Category: News

Target Cuts Synthetic Colors From Beloved Breakfast Food

Target Cuts Synthetic Colors From Beloved Breakfast Food

Authored by Elizabeth Troutman Mitchell via The Daily Signal,

The Make America Healthy Again movement has made its mark on one of America’s largest retailers.

Dr. Marty Makary, FDA commissioner. (Andrew Harnik/Getty Images)

Target announced Friday that every cereal it sells, including national brands, must exclude synthetic colors by the end of May.

Health and Human Services spokesman Andrew Nixon told The Daily Signal the move will “support healthier options for American families.”

“We’re encouraged to see companies listening to parents and taking voluntary steps to clean up ingredients in the foods they sell,” Nixon said. “Secretary Kennedy has been clear that families deserve transparency and the ability to make informed choices about what they’re feeding their children.”

Target is one of the first national retailers to remove synthetic colors across an entire grocery category. Food companies General Mills and Kraft Heinz have agreed to remove artificial colors from products in the United States by 2027, but Target has instituted a faster timeline.

“It’s great to see Target take the lead on the MAHA front with food dyes,” said Jay Richards, at the Heritage Foundation.

“This is a clear response to market signals from not only federal action but to consumers, who are waking up to the weird stuff in so much of our food. Let’s hope Target’s competitors get the message as well.”

This comes after the Food and Drug Administration came under fire for reportedly retreating from plans to ban artificial food dyes, a key goal of the MAHA movement.

The FDA announced in early February that food companies would be able to label their products as containing “no artificial colors” as long as they don’t use petroleum-based dyes.

FDA Commissioner Dr. Marty Makary pushed back on the report as “amusing fake news.”

“The FDA is moving full steam ahead,” he said.(se

In an interview with The Daily Signal on Dec. 9, Makary said he has seen a “tremendous amount of support in the food industry for our action to call for the removal of all nine petroleum-based food dyes from the U.S. food supply.”

He said he’s saying an awareness about the dangers of food dyes that America has not seen before.

“We again have to listen to parents; we have to listen to the American people,” he said.

“And when they say that they have seen their kids engage in aggressive behavior or attention deficit disorder behavior, they remove all petroleum-based food dyes completely from that food supply and the kids’ behavior improves or changes, and then a year down the road they’re reintroduced to the petroleum-based food dyes and the behavior regresses—those are data points.”

“We’ve got a randomized controlled trial of artificial petroleum-based dyes, and it did not—it was not favorable,” Makary continued.

“It suggested that it’s involved in behavioral disorders in children, specifically ADHD. So we want to create awareness.”

The Daily Signal depends on the support of readers like you. Donate now

Tyler Durden

Mon, 03/02/2026 – 10:30

https://www.zerohedge.com/medical/target-cuts-synthetic-colors-beloved-breakfast-food

Russia’s Key Novorossiysk Export Hub Again Pounded In Large Ukrainian Drone Wave

Russia’s Key Novorossiysk Export Hub Again Pounded In Large Ukrainian Drone Wave

Iran is understandably dominating global headlines, but major events are still happening in oh yeah that other war which has been raging for four plus years in eastern Europe.

Like with the Iran conflict theatre, major geopolitical repercussions impacting energy oil prices are coming out of the Ukraine war. An overnight Monday large-scale drone wave from Ukraine has severely damaged Russia’s Black Sea port of Novorossiysk.

Ukraine’s General Staff has described that the facility supplies Russian forces engaged in the war, after reports have indicated the intended target was the Sheskharis oil terminal, one of southern Russia’s largest oil and petroleum transshipment hubs.

A large fire was observed in the wake of the attack on the key oil export site. But civilian neighborhoods were also damaged in the assault, with debris from intercepted drones reportedly hitting multiple residential structures in the city, resulting in several hospitalizations of residents.

The attack was significant enough to force air travel delays and cancelations over much of southern Russia, including international routes to Istanbul. Routes to Tel Aviv and the Gulf have already been disrupted due to Trump’s ‘Operation Epic Fury’ targeting Iran.

As for this latest drone attack among many targeting Russian oil sites of late, the Security Service of Ukraine (SBU) has owned up to it, saying, “together with other components of the Defense Forces, struck Russian warships, air defense systems, and oil infrastructure in the port of Novorossiysk.”

According to more details via Reuters:

Russia said on Monday that five people had been injured, 20 buildings damaged, and a fire at a fuel terminal extinguished after what it said was a massive overnight Ukrainian drone attack on the Black Sea port city of Novorossiysk.

An official at Ukraine’s SBU security service said Ukrainian drones had struck the Sheskharis oil terminal at the port, hitting six of its seven loading facilities, and that Russian warships had also been hit. Ukraine’s General Staff said a naval base had also been struck, along with an S-400 air defense radar station.

Prior such Ukrainian attacks on Novorossiysk have caused oil prices to briefly spike; however, at the moment Iran war related sentiment and fast-moving events in the Hormuz Strait dominate.

🇷🇺🔥 Overnight, drones struck the oil terminal in Novorossiysk, a major fire is still burning this morning. pic.twitter.com/xP1ziRnScK

— Shaun Pinner (@olddog100ua) March 2, 2026

We’ve featured before of Russia’s largest Black Sea oil export terminal: Novorossiysk handles a major share of Russia’s seaborne crude exports, including Urals and CPC Blend. When it goes offline, millions of barrels per day are at risk.

Tyler Durden

Mon, 03/02/2026 – 10:15

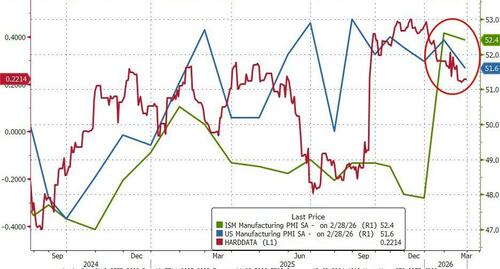

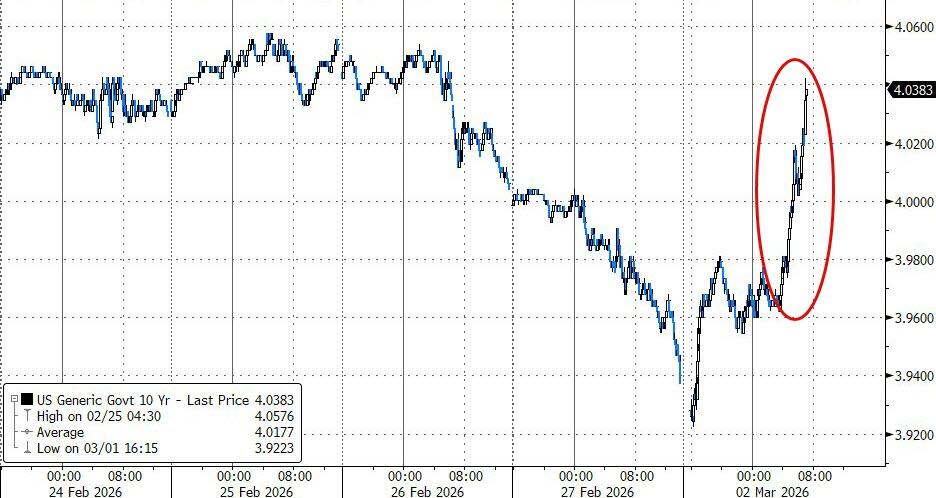

10Y Yield Extends Rise After Surge In ISM Manufacturing Prices

10Y Yield Extends Rise After Surge In ISM Manufacturing Prices

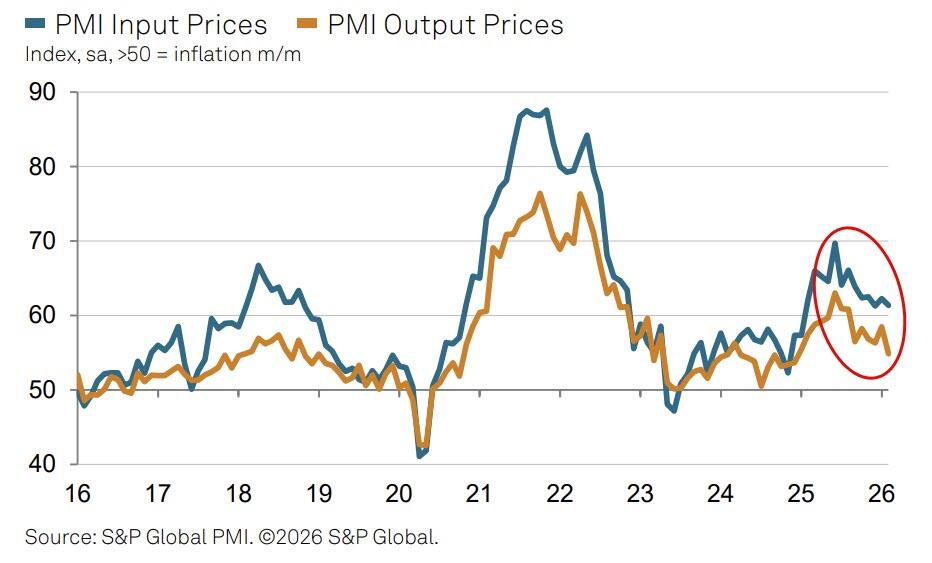

After ISM’s almost unprecedented bounce higher in January, US Manufacturing dipped in February:

S&P Global Manufacturing PMI fell from 52.4 to 51.6 – weakest in seven months

ISM Manufacturing PMI fell from 52.6 to 52.4 (better than expected)

And this is occurring as ‘hard’ data ebbs lower…

“February saw US manufacturers report the weakest expansion since last July, in a further sign that the overall pace of economic growth has moderated in recent months,” according to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

Under the hood we see the usual mixed bag of malarkey in surveys with S&P Global seeing input and output prices declining…

…but ISM seeing Prices explode higher…

ISM saw new orders decline, in line with S&P Global’s view:

“Production growth slowed in response to a near-stalling of orders from customers, with exports falling especially sharply. Factory payroll growth was also barely changed, as concern over order book health caused a growing reticence to add to workforce numbers.”

Rising oil prices – on the back of the military actions over the weekend – had already lifted UST yields early on but the surge in ISM prices (despite decline in S&P Global’s) prompted further pain in bonds…

Businesses were reportedly disrupted by extreme weather, “which has clouded insights into the underlying strength of economic growth and suggests we may see some rebound once the weather clears, and it is encouraging to see manufacturers reporting improved optimism about the outlook.”

However, Williamson notes that uncertainty over the political environment, and the tariff picture in particular, remains a drag on confidence, hiring and investment, which looks likely to persist in the coming months.

Tyler Durden

Mon, 03/02/2026 – 10:07

Iranian Drones Strike EU Country In War First

Iranian Drones Strike EU Country In War First

The Iran war has just for the first time, and rather quickly given it’s only the third day of the conflict, expanded to include an EU nation in the Mediterranean. Iranian-made drones have reached Cyprus and at least one has made ground impact. But they may have been launched from nearby Lebanon.

The British Royal Air Force (RAF) base in Akrotiri, Cyprus came under attack Monday morning, with an Iranian drone striking the runway in the early hours, several reports say. This comes as Britain has mulled directly joining Trump’s Iran operation, but now appears to be pulling back from the prospect.

General view of RAF Akrotiri in Cyprus, via PA/The Independent

“Our force protection in the region is at the highest level and the base has responded to defend our people,” a British Ministry of Defence spokesperson has told international media.

Hours after the initial salvo, two more unmanned aerial vehicles were successfully intercepted while inbound over the same base. “Our armed forces are responding to a suspected drone strike at RAF Akrotiri in Cyprus at midnight local time,” the MoD statement continued. “Our force protection in the region is at the highest level and the base has responded to defend our people.”

The RAF is now taking emergency precaution measures is at least partially evacuating the base after a prior build-up:

The attacks on Akrotiri, a British sovereign base area, comes after the RAF recently moved additional defensive capabilities to the location—including radar systems, anti-drone defenses, and F-35 jets—as part of ongoing efforts to support stability in the Middle East.

Showcasing the widening impact of the Iran conflict, an airport in Paphos, Cyprus, was later evacuated after a suspect object was picked up on radars.

Cooper spoke of the “international” threat Monday morning and expressed the importance of recognizing “the responsibilities we have around defensive support for areas where there are British citizens.”

Cooper further said that in private conversations with officials throughout the Gulf region, the leaders expressed they were “frankly shocked and horrified at the way their countries have been targeted by Iran over the weekend.”

Family members of UK military members have been ordered to leave the base as it is now clearly being targeted:

Family members of British military personnel have been asked leave to leave the base for their own safety, and will be based elsewhere in Cyprus until the alert passes.

The drone struck hours after the UK agreed to let the US use British military bases to attack Iranian missile sites, but officials indicate the possible flight times mean it was launched before the prime minister announced the new policy.

Cyprus President Nikos Christodoulides has stated that “All the competent services of the republic are on alert and in full operational readiness.” He also clarified his country has nothing to do with the war.

🇮🇷🚀🇬🇧🇨🇾 BREAKING: Cypriot media has confirmed that an Iranian drone has damaged one of the runways at the UK Akrotiri airbase in Cyprus almost 1000km from Iran itself💥 pic.twitter.com/mTwsZAIhQk

— World War Now (@WorldWarNow_) March 1, 2026

“I want to be clear: Our country does not participate in any way and does not intend to be part of any military operation,” the Cyprus president added.

There’s growing concern that the drones could have been sent from Iran’s proxy arm in Lebanon: Hezbollah. Israel has just renewed its bombing of Beirut and other parts of Lebanon after the Shia paramilitary group (or possibly another group) fired rockets on northern Israel.

Lebanon is only a short, hours-long boat ride away from Cyprus. Israel is also not very distant. The British military has two sovereign military bases which it has maintained on Cyprus since the independence of its former colony in 1960.

Tyler Durden

Mon, 03/02/2026 – 10:00

https://www.zerohedge.com/geopolitical/iranian-drones-strike-eu-country-first-war

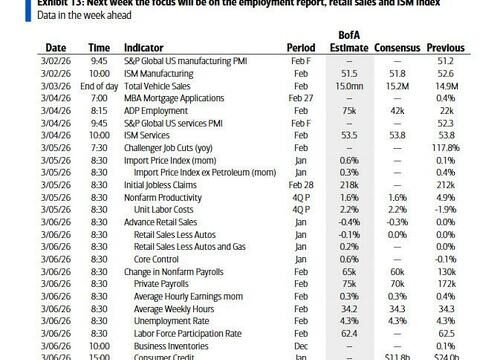

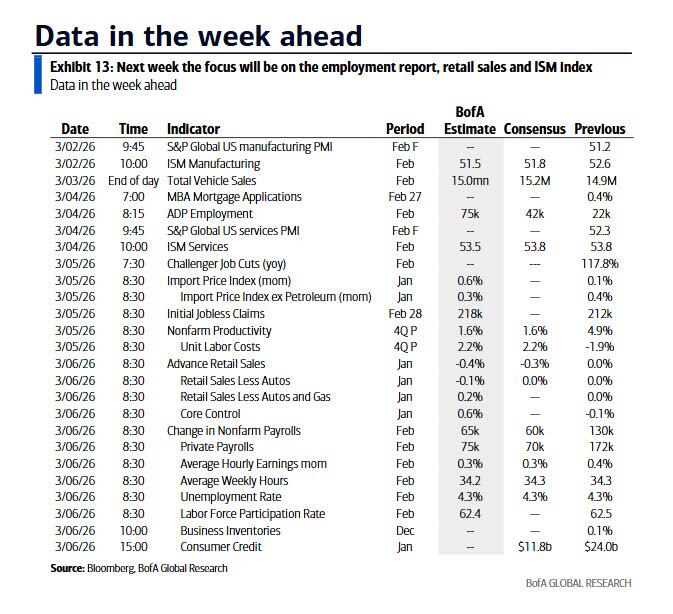

Key Events This Week: Payrolls, Retail Sales, ISM, Beige Book… And War In Iran

Key Events This Week: Payrolls, Retail Sales, ISM, Beige Book… And War In Iran

Outside the obvious and huge attention on the Middle East, the key focus this week will be on the US jobs report on Friday, retail sales on the same day, the ISM indices (today and Wednesday), and the Fed’s Beige Book, also due on Wednesday. European releases will include inflation data tomorrow and the ECB’s accounts of their February meeting on Thursday. Various global PMIs are also out this week.

In politics, highlights include the Two Sessions in China as well as the Spring Statement in the UK. Earnings reports will be due from Costco and Broadcom.

Delving deeper into the US data, the most important release in the week ahead is Friday’s February employment report. DB economists forecast headline payroll growth of 30k, down from 130k previously, with private payrolls rising by 50k after January’s unusually strong 172k gain. The moderation largely reflects payback from outsized hiring last month in private education and health services and construction, where job gains more than doubled their six month averages. Elsewhere in the establishment survey, economists expect average hourly earnings to rise 0.4% month over month, unchanged from January, while the average workweek remains steady at 34.3 hours.

The household survey adds an additional layer of uncertainty this month, as the BLS implements its delayed annual population controls. DB’s economists forecast the unemployment rate at 4.3%, though risks around this estimate are elevated in both directions. January data will also be revised using the new controls, and attention will be focused on whether these adjustments meaningfully alter unemployment rates across demographic groups, particularly among younger cohorts, where concerns around entry level hiring remain heightened.

Friday also brings January retail sales, where weather related weakness in auto sales is likely to weigh on the headline figure. DB economists expect headline sales to decline 0.6%, with sales excluding autos down 0.1%, partly reflecting lower gasoline prices. That said, retail control sales are forecast to rebound by 0.3%, pointing to a firmer underlying pace of goods consumption. Tax refunds should provide additional support to spending in coming months, with the average refund running meaningfully higher than a year ago.

Ahead of Friday, several other releases will help set the tone. Today’s manufacturing ISM is expected to edge up to 53.3 from 52.6. Wednesday brings the ADP employment report, forecast at 50k (though seasonals might push it higher), alongside the non manufacturing ISM, seen at 54.0.

Other notable data include February unit motor vehicle sales tomorrow, which is expected at 15.1 million, potentially restrained again by adverse weather. Thursday’s preliminary Q4 productivity and unit labor cost figures are forecast at 1.3% and 2.2%, respectively.

Moving to Europe, the focus will continue to be on inflation, with February prints due for the Eurozone and Italy tomorrow, Switzerland on Wednesday, and Sweden on Thursday. ECB speakers will include President Lagarde today, and the central bank will release the accounts of its February meeting on Thursday.

In the UK, attention will be on the Spring Statement delivered by the Chancellor tomorrow, and our UK economist previews it here. There will also be the February DMP survey from the BoE on Thursday.

Over in Asia, the spotlight will be on China’s annual Two Sessions starting Wednesday (running through March 11), followed by the National People’s Congress session opening on Thursday, with the 15th Five Year Plan expected. Elsewhere, data highlights will include the February PMIs, both the official and private gauges, in China on Wednesday.

In Japan, the Shunto wage demands due on Thursday are the most anticipated event next week and expects wage demands this year to come in at 6.0%. There will also be the Financial Statements Statistics of Corporations (MoF survey) for Q4 on Tuesday, as well as the February consumer sentiment index on Wednesday.

Earnings will include tech firms Broadcom, CrowdStrike and Marvell. US consumer firms will continue to be in focus, with reports from Costco and Target.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 2

Data: US February ISM manufacturing, UK January net consumer credit, M4, Germany January retail sales, Italy February manufacturing PMI, new car registrations, Canada February manufacturing PMI

Central banks: ECB’s Lagarde, Nagel and Stournaras speak, BoJ’s Himino speaks, BoE’s Taylor speaks, BoC’s Kozicki speaks

Earnings: AST SpaceMobile, EchoStar, Venture Global, Norwegian Cruise Line

Tuesday March 3

Data: US February total vehicle sales, Japan January jobless rate, job-to-applicant ratio, February monetary base, Q4 Ministry of Finance survey, France January budget balance, Eurozone February CPI, Italy February CPI

Central banks: Fed’s Williams and Kashkari speak, ECB’s Kocher and Sleijpen speak

Earnings: Crowdstrike, Thales, AutoZone, Target, ASM, Kuehne + Nagel, On Holding, Gitlab

Other: UK Spring Statement

Wednesday March 4

Data: US February ISM services, ADP report, UK February official reserves changes, China February PMIs, Japan February consumer confidence index, Italy February services PMI, January unemployment rate, Eurozone January PPI, unemployment rate, Canada Q4 labor productivity, February services PMI, Switzerland February CPI, Australia Q4 GDP

Central banks: Fed’s Beige Book, ECB’s Muller, Cipollone, Villeroy and Guindos speak, BoC’s Macklem speaks

Earnings: Broadcom, Bayer, adidas, Veeva, Okta, Davide Campari-Milano

Other: China’s Two Sessions start

Thursday March 5

Data: US January import price index, export price index, Q4 nonfarm productivity, Q4 unit labor costs, initial jobless claims, UK February new car registrations, construction PMI, Germany February construction PMI, France January industrial production, Italy January retail sales, Eurozone January retail sales, Sweden February CPI

Central banks: ECB’s accounts of the February meeting, ECB’s Lagarde, Guindos, Rehn and Nagel speak, BoE’s February DMP survey

Earnings: Costco, Petroleo Brasileiro, Marvell, Deutsche Post, Reckitt Benckiser, Ciena, Galderma, Kroger, Universal Music Group

Other: China’s NPC’s session starts

Friday March 6

Data: US February jobs report, US Retail Sales, January consumer credit, Germany January factory orders

Central banks: Fed’s Hammack speaks, ECB’s Cipollone and Schnabel speak

* * * * *

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the retail sales report and the employment report on Friday. There are several speaking engagements by Fed officials this week, including an event with New York Fed President Williams on Tuesday.

Monday, March 2

09:45 AM S&P Global US manufacturing PMI, February final (consensus 51.4, last 51.2)

10:00 AM ISM manufacturing index, February (GS 51.0, consensus 51.5, last 52.6): We estimate that the ISM manufacturing index declined by 1.6pt to 51.0 in February, reflecting reversion after an outsized increase in the prior month. Our manufacturing survey tracker edged up by 0.1pt to 52.4.

Tuesday, March 3

09:55 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will give keynote remarks at America’s Credit Union Government Affairs conference in Washington DC. Speech text and Q&A are expected.

11:55 AM Minneapolis Fed President Kashkari (FOMC non-voter) speaks: Minneapolis Fed President, Neel Kashkari, will participate in a conversation with Mike McKee at the Bloomberg Invest conference in New York City. Q&A is expected. On January 5, Kashkari said, “My guess is we are pretty close to neutral right now.” He added that “we just need to get more data to see [whether inflation or the labor market] is the bigger force, [and] then we can move from a neutral stance to whatever direction is necessary.”

05:00 PM Lightweight motor vehicle sales, February (GS 15.6mn, consensus 15.4mn, last 14.9mn)

Wednesday, March 4

08:15 AM ADP employment change, February (GS +50k, consensus +50k, last +22k)

09:45 AM S&P Global US services PMI, February final (consensus 52.3, last 52.3)

10:00 AM ISM services index, February (GS 53.5, consensus 53.5, last 53.8): We estimate that the ISM services index edged down by 0.3pt to 53.5 in February, reflecting a decline in our non-manufacturing survey tracker (-1.3pt to 52.0) but a tailwind from potential residual seasonality.

02:00 PM Fed Releases Beige Book, March meeting period: The Fed’s Beige Book is a summary of regional economic anecdotes from the 12 Federal Reserve districts. The Beige Book for the January FOMC meeting period noted that overall economic activity increased at a slight to modest pace in eight of the twelve Federal Reserve Districts, with three Districts reporting no change and one reporting a modest decline, marking an improvement over the last three reports. In this month’s Beige Book, we will look for anecdotes related to the evolution of labor demand and firms’ expectations of activity growth for the remainder of the year.

Thursday, March 5

08:30 AM Import price index, January (consensus +0.3%, last +0.1%)

08:30 AM Nonfarm productivity, Q4 preliminary (GS +2.2%, consensus +1.8%, last +4.9%): Unit labor costs, Q4 preliminary (GS +2.4%, consensus +2.0%, last -1.9%)

08:30 AM Initial jobless claims, week ended February 28 (GS 215k, consensus 215k, last 212k): Continuing jobless claims, week ended February 21 (consensus 1,845k, last 1,833k)

Friday, March 6

08:30 AM Nonfarm payroll employment, February (GS +45k, consensus +60k, last +130k); Private payroll employment, February (GS +45k, consensus +70k, last +172k); Average hourly earnings (MoM), February (GS +0.3%, consensus +0.3%, last +0.4%); Unemployment rate, February (GS 4.4%, consensus 4.3%, last 4.3%): We estimate nonfarm payrolls increased 45k in February. On the negative side, we expect a 31k drag from newly striking workers and a modest headwind from poor winter weather after it likely boosted January payroll growth. Additionally, we expect unchanged government payrolls—reflecting a 5k decline in federal government payrolls that is offset by a 5k increase in state and local government payrolls. The big data indicators of job growth we track were mixed in February. On the positive side, the pace of layoffs remained subdued and online measures of job openings stabilized. We estimate that the unemployment rate edged up to 4.4% in February. While other measures of labor market tightness improved slightly on net, the February unemployment rate appears to suffer from positive residual seasonality (the unrounded unemployment rate has increased in each of the last three Februarys by an average of 0.15pp). The report will be accompanied by updated population controls, which are likely to lead to downward revisions to the level of the population, labor force, and household employment. The impact on ratios in the survey (e.g., the unemployment rate and labor force participation rate) is likely to be negligible. We estimate average hourly earnings rose 0.3% month-over-month in February, reflecting neutral calendar effects.

08:30 AM Retail sales, January (GS -0.1%, consensus -0.3%, last flat); Retail sales ex-auto, January (GS +0.1%, consensus flat, last flat); Retail sales ex-auto & gas, January (GS +0.3%, consensus +0.2%, last flat); Core retail sales, January (GS +0.5%, consensus +0.3%, last -0.1%): We estimate core retail sales increased 0.5% in January (ex-autos, gasoline, and building materials; month-over-month SA), reflecting solid alternative data and a tailwind from potential residual seasonality. We estimate headline retail sales declined 0.1%, reflecting a decline in auto sales and lower gasoline prices.

10:15 AM San Francisco Fed President Daly (FOMC non-voter) and Philadelphia Fed President Paulson (FOMC voter) speak: San Francisco Fed President Mary Daly and Philadelphia Fed President Anna Paulson will discuss private sector data at the US Monetary Policy Forum held by the University of Chicago Booth School of Business in New York City. Text and Q&A are expected. On February 17, Daly said, “The Fed has roughly 75bps to go until getting to neutral…the policy stance now is modestly or slightly restrictive.”

01:30 PM Cleveland Fed President Hammack (FOMC voter) speaks: Cleveland Fed President Beth Hammack will participate in a panel discussion on the dollar’s safe-haven status at the US Monetary Policy Forum in New York City. Text and Q&A are expected. On February 10, Hammack said, “Rather than trying to fine-tune the fed funds rate, I’d prefer to err on the side of patience as we assess the impact of recent rate reductions and monitor how the economy performs.” She also noted, “Based on my forecast, we could be on hold for quite some time.”

Soruce: DB, Goldman

Tyler Durden

Mon, 03/02/2026 – 09:53

https://www.zerohedge.com/markets/key-events-week-payrolls-retail-sales-ism-beige-book-and-war-iran

Migrants Filmed Catching And Butchering Swans, Ducks In UK And Ireland

Migrants Filmed Catching And Butchering Swans, Ducks In UK And Ireland

Authored by Steve Watson via Modernity.news,

Shocking videos reveal migrants setting traps and snatching protected birds from public waterways, fueling outrage over unchecked immigration destroying local wildlife.

Video evidence from Ireland shows a local resident dismantling crude wire cages placed along Dublin’s Grand Canal by tent-dwelling migrants, believed to be targeting swans and ducks for consumption.

The footage captures the man, accompanied by his dog, uprooting the traps hidden in the grass near the water’s edge.

Ever wonder why swans and ducks are disappearing from our rivers, canals and ponds in Ireland? Fair play to this man (and his dog), who paid a visit to the Grand Canal to dismantle cage traps set up by male migrants in tents. pic.twitter.com/aiV2PjyX44

— Susanne Delaney (@SuzieD755164) February 27, 2026

In the clip, no direct dialogue is heard, but the intent is clear as the resident methodically removes the snares, preventing what could have been a slaughter of iconic birds.

This incident echoes similar scenes across the UK. One video documents an RSPCA officer confronting a migrant family suspected of poaching and cooking a large white bird, possibly a swan.

?NEWS: MIGRANTS EATING SWANS WILL NOT BE CHARGED

– They have been warned not to do it again by the RSPCA

Swans are a protected species

These people don’t care

We need mass deportations pic.twitter.com/eWeX2O7lKS

— Basil the Great (@BasilTheGreat) June 12, 2025

“I’m going to get someone to check what bird this is. I think it might be a swan, but do you know the big white birds that you see on the park?” the officer questions.

She inspects the pot: “You can see bones in this bird because he isn’t chicken so I am concerned. There are laws against people taking animals… It’s very serious. It’s very serious if that happens.”

Examining the bin, she notes: “You see problem is there are lot of big white feathers here.”

The family claims the birds were bought and released during a children’s chase game, but the officer warns: “What I need to make sure is everybody here knows that they’re not allowed to take anything from the park. I’m not saying you did.”

Another clip shows a family carrying a wild bird they have clearly taken and are intending to eat.

— Sandra White (@SandraW42990) September 25, 2025

Another clip shows a migrant grabbing a swan in a park.

This has to be false. The mainstream media told us migrants were not eating the swans! pic.twitter.com/QXyb2kJrdq

— Ian Miles Cheong (@ianmiles) October 27, 2025

Another post asks “What is this migrant doing?” as a man hauls a struggling swan over a railing.

The migrants are eating the swans pic.twitter.com/LHF08sCEI7

— karma (@karma44921039) September 26, 2025

Similar footage captures a man on a bridge snatching a swan from the water below, swinging it by the neck before walking away.

So cool that there is a large amount of video and photographic evidence showing Middle Eastern migrants stealing swans from public parks in the UK and the political-media class establishment just treat you like you’re an idiot if you talk about it

We’re still at the “it’s not… https://t.co/1pLMzwIiLL pic.twitter.com/fzv0Ig3JMV

— Drew Pavlou ???????? (@DrewPavlou) September 27, 2025

These videos and many more like them have sparked furious reactions online.

Fuck me is there anything these cunts won’t steal/kill

— BigStar (@BigStarDub) February 27, 2026

Everything that isn’t nailed down is fair game to these grifting free loaders.

— Erin’s Bestie (@SarahConnorIE) February 27, 2026

fucking bastards. Such a betrayal of these animals that don’t really see us as a threat.

— Kenny (@kenny_Irl) February 27, 2026

Yep me and some angling friends have noticed pike numbers way down. They are also being eaten. ?

— Bríain Ó Éire (@Eirinn76) February 27, 2026

Is nothing safe from the savages ? ??

— Alexa (@Alexa69484823) February 27, 2026

Dear Lord these people are really sick,life in the UK is just getting so hard ,these people are not like us they have no heart void of any feelings ?

— Ann Spence (@Annspence108Ann) February 27, 2026

The cases parallel the chaos in Springfield, Ohio, where Haitian migrants have been accused of decapitating and eating ducks in parks.

A resident testified at a city commission meeting: “They’re in the park grabbing up ducks by their neck and cutting their head off and walking off with ’em and eating them.”

He questioned officials: “Who is getting paid? Like how much money is y’all really getting paid? Like to bring them over here, like I know it’s deeper than them.”

NEW: Springfield, Ohio man says Haitian illegals are decap*tating ducks from parks & eating them, accuses commission members of getting paid off for allowing it.

“They’re in the park grabbing up ducks by their neck and cutting their head off and walking off with ’em and eating… pic.twitter.com/uE3wI3CXl3

— Collin Rugg (@CollinRugg) September 8, 2024

As we previously reported, Springfield’s city manager admitted hearing such reports, despite later denials amid media “fact checks” dismissing the issue as misinformation.

This pattern exposes the failures of open-border policies, importing incompatible cultural practices that harm protected wildlife and erode community safety. From Ohio’s overwhelmed streets to Britain’s depleted parks, the toll of mass migration mounts.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Mon, 03/02/2026 – 09:15

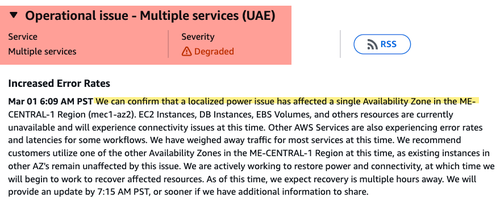

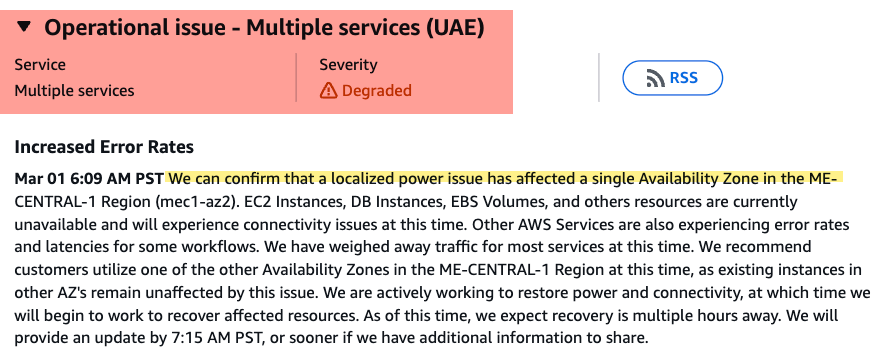

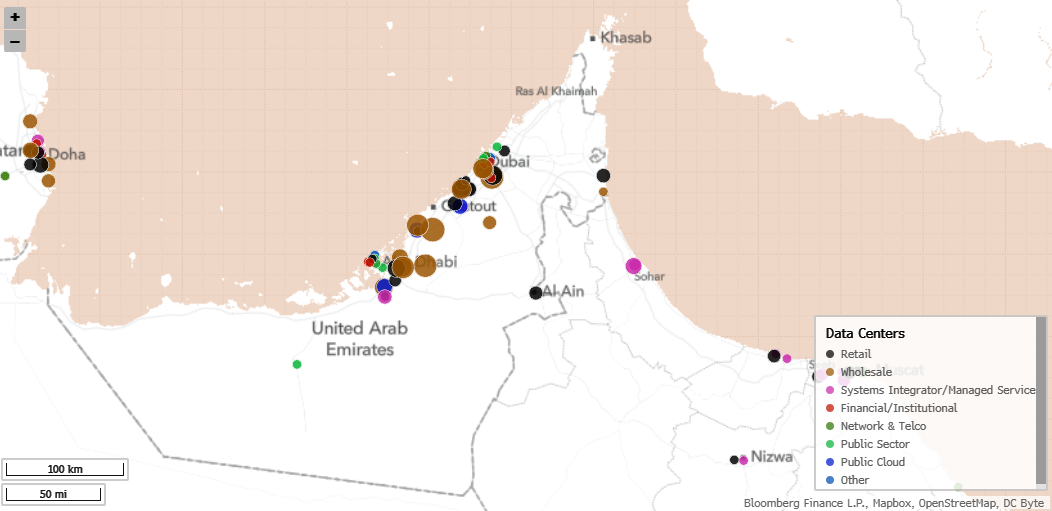

Modern Warfare Sees First Drone Strike On A Commercial Data Center

Modern Warfare Sees First Drone Strike On A Commercial Data Center

We told readers one month ago that, while trillions of dollars are being allocated to the global data center buildout, virtually every Wall Street analyst remains fixated on financing, chip stacks, power, land, water, and other obvious mainstream inputs. However, we identified one overlooked emerging threat they missed: the risk of kamikaze drone attacks.

By Sunday morning, that risk was realized, as our note pointed out that Amazon’s cloud unit, AWS, experienced degraded service in the United Arab Emirates due to a “localized power issue.”

Now, a Reuters report provides more color on what exactly happened after an AWS data center in the UAE had to shut down operations, in what appears to be the first known instance of a commercial data center being physically targeted in a conflict.

Reuters reports that an object struck an AWS data center in the UAE, causing a fire and shutting it down. Assuming this was an Iranian drone strike, it is the first time a commercial data center was physically targeted in a conflict. It won’t be the last.https://t.co/4b7DHklwoU

— Chris McGuire (@ChrisRMcGuire) March 1, 2026

UAE Data Center Map

The first commercial data center to be damaged on the modern battlefield is certainly not going to be the last, as the Ukraine war has created a period of rapid weapon development over the last four years, as well as in other conflict areas around the world, with the proliferation of FPVs and cheap drones with warheads and AI kill chains.

This threat was outlined in our note titled “Explosion In AI Data Center Buildouts Will Demand Next-Gen Counter-Drone Security,” as we recognized that the rapid development in this war technology has effectively accelerated war tech from the 2030s to today (read here). There were absolutely no Wall Street analysts we read on a daily basis discussing this emerging drone threat to data centers as the great buildout unfolded. Analysts were too busy talking about power and AI chips.

But guess who was talking about the data center threat about a year ago? Well… former Google CEO Eric Schmidt (read here). Schmidt was in Ukraine in January (read here).

Tyler Durden

Mon, 03/02/2026 – 08:55

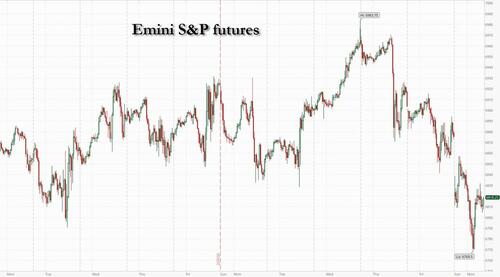

Futures Tumble As Iran War Sends Oil, Gold And Dollar Sharply Higher

Futures Tumble As Iran War Sends Oil, Gold And Dollar Sharply Higher

US equity futures and global stocks tumbled, the dollar and gold rallied and oil soared as military strikes intensified across the Middle East, sending oil to its biggest surge in four years and stoking concern that faster inflation could weigh on the global economy. AS of 8:10am ET, S&P 500 futures are down more than 1% – but off overnight lows – after the cash index fell nearly 1% over the previous two trading days; Nasdaq futures tumbled 1.5% with all Mag 7 stocks lower by more than 1% in premarket trading; Aerospace/Defense, Energy, and Gold Miners are the safety havens in equities and all are bid pre-mkt; PLTR +4% may help +Software/-Semis. In the latest war news, AMZN data centers were hit in Bahrain/UAE, as was a UK base in Cyprus; with Israel attacking Lebanon; both Israeli and Saudi indices opened higher before reversing lower due to escalation. After soaring 13% at the open, crude oil traded down to +4% and was now +7.5% after Saudi Aramco halted operations at its Ras Tanura refinery after a drone strike in the area. Bond yields are notably higher, rising +4-5bps with the USD bid against all major FX and DXY +57bp which would be its best day since Feb 2. Energy is unsurprisingly leading commodities higher with double-digit gains in gasoil, heating oil, and EU natgas. Gold, which is now at $5400, is leading silver ($94/oz) with platinum flat.

In premarket trading, energy and defense stocks rallied, with Exxon Mobil shares climbing 5.2% in early trading. British Airways owner IAG SA fell 5.4% amid a widespread disruption to flights in the Middle East. Mag 7 stocks all fall (Microsoft -0.8%, Apple -1%, Nvidia -1.3%, Meta -1.7%, Amazon -2.4%, Alphabet -2.6%, Tesla -2.1%)

The Iran conflict is pushing shares of airlines and cruise operators lower, while energy stocks jump. Movers include American Airlines (AAL) -6% and Exxon (XOM) +4%.

US banks and financials are pointing lower as risk off sentiment extends with military strikes intensifying across the Middle East. JPMorgan Chase (JPM) -2%, Wells Fargo (WFC) -1.7%.

AES Corp. (AES) falls 16% after a consortium led by Global Infrastructure Partners and EQT agreed to buy the electric utility.

Berkshire Hathaway (BRK/B) slips 1% after the conglomerate’s operating profits fell nearly 30% in Warren Buffett’s last quarter as CEO. Analysts note weakness in the company’s insurance businesses.

EchoStar (SATS) declines 2% after the parent of Dish Network posted a net loss in the fourth quarter.

Paramount Skydance (PSKY) rises 5% after Warner Bros. Discovery filed a join-statement following the market close on Friday announcing that they had entered into a definitive merger agreement.

UniQure (QURE) tumbles 41% after US regulators said the company should conduct a pivotal study before getting approval of its gene therapy for Huntington’s disease, another example of the Trump administration slowing a treatment for a rare disease drug.

While markets are recoiling from the latest war in the Middle East, the strikes on Iran were heavily telegraphed and traders had built up meaningful hedging. Still, the conflict may be longer and wider than some expected. Trump said the bombing campaign against Iran will continue, perhaps for weeks. Iran fired missiles on Israel, US military bases and Persian Gulf countries including the financial hub of Dubai (there is a full summary of all the latest war news in the section below).

The war in Iran is adding to a list of headwinds for markets already on edge after fears over disruption from artificial intelligence and pressure in private credit have nearly erased this year’s gains in the S&P 500. Investors are now focused on how long the conflict will last and how far hostilities might spread, after President Donald Trump said the campaign could continue for weeks.

“The endgame remains highly uncertain, ranging from a relatively swift political exit to a broader regional spillover,” said Mathieu Racheter, head of equity strategy at Julius Baer. “In such a fog of war, markets tend to trade probabilities rather than shifting facts.”

The dollar strengthened as a spike in oil prices spurred traders to dial back bets on Fed rate cuts this year, with Bloomberg economists writing that changes to Fed policy are far from guaranteed, despite the war. The team’s risk scenario is for oil to raise to $108 a barrel, while a more temporary spike would keep the Fed on alert, but not trigger a shift in policy.

Meanwhile, Aramco halted operations at Saudi Arabia’s largest refinery after a drone strike in the area, Bloomberg reported. QatarEnergy’s decision to cease LNG production followed attacks on its Ras Laffan complex, sending European gas prices soaring.

“It is still very unclear what the duration of the conflict will be and more importantly, how the energy market reacts,” said Andrea Gabellone, head of global equities at KBC Securities. “One positive for the US is that the market has corrected since January, so we are not in overbought territory. It’s fair to say havens should continue to outperform.”

Strategists are coalescing around the view that a buying opportunity for US stocks may emerge. JPMorgan’s Mislav Matejka said the weekend’s events will naturally lead to risk-off in the short term, but investors with a 3/6/12-month time frame should use weakness to increase exposure. Morgan Stanley’s Mike Wilson agrees that the bullish view is intact for now, with a lasting spike in oil above $100 needed to impact the US equity outlook.

Still, geopolitical events underscore the need to diversify and hedge portfolios at a much faster pace over the next few months, according to today’s Taking Stock column. The impact on the stock market will be determined by its duration, Citigroup strategists said, as they presume a shorter-term impact.

Prashant Bhayani, chief investment officer for Asia at BNP Paribas Wealth Management, said the main questions traders are looking out for are how long the disruption lasts, developments in the Strait of Hormuz, any impact on oil infrastructure and whether Iran and the US can reach a negotiated settlement. “Most geopolitical events have limited long-term impact on asset markets,” Bhayani said. “There is already a premium in oil of circa $7-$10 before today’s trading. Only in an extended conflict, with oil prices over $100, would it materially impact the global economy.”

On the economic front, payrolls come back into focus later this week with the survey forecasting a more modest pace of hiring in February relative to the start of the year. January retail sales data is also due Friday, while the Fed’s Beige Book is released on Wednesday.

The Stoxx 600 has pared its fall, to 1.4%, although remains on course for its worst daily performance since November after conflict in the Middle East escalated over the weekend. Energy is the only sector in the green, while retail, travel and consumer product stocks fall the most. Here are some of the biggest movers on Monday:

Shipping and logistics stocks are among the few gainers in European trading on Monday as conflict in the Middle East disrupts the Strait of Hormuz and Red Sea shipping routes.

Energy stocks rise on back of an oil-price surge triggered by US and Israeli strikes against Iran. Morgan Stanley upgraded the sector to overweight, while JPMorgan upped its price targets on a slew of companies.

Galp Energia shares rise as much as 9.6%, hitting their highest level since mid-2024, as rising Middle East tensions cause oil prices to surge.

European defense stocks jump, with BAE Systems among those hitting record highs, as conflict in the Middle East spurs expectations of elevated security spending.

Novo Nordisk shares fall as much as 5.7% and were downgraded to neutral from buy at Goldman Sachs after data last week showed its next-generation obesity drug CagriSema delivered less weight loss than Eli Lilly’s rival blockbuster.

European banks fall as war between the US and Iran triggered a broad-based selloff.

European airlines stocks slump as conflict in the Middle East causes major disruptions at some of the world’s busiest airports. Analysts flag higher fuel costs and air space closures as factors likely to disrupt the sector.

Informa shares sink as much as 11%, the biggest intraday drop since the Covid outbreak of 2020, as the events firm got swept up in the selloff of stocks exposed to the conflict in the Middle East.

Oxford Nanopore shares drop as much as 18% after the British DNA-sequencing company cut its medium-term growth guidance, which analysts say will spark consensus downgrades.

Luxury stocks fall as the escalating conflict in the Middle East creates a “highly uncertain backdrop” for the sector, according to Vontobel.

Earlier in the session, Asian stocks dropped for the first time in six days as the US-Israeli war against Iran prompted investors to reduce exposure to risk assets. The MSCI Asia Pacific Index slid as much as 1.8%, the most in a month, with financials and health-care the worst-performing sectors. A subgauge of energy shares climbed nearly 1% as oil rallied. Pakistani shares plunged the most on record after geopolitical tensions in the Middle East escalated, while benchmarks in Thailand, the Philippines and Hong Kong were leading declines in the region. Markets in South Korea were shut for a holiday. For Asian assets, the main risk from a prolonged Middle East conflict lies in a stronger dollar and higher oil prices, given that most economies in the region are net energy importers. A gauge of the greenback advanced on Monday and oil prices spiked before paring gains following a report that indicated at least one top official in Tehran sought to resume nuclear talks with the US. Japan’s Topix also dropped nearly 3% before paring declines, with bank stocks among the biggest losers.

The Hang Seng China Enterprises Index slumped 1.8% to enter a technical correction. A gauge of Chinese tech shares listed in the financial hub — which entered a bear market last month — shed 2.9%. The declines came as investors keenly awaited the start of China’s most important annual political meeting from Thursday, where top leaders are expected to set the growth target for 2026 and lay out economic priorities for the coming five years.

In FX, the dollar has pulled back from the highs. The Bloomberg Dollar Spot Index is up 0.5%. The Swedish krona is the weakest of the G-10 currencies, falling 0.9%. The Canadian dollar and Norwegian krone have been the most resilient.

In rates, treasuries hold losses after erasing opening gains that were spurred by broadening Middle East warfare after the US struck Iran. The reversal suggested that traders chose to bet on the potential inflationary aspects of the US-Iran conflict rather than rush to safe havens which helped Friday’s rally into month-end. Adding to upside pressure on yields, US benchmark crude oil futures are up about 8% with tanker traffic through the Strait of Hormuz at a near standstill. US yields are 3bp to 4bp higher, keeping curve spreads within 1bp of Friday’s closing levels. 10-year is near 3.98% vs session low 3.922% reached shortly after the Asia open. European government bonds are also in the red with underperformance seen in shorter-dated maturities as traders trim bets on interest rate cuts by the Bank of England and European Central Bank.

For Geoff Yu, senior macro strategist at BNY, Monday’s rise in US yields came as no big surprise given the elevated levels at which bonds were trading. The 10-year rate was at 3.99%, five basis points higher for the day.

In commodities, WTI crude oil futures rose the most in four years, while Brent crude soared more than 7%, topping $80 a barrel as traders assess how quickly Hormuz traffic can normalize. In Europe, natural gas jumped as much as 28%, the biggest increase since August 2023 after Goldman warned that European natural gas prices could more than double if shipping through the Strait of Hormuz is halted for one month. Spot gold rises 2% and briefly topped $5,400/oz. Silver logs a slightly smaller gain. Bitcoin rises 0.8%.

US economic data slate includes February final S&P Global US manufacturing PMI (9:45am) and February ISM manufacturing (10am); no Fed speakers are scheduled

Market snapshot

S&P 500 mini -1%

Nasdaq 100 mini -1.4%

Russell 2000 mini -1.3%

Stoxx Europe 600 -1.3%

DAX -1.6%

CAC 40 -1.5%

10-year Treasury yield +3 basis points at 3.96%

VIX +3.4 points at 23.3

Bloomberg Dollar Index +0.4% at 1192.78

euro -0.6% at $1.1743

WTI crude +7.4% at $72.01/barrel

Top Overnight News

Donald Trump said the bombing campaign against Iran may last for weeks and called on the nation’s leaders to capitulate. Blasts were heard across several Gulf states as they intercepted missiles launched by Iran. Trump is pushing for an Iranian leadership change but told ABC his preferred candidates to lead Iran were killed in the initial US strike. BBG

Iran is planning to name a new supreme leader within days after Saturday’s killing of Ayatollah Ali Khamenei. While Trump has urged Iranians to seize power from the regime, there’s no sign the US has laid the groundwork for an opposition movement. BBG

The IDF bombed Lebanon after Hezbollah fired rockets and drones into Israel, opening a new front in a widening regional war. Lebanon ordered the militant group to disarm. BBG

Chinese Foreign Minister Wang Yi called the killing of Khamenei “unacceptable,” complicating the planned summit between Trump and President Xi Jinping. Beijing said Washington gave it no advance warning of the attack, and added that they are in communication with the US about exchanges between their leaders. BBG

China Foreign Ministry said they are in communication with the US about exchanges between their leaders.

Wealthy investors who ploughed hundreds of billions of dollars into private credit are pulling back, cutting off a key source of funds that investment giants including Blackstone, Blue Owl, and Ares Management have used to fuel their growth. New commitments to so called non traded business development companies slid 40% to $3.2bn in January compared with December. FT

DeepSeek is set to release its latest large language model next week, more than a year since its last major release in a fresh test of China’s ambitions to challenge US rivals in AI.

A gauge of manufacturing activity signaled continued improvement in some of Asia’s top exporting economies midway through the first quarter, as demand for the region’s goods defied a volatile global environment. WSJ

Bank of Japan Deputy Governor Ryozo Himino said the central bank is expected to keep raising interest rates but gave no hints on the timing of the next hike, as the Middle East conflict heightened uncertainty over the economic outlook. RTRS

Russian officials increasingly consider there’s no point to continue US-led peace talks with Ukraine unless Kyiv is willing to cede territory to reach a deal, according to people familiar with the negotiations. BBG

Iran War

US and Israel launched a large-scale joint military operation against Iran on Saturday, 28th February, with explosions reported across Tehran shortly after 09:30 local time (06:00 GMT / 01:00 EST), and additional strikes were confirmed in Isfahan, Qom, Karaj and Kermanshah, while the Israeli military confirmed it launched an additional wave of strikes on Sunday morning, targeting Iran’s ballistic missile and aerial defence systems.

Iran launched immediate retaliatory missile and drone attacks against Israel, and multiple US military installations across the Gulf and multiple Gulf states, including the UAE, Qatar, Kuwait and Bahrain. Iranian state television officially confirmed the death of Supreme Leader Ayatollah Ali Khamenei following Saturday’s US–Israeli “decapitation strike” on his secure residence and office compound in central Tehran. Furthermore, IRGC declared the Strait of Hormuz closed to international navigation until further notice, while major tanker operators and global trading houses have halted crude, fuel and LNG shipments through the waterway. IRGC also announced on Sunday that they hit 3 US and UK oil tankers with missiles in the Gulf and Strait of Hormuz.

Iran launched a fresh wave of missile and drone attacks on Sunday, while Iranian sources stated that 27 US bases across the region were targeted, along with Israel’s military headquarters in Tel Aviv. It was also reported that Iran fired missiles towards British military bases in Cyprus and that rockets landed near British troops in Bahrain.

Israeli Air Force launched a new wave of attacks on Iranian regime targets in Tehran early on Monday and bombarded Hezbollah strongholds in the southern suburb of Beirut, while Hezbollah fired rockets towards Northern Israel for the first time since the ceasefire agreement, and it was also reported that Hezbollah parliamentary bloc head Mohammed Raad was killed in an Israeli raid.

US President Trump said the US military launched “major combat operations” in Iran with the objective of defending the American people by eliminating imminent threats from the Iranian regime. Trump said people in Iran should stay at home and that bombs will be dropping everywhere, while he called for Iranians to take over the government.

US President Trump said that Iran’s Supreme Leader Khamenei had died, and he was informed that they destroyed and sank nine Iranian ships, as well as largely destroyed the naval headquarters. Trump separately commented that the military operations are ahead of schedule and that 48 leaders were killed in strikes on Iran, while he also stated that Iranian leaders want to talk and he has agreed to talk, but couldn’t say if it would happen soon, according to Atlantic Magazine and Daily Mail. Furthermore, Trump suggested that the fighting with Iran could go on for four weeks, while he also stated on Sunday that they have hit hundreds of targets in Iran under ‘Operation Epic Fury’ and combat operations will continue in full force until all objectives are complete.

US President Trump said he could lift sanctions on Iran if its next leader proves pragmatic and that he had three very good choices for Iran’s next leader, although he also commented that the people he considered for Iran’s next leader died in the air attacks.

US Secretary of War Hegseth is to hold a press conference at 08:00EST/13:00GMT. White House separately announced that US Secretary of State Rubio and Secretary of War Hegseth are to brief a full Congress on Tuesday.

US officials told Al Jazeera that the strikes on Iran are focused on military targets and will be far more extensive than the US strikes last June, while the US reported that three US service members died and five were seriously wounded amid the operations against Iran.

Israeli PM Netanyahu said the US and Israel operations are to remove the existential threat from the Iranian regime, while Israeli officials characterised the action as a “pre-emptive strike” to prevent Iran from obtaining nuclear weapons. Israel ordered the shutdown of some natural gas fields as a security measure following the US-Israel strike on Iran, while it pre-approved a USD 2.9bln supplement to the defence budget to fund the war with Iran.

Trade/Tariffs

India’s Foreign Ministry announces that they have signed an uranium supply agreement with Canada.

Singapore and South Korea are in talks to upgrade a free trade agreement.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly pressured as all focus centred on geopolitics following the US and Israeli strikes on Iran, which killed its Supreme Leader and dozens of officials, while Iran responded with retaliatory strikes against the US and allies, including several neighbours in the Gulf. ASX 200 was rangebound with weakness seen in tech, financial and airlines stocks as the latter got a double whammy from flight disruptions and higher fuel costs, while energy stocks benefitted from the surge in oil due to the Iran conflict.

Nikkei 225 fell beneath the 58,000 level as exporters suffered from the worsening geopolitical climate and disruption in the Strait of Hormuz, which the IRGC shut. Hang Seng and Shanghai Comp were mixed with heavy losses in Hong Kong due to tech weakness, while the mainland shrugged off early jitters and climbed ahead of the annual ‘two sessions’ in Beijing, where top officials are set to unveil economic strategies.

Top Asian News

China overhauled a key micro credit program in which the focus is shifting to longer-term income support for rural households from a prior focus on poverty alleviation.

Macau gaming revenue in February rose 4.5% Y/Y to MOP 20.6bln (exp. 1% growth).

DeepSeek is to release the long-awaited DeepSeek 4 model in the week ahead.

European bourses (STOXX 600 -1.3%) are entirely in the red due to instability in the Middle East. In brief, the US-Israeli war with Iran has entered its third day, with all sides conducting large-scale airstrikes. Airspaces have been closed, oil refineries and tankers have been hit, and threats of further attacks continue (see “Iran Situation Report – Day 3” on the headline feed for more detailed analysis). The FTSE 100 (-1.0%) is being supported, albeit posting slight losses, helped by the major oil names (BP +1.8%, Shell +2.2%) as oil prices rise. The banking-heavy IBEX 35 (-2.2%) and FTSE MIB (-1.7%) have been hit the hardest on the prospect of increased war-risk claims.

From a sectoral perspective, Energy leads the pile, given the strength in underlying oil prices; Defence names are also stronger across the board, given the increased tensions; Rheinmetall +1.3%, BAE +5.2%, Leonardo +4.7%. One other key space of the market that has benefited is shipping names such as Maersk (+4.5%), Kuehne+Nagel (+0.4%), due to higher freight rates. US equity futures (ES -1.0%, NQ -1.4%, RTY -1.4%) have followed the global risk tone; in recent trade, contracts are attempting to rebound off worst levels, though remain significantly in the red. ASML (ASML NA) is planning to expand into advanced packaging for AI chips, and is exploring larger chip sizes and scanner systems

Top European News

Top academics warned that planned cuts to physics and astronomy funding risk undermining a key government strategy to harness innovation to boost economic growth, according to FT.

FX

DXY gains but trades off best levels as participants flock to the USD in light of the weekend geopolitics, with the initial US-Israel strike on Iran expanding throughout the Gulf and Middle East. Analysts at ING highlight three main channels that keep the USD in demand: 1) the US is less dependent on imported energy vs Europe and most of Asia. Higher energy hurts importers (EUR, JPY), whilst European Nat Gas opened up around 25%. 2) Markets are scaling back expectations for rate cuts from the Fed, with higher energy also proving headwinds for disinflation. A “bearish flattening” in the US yield curve (short-end yields rising) supports the dollar. 3) Higher energy and reduced Fed easing expectations could reverse capital flows into EM, which would further support the USD. DXY is around the middle of a 97.768-98.566 range after hitting highs around an hour after the European cash open.

GBP is the worst performer amid the RAF base in Cyprus being struck by an Iranian drone. The UK has confirmed it is not participating in offensive operations but is permitting defensive use of bases. GBP/USD slipped from a 1.3456 peak to a 1.3314 trough.

EUR has been hit by the aforementioned surge in energy prices, with EUR/USD slumping from near 1.1800 to lows of 1.1698 before trimming losses at the time of writing. ING suggests EUR/USD could slide back toward the 1.1575–1.1600 area if escalation continues.

JPY and CHF are softer despite their haven appeals, with the USD sought after given its reduced dependency on energy imports. USD/JPY is +0.6% in a 156.04-157.25 range. USD/CHF trades +0.5% in a 0.7668-0.7742 parameter.

Antipodeans also post losses amid their high-beta properties and sensitivity to risk. AUD/USD resides in a 0.7032-0.7117 range and NZD/USD in a 0.5928-0.5995 band.

Fixed Income

USTs opened higher, then jumped to a session high of 114-12, before quickly paring much of the upside as the APAC session progressed. The narrative quickly shifted from “haven” related upside, to traders assessing and then pricing in the inflationary impacts of the closure of the Strait of Hormuz. This impacts both: a) energy prices, b) prices of goods which are subject to longer trading routes, as shipping giants avoid the chokepoint. From a central banking perspective, inflationary pressures could see policymakers shift hawkishly – though, Danske Bank suggested that the Fed is unlikely to trigger speculations of near-term policy shifts following the rise in energy prices. Geopols aside, the US ISM manufacturing survey for February is expected to be little changed at 52.3 (from 52.6). The Atlanta Fed will update its GDPnow tracking estimate, which is currently modelling growth of 3.0% in Q1. Later in the session, the Fed will publish its Senior Loan Officer Survey. USTs currently trade around 113-23 within a 113-22+ to 114-12 range.

Bunds moving in-line with peers and currently trading around 130.05 to 130.53 range. Price action is similar to the above, initial haven flows buoyed German paper, before markets began factoring in inflationary impacts. Danske expect short-term widening Schatz spreads, but the bank highlights that safe-haven inflows are often short-lived and modest.

Gilts are underperforming, and trades lower by around 30 ticks within a 93.31 to 93.57 range. Underperformance, which perhaps can be explained given that the region is a net-importer of oil, and as such has long been considered highly vulnerable to energy volatility. Elsewhere, ahead of this week’s UK Spring Statement, Chancellor Reeves has received a GBP 22bln windfall as tax receipts outperformed forecasts, according to Bloomberg; analysis of official data showed stronger than expected self-assessed income tax and sales levy revenues, alongside lower debt-interest spending, contributing to the improvement in the public finances.

Commodities

Crude futures surged at the reopen in reaction to the geopolitical escalation in the Middle East owing to the strikes against Iran and the killing of its Supreme Leader, as well as its retaliation against the US and several neighbours in the Gulf, while it also announced the closure of the Strait of Hormuz. (Newsquawk analysis available on the feed). However, prices waned off their opening highs as Brent returned to beneath the USD 80/bbl and WTI briefly retreated to below 70/bbl levels before recovering, with Brent May’26 currently within USD 74.54-80.82/bbl (+6.2% at the time of writing) and WTI Apr’26 within USD 71.88-75.33/bbl (+7.3% at the time of writing).

Spot gold rallied on a haven bid amid the weekend geopolitics (Newsquawk analysis available on the feed) but then mildly pulled back after stalling just shy of the USD 5,400/oz level in APAC trade, before mounting the level to a USD 5,419.15/oz peak. Spot silver hit a USD 92.42/oz peak from a USD 92.02/oz trough.

Copper futures ultimately weakened overnight but trades flat in European hours, in choppy trade amid the mostly negative risk appetite in the region, with all focus on geopolitics. 3M LME copper resides in a narrow USD 13,249.60-13,444/t range at the time of writing.

OPEC+ is to resume oil output increases, in which it will add 206k bpd in April. It had been previously reported over the weekend that OPEC+ could consider a larger production hike of as much as 441k bpd following the strike on Iran.

IRGC declared the Strait of Hormuz closed to international navigation until further notice, while major tanker operators and global trading houses have halted crude, fuel and LNG shipments through the waterway. Furthermore, analysts warned of a potential Brent crude move above USD 100/bbl if the blockade persists.

Oil facilities of regional countries are not Iran’s targets, via Mehr.

Chevron (CVX) said it was instructed by Israel’s Ministry of Energy to temporarily shut-in production at the Leviathan gas production platform.

Middle East crude benchmark Dubai’s premium rises to around USD 5.90/bbl, the highest since 2022, sources say.

IAEA Director General Grossi said we have no indication that any of Iran’s nuclear installations have been damaged or hit. The situation is very concerning, cannot rule out a possible radiological release with serious consequences. No elevation of radiation levels above the usual background levels have been detected so far in countries neighbouring Iran.

Saudi Energy Ministry says limited fire at Aramco’s Ras Tanura refinery, no impact on supplies.

The limited fire at Ras Tanura refinery was due to shrapnel falling during an interception operation, Al Hadath reported.

Central Banks

BoJ Deputy Governor Himino said to raise rates if economic outlook is met, adds the goal is to maintain price stability by avoiding excessive inflation and deflation, thereby supporting sustainable economic growth. said:Impact of rate hikes has been limited so far.

SNB states that in view of the international situation, we are more prepared to intervene in the FX market.

Swiss Sight Deposits (w/e Mar 1). Domestic Banks CHF 440.5bln (prev. 440.6bln), Total CHF 459.8bln (prev. 457.6bln).

Geopolitics: Middle East

Israeli military says it has begun additional strikes on Tehran.

Qatar Defence Ministry says it intercepted two Iranian drones, which targeted energy facilties; one drone headed towards QatarEnergy’s Raf Laffan facility

“Israel army said there is no reason for Lebanon ground invasion for now”, via Al Arabiya citing AFP.

Israel’s IDF said “We are discussing the option of carrying out a ground operation inside Lebanon”, via Al Jazeera.

Iran’s ambassador to the IAEA said Israel and the US attacked Iranian nuclear facilities on Sunday.

Iran’s Larijani said they will not negotiate with the US.

Iran’s Secretary of the Supreme National Security Council Larijani said US President Trump has brought chaos to the region with “false whims” and is now worried of more casualties among US forces. Trump is sacrificing American soldiers for Israel’s quest for power.

Iran warns that those responsible for killing Supreme Leader Khamenei will face consequences.

US President Trump said he could lift sanctions on Iran if its next leader proves pragmatic, according to New York Times. said:He had three very good choices for next Iran leader.

US President Trump said the people he considered for Iran’s next leader died in the air attacks, according to ABC News.

US President Trump said Iran does not want to go quite far enough and it’s too bad and are not happy with Iran negotiation.

US Secretary of State Rubio designating Iran as state sponsor of wrongful detention; Iran must stop taking hostages; will consider other measures if Iran does not stop.

US State Department said no American should travel to Iran for any reason and reiterate their call for Americans who are currently in Iran to leave immediately.

Hezbollah reportedly fires rockets towards Northern Israel for the first time since the ceasefire agreement, according to Israel Broadcasting Corporation.

Omani Foreign Minister said “The single most important achievement, I believe, is the agreement that Iran will never, ever have a nuclear material that will create a bomb…”, according to CBS interviewing Albusaidi. ”

Geopolitics: Ukraine

Ukraine President Zelensky says long war in Iran may impact air defence for Ukraine.

Russia is said to consider a halt in peace talks unless Ukraine cedes land. Talks planned for the week ahead will be decisive on whether or not the sides can agree on terms to end the war, while Russia will likely walk away if Ukrainian President Zelensky fails to make the concession.

A fuel terminal in Russia’s Novorossiysk is on fire, according to local authorities.

US Event Calendar

9:45 am: United States Feb F S&P Global US Manufacturing PMI, est. 51.35, prior 51.2

10:00 am: United States Feb ISM Manufacturing, est. 51.5, prior 52.6

10:00 am: United States Feb ISM Prices Paid, est. 60, prior 59

DB’s Jim Reid concludes the overnight wrap

Those who read my EMR on Friday will appreciate that frantic emails around a major international conflict were an interesting additional challenge to try to squeeze into a packed weekend of “daddy childcare”. By now, there is little point in recapping much of the news around the strikes on Iran, so instead we’ll jump straight into the latest market reaction.

As regular readers will know from the work we have shared from DB’s Binky Chadha, the negative market impact of notable geopolitical events is usually measured in only days and weeks, and you could argue that the market has increasingly realised this and now reacts less to big geopolitical events than it may have done a few years ago. However, one persistent risk is always a prolonged impact on the oil price. As such, that is the main market to watch today and for the duration of this episode. How firmly, or officially closed, the Strait of Hormuz remains will probably play a big part in this.

So far, Brent is about +7% higher at $77.60/bbl as I type this morning, having briefly been as high as $82 as trading in Asia opened. The spike comes as tanker traffic via the Strait of Hormuz has largely stopped with Iran having attacked three oil tankers over the weekend, though Iran’s foreign minister said on Sunday that Iran was not seeking to close the strait. There is a view that ahead of the mid-terms, the US administration will do what they can to ensure Iran struggles to block the Strait for long. Investors will also be watching the extent of damage to Iran’s oil export facilities.

Meanwhile, OPEC+ yesterday announced a supply increase of 206k barrels a day in April, following an increase of 137k a day in December. This is a decent rise, but it would not change the bigger picture if there were a sizeable disruption to oil flows.

With most markets closed over the weekend, Bitcoin served as a barometer of sentiment and immediately dropped around -4% when news of the attacks broke early London time on Saturday morning. From these lows, it rebounded around 7% through Saturday and into Sunday as mounting speculation that Supreme Leader Khamenei had been killed was confirmed. This raised hopes of a decisive operation with an obvious ending. As things stand, Bitcoin is about -2% down off these highs, but still +2% above where we were just before the strikes.

Market sentiment bounced shortly after the Asia open amid some more encouraging reporting. According to the New York Times, Trump said that he was open to lifting sanctions on Iran if its new leadership was pragmatic though he also said that the US could keep up its campaign against Iran for “four to five weeks”. Meanwhile, the Wall Street Journal reported that Ali Larijani, the secretary of Iran’s Supreme National Security Council who’s seen as leading Iran’s current effort, made a fresh push to resume nuclear talks with Washington via Omani mediators. However Larijani has poured some cold water on this on X, stating that “We will not negotiate with the United States.” This has taken oil off its lows for the session.

With the US unlikely to put boots on the ground, it’s not clear if full regime change is achievable and its outcome would be highly unpredictable, which naturally leaves questions of whether a negotiated resolution can still be found. At the same time, we’ve seen a widening of the conflict to Lebanon overnight, with Israel striking targets in the country after Hezbollah fired rockets into Israel.

So that all leaves global markets with a clear but not extreme risk-off reaction this morning. S&P 500 futures are down -0.81% from Friday’s close, with those on the STOXX 50 down a larger -1.47%. Note that Europe is more negatively exposed to higher energy prices, including also possible disruptions to LNG shipments from the Gulf. Meanwhile, in Asia, the Hang Seng (-1.59%) and the Nikkei (-1.51%) are among the worst performers, also affected by declines in technology stocks. The Shanghai Comp has turned positive (+0.33%). In FX, the dollar index is +0.29% higher, while the Swiss Franc is the best performing G10 currency amid the safe-haven demand. And gold is +1.41% higher. For Treasuries, yields initially opened a touch lower amid the safe-haven bid but this has quickly reversed this morning with the 10yr +2.8bps higher at 3.97%, after ending last week at post-2024 lows. So overall fairly measured response in Asia to the weekend events.

Outside the obvious and huge attention on the Middle East, the key focus this week will be on the US jobs report on Friday, retail sales on the same day, the ISM indices (today and Wednesday), and the Fed’s Beige Book, also due on Wednesday. European releases will include inflation data tomorrow and the ECB’s accounts of their February meeting on Thursday. Various global PMIs are also out this week.

In politics, highlights include the Two Sessions in China as well as the Spring Statement in the UK. Earnings reports will be due from Costco and Broadcom.

Delving deeper into the US data, the most important release in the week ahead is Friday’s February employment report. Our economists forecast headline payroll growth of 30k, down from 130k previously, with private payrolls rising by 50k after January’s unusually strong 172k gain. The moderation largely reflects payback from outsized hiring last month in private education and health services and construction, where job gains more than doubled their six month averages. Elsewhere in the establishment survey, our economists expect average hourly earnings to rise 0.4% month over month, unchanged from January, while the average workweek remains steady at 34.3 hours.

The household survey adds an additional layer of uncertainty this month, as the BLS implements its delayed annual population controls. Our economists forecast the unemployment rate at 4.3%, though risks around this estimate are elevated in both directions. January data will also be revised using the new controls, and attention will be focused on whether these adjustments meaningfully alter unemployment rates across demographic groups, particularly among younger cohorts, where concerns around entry level hiring remain heightened.

Friday also brings January retail sales, where weather related weakness in auto sales is likely to weigh on the headline figure. Our economists expect headline sales to decline 0.6%, with sales excluding autos down 0.1%, partly reflecting lower gasoline prices. That said, retail control sales are forecast to rebound by 0.3%, pointing to a firmer underlying pace of goods consumption. Tax refunds should provide additional support to spending in coming months, with the average refund running meaningfully higher than a year ago.

Ahead of Friday, several other releases will help set the tone. Our economists expect today’s manufacturing ISM to edge up to 53.1 from 52.6. Wednesday brings the ADP employment report, forecast at 50k (though seasonals might push it higher), alongside the non manufacturing ISM, seen at 54.0.

Other notable data include February unit motor vehicle sales tomorrow, which our economists expect at 15.1 million, potentially restrained again by adverse weather. Thursday’s preliminary Q4 productivity and unit labour cost figures are forecast at 1.3% and 2.2%, respectively.

Moving to Europe, the focus will continue to be on inflation, with February prints due for the Eurozone and Italy tomorrow, Switzerland on Wednesday, and Sweden on Thursday. ECB speakers will include President Lagarde today, and the central bank will release the accounts of its February meeting on Thursday.

In the UK, attention will be on the Spring Statement delivered by the Chancellor tomorrow, and our UK economist previews it here. There will also be the February DMP survey from the BoE on Thursday.

Over in Asia, the spotlight will be on China’s annual Two Sessions starting Wednesday (running through March 11), followed by the National People’s Congress session opening on Thursday, with the 15th Five Year Plan expected. Elsewhere, data highlights will include the February PMIs, both the official and private gauges, in China on Wednesday.

In Japan, our Chief Japan economist highlights the Shunto wage demands due on Thursday as the most anticipated event next week and expects wage demands this year to come in at 6.0%. There will also be the Financial Statements Statistics of Corporations (MoF survey) for Q4 on Tuesday, as well as the February consumer sentiment index on Wednesday. For more detail and forecasts, see our Chief Japan economist’s week ahead for the country here.

Earnings will include tech firms Broadcom, CrowdStrike and Marvell. US consumer firms will continue to be in focus, with reports from Costco and Target.

Looking back at last week, which now feels like a long time ago, the main theme was the ongoing AI disruption narrative, which continued to affect a range of assets. In part, this reflected the now infamous memo from Citrini Research, which outlined a hypothetical scenario in which AI adoption drove the US unemployment rate into double digits by mid 2028. We also had Nvidia’s earnings, which once again failed to deliver the kind of positive surprise markets had grown used to in 2023–24, even as they beat analysts’ estimates. Against this backdrop, the S&P 500 fell -0.44% (-0.43% on Friday), with the Magnificent 7 down -1.80% (-1.41% on Friday). The Philadelphia Semiconductor Index fell -1.96% (-1.21% on Friday), ending a run of 10 consecutive weekly gains.

Performance outside the US was notably stronger. The STOXX 600 posted a fifth consecutive weekly gain of +0.52% (+0.11% on Friday), closing at a record high. In Japan, the Nikkei rose +3.56% (+0.16% on Friday) to also hit a new record, taking its year to date gains to +16.91%.

The biggest news on Friday was rising concern about a possible US strike against Iran, which added further upward pressure on oil prices. Brent crude ended the week up +1.00% (+2.45% on Friday) at a seven month high of $72.48/bbl. It was also another strong week for precious metals, with gold prices up +3.36% (+1.81%) in their fourth consecutive weekly gain, and both are obviously seeing significant action again this morning.

Finally, in fixed income, sovereign bonds benefited from the broader caution. Ten year Treasury yields fell -14.4bps last week (-6.4bps on Friday) to 3.94%, their lowest level since October 2024. In Europe there were similar moves, with 10 year Bund yields down -9.4bps last week (-4.7bps on Friday) to 2.64%, marking their biggest weekly decline since April last year around the Liberation Day turmoil. Credit spreads widened on both sides of the Atlantic, with US high yield up +21bps (+9bps on Friday) and US investment grade up +7bps (+2bps on Friday), their biggest weekly widening since the Liberation Day tariffs. In Europe, high yield widened +13bps (+5bps on Friday), while investment grade widened +5bps (+3bps on Friday).

Tyler Durden

Mon, 03/02/2026 – 08:39

https://www.zerohedge.com/markets/futures-tumble-iran-war-sends-oil-gold-and-dollar-sharply-higher

River Plate sondea a Coudet para suceder a Gallardo como técnico

BUENOS AIRES (AP) — Un día después de la emotiva despedida a su entrenador Marcelo Gallardo, River Plate puso en marcha la sucesión y todos los caminos parecen conducir a Eduardo Coudet, el argentino que actualmente dirige al Alavés de España.

Christian Bragarnik, representante del “Chacho” Coudet, confirmó que recibió el viernes el llamado del presidente del club “millonario”, Stéfano Di Carlo, quien le manifestó que “es uno de los candidatos que van a evaluar”.

“Me preguntó cuál era su situación y me pidió tener una entrevista con él ”, reveló Bragarnik en diálogo con las cadenas ESPN y TyC Sports. “A partir de eso hay un montón de cosas por definir”.

Los contactos formales con el entorno de Coudet ocurrieron un día después del último partido de Gallardo al frente de River, con victoria 3-1 sobre Banfield por la séptima fecha de la liga local.