Category: News

Potential Strikes On Iran’s Reactor and Nuclear Complexes

Potential Strikes On Iran’s Reactor and Nuclear Complexes

Update: Iran Alleges Strikes on Natanz Enrichment Facility

Amid ongoing military operations that have targeted Iran’s Arak heavy-water reactor site, Tehran claims the United States and Israel also struck its key Natanz uranium enrichment complex on Sunday, March 1.

According to Iran’s state news agency IRNA, Atomic Energy Organization chief Mohammad Eslami informed IAEA Director General Rafael Grossi in a letter that “the criminal regimes of the United States and Israel… again targeted the Natanz nuclear site on Sunday afternoon.”

The Institute for Science and International Security claims they have verified the strikes.

The buildings visibly destroyed in the low resolution imagery taken by Copernicus on March 2, 2026 ( published by @BenTzionMacales ) at Natanz Fuel Enrichment Plant are the personnel entrances and a dummy building covering the only vehicle entrance to the underground site. Iran… pic.twitter.com/FZOb98riIu

— Inst for Science (@TheGoodISIS) March 2, 2026

Iran’s IAEA ambassador Reza Najafi repeated the accusation to reporters during Monday’s emergency Board of Governors meeting in Vienna, calling the facilities “peaceful” and “safeguarded.”

However, Grossi told the same session that the agency has “no indication that any of the nuclear installations have been damaged or hit.” He added that IAEA monitoring, including satellite imagery, has revealed nothing comparable to the major damage at Natanz during the June 2025 strikes, though contact with Iranian authorities remains limited.

The Iranian claims have not been independently verified. Israel and the United States have not commented on any specific strike at Natanz. The head of Iran’s atomic energy organization reiterated the claim from earlier this morning that the US has bombed the Natanz nuclear facility again.

* * *

Foreign media sources are circulating claims US/Israeli forces struck Iran’s Arak heavy-water reactor complex. If confirmed, this would mark the second major hit on the facility in less than a year, underscoring Jerusalem and Washington’s determination to eliminate every pathway to an Iranian nuclear weapon.

🚨🇮🇷 BREAKING:

The nuclear reactor in Arak, Iran, has been bombed, according to a foreign report.

yediot news https://t.co/Aaijy0nzYs pic.twitter.com/qoTkCcZhPX

— Mario Nawfal (@MarioNawfal) March 2, 2026

The Arak site, located about 250 km southwest of Tehran in Markazi Province, houses the unfinished IR-40/Khondab 40-megawatt thermal heavy-water research reactor and an adjacent Heavy Water Production Plant (HWPP). Originally designed in the early 2000s to potentially produce weapons-grade plutonium, the reactor was partially redesigned under the 2015 JCPOA to limit plutonium output for civilian isotope production. The reactor core was filled with cement and remained non-operational and defueled.

During last year’s escalation, Israel conducted a precision strike on the site. Satellite imagery showed the reactor’s containment dome breached and the core likely destroyed to prevent any future plutonium pathway. The adjacent HWPP suffered damage to distillation towers, though the full extent of production capability loss remains unclear. The IAEA confirmed no radiological release occurred, as the site contained no nuclear fuel or fissile material.

The IAEA has repeatedly stated that strikes here pose negligible off-site contamination risks, unlike potential meltdowns at operational power reactors (Bushehr) or chemical hazards at enrichment halls. Monitoring stations in neighboring countries have reported no radiation spikes following recent operations.

Strategically, neutralizing Arak closes Tehran’s plutonium option, complementing earlier damage to Natanz, Fordow, and Isfahan enrichment facilities. It signals that no element of Iran’s nuclear program is off-limits, potentially setting back breakout timelines by years and weakening the regime’s deterrence posture

Tyler Durden

Mon, 03/02/2026 – 14:25

https://www.zerohedge.com/military/potential-strike-irans-arak-reactor-complex

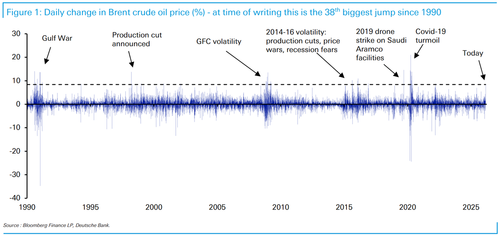

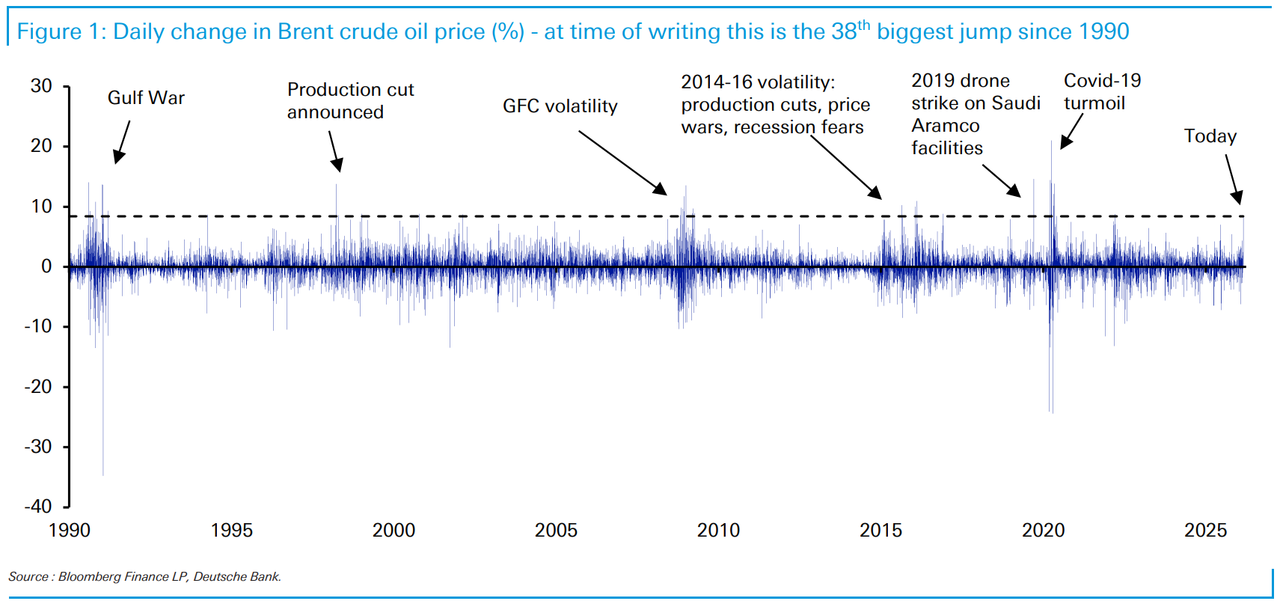

Only The 38th Largest Oil Spike Since 1990

Only The 38th Largest Oil Spike Since 1990

Today’s CoTD from DB’s Jim Reid shows the daily price of oil back to 1990. When he published the report, oil (+8.4%) was tracking to be the 38th biggest daily gain over this 36-year period. The graph annotates the clusters where we have seen larger moves.

So even though it’s a big move, to get into the top 20, 10 and 5 it would need to be up +9.6%, +13.6% and +13.9% respectively.

There were huge moves around the GFC and Covid-19 turmoil, whilst the Gulf War in 1990-91 also saw several double-digit gains.

Incidentally, since Jim published his chart of the day, oil has sold off more, and at last check it was up just 5.7% on the day, erasing its kneejerk spike by more than half.

Going forward, Reid says that much will depend on the Strait of Hormuz.

It seems it’s not officially closed but passage through it would be hazardous at the moment with self-imposed restrictions from virtually all that normally travel through it.

Tyler Durden

Mon, 03/02/2026 – 14:20

https://www.zerohedge.com/energy/only-38th-largest-oil-spike-1990

AI ‘Vibe Coding’ Could Put Ethereum Roadmap Ahead Of Schedule: Vitalik Buterin

AI ‘Vibe Coding’ Could Put Ethereum Roadmap Ahead Of Schedule: Vitalik Buterin

Authored by Martin Young via CoinTelegraph.com,

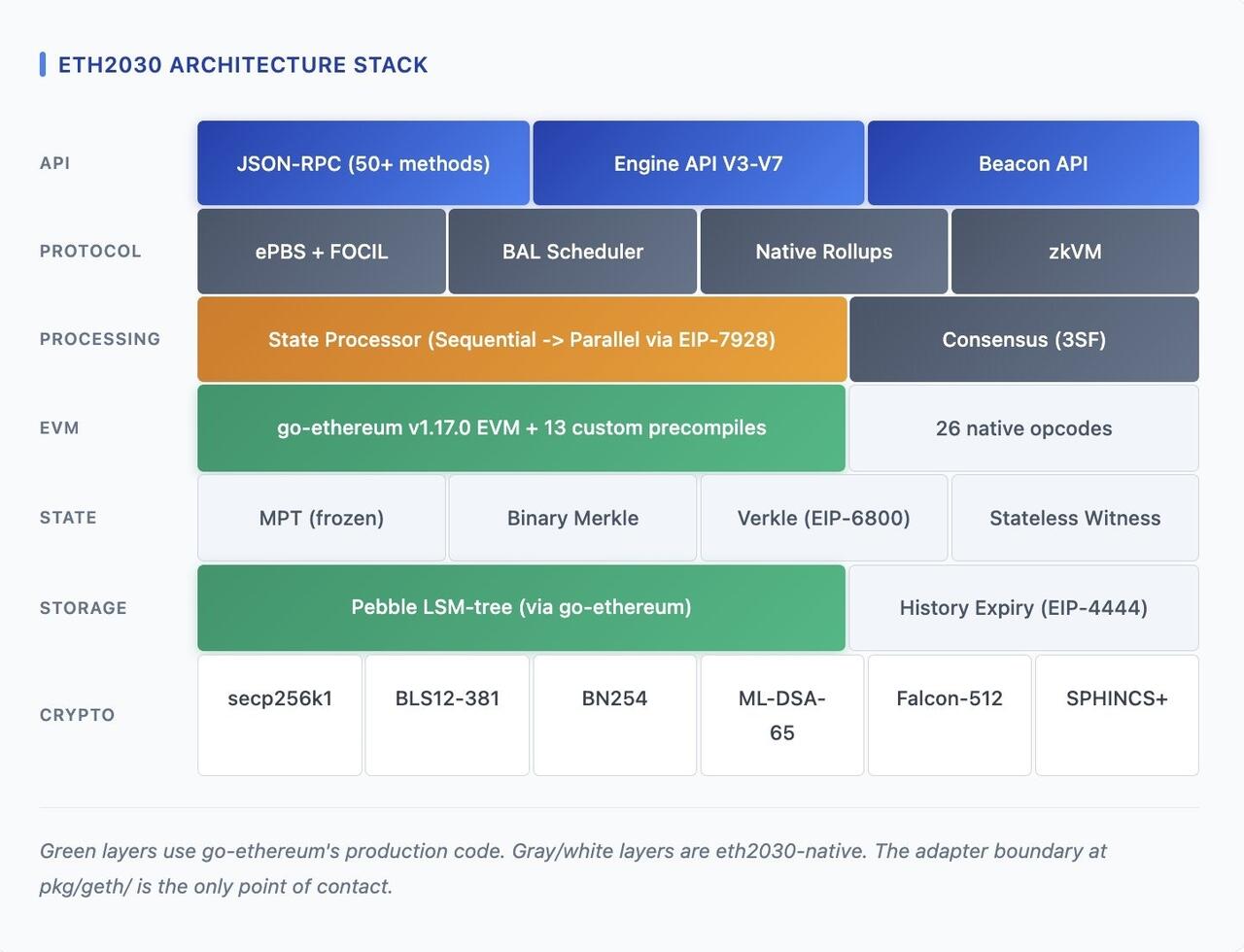

Ethereum co-founder Vitalik Buterin says an experiment that used artificial intelligence to prototype the blockchain’s roadmap out to 2030 in just a few weeks could have lessons for developers.

“This is quite an impressive experiment. Vibe-coding the entire 2030 roadmap within weeks,” Buterin posted to X on Saturday after a developer made a bet with Buterin in February that one person could use AI to code a reference implementation of the blockchain’s roadmap.

Buterin added that AI is “massively accelerating coding” and that people “should be open to the possibility that the Ethereum roadmap will finish much faster than people expect, at a much higher standard of security than people expect.”

Vibe coding is where AI creates the code for an application, allowing developers to quickly create software. The practice has become more popular as AI models have improved at coding; however, some warn that AI-generated code can be insecure.

ETH2030 architecture stack. Source: YQ

Buterin says AI code would have “critical bugs”

Buterin said that there were “massive caveats” to using AI, as the speed at which the code was written means it “almost certainly has lots of critical bugs, and probably in some cases ‘stub’ versions of a thing where the AI did not even try making the full version.”

“But six months ago, even this was far outside the realm of possibility, and what matters is where the trend is going,” he added.

Buterin cautioned that, instead of focusing on speed, more emphasis should be placed on security.

“The right way to use it is to take half the gains from AI in speed, and half the gains in security: generate more test-cases, formally verify everything, make more multi-implementations of things.”

He said that he was personally excited about the possibility that bug-free code, “long considered an idealistic delusion,” will finally become first possible and “then a basic expectation.”

Buterin has been active commenting on the recently released roadmap from the Ethereum Foundation, “Strawmap,” which outlines all upgrades planned for the next four years.

He has previously proposed plans to make Ethereum quantum-resistant and on Sunday said that account abstraction, or smart accounts, would “happen within a year.”

Tyler Durden

Mon, 03/02/2026 – 14:00

Construction Spending On Data Centers, Factories, Powerplants, And Office Buildings: Boom, Bust, And In Between

Construction Spending On Data Centers, Factories, Powerplants, And Office Buildings: Boom, Bust, And In Between

Authored by Wolf Richter via Wolf Street,

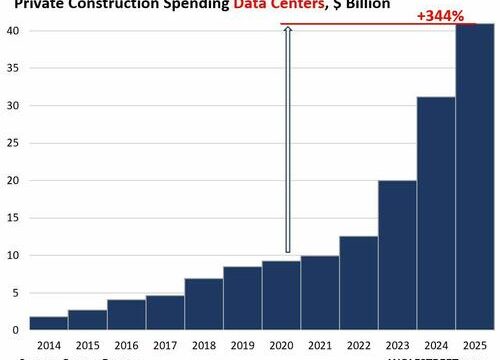

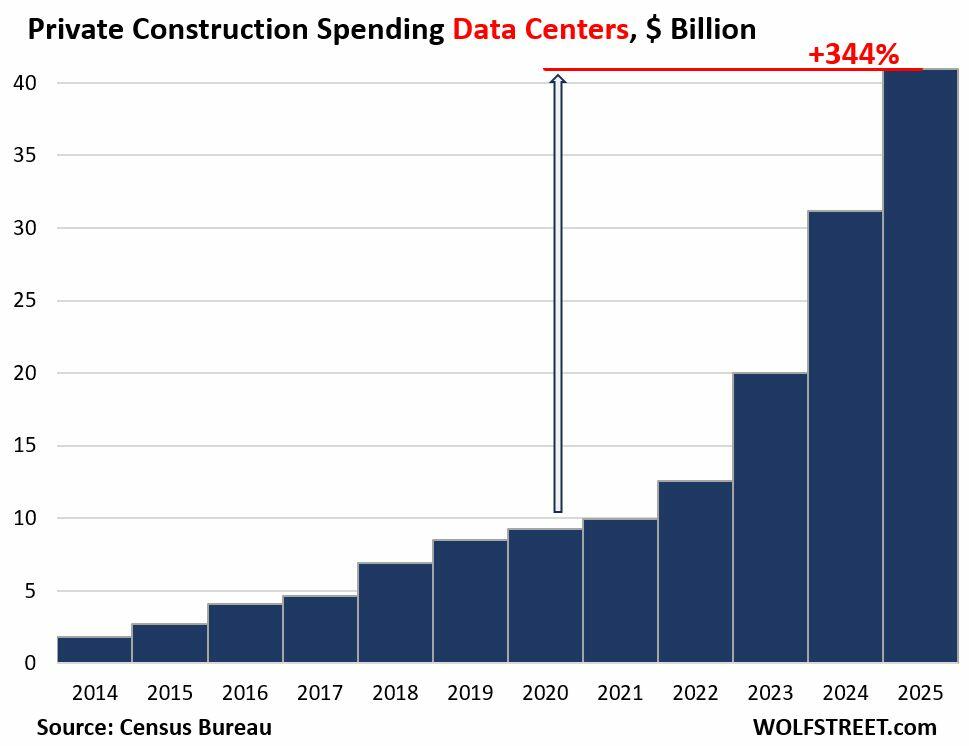

Construction spending on data centers in 2025 exploded by 32% from the prior year, by over 100% in two years, and by 344% from 2020, to $41 billion, according to the Census Bureau on Friday. Spending on construction costs of data centers used to be buried in office construction and was minimal compared to office construction. But more recently, the Census Bureau split out data-center construction spending going back to 2014.

Construction costs of data centers are only a relatively small portion of the immense amounts spent on AI infrastructure, most of which goes into electronic and electrical equipment, from AI servers to power generation equipment. Construction spending on data centers does not include the costs of the servers and racks but does include the cooling systems in the building and other built-in electrical equipment.

It takes years from the decision to build a data center to the data center being actually operational. And the massive amounts of capital expenditures announced by AI-related Corporate America in 2025 and the plans for 2026 haven’t yet shown up in the construction costs.

The amounts of capital expenditures being thrown around for 2026 are fantastical. Five companies alone – Amazon, Alphabet, Microsoft, Meta, and Oracle – have announced plans for $700 billion in capital expenditures for 2026, largely for AI-related projects. And how will they get this cash next year?

So this construction boom is not slowing down, unless tripped up by further the shortages of all kinds, such as power from the grid, power generators when there is no grid power, electrical equipment, electricians, specialized labor, etc.

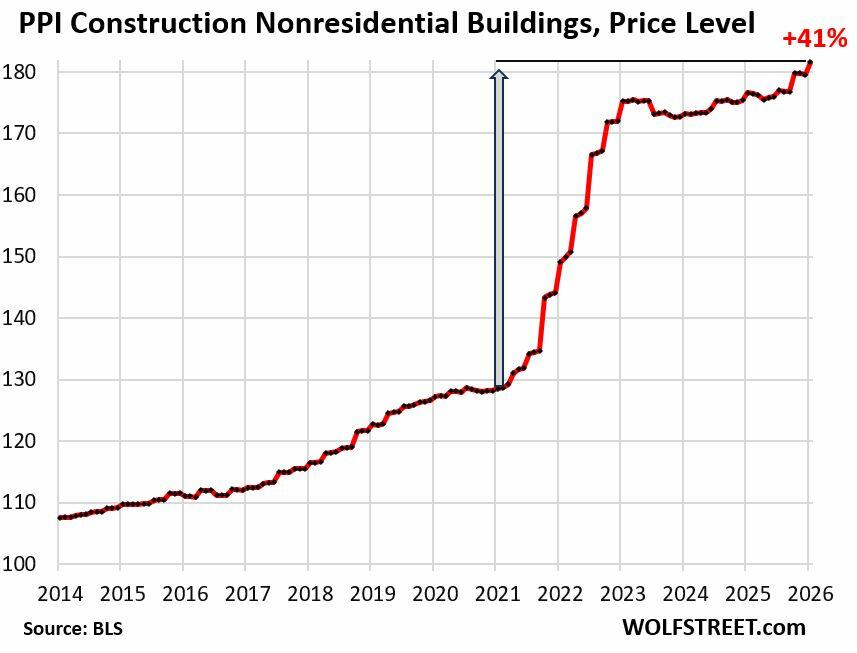

Inflation for construction costs for nonresidential buildings jumped by 1.1% in January from December, according to the Producer Price Index (PPI) for nonresidential construction, released by the Bureau of Labor Statistics on Friday (it was hot all around). Year-over-year, the nonresidential construction PPI was up by 2.8%, almost all of which occurred over the past four months.

From January 2021 through December 2022, over those two years, prices had exploded by 34%. From the beginning of 2023 to mid-2025, prices flattened out. But they’re now taking off again.

Over the years 2021-2025, the PPI for nonresidential construction rose by 41%. With spending on data center construction up by 344% over the same period, the red-hot construction spending boom is not a result of inflation – but of the AI investment mania.

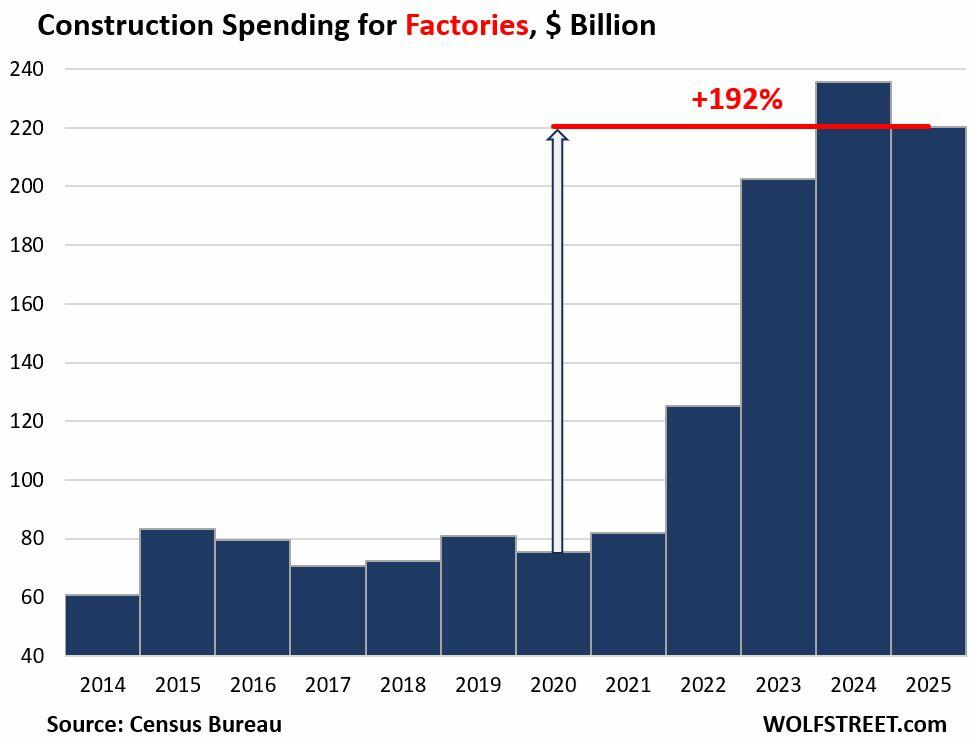

Construction spending on manufacturing plants has soared coming out of the pandemic. In 2025, at $220 billion, it was up by 192% from 2020.

This $220 billion in 2025 is over five times the amount spent on data centers ($41 billion).

The production equipment in the plant, such as the industrial robots, is not part of the construction costs. And they’re much more costly than the building itself.

Though still running at a red-hot pace, construction spending on factories has backed off from the spike in 2024, possibly as construction resources have been pulled away by the boom in data center construction, and amid reports of bottlenecks, shortages of skilled labor, and ICE hauling off workers from construction sites.

After decades of globalization, there is now a widespread rethink underway about production in the US.

These factories will all be highly automated to where manual labor is only a relatively small part of the product costs. Every year, year after year, decade after decade, automation improves, and companies try to cut their labor costs by expanding automation.

Within factory construction, spending on factories for computers, electronic, and electrical equipment exploded by 1,300% since 2020, from $9 billion in 2020 to $104 billion in 2025. This includes semiconductor plants and plants that build electrical equipment for the AI infrastructure boom.

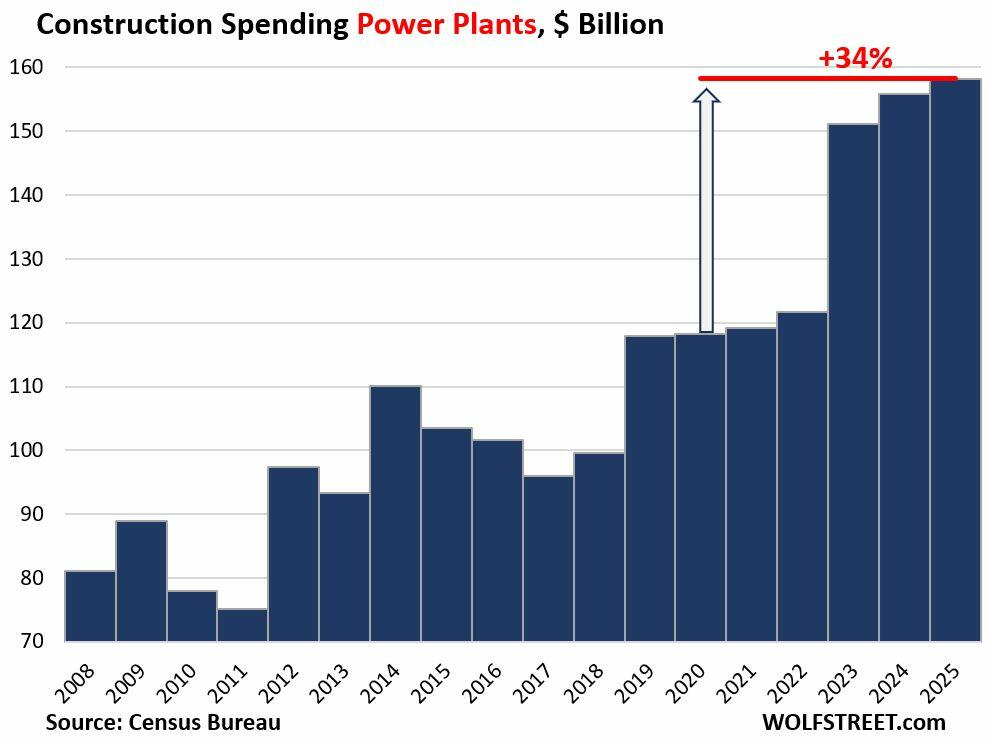

Powerplant construction is a highly regulated process in terms of permitting and approvals, and it takes years from the decision to build a power plant to having a functional power plant hooked to the grid.

In 2025, a record $158 billion was spent on building power plants, up by 34% from 2020.

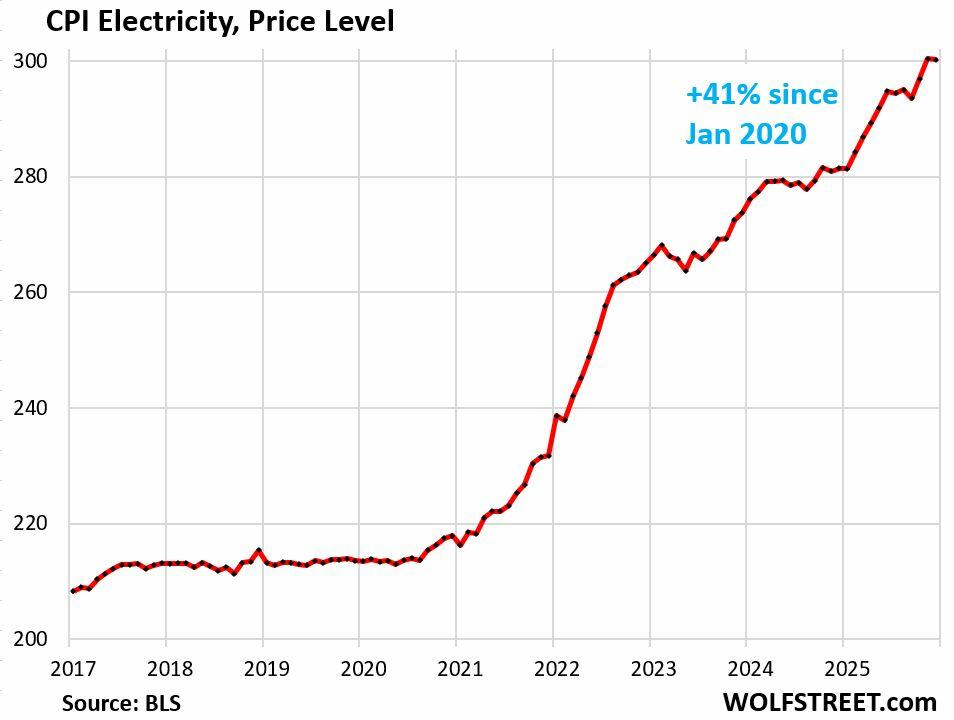

Electricity prices have soared by 41% over the past five years as demand for electricity has surged, after being roughly flat for 14 years. This increase in demand was largely driven by the new data centers.

But utilities and power generators are leery of spending billions of dollars on generation and distribution capacity for data centers that might never work out after the AI investment mania fizzles, which would turn these investments into stranded assets.

This leeriness is fed by the many hedge funds with ag land that want a utility to commit billions of dollars to run a high-voltage powerline to it, and possibly build a power plant to supply it with power, so that the hedge fund can then sell the ag land at a huge profit as data-center ready to some hyperscaler. If that deal doesn’t happen, the utility ends up with an expensive stranded asset.

Office building construction has taken a massive hit after it became clear that office landlords were getting into serious trouble as demand for office space collapsed during the pandemic. Countless landlords defaulted on their office mortgages, and numerous buildings were seized by lenders and sold in foreclosure sales for cents on the dollar. The going rate for office building transactions is now at discounts of 30% to 70% from pre-pandemic prices. The delinquency rate for office CMBS spiked to record 12.3% in January. And there are efforts underway in expensive markets to convert office towers into residential towers, while smaller office buildings get torn down and replaced with housing. Office CRE has been in a depression since 2022.

In a way, it seems surprising that anyone would still spend good money on office buildings, but it’s the old office towers that are in trouble, while the latest and greatest office towers see more demand from the flight to quality that high vacancy rates made possible.

So spending on office construction (not including data centers) dropped further in 2025, to $49 billion, the lowest since 2015, and down by 32% from the peak in 2020.

Some of this spending is for buildings that were planned years ago and that are being completed now. For example, JP Morgan’s $3-billion tower at 270 Park Avenue in Manhattan was announced in 2018, was formally topped off in November 2023, and had its grand opening in October 2025.

Tyler Durden

Mon, 03/02/2026 – 13:20

SaaS: Is There Opportunity In The Destruction?

SaaS: Is There Opportunity In The Destruction?

Authored by Lance Roberts via RealInvestmentAdvice.com,

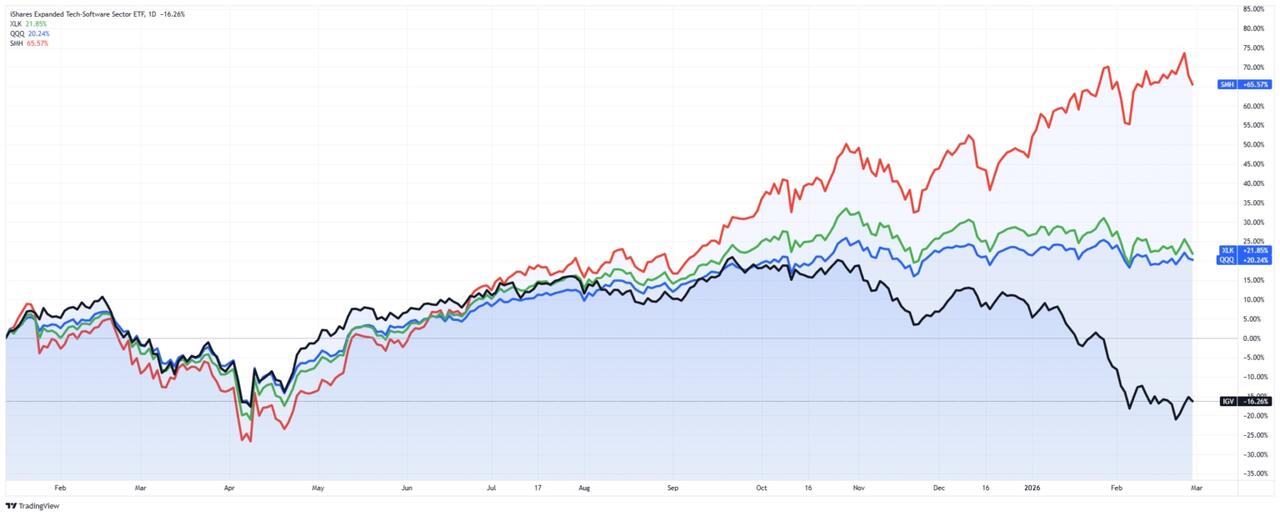

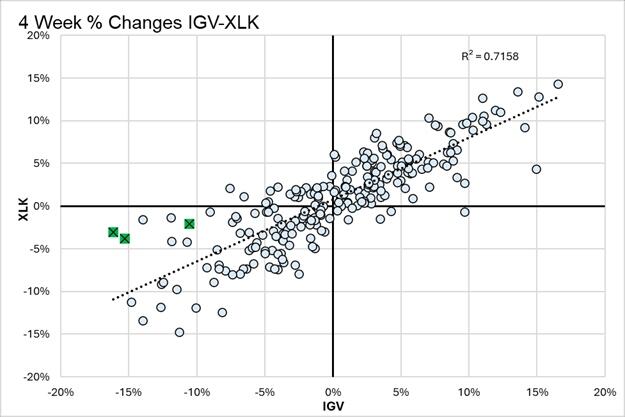

A specter is haunting Wall Street – the specter of the “SaaSpocalypse.” Since the iShares Expanded Tech-Software Sector ETF (IGV) peaked on September 19, 2025, it has fallen roughly 30%. For context, the broad technology indexes like XLK and QQQ are essentially flat over the same period, and the semiconductor ETF (SMH) is up 30%. Between mid-January and mid-February 2026 alone, approximately one trillion dollars was wiped from the collective value of software stocks, with the S&P North American Software Index posting its worst monthly decline since the 2008 financial crisis.

The catalyst was a series of AI product launches, most notably Anthropic’s Claude Cowork tool and OpenAI’s enterprise agent, Frontier, demonstrating that AI agents can now handle complex knowledge work autonomously. The market’s interpretation was simple. If AI agents can replicate what enterprise software does, then enterprise software is finished. That is the narrative that has taken hold in recent weeks. The consequence has been brutal. Workday is down 35% year-to-date. Adobe has shed 26%. Salesforce, 25%. Atlassian plunged 35% in a single week. Even Microsoft, the ultimate blue chip, fell by more than 10%.

The thesis is straightforward enough. Generative AI can now write code, automate workflows, and rapidly and cheaply create customized applications. Therefore, if enterprises can build their own “disposable software,” micro-apps tailored to specific workflows, instead of paying bloated subscription fees, then the traditional per-seat SaaS pricing model is dead. Potentially worse is that AI lowers barriers to entry, enabling more competitors to quickly replicate existing software. Such would compress margins and weaken the moats that once protected large software firms.

It is a compelling narrative. The question investors must answer is whether it is true.

Will AI Actually Kill Software Stocks? Not So Fast

Like most market narratives, the SaaSpocalypse contains some truth, a great deal of speculation, and several outright falsehoods. The most important rebuttal is that the value of enterprise software has never resided solely in its code. Enterprise software encodes institutional architecture. That architecture is the deep domain knowledge, compliance frameworks, workflow logic, and years of organizational customization that companies depend on to function. Think about it this way. If you are a medium to large enterprise dependent on data to service customers, maintain workflows, and fulfill orders, are you going to trust something that AI created that is potentially unreliable or error-ridden? Or, are you more likely to rely on software with deep local context, reliable outputs, and that has been rigorously tested and debugged over years of application use?

“Add deep workflow embedding to the mix and the picture becomes clearer still. When a SaaS platform is the system of record inside core banking, hospital EHRs, or government case management, replacement isn’t a technical decision, it’s an organisational trauma. Staff retraining, data migration, permission re-architecture, and regulatory re-certification make a rip-and-replace approach impractical, even when a cheaper AI-built alternative exists on paper.” – LiveWire

Furthermore, the underlying data does not support the skepticism either. Gartner’s February 2026 forecast projects worldwide software spending will grow 14.7% in 2026 to more than $1.4 trillion, accelerating from 11.5% growth in 2025. That represents roughly $180 billion in net new software spending in a single year. Global SaaS spending specifically is projected to rise from $318 billion in 2025 to $576 billion by 2029, according to Forrester. The reality is that enterprises are not abandoning software; they are spending more on it. As Mark Gardner recently noted:

“However, this sell-off is analytically lazy. And it’s being driven, at least in part, by the very technology it fears hallucinating on its own research. We believe the difference this time is that investors have the opportunity to look through the noise and identify the SaaS businesses where the structural moats are not just intact, they’re actually widening.

It was also fascinating to listen to Salesforce CEO Marc Benioff in CRM’s latest quarterly earnings report. He specifically addressed the panic, invoking the term “SaaSpocalypse” at least 6 times. His point was blunt: this is not Salesforce’s first existential scare, and AI is making their products more valuable, not less. The company introduced a new metric, agentic work units, designed to capture the output-driven value of its AI-enabled platform. More importantly, Gartner’s own analysts note that GenAI features are now ubiquitous across enterprise software and are increasingly costly. In other words, the cost of software is going up precisely because of AI, not in spite of it. There is a meaningful difference between a technology that changes how software works and one that makes software unnecessary.

Survivors and Thrivers: Which SaaS Companies Have the Strongest Moats

If the SaaSpocalypse narrative proves to be more panic than prophecy, the critical task becomes identifying which companies will emerge stronger. Forrester’s research provides a useful framework: horizontal point-solution vendors with low switching costs and weak enterprise integration face genuine existential risk. But vertical- or domain-specific SaaS vendors, those addressing complex industries like healthcare, manufacturing, or financial services, or those controlling unique proprietary data, have a substantially greater chance of survival and even growth.

Furthermore, even before the “SaaSpocalypse” began, the revaluation of these companies was already well underway, and current prices are nowhere near the 2021 froth levels.

Therefore, as investors, we need to think about “separating the wheat from the chaff.” While valuations and fundamentals are important, the key will be finding the companies best positioned in the market. Those companies share several characteristics.

First, platform-scale incumbents that serve as systems of record, Salesforce, Microsoft, Oracle, and ServiceNow, possess deep integration into enterprise workflows that cannot easily be replicated by a general-purpose AI agent. These companies are rapidly embedding AI agents alongside their existing deterministic processes, particularly for regulated industries.

Second, cybersecurity firms like Palo Alto Networks and CrowdStrike occupy a category where AI is additive rather than substitutive. As enterprises deploy more AI systems, the attack surface expands.

Third, data infrastructure and vertical SaaS companies that sit at the foundation of AI workloads or control proprietary domain data benefit directly from the same trend punishing commodity application vendors.

The table below highlights eight companies across four categories whose reported metrics most closely align with the characteristics that separate durable SaaS businesses from vulnerable ones.

So, where do you start your process?

Investor Playbook: Metrics That Matter and How to Position

For investors, the current dislocation presents both a challenge and an opportunity.

The biggest challenge is overcoming the “fear of loss.” Loss-avoidance is an emotional behavior that impedes our ability to “buy low,” as we fear prices will keep falling indefinitely. However, logic and fundamentals quickly refute that concern. However, it is a “barrier to entry” that keeps investors sidelined when prices decline, even as opportunities increase.

The statistical evidence of overshoot is significant. As Michael Lebowitz noted last week, the price ratio between IGV and XLK has diverged by nearly four standard deviations from historical norms over the past 100 days.

Based on the five-year relationship, either XLK is 10% overpriced, or IGV is 10% underpriced. When statistical relationships stretch this far, mean reversion eventually follows—though we caution that in environments where narratives are this powerful, divergences can persist longer than models suggest.

With this in mind, we suggest that doing your homework rather than listening to narratives is where the opportunity lies. Therefore, the right approach is to be surgical, rather than thematic. Rather than buying the entire beaten-down sector via IGV, which is okay if you only seek “average” returns, we think focusing on individual company fundamentals will yield better results. Therefore, here are a few metrics you can use to separate genuine AI beneficiaries from vulnerable incumbents. These metrics include:

Price-To-Earnings Growth (PEG): Measures the current price of the shares relative to their expected growth rate of earnings in the future. PEG ratios of 1 or less are considered to be cheap valuations.

Net Revenue Retention (NRR): Measures whether existing customers are spending more over time. Companies maintaining NRR above 120% demonstrate that AI features are expanding wallet share rather than cannibalizing it.

Remaining Performance Obligations (RPO): Measures whether forward demand is accelerating or decelerating, cutting through the noise of quarterly revenue.

Free cash flow margins: Reveals whether companies can fund their AI transformation internally or must dilute shareholders to compete.

AI attach rates: Measures the percentage of customers adopting AI-powered product tiers. It provides a real-time indicator of whether the AI transition is generating revenue or merely generating press releases.

A sustained SaaS recovery, as EBC Financial Group’s analysis notes, will likely require at least two of three conditions:

More accommodative financial conditions,

Enhanced earnings visibility, and/or

A shift in the narrative from viewing AI as a threat to recognizing its monetization potential.

We think the latter two are the most likely.

For now, investors should remain cautiously positioned. Make small bets, manage your risk exposure, and give yourself plenty of time. The recognition of value often takes longer than logic would suggest, particularly when negative momentum is strong.

The SaaSpocalypse makes for dramatic headlines, but the idea that AI agents will simply devour enterprise software whole ignores both the data and the institutional complexity of the businesses being disrupted. The real risk for investors is not that they are too slow to sell their SaaS holdings. It is that they eventually get stampeded by market panic into undervaluing companies whose competitive positions are, in many cases, strengthening.

Discipline, not panic, is the appropriate response.

Tyler Durden

Mon, 03/02/2026 – 12:40

https://www.zerohedge.com/markets/saas-there-opportunity-destruction

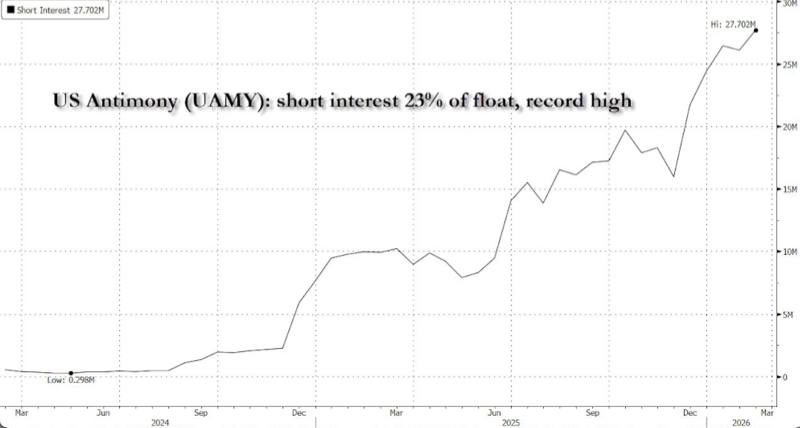

What’s Igniting Today’s U.S. Antimony Spike? Potential Catalysts

What’s Igniting Today’s U.S. Antimony Spike? Potential Catalysts

United States Antimony Corp. shares are surging in the early U.S. cash session as geopolitical risk around U.S.-China relations is set to deteriorate, with Beijing’s condemnation of the U.S.-Israeli strike on Iran raising the likelihood that President Trump’s upcoming trip to Beijing could be a bust.

The deterioration in Sino-U.S. relations was evident overnight, with China’s Foreign Minister Wang Yi calling for an immediate ceasefire in Trump’s Operation Epic Fury against Iran, which risks wider regional conflict.

Wang told Russia’s Foreign Minister Sergei Lavrov on a phone call that the “blatant killing of a sovereign leader” and the incitement of regime change were “unacceptable.” This phone call was based on reporting from China’s state-run Xinhua news agency.

The killing of Iranian Supreme Leader Ayatollah Ali Khamenei and the capture of Venezuelan leader Nicolas Maduro have created growing uncertainty around President Trump’s three-day trip to China later this month.

“I worry the U.S. side might use Iran, if it’s going poorly, to delay the trip,” a foreign business executive tracking meeting preparations told CNBC.

The executive added, “I think the risk [of the trip falling apart] is on the U.S. side more than the Chinese side.”

The likely deterioration in Sino-U.S. relations increases the risk of a new round of Chinese restrictions on critical-mineral and rare-earth exports targeting the U.S.

Let’s not forget that Trump has effectively shuttered cheap oil flows from Venezuela and Iran to China (read here). Beijing is infuriated.

Attention has shifted to UAMY’s strategic value as North America’s only operator of antimony smelting capacity. This creates a unique position for the company if imports from Asia are curbed.

UAMY +8% https://t.co/6fegdDj996

— zerohedge (@zerohedge) March 2, 2026

Shares are up more than 13% in the U.S. cash session.

Another potential catalyst (market-based):

Related:

China Introduces New Exports Controls On Antimony, Tungsten And Silver

US Antimony Strengthens Domestic Supply Chain With Montana Mill Purchase

Beyond the risk of rare earth metals becoming a major focal point between Beijing and Washington (again), UAMY may also be rising, as antimony is a critical rare earth used in military production, especially in ammunition and other defense-related materials, as the sheer amount of air-delivered munitions used by U.S. and Israeli forces only suggests weapons production in the U.S. will have to ramp.

Tyler Durden

Mon, 03/02/2026 – 12:20

https://www.zerohedge.com/commodities/whats-igniting-todays-us-antimony-spike-two-key-catalysts

US Government Seizes Over $580 Million In Crypto Linked To Southeast Asian Scams

US Government Seizes Over $580 Million In Crypto Linked To Southeast Asian Scams

Authored by Micah Zimmerman via Bitcoin Magazine,

U.S. Attorney Jeanine Ferris Pirro said federal authorities have frozen and seized more than $580 million in cryptocurrency tied to Southeast Asian scam networks, marking a major escalation in the government’s campaign against cross-border crypto fraud.

The funds were restrained through the Justice Department’s Scam Center Strike Force, a task force formed in November to target cryptocurrency investment and confidence schemes linked to Chinese transnational criminal organizations.

Officials said the groups use social media platforms and text messaging to target U.S. victims and siphon billions of dollars each year. Recent estimates place annual losses to Americans near $10 billion.

“In only three months, we have made significant progress, freezing, seizing, and forfeiting cryptocurrency worth more than $578 million from these criminals,” Pirro said in a statement. She said her office will seek forfeiture through the courts and aims to return funds to victims.

Authorities describe the schemes as “pig butchering” operations, in which fraudsters build relationships with victims before steering them into fraudulent crypto investments. Victims are persuaded to purchase legitimate digital assets and then transfer them to counterfeit trading platforms controlled by the scam networks.

The operations often run out of secured compounds in parts of Southeast Asia, including Burma, Cambodia, and Laos. U.S. officials said some workers inside the compounds are trafficking victims who are forced to carry out scams under threat of violence. In certain areas, revenue generated from scam activity accounts for a large share of local economic output.

The Strike Force is focused on identifying senior figures within the criminal networks, including organizers and money launderers who move proceeds through blockchain transactions and shell accounts. Investigators are tracing funds across exchanges and wallets to disrupt cash-out points and freeze assets before they are dispersed.

The initiative brings together the U.S. Attorney’s Office for the District of Columbia and several Justice Department divisions, along with the Federal Bureau of Investigation, the U.S. Secret Service, and the Internal Revenue Service’s Criminal Investigation unit. U.S. Attorney’s Offices in Rhode Island and the Western District of Washington are also participating.

The Justice Department said the Strike Force will continue targeting infrastructure, financial channels, and leadership structures tied to the fraud networks.

Crypto crime hit $154 Billion last year

Data from Chainalysis shows illicit crypto addresses received at least $154 billion in 2025, a 162% year-over-year increase, with sanctioned entities driving much of the surge. Nation-states including Russia, Iran, and North Korea played an outsized role, leveraging blockchain infrastructure for sanctions evasion, money laundering, and large-scale thefts.

Stablecoins accounted for 84% of illicit transaction volume, the report said.

The report also highlights the expansion of Chinese money laundering networks offering “laundering-as-a-service” and other full-stack illicit infrastructure. Although illicit activity still represents less than 1% of total crypto volume, the scale and geopolitical dimension of the activity pose rising risks for regulators, law enforcement, and national security.

Tyler Durden

Mon, 03/02/2026 – 12:00

Rep. Ted Lieu Spreads Bizarre Conspiracy In Congressional Hearing

Rep. Ted Lieu Spreads Bizarre Conspiracy In Congressional Hearing

Years ago, Rep. Ted Lieu (D., Cal.) demanded that “Facebook should do more internally to regulate fake news and point out fake news.”

This week, he finally made his case for such private censorship. Lieu went full conspiracy theorist during a congressional hearing this week, leaving many gobsmacked. Lieu’s rave about the alleged murder of a child made the National Inquirer look like the Bulletin of the Atomic Scientists.

In an age of rage, Lieu knows that you must go louder and bigger to be heard above the mob. Facts are no passé and Lieu is known for sensational claims like claiming that “Trump is broke.”

At a House Judiciary Committee hearing on the Epstein files, Lieu won the race to the bottom with his colleagues in making outrageous, unsupported claims. It was a moment reminiscent of the recent face-planting by Rep. Ro Khanna (D., Cal.) in disclosing the names of powerful men shielded by the Administration in the scandal. (Four had no connection to Epstein).

He suggested that Trump not only abused a minor, but that she was later bumped off to keep her from speaking. What Lieu does not inform the public is that his blockbuster disclosure was based on the unverified account of an anonymous man, who worked as a limo driver in 1995.

The bizarre account claimed the driver picked up Trump and overheard him on the phone with someone called “Jeffrey” and made references to “abusing some girl.” The driver said that he wanted to pull over and “hurt him”.

Driver Dan Ferree has self-identified as the source referenced by Lieu.

Ferree reportedly has posted hundreds of politically anti-Trump and extreme memes to his Facebook account, including a recent image of Trump in what appears to be a casket. He has also reportedly claimed that he was stalked by Trump associates.

In a defamation case, Ferree would be difficult to pass off as a credible source for a publication. The use of such sources is a familiar tactic in Washington. During the Chandra Levy scandal, politicians and pundits piled on Rep. Gary Condit (D., Cal.) as the presumptive murderer of the congressional intern. The source cited by Vanity Fair’s Dominick Dunne turned out to be a “horse whisperer” in Dubai who said that he had heard Condit arranged for her murder. (Condit was later cleared in the case).

Ferree is only marginally better than a horse whisperer as a source of Lieu. Ferree told the FBI that he met a young girl who told him she had been raped by Trump and Epstein at a “fancy hotel.” He claimed that the young girl was later found with her head “blown off.” He said that, while the officers at the scene thought it was murder, the coroner later ruled it a suicide. There was no proof of such a case.

It appears that Lieu knew or suspected that the source of the allegation was unhinged or unreliable because he later re-posted only two of the three pages of the statement to the FBI. The third page included other bizarre claims about the Oklahoma City Bombing and a drunk Hillary Clinton.

Lieu decided it was best to withhold the third page and the details of a raving, drunken Hillary Clinton and an effort to frame an innocent man for the Oklahoma bombing. It seems that he was not aggrieved that the FBI did not investigate that part of Ferree’s allegations.

Nevertheless, at an earlier event, Lieu declared:

“Why are Republicans so interested in Bill and Hillary Clinton? It’s because they’re trying to distract from the fact that Donald Trump is in the Epstein files thousands and thousands of times. In those files, there’s highly disturbing allegations of Donald Trump raping children, of Donald Trump threatening to kill children.”

What is striking is how so many politicians supporting the crackdown on disinformation on the right are purveyors of such disinformation. From the Russian conspiracy hoax to the flogging of migrants by Border agents, members and the media have regularly spread false accounts with impunity. It is not considered disinformation if it appears on BlueSky or MS NOW.

The intentional omission of the third page of the allegation puts this disinformation effort in a particularly menacing light. This was not some hair-triggered posting that failed to research the underlying story. This was a knowing effort to later re-post the sensational allegation while removing a third of the document that undermined the credibility of the source.

Indeed, while questioning why the FBI (including during the Biden Administration) failed to pursue this allegation, Lieu left out the part indicating that the source was utterly unreliable.

As an impeachment manager, Lieu condemned Trump over his “exhortations [and] the President’s sustained disinformation. We’ve seen a president stoking fears amidst these crises.” He demanded that Trump be removed from office based on that allegation of disinformation and inflammatory rhetoric.

Lieu knew that in our post-truth political environment, it really does not matter if an allegation is untrue. He is feeding a rage addiction among voters who ache for a steady stream of such outrageous claims. He is part of a trend that I have called the “new Jacobins” in Rage and the Republic, establishment figures who are pandering to the mob in seeking to ride the wave of rage back into power.

It was not long ago that Democrats and the media tore into members suggesting that the Clintons were involved in the suicide of key aide Vince Foster. The difference is that there was an actual body in that base. Lieu shows little concern over spreading a conspiracy theory based on an unestablished death raised by a driver who coupled his allegations with other wild claims about Hillary Clinton and the Oklahoma bombing.

It has long been accepted that “politics ain’t beanbag,” but Lieu shows that it is now simply bonkers.

Jonathan Turley is a law professor and the author of the New York Times bestselling “Rage and the Republic: The Unfinished Story of the American Revolution.”

Tyler Durden

Mon, 03/02/2026 – 11:20

https://www.zerohedge.com/markets/rep-ted-lieu-spreads-bizarre-conspiracy-congressional-hearing

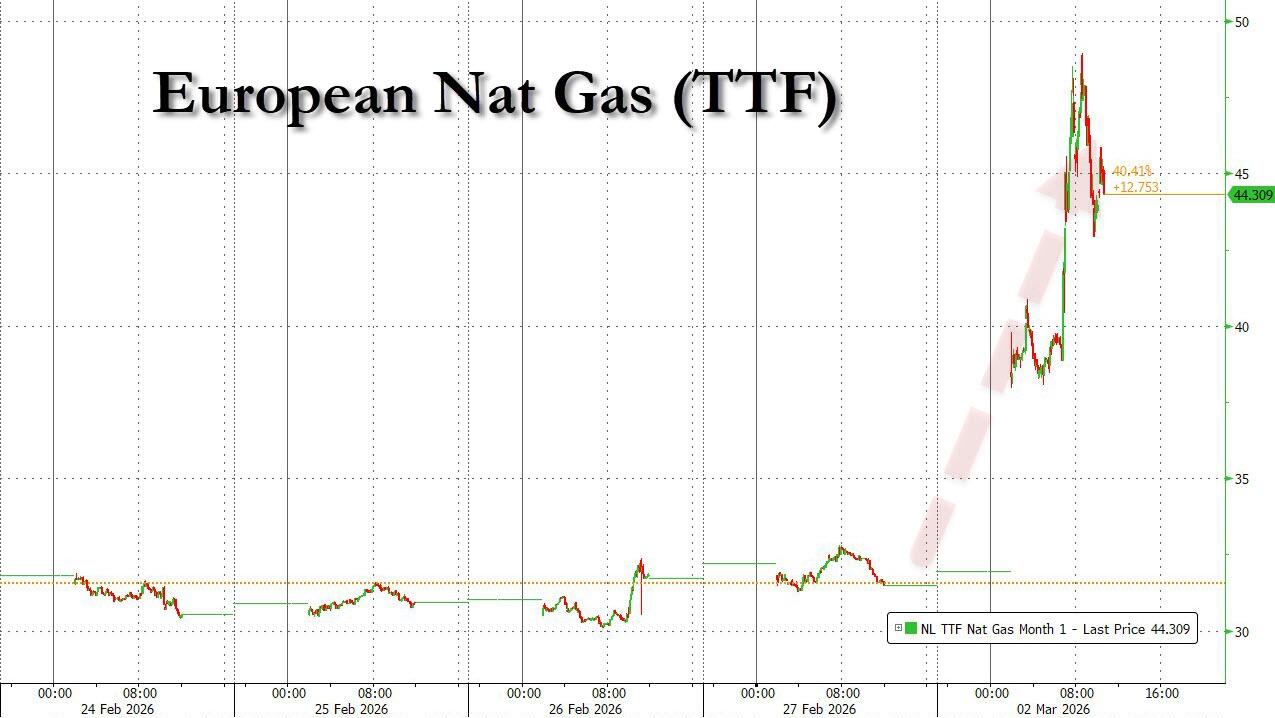

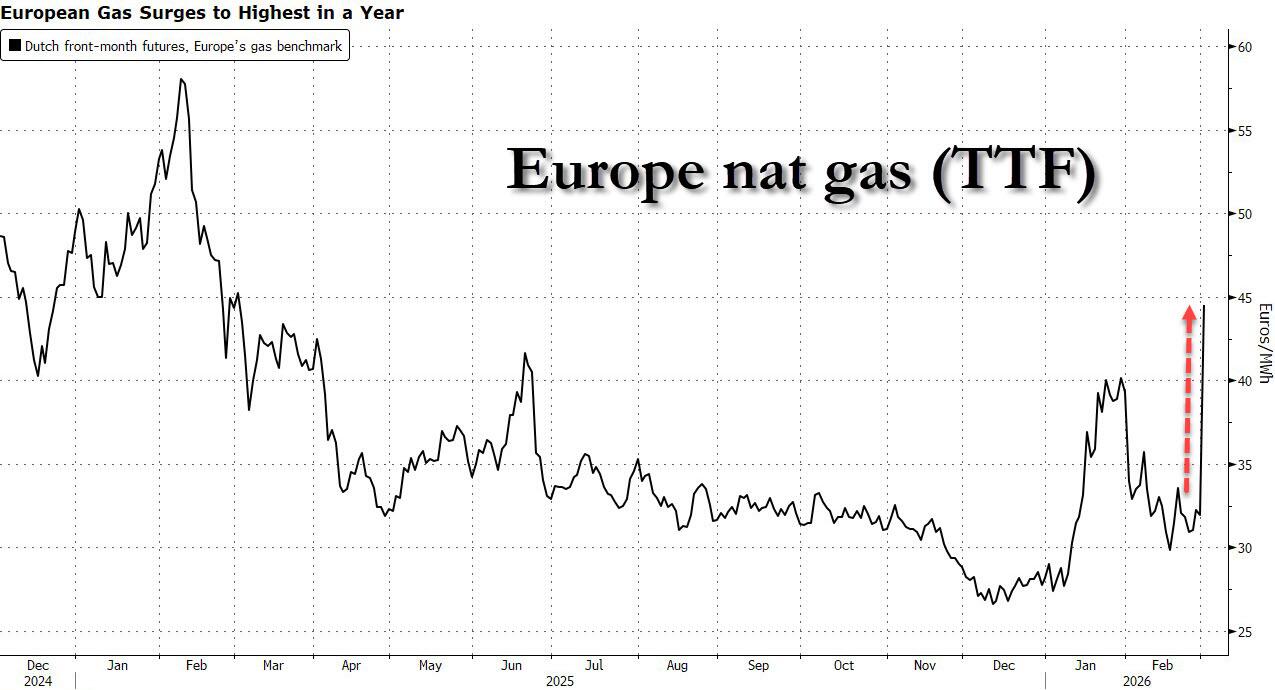

European Gas Prices Soar 50% After Qatar Shuts World’s Largest LNG Export Plant

European Gas Prices Soar 50% After Qatar Shuts World’s Largest LNG Export Plant

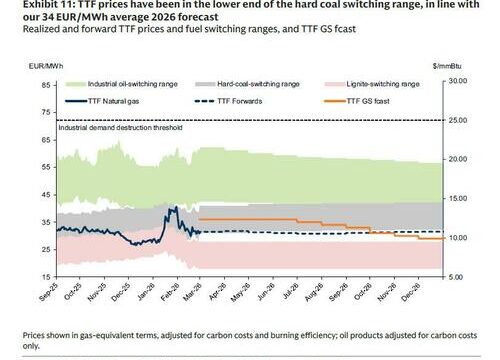

In its scenario analysis of how the Iran war could impact energy markets, Goldman laid out a section dedicated to nat gas, and specifically LNG, which like oil, is one of the commodities that is especially reliant on prompt passage through he Straits of Hormuz to reach its destination.

Specifically, unlike oil which Goldman calculated had already priced in substantial war risk premium, “European gas (TTF) and spot LNG (JKM) prices have embedded little-to-no risk premium until this past Friday” and so, the bank saw “significant upside risk to prices from a potential sustained disruption of LNG supply through the Strait of Hormuz. In a scenario where flows halt for one month, we think it is likely that TTF and JKM could approach 74 EUR/MWh ($25/mmBtu) — 130% above current levels — a threshold that triggered large natural gas demand responses during the 2022 European energy crisis.”

Here we go again: Europe among most exposed to Hormuz, with Goldman warning of massive 130% upside risk for European (TTF) gas prices, potentially hitting 74 EUR/MWh, if LNG flows are blocked https://t.co/yD07qFkNk4

— zerohedge (@zerohedge) March 2, 2026

Below we excerpt the key sections from the must read report (especially to European energy traders as we will discuss in a bit).

Q10. How much risk premium has been embedded in European gas prices?

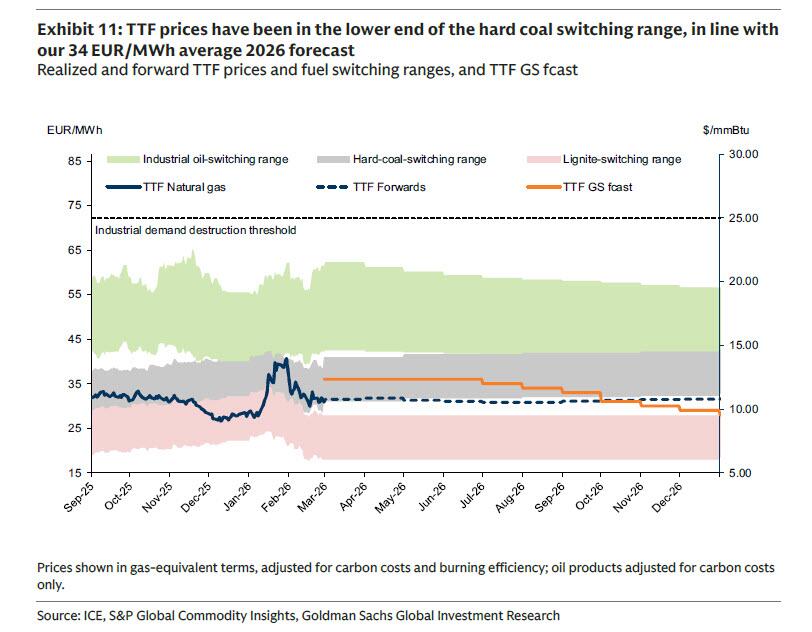

Differently from oil, we believe that until this past Friday, European natural gas prices had embedded little-to-no risk premium associated with Iran-related geopolitical risks. Specifically, TTF has been pricing in the bottom half of our estimated hard-coal-to-gas (C2G) switching range for the past month, modestly below our 36 EUR/MWh March 2026 TTF forecast (Exhibit 11). Once accounting for the recent sell off in carbon emission prices to below the 80 EUR/t embedded in our TTF price forecast, worth 2.0-2.5 EUR/MWh in gas-equivalent terms, prompt gas prices are still largely in line with our view that TTF needs to be in this C2G switching range to help manage NW European gas storage to above 80% full by end-Oct26, given that current inventory levels remain well below average. That remains our view, and we maintain our 34 EUR/MWh balance-of-the-year TTF price forecast.

Q11. What are the risks to global gas prices from this weekend’s developments in the Middle East?

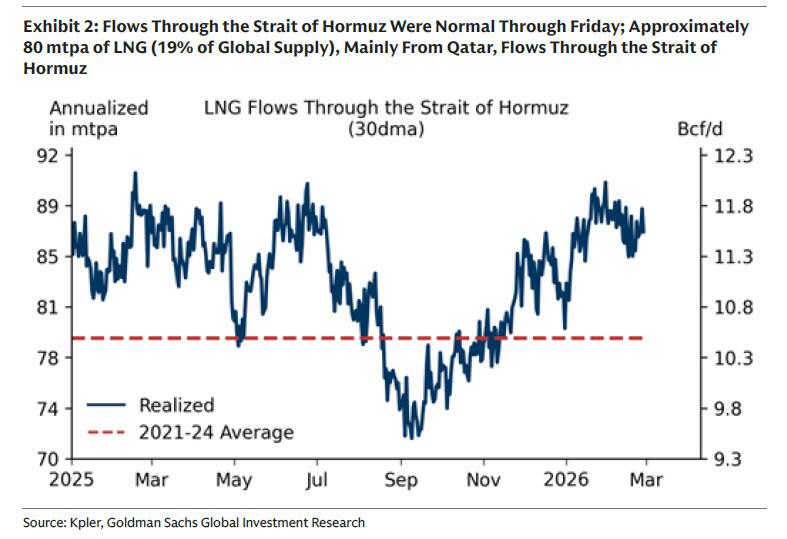

We see significant upside risk to European gas and global LNG prices. The most significant impact to global gas markets would come from a potential disruption of the approximately 80 mtpa (302 mcm/d or 11 Bcf/d, 19% of global LNG supply) of LNG that typically flow through the Strait of Hormuz (Exhibit 2), which could potentially arise from an escalation of the ongoing conflict.

Specifically, in a scenario where LNG flows through the Strait are fully halted for one month, we estimate a resulting tightening of NW European gas storage equivalent to 8% of capacity. Our fuel switching models suggest that European gas prices would need to maximize both switching into hard coal and into oil products by pricing at or above distillate fuel price levels for over three and a half months to offset it. At current oil prices this would imply TTF essentially doubling to 62 EUR/MWh[10] ($21/mmBtu). Given that oil prices would also likely rally in this scenario, it is likely that TTF could approach the 74 EUR/MWh ($25/mmBtu) threshold that triggered large natural gas demand responses during the 2022 European energy crisis.

A hypothetical longer disruption of natural gas supply transit through the Strait of Hormuz lasting more than two months would likely lift European natural gas prices above 100 EUR/MWh ($35/mmBtu) to trigger more significant global gas demand destruction given the increased difficulty for the market to fully offset such a tightening shock ahead of the next winter.

See “Goldman’s Commodity Desk Lays Out The Oil Price Scenarios From Iran War” for more details).

Well, for once Goldman’s commodity research desk was spot on… and very quickly at that, because just one day later, TTF shot up as much as 50%, sparking chaos across Europe’s energy markets in a deja vu moment of the start of the Ukraine war 4 years ago. Dutch front-month futures, Europe’s gas benchmark, traded 46% higher at €46.77 a megawatt-hour by 2:31 p.m. in Amsterdam. That’s the highest level since February 2025.

Qatar’s Defense Ministry said said earlier that two drones launched from Iran had struck facilities in the country, although there were no casualties.

The catalyst behind today’s sharp move is not the full closure of Hormuz, which Iran still claims is passable despite occasional ships in its vicinity randomly catching fire, but because early on Monday, Qatar Energy shut down liquefied natural gas production at the world’s largest export facility after it was targeted in an Iranian drone attack.

QatarEnergy to stop production of LNG

Due to military attacks on QatarEnergy’s operating facilities in Ras Laffan Industrial City and Mesaieed Industrial City in the State of Qatar, QatarEnergy has ceased production of liquefied natural gas (LNG) and associated products.…

— QatarEnergy (@qatarenergy) March 2, 2026

QatarEnergy’s Ras Laffan plant covers about a fifth of global LNG supply and the unprecedented halt now threatens energy security worldwide.

In kneejerk response, European benchmark gas futures jumped the most since the energy crisis in 2022, while tankers had already largely stopped transiting the Strait of Hormuz, a critical artery for global fuel shipments. Needless to say, one direct hit on an LNG ship and the fireworks would be historic.

“The threat to security of supply is here and now,” said Simone Tagliapietra, an analyst at Bruegel. “The extent of it will depend on the duration of the shutdown, but we are now into a new scenario.”

The good news, if only for the US, is that as Goldman notes, there is “limited upside risk to US natural gas prices.”

Bloomberg notes that while Asian countries buy most of the LNG shipped from the Middle East, a disruption will increase competition for alternative supplies pushing up prices worldwide, including in Europe.

European gas prices are also rallying as storage inventories are unusually low, and the region needs to import large volumes of LNG this summer to refill them ahead of next winter. While the intraday surge is the biggest since Russia’s invasion of Ukraine four years ago, benchmark prices are only at a one-year high because regional supplies haven’t been directly disrupted and traders are still assessing how long the conflict will last.

As we discussed yesterday, the key question for traders is how long the disruption will last: the longer, the higher prices will rise. Even if the US boosts LNG production, it’s unlikely to be enough to offset supply from Qatar in the near-term. QatarEnergy is scheduled to start its Golden Pass expansion project in the US in the coming weeks but the facility won’t be at full capacity until next year.

Gas trade disruptions in the Middle East could also eventually raise spot LNG demand from Turkey, according to BloombergNEF, as it imports pipeline fuel from Iran.

Late on Sunday, Trump said the bombing campaign against Iran could last for weeks; The conflict continues to deepen, with blasts heard across Israel, Saudi Arabia, Qatar and the United Arab Emirates, as states intercepted Iranian missiles launched in response to US-Israeli strikes.

Tyler Durden

Mon, 03/02/2026 – 11:02

Trump’s Strategy Is A High Risk-High Reward Gamble

Trump’s Strategy Is A High Risk-High Reward Gamble

By Rabobank

The New Age Of Empires

The U.S. and Israel attacked Iran on Saturday morning, and not a ‘one-and-done’ strike aimed at more negotiations. Rather, it’s an operation to destroy Iran’s nuclear program remnants, its ballistic missile production and stockpiles, its navy, and to back *regime change*.

Both the U.S. and Israel are calling on the Iranian people to rise up as they physically remove the Iranian Revolutionary Guards Council (IRGC) and Basij religious police. That said, it’s up to the Iranians and them alone.

Iran has already been decapitated, politically: Supreme Leader Khamenei is dead, as is much of the government and IRGC leadership – though new leaders are already emerging. The Islamic Republic has been smashed militarily: Israel and the U.S. have near total control of its skies to strike targets at will.

Nobody is stepping in to help Iran militarily now that the shooting has started. Once again, BRICS as an anti-US force is shown to have no mortars supporting it.

Needless to say, it is risk-off in markets this morning. The dollar is surging, high-beta currencies are offered, spot gold is up ~2%, bond yields are tumbling, US equity futures are pointing toward losses of 1% or more, and Brent crude has surged by ~9.2% to $79.60/bbl (and rising). ICE gasoil prices are up ~13% and fertilizer flows are likely to be disrupted both directly and through natural gas’s role as a feedstock in production. While yields are falling on risk-off sentiment this morning, all of the above is inflationary, just as it was when Russia invaded Ukraine.

As we have also warned – a fanatical regime fearing itself on the way out tries to burn everything down as it goes. Iranian drones have killed three US soldiers in Jordan and its missiles have hit Saudi Arabia and the Gulf States despite none having allowed the U.S. to use their territory to attack (even if it appears the Saudis were secretly lobbying for it). A number of Gulf states have now said that they reserve the right to act in self defence under Article 51 of the UN Charter, raising the prospect of reciprocal strikes. Iran’s actions are effectively locking the Gulf states tighter into the US alliance.

Europe has been an irrelevance in these events so far. Ursula von der Leyen was lampooned online after saying on Saturday that the EU will get around to holding a meeting about the war on Monday, while the British government – fresh off a devastating byelection defeat characterised by allegations of sectarian voting behaviour – initially barred the US from using its bases for strikes. Britain has since relented and joined with France and Germany to commit to “enabling necessary and proportionate defensive action to destroy Iran’s capability to fire missiles and drones at their source”. That means that the E3’s fortunes are now tied to the US, whether they like it or not.

The way in which these strikes were conducted also tell us something (again) about the state of the world order. In contrast to George W. Bush’s approach prior to the 2003 invasion of Iraq, no attempt was made to rally European allies, no attempt was made to secure the blessing of the United Nations, and no attempt was made to secure the agreement of the US Congress.

That last point has incensed Democrats domestically who point out constitutional requirements that decisions to go to war be made by Congress. The administration will point to Truman in Korea, Reagan in Grenada, Clinton in Kosovo and Obama in Libya as examples where that rule was allowed to bend. Clearly, executive power continues to grow and the United Nations is also seen as a pesky irrelevance.

The critical Strait of Hormuz is currently absent normal oil and LNG cargoes as ships wait to see how much insurance premiums are adjusted upwards. Likewise, the Iranian-backed Houthis in Yemen have claimed they will try to close the Bab-el-Mandeb, another chokepoint for global energy. Iran has already targeted three tankers in the Strait, while the US is labouring to prevent obstructions. Prolonged interruption to flows through this region has huge implications for oil and LNG and every market everywhere if it occurs. Energy is an input to ALL production.

How this plays out will determine the stability of the greater Middle East. Pakistan and Afghanistan are at war, with the former accusing the latter of becoming a “colony of India” and dozens of Pakistanis killed while attempting to storm a US consulate in Karachi. Do two wars combine into rolling regional chaos? Or does U.S. hard power achieve what endless technocratic talk has failed to do for decades?

Moreover, it will decide if Trumpism is a historic success or failure. U.S. voters don’t like inflation or presidents who get into Forever Wars, especially after being elected to end them. They do like easy foreign policy wins that boost U.S. global power and prestige.

So, why did Trump do this now? Because there was a strike opportunity; reportedly, a U.S. fear of an Iranian missile launch; Iran was rearming – China was about to supply it with new advanced missiles; India’s Modi had just talked up an alliance with Israel; and above all as the attack on Iran is an essential part of his Grand Macro Strategy to retain 21st century hegemony vs a rising China.

We’ve previously explained that Chinese control of supply chains and rare earths is an U.S. Achilles’ heel. The logical response is to ensure the raw materials China relies on –where it cannot project hard power now and the U.S. can– are in U.S. or U.S.-allied hands. That allows it to exert counter pressure to give it space to reindustrialise. Energy is the obvious candidate, and food is another.

This concept predicted the coup de main in Venezuela. The logic for Iran is clearer given it supplies China with much more energy that Venezuela did. Indeed, this leaves Russia as the main cheap oil vendor to China –strengthening Moscow’s hand in that partnership – but cuts off the flow of Shahed drones and ammunition that Iran was providing for the war in Ukraine. Equally, this latest action likely increases U.S. pressure on Moscow, or encourages further tactical outreach in an effort to isolate China. Is it a coincidence that Zelenskyy now says Putin has accepted the terms of a U.S. security guarantee for Ukraine?

There are parallel parts of the Trump plan in play. If Iran is flipped, it opens up the India Middle East Europe Economic Corridor (IMEC) that ties India’s growing economy to the West’s via the Middle East’s energy – with no role for China and the Belt and Road initiative effectively subverted. This would be impossible to achieve if Iran continued to play spoiler. Still, the Trump strategy is a high risk-high reward gamble. There is no safety net if the US doesn’t manage to land this manoeuvre.

If we see quick regime change, even just via a changing of the revolutionary guard as in Caracas, Trumpism will be entrenched. Most U.S. voters will appreciate the win; oil prices will fall and stay low; and all Middle Power ‘strategic autonomy’ alternatives to US hard power will be revealed as an irrelevance. The Trump focus can then swing back to reindustrialisation and affordability as the midterm elections approach.

The huge ‘what if?’ would be China immediately escalating in Asia vs a depleted U.S. military. Beijing has substantial oil reserves while the U.S. doesn’t yet have large rare earths equivalents – and its industrial capacity is still in no state to challenge China in a protracted confrontation. Beijing pursuing such a stratagem looks unlikely if US deterrence is maintained, but could the impending Trump-Xi summit fall through?

If we see a U.S. win but a chaotic Iranian collapse that opens the door to regional instability and/or a clash between U.S. allies Turkey and Israel as they jockey for power. This would be very bad for the US’s geostrategic ends. U.S. voters may not notice unless oil rises again, but IMEC will stumble and the U.S. won’t be able to walk away from the Middle East to focus on the Indo-Pacific. It also won’t be able to focus domestically as required. Anti-Trump Middle Powers would take no comfort from that backdrop.

If we see a U.S. and Israeli strategic defeat —Iran is aiming to drag this fight out until the U.S. and Israel are exhausted: as with Hamas, sheer survival is seen as victory— Trumpism will suffer both electorally and geopolitically: its grand macro strategy will unravel, to China’s advantage. That’s again not a world where rules-based actors do well; very far from it.

In short, how this plays out will determine not just the inflation direction short term but the stability of the greater Middle East and potentially further afield. Failure will ensure chaos both regionally and globally. Success will entrench the ascent of unilateral hard power over impotent multilateral gabfests.

Welcome to the new age of empires.

Tyler Durden

Mon, 03/02/2026 – 10:30

https://www.zerohedge.com/markets/trumps-strategy-high-risk-high-reward-gamble

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}