Category: News

Democrats Ask Judge To Block Parts Of Trump’s Election Order

Democrats Ask Judge To Block Parts Of Trump’s Election Order

Authored by Kimberley Hayek and Matthew Vadum via The Epoch Times,

Democrats asked a federal judge Wednesday to block parts of President Donald Trump’s executive order on federal elections.

The lawsuit challenges Trump’s directive, signed a day earlier, that will create a list of eligible voters in every state and prohibit the U.S. Postal Service (USPS) from sending absentee ballots to those not included on the list. The order, titled “Ensuring Citizenship Verification and Integrity in Federal Elections,” directs the Department of Homeland Security and Social Security Administration to conduct voter information collection.

Trump said the executive order was needed because “the cheating on mail-in voting is legendary. It’s horrible what has been going on.”

“The right to vote in Federal elections is reserved exclusively for citizens of the United States under the Constitution and Federal law,” the order reads. “The Federal Government has an unavoidable duty under Article II of the Constitution of the United States to enforce Federal law, which includes preventing violations of Federal criminal law and maintaining public confidence in election outcomes.”

Trump signed the order after Congress recently failed to pass the SAVE America Act, which would have imposed voter ID and election integrity requirements. Administration officials described the order as a necessary step to restore public confidence ahead of the midterm elections in November.

White House staff secretary Will Scharf said the provisions in the order would prevent past problems from being repeated.

“We believe, combined, the measures in this order will help secure elections in the future and ensure the many abuses of our elections in the past are not repeated in future elections,” Scharf said.

Commerce Secretary Howard Lutnick echoed the goal.

“The fundamentals of our democracy are built on voter integrity,” he said during a signing ceremony.

The order reiterates that only U.S. citizens are eligible to vote by mail, and that to enforce the relevant federal statutes, lists of voters are to be verified by the Department of Homeland Security in coordination with the Social Security Administration, “consistent with applicable law, including but not limited to the Privacy Act of 1974.”

The order directs USPS to send ballots only to verified individuals included in the lists, with unique bar codes applied to each envelope—one per voter—to facilitate tracking and audits.

The U.S. attorney general and the heads of various executive departments and agencies were directed to take steps to deter and address noncompliance with federal law by taking steps such as withholding federal funds from noncompliant state and local governments. Evidence that state or local election officials or other individuals of entities have violated existing federal laws is to be referred to the Department of Justice for investigation, the order said.

The Democratic Party campaign organizations that filed the lawsuit contend the order exceeds presidential authority and disrupts state election processes. They seek an immediate injunction to halt enforcement of parts of the order.

The legal complaint states that Trump “has tried again and again to rewrite election rules for his own perceived partisan advantage,” and that he wants to ban mail voting, “a favorite scapegoat for his 2020 electoral defeat,” and impose other restrictions on voting.

The executive order “dramatically restricts the ability of Americans to vote by mail, impinging on traditional state authority,” largely by requiring the USPS “to take actions unrelated to the agency’s statutory mandate that run roughshod over established protections for voters who rely on the mail to exercise their fundamental right to vote.”

This instruction violates the Administrative Procedure Act and the Privacy Act, which require agencies to follow existing law and forbid the use of federal records unless previously authorized under federal law, the complaint says.

The order would unlawfully take steps to create a “national citizenship registry” and require that “state citizenship lists” be shared with states within 60 days of each federal election, the complaint says.

The plaintiffs in this case—the Democratic Senatorial Campaign Committee, the Democratic Congressional Campaign Committee, the Democratic National Committee, the Democratic Governors Association, and the Democratic leaders of the U.S. House and Senate—urged the U.S. District Court in the nation’s capital to act quickly because federal elections are soon approaching.

The plaintiffs asked the court to block the sections of the executive order that mandate the creation of state citizenship lists and require the USPS to establish uniform standards for mail-in or absentee ballots. They also asked the court to block the parts of the order requiring the Department of Homeland Security, the Social Security Administration, and the USPS to coordinate with the Department of Commerce.

Democratic leaders reacted sharply to the executive order. Sen. Alex Padilla (D-Calif.) called the order “a blatant, unconstitutional abuse of power.”

California Gov. Gavin Newsom, a Democrat, vowed to sue over the order.

“The President wants to limit which Americans can participate in our democracy,” Newsom’s press office wrote on Tuesday on X. “California will see him in court.”

When signing the order, Trump said he anticipated legal challenges.

“I don’t know how it could be challenged. It could probably be challenged if you find a rogue judge,” he said. “We will appeal if it is, but I don’t see how anyone else could challenge it.”

Tyler Durden

Thu, 04/02/2026 – 08:46

https://www.zerohedge.com/political/democrats-ask-judge-block-parts-trumps-election-order

‘No Hire, No Fire’ Economy Continues As Job Cuts Tumble, Claims Near Record Lows

‘No Hire, No Fire’ Economy Continues As Job Cuts Tumble, Claims Near Record Lows

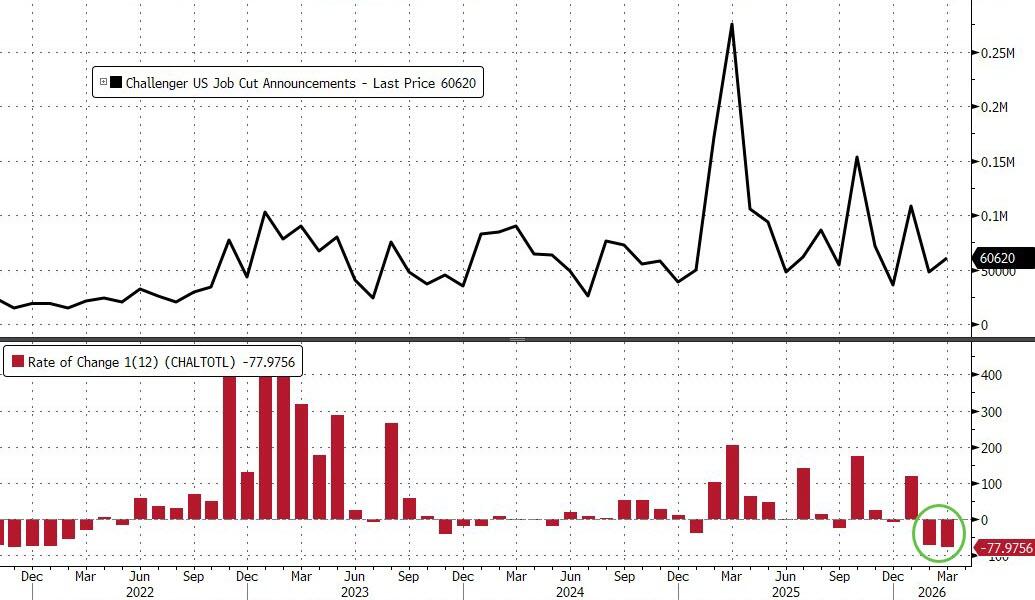

U.S.-based employers announced 60,620 job cuts in March, up 25% from 48,307 cuts announced in February.

It is down 78% from the 275,240 cuts announced during the same month last year, according to a report released Thursday from global outplacement and executive coaching firm Challenger, Gray & Christmas.

“Removing the wave of federal layoffs announced in February and March of last year, job cut announcements in 2026 are closely following the pattern of 2025. Last year it was Government, Retail, and Technology. This year, it’s Technology, Transportation, and Healthcare,” said Andy Challenger, workplace expert and chief revenue officer for Challenger, Gray & Christmas.

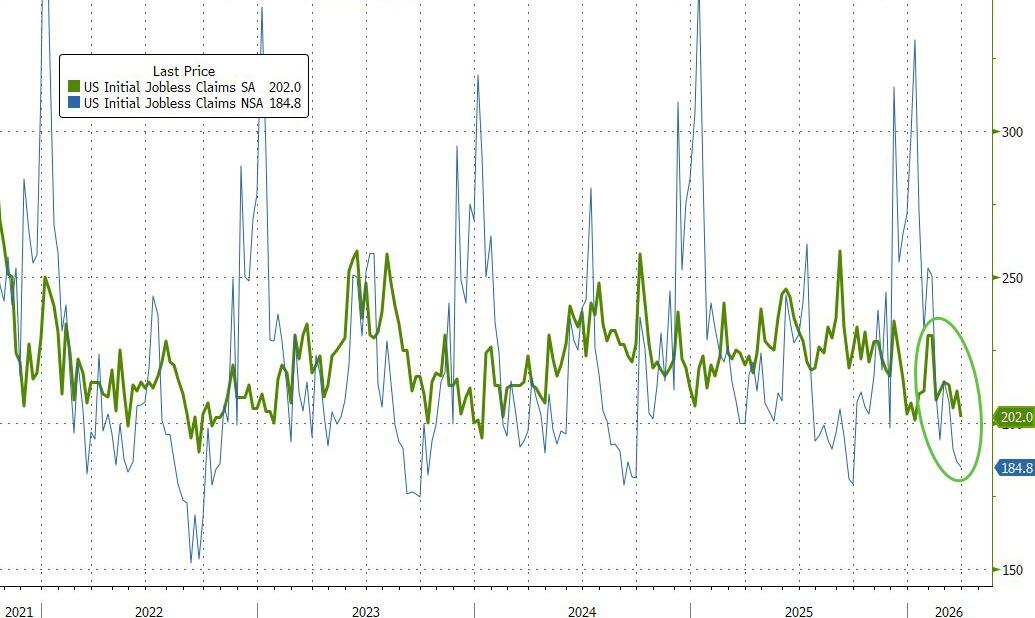

And affirming this relatively low job cuts level, the number of American filing for jobless benefits for the first time tumbled back to just 202k (from 211k) continuing to hover near record lows…

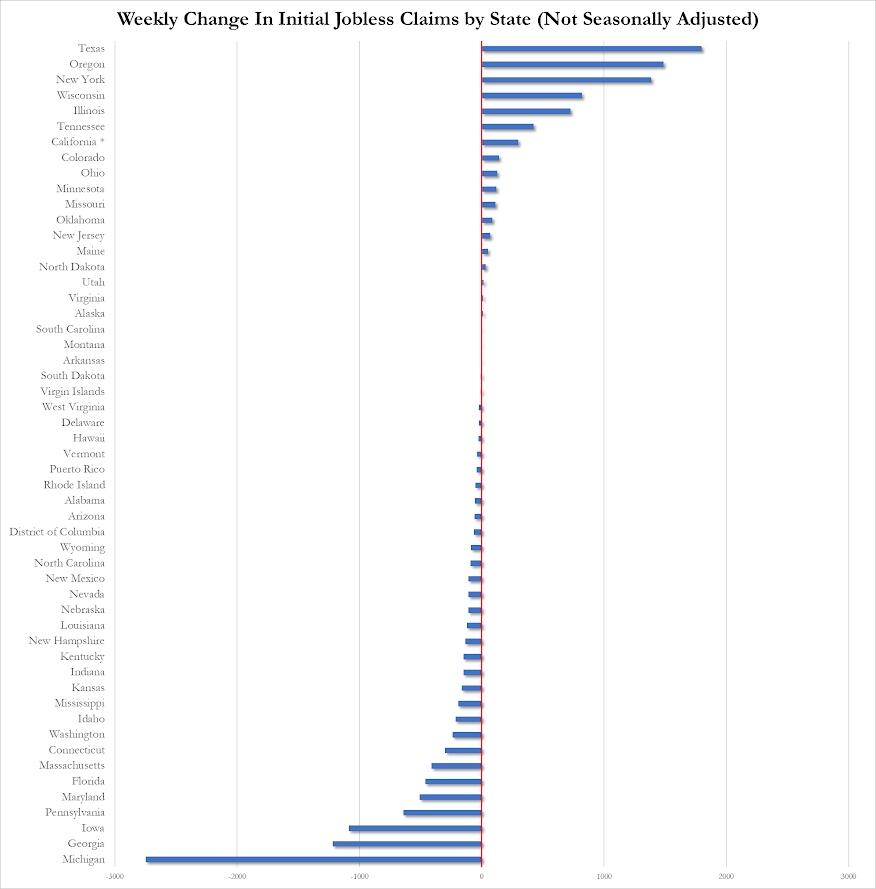

Michigan and Georgia saw the biggest declines in initial jobless claims while Texas and Oregon saw the biggest increases…

At the sector level, Technology dominated, announcing 18,720 job cuts in March for a total of 52,050 in 2026. That is an increase of 40% from the 37,097 cuts in this sector announced in the same period last year. It is the highest year-to-date total for the sector since 2023 when 102,391 Technology cuts were recorded.

More layoffs are likely to come from Technology companies in 2026. Last month’s total was made up primarily on a workforce reduction at Dell Inc., according to their latest annual filing. Oracle reportedly began layoffs late last month, though the company has not released a total figure. Meta, meanwhile, is undergoing layoffs in its Reality Labs division as it focuses on pivoting to artificial intelligence.

“Companies are shifting budgets toward AI investments at the expense of jobs. The actual replacing of roles can be seen in Technology companies, where AI can replace coding functions. Other industries are testing the limits of this new technology, and while it can’t replace jobs completely, it is costing jobs,” said Challenger.

“One thing that is clear is that AI is changing work and the workforce. Workers will need to be more strategic as they lead AI-powered agents that handle increasingly complex tasks. Human workers will need strong decision making and judgment skills in the age of AI,” he added.

Continuing jobless claims ticked up modestly from 1.816mm to 1.841mm Americans, but remains well below the 1.9mm Maginot Line…

The ‘no hire, no fire’ economy continues to chug along with yesterday’s Manufacturing PMIs and Retail Sales signaling the economic pain so many expected has been delayed… for now.

Tyler Durden

Thu, 04/02/2026 – 08:35

Futures, Bonds Tumble, Oil Soars After Trump Dashes Hopes For Early End To Iran War

Futures, Bonds Tumble, Oil Soars After Trump Dashes Hopes For Early End To Iran War

Global risk assets, including US equity futures and global markets, as well as Treasuries and precious metals, tumbled as oil soared with Brent hitting $110 this morning after Trump’s late Wednesday speech refused to pivot and dashed hopes that the Hormuz Strait would reopen soon and the war in the Middle East is nearing a swift resolution. As of 8:00am ET, S&P 500 futures dropped 1.7%, reversing yesterday’s short squeeze as investors refuse to add to risk positions ahead of the long weekend when many speculate a ground invasion of Iran may begin. Nasdaq 100 contracts slumped 2% amid a premarket selloff in big tech stocks and chipmakers. Tech is getting hit hard with Mag7 and Semis lagging while Cyclicals ex-Energy are underperforming Defensives with both Staples and Healthcare down in absolute terms pointing to broad-based de-risking into the holiday weekend. Energy should have a good day as investors re-gross in the sector and Integrateds are trading up ~3% pre-mkt. Brent soared 8.2% to more than $109 a barrel after Trump pledged more aggressive action against Iran and offered no concrete plans to reopen the Strait of Hormuz. European diesel futures hit $200 a barrel. Bonds tumbled as expectations that oil prices will stay higher for longer prompted traders to initiate fresh bets on tighter monetary policy. The dollar advance the most in a week while gold snapped a four-day streak of gains. US economic data calendar includes March Challenger job cuts (7:30am New York time), February trade balance and weekly jobless claims (8:30am). Fed speaker slate includes Logan (10:15am) and Bowman (12:45pm)

In premarket trading, Mag 7 stocks are all sharply lower (Nvidia -2.7%, Tesla -2.4%, Meta -2.4%, Alphabet -2.3%, Amazon -2.2%, Microsoft -1.3%, Apple -1%

Oil and gas companies rebound after Trump’s prime-time address. Movers include Chevron (CVX) +2.9% and Exxon (XOM) +3.2%.

Travel, mining and semiconductor stocks fall as the conflict and higher energy prices weigh on investor sentiment. Among movers: United Airlines (UAL) -4%, Newmont (NEM) -4.9%.

Globalstar (GSAT) rises 15% after a Financial Times report that Amazon.com Inc. is in talks to acquire the satellite provider.

Immunovant (IMVT) falls 7% after the drug developer said two late-stage studies of its experimental treatment for thyroid eye disease failed to meet their main goals.

Penguin Solutions (PENG) rises 9% after the semiconductor device company raised its full-year forecast for adjusted earnings.

Wingstop (WING) rises 1% as Piper Sandler and Raymond James upgrade the restaurant operator’s stock following a steep selloff.

In other corporate news, Amazon is said to be in talks to acquire satellite provider Globalstar, according to the FT, in a potential deal to bolster Amazon’s effort to build out its low-orbit satellite network to compete with SpaceX’s Starlink. In AI, Alibaba released its third proprietary AI model, Qwen3.6-Plus, in as many days to focus on profiting off its flagship AI services.

Global risk sentiment was crushed after Trump talked again about leaving Iran quickly, but warned of escalation as the US continues to amass military assets in the Middle East. Understandably, global headlines continue to be dominated by the Middle East conflict, geopolitics, oil and the Strait of Hormuz. Australia is weighing using powers amid a possible gas shortfall, oil inventory stockpiles are dropping and the UAE has called on the UN to approve measures, including force, to reopen the Strait of Hormuz.

“The speech didn’t bring forward an off-ramp, it pushed the timeline out and reintroduced escalation,” said Billy Leung, an investment strategist at Global X Management. While it is not a full big bear event, “the direction of travel has clearly worsened, and that’s what markets are reacting to.”

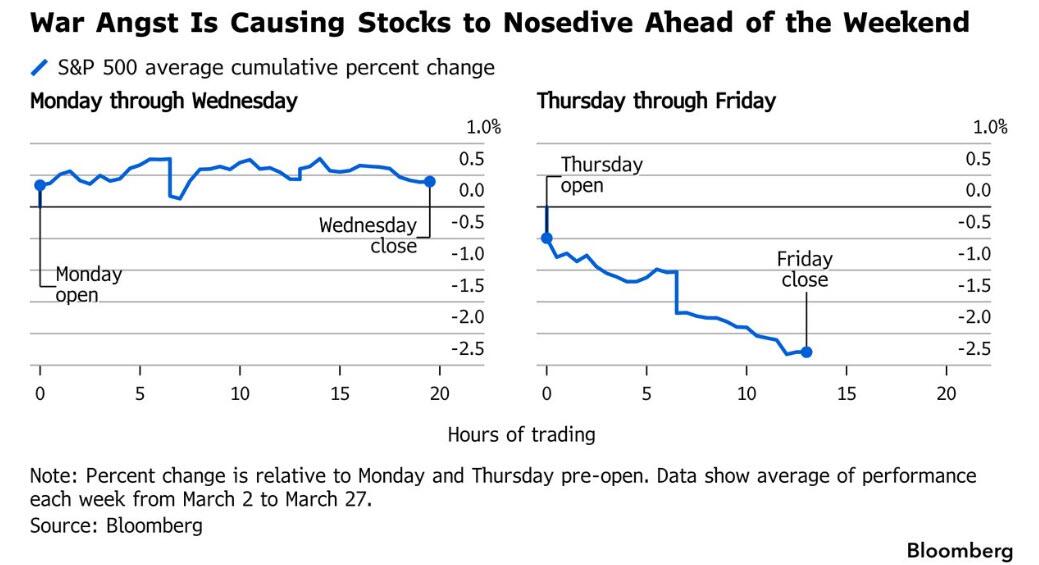

The US stock market has settled into a predictable weekly pattern since the Middle East war began. It starts the week on a strong note, drifts sideways toward the middle of the week and then collapses every Thursday and Friday, reflecting likely de-risking into a “trading blackout with unknowable risks.”

“This market just isn’t manageable,” said Laurent Lamagnere, deputy chief executive officer at Alphavalue in Paris. “We’re really concerned about second-round effects, not only on oil prices but also on oil supply, for example, airlines trimming destinations with harsh consequences for tourism.”

While markets are shut Friday, key economic data is still scheduled to be released. Bloomberg Economics expect March nonfarm payrolls rose 80k, reflecting a rebound in strike-affected payrolls, sluggish private-sector hiring and a continued drag from federal payrolls. Recent changes to the BLS’ birth-death model of business formations may continue to inject volatility into the monthly figures. As a net exporter of light, sweet crude, geopolitical risk is less concerning to US-levered energy operators relative to international peers and WTI oil-price inflation will likely be transitory, according to Bloomberg economists.

Elsewhere, the Trump administration is said to be close to announcing tariffs on drugmakers that haven’t struck deals guaranteeing low prices in the US. The US is set to roll out tiered tariffs on steel and aluminum products to simplify a process that has dogged American companies for months.

A KKR private credit fund for retail investors curbed redemptions after receiving an increase in such requests, according to a shareholder letter. Private equity sales have fallen by more than a third this year, with buyout firms selling deals valued at about $103 billion in the first quarter, roughly 36% lower than the same period a year ago. The SEC and Elon Musk said they are heading toward a trial over the regulator’s allegations that the billionaire cheated Twitter investors before his 2022 buyout.

Europe’s Stoxx 600 is down 1.2% with technology and mining stocks leading the decliners, while energy and food and beverage shares are the biggest outperformers. Here are the biggest movers Thursday:

European oil stocks gain after President Donald Trump dented hopes of a swift end to the war in Iran, sending crude prices higher. BP and Galp also benefited from analyst upgrades. Mining shares underperformed as metals prices eased

SSE shares gain as much as 0.7% after the utility firm upgraded the lower end of its guidance range for adjusted earnings per share this year

Fortum gains as much as 4% after Citi upgrades the Finnish utility to neutral and says its 2026 earnings may positively surprise the market on the back of higher spot power prices

Amplifon falls as much as 4% after the stock was downgraded to neutral from outperform at BNP Paribas, which called the Italian company’s plan to acquire GN Store Nord’s hearing-aid business a “discordant deal”

Mutares shares fell as much as 13%, the most in four months, on Germany’s Xetra exchange after the private equity firm sold shares via a private placement

Asian stocks fell after President Donald Trump’s threat to launch fresh attacks on Iran disappointed investors who were hoping for clearer signs of an end to the war. The MSCI Asia Pacific Index dropped as much as 2.6%, reversing small gains prior to Trump’s comments. South Korea, Japan and Taiwan led losses in the region. The Philippines market was closed for a holiday. The sudden downturn in sentiment came after Trump said that military operations could escalate over the next two to three weeks. Although he said the war in Iran was “very close” to completion, the US would hit electric plants in the country if no deal was reached, dampening hopes for a quick resolution to the conflict.

In FX, the Bloomberg Dollar Spot Index gains 0.5%. The Swedish krona is the weakest of the G-10 currencies, falling 1% against the greenback. The pound and Aussie dollar also underperform. Precious metals sink with spot silver down over 5%. Bitcoin falls 2.6%.

In rates, Treasury futures are off session lows with yields higher by 4bp to 6bp across the curve. Most losses occurred during Asia session following Trump’s prime-time address pledging more aggressive action against Iran and lacking a plan to reopen the Strait of Hormuz. 10-year Treasury yield near 4.36% is about 4bp cheaper on the day after peaking at 4.384%. Curve spreads remain within a basis point of Wednesday’s close. European government bonds fall as traders boost bets on rate hikes by the Bank of England and European Central Bank this year. UK and German 10-year yields rise 7 bps and 4 bps respectively. Gilts underperform, with 2-year yields are cheaper by around 10bp on the day. IG dollar issuance slate empty so far. Three offerings were priced Wednesday, with borrowers paying about 4bps in new issue concessions on deals that were 4.1 times oversubscribed. Dealers project about $115b of April supply vs about $105b a year earlier and about half of March’s $236.5b volume

In commodities, energy prices jump with Brent crude futures for June up around 7% and above $108 a barrel as investors weigh prolonged disruptions to energy flows through the vital Strait of Hormuz. European natural gas futures climb 4.5% while European diesel futures hit $200 a barrel.

US economic data calendar includes March Challenger job cuts (7:30am New York time), February trade balance and weekly jobless claims (8:30am). Fed speaker slate includes Logan (10:15am) and Bowman (12:45pm)

Market Snapshot

S&P 500 mini -1.6%

Nasdaq 100 mini -2.0%,

Russell 2000 mini -2.0%

Stoxx Europe 600 -1%,

DAX -1.6%,

CAC 40 -0.9%

10-year Treasury yield +5 basis points at 4.37%

VIX +2 points at 26.51

Bloomberg Dollar Index +0.4% at 1217.6,

euro -0.6% at $1.1524

WTI crude +7.2% at $107.31/barrel

Top Overnight News

Oil rose after President Trump’s prime-time address disappointed investors hoping for a quick end to the Iran war. In an address late Wednesday, Trump said he was still seeking a diplomatic agreement to end the conflict and that U.S. military aims would be completed “very shortly.” But he also vowed to hit Iran “extremely hard” in the coming weeks and pummel the country “back to the Stone Ages.” WSJ

Trump rattled markets and heightened political tensions with an address that offered no clear timeline for ending the Iran war, while pledging more aggressive action over the next two to three weeks. Iran and Israel continued to trade strikes and the US president renewed threats against Iranian electric plants. BBG

The Trump administration is preparing to impose tariffs of 100% on certain medicines as it pushes drugmakers to manufacture more in the US. The levies – set to be announced as soon as Thursday – would be applied to companies that have not struck deals with the White House. FT

Congressional Democrats sued to block Trump’s executive order that would prohibit mail-in voting for anyone not on a pre-approved list compiled by the DHS. BBG

China’s central bank withdrew cash from its financial system in March for the first time in a year, amid signs of an economic rebound. BBG

Former BOJ chief economist Toshitaka Sekine said the central bank may raise rates as soon as April, due to the risk of supply shocks. BBG

Swiss inflation accelerated 0.3% in March, the quickest pace in a year, as the energy supply crunch stoked the cost of heating oil. BBG

Global private equity sales have fallen by 36% this year, as developments in AI and the war in Iran heap pressure on a subdued exit market. FT

The US is set to outline a tiered regime for steel and aluminum, maintaining 50% duties on many products but applying lower rates to others. BBG

Oil’s near-term outlook turned more bullish after Trump’s speech, with June futures rising more than $8.5 a barrel above July as Hormuz disruptions cut about 11 million b/d. Traders expect continued supply strain and higher prices. BBG

Canadian PM said he spoke with US President Trump this evening to discuss Artemis II and the Middle East conflict.

US President Trump discussed firing Attorney General Pam Bondi and replacing Bondi with EPA Chief Zeldin, although he has not yet made a decision whether to fire Bondi, according to NYT.

US Senate may vote on DHS funding bill on Thursday, while the bill would fund DHS without ICE and CBP, according to NBC.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks failed to sustain initial gains after US President Trump’s primetime address disappointed those hoping for an immediate de-escalation in the Iran conflict, in which he said they will hit Iran very hard over the next 2-3 weeks and will ‘bring Iran back to the stone age, where they belong’, while he also threatened to hit Iran’s electric plants if there is no deal and could hit their oil. ASX 200 reversed early gains as Trump’s remarks soured the broad risk sentiment, and with the declines led by weakness in the tech, mining, materials and resources industries, while the latest trade data from Australia had very little influence on price action. Nikkei 225 wiped out the initial spoils and slumped beneath the 53,000 level as US President Trump’s remarks triggered a broad risk-off mood and lifted oil prices. Hang Seng and Shanghai Comp were subdued amid notable weakness in the Hong Kong-listed blue chip tech stocks, and with the mainland also dampened following another paltry liquidity operation by the PBoC.

Top Asian News

South Korean Vice Finance Minister said they are closely monitoring FX market as speculative trading is being seen; to respond sternly to excessive herd-like behaviour FX markets.

Magnitude 7.8 earthquake strikes 119km WNW of Ternate, Indonesia, according to the USGS.

EMSC announces a tsunami alert after earthquake in Indonesia region.

European bourses (STOXX 600 -1.1%) began the session with decent losses after US President Trump’s nationwide address reignited tensions. He said that the mission in Iran will be finished very fast and the US will hit Iran very hard over the next 2–3 weeks, while warning of strikes on electric plants if there is no deal and could also target its oil facilities. Since the start of cash trade, losses have pared back slightly but indices are holding around the -1% mark. European sectors are broadly in the red. Energy is the outperformer while Food, Beverage and Tobacco follow closely behind. Technology sits at the bottom of the pile, after performing well over the past 3 sessions, while Basic Resources also suffers as precious metals slip.

Top European News

Swiss Inflation Rate YoY (Mar) Y/Y 0.3% vs. Exp. 0.6% (Prev. 0.1%, Low. 0.1%, High. 1.0%); Core 0.4% (prev. 0.4%).

Swiss Inflation Rate MoM (Mar) M/M 0.2% vs. Exp. 0.5% (Prev. 0.6%, Low. 0.2%, High. 0.9%).

FX

DXY is stronger this morning, with traders flocking back to the USD after US President Trump’s address dampened hopes of de-escalation with Iran. Overnight, he stated that he will hit Iran very hard over the next two to three weeks, adding that the US could also target Iran’s oil facilities. Trump’s rhetoric has seemingly shifted from a focus on the timeline for wind-down to a more aggressive military escalation within that same window. DXY jumped back above the 100 mark, to currently trade at the upper end of a 99.44-100.17 range; recent levels above this include 100.64 (high from 31 Mar).

Focus for today remains on any geopolitical updates, but that aside, there are a few important domestic data points to keep an eye on. Weekly initial jobless claims (212k expected from 210k) and continuing claims (1.84mln expected from 1.819mln), Revelio’s public labour statistics report, Challenger job cuts (90k expected in March from 48.3k) and international trade data are due. This all precedes the March NFP report on Good Friday, which is expected at 65k.

G10s are all losing against the stronger USD; Antipodeans underperform, given the risk tone, whilst the Loonie fares a little better than peers, given it does not rely on external energy. GBP also sits right towards the foot of the G10 pile and is underperforming vs the EUR. A Wednesday rally in Gilts and traders believing the BoE may be slower vs the ECB in containing the energy shock may explain the slight underperformance between the two. This also comes after BoE Governor Bailey suggested earlier in the week that markets were getting ahead of themselves by pricing in rate hikes. Cable currently sits at the bottom end of a 1.3195-1.3320 range.

CHF is also amongst the worst performers against the USD, but is incrementally losing against the EUR. Earlier, a cooler-than-expected (but stronger-than-prior) Swiss inflation report spurred some modest pressure in the Franc, before then reversing soon after. In a bit more detail, headline Y/Y printed at 0.3% (exp. 0.6%, prev. 0.1%); M/M 0.2% (exp. 0.5%). Much of the upside was facilitated by stronger energy prices, leading inflation to the strongest in over a year, and back away from the lower end of the SNB’s 0-2% target. For the time being, this will help alleviate fears at the Bank of bringing back negative interest rates, though policymakers have long reiterated that there is a high bar for such a move.

Central Banks

ECB’s Panetta said leading indicators are pointing towards a slowdown in the economy; tensions in energy markets are a cause for concern not only for the immediate impact, but also on growth. Non-bank financial intermediaries in some sectors show levels of leverage and liquidity which could prove inadequate during periods of acute stress.

ECB Economic Bulletin Issue 2, 2026: The risks to the growth outlook are tilted to the downside, especially in the near term.

ECB’s Simkus said caution is needed on rates and it is too early to say what is needed at the April meeting.

BoE DMP (Mar): 1yr ahead CPI expectation 3.5% (prev. 3.00%), 3yr ahead CPI expectation 2.7% (prev. 2.8%).

Fixed Income

A bearish start to the day as US President Trump’s primetime address reignited geopolitical tensions (recap on the feed, 07:35BST), lifting energy and in turn fanning the inflationary flame.

Specifically, USTs dropped from 111-02 pre-Trump to a 110-24 knee-jerk low and have since hit a 110-16 trough. Lifting yields across the curve, 10yr to a 4.38% peak, though shy of Monday’s 4.42% WTD peak. Similarly, the 2yr to a 3.86% peak, but shy of Monday’s 3.89% WTD best. Action that has seen the implied magnitude of near-term tightening tick up by just under a bp worth. Geopols aside, Challenge Jobs, claims and import/export data; Fed speak is also due.

EGBs and Gilts, in line with the above bearishness, Bunds hit a 125.19 trough with losses of 51 ticks at most, while Gilts got to a 87.85 low, with downside of 75 ticks. Since, they have bounced by around 20 ticks from extremes, but remain firmly in the red.

The European docket is a light one; action will continue to be dictated by energy movements and associated inflation/central bank expectations from it. For the ECB and BoE, markets continue to price in 60bps and 41bps of 2026 tightening, respectively. Despite the recent inflation print from the EZ not yet showing second round effects, and despite Bailey pushing back on market pricing this week.

France sold EUR 12.5bln vs exp. EUR 10.5-12.5bln 3.00% 2034, 3.50% 2035, 0.50% 2044 and 2.00% 2048 OAT.

Japan sold JPY 1.97tln 10yr JGBs, b/c 2.57x (prev. 3.30x), average yield 2.350% (prev. 2.122%).

Commodities

In geopolitics, President Trump’s address largely repeated recent messaging on the Middle East, offering little fresh clarity on a path to de-escalation. That being said, Trump’s rhetoric has seemingly shifted from a focus on the timeline for wind-down to a more aggressive military escalation within that same window. On March 31st, Trump claimed the US could “leave” Iran within “two or three weeks” because the mission to prevent a nuclear weapon had been “attained.” He framed the upcoming period as “finishing the job,” asserting that the US would exit regardless of whether a formal deal was reached. On April 1st, in his televised address, he paired the same timeframe with a promise of violence, stating the US would hit Iran “extremely hard” over the next two to three weeks and bring them back to the “Stone Ages”.

WTI and Brent futures have surged after US President Trump’s televised address, which dampened hopes of a near-term end to the conflict. Brent Jun’26 currently eyes USD 109/bbl to the upside (USD 99.08-108.97/bbl range) while WTI May’26 sits around USD 107/bbl (USD 97.50-107.38/bbl range). Meanwhile, European diesel futures hit USD 200/bbl as the Iranian war curbs supply. Dutch TTF is +3.5% at the time of writing, but off its best levels, with some citing forecasts of milder weather as a drag on prices despite the ongoing geopolitics. Analysts at ING suggest that “even if shipping through the Strait of Hormuz resumes, a return to pre‑war market conditions is likely to be slow, as upstream production restarts, logistics normalisation and inventory rebuilding will take time.”

Spot gold reversed an earlier gain after Trump’s speech offered little clarity on how the war might end. The bullion entered the European day around USD 4,600/oz after trading above USD 4,800/oz earlier in the APAC session. Spot silver briefly dipped under USD 70/oz before recovering to around USD 71.50/oz, but well off its earlier high of USD 76.42/oz.

Industrial metals also fell after Trump repeated that the US could strike Iran “extremely hard” and target its power plants if talks fail. 3M LME copper fell under USD 12,500/t but found support at USD 12,250/t. Elsewhere, the WSJ reported Trump is expected to overhaul US steel and aluminium tariffs, with finished goods made from imported metals potentially facing a 25% duty, while the administration is also preparing tariffs on drugmakers, possibly from Thursday, that have not agreed to guarantee low US prices.

South Korea’s Blue House denies the report regarding considering fees on passing through Hormuz. This comes following earlier reports that South Korea is reportedly considering whether to pay Iran to bring in Middle Eastern oil and gas.

The 8 members of the OPEC+ group still plan to hold their virtual meeting on the 5th of April, according to Kpler’s Bakr.

China has reportedly asked private refiners to maintain fuel output at all costs.

Russia imposes ban on gasoline exports for producers until the end of July, IFX reported.

Kpler’s Bakr posted “At this point and under the most optimistic scenario Hormuz will remain shut till May. Now brace for impact.”

Iraq’s oil ministry said it has began exporting oil through Syria.

Reconstructing Iran’s Khuzestan steel factory will take between 6-12 months, Mizan news reported.

New Zealand associate energy minister said will enter into an agreement to support an additional 90mln litres of storage for diesel at Marsden Point in Northland.

Colonial pipeline is reportedly down due to damage in Georgia.

Venezuela’s oil exports in March surpassed 1mln bpd for the first time n six months, according to shipping data.

Trade/tariffs

US President Trump’s administration is readying to impose tariffs of 100% on certain medicines as it pushes pharmaceutical companies to manufacture more in the US, according to FT.

US President Trump is expected to overhaul steel and aluminium tariffs, while altered rates on finished products would simplify compliance, but could increase costs for many imports, according to WSJ. Plans to alter tariff duties to 25% on the entire value of finished products. 50% tariff will remain for commodity-grade steel and aluminium products. Executive order could come as early as this week.

China’s MOFCOM said they are to enhance communications with the US on trade.

The EU is discussing setting up digital tech dialogue with the US and reiterates that digital legislation is not up for negotiation.

Geopolitics

US President Trump said in his primetime address that Iran’s navy is gone and its air force is in ruins, while he noted most of Iran’s leaders are dead, and its ability to launch missiles and drones has been curtailed. Trump stated they will never allow Iran to have a nuclear weapon and that US strategic objectives are nearing completion, as well as stated that the mission in Iran will be finished very fast and the US will hit Iran very hard over the next 2–3 weeks, and will bring Iran back to the stone ages, where they belong. Furthermore, he said countries reliant on Hormuz oil should take the lead and that Hormuz will reopen once the conflict ends, while he warned the US will strike Iran’s electric plants if there is no deal and could also target its oil facilities.

US President Trump said strategic objectives are nearing completion, must complete mission in Iran and will finish the job very fast, adds Iran can never be trusted with nuclear weapons. US has plenty of gas. Countries that get oil via Hormuz must cherish it and must take the lead and suggests countries buy oil from the US. Hormuz will naturally open when conflict is over.

US intelligence agencies assessed that Tehran is not currently willing to engage in substantial negotiations to end the conflict, while US intelligence agencies believe Iran’s government thinks Trump is not serious about negotiations, according to NYT.

US VP Vance is engaging with Pakistan mediators over Iran deal and passed a message to Iran via Pakistan on Tuesday, while US and Iran are discussing ceasefire for Hormuz reopening and Vance warned of increasing pressure without a deal, according to ABC.

UAE reportedly preparing to help the US fight Iran and open the Strait of Hormuz by force after being repeatedly struck by Iranian drones and missiles since the war began, NY Post reported citing Arab officials.

Senior Iran source said Tehran demands a guaranteed ceasefire to end war permanently and no talks have taken place via mediators for a temporary ceasefire, while intermediaries contacted Iran on Tuesday and discussions were about continuing diplomacy.

Iran’s military spokesperson said bigger, wider and more damaging attacks are coming soon, Tasnim reported.

Iranian President Pezeshkian said attacking Iran’s vital infrastructure shows an inability to achieve a sustainable solution, IRNA reported.

Faytuks Network posted on X citing Fox News that “Trump’s speech tonight will inform the public that we may require the use of ground troops to round up uranium in Iran” – UNCONFIRMED. This was later deleted.

Israeli sources say they have not been given the green light from the US yet for Israel to target infrastructure in Lebanon, Al Hadath reported.

US Embassy in Baghdad has told US citizens to leave Iraq with expectations of Iran-aligned militia to carry out attacks in central Baghdad within 24-48 hours.

Iran Supreme Leader’s advisor, Kamal Kharazi, was reportedly injured in US-Israeli attack on Tehran.

Iran’s atomic energy agency said US-Israeli attacks against facilities under IAEA supervision are a ‘war crime’.

Reports of strong explosions in proximity to US bases in Kuwait, N12 reported.

Pakistan foreign ministry spokesperson said there is no confirmation so far of any US delegation arriving for talks.

Explosion reported in Kuwait; explosions are caused by an attack on American positions, Mehr and Fars News report.

US Event Calendar

8:30 am: United States Feb Trade Balance, est. -60.55b, prior -54.5b

8:30 am: United States Mar 28 Initial Jobless Claims, est. 212k, prior 210k

8:30 am: United States Mar 21 Continuing Claims, est. 1836.5k, prior 1819k

10:15 am: United States Fed’s Logan Speaks at Dallas Fed Banking Conference

12:45 pm: United States Fed’s Bowman Speaks at Banking Conference (Closed event)

DB’s Jim Reid concludes the overnight wrap

After rallying sharply over the previous two sessions, market sentiment has deteriorated overnight after Trump’s much anticipated address last night delivered little to nothing new on potential timelines or conditions for ending hostilities against Iran. The US President claimed that the operation against Iran was “very close” to completion but also said the US “will hit Iran extremely hard over the next 2-3 weeks”. Trump again raised the threat to hit Iran’s power plants if there is no negotiated deal and reiterated the view that shipping via the Strait of Hormuz was other countries’ problem. So while Trump sounded flexible on remaining war aims, for instance claiming that Iran is “no longer a threat”, there was no signal of the US seeking an imminent offramp out of the war.

In response, markets have reversed the continued positive momentum they’d seen yesterday amid rising hopes that an end to the conflict might be coming into view. In oil markets, Brent crude is +6.24% higher at $107.47 this morning, a level last seen on Tuesday, even as it had briefly fallen below $100/bbl yesterday evening just before Trump’s address. Equity futures are losing ground overnight, with S&P 500 futures (-1.25%) more than erasing yesterday’s +0.72% regular session gain, while STOXX 50 futures are down -1.75% after posting their best session in almost a year yesterday. In Asia, equity markets have lost ground, with the KOSPI (-4.23%) standing out as the largest underperformer this morning. The Nikkei (-2.42%), Hang Seng (-1.09%), and S&P/ASX 200 (-1.14%) are also seeing significant declines, though in mainland China the CSI (-0.75%) and the Shanghai Composite (-0.50%) are more stable.

In the rates space, 10yr Treasury yields are +5.5bps higher at 4.37% this morning after Wednesday’s stable session, while in FX, the dollar index (+0.39%) has more than reversed yesterday’s -0.31% decline. Gold (-1.89%) is similarly reversing yesterday’s +1.94% gain.

Prior to the overnight news, the continued rally yesterday appeared to be one of hope more than conviction as investors navigated a dizzying influx of competing headlines. Among those was Trump’s post early yesterday that Iran’s “New Regime President” had asked the US for a ceasefire, which Trump said he would only consider when the Strait of Hormuz is “open, free and clear”. Iran’s foreign ministry later responded, calling the ceasefire claim “false and baseless“. That response arrived amidst an Axios report that the US and Iran were negotiating a ceasefire. Meanwhile, Iran’s President Pezeshkian released an open letter, claiming that Iran harboured no enmity towards the people of America.

Another headline-drawing Trump comment yesterday was that he was strongly considering pulling out of NATO, though he then did not directly raise this topic in his overnight address. We also heard that NATO Secretary General Rutte is due to visit Washington next week. Note that the political bar for formal US withdrawal from NATO is high, as this would require a two thirds majority in the Senate or passing an act of Congress. The role of US allies has been a rising topic in its own right, with news that the UK will today convene virtual talks with some 35 countries not including the US to discuss a plan to restore shipping via the Strait of Hormuz.

In terms of yesterday’s other news, 2yr US Treasury yields (+0.9bps) inched higher as the decline in oil prices was outweighed by solid US data. The March ISM manufacturing came in at 52.7 vs 52.3 expected, with the prices paid component rising to 78.3 (vs 74.0 expected), its highest reading since mid-2022. The US ADP private employment figures for March (+62K vs +40K) were also on the stronger side.

US labour market data will remain in focus with the latest weekly claims today and then the March jobs report on Friday, even as most markets are closed for Good Friday. For Friday’s non-farm payrolls our US economists see headline gains of +50k (vs -92k previous) and private payrolls at +60k (vs -86k), reflecting a return closer to the average pace of job gains over the latter half of 2025. 01

In terms of the details of yesterday’s upbeat market moves, the +0.72% gain for the S&P 500 was again led by tech stocks, as the NASDAQ (+1.16%) and the Mag-7 (+1.37%) powered ahead for a second day. Credit also saw a strong rally, with US HY credit spreads (-16bps after -18bps Tuesday) registering their best two-day run since last May. And European equities saw a sharp surge as investors caught up to the US rally that started on Tuesday, with the STOXX 600 (+2.50%), DAX (+2.73%) and the FTSE 100 (+1.85%) all posting their largest jumps since last April.

European bonds also rallied on the prospect of lower oil prices as well as declining natural gas prices, as front month TTF futures fell by -5.49% to €47.51/MWh, their lowest level since March 10. Yields on 10yr bunds fell -1.8bps to 2.98%, while BTPs (-7.8bps) and OATs (-5.2bps) outperformed amid the risk-on mood. Gilt yields saw an even larger pullback, with the 10yr down -8.6bps as the UK manufacturing PMI for March was revised down from 51.4 to 51.0. That was in contrast to a moderate upward revision to the Euro Area manufacturing PMI (51.6 from 51.4), which showed more resilience to the energy shock.

Yesterday, I published a note looking at what the March PMIs tell us about the impact of the Iran war on the global economy. While we’ve seen a major inflation and supply shock, this has varied across countries and there are some silver linings. For instance, the behaviour of output prices across the G10 has been more akin to the pre-Covid era than the 2021-22 inflationary period, which may offer some breathing room for central banks concerned about inflationary risks. See the note here.

In data out of Asia this morning, South Korea’s consumer inflation picked up from +2.0% to +2.2% in March, though this is below consensus expectations of +2.3%. So providing some tentative relief to policymakers dealing with the spillover effects of curtailed energy supplies out of the Middle East.

To the day ahead now, we will get further US data, with the February trade balance and latest weekly jobless claims. And while we take a break on Good Friday, the US will release the March jobs report.

Tyler Durden

Thu, 04/02/2026 – 08:33

4 Million Children Have Been Signed Up For Trump Accounts: IRS

4 Million Children Have Been Signed Up For Trump Accounts: IRS

Authored by Naveen Athrappully via The Epoch Times,

American taxpayers have signed up over 4 million children to the tax-advantaged Trump Accounts, and more than 1 million of those accounts have elected to receive the $1,000 pilot contribution from the government, the IRS said in a March 31 statement.

“Contributions to Trump Accounts can be made starting July 4, 2026. All eligible children may receive deposits from parents, relatives, friends, employers, state governments, philanthropic organizations, and individuals, subject to an annual limit,” the IRS said.

The Trump Accounts, formally the Invest America accounts, were established under the One Big Beautiful Bill Act signed into law by President Donald Trump in July last year.

Every child under 18 who is a U.S. citizen and has a valid Social Security Number is eligible to open a Trump Account. In addition, any child born between Jan. 1, 2025, and Dec. 31, 2028, can get an initial seed contribution of $1,000 from the government.

According to a March 9 proposed rule from the IRS published in the Federal Register, contributions to Trump Accounts are, in general, subject to an annual limit of $5,000.

Employers can contribute up to $2,500 annually to the Trump Accounts set up by their employees, which will count toward the $5,000 annual threshold. Contributions from the government and nonprofits made via the Treasury Department are not counted in the $5,000 limit.

The annual contribution limits will be indexed to inflation, with adjustments starting after 2027.

Generally, funds in Trump Accounts cannot be withdrawn prior to the child turning 18. After hitting this age, account holders can withdraw the funds for certain qualified purposes such as paying for tuition, purchasing a home, or starting a business.

Funds from the Trump Accounts can be invested only in certain “eligible investments,” such as a mutual fund or exchange-traded fund that tracks stock indexes composed mainly of American companies for which futures contracts are traded in the market. The accounts must avoid using leverage in investments.

The IRS determined that Trump Accounts for more than 4 million children have been opened based on Form 4547 filings made by taxpayers together with their individual tax returns.

“The IRS has been working closely with the Treasury Department to make the election process as simple and easy as possible by permitting taxpayers to fill out a one-page form when they file their tax return,” IRS Chief Executive Officer Frank J. Bisignano said.

“Families with eligible children born between 2025 and 2028 just need to check the box on a form to stake their claim for the $1,000 contribution. It’s that simple.”

Investments made in Trump Accounts grow tax-deferred, meaning no taxes are charged on the account proceeds until funds are withdrawn, according to investment management company Vanguard.

However, California’s Franchise Tax Board recently announced that it will not treat Trump Accounts as tax-deferred accounts for state tax purposes. As such, families in the state will have to pay taxes on the Trump Accounts’ investment earnings rather than the accounts being taxed during withdrawal.

‘Could Become a Cornerstone’

In a Sept. 3 post, State Street Investment Management said there were some “outstanding issues” regarding the Trump Accounts that needed to be addressed.

For instance, employer contributions must be monitored to ensure compliance, according to the post, and there must be mechanisms to enforce prohibition of withdrawals before children turn 18. The Treasury Department must also remain flexible when it comes to adjusting rules for the accounts to address any new challenges or opportunities.

“The successful implementation of these accounts hinges on the Treasury Department’s ability to address and resolve the outstanding issues outlined,” the post said. “With careful regulation and clear guidance, Trump accounts could become a cornerstone of financial security for future generations.”

A June 12 analysis published by the Tax Law Center at the New York University School of Law raised concerns about the fact that funds in Trump Accounts must be invested in corporate equities, which it said makes the investments “high-risk.”

In a March 6 IRS statement, Bisignano cited the benefits provided by these accounts, terming them a “pro-family initiative that will help millions of Americans harness the strength of [the U.S.] economy to lift up this generation and generations to follow and unlock the American Dream.”

In January, House Ways and Means Committee Chairman Jason Smith (R-Mo.) highlighted how Trump Accounts are positively transformative for American children.

“[In] my hometown that I still live in today, the average income for an individual is less than $26,000 a year. And so when you look at that, this is the opportunity for those kids,” Smith said.

“It doesn’t matter if you live on a city block or a county road, you’re going to have this investment, and it will be transformational,” the lawmaker said. “Americans’ lives are going to be affected in such a positive way for generations.”

Tyler Durden

Thu, 04/02/2026 – 08:05

https://www.zerohedge.com/personal-finance/4-million-children-have-been-signed-trump-accounts-irs

U.S. Alerts Goldman Sachs Paris After Iranian Group Threatens Terror Bombing

U.S. Alerts Goldman Sachs Paris After Iranian Group Threatens Terror Bombing

Five days after French authorities foiled a terror plot targeting Bank of America’s Paris headquarters, the threat environment facing U.S. financial institutions in the French capital appears to be worsening.

New reporting from Le Parisien says Goldman Sachs’ Paris headquarters was placed under police surveillance on Wednesday night following threats allegedly linked to Iranian terror networks.

Le Parisien outlines the rationale behind the heightened security posture:

It’s 1:30 a.m. when the phone rings, shattering the night’s calm.

A security guard on duty at the American bank receives a call from his head of security, based in London.

According to our information, she informs him that she has received an email from the American authorities, advising him to “extend his vigilance” at the bank.

The reason? “An Iranian group is threatening to attack the buildings with explosive devices,” explains a source close to the matter.

By Thursday morning, however, the Paris prosecutor’s office said that “no suspicious elements were found at the scene” following surveillance operations in and around Goldman’s building at 85 Avenue Marceau in the 16th arrondissement.

Reuters reports that Goldman and Citigroup staffers in Paris are remote working amid threats.

The latest threat comes after last week’s arrest of three suspects linked to the foiled terror plot outside Bank of America’s Paris headquarters. French investigators have reportedly tied the BofA incident to broader tensions stemming from the U.S.-Iran conflict in the Middle East.

Separately, Iran’s Revolutionary Guard has threatened US companies with operations across the Middle East, including Nvidia, Apple, Microsoft, and Google.

“From now on, for every assassination, an American company will be destroyed,” the IRGC said.

It is no longer just U.S. banks being treated as part of the battlefield. U.S. tech firms are in the crosshairs of the IRGC. President Trump’s Wednesday night comments signaling another two to three weeks of military operations against Iran raise the odds of global spillover, including retaliatory or proxy threats against U.S. interests abroad and, potentially, elevated homeland risk.

Tyler Durden

Thu, 04/02/2026 – 07:45

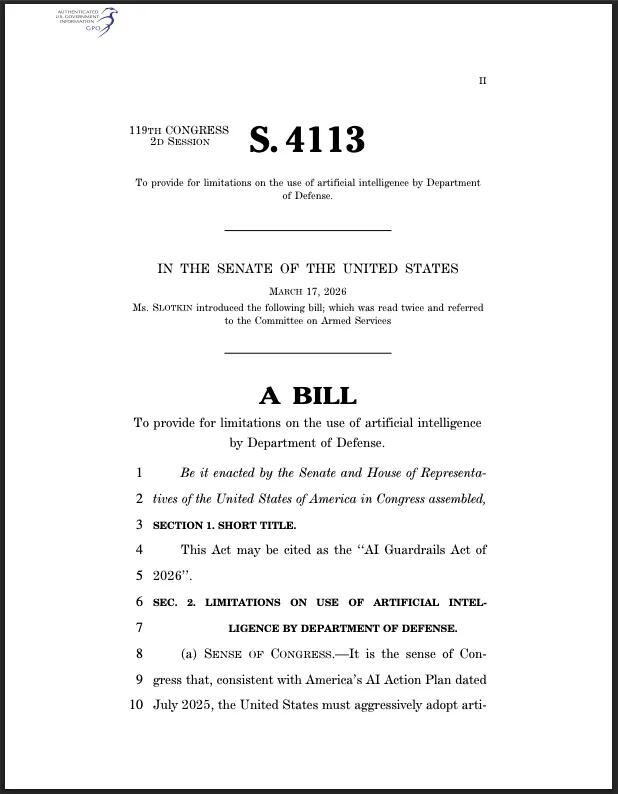

New Bill Opens Door For Killer AI Weapons

New Bill Opens Door For Killer AI Weapons

A newly introduced U.S. Senate bill would allow the military to deploy autonomous lethal artificial intelligence systems by granting the Secretary of Defense the authority to override its own restrictions.

Senate Bill S.4113—the “AI Guardrails Act of 2026,” introduced March 17, 2026 by U.S. Senator Elissa Slotkin (D-MI)—is being presented as a framework to limit how the Department of Defense uses AI.

But the actual text includes a built-in waiver mechanism that enables those same systems to be approved and used under national security justifications.

This means a Pentagon-approved AI system could independently identify and engage targets, making life-and-death decisions without real-time human input.

There is no language in that waiver clause limiting where the system can be used, whether targets are foreign or domestic.

The bill has been read twice in the Senate and referred to the Senate Armed Services Committee, where it now awaits further consideration.

The waiver raises questions about how often “extraordinary circumstances” will be invoked, who ultimately decides when autonomous lethal force is justified, and what meaningful limits—if any—remain once that authority is exercised.

Waiver Authority Built Into the Core Restriction

The bill prohibits the use of AI for:

Launching or detonating nuclear weapons

Domestic monitoring or targeting without legal basis

Using lethal force through autonomous weapon systems without human oversight

Immediately following that restriction, the bill states:

The Secretary of Defense “may waive the prohibitions… for up to one year” and renew that waiver if “extraordinary circumstances affecting the national security of the United States require the waiver”

How It Works

The decision to authorize autonomous lethal systems is placed with the Secretary of Defense.

Waivers last up to one year

Waivers can be renewed

Congress is notified after issuance

Notifications may include classified components

The bill requires certification that the system’s error rate does not exceed that of human operators performing comparable functions.

Operational Scope

The waiver applies to:

Development

Field deployment

System modifications

It also covers changes to:

Mission sets

Target sets

Operational environments

Algorithmic behavior

Each of those changes can trigger continued or expanded authorization under the same waiver structure.

Sponsor Background

The bill was introduced by Sen. Elissa Slotkin, whose background includes:

CIA analyst

Department of Defense official

Acting Assistant Secretary of Defense for International Security Affairs

Her professional history is directly tied to the national security institutions governed by the bill.

Campaign Finance Alignment

Slotkin’s donor base includes multiple sectors tied to AI development, autonomous systems, and the broader defense-tech pipeline enabled by this bill.

According to OpenSecrets data, top contributors include:

Alphabet Inc ($96,669) and Amazon ($53,771)—major AI developers and federal cloud contractors

General Motors ($57,081) and Ford ($54,020)—advancing autonomous and robotics systems applicable to military use

University of Michigan, Michigan State, Harvard, Stanford—key hubs for federally funded AI and defense-related research

Kirkland & Ellis ($52,360) and WilmerHale ($81,463)—heavily involved in structuring large-scale federal and defense contracts

The bill authorizes deployment of autonomous AI systems under a renewable waiver controlled by the Pentagon.

The companies and institutions funding Slotkin are directly tied to building the AI, infrastructure, and legal frameworks required to support that expansion.

The legislation opens the door, and her donor base sits inside the ecosystem that stands to operate and profit within it.

Bottom Line

The legislation places a restriction on autonomous lethal AI systems while granting the Secretary of Defense—currently Pete Hegseth—the authority to waive that restriction under “national security” conditions.

That waiver:

Is controlled by a single Pentagon official

Can be renewed indefinitely

Applies to real-world deployment, targeting, and system evolution

Contains no language limiting where such systems may be used

Congress is notified after the fact, not required to approve.

The authority to deploy autonomous lethal AI systems sits inside the same section that claims to restrict them.

Tyler Durden

Thu, 04/02/2026 – 07:20

https://www.zerohedge.com/military/new-bill-opens-door-killer-ai-weapons

New Warning Sign: 1 In 4 Workers Have Cut 401k Contribution Rate

New Warning Sign: 1 In 4 Workers Have Cut 401k Contribution Rate

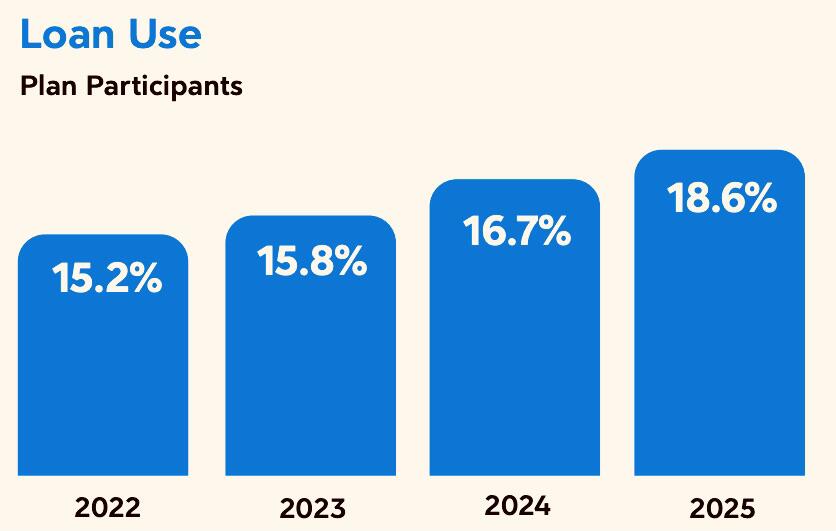

Another light on America’s economic dashboard is blinking red, as money-pinched workers are cutting their 401k contribution rates. The news follows our earlier report on hardship withdrawals from the cornerstone retirement savings accounts hitting a record high. Critically, these numbers don’t reflect what workers are doing right now — amid war-driven gas price-hikes and worries about the economy.

According to new data from Dayforce’s State of Retirement Savings 2026 report, in 2025, Americans trimmed their contribution rates to 401k and similar plans from 9.2% to 8.9%. While the decline was relatively modest, it was a widespread phenomenon, with more than one in four workers reducing their contributions. Employees earning between $50,000 and $150,000 were most likely to have eased back. The participation rate slipped from 78.6% in 2024 to 77.5%. The decreases come despite wider use of automatic enrollment in retirement plans, and increasingly-common auto-escalation features that ratchet up contributions each year.

Want an even better-proportioned one for yourself — the mug, that is? Get yours at the ZeroHedge Store today and support our work

“When you are struggling day to day, it’s hard to focus on your long-term goals,” Matt Bahl, vice president at the Financial Health Network, told CBS News. “We’re really seeing the crunch for those middle-income earners — it speaks to the affordability crisis.”

Dayforce cautioned that employers’ concern about the trend should go beyond future retirement security, and include their workers’ present-day financial stress. “[It] can influence engagement, productivity, and retention,” said the company, which offers a cloud-based “Global Human Capital Management” platform. As 2025 ended, roughly half of Americans in an Allianz Life survey said they had more financial stress than they did a year ago.

via Dayforce’s “The State of Retirement Savings 2026”

Reinforcing that picture of growing financial stress, loan use increased more than 20% since 2022. The Dayforce study didn’t cover hardship withdrawals, but Vanguard’s How America Saves 2025 study found that hardship withdrawal activity “increased to a new high” of 6% in 2025, up from 4.8% in 2024 and about 2% before the pandemic. In part, that trend was facilitated by a regulatory change — in 2018, Congress nixed a requirement that participants first take a 401(k) loan before they could take a hardship withdrawal.

Men’s 2025 savings rate topped women’s — 9.6% to 8.2% — though that gap was wider a few years ago. Asians had the top savings rate (10.4%), with whites close behind (10.1%), followed by blacks (6.0%) and then Latinos (4.7%). Conversely, 28.7% of blacks and Latinos collectively had an active loan from their retirement accounts, compared to 15.9% of whites. No loan data was given for Asians.

Watch for all these indicators to keep trending down: Cost-of-living effects of the US-Israeli war on Iran are poised to grow stronger as the global oil shockwave steadily moves closer to America’s shores.

Tyler Durden

Thu, 04/02/2026 – 06:55

https://www.zerohedge.com/economics/new-warning-sign-1-4-workers-have-cut-401k-contribution-rate

Is Trump About To Crush The Cartels In Ecuador?

Is Trump About To Crush The Cartels In Ecuador?

Authored by Steve Watson via Modernity.news,

President Trump is taking the fight directly to the drug cartels by launching aggressive military operations in Ecuador with the full backing of the country’s right-wing president.

Trump believes that the time has come to directly confront the narco-terrorists flooding American communities with poison.

Recent developments include joint US-Ecuador operations under “Operation Total Extermination,” with strikes on narco-terrorist targets along the Colombia-Ecuador border using special forces support, helicopters, boats, and drones.

🚨 BREAKING: President Trump is now going ALL-OUT on the cartels in Ecuador after their new right-wing President Daniel Noboa gave the US Pentagon a greenlight

THAT’S how you do it. Mexico should do the same, President Sheinbaum should STOP catering to the cartels! 🔥 pic.twitter.com/KLZ3je4tzN

— Eric Daugherty (@EricLDaugh) March 30, 2026

Ecuadorian President Daniel Noboa has invited US assistance, including intelligence and kinetic actions, as part of a broader 17-country alliance Trump launched at the Shield of the Americas summit.

This builds directly on Trump’s consistent stance against the cartels. As we reported earlier, Trump hinted at military strikes, noting “we know their front door”

Plans for ground troops and drone strikes in Mexico were also floated:

Former Green Berets have pointed out that Trump could unleash elite units like Delta Force.

While border czar Tom Homan has repeatedly emphasized that US special operations forces will wipe out the cartels.

The contrast with Mexico remains glaring. President Claudia Sheinbaum has resisted deeper US involvement, drawing criticism for appearing to prioritize other concerns over dismantling the networks.

Trump’s approach extends across the region. Venezuelan exiles hailed the raid that removed Nicholas Maduro as essential, with no alternative but to smash the cartel-linked regime.

Trump also suggested a military operation against Colombia’s President Petro could make sense in the context of dealing with a cocaine-linked leader.

Democrats have criticised Trump’s Venezuela action, totally ignoring the fact that for years the likes of Chuck Schumer and Joe Biden advocated for the exact same policy of using a strike force to crush the cartels:

Decades of weak enforcement allowed the problem to fester. Now, with willing partners like Ecuador under Noboa, real pressure is being applied.

By forming coalitions with leaders who refuse to tolerate cartel safe havens, Trump is delivering results where hesitation and open-border policies previously failed. The cartels thrive on weakness; they fold under sustained, coordinated force.

As more nations join the effort, the days of cartel impunity across the hemisphere are coming to an end.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Thu, 04/02/2026 – 06:30

https://www.zerohedge.com/geopolitical/trump-about-crush-cartels-ecuador

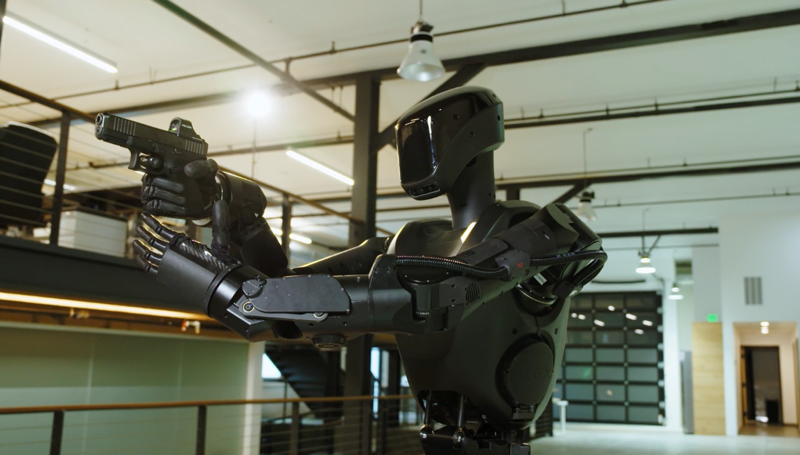

Watch: Armed Robot Dog Leads Close-Quarters Combat Drill

Watch: Armed Robot Dog Leads Close-Quarters Combat Drill

A video circulating on X appears to show a close-quarters battle exercise, possibly involving the Chinese military, in which a heavily armed quadruped robot is used for clearing of rooms and hallways.

A private company in Shandong, China, demonstrated the correct use of robotic “wolves” and drones: they first provide fire suppression, then soldiers advance.

I think the only shortcoming of the robotic wolves is that they don’t perform flanking maneuvers and are not yet smart… pic.twitter.com/QCgWIsS7xh

— China pulse 🇨🇳 (@Eng_china5) April 1, 2026

The big takeaway is that militaries from Ukraine to Russia to China and even the US are increasingly trying to push machines, robotic dogs, FPVs, and ground bots, into the most dangerous confined spaces before troops follow.

However, not everyone is impressed…

the quadruped is real but for now it would have been stopped

(1) it is not serious about clearing corners

(2) it aims by making small leg adjustments

(3) how good is it at aiming high or low?

(4) its chassis will show before the weapon can fire

(5) the squad in this video is… pic.twitter.com/o7OB65WcPi

— GROMPIYE (@civic_cat) April 1, 2026

That shift in letting robots handle the most dangerous jobs on the battlefield is already underway, and soon they will be clearing hallways, stairwells, tunnels, and rooms. These remain some of the deadliest areas on the modern battlefield, where first entry often means first casualties.

As we recently noted, Mike LeBlanc, co-founder of the humanoid robotics company Foundation, said its Phantom MK1 has been trained to breach rooms and other high-risk, enclosed environments ahead of human operators.

LeBlanc said, “The future of conflict is already here – our adversaries will use robots. The only real decision is whether we build and deploy systems to counter them, or ask someone’s son to do that job instead.”

Tyler Durden

Thu, 04/02/2026 – 05:45

https://www.zerohedge.com/ai/watch-armed-robot-dog-leads-close-quarters-combat-drill

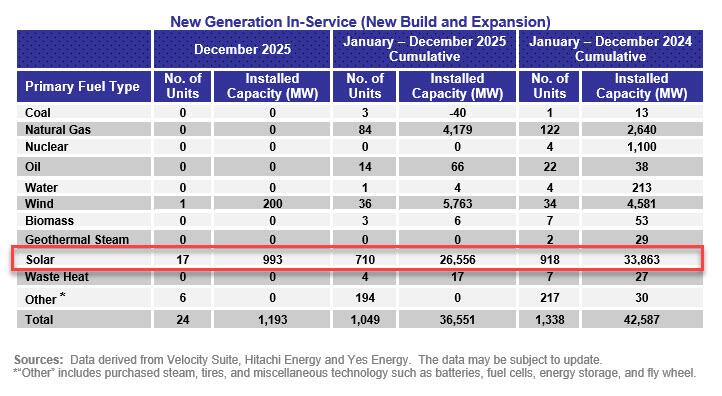

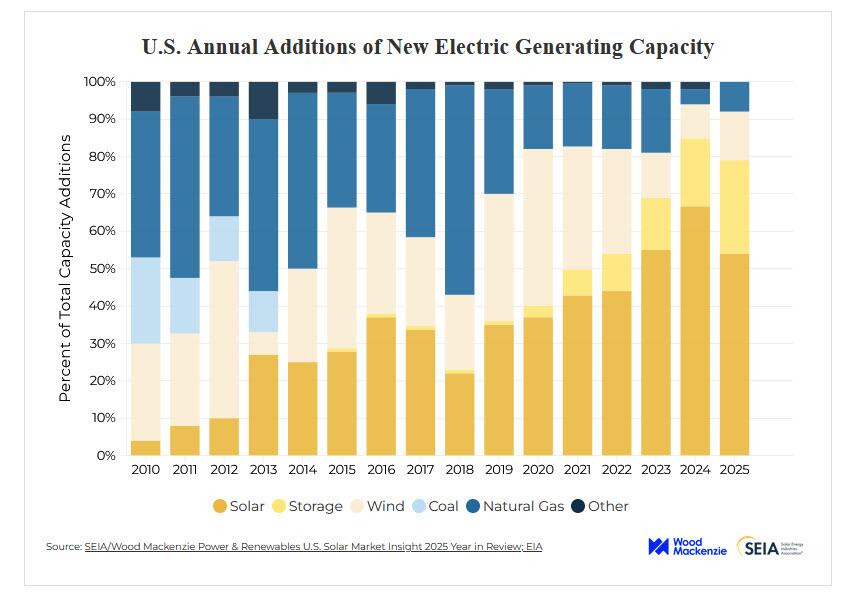

Solar Installations Fell 22% In 2025

Solar Installations Fell 22% In 2025

By Diana DiGangi of UtilityDive,

Solar developers installed 26.5 GW last year, down 22% from the 33.8 GW they installed in 2024, according to the Federal Energy Regulatory Commission (FERC).

The decline in solar installations took place despite the ongoing rush to bring projects online in order to qualify for the Inflation Reduction Act tax credits, which had their timelines curtailed by the One Big Beautiful Bill Act.

Despite this decrease, solar still led all other generation sources in 2025 installations. As of December, solar now makes up 12.2% of installed generating capacity in the U.S., according to FERC — trailing only natural gas, at 42.2%, and coal, at 14.3%.

SEIA noted that in the first three quarters of 2025, solar installations remained largely the same year over year, “but in the fourth quarter, volumes fell by nearly 40% year-over-year. By the end of 2025, installations totaled just under 35 GW as many utility-scale projects were delayed into 2026 and 2027.”

“As developers shifted their focus towards safe harbor strategies, there was less urgency to bring late-stage projects online by year end,” SEIA said. “This weakened fourth quarter deployment but created a more robust near-term pipeline for 2026 and 2027.”

FERC’s data shows that natural gas added fewer units in 2025 — 84, compared with to 122 the previous year — despite a 1.5 GW increase in installed capacity. Wind capacity also grew as developers added 5.7 GW in 2025 compared with 4.5 GW the previous year. No new nuclear capacity came online in 2025. U.S. nuclear capacity increased 1.1 GW in 2024, when Plant Vogtle Unit 4 came online in April that year.

In 2025, the U.S. solar industry “navigated unprecedented change, ranging from numerous trade actions to the reversal of renewable energy tax credit policy,” the Solar Energy Industries Association said in a March 9 report. “Many projects stayed on track, but the market and policy uncertainty took a toll, leading to project delays and cancellations across all segments.”

Tyler Durden

Thu, 04/02/2026 – 05:00

https://www.zerohedge.com/energy/solar-installations-fell-22-2025

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}