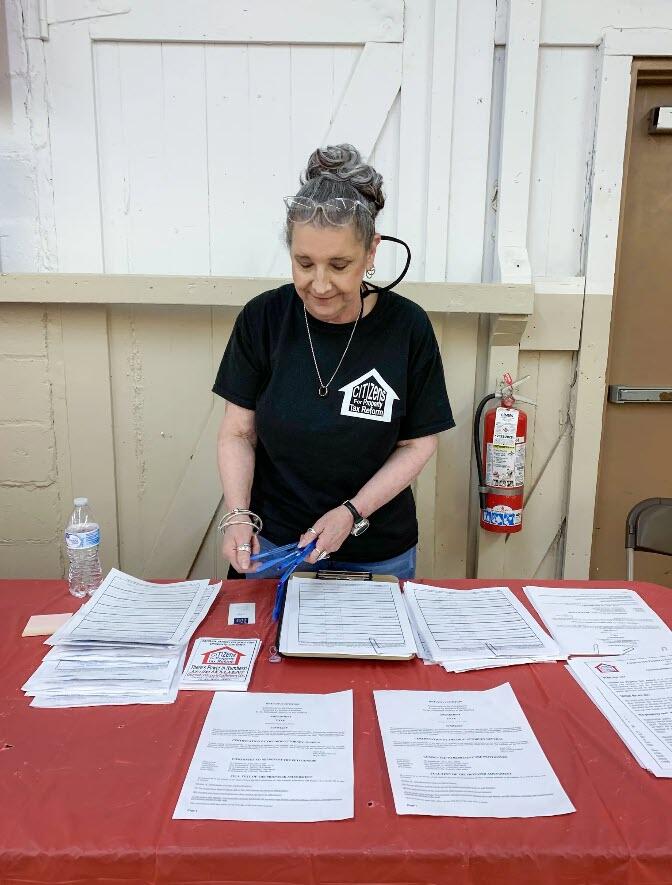

Beth Blackmarr, a volunteer with Ohio-based Citizens for Property Tax Reform, organizes forms during a petition drive at a gun show near Cleveland on April 25, 2026. The group is seeking enough signatures to place a measure eliminating local property taxes on the November ballot. Aaron Gifford/The Epoch Times

Ohio isn’t alone. Forty-six states and the District of Columbia already have limits on annual local property tax levy increases, and leaders in Florida and Texas are pursuing additional legislation to limit government “flexibility” in how it raises revenues, according to a September report from McKinsey and Co., a global management consulting firm whose clients include state and local governments.

Schools, already strapped for cash, hang in the balance. School districts struggle with declining student enrollment, unfunded mandates, state and federal aid loss largely due to skyrocketing Medicaid costs, and spiking employee health insurance costs.

On the local level, mayors and town boards face similar challenges as they try to continue providing public safety, utilities, and infrastructure services.

Fed-up homeowners say it’s high time to try another way to pay their community’s civil servants, perhaps through higher sales tax or state income tax rates, along with slashing administrative bloat in schools and city halls.

“Let the state find a way where 100 percent of the population pays for education,” Ron Shumate, one of Blackmarr’s volunteers from suburban Cincinnati, told The Epoch Times. “They give profit-making businesses a break, but not us.”

Ron Shumate, 83, a resident and homeowner of Springfield Township in Hamilton County, Ohio, on April 21, 2026. Shumate, a volunteer with Blackmarr’s group, helps to collect signatures to place a measure abolishing property taxes on the ballot. Glenn Hartong for The Epoch Times

Across States and Communities

In Massachusetts, a citizens group in Great Barrington, near Springfield, wants to shift more of the costs for schools and local infrastructure to part-time residents who own vacation homes. If All Band Together gets its way, the current annual property tax on a full-time residence assessed at $200,000, for example, would decrease by $1,293, while the amount for a seasonal home with the same assessment would increase by $356, according to the group’s website.

In Minnesota and North Dakota, Republican lawmakers have proposed a cap on property tax increases based on the rate of inflation and population growth. If the rate of inflation is 3 percent and the population of a community grows by 1 percent, for example, then the increase cap for the taxing entity would be 3.5 percent. Overriding the cap would require voter approval.

John Phelan, an economist for Minnesota-based Center of the American Experiment, which wrote the model legislation for both states, said the proposal was prompted by property tax hikes last year of between 8 percent and 9.5 percent in some counties. School boards decide on annual district operating budgets and subsequent tax levies; voters only have a say on major expenditures beyond personnel and fixed costs, such as the creation of a multimillion-dollar technology fund.

“The burden shouldn’t be driven by asset values,” Phelan told The Epoch Times. “If [school districts] want to spend more money, they should get permission from the population.”

In Montana, Republican state lawmakers are pursuing a 2 percent cap on property tax hikes for local government funding, but not for schools, which consume about 55 percent of property tax revenues.

Kendall Cotton, president and CEO of the Frontier Institute research and policy center, called the legislation a good start, but said more relief is needed, as home appraisals in growing communities increased by 60 percent this year, resulting in double-digit property tax hikes.

“These big jumps put a lot of pressure on the system, but governments have not been responding in kind,” Cotton told The Epoch Times.

He cited an example of a school district near the state capital, where taxpayers were asked on short notice to cover expensive boiler replacements ahead of Montana’s frigid winter. That project should have been paid in full with the federal COVID-19 relief aid years earlier, considering the heating equipment was approaching the end of its life cycle. Instead, school leaders used the grants to hire more administrators and mental health counselors.

“Misplaced priorities,” he said. “People are really being taxed out of their homes. We are just renting from the government.”

Members of Nebraska’s Epic Option citizen group, like their peers in Ohio, are collecting signatures for a ballot initiative to eliminate property taxes. They paused their efforts to obtain the required 160,000 signatures this year and instead will focus on 2028, according to the group’s website.

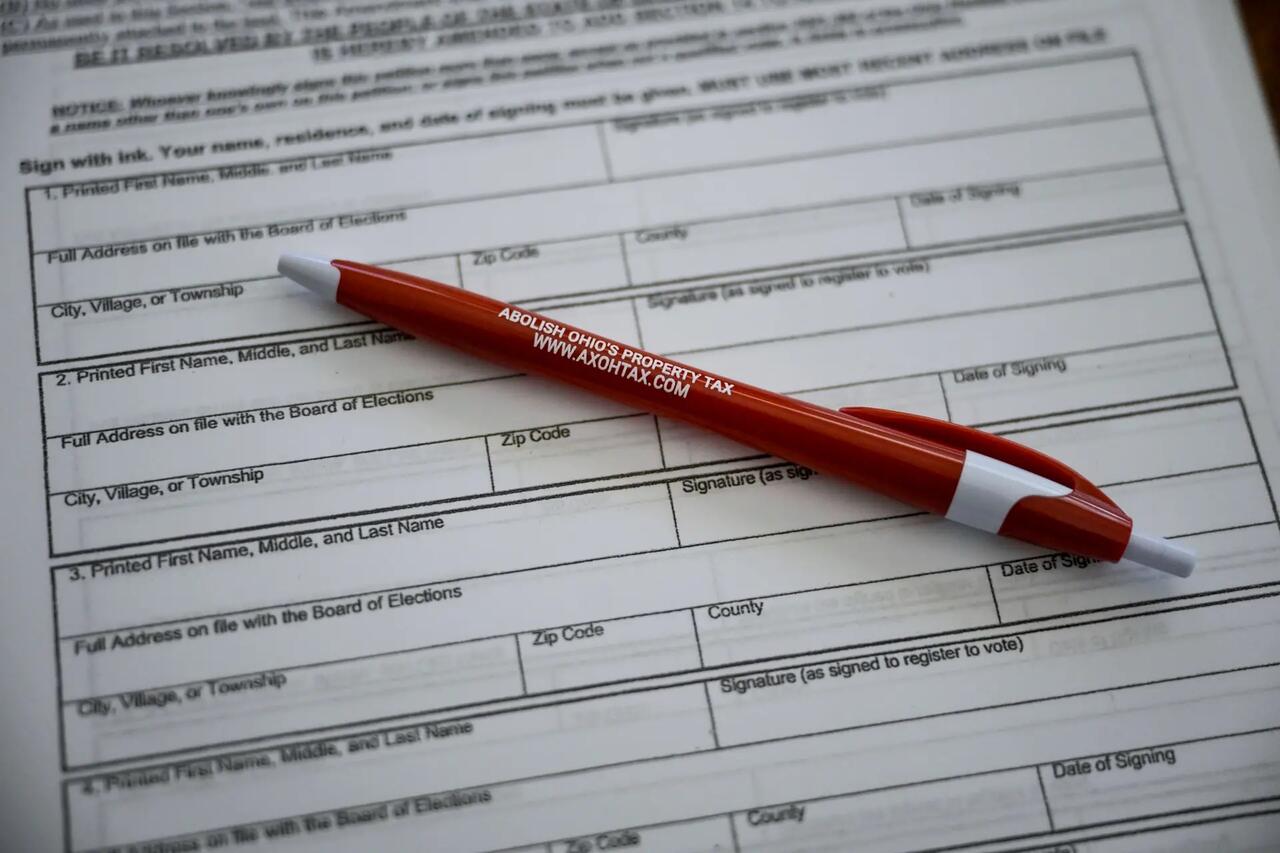

A pen and petition at Ron Shumate’s home in Springfield Township, Ohio, on April 21, 2026. Shumate said the state should find alternative revenue sources to fund schools and local government. Glenn Hartong for The Epoch Times

Texas Gov. Greg Abbott suggested eliminating school property taxes, and Florida state lawmakers have proposed ending local government property taxes but not school taxes.

A bill in the Georgia state legislature calls for phasing out property taxes and increasing the sales tax. A similar bill was introduced in Pennsylvania. Various property tax reform measures have been proposed in Idaho, Illinois, Indiana, Iowa, Kansas, Oklahoma, South Dakota, and Wyoming, according to their respective state legislature websites.

School Budget Woes

More than one-third of U.S. public school funding comes from local property taxes, while the remainder is provided by state and federal aid, as well as municipal and state sales taxes, according to the National Center for Education Statistics. Some states also apply lottery and gambling revenues.

All told, K–12 spending across the country now exceeds $1 trillion, the Edunomics Lab at Georgetown University reported on April 23.

It also said public per-student spending ranges from about $11,000 in Idaho to more than $31,887 in the District of Columbia. Staffing and school tax rates continue to increase in most districts, while student enrollment decreases.

Typical state and federal aid formulas are based on enrollment, so districts must either cut costs or raise local taxes to offset the decreasing amount of per-student aid. The dependence on $189 billion in federal COVID-19 pandemic relief money, which prompted massive hiring sprees but is now exhausted, has exacerbated the financial crisis in many districts that serve low-income communities with large populations of special needs students.

Morse High School students in Bath, Maine, on Dec. 4, 2025. More than a third of U.S. public school funding comes from local property taxes, while the remainder is provided by state and federal aid, as well as municipal and state sales taxes, according to the National Center for Education Statistics. Samira Bouaou/The Epoch Times

The Buffalo, New York, city school district, for example, added 900 workers between 2018 and 2025—including a 569 percent increase in administrative and central office employees—even though enrollment decreased by 11 percent, or 3,679 students, according to the Edunomics Lab.

Buffalo City School District officials previously told The Epoch Times that they implemented a four-year plan to eliminate more than 400 positions, mostly through attrition, and close two school buildings after 2026.

Nationally, public K–12 enrollment decreased by about 900,500 students in the past decade, while staffing during the same time period increased by about 700,000, or 11.9 percent, according to the Edunomics Lab. The organization also reported planned school layoffs or staff reductions this year in Boston; Cleveland; Milwaukee; Las Vegas; Los Angeles; San Diego; San Francisco; Fresno, California; Richmond, Virginia; Tulsa, Oklahoma; Toledo, Ohio; Anchorage, Alaska; Cedar Rapids, Iowa; Fort Lauderdale, Florida; and “countless small and mid-sized districts.”

“This isn’t temporary,” the Edunomics Lab said in an email to The Epoch Times. “It’s a reset.”

Rising Property Values, Higher Taxes

Local property taxes for funding schools and municipal governments are typically based on a $1,000 rate of a home’s assessed value. It’s expected that assessed values in most places are below what a property would sell for, though town, city, and county assessors are tasked with revaluing homes on a regular basis based on changing market values. Higher assessments equal more money for taxing entities.

In addition to school tax increase caps and percentage limits on the taxable values levied on a property, many states, including Ohio, offer slight discounts to low-income households, particularly those owned by seniors who rely on Social Security.

Still, opponents say, stagnant wage growth isn’t keeping up with inflation plus annual property tax increases.

Blackmarr said the monthly property taxes on her home in Lakewood, Ohio, total $383, or $31 more than the principal and interest payments on her mortgage. In 2007, her property taxes on the same house accounted for only 15 percent of the monthly payment, compared to nearly 50 percent today.

She knows of a 58-year-old property owner who extended his mortgage for at least another 30 years because increased property tax and home insurance rates recently pushed his monthly payments, which he began in 2001, out of reach.

Shumate, 83, is bracing for a big bill: A neighbor just sold a much smaller home for $348,000— more than twice as much as Shumate paid for his house seven years ago; the last municipal appraisal in the neighborhood took place in 2021. He believes he can afford higher taxes but worries about his neighbors. The system also discourages homeowners from improving their properties with additions, renovations, or swimming pools.

“The American dream is to own a home, work for at least 30 years, pay it off, retire 10 years later, and be comfortable,” he said. “If you’re relying on Social Security, that won’t happen.”

Taxpayers Want Their Say

The process for authorizing school district budgets varies across the country, with many states requiring voter approval for tax increases related to operational costs and major purchases, but not labor contracts.

Some allow residents to decide on local school board candidates, but not district spending plans, unless the proposal exceeds the state cap for property tax increases.

Either way, massive expenditures for things such as bus fleets, new athletic facilities, technology investments, or the creation of a new dedicated fund often require a public referendum.

In Western Massachusetts, voters in the South Hadley school district on April 14 rejected an override proposition that would raise property taxes by up to 50 percent to maintain all current staffing and programs. Now, school leaders there are poised to cut several administrator and teaching jobs, Advanced Placement courses, music classes, and all sports and extracurricular activities, according to documents on the district website.

Members of the Massachusetts Fiscal Alliance citizens’ group celebrated the outcome.

“People are tired of being taxed to death and seeing the money stolen,” a supporter posted on the group’s Facebook page.

In Minnesota, lawmakers approved enhanced summer unemployment benefits for school bus drivers and then eliminated them a year later because of the growing state budget deficit. Voters in most districts, Phelan said, probably wouldn’t have approved it in the first place; nor would they approve the progressive curricula mandates or taxpayer contributions to the teacher retirement fund.

In Ohio, the passage rate in public votes to override property tax hikes above the state cap reached a low of 19 percent in 2024, compared to a historical passing rate of 37 percent, according to the McKinsey report.

Ohioan Gene Wodzisz purchased his home, a bungalow in the town of Parma, 53 years ago for $42,000. The improvements and additions made to the property have significantly increased its taxable value in recent years.

Wodzisz told The Epoch Times that he can cover the taxes but disagrees in principle: He paid for his own children’s private school tuition while also contributing to local public schools for more than half a century now.

“I understand when it’s for families that don’t have much money, but if you’re making $100,000? Let’s be reasonable. Parents need to pay closer attention to their school boards,” he said.

Tyler Durden

Mon, 05/04/2026 – 13:10

https://www.zerohedge.com/personal-finance/property-tax-rebellion-emerging-america

Cigna To Exit Obamacare In 2027 Amid Rising Costs

Cigna To Exit Obamacare In 2027 Amid Rising Costs

Authored by Mary Prenon via The Epoch Times,

The Cigna Group, one of the country’s largest health services and insurance firms, is joining others, including Aetna and UnitedHealthcare, in divesting its individual health exchange business.

By the end of 2026, Cigna Group will no longer offer insurance through the Affordable Care Act (ACA), also known as “Obamacare,” the company said during its April 30 earnings call.

According to its first-quarter earnings report, as of March 31, the company’s individual exchange business had 369,000 members in individual and family plans.

“We did not make this decision lightly, and appreciate the importance of ensuring patients have continuity through the transition,” Brian Evanko, Cigna Group’s president, chief operating officer, and incoming CEO, said during the earnings call.

“Looking to the future, there’s no question that the status quo in healthcare is unsustainable. Costs continue to rise, as does demand for healthcare services, an untenable equation,” he said.

“We will support members through their open enrollment transitions into 2027.”

Cigna’s decision comes after other health insurance companies, such as CVS Health and UnitedHealthcare, divested insurance business under the ACA.

In its first-quarter 2025 earnings report, released on Feb. 10, CVS Health announced that it was exiting its individual exchange business, where its health insurance arm, Aetna, independently operates ACA plans, beginning in 2026.

Years earlier, UnitedHealthcare said in a filing to the Securities and Exchange Commission in December 2016 that its Employer and Individual program would participate in individual public exchanges in only three states in 2017, a sharp reduction from 34 states in 2016.

At the beginning of this year, the Alliance of Safety-net Hospitals predicted that expiring tax credits for buying health insurance under ACA exchanges could affect nearly 4.8 million people in 2026, as the cost of such plans continues to escalate.

Evanko said Cigna’s decision to vacate the individual healthcare business now is necessary in order to support the firm’s strategic direction for the future. This will allow the insurer to focus its efforts on enhancing customer service with streamlined pharmacy services and additional system improvements.

Evanko noted that over the years, Cigna has continued to add or subtract from its portfolio as needed to position its core healthcare business for sustainable growth.

Last year, Cigna divested its group life and disability business, touting the recent sale of its Medicare businesses.

“Divesting each of these assets enabled greater focus and investment in the remaining businesses within our portfolio, supporting our forward-looking growth path,” he noted.

However, in 2025, Cigna acquired CarepathRx, a pharmacy service dealing with more than 40 health systems and 1,000 hospitals. Last year, Cigna also invested in Shields Health Solutions, which allows it to partner with hospitals and health systems serving patients with complex needs or requiring specialty medications.

Cigna’s first-quarter earnings of $68.52 billion outpaced market expectations of $66.2 billion. Its earnings per share of $7.79 also exceeded the forecasted $7.61.

However, the company’s shares declined by 2.64 percent on May 1, closing at $282.90.

Going forward, Evanko said the insurer plans to continue embracing data and modern technology to improve customer satisfaction and offer more personalized services.

Evanko noted that Cigna has also introduced Signature, its new rebate-free pharmacy benefits model.

According to Evanko, high-cost branded prescriptions represent about 10 percent of all prescriptions nationwide, but nearly 90 percent of total drug spending. The new Signature model is designed with the patient at the center, and its Price Assure capacity guarantees consumers the lowest possible out-of-pocket costs when filling their prescriptions.

Cigna expects the Signature model to become standard in 2028 and for at least 50 percent of its Evernorth Pharmacy Benefit Services members to be enrolled in Signature by the end of 2028.

Tyler Durden

Mon, 05/04/2026 – 12:40

https://www.zerohedge.com/political/cigna-exit-obamacare-2027-amid-rising-costs

Trump, First Lady Demand Jimmy Kimmel Be Fired Over ‘Widow’ Joke Days Before Assassination Attempt

Trump, First Lady Demand Jimmy Kimmel Be Fired Over ‘Widow’ Joke Days Before Assassination Attempt

President Donald Trump and First Lady Melania Trump sharply escalated their long-running feud with late-night comedian Jimmy Kimmel on Monday, publicly demanding that the ABC host be immediately fired by Disney and the network over a joke he made days before a shooting incident at the White House Correspondents’ Dinner.

The controversy centers on a comedic monologue Kimmel delivered on his April 23 episode of Jimmy Kimmel Live!, in which he staged an “alternative” version of the annual dinner roast.

“Look at Melania, so beautiful. Mrs. Trump, you have a glow like an expectant widow.” Kimmel also performed a Jeffrey Epstein-style impression introducing “Donald” and “Melania” and referenced a deleted Trump meme depicting the president as Jesus.

‘AN EXPECTENT

WIDOW’

Jimmy Kimmel bashed for bad-taste joke about Melania becoming widow’ before shooting pic.twitter.com/ybuMaii3Y7

— Simo Saadi (@Simo7809957085) April 27, 2026

As the Epoch Times notes further, the Trumps took serious offense.

“Kimmel’s hateful and violent rhetoric is intended to divide our country. His monologue about my family isn’t comedy—his words are corrosive and deepens the political sickness within America,” Melania wrote on Monday in a post on X.

“People like Kimmel shouldn’t have the opportunity to enter our homes each evening to spread hate.”

Kimmel’s hateful and violent rhetoric is intended to divide our country. His monologue about my family isn’t comedy- his words are corrosive and deepens the political sickness within America.

People like Kimmel shouldn’t have the opportunity to enter our homes each evening to…

— First Lady Melania Trump (@FLOTUS) April 27, 2026

Video footage of the incident at the Washington Hilton ballroom, where the dinner was being held, showed Melania Trump sitting next to the president and White House press secretary Karoline Leavitt. The first lady looked visibly shocked at one point and began to move off stage before she and Trump were whisked to safety by Secret Service agents.

A White House official confirmed to The Epoch Times that Cole Allen was arrested in connection with the shooting. The official said Allen allegedly wrote a manifesto and sent it to members of his family, and that he traveled from California to Washington before the shooting.

On Sunday, acting Attorney General Todd Blanche told NBC’s “Meet the Press” that Allen was likely targeting Trump and members of his administration before he was tackled by security officials outside the dinner.

While Trump praised the Secret Service during a “60 Minutes” interview on Sunday evening, a senior White House official told The Epoch Times in an emailed statement on Monday that chief of staff Susie Wiles will convene a meeting to review security protocols with administration officials.

It’s not the first time Kimmel has drawn criticism from the Trump administration. In September 2025, his show was taken off the air for several days after comments he made about conservative activist Charlie Kirk following his assassination. At the time, Federal Communications Commission Chairman Brendan Carr said Kimmel may have made misleading comments.

When he returned to his show, Kimmel said, “It was never my intention to make light of a murder of a young man. I don’t think there’s anything funny about it.”

Responding to the controversy, Trump criticized ABC for allowing Kimmel back on the air in a Truth Social post, calling the host “in jeopardy” and saying the network is “not funny.”

Trump told Fox News on Sunday morning that his wife was unharmed and is “doing great” after the shooting incident. A lone Secret Service agent was shot in the chest but was protected by a bulletproof vest, Trump has said.

ABC, which is owned by Disney, did not immediately respond to an Epoch Times request for comment. Kimmel and ABC have not issued any public comments in response to Melania Trump’s post.

Tyler Durden

Tue, 04/28/2026 – 09:10

Iran Believes It Can Outlast US Based On ‘Munitions, Markets, & Midterms’; Trump ‘Not Open’ To Tehran’s Latest Proposal As ‘Tank Tops’ Loom

Iran Believes It Can Outlast US Based On ‘Munitions, Markets, & Midterms’; Trump ‘Not Open’ To Tehran’s Latest Proposal As ‘Tank Tops’ Loom

Summary

Trump doesn’t appear open to Iran’s proposal which hinges on US naval blockade ending & nuclear issue being pushed to future negotiations (CNN).

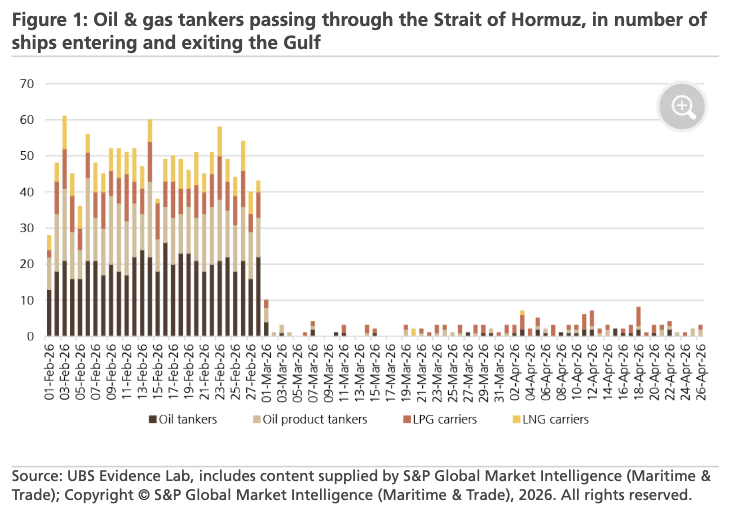

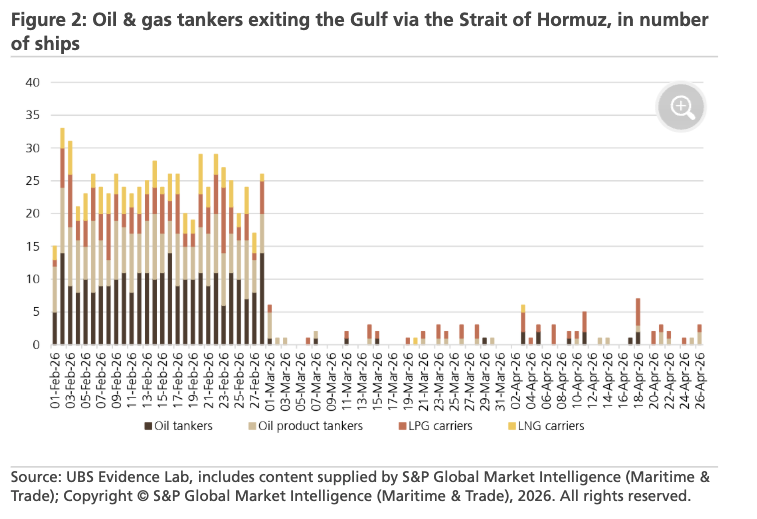

First crude-laden Japanese tanker from Saudi port exits Hormuz Strait successfully without Iranian interference.

Iranian analyst describes that Tehran believes it can outlast Trump & the standoff with US in Hormuz, citing “munitions, markets, and the midterms.”

Will Donald Trump announce that the United States blockade of the Strait of Hormuz has been lifted by May 31, 2026?

Yes 66% · No 34%

View full market & trade on Polymarket

* * *

Oil Rises to 3-week High as Trump Doesn’t Appear Open To Iran Proposal

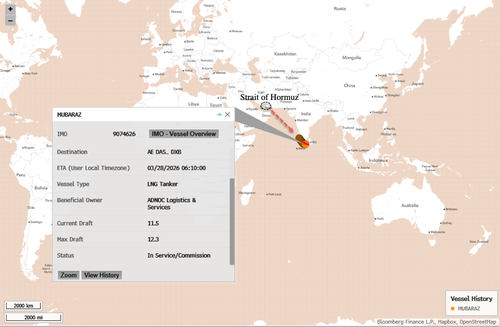

Reporting from Monday evening and overnight says President Trump doesn’t appear open to Iran’s latest proposal to end the war, which hinges on the US naval blockade being lifted but pushes the nuclear issue off to later negotiations. As a result, oil prices have continued to rise, climbing above $110 a barrel Tuesday morning – a first in three weeks, amid concerns of a prolonged strait closure. As for the latest tankers to actually make it through, CBS describes:

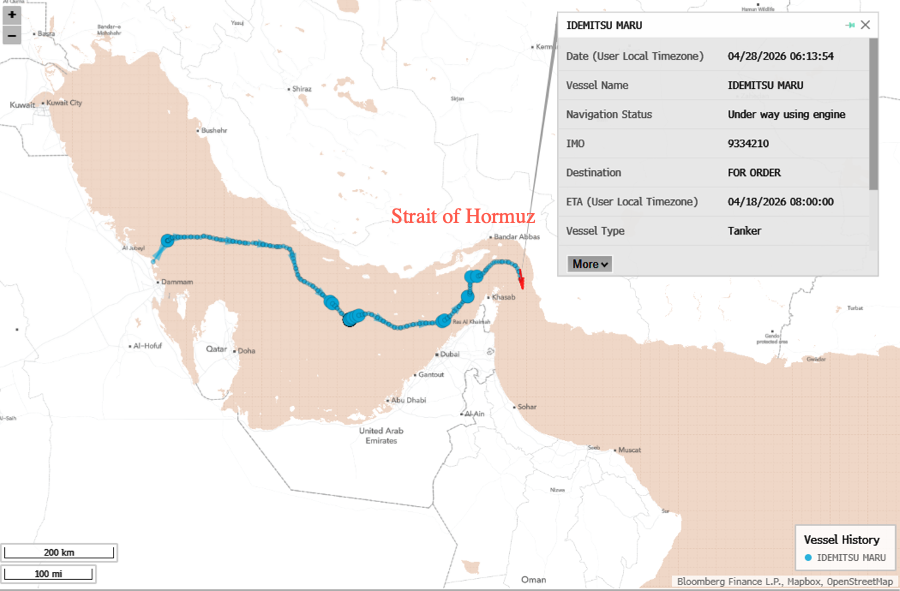

Four civilian ships appeared to leave the Persian Gulf through the Strait of Hormuz on Tuesday without Iranian interference, including a Japanese oil tanker carrying some two million barrels of crude from Saudi Arabia.

The Panama-flagged crude oil tanker Idemitsu Maru called at Saudi Arabia’s Juamyah industrial port in early March, according to open source data from the MarineTraffic ship tracking website. For the past week it had remained anchored off the coast of Abu Dhabi in the Persian Gulf, until late Monday, when it sailed toward Iran’s Larak island in the Strait of Hormuz.

On Tuesday morning, tracking data showed the vessel passing south of Iran’s Larak island, which analysts say the regime had used as a “toll booth” to collect fees from some ships before military authorities declared the strait entirely closed again last week.

The White House has insisted that there would be no scheme for Iran collecting tolls as part of any future deal, but the Iranians appear to be forcing the issue, and have said the funds will help with the country’s reconstruction after the devastation wrought by US-Israeli bombing raids.

Three M’s

Independent news organization Drop Site says that Iran is now setting its own terms for ending the war as President Trump’s narrative on negotiations flails. One Iranian analyst has said that Tehran believes it has the three M’s on its side: “munitions, markets, and the midterms.”

The report cites Hassan Ahmadian, a well-known Iranian analyst and associate professor at the University of Tehran, who explains: “The Iranians are saying time is working in our favor for the three Ms: munitions, markets, and the midterms. These three Ms help Iran in its position and weaken US positions.”

“Obviously in the U.S., they want something to say, ‘We squeezed Iran and we got this.’ My perception is that the Iranians are keen to deny the United States that – they wouldn’t give what Trump wants as a victory,” he added.

A separate Iranian official, privy to negotiations and so remaining anonymous, stated: “We’re currently moving forward with our own design, and we feel continuing negotiations doesn’t make sense until the U.S. government lifts the maritime blockade.”

“The scope of the conflict has expanded, and naturally the issue is no longer purely nuclear,” the official added. Indeed, the latest proposal for ceasefire out of Tehran focuses on the US Navy ending its blockade, and leaves the nuclear issue for future consideration, given it has proven an impasse in the prior Islamabad talks.

But Washington as been asserting its own leverage:

New reporting from Bloomberg shows Iran has 22 more days of available storage.

“The Islamic Republic has enough unused storage capacity to last another 12 to 22 days, Kpler analysts wrote in a report Monday.”

But even more importantly, they highlighted the time horizon until…

— Brett Erickson (@BrettErickson28) April 28, 2026

‘Tank Tops’ Loom

President Trump explained – in his own inimitable manner – what we described last week: time is running out for Tehran… as oil blockade stalls the flow state of Iran’s economy permanently…

Trump told Fox News on Sunday that the US blockade on traffic to and from Iranian ports is putting major pressure on the country’s export infrastructure:

“When you have, you know, lines of vast amounts of oil pouring through your system, if for any reason that line is closed because you can’t continue to put it into containers or ships, which has happened to them — they have no ships because of the blockade — what happens is that line explodes from within, both mechanically and in the earth.”

“It’s something that happens where it just explodes. And they say they only have about three days left before that happens. And when it explodes, you can never, regardless, you can never rebuild it the way it was.”

As Hugh Hendry noted, time is running out for Iran:

“Iran’s oil system is not built to pause. It’s built to flow. It’s a flow system.

Oil cannot simply sit in the ground while strategists argue over maps and how much uranium dust to give over. It has to move. Iran and its system has to move continuously from the rock underground to the tanker in the harbor to the Chinese buyer in Asia.

Pause long enough, and the whole machine breaks.

Interrupt that flow. And the problem isn’t just lost revenues of like forty, fifty, sixty billion dollars. It’s the least of your concerns. The problem is physical and is irreversible.

Because when you suddenly shut the well, remember there’s no physical storage. They pump, they load, they ship.

If they can’t load, if they can’t ship, they can’t pump. And when you suddenly shut the wells, the pressure underground drops fucking fast.

Do you know what happens?

The heavy, sticky crap in the oil, it gums up, gums up in the tiny holes within the rocks and becomes like glue. It traps the oil. It makes it really fucking hard to extract. And once that damage is done, it’s permanent. You lose a big chunk of the oil.

The more Iran is actively either through theater or through bluff, the more that it sits in a standoff, the more it is actively destroying the one thing that it actually depends upon.

That’s the trap. And you’re not reading in in the press, but you’re damn well reading it on your screens.

Because this is where the gap between the narrative of the media and the price stops being subtle and irrelevant, and it’s why stock markets have priced something entirely differently.

The Iranian system, the adversary, cannot afford to stay disrupted without hurting itself. That’s what’s in the equity market’s price.”

We covered the timeline for ‘tank tops’ here in detail – less than 15 days before shut-ins begin.

Tehran Won’t Talk Without JD Vance Present

The failed second round of Pakistan talks, which fell apart before they even began, was supposed to see Vice President JD Vance heading up the US side. This was reportedly something the Iranian side desired to see, and is likely still what its negotiating team would rather be dealing with. On the other hand, per Drop Site, “Iran has total disdain for Trump’s Special Envoy Steve Witkoff and views him as both oblivious of diplomatic processes and totally ignorant of technical issues.”

This is because “Kushner is viewed by Iran as Israel’s man at the table.” This has led to the following view and alleged conclusion: “Iran, the senior official said, does not see any reason to deal with these two without a figure like Vice President JD Vance present.”

Bombs have grown quiet across the Gulf amid the extended ceasefire, with the exception that fighting in southern Lebanon still rages, despite the US-mediated ‘Lebanon ceasefire’:

⚡️Hezbollah publishes footage of them striking 2 Merkava tanks belonging to the Israeli army in southern Lebanon with FPV drones pic.twitter.com/daqtTEqA4q

— War Monitor (@WarMonitors) April 27, 2026

Last week as an avalanche of headlines said that a second round of talks were imminent, and after the Iranian foreign minister had already landed in Islamabad for bilateral discussions with Pakistani mediators, there were premature reports that Vance was en route to Islamabad. The mainstream media claimed that it was Iran essentially begging Washington for negotiations. “But Vance, it turned out, was not on a plane, and Iran continued to deny it had any intention of meeting with U.S. officials in Pakistan,” Drop Site underscores.

Tyler Durden

Tue, 04/28/2026 – 08:55

First Of Many? UAE Exits OPEC As Iran Chaos Triggers Nationalistic Realignment Among Producers

First Of Many? UAE Exits OPEC As Iran Chaos Triggers Nationalistic Realignment Among Producers

Just days after the UAE publicly signaled liquidity concerns by requesting swap lines from the Federal Reserve to ease pressures on the country’s banks, major Gulf oil producer, the UAE, has decided to exit the oil cartel – an unexpected development that crossed Bloomberg headlines on Tuesday morning around 0822 ET.

OPEC finished https://t.co/RtxJdZQeQh

— zerohedge (@zerohedge) April 28, 2026

The official website of the Emirates News Agency (WAM) broke the story, stating that the UAE has decided to exit OPEC and OPEC+ as of May 1, in line with the country’s long-term strategic and economic plan.

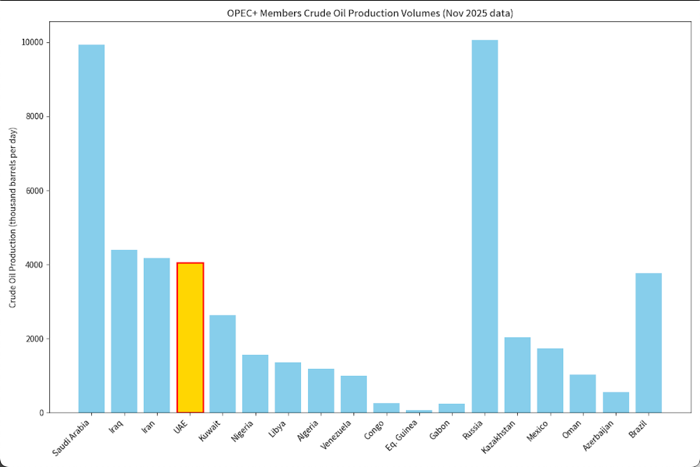

The move would represent a major rupture within OPEC, with direct implications for the remaining 11 members: Saudi Arabia, Iran, Iraq, Kuwait, Venezuela, Nigeria, Libya, Algeria, Congo, Equatorial Guinea, and Gabon.

Yes it was https://t.co/SqwLJlxmDV

— zerohedge (@zerohedge) April 28, 2026

WAM said the decision reflects the “evolution of sector policies to enhance flexibility in responding to market dynamics, while continuing to contribute to market stability in a thoughtful and responsible manner.”

OPEC was founded in Baghdad in September 1960 by Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela. Its original purpose was to give oil-producing states more control over pricing and production after Western oil majors dominated global crude markets.

Important to note: UAE ranks among the top producers in OPEC (~4.05 million bpd), making it a major player with growing capacity ambitions (targeting 5 million bpd by 2027).

WTI futures fell on the news but have since rebounded.

UAE credit risk has soared since the start of the war…

UBS analyst Matthew Cowley responded to the developing, telling clients: “This would weaken OPEC’s ability to defend price floors, especially during economic slowdowns.”

UAE’s full statement:

Abu Dhabi, April 28 / WAM / The United Arab Emirates announced today its decision to withdraw from the Organization of the Petroleum Exporting Countries (OPEC) and OPEC+, effective May 1, 2026.

This decision is in line with the UAE’s long-term strategic and economic vision and the development of its energy sector, including accelerating investment in domestic energy production, and reinforces its commitment to its role as a responsible and reliable producer that looks to the future of global energy markets.

This decision came after a thorough review of the UAE’s production policy and its current and future capacity, and in view of what the national interest requires and the state’s commitment to contribute effectively to meeting the urgent needs of the market, while geopolitical fluctuations continue in the near term through the disturbances in the Arabian Gulf and the Strait of Hormuz, which affect supply dynamics, as the basic trends indicate continued growth in global energy demand in the medium and long term.

The stability of the global energy system depends on the availability of flexible, reliable and affordable supplies, and the UAE has invested to meet the changing demands efficiently and responsibly, prioritizing supply stability, cost, and sustainability.

This decision comes after decades of constructive cooperation, as the UAE joined OPEC in 1967 through the Emirate of Abu Dhabi, and its membership continued after the establishment of the United Arab Emirates in 1971. During this period, the country played an active role in supporting the stability of the global oil market and promoting dialogue between producing countries.

The decision affirms the evolution of sector policies to enhance flexibility in responding to market dynamics, while continuing to contribute to market stability in a thoughtful and responsible manner.

The UAE is a reliable, cost-competitive, and low-carbon-intensity oil producer globally, contributing to global growth and emissions reduction.

After leaving OPEC, the UAE will continue its responsible role by gradually and thoughtfully increasing production, in line with demand and market conditions.

With a large and competitive resource base, the UAE will continue to work with partners to develop resources, supporting economic growth and diversification.

It is worth noting that this decision does not change the UAE’s commitment to the stability of global markets or its approach based on cooperation with producers and consumers, but rather enhances its ability to respond to changing market demands.

The UAE affirms its appreciation for the efforts of both OPEC and the OPEC+ alliance, as the country’s presence in the organization has made significant contributions and even greater sacrifices for the benefit of all. However, it is now time to focus efforts on what the UAE’s national interest requires, its commitment to its investment and importing partners, and the needs of the market, and this is what it will focus on in the future.

The UAE also affirms its continued commitment to responsible production policies and a focus on market stability, taking into account global supply and demand.

The state will continue to invest across the energy sector value chain, including oil and gas, renewable energy and low-carbon solutions, to support resilience and long-term transformation of the energy system.

The UAE values more than five decades of cooperation with partners, while continuing its active

Abu Dhabi’s departure weakens OPEC’s cohesion, and the oil cartel’s fate now remains uncertain.

Tyler Durden

Tue, 04/28/2026 – 08:40

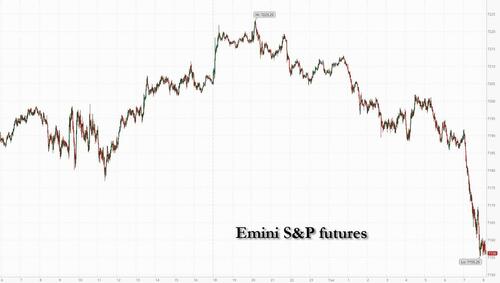

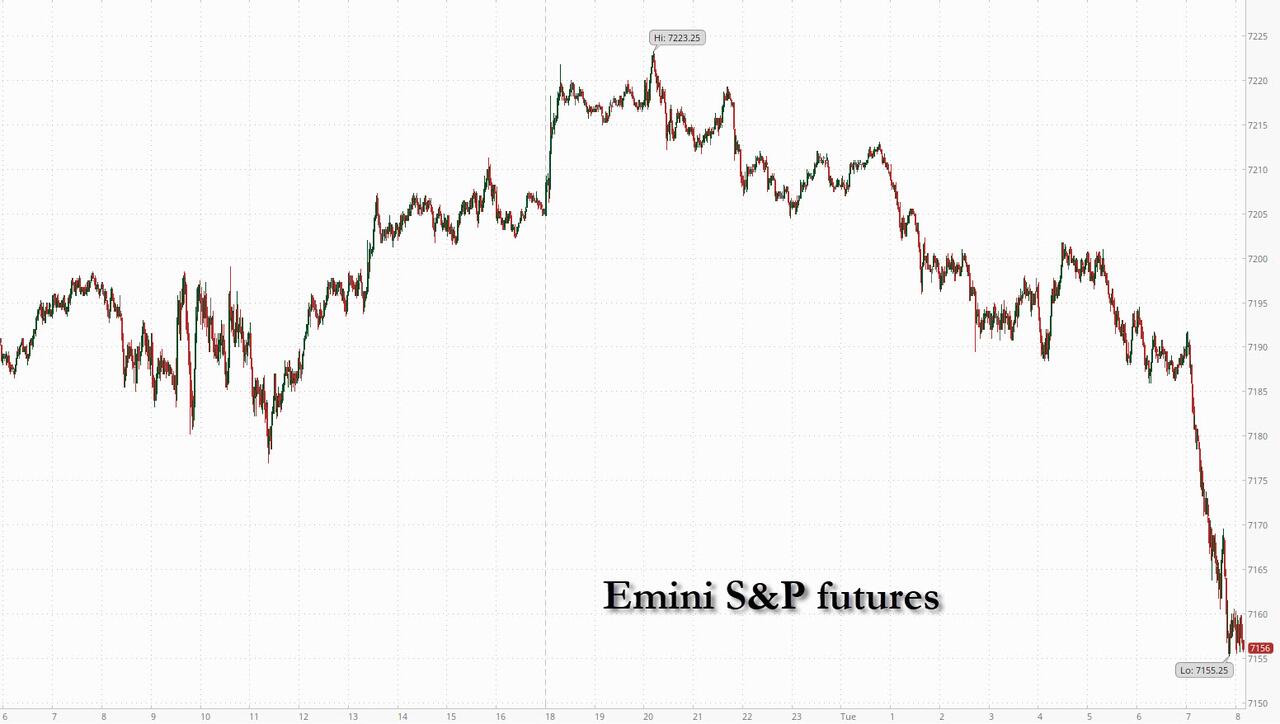

Futures Tumble On AI Spending Fears As Brent Hits 2 Week High

Futures Tumble On AI Spending Fears As Brent Hits 2 Week High

US equity futures are lower, dragged by tech, following a report that OpenAI missed revenue and user targets and there growing internal pushback against Sam Altman’s notorious aggressive spending (the company has $1.5 trillion in commitment it won’t be able to meet), which is hitting semiconductors and the broader supply chain. AS of 8:15am ET, S&P futures are down 0.7% and Nasdaq futures dropped 1.2% as concerns resurfaced over whether the vast amounts of investment in artificial intelligence will pay off. In pre market trading, Semis and Mag7 are under pressure. Defensives are leading Cyclicals ex-Energy. SoftBank, a key backer of ChatGPT’s owner, plunged 9.9% in Tokyo. US-based OpenAI partners including Oracle and CoreWeave fell in premarket trading. Nvidia was poised to drop 2.9% from a record high. Meanwhile, Brent rose above $111 a barrel, with the Strait of Hormuz still shut. Bond yields are 2-4bps higher as the yield curve flattens and USD appreciates, following the price of oil. Commodities continue to be led by Energy with WTI rising above $100/bbl after Trump signaled he was unlikely to accept Iran’s latest proposal to end the conflict which included a proposed a plan that would reopen the Strait of Hormuz while leaving questions about its nuclear program for later negotiations. There is material weakness in precious metals with silver’s underperformance possibly tied to Tech weakness. Today’s macro data focus is on weekly ADP, home price data, regional Fed activity indicators, and Consumer Confidence (though spending has de-coupled from sentiment). US economic data calendar slate includes weekly ADP employment change (8:15am), February FHFA house price index, S&P CS home prices (9am), April Richmond Fed manufacturing index and Conference Board consumer confidence (10am) and Dallas Fed services activity (10:30am)

In premarket trading, OpenAI partners such as CoreWeave (CRWV -7%) and Oracle (ORCL -7%) are falling after the Wall Street Journal reported that the AI startup recently failed to meet targets for sales and new users, reviving worries about spending ahead of tech earnings. Stocks linked to the buildout of AI infrastructure — from computing providers to the makers of semiconductors and power equipment used in data centers — are also down after the Wall Street Journal report on OpenAI.

Magnificent Seven stocks are also mostly lower: Nvidia falls 2% on the OpenAI report (Apple +0.4%, Alphabet -0.1%, Amazon -0.9%, Meta Platforms -0.8%, Microsoft -1.2%, Tesla -1.2%)

Celestica (CLS) falls 13% after the maker of electronic components reported first-quarter results that featured smaller upside to expectations than in recent quarters. While it raised its full-year forecast, analysts said the company had been facing high expectations.

Dynatrace (DT) gains 4% on a report that Starboard Value LP took a stake and is pushing the company to better capitalize on the shift to artificial intelligence.

Erasca (ERAS) slides 40% after the biotech said one patient withdrew from the trial after a severe treatment-related adverse event and later died, according to a filing.

General Motors (GM) rises 4% after raising its profit outlook for the year by $500 million, saying its pickups and sport utility vehicles continue to sell even as gasoline prices soar due to the war in Iran.

LendingClub (LC) rises 9% after the online lender’s first-quarter revenue and net interest income beat the average analyst estimate.

Nucor (NUE) rises 2% after the steelmaker reported first-quarter earnings per share that beat the average analyst estimate as steel shipments were stronger than expected.

Rambus (RMBS) plunges 17% after the semiconductor device manufacturer reported first-quarter results that were largely in line with expectations, which analysts said was a disappointment in the wake of recent strength in the stock.

Sanmina (SANM) rises 7% after the electronics contract manufacturing services company’s second-quarter results beat expectations and it gave a full-year outlook that is seen as positive.

Solaris Energy (SEI) rallies 5% after the firm’s first-quarter Ebitda beat the average analyst estimate.

Spotify Technology falls 11% after reporting results that underwhelmed Wall Street, forecasting operating income in the current quarter that missed analysts’ estimates.

UPS (UPS) falls 3% after the courier left financial guidance unchanged. Its profit beat expectations in the first quarter.

In other corporate news, Barclays traders struggled to capitalize on a volatile quarter with returns falling short of their US rivals. Eneos is said to be the last remaining bidder for some of Chevron’s Asian assets in a deal that might be valued at more than $2 billion. Google and the Department of Defense signed a deal allowing the Pentagon to use Google’s AI models on classified work, the Information reported.

Futures are sharply lower after closing at a new all time high yesterday. The market’s hottest theme took a knock from a report that OpenAI failed to meet internal targets, fueling internal concerns that it may struggle to support its spending on AI infrastructure, the WSJ reported. OpenAI partners including Oracle, CoreWeave and AMD fell in premarket trading, while SoftBank tumbled 10% in Japan. Resurgent optimism about AI had prompted the market’s charge as the rest of the market lagged due to rising oil prices. Wednesday’s earnings from four hyperscalers will offer the rally another test.

“The single most important line item isn’t revenue or margins; it’s capex,” said Amanda Lyons, IT-sector lead and head of research at Energy Group Capital. “Any hint of slowing spend would be taken negatively for the ecosystem, but a sharp step-up would likely raise questions around returns.”

The WSJ report is reviving worries about how fast companies can monetize their huge AI spending (while still investing enough to compete), leaving Alphabet, Amazon.com, Meta and Microsoft with a delicate message to convey tomorrow. For context, OpenAI revealed in March that it was generating $2 billion in revenue per month, while Bloomberg has reported that Anthropic is on track for annual revenue of almost $20 billion.

“The rising oil price is starting to feature in macro data,” said Anna Macdonald at Hargreaves Lansdown. “The longer the crisis rolls on, the more severe the impacts will be, and the more we expect it will dominate investor attention.”

The AI theme is playing out in other ways too. Battery maker CATL raised $5 billion after a Hong Kong share placement amid surging demand for data center energy storage. The shares have soared 139% since their debut. And Arizona’s data-center building boom is coming up against community opposition and dwindling water availability.

Ahead of this week’s policy meetings by the Federal Reserve, ECB and Bank of England, traders expect officials to keep rates on hold. The outlook gets cloudier for subsequent meetings, with everything hinging on the duration of the Middle East war. Money markets see the ECB and BOE hiking as soon as June, while odds are for the Fed to keep rates on hold for the rest of the year.

Brent advanced for a seventh straight day. The White House said President Donald Trump will address a proposal from Iran to resume oil flows through Hormuz “very soon.” The dollar rose alongside global bond yields. WTI rose above $100 as tankers laden with Iranian oil idle just shy of the US blockade line. There’s not much sign of progress toward ending the war, with Trump planning to address the matter “very soon.” The president has told his advisers he’s not satisfied with Iran’s latest suggestions, the NYT reported, citing people briefed on the discussions.

European stocks have swung to session lows, with Stoxx 600 down 0.6%. European stocks swing between gains and losses on a busy earnings day, with healthcare weighing after Novartis missed profit estimates and reported its first sales decline in almost two years. The energy subindex is the best-performing sector as Brent rose above $110 again. Here are the biggest movers Tuesday:

SIG Group shares gain as much as 12%, the most since 2020, as the Swiss maker of carton packaging posted stronger-than-expected profits, putting it on track to recover from a challenging year

BP shares rise as much as 3.3% after 1Q profit beat analyst estimates. Analysts at RBC Capital note outstanding downstream and trading results

Nexans shares rise as much as 9.6% and on course to close at a new all-time high, after the cable and electrification specialist bolstered its position in the US through the acquisition of Republic Wire

AAK gains as much as 8.6%, the most since July, after the Swedish maker of vegetable oils and fats reported earnings. DNB Carnegie says the print is “strong on all points” with volumes growing and “good” free cash flows

Zealand Pharma gains as much as 7.2% after the Danish drug developer’s partner Boehringer Ingelheim said patients using its experimental obesity shot — called survodutide — experienced weight loss above 16% in a late-stage trial

Nordic Semiconductor gains as much as 9.1% after the Norwegian chipmaker reported its latest earnings. Analyst sees a strong report from the company, with a broadening out of revenue trends and strong 2Q guidance

Novartis shares fall as much as 5.1%, the most in more than a year, after the Swiss drugmaker reported weaker-than-expected core operating profit for the first quarter, as well as a drop in revenue

Barclays declines as much as 4.3% after the British lender booked an extra £105m provision for missold car loans and announced an impairment of roughly £200m for a “single name” charge said to be tied to the UK property lender Market Financial Solutions

Air Liquide fallsas much as 5.2% with analysts saying a miss in the French chemicals firm’s Large Industries division isappoints especially in light of hopes that the company could benefit from supply chain disruption in the Middle East

Valmet shares fall as much as 9.1%, to the lowest in more than a year, after first-quarter orders and adjusted Ebita undershot expectations, and the Finnish machinery supplier announced plans for temporary layoffs to save costs

Telenor shares fall as much as 10%, the most since 2020, after the telecom reduced Ebitda growth targets for its core Nordic markets and on the group level. The move comes less than three months since the guidance was first issued

Sweco shares drop as much as 8.8%, hitting their lowest level since May 2024, after the architecture and engineering consultancy reported sales and earnings that fell short of consensus expectations

Wartsila falls as much as 6.2%, the most since March 3, after the Finnish marine and energy industrial equipment maker reported its latest earnings. Analysts say the report, while a beat, is not necessarily reassuring

Earlier, Asian stocks traded lower but continued to hold near a February peak as traders awaited earnings from key companies in the global technology sector. The MSCI Asia Pacific Index fluctuated before falling as much as 0.4%, dragged by information technology firms. Financials were among the biggest boosts. Key gauges declined in Hong Kong, Australia and India while South Korean equities gained. The Topix gauge closed higher after Bank of Japan held interest rates as expected. Among the region’s tech firms that rely on outlays from the global hyperscalers, Advantest saw its stock slide Tuesday on a weak outlook and an indication of capacity constraints. Its fellow Japanese chip-equipment maker Tokyo Electron is among Asian firms reporting later this week, along with Chinese EV maker BYD.

Of the 150 S&P 500 companies to have reported so far this earnings season, 80% have beaten analysts’ forecasts, while 13% have missed. Earnings revisions for 2026, measured by Citigroup’s Earnings Revisions Index, have been improving since the start of the month. Companies have been holding or lifting guidance even as executives repeatedly flag an uncertain macroeconomic backdrop, according to JPMorgan strategists.

In FX, the Bloomberg Dollar Spot Index is up by 0.2% and reversing an earlier decline against the yen sparked by the Bank of Japan holding rates in a split decision.

In rates, bond markets are under pressure as oil prices rise, with Brent topping $111 to increase inflationary concerns. Treasury front-end yields are higher by 2bp-3bp, underperforming long end as Fed-dated swaps price in less easing; 10-year is 2bp higher near 4.36%, just off session high reached during London morning, outperforming German and UK counterparts by about 1bp-2bp. European bonds jolted by a jump in ECB CPI inflation expectations in March, though the initial drop on that has eased. German two-year yields up five basis points as traders increase ECB rate-hike bets and a similar move for two-year gilts, but declines have pared at the long-end in Europe and the UK. US session includes 7-year note auction at 1pm, the week’s third and final coupon auction following small tails for Monday’s 2- and 5-year note sales.

BlackRock Investment Institute said the war and elevated inflation will keep government bond yields higher for longer. But companies don’t seem to be feeling the hit yet. The fallout from the conflict, which broke out two-thirds of the way through the quarter, “has barely been visible,” says Bloomberg Opinion columnist John Authers, while current earnings forecasts look “very, very stretched.”

In commodities, June WTI crude futures are up almost 5%, rising above $101 and at session highs as blockades of the Strait of Hormuz curtail supply. Gold prices sinking, down by around $75 and testing $4,600/oz.

US economic data calendar slate includes weekly ADP employment change (8:15am), February FHFA house price index, S&P CS home prices (9am), April Richmond Fed manufacturing index and Conference Board consumer confidence (10am) and Dallas Fed services activity (10:30am)

Market Snapshot

S&P 500 mini -0.7%

Nasdaq 100 mini -1.2%

Russell 2000 mini -0.6%

Stoxx Europe 600 -0.5%

10-year Treasury yield +3 basis points at 4.37%

VIX +0.2 points at 18.26

Bloomberg Dollar Index +0.2% at 1198.04

euro -0.2% at $1.1697

WTI crude +4.8% at $101 barrel

Top Overnight News

President Donald Trump signaled he was unlikely to accept Iran’s latest proposal to end the conflict after Tehran proposed a plan that would reopen the Strait of Hormuz while leaving questions about its nuclear program for later negotiations. CNN

OpenAI recently missed its own targets for new users and revenue, stumbles that have raised concern among some company leaders about whether it will be able to support its massive spending on data centers. WSJ

China’s top leadership on Tuesday pledged to take more “forceful” measures to strengthen energy security and shore up business confidence, as the country faces economic headwinds from the protracted US – Iran standoff in the ME. Nikkei

The BoJ kept interest rates steady on Tuesday but three of its nine-member board proposed hiking borrowing costs, signaling policymakers’ concerns over inflationary pressures from the Middle East conflict. The central bank also sharply revised up its price forecasts and stressed vigilance to the risk of an inflation overshoot, signaling a strong chance of a rate hike in coming months. RTRS

Investors are reverting to a pre-war playbook of betting Asian stocks will outpace US peers due to the region’s central role in the AI boom. The MSCI Asia Pacific Index’s 14% surge so far this month has outpaced the S&P 500’s 9.9% gain. BBG

ECB survey reveals a spike in inflation expectations as consumers react to fallout from the Iran war. Additionally, the survey revealed a larger than expected tightening of credit standards due to higher perceived risks and lower risk tolerance. ECB

Keir Starmer faces a high-stakes vote today on whether to begin an investigation into his assurances to Parliament that due process was followed in Peter Mandelson’s appointment as US ambassador. BBG

Wall Street dealers’ Treasury holdings have jumped to the highest level since the global financial crisis as the Trump administration’s cut to regulation nudges banks back into the $31tn debt market. FT

Foreign-based automakers have warned the Trump administration that they are looking at pulling their cheapest car models out of the U.S. market if the U.S.-Mexico-Canada Agreement isn’t renewed or is watered down, according to people familiar with the discussions. WSJ

Thus far in 2026, there have been 25 IPOs greater than $25 million in value, totaling $14 billion in gross proceeds. This represents a nearly 80% increase in both the number and value of IPOs relative to this time last year. Roughly 40% of this year’s IPOs have been Industrials companies compared with the historical annual average of 10% since 1995. In contrast, there have been no IPOs YTD in the Information Technology sector despite the sector representing 25% of IPOs since 1995: GS

Iran News

US President Trump has told advisers he is not satisfied with Iran’s latest proposal to reopen the Strait of Hormuz and end the war, NYT reported; a US official said that accepting it [the Iran proposal] could appear to deny Trump a victory. The proposal also called on the United States to end its naval blockade, but would have set aside questions about what to do with Iran’s nuclear program. A US official also said that accepting it [the Iran proposal] could appear to deny Trump a victory. US officials say Iran’s leadership has not authorised its negotiators to make concessions on the nuclear deal, frustrating any attempts to forge a compromise or peace agreement. At the heart of the debate over whether to accept the Iranian proposal were discussions in the Trump administration about the issue of economic leverage and what further American military operations would be needed to get Tehran to make significant concessions in negotiations. Some administration officials believe that continuing the blockade for two more months would cause significant long-term damage to Tehran’s energy industry. “Without a resumption of military action, there is little reason to think the Iranian position will shift.”.

US President Trump is reportedly sceptical of Iran’s Strait of Hormuz proposal, WSJ reported citing sources; said White House will continue to negotiate with Iran; White House expected to provide its response and counterproposals in the coming days. President Trump and his national security team are sceptical of Iran’s offer to open the Strait of Hormuz in exchange for tabling discussions on its nuclear work, according to US officials. Trump discussed the offer with aides on Monday morning, expressing doubts about Iran’s good faith and its willingness to meet his key demand of ending nuclear enrichment and committing never to develop a nuclear weapon. The US plans to continue negotiations with Iran, with the White House expected to provide its response and counterproposals in the coming days. White House spokeswoman stated that the US will not negotiate through the press and that anything not announced by President Trump or the White House should be considered speculation.

US and Iran are not as far apart as they seem, and that the first part of any potential agreement will focus on opening the Strait of Hormuz without restrictions or fees, CNN reported, citing sources. The US and Iran may not have met for a second round of talks in Pakistan, but the two sides are not as far apart as they seem, according to sources familiar with the mediation process. Intense diplomacy continues behind the scenes, the sources say, and ongoing talks are centred around a staged process in which the first part of a potential deal would focus on returning to the status quo before the war and reopening the Strait of Hormuz without restrictions or tolls. The issue of Iran’s nuclear program – which both the US and Israel cited as their casus belli – would be addressed later. US President Donald Trump has previously said that any deal would require Iran to forfeit its supply of near bomb-grade uranium and give up enrichment, demands Iran has steadfastly refused to accept. According to the sources, mediators are applying pressure on both sides to reach an agreement, with the next few days being especially crucial. Hanging over it all is the chance that the US may decide to disengage and return to war.

Israeli PM Netanyahu reportedly told US President Trump the Israel-Lebanon ceasefire is fragile, N12 reported citing sources. Netanyahu told Trump that he believes that the strategy he has chosen is correct for now, but that it can only succeed if there is no compromise with the Iranians regarding the Strait of Hormuz. Israel and the US see eye to eye on the Iranian issue. n discussions in Israel, the Iranian difficulty in pumping oil from the wells is raised, which puts them in great distress.

“Netanyahu informed his ministers that there is no more he can do in Lebanon and this is what Washington wants”, Al Jazeera reported citing an Israeli Radio source.

Pakistan Defence Minister said “our earnest efforts to end the conflict, impacting the entire region and beyond, are ongoing, and we remain hopeful of achieving a positive outcome”, reported Anas Mallick.

Iran’s Deputy Defence Minister Talaei-Nik said Tehran is ready to share its defensive weapons capabilities with members of Shanghai Cooperation Organisation.

“Kuwaiti News Agency: The Gulf Cooperation Council holds an extraordinary summit in Jeddah”, Sky News Arabia reported.

“Iran’s Foreign Minister is NOT returning to Pakistan following his Russia visit”, journalist Mallick reported; “team is currently in consultation mode and will return when there to Islamabad, soon, when they think there is headway in talks.”.

reported of Israeli airstrikes in the south of Lebanon, Al Jazeera reported.

US President Trump is unlikely to accept Iran’s plan, according to CNN citing sources; reopening the strait without resolving the nuclear issues could remove a key piece of US leverage.

“Guided-missile destroyer USS Rafael Peralta (DDG 115) enforces the U.S. blockade of Iranian ports against M/T Stream after it attempted to sail to an Iranian port, April 26”, US CENTCOM said.

US President Trump is unhappy with the Iranian proposal, according to a US official.

Taiwanese Defense Ministry said that Taiwan has spotted two Chinese warships operating in waters near the Penghu Islands and has sent its own naval and air forces to keep watch.

US Secretary of State Rubio said the ceasefire in Iran is unique because Israel is at war with Hezbollah, not Lebanon.

US Secretary of State Rubio said the Iran offer is better than we thought. Indications that Iranian Supreme Leader Khamenei is alive. Direct communications with Iran are very rare and discreet. Level of sanctions and pressure on Iran is extraordinary. Hopes the rest of the world will sanction Iran.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded broadly weaker, as risk sentiment weakened amid reports that US President Trump is unlikely to agree to Iran’s proposal. ASX 200 started the session on the backfoot, and held onto its earlier losses. Sectors were broadly in the red, as Utilities underperformed while Energy was supported by higher crude prices. Nikkei 225 opened flat but fell lower, a move which was later exacerbated after the hawkish hold by the BoJ. The Bank upgraded inflation outlook and downgraded growth, with FY27 growth only modestly cut. The index fell back towards the 60,000 handle. For single stock stories, DENSO reported earning in which all metrics rose annually, but the Co. cut its FY net and op. profit guidance while stating its withdrawal of the proposal of Rohn acquisition. KOSPI was the outperformer, with LG Electronics among those that lifted the index after reports that the Co.’s CEO is to meet Nvidia CEO Huang’s daughter to discuss strategic cooperation. Hang Seng and Shanghai Comp. followed the broadly negative bias. CATL’s HK shares were under pressure after the Co.’s announcement of a plan to raise over HKD 39bln in private share placement to step up expansion in its renewables business.

Top Asian News

China State owned refiners have begun applying for government permits that would allow them to resume fuel exports in May, Bloomberg reported.

European bourses (STOXX 600 U/C) spent most of the European morning a touch lower after several geopolitical updates spurred energy benchmarks higher on the day. On the geopolitical front this morning, journalist Mallick said Iran’s Foreign Minister was not returning to Pakistan following his Russia visit – a post which soured the risk tone. European sectors opened mixed, and continue this way. Energy tops the pile amid BP’s (+3.3%) stellar Q1 results, while Healthcare sits at the bottom amid losses in the sector’s second-largest constituent Novartis (-2.6%), alongside Bayer (-2.7%). The former reported disappointing earnings, whilst the latter is hit on reports that the US Supreme Court is split over Bayer’s fight against Roundup lawsuits.

Top European News

ECB Consumer Expectations Survey: 1yr CPI expectations 4% (exp. 2.8%, prev. 2.5%), 3yr CPI expectations 3.0% (exp. 2.6%, prev. 2.5%).

Trade/Tariffs

Indonesia’s Economy Minister said they are going to cut the import duty for naphtha to 0%.

FX

FX shows a risk-off bias with all G10 currencies lower against the Buck.

DXY is back above its 100 & 200 DMAs around 98.50, after falling below those levels on Monday. The buck saw weakness after the BoJ announcement, where the vote split was more hawkish than expected at 6-3. However, following the meeting, the USD moved higher in tandem with crude benchmarks after news that Iran’s Foreign Minister was not returning to Pakistan following his visit to Russia.

In addition to this, Ueda at the BoJ presser failed to support bets for a June hike, with the initial move seen on the 6-3 vote split paring to bring USD/JPY to above 159.50, to pre-announcement levels (ventured as low as 158.96). MUFG said the BoJ meeting was unlikely to trigger a sustained reversal of the bearish JPY trend that has been in place since the Middle East conflict started in late February

Elsewhere, NOK fares the best against the USD amid firmer oil prices. NOK/SEK, +0.4%, continues to edge towards the 1.00 mark not seen since November 2024, with a session high of 99.63.

GBP is one of the worst performers in the G10FX space, with UK Political developments in the spotlight ahead of a debate & vote on whether PM Starmer should be referred to the Privileges Committee (Full analysis on the headline feed at 09:05 BST) GBP/USD traders lower by 0.3% and breached the 1.35 mark, while EUR/GBP has been creeping higher throughout the session but remains flat on the day.

Japanese Finance Minister Katayama said volatility in crude is affecting FX, ready to take decisive action; will closely coordinate with the US and will act when necessary; standing by around the clock.

Fixed Income

Another bearish start for fixed income as energy climbs, and with some influence from a hawkish hold by the BoJ. (Details on geopols can be found in the commodities section below).

Most recently, the ECB SCE saw an increase in inflation expectations for the next 12 months, and for three years ahead, both saw a significant increase to 4.0% (prev. 2.5%) and 3.0% (prev. 2.5%), respectively. By way of comparison, the March baseline HICP peak was 2.6% in 2026, the adverse 3.5% for the same period, while the severe peaked at 4.8% in 2027. As such, 12-month expectations are hotter than all but the severe scenario, a point that adds a measure of hawkishness ahead of Thursday’s ECB. Though this view is somewhat offset by the tightening of credit conditions and weaker loan demand evidenced in the BLS, a survey that was released alongside the CSE.

Amidst all this, Bunds down to a 124.87 base with a downside of nearly 50 ticks. The low was printed just after the ECB SCE release.

USTs down to a 110-26 base into a session that is likely to once again be dominated by geopolitics, earnings and looking ahead to the FOMC on Wednesday. We do get supply, 2yr FRN and a 7yr note offered, following a strong 2yr and mixed 5yr on Monday.

JGBs gapped lower on the resumption after the BoJ announcement, before then filling the move in short order. To recap, the BoJ was a hawkish-hold with three dissenters in favour of a hike, citing price concerns. Forecasts showed an increased inflation view, while the growth view was cut. Thereafter, Ueda was non-committal regarding the timing of the next hike, and seemingly attempted to temper expectations around June, commentary that had little JGBs impact but spurred notable JPY moves.

Gilts gapped lower by 21 ticks, acknowledging the above, and have since fallen another 29 to an 86.51 trough. If the move continues, we look to 86.00 before 85.91 from the last week of March. Gilts underperform marginally, awaiting the start of the debate and then vote on whether UK PM Starmer should be referred to the Privileges Committee or not; full primer available at 09:05BST.

Commodities

Crude prices are once again on a stronger footing this morning, with a number of sentiment-hitting headlines helping to lift demand for energy. In brief, CNN reported that President Trump is not satisfied with the Iranian proposal, adding that he is unlikely to accept it. But the piece did suggest that the US and Iran are not as far apart as they seem. Thereafter, Pakistani journalist Mallick reported that Iran’s Foreign Minister would not return to Pakistan following his visit to Russia, adding that he would only head back to the region if his team thinks there is “headway in talks”. This helped to spur some strength in both WTI and Brent, by around a USD 1/bbl.

As it stands, WTI holds at the upper end of a USD 96.24-99.66/bbl range, whilst Brent sits at the upper end of a USD 107.81-111.86/bbl range.

Sticking with geopols, but over in Europe, Ukraine said that it had struck Russia’s Tuapse oil refinery. It is considered amongst the top 10 largest in the country, with a capacity of 240k BPD. Elsewhere, on the supply front, Bloomberg reported that Saudi Arabia may cut its June OSP to Asia, citing easing demand.

Spot gold is lower this morning, by around a percent, and currently resides towards the lower end of a USD 4,614-4,701/oz range. Ultimately, spot gold has been pressured throughout the Iranian conflict, given the inflationary implications – a theme which appears to have played out today; the mild strength in USD this morning is also a factor.

Base metals also hold a negative bias – likely hampered by the downbeat risk tone seen during overnight trade. 3M LME Copper trades within a USD 13,105.98-13,264/t range.

Saudi Arabia reportedly may cut its official June crude selling prices to Asia as spot premiums eased and demand eased, Reuters reported.

Eneos (5020 JT) is reportedly the final bidder for some of the Asian assets of Chevron (CVX).

ADNOC has told some oil buyers to pick up Gulf supply outside the Strait of Hormuz, as producers look to diversify to other routes and bring their oil to the market, Bloomberg reported. ADNOC has told customers of the availability of cargoes for loading off Fujairah.

ADNOC is planning to invest tens of billions of dollars to build a natural gas business in the US to diversify its commodity exposure and the XRG business.

Ukrainian drones attack Russia’s Tuapse oil refinery, causing a fire, according to authorities.

China allows the purchases of banned BHP (BHP AT) portside cargoes following a deal with the Co., according to sources.

Venezuela is to raise crude shipments to 1.06mln bpd and fuel sales to 134k by year-end, PDVSA vice president said.

Central Banks

BoJ Governor Ueda said there are possibilities of a rate hike if either upward risks to prices emerge or downside risks to the economy are limited. By June, probably no big upward pressure appears in consumer price data. It is possible to decide before confirming upward price pressure in price data. Communicating closely with government on monetary policy. When asked if a rate hike is not possible while the Strait of Hormuz is closed, the decision would depend on inflation risks and the economy beyond that. Not thinking there is a high likelihood of the current situation resembling the early 1970s. If the trend inflation overshoots by 2% by a big margin, then strong tightening could be required. In the process of adjusting rates towards neutral, all other conditions being equal. Japan’s exposure to private credit is not big; it requires caution, given transparency in the sector is low. Unless significant downside pressure to the economy, a rate hike is possible. Rate hike decision and QT adjustment will be separate. Inflation upward risk could be a reason for raising rates, but not the only reason. Can not say how many months it would take to gauge timing of next rate hike, will look to see if underlying inflation has a clear upward risks. Need to be mindful of further economic slowdown depending on supply shock levels; Japan economy has some degree of endurance.

BoJ maintains its short-term interest rate at 0.75%, as expected; vote split 6-3 to hold (exp. near-unanimous); Nakagawa, Takata and Tamura voted to hike by 25bps to 1.0%.

BoJ Outlook Report: Real GDP: Fiscal 2026 median forecast 0.5% (prev. 1.0%). Fiscal 2027 median forecast 0.7% (prev. 0.8%). Fiscal 2028 median forecast 0.8%. Core CPI. Fiscal 2026 median forecast 2.8% (prev. 1.9%). Fiscal 2027 median forecast 2.3% (prev. 2.0%). Fiscal 2028 median forecast 2.0%. Dissenters (voted for 25bps hike).

BoJ’s Takata: price stability target had been more or less achieved and that risks to prices in Japan were already skewed to the upside due to the second-round effects of price rises stemming from overseas developments.

BoJ’s Tamura: Considering that, with risks to prices becoming significantly skewed to the upside, the bank should set the policy interest rate as close to the neutral rate as possible.

BoJ’s Nakagawa: Risks to prices skewed to the upside under accommodative financial conditions. Monetary policy Will scrutinise timing, pace of policy adjustment with a close eye on economic and price impact from the Middle East developments.

Japanese Economy Minister Kiuchi will attend the BoJ policy meeting, hopes the BoJ communicates and coordinate policy closely with the government and work towards sustainably achieving a 2% inflation target.

ECB BLS: Banks tightened credit standards across all loan categories, driven by higher perceived risks and lower risk tolerance. Banks tightened credit standards across all loan categories, driven by higher perceived risks and lower risk tolerance. Banks expect to also tighten credit standards in the second quarter, influenced by geopolitical tensions, energy developments, and higher funding costs. Loan demand from firms and households expected to decrease, resulting from reduced financing for fixed investments, lower consumer confidence, and decreased spending on durables. Nearly half of euro area banks use securitisation to grant new loans, manage credit risk and enhance liquidity and funding, relying on non-bank financial entities to purchase securitised loans.

PBoC guided banks to increase lending in April, according to sources.

Geopolitics

Ukrainian drones attack Russia’s Tuapse oil refinery, causing a fire, according to authorities.

US Event Calendar

9:00 am: United States Feb FHFA House Price Index MoM, est. 0.1%, prior 0.1%

10:00 am: United States Apr Richmond Fed Manufact. Index, est. 0.7, prior 0

10:00 am: United States Apr Conf. Board Consumer Confidence, est. 89, prior 91.8

DB’s Jim Reid concludes the overnight wrap