Category: News

Momentos clave que llevaron al arresto del expríncipe Andrés por sus vínculos con Epstein

Por DANICA KIRKA and PAN PYLAS

LONDRES (AP) — Andrew Mountbatten-Windsor fue arrestado el jueves bajo sospecha de mala conducta en el ejercicio de un cargo público, tras una avalancha de revelaciones relacionadas con su relación con el fallecido delincuente sexual convicto Jeffrey Epstein.

El hombre, antes conocido como el príncipe Andrés, ha enfrentado durante años una serie de acusaciones por sus contactos con el desacreditado financista, más recientemente a raíz de la publicación de más de 3 millones de páginas de documentos relacionados con Epstein por parte del Departamento de Justicia de Estados Unidos.

Mountbatten-Windsor, de 66 años, ha negado haber cometido actos indebidos en su amistad con Epstein.

Estos son algunos momentos clave de la caída en desgracia de Mountbatten-Windsor como hermano menor del rey Carlos III:

___

2011

Andrés se ve obligado a dimitir como enviado especial de comercio de Reino Unido tras los primeros reportes sobre sus vínculos con Epstein, quien había sido condenado y encarcelado tres años antes por delitos sexuales relacionados con una menor.

Julio de 2019

Epstein es arrestado por segunda vez por cargos de tráfico sexual y posteriormente se suicida en la celda de una cárcel de Nueva York. La noticia centra la atención pública en acusaciones de que el entonces príncipe tuvo relaciones sexuales con al menos una adolescente menor de edad traficada por Epstein. Andrés niega las acusaciones.

16 de noviembre de 2019

Andrés intenta frenar la oleada de críticas al aceptar someterse a un duro interrogatorio ante cámaras por parte de la periodista de la BBC Emily Maitlis. La entrevista resulta contraproducente cuando Andrés defiende su relación con Epstein, no muestra empatía por sus víctimas y ofrece explicaciones sobre su conducta que a muchas personas les cuesta creer. El entonces príncipe afirma que rompió el contacto con Epstein en diciembre de 2010, una fecha que volverá para perseguirlo.

20 de noviembre de 2020

El Palacio de Buckingham anuncia que Andrés suspenderá todas sus funciones reales “durante el futuro previsible”. Cuatro días después, el príncipe es despojado de su papel como patrono de 230 organizaciones benéficas.

2022

Andrés acepta llegar a un acuerdo para resolver una demanda civil en Nueva York presentada por Virginia Giuffre, quien alegó que fue obligada a tener relaciones sexuales con el príncipe cuando tenía 17 años. Aunque no admitió ninguna de las acusaciones de Giuffre, Andrés reconoció que ella había sufrido como víctima de abuso sexual. Expertos legales estiman que el acuerdo, cuyo monto no se divulgó, le costó al hermano del rey hasta 10 millones de dólares. El origen de los fondos ha permanecido turbio desde entonces.

25 de abril de 2025

Virginia Giuffre se suicida en Australia, donde había vivido aproximadamente desde 2002.

12 de octubre de 2025

Periódicos británicos revelan que Andrés envió un correo electrónico a Epstein el 28 de febrero de 2011, más de dos meses después de haberle dicho a la BBC que había cortado todo contacto con su antiguo amigo. El príncipe escribió que estaban “en esto juntos” y que “tendrían que superarlo”.

17 de octubre de 2025

Andrés afirma que renuncia a sus títulos reales, incluido el de duque de York, y a otros honores porque “las continuas acusaciones sobre mí distraen del trabajo de Su Majestad y de la familia real”.

21 de octubre de 2025

En su libro póstumo, Giuffre relata detalles de cómo conoció por primera vez a Andrés en marzo de 2001 y que fue obligada a tener relaciones sexuales con él en tres ocasiones distintas.

30 de octubre de 2025

El rey despoja a su hermano de los títulos y honores que le quedaban, incluido el que ha ostentado desde su nacimiento: príncipe. A partir de entonces, será conocido como Andrew Mountbatten Windsor, y posteriormente, añadió un guion. El rey también le notifica que debe abandonar Royal Lodge, su residencia señorial de 30 habitaciones cerca del Castillo de Windsor, donde había vivido durante más de 20 años. Acepta trasladarse a la remota y privada finca Sandringham de su hermano.

30 de enero de 2026

El Departamento de Justicia de Estados Unidos publica los archivos de Epstein, que parecen revelar más detalles sórdidos sobre la relación entre el expríncipe y Epstein. Una foto de Mountbatten-Windsor agachado sobre una mujer inmóvil y no identificada en lo que parece ser el apartamento de Epstein en Nueva York provoca consternación y repulsión generalizadas. Entre las acusaciones que surgen en los días siguientes figura que Mountbatten-Windsor envió a Epstein informes confidenciales de una gira de 2010 por el Sudeste Asiático, que realizó como enviado de Reino Unido para el comercio internacional. Eso resultó ser el detonante de su arresto.

2 de febrero

Mountbatten-Windsor deja su mansión en el Castillo de Windsor para vivir en una propiedad mucho más pequeña en la finca Sandringham del rey.

9 de febrero

El rey indica que está listo para “apoyar” a la policía a analizar las afirmaciones de que su hermano entregó información confidencial a Epstein.

19 de febrero

Mountbatten-Windsor es arrestado bajo sospecha de mala conducta en el ejercicio de un cargo público. La Policía del Valle del Támesis, que supervisa un área al oeste de Londres, incluida la antigua residencia de Mountbatten-Windsor, señaló que estaba “evaluando” reportes de que el entonces príncipe envió a Epstein informes comerciales en 2010.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

Jeremy Zamost’s rise lifts all boats. He keeps ‘pushing, pushing, pushing,’ and Vernon Hills keeps winning.

This is the whole package that Vernon Hills’ Jeremy Zamost always envisioned.

That’s not to say Zamost hasn’t had plenty of good moments during his three-year varsity career. But the senior point guard has become a complete player at the most opportune time.

“I wish we would have won a few games that we lost, but as an individual, it’s been a lot of fun,” Zamost said. “I’ve always felt like my passing was solid, but the scoring wasn’t always there. But I feel like I’ve been playing pretty well and hopefully even better in the playoffs.”

Improving on his current run may be difficult to do because the 5-foot-11 Zamost is playing his best basketball to date. He’s averaging team highs of 14.9 points and 4.8 assists as well as 5.1 rebounds for Vernon Hills (21-9, 8-2), which finished second in the Central Suburban League North.

It’s no coincidence that the fifth-seeded Cougars, who will play 11th-seeded Amundsen in the Class 3A Wauconda Regional semifinals on Wednesday, have won eight of their past 10 games and go into their regular-season finale with the second-most wins in team history.

“My confidence in scoring continues to rise, and I trust that the shots will go in,” Zamost said. “All the training I do in the offseason helps, and I’m playing more aggressively. Before, sometimes I had open shots that I wouldn’t take, and I would just look to pass. I’m doing both now, and even my passing numbers have gone up.”

Vernon Hills’ Jeremy Zamost, left, drives against Niles West’s Asani Dixon during a Central Suburban League North game in Skokie on Friday, Dec. 5, 2025. (Talia Sprague / News-Sun)

Vernon Hills operates better when Zamost, an all-conference pick, has the ball in his hands, in part because he knows exactly what to do in those situations. His three-year journey to get to that point started when he opted for a varsity promotion as a sophomore that didn’t result in a ton of playing time but readied him both mentally and physically for what was ahead.

Back then, Zamost went toe-to-toe with then-senior point guard Dylan Chung every day in practice.

“I got in Dylan’s face, and how hard we worked against each other was beneficial,” Zamost said. “It made me better but also pushed him to get better.”

Zamost learned that doing the little things could go a long way toward being effective. Although he was certain he was worthy of contributing, he had to wait until a span of games when Chung was sidelined with an ankle injury to show what he could do.

“The first game I played was at Maine East, and everyone was saying we’d lose by 20 because we didn’t have a point guard,” Zamost said. “I knew I could play at that level, and we ended up winning by a lot. That was the best feeling. I’ll never forget that game.”

Zamost has had several games to remember this season. Over the weekend, he was the catalyst for overtime wins over Maine East and Lakes on consecutive days.

In the latter game, Zamost went 14 for 15 from the free-throw line, and many of those points came as the Cougars rallied from a nine-point deficit with five minutes remaining in regulation.

“We were on the ropes, but we got into the bonus, Jeremy just kept attacking and they were struggling keeping in front of him,” said Vernon Hills coach Matt McCarty, who recorded his 300th win that night. “He just kept pushing, pushing, pushing, and his footprint was on everyone’s play.”

Vernon Hills’ Jeremy Zamost (2) takes the ball to the basket against Deerfield’s Zach Friedman during a game in Vernon Hills on Monday, Dec. 9, 2024. (Rob Dicker / News-Sun)

Among Zamost’s other dominant games, he had a team-record 15 assists in a 52-28 win over Providence on Dec. 29 and scored a career-high 33 points in a 64-44 win over Grayslake North on Jan. 31.

“I felt like I couldn’t miss that game,” he said. “That was definitely a fun game.”

Zamost isn’t the only one having fun. Vernon Hills senior center Daniel Odhiambo‘s production has increased because of his chemistry with Zamost.

“He really knows how to get me the ball,” Odhiambo said. “If the defense helps off of me, it gives him an easy layup, and we run pick-and-roll really well. The other night against Maine South, it worked perfectly, and I got a wide-open dunk off it.

“Basketball is more fun when you have a good point guard.”

Zamost has offers from Benedictine and North Carolina Wesleyan to play basketball in college, and he hopes to attract even more attention down the stretch. If he continues to play at this level, the Cougars will benefit too.

“Recruiting has been on my mind, but that will be more of a focus after the season,” he said. “The biggest priority right now is winning so that we can keep playing together for as long as possible.”

Steve Reaven is a freelance reporter.

https://www.chicagotribune.com/2026/02/19/vernon-hills-high-school-basketball-jeremy-zamost/

Indiana lawmakers take another step in luring Chicago Bears to Hammond with stadium bill

Indiana lawmakers took another step Thursday to potentially lure the Chicago Bears to the state with a crucial committee approval to create an agency to build a new stadium for the team.

The Indiana House of Representatives Ways and Means Committee, which handles state spending, voted 24-0 to create a northwest Indiana stadium authority to issue bonds to finance, build and lease a stadium for the Bears near Wolf Lake in Hammond.

Republican House Speaker Todd Huston sponsored the measure, having called it “an incredible economic opportunity.” Indiana Gov. Mike Braun has called for bringing the Bears to “The Region,” as northwest Indiana is called.

The Bears would pay $2 billion toward the construction costs. The workings of the deal will be similar to the mechanism that created Lucas Oil Stadium, the home of the NFL Indianapolis Colts. The proposal calls for creating several new taxes to help pay for the stadium and its infrastructure, including toll road revenue, a 1% food and beverage tax in Lake and Porter counties, and a 5% innkeepers tax in Lake County.

What to know about the Chicago Bears’ possible move from Soldier Field

The Bears issued the following statement in response:

“The passage of SB 27 would mark the most meaningful step forward in our stadium planning efforts to date. We are committed to finishing the remaining site-specific necessary due diligence to support our vision to build a world-class stadium near the Wolf Lake area in Hammond, Indiana. We appreciate the leadership shown by Governor Braun, Speaker Huston, Senator Mishler and members of the Indiana General Assembly in establishing this critical framework and path forward to deliver a premier venue for all of Chicagoland and a destination for Bears fans and visitors from across the globe. We value our partnership and look forward to continuing to build our working relationship together.”

The action keeps the pressure on Illinois lawmakers to come up with a counter-proposal. The General Assembly is considering a bill that would allow the team, or any developer of a sufficiently big “Mega Project,” to negotiate long-term property taxes with local taxing bodies. The Bears have said they need that to use their own money to build a new $2 billion stadium in northwest suburban Arlington Heights.

The bill was initially scheduled to be discussed during Thursday morning’s House Revenue and Finance Committee hearing, but the hearing was canceled.

In order to move to Arlington Heights, the Bears face a major obstacle: Getting state lawmakers who represent the city of Chicago to incentivize the team to move out of the city limits. The chair of the House Revenue and Finance Committee is state Rep. Curtis Tarver, Democrat who represents a swath of Chicago’s South Side that stretches south from the North Kenwood area to the East Side, which borders Hammond, Ind.

Despite the outside pressure from Indiana’s overtures and his recent acknowledgement of “progress” in Illinois’ discussions with the team, Illinois Gov. JB Pritzker said his principles on the issue haven’t changed. The proposed megaprojects legislation in Springfield could help the state retain and attract a variety of businesses, not just the Bears, he told reporters after his Wednesday budget and State of the State address.

“There are some principles that I have laid out that we are following, and that continues; nothing has changed about that,” Pritzker said. “That is to say, this deal should be as it would be with any business coming to the state of Illinois or another one expanding in the state: has to be good for the taxpayers. This has to create enough economic opportunity, it has to create enough economic growth that the taxes that come from that over the years are good for the state, as well as lots of jobs and opportunity.”

Pritzker has said the state won’t pay for a stadium, but expressed support for helping to pay for $855 million in requested infrastructure, such as new expressway ramps and utilities. But Chicago lawmakers have been reluctant to help the team leave the city. Some have said the team should pay for more than half a billion dollars in debt left from the 2003 renovation of Soldier Field.

The clock is ticking. Bears President and CEO Kevin Warren had wanted to break ground last year, with a three-year construction period. As the Tribune first reported in December, Warren said Arlington Heights remained the “most viable” site, but the team was considering northwest Indiana after inaction by Illinois lawmakers.

The Illinois legislative session runs through May, often with lawmakers making deals at the last minute, and it may take time to hammer out an agreement with the team. Republican Indiana legislative leaders have said they want to finish a Bears deal by the intended end of their session, Feb. 27.

The Bears lease runs through 2033. They could leave early by paying a penalty of $81 million this year, or lesser amounts if they left in future years, but any additional amount would depend on negotiations with lawmakers.

As a comparison, after fighting in court, the Cleveland Browns recently agreed to pay $100 million to the city and pay to demolish their lakefront stadium for a new domed facility in suburban Brook Park.

The Bears project a stadium deal would create thousands of jobs and billions of dollars in economic development, with an enclosed facility allowing for many other events. Economists generally are skeptical of such projections, warning that public subsidies for sports stadiums are bad deals for taxpayers.

https://www.chicagotribune.com/2026/02/19/chicago-bears-indiana-stadium-bill/

Window Closing On Iran Diplomacy: IAEA’s Grossi Issues Pessimistic Outlook

Window Closing On Iran Diplomacy: IAEA’s Grossi Issues Pessimistic Outlook

Oil prices climbed early Thursday as markets zeroed in on the prospect of US action against Iran, lifting energy shares alongside crude – with West Texas Intermediate above $66 a barrel. The US military build-up in the Middle East means Iran’s window to reach a diplomatic agreement over its atomic activities – which Tehran insists is for peaceful domestic energy purposes – is at risk of closing fast, according to the head of the United Nations nuclear watchdog speaking to Bloomberg Television.

At this moment the Trump-assembled armada threatening Iran includes two aircraft carriers, a dozen warships, hundreds of jets, and advanced air defenses. Over 150 US military cargo flights have delivered weapons to the Middle East this month, with a surge of aircraft still headed to the region. Some say the build-up is already nearing Iraq war levels.

Director General Rafael Mariano Grossi underscored the clock is ticking. “There is not much time but we are working on something concrete,” said Grossi, in reference to meetings in Geneva with Iranian diplomats. “There are a couple of solutions the IAEA has proposed.

IAEA inspectors haven’t verified the state of Iran’s stockpile of near-bomb-grade uranium or assessed the scope of damage dealt to enrichment facilities for more than eight months.

Ironically enough, it was the unprovoked surprise Israeli and US attacks which shut the door on such inspections, also after the White House itself insisted on several occasions that the Islamic Republic’s nuclear program was “obliterated” in the series of US bunker-buster bomb attacks on Fordow, Natanz, and Isfahan. Which is it?

Bloomberg and various analysts have speculated that before the Israeli attacks in June, Iran had enough highly-enriched material to quickly craft about a dozen warheads, assuming the scenario Tehran issued the order to weaponize its nuclear program.

Grossi said he also met with Trump’s envoys on Tuesday in Geneva, alongside the IAEA’s some six hours of meetings with Iranian diplomats. He asserted that an IAEA return to the damaged facilities in Fordow, Isfahan and Natanz “hinges on the possibility of a wider type of agreement.”

“We are conscious of the fact that there is this political negotiation,” Grossi added. However, the Iranians are likely going to remain deeply distrustful of the UN watchdog and Grossi himself, given that the surprise June attack resulted in Iranian officials accusing the IAEA team of leaking sensitive data on Iranian facilities to Israel.

This is perhaps why Grossi himself appears pessimistic when commenting on the potential the forge a new deal before US military action ensues. “There cannot be a deal if the IAEA isn’t able to verify,” said Grossi, who described to Bloomberg he’s seeking a solution by threading the red lines set by both sides.

“It’s not impossible,” he said. “There are certain things that Iran understands cannot be pursued. We have to provide the watertight verification there is no deviation.”

Some reports say a US attack on Iran could come as early as this weekend…

Major US naval, air buildup in the Middle East sets stage for potential Iran war.

CNN and CBS reported Wednesday that the US military will be ready to launch strikes against Iran as early as this weekend, though Trump has reportedly not made a final decision yet… pic.twitter.com/cRJOwP2PY8

— AFP News Agency (@AFP) February 19, 2026

As the second US carrier, the USS Gerald R. Ford, is about to enter the Mediterranean while headed toward the CENTCOM area of responsibility, regional analyst Levent Kemal observes, “The US military buildup in the Middle East is going beyond dialogue or gunboat diplomacy. This is clearly an important preparation for a war aimed at removing the Iranian regime from the regional power balance equation.”

Tyler Durden

Thu, 02/19/2026 – 09:15

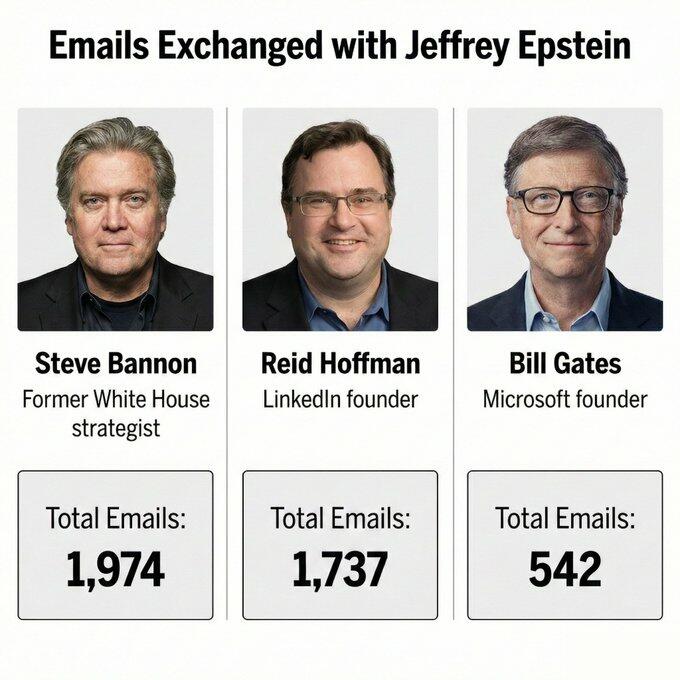

Bill Gates Pulls Out Of High-Profile Indian AI Summit As Epstein Fallout Accelerates

Bill Gates Pulls Out Of High-Profile Indian AI Summit As Epstein Fallout Accelerates

The Epstein fallout continues to spread by the day, with billionaire Les Wexner saying he was “conned” by Jeffrey Epstein and insisting he “did nothing wrong” earlier this week, and with Prince Andrew (Andrew Mountbatten-Windsor) being arrested on Thursday morning over allegations that he shared confidential government trade documents with Epstein.

Now, Bill Gates has pulled out of a keynote speech at a high-profile global AI summit in India amid the accelerating Epstein fallout.

— Gates Foundation India (@BMGFIndia) February 19, 2026

“After careful consideration, and to ensure the focus remains on the AI Summit’s key priorities, Mr. Gates will not be delivering his keynote address. The Gates Foundation will be represented by Ankur Vora, President of Africa and India Offices, who will speak later today at the Summit,” Gates Foundation India wrote on X.

The $86 billion philanthropic body’s last-minute decision to yank Gates out of a keynote address follows the billionaire’s involvement with Epstein for several years.

The Gates Foundation CEO recently told employees during a town hall event that the Gates-Epstein relationship had deeply tarnished the nonprofit’s reputation, according to a Financial Times report.

Related:

“I Deeply Regret”: Bill Gates, Reid Hoffman Deny Epstein Malarkey, And Here’s Some Weird Sh*t

New Mexico Launches Probe Into What Happened At Epstein’s ‘Zorro Ranch’

Epstein Ally Was Talking To Feds About Flip, Wanted $3 Million To Keep Quiet, Then Backed Off Deal

We asked earlier…

Hey @CERAWeek you still going with Bill Gates? https://t.co/za6L33BlOj pic.twitter.com/WsIPUddlgl

— zerohedge (@zerohedge) February 19, 2026

It is important to note that Gates has not been accused of involvement in Epstein’s sexual abuse. However, draft emails in the Epstein files show that the billionaire allegedly tried to hide a sexually transmitted disease from his then-wife, Melinda French Gates, after a sexual encounter with “Russian girls.”

Latest Epstein Emails Reveal Bill Gates Slipped Wife Antibiotics For STD He Got From Russian Hookers

FT cited a spokesperson for Gates who has said the claims are “absolutely absurd and completely false”, demonstrating only Epstein’s “frustration that he did not have an ongoing relationship with Gates.” The billionaire has publicly said that he “regrets ever having engaged with Epstein.”

Last week:

Goldman Sacks Ruemmler As Epstein Scandal ClaimsObama’ss Former Lawyer

Who gets caught up next in the Epstein fallout?

Tyler Durden

Thu, 02/19/2026 – 08:55

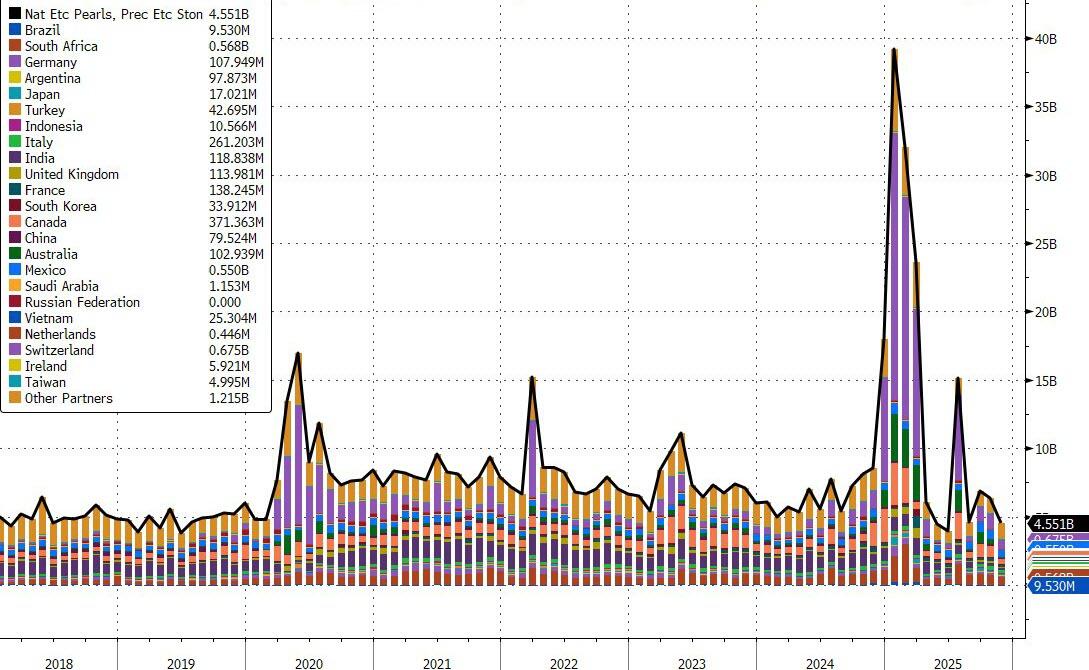

US Trade Deficit Unexpectedly Worsens As Exports Slump Again In December

US Trade Deficit Unexpectedly Worsens As Exports Slump Again In December

For the second month in a row, US exports declined and imports rose in December, pushing the US trade balance significantly deeper into deficit.

Imports rose (+3.6% vs +0.1% MoM exp) and exports fell (-1.7% vs +0.1% MoM exp) for the second month in a row…

Source: Bloomberg

Industrial Supplies appears to have seen the biggest shift in trade…

Gold imports fell back near their lowest since 2019…

The result of all this is a second monthly decline in the trade balance (worsening deficit)…

…dramatically worse than the Trump-bragged-about October highs.

Tyler Durden

Thu, 02/19/2026 – 08:51

https://www.zerohedge.com/markets/us-trade-deficit-unexpectedly-worsens-exports-slump-again-december

Futures Slide As Iran War Risks Add To Growing AI Disruption Fears; Oil Surges

Futures Slide As Iran War Risks Add To Growing AI Disruption Fears; Oil Surges

Equity futures and global markets are lower, ending a modest rebound in US stocks as concerns about a possible war with US and simmering angst over AI dent the fragile optimism seen on Wednesday. Oil extended its rally after its best day since 2021. Tech and small caps underperform which to JPMorgan’s market intel desk “feels more like profit-taking and position squaring as US / Iran tensions spike with Trump saying a deal is preferred but that a strike may occur as soon as this weekend.” As of 8:00am ET, S&P futures are down 0.2%, erasing an overnight gain, while Nasdaq futures drop 0.3%, with premarket weakness across all sectors ex-Energy and Aerospace/Def and tech came under renewed pressure; most Mag 7 members dropped in premarket trading. Futures dropped after the head of the UN nuclear watchdog warned that Iran’s window for diplomacy is at risk of closing. As for AI, IG’s chief market analyst Alexandre Baradez says there “seems to be no long-short strategy at play,” with hyperscaler capex and disruption to software firms both causing concern. WTI crude continues to rise and is trading at $66 after it added $2.86 /+4.6% yesterday, its strongest day since 2021. At some point Trump will have to decide if he wants war with Iran or risk soaring gas prices into the midterms. Treasuries extended their slide, pushing yields higher by 1-2bps, while the dollar was flat. Gold erased an advance above $5,000 an ounce. Today’s macro data focus is on Jobless data and the Leading Index

In premarket trading, Mag 7 stocks are mostly lower (Microsoft +0.3%, Amazon -0.2%, Alphabet -0.2%, Nvidia -0.2%, Apple -0.4%, Meta Platforms -0.5%, Tesla -0.6%)

Avis Budget (CAR) falls 16% after the car-rental company forecast adjusted Ebitda for 2026 that missed the average analyst estimate.

Carvana (CVNA) plunges 11% after rising costs at the online used-car retailer hit margins. Analysts flag weak retail gross profit per unit.

Cheesecake Factory (CAKE) falls 5% after the restaurant chain’s comp sales during the fourth quarter came in below the average analyst estimate.

Chewy (CHWY) rises over 3% after Raymond James upgraded to outperform, citing the attractive risk/reward created by recent stock weakness.

Deere (DE) is up 6% after the company boosted its annual profit outlook as the farm-machinery maker anticipates the agriculture economy will get better soon.

DoorDash (DASH) rises 9% after the food-delivery company issued a first-quarter orders growth forecast that topped estimates. Evercore ISI notes that fundamentals are improving and that the management’s commentary helped alleviate some investor concerns.

EPAM Systems (EPAM) slumps 17% after the IT services company forecast its FY revenue growth rate below Wall Street expectations.

Fiverr International (FVRR) slips 2% after receiving several analyst downgrades, with firms seeing a weaker outlook for the freelance-services marketplace in the wake of its results.

Herbalife (HLF) rises 12% after the nutrition company said football star Cristiano Ronaldo had invested $7.5 million and provided sponsorship rights for a 10% equity stake in HBL Pro2col Software.

Hims & Hers Health (HIMS) rises 5% after the telehealth company agreed to acquire Eucalyptus, a digital health company, for up to $1.15 billion.

Occidental (OXY) climbs 5% after the exploration and production company gave 2026 capital expenditure guidance that was lower than expectations.

ProPetro (PUMP) rises 3% after the fracturing company reported fourth-quarter earnings that beat the average analyst estimate and grew its contracted power capacity.

Remitly (RELY) climbs 22% after the international money transfer service provider reported results and issued a forecast that topped analyst expectations.

Walmart Inc. (WMT) slips 3% after issuing a forecast for full-year earnings that missed higher expectations, flagging the unpredictable state of trade and labor market conditions.

Wayfair (W) falls 6% after the ecommerce firm reported fourth quarter results.

In corporate news, OpenAI is said to be close to securing the first phase of funding likely to bring in more than $100 billion. Samsung is looking to price its latest AI HBM4 chip up to 30% higher than the previous generation, according to local media. The CEO of Google DeepMind warned about AI risks and called for global cooperation.

What started off a solid overnight session promptly reversed just around the time Europe opened when futures tumbled into the red after the head of the United Nations nuclear watchdog warned that Iran’s window for a diplomatic deal on its atomic program is closing. Brent rose above $71 a barrel, while West Texas Intermediate was near $66. The risk of conflict in the Middle East has emerged as a new worry for traders after technology stocks drove sharp swings in recent weeks.

Brent rose above $71 a barrel, while West Texas Intermediate was near $66. Inflation concerns are already at the forefront of investors’ minds after minutes of the Federal Reserve’s January policy meeting showed several officials suggested that the central bank may need to raise rates if price growth remains stubbornly high.

Investors also remain wary of further slowing in the S&P 500’s strongest driver of the past three years, amid concerns that AI could disrupt entire sectors and that heavy capital spending wouldn’t pay off.

“What’s really interesting is that there seems to be no long-short strategy at play,” said Alexandre Baradez, chief market analyst at IG in Paris. “This will continue at least until the next earnings season when we’ll get more insight. In the meantime, all eyes will be on Nvidia’s results next week.”

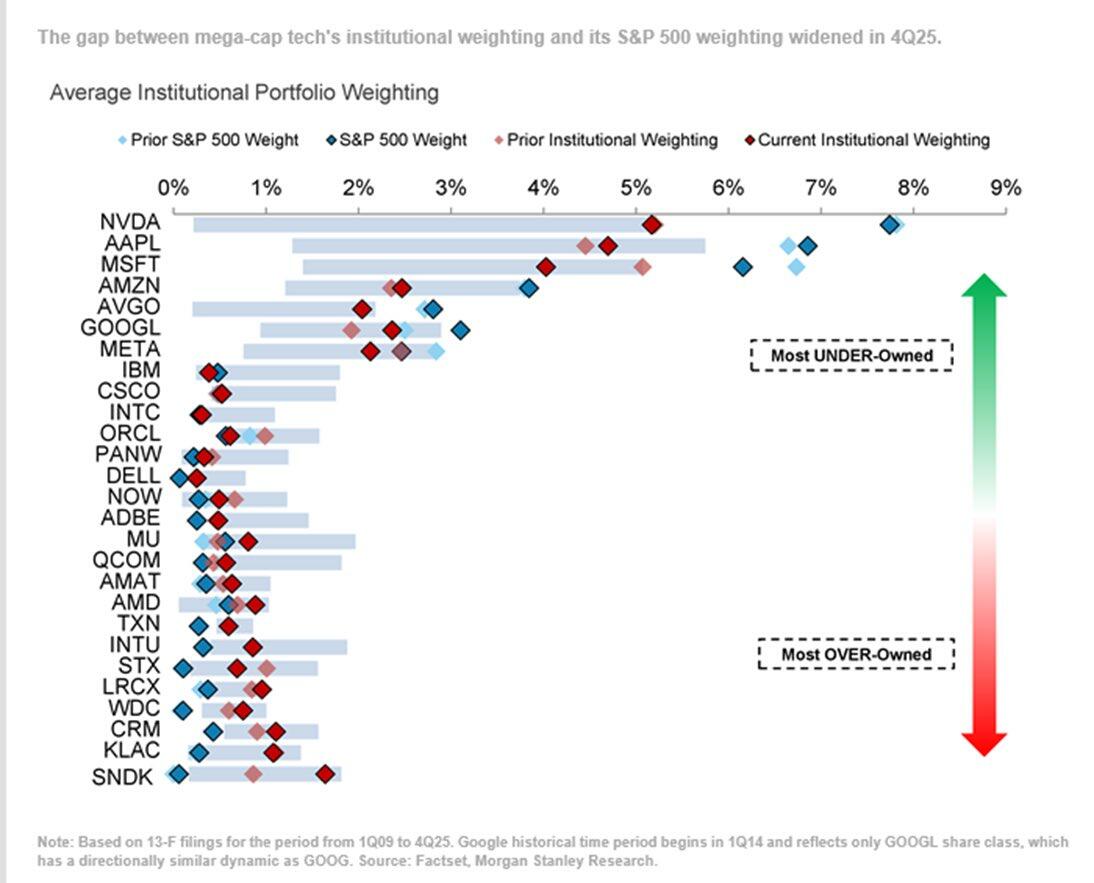

Indeed, doubts about Big Tech are playing out across the market. As we first showed here yesterday, Morgan Stanley’s analysis of 13F filings shows mega-cap tech stocks finished the year the most under-owned relative to their weightings in the S&P 500 in 17 years.

And Goldman Sachs data shows 57% of large-cap mutual funds outperforming their benchmarks year-to-date, the highest share since 2007, with rotation in the equity market leading to a broadening in returns.

Simmering geopolitical risks and still-elevated tech valuations could fuel further rotation out of megacaps and into defensive sectors, said Craig Cameron, a portfolio manager at Templeton Global Investments. Still, the vast amount of capital expenditure shows that exposure to technology remains vital, he said.

“These sectors that are feeding into the AI capex cycle and the electrification cycle, those are the right places to be,” he said. “As valuations move higher, the right thing to do is to move into unloved areas and reduce that overweight over time.”

Walmart and Deere are among companies expected to report results before the market opens. Walmart results face a high bar from investors, but the main focus will be guidance and the new CEO will contend with uneven consumer sentiment, fierce competition and a lackluster US labor market. Earnings from Newmont and Copart follow later in the day.

European stocks retreated from Wednesday’s record close with the Stoxx 600 down 0.7%, after underwhelming earnings from the likes of Airbus and Renault, with investors also monitoring geopolitical risks. Nestle gained after it said sales growth would likely quicken this year. Here are some of the biggest movers on Thursday:

FDJ United shares rally as much as 8.8%, the most since July 2024, as the lottery provider’s full-year results meet analysts’ expectations.

Air France-KLM shares rise as much as 16% to the highest level since September, after the airline operator reported better-than-expected earnings in the fourth quarter.

Covivio shares advance as much as 9.1%, the most since April 2025, with analysts describing the real estate investment trust’s 2025 performance as solid.

Azelis shares rise as much as 9.6% after the Belgian chemicals distribution firm posted results which JPMorgan said represented a smaller miss than peer IMCD reported yesterday, which had caused a sharp drop in the stock.

Tenaris shares rise as much as 6.5% in Milan, climbing to the highest since July 2008, after the steel pipe manufacturer reported robust results.

Orange shares rise as much as 5.6% to the highest levels since 2010 as investors cheered the telecom operator’s guidance, including a lower capital spending target.

Nestle shares rise as much as 4.5%, the most since October, after what RBC described as a “decent” fourth-quarter print from the Swiss food giant.

Arcadis shares plunge as much as 21%, crashing to a 2021 low, after the provider of consulting and engineering services reported earnings that were well below expectations and issued guidance that analysts at Jefferies say will significantly reduce expectations for this year.

Aegon shares drop as much as 6.8%, the most in two months, after the Dutch insurance group reported a mixed set of earnings and failed to provide an update on its UK strategic review.

Airbus shares fall as much as 5.9% after the French airplane company forecast commercial aircraft deliveries for 2026 of about 870 planes, lower than most previous estimates.

Rio Tinto shares decline as much as 4.4% in London, its biggest intraday drop since August, after the miner reported net debt that analysts say missed expectations.

Euronext drops as much as 5.1% after announcing cost guidance for 2026 that’s higher than consensus expectations, overshadowing its small fourth-quarter beats.

Centrica shares tumble as much as 9.6%, the steepest drop since July 2024, after the British energy company did not announce a new buyback in its results

Earlier in the session. Asian stocks climbed, led by South Korea. The MSCI Asia Pacific Index rose as much as 0.6%, extending gains to a second day. Samsung Electronics and Tokyo Electron were among the biggest boosts to the gauge. South Korea’s Kospi Index advanced to a fresh record as markets reopened after a three-day holiday, while benchmarks in Japan and Singapore jumped more than 1%.

In FX, the Bloomberg Dollar Spot index is a touch higher after dipping in the European morning as EUR/USD and cable briefly reclaimed 1.18 and 1.35 respectively, and USD/JPY slipped below 155. Aussie dollar is near the top of the G-10 pile following following strong jobs data overnight.

In rates, treasuries were on course for their longest losing streak in a month as tensions in the Middle East fuel oil-driven inflation fears. The 10-year yield rose for a third day, up one basis point to 4.09%. Treasury hold small losses into the Thursday open, with yields 1bp to 2bp cheaper across a slightly steeper curve, partially unwinding this week’s flattening trend. Oil prices, up 1.6% near high end of range since August on growing tensions between the US and Iran, add to upside pressure on Treasury yields via increased inflation expectations. US 10-year yield is less than 1bp higher on the day near 4.095% after topping 4.10% for first time this week; German and UK counterparts see steeper increases, adding to pressure on Treasuries. Treasury plans $9 billion 30-year TIPS new issue auction at 1pm New York time. Focal points of US session include weekly jobless claims, 30-year TIPS auction and several Fed speakers.

In commodities, oil has continued its climb with Brent making its way onto a $71/bbl handle as Iranian conflict concerns continue to support prices. Axios reported on Wednesday that a major US military operation in the Middle East could begin soon. Upside in energy is supporting global bond yields. Spot gold has slipped below the $5,000 mark, still up 0.2% but lagging silver, up 1.3%. Bitcoin of course tumbles to LOD.

US economic calendar slate includes December trade balance, wholesale inventories, February Philadelphia Fed business outlook and weekly jobless claims (8:30am), and December Leading index and January pending home sales (10am). Fed speaker slate includes Bostic (8:20am), Bowman (8:30am), Kashkari (9am) and Goolsbee (10:30am)

Market Snapshot

S&P 500 mini -0.4%

Nasdaq 100 mini -0.5%

Russell 2000 mini -0.5%

Stoxx Europe 600 -0.7%

DAX -0.9%

CAC 40 -0.9%

10-year Treasury yield +1 basis point at 4.09%

VIX +1 points at 20.66

Bloomberg Dollar Index little changed at 1189.41

euro little changed at $1.179

WTI crude +1% at $65.81/barrel

Top Overnight News

British Police arrest King Charles’ brother Andrew over misconduct relating to Epstein

U.S. Gathers the Most Air Power in the Mideast Since the 2003 Iraq Invasion: WSJ

The US military build-up in the Middle East means Iran’s window to reach a diplomatic agreement over its atomic activities is at risk of closing, according to the head of the United Nations nuclear watchdog. The International Atomic Energy Agency has discussed concrete proposals with Iranian Foreign Minister Abbas Araghchi to inspect sites bombed last year by Israel and the US: BBG

Ukrainian President Volodymyr Zelenskiy says the US, and perhaps some Europeans, are discussing a new document between NATO and Russia: BBG

OpenAI Funding on Track to Top $100 Billion in Latest Round: BBG

Bill Gates pulls out of India AI summit amid Epstein scrutiny: RTRS

Epstein Waged a Years-Long Quest to Meet Putin and Talk Finance: BBG

The Bank of Japan may raise interest rates as soon as March or April, Junichi Hanzawa, chairman of the Japanese Bankers Association, says at a regular news briefing in Tokyo

Swiss watch exports resumed their long slump in January after a brief respite the previous month triggered by the easing of US tariffs: BBG

France’s strategy to reduce its budget deficit this year remains “very uncertain,” even after the government set less ambitious targets than initially planned, the country’s audit court said: BBG

Walmart Sales Climb, Driven by Grocery and Online Gains: WSJ

Walmart Cites Trade, Labor Concerns in Cautious Profit Forecast: BBG

Top European spies sceptical US will clinch Ukraine peace deal this year: RTRS

Top Lawyers’ Fees Have Skyrocketed. Be Prepared to Pay $3,400 an Hour: WSJ

From Paris to New Delhi, the Push to Ban Teens From Social Media Is Going Global: WSJ

Steve Cohen’s $3.4 Billion Payday Tops Hedge Fund Ranks: BBG

The Far-Fetched Mission to Reclaim Islands That Host a Key U.S. Military Base: WSJ

Trade/Tariffs

US President Trump and his advisors have reportedly indicated that the USMCA could be scrapped, NY Times reports. Instead, the US could have bilateral deals with Canada and Mexico. US officials have been increasing pressure on Canada. Canadian officials cited add that their expectation for a full renewal of the USMCA is very low. Officials believe Trump is trying to weaken Canada economically to force it to give up some protectionist policies. The article reminds us that in 2018, the US proposed a bilateral deal with Mexico and told Canada to get on board or be left out.

US-ASEAN Business Council said US and Indonesian companies signed trade and investment deals covering critical minerals, semiconductors, agriculture and forestry, while deals include a USD 4.89bln semiconductor joint venture involving Essence Global Group. Indonesian firms are to purchase 1mln tons of US soybeans, 1.6mln tons of corn, and 93,000 tons of cotton over an unspecified period.

US President Trump posted that the US trade deficit has been reduced by 78% because of the tariffs being charged to other companies and countries, adds it will go into positive territory during this year for the first time in many decades.

Canadian minister responsible for Canada-US trade LeBlanc said Canadian companies from various provinces have signed 15 commercial partnerships in Mexico.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher following the positive handover from the US and with South Korea outperforming amid tech strength on return from the Lunar New Year holidays. ASX 200 rallied to a fresh record high with the gains led by strength in telecoms and energy, as the former was boosted alongside Telstra, which reported a 9.3% increase in H1 net profit, while energy stocks benefitted from the rise in underlying oil prices amid geopolitical frictions. Nikkei 225 gained with sentiment underpinned by a weaker currency and stronger-than-expected Machine Tool Orders. KOSPI outperformed on return from the Lunar New Year holiday closure as tech stocks played catch-up to the rebound in their US counterparts, including index heavyweight Samsung Electronics, as its shares rallied by around 5% to a record high.

Top Asian News

Australian Unemployment Rate (Jan) 4.1% vs. Exp. 4.2% (Prev. 4.1%).

Australian Employment Change (Jan) 17.8K vs. Exp. 20K (Prev. 65.2K, Low. -5K, High. 40K).

Australian Part Time Employment Chg (Jan) -32.7K (Prev. 10.4K).

Australian Full Time Employment Chg (Jan) 50.5K (Prev. 54.8K).

Australian Participation Rate (Jan) 66.7% vs. Exp. 66.8% (Prev. 66.7%).

Japanese Stock Investment by Foreigners (Feb/14) 1424.2 (Prev. 591.4, Rev. From 543.2).

Japanese Machinery Orders YoY (Dec) Y/Y 16.8% vs. Exp. 3.9% (Prev. -6.4%, Low. -1.1%, High. 10.6%).

Japanese Machinery Orders MoM (Dec) M/M 19.1% vs. Exp. 4.5% (Prev. -11.0%, Rev. From -11%, Low. 1%, High.

European bourses (STOXX 600 -0.7%) are entirely in the red. The FTSE MIB (-1.2%), DAX 40 (-0.9%) and CAC 40 (-0.8%) are the clear underperformers after a flurry of corporate news. European sectors are mixed, with a slight tilt to the downside. Food, Beverage and Tobacco (+0.7%) is outperforming following earnings by Nestle (+2.5%), which announced that it is in advanced negotiations to sell its remaining Froneri stake. At the bottom sits Basic Resources (-2.8%), Autos and Parts (-2.1%) and Utilities (-2.2%). The former continues to have a choppy week, this time catalysed by Rio Tinto (-4.6%) as FY profit failed to grow and a drag on its iron ore unit in China. For the latter, Italian utilities (A2A -3.7%, Enel -4.1%, Italgas -2.1%) have been hit after Italy approved a 2bp hike in its IRAP corporate tax. Renault (-5.9%) has been weighing on the Autos sector after posting a net loss worse than expected.

Top European News

UK’s ONS on ongoing data issues, reported the “Latest steps reaffirm commitment to quality over quantity”.

FX

DXY has waned from overnight highs after advancing yesterday and overnight amid better-than-expected data and as oil prices surged after sources noted the Trump administration is closer to a major war with Iran than people realise. On the US docket ahead, weekly initial jobless claims (which coincide with the traditional survey window for the BLS’ February jobs data) are expected little changed at 225k (prev. 227k), while continuing claims (this week does not coincide with the BLS window) are seen unchanged at 1.87mln. Most recently, a NYT report suggested that the Trump administration indicated that the USMCA could be scrapped, in favour of bilateral deals with Canada and Mexico. DXY resides in a current 97.572-97.777 range at the time of writing.

JPY is narrowly softer but off worst levels, with USD/JPY hovering around its 100 DMA (154.744), with some fleeting strength seen yesterday in wake of the FOMC minutes in which the Fed confirmed it did a USD/JPY rate check on behalf of the US Treasury in January. Analysts at ING highlight that “Something like this is extremely rare in foreign exchange markets and is a sign of a more activist White House when it comes to FX. The move was clearly designed to deliver maximum impact and reflects the shared desire from both Washington and Tokyo that USD/JPY does not sustain a move through 160”.

EUR trims some of yesterday’s losses after briefly slipping beneath the 1.1800 level (to a 1.1782 low on Wednesday) as the buck strengthened, and with the single currency not helped by conflicting reports about ECB President Lagarde’s future. Recent reports suggested ECB President Lagarde reportedly tells colleagues that she would tell them first if she were to step down, according to sources; colleagues reportedly interpreted this to mean her departure is not immediate, but the door is not closed. EUR/USD resides towards the top end of a 1.1781-1.1808 range.

Antipodeans outperform amid recent underperformance and following positive risk appetite in APAC (before waning in European hours), with AUD/USD supported following the mixed jobs data, which showed headline employment change slightly missed expectations, although the unemployment rate printed lower than expected, and the increase in jobs was solely fuelled by full-time work.

Central Banks

WSJ’s Timiraos noted regarding the January Fed meeting minutes that it was interesting there was no date specified for when inflation gets to 2%, and instead minutes states that forecast is “slightly higher, on balance”.

Japan Bank Lobby said markets expect a BoJ hike as soon as March; Lobby Head believes there is a reasonable possibility of a hike as early as March or April.

ECB President Lagarde reportedly tells colleagues that she would tell them first if she were to step down, according to sources; colleagues reportedly interpreted this to mean her departure is not immediate, but the door is not closed.

RBNZ Assistant Governor Silk said the easing cycle is likely over and there are risks on either side, adds maintaining accommodative policy for a while aligns with economic conditions.

SNB has defined a standardised and scalable process for the ELF that will enable participating banks to quickly obtain liquidity support against collateral as necessary.

Riksbank takes measures to facilitate banks’ liquidity management.

Fixed Income

USTs are lower by a handful of ticks this morning, and currently trade within a 112-24+ to 112-31 range. Moved lower for much of the morning, before picking up a touch as US/European equity futures dipped lower.

The bearish bias follows on from; a) the prior day’s stronger-than-expected US data, b) rising energy prices (spurred by geopolitical tensions), c) JGB pressure overnight, following strong Machine Tool Orders and a weak 20yr JGB auction, d) a poor 20yr auction; on the latter point, desks highlight that the 20yr has historically not been the markets favoured outing. On the geopolitical narrative, there have been continued reports that the US is upping its presence in Iran, with a US Senior Official telling Axios that US-Iran talks have been a “nothing burger”, and that is why POTUS is close to deciding on the issue of going to war with Iran. As it stands, US paper appears to be pricing in the inflationary impacts (higher oil prices), but an outright attack could lead to some haven-related demand.

Bunds are also pressured alongside global peers. Currently holds towards the lower end of a 129.05 to 129.31 range. Newsflow for German paper is lacking today, aside from ECB-related reporting. Source reports suggest that President Lagarde told her colleagues that she would tell them before she leaves; her colleagues reportedly interpreted this to mean her departure is not immediate, but the door is not closed. De Cos and Knot have been touted as potential replacements once President Lagarde leaves her role, though Rabobank cautions that the process is highly political and difficult to predict, noting markets should largely ignore speculation for now.

Gilts are trading in-fitting with peers, and trading around the 92.00 mark within a 91.96 to 92.03 range. UK data slate has paused for today, ahead of Retail Sales/PMIs on Friday. This follows on from dovish jobs/wages and mixed inflation metrics earlier this week, which confirmed the disinflation process but Services and Core topped-expectations, leaving the more hawkish MPC members cautious. Markets are currently torn between a cut in March or April; analysts at ING see a cut in March and then another by June.

Commodities

Crude benchmarks remain elevated amid heightening geopolitical tension between the US and Iran following the Axios report on Wednesday which noted that the US President Trump’s administration is closer to a major war with Iran than people realise. Tensions continue to persist, with an overnight report from CNN that the US military is ready to strike Iran as early as this weekend and the WSJ reporting that the US has gathered the greatest amount of air power in the Middle East since the 2003 Iraq invasion. WTI and Brent are trading at the upper end prices of USD 64.84-66.27/bbl and USD 70.18-71.60/bbl, respectively, with Brent touching the USD 71/bbl, which marks the first time since August last year.

Precious metals are firmer, benefiting from haven demand from the ongoing geopolitical tension between the US and Iran, with the yellow metal crossing the USD 5,000/oz mark. The weaker USD ahead of the FOMC minutes also spurred demand for the yellow metal. XAU and XAG are trading at the upper range of USD 4979.14-5040.21/oz and USD 76.355-79.355.

Copper price action is moving contrary to the trend seen in precious metals. Risk sentiment in the early European session as well as subdued activity from Asia due to the Chinese holiday has seen the red metal trading lower thus far. 3M LME copper trades at the lower price range of USD 12.846-12.937k/t.

US Energy Secretary Wright said the US could leave the IEA if the group does not change.

Hungarian PM Orban’s Chief of Staff said they would take steps in the scenario that Ukraine continues to halt Druzhba oil shipments.

US Treasury Department issues general license authorising transactions related to oil and gas sector operations in Venezuela.

US Private Inventory Data (bbls): Crude +0.6mln (prev. +13.4mln), Distillate -1.6mln (prev. -2.0mln), Gasoline -0.3mln (prev. +3.3mln), Cushing -2.4mln (prev. +1.4mln).

Geopolitics: Ukraine

Ukrainian President Zelensky said he is aware that the US and Europe have been talking to Russia and we must be prepared to react to surprises.

Russia’s Kremlin on the Iran situation said they see unprecedented escalation of tensions and on Ukraine talks, said there’s nothing to add following comments from the likes of Medinsky yesterday. Reiterates that no date has been set for the next Ukraine talks.

Geopolitics: Middle East

IAEA Director Grossi said Iran discussed a potential IAEA return to bombed nuclear sites, adds there is no deal unless the IAEA was in a position to verify and there is not much time to reach an Iran nuclear deal, via Bloomberg TV. His role is to get the nations into a position to come to a deal without the need for force. IAEA has proposed a few solutions.

Russian Foreign Minister Lavrov warns of any new US strike on Iran.

Israeli raid reported on areas of deployment of occupation forces east of Gaza City, according to Al Jazeera.

Two Israeli defense officials said that significant preparations were underway for possibility of a joint strike with the US against Iran, according to NYT.

US gathers the greatest amount of air power in the Middle East since the 2003 Iraq invasion and President Trump is being briefed on military options for striking Iran, even as aides hold talks with the Iranian regime, according to WSJ.

Iraqi Foreign Minister said any alternative to US-Iran deal would be disastrous, and they may not be able to export their oil if war breaks out in the region.

US military is ready to strike Iran as early as this weekend, although President Trump has yet to make the final decision, according to sources familiar with the matter cited by CNN.

US senior official said US expects Iran to submit a written proposal on resolving standoff in the wake of Tuesday’s talks.

Geopolitics: Others

US is pushing NATO to cut many foreign activities, including ending a key alliance mission in Iraq, according to four NATO diplomats cited by POLITICO.

Israeli Defense Forces announced they struck Hezbollah infrastructure sites in southern Lebanon, according to Sky News Arabia.

US Southern Command Commander Donovan met with Venezuela’s interim President Rodriguez and defence officials in Caracas.

North Korea’s Kim Yo Jong said military will take measures to strengthen its vigilance on border with South Korea; she appreciates South Korean Unification Minister’s official recognition of South Korea’s drone provocation. Border with the enemy should be solid.

US Event Calendar

8:30 am: United States Dec Trade Balance, est. -55.5b, prior -56.8b

8:30 am: United States Dec P Wholesale Inventories MoM, est. 0.2%, prior 0.2%

8:30 am: United States Feb Philadelphia Fed Business Outlook, est. 7.5, prior 12.6

8:30 am: United States Feb 14 Initial Jobless Claims, est. 225k, prior 227k

8:30 am: United States Feb 7 Continuing Claims, est. 1860k, prior 1862k

8:30 am: United States Fed’s Bowman Gives Opening Remarks at Banking Conferernce

9:00 am: United States Fed’s Kashkari in Fireside Chat on Economic Outlook

10:00 am: United States Dec Leading Index, est. -0.2%, prior -0.3%

10:00 am: United States Jan Pending Home Sales MoM, est. 2%, prior -9.3%

10:30 am: United States Fed’s Goolsbee Gives Opening Remarks

DB’s Jim Reid concludes the overnight wrap

The disruption narrative has taken a well-earned breather for much of this week, helping to steady nerves. Positive economic data and supportive tech news over the past 24 hours have built on that calm, pushing most major indices to solid gains. The S&P 500 advanced by +0.56%, the NASDAQ by +0.78%, while in Europe the STOXX 600 (+1.19%), FTSE 100 (+1.23%) and CAC (+0.81%) all reached new record highs. Overnight the KOSPI has reopened +2.81% higher after a 3-day break and the Nikkei (+0.78%) and Topix (+1.23%) are also higher.

Part of the catalyst for the rally were pre-US market reports that Nvidia (+1.63%) had agreed to supply Meta (+0.61%) with large quantities of processors over the coming years. The news boosted both technology and semiconductor stocks, with the Philadelphia Semiconductor Index up +0.96% and the Magnificent 7 rising by +0.77%. That said, the Magnificent 7 continues to underperform on a year to date basis (6.35%). Semiconductor sentiment was further supported by strong quarterly results and guidance from Analog Devices (+2.63%). US equity gains were also pretty broad, with almost two-thirds of the S&P 500 higher on the day, though defensive sectors including consumer staples (-0.53%) and utilities (-1.70%) underperformed.

The equity rally was reinforced by solid US economic data. January industrial production rose +0.7% m/m versus expectations of +0.4%, while factory output increased +0.6% m/m, also beating forecasts. These prints marked the biggest monthly rises in eleven months. Earlier in the morning, core capital goods shipments rose +0.9% in December (+0.3% expected), and with +0.4pp revision for the prior month. US housing starts also reached a five month high in November but that’s clearly a bit backward looking now. Next up on the data front, today’s jobless claims (215k vs. 226k) will be closely watched, given their overlap with the February employment survey period.

Treasury yields moved higher for a second day running in response to the data, with the 2yr yield up +2.7bps to 3.46% and the 10yr up +2.4bps to 4.08%. The grind higher in rates was also supported by hawkish-leaning minutes of the January FOMC meeting. Notably “the vast majority of participants judged that labor market conditions had been showing some signs of stabilization”, even though the meeting had taken place before the improved January jobs report. And “several participants indicated” support for more two-sided language on future rate moves, raising the possibility of rate hikes “if inflation remains at above-target levels”. While that’s still far from an active call to raise rates, it adds to the sense that most of the FOMC are in no rush to deliver further cuts. Overnight, US yields are up a further +1 to 1.5bps across the curve.

Elsewhere, oil rebounded sharply from Tuesday’s decline. The immediate trigger appeared to be an Axios op ed warning that the US and Iran may be moving closer to a major confrontation, though it is difficult to point to any single catalyst. More broadly, investors seem to have concluded that there has been no meaningful political breakthrough following talks earlier this week. Against that backdrop, Brent and WTI both rose by more than +4%, with Brent moving back above $70/bbl. Precious metals also recovered amid renewed geopolitical unease, with gold up +2.04% and silver jumping +5.00%. All three are edging up a little more this morning.

In Europe, front end bond yields edged higher on concerns about rising oil prices, while moves further along the curve were mixed. The 10yr bund yield was +0.1bps, while OATs (-0.6bps) and gilts (-0.2bps) edged lower. And 2yr gilts (-0.4bps) gained despite a slightly firm UK CPI print, which showed January inflation easing to +3.0% y/y from +3.4%, in line with consensus but 0.1pp above the Bank of England’s forecast. Core inflation was slightly stickier than expected at +3.1% y/y (+3.0% expected). While this does mark the lowest headline inflation in 10 months, the data could complicate the BoE’s March decision at the margin, though our UK economist still expects a cut next month given the deteriorating labour market.

Staying with Europe, the FT reported yesterday that Christine Lagarde is considering stepping down early as ECB President (as we mentioned as the story was breaking this time yesterday), ahead of the scheduled end of her term in October 2027. This potentially links to reports earlier in the week that EU leaders are discussing a package deal to fill upcoming ECB executive board vacancies at once, with Lagarde, Lane and Schnabel all due to leave during the course of 2027. A motivating factor for a possible bundling of appointments is that it would allow current European leaders to make the decision over ECB leadership, insulating it from the influence of a possible far-right French President after the next election in April 2027, especially given the RN’s past rhetoric on redefining the ECB’s mandate. Our European economists do not expect any early change in ECB leadership to significantly change the path of ECB policy going forward, with their baseline view that the ECB will keep rates on hold until mid 2027.

Other than what we discussed at the top about a rally this morning in Asia, the other story of note has been the Australian job numbers. Total employment increased by 17,800 in January, which was close to the consensus forecasts of around 20,000, but the unemployment rate surprisingly remained stable at 4.1%, a tenth below expectations. 3 and 10yr Aussie yields are +7.8bps and +6bps higher respectively. The ASX is +0.78% higher.

Looking ahead, today brings further US data including the February Philadelphia Fed business outlook, January pending home sales and initial jobless claims. Elsewhere, we’ll see France’s January retail sales, Italy’s December current account balance, Eurozone December construction output and February consumer confidence. Central bank events include the ECB’s economic bulletin and speeches from Fed officials Bostic, Kashkari and Goolsbee. Notable earnings include Walmart, Nestlé and Airbus, while the US will also auction $9bn of 30 year TIPS.

Tyler Durden

Thu, 02/19/2026 – 08:44

El Vaticano anuncia intensa gira del papa León XIV por Italia

Por NICOLE WINFIELD

ROMA (AP) — Lampedusa, y también atenderá a italianos envenenados por años de vertidos tóxicos de la mafia, según los planes de viaje anunciados el jueves por el Vaticano.

El Vaticano difundió la agenda del pontífice para distintos viajes de un día a media docena de ciudades italianas durante los próximos seis meses. El Vaticano pocas veces publica planes de este tipo en conjunto y con tanta antelación, pero la noticia de las visitas empezaba a filtrarse.

El apretado itinerario, que llevará a León de norte a sur por la península italiana, se suma a los planes de algunos intensos viajes internacionales previstos para 2026. Se estudian planes para un viaje a cuatro países de África después de Pascua, que llevaría al pontífice a Argelia, Guinea Ecuatorial, Angola y Camerún. El propio León ha dicho que espera visitar su querido Perú, así como Argentina y Uruguay, viajes que podrían realizarse hacia finales de año.

El Vaticano confirmó previamente que un viaje al extranjero que no figura en la agenda de este año es a Estados Unidos, país natal del papa.

El primer pontífice de la historia nacido en Estados Unidos no pudo salir mucho de Roma durante su primer año en el papado debido a la intensa agenda del Año Santo 2025, que llevó a millones de peregrinos al Vaticano para misas especiales y audiencias papales.

Ahora que ha finalizado el Jubileo, León puede salir de la ciudad con mayor facilidad: ha comenzado una serie de visitas a parroquias dentro de su diócesis romana cada domingo durante la Cuaresma, el periodo previo a la Pascua.

Y el itinerario por Italia anunciado el jueves lo llevará cerca y lejos, mientras conoce mejor a la Iglesia y a los fieles italianos.

Los viajes comienzan el 8 de mayo con una visita a Nápoles y a la cercana ciudad antigua de Pompeya. Regresará a la región más adelante ese mes, el 23 de mayo, para reunirse con los fieles de Acerra. La zona es conocida como la “Tierra de los Fuegos”, por los años de vertido de residuos tóxicos por parte de la mafia local, lo que ha provocado un aumento de las tasas de cáncer y otros padecimientos entre sus habitantes.

León viajará al norte, a Pavía, cerca de Milán, el 20 de junio, y luego, el 4 de julio, a Lampedusa, una isla italiana que está más cerca de África que del territorio continental italiano. Después de su elección en 2013, el papa Francisco visitó Lampedusa en su primer viaje fuera de Roma para mostrar solidaridad con los migrantes que llegaban a la isla tras ser introducidos clandestinamente desde el norte de África.

En un acto que se volvió famoso, Francisco celebró una misa en la isla sobre un altar hecho con restos de embarcaciones de migrantes y denunció la “globalización de la indiferencia” con la que se recibe a los migrantes que arriesgan la vida intentando llegar a Europa, un lema que llegaría a definir su pontificado.

León visitará el 6 de agosto la localidad umbra de Asís, situada en lo alto de una colina, que este año conmemora el 800mo aniversario de la muerte de su habitante más célebre, San Francisco. Y más adelante ese mes, el 22 de agosto, participará en una conferencia política y religiosa anual italiana en el balneario adriático de Rímini.

León, que nació en Chicago y pasó dos décadas como misionero en Perú, ha dicho que le encanta viajar. Pasó muchos años en la carretera cuando cumplió dos mandatos de seis años como superior de su orden religiosa agustina, lo que le exigía visitar comunidades agustinas en todo el mundo.

___

La cobertura de temas religiosos de The Associated Press recibe apoyo a través de la colaboración de la AP con The Conversation US, con financiación de Lilly Endowment Inc. La AP es la única responsable de este contenido.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

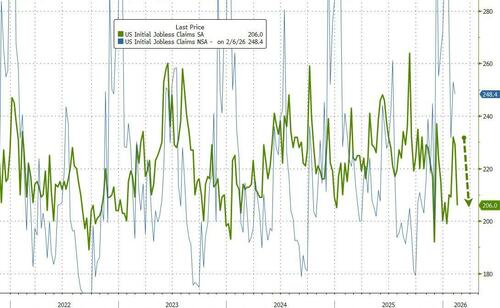

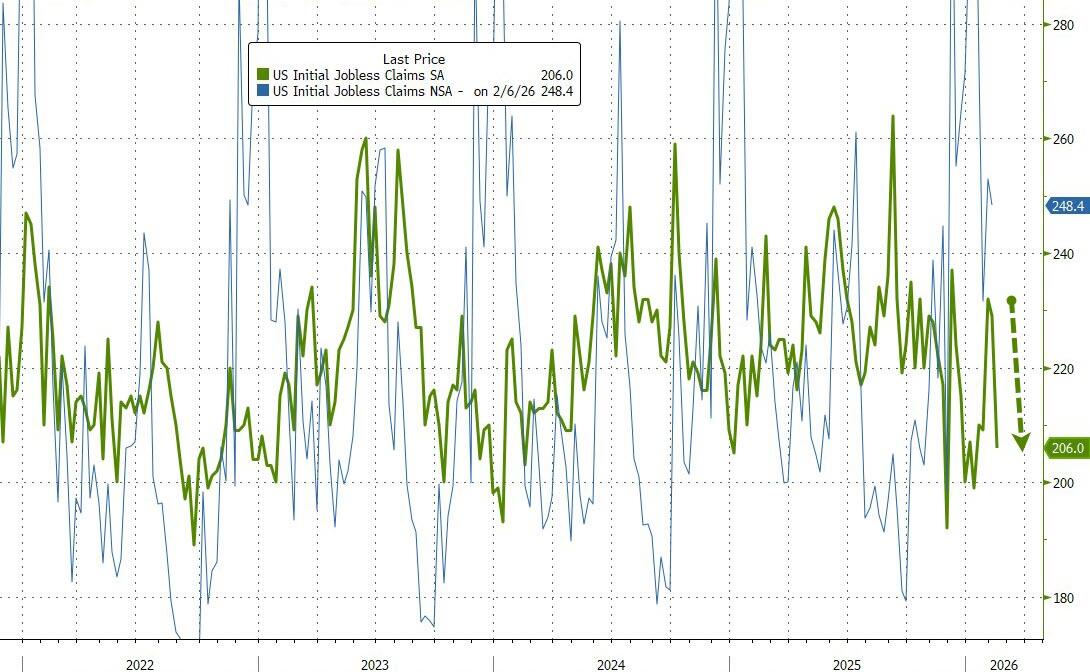

Initial Jobless Claims Tumble Back Near Multi-Decade Lows

Initial Jobless Claims Tumble Back Near Multi-Decade Lows

Despite the ongoing worsening trend in some labor market condition indicators – Payrolls revisions ugly, JOLTs are tumbling, Survey-based data showing jobs hard to get far worse than jobs plentiful – the number of Americans filing for jobless benefits for the first time fell to 206k (from 229k the prior week)…

Source: Bloomberg

That is back near multi-decade lows and at the lowest end of the range of the last five years.

Continuing jobless claims rose modestly (from 1.852mm to 1.869mm) but remains well below the 1.9mm Maginot Line…

So, should we just be ignoring surveys completely now?

Or are we solidly back in the ‘no hire, no fire’ economy?

Tyler Durden

Thu, 02/19/2026 – 08:36

https://www.zerohedge.com/personal-finance/initial-jobless-claims-tumble-back-near-multi-decade-lows

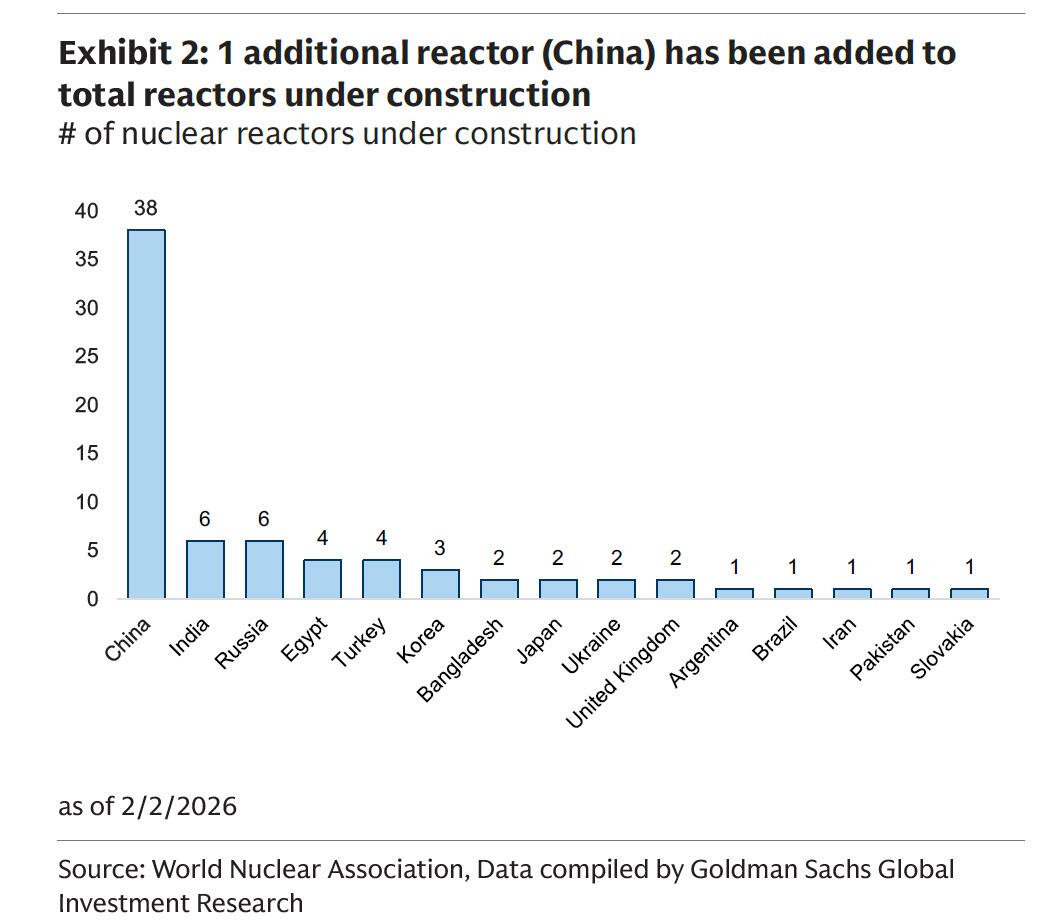

US Is Rapidly Expanding Its Nuclear Supply Chain: It’s Not Nearly Fast Enough

US Is Rapidly Expanding Its Nuclear Supply Chain: It’s Not Nearly Fast Enough

As we have repeatedly highlighted (most recently here), the much-hyped resurgence in US nuclear power is notable for one thing: the lack of actual new reactors. In fact, according to the latest Goldman Nuclear Nuggets monthly report, while China is currently building 38 new nuclear reactors – and both India and Russia have 6 reactors under construction – the US is not even on the chart.

Indeed, despite splashy announcements, like November’s agreement for Japan to fund a $80 billion plan to build as many as 10 big reactors in the US, no new commercial-scale facilities are actually under construction. Meanwhile in China, work has started on 10 new sites since the beginning of 2025 (for the full list see the February Nuclear Nuggets report).

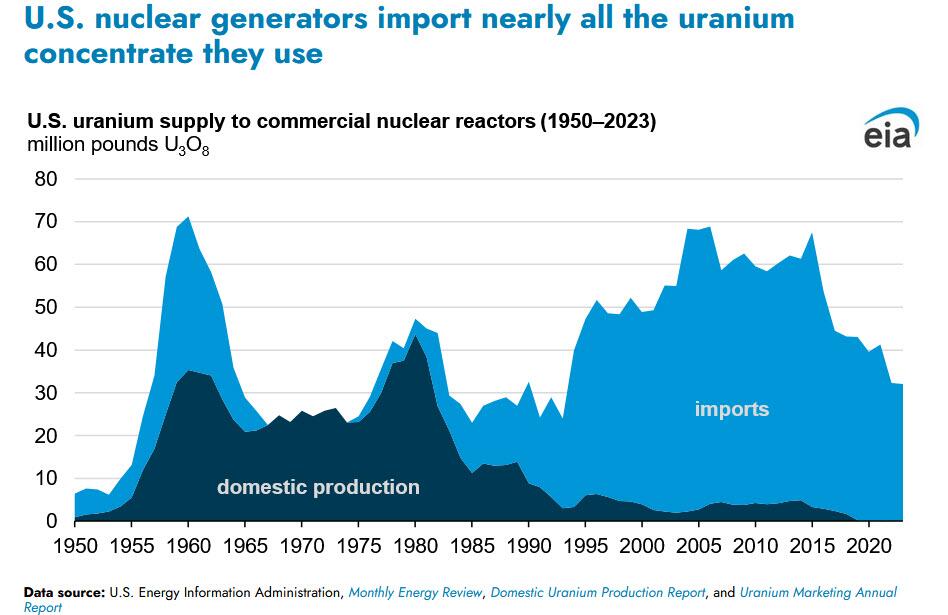

And even if reactors were being built in the US right now (which they aren’t) it’s unclear how they would be fueled.

As Bloomberg writes, almost all of the uranium going into the current US nuclear fleet is imported, and there’s only enough enrichment capacity to supply about one-third of domestic reactors.

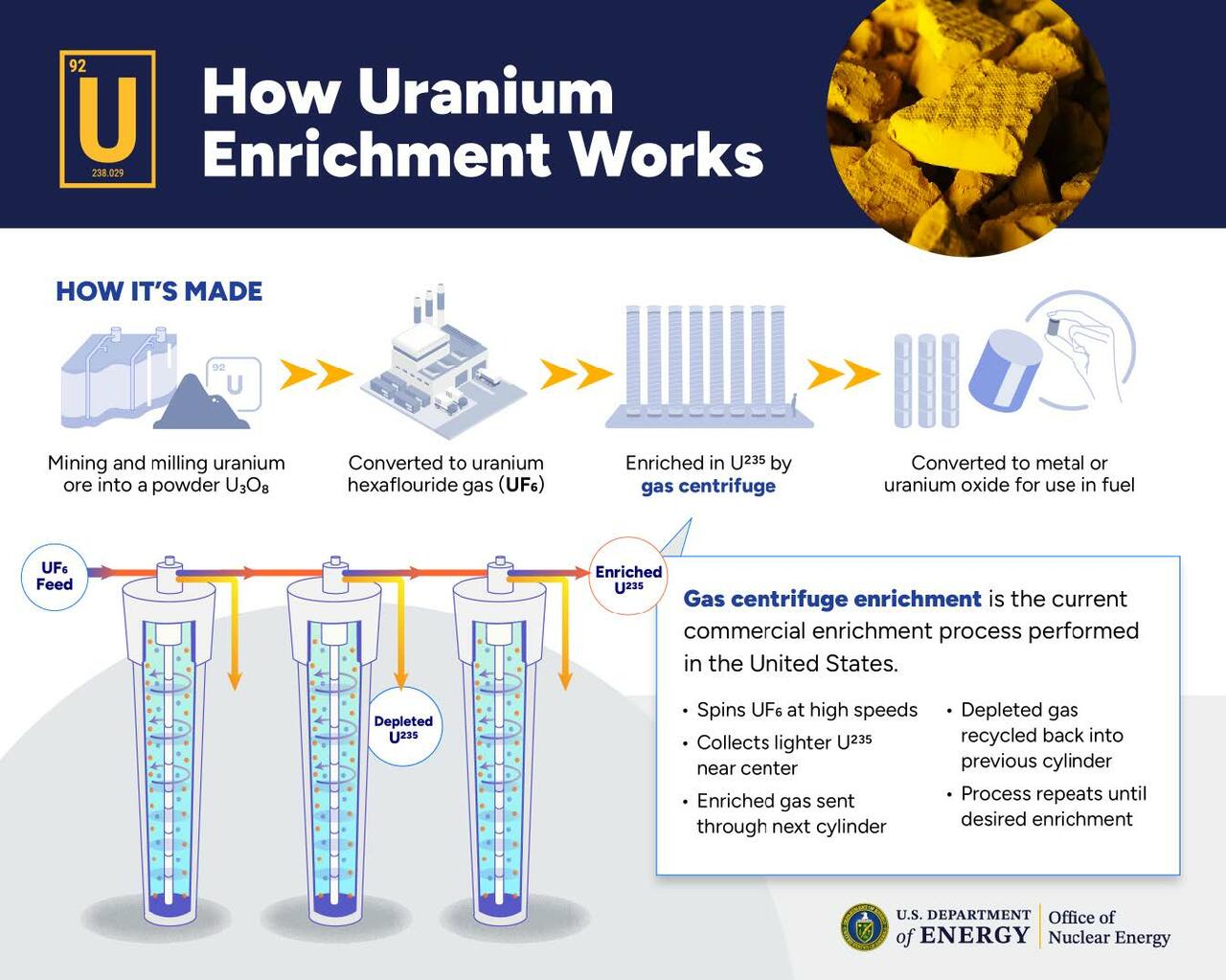

If next-generation atomic reactors eventually get built, they’ll need a new type of more potent fuel called high-assay low-enriched uranium, or HALEU, for which there’s just a single demonstration production line in the US that makes small volumes (it belongs to Centrus Energy, one of our favorite stocks).

“The core of the issue is insufficient capacity,” says Amir Vexler, the chief executive officer of enrichment company Centrus Energy Corp. “We need a lot of everything.”

However, efforts are under way to expand the nation’s nuclear supply chain, at all four stages of the fuel cycle.

First, several uranium miners, including Ur-Energy, are planning to boost US output. Next, when it comes to converting that uranium into gas, Solstice Advanced Materials – the only US conversion company – said last week it plans to increase capacity.

The third stage, enriching the gas, will get a boost from Centrus. It hired construction giant Fluor Corp. for a multibillion-dollar facility in Ohio, and was one of three companies that each received $900 million in January from the Department of Energy to expand US enrichment capacity.

The fourth and final stage in the chain, fuel fabrication, is also seeing progress. X-Energy Reactor, an advanced nuclear company backed by Amazon.com, received US approval for a new plant just last week.

It’s the first such license in more than five decades — another sign of how activity is picking up in the US nuclear sector, even if major new reactors remain years away.

Tyler Durden

Thu, 02/19/2026 – 08:20

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}