Category: News

“Awful News”: Nintendo Shares Get ‘Donkey Konged’ After Switch 2 Production Cut

“Awful News”: Nintendo Shares Get ‘Donkey Konged’ After Switch 2 Production Cut

Nintendo shares in Tokyo tumbled overnight after Bloomberg reported that the gaming company has slashed production of the Switch 2 handheld amid soft holiday-season demand and underwhelming U.S. sales.

*NINTENDO CUTS SWITCH 2 OUTPUT BY OVER 30% ON WEAK HOLIDAY SALES

wait, wasn’t this thing supposed to be as popular as chatgpt?

— zerohedge (@zerohedge) March 24, 2026

Nintendo is expected to produce 4 million Switch 2 units instead of the originally planned 6 million, with the lower production rate expected to continue into the second quarter.

Despite a record June 2025 launch and 17.37 million units sold since release, management appears disappointed that momentum and hype for the Switch 2 have faded. Japan has held up better than overseas markets, helped by a cheaper domestic-only variant, while U.S. demand has been soft.

“This hardware shortfall in its first year, during its big holiday season, is awful news,” Asymmetric Advisors analyst Amir Anvarzadeh wrote in a note.

Sources noted that the output reduction should not affect Nintendo’s ability to meet the average Wall Street analyst estimate of about 20 million Switch 2 units sold in the fiscal year through this month.

A soft U.S. market is yet another concern for Nintendo, as soaring memory chip costs squeeze margins and may force a price hike that could further crimp consumer demand.

Related:

Nintendo Profit Misses As Soaring Memory Prices Could Become Major Headache

The lack of a robust software pipeline has failed to energize consumers.

Anvarzadeh said, “Clearly, the software lineup has been poor, at least until most recently, with Pokémon showing some hope.“

The market reaction in Tokyo was negative following the BBG report, with shares closing down nearly 5%. For the year, shares are down 15.2% and nearly 39% from the peak in late summer 2025.

The big takeaway is that Nintendo is not facing a launch failure, but it is struggling to sustain excitement around the device – perhaps because of software issues and the lack of a robust gaming pipeline. Wait to see what happens to demand if Nintendo is forced into a price-hiking cycle because of the memory crunch.

Tyler Durden

Tue, 03/24/2026 – 09:40

Art Of The Dream

Art Of The Dream

By Bas van Geffen, Senior Macro Strategist at Rabobank

Trump’s 48-hour deadline turned into a weeklong one. Yesterday, the US president announced that he has “instructed the department of War to postpone any and all military strikes against Iranian power plants and energy infrastructure for a five day period.”

President Trump says he delayed the actions following “very good and productive conversations” with Iran, which he expects to continue throughout the week. However, reports about these talks are inconsistent at best. Iranian media reported that no such talks have taken place, to which Trump responded that he is not sure what they are talking about, adding that talks happened last night. Other media say that there has been some contact via backchannels or via third parties, but add that actual talks have not happened.

Was it all a dream? Or is the US president simply unwilling to follow through on his threats? Iran called Trump’s bluff, threatening to retaliate against energy infrastructure and desalination plants in neighbouring countries. US allies may have convinced Trump that this would create a much bigger crisis in the region. So, perhaps Trump is just buying time for an alternative form of escalation. The new deadline coincides with the expected arrival of US marines in the region.

*US MARINES SLATED TO ARRIVE IN MIDEAST FRIDAY: WSJ

just as Trump’s 5-day extension expires

— zerohedge (@zerohedge) March 23, 2026

Either way, Trump’s change of tone boosted risk sentiment and supported equity portfolios, particularly of those who just so happened to place large orders ahead of the presidential social media post. But markets may be dreaming too.

Further escalation has been averted for now, but don’t forget that Iran does not need to escalate. Iran continues to have full control over the Strait of Hormuz. As long as the regime is willing and able to execute pinpointed strikes, sailing through will be a prohibitively dangerous endeavour. And, the longer even an impasse lasts, the bigger the damage to energy supply chains and economies.

Moreover, while Trump is now talking about de-escalating the scenario and a potential peaceful resolution, Iran continues missile strikes on Israel – and Israel presses ahead with its military campaign. And several members of the Gulf Cooperation Council signaled willingness to join the fight against Iran. Closure of the Strait of Hormuz is impacting their energy exports, so the GCC nations may see a role for themselves to ensure that the Strait is reopened. But, more importantly, Iran’s retaliatory strikes against targets in neighbouring countries –and threats of more– may have struck a nerve.

As a result, some of the optimism waned this morning already. Energy prices are rebounding from yesterday’s lows, and equity traders are once again taking a more cautious stance than they did after Trump’s social media post yesterday.

Speaking of the economic damage caused, Eurozone consumer confidence took a significant hit in March, falling back to -16.3 from -12.3 in February. With the previous energy crisis still fresh in memory, that is no surprise. Faltering confidence has yet to affect actual consumer spending, but this does raise the risk that the war’s impact on economic activity in Europe could be visible relatively quickly.

Amidst the geopolitical risks, the EU continues to seek diversification of its economic alliances. Brussels signed a free trade agreement with Australia, following on the deals with Mercosur, India, and Indonesia. Parliament still has to approve the deal, but this should be less contested than the Mercosur agreement.

The EU-Australia deal includes a combination of tariff cuts and higher quotas for certain dairy products, beef and sheep meat. Geographical product names are protected by the deal, to the displeasure of Australian farmers, who believe that access to the European market remains impeded.

Trade Commissioner Sefcovic said that the deal should increase annual bilateral trade by about €20 billion over the next decade, but that’s arguably not the EU’s main motivation. A security and defense partnership underscores the geopolitical motive, and improved access to Australia’s critical raw materials may be an extension of this.

* * *

Tyler Durden

Tue, 03/24/2026 – 09:22

Iranian Missiles Pound Israel Overnight After US Claims Progress On Talks; Tehran Appoints Larijani Successor, Cuts Gas Flows To Turkey

Iranian Missiles Pound Israel Overnight After US Claims Progress On Talks; Tehran Appoints Larijani Successor, Cuts Gas Flows To Turkey

Summary

Backchannel diplomacy vs skepticism: Abbas Araghchi reportedly signaled openness to negotiations with the US via envoy Steve Witkoff, but Israel has appeared cool on deal prospects or offramp.

Heavy exchange of fire and testing red lines: Iran continues missile and drone waves targeting Israel and US bases, amid reports of overnight airstrikes on military and gas infrastructure near Isfahan.

Iran reshuffles its security leadership, appointing Mohammad Bagher Zolghadr: he’s a former IRGC commander and replaces the assassinated Ali Larijani.

Iran halts natural gas exports to Turkey: follows last week’s Israeli strike on the massive South Pars gas field.

* * *

Iran & Israel Trade Blows Despite US Promoting Backchannel Talks

Despite the White House touting backchannel interactions with the Iranians as basis for some kind of peaceful offramp, Israel and Iran intensified direct and regional strikes, in continued escalation of the war. The Israeli military said it had “completed a wave of extensive strikes targeting production sites” across Iran, including in Isfahan, following overnight reports that gas facilities were hit, triggering fears of potential Iranian retaliation on Gulf energy and infrastructure sites – which doesn’t appear to have happened yet.

Iran has kept up its attacks on Israel, launching at least eight overnight missile waves, including reports of cluster munitions as well as new cutting-edge warheads and projectiles. Impacts were reported across Tel Aviv, causing heavy building damage and multiple casualties, as well as with sirens sounding from the Judean Foothills to Eilat. One strike marked a shift in capability, per the NY Times: “One of the Iranian missiles that hit Tel Aviv carried a warhead of around 100 kilograms… This missile was ‘something we have not yet encountered in the war,'” said Col. Miki David.

A 100-kg warhead was used on the Iranian missile that slammed into Tel Aviv early this morning. Significant damage was caused to a residential area. pic.twitter.com/ujkuJpxUVO

— Trey Yingst (@TreyYingst) March 24, 2026

Iran Halts NatGas Exports to Turkey

More energy flows impact and blowback as Iran has halted natural gas exports to Turkey following last week’s Israeli strike on the massive South Pars gas field, according to regional sources and Bloomberg. Turkey sourced roughly 14% of its gas from Iran last year, per industry data, but continues to rely on Russia and Azerbaijan as primary suppliers while drawing on existing reserves. Ankara has not initially confirmed or commented.

The South Pars field, part of the world’s largest natural gas reserve, sits at the core of Iran’s energy system, underpinning both domestic supply and export flows. Per Middle East Eye: “Data from Turkey’s Energy Market Regulatory Authority suggests that the country imports around 13 percent of its gas needs annually, roughly 7 billion cubic metres (bcm), from Iran.”

The report concludes that “A sharp drop in Iranian gas flows to Turkey following Israel’s strike on the South Pars gas field and Tehran’s retaliatory attacks across the Gulf has raised energy security concerns. But analysts say Ankara will likely be able to cushion the blow.

⚡️Sky above Tel Aviv pic.twitter.com/skgWXTOWZ4

— War Monitor (@WarMonitors) March 24, 2026

New National Security Chief (former IRGC), Ongoing Retaliation on Gulf

Iran has continued to signal resilience, downplaying threats to its grid and stating damaged infrastructure could be quickly rebuilt, even as a gas pipeline at Khorramshahr was hit apparently without disruption. Saudi Arabia said it “intercepted and destroyed” more than a dozen drones in its east, while the UAE reported intercepting five ballistic missiles and 17 drones in a single day, bringing totals since the war began to hundreds of missiles and more than 1,800 drones. Bahrain said another facility was set ablaze “as a result of Iranian aggression.”

Tehran has reportedly simultaneously struck US bases, and Gulf states including Kuwait and Saudi Arabia, while warning any attack on its energy network will trigger region-wide blackouts. Northern Iraq has continued to see drone threats. “The entire region will go dark” – Iranian leadership has threatened. Meanwhile, Iran has reshuffled its security leadership, appointing Mohammad Bagher Zolghadr to replace the assassinated Ali Larijani, underscoring wartime consolidation at the top. Zolghadr is a former Revolutionary Guards commander.

Mohammad Bagher Zolghadr in 2013, via Wiki Commons

Status of Diplomacy

Lebanon has declared the Iranian ambassador persona non grata and ordered him to leave the country by Sunday, after an Iranian ballistic missile fell on Lebanese territory. This appears also a way to pressure Hezbollah, given the Lebanese state has long wanted the Tehran-linked group to lay down is arms so war doesn’t engulf the whole country.

Both Pakistan and Qatar have stepped up mediation efforts, with chatter that Islamabad could play host to future Iranian and US talks. Despite the rumors of ongoing backchannel communications, and President Trump himself insisting Sunday into Monday this is happening, there’s as yet no clear evidence that Tehran and Washington are actually dialoguing. Pakistan’s Foreign Ministry has told Al Jazeera that Islamabad is ready to host talks between the US and Iran: “If the parties desire, Islamabad is always willing to host talks,” Foreign Ministry spokesman Tahir Andrabi said. Andrabi’s comment came a day after Trump put on hold, for a period five days, his threat to bomb Iranian power plants.

WSJ meanwhile writes, “Foreign ministers from Egypt, Turkey, Saudi Arabia and Pakistan gathered before dawn Thursday in Riyadh for talks aimed at finding a diplomatic off-ramp to the war in Iran.” The report continues, “But there was one big problem, according to Arab officials involved in the discussions: finding a counterpart in Iran to negotiate with. Earlier that week, Israel killed Iran’s national security chief, Ali Larijani, who had been considered a viable partner who could engage with the West.”

USAF B-52s began to carry out Iran strike missions yesterday using 2,000 pound JDAM guided bombs.

Indicates that the BUFFs are finally carrying out bombing runs over Iran. pic.twitter.com/tzcJQc6LLp

— OSINTtechnical (@Osinttechnical) March 23, 2026

And Bloomberg’s assessment: “Fighting between the US-Israeli alliance and Iran raged unabated, even as President Donald Trump claimed talks are under way to end the conflict.” The report then notes no observable cooling or offramp in the tit-for-tat exchanges of fire:

Iran carried out overnight missile and drone attacks on the Israeli cities of Tel Aviv, Eilat and Dimona, as well as on US bases in the Middle East. Israel launched a wave of strikes in western and central Iran, including Tehran, with Defense Minister Israel Katz saying the campaign would continue “at full intensity.”

Israel is Cool on Prospect of a Deal

Reports out of regional and Israeli media claim Iranian Foreign Minister Abbas Araghchi quietly signaled to US envoy Steve Witkoff that Supreme Leader Mojtaba Khamenei has agreed to negotiations, while Iranian officials said they have received US proposals via intermediaries and are reviewing them. However, Tehran keeps threatening and delivering more ‘retaliatory’ action, perceiving that it has the long-term strategic leverage given the Strait of Hormuz crisis and Trump seeming to issue forth dictates on a back foot.

Israeli officials have by and large dismissed the prospects of a deal, warning the chances of agreement are “very small” and stressing that US force deployments and joint operational planning remain unchanged.

More Regional Spillover: Caspian & Lebanon

The Kremlin has newly warned that any expansion into the Caspian Sea would be viewed “extremely negatively” after Israeli strikes reportedly targeted Iranian naval assets there. Meanwhile, a parallel ground war in Lebanon is accelerating. Israeli Defense Minister Israel Katz signaled a long-term buffer zone and mass displacement, stating, “Hundreds of thousands… will not return south of the Litani River until security is guaranteed.”

Video purports to show large Israeli strike on Southern Lebanon overnight – an apparent hit on a gas station:

⚡️Israeli strike on Southern Lebanon tonight. Strike on Gas Station pic.twitter.com/5r0teCUZ6n

— War Monitor (@WarMonitors) March 24, 2026

Israel has already destroyed key infrastructure, with Katz confirming, “All five bridges over the Litani… have been blown up,” as forces move to control the area. There are over 1,000 dead and more than a million displaced in Lebanon, with much of Israel’s north also still under emergency evacuation orders, given Hezbollah rocket fire there. At least two Lebanese died in the last day due to Israeli strikes Bshamoun.

Tyler Durden

Tue, 03/24/2026 – 09:00

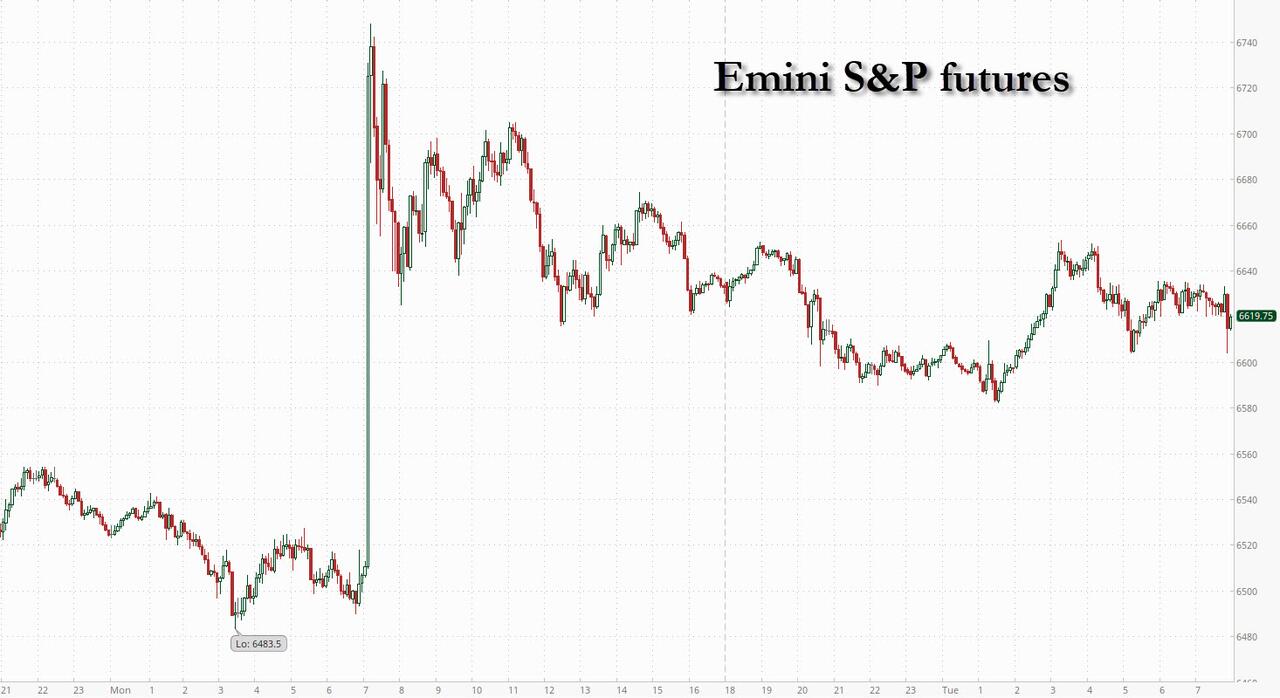

Futures Drop As Oil, Yields Rise On Relentless War Headline Ping-Pong

Futures Drop As Oil, Yields Rise On Relentless War Headline Ping-Pong

Futures are lower but well off session lows, as overnight headlines induced another bout of aggressive choppiness: those headlines include strikes on Iranian gas facilities, Saudi and UAE considering entering the war, Iranian lawmaker ruling out US negotiations, and then reports of Iran / Egypt discussions on the region pointing toward mediation.As of 8:00am ET, S&P futures were down 0.2%, but moves are staggered jittery and extremely illiquid, and swung earlier between gains and losses. Nasdaq futures are down 0.1% with Mag7 mostly lower, Energy is higher with the balance of Cyclicals flat to Defensives. Treasuries dipped, with the two-year yield climbing two basis points to 3.88%, giving back most of yesterday’s moves; The dollar gained 0.2% while gold edged 0.3% higher. In commodities, Energy leads and precious metals have caught a bid despite the stronger USD. Oil rebound partially from Monday’s slump, with Brent crude back above $100 a barrel. Today’s macro data focus is on weekly ADP, regional Fed activity indicators, and Flash PMIs which may give us an early look at the impact of the Middle East conflict.

In premarket trading, Mag 7 stocks are mixed (Nvidia +0.2%, Microsoft +0.1%, Apple -0.1%, Meta -0.1%, Tesla -0.2%, Amazon -0.2%, Alphabet -0.3%)

Applied Optoelectronics Inc. (AAOI) gains 2.4% after the electronics component manufacturer said it has received a new volume order from one of its major hyperscale customers for 800G single-mode data center transceivers to help expand its network capacity for AI-driven workloads.

Jefferies Financial Group Inc. (JEF) is up 7.6% after the Financial Times reported that Sumitomo Mitsui Financial Group Inc. is working on plans for a potential takeover of the bank.

JFrog (FROG) is up 3.6% after UBS upgraded the software firm to buy from neutral following recent stock weakness, with the analyst noting that there are no signs of a slowdown.

Netgear (NTGR) gains 11% after the US Federal Communications Commission ordered a ban on the import of new models of foreign-produced consumer wireless routers.

In corporate news, Japan’s SMFG is working on plans for a possible takeover of Jefferies, according to the Financial Times. In Europe, Estée Lauder is in talks to buy Puig Brands in a deal that would create a cosmetics giant. The Korea Economic Daily reported that SK Hynix is said to be seeking to raise $10 billion from a potential listing in the US. And Nintendo is cutting back production of the Switch 2 after demand trailed expectations.

Traders continue to juggle headlines around the US-Israeli war against Iran after Trump signaled a possible end to hostilities on Monday following what he described as productive talks. The positive sentiment from those comments faded after Iran denied substantive discussions, while the Wall Street Journal reported that Saudi Arabia and the UAE have taken steps toward joining US efforts in the war against Tehran. Meanwhile, Iran launched overnight missile and drone attacks on the Israeli cities of Eilat, Dimona and Tel Aviv, as well as US bases in the Middle East. Saudi Arabia said it intercepted a drone in its eastern region, and Kuwait said some power lines were put out of service after an Iranian attack. Sirens sounded in Bahrain. Pakistan is said to be making a push to mediate talks to end the hostilities.

In Iran, the Fars news agency reported US-Israeli attacks that damaged a gas pressure-regulation plant and an administrative building in the central city of Isfahan. There was also a strike on a pipeline supplying gas to the Khorramshahr Combined Cycle Power Plant in southwestern Iran, according to Fars.

“It’s a very tricky situation,” said Arnaud Girod, head of cross-asset strategy at Kepler Cheuvreux. “If there’s a deal in five days then there’s a chance the market can bounce back and investors may be able to look through the crisis but if there’s not, a recession is a possibility. The range of outcomes is very large still, which explains the volatility.”

Renewed tensions risk keeping oil prices elevated, potentially stoking inflation and reinforcing expectations that policymakers may delay easing or even tighten monetary policy. Investors are concerned the war will have lasting effects on economic growth and prices, even if hostilities end soon.

“Yes, markets can rebound if talks succeed but even in that case we’re expecting volatility to remain,” said Claudia Panseri, chief investment officer at UBS Wealth Management, who is “as defensive as possible” in Europe and cutting exposure to cyclical stocks like banks. “Oil reserves must be replenished, supply bottlenecks tackled, so things will not go back to where they were prior to the strikes. That means that there would still be an impact on growth and inflation.”

Markets remain on “hyper alert” for the next development, said Anna Wu, a cross asset strategist at Van Eck Associates Corp. “Most investors are still waiting for some sort of talk to be confirmed between Iran and the US for clarity,” she said.

Private credit headlines are adding to the nervousness in markets. A fund jointly run by Future Standard and KKR was cut to junk by Moody’s Ratings, while Apollo capped redemptions from one of its largest non-traded private credit funds for retail investors, after clients sought to redeem 11.2%. Ares gated investors shortly after too. Michael Dell’s family office see the tumult in private-credit markets turning into a buying opportunity.

In politics, Markwayne Mullin was confirmed Department of Homeland Security secretary, placing the Oklahoma senator in charge of a Trump administration immigration crackdown that has triggered a 37-day funding shutdown of the cabinet agency.

For markets, it’s difficult to know what to do. “There are no reliable havens right now; even the dollar, typically the biggest beneficiary of a flight to safety, has made only modest gains compared with the world’s major currencies,” writes Bloomberg Opinion’s Marcus Ashworth. Goldman strategists, meanwhile, recommend allocations to real assets such as TIPS and infrastructure stocks to mitigate stagflation risks.

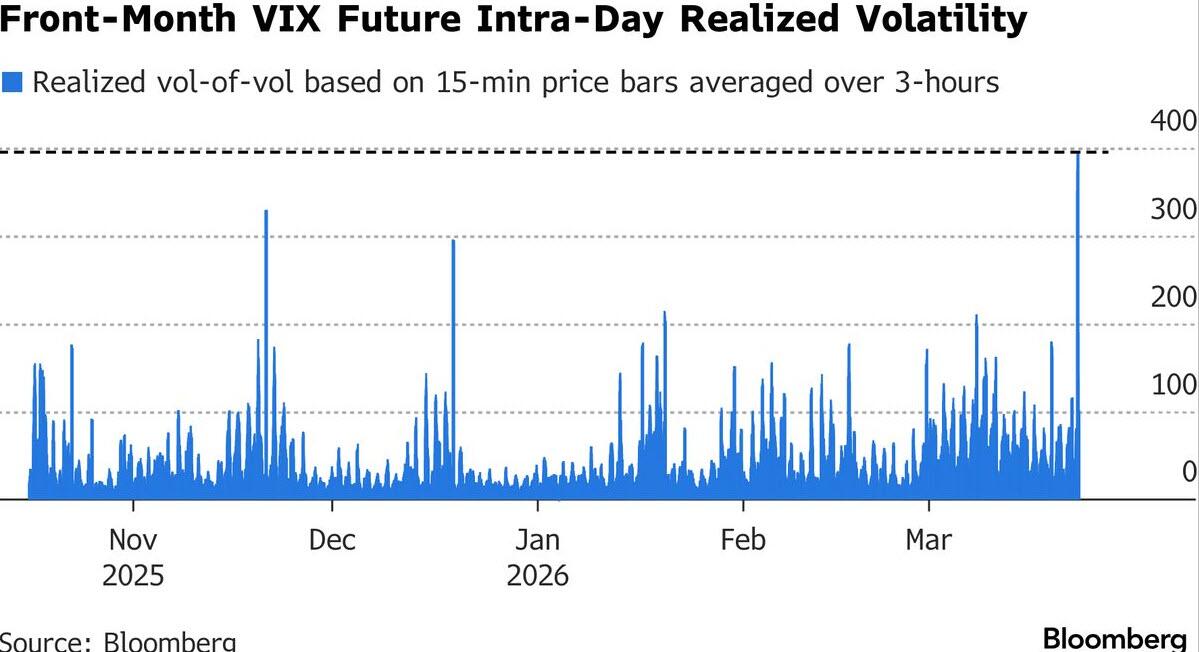

Hedging is increasingly expensive, raising the question of whether there is even any point in buying protection, with moves playing out within minutes instead of weeks.

The latest Options Snapshot looks at realized vol-of-vol soaring on Monday and the VIX term structure flip-flopping in and out of inversion, reflective of unstable short-term implied volatility. Some spreads have reached quite extreme levels, including the MSCI Emerging Markets ETF/State Street SPDR S&P 500 ETF ratio.

US PMI data for March is due this morning, after numbers in France and Germany signaled corporate profits are already being squeezed by the war. Houston’s showpiece energy conference, CERAWeek by S&P Global, kicked off on Monday, bringing together top executives in the sector. “We’ve never been in such a crisis, which has so many repercussions long term,” said Carlyle’s chairman of energy, Marcel van Poecke.

European futures marked lower during APAC hours before staging a recovery with the Eurostoxx 50 contracts now basically unchnaged with energy and health care stocks the biggest gainers, while mining and bankiing shares are the worst-performing sectors. Here are the biggest movers Tuesday:

Puig shares rise as much as 17%, their largest-ever intraday gain, after Estée Lauder said the companies were discussing a deal that would create a cosmetics giant with about $20 billion in annual sales

Straumann shares rise as much as 5.6%, the biggest gainers in the Stoxx 600 Health Care Index on Tuesday, after a sell-side meeting with CFO Isabelle Wege reassured analysts

INWIT shares rose as much as 5.3% after Il Sole 24 Ore reported Ardian is exploring strategic options for its stake, including a potential joint bid with Brookfield Asset Management to take full control of the Italian tower group

Tecan shares gain as much as 8%, the most since Jan. 9, after a regulatory disclosure showed SEO Management held a 3.4% stake on March 16

SAP shares slip as much as 5.1% after JPMorgan downgraded the software maker to neutral from overweight on a view that margin expansion will decelerate due to a business model transition as the AI cycle unfolds

Exor shares fall as much as 7.7%, hitting the lowest level since September 2022, after the Agnellis’ investment company reported net assets for the full year that missed the average analyst estimate

Exail Technologies shares drop as much as 9.7% after one of the investors in the French company offloaded shares at a discount to Monday’s closing price

Bytes Technology shares slide as much as 16% to their lowest intraday level on record after the information technology company said it expects 2027 full-year operating profit to be broadly flat

Skan drops as much as 16% after reporting its full-year results, with UBS saying the health care supplier’s 2026 targets are below expectations

YouGov falls as much as 17% as the research company’s first-half adjusted Ebit misses expectations, with JPMorgan saying this is attributable to sizable investments in both Shopper and AI-enabled products

Earlier in the session, Asian stocks rose, recovering some losses of the previous session, as US comments about discussions with Iran sparked fresh optimism, although market watchers cautioned against over-exuberance. The MSCI Asia Pacific Index rose as much as 2.2%, halting a three-day rout. Advances in Hong Kong, Japanese, Indian and South Korean equity markets led gains in the region, while Malaysia fell. The technology sector, which is closely tied to risk sentiment in the region, rose to support the broader Asian index higher. Indonesia remains shut. Meantime in Japan, a key inflation gauge slowed more than expected to its weakest pace in nearly four years. Japan consumer prices excluding fresh food climbed 1.6% from a year earlier in February, the smallest gain since March 2022.

“It is quite likely that this week we see a relief rally given the market was oversold, but this might be a final solution. The situation is still very fluid,” said Suresh Tantia, head CIO of Asia equity strategy at UBS Global Wealth Management, in a Bloomberg TV interview.

In FX, the Bloomberg Dollar index is higher by 0.2%. The euro and pound saw little follow-through from flash PMI metrics which saw misses on composite readings for the UK and Eurozone – manufacturing prints beat, services missed.

In rates, treasuries hold small losses as US trading begins, with futures just off session lows. US yields are higher by 3bp to 4bp across the curve, keeping curve spreads within a basis point of Monday’s close; 20-year sector underperforms, widening 10s20s30s fly by almost 2bp on the day. US 10-year near 4.37% is cheaper by 2.5bp with UK and German counterparts richer by less than 1bp; UK 2- and 5-year yields outperform, trading richer by 1bp-2bp. European bonds outperform led by gilts after UK March Services PMI missed estimate. This week’s Treasury auction cycle begins at 1pm in New York with $69 billion 2-year note sale; $70 billion 5-year and $44 billion 7-year follow on Wednesday and Thursday. WI 2-year yield near 3.892% is ~44bp cheaper than last month’s, which tailed by 0.1bp

In commodities, brent crude has pulled back a touch in recent trading but remains higher by 0.6% and holding above the $100/bbl level. Prices had been underpinned by an Iranian lawmaker reportedly ruling out negotiations with US President Trump and a Wall Street Journal report that Saudi Arabia and UAE have taken steps toward joining the war. Spot gold is attempting to recover recent losses, up 0.5% versus a 1.5% gain for silver. Bitcoin is up 0.4%.

Today’s US economic data scheduled includes weekly ADP employment change (8:15am), March Philadelphia Fed non-manufacturing activity, 4Q unit labor costs (8:30am), S&P Global US March manufacturing and services PMIs (9:45am) and Richmond Fed manufacturing index (10am). Fed speaker slate includes Barr speaking on the economic outlook at 6:30pm. Core & Main and Dollarama are among companies due to report results before the market open. Dollarama’s Canadian total sales for fiscal 4Q could rise 7%, BI’s scenario analysis suggests, as value-seeking behavior continues to drive traffic. Earnings from GameStop and KB Home follow later.

Market Snapshot

S&P 500 mini -0.3%

Nasdaq 100 mini -0.3%

Russell 2000 mini -0.4%

Stoxx Europe 600 -0.5%

DAX -1%

CAC 40 -0.6%

10-year Treasury yield +3 basis points at 4.37%

VIX +1 points at 27.1

Bloomberg Dollar Index +0.3% at 1209.28

euro -0.3% at $1.1582

WTI crude +3.4% at $91.09/barrel

Top Overnight News

Iran publicly denied that any direct negotiations were occurring, and US officials said the contacts were at a “very early stage and not substantive.” NYT

Fighting between Iran and the US-Israeli alliance continued with Iran launching overnight missile and drone attacks on Israeli cities and US bases in the Middle East. Trump claimed talks are under way to end the conflict, but Iranian officials denied his claims of behind-the-scenes diplomacy, causing confusion over the participants in the talks and the parameters of a potential deal. BBG

Oil rebounded as Iran launched overnight attacks on several targets, including in Bahrain and Kuwait, while Israel said its Iran strikes are continuing at full intensity. Kuwait said some power lines were put out of service after Iranian attacks. Saudi Arabia and the UAE have taken steps toward joining the war. BBG, WSJ

The Trump administration is quietly weighing Iran’s parliament speaker as a potential partner — and even a future leader — as the president signals a shift from military pressure toward a negotiated endgame. Mohammad Bagher Ghalibaf is seen by at least some in the White House as a workable partner. Politico

Oil companies and the world’s largest energy consumers face a significant challenge to rebuild global petroleum supply chains and inventories once the critical Strait of Hormuz bottleneck opens, Chevron CEO Mike Wirth said Monday. Wirth cautioned that Iran’s attacks on oil tankers and the broader damage of the Middle East war did greater damage to oil and gas markets than the Russia-Ukraine war. Politico

Chinese banks are experiencing system failures due to surging volumes in gold investment products as investors buy on dips, according to China Securities Journal. BBG

Japan’s core inflation rose 1.6% from a year earlier in February, below the BOJ’s target for the first time since 2022. BBG

The ECB must be “very agile and vigilant” to keep prices in check as the Iran war brings stagflation risks closer, said incoming ECB vice president Boris Vujcic. BBG

A fund run by Future Standard and KKR was cut to junk by Moody’s, a rare occurrence in the $1.8 trillion market. Apollo capped withdrawals from one of its largest non-traded funds for retail investors. BBG

US GOP senators see a path to ending the Department of Homeland Security shutdown after a Trump meeting on Monday: POLITICO.

Four Senate Republicans meeting with US President Trump at the White House and discuss funding for the Department of Homeland Security: POLITICO.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks took their cues from the positive performance on Wall Street, where the major indices rallied, and oil dropped after US President Trump announced US-Iran conversations and a five-day halt of strikes against Iranian energy infrastructure, while Iran denied the talks and called it fake news. Nonetheless, stocks gained in Asia but are well off their earlier highs as the conflict persisted overnight, while oil prices also partially rebounded amid news that gas-related facilities were hit in strikes on Isfahan in central Iran, where offices belonging to a gas company and a gas pressure reduction station were damaged. ASX 200 climbed at the open with outperformance in mining, materials and resources, although the index eventually pared the majority of gains with losses seen in tech and financials, while flash PMI data weakened. Nikkei 225 traded higher but had given back a chunk of the earlier spoils and briefly returned to beneath the 52,000 level with headwinds seen as oil prices partially rebounded from yesterday’s slump. Hang Seng and Shanghai Comp gained with outperformance in Hong Kong amid tech strength and with attention on earnings.

Top Asian News

Japanese Inflation Rate YoY (Feb) Y/Y 1.30% vs. Exp. 1.50% (Prev. 1.50%).

Japanese Core Inflation Rate YoY (Feb) Y/Y 1.60% vs. Exp. 1.70% (Prev. 2.00%, Low. 1.50%, High. 1.80%).

Japanese Inflation Rate MoM (Feb) M/M -0.2% (Prev. -0.1%).

Japanese Inflation Rate Ex-Food and Energy YoY (Feb) Y/Y 2.50% vs. Exp. 2.70% (Prev. 2.60%).

Japanese S&P Global Services PMI Flash (Mar) 52.8 vs. Exp. 51.8 (Prev. 53.8).

Japanese S&P Global Manufacturing PMI Flash (Mar) 51.4 vs. Exp. 52.8 (Prev. 53).

Japanese S&P Global Composite PMI Flash (Mar) 52.50 vs. Exp. 51.3 (Prev. 53.90).

Australian S&P Global Services PMI Flash (Mar) 46.6 (Prev. 52.8).

Australian S&P Global Composite PMI Flash (Mar) 47.0 (Prev. 52.4).

Australian S&P Global Manufacturing PMI Flash (Mar) 50.1 (Prev. 51.0).

European bourses (STOXX 600 U/C) trade mixed, with the AEX outperforming its peers while the FTSE MIB lags. The market reaction to the Flash PMIs were muted. However, the commentary within the PMIs gave the first glimpse at the effects of the Iranian war on businesses sentiment and the economy. The EZ release suggested the “eurozone GDP growth slowing to a quarterly rate of just below 0.1% in March with the forward-looking indicators pointing to a heightened risk of a downturn the coming months”. European sectors show a positive bias. Energy tops the sector pile, closely followed by Chemicals following broker upgrades for BASF and Brenntag. At the bottom of the pile lies Banks and Basic Resources. In the Luxury space, Puig (+14%) soars after Estee Lauder confirmed it is in talks with the Spanish company, regarding a potential merger.

Top European News

UK S&P Global Composite PMI Flash (Mar) 51.0 vs. Exp. 52.8 (Prev. 53.7, Low. 51.3, High. 53.6). “The war in the Middle East has hit the UK economy in March, stalling growth while driving inflation sharply higher.”. “Inflationary pressures have surged higher on the back of rising energy prices and fractured supply chains. The acceleration in cost growth in the manufacturing sector was especially severe, being the sharpest since the depreciation of sterling following Black Wednesday in 1992.”

UK S&P Global Manufacturing PMI Flash (Mar) 51.4 vs. Exp. 50.5 (Prev. 51.7, Low. 48.0, High. 51.6).

UK S&P Global Services PMI Flash (Mar) 51.2 vs. Exp. 53 (Prev. 53.9, Low. 50.0, High. 53.8).

EU S&P Global Composite PMI Flash (Mar) 50.5 vs. Exp. 51 (Prev. 51.9, Low. 49.7, High. 51.5). “The survey data are indicative of eurozone GDP growth slowing to a quarterly rate of just below 0.1% in March with the forward-looking indicators pointing to a heightened risk of a downturn the coming months. The survey’s price gauge is meanwhile indicative of consumer price inflation accelerating close to 3%, with cost pressure likely to add still further to selling price inflation in the coming months.”

EU S&P Global Manufacturing PMI Flash (Mar) 51.4 vs. Exp. 49.4 (Prev. 50.8, Low. 48.2, High. 50.3).

EU S&P Global Services PMI Flash (Mar) 50.1 vs. Exp. 51 (Prev. 51.9, Low. 50.2, High. 51.9).

German S&P Composite PMI Flash (Mar) 51.9 vs. Exp. 51.8 (Prev. 53.2, Low. 50.7, High. 52.7). “The service sector has seen an immediate negative impact. Growth in business activity has slowed sharply to its weakest since the current upturn began last September, weighed down by a drop in inflows of new work that reflects a combination of increased uncertainty and rising price pressures.”. “The big surprise is perhaps the acceleration in growth in the manufacturing sector. Reports from goods producers indicate that demand has in some cases been boosted by companies reacting to the disruption and uncertainty brought on by the war in the Middle East.”

Trade/Tariffs

EU farmers see the concessions offered as part of the EU-Australia trade deal as ‘unacceptable’, AFP reported.

EU and Australia agreed to a free trade deal, according to a joint statement.

Chinese Commerce Minister Wang Wentao meets the US-China Business Council delegation; details light.

FX

DXY is firmer this morning and currently holds at the upper end of a 99.09-99.39 range. Action which appears to be a slight bounce back from the pressure seen in the prior session after US President Trump announced a five-day postponement to military strikes on Iranian power plants. Since, Iran has reportedly denied the notion that talks took place, whilst Israeli press suggested that Iranian Foreign Araghchi informed US envoy Witkoff that Mojtaba Khamenei agreed to negotiations. Markets will await more clarity on the matter in the near term, which may cap the index below recent highs (100.54). Geopols aside, focus later on will be on the weekly ADP jobs stats (last week, the series reported an average of +9k/week over the four-week window) and also Flash PMIs.

G10s are entirely losing against the USD, with clear underperformance in the Antipodeans, which have been impacted by regional factors. For AUD/USD, the pair currently trades around 0.6955, but is still far from Monday’s trough of 0.6910; pressure which stems from weak flash PMIs. As for the Kiwi, RBNZ Governor Bremen highlighted that they would see higher inflation in the near term, which may have impacts on growth.

Over in Europe, a number of PMI metrics have been released. In brief, Manufacturing appears to be remaining resilient whilst the Services component has deteriorated. However, markets looked to the figures for any early indications of the impact on the economy following the Iran conflict. Within the accompanying German report, analysts highlighted that “the service sector has seen an immediate negative impact”, whilst describing manufacturing resilience as a “surprise” – but potentially on “forward purchases over concerns about potential supply disruption in the coming months”. EUR/USD was ultimately little moved on these metrics, and currently trades within a 1.1575-1.1618 range, and around its 21 DMA at 1.1617.

JPY is also a touch lower vs USD, with USD/JPY currently trading within a 158.27-158.79 range. Overnight, Japanese inflation was softer than expected, with headline Y/Y printing at 1.3% (exp. 1.5%). ING opines that the soft print will prove temporary and will not alter the BoJ’s rate hike cycle.

Finally, the UK’s PMI metrics also indicated resilience in Manufacturing, whilst Services were weaker than expected. The accompanying release highlighted that “the war in the Middle East has hit the UK economy in March, stalling growth while driving inflation sharply higher”. Cable saw some fleeting pressure on the report itself, but this was ultimately short-lived; currently trading around its 200 DMA at 1.3434.

Central Banks

BoJ Governor Ueda said he expects underlying inflation to accelerate moderately and price trend is to rise gradually. Tight labour market, firms’ active wage, price-setting behaviour will keep in place a cycle in which wages and prices rise in tandem. Temporary freeze on food sales tax may briefly push down inflation, but is likely to have a limited impact on inflation expectations. Will guide monetary policy appropriately to stably achieve the inflation target, accompanied by wage gains. To conduct policy for stable prices with wage growth.

ECB’s Kazaks says it is clear prices will be higher, and growth will be slower.

ECB’s Vujcic said ECB must be vigilant facing stagflation risk and officials will know soon whether they must act, adds if hikes are needed, better to start with a small move.

RBNZ Governor Bremen said will see higher inflation over the near term and some growth impacts, adds will be looking if firms are passing on costs or absorbing them, also looking for second round effects and will act if inflation expectations shift.

Fixed Income

A bearish start to the day has given way to a slightly mixed session as the morning progresses and broader market benchmarks move.

USTs in the red, lower by just under 10 ticks as it stands, but a few ticks off worst levels. Specifics for the space have been a little light in the early hours, with the market focused primarily on geopolitics and reporting around the Iranian Supreme Leader; see Commodities for a full breakdown.

As it stands, USTs in 110-16 to 110-29 confines, awaiting Flash PMIs for timely insight into how the Middle East situation is impacting the US economy; a point that may be of note as domestic focus turns increasingly to the midterms. Elsewhere, the docket features 2yr supply.

Bunds are now nearly unchanged. Started the day lower by 21 ticks, hitting a 125.24 trough as yesterday’s move retraced. Thereafter, the benchmarks lifted in the mid-morning alongside a modest bounce in peers. More recently, a bout of fresh pressure has been seen on Flash PMIs that point to a stagflation environment for the bloc, and one where price pressures are already evident.

Gilts started on the front foot, got to an 88.17 high early doors, as while the benchmark hadn’t fully acknowledged the bearishness in fixed seen late-US/early-APAC, the narrative had by the open reverted back to one of modest fixed upside as the energy space came under pressure once again. More recently, Flash PMIs for the UK also point to stagflation, as inflationary pressure “surged” while growth has “stalled”. A dynamic that underscores the difficult balancing act the BoE has at the moment, given a desire to avoid a return to price upside, but the already precarious labour and growth narrative factor against tightening.

Commodities

WTI and Brent futures are trimming some of the prior day’s heavy losses that were triggered by US President Trump’s announcement to postpone military strikes against Iranian power plants and energy infrastructure after the US and Iran had ‘very good and productive conversations’. Nonetheless as it stands, Iran denied talks with the US and called it fake news, but said messages had been conveyed in recent days through several friendly countries, while the partial rebound in oil was also spurred by a report that some gas-related facilities were hit amid US-Israeli strikes on Isfahan. Price action this morning has been rather rangebound, although some downside was seen following reports that Iranian Foreign Minister Araghchi is said to have secretly informed US Envoy Witkoff of Iranian Supreme Leader Mojtaba Khamenei’s agreement to negotiate, Al Arabiya reported citing Israeli press Yedioth Ahronoth citing sources, although this remains unconfirmed. Prices clambered off those lows as Israeli official suggests that it is unlikely that Iran will agree to US demands. WTI resides in a current USD 88.50-92.29/bbl range, and Brent in a USD 101.93-101.93/bbl parameter.

Spot gold is subdued amid a firmer USD as traders continue to weigh conflicting reports, with the yellow metal at the whim of the USD and oil prices, trading off lows in a current USD 4,305.94-4,448.33/oz range, but well within yesterday’s USD 4,099-4,536/oz range.

Base metals are mixed with a softer bias. 3M LME copper futures hover on either side of USD 12k/t as concerns over the Iran war’s impact on global growth and inflation weighed on sentiment, with PMIs also pointing to stagflation. 3M LME copper resides in a USD 11,908.00-12,111.98/t range at the time of writing.

Russia’s agriculture ministry said the fertiliser export restrictions only concern ammonium nitrate. This comes following TASS reporting that Russia is introducing some limits on fertiliser exports until April 21st.

India’s Reliance (RIL IS) has reportedly purchased 5mln bbls of Iranian oil following the US sanctions waiver.

The attacks on the gas pipeline in Khorramshahr did not affect its operations, Iran’s Fars News agency reported.

Mitsui O.S.K. Lines (9104 JT) denies reported its vessel passed through Strait of Hormuz.

Japanese PM Takaichi said will start releasing joint oil storage with oil producing countries by end of March.

Macquarie forecasts Brent hitting a floor of USD 85-90/bbl if the Iranian tensions decrease; said USD 150/bbl is still an option if the Strait of Hormuz remains shut until April.

Geopolitics

Iranian Foreign Minister Araghchi is said to have secretly informed US Envoy Witkoff of Iranian Supreme Leader Mojtaba Khamenei’s agreement to negotiate, Al Arabiya reported citing Israeli press Yedioth Ahronoth citing sources.

Senior Iranian Foreign Ministry official said Iran received points from the US through mediators and that they are being reviewed, according to CBS News.

Iranian Revolutionary Guard said it is launching the 78th wave of Operations Al-Waad Al-Sadiq 4 towards the occupied territories and American bases.

The chances of an agreement between the US and Iran are “very small,” Israeli officials told The Jerusalem Post; sources said the deployment of American forces in the Middle East is continuing as usual. Israeli officials also said there has been no change in coordination with the US military or in operational plans.

Israeli official suggests that it is unlikely that Iran will agree to US demands; said US President Trump is determined to reach a deal with Iran.

Israel’s Air Force is launching raids on military infrastructure and production sites near Isfahan,, Israel’s Channel 12 reports.

Israeli Defence Minister Katz says Israel will establish a buffer zone in southern Lebanon, modelled on what was implemented in Rafah, Al Jazeera reports; the army is now carrying out ground operations in Lebanese territory to control the front line.

Gas-related facilities said to be hit in strikes on Isfahan in central Iran, in which offices belonging to a gas company and a gas pressure reduction station were damaged in a US-Israeli attack on Isfahan in central Iran, according to Fars News Agency.

A projectile fell on a gas pipeline feeding a power station in Khorramshahr, Iran, while there were no casualties.

Saudi Arabia reportedly told the US it was ready to strike Iran if its own power and water facilities were targeted by Iran, according to reported citing sources.

US President Trump’s admin is eyeing Iran’s parliament speaker Ghalibaf as US-backed leader, according to POLITICO.

The US is ready to provide real security guarantees if Ukraine withdraws from Donbas, according to Ukrainian press citing sources. According to the interlocutors, in the absence of progress, the American side is allegedly considering the possibility of withdrawing from the negotiations and switching attention to other areas, in particular Iran.

US Event Calendar

9:45 am: United States Mar P S&P Global US Manufacturing PMI, est. 51.45, prior 51.6

9:45 am: United States Mar P S&P Global US Services PMI, est. 52, prior 51.7

9:45 am: United States Mar P S&P Global US Composite PMI, est. 51.9, prior 51.9

10:00 am: United States Mar Richmond Fed Manufact. Index, est. -8, prior -10

6:30 pm: United States Fed’s Michael Barr Speaks on Economic Outlook

DB’s Jim Reid concludes the overnight wrap

If Friday does mark the worst point for markets in this conflict (and it’s a big if), you’d have to say bravo to the geopolitical playbook often cited by us but borrowed from Binky Chadha and Parag Thatte in our equity strategy team. The average US equity market bottom after a geopolitical shock is 15 days as you can see from last week’s CoTD here. Friday was trading day 15 and a horrible close.

We had a horrible open yesterday as well but markets ultimately saw a massive turnaround, with a huge multi-asset rally after Trump said that the US and Iran were talking, alongside a 5-day suspension of US strikes against Iran’s power plants and energy infrastructure that he had threatened on Saturday. For markets, the fact that the two sides might be talking was taken as a huge positive, because it opened up the tail outcome of a much quicker end to the conflict than previously supposed. So by the close, Brent crude oil prices (-10.92%) were back down to $99.94/bbl, which significantly eased fears about the scale of any inflation shock. And in turn, other markets surged back, with the S&P 500 up +1.15% by the close, even though futures were down -1.15% in the European morning, whilst bond yields fell sharply on both sides of the Atlantic. Perhaps bond yields played a part in the strategic calculations with 10yr US yields up +50bps from just before the strikes 3 weeks ago in the London morning yesterday. Stand by today for the European and US flash PMIs for the first signs of the data impact from the war.

Obviously much now depends on the progress of any talks, and whether the more optimistic rhetoric is followed up by concrete action. Indeed, Iranian officials have repeatedly denied that talks with the US were even happening, which had contributed to markets reversing some of the initial risk-on reaction late yesterday and overnight. Brent crude has edged back up nearly 4 percent to $103.88/bbl this morning, with futures on the S&P 500 (-0.69%) and STOXX 50 (-0.84%) notably lower. 10yr USTs are +3.8bps at 4.38%. So some nervousness has crept back in. The WSJ last night reported that Saudi Arabia and the UAE were considering joining the war against Iran which hasn’t helped sentiment.

Before this, the catalyst for yesterday’s big moves was a post from Trump on his Truth Social platform, where he said the US and Iran had held “very good and productive conversations regarding a complete and total resolution of our hostilities”. Moreover, he added the US would “postpone any and all military strikes against Iranian power plants and energy infrastructure for a five day period”. Later on, Trump added that the most recent discussions happened the previous evening, with Steve Witkoff and Jared Kushner on the US side. Admittedly, there was a bit of a pullback to the news shortly after, as Iran’s state-run Mizan news said there were no talks between Iran and the US, and that Trump’s statements were “part of efforts to reduce energy prices and buy time for the implementation of his military plans”. Nevertheless, even that statement said there were “initiatives from regional countries to reduce tensions”. And later on, an Axios reporter tweeted that an Israeli official had told him that Witkoff and Kushner were negotiating with the speaker of Iran’s parliament.

The trajectory of this newsflow was taken positively, with the prospect of talks leading to a huge slump in oil prices. So Brent crude fell from $113/bbl right before Trump’s post to close at $99.94/bbl. It was a similar story for WTI as well, which fell from around $99/bbl immediately beforehand to just $88.13/bbl by the close. And as optimism mounted about a potential deal, those declines were echoed further out the energy futures curve. So the 6-month Brent future was down from $92/bbl before the post to $83.22/bbl by the close. It’s back up to $86.39/bbl as I type this morning.

We’re still comfortably below the highs from yesterday morning and that pullback in oil prices was treated with a huge sigh of relief, as it significantly eased fears about a stagflationary shock, and also pushed back against the prospect of imminent rate hikes. That was a big theme yesterday, and during the European morning, investors had moved to fully price an ECB hike as soon as the next meeting in April, which helped trigger a fresh bout of records for sovereign bond yields. In fact at the intraday high, the 10yr bund yield got as high as 3.07%, a level last seen back in 2011 during the Euro crisis.

However, it was a completely different story by the close, with investors ultimately pricing in a less hawkish path for the ECB relative to Friday. For instance, the chance of an April hike was down to 68%, having been at 80% on Friday. And looking further out, 63bps of hikes were priced by the December meeting, down from 77bps on Friday. So that eased the pressure across European sovereigns, with yields on 10yr bunds (-3.9bps), OATs (-4.6bps) and gilts (-7.4bps) all seeing sharp declines. 10yr Bunds traded as low as 2.95% before closing at 3.00%. The yield declines were particularly clear at the front-end of the curve, with the 2yr German (-9.9bps) and 2yr UK (-15.1bps) yields posting their biggest daily drop since the Liberation Day turmoil last April. They’ll give up some of these gains at the open this morning though.

For US Treasuries it was much the same pattern, as market pricing for the Fed oscillated dramatically through the session. At the most hawkish point shortly before Trump’s post, futures were pricing in a 90% chance of a hike by December. But that completely turned around afterwards, with futures basically pricing in a flat path for the year ahead. So that also led to a big turnaround for US Treasuries, with the 10yr yield (-3.7bps) eventually closing at 4.34%, despite being at an 8-month high of 4.44% earlier in the day. As mentioned at the top, US yields have reversed some of those gains this morning.

The turnaround was evident for equity markets too, as an initial slump gave way to a strong recovery. Indeed at the open, the STOXX 600 was into technical correction territory on an intraday basis, with the index down -11.8% from its record high before the strikes began. But that then completely turned around, with the index rising to as much as +2.30% intra-day, though it pared those gains to +0.61% by the close. And it was much the same story in the US, with S&P 500 futures down -1.15% in the European morning, before the index closed +1.15% higher and having traded as high as +2.23%. Moreover, the VIX had risen above the 30 mark once again, before also coming down to close at 26.15pts.

The partial reversal of the initial market relief came amid doubts over prospects for a negotiated resolution. Iran denied the premise of that Axios report, with the speaker of Iran’s Parliament saying that fake news was being used “to manipulate the financial and oil markets and escape the quagmire in which the US and Israel are trapped”. Meanwhile, Iranian state TV said that the US had tried to negotiate with Iran via intermediaries, but that Iran hadn’t responded to the request. And then overnight, Iran’s Deputy Speaker of Parliament said there would be no negotiations, and that Iran will not “return the Strait of Hormuz to its previous state”.

In Asia markets are off their highs as nervousness around a deal increases. Remember they closed yesterday with sentiment near its lows so markets are still higher. The KOSPI (+2.53%), Hang Seng (+1.48%), Shanghai Composite, and Nikkei (+0.64%) are all higher.

In terms of data, Japanese core CPI inflation decreased to a near four-year low of +1.6% (v/s +1.7% expected), attributed to ongoing government initiatives aimed at alleviating elevated food and utility costs. It was also lower than the 2.0% figure recorded last month. The headline CPI inflation increased by 1.3% y/y, marking its slowest growth since March 2022. The core-core CPI, which excludes fresh food and energy prices, rose by +2.5% y/y in February, a slight deceleration from the +2.6% increase last month. The preliminary Japanese S&P Global flash composite PMI dropped to 52.5 in March from 53.9 in February, indicating the slowest rate of expansion in three months. This deceleration was widespread across various sectors. Services activity decreased to 52.8 from 53.8, while manufacturing exhibited a more significant decline in momentum, with the headline PMI falling to 51.4 from 53.0. Around all the news flow over the last 24 hours, 10yr JGBs are -3.2bps lower trading at 2.27%.

Elsewhere, the S&P Global Australia manufacturing PMI fell to 50.1 in March 2026 from 51.0 in February. The services PMI dropped from 52.8 to 46.6, signalling the first contraction in over two years. This is the first signs of the impact of the war on the global data. We’ll get the rest of the numbers from Europe and the US today, which are important because they’re one of the first indicators we’ll have covering the period since the strikes began on February 28.

Looking at the day ahead, data releases include the March flash PMIs from the US and Europe, whilst there’s also the Richmond Fed’s manufacturing index for March. Central bank speakers include the Fed’s Barr, and the ECB’s Kocher, Sleijpen, Cipollone and Lane, and the BoE’s Pill. Finally, there’s a general election taking place in Denmark.

* * *

Tyler Durden

Tue, 03/24/2026 – 08:35

https://www.zerohedge.com/markets/future-drop-oil-yields-rise-relentless-war-newsflow

Senators Close To Deal To End Airport TSA Crisis As Americans’ Fury Mounts

Senators Close To Deal To End Airport TSA Crisis As Americans’ Fury Mounts

With no-shows by unpaid TSA agents imposing hours-long security-line waits and missed flights on flyers at major airports across the country, senators on Monday night signaled that a deal to end the TSA crisis is finally within sight.

The leap toward a deal followed a White House meeting of a group of Republican senators hosted by President Trump. “It went really well,” said Alabama Sen. Katie Britt, who was among the attendees. Asked if the group had a solution in hand, she replied “We do.” Optimistic signals came from the other side of the aisle as well. “Both sides are talking in a serious way,” Senate Minority Leader Chuck Schumer told the Wall Street Journal on his way out of the Capitol on Monday night.

Chaos at PHL International airport right now😳😳several TSA checkpoints are closed @FOX29philly pic.twitter.com/1n3zq9gYwz

— Morgan Parrish (@MorganParrishTV) March 19, 2026

The crisis sprang from Democrats’ refusal to fund the Department of Homeland Security unless reforms are made to how Immigrations and Customs Enforcement (ICE) officers carry out their duties. Those demands came after ICE agents shot two aggressive anti-ICE activists to death in two separate incidents in Minnesota.

Some of the leftists’ demands may actually be considered reasonable by those right-wingers and libertarians who are wary of police overreach — such measures include refraining from forcible entry into private homes without a warrant, a ban on agents wearing masks, and the implementation of body cameras. Democrats have also demanded an end to roving patrols and additional training on use of force and de-escalation. With Republicans only holding a 53-47 margin, the Democrats have the numbers to block funding, since it takes 60 votes to get by a filibuster.

🚨#BREAKING: ABSOLUTE PANDAMONIUM at the New Orleans airport this morning where the TSA security line stretched…

…ALL THE WAY OUT INTO THE PARKING GARAGE!!!!

WE SHOULDN’T HAVE TO DEAL WITH THIS JUST TO GET ON AN AIRPLANE!!!! pic.twitter.com/Qs7ZnqpMYL

— Matt Van Swol (@mattvanswol) March 22, 2026

The deal that’s taking shape would fund all of the sprawling, 260,000-employee DHS except for Enforcement and Removal Operations, which is the ICE group that arrests and deports immigrants.

Money would flow to ICE’s Homeland Security Investigations, which focuses on international crimes like human trafficking and drug smuggling, Democratic Delaware Sen. Chris Coons told the Journal.

As for the next step:

Coons and other Democrats said they expect an offer on paper from Republicans as soon as Tuesday, and the details would matter.

“Trust but verify. It’s part of the challenge of our dear president,” Coons said, making a roller-coaster motion with his hand.

— WSJ

The shutdown started on Valentine’s Day, and TSA and other DHS workers missed their first full paycheck on March 13. Things started getting progressively worse at the largest US airports, with nightmarish imagery of three-hour lines going viral on social media.

To improve the situation, the Trump administration ironically deployed ICE agents to airports to fill in for the no-show TSA employees. This leftist opted to heckle them:

A woman shouted “ICE out now” at agents inside Newark Airport, then another passenger stepped in, thanked them and shook their hands pic.twitter.com/ACodQfTMpX

— Surajit (@surajit_ghosh2) March 23, 2026

Exasperatingly, the Democrats’ shutdown hasn’t even affected its main target: ICE has been going full-steam-ahead during the shutdown, tapping $75 million in appropriations in the 2025 One Big Beautiful Bill — enough to keep ICE from melting for years.

Earlier on Monday, Trump had signaled that he wanted the deal to be reached by merging it with the SAVE America Act, which would make ID requirements for voting in federal elections more strict. It would also require proof of citizenship during voter registration. That avenue seemed unlikely then and even more so now.

Tyler Durden

Tue, 03/24/2026 – 08:20

https://www.zerohedge.com/political/senators-close-deal-end-airport-tsa-crisis-americans-fury-mounts

Dry Van Spot Rates Highest Since 2022 As Spring Tightens Capacity

Dry Van Spot Rates Highest Since 2022 As Spring Tightens Capacity

Submitted by FreightWaves,

The freight market momentum is building at a rapid clip.

National dry van spot rates — tracked via the SONAR National Truckload Index, the 7-day moving average of booked rates including fuel — have broken out to a new cycle high of $2.89 per mile.

This represents the strongest level since 2022 and confirms the market’s shift toward carriers is gaining real traction.

Even more telling: rates jumped $0.12 per mile in the past week alone. That’s a sharp weekly gain that underscores accelerating tightness and carrier pricing power. Spot rates have now recaptured roughly $0.50–$0.60 per mile net of fuel over recent months, climbing from the low $2.00s that defined much of 2023–2024. We’re witnessing 20–25% year-over-year recovery in key lanes and metrics, with volumes holding at multi-year highs reminiscent of late 2022.

This isn’t isolated noise — it’s driven by fundamentals. The return of industrial demand remains the core engine, with stronger manufacturing signals, flatbed activity, and overall domestic freight resilience putting sustained pressure on a shrunken truckload supply. Multi-year carrier attrition (exits, driver regulations, and structural challenges) has left capacity thin, making the market highly responsive to any demand pickup. National tender rejection rates sit stubbornly in the low-to-mid teens (around 13–14% recently), with the Midwest still leading above 18% and tightness now spreading more broadly.

Seasonal layers are piling on:

Produce season is ramping in major growing regions.

Construction is accelerating as weather improves.

Gardening and home improvement demand is building.

Beverage season is gearing up for warmer months.

These verticals compound the industrial rebound, further squeezing available trucks.

The West Coast awakening adds a powerful pull. Chinese New Year landed later this year (February 17, 2026, vs. earlier in prior cycles), prolonging the post-CNY slowdown and keeping Southern California unusually loose into early March (outbound rejections below 5%). But the rebound is hitting hard now: inbound containers are surging, outbound tenders are recovering, and rejections are set to rise meaningfully.

This creates a classic “magnet” for capacity. Long-haul carriers chase West-to-East port loads for their superior length of haul (1,500–2,000+ miles per move) versus shorter eastern runs that demand multiple loads for equivalent paid miles. As trucks reposition westward from Midwest/Southeast corridors (along I-35 and parallels) to capture higher-paying outbound freight via I-20 and I-40, interior markets face no relief — expect even tighter conditions back east. The Midwest’s industrial strength and elevated rejections mean any capacity drain will intensify pressure, not ease it.

Broader indicators align:

Tender rejection rates remain high nationally, with seasonal builds accelerating the spread.

Dry van spot rates continue rising on resilient volumes and persistent constraints.

Ocean bookings are starting to recover sharply from Chinese New Year

The bottom line: Spring 2026 is igniting hotter and earlier than recent years. The $2.89 cycle high — fueled by a $0.12 weekly jump — reflects tightening capacity, resurgent industrial demand, seasonal verticals firing up, and the delayed-but-powerful post-CNY import surge creating synchronized tightness. Shippers unprepared for higher costs are under immediate strain, with routing guides tested early. Carriers positioned for West Coast outbound, industrial, and seasonal lanes are capturing the gains as capacity reallocates — but back east, conditions are set to tighten further as carriers shift their focus towards the West to East longhaul.

Monitor SONAR outbound rejections and spot rates from Southern California over the next 2–4 weeks, alongside Midwest/Southeast trends. The speed of this spread will show how broad and sustained the impact becomes.

The spring shipping season is just getting started — and it’s going to be a hot one

Tyler Durden

Tue, 03/24/2026 – 08:05

https://www.zerohedge.com/economics/dry-van-spot-rates-highest-2022-spring-tightens-capacity

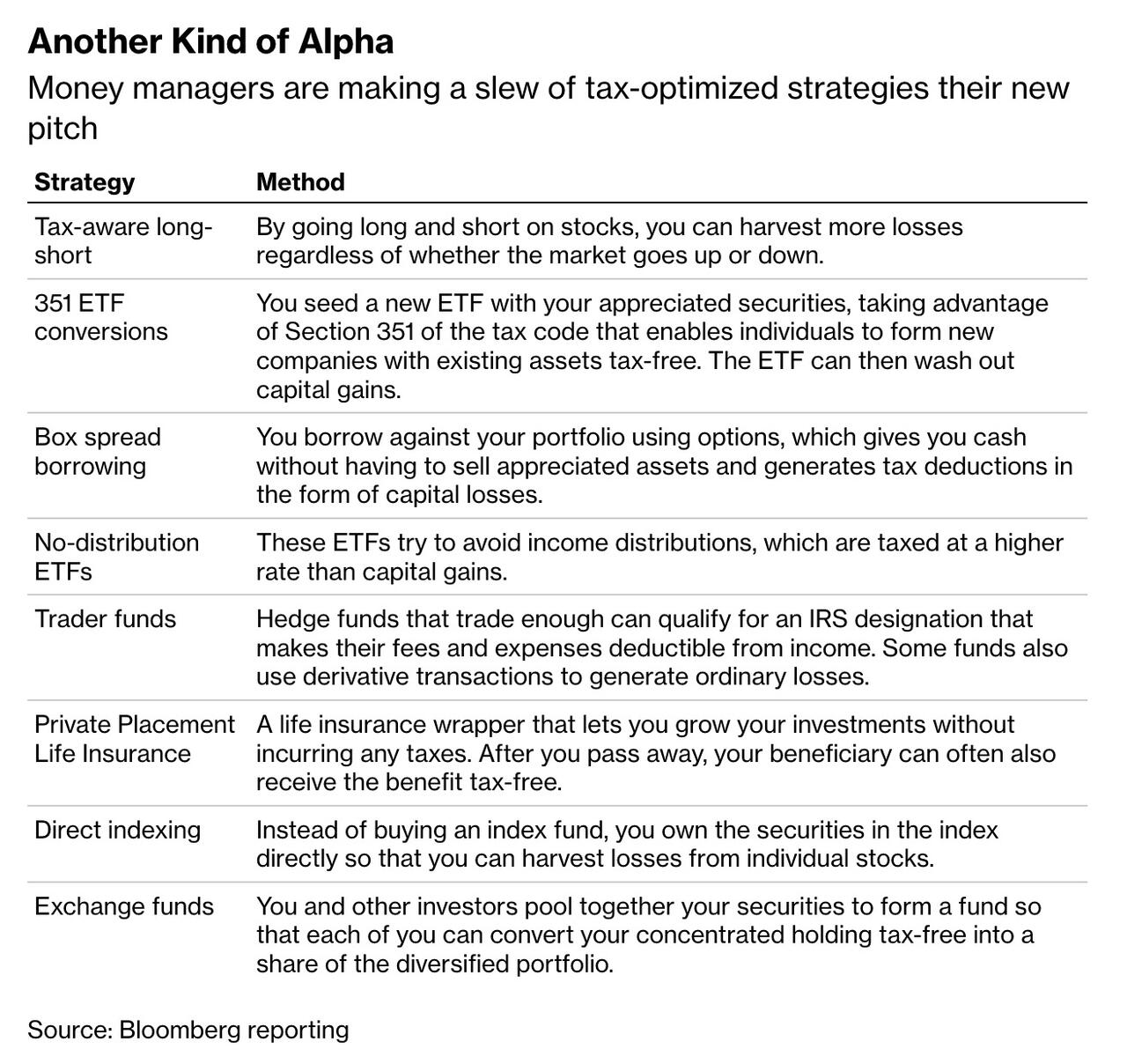

Wall Street’s Trillion-Dollar Bet On “Tax Alpha”

Wall Street’s Trillion-Dollar Bet On “Tax Alpha”

Tax alpha — the practice of improving investment returns by reducing taxes — has become one of the fastest-growing strategies on Wall Street, according to Bloomberg.

Rather than focusing only on beating the market, many investment firms now design portfolios to minimize taxes, often producing higher after-tax returns even if pre-tax performance is similar to traditional strategies.

After years of rising markets, many wealthy Americans hold large unrealized gains in stocks and funds. To address the resulting tax burden, asset managers have developed a wide ecosystem of tax-optimization techniques. More than $1 trillion is now invested in strategies built around tax efficiency, ranging from simple ETF structures to complex hedge fund portfolios.

Some of the simplest approaches involve structuring funds to limit taxable events. Certain exchange-traded funds minimize distributions by carefully timing stock sales, reducing investors’ annual tax bills. At the other end of the spectrum are more complex strategies that deliberately generate losses or deductible expenses that can offset gains — and sometimes even ordinary income.

One of the fastest-growing segments is tax-aware long-short investing. These portfolios simultaneously hold long and short positions in stocks, seeking both overall market returns and realized losses that investors can use to offset capital gains elsewhere. Estimates suggest more than $100 billion is invested in these strategies.

Technology and new financial startups have also made tax optimization more accessible. Strategies once limited to ultra-wealthy investors with millions of dollars are increasingly available to clients with much smaller portfolios, thanks to automation and lower costs.

Bloomberg writes that large asset managers have joined the trend as well. Firms such as BlackRock and Vanguard have expanded offerings in separately managed accounts and direct indexing. Instead of buying a fund that tracks an index, direct indexing allows investors to own the individual stocks themselves, making it easier to sell losing positions and offset gains elsewhere in the portfolio. Direct indexing alone has grown to more than $1 trillion in assets.

Hedge funds are also adapting their strategies to focus on after-tax returns. Quantitative firms including AQR Capital Management and Man Group have introduced tax-aware versions of their portfolios that actively manage gains and losses to improve clients’ tax outcomes.

The growth of tax-alpha strategies has attracted criticism from policymakers and tax experts. Because every dollar saved by investors reduces government revenue, critics argue the trend widens inequality by giving wealthy investors sophisticated tools to lower their tax bills. Many of the strategies rely on provisions in decades-old tax laws that were written long before the speed and complexity of modern financial markets.

Some of these techniques — such as exchange funds and certain corporate restructuring transactions used to move appreciated assets into ETFs without triggering taxes — are beginning to draw scrutiny from regulators and lawmakers. However, meaningful legislative action appears unlikely in the near term.

Despite the criticism, demand continues to rise. Advisors argue that after-tax performance often matters far more than headline investment returns, especially for investors facing high capital-gains taxes. Deferring taxes allows more money to remain invested and compound over time.

Many tax-alpha strategies rely on deferral rather than permanent avoidance. Investors may still owe taxes when they eventually sell assets. But if those taxes can be postponed for years — or even decades — the additional compounding can significantly increase long-term wealth.

In some cases, taxes may never be realized at all. Under current U.S. law, inherited assets receive a “step-up in basis,” meaning unrealized gains can effectively disappear when wealth passes to heirs. This possibility makes long-term tax deferral one of the most powerful forms of tax alpha.

* * * Add Alpha to your garden with CLEAN FOOD

Tyler Durden

Tue, 03/24/2026 – 07:45

https://www.zerohedge.com/markets/wall-streets-trillion-dollar-bet-tax-alpha

Amazon Data Centers “Disrupted” Across Bahrain After Drone Activity

Amazon Data Centers “Disrupted” Across Bahrain After Drone Activity

Brent crude futures are back in triple-digit territory as fighting in the Middle East continued overnight, even as President Trump claimed that talks are underway with Iran to resolve the conflict, which has now entered its fourth week.

Overnight, the Amazon Web Services in the Bahrain region was severely “disrupted,” according to Reuters, citing an Amazon spokesperson, following drone activity in the area. The spokesperson would not confirm whether Iranian drones struck any data centers.

“As this situation evolves and, as we have advised before, we request those with workloads in the affected regions continue to migrate to other locations,” Amazon wrote in a statement.

Bahrain News Agency reported on Monday that its armed forces had intercepted and destroyed 147 Iranian ballistic missiles and 282 drones since the start of the conflict.

Amazon’s cloud computing unit is critical for Bahrain’s digital infrastructure and is embedded in public-sector cloud operations.

This disruption to AWS data centers in the Gulf is the second instance in the US-Iran conflict of IRGC forces targeting data centers with drones in early March.

Latest reporting:

Data Center Hunter: Iran Expands Drone Target List, From AWS To Microsoft Facilities

Drone Strikes On Amazon Data Centers In Middle East Reveal Urgent Need To Defend AI

“Bomb Data Center”: Eric Schmidt Warns AI Arms Race Could Spark Global Conflict

“The targeting of Amazon and Microsoft in these operations has dealt a serious blow to the enemy’s technological and information infrastructure,” Iranian news outlet Fars News Agency said in a Telegram post, as quoted by the Financial Times earlier this month.

We warned, one month before two AWS data centers in the UAE were hit by IRGC drones, that Wall Street analysts had completely missed the fact that, with trillions of dollars being deployed over the next several years worldwide on data center buildouts, one major security gap had emerged: the urgent need for counter-UAS systems.

We know exactly why Wall Street analysts completely missed this security gap: they were too weirdly fixated on a non-existent climate crisis and could not properly identify the most immediate threat. These Ivy League-educated analysts simply had the wrong framework to operate on.

Since the US-Iran conflict began, it has confirmed that civilian infrastructure will not be spared (and in fact increasingly targeted over explicit military assets), and this is a wake-up call for data-center builders worldwide. Time to deploy counter-UAS systems.

Tyler Durden

Tue, 03/24/2026 – 06:55

International Energy Agency Pushes Rationing

International Energy Agency Pushes Rationing

Authored by Jeffrey Tucker via The Epoch Times,

The International Energy Agency in Paris has released a new and urgent document that it wishes all nations with energy struggles to adopt.

Many are doing that now.

The website even maintains a spreadsheet updated daily to celebrate the countries that are following its plan for controlling energy use.

Before explaining why none of this will work, let’s look at what they are suggesting.

Seeming out of nowhere, the head of the IEA, Dr. Fatih Birol, is being quoted in the high-end press as the world’s expert.

His Wikipedia page says that he is from Turkey but works closely with China on the “energy transition.”

Indeed, he has been a member of the Chinese Academy of Engineering since 2013.

Inspired by the manner in which governments were able to control communication and people during the COVID crisis, the IEA advises the following:

1. Work from home where possible. You read that right: we are back to languishing at home and consuming entertainment through laptops. Some governments (Indonesia, Vietnam, Pakistan, Philippines) have already adopted this policy loosely, with new measures such as four-day work weeks. IEA comments: “Displaces oil use from commuting, particularly where jobs are suitable for remote work.”

2. Reduce highway speed limits by at least 10 km/h. That means lowering all speed limits by 6-7 miles per hour, which is really nothing more than a method to create an annoyance. The IEA says “lower speeds reduce fuel use for passenger cars, vans and trucks,” but is that even true? Not always. Boggy traffic creates more stop/start situations that cause more gas consumption.

3. Encourage public transport. That exhortation has been the dream of city planners for probably 50 years. Not everyone can do this of course and a mandate like that will cause many just to stay home. In this case, IEA is probably correct: “A shift from private cars to buses and trains can quickly reduce oil demand.” But not for the reason you might think. It just means more staying at home.

4. Alternate private car access to roads in large cities on different days. Now we are getting to a policy that drove an entire generation batty in the 1970s. In those days, even/odd license plates were allowed access to gas but this is more intense. Alternating access would require a massive policing effort, one that is without precedent. IEA comments: “Number-plate rotation schemes can reduce congestion and fuel-intensive driving.”

5. Increase car sharing and adopt efficient driving practices. This is easily done in the same way police enforce HOV lanes. You cannot drive alone. You must have other passengers if you are going to be out on the road. One can imagine a future in which people routinely grab a family member or friend to sit in the passenger seat for compliance purposes. IEA comments: “Higher car occupancy and eco-driving can lower fuel consumption quickly.”

6. Efficient driving for road commercial vehicles and delivery of goods. Here we get to the old essential/nonessential divide. Commercial deliveries are allowed because we have to live somehow but driving to the park for a picnic or visiting friends and families is not.

7. Divert LPG [Liquefied Petroleum Gas] use from transport. This is the planner’s vision to preserve propane for “essential needs.”

8. Avoid air travel where alternative options exist. You will surely notice that this is already happening. My recent flight bookings have doubled in price. Because of the limited government shutdown, airport security lines can be 2-3 hours. People miss flights or simply bail out and go home. This is also causing connections to fail. Events this weekend that relied on travel are a bust. IEA comments: “Reducing business flights can quickly ease pressure on jet fuel markets.”

9. Where possible, switch to other modern cooking solutions. Earlier we saw an exhortation to save propane for cooking but here we see that this is not recommended either. We are supposed to switch to electric appliances. IEA comments: “Encouraging electric cooking and other modern options can reduce reliance on LPG.”

10. Leverage flexibility with petrochemical feedstocks and implement short-term efficiency and maintenance measures. This advice is directed toward energy plants to switch from one source to another to conserve oil. This suggestion reaches deep into industrial planning and would require draconian enforcement.

There are features of this plan that surely remind you of what we went through just a few years ago for purposes of controlling infectious disease. It’s uncanny how there is a spooky overlap between those methods and these. They all require staying home, hunkering down, reducing consumption, complying with edicts, feeling afraid both of shortages and of methods of enforcement.

To be sure, you could say that the International Energy Agency has no actual power. It was founded in 1974 to monitor global energy use. It has more recently been a top advocate of net-zero energy policies associated with what is known popularly as the “Great Reset.” It is not a private organization as such but a non-government branch of the Organization of Economic Cooperation and Development, meaning quasi-official but without the power to enforce its edicts.