Category: News

OpenAI Lures Private-Equity Firms With 17.5% Guaranteed Returns As AI Rivals Race For Enterprise Deals

OpenAI Lures Private-Equity Firms With 17.5% Guaranteed Returns As AI Rivals Race For Enterprise Deals

OpenAI, the maker of ChatGPT, is offering private-equity firms a more generous financial package than rival Anthropic as the two artificial-intelligence companies court buyout shops to create joint ventures aimed at raising fresh capital and accelerating the rollout of enterprise AI products.

To lure PE firms, OpenAI is promising investors a guaranteed minimum return of 17.5%, a figure significantly above what is typical for preferred equity instruments, according to people familiar with the discussions who spoke with Reuters. The company is also providing early access to its latest AI models as it seeks commitments from firms including TPG Inc. and Advent International Corp., the people said. OpenAI has recently intensified its focus on corporate customers, an area where Anthropic has long held an edge.

Anthropic’s parallel effort offered no such guaranteed returns, the people said.

The timing of these overtures is notable. Just weeks ago, both companies became embroiled in a high-profile dispute with the Pentagon – with Anthropic walking away from a potential $200 million Defense Department contract after insisting on being the final arbiter over safeguards preventing its Claude AI from being used in fully autonomous weapons systems or mass surveillance of American citizens. The Pentagon responded by labeling Anthropic a “supply chain risk” – an unprecedented move against a U.S. technology company – blacklisting it from federal agencies and posing a risk to industry partners who also work with the Pentagon. President Trump directed all government entities to cease using Anthropic’s tools. The company has sued over this.

Hours after the deal fell apart on Feb 28, OpenAI announced its own agreement to supply AI tools for the Pentagon’s classified systems. The deal, initially criticized as opportunistic, triggered internal dissent at OpenAI, including the resignation of a senior robotics executive, and a consumer backlash that caused a surge in ChatGPT uninstalls among ‘I bought this Tesla before Elon went crazy’ types. OpenAI later amended the terms to strengthen guardrails.

And apparently there’s no such thing as bad news, as Anthropic’s stance earned it a surge in popularity: Its Claude app climbed to the top of U.S. download charts, with sign-ups hitting record levels.

The Race Is On

The joint ventures would enable both companies to rapidly deploy customized AI across hundreds of established companies owned by private-equity firms, creating deep integration that boosts customer retention at scale.

“There’s a big race to lock in as much enterprise, as many desks as possible,” said Matt Kropp at Boston Consulting Group’s AI unit. “Once a customized AI model is integrated into a company’s systems, switching becomes much harder.”

That said, some buyout firms have passed on the deals – citing concerns about economics, flexibility, and profit. Thoma Bravo LP opted out after internal reviews, with Managing Partner Orlando Bravo questioning the long-term profit profile, people familiar said.

Skeptics argue large PE firms already have direct access to the AI providers and question whether the ventures deliver enough incremental value. Others see pressure on buyout shops to showcase AI strategies to their own investors.

Still, discussions continue with several firms expected to take smaller stakes. OpenAI is in advanced talks to raise about $4 billion for its venture at a roughly $10 billion pre-money valuation, with participants including TBG, Bain Capital and Brookfield Asset Management. Anthropic has approached Blackstone, Hellman & Friedman and Permira for its enterprise-focused push.

Tyler Durden

Mon, 03/23/2026 – 11:25

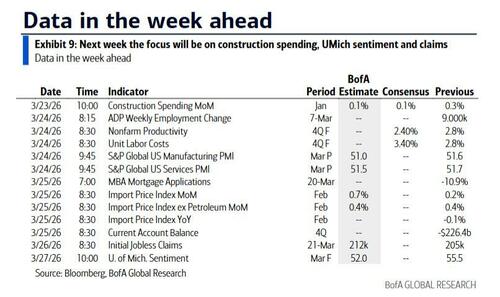

Key Events This Week: PMIs, Productivity And Consumer Sentiment

Key Events This Week: PMIs, Productivity And Consumer Sentiment

As has become customary for Monday, we have seen a dramatic surge in risk assets (3rd Monday in a row) on what at least superficially appears to be de-escalation after Trump announced strikes against Iran’s power plant would be delayed by 5 days as a result of talks with Iran, talks which at least Iran’s domestic news sources have so far denied.

And the market lurches from headline to headline, it feels somewhat trivial to focus on the week ahead data calendar, but there will nevertheless be interest in the global flash PMIs for March, due tomorrow. As DB’s Jim Reid notes, these surveys cover the period through roughly the end of last week and should therefore be heavily influenced by developments in the conflict. Elsewhere, inflation indicators are due in the UK, Japan and Australia, although these will now be quite backward looking. The German IFO survey on Wednesday may provide another timely read on sentiment, and Lagarde’s speech the same day will also be closely watched. The week concludes with the final March reading of the University of Michigan US consumer sentiment survey, which incorporates an additional couple of weeks of responses from the initial reading. DB’s economists expect a modest downward revision to 55.0 from the preliminary 55.5 as more respondents reflect heightened geopolitical uncertainty related to Iran. More important for policymakers, however, will be the inflation expectations components. Both one year and five to ten year expectations have historically tracked energy prices closely, making them particularly relevant in the current environment.

Overall the data calendar is light in the US, and even if it were busier it would likely pale in significance relative to events in the Middle East. On the policy front, scheduled Fed appearances are limited, with only three officials due to speak. The first comes from Vice Chair Jefferson, who is set to deliver an outlook speech on Thursday. He is likely to broadly echo the themes laid out by Chair Powell at the post meeting press conference, where Powell placed greater emphasis on inflation dynamics and the outlook than on potential labor market weakness, giving the discussion a distinctly hawkish tone. Inflation, rather than employment, clearly remains the Fed’s primary concern at this stage of the cycle.

Any divergence by Jefferson from Powell’s messaging would more likely be aimed at tempering expectations of imminent tightening rather than endorsing them, particularly given the sharp repricing from roughly 62bps of cuts before the strikes on Iran to around 7bps of hikes this morning (although that number has also reversed after this morning’s newsflow). The same logic applies to remarks expected on Friday from San Francisco Fed President Daly and Philadelphia Fed President Paulson, both of whom are non voters this year and are also scheduled to deliver outlook speeches. In markets where incoming data is increasingly backward looking, there is limited value in dwelling on the remainder of the week ahead calendar, which is set out day by day at the end as usual.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 23

Data: US February Chicago Fed national activity index, January construction spending, Japan first survey of shunto results, Eurozone March consumer confidence

Central banks: ECB’s Escriva and Lane speak

Other: UK PM Starmer faces the House of Commons’ Liaison committee

Tuesday March 24

Data: US, UK, Japan, Germany, France and the Eurozone flash March PMIs, US March Philadelphia Fed non-manufacturing activity, Richmond Fed manufacturing index, business conditions, Japan February national CPI, EU27 February new car registrations,

Central banks: ECB’s Kocher, Sleijpen, Cipollone and Lane speak

Auctions: US 2-yr Notes ($69bn)

Other: General election in Denmark

Wednesday March 25

Data: US February import price index, export price index, Q4 current account balance, UK February CPI, RPI, PPI, January house price index, Japan February PPI services, Germany March Ifo survey, Australia February CPI

Central banks: ECB’s Lagarde, Lane, Rehn and Kocher speak, BoE’s Greene speaks, BoJ minutes of the January meeting

Earnings: Jefferies, PDD Holdings

Auctions: US 2-yr FRN (reopening, $28bn), 5-yr Notes ($70bn)

Thursday March 26

Data: US March Kansas City Fed manufacturing activity, initial jobless claims, Germany April GfK consumer confidence, France March business confidence, consumer confidence, Italy March consumer confidence index, economic sentiment, manufacturing confidence, Eurozone February M3

Central banks: Norges Bank decision, Fed’s Jefferson speaks, ECB’s Guindos and Muller speak, BoE’s Breeden, Taylor and Greene speak, BoC’s Rogers speaks

Earnings: Meituan

Auctions: US 7-yr Notes ($44bn)

Other: G7 foreign ministers meeting (through Friday)

Friday March 27

Data: US March Kansas City Fed services activity, UK March GfK consumer confidence, February retail sales, China February industrial profits

Central banks: ECB consumer expectations survey, Fed’s Daly and Paulson speak

Earnings: Carnival, BYD

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the productivity and costs report on Tuesday and the University of Michigan report on Friday. There are several speaking engagements by Fed officials this week, including events with Governors Miran, Barr, and Cook, and Vice Chair Jefferson.

Monday, March 23

08:45 AM Fed Governor Miran speaks: Fed Governor Stephen Miran will appear on Bloomberg TV. On February 26, Miran said, “Four cuts [in 2026] I think are appropriate. I’d rather get them sooner than later.” Additionally, on March 6, Miran said, “Labor demand is not strong enough because monetary policy is too tight… I think the labor market could use some more support from monetary policy.”

10:00 AM Construction spending, January (GS +0.3%, consensus +0.1%, last +0.3%)

Tuesday, March 24

08:30 AM Nonfarm productivity, Q4 final (GS +1.7%, consensus +1.8%, last +2.8%); Unit labor costs, Q4 final (GS +4.3%, consensus +3.4%, last +2.8%): We estimate that nonfarm productivity growth will be revised down by 1.1pp to +1.7% quarterly annualized in the second release for 2025Q4. Since 2019Q4, labor productivity has grown at an annualized rate of 2.2%, or 2.0-2.1% after adjusting for measurement distortions in the productivity statistics, a much stronger pace than the 1.5% average pace in the pre-pandemic cycle.

09:45 AM S&P Global US manufacturing PMI, March preliminary (consensus 51.2, last 51.6): S&P Global US services PMI, March preliminary (consensus 52.0, last 51.7)

06:30 PM Fed Governor Barr speaks: Fed Governor Michael Barr will speak on the economic outlook and community development at the National Community Investment Conference in Phoenix. Speech text is expected. On February 17, Barr said, “Based on current conditions and the data in hand, it will likely be appropriate to hold rates steady for some time.” He also said, “With very low levels of job creation and also a low firing rate, there seems to be a tentative balance in labor supply and demand. But it is a delicate balance, and that means that the labor market could be especially vulnerable to negative shocks.”

Wednesday, March 25

08:30 AM Import price index, February (consensus +0.6%, last +0.2%); Export price index, February (consensus +0.6%, last +0.6%)

04:10 PM Fed Governor Miran speaks: Fed Governor Stephen Miran will participate in a conversation on digital assets at the 2026 Digital Asset Summit in New York.

Thursday, March 26

08:30 AM Initial jobless claims, week ended March 21 (GS 205k, consensus 210k, last 205k); Continuing jobless claims, week ended March 14 (consensus 1,853k, last 1,857k): We estimate that initial jobless claims were unchanged around 205k. Initial claims remain below their average level in 2025H2 and the layoff rate edged down in January, suggesting that nationwide layoffs remain low despite the increase in alternative layoff measures in Q4 of last year.

04:00 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will speak on financial stability at the Yale School of Management. Speech text and Q&A are expected. On February 4, Cook said, “[Recent] readings indicate that progress on inflation essentially stalled in 2025… After nearly five years of above-target inflation, it is essential that we maintain our credibility by returning to a disinflationary path and achieving our target in the relatively near future.” She also said, “The labor market is roughly in balance, but I am highly attentive to developments, knowing it can shift quickly.”

06:30 PM Fed Governor Miran speaks: Fed Governor Stephen Miran will speak on the Fed’s balance sheet at the Economic Club of Miami. Speech text and Q&A are expected.

07:00 PM Fed Vice Chair Jefferson speaks: Fed Vice Chair Philip Jefferson will speak at the Dallas Fed. On February 6, Jefferson said “I am cautiously optimistic about the economic outlook. I see signs suggesting that the labor market is stabilizing, that inflation can return to a path toward our 2% objective, and that sustainable economic growth will continue.”

07:10 PM Fed Governor Barr speaks: Fed Governor Michael Barr will participate in an event at the Brookings Institution. Speech text and Q&A are expected.

Friday, March 27

10:00 AM University of Michigan consumer sentiment, March final (GS 52.0, consensus 54.0, last 55.5): University of Michigan 5-10-year inflation expectations, March final (GS 3.5%, last 3.2%)

11:30 AM San Francisco Fed President Daly (FOMC non-voter) speaks: San Francisco Fed president Mary Daly will give introductory remarks at the San Francisco Fed’s Macroeconomics and Monetary Policy Conference. On March 6, Daly said, “We really have to keep our eye on the labor market. But we also have inflation printing above our target and oil prices rising. How long it will last we don’t know. But both our goals are at risk now and we have to keep our eye on both.”

11:40 AM Philadelphia Fed President Paulson (FOMC voter) speaks: Philadelphia Fed president Anna Paulson will give remarks at the San Francisco Fed’s Macroeconomics and Monetary Policy Conference.

Source: DB, Goldman

Tyler Durden

Mon, 03/23/2026 – 11:15

https://www.zerohedge.com/markets/key-events-week-pmis-productivity-and-consumer-sentiment

“The Numbers Are Shocking”: California Faces Scrutiny Over Hospice Fraud

“The Numbers Are Shocking”: California Faces Scrutiny Over Hospice Fraud

Authored by Tom Gantert via The Epoch Times,

Dr. Mehmet Oz, administrator of the Centers for Medicare and Medicaid Services, posted an Instagram video this week detailing ongoing fraud among hospice and health care facilities in Los Angeles County.

Investigations have focused on Los Angeles County, where officials said state regulators did little to stop fraud.

Investigators believe that the start of the hospice fraud can be traced as far back as 2010.

“The normalization of hospice fraud in California has to stop,” Oz said in his Instagram video while standing in front of one of the Los Angeles County homes that served as a hospice. “The numbers are shocking.”

Here’s what to know about the ongoing fraud scandal and how it is being addressed.

How Do Hospice Schemes Work?

Oz described in his video how the people running that particular hospice allegedly enrolled six individuals into their program.

The patients in the facility allegedly weren’t dying but were put on hospice so the owners of the business could charge Medicare for providing care. The owners also shared their patients’ information with other hospice centers that were in on the scam so they could get paid, Oz said.

Government investigations into Los Angeles County’s operations showed that some hospice agencies might be using stolen identities of medical personnel and that many of the so-called terminal patients were living well beyond expectations.

Investigators believe that the hospices are enrolling patients who are not suffering from terminal illnesses because the patients were found to have “unusually long” stays at the facilities, and high rates of patients were discharged alive.

The financial incentives for fraud are significant. A California state auditor report states that a hospice agency that bills for 20 patients at the going rate can make $122,000 per month.

In 2023, the Centers for Medicaid and Medicare Services estimated that improper payments in home health claims totaled $1.2 billion.

‘People Aren’t Paying Attention’

Investigators said the growth in Los Angeles County hospices began in 2010.

There were 109 hospice agencies in Los Angeles County serving 1 million elderly people in 2010. By 2021, there were 1,841 hospice agencies serving 1.4 million elderly people. From January 2019 to August 2021, the state received 2,600 applications for hospice agencies in Los Angeles County.

According to one government investigation, a single building with 22,500 square feet of space in the community of Van Nuys contained more than 150 licensed hospice and home health agencies—a number investigators believe exceeded the structure’s capacity. The building had no signage indicating that it was housing so many hospices.

Oz said Los Angeles County accounts for about one-third of all hospices in the United States. Of the 2,836 hospices in California, 1,841 were located in Los Angeles County, or nearly two out of every three hospices.

“That only happens because people aren’t paying attention,” Oz said in his Instagram video.

Lack of Oversight

In March 2022, the state auditor warned that the state’s “weak” oversight of the hospice and health care business has “created the opportunity for large-scale fraud and abuse.”

The Centers for Medicare and Medicaid Services directed the California Department of Public Health, the state agency responsible for licensing and oversight, to investigate the single Van Nuys building that was found to have 150 licensed hospice and home health agencies.

The Van Nuys hospice agency door was locked, and the office phone was not working when investigators showed up in January 2021, according to a state audit report. The California Department of Public Health had to contact the building’s landlord to get the owner’s contact information. The owner didn’t show up for scheduled meetings with Public Health for three days, and Public Health was unable to obtain any records. The owner was not able to answer questions regarding the agency, and when asked about her title, she told investigators, “We have not decided yet.”

The California Department of Public Health stated that it couldn’t substantiate any fraudulent activities and closed the investigation without taking any action.

The state auditor also discovered that Public Health became aware of possible fraud during the licensing process but still granted licenses to those hospice agencies. Public Health has not suspended a single hospice license since 2015 and revoked only one license, the auditor said.

Public Health was also taking five months to complete its investigations of patient abuse, which investigators considered “near the upper limit” of a hospice patient’s expected life span.

The auditor’s report states that Public Health agreed with most of the recommendations but stated that some might require legislation to be passed.

The California Department of Public Health didn’t respond to an email seeking comment from The Epoch Times.

Attempts at Reform

Politicians have attempted to address the fraud with legislation, litigation, and other actions.

California Gov. Gavin Newsom signed a law on Oct. 4, 2021, that stopped all new hospice licenses due to fraud concerns. The ban was extended through January 2027.

In November 2025, the Department of Justice reported that its fraud division had charged more than 5,800 defendants nationwide involved in health care fraud since 2007. Those 5,800 defendants billed federal health care programs and private insurers for more than $30 billion.

On Jan. 27, Newsom said the California Department of Public Health had revoked more than 280 hospice licenses in the past two years and had identified about 300 more hospices to be evaluated for potential revocation of their licenses.

Since 2021, the California Department of Justice has investigated 101 criminal enterprises and 284 criminal defendants and filed 24 civil cases. As of January, 109 individuals have been charged with hospice-related offenses.

At the federal level, Congress is looking into the issue. A March 17 hearing in the House addressed fraud in hospices across the country.

Rep. Linda Sanchez (D-Calif.) and Sen. Mark Warner (D-Va.) introduced a bill that aims to protect hospice patients and taxpayers from fraud.

At the state level, California Assemblywoman Alexandra Macedo, a Republican representing a rural San Joaquin Valley district, sent a letter on March 16 to the Subcommittee on Health criticizing the Newsom administration for not doing enough to stop the fraud.

Macedo said in the letter that she visited a dilapidated building in Van Nuys that had 197 hospice agencies registered to that address.

She said that Newsom’s administration has “failed to provide the aggressive oversight necessary to stop this hemorrhaging of public funds.”

“Despite a state audit and supposed moratorium on new licenses, these fraudulent hubs continue to operate in broad daylight,” Macedo said.

In January, Newsom said that the Trump administration has “dismantled the federal government’s ability to prevent and address fraud.”

“California didn’t wait—we’ve identified and cracked down on hospice fraud for years, taking real action to protect patients and taxpayers,” Newsom said in a statement.

The National Partnership for Healthcare and Hospice Innovation (NPHI) stated that it is involved with federal leaders to find solutions. The NPHI stated that the fraud issues are not “representative of the majority of hospice providers, who are focused every day on delivering high-quality, compassionate care to patients and families.”

“NPHI is actively working with the Administration and CMS to identify ways to target and root out bad actors,” said Tom Koutsoumpas, founder and CEO of NPHI. “We are encouraged to see decisive steps being taken to crack down on fraud and remove these bad actors from the hospice system, while safeguarding the integrity of hospice care for patients and families nationwide.”

Tyler Durden

Mon, 03/23/2026 – 11:05

“Far-Right” AfD Party Makes Historic Gains In German State Elections

“Far-Right” AfD Party Makes Historic Gains In German State Elections

Only a year ago, the AfD was the target of an orchestrated media smear campaign, not to mention leftist government attempts to ban the party from elections. The same tactics have been used to stifle conservative and nationalist movements across Europe, but these movements are proving to be resilient. The latest Le Pen success story in France’s small town areas runs in tandem with the latest news from Germany.

In the recent Rhineland-Palatinate state election, the Christian Democrats have, according to projections, won just over 30% of the vote and are well ahead of the leftist Social Democrats. However, the AfD is quickly catching up to the CDU, nearly doubling their seats in the same election with 20% of the voter share.

For reference, CDU is a mainstream center-right party that supports strong EU integration, social market economy, NATO alliances, and has governed for decades. AfD is a right-wing populist movement that demands the EU reform, near-zero immigration, and prioritizes German national sovereignty over international commitments.

🚨 BREAKING: Germany’s right-wing anti-Islamic migration party just SURGED in tonight’s West Germany state elections, making a SURPRISING +11 point gain

AfD has nearly DOUBLED its seats from just a few years ago

Take your country BACK from the 3rd world! pic.twitter.com/SgA4JtClTY

— Eric Daugherty (@EricLDaugh) March 22, 2026

The biggest gains went to the AfD, which, according to projections, comes in third. All three governing parties (SPD, Greens, and FDP) suffered significant losses. The CDU and Left Party’s enjoyed small gains of two to three percentage points. Meanwhile the AfD’s jump of more than eleven points is striking.

The AfD is clearly established as Germany’s second-strongest party at the national level with 152 seats total. These gains position the right-wing populists as a strong opposition force and Party leader Alice Weidel is already promising “excellent opposition work”. They are currently challenging the CDU to explain how they are going to tackle Germany’s mass immigration problem.

Germany is finally waking up, I just hope it’s in time

“They FLOOD our countries with illegals and force our own people to feed and house them, all while terrorism stalks our streets, crime explodes, and Islamic extremism takes root!”pic.twitter.com/tIAuxnkSpc

— Kevin Sorbo (@ksorbs) March 22, 2026

As noted above, Christian Democrats are considered “conservative“, and the party continuously claims it wants secure borders and deportations. However, the CDU refuses to work with the AfD; CDU candidate Gordon Schnieder argues that the party would not join forces with the far-right.

“It would spell the downfall of this country if we were to bring the AfD on board here,” he said. This is known as the “coalition firewall”.

The refusal to work with the AfD means that Germany’s immigration struggles are likely to continue. Leftist parties, despite losing significant ground, are still in a position to prevent any meaningful policy changes on borders and deportations. Some critics argue that the CDU is a “fake front” and not truly interested in taking on the progressive multiculturalists.

The AfD’s best strategy is to make themselves a thorn in the side of the status quo parliamentary process until the CDU is willing to cooperate, or, the next elections in September give the AfD an even greater share of seats.

The biggest loser in the recent elections has been the Social Democrats (SPD). Following their debacle in the Baden-Württemberg state elections two weeks ago, the party has suffered another sharp loss in Rhineland-Palatinate, dropping around nine percentage points.

The Social Democrats, who have governed for 35 years under incumbent state premier Alexander Schweitzer, are the primary culprits behind the surge of third-world immigrants and Islamic immigrants into Germany. By extension, Germany’s massive welfare structure gave migrants a lucrative reason to travel to the country, where they fed on the system and then spread to neighboring EU member states.

The immigration problem is consistently listed among the top three issues worrying German citizens in recent polling. At bottom, the political landscape is changing rapidly and the leftists could soon be relegated to the dustbin if they continue to impede common sense immigration reforms.

It is obvious that the progressive agenda has long been to saturate their respective nations with migrants and use these people as a voting block to secure power for decades to come. But, this plan has been exposed and opposition has grown far faster than they intended. There is no way to bypass or stop nationalist movements, now.

Tyler Durden

Mon, 03/23/2026 – 10:45

Supreme Court To Decide If Federal Ballots Received After Election Day Are Counted

Supreme Court To Decide If Federal Ballots Received After Election Day Are Counted

Authored by Matthew Vadum via The Epoch Times,

The U.S. Supreme Court on March 23 will hear Mississippi’s appeal against a lower court ruling striking down its law counting ballots received after Election Day.

The counting of ballots received after Election Day has become an increasingly contentious political issue in recent years.

Those who support the practice say it is necessary to maximize participation in the democratic process and that states should be able to craft ballot rules to accommodate voters’ needs. Those who oppose it say that allowing ballots to be accepted after Election Day invites fraud and erodes trust in the system.

The Mississippi law allows the state to count mail-in ballots that officials receive within a five-day grace period after Election Day. The law was enacted in July 2020 during the COVID-19 pandemic to provide flexibility to voters.

Eighteen states accept mailed ballots received after Election Day if they bear a postmark made on or before Election Day, according to a National Conference of State Legislatures report.

Mississippi argues that striking down its law will cause upheaval in those states that allow ballots received after Election Day to be counted.

The Republican National Committee (RNC), the state’s Republican Party, and the state’s Libertarian Party sued over the state law, arguing that the federal election-day statute preempts—or prevails over—the state law.

Three federal statutes—U.S. Code Sections 7 and 1 of Title 2, and Section 1 of Title 3—set the Tuesday after the first Monday in November in certain years as the Election Day for federal offices. A presidential election takes place every four years; a congressional election occurs every two years.

President Donald Trump signed Executive Order 14248 on March 25, 2025, stating that his administration would enforce those statutes and “require that votes be cast and received by the election date established in law.”

Several states continue to count ballots received after Election Day, Trump said, likening the practice to letting individuals who show up three days after Election Day, possibly after a winner has already been declared, vote in person at a voting precinct.

A federal district court in Washington state blocked part of the executive order in January.

The respondents, including the RNC, challenged the state law, saying that federal laws both establish a uniform election day for federal elections and require that ballots must be received by that day.

Mississippi argues that its law allowing late receipt of ballots does not conflict with the federal election day law and that states are allowed to regulate aspects of federal elections that take place within their borders.

U.S. District Judge Louis Guirola Jr. upheld the Mississippi law in July 2024, finding that the Mississippi statute “operates consistently with and does not conflict with the Electors Clause [of the U.S. Constitution] or the election-day statutes.”

“In the absence of federal law regulating absentee mail-in ballot procedures, states retain the authority and the constitutional charge to establish their lawful time, place, and manner boundaries,” the district court stated.

The state appealed, and in October 2024, the U.S. Court of Appeals for the Fifth Circuit reversed.

The Elections Clause in the Constitution allows states to determine the time, place, and manner of federal elections, but also allows Congress to “make or alter such Regulations,” the appeals court ruled.

Many states had been in the habit of having two separate days for federal elections, so in 1872, Congress decided that all elections for the U.S. House of Representatives should take place on the presidential election day. In that situation, Congress had authority to act, the appeals court said.

Late Receipt Erodes Confidence

Christian Adams, president of the Public Interest Legal Foundation, suggested that the case was straightforward, and that it turns on statutory interpretation and “nothing else.”

“The question is whether the federal statute requires ballots in by Election Day,” he told The Epoch Times.

In his group’s brief, the foundation argues that the federal law preempts the state law. The federal statute established a uniform Election Day for federal offices to promote “finality, public confidence, and administrable election rules,” and allowing states to extend the receipt of ballots beyond Election Day has the effect of “prolonging federal elections after voting has concluded.”

Michael J. O’Neill, vice president for legal affairs at the Landmark Legal Foundation, said federal law established a single, nationwide Election Day, and that “an election cannot extend beyond that date without undermining both statutory meaning and electoral integrity.”

Allowing mail-ballots received after Election Day creates “uneven election practices and erodes public confidence,” O’Neill told The Epoch Times.

“It also invites uncertainty, delays finality, and conflicts with Congress’s intent to prevent precisely such rolling or prolonged elections,” he added.

Tom Fitton, president of Judicial Watch, said in recent years there has been a “contagion” going through the states in which they are “gutting the very notion of Election Day and allowing votes to arrive and be counted days and weeks after an election.”

Judicial Watch represents the Libertarian Party of Mississippi, a co-respondent in the case.

“Your mailbox isn’t a ballot box,” Fitton told The Epoch Times. “The idea that you drop your ballot in the mail and it gets there whenever, and it gets counted—that’s not the way it’s supposed to work.”

Potential for Upheaval

Lisa Dixon, executive director of the Center for Election Confidence, said she hopes the Supreme Court will decide that the federal election-day statute prevails over the Mississippi law.

When ballots continue to be received for up to two weeks after Election Day, and the public sees vote totals changing “sometimes even weeks” after Election Day, that erodes public confidence in the election results, she said.

The court should decide the case quickly to give states time to educate their voters and update their written materials “so voters have time to adjust,” Dixon told The Epoch Times.

“We don’t want anyone to be disenfranchised because the deadline has changed,” she said.

The Center previously filed a friend-of-the-court brief urging the high court to take up the case.

Adams indicated he wasn’t overly concerned about the potential for temporary administrative upheaval in the several states that allow receipt of ballots after Election Day if the Supreme Court strikes down the Mississippi statute.

“The law is more important than North Dakota being offended,” he said, referencing a lawsuit his foundation brought against that state for counting ballots received after Election Day.

None of the sources interviewed for this article offered a prediction on how the Supreme Court might rule.

“Predictions are too difficult, especially regarding matters of statutory interpretation,” Adams said. “Coin toss at best.”

Tyler Durden

Mon, 03/23/2026 – 10:20

Nearing Psychological Gas Price Level Where Consumers Drive Less

Nearing Psychological Gas Price Level Where Consumers Drive Less

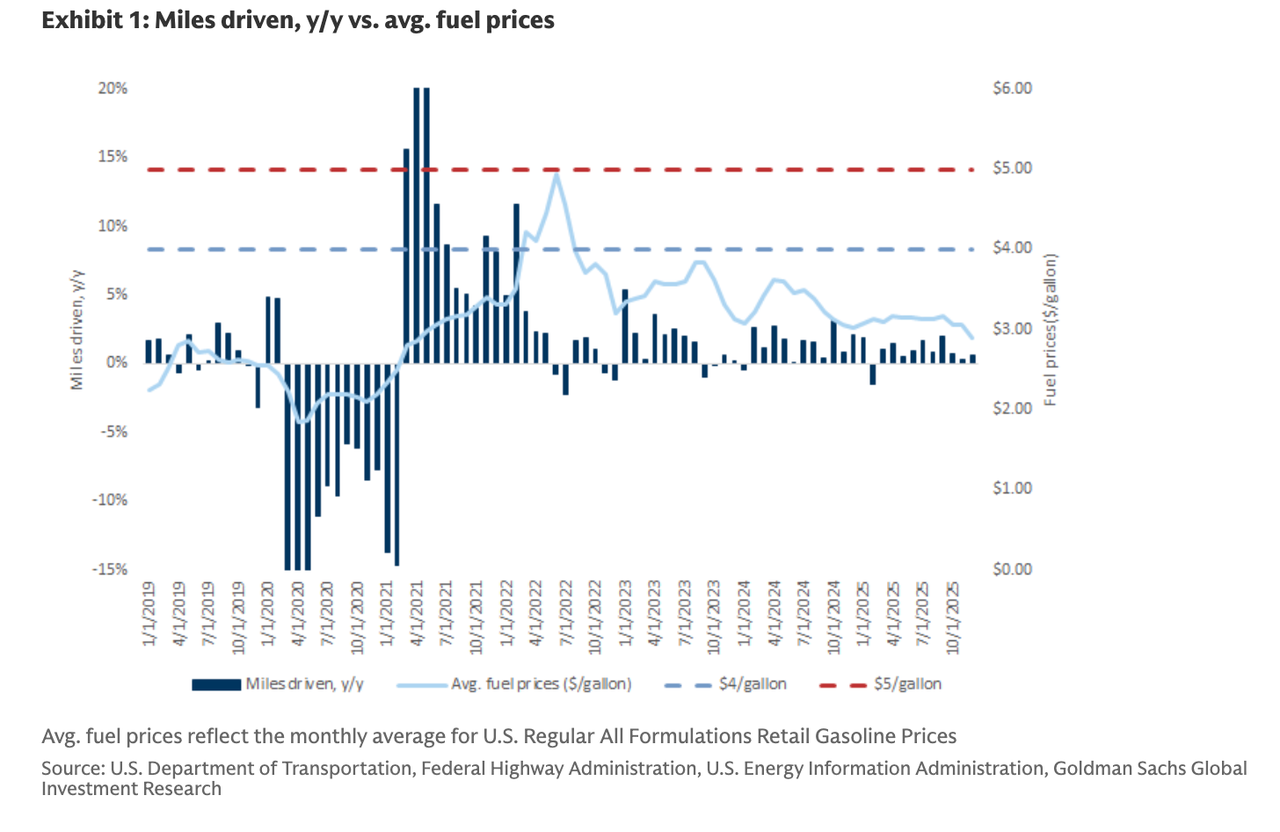

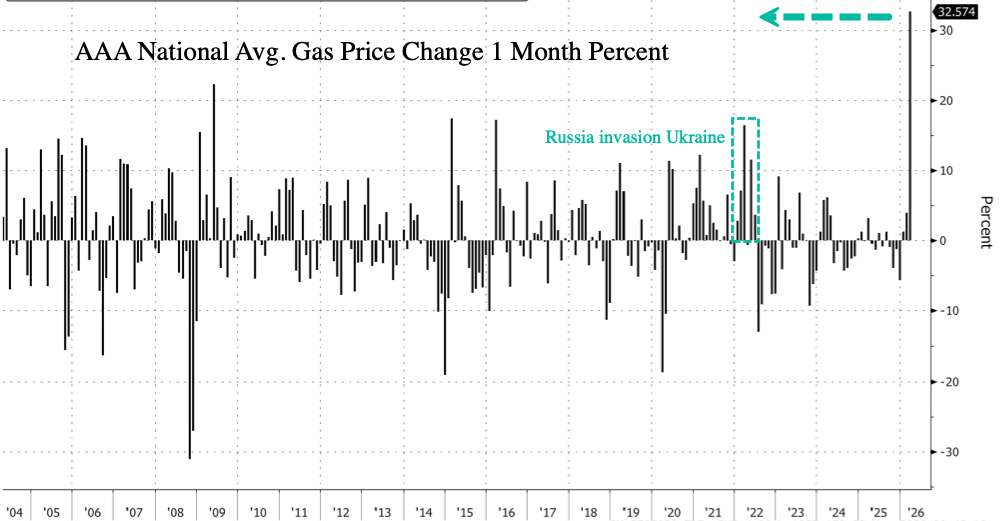

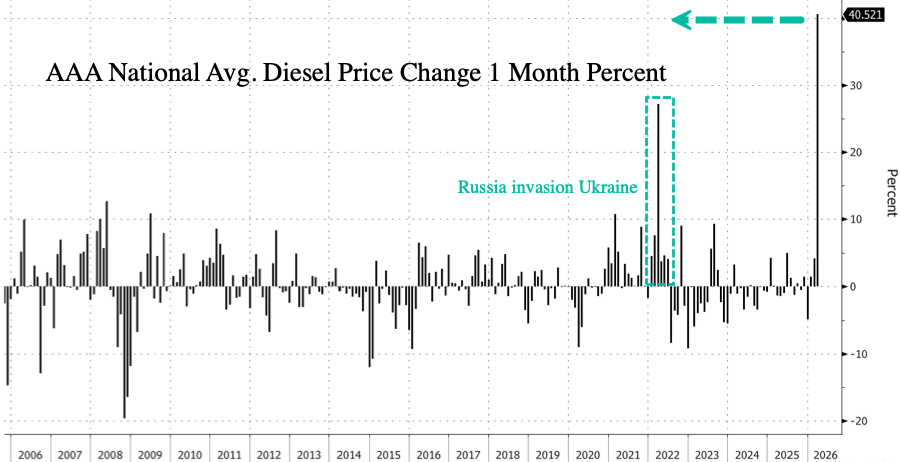

The latest AAA data show the national average price for regular gasoline at the pump is now just four cents below the politically sensitive $4-a-gallon mark. This month’s surge in retail fuel prices (gasoline and diesel) marks the largest increase on record and is delivering a nasty shock to the pocketbooks of cash-strapped consumers.

Bonnie Herzog, managing director and senior consumer analyst at Goldman Sachs, wrote in a note that when fuel prices spike to these “psychological threshold” levels, above $3 and approaching $4 a gallon, consumers tend to drive less and fill up their tanks less frequently.

“Historically, when retail gas prices increase (especially above the $3/gal psychological threshold, although that’s been rebased higher), consumers make the concerted decision to drive less, don’t always fill up their tanks (i.e., lower fill rates),” Herzog told clients on Friday.

But Herzog pointed back to history, noting that the real demand destruction for drivers comes when gasoline prices at the pump reach $ 5 a gallon.

She noted, “Further, we recognize that, in times of a significantly rising fuel-price environment, consumers may opt to trade down the fuel-price spectrum (i.e., from premium to regular).”

The vertical move in gasoline and diesel this month, according to AAA data, is record-setting. Gas prices at the pump have jumped nearly 33% on the month, far outpacing the Russia-Ukraine invasion in 2022 or the Iraq war, with data dating back to 2005. The shock here will certainly leave some cash-strapped drivers dialing back miles on the road.

Diesel spike! Small businesses are warning of shock (read here).

Herzog offered a warning that elevated “retail prices at the pump matter” because “low-income households spend 3x more of their incomes on gas vs. the average household, and broadly speaking, c-stores over-index to low-income consumers.”

Let’s not forget that pressure on pocketbooks from a fuel-pump shock may weigh on consumer sentiment if the spike proves not to be temporary. However, Trump headlines Monday morning may suggest the administration is finding an offramp to the conflict.

Professional subscribers can read much more from Herzog’s team here at our new Marketdesk.ai portal

Tyler Durden

Mon, 03/23/2026 – 10:00

https://www.zerohedge.com/energy/nearing-psychological-gas-price-level-where-consumers-drive-less

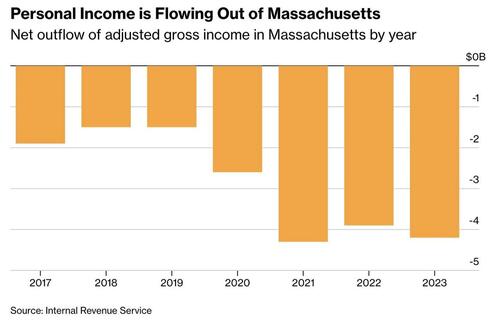

Mamdani’s Tax Fantasy Is Already Failing Somewhere Else

Mamdani’s Tax Fantasy Is Already Failing Somewhere Else

Submitted by QTR’s Fringe Finance

Last week I wrote that Zohran Mamdani is a f***ing moron has proposed a new estate tax that is not really aimed at billionaires but at ordinary New Yorkers whose so called wealth is largely tied up in the homes they spent decades paying off.

That argument may have sounded abstract to some readers, like a warning about unintended consequences that might or might not materialize. But we do not have to speculate about how these kinds of burdensome taxation policies play out. Other than the Laffer Curve, which exists for a reason and has existed for 50 years now, we have another real world example, and it is happening in a state that shares many of New York’s political instincts and fiscal habits.

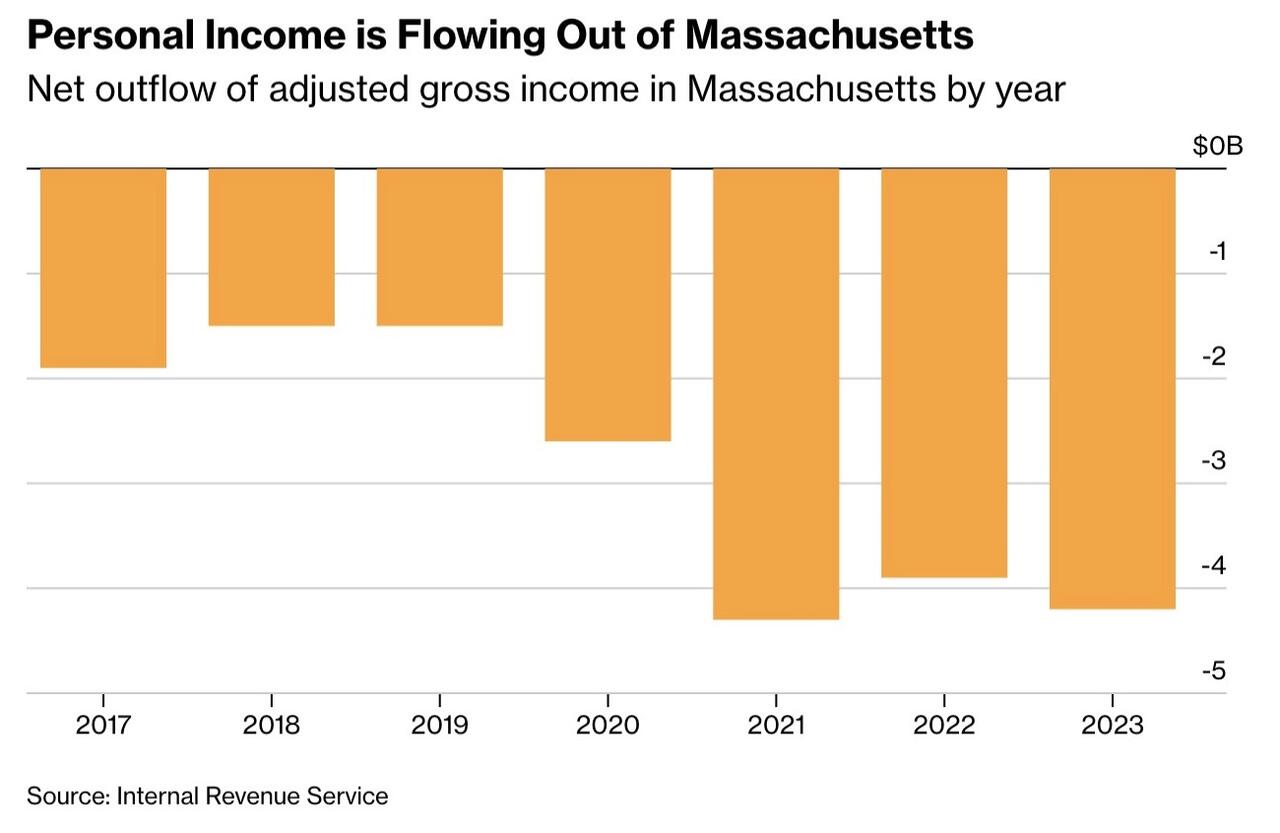

Massachusetts recently implemented a new 4% surtax on income above one million dollars after voters approved the measure in 2022. Supporters framed it as a targeted, reasonable way to raise revenue from top earners in order to fund public priorities like education and transportation. In theory, it was precisely the kind of policy that politicians like Mamdani claim will generate large sums of money without broader economic consequences.

But, of course, the early data tells a more complicated and far less comforting story.

In 2023, the first year the surtax took effect, Massachusetts experienced a net outflow of $4.2 billion in adjusted gross income. That number increased eight percent from the prior year. This was not driven by a sudden collapse in population or some unrelated shock. It reflects a steady and measurable movement of income and the people who earn it out of the state. Even more telling is that this shift occurred despite the fact that overall migration patterns did not dramatically worsen. In other words, fewer people may have left, but those who did leave took significantly more income with them.

Chart: Bloomberg

This is the dynamic that advocates of higher taxes on so called targeted groups consistently ignore. Taxes change behavior, particularly among people with the greatest flexibility to respond.

High earners, business owners, and investors do not passively absorb higher tax burdens if they have realistic alternatives. They look for jurisdictions that treat them more favorably, and in the United States those alternatives are abundant. States like Florida and New Hampshire offer dramatically lower tax burdens and have become magnets for precisely the kind of taxpayers that high tax states increasingly depend on.

Supporters of the Massachusetts surtax will point out that it has generated billions in new revenue, and that claim is accurate as far as it goes. What it leaves out is the longer term erosion of the tax base that can accompany those gains. When billions of dollars in income leave a state, that loss compounds over time through reduced investment, fewer business formations, and lower future tax collections. The short term revenue boost can obscure a slower but more consequential decline underneath.

Now consider what Mamdani is proposing in New York. His plan rests on the same magical thinking that drove the Massachusetts surtax, namely that the government can squeeze significantly more revenue out of a conveniently defined group without that group noticing or doing anything about it. This is a comforting theory if you spend most of your time in policy seminars and very little time observing how actual humans behave.

In the real world, people respond to incentives, especially when those incentives involve large sums of money and the option to simply leave. New York, of course, is already one of the most heavily taxed places in the country and has been bleeding residents to lower tax states for years. Piling on a dramatically more aggressive estate tax is not bold policy innovation. It is doubling down on a problem everyone can already see.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

What makes Mamdani’s proposal even more impressive, and by that I mean in the worst possible way, is how wide a net it casts while still pretending to target only the rich. Massachusetts at least aimed its surtax at income above one million dollars, which, while debatable policy, is at least rhetorically consistent. Mamdani wants to drop the estate tax threshold to $750,000, which in New York City is less a marker of wealth than a marker of having bought a house at some point in the last thirty years and not lost it. A modest home in Queens or Brooklyn plus a retirement account is enough to trip that wire. Apparently, in this framework, a retired city worker with a paid off house now qualifies as landed gentry. The rhetoric says oligarchs. The math says your parents.

The behavioral response here does not require a PhD in tax law to understand, which is perhaps why it gets so little attention from the people proposing it. Avoiding an estate tax is not like restructuring a business or navigating some obscure loophole. In many cases, it is as simple as changing your address. That is not a hypothetical. Retirees already move to states with lower taxes all the time. Mamdani’s plan just gives them one more very concrete reason to do it, preferably before the state gets a final look at their life savings. It turns out that when the choice is between leaving New York or handing over a large chunk of what you planned to pass on to your children, a nontrivial number of people will start browsing real estate in Florida.

The predictable result is then treated as some kind of mystery. Instead of a stable and growing stream of revenue extracted from the rich, you get a slow but steady erosion of the tax base as wealth, income, and taxpayers relocate to friendlier jurisdictions. That loss does not show up all at once, which makes it easy for policymakers to ignore in the short term while they celebrate the initial revenue bump. Over time, though, the math stops cooperating, and the response is almost always the same. If the rich are not paying enough, the definition of rich quietly expands until it includes whoever is still around.

New York does not need a crystal ball to see how this plays out. The preview is already running in places like Massachusetts. Ignoring it is not bold or visionary. It is just willful blindness. And if Mamdani’s proposal moves forward, the ending will not be surprising. It will be the same story New York has been telling for years, only faster, louder, and far more expensive for the people who do not have the option to leave.

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Mon, 03/23/2026 – 09:40

https://www.zerohedge.com/markets/mamdanis-tax-fantasy-already-failing-somewhere-else

Iran Phones Russia Immediately On Heels Of Trump’s Announcement Of US-Iran Talks

Iran Phones Russia Immediately On Heels Of Trump’s Announcement Of US-Iran Talks

Iranian Foreign Minister Abbas Araghchi held talks with Sergei Lavrov quickly on the heels of President Trump early Monday having claimed Washington and Tehran had “very good and productive conversations regarding a complete and total resolution of our hostilities” – as the war is in its fourth week.

Moscow appears to be moving to position itself as a broker, with Russia’s foreign ministry announcing that FM Lavrov called for an “immediate cessation of hostilities and a political settlement that takes into account the legitimate interests of all parties involved, above all Iran,” in a call initiated by Tehran.

The Kremlin followed this by its spokesman Dmitry Peskov stating negotiations should have begun “yesterday” – adding that “this is the only way to effectively ease the catastrophically tense situation in the region.”

Trump had on Saturday unveiled a time-specific ultimatum which threatened to “obliterate” Iranian power plants if Tehran refuses to reopen the Strait of Hormuz. The clock is ticking on the 48-hour timeline, and it’s unclear how the Trump-touted Tehran-Washington contacts will impact that (contacts which Tehran has denied).

As for the Kremlin, Peskov also warned against strikes on nuclear infrastructure following reported attacks on Natanz nuclear facility, stating: “We believe that strikes on nuclear facilities are potentially extremely dangerous … Therefore, the Russian side, taking an extremely responsible stance on this issue, has repeatedly voiced its concerns.”

The risk is no longer theoretical given that Russia’s state nuclear firm Rosatom and the International Atomic Energy Agency had confirmed a projectile strike on the Bushehr Nuclear Power Plant, marking a dangerous new phase where nuclear sites are no longer off limits.

This in turn resulted in Iran for the first time targeting Dimona, home to Israel’s major nuclear reactor and research complex. But there’s no indication it suffered any direct hits.

“Dimona, where the second missile hit, is perilously close to Israel’s main nuclear reactor and research site. Iranian state media said the strike targeted the nuclear facility in retaliation for an attack on an Iranian nuclear enrichment site at Natanz, though the IDF has said it was unaware of that operation,” NBC reports.

“The International Atomic Energy Agency said that no abnormal off-site radiation levels had been observed following the strikes, though it urged all sides to exercise restraint near nuclear sites,” the report added.

At this point it’s anything but clear whether Trump’s announcement of talks will lead to an actual slowdown or pause in fighting. Here’s how Russia’s RT framed Iran’s stance:

Iranian sources, however, have told state media that no negotiations have been held with Washington, even through intermediaries. The Iranian Embassy in Afghanistan has stated that Trump “backed down” after Iran’s “firm warning” that it would retaliate to strikes on its energy infrastructure by attacking power plants across the region.

On Sunday US Treasury Secretary Scott Bessent told “Meet the Press” that Washington must “escalate to de-escalate” in the Iran and Strait of Hormuz situation. However, Washington never seems to be able get to the “de-escalate” part.

Tyler Durden

Mon, 03/23/2026 – 09:00

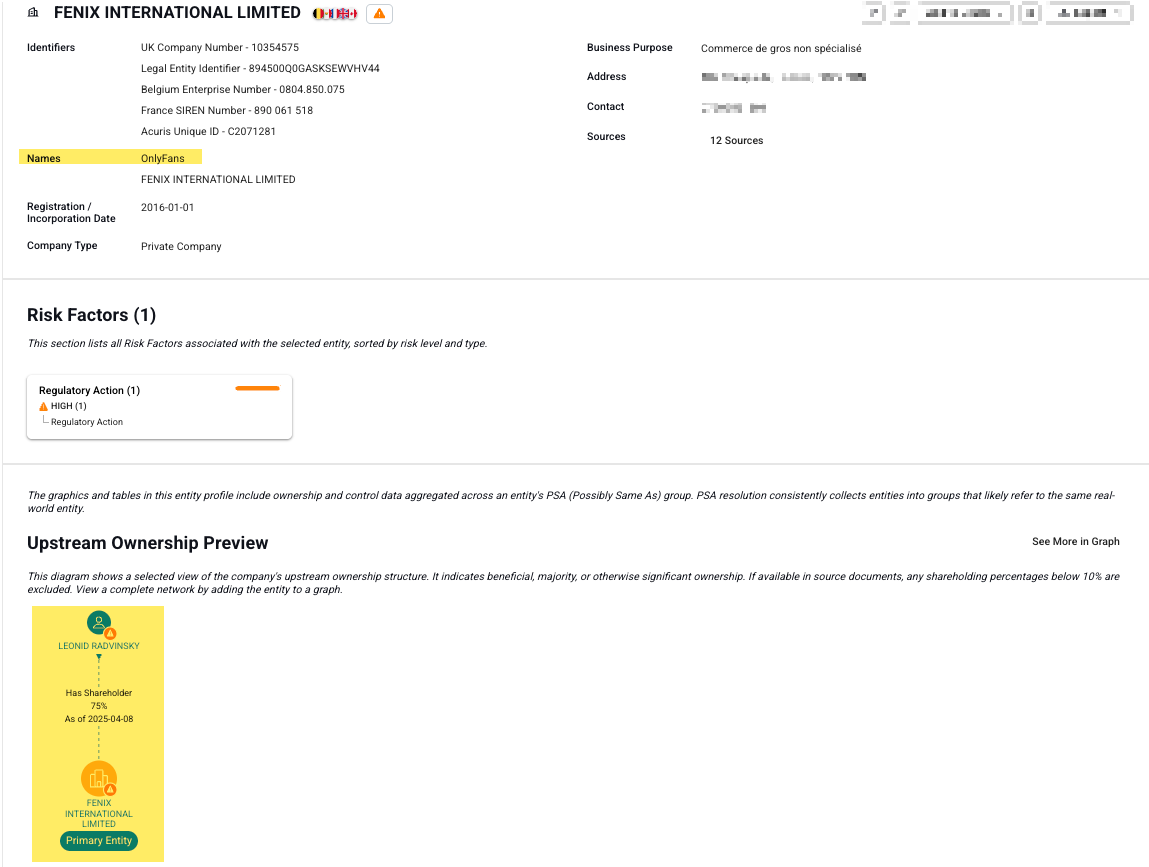

“We Are Deeply Saddened”: OnlyFans Owner Leonid Radvinsky Dead At 43

“We Are Deeply Saddened”: OnlyFans Owner Leonid Radvinsky Dead At 43

The billionaire owner of adult content platform OnlyFans has died after a long battle with cancer, according to Bloomberg, citing a statement from the company.

Leonid Radvinsky died at the age of 43, according to the company, which added, “We are deeply saddened to announce the death of Leo Radvinsky. He passed away peacefully after a long battle with cancer.”

Radvinsky’s death raises new questions about the platform’s future ownership, especially since he reportedly placed his majority stake in a trust in 2024.

According to his website, Radvinsky donated to several charities, including Memorial Sloan Kettering Cancer Center, West Suburban Humane Society, and EB Research Partnership.

Radvinsky studied economics at Northwestern University and by 2018 had bought a majority stake in OnlyFans and helped transform the video content platform into an adult-content subscription business’ powerhouse that reshaped how women monetize their bodies.

OnlyFans was founded in 2016 and exploded in popularity during the Covid pandemic. Some of the latest data from 2024 showed the website had 4.6 million creators, 377 million fans, and $1.4 billion in revenue.

In a separate report by platform search engine OnlyGuid, Americans spent an estimated $2.6 billion on OnlyFans in 2025.

A little less than one year ago, OnlyFans’ parent company, Fenix International Ltd., was reportedly in talks to sell the video platform at an estimated $8 billion valuation.

None of these talks resulted in a completed sale, at least publicly confirmed.

Tyler Durden

Mon, 03/23/2026 – 08:40

https://www.zerohedge.com/technology/we-are-deeply-saddened-onlyfans-owner-leonid-radvinsky-dead-43

IEA Head Warns Iran War Sparked Energy Crisis Worse Than 1970s Oil Shocks, Ukraine Fallout

IEA Head Warns Iran War Sparked Energy Crisis Worse Than 1970s Oil Shocks, Ukraine Fallout

The head of the International Energy Agency intensified his apocalyptic warning about the global energy crisis, stating early Monday that the US-Israel war with Iran has sparked a shock far greater than the twin oil crises of the 1970s and the turmoil from the war in Ukraine combined.

US-Israeli Operation Epic Fury has entered its fourth week, and emerging from the fog of war is the understanding that 44 energy assets across the Gulf region have been severely or very severely damaged by either U.S. and allied forces or by Iranian forces, according to IEA Executive Director Fatih Birol, who spoke at a media event in Australia on Monday.

“This crisis, as things stand, is now two oil crises and one gas crash put all together,” Birol warned at the National Press Club of Australia in Canberra.

So far, the conflict has removed 11 million barrels of oil per day from global supply, which is more than the two prior oil shocks combined.

There are concerns that repairs to QatarEnergy’s damaged LNG facility could take up to five years, while the disruption to energy flows has sparked a fuel crisis across Asia and is set to affect fertilizer and food supplies, as well as helium, potentially jeopardizing AI chip production.

“The global economy is facing a major, major threat today, and I very much hope that this issue will be resolved as soon as possible,” Birol said.

As of 0710 ET, Brent crude futures plunged 11% on President Trump’s Truth Social desesclation comments – a sign the administration needs an offramp to avoid a further energy crisis globally, but more importantly, one at home with fuel prices at the pump exploding higher.

Overnight, President Trump gave Iran a 48-hour ultimatum to reopen the Hormuz chokepoint or face a bombing campaign targeting Iran’s power plants.

There were reports overnight that the Trump administration was preparing a diplomatic off-ramp plan, but Iran says the expanding war has effectively shut the door.

Betting website Polymarket shows that ten new wallets are betting $160,000 on a U.S.-Iran ceasefire by the end of March.

“Almost no history, all created around the same time. Potential payout: over $1,000,000,” the Polymarket History account wrote on X.

🚨 NEW SUSPICIOUS WALLETS

10 fresh wallets just loaded over $160,000

on a ceasefire by end of March

Almost no history

all created around the same time

Potential payout: over $1,000,000 https://t.co/QvC48Md5iD pic.twitter.com/XzwBBLyBXz

— PolymarketHistory (@PolymarketStory) March 22, 2026

On Friday, Birol told the Financial Times in an exclusive interview that the world is severely underestimating the scale of the Gulf energy shock and that it may take at least six months to restore disrupted oil and gas flows.

Related:

Morgan Stanley Explains How Central Banks Are Reacting To The Historic Energy Shock

“Tactically More Defensive”: Top Goldman Trader Muses On Macro, Markets, & The Middle East

“It will be six months for some [sites] to be operational, others much longer,” Birol warned.

Tyler Durden

Mon, 03/23/2026 – 08:25

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}