Category: News

The Four Iran War End-Games Revisited, And The Peak Pressure Points

The Four Iran War End-Games Revisited, And The Peak Pressure Points

Submitted By Peter Tchir of Academy Securities

A Yogi Berra Kind of Weekend

There is something special about “home openers.” The baseball season can drag on, but the home opener is such a great reminder that summer is on the way and that the possibility of winning it all remains in your reach. Maybe that is why I have Yogi Berra on my mind.

Or maybe, and far more likely, it is because a lot of recent discussions seem to lend themselves well to Yogi-isms. It is easy to start a conversation with a mindset of “we are pulling out soon, with a weak deal,” and wind up ending at “we are all-in” for a final victory. And vice versa.

It ain’t over ‘til it’s over.

When you come to a fork in the road, take it.

I didn’t really say everything I said.

The future ain’t what it used to be.

To name a few.

On Wednesday we published our take on the likely and possible paths we would be on after the Presidential Address. After the address, all we could say was – all the paths are still in play. If that isn’t in the realm of Yogi Berra, nothing is.

Media and Academy’s Podcast

On Friday, after the More Strange than Strong jobs report, Academy was on Bloomberg TV. The Academy segment starts at the 1:52:40 mark. It isn’t important that I wore a pink shirt and purple tie for the Easter weekend, it was important that the 2nd half of the interview was very focused on the conflict in Iran. The hosts were incredibly complimentary of Academy’s Podcast, so it seems like a good time to provide you with the links to our podcasts.

End State and Timing

It is so easy to get twisted in circles on the subject of where this conflict is going. One moment it seems like there might be cooperation to open the Strait. The next moment, more infrastructure in Iran and the region is being hit.

The “four” end conditions that we see are:

No Deal. The U.S. just pulls out, without any real political change. The message will be – we broke it again (even more than in June 2025) and we will continue to break it if we have to. You will hear the phrase “mowing the lawn” over and over until you are numb as to what that really means for the region. This is a very bad outcome for the U.S. and for the world.

If this is the outcome, almost irrespective of whether we get there tomorrow, next week, or a month from now, there will be dramatic power shifts in the region. Countries across the globe will rethink many of their political alignments. Remember when we wrote, back in early February, Molotov Cocktails, Volatility, and Stability (well before the U.S. vs Iran conflict started)? This would leave the region with Molotov cocktails everywhere, just waiting to be ignited.

A Weak Deal. It could be the terms of the deal. It could be who, in Iran, is on the other side of the deal. It could be the ability to really monitor/enforce that the terms of the deal are being abided by. It could just be that it leaves the risk of “mowing the lawn,” in the relatively near-term, as highly likely. Also, if there is no deal to officially open the Strait, the U.S. would be in a very difficult position, making it harder to claim a win. It could be some combination of all of the above. Basically, it is a “deal” that the admin tries hard to sell as a “win” that most of the U.S. (and probably the entirety of the rest of the world) doesn’t see as a win at all. This is better than no deal, but only marginally so.

Timing probably matters here, a little bit. A weak deal today, while not particularly good, is probably easier to sell as a win today, than it will be a few weeks down the road. Veni, Vidi, Vici. It is easier to spin the “we came, we saw, we conquered” nature of this sort of deal today. The more damage that is done in the region, the more difficult it will be to claim victory. The longer that fighting continues and this is the “best” we can get, the more questions will be raised about what actually happened behind the scenes. Not good for global stability.

A Strong Deal. Everything that a weak deal is not. Negotiated with someone clearly in power in Iran for the foreseeable future. Steps taken to reduce the threats from missiles and nuclear weapons going forward that have teeth and an enforcement mechanism that seems viable. It could include protections for the people of Iran. It could include (though this seems less likely by the day) provisions to open the country to investment by American businesses (which would be part of shaping the regime longer-term). This would have to include a deal on the nuclear program as well as a turnover of the Iranian nuclear material. A really, really, really good win.

The sooner the better, but timing isn’t crucial. The longer it takes to reach this end state, the worse shape the global economy will be in. The supply chain disruptions, already occurring, will continue. Problems will compound. Presumably, the longer things go on, the worse the damage to infrastructure in the region will be. Sooner is better, but only at the margin.

Complete Victory. Some sort of uprising. Something where nascent signs of insurrection (which were seen in January and February – with “mysterious” fires and other things in Iran) reveal themselves. Where we wind up with true regime change. An Iran that no longer threatens not just Israel and the U.S., but also anyone it considers to be standing in its way. This is a country, the GIG generally agrees, is the one nation most likely to use nuclear weapons if they manage to get them. The balance of power between “good” and “evil” will have shifted dramatically. This would be a great outcome for the admin and the world!

This is by far the most dangerous timeline. Ideally countries in the region and across the globe support the effort. Enhancing capabilities while spreading the risk. But it is difficult to see this achieved in a “2 to 3” week timeframe. Not that it is impossible, but it is just unlikely. It is also difficult to see this occurring without a serious uptick in casualties. It seems awful to have people pay the price for this success. It will affect friends, families, neighbors, and colleagues. Yet, while I have no military experience, that has often been the cost of changing the world for the better. This outcome is likely to come only with a lot of soul-searching and risk. Having said that, the outcome changes things dramatically. It was in 2002 (almost 25 years ago) that President Bush delivered his “Axis of Evil” speech. The magnitude of what this potentially does in terms of a safer world is difficult to overstate.

The Pressure Points

The U.S. is applying key pressure points on Iran:

Systematically eliminating their ability to wreak havoc. Degrading their military and their ability to resupply themselves is the main pressure point the U.S. and Israel are exerting. Only Iran knows what capabilities they have left, but the more we destroy things, the worse shape they are in, at least with respect to continuing the fighting.

Hitting their economy and their will to fight. So far it is unclear how much damage we have done to their economy. Their economy was always clandestine, and they should have been prepared for this, so putting a length of time on economic conditions forcing Iran to the table is very difficult. So far, we haven’t gone “all in” on this path (like taking Kharg Island) but look for increased focus on economic pressure points in Iran.

Iran is applying key pressure points on the U.S.:

Economic hardship. Affordability. Is the U.S. willing to continue to fight a conflict that was not sold well to the nation initially (the admin has improved on this front lately) and is causing problems at home? This is the main pressure point Iran has. Basically, betting that America doesn’t have the fortitude to withstand economic challenges, even if, in the grand scheme of things, those challenges are small and short in duration. That is the main pressure point.

The Iranian Proxies.

So far the proxies have been quiet. The Houthis started firing some missiles as Isreal, but so far have not tried to deter shipping through the Red Sea. The proxies may not have faith in Iran’s ability to support them going forward, so they are laying relatively low. So much damage was done to the proxies that they don’t have the ability to do much damage this time around. Both of those are probable, which is good. The tail risk is that they are waiting to choose a “time and place” that maximizes whatever they have left.

U.S. casualties. Ultimately this pressure point depends on the steps the U.S. military takes. If the attacks remain primarily “standoff” as opposed to boots on the ground, the American casualties can be kept small. But any casualty gives much of the country cause for concern and causes some domestic pressure to end things. More casualties, which is almost a certainty if the U.S. enters a “boots on the ground” phase, will turn that concern into a cacophony of people calling to end the war. This is ultimately a more powerful pressure point than the economy, but fortunately, is at least partially out of Iran’s control, since it is dependent on the types of attacks the U.S. deploys.

Both Sides Trying to Apply Pressure:

NATO has done very little to aid the effort. In some cases, even restricting airspace. Iran seems to be trying to negotiate “safe passage” for tankers headed to countries that do not help the U.S. All of this is designed to “drive a wedge” between the U.S. and traditional allies. The admin has taken a relatively aggressive posture with those allies, and that doesn’t seem to be helping.

The Gulf Countries. At the start of the conflict Iran attacked many of these countries. They did target American bases more than anything else, but it turned the Gulf against Iran. That continues to be the status quo. On an almost daily basis I see stories about potential military commitments from countries in the region. That would be good (though there are questions about their training and readiness). At the same time there are risks that their attitude changes and they “just want out” of the current state of affairs, even if it leaves Iran as a threat. Not seeing that yet, but…

This is an incredibly tense moment for all those in power.

More Background

While things have been evolving rapidly, last weeks From Economist to Military Strategist, Another Manic Monday, and Ceasefire Negotiations are worth reading as they highlight not just the framework about how Academy is thinking about the conflict, but also how we’ve been adapting and changing as the information unfolds.

Vertically Integrated Countries

One outcome of the war will be more Vertically Integrated Countries, which aligns with our ProSec thesis.

Bottom Line

The “sell” everything risk remains high. Bonds are just not behaving as “Safe Havens” when countries need to spend more on energy and everything derived from energy, and are also likely to have to ramp up their defense spending!

The best outcomes, as we see them, are likely going to take time. Time is not the friend of markets right now. The “easiest” way to extend the relief rally with another big pop in stock and bond prices, is likely to be the “least good” from a longer-term perspective.

It is incredibly difficult. It seems that the admin does pay attention to the stock market as some sort of metric. Weirdly, that might not be helping as it makes it extremely difficult to judge the real direction vs what is just something designed to help the market near-term. The “fog of war” is real and while this is unsettling for markets, it is hopefully equally unsettling for the Iranian regime.

Hope you are enjoying this long weekend (for those who had Friday off) and are prepared for next week! Which will likely start with another “green dot” Sunday and then Academy kicks off the week at 5:45am ET on CNBC.

And let’s finish with more words of wisdom from Yogi Berra – “If the world were perfect, It wouldn’t be.”

Tyler Durden

Sun, 04/05/2026 – 15:30

https://www.zerohedge.com/geopolitical/four-iran-war-end-games-revisited-and-peak-pressure-points

Feds Clear Path To Keep California’s Last Nuclear Power Plant Open For 20 More Years

Feds Clear Path To Keep California’s Last Nuclear Power Plant Open For 20 More Years

Federal regulators have approved keeping the Diablo Canyon nuclear plant running for decades longer, granting 20-year license renewals for its two reactors, according to Yahoo/San Fran Chronicle.

Located on the San Luis Obispo County coast, Unit 1 is now cleared to operate through 2044 and Unit 2 through 2045.

The decision marks a significant win for Gov. Gavin Newsom, who pushed in 2022 to delay the facility’s closure in order to avoid power shortages during California’s transition to renewable energy. Diablo Canyon supplies roughly 9% of the state’s electricity and about 17% of its carbon-free power.

Newsom said the extension supports grid reliability and helps the state handle extreme weather while maintaining an affordable and resilient energy system.

The report says that even with federal approval, the plant’s long-term future still depends on state action. Current California law only allows operations through 2030, so lawmakers would need to pass new legislation for the plant to run beyond that date.

The extension remains controversial. Pacific Gas & Electric estimates customers will pay around $7.6 billion to keep the plant open through 2030, drawing criticism from consumer advocates and environmental groups. Critics also point to concerns about earthquake risks and the plant’s seawater cooling system, which uses large volumes of ocean water.

Federal regulators concluded the environmental impact of continued operation would be minimal, though opposition groups continue to raise safety and environmental concerns.

* * * Order Rancher-Direct tonight. $25 shipping now on most items.

Tyler Durden

Sun, 04/05/2026 – 14:55

Trump Seeks $152 Million To Reopen Alcatraz Prison

Trump Seeks $152 Million To Reopen Alcatraz Prison

Authored by Kimberley Hayek via The Epoch Times,

The White House on Friday requested $152 million to reopen Alcatraz, which is offshore from San Francisco, as a federal prison.

The funding appears in the proposed budget for fiscal year 2027, released by the administration.

It would cover first-year costs for the Federal Bureau of Prisons to rebuild the island facility into “a state-of-the-art secure prison facility,” according to the document. Alcatraz has operated as a National Park Service tourist site since 1973, after the federal prison closed in 1963.

The request directly advances President Donald Trump’s earlier call to restore the prison. Congress treats such budget proposals as suggestions rather than guaranteed spending.

Trump first directed federal agencies to revive Alcatraz in May 2025.

In a social media post that month, he instructed the Bureau of Prisons, the Department of Justice, and other agencies to “reopen a substantially enlarged and rebuilt Alcatraz, to house America’s most ruthless and violent Offenders.”

Trump said the project is a “symbol of law, order, and justice.”

The plan drew both support from those favoring tougher crime policies and resistance from Democrats concerned about costs and the island’s current use as a tourist attraction.

“It would also be a financial boondoggle—not just the massive amount it would cost to reopen Alcatraz as a prison, but all the money and goodwill the park service would lose from closing one of America’s most popular tourist destinations,” Rep. Jared Huffman (D-Calif.) said in a statement in July 2025.

Alcatraz Island sits 1.25 miles offshore in San Francisco Bay. The current facility is 960,000 square feet, nearly the size of 17 football fields. Its frigid waters and powerful currents made it one of the nation’s most secure prisons during its operation. No successful escapes were ever officially recorded, though five inmates were listed as missing and presumed drowned. Alcatraz opened as a federal prison in 1934 and quickly earned a reputation for holding the country’s most notorious criminals.

Famous inmates included Chicago gangster Al Capone, Boston mobster James “Whitey” Bulger, and George “Machine Gun” Kelly. The Bureau of Prisons closed the facility in 1963, citing operating costs nearly three times higher than those of any other federal prison. The National Park Service later took control of it, and it became a popular tourist destination visited by more than a million people each year.

Trump’s current push revives a site long viewed as escape-proof. The latest budget request marks the first concrete federal funding step toward converting the island back into an active maximum-security prison.

Lawmakers will now review the proposal as part of broader spending negotiations.

Tyler Durden

Sun, 04/05/2026 – 14:20

https://www.zerohedge.com/political/trump-seeks-152-million-reopen-alcatraz-prison

The New York Times Made A Humiliating Error, And Trump Is Just Loving It

The New York Times Made A Humiliating Error, And Trump Is Just Loving It

Authored by Matt Margolis via PJ Media,

The New York Times set out Friday to embarrass President Donald Trump over his hardline stance on NATO. It wound up spectacularly backfiring on them.

Several NATO nations have declined to join a U.S.-Israel military operation targeting Iran. Alliance members also refused Trump’s requests to deploy their forces to reopen the Strait of Hormuz, much to the chagrin of President Trump, who figures that if NATO allies won’t help the United States, then the alliance has become meaningless.

So the paper ran a piece criticizing Trump’s threats to withdraw from the alliance, and the print edition’s headline asked a pointed question: “A North American Treaty Organization Without America?”

There’s just one problem.

NATO stands for the North Atlantic Treaty Organization.

The Times apparently forgot that detail, and, after being mocked on social media, quietly issued a correction through its communications team on X.

A correction will appear in tomorrow’s print edition:

“A headline with an article on Friday about President Trump’s threats to leave NATO misstated the full name of the body. It is the North Atlantic Treaty Organization, not the North American Treaty Organization.”

— NYTimes Communications (@NYTimesPR) April 3, 2026

Trump also joined in on the mocking.

“The Failing New York Times, whose lack of credibility, and their constant Fake News attacks on your favorite President, ME, has caused its circulation to absolutely PLUMMET, referred to our severely weakened and extremely unreliable ‘partner,’ NATO, as the North American Treaty Organization,” Trump wrote in a post on Truth Social Saturday morning. ‘The correct name is the North Atlantic Treaty Organization – A very interesting mistake! The hiring and educational standards have gone way down at the NYT.”

He added, “Bring back, ‘ALL THE NEWS THAT’S FIT TO PRINT’ and, Make America Great Again!”

Here’s what makes this especially painful for the Times. The article wasn’t some throwaway weekend filler. It was a deliberate piece designed to frame Trump as reckless for pushing back against an alliance his critics treat as sacred.

Related: Democrats Are Openly Rooting for Iran to Win the War

“Since his re-election, President Trump has threatened to leave the NATO alliance several times. On Wednesday, he did it again, frustrated that European nations had refused to join the so-far indecisive United States-Israeli war against Iran,” the article began. “But the more he disparages NATO and threatens to abandon it, the more hollow it becomes.”

The alliance, built after World War II to deter the Soviet Union and keep the peace in Europe, is in crisis, with some questioning whether it can survive. The Mideast war has brought existing doubts about American commitment to the alliance to the fore, argued Ivo Daalder, a former American ambassador to NATO.

“It’s hard to see how any European country will now be able and willing to trust the United States to come to its defense,” he said. “Hope, perhaps. But they can’t count on it.”

In his speech to the nation Wednesday night, Mr. Trump did not mention NATO, to the relief of allies.

But a senior European official said he thought most Europeans did not believe that Article 5, the NATO commitment to collective defense, still had teeth. The United States now seems part of the problem of world disorder, the official said, speaking anonymously given the sensitivity of the topic. The country is no longer the solution and the guarantor of last resort, he said.

The whole premise depended on the Times looking like the serious, credentialed adults in the room. Instead, they demonstrated that they didn’t even know the true name of the organization they were defending — right there in the headline, in print, that no amount of corrections can erase.

NATO Secretary General Mark Rutte is scheduled to travel to Washington next week to try to smooth things over with Trump directly.

Tyler Durden

Sun, 04/05/2026 – 13:10

https://www.zerohedge.com/political/new-york-times-made-humiliating-error-and-trump-just-loving-it

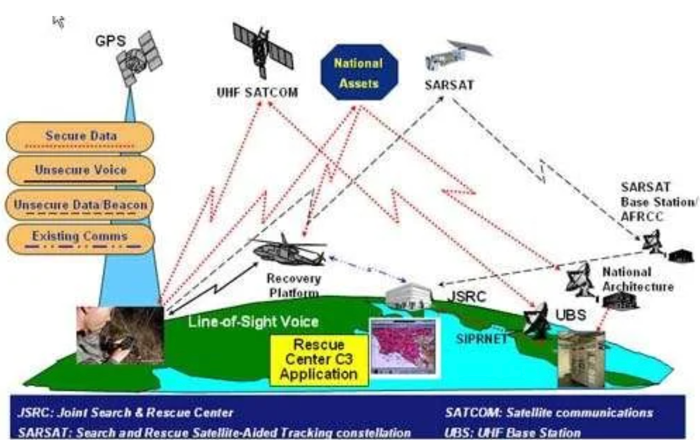

Did This Small Device Help Special Forces Locate Downed F-15 Crew

Did This Small Device Help Special Forces Locate Downed F-15 Crew

The New York Times confirmed that U.S. Special Forces operators were behind the recovery of the second crew member from the downed F-15E fighter jet, locating and extracting the weapons systems officer in a daring overnight mission deep inside Iranian territory.

Confirmed presence of Seal Team 6 in pilot rescue op moved the “US forces entering Iran” market to 100%.

Per NYT: “Navy SEAL Team 6 commandos extracted the officer in a massive operation that involved hundreds of special operations troops and other military personnel.” https://t.co/szkJUBbP5s pic.twitter.com/W05LYaRDBv

— zerohedge (@zerohedge) April 5, 2026

The pilot had been recovered earlier, while the second airman remained hidden from Iranian forces for days as Special Forces operators raced to reach his position before Iranian forces did.

Around 200 soldiers from special operations units participated in the operation, Trump told Axios.

Trump said the Iranian military shot down the F-15 using a shoulder-fired missile. “They got lucky.”

Speaking to Axios an hour after confirming the rescue, Trump said that “thousands of these savages were hunting him down,” using that loaded term to refer to members of the Iranian military.

“Even the population was looking for him. They offered people a bonus if they captured him.”

The officer hid in a crevice in the mountain, Trump said, and the U.S. managed to spot him with its technology.

Trump said that the U.S. military had “beeping information” about the officer’s location.

But after a radio message, officials suspected he might be in Iranian captivity and the Iranians were “sending false signals” to try to lure U.S. forces into a trap.

One of the key devices that appears to have helped the survival and recovery of both pilots was Boeing’s Combat Survivor Evader Locator, or CSEL, a secure communications device that can transmit encrypted location and status bursts without exposing their position to enemy forces.

CSEL is a combat search-and-rescue survival radio system used by downed aircrew. Its purpose is to help rescue forces quickly and securely locate, authenticate, and communicate with a survivor without allowing enemy forces to triangulate the survivor’s position.

Israeli-based Ynetnews provided more context on how critical CSEL was to the survival of both aircrew members and how important it was for location and extraction operations:

To evade Iran’s advanced electronic warfare systems, reportedly supplied by China and Russia, the device uses techniques such as ultra-short burst transmissions and rapid frequency hopping.

These signals appear as random background noise to enemy intercept systems, making them extremely difficult to detect or trace.

The CSEL system relies on military communication satellites to relay data from hostile territory to command centers in the United States and other global bases.

The successful extraction of both the pilot and weapons systems officer deep behind enemy lines offered a rare look into the U.S. military’s doctrine for recovering isolated personnel during combat, otherwise known as Combat Search and Rescue, or CSAR.

Spotted flying at low level over western Iran this morning; a C-295W from the USAF’s 427th Special Operations Squadron, a clandestine unit that reportedly specializes in infiltration and exfiltration into enemy territory. pic.twitter.com/4UfAFj7AQb

— OSINTtechnical (@Osinttechnical) April 5, 2026

How long until a U.S. studio makes a sequel to the 2001 action-war film “Behind Enemy Lines”?

Next year?

Tyler Durden

Sun, 04/05/2026 – 12:35

https://www.zerohedge.com/military/did-small-device-help-special-force-locate-downed-f-15-crew

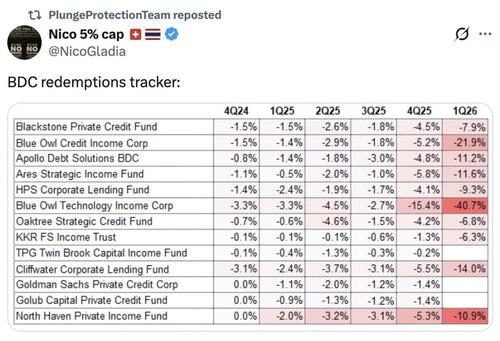

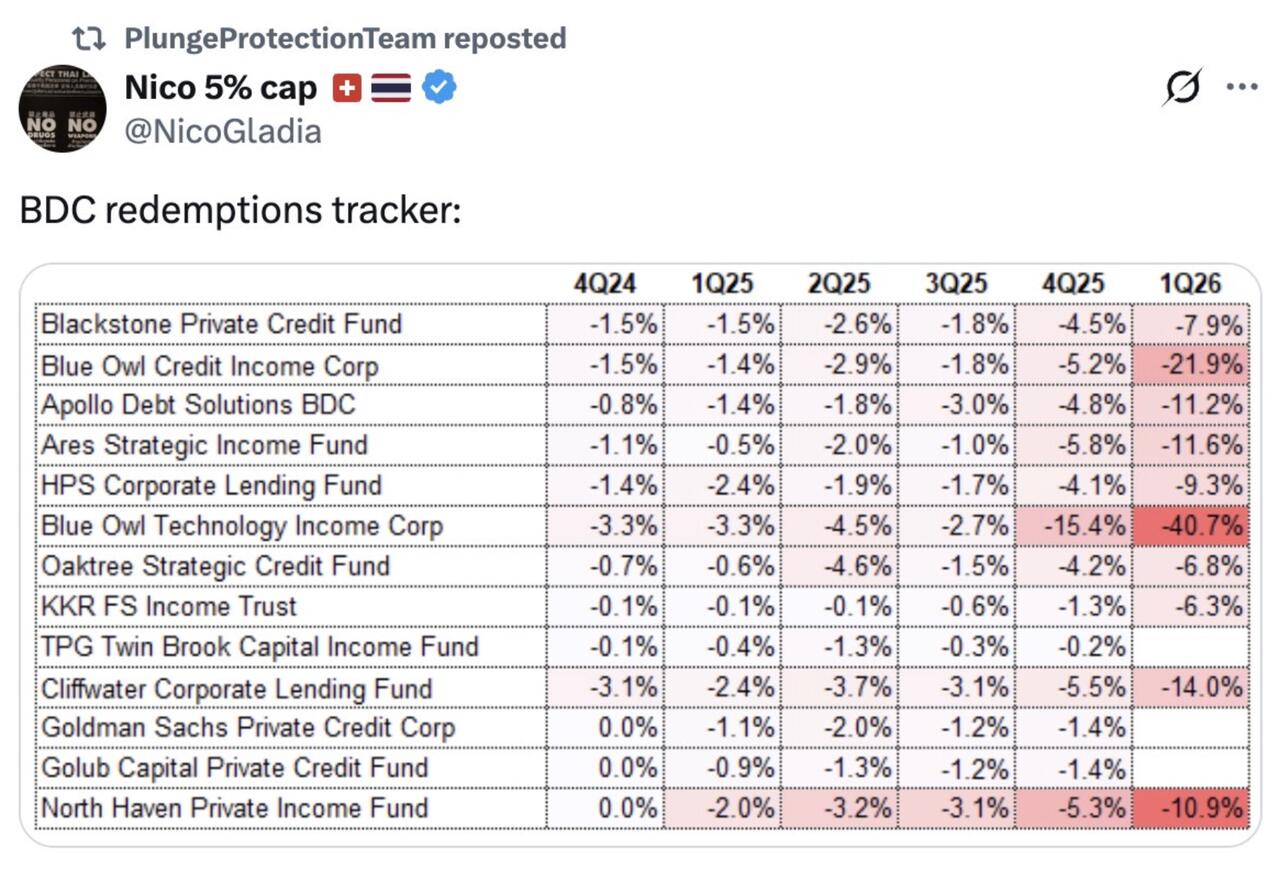

“Unprecedented” Withdrawal Requests Now Hitting Private Credit

“Unprecedented” Withdrawal Requests Now Hitting Private Credit

Submitted by QTR’s Fringe Finance

Late last week it was reported that one private credit company has effectively frozen up under a wave of redemption requests, an abrupt liquidity crunch that will likely do lasting damage to what little credibility it still had with investors.

This is exactly the kind of stress event I’ve been expecting ever since I flagged that psychology in the private credit space was starting to break—and I still believe conditions in private credit will get worse before they get better.

I’ve been flagging the sector as one of ten that I see as an avoid at all costs, and just days ago I wrote that conditions were worse than they appeared on the surface. This latest development only reinforces that view.

According to reporting from Bloomberg, Blue Owl Capital Inc. is now limiting redemptions from two of its flagship private credit funds after facing an unprecedented surge in withdrawal requests in the $1.8 trillion market. Blue Owl shares are down about -40% so far this year.

Investors in the $36 billion Blue Owl Credit Income Corp. asked to redeem 21.9% of shares in the latest quarter (up from 5.2%), while the smaller Blue Owl Technology Income Corp. saw redemption requests spike to a staggering 40.7% (up from 15.4%). This trend is…alarming…

Despite previously meeting withdrawals above their standard limits, the firm is now capping redemptions at 5%, effectively gating investor exits. In practical terms, that means billions in requested withdrawals are not being honored—roughly $3.2 billion remains locked in the larger fund alone.

Recall just days ago I highlighted how things were likely far worse in private credit than they appeared. As I’ve written, investors have already started pulling money, with withdrawals hitting records just as concerns about software exposure and valuation pressure have picked up.

What happens next from here shouldn’t surprise anyone who’s been paying attention. If anything, this is just the beginning. As we move into Q2, expect more massive redemption requests across private credit vehicles as investors digest what gating actually means in practice. Once one fund limits withdrawals, it doesn’t calm nerves, it accelerates the exit impulse elsewhere.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

And to be clear, this is not the bottom, in my opinion. It will get worse before it gets better. The core issue isn’t just fundamentals, it’s psychology. As I’ve been saying, psychology in private credit is already broken. Investors are now realizing that liquidity was never what it seemed, and that realization tends to spread quickly and feed on itself.

That’s why this is not the environment to be stepping in early. Do not try to catch a falling knife here. When structures depend on confidence and that confidence is cracking, price and flows can overshoot to the downside in a way that surprises even seasoned allocators. Personally, I’d avoid all private credit names, BDCs and regional banks and not try and go bottom fishing in this sector.

As I’ve said, at some point, there will likely be a private credit bailout or backstop, whether through policy support, institutional capital, or creative restructuring.

But that doesn’t come early. It comes after things get meaningfully uglier, when the pressure is no longer containable and losses are already visible.

We’re not there yet.

Tracking the private credit meltdown:

March 31, 2026 – WSJ reports that software exposure among private credit funds is larger than disclosed

March 27, 2026 – Cracks in private credit reach UBS Real Estate fund, forced to suspend withdrawals

March 24, 2026 – Ares restricts withdrawals on its Strategic Income Fund after redemption requests hit 11.6%

March 23, 2026 – Apollo caps withdrawals on its $25 billion Apollo Debt Solutions vehicle after redemptions hit 11%

March 19, 2026 – Stone Ridge’s Alternative Lending Risk Premium Fund gates redemptions after overwhelming redemption requests

March 16, 2026 – Apollo co-president says that “all” marks in parts of the private markets industry are “wrong”

March 11, 2026 – Morgan Stanley and Cliffwater cap redemptions in $8 billion, and $33 billion funds, respectively

March 6, 2026 – BlackRock begins limiting withdrawals from its $26 billion HPS Corporate Lending Fund

March 3, 2026 – Blackstone faces “record” redemptions from its flagship private credit vehicle, investors sought to redeem 7.9% of fund’s $82B in assets

February 19, 2026 – Blue Owl restricts redemptions from its retail private credit fund

January 26, 2026 – Blackrock takes 19% markdowns on TCP Capital Corp.

December 17, 2025 – Blue Owl walks away from $10 billion data center deal for Oracle

October 15, 2025 – QTR warns private credit is one of 10 areas of the market that I would avoid heading into 2026

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Sun, 04/05/2026 – 12:00

https://www.zerohedge.com/markets/unprecedented-withdrawal-requests-now-hitting-private-credit

DOE FY27 Budget Requests $45 Billion in Nuclear Funding

DOE FY27 Budget Requests $45 Billion in Nuclear Funding

The White House fiscal year 2027 budget proposal has requested almost $54 billion for the Department of Energy in fiscal year 2027, with almost 80% of that funding going towards nuclear energy and nuclear deterrent programs. The funding request represents a nearly $5 billion increase from 2026 levels.

Outside of the $32.8 billion in funding requested for the National Nuclear Security Administration (NNSA), the Trump admin cites a $2.7 billion reduction in funding requests achieved by “slashing Green New Scam initiatives and rooting out woke diversity, equity, and inclusion (DEI) programs”.

The NNSA receives a $3.6 billion (12%) increase from the prior year. The request supports warhead modernization, infrastructure recapitalization, life-extension programs, next-generation naval reactor technology, and nuclear emergency response teams.

These defense nuclear activities also advance high-assay low-enriched uranium ((HALEU) production with direct benefits for commercial reactor fuel supply chains.

Environmental Management is funded at $8.2 billion, down $386 million from the enacted level. The program addresses legacy radioactive waste and contamination at former Manhattan Project and Cold War weapons sites. Approximately $3 billion targets the Hanford site in Washington state for continued operation of the Direct Feed Low-Activity Waste Facility and other near-term cleanup milestones. The initiatives reduce long-term federal liability and clear land for potential future nuclear or industrial reuse.

The budget makes a specific call out for an additional $3.5 billion to “rapidly deploy firm baseload power”. No further explanations are given for what exactly is covered under this initiative, but it is assumed to be a combination of nuclear energy and geothermal power-related programs. The DOE and its various offices have issued multiple award programs to kickstart the expansion of two of the current administration’s preferred power generation methods.

The $53.9 billion figure captures the entire department request while nuclear security, cleanup, and energy investments form the dominant share. Civilian nuclear energy programs such as advanced reactor demonstrations and fuel-cycle work appear folded into the non-NNSA portion or supported through targeted baseload funding.

The proposal continues the pattern of prioritizing nuclear deterrence and legacy stewardship even as other energy accounts face reductions or proposed cancellations.

Tyler Durden

Sun, 04/05/2026 – 11:40

https://www.zerohedge.com/energy/doe-fy27-budget-requests-45-billion-nuclear-funding

Eisen Vs Every ‘Trumper’: There Is Quite A Battle Shaping-Up…

Eisen Vs Every ‘Trumper’: There Is Quite A Battle Shaping-Up…

Authored by James Howard Kunstler,

The Red Line

“The ends must justify the means — the only question is what means are necessary.”

– Saul Alinsky

Why do the news anchor ladies of CNN, Erin Burnett, Kate Bolduan, always look so depressed on the air? They never smile. Their faces always register something between grave concern and hysteria. Is it the network’s cratered ratings? The pending hostile takeover by Paramount / Skydance (led by conservative David Ellison)? Too much botox, zombifying the small facial muscles? Or is it self-loathing from being compelled to slant everything they report on in the direction of a lie?

There does seem to be some hidden hand in Narrative Central issuing prescribed story-lines to the networks, and that hand seems to be tinged with malice for anything and anyone seeking to rescue our country from chaos, penury, psychosis, and jihad. It looks like the hidden hand wants the country to go down in flames, and will resort to any means necessary to get it done. The template for that is so-called “color revolution,” which is a hyper-accelerated version of “Red Rudi” Dutschke’s “march through the institutions” to “capture the transmitters of culture” so as to produce a communist utopia, as cribbed from the writings of Antonio Gramsci, (1891 – 1937) founder of the Italian communist party.

The fascist Mussolini tossed Gramsci in jail where he scribbled three thousand pages of his Prison Notebooks, in which he laid out his strategy for destroying civil society, later adapted by the Americans Saul Alinsky (1909-1972) in his Rules for Radicals and Gene Sharp (1928-2018), who penned several concise manuals of strategic mechanics for dismantling targeted governments.

These are the mentors of chief Lawfare ninja Norm Eisen, who has made a specialty of marching through the institution of American law in order to advance the agenda of the Democratic Party allied with cohorts of the permanent Washington bureaucracy (or Deep State) to fend off any challenge to the corruption and racketeering embedded in those two symbionts.

The challenge obviously presents in the form of Donald Trump, the once and current president battling an increasingly rabid set of opponents. Norm Eisen has been deeply involved in every attempt to undermine and disable Mr. Trump since 2016. He wrote briefs for the Mueller Special Counsel operation; he acted as prosecutor in Trump’s impeachment # 1 (prompted by CIA agent and so-called “whistleblower” Eric Ciaramella, as facilitated by then Rep. Adam Schiff); he assisted ex parte in the House Jan 6 Committee proceedings; he prepared legal arguments for the Fani Willis prosecution of Mr. Trump and 18 co-defendants; and he helped construct the legal framework for Special Counsel Jack Smith’s cases against Mr. Trump. In short, Norm Eisen spent the past decade laboring to brand Donald Trump as a criminal and shove him out of the political arena. His efforts failed.

Norm Eisen founded or is associated with several swamp NGOs active in Trump-hunting operations, including Citizens for Responsibility and Ethics in Washington (CREW), the States United Democracy Center, the Democracy Defenders Fund, Democracy Defenders Action — all posing as anti-autocracy operations. Eisen and his orgs have filed hundreds of lawsuits against the Trump administration to obstruct any initiative the President advances to stop Democratic Party sanctioned grift, deport illegal aliens ushered in during the “Joe Biden” years, and especially to derail investigations of election fraud. These orgs are well-funded by George Soros’s Open Society NGO and its spinoffs, Arabella Advisors (rebranded as Sunflower Services), the Tides Foundation, that is, the usual suspects.

In the face of all that, plus a dysfunctional Congress and a hostile federal judiciary, the President has struggled to find work-arounds for every piece of the agenda he was elected to carry out. What can be done about it? Even if evidence was produced to show that Norm Eisen acted improperly in the cases brought against the President, it is unlikely that a case brought against Norm Eisen would get any traction in a DC district federal court. He is a longstanding friend of James “Jeb” Boasberg, Chief Judge of the DC District. Norm Eisen was in the same 1991 class at Harvard Law School as Barack Obama, an architect of the Left’s movement to destroy the Republic.

All of this suggests that if Mr. Trump needs to accomplish something critical, such as basic reform of our election procedures, and if any of his executive orders are thwarted by Norm Eisen-backed lawsuits for judicial nullification of executive powers, Mr. Trump will have to declare some kind of extraordinary national emergency. That will be the red-line that Norm Eisen has been seeking for ten years: his chance to brand Mr. Trump as a “tyrant” and commence a new impeachment effort, in theory coinciding with the seating of a Democratic Party majority in both houses of Congress.

This is quite a battle shaping up. Norm Eisen has been adroit to a fault in all his nefarious endeavors.

But then, Mr. Trump has performed as a veritable Scarlet Pimpernel of American politics, ruthless, resourceful, self-consciously comical, and genuinely motivated to save the USA from a cabal of prodigious villains.

He is in it to win it. His crowning achievement might be getting the morose ladies of CNN to finally crack a smile.

Tyler Durden

Sun, 04/05/2026 – 11:05

https://www.zerohedge.com/political/there-quite-battle-shaping

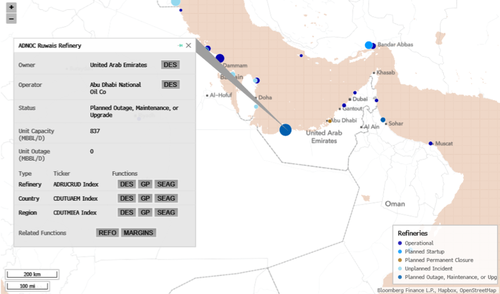

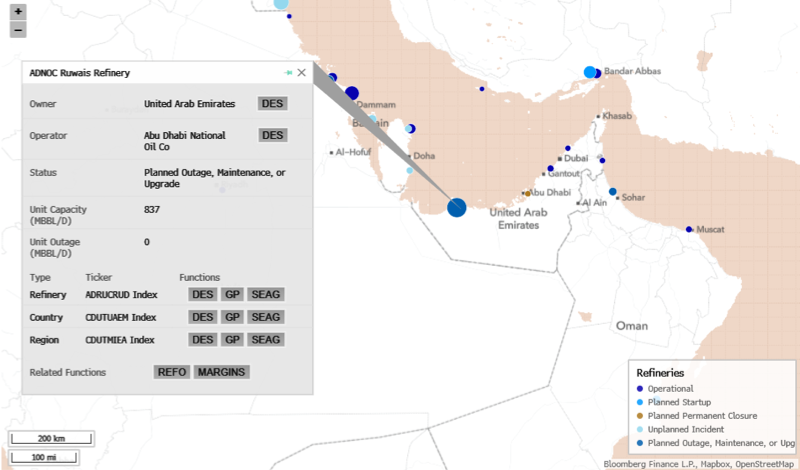

Global Plastics Supply Chains Further Pressured As Abu Dhabi Petrochemicals Plant “Suspended” After Attack

Global Plastics Supply Chains Further Pressured As Abu Dhabi Petrochemicals Plant “Suspended” After Attack

One of the UAE’s key petrochemical hubs halted operations early Sunday after falling debris from an air-defense interception sparked multiple fires. The incident adds to a growing list of disruptions across Gulf petrochemical infrastructure, highlighting major risks and potential incoming disruptions to the global supply chain for critical inputs used to make plastics.

Abu Dhabi authorities are responding to multiple fires in Borouge petrochemicals plant, caused by falling debris following successful interceptions by air defence systems.

Operations at the facility have been immediately suspended while damage is assessed. No injuries have been…

— مكتب أبوظبي الإعلامي (@ADMediaOffice) April 5, 2026

Borouge’s Abu Dhabi petrochemicals operations at Al Ruwais Industrial City in the Al Dhafra region halted operations after an attack sparked multiple fires across the plant. The plant produces polyethylene and polypropylene, which are building blocks for plastic manufacturing.

Polyethylene is widely used in packaging films, shrink wrap, heavy-duty sacks, liners, caps and closures, and infrastructure applications such as pipes, as well as in some healthcare packaging. Polypropylene is used in rigid packaging, including food and beverage containers, bottle caps, and housewares, as well as in medical products such as masks, gowns, syringes, catheters, inhalers, and pharmaceutical packaging.

Bloomberg first reported the incident at the petrochemicals plant earlier but provided no details on when the facility would restart operations or whether any critical components were damaged.

There were troubling reports last week that key players in the global plastics manufacturing supply chain declared force majeure due to the limited supply of monoethylene glycol and purified terephthalic acid caused by the heavily disrupted Hormuz chokepoint.

Disruptions reported last week, courtesy of Bloomberg:

Oriental Union Chemical Corp. warned US customers it would temporarily suspend MEG shipments for early March. The suspensions would persist until conditions stabilize, the Taipei-based company wrote in a customer letter. After March 11, shipments to customers continued as normal, with monthly pricing adjusted to reflect higher crude costs, spokesperson Daniel Yu said. Ethylene oxide and ethylene glycol sales are mainly for customers on long-term contracts, he added. As disruptions mount across the industry, Taiwan has moved to boost capacity for ethylene output, according to a report by the semi-official Central News Agency.

Hainan Yisheng Petrochemical Co. declared force majeure “for affected contracts/orders/delivery obligations,” according to a letter sent to US customers. The Chinese maker of PET and PTA flagged disruptions stemming from the Hormuz shutdown.

Indorama Ventures said in an early-March letter from its US and Canada regional sales team that it would raise prices on PET resin by 10 cents a pound across all businesses, citing higher feedstock costs and supply-chain disruptions linked to the Middle East conflict. The company said in a letter sent the following week that it would add an additional temporary 5-cent war surcharge. The company has also declared force majeure on shipments from two PET units in Europe, S&P Global’s Chemweek reported.

Saudi Basic Industries Corp. last week told customers it would invoke force majeure for MEG and diethylene glycol. The duration of the disruptions “cannot be reasonably determined given the evolving nature of the circumstances,” the company said, citing “unforeseen supply chain disruptions in the Strait of Hormuz.”

Last week, Dow CEO Jim Fitterling warned that Gulf petrochemical flows could take upwards of nine months to normalize if the Hormuz chokepoint were to reopen in the near term.

Let’s remind readers that China is the world’s largest producer and consumer of plastics, according to OECD data. Any supply disruption would ripple through the industrial base of the world’s second-largest economy.

Read the key JPMorgan note on how the energy shockwave travels across the world like falling dominoes (read).

Tyler Durden

Sun, 04/05/2026 – 10:30

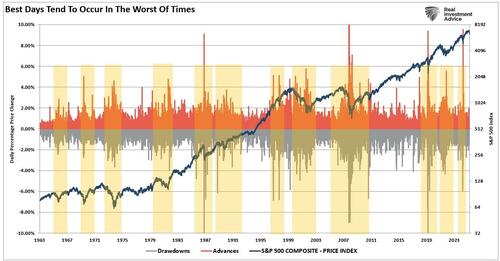

The Reflexive Rally Was Not Surprising

The Reflexive Rally Was Not Surprising

Authored by Lance Roberts via RealInvestmentAdvice.com,

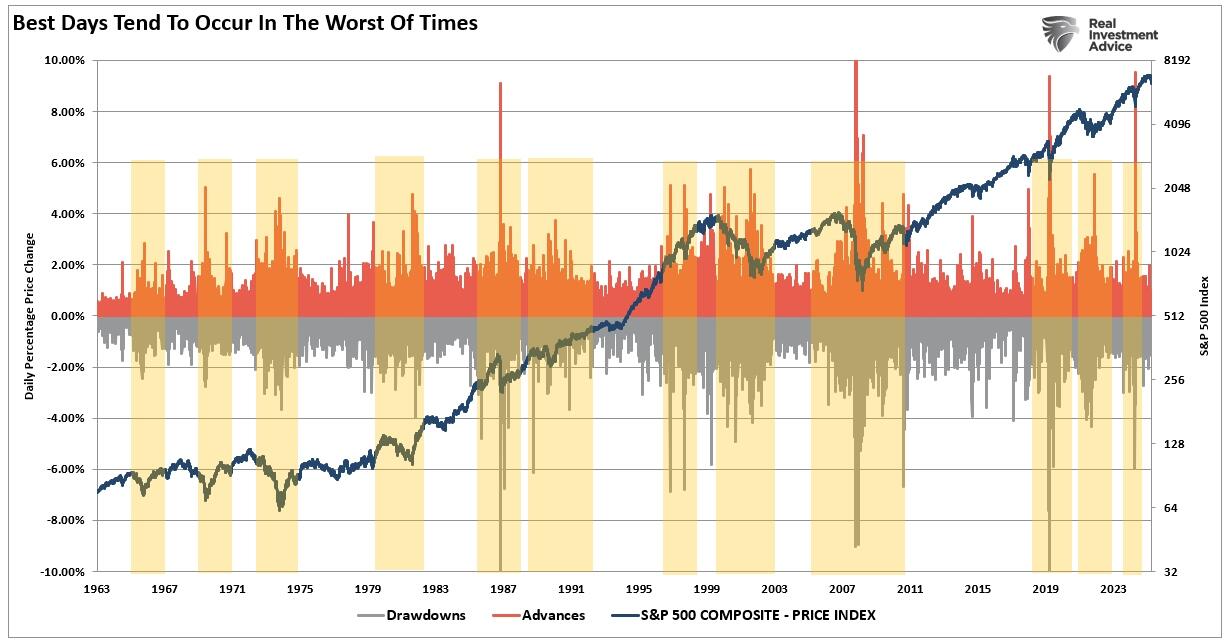

The market rallied on Tuesday and Wednesday, with Tuesday’s rally one of the best trading days since 2022. However, that should also be unsurprising, since the best trading days tend to cluster with the worst market periods. As we noted in Stock Market Breadth on Monday:

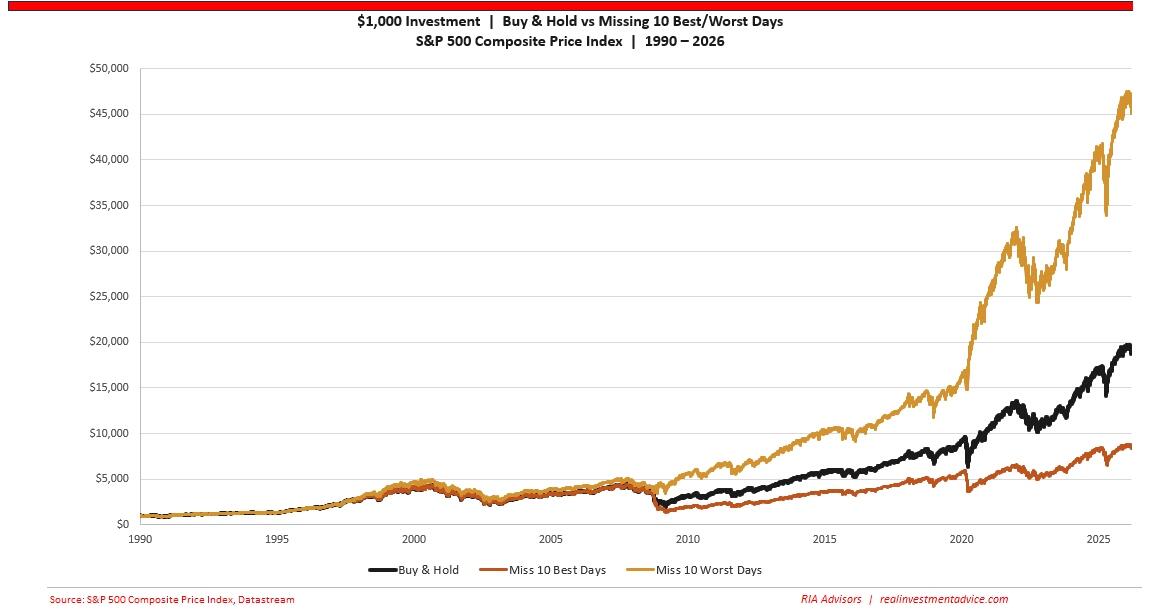

“The single most damaging decision most investors make during periods of falling stock market breadth is selling. The data on this is unambiguous. Seven of the market’s 10 best days in any given 20-year period occur within two weeks of the 10 worst days, according to JPMorgan Asset Management research. The best days follow the worst days because fear-driven selling creates dislocations that are rapidly corrected. You can see this in the chart below, that the best and worst days are clustered together.”

In other words, while investors are always told to just “buy and hold” because they will miss the 10-BEST days if they don’t, investors should focus on mitigating the risk of significant capital losses during those periods.

This doesn’t mean you can effectively miss all the bad days; however, given that higher-volatility periods tend to cluster, understanding when to reduce exposure can significantly improve outcomes over time. Even if you miss the 10-best days along the way. That math applies with particular force in setups like the current one. Since 1974, according to data compiled by Clear Perspective Advisors, the S&P 500 has returned more than 24% on average following a market correction. Only 25% of the 48 corrections since World War II have progressed into full bear markets. In other words, there is a 75% chance this correction will not turn into a bear market. However, dismissing that 25% entirely is just as foolish for future outcomes.

This is why the rally this past week was not unexpected. Oversold conditions, exhausted sellers, aggressive short positioning, and algorithmic covering all tend to converge after sustained selling pressure. Goldman’s trading desk noted this week that the capitulation checklist is nearly complete, with the S&P now below all key moving averages and below critical CTA selling thresholds. When those conditions are clear, the snap-back can be sharp. But it’s a trap.

Why do I say that? Because that is what I have learned repeatedly over 35 years of managing money. The rallies that come off oversold extremes are seductive precisely because they feel like confirmation that the worst is over. They’re fast, they’re loud, and they draw in sidelined capital chasing performance. Sentiment indicators flip from extreme fear to cautious optimism in a matter of days.

Bottom line: If the bull case for this rally is ‘stocks were down a lot, and people were scared,’ that’s not a fundamental argument. It’s a positioning argument. It expires quickly.

And in the current environment, the macro headwinds haven’t gone anywhere. Even if the Iranian conflict is resolved on Monday, private credit stress remains, the impact of higher oil and gasoline prices is working its way through the economy, and questions remain about artificial intelligence.

But there is another reason to fade this rally.

Earnings Hit Still Coming

The difference between a durable recovery and a dead-cat bounce is almost always visible in the underlying fundamentals, not the price action alone. Right now, the fundamentals argue for caution.

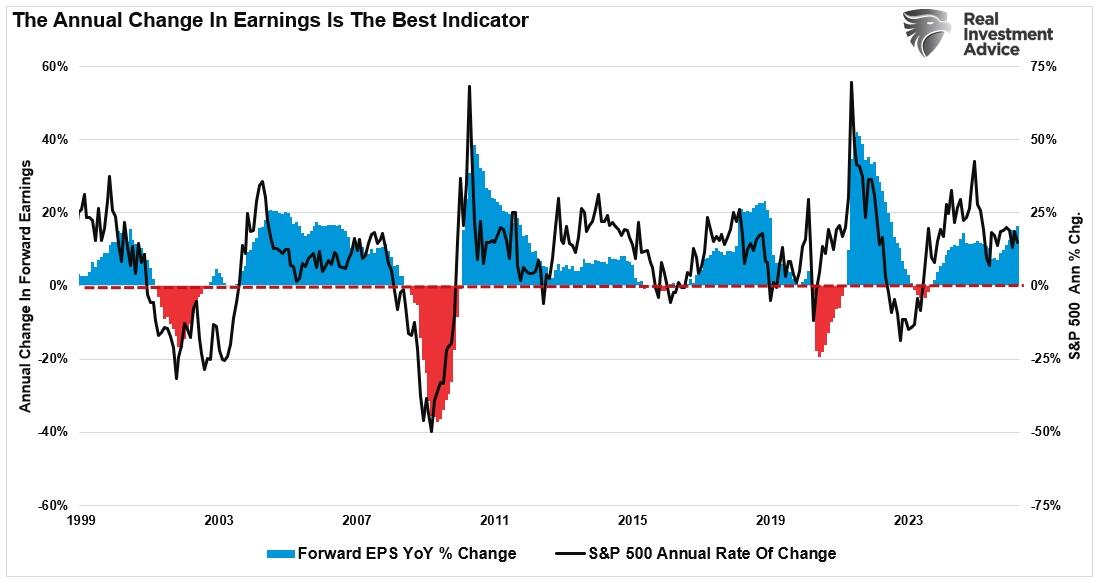

Goldman’s own scenario analysis puts a moderate slowdown path at 6,300 on the S&P 500 and a severe oil-shock path as low as 5,400. Neither of those scenarios is priced into current earnings estimates. S&P 500 companies are still being modeled at roughly $309 per share in earnings for 2026, figures built on assumptions about GDP growth and energy costs that the past eight weeks have materially challenged. When earnings revisions begin in earnest, they tend to hit in waves. We’re likely in the early innings of that process, and it will impact forward returns. The reason is that the market trades off forward earnings expectations; if those expectations fall, the market reprices for lower earnings growth.

Add to that the technical damage. Breaking below the 200-day moving average is not a minor event. Historically, a clean break below that level without a swift recapture has resolved to the downside more often than not. The index now sits below all key moving averages, and the burden of proof has shifted. Bulls need to prove the trend has reversed. Sellers don’t need to prove anything.

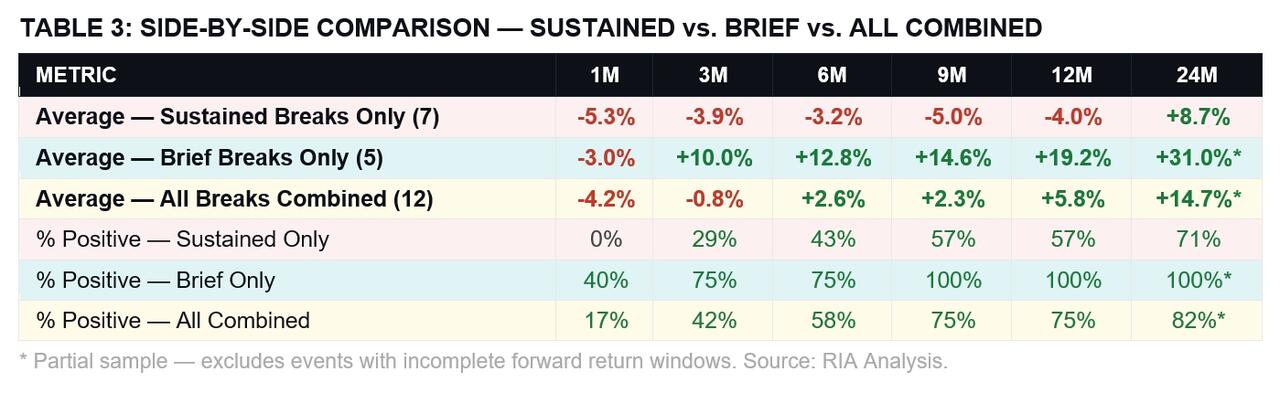

“As shown in the comparative table below, understanding the difference between a sustained break of the 200-dma and one that wasn’t was critical to future returns.” – Break Of The 200-DMA

We are still within the first 4-weeks of the break of the 200-day moving average. The market rally this past week, following those five consecutive weekly declines, doesn’t mean the downside risk is over. If the market fails to climb above that now-critical resistance level, the potential for a retest of recent lows increases.

However, this doesn’t mean you get out of the markets entirely.

So, When Should You Start Accumulating

The one thing that bothers me most about the “Perpetual Purveyors of Doom” is that they repeatedly tell you for years that the market is going to crash. Eventually, they will be correct. However, what they don’t tell you is when to start buying the cataclysm. The voices are currently louder than ever.

However, the current market backdrop is nothing like the catastrophic events of the past, such as the financial crisis or the Dot-com crash. This is a well-needed correction after the massive post-“Liberation Day” rally last summer. Nonetheless, the damage done during declines is always troublesome, but it needs to be kept in perspective.

Yes, we certainly suggest using this rally to cash in and reduce risk. After consecutive weekly declines, a rally was inevitable. However, I am also not saying “sell everything” or “stay in cash indefinitely.” The market will eventually bottom and recover. The reason is that the market will eventually “price in” the risk and begin to look forward. The economy will adapt and begin to grow. As such, the question isn’t whether to own equities, it’s just a question of when and at what price.

There are four specific conditions I want to see before moving from a defensive to a constructive stance. None of them requires perfect clarity. All of them require meaningful evidence.

None of these conditions exists today. They may develop over the coming weeks or months. When they do, I’ll tell you. However, here is how to position for what is likely coming next.

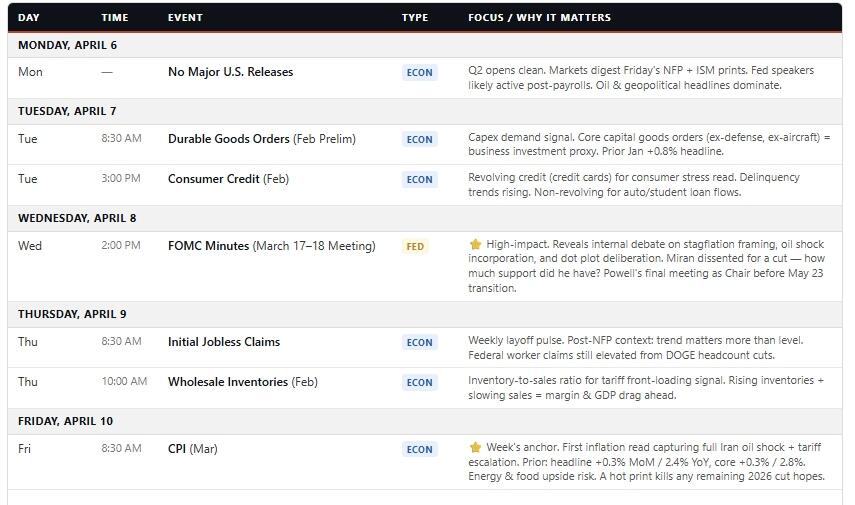

🔑 Key Catalysts Next Week

The first full week of Q2 is book-ended by two events that will define the rate narrative for the next two months: the FOMC Minutes on Wednesday and March CPI on Friday. Everything else is secondary, other than what oil prices are doing.

The March 17–18 FOMC Minutes are the week’s first inflection point, but we already know the outcome. The Fed held rates steady at 3.50–3.75%, with only Miran dissenting in favor of a cut. However, the minutes will reveal how close the internal debate actually was. Given that the March meeting was the first to formally incorporate the Iran oil shock, the 15% global tariff regime, and the February payroll collapse into the Summary of Economic Projections, the minutes will be important to consider. In those projections, core inflation forecasts were revised higher to 2.7% for 2026, while GDP was upgraded to 2.4%. That combination, hotter inflation with resilient growth, justified the hold. But the question the markets need answered now is whether the spike in oil prices, which will eventually weigh on economic growth, changes that math.

Speaking of oil prices, Friday’s March CPI is the week’s anchor and arguably the most consequential inflation print of the year so far. February came in at +0.3% MoM headline and +2.4% YoY, with core at +0.3% / 2.8%. But March is the first month that fully captures the oil price surge toward $100 following the U.S.-Israel strikes on Iran. Energy-specific CPI rose 0.6% in February before the worst of the oil spike, which March will make materially worse. Food prices were already accelerating at +0.4% MoM. The core goods basket is where tariff passthrough resided, and RBC’s analysis flagged that declines in used-car prices had been masking the pressure in prior months. A hot March CPI could push rate cuts into December at the earliest, or off the table entirely. Any print above 0.4% MoM headline or 0.3% core will confirm those expectations.

Bottom line: The FOMC Minutes tell us what the Fed was thinking. The March CPI tells us whether they were right to hold. If inflation is accelerating while the labor market weakens, the policy trap is confirmed, and the market will have to price accordingly.

Investor Tactics For What Comes Next

Following five consecutive weekly declines, the market’s bounce this week could continue for a bit longer. This isn’t rocket science, and is something we repeat often. It is just a process to manage near-term risk.

Treat any near-term rally as an opportunity to rebalance, not to add exposure. Use strength to trim positions outside your target allocation and to reduce concentration in sectors most exposed to energy-cost pressure — consumer discretionary, industrials, and highly leveraged names.

Raise cash to a level that lets you sleep at night and act when opportunities arrive. That number is different for every investor, but the point is intentional: cash is a position, not a failure of nerve. Having it means you can be opportunistic when others are forced to sell.

Hedge risk that you want to keep. If you hold long-term positions, consider hedging them to reduce portfolio volatility.

Watch the 200-DMA retake attempt closely. A failed retake — where the market rallies back toward that level and then rolls over — is one of the clearest signals that the intermediate-term trend remains down. A successful retake on expanding volume materially changes the picture.

Stress-test your portfolio for oil above $100 through year-end. Goldman’s bear case is 5,400 on the S&P. That’s a decline from current levels that would test the tolerance of most retail investors. Know your number before the market finds it for you.

Don’t abandon fixed income. Duration has been painful, but investment-grade credit and short-term Treasuries are doing exactly what they should: providing ballast. A barbell approach — short-duration credit on one side, selectively opportunistic equity exposure on the other — remains the structure most likely to survive what comes next.

Again, this is nothing new, and we can sum it all up in just five words:

Defense over offense. Trade accordingly.

The one silver lining is valuation. As Morgan Stanley noted this past week, the S&P now trades roughly 17% cheaper than pre-war levels on forward earnings. That is approaching ranges historically associated with correction endings, provided the economy avoids recession, and the Fed doesn’t hike.

There is no guarantee of either, so caution remains a “trading position.”

Tyler Durden

Sun, 04/05/2026 – 09:55

https://www.zerohedge.com/markets/reflexive-rally-was-not-surprising

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}