Category: News

Iceland Strips Father Of Custody After Questioning Gender Transitioning Of His Minor Child

Iceland Strips Father Of Custody After Questioning Gender Transitioning Of His Minor Child

We just discussed the horrifying story of a Christian family in Sweden who have been unable to regain custody of their daughters after the government declared them religious extremists.

In Iceland, a father has been stripped of his parental rights after speaking out against his 11-year-old autistic son‘s sex change.

Alexandre Rocha, a French national who has lived in Iceland for 25 years, lost custody of the child to the child’s mother in December after questioning the long-term impacts of puberty blockers and hormone therapies.

Rocha says that his child is confused and exposed to little beyond video games.

He argued that his child’s autism and the trauma of the marital separation led to the findings of mental and emotional instability.

He believes that his child was pulled along this course, attracted by the attention from the various advisers.

The issue is not who is right or wrong, but why Iceland would terminate his parental rights because he has spoken out against what he believes is a harmful course of treatment for his child.

He believes that experts ignored how autism can produce the same feelings that they used to justify his gender transition as a minor.

He noted that his child also wanted to be a cat–often wearing cat ears in public.

Elon Musk has supported the father.

Musk has complained that he felt “tricked’ by experts in consenting to his own child to transition into a female.

Rocha had accused the mother of obstructing visits. Court documents show that the mother denied intentionally obstructing court-ordered visitation. She alleged that the child refused visits because Rocha did not affirm the child’s gender identity or use the new name.

There is an intense debate over the gender transitioning of minors.

Various European countries have also halted certain procedures after countervailing studies suggesting that the risks are too high.

England’s National Health Service 2024 report on the subject, known as the Cass Report, found concerning evidence of harm for minors and inconclusive benefits.

The Trump Administration has moved against hospitals engaging in such treatments.

Dozens of hospitals have halted such work, but New York Attorney General Letitia James has threatened to sue any hospital that refuses such treatment for discrimination under New York law.

Tyler Durden

Tue, 03/24/2026 – 05:00

Watch: McDonald’s Restaurant Rolls Out Robots To Greet, Serve Customers

Watch: McDonald’s Restaurant Rolls Out Robots To Greet, Serve Customers

A McDonald’s restaurant in Shanghai is trialling a team of humanoid robots as staff, offering a glimpse into what is likely to be the future of fast-food, Digitaltrends reports.

The robots, developed by Keenon Robotics, were spotted at a McDonald’s in the Shanghai Pudong New Area, where they picked up orders from customers at the front counter using a touchscreen. The video also shows children in the restaurant playfulling chasing after the animal-like robots that were greeting customers.

McDonald’s has yet to issue a statement on the now-viral video of the robot, but Keenon confirmed that its robots were deployed at the location.

“Watch the Keenon robot squad suit up and join the McDonald’s party,” the firm said, sharing a clip of its breakthrough technology. “Our humanoid series is leading the squad and hitting the streets,” Keenon Robotics said in a statement. “It’s a showcase of how service automation is becoming a seamless part of global dining, and how technology brings more smiles to every mealtime.”

The sighting of robots at McDonald’s comes as fears over robots and AI causing widespread job displacement has reached a feverish pitch. A recent Wall Street Journal report revealed that Amazon soon plans to roll out a million robots at its warehouses. Amazon currently has more robot workers than human workers, the Journal also said.

* * * McFuck that. Cook clean beef at home.

Tyler Durden

Tue, 03/24/2026 – 04:15

Russia-Linked Arms Trafficker, Corrupt African Officials Tried To Supply Mexican Cartel With Surface-To-Air Missiles

Russia-Linked Arms Trafficker, Corrupt African Officials Tried To Supply Mexican Cartel With Surface-To-Air Missiles

Submitted by The Bureau’s Sam Cooper (emphasis our own),

Federal prosecutors in Virginia have charged four men — a Bulgarian arms trafficker with ties to the notorious Russian weapons dealer Viktor Bout, and several African co-conspirators with connections to the governments of Uganda and Tanzania — with conspiring to supply the Cartel de Jalisco Nueva Generación with a $58 million military arsenal that included rocket launchers, surface-to-air missiles, anti-aircraft drones, and high-powered explosives the brokers boasted could bring down helicopters.

The international arms trafficking conspiracy deepens an already troubling portrait of the military reach and intelligence ties of the Cartel de Jalisco Nueva Generación. Court documents unsealed by the Department of Justice, in an investigation first reported by The Bureau, revealed that Iran’s Ministry of Intelligence and Security publicly issued threats directing the cartel to execute Goldie Ghamari — a prominent Iranian-Canadian activist and former Ontario politician — at her Ottawa home, offering a $250,000 bounty. The arms case suggests that the cartel Iran chose as its instrument of political assassination was simultaneously seeking the weapons inventory of a mid-tier military force.

The investigation was carried out by the Drug Enforcement Administration’s Special Operations Division — an elite, little-known counternarcotics unit that deploys high-grade intelligence tradecraft and has built its reputation targeting criminals of international reach, including those with connections to senior officials in hostile and corrupt states.

The April 2025 indictment, unsealed this month, identifies Peter Dimitrov Mirchev as the network’s central architect — a Bulgaria-based international arms trafficker the grand jury describes as having engaged in weapons trafficking for approximately 25 years. Court records note that Mirchev was previously implicated in supplying arms to Bout, the Russian weapons trafficker convicted in a New York federal court of conspiring to kill United States nationals, and conspiring to provide material support to a designated foreign terrorist organization.

Scott McGregor, a Canadian former military intelligence and federal police adviser, pointed to the case’s geographic sprawl as evidence of something beyond a conventional cartel prosecution.

“Not just a Mexico story. Not just a U.S. case,” McGregor wrote. “This DOJ case runs thru Bulgaria, Spain, Kenya, Tanzania, Uganda, Morocco, and Ghana, tied to an effort to arm the CJNG with military grade weapons. That is the anatomy of a transnational threat network.”

Arms transactions of this scale require End-User Certificates and Delivery Verification Protocols — import-export documentation that tracks military hardware from manufacturer to declared recipient, and that exists specifically to prevent transnational criminal organizations from acquiring weapons through legitimate channels.

According to the indictment, Mirchev recruited Kenyan national Elisha Odhiambo Asumo — described by prosecutors as a longstanding associate who sources arms certifications from various African countries “through bribery” — to obtain fraudulent documentation that would falsely identify the Tanzanian military as the weapons’ end-user.

Asumo in turn recruited Michael Katungi Mpeirwe, a Ugandan national described in the filing as a Policy Advisor employed by the Government of Uganda and as a security logistics officer associated with the African Union Commission. Mpeirwe recruited Tanzanian national Subiro Osmund Mwapinga.

Together, the three men obtained an arms certificate bearing the seal of Tanzania’s Ministry of Defence and National Services, certifying that 50 AK-47 automatic assault rifles were destined “for the Sole use of” the Tanzanian military.

At meetings in Cape Town, according to the indictment, Asumo and Mwapinga described their work openly — they had been constructing a “paper trail,” designed to conceal that the weapons were intended for Mexican drug traffickers. In July 2024, Mirchev and others exported the 50 rifles and accompanying magazines and ammunition from Bulgaria. After the shipment was seized, Asumo obtained a false Delivery Verification Protocol purportedly signed by Tanzania’s Permanent Secretary for Defence, confirming the Tanzanian military had received the weapons — even though it had not.

In April 2024, Mpeirwe attended a meeting in London where he offered to obtain additional firearms for the cartel through a planned arms deal between the governments of Russia and Uganda, explaining that his government connections across Africa would allow him to easily procure End-User Certificates for future transactions in exchange for a two percent commission.

The test shipment, prosecutors allege, was only the beginning.

By October 2024, Mirchev was in discussions about supplying the cartel with surface-to-air missiles, anti-aircraft drones, and the ZU-23 anti-aircraft weapon system — a Soviet-era gun platform capable of firing 23x152mm high-explosive rounds.

Mirchev described the ZU-23 as able to “automatically” track targets, firing rounds that “could put down helicopters.”

These discussions led to the procurement list totaling approximately 53.7 million euros: 2,000 modernized Kalashnikov assault rifles, 68 rocket-propelled grenade launchers, 60 PKM machine guns, multiple grenade launcher systems, sniper rifles, night vision equipment, anti-drone systems, drones with multi-spectrum cameras, armored vehicles, and tens of millions of rounds of ammunition across multiple calibers.

The scale of the procurement — a combined-arms package of the kind assembled by small national militaries — offers a measure of why the United States government has come to regard the Cartel de Jalisco Nueva Generación as an acute national security threat, not merely a criminal one.

According to the indictment, the cartel is one of Mexico’s most violent and prolific transnational criminal organizations, formed around 2011 and now operating across South and Central America, Europe, Asia, Australia, Africa, and throughout the United States.

Its primary criminal activity is the trafficking of cocaine, fentanyl, and methamphetamine, financed by billions of dollars in drug proceeds. The cartel uses violence against journalists, local communities, rival organizations, and government officials — attacks on military convoys and helicopters, assassinations and attempted assassinations — violence the indictment states is made possible in part by the illegal transfer of military-grade weaponry to transnational criminal organizations.

On February 20, 2025, the United States Secretary of State designated the cartel a Foreign Terrorist Organization and a Specially Designated Global Terrorist — a designation that triggers the indictment’s third count, conspiracy to provide material support to a foreign terrorist organization, which carries a mandatory minimum of ten years and up to life in prison.

The case is being prosecuted as part of Operation Take Back America. Mirchev was extradited from Spain. Asumo was extradited from Morocco. Mwapinga was extradited from Ghana. Mpeirwe remains at large.

Tyler Durden

Tue, 03/24/2026 – 03:30

Chinese Containership Is First To Pay Iran For “Safe Passage” Through Strait As Iraqi Tanker Crosses With Signal Off

Chinese Containership Is First To Pay Iran For “Safe Passage” Through Strait As Iraqi Tanker Crosses With Signal Off

The blockaded Strait of Hormuz is getting progressively less “blockaded” by the day.

Over the weekend we reported that “Iran was Ready To Let Japanese Ships Use Hormuz As Chinese, Indian Tankers Already Allowed Passage.” We can now add Iraq to the growing list of nations whose vessels are transiting the infamous Strait.

An oil supertanker hauling two-million barrels of Iraq’s crude got through the Strait of Hormuz, the first vessel observed moving Baghdad’s barrels through the the vital waterway – according to Bloomberg – since it all but closed to commercial shipping because of the Iran war.

The Omega Trader tanker Source: MarineTraffic

The Omega Trader, managed by Japan’s Mitsui OSK Lines Ltd, signaled over the past few days that it reached Mumbai. Its prior signal before reaching the Indian port city had been from inside the Persian Gulf more than ten days ago, suggesting the tanker had shut off its tracking beacon while making the transit.

While only a few tankers have gone through since the conflict began, the transits help to alleviate what the International Energy Agency describes as the biggest supply disruption in the history of the oil market.

Many of the ships that have managed to get through Hormuz have discharged in India (the rest have proceeded onward to Singapore and “friendly” China). The nation’s government has engaged with Iranian officials to seek passage for vessels due to haul energy to the country, and one liquefied petroleum gas vessel was guided through Hormuz by the Iranian navy.

The ship’s technical manager is Mitsui OSK, according to data on the Equasis maritime database. The company didn’t respond to a request for comment outside of normal business hours.

Meanwhile, in a first for the Strait’s new role as Iran’s (temporary), toll road a Chinese-owned feeder containership has become the first vessel with confirmed mainland Chinese ownership to pay Iran for passage through the Strait of Hormuz, transiting via a so-called “safe” shipping corridor near Tehran’s Larak Island, Lloyd’s List reported.

As previously reported, multiple oil tankers and containerships have made a break from the Persian Gulf in recent days. The Al Ruwais loaded naphtha from the UAE in early March and is now heading to Asia, while the Abu Dhabi-III is expected to arrive in India’s Vadinar port on Monday after also loading fuel at Ruwais. Given that a lot of ships go through with their signals off, it’s possible that other tankers will pop up having already left the Persian Gulf.

Tyler Durden

Tue, 03/24/2026 – 02:45

Second Youth-Center Gang-Rape Case Emerges As Cover-Up Fears Grow In Germany

Second Youth-Center Gang-Rape Case Emerges As Cover-Up Fears Grow In Germany

A mother in Lower Saxony who found a disturbing video on her daughter’s phone that revealed that she was gang raped inside a church-run youth center by three teens, including a Syrian, Iranian, and Dutch national, in Gnarrenburg. However, once the story came out, it only grew darker, as it was revealed that staff, church officials and local authorities subsequently did everything possible to bury the story.

This gang rape comes after national news reports revealed that a gang rape sexual assault occurred in another youth center in Berlin, but which was covered up because the assailants were Muslims and the youth center workers did not want to increase stigmatization.

In this latest case, the woman, 43, says she first suspected something was wrong when she found a disturbing video on her daughter’s phone. It showed a girl being pinned down by a boy, filmed from behind. Confronted with the footage, her daughter was defensive, saying she had “no idea” where the footage came from and claimed, “It’s not me!”

However, within days, the truth emerged in a WhatsApp message the girl sent to her mother: “Then they all did it to me and locked the door and turned on music so you wouldn’t hear anything.”

The assault is alleged to have taken place in an upper room of the youth center in Gnarrenburg. The facility is jointly run by the local Protestant church and the Gnarrenburg community.

Three suspects have been identified — a 16-year-old Dutch national who attends the vocational school across the street and is said to have lured the girl there via Snapchat, an 18-year-old Iranian with a substantial file at the youth welfare office, and a 15-year-old Syrian who, according to the mother, later claimed he was coerced into participating.

The supervisor on duty, a part-time church deacon, later claimed he heard nothing.

When the girl showed him a pregnancy test in the days that followed, he neither contacted her parents nor the police, reportedly telling the family he was bound by a duty of confidentiality.

Experts say no such obligation exists in cases of serious criminal conduct.

During the rape, other young people were reportedly cheering outside the locked door during the attack.

The story only became impossible to contain a week later, when recordings of the incident began circulating among local young people. The girl told her mother: “This video is going around everywhere. I was also approached by two girls at the outdoor pool that something had probably happened before.”

She ultimately documented her account across seven handwritten pages for police. The Stade public prosecutor’s office has confirmed to Bild newspaper that the case is a priority, though no outcome is expected for at least two months.

The mother says she has received no support from the church, the youth center, or the local administration. The mayor of Gnarrenburg was reportedly informed that boys had allegedly been arranging such encounters at his municipality’s youth center, yet was unavailable to speak with Bild.

“We’re fighting windmills,” said the mothers.

“The congregation, the church, everyone remains dead silent, as if nothing had happened. Everyone carries on as if nothing happened. Only we as a family will never be able to forget it. It will always accompany us.”

Her decision to go public, she says, was driven by her daughter’s isolation.

“The story is all over the whole village and at the school. My daughter doesn’t go anywhere anymore. I want to give her a sign: you are not to blame.”

The mother continued, saying: “We simply want the alleged perpetrators to receive their just punishment, and most importantly, we want our daughter to be able to walk through the community with her head held high, without feeling ashamed or anything like that.”

The doors to the room where the assault allegedly took place have since been removed from their hinges. In a joint statement to Bild, the mayor and the superintendent of the Bremervörde-Zeven church district said the team had acted correctly at all times based on their knowledge at the time.

Tyler Durden

Tue, 03/24/2026 – 02:00

Israel’s Mossad Promised It Could Ignite Regime Change In Iran: Report

Israel’s Mossad Promised It Could Ignite Regime Change In Iran: Report

Israel’s intelligence agency Mossad had a plan to ignite public protests that would lead to the collapse of Iran’s government, the New York Times has reported.

David Barnea, Mossad’s chief, met with Israeli Prime Minister Benjamin Netanyahu days before the US and Israel began their war on Iran and told him that the agency would be able to galvanize Iranian opposition in order to bring about regime change.

Barnea, according to the report, which cites interviews with US and Israeli officials, also presented this proposal to senior US officials during a visit to Washington in mid-January.

The plan was then taken up by Netanyahu and Trump, despite doubts among some senior American officials and Israeli military intelligence. Mossad’s promises were, according to US and Israeli officials, used by Netanyahu to convince the US president that collapsing the Iranian government was possible.

In the plan’s conception, the war would begin with the killing of Iranian leaders, followed by a “series of intelligence operations intended to encourage regime change.” This could, Mossad believed, lead to a mass uprising that would bring about victory for Israel and the US.

As the war began, Trump’s public messaging reflected this. In an eight-minute video statement he said:

“Finally, to the great, proud people of Iran, I say tonight that the hour of your freedom is at hand…when we are finished, take over your government. It will be yours to take. This will be probably your only chance for generations.”

But talk of regime change quickly evaporated. Less than two weeks in, US senators came out of a briefing on the war to say that overthrowing the Islamic Republic was not one of its goals, and that in fact there was “no plan” at all for the military operation.

Netanyahu frustrated with Mossad

The CIA’s own assessment of the situation is that the Iranian administration will not be overthrown. In fact, the US intelligence agency had said that if Iran’s leaders were killed, a “more radical” leadership would take power.

Israeli intelligence sees Iran’s government as weakened but intact. “The belief that Israel and the United States could help instigate widespread revolt was a foundational flaw in the preparations for a war that has spread across the Middle East,” the NYT report said.

While Netanyahu has remained bullish about the prospect of putting troops on the ground in Iran, he is said to be frustrated that Mossad’s promises to bring about an uprising have not come to fruition.

According to the NYT, Netanyahu said in a security meeting days after the war began that Trump could end the war at any moment if Mossad’s operations did not bear fruit.

Allegations that the White House went in the direction of ‘optimistic’ Israeli assessments over US intelligence consensus:

Another example of that high-value intelligence we get from Israel, I guess. The CIA doubted that a war would quickly lead to a democratic uprising against the Iranian regime. But Israel’s Mossad was optimistic it could spur regime change. Trump listened to the Israelis. https://t.co/knLLHpzSyw

— Andrew Day (@AKDay89) March 23, 2026

Mossad’s promises were, according to the report, disputed by many senior US officials and analysts at the Israeli army’s intelligence agency, Aman.

US military leaders told Trump that Iranians would not take to the streets while bombs were falling, while intelligence officials assessed that the chances of a mass uprising were low.

Tyler Durden

Mon, 03/23/2026 – 23:05

Oil Jumps After Explosion And Massive Fire At One Of The Largest US Oil Refineries

Oil Jumps After Explosion And Massive Fire At One Of The Largest US Oil Refineries

An explosion and large plumes of smoke at the Valero refinery in Port Arthur prompted officials to order west-side residents to shelter in place according to 12 News Now.

🚨 Jefferson Co. Commissioner says “I’m asking people to stay tuned because if this chemical is deemed to be toxic or carcinogenic … then I guarantee we’re going to order to evacuate.” pic.twitter.com/MVpOu5b28M

— Chief Nerd (@TheChiefNerd) March 24, 2026

A fire broke out at a diesel hydrotreater, with the unit suffering severe damage, according to people familiar with the incident. The fire was near the plant’s fluid catalytic cracker, and part of the refinery has been shut down, according to the people, who said a decision hasn’t yet been made whether to shut the entire plant.

A few minor injuries were reported, according to people familiar. A Valero spokesperson said all personnel have been accounted for. Local officials have shut two nearby state highways as a precaution, the spokesperson said.

Footage reportedly shows the effect of a large explosion at the Valero oil refinery in Port Arthur, Texas that resulted in a massive fire. Residents are currently advised by emergency services to shelter in place. pic.twitter.com/50qaqsuVec

— OSINTdefender (@sentdefender) March 24, 2026

Witnesses across the Mid-County area reported hearing a loud boom that rattled car windows. A resident near the scene told a 12News crew the area smelled of rotten eggs, an indication of sulfur in the air.

Antonio Mitchell with the Port Arthur Fire Department confirmed an incident at the Valero facility, though details remained limited. “The type of incident is unknown at this time,” Mitchell said not long after the explosion as his crews headed to the scene.

Following reports of an explosion, a massive fire can be seen at the Valero oil refinery in Port Arthur, Texas. pic.twitter.com/I3UYBTS41A

— OSINTdefender (@sentdefender) March 24, 2026

No injuries have been reported, and no evacuations have been ordered. Officials are monitoring air quality in the area.

Aerial footage shows the massive fire at the Valero refinery in Port Arthur, Texas following an explosion.

IRGC affiliated accounts claim

“Sabotage” pic.twitter.com/HvnQ2wSMEL

— Open Source Intel (@Osint613) March 24, 2026

Interim Port Arthur Fire Chief Louie Havens said two engines were initially sent to the refinery and a hazmat team is being deployed to Valero. Havens also confirmed there have been no injuries or deaths reported. Beaumont Fire Department and the Jefferson County Sheriff’s Office are assisting the Port Arthur Fire Department.

The City of Nederland issued a statement through the Southeast Texas Alerting Network saying its police and fire departments are actively patrolling and conducting air monitoring on the south side of the city.

“At this time, there is no impact to the City of Nederland,” officials said, adding that updates would be provided if conditions change.

The Texas Commission on Environmental Quality said emergency response coordinators and regional staff have been deployed with handheld and mobile air monitoring assets in response to the Valero fire in Port Arthur and are coordinating through incident command. Officials said updates will be shared as they become available.

The Texas Department of Transportation urged drivers to avoid the area, asking motorists to steer clear of SH 87 and SH 82 near the refinery.

The refinery can process 435,000 barrels of heavy sour crude a day, making it one of the top 10 largest refineries in the US.

News of the fire, coupled with fresh reports of hostilities in Iran, sent WTI crude – which earlier in the day dropped as low as $85 – back over $90 and rising.

Which in turn is weighing on equity futures, erasing much of the earlier gains.

Tyler Durden

Mon, 03/23/2026 – 22:39

Working While You’re Collecting Social Security

Working While You’re Collecting Social Security

Authored by Anne Johnson via The Epoch Times (emphasis ours),

Choosing when to collect Social Security retirement benefits is a consequential decision. It will affect your finances for the rest of your life. You’ll be able to claim reduced retirement benefits as early as 62.

In fact, in 2022, nearly 30 percent of new Social Security beneficiaries began receiving benefits at age 62, according to the Bipartisan Policy Center. The full retirement age (FRA) for those born in 1960 or later is 67, according to the Social Security Administration (SSA). Although you can claim the benefits early, there are drawbacks. And one of them relates to any continued employment.

Social Security Earnings Test

You can receive Social Security or survivors’ benefits and work at the same time. But the Social Security earnings test will be applied to you.

According to the SSA, if you start collecting retirement benefits before FRA and earn more than $24,480 in 2026, you will be penalized. The SSA deducts $1 from your benefits for every $2 you earn above $24,480.

If you reach FRA in 2026, the SSA deducts $1 from your benefits for every $3 you earn above $65,160 until the month you reach FRA.

For example, you file for benefits in January 2026, and your payment is $600 monthly, or $7,200 annually. But during 2026, you plan to work and earn $26,080. You will be $1,600 above the limit. The SSA would withhold $800 of your Social Security benefits.

How Do You Pay the Penalty?

If you file for Social Security benefits at 62 in January 2026, and your benefit is $600 a month, or $7,200 per year. During 2026, you plan to work and earn $26,080, which is $1,600 above the limit. The SSA would withhold $800 of your Social Security benefits ($1 for every $2 you earned over the limit).

To do this, they would withhold all $600 benefits in January and all $600 benefits in February to take the $800. Keep in mind that the SSA does not make partial payments. So, they would take all the February benefits. In other words, you would go two months without benefits. But you would receive all your $600 benefit in March.

The SSA would pay you the additional $400 they took from February 2026 back to you in January 2027.

The SSA doesn’t actually know your earnings in advance. They rely on three items: your estimate when you apply; your employer’s wage reports; and your tax return later.

Often, they don’t know you’ve gone over the maximum until the following year. At that point, they would withhold the overage.

First-Year Rule Saves Money

Sometimes, people younger than FRA begin receiving benefits in the middle of the year. At that point, they may have already exceeded the yearly limit.

According to the SSA, under the first-year rule, you can receive full Social Security benefits for any whole month you are retired, and earnings are below the monthly limit. In other words, the limit starts the month you start receiving benefits, not for the prior months when you may have gone over the limit.

So, if you started receiving benefits in July 2026, you must be under the limit from July through December 2026. But you don’t have to be below the limit from January 2026 through June 2026.

This rule allows you to work earlier in the year, retire midyear, and still collect Social Security immediately without losing benefits earned before you started collecting them.

Social Security Refunds Penalties at FRA

Although some of your benefits may be reduced if you work, they will be returned later. According to the SSA, if some of your benefits are withheld because of your earnings, your monthly benefit will increase starting at FRA. It will take into account those months when benefits were withheld.

Earnings Drawback to Collecting Social Security Before FRA

Whether or not you’re working, if you start drawing your Social Security benefits before FRA, you’ll receive less money.

If you start receiving benefits early, your benefits will be reduced by a small percentage for each month before your FRA. According to the SSA, those born in 1960 or later will have their benefits reduced by 30 percent if they retire at 62.

So, if your FRA benefit is $1,000, because of the reduction, you’ll receive $700 if you start benefits at age 62. A spouse’s benefit is reduced by 35 percent, which brings it down to $325, according to the SSA.

How to Contact the Social Security Association

The best and most convenient way to contact the SSA is to visit www.ssa.gov. You’ll be able to use their services and receive information. If you live outside the United States, visit www.ssa.gov/foreign to access online services.

If you don’t have internet access, call 1-800-772-1213 or the TTY number, 1-800-325-0778 if you’re deaf or hard of hearing. They recommend calling between Wednesday and Friday and later in the month when it’s less busy.

Tyler Durden

Mon, 03/23/2026 – 22:15

https://www.zerohedge.com/personal-finance/working-while-youre-collecting-social-security

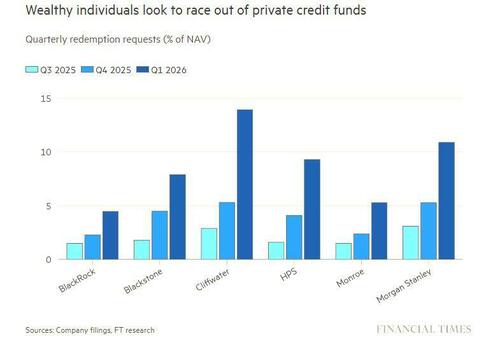

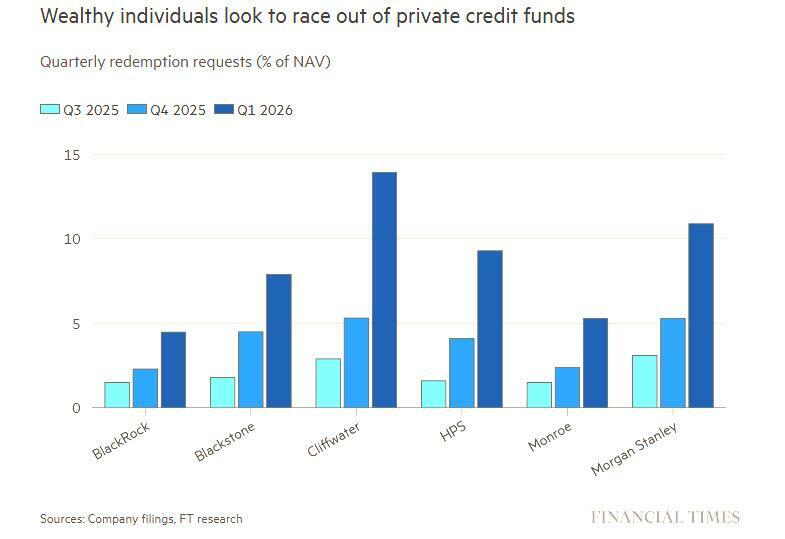

Apollo Private Credit Fund Is Latest To Gate Investors As KKR Fund Gets Junked By Moody’s

Apollo Private Credit Fund Is Latest To Gate Investors As KKR Fund Gets Junked By Moody’s

Amid the ongoing fracturing of the private credit industry, which after enjoying years of stable, levered growth (and when it ran out of institutional greater fools, it aimed lower, toward HNWs and retail) finally hit a brick wall thanks to the Claude-inspired SaaSpocalypse, which has led to a historic surge in redemption requests across the biggest (and certainly smallest) names in the industry, last week we said that debt funds managed by powerhouse firms including Blackstone, BlackRock, Cliffwater, Morgan Stanley and Monroe Capital have agreed to honor only 70% of the $10.1bn of redemption requests they have faced, according to FT calculations, as fund after fund is gating investors.

We also said that the number of both redemptions and gates is expected to spike over the coming weeks, as funds managed by Ares Management, Apollo Global, Blue Owl, Oaktree and Goldman Sachs tally up how many of their investors are heading for the exits, as discussed here.

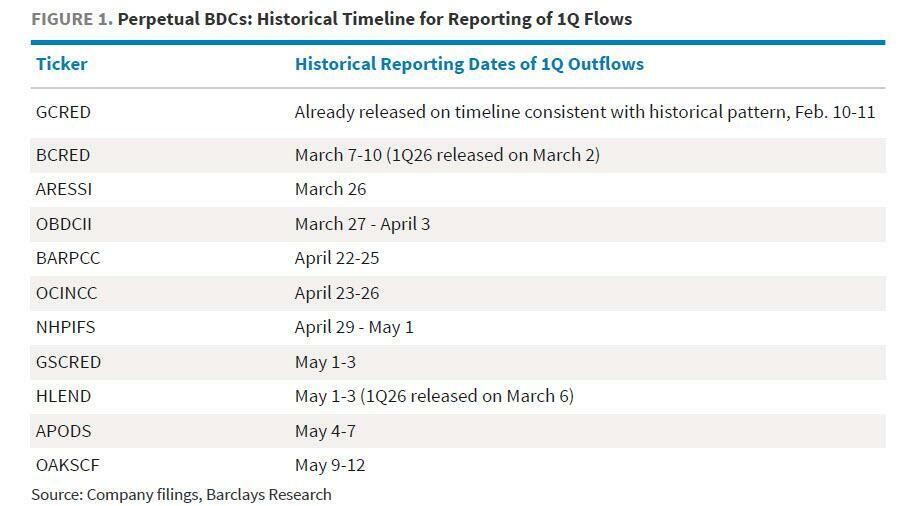

According to the above table, Apollo’s private credit fund, APODS, was supposed to report its Q1 outflow in early May. However, the surge in redemptions was so big the private equity giant decided not to wait that long, and according to Bloomberg, Apollo Global Management has joined a growing number of its peers in gating redemptions from one of its largest non-traded private credit funds for retail investors, becoming the latest alternative asset manager to be flooded by a surge in such requests.

The $25 billion business development company, Apollo Debt Solutions (APODS), capped withdrawals at 5% of outstanding shares Monday after clients sought to redeem 11.2%, according to a shareholder letter seen by Bloomberg, thus gating more than half of the redemption requests.

“Periods of complexity and uncertainty can create some of the most attractive investment opportunities, but only for those with the flexibility to act decisively,” the firm said, adding that “while the market has repriced risk, the fundamentals of the fund’s underlying borrowers remain strong.”

The firm expects the granted redemptions to amount to roughly $730 million of gross outflows for the first quarter, offsetting the roughly $724 million of inflows for the period. Apollo Debt Solutions has been building its reserves in the past month, doubling the size of one credit line to $1 billion and signing a new $500 million facility.

What’s worse is Apollo has effectively pre-gated next quarter’s redemption requests, saying that it intends to stick to the same cap next quarter as it balances “the interests of shareholders seeking liquidity with those who choose to remain invested,” it said in the letter, noting that challenging times can benefit investors in the long run.

With redeeming investors receiving just 45% of their capital, Apollo Debt Solutions is returning less cash to clients than some of its peers that capped withdrawals. As we reported previously, while BlackRock also capped redemptions from its $26 billion non-traded BDC at a pre-set 5% earlier this month, investors had “only” requested 9.3% of their shares. Meanwhile, Morgan Stanley’s North Haven Private Income Fund’s pro-rated redemptions were granted at a similar rate to Apollo’s.

It seems that with every passing week, after Blue Owl started the private credit firesale a month ago, more investors are seeking to return their capital… and more are being gated.

As regular readers are aware, while private credit funds typically limit redemptions to 5% of outstanding shares, the recent bank run redemption scramble among retail investors has tested firms’ flexibility. Some firms such as Blackstone opted to exceed the cap – and fund the shortfall out of the partners’ own pocket – in the hopes of quelling investor panic and stanching further outflows. That valiant effort failed after Blackstone’s peers such as Blackrock, Cliffwater and Morgan Stanley gated their own investors.

Apollo, which has been pushing for more transparency in private markets, also said Monday that Apollo Debt Solutions had returned 1% over the past three months. At the same time, its net asset value dipped by 1.2% over the same period. Last night we reported that the largest private credit fund, Blackstone’s BCRED, reported its first monthly decline since September 2022.

Meanwhile, in related news, late on Monday a private credit fund jointly run by Future Standard and KKR was the first to get junked, losing one of its investment-grade ratings, a rare occurrence in the $1.8 trillion private credit market, and one which will certainly result in higher borrowing costs for the $14 billion investment vehicle.

Moody’s Ratings lowered its assessment of FS KKR Capital Corp. to Ba1, or one level into junk, because of what it described as “continued asset quality challenges” that have hurt profitability and the value of the fund’s portfolio relative to peers, the credit grader said in a statement on Monday.

The fund’s non-accrual rate, which measures soured loans, rose to 5.5% of total investments as of the end of last year, one of the highest percentages among peers. It also expressed concern over other investments not classified as non-accrual that have have suffered significant markdowns, including a loan to software company Medallia.

The rating agency also called out FSK’s higher proportion of payment-in-kind income relative to peers, which it said is a sign of “weaker earnings quality.” PIK provisions allow borrowers to pay interest by accumulating additional debt instead of paying out cash.

That said, the ratings firm said the fund is “well positioned” from a liquidity perspective, with about $2.5 billion available after repaying a $1 billion note earlier this year.

“FSK remains well positioned despite the decision,” a spokesperson for the fund, referring to its stock-exchange ticker, said in an emailed statement. “It has a strong, well‑laddered liability structure with no 2026 unsecured maturities and limited near‑term maturities, enabling us to continue supporting our portfolio companies and navigate the current market environment.”

And now it’s junk.

Tyler Durden

Mon, 03/23/2026 – 21:50

Bovard: The Late Robert Mueller, Bill Of Rights Executioner

Bovard: The Late Robert Mueller, Bill Of Rights Executioner

Obituaries on eminent Washingtonians usually omit the dreadful precedents they set that will vex Americans long after their death. Not this piece.

Former FBI director Robert Mueller died last week at the age of 81. The New York Times eulogized him as a “button-down, lockjawed, rock-ribbed exemplar of a vanishing caste.” In reality, Mueller was simply a twenty-first century version of J. Edgar Hoover, trampling the Constitution and seizing new power on any pretext.

Mueller took over the FBI one week before the 9/11 attacks and he was worse than clueless afterwards. On September 14, 2011, Mueller declared, “The fact that there were a number of individuals that happened to have received training at flight schools here is news, quite obviously. If we had understood that to be the case, we would have—perhaps one could have averted this.” Three days later, Mueller announced, “There were no warning signs that I’m aware of that would indicate this type of operation in the country.” His protestations helped the W. Bush administration railroad the Patriot Act through Congress, vastly expanding the FBI’s prerogatives to vacuum up Americans’ personal information.

Photo by Jim Bovard while covering the 2018 Women’s March in Washington.

Deceit helped capture those intrusive new prerogatives. The Bush administration suppressed until the following May the news that FBI agents in Phoenix and Minneapolis had warned FBI headquarters of suspicious Arabs in flight training programs prior to 9/11. A House-Senate Joint Intelligence Committee analysis concluded that FBI incompetence and negligence “contributed to the United States becoming, in effect, a sanctuary for radical terrorists.” FBI blundering spurred The Wall Street Journal to call for Mueller’s resignation, while a New York Times headline warned: “Lawmakers Say Misstatements Cloud F.B.I. Chief’s Credibility.”

But the FBI was off and running. Thanks to the Patriot Act, the FBI increased by a hundredfold—up to 50,000 a year—the number of National Security Letters (NSLs) it issued to citizens, business, and nonprofit organizations, and recipients were prohibited from disclosing that their data had been raided. NSLs entitle the FBI to seize records that reveal “where a person makes and spends money, with whom he lives and lived before, how much he gambles, what he buys online, what he pawns and borrows, where he travels, how he invests, what he searches for and reads on the Web, and who telephones or e-mails him at home and at work,” The Washington Post noted. The FBI can lasso thousands of people’s records with a single NSL—regardless of the Fourth Amendment’s prohibition of unreasonable warrantless searches.

The FBI greatly understated the number of NSLs it was issuing and denied that abuses had occurred, thereby helping sway Congress to renew the Patriot Act in 2006. The following year, an Inspector General report revealed that FBI agents may have recklessly issued thousands of illegal NSLs. Shortly after that report was released, federal judge Victor Marrero denounced the NSL process as “the legislative equivalent of breaking and entering, with an ominous free pass to the hijacking of constitutional values.”

Rather than arresting FBI agents who broke the law, Mueller created a new FBI Office of Integrity and Compliance. The Electronic Freedom Foundation, after winning lawsuits to garner FBI reports to a federal oversight board, concluded that the FBI may have committed “tens of thousands” of violations of federal law, regulations, or Executive Orders between 2001 and 2008.

President George W. Bush, scorning a unanimous 1972 Supreme Court ruling, decided he was entitled to impose warrantless wiretaps on Americans. At an April 2005 Senate hearing, Senator Barbara Mikulski (D-MD) asked Mueller, “Can the National Security Agency, the great electronic snooper, spy on the American people?” Mueller replied, “I would say generally, they are not allowed to spy or to gather information on American citizens.”

Mueller presumably knew his answer was at least misleading if not blatantly deceptive. Nearly nine months later, The New York Times revealed that Bush had unleashed NSA to illegally wiretap up to five hundred people within the United States at any given time and peruse millions of other Americans’ emails. Attorney General Alberto Gonzales responded to the uproar by asserting that “the president has the inherent authority” to order such wiretaps. Mueller had no trouble with that dictatorial doctrine—even though the same claim spurred one of the articles of impeachment crafted against President Richard Nixon.

Mueller’s biggest coup against privacy occurred with Section 215 of the Patriot Act, which entitles the FBI to demand “business records” that are “relevant” to a terrorism or espionage investigation. In 2011 testimony to the Senate Intelligence Committee, Mueller “suggested the FBI interpreted (Section 215) narrowly and used it sparingly,” the ACLU noted. But Mueller was the point man for the Bush administration’s bizarre 2006 decision (perpetuated by Barack Obama) that all Americans’ telephone records were “relevant” to terrorism investigations. Several times a year, Mueller signed orders to the Foreign Intelligence Surveillance Court, swaying it to continually renew its order compelling telephone companies to deliver all their calling records (including time, duration, and location of calls) to the National Security Agency.

On June 5, 2013, leaks from former NSA contractor Edward Snowden blew the lid off this surveillance regime. Federal judge Richard Leon slammed that records roundup as “almost Orwellian…I cannot imagine a more indiscriminate and arbitrary invasion than this systematic and high-tech collection and retention of personal data on virtually every single citizen for purposes of querying and analyzing it without prior judicial approval.”

Mueller sought to dampen the Snowden uproar by testifying to Congress that the feds could not listen to Americans’ calls without a warrant for that “particular phone and that particular individual.” But NSA employees had broad discretion to vacuum up Americans’ info without warrants, and NSA’s definition of terrorist suspect was so ludicrously broad that it includes “someone searching the web for suspicious stuff.”

Mueller was replaced at the FBI by James Comey. After Comey was fired in May 2017 by President Donald Trump, Comey leaked official memos with confidential information to a lawyer who delivered them to The New York Times. Comey’s leak triggered the appointment of Special Counsel Robert Mueller to investigate Trump. Mueller’s investigation generated endless allegations and controversies and helped Democrats capture control of the U.S. House of Representatives in 2018. In April 2019, after two years of media frenzies, Mueller finally admitted he found no evidence to prosecute Trump or his campaign officials for colluding with Russia in the 2016 campaign. In July 2019, Mueller testified to Congress on his investigation and the nation was shocked to see Mueller looking mentally clueless time and again under questioning.

It remains to be seen whether the media can restore Mueller’s halo after his death. But whitewashing Mueller’s record will simply invite more FBI depredations of Americans’ rights and liberties.

Tyler Durden

Mon, 03/23/2026 – 21:25

https://www.zerohedge.com/political/bovard-late-robert-mueller-bill-rights-executioner

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}