Category: News

Mexico Truck Production Plunges 50% In February As US Exports Slow

Mexico Truck Production Plunges 50% In February As US Exports Slow

By Noi Mahoney of FreightWaves

Mexico’s heavy-vehicle industry posted sharp year-over-year declines in production, exports and sales in February, signaling continued weakness across the country’s truck manufacturing sector.

Mexico’s National Institute of Statistics and Geography (INEGI) reported that 6,974 heavy vehicles were produced in February, a 49.1% decline compared to the same month in 2025. Exports also fell, with 7,849 units shipped abroad, a 32% drop year over year.

The declines also offer a window into the broader North American freight cycle. Mexico is a key production hub for tractor-trailers used by U.S. fleets moving goods across the U.S.-Mexico border. When freight demand softens or carriers delay fleet upgrades in the U.S., Mexico’s truck factories and export volumes often move in tandem.

Domestic demand also weakened significantly. Retail sales totaled 2,303 units in February, down 38.9% from a year earlier, while wholesale sales reached 1,836 units, a 27.3% decline compared with February 2025.

For the first two months of 2026, the industry produced 13,767 heavy vehicles, representing a 50.5% decline from the same period last year, while exports totaled 12,925 units, down 42.6% year over year.

Domestic truck demand continues long slide

Industry officials say the downturn reflects weakening demand in Mexico’s domestic trucking market, which has now posted more than a year of declines.

Cristina Vázquez, coordinator of economic studies for the Mexican Association of Automotive Distributors (AMDA), said the market has been in a prolonged contraction.

“With the results released today, we have accumulated 14 consecutive months of decline in the Mexican market in year-over-year terms,” Vázquez said during a news conference on Tuesday.

Retail sales in February totaled 2,303 heavy vehicles, nearly 39% fewer than the same month in 2025, reflecting a slowdown after record demand in 2024.

Vázquez said weakening investment trends are also weighing on truck purchases.

“The fixed gross investment indicator — particularly machinery and equipment — has been in negative territory for more than a year,” she said. “That sends a very relevant signal about confidence in the economic environment and the willingness of companies to invest in capital assets such as heavy vehicles.”

Production slump spreads across truck segments

Manufacturing declines were widespread across the heavy truck sector.

Of the 6,974 heavy vehicles produced in February, about 6,739 were cargo trucks and tractor-trailers, while 235 were passenger buses, according to figures presented during the news conference.

Cargo vehicles account for the vast majority of Mexico’s heavy-vehicle production, representing more than 97% of total output during the first two months of 2026.

Exports still dominated by U.S. market

Despite the sharp annual decline, exports rebounded slightly compared with January.

Mexico exported 7,849 heavy vehicles in February, up more than 50% from January, according to data from Mexico’s National Association of Bus, Truck and Tractor-Trailer Producers (Anpact).

Alejandro Osorio, director of public affairs and communication at ANPACT, said the month-to-month improvement offered cautious optimism.

“These are incipient but encouraging signs in the behavior of exports,” Osorio said during the news conference.

However, exports remain significantly lower than a year earlier. The U.S. accounted for 91.3% of shipments in February, followed by Canada (5.7%) and Colombia (2.6%).

The 16 members of Anpact in Mexico are Freightliner, Kenworth, Navistar, Hino, International, DINA, MAN SE, Mercedes-Benz, Isuzu, Scania, Shacman Trucks, Foton, Cummins, Detroit Diesel, Daimler Buses Mexico and Volkswagen Buses.

Osorio said the industry is navigating a volatile global environment that continues to affect demand.

“The industry is facing a complex environment marked by adjustments in domestic demand and volatility in international markets,” he said. “Strengthening competitiveness and recovering the internal market will be key for the sector going forward.”

Freightliner was the top truck producer and exporter in Mexico in February, producing 5,538 trucks, a 32% year-over-year decline. The truck maker exported 5,264 units during the month, a 31% year-over-year decrease.

International Trucks Inc. was the No. 2 producer and exporter during February, manufacturing 307 trucks, a 91% year-over-year decrease. The truck maker’s exports fell 31% year-over-year to 2,251 units during the month.

Used truck imports cited as industry concern

Industry representatives also warned that rising imports of used trucks from the U.S. are undercutting new-vehicle sales in Mexico.

Osorio said the imbalance between new and used truck purchases has become a major distortion in the market.

“For every 100 new heavy vehicles sold in Mexico, about 64 used trucks enter the country,” he said, warning the trend is harming domestic manufacturers and transport companies.

Older imported trucks also raise environmental and safety concerns, he added, because many units arriving in Mexico have already logged hundreds of thousands of miles in the U.S.

Industry outlook uncertain

Guillermo Rosales, executive president of AMDA, said the heavy-vehicle sector is facing multiple economic headwinds, including geopolitical uncertainty and fuel price volatility.

“We are living through a period of tariff volatility and also volatility in fuel prices derived from international conflicts,” Rosales said during the briefing.

Despite the slowdown, Rosales said the industry expects demand to eventually stabilize as freight activity improves.

“The heavy-vehicle industry established in Mexico has historically relied on the recovery of both the domestic and external markets to return to normality,” he said.

Industry leaders say the outlook for the remainder of 2026 will depend heavily on freight demand, investment trends and cross-border trade activity across North America.

Tyler Durden

Mon, 03/16/2026 – 11:20

https://www.zerohedge.com/economics/mexico-truck-production-plunges-50-february-us-exports-slow

Woke Celebrities Applaud Themselves At Oscars As Hollywood Burns

Woke Celebrities Applaud Themselves At Oscars As Hollywood Burns

There is something rather uncomfortable about the Hunger Games aesthetics of Hollywood and the Oscars these days. The pomp is tinged and the glamour faded. The glitter and velvet curtains no longer hide the stinking rot that hides underneath. The fact that a bunch of washed-up and histrionic celebrities are still swimming in the fantasy that they matter is simultaneously alarming and hilarious.

Most of the world is celebrating the ongoing demise of Tinseltown, certainly after a long decade of endless woke propaganda. This includes blatant attempts to indoctrinate children with LGBT ideology. Bombarding the public with insufferable feminist prattle and “girl boss” delusions. Open discrimination against white people through DEI policies and race swaps of almost every significant white character in every franchise imaginable.

As a result, Hollywood is dying. According to recent numbers, Hollywood productions have imploded by 50% or more since 2023. Even covid was not able to destroy the movie industry the way wokeness did. In fact, it was the pandemic that allowed Hollywood to dismiss their dwindling numbers through 2023, but that scapegoat is now gone.

From 2019 to 2025, total box office receipts adjusted for inflation have plunged by 40% and audience numbers are cut in half. The bottom line? Get woke, go broke. No one wants to buy what the leftist film industry is selling. Yet, they continue onward as if they are still American royalty, ignoring their abject failures and spouting their political opinions as if they have influence.

Conan O’Brien hosted the 2026 Oscars event, perhaps with the expectation that his career and audience has not yet completely evaporated.

Conan was quick to poke at conservatives, making fun of the TPUSA alternative Super Bowl half time show.

Conan O’Brien insults TPUSA’s All-American halftime show:

“Tonight could get political, and if that makes you uncomfortable, there’s an alternate Oscars being hosted by Kid Rock. It’s at the Dave & Buster’s down the street.” pic.twitter.com/rfRUucEj6r

— Daily Wire (@realDailyWire) March 16, 2026

The real joke being that any alternative to the Oscars would likely draw a far larger audience. Keep in mind, this is the man who filmed an entire propaganda segment on Haiti because Trump called the island a “shithole”. He argued that it is a “truly beautiful country”, then shared vacation pictures on social media as he consumed flavored drinks in a walled off and fortified beach resort protected by armed security guards.

Conan did redeem himself briefly with a quick pedophile joke…

Conan O’Brien just called out everyone at the Oscars to their faces ☠️ pic.twitter.com/OEcSLz95AP

— Matt Wallace (@MattWallace888) March 16, 2026

But the celebrities could not help themselves…

Jane Fonda fell apart and froze several times during an interview at the Oscars on Sunday.

She insisted on getting political, of course, and she struggled to find her words.

This is honestly quite sad to watch.

Broken minds go woke.pic.twitter.com/girUqaNFWJ

— Paul A. Szypula 🇺🇸 (@Bubblebathgirl) March 16, 2026

Jimmy Kimmel says the United States is a “ridiculous country”

Who else would be more than happy if Jimmy Kimmel left the US?? 🖐️pic.twitter.com/uv3Zyi50xM

— Libs of TikTok (@libsoftiktok) March 16, 2026

Most of the celebrity commentary strayed far from the job of making movies as they struggled to say something profound about Donald Trump and world events. Most of the speeches came out sounding like regurgitated talking points from Bluesky.

Oscars gets slammed online for endless ‘virtue signaling’ from ‘woke’ Hollywood filmmakers.

“When we act complicit when a government m*rders people on the streets…when we don’t say anything when oligarchs take over the media… we all face a moral choice.” pic.twitter.com/zOHj4RVAZJ

— Oli London (@OliLondonTV) March 16, 2026

There was the predictable stage protests against the war in Iran, though, not one Oscar winner thought to condemn the tens of thousands of protesters reportedly killed by the Iranian government last month.

Javier Bardem says “no to war and free Palestine” at the #Oscars, earning a huge round of applause from everyone in the room.

(via ABC/AMPAS) pic.twitter.com/7p3whJzhbm

— Variety (@Variety) March 16, 2026

The big winners for the night included Best Picture for “One Battle After Another”, a film which glorified Antifa terrorism in the wake of numerous attacks by far-left activists. The movie was one of the biggest box office bombs of 2025, losing around $100 million.

Best Actor went to Michael B. Jordan of “Sinners”, a vampire survival movie knock-off of the film “From Dusk Till Dawn”. Such a movie would not normally be included in the Oscars except that it had a majority black cast and includes commentary about segregation. Meaning, it was going to win awards due to DEI default.

Not surprisingly, the vampires of Sinners are mostly white (designed to act as an allegory for the supposed ongoing white exploitation of minorities in America). The horror flick was the only movie of the nominees that made a real profit, bringing in around $100 million. Adjusted for inflation, its performance was still weak compared to the majority of big budget movies pre-2020.

Best Actress went to Jessie Buckley for the film “Hamnet”, a feminist themed story focusing on the wife of William Shakespeare (no one cares).

The only truly good and original film on the list was “Weapons”, an expertly constructed horror story about the mass disappearance of children in a small town. It received little attention beyond a best supporting actress win.

If you have the feeling lately that there is just nothing good coming from the entertainment industry anymore, you’re not alone. The anorexic selections are a consequence of a corpsified media community obsessed more with spreading their political message than making money and staying relevant. The Oscars awards are a depressing reminder of this condition, which is why most people don’t watch them anymore.

Tyler Durden

Mon, 03/16/2026 – 11:05

https://www.zerohedge.com/political/woke-celebrities-applaud-themselves-oscars-hollywood-burns

The Wrath Of Kharg

The Wrath Of Kharg

By Ben Picton, Senior Market Startegist at Rabobank

Brent crude is bid again this morning as markets digest the dump of news over the weekend relating to the Iran war. On the bullish side for crude was the US decision to bomb Iranian military assets on Kharg Island – the Persian Gulf port where up to 90% of Iranian oil exports are typically loaded onto tankers. Announcing the strikes via Truth Social, President Trump was at pains to be clear that oil infrastructure was not targeted, but the implicit threat that it could be is an unsubtle one. Trump later said that the US may conduct further strikes on the island “just for fun”.

News also emerged over the weekend that the USS Tripoli has been redeployed from the Western Pacific to the Persian Gulf. The Tripoli is a light aircraft carrier with a complement of 2,500 marines and an F35B stealth fighter air wing. Speculation is rife that the marines could be used to secure oil infrastructure on Kharg Island, or perhaps to help clear the mountains north of the Strait of Hormuz of Iranian belligerents (the latter seems less likely). Either would be a case of ‘boots on the ground’ and interpreted as a major escalation. Iranian officials have said over the weekend that they would respond in kind to any attacks on their oil infrastructure. Indeed, there were further limited attacks on oil assets of US-aligned Gulf states over the weekend, which may explain the bid tone in Brent this morning and a lift in the forward curve since this time last week.

A bizarre intervention in the war came from Hamas, who called for Iran to cease attacks on regional neighbors. Hamas is well-known as an Iranian proxy, so there is some speculation circulating that this may be an attempt from the Iranian side to begin to engineer an off-ramp. Coupled with news last week that Iran had struck agreements with India and Bangladesh to allow crude cargoes to pass, and comments from the Iranian Foreign Minister over the weekend that the Strait was not closed to anyone other than the US, Israel and their allies, there appears to be some cautious optimism in markets this morning that glimmers of hope for an end to hostilities are emerging. AUD and NZD are both trading higher, spot gold is down to almost $5,000/oz and bitcoin is catching a bid.

However, ‘glimmers’ is the operative word. While Hamas was calling for Iran to end strikes on neighboring states the Houthis (another Iranian proxy) were giving signs that they are ready to escalate against shipping being diverted into the Red Sea to load crude cargoes at the Saudi port of Yanbu. Disruptions to Red Sea shipping – which the Houthis have proven adept at over the years – would close off the release valve of the Saudi East-West pipeline that is capable of redirecting 5-7mn bbl/day to offset the ~18-20mn bbl/day supply interruption.

There is also the fact that South Korea and Japan – both major destinations for Gulf energy cargoes – would likely be considered US allies and therefore not allowed to receive crude shipments under the terms of the Iranian toll road. Trump himself has rebuffed suggestions of a ceasefire over the weekend, saying that he is not yet ready to end the war because the terms offered by Iran are not good enough. Iranian officials deny that any terms have been offered at, beyond the US’s withdrawal from the Middle East and payment of reparations. No wonder Trump isn’t keen. Prediction markets are this morning implying odds of a ceasefire before month end of just 14%, down from 21% on Friday.

There are glimmers of hope in other areas. The Wall Street Journal is this morning reporting that the United States is set to announce the formation of an international coalition to provide naval escorts to tankers transiting Hormuz. Some commentators on X have already observed that this would run counter to Donald Trump’s recent shot at UK PM Starmer, where he said that the US doesn’t need allies who only turn up after the war is won (the British might have their own thoughts on allies who arrive late to wars). Nevertheless, there does seem to be a plan developing, though both South Korea and Japan have signalled caution about deploying warships to the Gulf as China resumes military exercises around Taiwan after a 10-day hiatus.

Speaking of China, US Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer are currently meeting with Chinese officials, including Vice Premier He Lifeng, in Paris to discuss trade. The talks come ahead of a much anticipated Trump-Xi summit in Beijing on March 31st and are expected to lay the groundwork for that meeting. Early reports suggest that the American side asked China to buy more Boeing aircraft, and US coal and gas. With Qatari liquified natural gas exports currently out of the market, and the Chinese economy approximately 50% dependent on imports for its domestic needs, it should be an easy sell. Japan’s Industry Minister has also recently reached out to Australia to urge a ramping up of LNG production, though this will take time and is sure to face opposition from environmentalists in Australia.

The timing of the Trump-Xi meeting is interesting. Trump will be headed to Beijing with Chinese influence having recently been ejected by America power in Venezuela, Cuba and the Panama Canal. The strikes on Kharg Island – which is the main port of origin for a large slice of China’s oil imports – also raises the prospect of Chinese influence in central Asia being severely curtailed. The US is a mostly self-sufficient net energy exporter who suddenly occupies several key maritime chokepoints for Chinese energy imports. The message to Beijing couldn’t be more clear: if you attempt to leverage rare earth supply chains against US interests, the US will leverage energy supply chains against Chinese interests. Regular readers would be aware that we have argued the logic of this for the last 18 months.

So, again we see that economic statecraft is employed to create supply chain pressure to get what you want. To appreciate this disruptive power fully, it must be recognised that the Iran crisis goes far beyond energy and the supply shock will reverberate through everything from petrochemicals, to agriculture to pharmaceuticals and beyond. China’s industrial dominance therefore becomes an Achilles heel in a global economic shock. For a comprehensive accounting of the likely impacts, see this excellent piece produced by the RaboResearch Food and Agribusiness team.

Trump wants Hormuz open again. Xi wants guarantees that Gulf oil will continue to flow to Chinese refineries, Chinese industrial producers will have markets to sell to, and Chinese consumers will have food to import. Trump thinks he has the upper hand in this negotiation and so on Sunday night he told media that he could seek to delay the Beijing summit and that he expected China to help open the Strait of Hormuz. He is playing hard to get, and trying to put all of the pressure on Xi to force a resolution. To paraphrase Nixon’s Treasury Secretary John Connally: “it’s our war, but it’s your problem.”

So, could the upcoming summit be the moment where we see Beijing issue the directive to its allies in Tehran to end the blockade? For Xi it may be a choice between that, or suffering the wrath of Kharg on the Chinese industrial economy.

Tyler Durden

Mon, 03/16/2026 – 10:45

Nano Nuclear Progresses HALEU Transport Package

Nano Nuclear Progresses HALEU Transport Package

Nano Nuclear released a notable update this morning for achieving conceptual design milestones on its proprietary, optimized High-Assay Low-Enriched Uranium (HALEU) transportation package, developed in partnership with German nuclear logistics heavyweight GNS.

Through subsidiary Advanced Fuel Transportation (AFT), the company has nailed down two optimized payload baskets capable of hauling multiple advanced fuel forms including uranium oxide, TRISO, uranium-zirconium hydride, uranium mononitride, and even molten salt reactor fuel. All of it was run through an NRC Quality Assurance program, with initial analyses indicating full regulatory compliance. Next up is full regulatory engagement and certification.

The tech builds on Nano’s exclusive license for a high-capacity basket originally designed by Idaho National Lab. Jay Yu, founder and chairman, called it “an important step toward building the infrastructure needed to support the deployment of advanced reactors”.

As we covered last year, Nano broke ground on its Kronos microreactor facility at the University of Illinois Urbana-Champaign, complete with state backing and a manufacturing/R&D site announcement from Governor Pritzker. We followed up with coverage of their engineering firm partnerships and the founder’s Shawn Ryan Show appearance touting laser enrichment ambitions. The Illinois project has been the headline (and only) act, until now.

It’s a mild surprise: while the reactor side hogs the press and investor imagination, the transport business segment has been making tangible development progress. In an industry starved for HALEU shipping solutions, this could become a revenue driver years before any microreactor fires up commercially.

Nano’s vertical-integration bet with enrichment, fuel fab, transport, and reactors, looks a touch less aspirational today.

Tyler Durden

Mon, 03/16/2026 – 10:20

https://www.zerohedge.com/energy/nano-nuclear-progresses-haleu-transport-package

BYD Shares Soar Most In 13 Months As Chinese EV Push Into Americas Accelerates

BYD Shares Soar Most In 13 Months As Chinese EV Push Into Americas Accelerates

Shares of Chinese EV maker BYD surged the most in 13 months after a report that its factory in Bahia, Brazil, a former Ford Motor plant, secured export orders for about 100,000 vehicles from Argentina and Mexico. This development suggests BYD’s strategy to localize production in South America is still in its early stages and set to flood the continent with Chinese EVs.

Bloomberg quoted Macquarie Capital analyst Eugene Hsiao, who said the local Chinese media report about BYD’s Brazil factory receiving large orders from Argentina and Mexico suggests that “this is positive for the broader BYD thesis, which is that overseas sales will become the core growth and profit driver over time.”

Brazil is BYD’s largest market outside China. The factory in Bahia is critical to the Chinese company’s overseas expansion plans in the Americas. The plant has a capacity to make 150,000 EVs per year.

In BYD’s home market of China, overall sales for the first two months of the year slumped 36% to 400,241 units. Competition in China has intensified as rivalry among domestic brands grows fiercer. However, exports have gained solid traction, with the company now planning to sell 1.3 million cars abroad.

“A higher gas price would potentially drive demand in the European market, which would benefit Chinese automakers that export to that market such as BYD,” Morningstar analyst Vincent Sun said, adding, “For Chinese market, gas bill is not as big a driver to EV demand as in overseas market.”

BYD shares in Hong Kong surged 8% on Monday, marking the largest gain in 13 months, as news of overseas expansion lifted investor sentiment.

The stock was a top performer on the Hang Seng Tech Index, with trading volume doubling to 35.7 million shares. Peers including Nio and Xiaomi climbed more than 5%.

Top BYD headlines (courtsey of Bloomberg):

The Brazil plant has annual capacity of 150,000 vehicles and will increase production to 600,000 vehicles in phases

BYD will launch the premium Denza Z9GT electric vehicle in Europe on April 8, offering up to 800 kilometers range

The new vehicle can charge from 10% to 70% in about five minutes using BYD’s latest fast-charging system

BYD unveiled its second-generation Blade Battery on March 9, promising to charge EVs from 10% to 97% in under nine minutes

BYD is exploring entry into Formula 1 and endurance racing to boost global brand appeal

BYD is actively considering building a manufacturing plant in Canada and keeping options open to acquire a global automaker

For readers heading to Mexico for spring break, one of the first things you may notice after stepping outside the airport terminal is how many BYD vehicles are already on the road. The flood of Chinese EVs is shifting into hyperdrive, and in the Americas, the invasion is already underway.

Tyler Durden

Mon, 03/16/2026 – 10:00

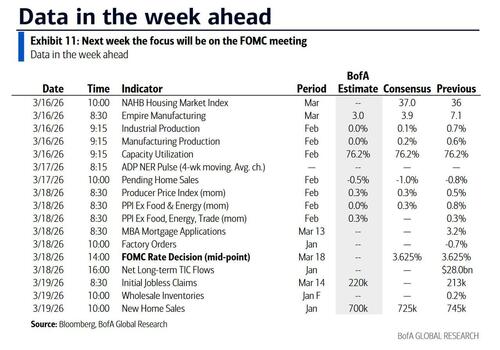

Key Events This Week: Central Banks Galore, PPI, And The War In Iran

Key Events This Week: Central Banks Galore, PPI, And The War In Iran

After Friday’s revelation that it was the first consecutive monthly Friday 13th for 11 years, DB’s Jim Reid writes that today’s nearly-as-impressive revelation is that this week sees the Fed, ECB, BoJ and BoE all meet in a single calendar week for the first time since December 2021. So a “super week” for central banks. All of them will have a very complex backdrop to deal with, shaped by geopolitical risk, volatile energy prices, and unsettled inflation dynamics.

Clearly the Middle East is the center of attention for markets right now, with oil prices fluctuating rapidly depending on the mood of the moment, which in turn is set by rapid burst headlines which are stale by the time the next flashing red headline hits. And since every asset class now reacts to any up or down tick in oil, it leads to cross-asset chaos, to say the least. The bigger problem, of course, is that the longer the conflict lasts, and the higher oil prices rise, the more hawkish central banks will have to be no matter the AI-driven bloodbath in the labor market.

Indeed, while the Iran war is set to dominate the week ahead, we do still have those four big central bank meetings, where all eyes will be on their reaction functions to the war’s impact and the latest oil shock. Starting with the Fed, DB economists expect them to keep rates unchanged this week and think they’ll emphasize elevated geopolitical uncertainty. They only expect minor statement tweaks, including smoothed language on recent labor data (especially given January and February’s conflicting payrolls) and a nod to geopolitical risks, highlighting uncertainty and near-term upside pressure on inflation. Then at the press conference, they think Chair Powell is likely to stress that recent events mainly transmit through financial conditions—particularly oil prices. For now, however, economists think he’ll avoid signalling any meaningful shift in the near term policy outlook.

For the Fed, an important consequence of the conflict is that higher energy prices have begun to feed into inflation assumptions. So DB’s economists have nudged up their headline inflation estimates for this year, and they expect Fed officials to reflect a similar adjustment when they publish their updated Summary of Economic Projections. Indeed, core PCE inflation has registered back-to-back 0.4% monthly increases now, pushing the year-on-year rate to 3.1%, the highest since early 2024. For the dot plot, economists are still expecting it to signal one rate cut this year, although it wouldn’t take much to shift the median dot for 2026. Clearly though, the outlook is going to remain heavily dependent on the oil price. For example, our economists have found that a sustained oil price around $100/bbl would still see the projected tax benefits to consumers from the One Big Beautiful Bill Act outweigh the drag from higher effective energy costs. However, a move toward $150/bbl would pose a more material risk to consumer spending and the broader outlook.

Beyond the Fed, this week’s incoming data is unlikely to materially alter the tone of the meeting. February’s industrial production today is expected to rise by 0.3%, slower than January’s 0.7%, largely due to softer utility output, though oil and gas extraction will be worth monitoring. Otherwise, the regional manufacturing surveys from New York and Philadelphia could reflect some drag from geopolitical uncertainty, with particular attention on capital spending components. And given the recent labor market volatility, Thursday’s initial jobless claims will take on added importance as they fall within the March employment survey window.

Away from the US, this Thursday will bring the ECB, BoE and BoJ meetings, with DB economists expecting all three to leave rates on hold, with the emphasis firmly on guidance rather than action. At the ECB, expect the Governing Council to acknowledge heightened uncertainty and near-term upside risks to inflation, while stopping short of explicitly flagging medium term risks. Also expect a strong reiteration of policy flexibility and a clear message underscoring the ECB’s unwavering commitment to price stability, with officials keen to signal that they stand ready to act to avoid a repeat of the 2022–23 inflation episode.

Then in the UK, DB thinks the MPC will lean into a dovish wait and see stance amid a more clouded outlook following the Iran related energy shock. Expect a less divided vote than in February, with the majority favoring an unchanged Bank Rate, while two members continue to favor a cut. Although DB economists still sees two rate cuts this year, recent developments have pushed back the expected timing.

Over in Japan, the BoJ is expected to maintain its current stance, with attention focused on Governor Ueda’s press conference. While underlying fundamentals could justify an early hike, elevated oil prices and growth risks are likely to temper near term action, and sustained crude prices above $100/bbl would reduce the likelihood of an April move. Meanwhile, other central banks making decisions this week include the RBA (Tuesday; expect a hike), the BoC (Wednesday), the SNB and the Riksbank (Thursday). The latter three are widely expected to see no change in rates.

Finally this week, notable data includes Germany’s Zew survey for March tomorrow and UK labor market data due Thursday. In the geopolitical sphere, President Trump and Japanese PM Takaichi are meeting in Washington, with defence cooperation expected to be the primary topic (see more in our Chief Japan economist’s week ahead here). In Europe, this week’s events include an EU leaders’ summit (Thursday to Friday). And on earnings, the lineup includes Micron, FedEx and Lululemon in the US as well as Tencent and Alibaba in China. See the day-by-day calendar of events at the end as usual for more.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 16

Data: US March Empire manufacturing index, NAHB housing market index, February industrial production, capacity utilisation, China February retail sales, industrial production, home prices, investment, Italy January general government debt, Canada February CPI, housing starts

Earnings: Standard Life

Other: EU foreign affairs council meeting

Tuesday March 17

Data: US March New York Fed services business activity, February leading index, pending home sales, Germany March Zew survey, Eurozone March Zew survey, Canada February existing home sales

Central banks: RBA decision

Earnings: Lululemon, Oklo

Auctions: US 20-yr Bond (reopening, $13bn)

Wednesday March 18

Data: US February PPI, January factory orders, total net TIC flows, Japan January Tertiary industry index, February trade balance, Canada January international securities transactions

Central banks: Fed decision, BoC decision

Earnings: Tencent, Micron

Thursday March 19

Data: US March Philadelphia Fed business outlook, January new home sales, wholesale trade sales, initial jobless claims, UK January average weekly earnings, unemployment rate, February jobless claims change, Japan January core machine orders, capacity utilisation, Eurozone January construction output, Q4 labour costs, Australia February labour force survey

Central banks: rate decisions from the ECB, the BoJ, the BoE, the SNB and the Riksbank

Earnings: Alibaba, Accenture, Enel, FedEx, Vonovia

Auctions: US 10-yr TIPS (reopening, $19bn)

Other: Leaders of US and Japan meet in Washington, European Council meeting (through Friday)

Friday March 20

Data: UK February public finances, Germany February PPI, Italy January trade balance, current account balance, ECB January current account, Eurozone January trade balance, Canada January retail sales, February industrial product price index, raw materials price index

Central banks: China 1-yr and 5-yr loan prime rates, ECB’s Nagel speaks

* * *

Finally, looking at just the US, the key economic data release this week is the PPI report on Wednesday. The March FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM.

Monday, March 16

08:30 AM Empire State manufacturing survey, March (consensus +3.9, last +7.1)

09:15 AM Industrial production, February (GS flat, consensus +0.1%, last +0.7%); Manufacturing production, February (GS +0.1%, consensus +0.1%, last +0.6%); Capacity utilization, February (GS 76.1%, consensus 76.2%, last 76.2%): We estimate industrial production was unchanged in February, reflecting strong auto production but weak electricity production. We estimate capacity utilization edged down to 76.1%.

10:00 AM NAHB housing market index, March (consensus 37, last 36)

Tuesday, March 17

10:00 AM Pending home sales, February (GS flat, consensus -0.7%, last -0.8%)

Wednesday, March 18

08:30 AM PPI final demand, February (GS +0.4%, consensus +0.3%, last +0.5%); PPI ex-food and energy, February (GS +0.3%, consensus +0.3%, last +0.8%); PPI ex-food, energy, and trade, February (GS +0.3%, consensus +0.3%, last +0.3%); 10:00 AM Factory orders, January (GS +0.1%, consensus +0.1%, last -0.7%) : We forecast that factory orders increased by 0.1% in January, driven by a rebound in commercial aircraft orders.

02:00 PM FOMC statement, March 17-18 meeting: As discussed in our FOMC preview, we expect the FOMC to leave the funds rate unchanged at 3.50–3.75%. We expect Governors Bowman, Miran and Waller to dissent in favor of a 25bp cut. The Committee is likely to note in its statement that the war in Iran has increased uncertainty about the outlook and will likely raise inflation and weigh on economic activity in the near term. The Summary of Economic Projections is likely to show changes to the 2026 forecasts in line with our own, including higher core (+0.2pp to 2.7% Q4/Q4) and headline (+0.6pp to 3.0%) inflation, lower GDP growth (-0.2pp to 2.1%), and a higher unemployment rate (+0.2pp to 4.6%). We expect little change in the dot plot, where the median is likely to continue to show one cut in each of 2026 and 2027. We recently pushed the two additional rate cuts in our forecast back to September and December.

Thursday, March 19

08:30 AM Initial jobless claims, week ended March 14 (GS 210k, consensus 215k, last 213k); Continuing jobless claims, week ended March 7 (consensus 1,850k, last 1,850k): We expect initial jobless claims to decline by 3k. Initial claims remain below their average level in 2025H2 and the layoff rate edged down in January, suggesting that nationwide layoffs remain low despite the increase in alternative layoff measures in Q4 of last year.

08:30 AM Philadelphia Fed manufacturing index, March (GS 7.0, consensus 10.0, last 16.3)

10:00 AM New home sales, January (GS -2.0%, consensus -2.7%, last -1.7%): We estimate that new home sales fell by 2.0% in January, reflecting a drag from winter storm Fern.

Friday, March 20

There are no major data releases scheduled.

Source: DB, Goldman

Tyler Durden

Mon, 03/16/2026 – 09:50

https://www.zerohedge.com/markets/key-events-week-central-banks-galore-ppi-and-war-iran

Israel Expects Iran War To Continue At Least Into April, Lebanon Conflict Longer

Israel Expects Iran War To Continue At Least Into April, Lebanon Conflict Longer

The White House has struggled to present the American public and the world with a clear timeline or precise strategy on Operation Epic Fury, but Israel has seemed clearer on signaling it is settling in for a longer war.

Israel is bracing for its war with Iran to stretch well into April, even as officials quietly concede the government in Tehran is unlikely to collapse, according to Israeli media.

Damage from the June war which lasted 12 days, in Bnei Brak, Israel. via Reuters.

This has Israel has expanded its attacks not just to Iran’s oil and energy sites, but more broadly to its defense industrial sector, wanting to see even Tehran’s ability to manufacture new missiles utterly destroyed.

And according to Ynet, “At the same time, the idea of encouraging public unrest inside Iran has not been abandoned, though officials acknowledge uncertainty about how effective such efforts might be.”

“We continue to strike regime targets, mainly in Tehran. We are entering the decisive phase. We are aiming to bring the people out into the streets. It’s not only us – the Americans are also working toward that,” an Israeli official stated.

“Not everything can be controlled, but everything possible is being done to make it succeed. The regime must be weakened as much as possible, including the Basij,” the official added. “We are striking them and killing them in the thousands.”

Israeli officials have further made clear they have assets on the ground, or Iranians who have helped spot IRGC/Basij checkpoint and security locations. Israel’s military has publicized some instances of active strikes on these locations.

As for whether targeting information is actually being communicated by anti-regime Iranians, this could just be Israeli propaganda intent on sowing discord and suspicions among the Iranian populace.

Still, Israeli officials have admitted they are skeptical that street protests alone could topple the Iranian government. Over in Washington, President Trump apparently thought ‘decapitation strikes’ would quickly result in some kind of rapid uprising in the streets and change of government, but that didn’t appear even close to happening.

On the White House’s series of miscalculation as this war is in week three with no signs of an off-ramp, Robert D. Kaplan has written in Foreign Affairs:

The biggest U.S. foreign policy fiascos happened because policymakers were obsessed with regional and global consequences they often could not properly manage, and thus ignored critical conditions on the ground. In Vietnam, U.S. leaders overlooked the history and nature of Vietnamese nationalism; in Iraq, it was sectarianism. Tuchman has encouraged leaders to trust area specialists more than grand strategists or democracy promoters. Sophisticated and specific cultural knowledge, she has observed, is much more useful than metrics and shadowy schemes.

Middle-sized wars often stem from misunderstandings about the place intervention is meant to help. The key, then, is for the intervening country to know what it is getting itself into. This may seem easy, but it can be the hardest part of policymaking. Bringing up cultural matters and differences is tricky because it can easily be misconstrued as prejudice, which pushes people to avoid critical conversations about realities on the ground. But it is such discussions that can keep a superpower out of trouble.

Meanwhile, as far as a timeline, Israeli leaders have admitted that it’s renewed war with Hezbollah is expected to outlast the conflict with Iran. Hezbollah has been launching missiles on northern Israel, while IDF ground forces have moved in, also as Beirut continues to get pounded from the air.

Tyler Durden

Mon, 03/16/2026 – 09:45

Florida Passes Voter ID Bill Modeled After SAVE Act

Florida Passes Voter ID Bill Modeled After SAVE Act

Authored by Jill McLaughlin via The Epoch Times,

The Florida Legislature passed new election legislation modeled after President Donald Trump’s proposed SAVE America Act.

House Bill 991, sponsored by state Rep. Jenna Persons-Mulicka, passed along party lines by a vote of 83 to 31.

“We are the Election Integrity State!” Persons-Mulicka wrote on X after the vote.

Sponsors of the bill moved the effective date to appease critics who feared the new identification requirements would discourage some voters from participating in midterm elections. The new laws won’t take effect until Jan. 1, 2027.

The bill requires Floridians to show proof of citizenship to register to vote, requires a valid photo ID to vote, makes paper ballots the primary method of voting, and bans student IDs as an acceptable voter ID.

Nearly all Florida driver’s licenses and ID cards are Real-ID compliant—a process that already verifies citizenship.

Once in place, the new regulations will also make it a felony for political parties, committees, organizations, and candidates to accept or solicit contributions from foreign nationals for any state elections.

Florida state Democrats voted against the bill, dubbing it the “Show Your Papers Act.”

Rep. Anna Eskamani, a Democrat representing Orlando, said the measure would restrict “all kinds of IDs Florida voters can use.”

“Student IDs and retirement center IDs would no longer be valid; driver’s licenses, state ID cards, military ID, and licenses to carry concealed weapons would still be accepted as proof of voter identity,” Eskamani said in a Facebook post.

The ACLU’s Florida Chapter condemned the measure’s passage, calling it an anti-voter bill.

“These changes are not neutral or harmless—they would fall hardest on low-income voters, students, seniors, women, and Black and brown Floridians,” said Bacardi Jackson, executive director of the ACLU Florida chapter.

“This wave of anti-voter legislation is advancing amid ongoing abuses of power that pose unprecedented threats to American democracy.”

Florida State Rep. Jenna Persons-Mulicka, R-Fort Myers. Courtesy of the Florida House of Representatives

A similar effort by congressional Republicans has stalled for months in the U.S. Senate.

Florida Secretary of State Cord Byrd encouraged Congress to move forward with the SAVE Act after Florida’s bill passed.

“Florida leads the nation in election integrity because we don’t rest on our laurels and are always looking to improve,” Byrd posted on X. “It’s now time for Congress to act on critical election integrity measures.”

Republican Leader John Thune (R-S.D.) has been unable to advance the SAVE Act, despite growing pressure from the public and within his party.

Thune told colleagues on March 10 that he didn’t have the votes to pass the act by employing the talking filibuster. He plans to bring the bill to the Senate floor next week.

Tyler Durden

Mon, 03/16/2026 – 09:30

https://www.zerohedge.com/political/florida-passes-voter-id-bill-modeled-after-save-act

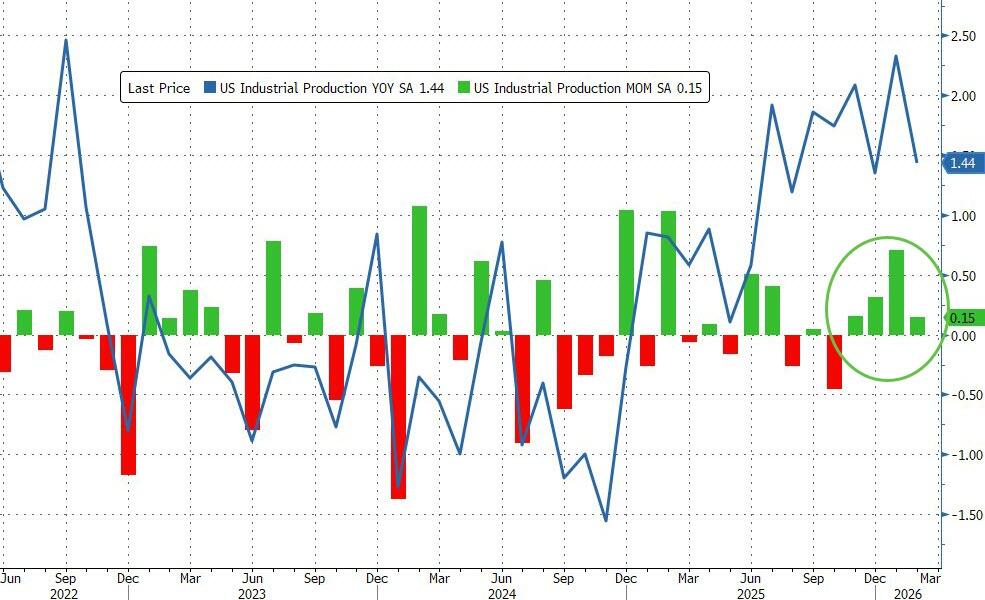

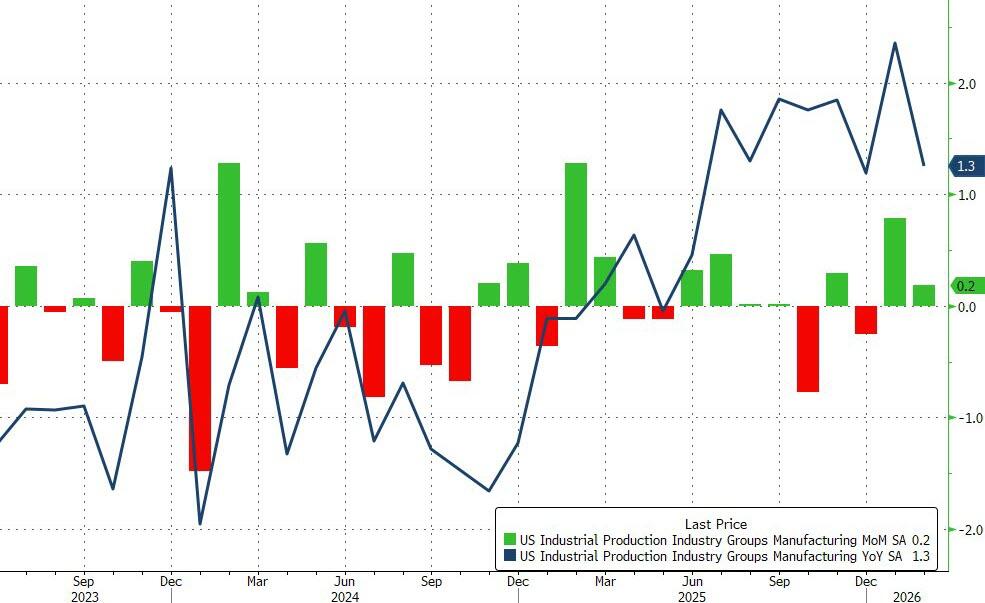

US Industrial Production Rises For 4th Straight Month In February

US Industrial Production Rises For 4th Straight Month In February

After a strong gain in January, US Industrial Production continued to expand in February, rising 0.2% MoM (better than expected +0.1%) – the fourth straight month of gains with Production up 1.44% YoY…

Source: Bloomberg

Manufacturing output also beat expectations, rising 0.2% MoM in February.

Durable manufacturing output edged up 0.1 percent, with mixed results across categories; the index for motor vehicles and parts posted the largest gain, and the index for machinery posted the largest loss.

Nondurable manufacturing output rose 0.2 percent, with gains in the production of chemicals, of plastic and rubber products, and of paper products outweighing declines in the output of petroleum and coal products and of food, beverage, and tobacco products. The output of other manufacturing (publishing and logging) rose 1.3 percent.

Mining output increased 0.8 percent in February, following a 0.9 percent increase in January. The output of utilities fell 0.6 percent in February, reflecting no change in the index for electric utilities and a 4.7 percent drop in the index for natural gas utilities.

Source: Bloomberg

Capacity Utilization printed 76.3 (better than expected)…

…maintaining the positive trend since Trump’s second term began.

Tyler Durden

Mon, 03/16/2026 – 09:23

https://www.zerohedge.com/economics/us-industrial-production-rises-4th-straight-month-february

Starmer Vows UK Won’t Be Drawn Into Wider War In Middle East, Hormuz Crisis ‘Not A Simple Task’

Starmer Vows UK Won’t Be Drawn Into Wider War In Middle East, Hormuz Crisis ‘Not A Simple Task’

British Prime Minister Keir Starmer spoke to President Trump on Sunday night, with Starmer on Monday describing that the two leaders discussed events “in the way that you would expect between two allies and two leaders” and he had a “good relationship” with the US president.

His articulation of an apparently positive and frank talk comes while he trying to dismiss suggestions the relationship with Britain’s key ally had been damaged due to the Iran war.

President Trump has been very clearly making the case that European and NATO countries must back his effort to unblock global oil transit in the Strait of Hormuz

However, Starmer has made clear to his domestic population that the UK won’t be dragged into a wider war with Iran, even as London tries to figure out what role in might play in any US-led Hormuz plan.

“Ultimately, we have to reopen the Strait of Hormuz to ensure stability in the (oil) market. That is not a simple task,” Starmer told reporters.

“So we’re working with all of our allies, including our European partners, to bring together a viable collective plan that can restore freedom of navigation in the region as quickly as possible and ease the economic impact,” he added.

Below is a key line of Starmer’s:

“While we are taking the necessary action to defend ourselves and our allies, we will not be drawn into the wider war,” he said.

But it seems he’s trying to have his cake and eat it too, acknowledging that Britain is on board with trying to piece together a multinational security effort – and yet Starmer has stressed it would not be a NATO-led mission.

According to more of his comments at a Downing street press conference:

The prime minister said the UK, which is considering sending ships and mine-hunting drones to the Middle East, was working with allies on a “viable plan” to reopen shipping lanes. Otherwise energy prices would remain high.

“It’s a discussion; we’re not at the point of decisions yet. It’s obviously a difficult question, that goes without saying, in relation to how you safeguard maritime traffic … But we are discussing that with the US, with Gulf partners and with Europeans,” he said.

He said that while the UK would take “necessary action” to defend itself and allies “we will not be drawn into the wider war”, as concern mounts at home over the prospect of a drawn-out conflict.

“I want to see an end to this war as quickly as possible, because the longer it goes on, the more dangerous the situation becomes, and the worse it is for the cost of living back here at home,” he said.

President Trump on Air Force One after he spoke to the UK’s Prime Minister Keir Starmer,

“I don’t want the UK after we win the war, I want them before”

“Whether we get their support or not”

“I can say this, and I said it to Keir Starmer”

“We will remember” pic.twitter.com/DUb7xxXzBM

— Farrukh (@implausibleblog) March 16, 2026

The British leader also rolled out the first domestic relief package tied to the US and Israeli-initiated war’s economic fallout, announcing a £53 million ($70 million) support plan for vulnerable households that rely on heating oil after fuel prices surged.

Tyler Durden

Mon, 03/16/2026 – 09:00

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}