Category: News

DOJ, CTFC Investigating $2.6 Billion In Suspicious Iran War Oil Trades

DOJ, CTFC Investigating $2.6 Billion In Suspicious Iran War Oil Trades

U.S. authorities are investigating more than $2.6 billion in oil futures shorts that landed within minutes of major announcements tied to the 2026 U.S.-Iran conflict. The Department of Justice (DOJ) has joined the Commodity Futures Trading Commission (CFTC) in a widening inquiry into potential misuse of material non-public information in one of the most liquid and geopolitically sensitive commodity markets on earth, ABC News reports.

The trades in question involved bets that oil prices would fall shortly before major U.S. or Iranian announcements tied to the Iran war. .

The Trades

Data sourced from the London Stock Exchange Group (LSEG) – which captures exchange-traded futures flow but strips identities – reveals four distinct clusters of aggressive shorting in WTI and Brent crude futures:

March 23: >$500 million in shorts executed in a one-minute burst roughly 15 minutes before President Trump announced a five-day delay on planned strikes against Iran’s energy infrastructure. Oil prices subsequently plunged ~15%.

April 7: ~$960 million short position placed hours before the temporary ceasefire announcement (oil dropped sharply on the news).

April 17: $760 million short bet executed ~20 minutes before Iranian Foreign Minister Abbas Araghchi declared the Strait of Hormuz open to commercial traffic.

April 21: $430 million additional short layer placed 15 minutes before Trump extended the ceasefire.

Total exposure: >$2.65 billion in directional bets that oil’s geopolitical risk premium was about to collapse. These were institutional-sized clips that moved the tape.

The CTFC began investigating suspicious oil trades last month, which has now expanded under DOJ scrutiny.

Oil futures (CL on CME/NYMEX and Brent on ICE) price in both physical supply/demand and a geopolitical risk premium. When headlines shift from “imminent strikes” or “Hormuz closure” to “ceasefire” or “shipping lanes open,” that premium evaporates in minutes. A well-timed short captures the entire move plus any subsequent contango/backwardation shift.

These are classic event-driven alpha trades – except the “alpha” here appears to have arrived with near-perfect foresight. In futures markets, unlike equities, there is no uptick rule and leverage is extreme (often 10-20x on margin). A few basis points of edge on a $2.6 billion book compounds into a staggering P&L for the desk or fund that executed it.

Regulatory Escalation

The CFTC has primary jurisdiction over commodity futures manipulation and insider trading under the Commodity Exchange Act. Its enforcement division can subpoena “Tag 50” firm identifiers from exchanges and pursue civil penalties, disgorgement, and trading bans. The DOJ’s involvement signals potential criminal exposure – wire fraud, securities/commodities fraud, or conspiracy charges – which carries prison time.

Congressional Democrats moved quickly:

Senators Elizabeth Warren and Sheldon Whitehouse formally requested a CFTC investigation on April 9–10, citing a “recurring pattern” of trades anticipating Trump administration decisions.

Rep. Sam Liccardo wrote to both the SEC and CFTC on April 17, explicitly referencing possible violations of the STOCK Act (which already prohibits federal officials from trading on non-public info in futures markets).

Rep. Ritchie Torres later pushed to expand the probe to the April 17 Hormuz trade.

The White House itself issued an internal memo on March 24 warning staff against using confidential information for futures or prediction-market bets – a tacit admission that the temptation was real.

CFTC Chairman Michael Selig has been unambiguous: “We will find you, and you will face the full force of the law.”

Unanswered Questions

Who were the counterparties? LSEG data does not name them. CFTC/DOJ subpoenas to CME and ICE will. Expect hedge funds, prop shops, or family offices with deep political or intelligence ties to surface – or perhaps entities with access to real-time diplomatic cables.

Was this pure MNPI or sophisticated OSINT + positioning? The minute-level clustering before public posts makes the former more plausible.

What about prediction markets? Polymarket and similar platforms have faced parallel scrutiny. Bills introduced in late March aim to ban or restrict federal officials and Congress from trading event contracts.

Precedent and spillover? Energy desks, shipping companies (tankers through Hormuz), and even defense contractors with Iran exposure are now on notice. Any large, well-timed position in CL, Brent, or related equities (XOM, CVX, tanker stocks) will face heightened post-trade analysis.

Of course, traders of size can now assume every major geopolitical headline now carries a compliance overlay. Position sizing on event risk just became more expensive thanks to regulatory tail risk. For funds with political connections or Washington presence: the bar for “plausible deniability” has been raised dramatically.

The CFTC and DOJ have requested and are receiving detailed trading data and order book records from CME and ICE, so the next 30–60 days should be interesting.

Tyler Durden

Thu, 05/07/2026 – 09:55

https://www.zerohedge.com/political/doj-ctfc-investigating-26-billion-suspicious-iran-war-oil-trades

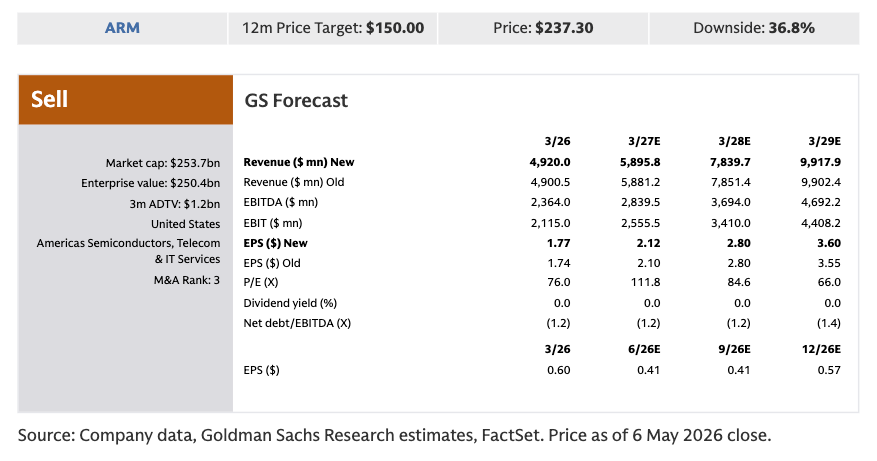

Goldman Cuts ARM To Sell On Shocking Smartphone Weakness

Goldman Cuts ARM To Sell On Shocking Smartphone Weakness

Arm Holdings ADRs sank nearly 9% in premarket trading, on track for the largest intraday decline in almost a year, after the chip-architecture company reported softer-than-expected fiscal fourth-quarter royalty revenue tied to a slowdown in the smartphone industry, while assuring investors that data center demand can offset the slump.

During an earnings call, Wells Fargo analyst Joe Quatrochi asked Arm CEO Rene Haas:

“Clearly, data centers are very strong and accelerating, but then how do you think about consumer electronics, smartphones, et cetera?”

Haas responded:

So in terms of Q4, as we said before the quarter, we had a bit of a tough comp in that. We had a particularly strong ramp of maybe 400 [ph], a year ago, more so than what we expected this year.

As a result, you saw a bit of a slowdown in royalty revenue. As indicated by our guidance, we’re expecting that to get back to the kind of 20% range by Q1.

So I would say within — you know, the assumptions within our expectations are, we will probably continue to see unit growth, I think actually flip to negative for the mobile market in this last quarter. We’re going to continue to see very flattish, maybe slightly negative numbers for the overall market.

Haas’ comments about the smartphone slowdown are key because Arm’s smartphone exposure remains large, and mobile application processors accounted for about 46% of its total royalty revenue in 2025.

Haas has made clear to analysts that the push into data centers and other markets will help offset Arm’s high exposure to a softening smartphone market.

Royalties, a closely watched metric for Arm, generated $671 million in fourth-quarter revenue, missing the Bloomberg Consensus estimate of $693.3 million.

“We’re seeing the acceleration of Arm being a significant player in the data center,” Haas said in an interview, quoted by Bloomberg.

As for the rest of fourth-quarter earnings, Arm beat on total revenue, adjusted EPS, operating income, margins, and licensing revenue. Revenue rose 20% year over year to $1.49 billion, slightly ahead of estimates, while adjusted EPS of 60 cents beat the 58-cent estimate. Adjusted operating income also beat at $731 million, with a very strong operating margin of 49.1%.

The strongest part of the report was license and other revenue, which jumped 29% year over year to $819 million, well above estimates of $775.6 million. That suggests strong customer demand for future Arm designs, particularly in AI, data centers, and new chip programs.

But as we noted above, royalty revenue missed expectations …

Here’s a snapshot of the fourth quarter (courtesy of Bloomberg):

Adjusted EPS 60c vs. 55c y/y, estimate 58c

EPS 29c

Total revenue $1.49 billion, +20% y/y, estimate $1.47 billion

License and other revenue $819 million, +29% y/y, estimate $775.6 million

Royalty revenue $671 million, +11% y/y, estimate $693.3 million

Annualized contract value $1.66 billion, estimate $1.58 billion

Adjusted net income $641 million, estimate $624.3 million

Adjusted gross profit $1.47 billion

Adjusted gross margin 98.3%, estimate 98.1%

Adjusted operating expenses $734 million, estimate $743.6 million

Adjusted operating income $731 million, estimate $696.4 million

Adjusted operating margin 49.1%

Adjusted free cash flow $152 million, estimate $374 million

Arm’s first-quarter forecast is broadly in line on revenue, better on earnings, and better on costs (courtesy of Bloomberg):

Sees revenue $1.21 billion to $1.31 billion, estimate $1.25 billion (Bloomberg Consensus)

Sees adjusted EPS 36c to 44c, estimate 37c

Sees adjusted operating expenses about $760 million, estimate $803.1 million

In markets, Arm ADRs sank nearly 9%, the largest intraday decline since July 31, 2025, of -13.5%. On the year, shares are up 117%.

Goldman analyst James Schneider told clients following earnings, “We expect the stock to be range-bound following revenue and EPS guidance that was just above the Street, with an increase to demand expectations for the company’s CPU business.”

“We are Sell rated on ARM given our concerns around the near-term pressures in the royalty business, the lack of clear competitive advantage relative to peers in chip manufacturing, and elevated valuation relative to peers – but could be more constructive if we see greater evidence of an acceleration in royalty growth or more visibility into greater scale in chip manufacturing,” Schneider added.

Additional analyst commentary (courtsey of Bloomberg):

Bloomberg Intelligence analyst Kunjan Sobhani

“Arm’s fiscal 4Q results reflect a mixed near-term setup, with handset and memory-related weakness weighing on royalties, but partly offset by persistent AI strength.”

Daiwa analyst Louis Miscioscia

Arm’s royalty revenue missed due to a shortfall in lower-end cell phone demand, which was weaker than expected due to the higher cost of memory.

Evercore ISI analyst Mark Lipacis (outperform, price target $326)

Lipacis was more bullish, saying that after examining other trillion dollar market cap companies, believe “ARM has the similar necessary ingredients to cross that $1T threshold themselves”

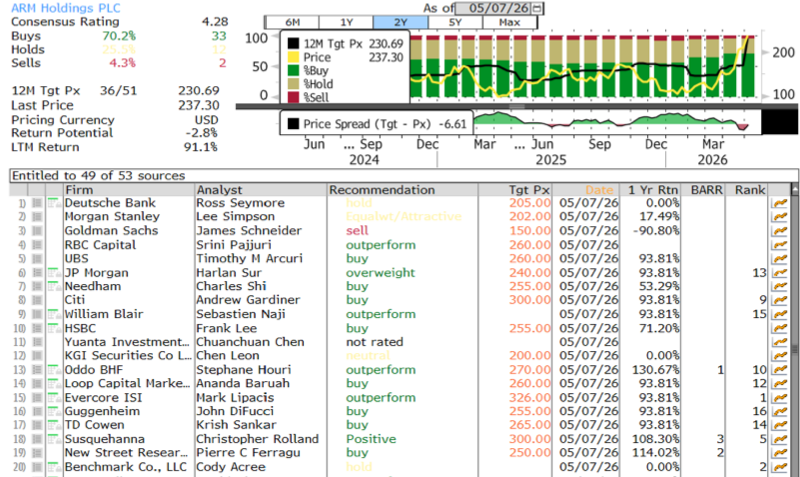

Bloomberg data shows most of Wall Street is bullishing on ARM… Goldman and AlphaValue are the only with “Sell” ratings …

Professional subscribers can read the full GS Earnings ARM note here at our new Marketdesk.ai portal

Tyler Durden

Thu, 05/07/2026 – 09:20

Over 80% Of Young Adults Believe Economy Is ‘Bad/Terrible’ And We’re Seeing The Consequences All Over America

Over 80% Of Young Adults Believe Economy Is ‘Bad/Terrible’ And We’re Seeing The Consequences All Over America

Authored by Michael Snyder via The Economic Collapse blog,

Decades of economic decline have brought this country to a breaking point. The vast majority of the population is barely scraping by from month to month as prices continue to rise, thousands of stores and restaurants close, foreclosures spike to alarming levels and the middle class continues to shrink. Now the crisis in the Strait of Hormuz threatens to make things a whole lot worse, and a lot of people are justifiably concerned about what this will mean for their futures.

Our young adults are being hit particularly hard. If you purchased a home 20 or 30 years ago, you are insulated from what is really going on out there. Housing costs are more unaffordable than ever, and many young people have completely given up on the dream of homeownership. Meanwhile, the employment market has gotten very tight, and this is especially true for entry-level jobs.

Do you know anyone under the age of 40 that is doing really well in this economy?

Yes, there are some exceptions, but in general our young adults are really struggling.

As a result, homelessness is at record levels and hordes of drug addicts are roaming the streets of our major cities.

If you doubt this, just check out this video that shows what has happened to the once great city of Los Angeles.

It was once a playground for the rich and famous, but now it has been transformed into a rotting, decaying hellhole.

It is undeniable that most of our young adults hate this economy.

In fact, a new survey that was just released found that a whopping 84 percent of Americans between the ages of 18 and 24 believe that economic conditions in the U.S. are either “bad” or “terrible”…

A recent survey by Generation Lab found that more than 8 in 10 young adults rate economic conditions in the U.S. as either bad or terrible.

The survey, conducted April 26-29, found that 55 percent of 546 respondents ages 18-24 said they view the economy as bad, while 29 percent said it was terrible.

The same survey discovered that 81 percent of Americans between the ages of 25 and 29 believe that economic conditions in the U.S. are either “bad” or “terrible”…

As for those in the 25-29 age range, 52 percent of 266 such respondents said the economy was bad. About 3 in 10 respondents said it was terrible, for a combined percentage of 81 percent that view the economy negatively.

This is what a long-term economic collapse looks like.

Many people have had their heads in the sand for years, but meanwhile economic conditions have continued to deteriorate all around us.

A different survey that polled American adults of all ages found that 78 percent of us do not feel financially secure at this stage…

A new Intuit Credit Karma/Harris Poll study found that 78% of Americans don’t feel financially secure, even if they’ve been saving and playing by the rules.

Moreover, nearly 3 in 4 Americans (72%) shared that their current financial standing makes them feel like they will never have enough money to achieve the American dream.

Let’s get real.

These numbers didn’t suddenly appear in a vacuum.

The truth is that our standard of living has been declining for a very long time.

I am about to share something with you that is absolutely shocking.

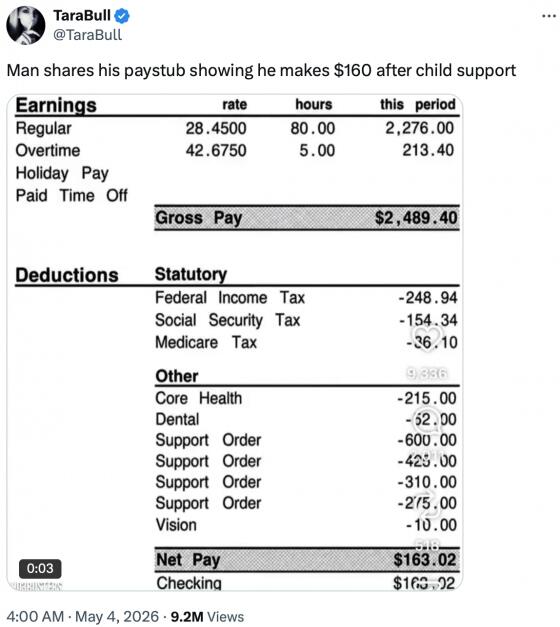

One man recently shared his paystub that shows what he brings home every two weeks.

After taxes, healthcare and child support, his net pay after working 85 hours is just $163.02…

How is he supposed to live on that?

I am so frustrated with those that think that everything is going to be just fine.

The number of foreclosure filings in the U.S. skyrocketed in 2025, and in the first quarter of this year they were 26 percent above last year’s blistering pace…

The Wall Street Journal reported that data from Attom shows the number of U.S. properties with a foreclosure filing has trended up to nearly 119,000 in the first quarter, an increase of 26% from the same period last year.

That figure is the highest since the first quarter of 2020, when mortgage relief measures implemented to mitigate the economic impact of COVID shutdowns led to a steep decline in foreclosures.

Unfortunately, the crisis in the Strait of Hormuz is making things even worse.

The average price of a gallon of gasoline in California is now up to $6.114…

California gas prices have climbed to eye-watering levels, with one rural county emerging as one of the most expensive fuel markets in the United States.

Mono County, a remote area in eastern California just east of Yosemite National Park, is seeing average prices close to seven dollars per gallon, according to AAA data. That compares with a statewide average of $6.114 per gallon and a national average of $4.457.

As I discussed yesterday, some residents of Los Angeles are now paying more than 8 dollars a gallon.

Higher gasoline prices will mean that Americans have even less discretionary income to play around with.

Some restaurant chains are already feeling this…

Wingstop, a chicken-wing chain that touts its affordability, said that higher fuel prices contributed to an 8.7% decline in quarterly same-store sales.

The chain’s CEO, Michael Skipworth, said Wednesday on a call with investors that it was “extremely difficult for anyone to predict this macro environment,” adding that he expects shrinking sales over this year in part because of expectations that gas prices will remain high.

This is not something that may or may not happen someday.

This is happening right now, and we are witnessing the consequences all over America.

In Los Angeles, rampant social decay has become a way of life…

Reality star-turned-Los Angeles mayoral candidate Spencer Pratt shared a devastating must-see campaign advertisement on X, showing how dire the situation is in LA under Democrat leadership.

The somber video, titled “City of Angels, Fallen – Part 1,” uses a rapid montage of raw street footage, news clips, and on-screen text to show just how far Los Angeles has declined under Karen Bass and Democrats, noting, “business as usual is a death sentence.”

Included in the video are stark images of homeless camps, a person lying unconscious or asleep on a dirty sidewalk next to trash bags, a sandwich on a plate, scattered belongings, and individuals who appear to be in the throes of drug abuse.

How could we have allowed this to happen?

According to Pratt, there are 70,000 drug addicts that are roaming the streets…

Speaking on fire recovery, Pratt notes, “The city failed everyone. The insurance companies failed everyone.”

He continues, “Mothers who want to go to the park but don’t want to inhale fentanyl from the 70,000 drug addicts that the Mayor currently let’s live on our streets.”

Of course this isn’t just happening in Los Angeles.

In Seattle, street violence has become so common outside of one McDonald’s restaurant that it has become known as “McStabby’s”…

Two thugs were caught on video viciously beating an elderly man outside of ‘America’s scariest McDonald’s.’

The Seattle restaurant is so dangerous it is nicknamed ‘McStabby’s’, and bans customers from going inside due to constant mayhem.

In the latest chaotic scene, two men were seen standing on the street outside the eatery around 10pm on April 19 when a frail 77-year-old man walked towards them.

The two men then approached the victim before one struck him in the head.

Needless to say, it isn’t just old men that are being viciously attacked for no reason.

One very unfortunate 33-year-old man is on the verge of death after being hit in the head with a hammer more than a dozen times…

A 33-year-old Seattle man is fighting for his life after his mother says a stranger repeatedly hit him in the head with a hammer in an unprovoked assault.

Lisa Driscoll is calling for justice after her son, 33-year-old George Miller, was beaten repeatedly with a hammer just after midnight Monday outside the Renaissance Hotel. She says a stranger hit him in the head more than a dozen times.

“It was an evil, brutal, unprovoked, horrific attack,” Driscoll said. “Someone who was reported to appear to be hunting to attack someone crossed over, took a hammer out of their backpack and started beating him over the head repeatedly.”

Whether we like it or not, this is our country now.

We have raised an entire generation of young people that is simply not equipped to deal with very harsh economic conditions.

Sadly, economic conditions are only going to get harsher.

It is time to wake up, because a nightmare scenario really is upon us.

Michael’s new book entitled “10 Prophetic Events That Are Coming Next” is available in paperback and for the Kindle on Amazon.com, and you can subscribe to his Substack newsletter at michaeltsnyder.substack.com.

Tyler Durden

Thu, 05/07/2026 – 09:00

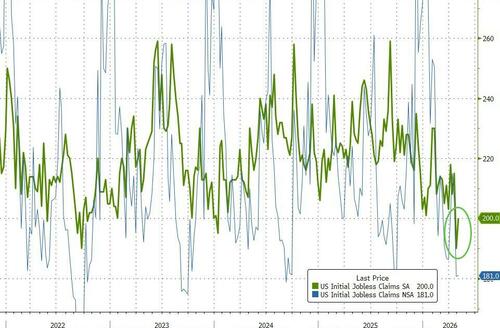

Jobless Claims & JOLTs Confirm ‘Higher Hire, No Fire’ Economy

Jobless Claims & JOLTs Confirm ‘Higher Hire, No Fire’ Economy

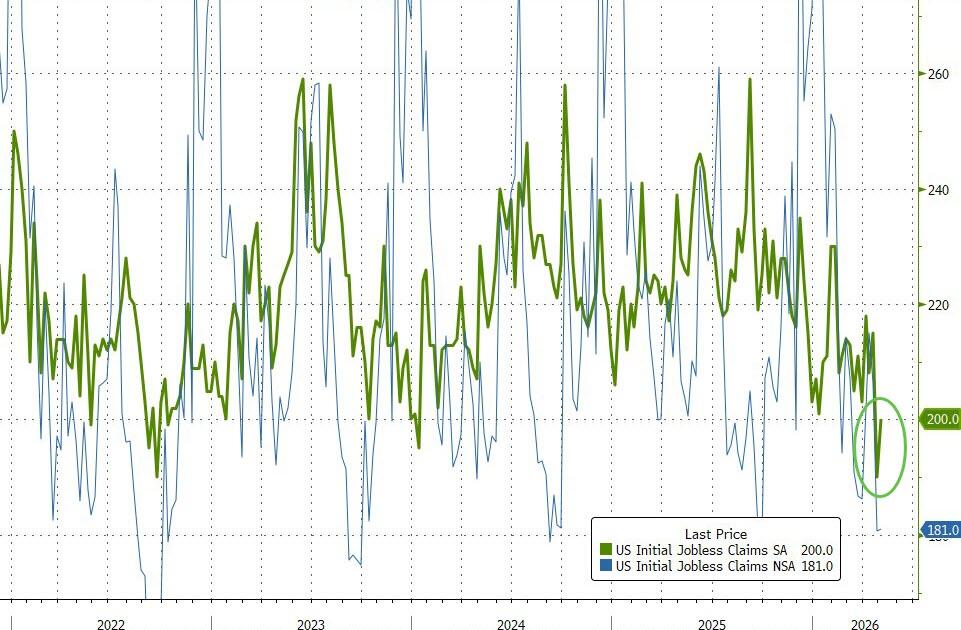

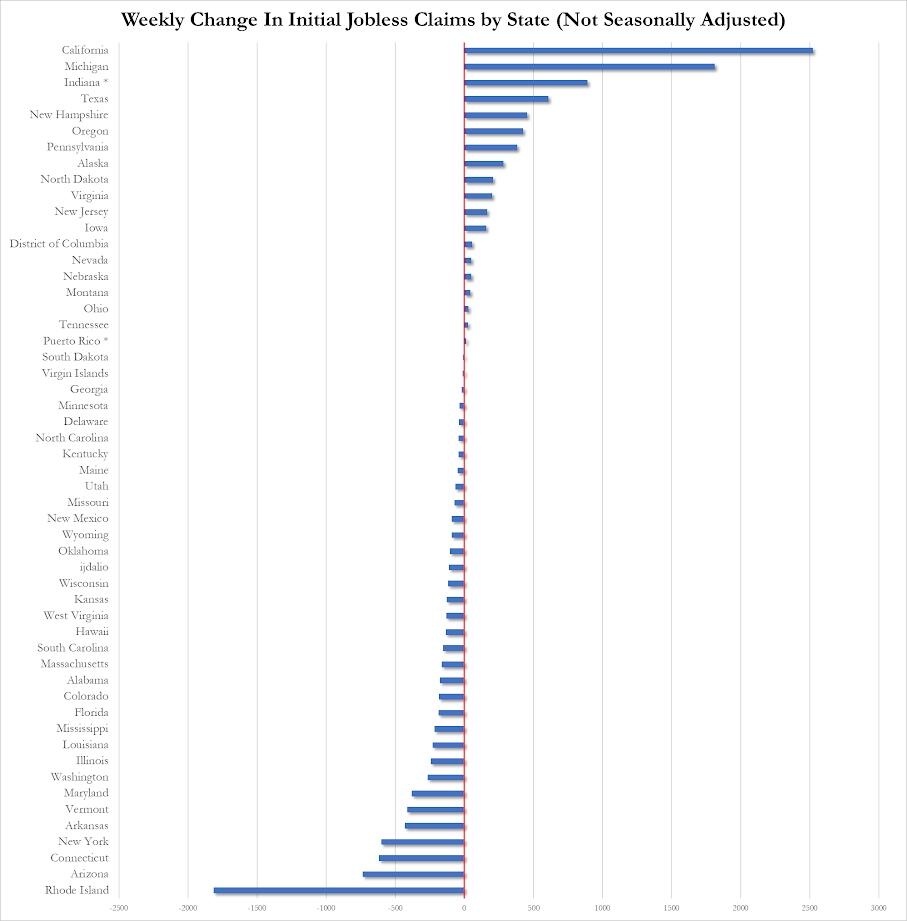

With JOLTs data showing record hiring (and ADP signaling acceleration in job additions), today we get some signal on firings as the number of Americans filing for unemployment benefits for the first time was at 200k last week (below the 205k exp) and continuing to languish near multi-decade lows (near 1967 lows!!)…

Source: Bloomberg

Non-seasonally adjusted across all the states saw a 299k drop in claims led by Rhode Island and Arizona (California and Michigan saw the biggest increases)…

Continuing jobless claims also fell, now at 1.766 million Americans receiving unemployment benefits (better than the expected 1.8 million expected) and at its lowest since Jan 2024…

Source: Bloomberg

Finally, we note that Challenger, Gray, & Christmas pointed out that in April, Artificial Intelligence (AI) led all reasons for job cuts for the second month in a row, with 21,490 announced during the month, 26% of total cuts. This reason has been cited for 49,135 cuts this year, and it is the third-leading cause of layoff plans.

AI accounts for roughly 16% of all 2026 job cut plans, up from 13% through March.

“Technology companies continue to announce large-scale cuts and are leading all industries in layoff announcements,” said Andy Challenger, the company’s chief revenue officer.

“Regardless of whether individual jobs are being replaced by AI, the money for those roles is.”

Overall, Challenger, Gray, & Christmas says U.S.-based employers announced 83,387 job cuts in April, down 21% from the 105,441 cuts announced during the same month last year.

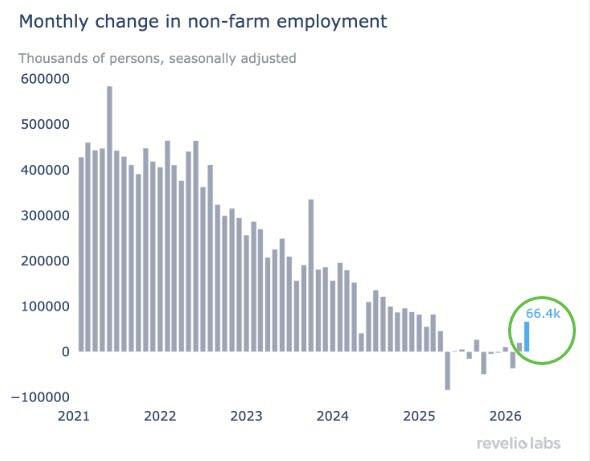

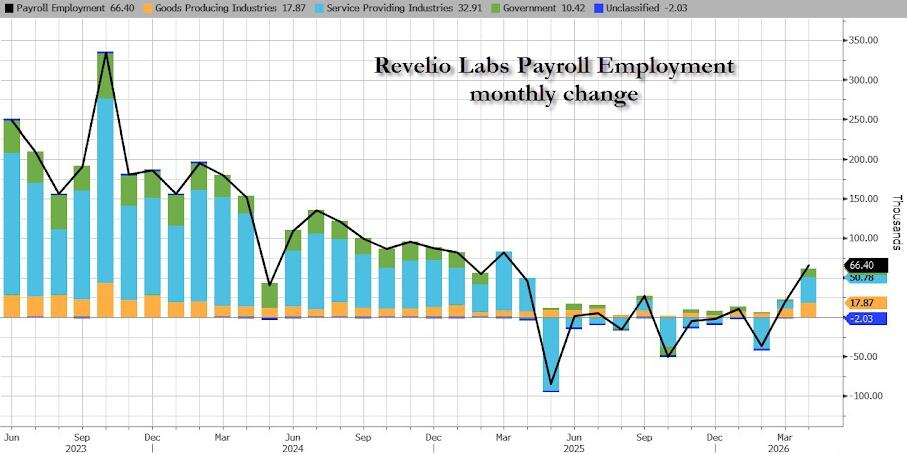

Another alternative labor market data source, Revelio Labs, shows a sizable rise in jobs this month – best since March 2025 (all adding up to a solid print for tomorrow)…

Led by a big uptick in Services jobs…

Taking all of that into account, it appears we have morphed into a ‘higher hire, no fire’ economy (but tomorrow’s payrolls print could throw shade on that idea).

Tyler Durden

Thu, 05/07/2026 – 08:35

https://www.zerohedge.com/markets/jobless-claims-jolts-confirm-higher-hire-no-fire-economy

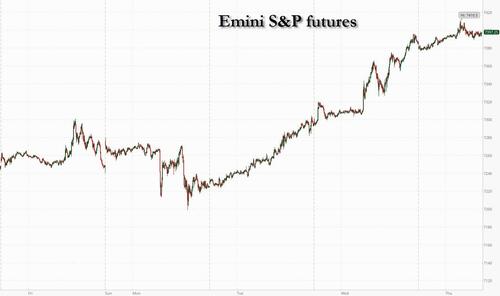

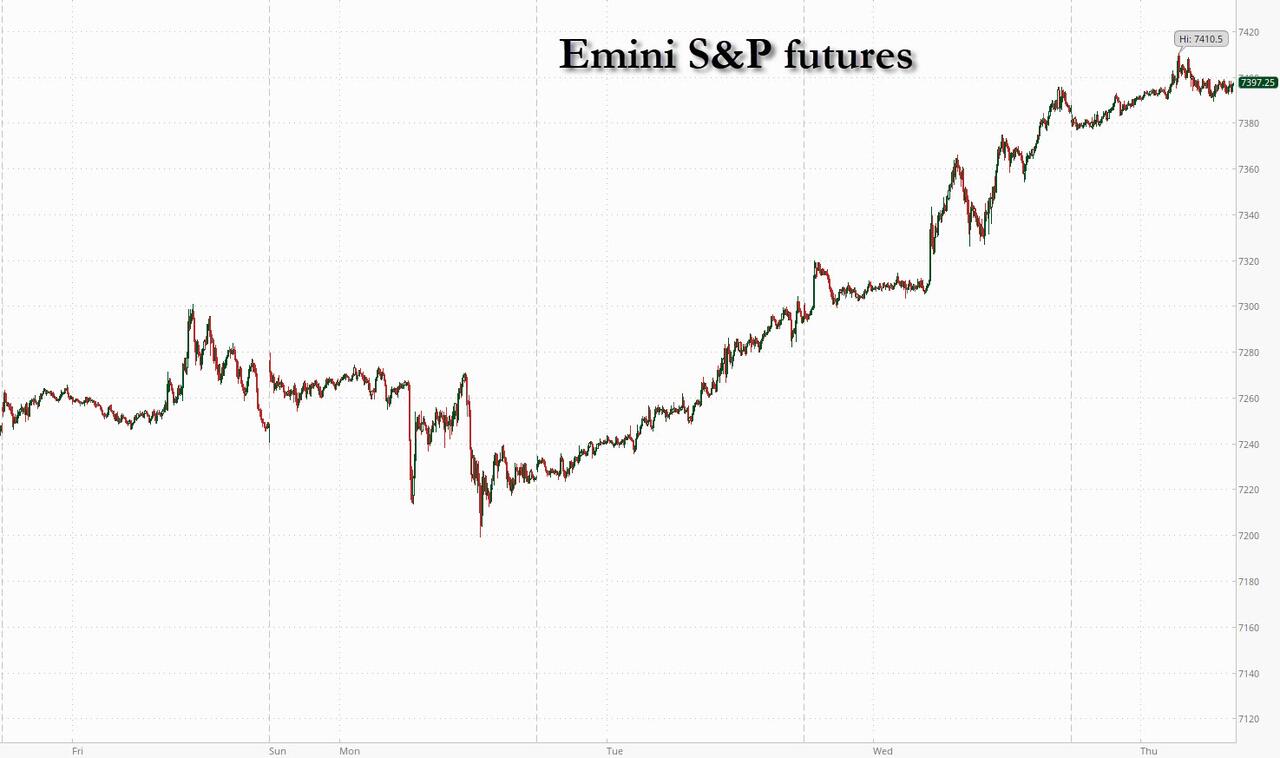

“Semi-Irrational Chase” Sends Futures To Another Record High, Oil Drops On Iran Optimism

“Semi-Irrational Chase” Sends Futures To Another Record High, Oil Drops On Iran Optimism

The global market meltup is rolling on. US stock futures inch higher, but are off session highs, with oil falling for a third straight day as traders waited for updates on a potential US-Iran peace deal that would reopen oil flows through the Strait of Hormuz. As of 8:00am ET, S&P and Nasdaq futures were 0.1% higher, after the benchmarks notched back-to-back record highs. In premarket trading, most Mag 7 stocks were higher although Arm Holdings dropped 8% after the chip company reported weak fourth-quarter royalty revenue, hurt by sluggishness in the smartphone industry; the company warned about weaker demand for lower-end phones due to higher memory cost. Whirlpool plunged 18% after the household appliance manufacturer cut its revenue forecast for the full year, missing the average analyst estimate. Overseas indexes are also rising, bolstered by stocks tied to artificial intelligence. Japan’s Nikkei 225 was a particular standout, climbing 5.6% after an 18% rally in Softbank shares. Brent traded near $99 a barrel, extending a 12% slump in the two prior sessions on mounting confidence that an agreement in the Middle East is within reach. The dollar headed for its worst week in a month. Global bonds continued their advance as inflationary pressures receded. Today’s US economic data calendar slate includes 1Q preliminary nonfarm productivity and jobless claims (8:30am), March construction spending (10am), April New York Fed 1-year inflation expectations (11am) and March consumer credit (3pm). Fed speaker slate includes Hammack (10am, 2:05pm), Daly (12:30pm), Kashkari (1pm) and Williams (3:30pm)

In premarket trading, Mag 7 stocks are mostly higher (Tesla +1.7%, Alphabet +1.1%, Nvidia +0.1%, Microsoft +0.7%, Amazon +0.3, Meta Platforms +0.02%, Apple -0.1%).

Albemarle (ALB) climbs 6% after the chemical producer reported net sales for the first quarter that beat the average analyst estimate.

Arm Holdings ADRs (ARM) drop 8% after the chip company reported weak fourth-quarter royalty revenue, hurt by sluggishness in the smartphone industry. Daiwa’s analyst notes that there was weaker demand for lower-end phones due to higher memory cost.

Celsius Holdings (CELH) rises 4% after the energy drink maker’s first quarter adjusted Ebitda and revenue beat consensus estimate.

Coherent (COHR) drops 3% as analysts note that the optical communications company’s gross margins underwhelmed.

DoorDash (DASH) jumps 10% after the delivery firm gave a forecast for order value in the current period that topped analyst estimates, signaling healthy consumer demand for its services in the US and international markets.

Fluence Energy (FLNC) jumps 31% after the company reported a narrower-than-estimated second-quarter adjusted Ebitda loss. Additionally, Fluence maintained its 2026 total revenue forecast, which has a midpoint above the average analyst estimate.

Fortinet (FTNT) gains 15% after the cybersecurity company forecast earnings that beat the average analyst estimate. The company also boosted its full-year revenue outlook. Analysts note particular strength at its hardware business.

Fastly (FSLY) slumps 25% after the software company reported first-quarter earnings, a report that wasn’t strong enough to extend a rally that has lifted shares nearly 300% off a February low.

McDonald’s (MCD) gains 3% after the fast-food chain said bigger orders bolstered results in the US in the first quarter.

Sezzle (SEZL) climbs 15% after the financial technology company raised its total revenue growth forecast for the full year.

Shake Shack (SHAK) falls 18% after the burger chain reported revenue for the first quarter that missed the average analyst estimate.

Warby Parker (WRBY) gains 7% after the the eyeglass company reported net revenue for the first quarter that beat the average analyst estimate.

Whirlpool (WHR) is down 18% after the household appliance manufacturer cut its revenue forecast for the full year, missing the average analyst estimate.

Zoetis (ZTS) falls 10% after the animal health firm cut its adjusted earnings per share guidance for the full year.

Elsewhere in AI, Anthropic signed an agreement with Elon Musk’s SpaceX to access computing resources from a large SpaceX data center. Anthropic’s CEO said his company is “working as quickly as possible” to secure more computing resources after experiencing “80x growth” in annualized revenue and usage in 1Q.

An ongoing slide in oil prices is helping to lift investors’ mood, with Brent crude futures trading below $100 a barrel this morning. The U.S. and Iran are getting closer to restarting talks to end the war and reopen the Strait of Hormuz, with discussions possibly resuming as early as next week in Islamabad. While the US is waiting on Iran to respond to its proposal which sent stocks surging yesterday, and it’s unclear whether they’ll accept. But stocks have largely focused on a solid earnings season and the tech trade anyway. The inverse relationship between stocks and oil prices is “long gone,” wrote Bloomberg Opinion columnist John Authers. The resumption of shipments through Hormuz would also reduce risks around the economic impact of the war. US Treasury yields are retreating for a third straight session alongside the dollar, which is now trading lower than when the war began.

“Even though there is not yet a final peace agreement, markets are clearly pricing in a meaningful step forward toward a resolution,” said Francisco Simón, head of investment strategy at Santander Asset Management. “The key point is that this reduces the probability of the most negative scenarios, particularly those involving a more prolonged shock to global growth.”

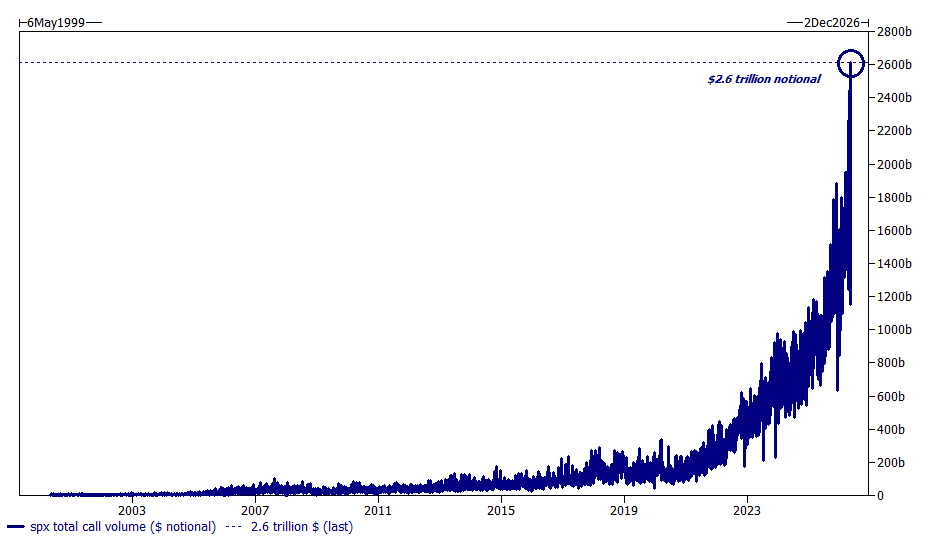

That said, there are clear signs of mania: the SOX chip index is now up more than 60% this year – a parabolic move that suggests “we are in semi-irrational chase mode,” Goldman Delta-One head Richard Privorotsky warns. Meanwhile, in a sign the entire market has become one giant gamma squeeze, the S&P traded a record $2.6 trillion notional of calls yesterday..

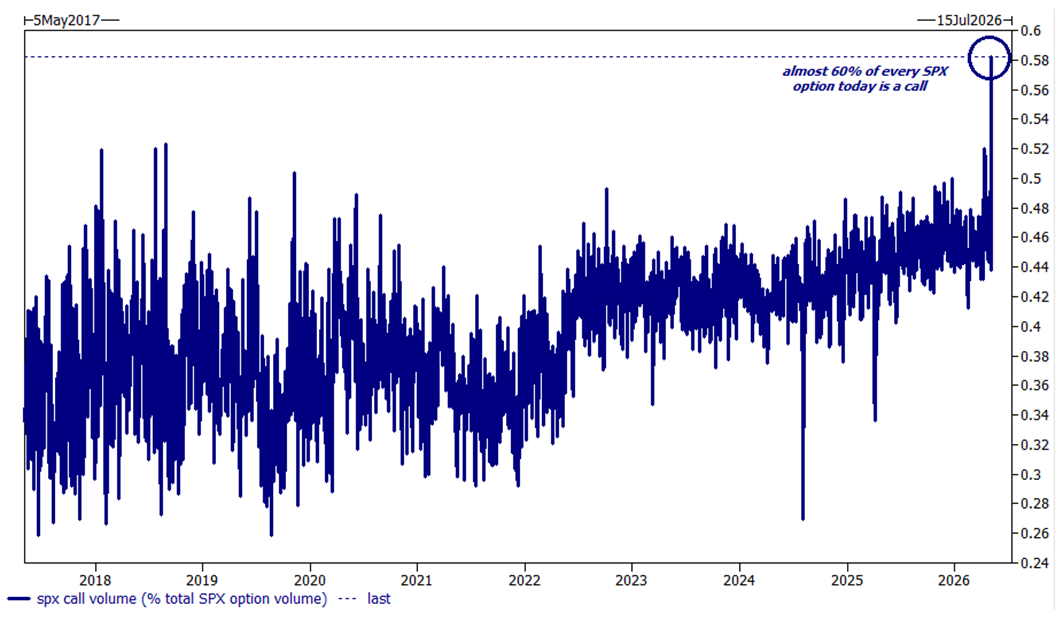

… with almost 60% of every SPX option yesterday traded a call.

There are a few signs of the rally broadening out, with the S&P 500 equal-weight index closing at a record for the first time since late February. But there’s really just one trade in town, with the SOX hitting new records almost daily. “Until supply normalizes, the market can continue to justify increasingly large numbers across the ecosystem, although the obvious risks are building,” Goldman partner Privorotsky wrote in a note.

The global chip euphoria helped South Korea’s stock market to overtake Canada’s, and is boosting niche firms around the world, with Sweden’s Silex Microsystems having the strongest first day of trading for a sizable European IPO in almost five years. Still, there may be a limit — after more than doubling in value this year, ARM shares fell after it warned of sluggishness in the smartphone industry.

In eco data, planned job cuts continued to mount in the tech sector last month, even as overall private-sector layoff announcements receded, according to Challenger data. And consumer sentiment remains closely watched. Costco’s April comparable sales rose 11.6%, aided by 3.2% gas-price inflation. Whirlpool cut its revenue forecast, noting North American industry demand reached recession-level lows.

The Trump administration has begun paying out refunds for the $166 billion in global tariffs that the US Supreme Court declared unlawful earlier this year. The FCC said that an inquiry the commission launched into the rising cost of watching sports on TV may not lead to any regulatory action. In hedge funds, SPX Capital is undergoing a major restructuring, with senior partners departing and a rethink of operations that will include shutting its London office. Point72 is creating a new fundamental stock-picking unit led by Hong Kong-based star portfolio manager James Lau.

With earnings season gradually drawing to a close, of the 411 S&P 500 companies to have reported so far this earnings season, 84% have beaten analysts’ forecasts, while 11% have missed

In Europe, the Stoxx 600 is down 0.2% after erasing an earlier gain.Uutilities and food beverage shares led declines while luxury, travel and leisure stocks are among the best performers. Here are the biggest movers Thursday:

Luxury stocks are among Europe’s best performers on Thursday, with strong Chinese consumer data adding to hopes for a turnaround that’s already been fueled by optimism about a peace deal in the Iran war

Stora Enso gains as much as 5.4%, the most in a month, following a first-quarter Ebit beat from the paper, packaging and forestry company

Tenaris falls as much as 7.1%, the most since July last year, after the Italian pipeline and steel-pipe manufacturer reported its latest earnings

Maersk falls as much as 5.3%, the most since March, after the Danish shipping giant reported its latest earnings and reaffirmed its full-year guidance, with the latter being a small negative for analysts as consensus already sits at the upper end of the guided range

Orsted shares drop 2.4% after the Danish wind farm operator reported 1Q Ebitda that beat the average analyst estimate, while after-tax profit missed. Analysts at Jefferies and JP Morgan point to rising interest rates and higher-than-expected taxes for the miss

Siemens Healthineers drops as much as 5.7%, the most in six months, after the German medical equipment maker cut its comparable sales forecast for the full year and lowered the upper end of the guidance range for adjusted EPS

GN Store Nord shares fall as much as 8.7%, the most in three months, after the Danish communication solutions company reported what Jefferies described as a “weakish” quarter

Vestas shares see choppy trading as the Danish wind-turbine maker reported first-quarter EBIT before special items that beat the average analyst estimate, though Morgan Stanley flagged weakness in services

Earlier, Asian stocks rose to a record high, supported by a catchup rally in Japanese shares and optimism that the US and Iran are nearing a deal to end their war. The MSCI Asia Pacific Index climbed as much as 2.3% after gaining 2.4% in the previous session. TSMC, SoftBank Group and SK Hynix provided the biggest boost to the advance. Japan led gains in the region as trading resumed after a long holiday. Shares in Taiwan and Hong Kong also outperformed. Tech shares continued to draw investor interest, with the MSCI Asia Pacific Information Technology Index gaining as much as 3.4% to a record.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The Norwegian krone outperforms, rising 0.9% against the greenback after the Norges Bank hiked interest rates. Most economists had them on hold. The Riksbank did stand pat.

In rates, treasuries hold small gains into early US session, supported by lower oil prices and European bond rally. Brent crude oil holds below $100 a barrel, extending Wednesday’s nearly 8% slump, as investors weigh latest attempts by US and Iran to reach a peace agreement. US yields are 2bp-3bp richer on the day with curve spreads narrowly mixed; 10-year, lower by 2bp near 4.33%, slightly outperforms German and UK counterparts. European government bonds also edge up. Gilts are also in focus with UK local elections underway. US session includes weekly jobless claims and several Fed speakers. IG dollar issuance slate includes a couple of deals. Three names priced $14.5 billion Wednesday, led by Eli Lilly’s $9b eight-part offering. On average, issuers paid negative concessions on deals that were 3.7 times oversubscribed.

In commodities, brent crude futures fall another 2% to around $99 a barrel as the US waits on Iran to respond to its proposal to reopen the Strait of Hormuz and end the war. Precious metals gain with spot silver up 4%. Bitcoin falls.

Today’s US economic data calendar slate includes 1Q preliminary nonfarm productivity and jobless claims (8:30am), March construction spending (10am), April New York Fed 1-year inflation expectations (11am) and March consumer credit (3pm). Fed speaker slate includes Hammack (10am, 2:05pm), Daly (12:30pm), Kashkari (1pm) and Williams (3:30pm)

Market snapshot

S&P 500 mini +0.1%

Nasdaq 100 mini +0.1%

Russell 2000 mini +0.1%

Stoxx Europe 600 -0.2%,

DAX little changed,

CAC 40 little changed

10-year Treasury yield -2 basis points at 4.33%

VIX +0.1 points at 17.48

Bloomberg Dollar Index -0.1% at 1187.37,

euro +0.2% at $1.1768

WTI crude -2.6% at $92.6/barrel

Top Overnight News

The U.S.-Iran war had created a “new wake-up call” for global trade, Maersk CEO Vincent Clerc told CNBC on Thursday, warning that the impact could worsen in the coming months. “And there is so much we can do on reducing costs, but there is a lot we need to do on passing on these costs to customers, because it’s such a massive cost increase that we can’t shoulder it.” CNBC

Privately, President Trump’s advisers are increasingly worried that Republicans will pay a political price for the rising fuel costs, according to people familiar with the matter. Many of those advisers are eager to end the war in hopes that prices will begin moderating before November’s midterm elections. WSJ

Hungry to sell, UAE slips hidden oil tankers through Strait of Hormuz: RTRS

The jet fuel shock triggered by the Iran war has been a bigger crisis for the global airline industry than the Covid-19 pandemic, according to one of Asia’s biggest carriers AirAsia. FT

Japan probably spent around $30 billion since its currency intervention on April 30, according to a Bloomberg analysis. Their top FX official Atsushi Mimura signaled authorities are prepared to respond on all fronts to speculative moves. BBG

Chinese households increased their pace of spending over the recent Labor Day extended holiday weekend, with a 14.3% jump in consumer sales from the same holiday last year. The increase is seen as an encouraging sign for the world’s second-largest economy, but household spending over holidays can be volatile, and big-ticket purchases remain subdued. BBG

China asked its biggest banks to pause new yuan loans to five US-sanctioned refiners tied to Iranian oil, people familiar said. BBG

The US and China are considering launching official discussions on AI when US President Trump visits China next week. With the proposed recurring conversations, risks from unexpected AI model behaviour, autonomous military systems, and attacks by non-state actors using open source tools will be addressed: WSJ

Norway’s central bank unexpectedly hiked rates (from 4% to 4.25% – the Street was expecting rates to stay unchanged) due to upward inflation pressures. BBG

BOE officials are privately concerned UK economic data may be sending false signals, complicating rate-setting, people familiar said. BBG

Federal Reserve officials said on Wednesday the ongoing U.S.-backed war with Iran is raising the risk of a sustained inflation shock, with continued high oil prices and developing concerns about problems with global supply chains. BBG

Iran News

Al Arabiya reported that “the coming hours will witness a breakthrough for the situation of the ships stuck in the strait”, spurring pressure in the crude complex.

Iran is expected to provide its reply to the US proposal for ending the war to mediators on Thursday, according to CNN, citing a regional source.

US President Trump could turn to military action without an agreement with Iran ahead of the China trip, according to Axios, citing US officials.

Iran is expected to provide its reply to mediators on Thursday, CNN reported citing a regional source.

“Arabic sources: Reaching understandings regarding easing the siege in exchange for the gradual opening of the Strait of Hormuz “, Al Arabiya reported; “The coming hours will witness a breakthrough for the situation of the ships stuck in the strait”.

Pakistani Foreign Ministry spokesperson said, “We do not talk about war and instead talk about dialogue and diplomacy. However, if any aggression similar to what we saw last year, we will respond; Pakistan will respond just as it did”, Mallick posted.

Pakistani Foreign Ministry Spokesperson said “We have not yet received a response from Iran regarding the US amendments”, Al Jazeera reported.

“Pakistani source to Al Arabiya said Iran may hand over its response to the US proposal to the Pakistani mediator today”, Al Arabiya. “No arrangements for any direct meetings between the Iranians and the Americans so far.”. “Contacts with the Iranians are ongoing and there are no obstacles hindering continued”. “Discussions are ongoing regarding the status of the Strait of Hormuz, and reaching understandings is still possible”.

Pakistani Foreign Ministry said “We expect an urgent agreement between Iran and the United States”, Al Araby reported.

“Israel was informed that Iran has agreed to transfer its stockpile of 60% enriched uranium to a third country that remains unknown”, Sky News Arabia reported citing Israeli Channel 12.

Pakistani Foreign Ministry spokesperson, on US-Iran agreement, said “we would expect an agreement sooner rather than later”, Pakistani journalist Mallick posted. “We will welcome any settlement wherever that takes place, if it takes place in Islamabad, it would be an honour and privilege.”.

The proposed agreement between the US and Iran may limit the IDF’s action in Lebanon, Israeli press reported citing an Israeli official.

US President Trump, on Iran, said it will all work out very quickly.

IDF said it has intercepted suspicious aerial target launched from Lebanon towards Israel following sirens that sounded in Manara, Margaliot and Kiryat Shmona.

Lebanon’s PM Salam said it is not seeking normalisation with Israel and it is too early to discuss any possible meeting with Israeli PM Netanyahu.

Iran has issued a message to commercial vessels in the Strait of Hormuz, saying Iran’s port is fully prepared to provide general maritime services and support to the vessels, IRNA reported.

US President Trump could turn to military action without an Iran agreement ahead of the China trip, Axios reported citing US officials.

US President Trump’s reversal on his plan to help ships go through the Strait of Hormuz came after Saudi Arabia suspended the US’s ability to use its bases and airspace to carry out Project Freedom, NBC reported citing US officials.

IRGC Navy Political Affairs Official said we will impose our control over the Strait of Hormuz, and any attack will be met with a plan beyond the enemy’s calculations, Al Jazeera reported.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded broadly in the green, as a continuation of gains seen stateside as hopes of an end of the US-Iran conflict spurred risk-on flows. ASX 200 continued its rebound and is set for 2 consecutive days of gains. Miners were the biggest gainers while Energy names slumped. Shares of Tabcorp have nose-dived after the Co. stated that AUSTRAC has commenced an enforcement investigation with serious concerns over money laundering and terrorism financing risks. Nikkei 225 returned from its holiday with the need to catch up to the gains seen in equities while it was closed. As a result, the Nikkei surged to new ATHs and extended above the 63,000 handle, driven by tech majors SoftBank and Ibiden. KOSPI underperformed its APAC peers, as it consolidated following its surge beyond the 7,000 handle. SK Securities raised its PT for Samsung Electronics and SK Hynix to a price that is 88% and 87% higher, respectively, than their current price, reaffirming the tech strength. Shanghai Comp. and Hang Seng gained despite a lack of single-stock news. Continuing on the chip theme, Montage has overtaken CATL as the most expensive dual-listed stock in Hong Kong relative to its mainland shares

Top Asian News

Philippine’s Economic Minister said controlling inflation, even if it will cost growth, is not necessarily bad.

China’s top diplomat Wang Yi met with a delegation led by Steve Daines on Thursday, Xinhua reported.

South Korea’s government is to invest KRW 30bln in a project aimed at establishing an AI data platform for autonomous vessels, Yonhap reported.

Indonesia’s Planning Minister said the 2027 government working plan is set with GDP growth target in a range of 5.9-7.5%.

Hong Kong Financial Secretary Chan announces plans to promote the use of the CNY in commodity pricing.

China rural banks have reportedly cut its deposit rates, with further cuts expected.

Japan’s Top FX Diplomat Mimura does not comment on FX intervention but said FX is being closely watched and are in daily contact with US authorities. IMF’s classification of free floating regime does not restrict frequency of intervention. Will not comment on FX levels. Too early to comment on US Treasury Secretary Bessent’s upcoming visit.

US Treasury Bessent is to meet with Japanese PM Takaichi, Finance Minister Katayama and BoJ Governor Ueda for 3 days, starting Monday 11th, to discuss the weak yen, Nikkei reported.

European bourses are broadly modestly firmer, attempting to build on the hefty gains seen in the prior session. Geopolitics remains the key focus this morning, with Iran expected to provide its reply to the US proposal for ending the war to mediators on Thursday, CNN reported. Sentiment in early morning trade was lifted after Al Arabiya reported that “the coming hours will witness a breakthrough for the situation of the ships stuck in the strait”. European sectors are mixed. Travel & Leisure takes the top spot, joined closely by Consumer Products and then Autos. Sectors which have broadly benefited from the risk-tone and/or lower energy prices. Elsewhere, Utilities is found right at the foot of the pile, joined closely by Telecoms. In terms of key movers: Henkel (+3.9%, sales topped exp.), Rheinmetall (-3.1%, missed on Q1 EPS, but reaffirmed outlook), Telecom Italia (+3.2%, revenue +1.4% amidst strong Brazil growth), Shell (-1.7%, EPS and Rev. topped expectations whilst announcing a USD 3bln buyback), Flutter (-3.6%, cut guidance despite reporting higher Q1 revenue).

Top European News

A Cyprian official said EU countries and lawmakers have reached a provisional deal to delay the implementation of watered-down AI rules.

Palliser Capital has reportedly begun building a stake in FTSE-100 firm Autotrader Group (AUTO LN) and pushing for it to set out plans to return up to GBP 700mln to shareholders alongside full-year results this month, Sky News reported.

Maersk (MAERSKB DC) CEO said if the Middle East situation becomes more peaceful, will then assess whether Red Sea transit can resume.

Maersk (MAERSKB DC) Q1 2026 (USD): Revenue 12.97bln (prev. 13.32bln Y/Y), EBITDA 1.75bln (prev. 2.71bln Y/Y), PBT 292mln (prev. 1.43bln Y/Y); maintains FY outlook. The Middle East conflict had limited impact on the quarter’s realised financial results.

Shell (SHEL LN) Q1 2026 (USD): EPS 1.22 (exp. 1.06), Adj. EBITDA 17.7bln (exp. 15.1bln); announces a USD 3bln share buyback and a 5% quarterly dividend increase. Other Metrics. Adj. Earnings 6.915bln (prev. 3.256bln Y/Y),. CFFO 6.062bln (prev. 9.438bln Y/Y). Cash capex 4.202bln (prev. 6.015bln Y/Y). Free cash flow 2.9bln (prev. 4.2bln Y/Y). Net debt 52.6bln (prev. 45.7bln Y/Y). Gearing 23%, dividend +5% to 0.3906. Capex guide USD 24-26bln FY. Comments. Q2 2026 outlook reflects lower expected volumes and a weaker margin environment. Q2 2026 production outlook reflects higher planned maintenance across the portfolio. Q2 2026 production and liquefaction outlook reflects the impact of Middle East conflict including Qatar and higher planned maintenance across the portfolio.

EU Transport Commissioner said airlines must continue to reimburse passengers for flight cancellations caused by high energy prices, the FT reported.

FX

DXY is on a softer footing amid renewed downside in crude prices following headlines in Arabian press that a breakthrough may be reached between the US and Iran in the coming hours regarding the Strait of Hormuz. Further, Israeli press suggested Iran has agreed to transfer its 60% HEU to a third unknown country. That being said, it’s worth noting that none of the reports thus far have come from Iranian outlets. DXY resides in a 97.856-98.058 range, still within yesterday’s 97.625-98.342 parameter.

G10 price action has largely been dictated by the Iranian war optimism. EUR/USD is back over 1.1750 in a 1.1741-1.1775 range and still within yesterday’s parameter.

GBP/USD rose back above the 1.3600 mark but remains within Wednesday’s parameter, although traders also eye UK local elections. A full preview can be found on the headline feed, but in brief, a worse-than-expected outcome for the Labour Party could see renewed pressure on PM Starmer.

USD/JPY is softer but only marginally, and within a narrow 156.02-156.53 range. Japanese participants returned overnight from Golden Week. Japan’s Chief FX Diplomat Mimura made comments earlier in the APAC session but refused to comment on FX intervention, and reiterated that FX is being closely watched. USD/JPY did see some fleeting pressure as Mimura spoke. Further on the FX front, US Treasury Secretary Bessent is to meet with Japanese PM Takaichi, Finance Minister Katayama and BoJ Governor Ueda for 3 days, starting Monday 11th, to discuss the weak yen.

Antipodeans are firmer amid their high-beta properties coupled with upside across base and precious metals, albeit both the AUD/USD and NZD/USD pairs reside within the upper end of yesterday’s range.

Central Banks

Fed’s Goolsbee (2027 voter) said he is open to new ways of thinking about inflation. Overhauling the Fed’s inflation framework is ‘not an easy space’. Kevin Warsh has some fresh ideas worth thinking about. Fed should incorporate all the data it can, but he doesn’t think there is a silver bullet for the inflation problem. He would be on the lookout for ‘underheating’ demand if low consumer confidence translates into falling consumer spending. US might be approaching an era of labour scarcity due to a combination of population aging and limited immigration.

BoJ data up to April 30th shows Japan spent around JPY 4.68tln to support the JPY.

BoJ Minutes from the March 18th-19th meeting stated that many members shared the view that it was appropriate to maintain the policy rate at 0.75%.

ECB’s Villeroy said they must be data dependent.

ECB’s Nagel said likely to raise interest rates unless the outlook improves markedly.

ECB’s Kocher said ECB is to consider hikes in the next months if there is no improvement; ECB is in data-dependent meeting-by-meeting mode.

BoE officials are privately concerned that UK economic data may be sending false signals that complicate the job of setting interest rates, according to Bloomberg citing sources.

RBNZ Governor Breman said higher near term inflation and weaker growth is somewhat expected, still expect growth this year.

PBoC injected CNY 27bln via 7-day reverse repos with the rate maintained at 1.40%.

PBoC set USD/CNY mid-point at 6.8487 vs exp. 6.8087 (prev. 6.8562).

BoC Governor Macklem said inflation forecasts in the July monetary policy report will not change much after including the government fiscal update.

BoC Governor Macklem said if oil prices keep rising and stay elevated “there may be a need for consecutive increases in the policy rate”. If the United States imposes significant new trade restrictions on Canada, we may need to cut the policy rate further to support economic growth. Alternatively, if oil prices continue to increase, and particularly if they remain elevated, the risk that higher energy prices become ongoing generalized inflation increases. If this starts to happen, there may be a need for consecutive increases in the policy rate.

Norges Bank hikes rates by 25bps to 4.25% (prev. 4.00%); “The Committee judges that a higher policy rate is needed to return inflation to target within a reasonable time horizon”.

Riksbank maintains its Policy Rate at 1.75% as expected, “there is scope to wait until there is a clearer picture”, “current level of the policy rate gives a good initial position to adjust monetary policy if required to safeguard the inflation target”.

Fixed Income

A modestly firmer session for fixed benchmarks, driven higher by a pullback in energy this morning on a handful of constructive geopolitical updates ahead of the expected Iranian response, via Pakistan, to the US proposal.

Updates that lifted the benchmarks from near-enough unchanged this morning to gains of a handful of ticks in USTs, but pertinently to a new WTD high of 111-01+. Bunds were similarly bid at the time, got to 126.12, also a new WTD peak, posting gains of 42 ticks at the time.

Since, the benchmarks have pulled back modestly from the above peaks but remain in the green by a few ticks into an afternoon that is likely to be dominated once again by geopolitical updates, but the docket is also packed with data and Fed speak.

For Gilts, they gapped higher by 31 ticks to a 87.70 session high, driven by the above geopolitical move being in full swing at the time. Gilts have also waned from best and currently hold onto gains of c. 10 ticks. Voting in the UK’s local elections is now underway, polls close at 22:00BST. Thereafter, a drip feed of results will occur throughout the night and well into Friday, the results of which could spark the formal start of a leadership challenge against PM Starmer, in the days and weeks ahead.

Saudi Arabia’s PIF is offering three-, seven- & 30yr USD benchmarks bonds, Bloomberg reported citing sources; IPTs are USTs +130-170bps.

Australia sold AUD 150mln 0.25% 2032 I/L bonds: b/c 3.97x, average yield 2.172%.

Commodities

Renewed downside was seen in crude prices following headlines in Arab press that a breakthrough may be reached between US and Iran in the coming hours regarding the Strait of Hormuz. Further, Israeli press suggested Iran has agreed to transfer its 60% HEU to a third unknown country. That being said, it’s worth noting that none of the reports thus far have come from Iranian outlets.

Regarding the state of talks, US President Trump is optimistic about a framework, and Iran is expected to respond to the US proposal via mediators on Thursday. Axios reported Trump could still turn to military action without an agreement before his China trip. Iran is expected to provide its reply to the US proposal for ending the war to mediators on Thursday, CNN reported, citing a regional source. WSJ editorial said, from its discussions with senior officials, current US red lines in the talks include Iran confirming it does not seek nuclear weapons; the dismantlement of Fordow, Natanz and Isfahan; a ban on underground nuclear work; and on-demand inspections with penalties for violations.

WTI and Brent futures have been trading off the hopes of oil flowing through the Strait once again. Brent July resides towards the bottom end of a USD 97.44-102.55/bbl range; WTI June sits towards the bottom of a 91.92-96.48/bbl range at the time of writing. Dutch TTF this morning dropped to EUR 42/MWh on the report from near EUR 45/MWH before stabilising around EUR 43.50/MWh.

Spot gold topped Wednesday’s USD 4,723/oz high to reach a current peak of USD 4,753.43/oz, amid the aforementioned pullback in energy. Spot gold sees its 100 DMA at USD 4,774.67/oz.

Base metals are mostly firmer as the pullback in crude prices bodes well for risk sentiment and broader global economic growth. That being said, 3M LME copper is flat within a USD 13,331.58-13,448.83/t range as it takes a breather from yesterday’s gains.

Chinese Gold Reserves at 74.64mln troy oz at end-April (prev. 74.38mln in March); extends gold buying streak to 18 months.

German government has rejected a return to nuclear power.

A drone crashed into an oil storage facility in a Latvian town close to the Russian border, according to LSM.

LME’s CEO said it is ready to expand its suite of approved warehouses in Hong Kong.

Australia set domestic gas reservation scheme at 20%.

HKEX CEO said the LME warehouses approved in Hong Kong are close to full capacity.

China has reportedly asked banks to pause new loans to US-sanctioned refiners, Bloomberg reported citing sources.

The Trump administration is studying using oil under land at US military bases and other DoW sites to help refill the emergency reserves, Bloomberg reported citing sources.

North Korea said it will not join the nuclear non-proliferation treaty, according to KCNA.

Trade/Tariffs

A South Korean official said the country’s first US investment under trade deal is to be announced after law takes effect in June.

European Parliament’s Top Negotiator said that good progress has been made in the EU-US talks though issues remain unsolved and that we will continue advancing progress and ensure stronger protections for citizens and businesses.

Geopolitics

Romanian Defence Ministry said a drone briefly breached Romanian airspace during a Russian attack on Ukraine.

A drone crashed into an oil storage facility in a Latvian town close to the Russian border, according to LSM.

Ukrainian President Zelensky said Russia has ignored our ceasefire proposal.

Russian Foreign Ministry spokesperson said that Russia is ready to negotiate about Ukraine and emphasises that Moscow has never refused called and talks that have real results.

Russia has decided to use its veto against the US-Gulf draft resolution on Hormuz; Russia rejects the chapter VII wording of the draft resolution on Hormuz, via Al Hadath.

US Event Calendar

8:30 am: United States May 2 Initial Jobless Claims, est. 205k, prior 189k

8:30 am: United States Apr 25 Continuing Claims, est. 1799.7k, prior 1785k

10:00 am: United States Mar Construction Spending MoM, est. 0.2%

10:00 am: United States Fed’s Hammack Appears on WOSU Public Radio

11:00 am: United States NY Fed Releases Survey of Consumer Expectations

12:30 pm: United States Fed’s Daly on Bloomberg Television

1:00 pm: United States Fed’s Kashkari Participates in Fireside Chat

2:05 pm: United States Fed’s Hammack Speaks in Fireside Chat

3:30 pm: United States Fed’s Williams in Moderated Discussion

DB’s Jim Reid concludes the overnight wrap

I wake up this morning to be told by my new WHOOP that after two weeks of sleep and activity data it can now reveal I’m only 43.2 years old in WHOOP years, nearly 9 years younger than my biological age. However just as I was about to crack open a bottle of morning champagne, alongside a bacon sandwich to celebrate, it told me that current data momentum suggests I’m ageing 1.6 times quicker than the average. So by the end of next week I could be in my 70s! Sounds like a recipe to be up all night tonight worried.

The time to be up all night and worried about the war in Iran might be past its peak after the news flow of the last 24 hours with no substantial push back to the optimistic Axios story that broke yesterday mid-morning London time. Oil is consolidating this morning after a big slump yesterday, which left Brent crude -7.83% lower on the day at $101.27/bbl. So that led to a huge bond rally as investors priced out the chance of rate hikes, with European front-end yields seeing double digit declines. Moreover, continued momentum from the AI trade helped propel risk assets to new highs as well, with the S&P 500 (+1.46%) at another record. So it was a strong session all round as stagflationary fears eased.

In Asia we’re also largely higher, boosted by a surging Nikkei (+5.68%) which is catching up after three days of holiday. Elsewhere the CSI (+0.20%) and the Shanghai Composite (+0.25%) are trading slightly higher, while the Hang Seng (+1.56%) is performing significantly better due to gains in technology shares. In contrast, the KOSPI (+0.11%) is underperforming relative to its regional peers after reaching a series of highs driven by gains in chipmakers. It’s up over +75% YTD. Elsewhere, S&P ASX 200 (+0.80%) is brushing off data that showed Australia logging an unexpected trade deficit in March. US and Europe equity futures are fairly flat, pausing for breath after yesterday’s surges.

The main driver of the moves over the last 24 hours was that Axios report that the US and Iran were close to agreeing a one-page memo that would end the war and set a framework for more detailed nuclear negotiations. Its provision would reportedly include a moratorium on nuclear enrichment for Iran, whilst the US would lift its sanctions and release billions in frozen Iranian funds in return, as well as both sides lifting restrictions around the Strait of Hormuz. And whilst the report left plenty of questions, a more positive tone continued during the day with Trump saying he thought the war “had a very good chance of ending” by next week and telling Fox News that he was “cautiously optimistic” about the proposal. He didn’t look to dispute the Axios report which was notable. Meanwhile, Iran’s ISNA said that Iran was looking at the US proposal, with Bloomberg reporting that Iran is expected to send a response via Pakistan in the next two days.

That backdrop triggered a steep fall in oil prices, with Brent crude down -7.28% to $101.87/bbl, while WTI fell -7.03% to $95.08/bbl. Indeed, Brent even fell beneath $97/bbl at one point, which was its lowest intra-day level in over two weeks, though it then rebounded a bit as Trump threatened to restart bombing unless Iran “agrees to give what has been agreed to”. Still, the overarching theme was one of rising optimism and oil markets priced easing risks of persistent disruption, as 6-month Brent futures (-6.02%) saw their biggest decline since March to $85.12/bbl.

With fears of a stagflationary shock easing again, multiple equity indices like the S&P 500 (+1.46%), Nasdaq (+2.02%) and the Mag 7 (+2.00%) roared to new highs. Within the rally, chipmakers continued to outperform, driven by strong earnings from AMD (+18.61%) after it reported strong demand for AI agents. So this powered the Philly semiconductor index up +4.48%, extending its YTD gain to 62%. The positive mood was also visible in other risk assets, with US HY credit spreads tightening by 4bp to their narrowest level in three months.

Bonds also saw strong gains, with 10yr Treasury yields falling -7.6bps to 4.35%, while 2yr yields fell -7.7bps to 3.87%. That rally came as investors priced out the chances of the Fed having to hike rates over the next year, with only 5bps of hikes now being priced by next March, down from 14bps the day before. While oil drove the rally in Treasuries, we also saw the latest quarterly refunding announcement confirm that the US Treasury expects to keep bond auction sizes unchanged “for at least the next several quarters”. Elsewhere, anticipation of the conflict easing led the dollar (-0.43%) to fall to its lowest level since the strikes against Iran began, while gold (+2.95) had its best day since March.

Over in Europe, markets saw an even stronger rally, given the continent’s greater exposure to the energy shock. That included significant advances for the STOXX 600 (+2.22%), FTSE 100 (+2.15%), DAX (+2.12%) and the CAC 40 (+2.94%). Moreover, bonds extended their gains as investors dialled back the prospect of imminent rate hikes. Indeed, the chance of an ECB rate hike by the June meeting fell beneath 80% by the close, its lowest in a couple of weeks. So that helped bonds extend their gains, with yields on 10yr bunds (-6.2bps), OATs (-8.8bps) and BTPs (-11.6bps) all falling. The rally was even stronger at the front-end, with 2yr bund yields falling -10.7bps. The mood in Europe was also aided by slightly better news from the PMI data, with the final Euro Area composite PMI revised up to 48.8 (vs. flash 48.6).

Staying with Europe, a key event today will be the UK’s local elections, although we won’t start to get the results until tomorrow morning. This will be important for markets because the governing Labour Party are expected to do badly, which has raised speculation that there might be a challenge against PM Keir Starmer. And in turn, the expectation is that a new Labour leader would face pressure to ease the fiscal rules and hence raise gilt issuance. That uncertainty has weighed on gilts, and the 2yr yield had risen by 100bps since the end of February, though it fell -13.8bps yesterday given the oil decline.

Finally, there wasn’t much data in the US, but we did get the ADP’s latest report of private payrolls for April, which came in a bit shy of expectations at 109k (vs 120k expected) ahead of the more important payrolls print tomorrow. That said, there was still a notable acceleration relative to prior months, and it was the strongest monthly print since January 2025.

To the day ahead now, in addition to the UK local elections we’ll receive US Q1 nonfarm productivity, March construction spending and the NY Fed inflation expectations for April. Then in Europe, we’ll get the UK April construction PMI, Germany April Construction PMI, France March trade balance and Eurozone March retail sales. Central Bank events include the Riksbank decision and Norges Bank decision, whilst speakers include the Fed’s Hammack and Williams, along with the ECB’s Kocher, Villeroy, Guindos, Lane and Schnabel. Earnings include McDonald’s, Gilead and McKesson.

Tyler Durden

Thu, 05/07/2026 – 08:27

Trump Paused Project Freedom After Gulf Allies Reportedly Suspended Base, Airspace Access

Trump Paused Project Freedom After Gulf Allies Reportedly Suspended Base, Airspace Access

It’s no secret that America’s Gulf allies bore the brunt of Iran’s military retaliation in the wake of Operation Epic Fury. Now there are reports of Washington being brushed back when it comes to ongoing base access in the region.

President Trump abruptly halted plans to support commercial shipping through the Strait of Hormuz after Saudi Arabia suspended US military access to its bases and airspace for the operation, two US officials told NBC. Kuwait is reported to have imposed similar restrictions in wake of being on the receiving end of Iranian missiles.

Prince Sultan Air Base in Saudi Arabia, file image

According to the officials, Trump caught Gulf allies off guard when he announced Project Freedom on Truth Social, triggering anger in Riyadh. Saudi Arabia is said to have responded by informing Washington that US forces would not be permitted to operate aircraft from Prince Sultan Air Base southeast of Riyadh or transit Saudi airspace in support of the mission.

Other Gulf allies were also reportedly surprised by the development, with Drop Site News also reporting Kuwait has made a similar move to cut or restrict base access. According to more details from the NBC report:

In response, the Kingdom informed the U.S. it would not allow the U.S. military to fly aircraft from Prince Sultan Airbase southeast of Riyadh or fly through Saudi airspace to support the effort, the officials said.

A call between Trump and Saudi Crown Prince Mohammed bin Salman did not resolve the issue, the two U.S. officials said, forcing the president to pause Project Freedom in order to restore U.S. military access to the critical airspace.

But here is how Trump framed the pause at the time in a Truth Social post: “Based on the request of Pakistan and other Countries, the tremendous Military Success that we have had during the Campaign against the Country of Iran and, additionally”… and he also said it was necessary “to see whether or not the Agreement can be finalized and signed.“

By the following day it became clear that the two sides were no closer to getting to the negotiating table, much less actually inking an agreement to end the war.

The White House is meanwhile denying the main content of the NBC report, with one official insisting that “regional allies were briefed in advance.”

Washington seemed genuinely shocked and surprised at the level of retaliation Iran unleashed on the region. Tehran has said it went after American bases in the Gulf, and as punishment for the countries hosting them. The response involved weeks of literally hundreds if not thousands of missiles and drones being launched. These hit oil, gas, and energy infrastructure – as well as radar, airbases, and military outposts.

Saudi Arabia BLOCKS US access to bases and airspace for ‘PROJECT FREEDOM’ — NBC

Saudi leadership reportedly ‘angered’ by Trump’s surprise announcement — prompting refusal pic.twitter.com/ULGG7WVWcB

— RT (@RT_com) May 6, 2026

Follow-up reports have said that well over a dozen US regional bases were decimated and made uninhabitable – something which the Pentagon has sought to downplay or else keep totally under wraps.

Tyler Durden

Thu, 05/07/2026 – 08:20

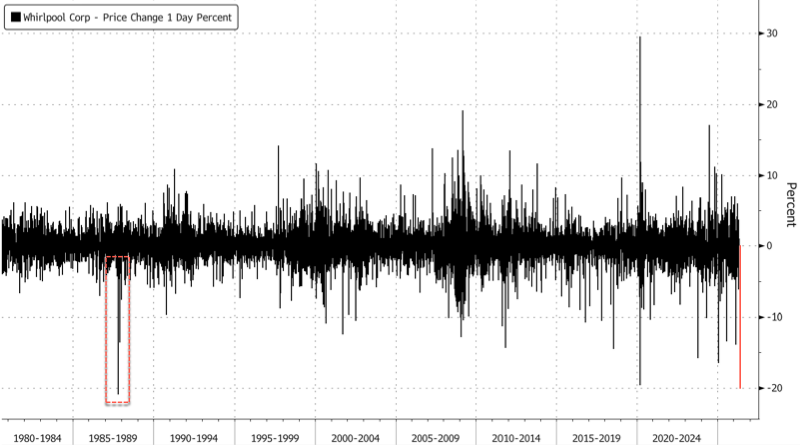

Whirlpool Crashes After Iran Shock Sparks “Recession-Level” Appliance Slump

Whirlpool Crashes After Iran Shock Sparks “Recession-Level” Appliance Slump

Whirlpool shares crashed as much as 20% in premarket trading after the appliance maker slashed its full-year outlook and posted weaker-than-expected first-quarter results. Management directly blamed the three-month war in the Middle East for triggering a collapse in U.S. appliance demand.

Whirlpool began the earnings release with this statement: “War in Iran resulted in a recession-level industry decline in the U.S. as consumer confidence collapsed in late February and March.”

For the first quarter, the maker of refrigerators, freezers, dishwashers, ovens, ranges, cooktops, microwaves, and range hoods missed Bloomberg Consensus estimates across key metrics, underscoring a sharp deterioration in demand and profitability.

Net sales in the quarter came in at $3.27 billion, below the $3.42 billion estimate. North America sales were soft at $2.24 billion, missing expectations of $2.4 billion, while Latin America sales were weak at $774 million, missing estimates of $785.5 million.

The company posted an ongoing loss of 56 cents per share, compared with earnings per share of $1.70 a year earlier. This result was far below analyst expectations of a loss of 36 cents per share.

EBIT, or earnings before interest and taxes, plunged 79% year over year to $44 million, missing the $110.8 million consensus estimate.

Snapshot of 1Q Earnings (courtsey of BBG):

Net sales $3.27 billion, estimate $3.42 billion

MDA North Amer. Net Sales $2.24 billion, estimate $2.4 billion

MDA Latin America Net Sales $774.0 million, estimate $785.5 million

Ongoing loss/share 56c vs. EPS $1.70 y/y, estimate EPS 36c

Ongoing EBIT $44 million, -79% y/y, estimate $110.8 million

Snapshot of 2026 forecast (courtsey of BBG):

Sees revenue $15.0 billion, saw $15.3 billion to $15.6 billion, estimate $15.21 billion (Bloomberg Consensus)

Sees ongoing EPS $3.00 to $3.50, saw about $7, estimate $4.84

Sees cash from operating activities about $700 million, saw about $850 million, estimate $763.9 million

Still sees adjusted tax rate about 25%

Shares crashed as much as 20% in premarket trading after first-quarter sales showed weaker demand, mounting margin pressure, and a decline in North American appliance demand. If these losses persist through the cash session, it would be the steepest intraday decline since the October 19, 1987, crash of 21%.

Year to date, shares are already down 24% as of Wednesday’s close. The stock is now trading at 2011 levels.

Is management conveniently blaming the U.S.-Iran war? The largest trend impacting home appliance sales has been a frozen housing market over the past several years.

Tyler Durden

Thu, 05/07/2026 – 07:45

https://www.zerohedge.com/markets/whirlpool-shares-crash-after-iran-war-shock-crushes-profit

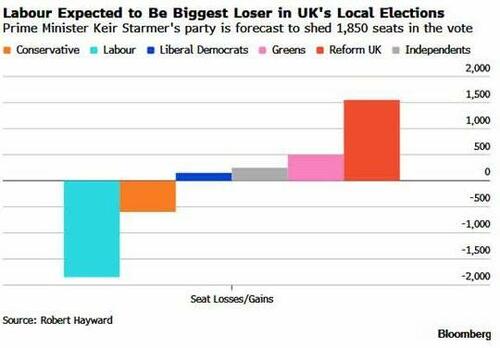

Will Today’s British ‘Midterms’ Spark ‘Starmageddon’ For The Labour Party?

Will Today’s British ‘Midterms’ Spark ‘Starmageddon’ For The Labour Party?

All eyes on UK local elections (Britain’s ‘Midterms’) today.

As JPMorgan’s Market Intel desk noted this morning, while the seats up do not influence national policy, Brits have historically used local and regional elections to punish the party in power in Westminster.

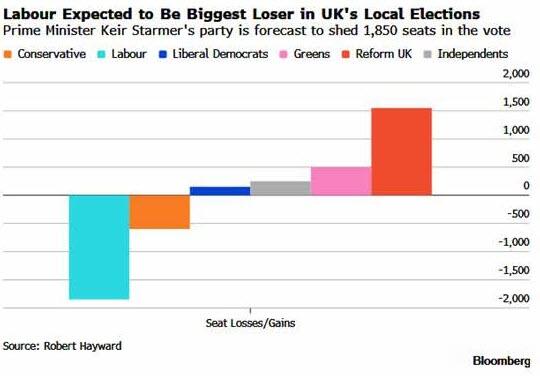

Reform UK is expected to come out as the main beneficiary of the elections, with Labour the biggest loser.

The key risk is that Labour’s poor performance causes MPs to push Starmer out in an attempt to improve the party’s standing ahead of 2029 elections.

This could come in the form of a formal leadership challenge or a ministerial resignation that triggers others to follow suit (for the former, Rayner seen as the most likely candidate for now, while Andy Burnham could make another attempt to enter parliament in the summer).

Gilts are especially sensitive to political developments (muscle memory from LDI crisis and the 2024 Autumn Budget) and renewed fiscal concerns could drive further underperformance – risk premia has been building as 30Y yields surged to their highest level since 1998 on Tues, underperforming EA rates by ~35bps since the war.

While risks are skewed bearish for GBP and rates, our economist emphasizes changes to fiscal strategy are not a foregone conclusion.

With the market impact out of the way, LibertyNation.com’s Mark Angelides explains below, such small-scale ballots were traditionally focused on garbage collections and potholes, but with the growing disaffection in politics – aimed squarely at the ruling Labour Party and the Conservative Party – politicos and pundits are treating them as a midterm equivalent. And with potentially the biggest defeat for any establishment party ever as the most likely outcome, UK politics may never be the same again.

End of the Line?

Before getting to the almost certain defeat of Sir Keir Starmer’s ruling Labour Party, it’s worth sparing a thought for His Majesty’s loyal opposition, the Conservative Party.

The party of Margaret Thatcher and Winston Churchill, rightly regarded as the most successful political outfit of all time, is on the cusp of no longer being a national party. But how could such a reversal of fortunes happen in a contest that is not even a general election?

As well as in local council elections in large parts of England today, voters are also casting ballots in the devolved parliaments of Scotland and Wales: Holyrood, the Scottish body, and the Welsh Senedd elections. The Labour Party is in the unenviable position of having to defend the lion’s share while contending with historic deficits in overall approval. But the rise of the Reform Party and the reinvigorated Green Party is at the root of the anticipated toppling of the UK’s two great parties.

Reform UK – An Unstoppable Force?

Labour won the general election in a landslide back in 2024, and it has all been downhill since then. Nibbling away at the edges of its supposed “red wall” support in the north of the country is the Reform Party, whose leader, Nigel Farage, made his own parliamentary breakthrough in ’24. Notably, in every single poll for the last 12 months, Reform has placed first – not bad for a new party. And while it was initially thought it was only the Conservatives who were bleeding members, support, and treasure to Reform, the surveys show a clear decline for Labour, too.

Indeed, if a general election were held today, a polling aggregate suggests Reform would be the largest party in Parliament with around 250 seats (out of 650). Second place would go to Conservatives with just 128, and Labour a distant third on only 78 (a loss of 334 seats). This is the backdrop as the two parties that have exchanged power for the last 100 years head into today’s elections – a midterm referendum by another name would smell as sour. But that is the big picture; the local contests are set to be even more damning.

The projections are enough to create panic across Westminster.

Local Elections Matter

Of the almost 5,000 local seats up for grabs, Labour is defending 2,557; polling suggests it will lose between 50% and 75% today.

The Conservatives are defending more than 1,300 and will be lucky to save even a third of that number.

Different parts of the country hold local elections in different years, so Reform currently has zero seats to defend. However, if last year’s elections are any indication, it is likely to score big – with an estimated 1,300 pick-ups. This will mean that not only does it win more seats than any other party, but also more votes.

[ZH: DailySceptic’s Mark Littlewood notes that the scale of the apocalypse facing Labour is almost unimaginable. Last year the party lost two thirds of the seats it was defending and it may fare even worse this time. In absolute rather than relative terms, the position is bleaker still. In 2025, it had fewer than 300 councillors up for re-election as the areas voting were largely the Tory shires. This time, over 2,000 seats start in the Labour column and it could be reduced to 600 or even fewer. Swathes of the party’s campaigning infrastructure will be overwhelmed as a turquoise tsunami engulfs the Red Wall. Outside London it may struggle to maintain majority control in any area at all with ‘all out’ elections – although it has sufficiently impregnable majorities to remain in power in a good number of places which elect in ‘thirds’.]

But that’s not the end of the bad news for the big two.

The Green Party has been on the eco-fringes of UK politics for several decades. With a core message on tree-hugging and environmental issues, it failed to make a significant breakthrough. Until now. Headed by new leader Zack Polanski, the party has shifted its focus from the environment to Gaza and has been courting the “independent Palestine” vote among the Muslim voting blocs.

One might assume this was a recipe for electoral disaster, and yet, with sizable, concentrated Muslim enclaves across the country, it is a formula for a certain amount of success.

The Muslim vote has been reliably Labour since it became a bloc. So, while Reform has been taking Labour votes in the traditional working-class heartlands from the right, the Greens are now encroaching on its territory from the left. The Greens are projected to win almost 700 seats in today’s contests.

What does this mean for Starmer?

Parliament on Maneuvers

Sir Keir is arguably the least popular prime minister since records began. His downfall from winning a huge majority in 2024 to being on the outs in 2026 is nothing short of a lesson in failure.

And his own party would have already moved to oust and replace him if it were not for today’s elections.

Unlike Americans, who vote for a president, Brits don’t vote for a prime minister but for a party – meaning that the current leading party can have an internal election to jettison an unpopular leader while still remaining the party of government.

So why haven’t they?

The simple answer is that no one wants to be the leader of a party that oversees a crushing local election result. In normal times, that leader must resign, step aside, or be removed by a party vote. Starmer is holding on only because they want him to shoulder the blame for the anticipated losses. And when the dust settles, the smart money says he will be shuffled off to “gardening duty,” while the Labour hopefuls pitch their dreams and schemes.

[ZH: Goldman Sachs base case is that a poor Labour result will not lead to an immediate leadership challenge for a two main reasons:

1) The three most likely leadership contenders (Burnham, Rayner, Streeting) all have recent / current issues limiting their prospects, and