Category: News

China Loads Up On US Chip Tools Via Southeast Asia Amid Supply Chain Shift

China Loads Up On US Chip Tools Via Southeast Asia Amid Supply Chain Shift

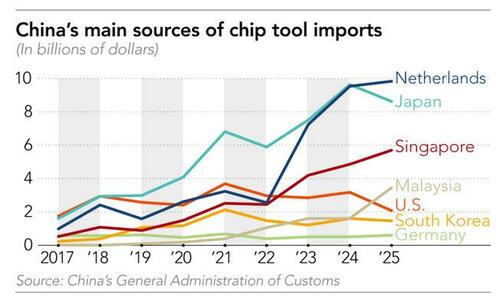

China’s imports of chipmaking equipment from Malaysia and Singapore rose sharply in 2025 to surpass those from the US, which sank to an eight-year low, an analysis by Nikkei Asia has found – even as American companies remain a vital source of advanced tools for the country.

While the Netherlands and Japan remain China’s primary foreign sources of critical semiconductor manufacturing machines by shipment origin, imports from the two Southeast Asian countries reached record levels: $5.7 billion for Singapore, up more than 17% year over year, and $3.4 billion for Malaysia, more than double the 2024 figure.

Direct imports from the US, meanwhile, declined more than 34% to about $2 billion, the lowest level since 2017, according to Chinese customs data. The decline was to be expected following President Trump’s return to the White House, as he sharply limited access of US semiconductors to China, although tensions began earlier. Since Trump’s first term and during the subsequent Biden administration, the US has raised tariffs and imposed fresh export controls aimed at slowing China’s advances in chipmaking technologies for defense, space and artificial intelligence applications.

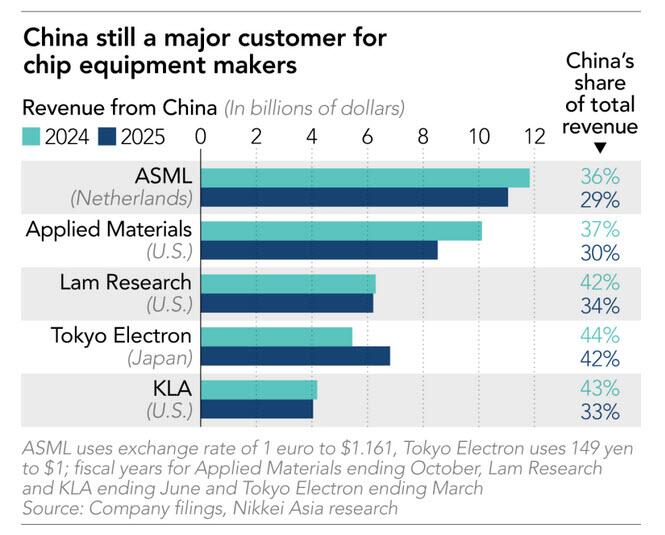

Despite the decline, the Chinese market remained a critical revenue source for leading US chip equipment makers last year. Applied Materials, Lam Research and KLA all earned more than 30% of their total sales from China in fiscal 2025.

Charles Shi, a veteran semiconductor analyst with Needham & Co., told Nikkei Asia that the uptick in China’s imports from Southeast Asia is mainly due to the large number of U.S. chip equipment makers expanding manufacturing capacity in the region to better serve non-U.S. clients.

“Lam Research is building significant manufacturing capacity in Malaysia as they work to meet growing equipment demand beyond what their U.S. manufacturing capacity can serve,” Shi said. “Singapore has been a popular destination for [the] U.S. equipment industry to go overseas. For example, both Applied Materials and KLA have been manufacturing in Singapore.”

The three top U.S. chip tool makers generated nearly $19 billion in combined revenue from China in fiscal 2025, significantly exceeding figures implied by customs data based on where shipments originated from and underscoring the effectiveness of American vendors’ production diversification strategies. Nikkei Asia first reported their production shift toward Southeast Asia in early 2023.

For ASML of the Netherlands, China’s share of revenue came to 29.1% in 2025, while the figure for top Japanese chip tool maker Tokyo Electron was more than 40% for fiscal 2025.

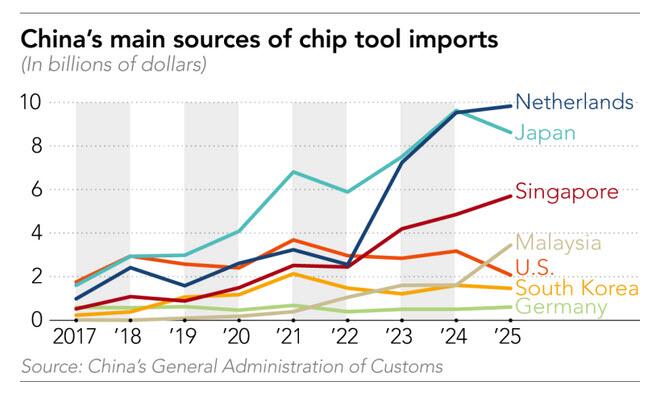

Anticipating major chip wars, over the course of 2020 to 2025, China’s accumulated chip tool imports from Japan reached more than $42 billion, followed by the Netherlands’ $35 billion . Japan is home to many top chip equipment makers such as Tokyo Electron, Screen Semiconductor Solutions and Ebara, while the Netherlands has the world’s largest chip equipment maker, ASML, as well as key suppliers such as ASM, an atomic-level deposition tool specialist, and Besi, a maker of advanced chip packaging tools.

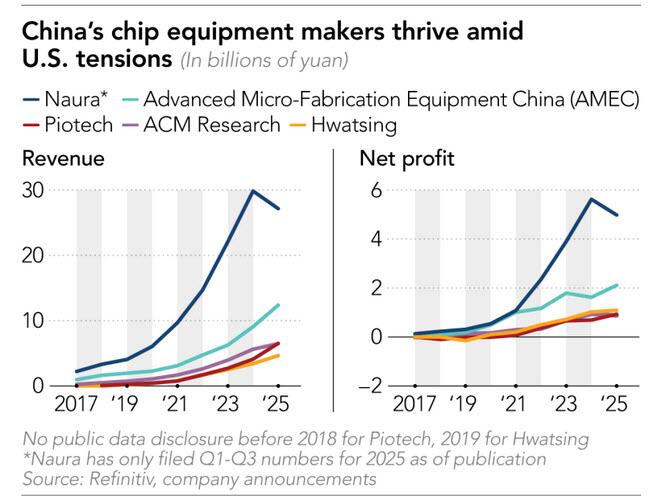

Meanwhile, China’s domestic chipmaking equipment makers are experiencing a once-in-a-generation surge in growth, driven by Beijing’s push to foster homegrown tools and reduce reliance on foreign technologies. Top suppliers all reported record revenue and profits for 2025, led by Naura, Advanced Micro-Fabrication Equipment Inc. China (AMEC), ACM Research and Piotech.

Naura, China’s answer to Applied Materials, has seen its revenue balloon from 6.05 billion yuan ($887 million) in 2020 to 27.14 billion yuan in the first three quarters of 2025. Revenue for AMEC skyrocketed more than 400% from 2020 to 2025. Piotech, a thin-film deposition chip tool specialist, has seen its revenue grow 13 times between 2020 and 2025.

Shi of Needham said China has made good progress in fostering local chip tool makers, but internal competition is intensifying. “While leading domestic equipment companies are still posting strong revenue growth, there are indications that their margin performance is deteriorating,” Shi said of Chinese chipmaking companies. “We believe intensifying domestic competition might have forced domestic equipment companies to ‘race to the bottom’ by undercutting each other’s prices.”

With China’s equipment suppliers becoming more competitive in recent years, US policymakers are seeking to further close loopholes in export rules. In April, bipartisan lawmakers introduced the MATCH Act, which calls on “multilateral allies” to coordinate more closely in aligning and tightening export restrictions across key segments of the chipmaking equipment industry. These measures would further target critical “chokepoint” components and machinery, as well as shipments to leading Chinese memory and logic chipmakers, including CXMT, YMTC, SMIC and Hua Hong.

“Chinese tool companies on the Entity List are unable to get access to U.S. parts, but there are many parts that Europe and Japan can backfill, and that’s the conundrum that we find ourselves in today,” Kevin Kurland, a former official at the U.S. Department of Commerce and current senior advisor at Beacon Global Strategies, told Nikkei Asia. “If controls don’t get aligned multilaterally with allies, U.S. controls can undercut American companies’ competitiveness while allowing Chinese companies to continue to function and operate – a lose-lose outcome.

Alex Rubin, a former CIA China analyst and visiting fellow at the Hoover Institution, told Nikkei Asia that “component export controls definitely make sense.”

“It’s very similar to what we are seeing in commercial aviation: China is assembling the finished C919 aircraft, but is sourcing parts from U.S. and European suppliers. Chinese companies are trying to compete with Boeing and Airbus, while sourcing from a similar supply chain,” Rubin said.

While China is still massively sourcing foreign chip tools, its ultimate goal is self sufficiency, industry sources say.

While durability, reliability and performance may not be at the same level, “for every foreign chipmaking tool, material and component you can think of, you could find Chinese versions,” said an executive with a Taiwanese chipmaking tool who participated in the Semicon China industry event in late March. “Chinese chipmakers will continue to buy foreign solutions while they can, but there’s no doubt about the country’s will to increase the use of homegrown suppliers.”

“China is adopting a two-way approach: developing homegrown tools while continuing to purchase foreign equipment whenever possible. Since imported tools often offer better performance, they are still buying aggressively — and even repurposing consumable parts from one piece of equipment to repair other chipmaking machines,” another chip industry executive with knowledge of the matter told Nikkei Asia.

A third executive with a Chinese chipmaking tool supplier told Nikkei Asia that the aggressive expansion plans by Chinese logic and memory chipmakers have given local vendors more opportunities to break into and secure a position in the domestic supply chain.

Nikkei Asia was the first to report that Chinese top chipmakers led by SMIC, Hua Hong and Huawei-linked chipmakers are aiming to aggressively expand advanced chip production capacity, including on the performance level of 7-nanometer or even 5-nm technologies, to support the rise of domestic AI chip developers. Meanwhile, top Chinese memory chip producers CXMT and YMTC are launching their largest expansions in response to the unprecedented global memory crunch amid the AI boom, Nikkei revealed in early February.

American allies such as the Netherlands and Japan have already introduced rules to align with U.S. export controls, but policymakers in Washington feel those restrictions are still much too loose. The U.S. has imposed multiple rounds of regulation on exports to China and has added many leading Chinese chip equipment suppliers and chipmakers to its Entity List.

The MATCH Act, if passed, could further limit global vendors’ ability to supply critical tech to China. The bill targets some older – though still critical – generations of chipmaking machines as well as components, both of which can be chokepoints for China’s efforts to build up its domestic chip industry. Introduced in early April, the bill still needs to go through the legislative process, and it remains unclear how the Netherlands, Japan and other countries would respond to any diplomatic pressure to comply. For example, only ASML in the Netherlands and Canon and Nikon in Japan can produce commercially viable lithography machines — an area where China continues to face significant challenges.

Tyler Durden

Wed, 04/22/2026 – 02:45

https://www.zerohedge.com/markets/china-loads-us-chip-tools-southeast-asia-amid-supply-chain-shift

Spain’s Services Crumble; Military-Aged Male Migrants Overwhelm Registry Offices

Spain’s Services Crumble; Military-Aged Male Migrants Overwhelm Registry Offices

Authored by Steve Watson via Modernity.news,

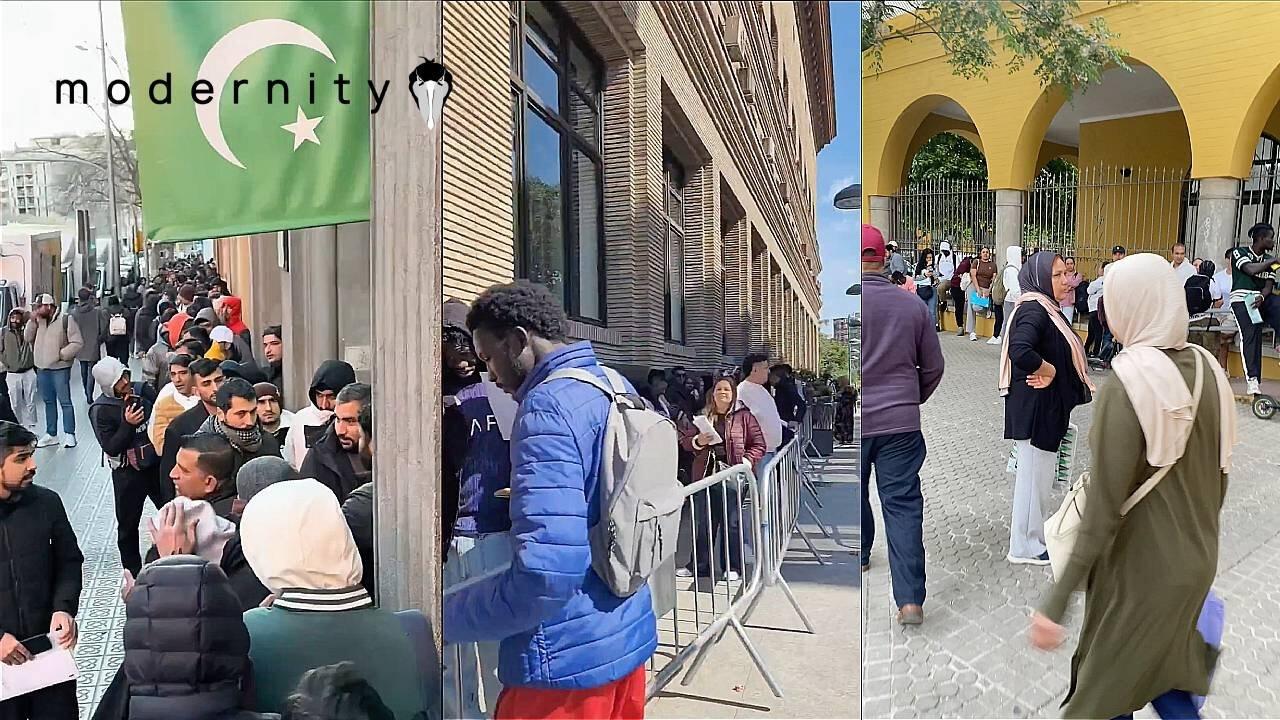

Huge queues of migrants continue to snake through Spanish cities this week as Prime Minister Pedro Sánchez’s socialist government opened the floodgates on its controversial mass regularization program. Applications for legal status and work permits kicked off last Thursday following cabinet approval, and the scenes unfolding in Barcelona, Zaragoza, Sevilla and beyond confirm the worst fears of those who warned this amnesty would break the system.

It is the direct result of the chaos already documented after Sánchez rammed through his plan to legalize half a million undocumented migrants already inside the country. As thousands swarmed consulates and offices demanding paperwork, the very public services Spaniards rely on are now buckling under the pressure.

In Barcelona, Pakistani migrants rushed the consulate for criminal record certificates required under the scheme.

SPAIN: Pakistani migrants are rushing to the consulate in Barcelona for their paperwork, as the government plans to regularize 500,000 illegals.

Notice they are all military-aged men, no women or children. They will soon be able to move freely across Europe. This won’t end well. pic.twitter.com/tSepsIqY55

— Dr. Maalouf (@realMaalouf) April 19, 2026

Miles de pakistaníes después de ser regularizados por Pedro Sánchez se van a la oficina de servicios sociales del Ayuntamiento de Barcelona?? para coger el certificado de vulnerabilidad y tener derecho a casa gratis y el IMV

Todo esto pagado por ti por supuesto. pic.twitter.com/EWtILqPBcE

— Anonymous Tabarnia ? (@Anonymous_TA) April 18, 2026

Footage from Zaragoza showed similar crowds overwhelming local offices:

???Footage from Spain’s Zaragoza as thousands of migrants rush to be legalized.

The VOX party: “Total collapse of the City Council in the face of the avalanche of illegal immigrants who want to take advantage of Sánchez’s regularization.”pic.twitter.com/OISJ1gsyXs

— Remix News & Views (@RMXnews) April 20, 2026

In Valencia the lines were massive:

?? Así son las kilométricas que colapsan el centro de Valencia por la regularización masiva de Sánchez. pic.twitter.com/SjyUctmL0I

— okdiario.com (@okdiario) April 20, 2026

In Sevilla, VOX candidate Manuel Gavira posted video of long lines outside city hall and delivered a stark warning: “These are the lines in Seville to manage mass regularization. What you see here today… tomorrow you’ll see it in the clinics, in social assistance, in housing, and in all public services. It’s called collapse. And it has already begun.”

Estas son las colas en Sevilla para gestionar la regularización masiva.

Lo que hoy ves aquí… mañana lo verás en los ambulatorios, en las ayudas sociales, en la vivienda y en todos los servicios públicos.

Se llama colapso. Y ya ha empezado. pic.twitter.com/4rrHZUVDGs

— Manuel Gavira ?? (@GaviraVox) April 20, 2026

The Daily Mail reports that migrants are camping overnight outside registry offices and shopping-mall centers in Catalunya, Andalucia and Asturias. One Colombian in Barcelona told reporters he arrived at 10 or 11pm and waited 15 hours. A Honduran migrant who slept on the floor said, “A very large group of people almost trampled me… We risked our lives, but it will be worth it.”

Spain throws open its doors to undocumented migrants: Huge queues continue to form after socialist government granted citizenship to 500,000 people https://t.co/2kaUvoPqlr

— Daily Mail (@DailyMail) April 20, 2026

Sánchez himself defended the move in a public letter, claiming it was both moral and economic: “Spain is ageing… Without more people working and contributing to the economy, our prosperity slows, and our public services suffer.”

In every city in Spain there are lines of invaders to whom Pedro Sanchez has promised identity documents to regulate them. Pedro Sanchez, public enemy number one of Europeans. pic.twitter.com/k1Mo3Kpa2u

— RadioGenoa (@RadioGenoa) April 17, 2026

Yet critics point out the obvious: Spain already has roughly 840,000 undocumented migrants and a foreign-born population nearing 10 million out of 50 million total. Ninety percent of new jobs have gone to immigrants while native Spaniards face housing shortages and strained services. Legalizing another half-million without fixing those problems only accelerates the breakdown.

The nationalist VOX Party has labeled the policy an “invasion” that “attacks our identity” and has vowed to challenge it in the Supreme Court. Meanwhile, immigration officers are threatening to strike over lack of resources. Local councils are already talking about early closures because the system cannot cope.

Just days before the avalanche of applications began, legal challengers warned that Sánchez’s mass amnesty could still be stopped. A conservative group, Hazte Oír, successfully petitioned the Spanish Supreme Court to review the controversial Royal Decree used to bypass parliament. The court has given the government a non-extendable 20-day deadline to hand over all files, raising the real possibility of a precautionary suspension that would freeze the entire legalization process.

Hazte Oír argued the decree creates “irreparable damage” by granting residence, work permits, Social Security registration, access to benefits and the suspension of expulsion orders to hundreds of thousands of people — changes that would be almost impossible to reverse even if the court later rules the shortcut illegal.

The group stressed that the measure “structurally alters the State’s immigration policy, with direct and lasting effects” on the labour market, public benefits system, municipal registry, “and, in the medium term, the electoral roll.”

Lawyer Javier María Pérez-Roldán warned: “Massive regularization without planning directly impacts the saturation of essential public services (educational and social), affecting the collective interests that this association defends.”

VOX leader Santiago Abascal had already sounded the alarm as the first queues formed: “These are the lines to manage mass regularization in each municipality of Spain. Tomorrow this chaos will move to the centres of health, to the social services, to the real estate agencies… It’s called thirdworldization. It’s already happening. Our priority is to reverse it, radically.”

The scenes unfolding this week prove Abascal correct: the chaos has already begun. If the Supreme Court does not intervene quickly, Spain will have crossed a point of no return — handing EU-wide freedom of movement to half a million undocumented migrants while its own public services buckle.

The pattern is unmistakable. Sánchez’s progressive coalition ignores the strain on housing, healthcare, schools and welfare while fast-tracking residency permits that will let recipients work legally and eventually travel freely throughout Europe in Schengen. Once again, Spanish citizens are told to accept lower wages, longer waits and cultural transformation in the name of “diversity” and GDP growth that never seems to reach the native population.

Spain is not alone in Europe, but it stands out for doubling down while neighbors tighten borders. The queues in Barcelona, Zaragoza and Sevilla are not a one-off photo opportunity. They are the visible symptom of a policy that prioritizes outsiders over citizens and votes over sovereignty. As VOX has warned, the collapse has already begun. Spaniards who value their country, their culture and their children’s future have been put on notice.

The rest of the West should watch closely. When governments treat borders as suggestions and citizens as afterthoughts, the consequences arrive faster than any press release can spin them.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Wed, 04/22/2026 – 02:00

Ukraine Billionaire Spends $554 Million For World’s Most Expensive Apartment In Monte Carlo

Ukraine Billionaire Spends $554 Million For World’s Most Expensive Apartment In Monte Carlo

It makes sense that a nation which has consistently ranked at the top in all global corruption rankings, produces some of the most extravagant demonstrations of stolen wealth.

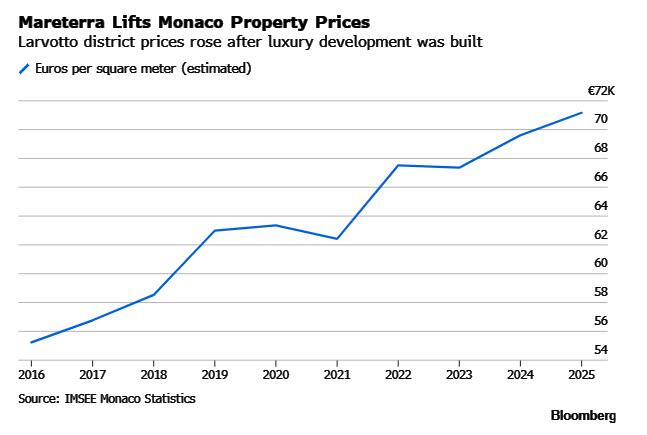

Take billionaire Rinat Akhmetov, among many other assets owner of the Azovstal steel complex in Mariupol which became one of the defining clashes in the Ukraine war, and Ukraine’s richest man, who bought a vast, five-floor luxury apartment in Monaco’s most prestigious new development for an eye-popping €471 million ($554 million), making it the biggest single home transactions in history according to Bloomberg.

The 21-room waterfront property, acquired by the businessman’s holding company, is located in the principality’s Mareterra district. The new area, built on reclaimed land, was inaugurated by Prince Albert II in 2024 and has drawn ultra-rich investors from around the world.

Le Renzo in Mareterra, Monte Carlo

Situated in the flagship “Le Renzo” building, the apartment stretches over about 2,500 square meters (27,000 square feet), not counting balconies and terraces looking out over the Mediterranean Sea. It also has a private swimming pool, jacuzzi and comes with at least eight parking spots.

Details of the sale, which was finalized in 2024, or about two years after Akhmetov’s country was deep in a brutal war with thousands of his countrymen dying on the front every day, come from the principality’s property records, as well as a stash of emails and preliminary deeds reviewed by Bloomberg Businessweek from Distributed Denial of Secrets, a nonprofit that preserves hacked and leaked materials believed to be in the public interest.

Akhmetov’s holding company, System Capital Management, or SCM, confirmed it it had made an acquisition in the development, though declined to provide details about the property or price.

“SCM’s international investment portfolio has included a standalone premium real estate portfolio for over ten years, as has been publicly stated on multiple occasions,” it said in a statement. “Among its assets is the ‘Le Renzo’ project, in which we made an investment on the primary market in 2021.”

Premium real estate; half a billion dollars for an apartment is a different galaxy, especially sine most of the money was likely sourced from US taxpayers. The reported price would make it the biggest known home sale in history, outstripping the recent sale of developer Nick Candy’s Chelsea mansion for more than $350 million or the sale of a New York penthouse apartment to hedge fund manager Ken Griffin for about $240 million.

Perched on a rocky outcrop between France and Italy, Monaco has long been the priciest real-estate market in the world because of its small size and tax haven status. The Mareterra development was built up over a decade on land reclaimed from the sea and includes 114 luxury villas, townhouses and apartments set around gardens, a harbor and public promenade.

Akhmetov’s purchase agreement in the principality came just before Russia’s invasion of Ukraine in 2022. The war subsequently created upheaval within his business empire including attacks on energy assets in his home country.

Akhmetov was pivotal in arranging a lasting relationship between his employee and close friend Paul Manafort and former Ukraine president Viktor Yanukovich, whose US-mediated ouster was the trigger for the eventual war between Ukraine and Russia.

The tycoon has a net worth of more than $7 billion, according to the Bloomberg Billionaires Index. His fortune is rooted in SCM, Ukraine’s largest industrial conglomerate with investments in metallurgy, mining and energy, in addition to property.

Akhmetov has also been associated with a string of other ultra high-end property acquisitions in the past, including the 2019 purchase for €200 million of the historic Villa Les Cèdres on the French Riviera. The sprawling estate in the exclusive Saint-Jean-Cap-Ferrat was once owned by King Leopold II of Belgium. In 2011, Akhmetov also reportedly bought a penthouse in London’s prestigious One Hyde Park development opposite the Harrods department store in Knightsbridge.

Mareterra properties have sold for prices surpassing the symbolic €100,000 a square meter, according to local property agents, who asked not to be named because the details aren’t public. One three-bedroom property is currently on the market for about €76 million. There are also rental listings for four and five-room apartments for €150,000 a month.

Official statistics show that the Larvotto district where Mareterra is located has become the principality’s most expensive in terms of estimated selling prices per square meter. The data doesn’t break out prices for properties in the development and these aren’t generally listed on broker websites.

“Monaco remains one of the world’s most exclusive and resilient residential markets,” Savills said in a report published in March, noting that it’s “shaped by structural scarcity and sustained high international demand.”

Tyler Durden

Wed, 04/22/2026 – 00:05

Nobel Physicist Predicts ‘End-Date’ For Modern Civilization

Nobel Physicist Predicts ‘End-Date’ For Modern Civilization

Authored by Steve Watson via Modernity.news,

Nobel Prize-winning physicist David Gross has provided a sobering timeline for the potential end of modern civilisation, citing the escalating risks of nuclear war.

The 2004 Nobel laureate estimates that humanity may have roughly 35 years remaining before facing existential catastrophe from nuclear conflict.

In an interview, Gross detailed his assessment based on probability calculations similar to radioactive half-life models. He noted that after the Cold War, estimates put the annual chance of nuclear war at one percent. However, he believes the figure is now closer to two percent.

Chilling warning from Nobel physicist as date is set for humanity’s final destruction https://t.co/WKhFHWcIs3

— Daily Mail US (@Daily_MailUS) April 20, 2026

“Even after the Cold War ended, when we had strategic arms control treaties, all of which have disappeared, there were estimates that there was a one percent chance of nuclear war every year,” Gross said.

He continued, “I feel it’s not a rigorous estimate that the chances are more likely two percent. So that’s a one-in-50 chance every year. The expected lifetime, in the case of two percent per year, is about 35 years.”

Gross pointed to deteriorating global conditions as justification for his higher estimate. “Things have gotten so much worse in the last 30 years, as you can see every time you read the newspaper,” he stated.

He highlighted ongoing conflicts and nuclear proliferation. There are now nine nuclear powers, complicating arms control significantly. “Even three is infinitely more complicated than two,” Gross observed.

Recent developments include the expiration of the New START treaty on February 5, 2026, with no major nuclear arms-control agreements signed in the past decade.

Gross also raised concerns about advancing technology, particularly automation and artificial intelligence in weapons systems.

“The agreements, the norms between countries, are all falling apart,” he said. “Weapons are getting crazier. Automation, and perhaps even AI, will be in control of those instruments pretty soon.”

“It’s going to be very hard to resist making AI make decisions because it acts so fast,” Gross warned, noting that AI can sometimes “hallucinate” or produce inaccurate outputs.

He expressed deep concern for humanity’s future beyond scientific progress: “You asked me to think about the future, and I am obsessed the last few years, thinking about that, not the future of ideas and understanding nature, but of the survival of humanity.”

Despite the grim outlook, Gross expressed some optimism, stating of nuclear weapons: “We made them; we can stop them.”

The post quickly drew responses on X reflecting a range of views.

One took a philosophical stance: “There no end date.. people have been guessing.. for a long time.. when it our time it’s our time… an Asteroid can hit Tomorrow and wipe out the planet and we probably wouldn’t be able to process it… a renegade Volcano can explode setting off the next extinction event and we wouldn’t know what to do.. live your life.. it’s all you can do..”

Several users ironcially turned to AI for answers, with one writing: “Tell us the date and time @grok.” and another echoing: “@grok what’s the date and time?”

A different commenter expressed skepticism about the role of global elites: “If his thinks rich billionaires are going to allow nuclear war.. then take away his Nobel prize cause that not happening any time soon.”

Gross, who won the Nobel Prize for his work on asymptotic freedom in quantum chromodynamics, has shifted much of his recent focus to humanity’s long-term survival. His remarks connect the probability model directly to current events, including tensions in Europe, the Middle East, and South Asia.

By framing the risk in concrete yearly percentages and an expected timeframe, the physicist aims to translate abstract geopolitical dangers into something more immediate and calculable. Whether the two-percent annual figure holds or shifts with future developments remains to be seen, but the underlying message is clear: the window for preventive action is narrowing.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Tue, 04/21/2026 – 23:25

https://www.zerohedge.com/geopolitical/nobel-physicist-predicts-end-date-modern-civilization

South Korea Curbs Syringe Hoarding As Iran War Cripples Supply

South Korea Curbs Syringe Hoarding As Iran War Cripples Supply

The downstream consequences from the Hormuz closure are popping up in the most unexpected places.

According to Bloomberg, South Korea’s health regulators are stepping in to curb syringe hoarding as supply chain disruptions tied to the Middle East conflict threaten the availability of essential medical supplies.

While overall syringe production remains steady at about 4.5 million units a day – slightly above 2025 averages – hospitals report dwindling inventories, and online platforms show rising prices and empty virtual shelves, according to the Ministry of Food and Drug Safety.

Starting Monday the ministry will deploy 35 inspection teams, made up of police and medical device officials, to carry out a nationwide probe into intermediaries and other firms suspected of creating artificial shortages to drive up profits.

Syringes are the latest everyday item in South Korea to be hit by spillover from the Iran war, which has disrupted supplies of naphtha, a petroleum derivative used in plastics manufacturing. Products such as syringes and intravenous fluid bags rely on polypropylene and polyethylene, both derived from naphtha.

Earlier, we discussed how US exports of ethane – which is also a key building block in plastics production – to China have soared, as naphtha supply remains indefinitely blocked as a result of the Hormuz closure.

“We’ve seen a surge in speculative demand as hospitals and clinics are preemptively ordering extra stock in anticipation of price hikes, which is creating artificial bottlenecks,” said spokesperson Jung Chul-woo of the Korea Medical Devices Association, which represents more than 700 suppliers.

Shortages of Middle Eastern crude have already stoked supply concerns in Asia’s fourth-largest economy, threatening everything from garbage bags to popular instant noodle brands, while also contributing to a broader jet fuel crunch across the region.

After manufacturers raised concerns about potential naphtha shortages, the government called on domestic refiners to prioritize supply allocations for local companies for the next three months, an official at the Ministry of Trade, Industry and Energy said. The ministry’s crackdown comes after a government mandate took effect April 14 banning the hoarding of syringes and needles. Withholding inventory or inflating prices is now punishable by up to three years in prison, or 100 million won ($68,000) in fines.

“Acts of hoarding medical devices essential to public health while exploiting a crisis are unacceptable,” Food and Drug Safety Minister Oh Yu-Kyoung said in a statement.

Tyler Durden

Tue, 04/21/2026 – 23:00

https://www.zerohedge.com/markets/south-korea-curbs-syringe-hoarding-iran-war-cripples-supply

From Tank Rides To Overseeing Missile Tests: Kim Jong Un’s Teenage Daughter Prepped As Likely Successor

From Tank Rides To Overseeing Missile Tests: Kim Jong Un’s Teenage Daughter Prepped As Likely Successor

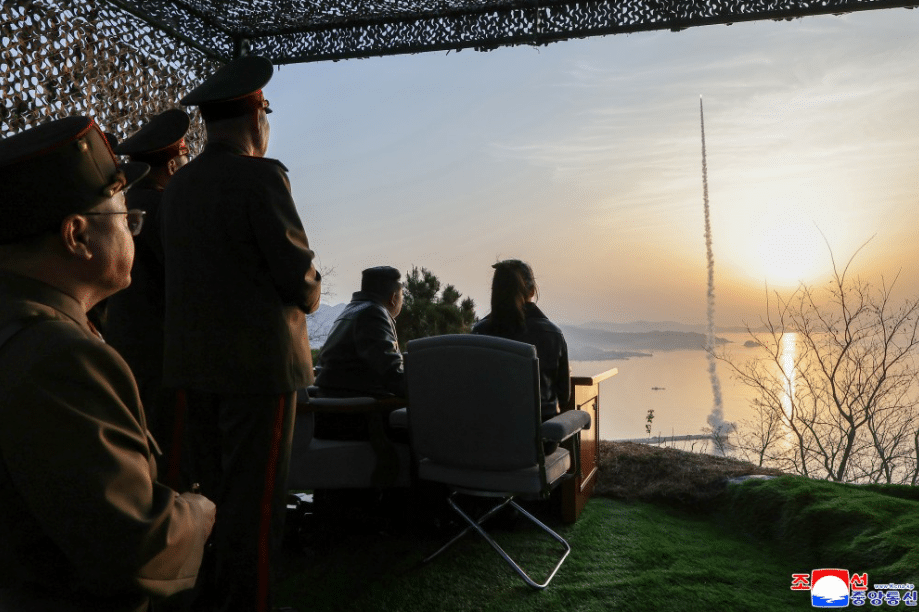

Longtime North Korean Leader Kim Jong Un oversaw a test launch of missiles equipped with multiple reentry vehicles, a move that drew limited international attention despite its escalation risk.

“The purpose of the test-fire is to verify the characteristics and power of cluster bomb warhead and fragmentation mine warhead applied to the tactical ballistic missile,” North Korean state media reported Sunday. “Five tactical ballistic missiles, launched towards the target area around an island about 136 km away, struck the area of 12.5~13 hectares with the very high density, fully displaying their combat might.”

Kim’s daughter, Kim Ju Ae, attended the launch – the latest in a series of recent public appearances alongside her father – a trend which has only intensified speculation about his succession planning.

Just several weeks ago, his daughter was filmed and photographed enjoying a battle tank ride alongside her father. Per prior reporting in the NY Times:

It seems like a familiar rite of passage: a dad teaching his daughter to drive. Except in this case, the girl is at the helm of a hulking battle tank, her head sticking out from the driver’s hatch, while the father — the North Korean leader, Kim Jong-un — reclines on the hull behind her.

The video and photographs of the girl, Kim Ju-ae, who is believed to be around 13, apparently driving the heavily armed vehicle during a military exercise, were published last month by North Korean state media. It was the latest in a series of public appearances that have fueled speculation that she is being groomed to succeed her father.

That theory has gained added credence from South Korea’s spy agency, which now believes Ju-ae has officially been chosen to succeed her father, South Korean lawmakers briefed on the matter said on Monday. They added that the agency’s analysis was based on “credible intelligence” rather than circumstantial context.

In the tank video, Mr. Kim is shown riding on the hull, smiling and occasionally leaning down to speak to his daughter, who is looking straight ahead.

A South Korean lawmaker subsequently saw in the whole scene “an intent to highlight Ju-ae’s military exceptionality” and “dilute skepticism of a female heir.”

Trump and Kim met three times between 2018 and 2020, but talks collapsed without an agreement – and this was followed by a period marked by rising tensions under Biden.

WATCH: North Korea’s Kim Jong Un rides in new tank with daughter pic.twitter.com/Pq78MSNjKt

— Rapid Report (@RapidReport2025) March 20, 2026

North Korea’s freshly conducted the test reportedly utilized fragmentation-style munitions after Iran deployed similar systems against Israel. Missiles carrying cluster or fragmenting warheads can overwhelm and evade advanced air defense systems.

Tyler Durden

Tue, 04/21/2026 – 22:10

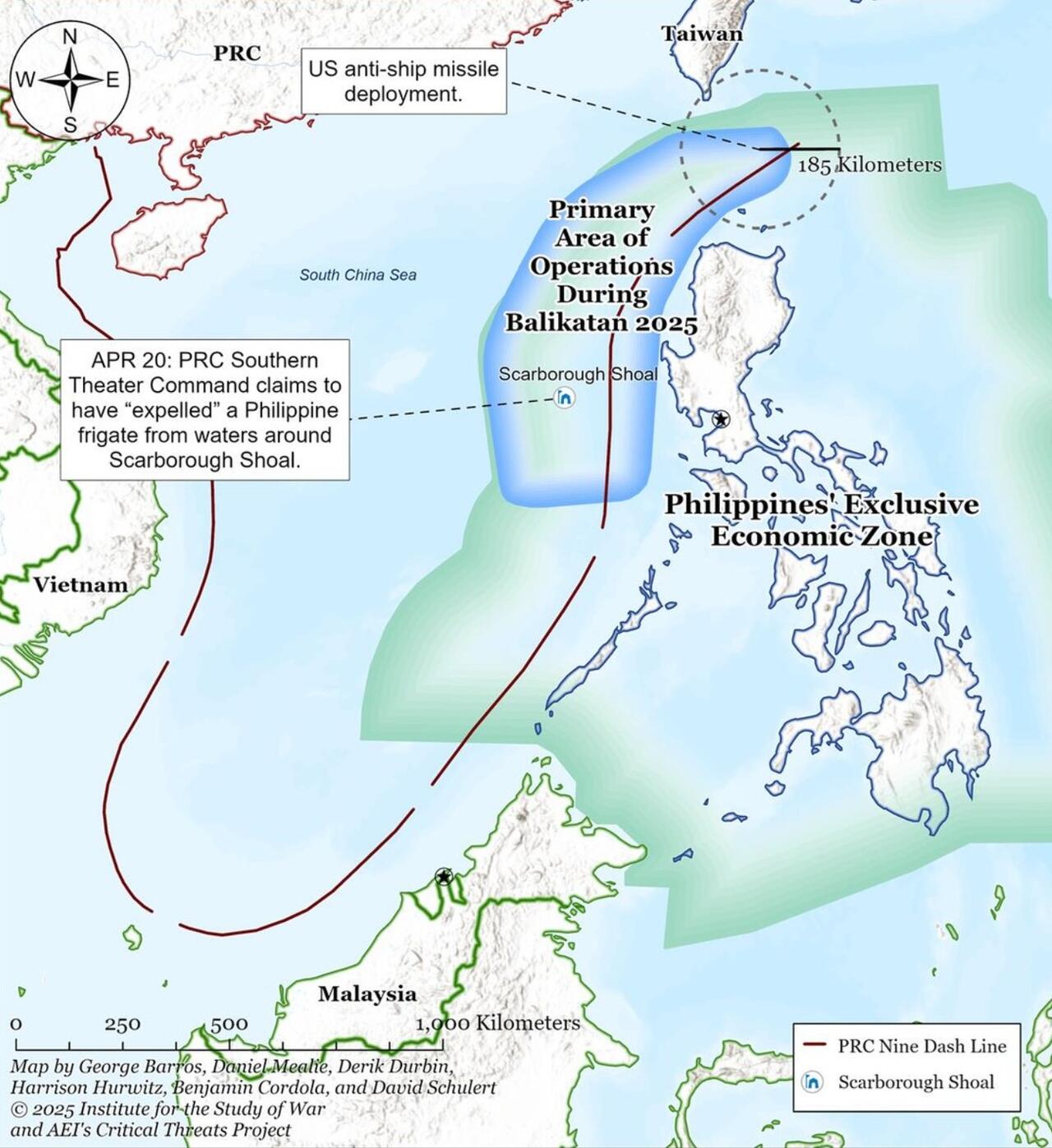

US, Philippines Launch Their ‘Biggest Ever’ Balikatan Drills With Large Japanese Contingent

US, Philippines Launch Their ‘Biggest Ever’ Balikatan Drills With Large Japanese Contingent

Authored by Dave DeCamp via AntiWar.com,

The US and the Philippines on Monday launched what’s being billed as the “biggest ever” Balikatan Exercise, an annual military drill that, for the first time, includes a significant contingent of Japanese troops as Tokyo increases its military activity in the region, ramping up tensions with China.

The drills are scheduled to take place from April 20 to May 8 and will involve more than 17,000 troops, including about 1,400 Japanese military personnel.

Importantly, exercises will include live-fire drills in the northern Philippines, facing Taiwan, and in Palawan, an island province facing the disputed South China Sea.

The start of the drills comes amid a very fragile ceasefire between the US and Iran, which is due to expire on Wednesday if it’s not extended.

While the US has committed more than 60,000 troops to the Middle East, the Trump administration continues to focus on building alliances in the Asia-Pacific as part of its strategy against China, including a new security deal with Indonesia.

In response to the start of the Balikitan drills, the Chinese Foreign Ministry strongly condemned the US activity in the region.

“The world has seen enough damage done by unilateralism and abuse of military might. What the Asia-Pacific needs most is peace and tranquility, and the last thing the region needs is division and confrontation as a result of the introduction of external forces,” said spokesman Guo Jiakun.

The location of the same drills last year, via AEI’s Critical Threats Project

“No military and security cooperation should be conducted at the expense of mutual understanding and trust as well as peace and stability in the region. Such cooperation should not target any third party or harm the interests of any third party. For countries that tie their own security to others, it is important to bear in mind that this may very well backfire,” Guo added.

Tyler Durden

Tue, 04/21/2026 – 21:45

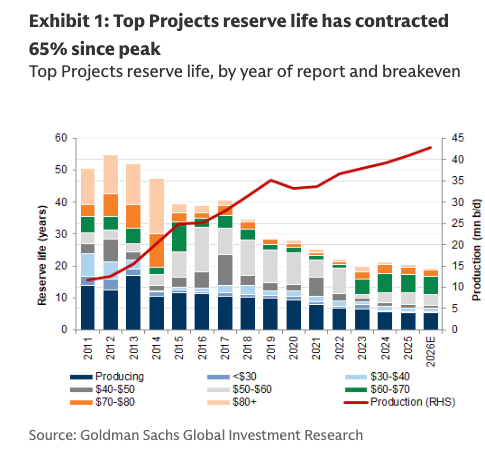

Halliburton Sees First Signs Of Life In America’s Oil Patch: “We Are In Early Innings”

Halliburton Sees First Signs Of Life In America’s Oil Patch: “We Are In Early Innings”

An emerging theme we are focusing on is the early stage of a major capex upcycle in America’s oil patch, with even Goldman now moving in that direction and forecasting a boom that could echo the industry’s expansion cycle of the early 2000s.

Continental Resources CEO Doug Lawler was the first of the major oil patch players to mention in early April that “Continental is increasing our capital budget, which will increase production.”

Now, another giant of the oil patch, Halliburton, a major supplier of the gear, crews, and services that keep drilling and fracking going, reports new signs of life in oilfield activity across North America.

“While these calls are not for committed crews, they do suggest incremental demand is building in spot markets with smaller operators. This is the leading edge of capacity tightening. While we are in the early innings, in my view the setup for North America is constructive. Premium equipment is already tightening,” Halliburton CEO Jeff Miller told investors in the company’s first-quarter earnings statement earlier today.

Halliburton reported strong international performance, especially in Latin America, where revenue jumped 22% year over year, helping to offset disruptions in the Gulf area. The company still beat Bloomberg Consensus expectations on adjusted earnings, though the conflict in the Middle East reduced profit in its drilling and evaluation units by about 2 to 3 cents per share.

Melius Research analyst James West noted that Halliburton “posted a solid beat across the board” that was “driven by international strength that more than offset continued North America softness.”

Miller’s comments about signs of life returning to the oil patch add to remarks made by Continental Resources CEO Doug Lawler earlier this month.

This leaves us asking whether a broader shale response is still to come…

Answering that question is a team of Goldman analysts led by Michele Della Vigna, who now expects “the sector is poised for a major oil capex upcycle, similar to that of the early 2000s.”

We must point out that the oil patch has yet to respond to WTI futures topping $110 a barrel, before sliding to $83 a barrel. WTI tradnig around $89 on Tuesday morning.

Della Vigna outlined, “The escalation of geopolitical tensions in the Middle East since February 28 may have accelerated the timing of a structural capex upcycle, which we now expect to start in 2027.“

She also laid out a list of companies that clients should be long as this emerging theme begins to revive life in the oil patch. Read the report here.

In short, Halliburton has been a leading oilfield services player in North America for decades, and its commentary may be one of the first real signals that the investment cycle is turning up. After a long stretch of under investment, the trend now appears to be shifting back toward renewed capital spending and reserve expansion.

Tyler Durden

Tue, 04/21/2026 – 21:20

US Treasury Sanctions 14 Targets For Helping Iran Obtain Weapons

US Treasury Sanctions 14 Targets For Helping Iran Obtain Weapons

Authored by Joseph Lord via The Epoch Times,

The U.S. Treasury Department on April 21 announced that it is imposing sanctions on 14 targets “for their involvement in helping the Iranian regime obtain weapons,” in contravention of international sanctions.

“As the regime attempts to reconstitute its production capacity, the United States will continue to deplete Iran’s ballistic missile inventories,” the Treasury wrote in a post on X.

According to a press release from the Treasury, the targets include 14 “individuals, entities, and aircraft” based in Iran, Turkey, and the United Arab Emirates, “for their involvement in procuring or transporting weapons or weapons components on behalf of the Iranian regime.”

During the military operations in the region, the United States and Israel have sought to deplete Iran’s weapons reserves, particularly targeting Iranian ballistic missile sites.

Amid these operations, the Treasury said, Iran “is seeking to reconstitute its production capacity.”

The Treasury noted that increasingly, the Persian state is relying on one-way, unmanned drones to target U.S. and allied locations in the Middle East, and indicated that the Treasury would continue to work to prevent Iran from obtaining weapons.

“The Iranian regime must be held accountable for its extortion of global energy markets and indiscriminate targeting of civilians with missiles and drones,” Treasury Secretary Scott Bessent said.

“Under President [Donald] Trump’s leadership, as part of Economic Fury, Treasury will continue to follow the money and target the Iranian regime’s recklessness and those who enable it,” Bessent added.

Currently, the ceasefire between the United States and Iran is holding. On Tuesday, Trump agreed to extend the ceasefire, but tensions with Iran remain high.

“Based on the fact that the Government of Iran is seriously fractured, not unexpectedly so and, upon the request of Field Marshal Asim Munir, and Prime Minister Shehbaz Sharif, of Pakistan, we have been asked to hold our Attack on the Country of Iran until such time as their leaders and representatives can come up with a unified proposal,” Trump wrote in a post on Truth Social.

Simultaneously, Trump said the U.S. military will extend the more-than-week-long naval blockade of Iranian ports, saying that it will, “in all other respects, remain ready and able, and will therefore extend the Ceasefire until such time as their proposal is submitted, and discussions are concluded, one way or the other.”

Meanwhile, the Strait of Hormuz remains closed to commercial traffic.

Iran briefly opened the all-important shipping route on April 17 after the initial ceasefire agreement, but again closed the area to commercial shipping the next day, citing the ongoing U.S. blockade of its ports.

Tyler Durden

Tue, 04/21/2026 – 20:55

https://www.zerohedge.com/geopolitical/us-treasury-sanctions-14-targets-helping-iran-obtain-weapons

Conservative-Targeting SPLC Indicted By Trump DoJ For Fraudulently Funding KKK & Other Extremist Groups

Conservative-Targeting SPLC Indicted By Trump DoJ For Fraudulently Funding KKK & Other Extremist Groups

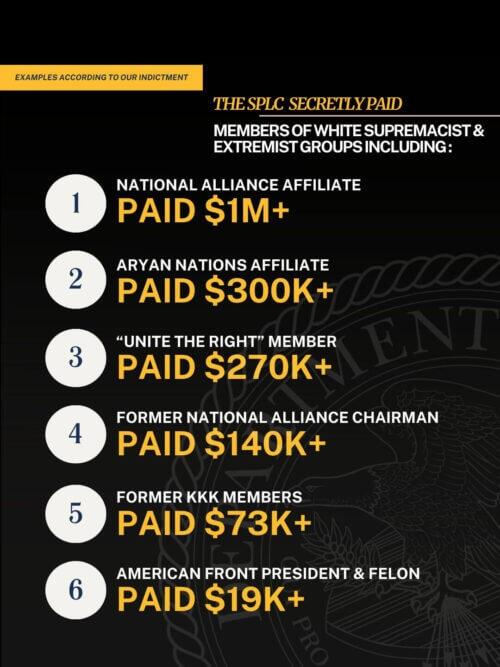

The Southern Poverty Law Center was indicted on federal fraud charges that accused it of illegally raising millions of dollars to pay informants in white supremacist and other extremist groups, acting Attorney General Todd Blanche said.

An Alabama grand jury returned an indictment on April 21 with 11 counts of wire fraud, making false statements, and conspiracy to commit money laundering, according to the Justice Department (DOJ).

Acting Attorney General Todd Blanche said SPLC used paid operatives within extremist circles to incite and intensify racial tensions, arguing the group fostered the very threats it claimed to fight.

“The SPLC is manufacturing racism to justify its existence,” Blanche said in a statement.

“Using donor money to allegedly profit off Klansmen cannot go unchecked. This Department of Justice will hold the SPLC and every other fraudulent organization operating with the same deceptive playbook accountable. No entity is above the law.”

A federal grand jury in the U.S. District Court for the Middle District of Alabama brought 11 charges against the nonprofit, including six counts of wire fraud, four counts of bank fraud, and one count of money laundering.

The indictment covered the years from 2014 through 2023 and alleged that the Southern Poverty Law Center (SPLC) paid at least $3 million to at least eight informants affiliated with the Ku Klux Klan, United Klans of America, the National Socialist Movement, Aryan Nations-affiliated Sadistic Souls Motorcycle Club, the National Socialist Party of America, and the American Front.

In a twist that no one saw coming, one of the SPLC’s paid informants was a member of the leadership group that planned the Unite the Right protest in Charlottesville, Virginia, in 2017 that resulted in one death, according to the DOJ.

“As the indictment lays out, after SPLC paid members of these extremist groups, it created work product that reported on these activities that the members participated in or contributed to,” Blanche explained.

“And to that end, it was doing the exact opposite of what it told its donors it was doing.”

Patel said the SPLC facilitated state and federal crimes by funding these groups.

“The SPLC allegedly engaged in a massive fraud operation to deceive their donors, enrich themselves, and hide their deceptive operations from the public,” Patel stated on X.

“They lied to their donors, vowing to dismantle violent extremist groups, and actually turned around and paid the leaders of these very extremist groups—even utilizing the funds to have these groups facilitate the commission of state and federal crimes.”

“That is illegal—and this is an ongoing investigation against all individuals involved,” Patel added.

The FBI director accused the SPLC of using donors to pay the leaders of extremist groups to stage “hate crimes”

They used the fraudulently raised money by lying to their donor network—thousands of Americans—to go ahead and actually pay the leadership of these supposed violent extremist groups.

Furthermore, our investigation revealed that the Southern Poverty Law Center—on TOP of perpetuating this widespread decade-long multimillion dollar fraud—conducted more criminal activity.

They attempted to HIDE their criminal activity from our financial banking network.

They set up shell companies and entities around America so that the financial institutions that we rely on as everyday Americans were DECEIVED in believing that money was NOT coming from the Southern Poverty Law Center in the perpetration of this scheme and fraud, but rather fictitious entities they stood up to perpetuate this ongoing fraud.

Watch the full press conference below:

But it gets even better worse, during an appearance on FOX News, acting AG Todd Blanche reveals the Biden regime actually closed the investigation into the Southern Poverty Law Center — even though they were paying people to stage “hate crimes”.

As Nick Sortor noted, the Biden regime was directly involved in the coverup!

🚨 WOW! Acting AG Todd Blanche reveals the Biden regime actually CLOSED the investigation into the Southern Poverty Law Center — even though they were PAYING people to stage “HATE CRIMES”

The Biden regime was DIRECTLY INVOLVED in the coverup!

Biden DOJ officials KNEW! pic.twitter.com/k8fDtloCDz

— Nick Sortor (@nicksortor) April 21, 2026

America First Legal broke down some additional ‘easter eggs’ in the whole

/3 The SPLC also received early access to FBI hate-crime data and drafted talking points for Biden’s DOJ. https://t.co/M42eC5vYg2

— America First Legal (@America1stLegal) April 21, 2026

/5 The SPLC was also personally asked by the Assistant Attorney General for the Civil Rights Division at Biden’s DOJ to flag “civil rights matters” for the department. https://t.co/UV7HJrSJKn

— America First Legal (@America1stLegal) April 21, 2026

Simply put, the SPLC’s hypocrisy is now on full display – At the same time that the SPLC wielded unprecedented influence over federal civil rights enforcement, it was also allegedly bankrolling the very extremist groups it purported to seek to destroy.

As Tom Gantert reports for The Epoch Times, the SPLC announced earlier Tuesday that it was the subject of a Justice Department criminal investigation and was facing possible charges related to its use of “paid confidential informants” to infiltrate alleged “extremist” organizations.

Bryan Fair, interim president of the SPLC, said in a video posted on its website before the DOJ news conference that the investigation was “the most serious” of recent acts against it.

“Although we don’t know all the details, the focus appears to be on the SPLC’s prior use of paid, confidential informants to gather credible intelligence on extremely violent groups,” Fair said.

“This use of informants was necessary because we are no stranger to threats of violence.”

Fair said the SPLC no longer works with paid informants but did frequently share the information gained by them with law enforcement. Fair said the informants risked their lives to infiltrate radical groups and the SPLC began working with them during the height of the Civil Rights Movement.

“There is no question that what we learned from informants saved lives,” Fair said.

Rep. Daniel Goldman (D-N.Y.) defended the SPLC on X.

“The DOJ uses paid informants all the time—why is it OK for them but not the SPLC?” Goldman wrote.

He said that the organization “plays a vital role in fighting hatred, yet has been unfairly targeted by [President Donald] Trump and House Republicans since day one.”

“This politicized intimidation needs to stop, now,” he said.

Kyle Shideler, the director for Homeland Security and Counterterrorism at the Center for Security Policy, said the issue is not the use of informants—as long as the informants were not involved in criminal activity, which he presumed the DOJ investigation would determine.

“The issue is that the SPLC always sought to use its supposed expertise on Right Wing Extremists to slander their non-extremist opponents,” Shideler said on X.

“Linking groups like [Turning Point USA] (or my employer) to actual violent actors by putting them all on the same list was the political purpose.”

The Republican National Committee adopted a resolution in 2020 refuting the legitimacy of the SPLC when it came to identifying hate groups.

The resolution said the SPLC “makes a practice of incorrectly labeling persons and organizations as ‘hate groups,’” which mobilizes people to act “in hate and violence” against the people on the SPLC’s list.

The group has vowed to “vigorously defend” itself, its staff, and its work against the allegations.

Tyler Durden

Tue, 04/21/2026 – 20:30

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}