Category: News

Vance Claims Iran Could Make Nuclear Suicide Vest

Vance Claims Iran Could Make Nuclear Suicide Vest

Authored by Dave DeCamp via AntiWar.com,

Vice President JD Vance on Thursday attempted to justify the continued US-Israeli war against Iran by implying that Iran could potentially turn a nuclear bomb into a suicide vest, a claim not grounded in reality.

Vance made the claim during a cabinet meeting while discussing military and diplomatic “options” that the US has regarding the conflict with Iran. He has continued to portray the war as being necessary to prevent Iran from making a nuclear weapon, though there was no evidence that Tehran had decided to build a bomb either before the June 2025 war or the current war that was launched on February 28.

File, illustrative: The Kansas City Star

“What we have now that we didn’t have when the president took over, just a little over a year ago, is the ability to use every tool at our disposal to ensure that Iran doesn’t get a nuclear weapon,” Vance said.

“Because when I say options, I think it’s important the American people know options for what? And it’s options to ensure that Iran never has a nuclear weapon,” the vice president added.

“You talk about people who walk into a crowded supermarket and have a vest on, and they blow up the vest and a couple of people get killed, and that’s a terrible tragedy. What happens when what’s on the vest is not something that can kill a couple of people, but can kill many, many tens of thousands of people?”

A nuclear bomb could not be miniaturized to the point where it could be worn as a vest, and if Vance was alluding to a “dirty bomb” that uses some nuclear material, such a weapon at that size would not cause tens of thousands of casualties (and likely in the ‘dirty bomb’ scenario the wearer would die or become incapacitated from the radiation).

Plus, in recent decades, the overwhelming majority of suicide bombings in the region were carried out by Sunni Muslim extremists, not Iran and its Shia allies.

Vance suggests Iran could have used nuclear suicide vests: “You talk about people who walk into a crowded supermarket and have a vest on, and they blow up the vest and a couple of people get killed, and that’s a terrible tragedy. What happens when what’s on the vest is not… pic.twitter.com/6HiCHhi4S9

— The Bulwark (@BulwarkOnline) March 26, 2026

Before the US and Israel launched the war, Vance became one of the leading voices in the administration, making the claim that the coming conflict was about preventing Iran from developing a nuclear bomb, contradicting President Trump’s insistence that US airstrikes in June 2025 “obliterated” Iran’s nuclear program.

At one point, Vance even claimed there was evidence Iran was trying to “rebuild a nuclear weapon,” something Iran has never had.

Tyler Durden

Fri, 03/27/2026 – 21:25

https://www.zerohedge.com/political/vance-claims-iran-could-make-nuclear-suicide-vest

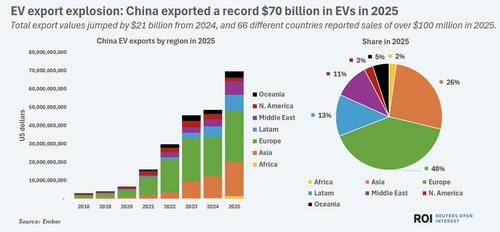

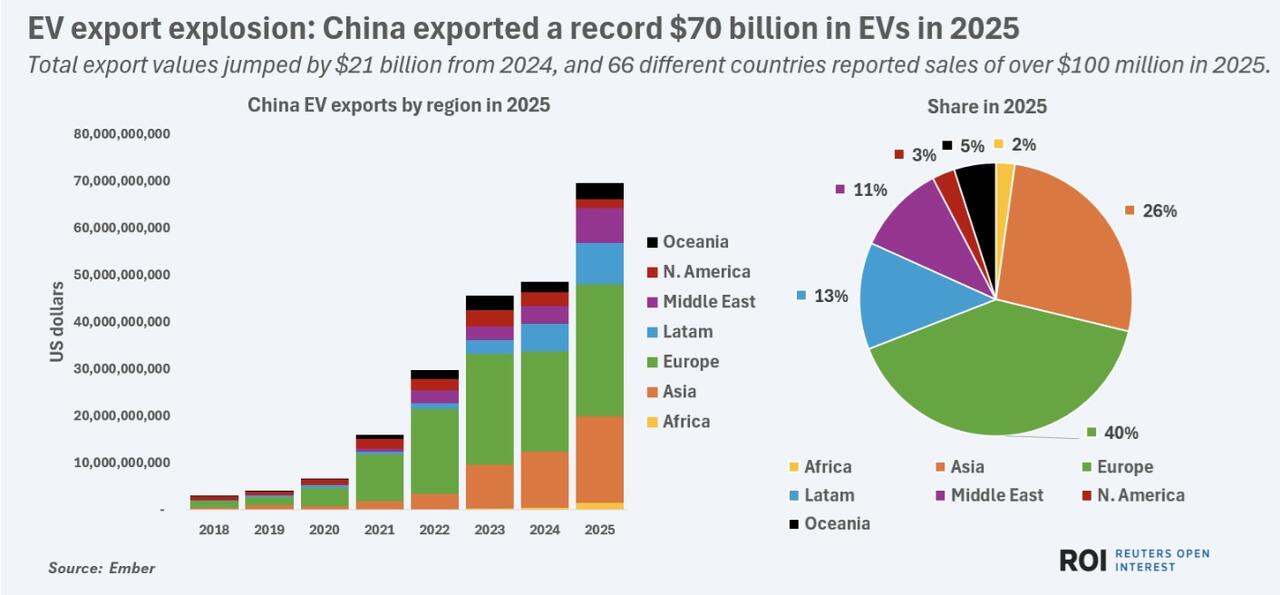

Americans Are Becoming More And More Interested In Buying Chinese EVs

Americans Are Becoming More And More Interested In Buying Chinese EVs

As electric vehicle (EV) adoption grows in the United States, a segment of American consumers is increasingly drawn to Chinese-made models—largely due to their affordability, advanced technology, and feature-rich designs. However, steep trade barriers and political resistance continue to keep these vehicles out of the U.S. market, according to Reuters.

With the average price of a new car in the U.S. մոտ $50,000, Chinese EVs—many of which sell for under $30,000 in international markets—are gaining attention for offering strong value. Models from automakers such as BYD, Geely, and Zeekr often include premium interiors, advanced driver-assistance systems, and unique features like in-car entertainment and mini refrigerators, typically found in higher-end vehicles.

Reuters writes that industry experts note that Chinese automakers have rapidly improved both quality and innovation. China has recently surpassed Japan to become the world’s largest vehicle exporter, with growing sales across Europe, Latin America, and parts of North America. Countries such as Canada and Mexico have already begun integrating Chinese EVs into their markets at lower tariff rates.

In contrast, the United States has imposed tariffs exceeding 100% on Chinese vehicles, effectively blocking their entry. Policymakers cite concerns over data security, regulatory compliance, and the potential impact on domestic manufacturing jobs. Major U.S. auto industry groups have also urged continued restrictions, arguing that domestic automakers could face significant competitive pressure.

Despite these barriers, consumer curiosity remains strong. Surveys indicate that nearly half of prospective U.S. car buyers view Chinese vehicles as offering high value, and a notable share support allowing them into the domestic market. At the same time, concerns persist around safety standards, data privacy, and broader economic implications.

Auto dealers remain cautious. While many acknowledge that competitively priced Chinese EVs could attract buyers, only a small percentage currently support their introduction, citing uncertainty over compliance with U.S. regulations and market disruption.

For now, Chinese EVs remain largely absent from American roads. Yet as global competition intensifies and affordability becomes a growing concern for consumers, pressure may continue to build for greater access to lower-cost electric vehicles in the U.S. market.

* * * Be Prepared

Tyler Durden

Fri, 03/27/2026 – 21:00

https://www.zerohedge.com/markets/americans-are-becoming-more-and-more-interested-buying-chinese-evs

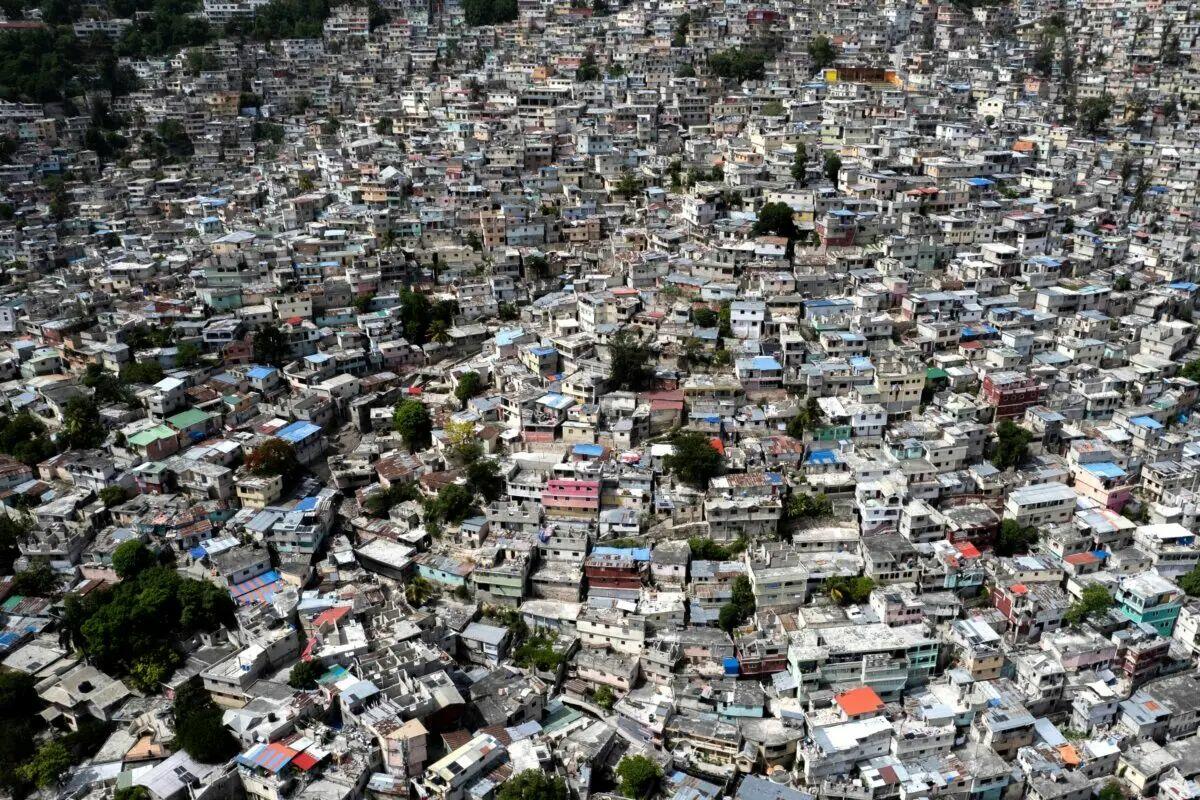

US Offers Up To $3 Million Bounty For Information On Finances Of Haitian Gangs

US Offers Up To $3 Million Bounty For Information On Finances Of Haitian Gangs

Authored by Kimberly Hayek via The Epoch Times (emphasis ours),

The U.S. government on March 25 announced a bounty of up to $3 million for information on the finances of Haiti’s Viv Ansanm and Gran Grif gangs.

The United States designated both groups, which bring together hundreds of gangs in the capital Port-au-Prince, the agricultural Artibonite region, and central Haiti, as terrorist organizations in May 2025.

The two gangs are a “primary source of instability and violence in Haiti” and are a “direct threat to U.S. national security interests in our region,” Secretary of State Marco Rubio said at the time, adding that they are “committed to overthrowing the government of Haiti.”

Gangs have grown in power since the assassination of President Jovenel Moïse in 2021. They are estimated to control about 90 percent of the capital, Port-au-Prince, according to a 2025 U.N. security briefing, and have expanded their activities into the countryside, including looting, kidnapping, sexual assaults, and rape. Haiti has not had a president since the assassination.

The U.S. Embassy in Haiti said in a March 25 statement that Viv Ansanm members are “responsible for an ongoing campaign of violence, including attacks against the government of Haiti, prison systems, police stations, hospitals, and the nation’s main airport in Port-au-Prince,” while Viv Ansanm is “directly involved in the mass murder and collective rape of Haitian civilians, including violence against American citizens in Haiti.”

Haitian security forces, with the support of a partially deployed U.N.-backed force and a U.S. private military company, have intensified attacks on armed gangs that control most of the capital, but have yet to make a major gang leader’s arrest.

Even if gang members are arrested, Haiti’s judicial system is barely functional. A 2024 U.N. report found that “many courthouses remain destroyed, non-operational, or located in inaccessible areas, effectively barring judicial personnel and lawyers from accessing them.”

More than a million people have been displaced by the conflict with gangs, which has exacerbated food insecurity, and close to 20,000 have been reported killed in Haiti since 2021. The death toll has climbed every year.

According to a Mercy Corps survey published this month, which surveyed thousands of displaced people across the capital Port-au-Prince, 99 percent had no job or income after being displaced, and 95 percent felt unsafe in their new lodgings.

An overview of Port-au-Prince, Haiti, on June 3, 2025. Clarens Siffroy/AFP via Getty Images

Less than half had access to a functioning toilet, and the vast majority were eating fewer than two meals a day. Just a third of children were attending school, and a third of women said they had suffered physical or sexual violence at the displacement site, the report found.

The United Nations estimated that 1.45 million people were internally displaced across Haiti by the end of last year, with more than 400,000 displaced in the past year alone.

Reuters and The Associated Press contributed to this report.

* * * Nighty night

Tyler Durden

Fri, 03/27/2026 – 20:35

https://www.zerohedge.com/geopolitical/us-offers-3-million-bounty-information-finances-haitian-gangs

Moore Problems? Maryland Gov. Wes Moore Booed At Baltimore Stadium In Deep-Blue Territory

Moore Problems? Maryland Gov. Wes Moore Booed At Baltimore Stadium In Deep-Blue Territory

Left-wing Maryland Gov. Wes Moore was greeted Thursday afternoon by a stadium full of boos at Camden Yards on Opening Day for Orioles baseball, a striking public rebuke of the struggling governor and the one-party rule of Democratic Party kings and queens running the state into the ground.

Gov. Wes Moore was booed by the crowd ahead of the Orioles home opener on Thursday. https://t.co/KdJaF2jx68 pic.twitter.com/pA0p6G2z8m

— FOX Baltimore (@FOXBaltimore) March 26, 2026

After years of fiscal mismanagement, Annapolis Democrats have driven Maryland into a fiscal crisis, compounded by the death spiral of higher taxes and backfiring green energy policies that are now colliding with surging data-center power demand across the region, sparking a power bill crisis for Marylanders.

The end result of this epic mismanagement is extraordinarily sad: a growing exodus of residents, with net migration trends turning negative for the state as people flee to places where common sense is prioritized, not state-ruining far-left experiments.

One notable observation about the boos is that they occurred at Camden Yards in Baltimore City, which is controlled by a crazed left-wing mayor in a deeply blue city. In fact, the boos should never have been heard there, but among voters in the state, left or right, the cost-of-living crisis sparked by out-of-control taxes and state-ruining progressive policies is crushing pocketbooks everywhere.

Let’s remind readers that Gov. Moore has been positioned by the Democratic Party machine as a possible nominee in 2028.

Moore smiling with far-left radical Alex Soros.

However, Polymarket odds show his chances of securing the nomination at just 2%, and for good reason: the endless mismanagement of the state is a massive liability on the national stage.

On Friday morning, Republican Del. Matt Morgan joined local outlet Fox 45 Morning News to discuss the boos at Camden Yards. He said the crowd at the stadium was upwards of 40,000 people and nonpartisan.

Morgan said, referring to the boos, “It was basically a state poll that told you Marylanders are fed up with the policies coming out of Annapolis and the Moore administration.”

Earlier this week, on the two-year anniversary of the catastrophic collapse of the Francis Scott Key Bridge at the Port of Baltimore, there is still no bridge, while Democrats in recent days prioritized “appropriately sized tampons” for men’s bathrooms.

Maryland Delegate Kathy Szeliga (R) EMBARESSES Democrats who want to force “appropriately sized tampons” into men’s bathrooms.

Szeliga: “I’ve never heard of such a thing… what do you consider appropriate???”pic.twitter.com/jjasHIMtRE https://t.co/gsjXEzXVre

— Libs of TikTok (@libsoftiktok) March 24, 2026

Baltimore City is broken. Maryland is broken. Democrats broke the state. Moore’s aspirations for 2028 have imploded. Perhaps he can work on his golf swing at the local elite golf clubs he frequents in Baltimore.

Tyler Durden

Fri, 03/27/2026 – 20:10

$100 Oil Is Solving Russia’s Budget Problem

$100 Oil Is Solving Russia’s Budget Problem

Submitted by Charles Kennedy of OilPrice.com

Russia is getting an unexpected windfall from the war in the Middle East. The Kremlin’s oil revenues this month hit a four-year high as oil prices jumped to $100 per barrel amid the Iran war and the de facto closed Strait of Hormuz.

Moscow expects so much additional revenues from the oil price spike that authorities are unlikely to downgrade Russia’s economic prospects, hold off on planned budget cuts, and even boost military spending on the war in Ukraine, Bloomberg reports, citing sources with knowledge of the matter.

A month ago, Russia was considering lowering the oil price level above which it sends the proceeds to its wealth fund as oil and gas revenues were plummeting with widening discounts and key Russian buyers like India pulling out of the spot market.

But the Middle East war and the worst disruption in the history of the global oil market pushed oil prices above $100 per barrel and prompted the United States to give buyers a free pass on Russian oil purchases.

As a result, the price of Urals, Russia’s flagship crude, has now nearly doubled to about $100 per barrel as demand for Russian oil in India is soaring again.

The oil price spike has already given Russia a reason to postpone the planned budget tightening.

Moscow has now scrapped plans to make a substantial downgrade to its economic growth forecast for 2026, according to Bloomberg’s sources.

Russian oil revenues have steadily increased in March, thanks to higher shipments and soaring oil prices, according to tanker-tracking data monitored by Bloomberg. In two of the weeks this month, Russia was estimated to cash in the highest amounts of oil revenues since 2022, just after its invasion of Ukraine drove prices above $100 per barrel.

Russia is cashing in on the Iran war even as it cannot take full advantage of the oil price spike as Ukraine targets its key Baltic Sea ports in an attempt to undermine Moscow’s oil export capabilities.

Tyler Durden

Fri, 03/27/2026 – 19:45

https://www.zerohedge.com/markets/100-oil-solving-russias-budget-problem

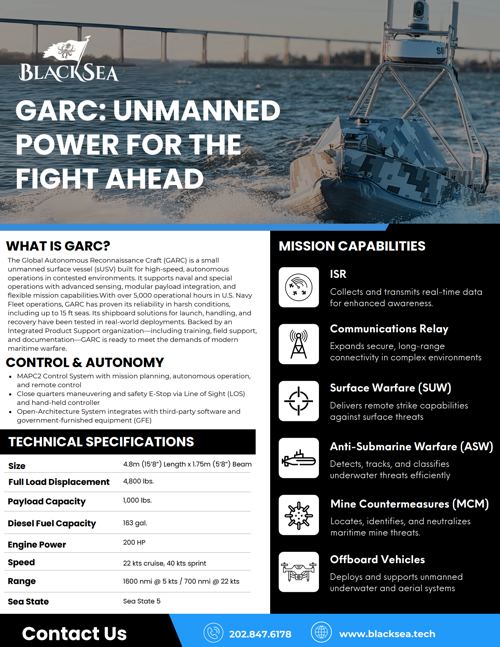

US Deploys Ukrainian-Style Drone Boat In Iran War As AI Weapons Race Accelerates

US Deploys Ukrainian-Style Drone Boat In Iran War As AI Weapons Race Accelerates

The Department of War confirmed to Reuters that it deployed Ukrainian-style drone boats to the Middle East as part of Operation Epic Fury against Iran. This move signals that the DoW is quickly learning a major lesson from the four-year Russia-Ukraine war: inexpensive autonomous systems, from drone boats to kamikaze drones, are necessary and are becoming core assets (very cheap) on the modern battlefield.

Tim Hawkins, a DoW spokesperson for Central Command, told the outlet that the drone boats deployed in the operation were built by Baltimore-based BlackSea and are known as the Global Autonomous Reconnaissance Craft, or GARC. He said the drone boats are being used for reconnaissance missions.

“U.S. forces continue to employ unmanned systems in the Middle East region, including surface drone assets like the GARC. This platform, in particular, has successfully logged over 450 underway hours and more than 2,200 nautical miles during maritime patrols in support of Operation Epic Fury,” Hawkins said.

BlackSea’s high-speed drone boat is described as a modular, autonomous, and remotely operated USV (unmanned surface vehicle) built for missions such as ISR (Intelligence, Surveillance, and Reconnaissance), communications relay, mine countermeasures, survey, interdiction, and potentially strike roles.

The DoW’s push for inexpensive, scalable autonomous air, ground, and maritime systems has only been reinforced by Operation Epic Fury and appears to take a page from Ukraine’s playbook in its war of attrition against Russia, where FPVs and killer ground bots have dominated ‘no man’s land.’

In addition to drone boats, U.S. forces have deployed kamikaze drones based on the Iranian Shahed-136 attack drone – yet another acknowledgment by the DoW that autonomous systems are the future of warfare.

None of this should surprise readers, as we have outlined how four years of rapid development in war technology across Ukraine, Russia, and China have provided a glimpse of 2030s warfare.

AI’ Kill Chains’ And Rise Of Skynet-Like Weapons Offer Glimpse Of 2030s Battlefield

Latest snapshot of the two wars across Eurasia: we overlaid natural gas pipelines on the map.

Next up are humanoid robots as physical AI on the battlefield.

* * *

Grab our favorite knife. Hand-made in the USA.

Tyler Durden

Fri, 03/27/2026 – 19:20

Louisville Shells Out $800,000 For Unconstitutional Demands On Christian Photographer

Louisville Shells Out $800,000 For Unconstitutional Demands On Christian Photographer

The city of Louisville, Kentucky, has agreed to pay $800,000 in attorney fees to settle a case with a Christian photographer who fought to protect her religious and free speech rights over the years of litigation.

Louisville ultimately spent a fortune to force Chelsey Nelson to photograph same sex marriages under its nondiscrimination laws.

When combined with its own litigation costs, the case likely cost the city and the courts millions to deny Nelson her constitutional rights.

In prior columns, academic articles, and my book, “The Indispensable Right, I discussed the never-ending litigation targeting Jack Phillips, the Christian baker who declined to make cakes that violated his religious beliefs.

The case went all the way to the Supreme Court in what many of us hoped would be a final resolution of this conflict.

I had long criticized the framing of the case (and other cases) under the religious clauses rather than treating it as a matter of free speech.

In the end, the Supreme Court punted in a maddening 2018 decision that technically ruled in favor of Phillips based on a finding that the Commission showed anti-religious bias against Phillips.

In 2023, the Supreme Court delivered a major victory for free speech in 303 Creative v. Elenis, when it ruled that Lorie Smith, a Christian website designer, could refuse to provide services for a same-sex marriage.

Justice Neil Gorsuch wrote, “the framers designed the Free Speech Clause of the First Amendment to protect the ‘freedom to think as you will and to speak as you think.’ … They did so because they saw the freedom of speech ‘both as an end and as a means.’”

In the September ruling, the court cited 303 Creative:

“That 2023 decision confirmed this Court’s 2022 interpretation of the First Amendment to bar the City of Louisville from enforcing an ordinance prohibiting wedding photographer Chelsey Nelson from stating her traditional (now dissenting) views on traditional marriage or declining to participate in those ceremonies.”

Louisville is only the latest blue city to spend millions trying to force individuals to create products — from cakes to wedding albums — that violate their religious, speech, and associational rights.

The settlement is a victory not just for Nelson but also for the Alliance Defending Freedom.

Tyler Durden

Fri, 03/27/2026 – 18:55

After Putin’s Guarded Iran War Comments, Medvedev Enters The Chat

After Putin’s Guarded Iran War Comments, Medvedev Enters The Chat

Earlier this week President Putin weighed in on America’s Iran operations, and as we detailed his comments were predictably a bit guarded. He had compared the war and the Hormuz Strait closure – and subsequent impact on global energy – to the massive widescale impact of the Covid-19 pandemic. But fundamentally he highlighted the “unpredictable” nature of the conflict in terms of where it’s headed, as Washington appears to be searching for an offramp on its terms.

On Friday Dmitry Medvedev weighed in, and as expected the former Russian president and current Deputy Chairman of the Security Council was much less guarded in his assessment. He warned at a moment thousands of US Marines and Airborne troop are en route to the Middle East that if the US enters a ground war in Iran it will be another “Vietnam”.

American boots on the ground so far from US shores “threatens roughly the same consequences as what happened in Vietnam,” Medvedev said as quotes in NBC and others.

“When Washington intervened in a foreign country, located a thousand miles away, and for ten years was unable to find a dignified way out of this conflict,” he told the state-run RIA news agency.

He added that a potential ground operation in Iran would have “fatal consequences” for the broader region and for all involved in the war.

Size comparison: Vietnam overlaying Iran

The White House has been insistent that Trump’s Iran “excursion” is not a quagmire. It has especially been Pentagon chief Pete Hegseth who has repeatedly denied that this conflict can be comparable to the start of ‘forever wars’ in Iraq and Afghanistan.

But clearly the US doesn’t have good track record when its forces must endure extended asymmetric warfare and insurgency conditions. Yet that’s exactly where things will likely head if the White House introduces ground forces.

Iran’s Foreign Minister Abbas Araghchi has actually seized on this historic theme as well, earlier writing on X: “Americans haven’t forgotten how (in 1967), even as hundreds of U.S. soldiers were dying in Vietnam, and the outcome was already clear, General William Westmoreland was flown home to reassure everyone that the war was going well – that the U.S. was ‘winning’.”

“The media haven’t forgotten either; those briefings full of fantasy from the frontlines became infamous as the ‘Five O’Clock Follies’,” he said. The “same script, different stage” is now unfolding, Araghchi insisted, adding: “Hegseth steps up, and the message is still detached from reality.”

* * * CHECK IT OUT

Spring Sale – Readywise

Anza – limited edition knives & mini shanks

Protein – your daily usual + peptides

Tyler Durden

Fri, 03/27/2026 – 18:30

https://www.zerohedge.com/geopolitical/after-putins-guarded-iran-war-comments-medvedev-enters-chat

Trump To Put His Signature On US Dollar Bills, Breaking Tradition Since 1861

Trump To Put His Signature On US Dollar Bills, Breaking Tradition Since 1861

Authored by Brian Quarmby via CoinTelegraph.com,

US President Donald Trump is set to become the first sitting president in history to have his signature put on US paper currency.

In an announcement on Thursday, the US Department of the Treasury said the move would mark the 250th anniversary of the US.

It will put both Trump and Treasury Secretary Scott Bessent’s signatures on future US notes.

“There is no more powerful way to recognize the historic achievements of our great country and President Donald J. Trump than U.S. dollar bills bearing his name, and it is only appropriate that this historic currency be issued at the Semiquincentennial,” Bessent said.

Until now, the tradition has been to put the signatures of the treasurer and the Treasury secretary on US paper currency.

This move would mark the first time in history that a sitting president is placing his signature on US currency.

Source: Brandon Beach

According to a report from Reuters on Thursday, the first $100 bills with Trump and Bessent’s signatures will be printed in June, with other bills following in later months.

Trump’s name and likeness have also made their way to cryptocurrencies, famous landmarks and commemorative coins.

Alongside the Treasury’s plans to put Trump’s signature on US notes, there are also potentially $1 coins with the president’s face on them that could enter circulation as part of the US’s 250th anniversary.

In late 2025, the US Mint released three proposed designs bearing Trump’s face and the caption “In God We Trust.”

Proposed $1 coin designs. Source: US Mint

Trump has also helped oversee the renaming of major US landmarks such as the John F. Kennedy Center for the Performing Arts.

The board of the Kennedy Center, reportedly filled with Trump appointees, voted in late December to change the name to the “Donald J. Trump and the John F. Kennedy Memorial Center for the Performing Arts.”

This has prompted pushback, however, with lawmakers arguing that the move is illegal when done without authorization from Congress.

In the crypto world, Trump has a memecoin named after himself and he has also released multiple NFT projects, including the Trump Digital Trading Cards.

Tyler Durden

Fri, 03/27/2026 – 18:05

https://www.zerohedge.com/political/trump-put-his-signature-us-dollar-bills-breaking-tradition-1861

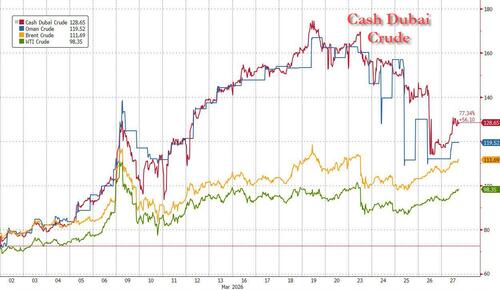

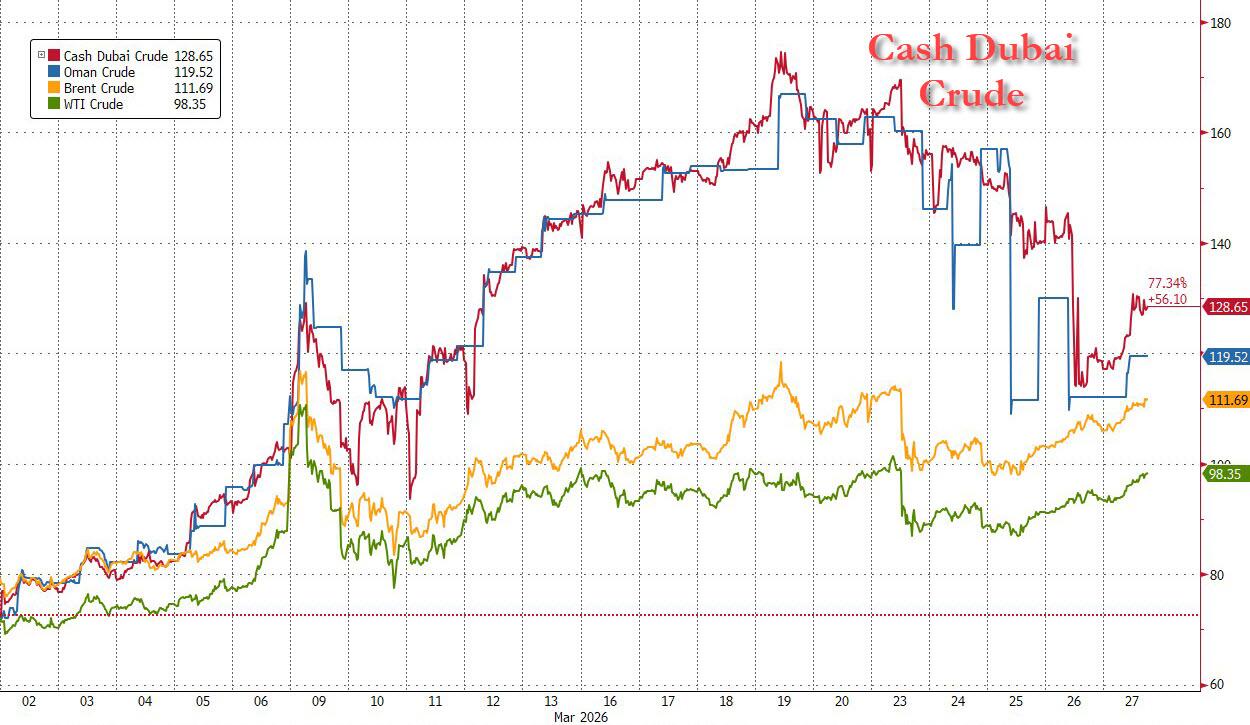

Asia Begins Pricing US Oil Against Brent As Dubai Volatility Spikes

Asia Begins Pricing US Oil Against Brent As Dubai Volatility Spikes

Submitted by Michael Kern of OilPrice.com

Asian refiners have started pricing their orders for U.S. crude oil against the ICE Brent benchmark instead of the typical pricing on Dubai crude, as the Middle Eastern benchmark has seen wild fluctuations amid choked physical supply from the Persian Gulf.

Dubai crude prices soared last week to an all-time high of $169.75 per barrel, and were around $130 a barrel early on Friday.

These highly volatile prices and the uncertainty about supply from the Middle East have prompted refiners in Asia to seek pricing against Brent, instead of the Dubai benchmark which has traditionally been the marker dictating the price of imports into the world’s top crude-importing region.

Some Japanese refiners have already bought U.S. crude cargoes for delivery in July priced against ICE Brent, sources at trading and refining firms told Reuters on Friday. Taiyo Oil, for example, has purchased 2 million barrels of U.S. light crude via a tender at a premium of $19 per barrel over ICE Brent for July delivery, according to Reuters’ sources. Taiyo Oil usually buys U.S. West Texas Intermediate crude priced against the Dubai benchmark.

The major shift in Asian pricing shows the market’s unwillingness to price trades against Dubai crude, whose prices have been severely distorted in recent weeks due to the major physical supply disruptions with the de facto closure of the Strait of Hormuz.

Asian refiners are also forced to pay massive premiums for non-Middle Eastern crude, especially for the sour variety suitable for Asian refineries geared to process the sulfur crude from the Persian Gulf. The most suitable grade from Norway, Johan Sverdrup, was being bid last week at record-high double-digit premiums over Dated Brent.

Refiners in Asia are also cutting processing rates due to a lack of crude, fuel prices are skyrocketing, and governments are implementing fuel-saving measures such as four-day work weeks, work from home, and extended national holidays. Many Asian countries are also banning exports of fuels, which ripples through the global fuel supply, especially in jet and diesel markets.

Tyler Durden

Fri, 03/27/2026 – 17:15

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}