Category: News

‘Next Step Mars’: Trump Congratulates Artemis II Astronauts On Historic Lunar Mission

‘Next Step Mars’: Trump Congratulates Artemis II Astronauts On Historic Lunar Mission

Authored by Aldgra Fredly via The Epoch Times,

President Donald Trump congratulated the crew of NASA’s Artemis II mission after their spacecraft splashed into the Pacific Ocean on April 10, capping their 10-day lunar voyage.

Artemis II, NASA’s 10-day test flight around the moon, concluded just after 5 p.m. PT, 8 p.m. ET, on April 10 when the Orion spacecraft gently parachuted into the Pacific Ocean off San Diego, California.

Artemis II splashdown. pic.twitter.com/UUvbvVfGey

— Joyce (@Trefejoy4) April 11, 2026

In a Truth Social post, Trump said he “could not be more proud” of the lunar mission and invited the Artemis II crew to the White House.

He anticipated the next phase of U.S. exploration of Mars.

“Congratulations to the Great and Very Talented Crew of Artemis II. The entire trip was spectacular, the landing was perfect and, as President of the United States, I could not be more proud,” the president wrote.

“I look forward to seeing you all at the White House soon. We’ll be doing it again and then, next step, Mars.”

The Artemis II mission – carrying a crew of four: NASA astronauts Reid Wiseman, Victor Glover, and Christina Koch, and Jeremy Hansen of the Canadian Space Agency – marked the first time that humans traveled to the moon and back since Apollo 17 in 1972.

🔥HISTÓRICO🔥

Estes são os astronautas que retornaram à Terra após sua missão ao redor da Lua. A tripulação da missão Artemis A missão da NASA retorna ao nosso planeta depois de orbitar a Lua na nave da nave Orion. Siga-nos @Blognetosilveir pic.twitter.com/YSmPhPo5Xq

— BlogdoNetoSilveira (@BlogNetoSilvei) April 11, 2026

The Orion spacecraft traveled 694,481 miles, surpassing the previous record set by Apollo 13 in 1970, according to NASA.

NASA said the astronauts tested the spacecraft’s life support systems, emergency equipment and procedures, survival system spacesuits, and other critical spacecraft systems to guide future lunar missions. They captured more than 7,000 images of the lunar surface and its terminator, the boundary line separating lunar day and night, the space agency said.

Their Orion capsule, dubbed Integrity, made the plunge on automatic pilot. The lunar cruiser hit the atmosphere traveling Mach 32—or 32 times the speed of sound—a blistering blur not seen since the 1960s and 1970s Apollo.

Extreme close up footage of the Artemis II Orion capsule right after splashdown and Navy divers starting recoverypic.twitter.com/fqwQ3dARQU

— All day Astronomy (@forallcurious) April 11, 2026

A joint NASA and U.S. military team retrieved the crew after splashdown in the Pacific Ocean, transporting them via helicopter to the USS John P. Murtha for initial medical assessments. All four crew members were reported to be in great health by medical staff.

The space agency said the crew is set to return to NASA’s Johnson Space Center in Houston on April 11.

In a statement after the splashdown on April 10, NASA Administrator Jared Isaacman called the mission a “historic achievement” and thanked the president and Congress for their support.

“With Artemis II complete, focus now turns confidently toward assembling Artemis III and preparing to return to the lunar surface, build the base, and never give up the Moon again,” Isaacman said.

Tyler Durden

Sat, 04/11/2026 – 12:50

‘Next Step Mars’: Trump Congratulates Artemis II Astronauts On Historic Lunar Mission

‘Next Step Mars’: Trump Congratulates Artemis II Astronauts On Historic Lunar Mission

Authored by Aldgra Fredly via The Epoch Times,

President Donald Trump congratulated the crew of NASA’s Artemis II mission after their spacecraft splashed into the Pacific Ocean on April 10, capping their 10-day lunar voyage.

Artemis II, NASA’s 10-day test flight around the moon, concluded just after 5 p.m. PT, 8 p.m. ET, on April 10 when the Orion spacecraft gently parachuted into the Pacific Ocean off San Diego, California.

Artemis II splashdown. pic.twitter.com/UUvbvVfGey

— Joyce (@Trefejoy4) April 11, 2026

In a Truth Social post, Trump said he “could not be more proud” of the lunar mission and invited the Artemis II crew to the White House.

He anticipated the next phase of U.S. exploration of Mars.

“Congratulations to the Great and Very Talented Crew of Artemis II. The entire trip was spectacular, the landing was perfect and, as President of the United States, I could not be more proud,” the president wrote.

“I look forward to seeing you all at the White House soon. We’ll be doing it again and then, next step, Mars.”

The Artemis II mission – carrying a crew of four: NASA astronauts Reid Wiseman, Victor Glover, and Christina Koch, and Jeremy Hansen of the Canadian Space Agency – marked the first time that humans traveled to the moon and back since Apollo 17 in 1972.

🔥HISTÓRICO🔥

Estes são os astronautas que retornaram à Terra após sua missão ao redor da Lua. A tripulação da missão Artemis A missão da NASA retorna ao nosso planeta depois de orbitar a Lua na nave da nave Orion. Siga-nos @Blognetosilveir pic.twitter.com/YSmPhPo5Xq

— BlogdoNetoSilveira (@BlogNetoSilvei) April 11, 2026

The Orion spacecraft traveled 694,481 miles, surpassing the previous record set by Apollo 13 in 1970, according to NASA.

NASA said the astronauts tested the spacecraft’s life support systems, emergency equipment and procedures, survival system spacesuits, and other critical spacecraft systems to guide future lunar missions. They captured more than 7,000 images of the lunar surface and its terminator, the boundary line separating lunar day and night, the space agency said.

Their Orion capsule, dubbed Integrity, made the plunge on automatic pilot. The lunar cruiser hit the atmosphere traveling Mach 32—or 32 times the speed of sound—a blistering blur not seen since the 1960s and 1970s Apollo.

Extreme close up footage of the Artemis II Orion capsule right after splashdown and Navy divers starting recoverypic.twitter.com/fqwQ3dARQU

— All day Astronomy (@forallcurious) April 11, 2026

A joint NASA and U.S. military team retrieved the crew after splashdown in the Pacific Ocean, transporting them via helicopter to the USS John P. Murtha for initial medical assessments. All four crew members were reported to be in great health by medical staff.

The space agency said the crew is set to return to NASA’s Johnson Space Center in Houston on April 11.

In a statement after the splashdown on April 10, NASA Administrator Jared Isaacman called the mission a “historic achievement” and thanked the president and Congress for their support.

“With Artemis II complete, focus now turns confidently toward assembling Artemis III and preparing to return to the lunar surface, build the base, and never give up the Moon again,” Isaacman said.

Tyler Durden

Sat, 04/11/2026 – 12:50

‘Next Step Mars’: Trump Congratulates Artemis II Astronauts On Historic Lunar Mission

‘Next Step Mars’: Trump Congratulates Artemis II Astronauts On Historic Lunar Mission

Authored by Aldgra Fredly via The Epoch Times,

President Donald Trump congratulated the crew of NASA’s Artemis II mission after their spacecraft splashed into the Pacific Ocean on April 10, capping their 10-day lunar voyage.

Artemis II, NASA’s 10-day test flight around the moon, concluded just after 5 p.m. PT, 8 p.m. ET, on April 10 when the Orion spacecraft gently parachuted into the Pacific Ocean off San Diego, California.

Artemis II splashdown. pic.twitter.com/UUvbvVfGey

— Joyce (@Trefejoy4) April 11, 2026

In a Truth Social post, Trump said he “could not be more proud” of the lunar mission and invited the Artemis II crew to the White House.

He anticipated the next phase of U.S. exploration of Mars.

“Congratulations to the Great and Very Talented Crew of Artemis II. The entire trip was spectacular, the landing was perfect and, as President of the United States, I could not be more proud,” the president wrote.

“I look forward to seeing you all at the White House soon. We’ll be doing it again and then, next step, Mars.”

The Artemis II mission – carrying a crew of four: NASA astronauts Reid Wiseman, Victor Glover, and Christina Koch, and Jeremy Hansen of the Canadian Space Agency – marked the first time that humans traveled to the moon and back since Apollo 17 in 1972.

🔥HISTÓRICO🔥

Estes são os astronautas que retornaram à Terra após sua missão ao redor da Lua. A tripulação da missão Artemis A missão da NASA retorna ao nosso planeta depois de orbitar a Lua na nave da nave Orion. Siga-nos @Blognetosilveir pic.twitter.com/YSmPhPo5Xq

— BlogdoNetoSilveira (@BlogNetoSilvei) April 11, 2026

The Orion spacecraft traveled 694,481 miles, surpassing the previous record set by Apollo 13 in 1970, according to NASA.

NASA said the astronauts tested the spacecraft’s life support systems, emergency equipment and procedures, survival system spacesuits, and other critical spacecraft systems to guide future lunar missions. They captured more than 7,000 images of the lunar surface and its terminator, the boundary line separating lunar day and night, the space agency said.

Their Orion capsule, dubbed Integrity, made the plunge on automatic pilot. The lunar cruiser hit the atmosphere traveling Mach 32—or 32 times the speed of sound—a blistering blur not seen since the 1960s and 1970s Apollo.

Extreme close up footage of the Artemis II Orion capsule right after splashdown and Navy divers starting recoverypic.twitter.com/fqwQ3dARQU

— All day Astronomy (@forallcurious) April 11, 2026

A joint NASA and U.S. military team retrieved the crew after splashdown in the Pacific Ocean, transporting them via helicopter to the USS John P. Murtha for initial medical assessments. All four crew members were reported to be in great health by medical staff.

The space agency said the crew is set to return to NASA’s Johnson Space Center in Houston on April 11.

In a statement after the splashdown on April 10, NASA Administrator Jared Isaacman called the mission a “historic achievement” and thanked the president and Congress for their support.

“With Artemis II complete, focus now turns confidently toward assembling Artemis III and preparing to return to the lunar surface, build the base, and never give up the Moon again,” Isaacman said.

Tyler Durden

Sat, 04/11/2026 – 12:50

‘Next Step Mars’: Trump Congratulates Artemis II Astronauts On Historic Lunar Mission

‘Next Step Mars’: Trump Congratulates Artemis II Astronauts On Historic Lunar Mission

Authored by Aldgra Fredly via The Epoch Times,

President Donald Trump congratulated the crew of NASA’s Artemis II mission after their spacecraft splashed into the Pacific Ocean on April 10, capping their 10-day lunar voyage.

Artemis II, NASA’s 10-day test flight around the moon, concluded just after 5 p.m. PT, 8 p.m. ET, on April 10 when the Orion spacecraft gently parachuted into the Pacific Ocean off San Diego, California.

Artemis II splashdown. pic.twitter.com/UUvbvVfGey

— Joyce (@Trefejoy4) April 11, 2026

In a Truth Social post, Trump said he “could not be more proud” of the lunar mission and invited the Artemis II crew to the White House.

He anticipated the next phase of U.S. exploration of Mars.

“Congratulations to the Great and Very Talented Crew of Artemis II. The entire trip was spectacular, the landing was perfect and, as President of the United States, I could not be more proud,” the president wrote.

“I look forward to seeing you all at the White House soon. We’ll be doing it again and then, next step, Mars.”

The Artemis II mission – carrying a crew of four: NASA astronauts Reid Wiseman, Victor Glover, and Christina Koch, and Jeremy Hansen of the Canadian Space Agency – marked the first time that humans traveled to the moon and back since Apollo 17 in 1972.

🔥HISTÓRICO🔥

Estes são os astronautas que retornaram à Terra após sua missão ao redor da Lua. A tripulação da missão Artemis A missão da NASA retorna ao nosso planeta depois de orbitar a Lua na nave da nave Orion. Siga-nos @Blognetosilveir pic.twitter.com/YSmPhPo5Xq

— BlogdoNetoSilveira (@BlogNetoSilvei) April 11, 2026

The Orion spacecraft traveled 694,481 miles, surpassing the previous record set by Apollo 13 in 1970, according to NASA.

NASA said the astronauts tested the spacecraft’s life support systems, emergency equipment and procedures, survival system spacesuits, and other critical spacecraft systems to guide future lunar missions. They captured more than 7,000 images of the lunar surface and its terminator, the boundary line separating lunar day and night, the space agency said.

Their Orion capsule, dubbed Integrity, made the plunge on automatic pilot. The lunar cruiser hit the atmosphere traveling Mach 32—or 32 times the speed of sound—a blistering blur not seen since the 1960s and 1970s Apollo.

Extreme close up footage of the Artemis II Orion capsule right after splashdown and Navy divers starting recoverypic.twitter.com/fqwQ3dARQU

— All day Astronomy (@forallcurious) April 11, 2026

A joint NASA and U.S. military team retrieved the crew after splashdown in the Pacific Ocean, transporting them via helicopter to the USS John P. Murtha for initial medical assessments. All four crew members were reported to be in great health by medical staff.

The space agency said the crew is set to return to NASA’s Johnson Space Center in Houston on April 11.

In a statement after the splashdown on April 10, NASA Administrator Jared Isaacman called the mission a “historic achievement” and thanked the president and Congress for their support.

“With Artemis II complete, focus now turns confidently toward assembling Artemis III and preparing to return to the lunar surface, build the base, and never give up the Moon again,” Isaacman said.

Tyler Durden

Sat, 04/11/2026 – 12:50

Orban Warns “We Could Now Lose Everything”: Sunday’s Hungarian Elections Have Profound Implications For Europe

Orban Warns “We Could Now Lose Everything”: Sunday’s Hungarian Elections Have Profound Implications For Europe

As Hungarians head to the polls on Sunday, April 12, 2026, the country stands at a historic inflection point. For the first time since Viktor Orbán’s Fidesz party swept back into power in 2010, a credible challenger – Péter Magyar and his Tisza party – has a genuine shot at ending 16 years of what Orbán proudly calls his “illiberal laboratory.” In a final campaign rally, Orbán warned supporters they are choosing “not just a government, but the fate of the country” and could “now lose everything we have built together.”

Bluntly put the election is a referendum on the durability of nationalist populism in Europe, the future of EU integration, energy security amid the Ukraine war, transatlantic conservative alliances under Trump 2.0, and even the fate of billions in Chinese investment that have reshaped Hungarian industry.

Right now, it looks like Magyar has it in the bag, so read on for the implications:

Will the next Prime Minister of Hungary be Péter Magyar?

Yes 72% · No 28%

View full market & trade on Polymarket

As Goldman notes, independent polls, seat projections, and prediction markets all point to a likely Tisza victory – potentially with the two-thirds supermajority needed to rewrite the constitution. Markets have been pricing it in for over a year, yet the stakes could hardly be higher, and the outcome remains fluid until the ballots are counted. A Fidesz upset or narrow hold would reverberate from Brussels to Beijing, from Kyiv to Washington. This is the “Battle for Hungary” – and its ripples could redefine the continent’s political fault lines, as noted by Andrew Korybko.

The Two-Man Race: Orbán’s Empire vs. Magyar’s Surge

Orbán, 62, has dominated Hungarian politics since 2010, crafting a model of “illiberal democracy” that mixes nationalist rhetoric, state-orchestrated economic control, and defiance of EU norms.

He positioned Hungary as a bulwark against mass migration, gender ideology, and Brussels overreach – exporting the playbook to allies like Donald Trump. Under his watch, Fidesz built an electoral machine that delivered supermajorities in 2010, 2014, 2018, and 2022, despite never exceeding roughly 54% of the vote, thanks to gerrymandering, diaspora voting, and first-past-the-post districts.

Enter Péter Magyar, 43, a former Fidesz insider turned insurgent.

A lawyer and ex-husband of a former justice minister, Magyar burst onto the scene in 2024 after a dramatic break with the party, railing against corruption, cronyism, and economic mismanagement. His Tisza party has consolidated the fragmented opposition into a genuine two-party contest. Magyar campaigns on restoring rule of law, unlocking frozen EU funds, and delivering economic relief without sacrificing sovereignty. He is explicitly targeting the two-thirds supermajority (133 of 199 seats) to repeal Fidesz’s “Cardinal Acts” and constitutional changes.

The numbers tell the story. Long-term polling charts show Fidesz’s support eroding from peaks near 48% in 2024 to the low 30s–low 40s today, while Tisza has rocketed from the mid-20s to 50–58% among decided voters.

Taking a ‘Naive’ Average of All Polls Suggests Tisza Will Receive Most Votes, But Fall Short of 50%

Independent pollsters like Medián consistently show Tisza at 55–58% and Fidesz at 35–38%, with “Other” parties collapsing into single digits.

On Polymarket, Péter Magyar is trading at 72% to become the next Prime Minister (versus 28% for Viktor Orbán), with over $62 million in trading volume. The “Hungary Parliamentary Election Winner” market gives Tisza a 75% probability of winning the most seats and forming the next government (Fidesz at 26%), with roughly $60 million traded.

Will TISZA – Respect and Freedom Party (TISZA) win the most seats in the next Hungarian parliamentary election?

Yes 75% · No 26%

View full market & trade on Polymarket

Even accounting for the system’s built-in advantages for incumbents – 106 single-member FPTP districts, strong rural and Romanian-diaspora support for Fidesz – the market consensus strongly favors a decisive shift in power.

The Domestic Reckoning: Economy, Corruption, and Voter Fatigue

Hungary’s voters are not marching to the polls in a vacuum. Beneath the ideological battle lies raw economic pain. As Goldman notes further, cumulative price rises of 40% since 2021 have hammered households despite inflation cooling to +1.4%. Growth has stagnated. Corruption perceptions rank Hungary as the EU’s most graft-prone member, per Transparency International. Many Hungarians see Orbán’s system – subsidies, tax breaks, and special deals – as having enriched insiders while ordinary people footed the bill for the cost-of-living crisis.

Orbán has countered by highlighting 16 years of achievements – job creation, pension increases, and border barriers to halt illegal immigration – and warned that losing power would mean Hungarians “lose everything we have built together.”

A Tisza victory would likely deliver immediate relief: the unlocking of roughly €20 billion in frozen EU funds, contingent on judicial and anti-corruption reforms. Magyar has pledged a credible path to euro adoption by 2030, which would stabilize the forint and lower borrowing costs long-term. A supermajority would let Tisza dismantle the “Cardinal Acts” that entrenched Fidesz power over media, elections, pensions, and taxation.

As Korybko notes, the emotional undercurrent runs deeper. Orbán’s defenders credit him with shielding Hungary from the worst of the Ukraine war fallout – keeping Russian energy flowing, avoiding direct involvement, and preserving sovereignty. Many Chinese business owners in Hungary quietly echo that view: they grumble about bribes and cronyism but prefer the “devil they know” because “at least things get done,” according to SCMP.

How Hungarian Elections Work

Voters cast two ballots: one for a local candidate (106 seats via first-past-the-post) and one for a national party list (93 seats via proportional representation). A simple majority elects the prime minister and passes ordinary laws; two-thirds is required for constitutional amendments and Cardinal Acts.

Ballots open at 06:00 CEST and close at 19:00 CEST on Sunday. Counting begins immediately; a clear winner typically emerges election night, with official certification roughly one week later. Recounts are possible if margins are razor-thin. Turnout will be decisive: high participation historically favors challengers riding waves of discontent.

Geopolitical Earthquake: From Brussels to Beijing

Europe and the EU

Orbán has been the bloc’s most stubborn spoiler – vetoing Ukraine aid packages, blocking rule-of-law sanctions, and slowing federalization. A Tisza win would remove that veto leverage overnight. Brussels-friendly governance could accelerate EU integration, restore Hungary’s access to cohesion funds, and align Budapest with mainstream European policy.

Ukraine

Kyiv has clashed repeatedly with Orbán over energy imports from Russia and reluctance to arm Ukraine. Ukrainian pressure tactics – including weaponizing the Druzhba pipeline – have failed to move him. A

Ukraine hates Hungary too, but only because Orban refuses to arm it, continues purchasing energy from Russia, and has occasionally obstructed EU funding for this former Soviet Republic. In response, Ukraine has weaponized the Druzhba oil pipeline from Russia upon which Hungary relies to a large degree to pressure him into reversing his policies, but to no avail. Ukraine also colludes with the Hungarian opposition, which is now Ukraine’s and the EU’s joint proxy, in their Russiagate conspiracy theories. –Korybko

Magyar government would likely soften Hungary’s stance, easing EU-Ukraine funding bottlenecks and reducing pipeline friction.

United States and Trump 2.0

The international right has rallied behind Orbán. Former President Donald Trump endorsed him on social media, calling him “a truly strong and determined leader” with “a proven record of outstanding results” and a “true friend, a fighter, and a winner.” U.S. Vice President JD Vance visited Budapest and sharply criticized Brussels for “unprecedented interference” in the election process. A Fidesz hold would bolster that transatlantic populist axis; a Tisza victory would be a setback, signaling that even the strongest illiberal outpost can fall to domestic economic grievances.

European Populist Allies

Orbán has also received strong backing from key figures on the European right. France’s Marine Le Pen praised his stance on the Ukraine war as “very brave,” Italy’s Matteo Salvini framed the vote as a contest over Europe’s future and national sovereignty versus centralized EU control, and Germany’s AfD co-leader Alice Weidel voiced her support.

Russia

Moscow’s stake is modest but real: Orbán’s pragmatic energy deals and occasional obstruction of anti-Russia measures have been valuable. Putin sees Hungary as a potential future bridge for EU-Russia détente once the Ukraine war ends. Russia has avoided overt meddling, but a Tisza shift would narrow that window.

Out of the four foreign parties with stakes in the “Battle for Hungary”, Russia’s are the least. It supports Orban’s pragmatic approach to the Ukrainian Conflict and views Hungary as a valuable partner in Europe. More than that, however, Putin believes that Orban can help repair Russian-EU relations sometime after their proxy war in Ukraine ends. While certainly game-changing if it occurs, this scenario is admittedly unlikely, ergo why Russia isn’t meddling in his support despite conspiracy theories to the contrary. –Korybko

China

Billions in Chinese FDI – most visibly CATL’s massive battery plant in Debrecen – have become politically radioactive. Banners reading “No battery, no deal,” “Debrecen belongs to Hungarians,” and “Chinese, go home” dot the city. Chinese firms face local backlash over imported labor, environmental risks, and meager local economic spillovers. Tisza has been measured – calling for “pragmatic, mutually beneficial” ties while demanding stricter EU-compliant rules on labor, environment, and taxes. Projects already under construction are unlikely to be seized, but a new government would pivot from “seduction” (subsidies and visas) to enforcement.

Market Verdict: The Forint Has Already Spoken

Investors have been positioned for a Tisza outcome since early 2025. The forint has strengthened in anticipation. Goldman’s EM desk outlines clear scenarios:

Tisza win (base case): EUR/HUF –2%, swaps –20 to –30 bps, credit spreads –15 to –25 tighter.

Tisza + supermajority: EUR/HUF –4%, swaps –30 to –40 bps, spreads –25 to –40 tighter (+ €20bn EU funds unlock).

Fidesz hold / upset: EUR/HUF +4%, swaps +40 to +50 bps, spreads +25 to +40 wider.

FX volatility desks price roughly 3% gap risk around the event, with positioning long HUF but some profit-taking near 375.

Aftermath Scenarios: Victory, Narrow Hold, or Chaos

A decisive Tisza victory would mark the end of the Orbán era and a constitutional reset. A narrow Fidesz government or blocking minority could trigger exactly the Color Revolution fears some analysts warn of – EU- and Ukraine-backed protests framed around “Russian meddling,” exactly the kind of destabilization Orbán has accused opponents of preparing. Hungarians themselves hold the greatest stake. They will live with the consequences – economic relief or continued stagnation, EU integration or defiant sovereignty, pragmatic Chinese investment or stricter oversight.

Why Europe – and the World – Should Watch Closely

This is more than a Hungarian election. It is a stress test for the durability of the populist wave that Orbán helped pioneer. A Tisza supermajority would deliver the clearest repudiation yet of illiberal governance in Europe, emboldening Brussels and weakening nationalist holdouts elsewhere. It would signal that economic pain and corruption fatigue can trump sovereignty rhetoric even in the EU’s most defiant member.

Conversely, an Orbán hold – against the polling tide – would validate the model’s resilience and give fresh oxygen to conservative-nationalist forces from Warsaw to Washington.

Sunday’s result will not just decide Hungary’s next prime minister. It could redraw the map of European populism, recalibrate great-power alignments, and determine whether the “illiberal laboratory” survives or becomes a historical footnote. Polls close at 19:00 CEST. By nightfall, we may know whether the Battle for Hungary ends in revolution – or resilience. The continent is watching.

Tyler Durden

Sat, 04/11/2026 – 12:15

Three Contrarian Signals That Aren’t Easy To Ignore As Earnings Season Begins

Three Contrarian Signals That Aren’t Easy To Ignore As Earnings Season Begins

Authored by Lance Roberts via RealInvestmentAdvice.com,

💰 Q1 Earnings Season Begins

As a fragile ceasefire with Iran hangs in the balance and oil trades near multi-year highs, the Q1 earnings season is arriving in one of the most negatively positioned markets in years. That backdrop may be exactly the reason it’s worth reconsidering the “fade the rally” stance we posited last week. For individuals who have not been in the financial markets for very long, there is an important lesson to learn.

“The markets are designed to inflict the maximum amount of pain on the maximum number of participants at any given moment.”

Right now, given the numerous “Purveyors of Persistent Doom” on social media, the most crowded trade on Wall Street isn’t a long position…it’s fear. Furthermore, as we discussed last week, after 5 weeks of consecutive declines, the market rally this past week was not unexpected.

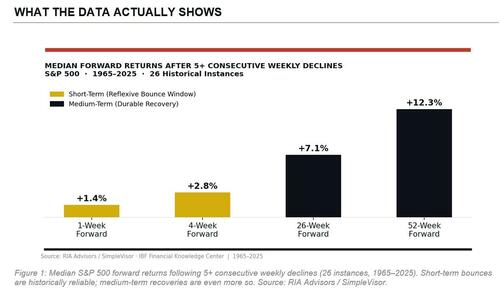

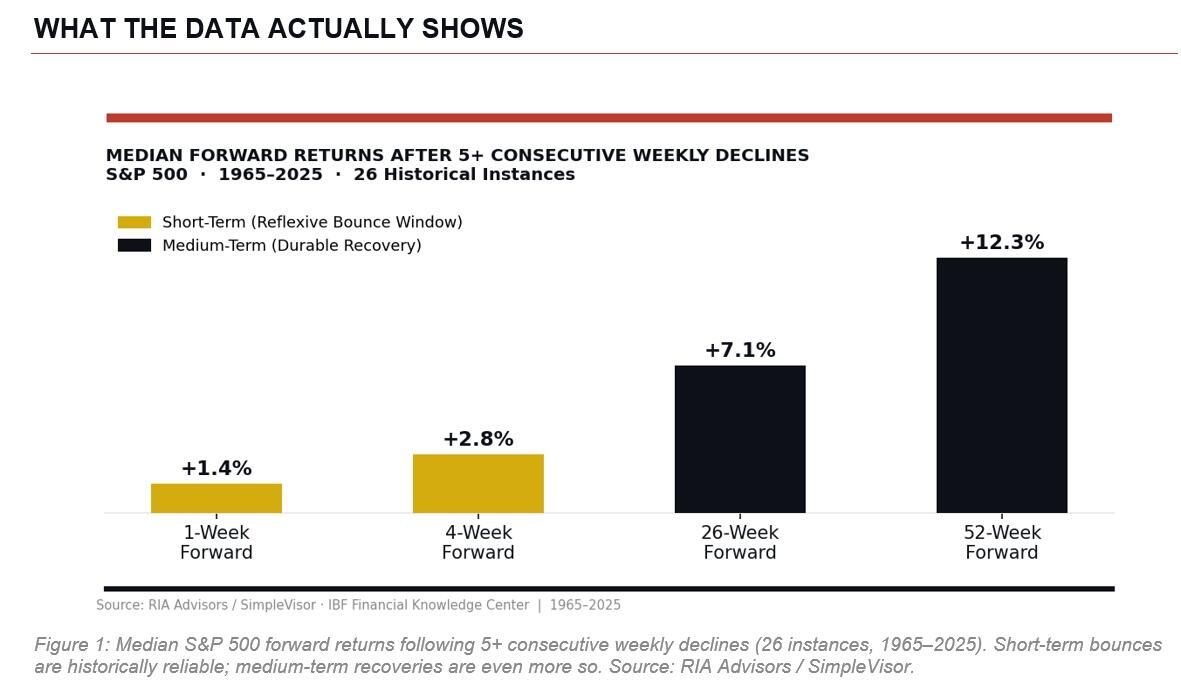

“Since 1965, the S&P 500 has recorded 26 separate instances of five or more consecutive weekly declines. That’s roughly once every 2.3 years, and these streaks feel catastrophic in real time. This is when investors make the most mistakes over time. The emotional stress of the decline, combined with “doomsayers,” drives investors to sell at the bottom. It is important to understand that, while these streaks feel alarming in real time, historical evidence suggests they function more as contrarian buy signals than as warnings of further collapse.”

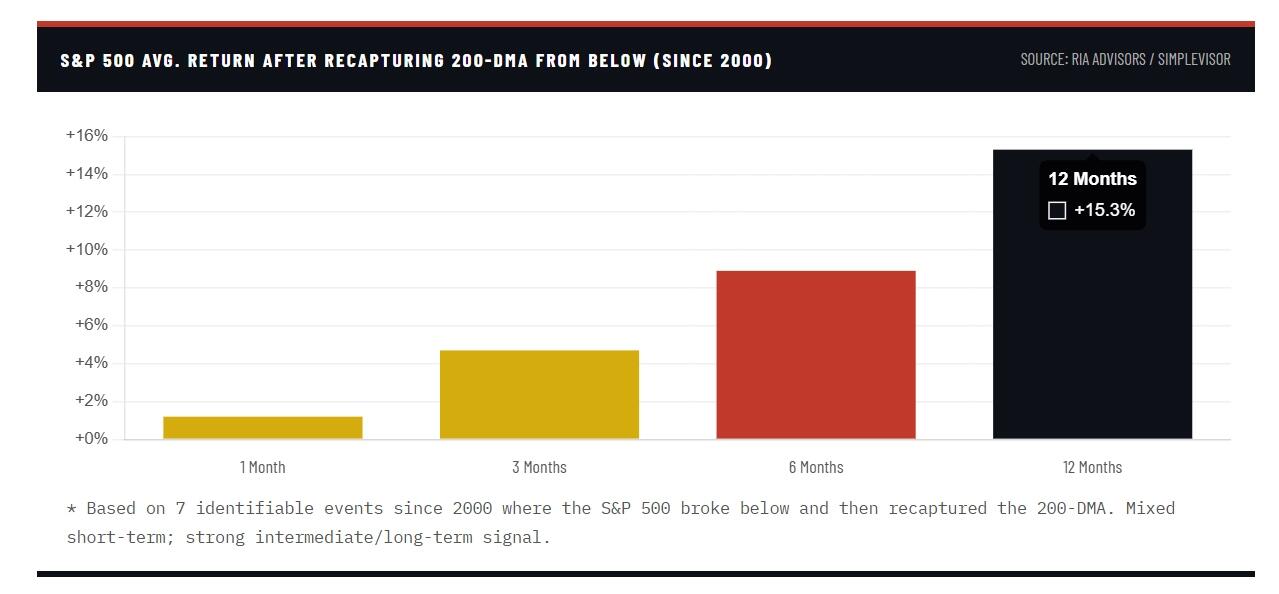

In fact, that rally was one of the strongest in nearly a year, despite the constant stream of negative headlines. The S&P 500 surged on relief that U.S.-Iran tensions had temporarily de-escalated, gaining ground and recapturing the 200-day moving average on a closing basis for the first time since the initial shock of the conflict sent it plunging through that critical floor in mid-March. That single technical event, a clean close back above the 200-DMA, changes the conversation about what comes next, especially with the Q1 earnings season now underway.

The question everyone is wrestling with is simple: do you fade this rally, or do you use it to add exposure? I’ve been skeptical since March, and I still have reservations. But the data is shifting, and intellectual honesty requires acknowledging that.

Three Contrarian Signals That Aren’t Easy To Ignore

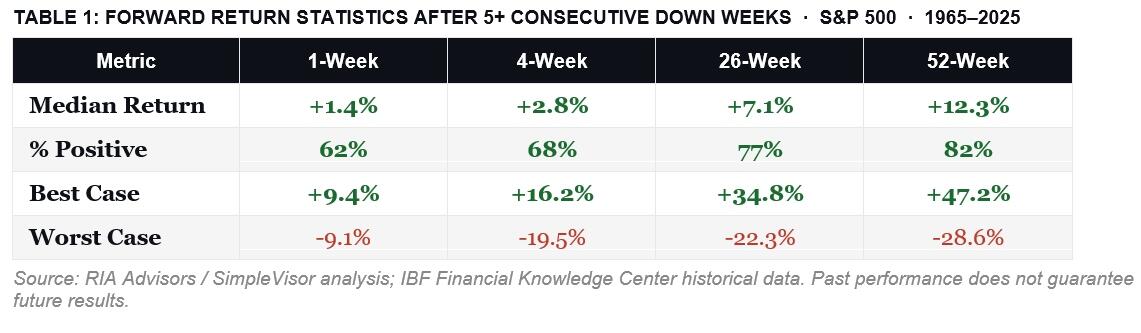

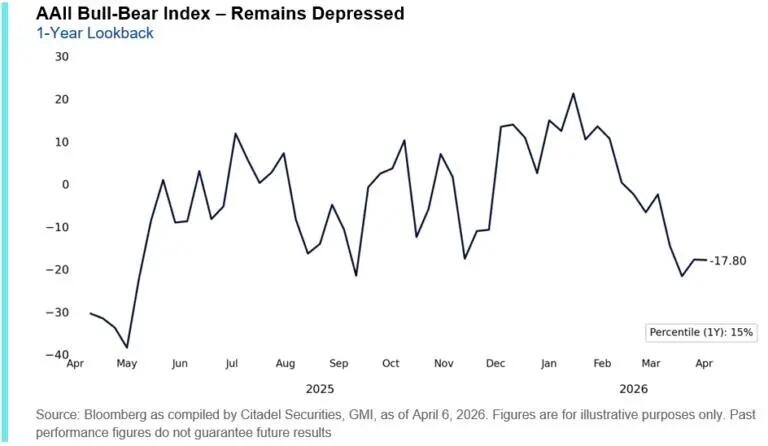

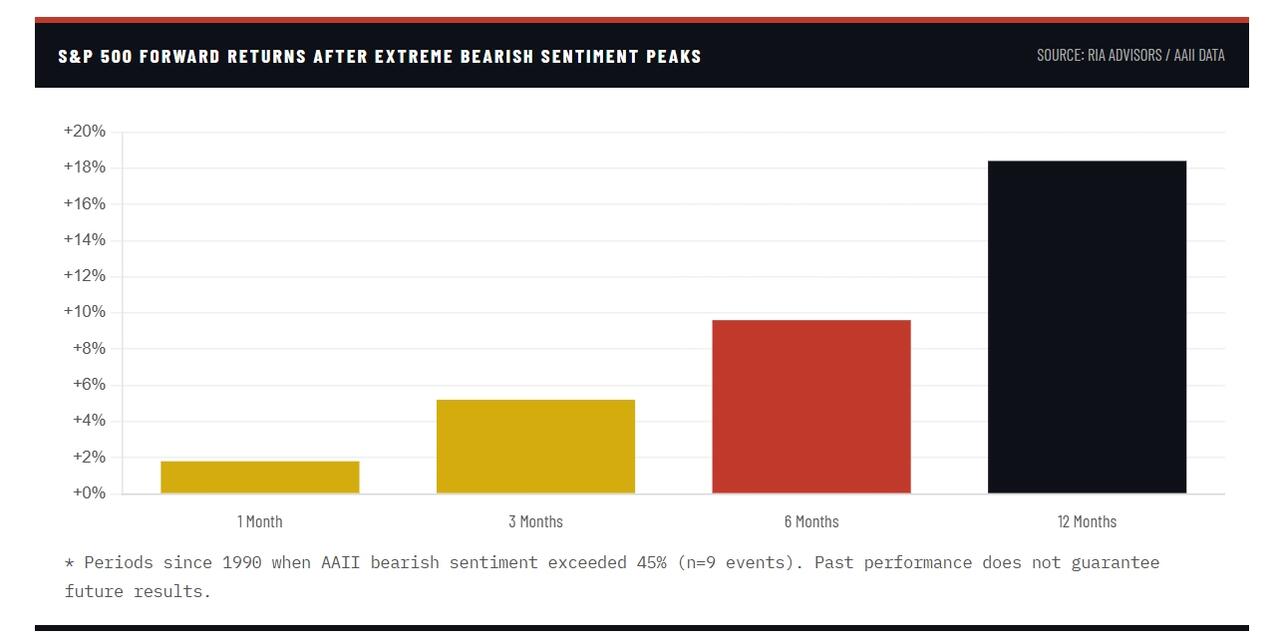

Let’s start with sentiment. The AAII Sentiment Survey saw bearish readings spike to 52.9% at the March low, one of the highest in eight years and well above the long-term average of 31.0%. That has since pulled back to 35.5%, still above average, while bullish sentiment is at just 33.1%, below the historical norm of 37.5%. Historically, whenever the bull-bear spread reaches these levels of negative divergence, forward returns over the subsequent 12 months have been strongly positive. The market tends to move against the crowd, and right now, the crowd is still more scared than optimistic.

That negative sentiment has also manifested itself in the cash and options markets.

“We are now seeing early signs of retail capitulation across both cash and options. Last week, retail flows were net sellers across both platforms – an infrequent occurrence that has only been observed 18 times since January 2020 (most recently the week of April 7-11, 2025). Historically, forward returns following these signals have been positive on average, with performance improving over longer horizons. S&P 500 returns have been positive ~82% of the time by T+60, with average returns of +4.1%, and average positive returns of +6.9%.” – Goldman Sachs

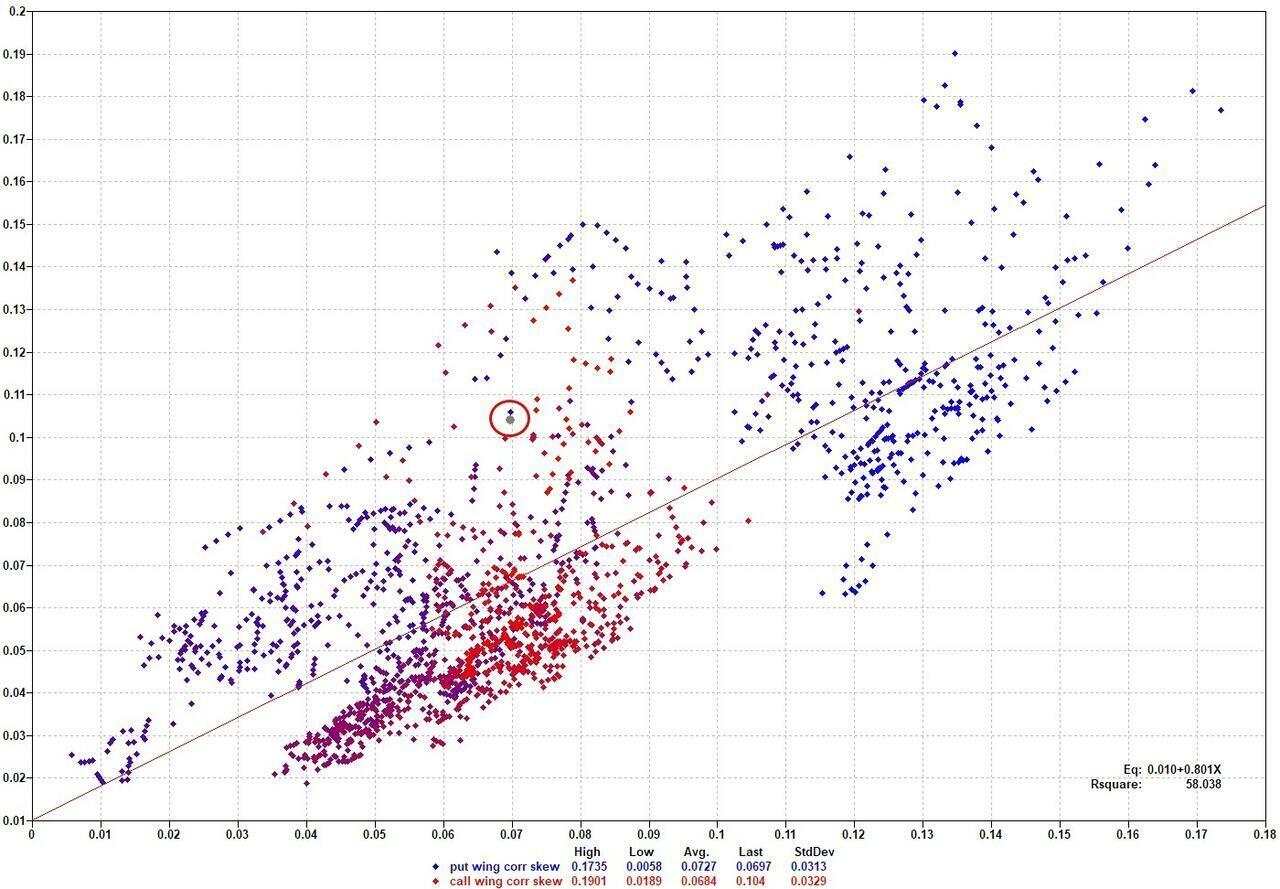

Goldman Sachs trader Shawn Tuteja recently noted that the options market’s implied correlation skew has been pricing very low correlation on the call side, effectively suggesting that the right-tail risk in the S&P 500 was underpriced heading into last week. That asymmetry, excessive put protection, underpriced upside, is exactly the type of positioning squeeze that produces face-ripping rallies. We saw one last week. There may be more ahead.

The third signal is our own Money Flow Breadth Ratio, or MFBR. When the MFBR drops below 30%, our 25-year backtest identifies a genuine capitulation washout. In those circumstances, the subsequent return profile flips dramatically: a positive outcome at one month 100% of the time, positive at six months, and a 100% win rate at twelve months. We’re in that zone right now. That doesn’t mean pain can’t persist for another few weeks, but it does mean the odds strongly favor higher prices a year from today.

The Q1 Earnings Season Could Be The Catalyst

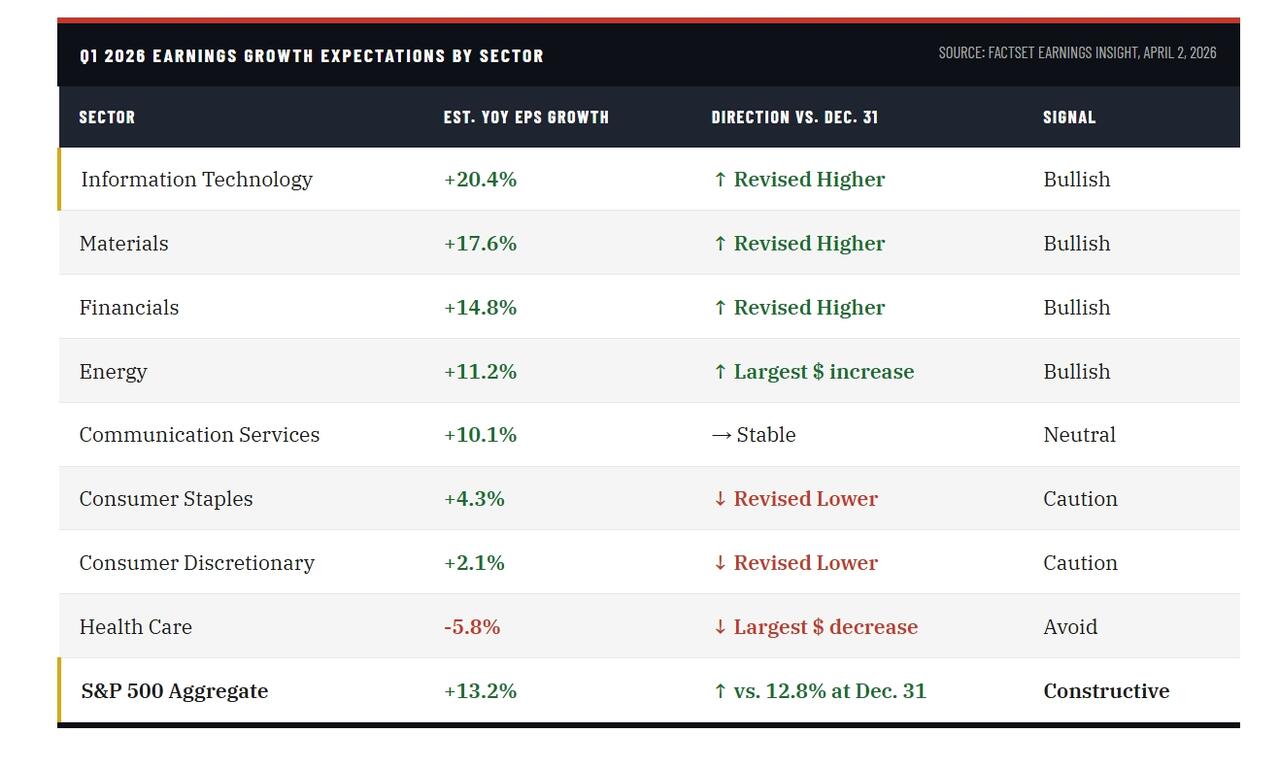

The Q1 earnings season will begin in earnest this coming week, with the major financials reporting starting with Goldman Sachs and JPMorgan. What’s important to understand is that analysts have already trimmed estimates heading into the announcements. The bottom-up Q1 EPS estimate fell 0.3% during the quarter itself, versus a historical average decline of 1.6% to 4.2% over the past five to twenty years. In other words, the bar has been reset lower than it appears on the surface, which sets up a classic beat-and-raise scenario if corporate America can simply maintain its recent pace. FactSet estimates Q1 year-over-year earnings growth at 13.2%, up from the 12.8% expectation at the start of the year, with nine of eleven sectors projected to show positive growth. Barclays recently bumped its full-year 2026 S&P 500 EPS forecast to $321, projecting 15% to 16% annual growth.

The Q1 earnings season matters even more than usual right now because it provides a factual anchor in a market driven almost entirely by headline risk. Investors need something concrete to price. Strong numbers from JPMorgan, Bank of America, Netflix, and TSMC, the first major reporters, would confirm that corporate America is absorbing the oil shock and geopolitical uncertainty better than feared. That confirmation is the trigger that shifts money from the sidelines back into equities. Think of what happened in Q1 2003. When U.S. forces entered Iraq, the S&P 500 had already sold off aggressively on the uncertainty. Once the conflict began in earnest and earnings season confirmed business resilience, the index gained more than 25% in the following six months. The Q1 earnings season was the evidence the market needed that the macro fear had been overpriced.

Will that be the case this time? I don’t know for certain, but when everyone is negative about everything, the market tends to find something to latch onto.

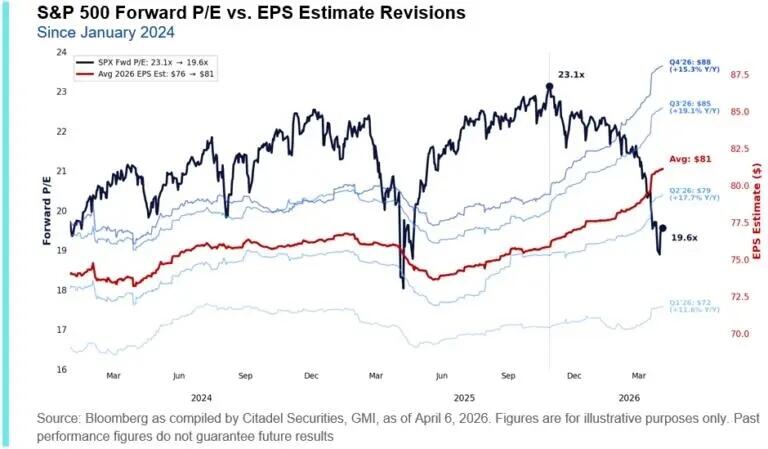

There’s a valuation argument here that also deserves attention. The forward P/E on the S&P 500 stood at 22.0x on December 31. As of today, with prices down roughly 5% from the start of the year and earnings estimates rising modestly, that multiple has compressed to 19.8x, below the five-year average of 19.9x. That’s not cheap by any historical standard, but it represents a genuine reset from the stretched valuations that made us cautious in January. With the Q1 earnings season potentially delivering another round of upward revisions, valuations could look even more reasonable by the time reporting wraps up.

The Risks That Could Still Derail Everything

I want to be honest about what could go wrong, because this market isn’t out of the woods. The Iran ceasefire remains fragile. We’ve watched this pattern before: a burst of optimism on de-escalation language, followed by a return to hostilities that sends oil back toward recent highs near $111 a barrel. Every leg higher in crude acts like a slow tax on both corporate margins and consumer purchasing power. That’s a direct headwind to the earnings beat cycle we need to see from the Q1 earnings season to validate higher prices.

“Ceasefires are fragile by definition… and we’ve already seen strikes overnight across the Gulf. You can hand-wave some of that as lag effects, but the disagreement around proxies (e.g. Lebanon with Israel) leaves plenty of scope for this to break. Ultimately though, the market will judge one thing… actual flows through the Strait over time. I struggle to see new highs for Equities, but positioning still argues for forced buying to run its course first. Europe in particular feels extended… a “fair” move might have been +2–3%, not +5%. From here, it’s all about triangulation… rates, credit, and oil. Rates matter most and are function of not just where oil goes, but where it settles. Credit will likely see aggressive covering as tail hedges decay… so less signal there in the near term. Vol compression ties it all together in determining fair spot.” – Goldman Sachs

The Federal Reserve is also paralyzed in a way that markets haven’t fully priced. With the CME FedWatch tool showing a 99.5% probability of no rate change at the April meeting, and zero-rate-cut expectations now extending through most of 2026, the policy backstop that investors have leaned on since 2020 isn’t available. The 10-year Treasury closed near 4.36%, and CTAs have pushed their Treasury shorts to maximum levels, which in turn creates an overshoot risk that could send yields spiking further on any oil-related inflation surprise. When bonds and equities both sell off together, as we saw in March, there is nowhere to hide in a traditional portfolio.

So Is It Time To Add Exposure?

This isn’t the environment to aggressively add exposure to risk. However, we can selectively add to our holdings heading into the Q1 earnings season. However, we are still maintaining a short leash in case things reverse quickly. The combination of a recaptured 200-day moving average, extreme bearish investor sentiment that has historically resolved higher, deeply depressed put-call ratios acting as coiled fuel for any upside surprise, a Q1 earnings season entering with a low bar and improving guidance, and valuations that have genuinely reset from their January extremes, that’s a setup that demands action. Not reckless action. Measured action.

My recommendation is to add exposure selectively to sectors with the strongest earnings momentum: technology, financials, and healthcare, in that order. Use any geopolitical flare-up that tests the 200-DMA as a re-entry point rather than a reason to exit. If oil de-escalation holds and the Q1 earnings season delivers even close to the 13.2% growth FactSet is projecting, the path of least resistance for the second quarter is higher.

The traders who will get destroyed in this environment are the ones who fade every rally out of fear and chase every selloff into panic. The data says the extreme pessimism of March was a buying signal. The Q1 earnings season is the catalyst that will prove or disprove it.

We will continue to watch the data closely and trade accordingly.

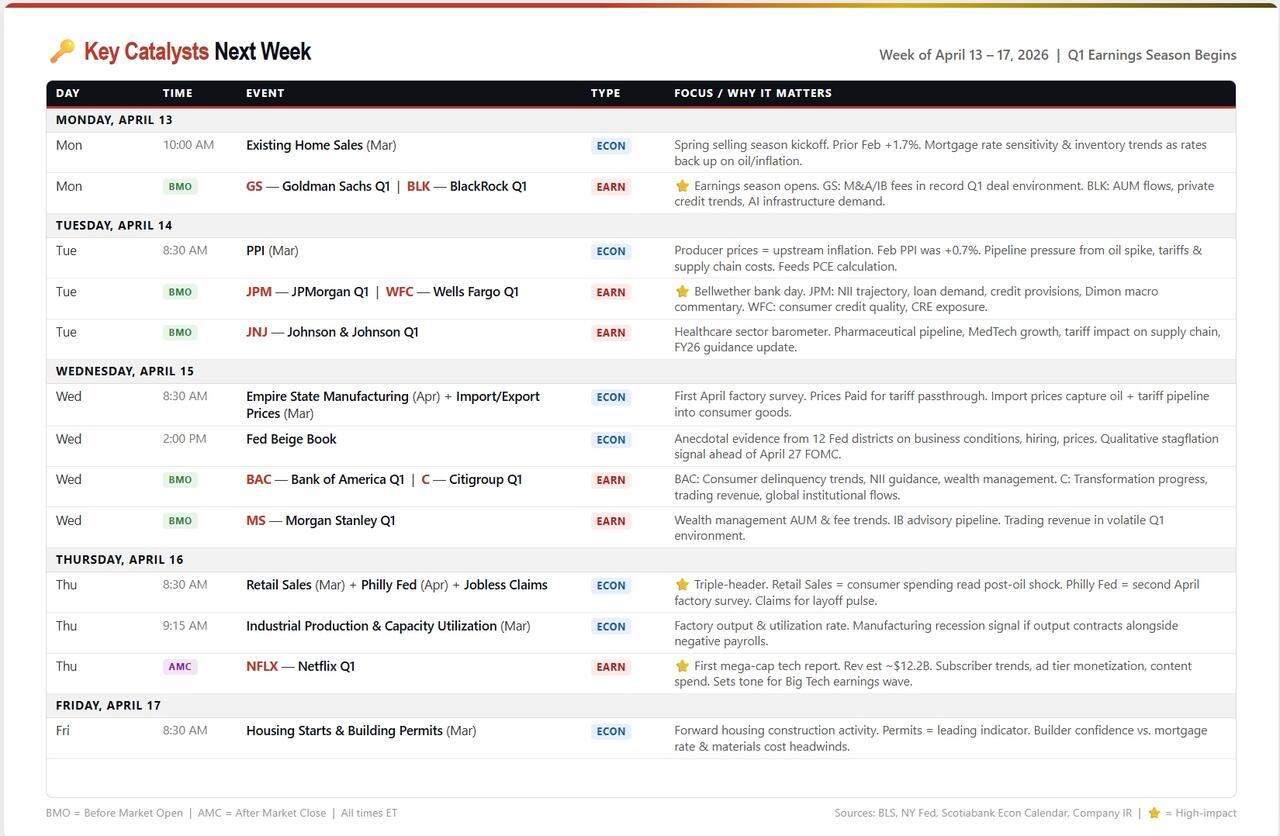

🔑 Key Catalysts Next Week

Q1 earnings season arrives in force alongside a stacked economic calendar; this is the most dense week of crosscurrents since the March FOMC. Six of the nation’s largest banks report in a three-day blitz, Netflix sets the tone for mega-cap tech, and Thursday delivers a triple-header of Retail Sales, Philly Fed, and Industrial Production that will reshape the macro narrative heading into the April 27 FOMC meeting.

Goldman Sachs and BlackRock open the season Monday morning. Goldman is the M&A bellwether. Q1 set a record for deal activity, and GS derives a higher share of revenue from investment banking than any of its major peers. BlackRock’s report will be watched for AUM flows, private credit exposure (a growing risk theme), and how institutional allocators positioned through the March oil shock. Tuesday escalates with JPMorgan, the market’s definitive “economy report card.” Jamie Dimon’s macro commentary carries as much weight as the numbers.

The trajectory of net interest income, loan loss provisions, and consumer credit quality will tell us whether the March shock left scars on Main Street. Wells Fargo is alongside for the consumer banking read. Johnson & Johnson adds the healthcare sector barometer. Wednesday brings Bank of America, Citigroup, and Morgan Stanley to round out the bank earnings wave. The collective message from six megabank reports will answer whether the“soft landing” thesis survived Q1 or whether credit stress, CRE maturities, and consumer deterioration are showing up in provisions.

On the economic side, Tuesday’s March PPI is the upstream inflation signal; February ran hot at +0.7%, and feeds directly into the PCE calculation that the Fed watches. Wednesday’s Beige Book provides the qualitative color from all 12 Fed districts ahead of the April 27 FOMC. But Thursday is the marquee data day: March Retail Sales will reveal whether the consumer held up amid oil at $100+ and tariff price hikes; Philly Fed is the second April factory survey, alongside Empire State from Wednesday; and Industrial Production will tell us if factory output contracted alongside the negative payrolls trend. Netflix, after the close on Thursday, will be the first mega-cap tech to report and set the sentiment template for the Big Tech earnings wave that follows.

Bottom line: Banks tell us if the financial system is absorbing the shocks. Retail Sales tell us if the consumer is. Netflix tells us if growth is. All in one week. Define your risk levels before Monday’s open.

Tyler Durden

Sat, 04/11/2026 – 11:40

https://www.zerohedge.com/markets/three-contrarian-signals-arent-easy-ignore-earnings-season-begins

Watch: Axe-Wielding Man Attacks U.S. C-130 Cargo Plane At Irish Airport

Watch: Axe-Wielding Man Attacks U.S. C-130 Cargo Plane At Irish Airport

Footage posted on X appears to show a deranged man hammering away on top of a U.S. Air Force C-130H Hercules parked at Shannon Airport on Ireland’s west coast on Friday.

“A man breached security at Shannon Airport in Ireland, climbed onto a parked C-130 Hercules, and damaged it with a tool,” the Clash Report wrote on X.

WATCH: A man breached security at Shannon Airport in Ireland, climbed onto a parked C-130 Hercules, and damaged it with a tool.

He was arrested. pic.twitter.com/uls2tfgGND

— Clash Report (@clashreport) April 11, 2026

Local media outlet Clare FM described the incident as a “security breach,” with airport operations briefly suspended while police arrested “the person, understood to be a male,” who was “seen in the vicinity of a United States Air Force C-130 Hercules transport aircraft that had been parked on a remote taxiway at the airport.”

US Air Force C-130H Hercules 91-1653 landed at Shannon yesterday from Rosecrans Air National Guard air base St Josephs Kansas, via St. John’s Canada. It spent the night at Shannon, and hasn’t yet gone in to its next military base.#USMilitaryOutOfShannon pic.twitter.com/BkllQx68HX

— Shannonwatch (@shannonwatch) April 11, 2026

“A man breached security at Shannon Airport in Ireland. It’s understood that the person climbed onto the wing of the aircraft and caused damage to the fuselage with an implement, possibly an axe, while it was parked,” the outlet said.

In recent months, at least one far-left group has attacked a critical supply chain node supporting the F-35 stealth fighter jet program in the UK. There are no indications yet from authorities as to whether the C-130 attacker was part of a left-wing threat network

Tyler Durden

Sat, 04/11/2026 – 11:05

https://www.zerohedge.com/military/watch-axe-wielding-man-attacks-us-c-130-cargo-plane-irish-airport

IMF Warns Iran War Will Slow Global Growth, Raise Inflation, And Worsen Food Insecurity

IMF Warns Iran War Will Slow Global Growth, Raise Inflation, And Worsen Food Insecurity

Submitted by OilPrice.com

Severe fuel shortages, hunger, and spiralling inflation will be some of the consequences of the Iran war as the head of the International Monetary Fund said that it would leave “scarring effects” on the global economy.

In a speech by Kristalina Georgieva, the IMF’s managing director, global policymakers were warned that trade disruption across the Middle East over the last month would lead to lower growth and higher inflation.

IMF Başkanı Kristalina Georgieva, İran savaşının küresel ekonomik büyümeyi yavaşlatacağı konusunda uyarıda bulundu. pic.twitter.com/KJjRWlQvYl

— Voice Of Middle East (@VOME_TR) April 10, 2026

The impact of the war was also predicted to be uneven between different countries depending on levels of energy imports and their proximity to the war, according to the world’s foremost economic organisation.

Georgieva’s address on Thursday morning underlined the consequences of what one month of the US and Israel’s war with Iran, and the subsequent hold-up in trading flows across the Strait of Hormuz, would mean for the world economy.

She warned that the most severe fuel disruptions will come for islands in the Pacific Ocean, with the ripple effects then spreading around the world.

She also said that 45 million more people would suffer from food insecurity, while there were “warning lights flashing red” for fuel shortages in several countries.

Inflation expectations could also “break anchor and ignite a costly inflation process”, though Georgieva said long-run confidence in price growth among households and businesses presented “very good and very important” readings.

IMF: Fuel shortages to lead to ‘ripple effects’

The IMF chief added that infrastructure damage, particularly at Qatar’s Ras Laffan gas complex that is critical for energy supplies in Asia, would lead to “no neat and clean return to the status quo”.

The IMF will update its economic forecasts next week, which will feature specific changes on the outlook for the UK economy.

Georgieva asserted that the world economy would suffer from lower growth and warned decision-makers “not to make things worse”.

“I appeal to all countries to reject go-it-alone actions—export controls, price controls, and so on—that can further upset global conditions,” she said.

“Don’t pour gasoline on the fire.”

The IMF’s forecast revisions next week will be the second major update on the global economic outlook after the OECD, a Paris-based think tank, said the UK economy would be harder hit than any other G7 country by the war.

It suggested the UK would suffer the second-lowest level of growth this year and the second-highest level of inflation after the US.

There are renewed hopes that the Strait of Hormuz could reopen and allow trade and production to resume, but economists and policymakers have warned that the full reopening will take weeks, given the risk of further escalation and the wobbly terms of the current ceasefire agreement.

President Trump and Iranian leadership officials have floated the prospect of imposing a toll on ships passing through the critical trading route. Foreign Secretary Yvette Cooper has urged the US administration to resist slapping a tax on ships passing through the Strait of Hormuz.

The UK economy is also predicted to suffer the worst impacts of the war later in the year after the energy price shock from higher oil and gas prices passes through into household bills from July.

Tyler Durden

Sat, 04/11/2026 – 10:30

Mamdani’s First 100 Days Aren’t Getting High Marks From Voters

Mamdani’s First 100 Days Aren’t Getting High Marks From Voters

Zohran Mamdani rode a wave of progressive enthusiasm and sweeping promises to become the Mayor of New York City.

Now, as he closes in on his first hundred days in office, he’s learning that governing is a lot harder than campaigning, and a new poll suggests New Yorkers are starting to be skeptical about what they voted for.

Some of Mamdani’s campaign promises won’t be fulfilled because Gov. Kathy Hochul is refusing to subsidize them. Earlier this year, snow and trash removal problems became major issues, as residents were forced to endure eight-foot-high piles of garbage on the street and rat infestations, all while the area around Gracie Mansion was kept perfectly clean. The brutal winter also resulted in a cold-related death toll of 29. These kinds of crises test political leaders quickly, and he failed.

Then came Monday, when Mamdani held a public event to congratulate himself for New York City filing its 100,000th pothole since he took office in January.

The reaction was swift and unkind.

“Taking credit for filling potholes is like taking credit for changing a lightbulb. It’s what you’re supposed to do,” scoffed Councilman Frank Morano (R-Staten Island) told The New York Post.

A Marist College survey released Wednesday puts Madani’s approval rating at 48% — a number that tells an incomplete story, but not a flattering one.

Mamdani won his election in November with just over 50% of the vote, with Andrew Cuomo coming in second at 41.6% and Curtis Sliwa at 7%.

Clearly, Mamdani is struggling to convince even progressive voters who didn’t vote for him that he’s doing a good job.

But the numbers are even more devastating when you add more context.

Former New York City Mayor Eric Adams had a 61% approval rating at the same point in his term, proving that Mamdani is having a harder time convincing New Yorkers he’s doing a good job than his predecessor did.

The Marist poll, conducted March 26-31 among 1,454 New York City adults with a margin of error of plus or minus 3.3 percentage points, reveals a city that remains skeptical but is still forming its verdict. While 30% disapprove of Mamdani’s performance. 23% remain undecided — a number that Marist polling director Lee Miringoff flagged as a meaningful vulnerability. “There are a lot of people still on the fence. The jury is out,” Miringoff told The New York Post.

The sharpest drag on Mamdani’s numbers comes from a specific and politically significant corner of the electorate: Jewish voters. Only 38% of Jewish residents view Mamdani favorably, while 55% view him unfavorably, putting him underwater with Jewish New Yorkers by 17 points. They are the only religious group in the poll giving him a net-negative rating.

Miringoff noted Mamdani’s continued unpopularity in this community directly.

“Mamdani is going to have to pass the test of time with the Jewish community,” he said.

“Jews are the voters least likely religious group to give Mamdani the benefit of the doubt.”

It’s easy to understand why.

Mamdani has accused Israelis of genocide in Gaza, publicly backed the BDS movement, and aligned himself with left-wing activists — including Hasan Piker — whom many Jewish voters view as antisemitic. Mamdani’s wife has also come under fire for liking posts on social media celebrating the October 7 attacks in Israel.

Still, the broader portrait from the Marist poll is complicated.

Despite having an approval rating below 50%, the poll found 55% of registered voters hold a favorable view of the mayor, and 60% believe he’s fulfilling his campaign promises. Fifty-six percent say the city is moving in the right direction, and 52% think he’s changing New York for the better. Nearly 75% say he works hard. These are not the numbers of a mayor in collapse. They are, however, the numbers of a mayor who hasn’t yet closed the sale.

When asked about the poll at a Brooklyn press conference, Mamdani deflected with characteristic self-assurance.

“You know, I will always leave the grades to New Yorkers themselves,” he said.

“What I will say is that we are coming to the end of a hundred days in office, and we have sought to make this period one where we provide New Yorkers with a glimpse as to what these next four years will look like.”

Tyler Durden

Sat, 04/11/2026 – 09:55

https://www.zerohedge.com/political/mamdanis-first-100-days-arent-getting-high-marks-voters

Several US Warships Reportedly Transit Strait Of Hormuz As Pakistan Talks Led By Vance Start With Indirect Format

Several US Warships Reportedly Transit Strait Of Hormuz As Pakistan Talks Led By Vance Start With Indirect Format

Summary:

Axios reporting that ‘several’ US Navy warships crossed the Hormuz Strait on Saturday without coordination with Tehran in a huge, surprising development.

Peace talks in Pakistan begin in indirect format, led by Vance and on Iran side – Ghalibaf, Arachchi.

Saturday sees more Israeli strikes on Lebanon, with Hezbollah supporting Pakistan talks but rejecting ‘separate deal’ directly with Israel.

Trump on talks and potential bigger future attacks on Iran: “You don’t need a backup plan” as Iran’s “military is defeated”.

Will the U.S. invade Iran before 2027?

Yes 31% · No 70%

View full market & trade on Polymarket

* * *

Several US Warships Cross Hormuz Strait: Axios

Just as indirect talks kick off in Islamabad, a shocking and surprise development is being reported by Axios’ Barak Ravid, though this is not confirmed:

🚨🇺🇸🚢Several U.S. navy ships crossed the Strait of Hormuz on Saturday, U.S. official says

🚨🇺🇸🚢The move was not coordinated with Iran. It’s the first time this happens since the beginning of the war

— Barak Ravid (@BarakRavid) April 11, 2026

If accurate, are we witnessing Trump suddenly pile on more leverage before negotiations even get off the ground? It seems like the Iranians would have noticed several US Navy warships passing. Either they held off attack for the sake of pursuing peace, or this was truly done ‘stealthily’ and Iranian capabilities are degraded to the point they may have ‘missed’ it. Or is this an attempt to muddy the negotiations? Sabotage? Ravid after all has long stood accused of pushing an Israeli agenda in his reporting.

Talks Begin with Indirect Format Mediated by Pakistanis

By Saturday afternoon (local), the highest-level US-Iran-related talks since the 1979 Islamic Revolution have kicked off in Islamabad. Vice President JD Vance met Pakistan’s Shehbaz Sharif just ahead of the negotiations, and also senior Iranian officials were greeted by Sharif and other Pakistani leaders. Iran’s delegation is led by Parliament Speaker Mohammad Bagher Ghalibaf and Foreign Minister Abbas Araghchi. The engagement by each side has begun indirectly.

Pakistan has made clear it is working to facilitate direct negotiations between the US and Iran to fully bring to an end the six-week war in the Middle East. Sharif hailed both sides’ commitment to engaging constructively, and “expressed the hope that these talks would serve as a stepping stone toward durable peace in the region,” his office stated in a news release.

“Vance was joined for the bilateral meeting by special envoy Steve Witkoff and President Donald Trump’s son-in-law, Jared Kushner,” CNN reviews. “Sharif was joined by Deputy Prime Minister and Foreign Minister Sen. Mohammad Ishaq Dar, along with Interior Minister Sen. Syed Mohsin Raza Naqvi, according to a news release from the Pakistani prime minister’s office. There was no press coverage of the meeting.”

CNN also has this interesting detail on just how many officials have traveled with the Iranian side: “Iran’s delegation in Islamabad is made up of 71 people, including negotiators, experts, media representatives and security, Tasnim reported.” According to some of the latest:

Tehran reportedly set 2 main conditions. The issue of frozen funds being already accepted by Washington. Despite no strikes on Beirut, attacks in southern Lebanon are ongoing and are now part of the negotiations.

Below: Ghalibaf (Speaker of Parliament) – Araghchi (Foreign Minister) – Ahmadian (Secretary of the Defense Council) – Hemmati (Central Bank Governor)

Lebanon Fighting Has Not Stopped But Rare Diplomatic Contact Made

Fighting has not fully stopped in Lebanon, raising the possibility of derailing the Pakistan talks, after Tehran had earlier in the week threatened that it could pull out if Israel keeps ups its attacks. On Saturday, Lebanon’s Health Ministry raised the death toll from the Israeli surprise Wednesday strikes to 357, and suggested the figure could rise amid several days of search and recovery operations.

But one rare bright spot in terms of diplomatic contact, as international reports say the Lebanese and Israeli ambassadors to the United States held a phone call in the first direct contact reported between the two countries, ahead of ceasefire talks scheduled in Washington for next week.

Meanwhile, Iran confirmed it is coordinating with Lebanon to ensure ceasefire commitments are upheld across all fronts, a foreign ministry spokesperson said on state TV from Islamabad, where senior US and Iranian officials are holding talks to end the six-week war. At the same time, Lebanese officials close to Hezbollah told Reuters the group supports the Pakistan dialogue and considers it the appropriate path, rejecting a separate round of talks planned in Washington next week.

Iranian delegation in Pakistan seeks to present ‘unity’ of government/military leadership and coordination:

I told @nytimes that the size and composition of Iran’s delegation shows “that they have not come to stonewall,” but are there with full authority and seriousness to reach a deal with the United States. Such a large delegation of experts would only be deployed if negotiations…

— Vali Nasr (@vali_nasr) April 11, 2026

Israeli airstrikes have continued on a sporadic basis: “Lebanon’s National News Agency (NNA) reports that an Israeli air attack on the town of Kfar Sir in the Nabatieh district has killed four people, including a paramedic, and injured four,” writes Al Jazeera Saturday. “Another Israeli attack on the town of Zefta, also in the Nabatieh district, killed three people, including a member of the Lebanese Civil Defense, and wounded two.” There’s been an additional third attack on Toul and Nabatieh, killing three and injuring several more.

Trump: ‘No Backup Plan’ Needed Since Iran’s Military ‘Defeated’

“You don’t need a backup plan,” Trump told reporters Friday when asked about possible next steps of Pakistan talks fail, according to a report by The Hill as he departed Washington en route to Florida. “The military is defeated.”

“Their military is gone. We’ve degraded just about everything,” Trump added. These words suggest he sees the Pakistan peace process as a serious offramp. However, as we and others have reported, there’s an ongoing Pentagon build-up in the region. This has kicked off speculation that a bigger US attack could be around the corner, at that the Islamabad summit is cover for ongoing military preparations.

NEW: US officials tell the WSJ that jets have recently arrived in the Middle East, and 1,500 to 2,000 troops from the Army’s elite 82nd Airborne could arrive in the coming days, as well as thousands of sailors and Marines.

The USS George H.W. Bush carrier strike group and 11th… pic.twitter.com/dXxG9q28N5

— Faytuks Network (@FaytuksNetwork) April 10, 2026

And yet, the reality is that Iran remains in control of the Strait of Hormuz, with only a tiny trickle of ‘vetted and approved’ vessels making it through, and reportedly paying hefty toll fees to Tehran, which Trump has warned against. Iran in Pakistan is asking for sanctions to be lifted. If the US grants this, Iran will be in a better position than went the war started, which will be tantamount to gains made through the fight.

Tyler Durden

Sat, 04/11/2026 – 09:55

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}