Category: News

Futures Slide, Oil Jumps After US Attacks Kharg Island Ahead Of Trump’s 8pm Iran Deadline

Futures Slide, Oil Jumps After US Attacks Kharg Island Ahead Of Trump’s 8pm Iran Deadline

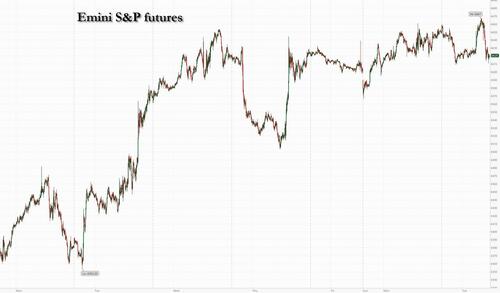

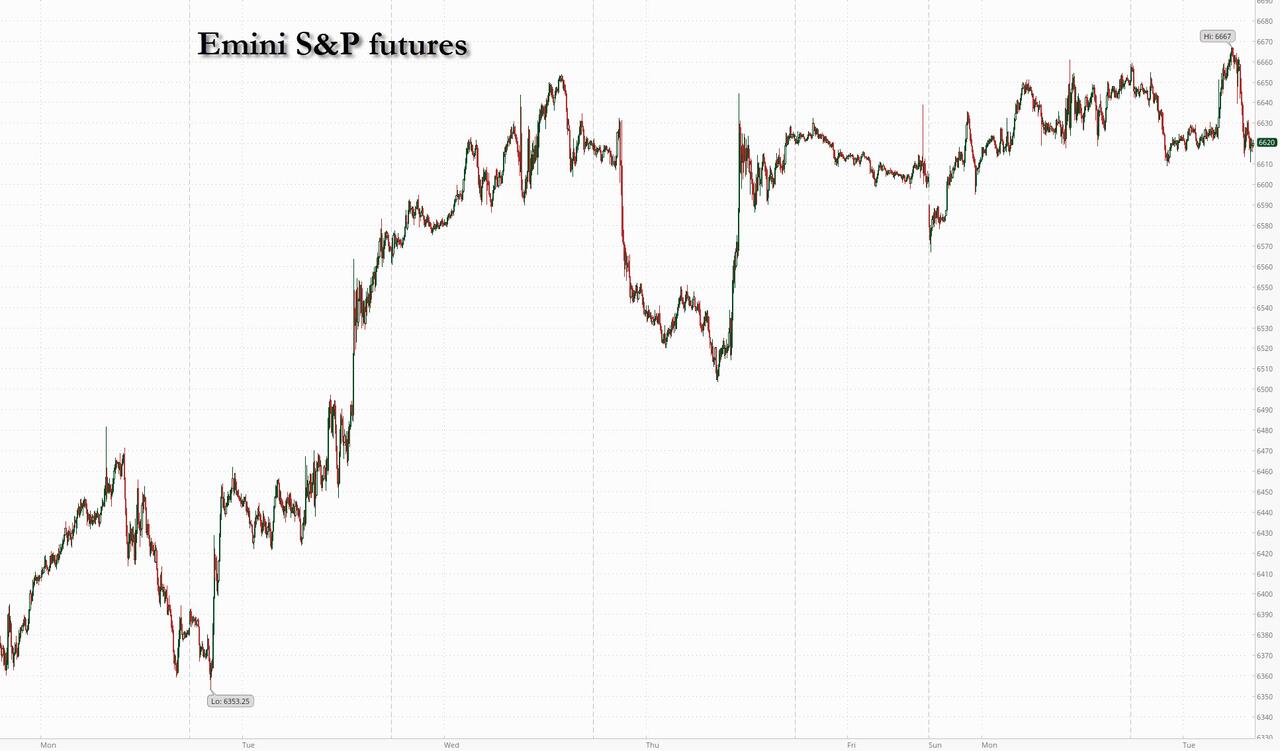

US futures reversed earlier gains and oil advanced following reports that Iran’s Kharg island was targeted earlier on Tuesday, while the market was largely paralyzed ahead of Trump’s 8pm ET deadline for Iran to agree to a ceasefire or face escalation. As of 8:00am ET, S&P futures are down 0.4%, and Nasdaq futures slide 0.6%. In premarket trading, all Mag7 names are lower even as AVGO (+3% pre-mkt) is bid after a TPU supply pact with GOOGL (+55bps) while ASML (-80bps) is weaker following a proposed US law that would further curb semiconductor exports to China (targeting ASML’s deep ultraviolet lithography machine ). Managed care is well bid after the final Medicare Advantage rate of +2.48% (vs ~1% bogey) was released last night (HUM +9%, CVS +7%, UNH +6%, ALHC +11%). Bond yields rise 1bp, 10Y TSY yield at 4.34%, the USD is also higher while commodities are mixed with oil reversing earlier losses and rising over 2%. Today’s macro data focus is weekly ADP, Durable / Cap Goods, and NY Fed 1-year Inflation Expectations. Ultimately, expect weaker volumes today with some market swings on unconfirmed ceasefire / deal chatter.

In premarket trading, Mag 7 stocks are all lower (Alphabet -0.06%, Amazon -0.4%, Meta -0.6%, Microsoft -0.4%, Tesla -1.3%, Nvidia -1.2%, Apple -1%)

Managed care companies including Humana gain after the Centers for Medicare & Medicaid Services finalized a 2.48% rate hike for health insurers in 2027. Investors see the pay boost as a meaningful improvement over the initial rates the agency proposed in January. Humana (HUM) rises 9% and CVS Health gains 6%.

Broadcom (AVGO) rises 3% after the chipmaker announced a long-term agreement with Google to develop and supply Tensor Processing Units. The companies also confirmed plans to work with Anthropic to power the AI startup’s burgeoning operations.

Estée Lauder (EL) slips 1% after Spanish newspaper Expansion reported that the the company and Puig owning families are set to hold talks this week in New York over their potential merger.

Organogenesis Holdings Inc. (ORGO) rises 19% after the company said a randomized controlled trial of 170 patients in a diabetic foot ulcer trial achieved its primary endpoint.

Wingstop (WING) rises 1.9% as Citi upgrades the fried chicken restaurant operator to buy, saying the valuation offers an attractive entry point.

Pershing Square proposed a combination with Universal Music Group that would move the listing into a US-based acquisition vehicle. It’s a deal that Bill Ackman’s fund said values the world’s biggest music label at a 78% premium to its last closing price.

In other news, Samsung reported preliminary operating profit that soared 755% to a record, with memory’s contribution estimated to be close to 90% of total operating profit. Rivals OpenAI, Anthropic, and Alphabet’s Google have begun working together to try to clamp down on Chinese competitors extracting results from cutting-edge US AI models. And Anthropic said its revenue run rate has now topped $30 billion, with more than 1,000 businesses spending over $1 million annually, a rate that has doubled since February. BlackRock is setting its sights on a corner of the $13.7 trillion US ETF industry long controlled by Invesco — tracking the Nasdaq 100 Index. Some Tiger Cub funds incurred losses in March. Maverick Capital’s Long Enhanced Fund and its main hedge fund tumbled 8.1% and 5%, respectively, while Viking Global Investors’ flagship fund lost 4.1%, according to people familiar with the matter.

Trump has threatened “all Hell” will rain down on Iran if it doesn’t agree to a ceasefire that reopens the Strait of Hormuz by 8 p.m. Eastern time. The Pentagon canceled the morning press briefing due to be led by Pete Hegseth, giving no reason. WSJ reported last night that hope is fading for a final deal by the deadline and RTRS reported this morning that a Senior Iranian Source said Tehran has rejected any temporary ceasefire with the U.S. and the IRGC warned neighboring countries “restraint is over” and threatened to disrupt regional oil and gas supplies for years to come. Strikes continued overnight.

“It seems clear that it is extraordinarily difficult to invest on expectations for binary outcomes,” notes Jeffrey Palma at Cohen & Steers. On the other hand, David Kruk at La Financiere de l’Echiquier, set out the dilemma confronting traders, observing that the “market is now set up in such a way that the real pain trade is upwards.”

Investors are watching for any sign of a breakthrough amid a flurry of diplomacy before the 8 p.m. Eastern Time deadline. Trump insists any deal must ensure uninterrupted transit through the Strait of Hormuz — a key artery for Middle East oil flows. He’s threatened to destroy Iran’s bridges and power plants if no accord is reached. “The market remains volatile,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin. “It continues to swing between de-escalation hopes and Trump following through on his threats.”

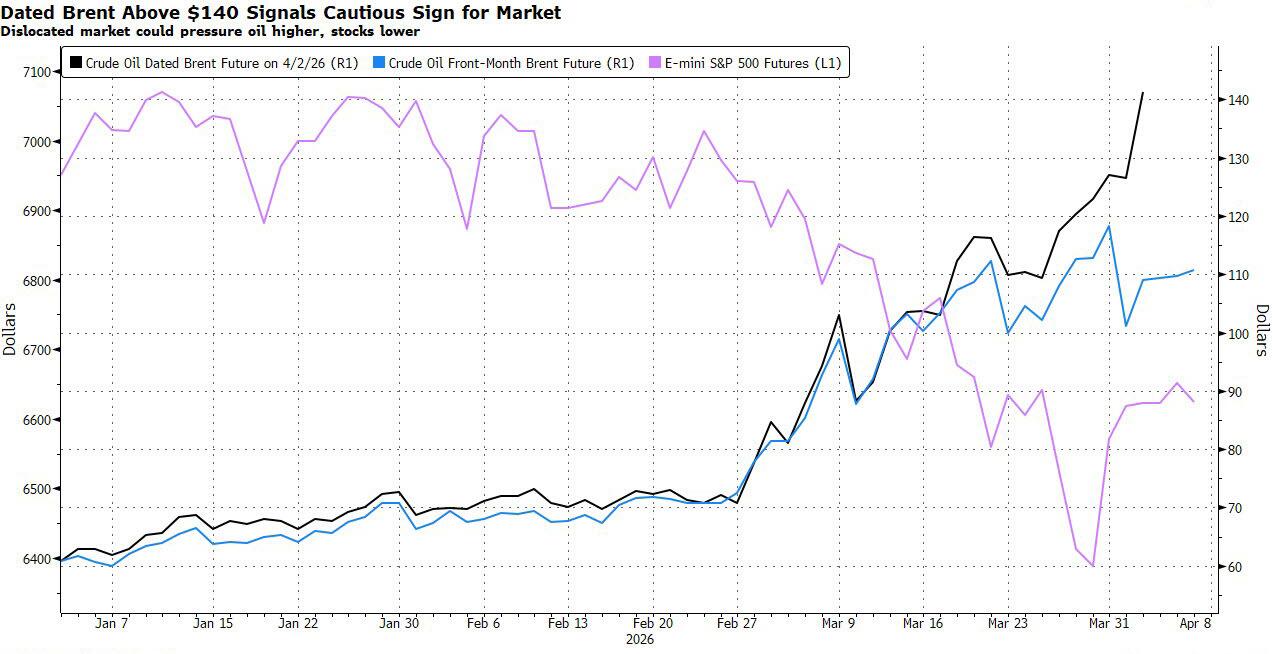

Oil remains in focus, with WTI crude rising to the highest since June 2022. Meanwhile, Bloomberg Intelligence analysts expressed caution over the wide gap between the Brent spot price, which reflects expectations of a resolution, and Dated Brent, which represents actual cargoes assigned specific loading dates. At above $140, the latter signals acute spot scarcity.

Trump’s deadline marks the latest pivotal moment in the war, which has killed thousands of people and triggered the largest-ever disruption to the global oil market. Israel told Iranians to refrain from using their country’s railway network until 9 p.m. local time, the first warning about such infrastructure that usually precedes an attack. Iran launched seven ballistic missiles and several more drones at Saudi Arabia overnight into Tuesday, while the Israel Defense Forces reported two missile volleys from Iran since midnight.

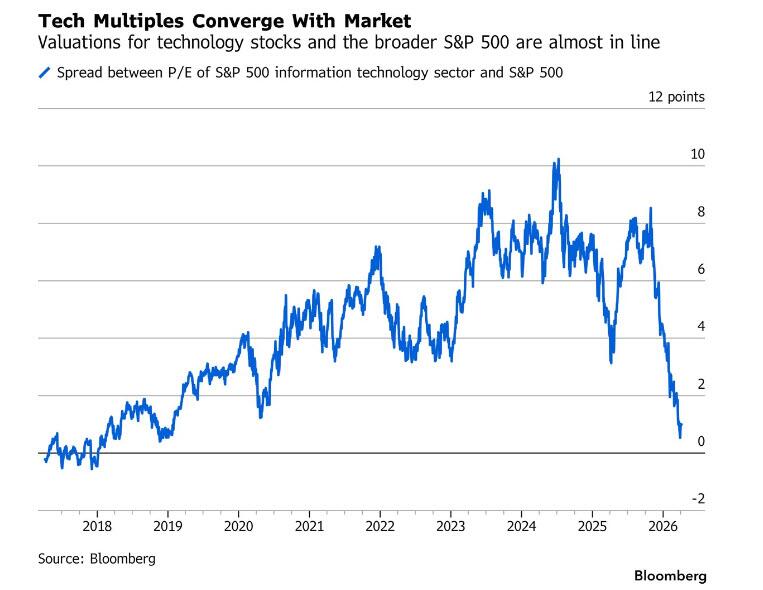

Meanwhile, the technology sector is looking increasingly attractive for investors as valuations fall below those of the wider stock market, according to Goldman strategists. Any lasting shock to the global economy from the war in Iran is also likely to benefit the sector as tech cash flows are less sensitive to economic growth, the strategists said.

The recent economic numbers aren’t boosting the case for the Federal Reserve to resume cutting rates anytime soon. March CPI on Friday is predicted to show the largest month-over-month increase in headline inflation since June 2022, largely driven by a spike in gasoline prices tied to the Iran conflict.

Europe’s Stoxx 600 is up by 0.6%, with the media subindex leading the way on a jump for Universal Music on a €56 billion takeover proposal. UMG is the biggest gainer after Pershing Square offered to buy the entertainment company, while tech underperforms, weighed down by ASML as US lawmakers propose tighter curbs on chip equipment exports to China. Here are the biggest movers:

Universal Music Group shares rise as much as 24% in Amsterdam, but trade well below the value of an offer from Pershing Square Capital Management amid doubt over whether the deal will happen

JCDecaux rises as much as 5.8% as TD Cowen upgrades the outdoor advertising company to buy from hold, seeing a clear inflection point as China returns to growth

Volati gains as much as 7.2%, the most since November, as Nordea reiterates its buy rating and raises its price target on the Swedish industrial group, saying the company is well-positioned to benefit from a cyclical rebound

ASML shares fall as much as 4.7% on Tuesday after US lawmakers unveiled legislation aimed at tightening restrictions on chip tool exports to China. The goal is to subject Dutch and Japanese firms to the same curbs that American companies face

Leonardo shares fall as much as 5.5% on the possibility of a management change at the Italian defense group; Bloomberg News reported that CEO Roberto Cingolani could be replaced as soon as this week

AddTech falls as much as 5.9% after DNB Carnegie downgraded the stock to hold from buy, saying the Swedish industrial equipment maker could face weakening earnings growth momentum in 4Q

Ninety One tumbles as much as 14% as BofA Global Research downgrades its rating on the investment management firm to neutral from buy and cuts its target price to 260p from 280p because of lower expected market returns

Colruyt drops as much as 4.3%, biggest decliner in Belgium’s BEL Mid Index, after UBS downgraded the stock to neutral from buy, saying it looks “fairly valued for modest growth”

Asian stocks advanced for a third-straight session even as the approach of President Donald Trump’s deadline for a peace deal with Iran kept traders on edge. The MSCI Asia Pacific Index rose 1%, with technology shares including TSMC and SK Hynix among the biggest boosts. Stocks climbed in Taiwan and Australia. Hong Kong’s market remained shut for holidays. Stocks also gained in India, while equities traded mixed in Japan, China and much of Southeast Asia. South Korea’s Kospi climbed after better-than-expected results from Samsung Electronics.

“While oil prices remain elevated for now, there is a strong view that the conflict will come to an end within the next one to two weeks, with crude prices returning to prior levels,” said Hideyuki Ishiguro, chief strategist at Nomura Asset Management. “Geopolitical risks themselves have not been resolved, but VIX in Japan, US, and Europe have peaked, suggesting that markets may have largely priced in these risks,” he added.

In FX, the Bloomberg Dollar Spot Index rises by 0.1%, with Aussie dollar and sterling the outperformers and Swedish krona lagging after a surprise cooling in inflation.

In rates, treasury futures hold small losses after erasing gains amid rising oil prices, with yields across tenors slightly higher on the day. US 10-year yield is less than 1bp higher near 4.34%, and curve spreads are within a basis point of Monday’s closing levels. With European bond markets open for first time since Thursday, German and UK yields are 2bp-5bp cheaper across flatter curves. The US session includes the first of this week’s three Treasury coupon auctions, a 3-year note sale at 1pm. Treasury’s $58 billion 3-year new-issue auction, to be followed by $39 billion 10-year and $22 billion 30-year reopenings Wednesday and Thursday, has WI yield near 3.895%, about 32bp cheaper than last month’s, which tailed by 1.1bp, a notably poor result.

In commodities, WTI crude oil futures are up about 2% from Monday’s multiyear high close, which followed Trump’s threat to obliterate key Iranian infrastructure if an agreement to end the war isn’t reached by 8pm Tuesday. Gold prices up, though paring back from highs near $4,700/oz.

US event calendar, includes ADP weekly employment change (8:15am), February durable goods orders (8:30am), March New York Fed 1-year inflation expectations (11am) and February consumer credit (3pm). Fed speaker slate includes Williams (8:30am), Goolsbee (12:35pm, 1:45pm) and Jefferson (5:50pm)

Market Snapshot

S&P 500 mini -0.6%,

Nasdaq 100 mini -0.7%,

Russell 2000 mini -0.2%

Stoxx Europe 600 +0.3%

DAX +0.5%

CAC 40 +1.0%

10-year Treasury yield +1 basis point at 4.34%

VIX +0.3 points at 24.48

Bloomberg Dollar Index -0.2% at 1211.85

euro +0.3% at $1.1571

WTI crude -0.4% at $111.97/barrel

Top Overnight News

Negotiators are pessimistic Iran will bend to meet President Trump’s demand to reopen the Strait of Hormuz before his Tuesday-night deadline, paving the way for the U.S. to target Iranian bridges and power plants in a fresh escalation of the war. Twice in his second term, Trump set a deadline for a deal with Iran, said he would bomb the country if its leaders didn’t comply, then followed through with military operations. WSJ

Airstrikes pounded Tehran on Tuesday, and Iranian officials urged young people to form human chains to protect power plants, hours before the expiration of U.S. President Donald Trump’s latest deadline for the Islamic Republic to reopen the crucial Strait of Hormuz or face punishing strikes on its infrastructure. AP

Iran on Monday delivered a 10 point proposal to end the war with the US and Israel. The plan was conveyed by Pakistan, which has been acting as a primary intermediary, but appeared unlikely to resolve major questions ahead of Trump’s Tuesday evening deadline for new attacks on Iran. NYT

A cross-party group of U.S. politicians have proposed a law to impose further restrictions on exports of computer chipmaking equipment to China, affecting companies such as ASML and China’s top chipmakers. RTRS

Japan’s households reduced spending for a third straight month even after real wages turned positive. Outlays by households adjusted for inflation fell 1.8% in February from a year earlier, a faster decline compared with January’s 1% retreat. Real consumption remains weak, with economists citing growing consumer fatigue and inflation pressure as key challenges to domestic demand. BBG

Taiwan’s opposition leader is set to arrive in China on Tuesday on what she has called a “historic journey for peace” as she hopes for a face-to-face meeting with Chinese leader Xi Jinping, the first such contact in a decade. FT

Anthropic’s revenue run rate has topped $30 billion and the company confirmed partnerships with Broadcom and Google. BBG

Cleveland Federal Reserve President Beth Hammack and Chicago Fed President Austan Goolsbee both see inflation as a far bigger problem than employment, underscoring their support for tighter rather than looser monetary policy as the Iran war puts upward pressure on energy prices and the job market remains stuck in low gear. RTRS

Bill Ackman’s Pershing Square offered to buy Universal Music Group in a cash-and-stock deal at a 78% premium to Thursday’s closing price. Ackman cited UMG’s stock underperformance as a trigger for the bid. BBG

Republicans are reportedly weighing how broadly to structure a party-line bill to fund President Trump’s immigration enforcement, with some senators seeking multi-year DHS funding and others favoring a narrower ICE and CBP measure: Semafor

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded cautiously following the positive lead from the US and with all focus remaining on geopolitics heading into US President Trump’s Tuesday evening deadline for Iran to open up the Strait of Hormuz or face the US destroying its power plants and bridges, although President Trump had also previously stated that he thinks talks are going well with Iran and they would like to be able to make a deal. ASX 200 rallied with tech and miners leading the upside and with almost all sectors in the green aside from industrials and consumer staples. Nikkei 225 failed to sustain its initial advances with the index pressured amid headwinds from higher oil prices and following disappointing Household Spending data. KOSPI surged at the open with strong gains in Samsung Electronics after its preliminary results topped forecasts and showed around an eight-fold jump in Q1 operating profit, although most of the advances were then pared as shares in the index heavyweight also pulled back. Shanghai Comp lacked conviction on return from the long weekend, with upside limited after another meek PBoC liquidity operation and with the Stock Connect still closed as Hong Kong markets remained shut.

Top Asian News

Japanese Finance Minister Katayama said won’t comment on JGB yield levels and will refrain from commenting on levels in the markets, adds impact of Middle East and oil prices on the market is high.

Chinese President Xi called for new energy system as war on Iran rocks global economy and said China needs to accelerate planning and construction of a new energy system to ensure the country’s energy security.

South Korean FX Chief said are to deploy bold measures in the FX market, if needed.

South Korea policy chief Kim said the chip industry secures four month’s worth of helium and it is premature to discuss a second extra budget.

Morgan Stanley cuts its China 2026 GDP growth forecast to 4.7% due to oil shock.

European bourses (STOXX 600 +0.7%) re-open from the 4-day Easter closure with mild gains, as traders countdown to Trump’s Iran deadline at 20:00EDT/01:00BST. France’s CAC 40 outperforms its peers, while the FTSE 100 underperforms. Worth noting that European indices opened mixed, but then moved higher, without a clear driver. Some may point to reports via a Pakistani journalist which suggested that a “framework of understanding for ceasefire” between US and Iran is “closer than ever”. European sectors are broadly in the green. Media is the clear outperformer, driven by gains in UMG (+12.2%) after Pershing Square announced a EUR 9.4bln bid to take over the media company. Technology sits at the bottom of the pile. Despite the majority of the sector components in the green, ASML (-2.3%) is weighing on the sector. This comes following a group of US politicians proposing a law to impose further export restrictions on computer chipmaking equipment to China.

Top European News

UK S&P Global Services PMI Final (Mar) 50.5 vs. Exp. 51.2 (Prev. 53.9). “Stagflation risks appear to have increased, with the final Services PMI data signalling slower growth and higher cost pressures than the earlier ‘flash’ estimates based on data compiled up to 20th March.”

UK S&P Global Composite PMI Final (Mar) 50.3 vs. Exp. 51 (Prev. 53.7).

EU S&P Global Composite PMI Final (Mar) 50.7 vs. Exp. 50.5 (Prev. 51.9). “The near-stalling of growth in March drags the PMI’s signal for first quarter GDP growth down to 0.2%. More worrying is that there are clear risks of the economy contracting in the second quarter unless there is a swift resolution to the conflict.”

EU S&P Global Services PMI Final (Mar) 50.2 vs. Exp. 50.1 (Prev. 51.9).

German S&P Global Services PMI Final (Mar) 50.9 vs. Exp. 51.2 (Prev. 53.5).

German S&P Global Composite PMI Final (Mar) 51.9 vs. Exp. 51.9 (Prev. 53.2).

French S&P Global Services PMI Final (Mar) 48.8 vs. Exp. 48.3 (Prev. 49.6).

French S&P Global Composite PMI Final (Mar) 48.8 vs. Exp. 48.3 (Prev. 49.9).

FX

FX markets saw a sharp risk-on move in the European morning, with no specific headline, but several outlets reporting optimism in US/Iran negotiations ahead of Tuesday’s deadline. DXY fell as much as 0.2% from 100.04 to a trough of 99.77, and high-beta FX was helped against the weaker buck, with Aussie the outperformer and Sterling also performing notably well.

Some participants flagged an Axios article six hours before the move, which quoted a US official, “If the president sees a deal is coming together, he’ll probably hold off…” it is unclear whether this led to the reaction, though other reports following this initial move have added to the constructive risk environment, “mediators are close to reaching an agreement” on a “framework of understanding for ceasefire”, according to Pakistani reporter Anas Mallick.

Elsewhere, EUR and GBP were unreactive to mixed European Final PMIs. To recap, the EZ wide composite and services were revised a touch higher while the UK’s were revised lower.

The session ahead sees US ADP Employment Change Weekly, US Durable Goods RCM/TIPP Economic Optimism Index (Apr), Atlanta Fed GDP and President Trump’s Iran deadline. Fed speak is expected from Fed’s Williams (13:30 BST), Goolsbee (17:35 BST) and Jefferson (22:50 BST). Full primer on the Newsquawk headline feed.

Central Banks

ECB’s Wunsch said he is open to an interest rate rise at the April meeting; a lasting crisis would warrant a series of rate rises.

ECB’s Radev said the ECB must be ready to act if inflation persists, sees a rising likelihood of adverse scenario but too early to say if April rate hike is needed. Inflation expectations at risk of rising too quickly.

Fixed Income

Initial bearish bias across the fixed income was facilitated by stronger energy prices, as the geopolitical environment remains exceptionally turbulent and as traders count down their clocks to President Trump’s 20:00EDT Iran deadline. However, in recent trade the crude complex took a tumble – but lacked a clear driver. Some market participants pointed towards an Axios piece from overnight, which reported that Trump may hold off from strikes on Iran if he sees a “deal coming together”. Markets also appear to be digesting some relatively positive mood from the Pakistani side, with a couple analysts suggesting a breakthrough could be close; whilst another suggested that a “framework of understanding” for a ceasefire is close. The pressure in energy prices therefore helped to boost fixed benchmarks to session highs.

USTs were initially lower and were holding near troughs throughout the early portion of the morning, before then surging alongside the pressure in the crude complex. Currently holding at the upper end of a 110-21+ to 110-29+ range. On the data front, weekly ADP jobs figures, durable goods orders for February. On today’s speakers’ slate, Fed’s Williams (voter) will speak on Bloomberg TV; Fed’s Goolsbee (2027 voter, dovish) will speak on the outlook for policy and the economy; Fed’s Vice Chair Jefferson (voter, dovish) will speak on the economic outlook and the labour market.

Bunds followed the above, and currently holding at the upper end of a 125.31-125.73 range – though still remains incrementally in the red. Geopols aside, German benchmarks have had a number of European PMI Final metrics to digest; Spain topped expectations, Italy missed whilst the EZ-wide figure was revised incrementally higher. Interesting commentary from within the German release suggested that, “the lack of pricing power in the service sector is important from a monetary policy perspective, as it limits the amount of upward pressure on core inflation, a measure that the ECB will be closely watching when considering interest rate increases.”

Gilts are currently flat. As above, initially weighed by stronger energy prices, but UK paper then soared to highs as energy prices dipped. Currently towards the upper end of a 88.23-88.72 range. UK PMI Finals were revised lower, with analysts citing slower output growth as a result of the war in the Middle East. It also highlighted increasing risks to “stagflation”, and increasing costs pressures.

Commodities

Crude futures gained at the start of the APAC session and held onto gains as European traders stepped in as US President Trump’s 20:00EDT deadline approaches. If Iran does not agree to a ceasefire and reopen the Strait of Hormuz, he said the US will decimate Iran’s bridges and didn’t rule out striking power plants. However, Trump did also state that he thinks talks are going well and that Iran has “an active and willing participant on the other side.” Further reporting throughout the European morning indicates that an agreement could be near, with Pakistani reporter Mallick suggesting that the interlocutors are ‘closer than ever for an agreement’ to get a “framework of understanding for ceasefire” between the US and Iran.

WTI and Brent topped at USD 116.56/bbl and USD 111.80/bbl, respectively, before sinking – a move which lacked a clear driver. However, the move appeared to follow the aforementioned reports from the Pakistani reporter. At the time of writing, WTI May’26 has returned below USD 113/bbl while Brent Jun’26 oscillates on either side of USD 110/bbl.

Spot gold trades relatively contained within a USD 4617-4691/oz range. Upticks have picked up pace in recent trade as the USD softens amid downside in energy prices. However, the 20-SMA at USD 4,732/oz and last week’s high of USD 4,800/oz remain as near-term resistance levels. To add, China added gold to its reserves for a 17th consecutive month, highlighting that demand for the yellow metal is still high. However, UBS lowered its end-June forecast to USD 5,200/oz due to softer investor demand.

3M LME copper is rangebound, oscillating in a USD 12.37k-12.46k/t range. This comes as participants remain cautious as the Trump deadline looms.

Hungary to agree to buy oil from US at Orban-Vance meeting, Bloomberg reported. Hungary’s Mol will agree to purchase 500,000 tons for approximately USD 500mln.

Kazakhstan’s Energy Ministry said the oil shipments via CPC pipeline is stable, IFX reported.

IRGC’s public relations channel reported of “explosion and extensive damage to the Al-Jubeil industrial area”.

Attacks reportedly hit Saudi Aramco’s petrochemical plant in Saudi Arabia, AFP reported citing sources.

China has provided Iran with a financial lifeline during the past half decade by purchasing most of its oil, according to WSJ.

Tanker explosion near the Bridge of Americas in Panama City caused a massive fire.

Japan’s Industry Minister Akazawa said crude oil procurement is progressing.

China gold reserves at end-March (USD) 342.76bln (prev. 387.59bln).

UBS lowers end-June gold forecast to USD 5,200/oz, amid softer investor demand amid elevated volatility.

Goldman Sachs analyst raises 2026 copper price forecast to USD 12,650/ton from USD 11,400/ton and expects copper prices to remain volatile as the market continues to assess impacts of the events in the Middle East on economic growth.

Geopolitics

Pakistani reporter Anas Mallick suggests that, “to my understanding, the interlocutors (Pakistan, Turkiye and Egypt) are ‘closer than ever for an agreement’ to get a “framework of understanding for ceasefire” between US and Iran”.

Some geopolitical analysts say signals from Pakistan suggest a possible breakthrough in the coming hours, with Egypt, Turkey, Saudi Arabia and reportedly Beijing involved. said that a ceasefire could be near, but the situation remains early and fragile, so caution is warranted.

Pakistan in last-minute efforts, along with Turkey and Egypt, to convince Iran to agree to the outline proposed by Pakistan, according to I24’s Stein.

Five friendly countries leaders’ and eight intelligence agencies have reached out to Iran seeking to open a path for a ceasefire, Fars News reported.

Israeli Source tells N12 news “The next 24 hours are the most decisive in the war, if it were up to political leadership in Iran, there would have been a ceasefire long ago, there is doubt about their control”, N12’s Segal reported.

Iran’s Spokesperson of the National Security Commission of the Parliament said “we are making special arrangements for the Strait of Hormuz”, via Tasnim.

Spokesman of Iran’s National Security and Foreign Policy Committee of Parliament said oil exports are going on as usual, and with even more capacity than before, IRIB reported.

Iran atomic agency said heavy bombs won’t halt nuclear tech progress.

China has provided Iran with a financial lifeline during the past half decade by purchasing most of its oil, according to WSJ.

Saudi Arabia, UAE and Israel report Iranian drone and missile attacks, according to CBS.

Israel announces a new wave of strikes on Iran and issues incoming missile alert.

Iran launches new batch of missiles towards southern Israel.

Israeli military said it completed airstrike wave aiming to damage Iranian terror regime infrastructure in Tehran and additional areas across Iran.

US House Democrat Ansari intends to introduce articles of impeachment against Secretary of War Hegseth, cites Iran war and war crimes as grounds for Hegseth impeachment, according to NBC.

Japanese PM Takaichi said in parliament said in Parliament, want to take next step in talks with Iran and is strongly urging Iran to allow Hormuz safe passage, while she is seeking phone talks with the presidents of US and Iran.

Iranian Parliament Speaker Ghalibaf’s adviser Mohammadi said it is Trump who has about 20 hours to either surrender to Iran or his allies will return to the Stone Age, while he added that they will not back down.

Iran said non-hostile countries can coordinate access to the Strait of Hormuz, according to Press TV.

US Vice President J.D. Vance is on standby for Iran negotiations, according to POLITICO. “The negotiations are led by Steve Witkoff and Jared Kushner but Vance could be tagged in if there is a direct meeting with Iranian officials.”.

Iran’s top joint military command said Trump’s threats are ‘delusional’ and his threat have no effect on operations against US and Israel.

US data centres of Amazon (AMZN), Microsoft (MSFT), Oracle (ORCL), and Equinix (EQIX) in the UAE are now identified as potential targets for Iran’s counter response in the region.

Iranian securities exchange chief outlines conditions needed to reopen the Iranian capital markets: said outcomes could include a ceasefire with a formal agreement and full reopening, or a ceasefire without agreement and a gradual reopening.

Explosions reported in eastern regions of Saudi Arabia and alarms sounding in Bahrain, Tasnim reported.

Israeli reporter Stein said “Unexpectedly: the press conference planned for today with Defence Minister Hegseth and US Chief of Staff was cancelled”.

Fars news citing an informed source said “Trump is clearly looking for a meeting and an agreement. The American proposal includes the removal of “Witkoff” due to his closeness to Netanyahu’s circle and negotiations with “Vance” to build a serious path. In the end, this source noted: Americans believe that fuel prices will increase explosively from next week and are not willing to accept this risk.

The Iranian Ambassador to Pakistan said Pakistan’s positive and productive attempt to step the war is approaching a critical and sensitive stage.

Iranian outlets report that Yazd and Shiraz were shaken by blasts.

Large barrage of missiles were reportedly headed for Bahrain, with air raid sirens and alerts in multiple areas.

Drone strike reportedly hit US Victoria base in Baghdad, according to Iraqi sources cited by Fars.

Missiles hit Saudi Arabia’s Jubail which is largest industrial hub in the Middle East where large petrochemical and energy facilities are located.

IRGC Aerospace Force Commander said they targeted the oil refinery, power plants, ports, and railway lines in Haifa Bay, and no interception of our missiles was recorded, Al Jazeera reported.

Russia’s Yamal LNG ships first cargo to China since November, LSEG data shows.

Russia’s Ministry of Defence reported that air defence forces have downed 45 Ukrainian drones over Russian regions overnight.

US Event Calendar

DB’s Jim Reid concludes the overnight wrap

US and Asia markets had a decent start to the week yesterday while Europe was off for Easter Monday. However, sentiment has turned more cautious this morning as investors grapple with President Trump’s new deadline of 8pm Eastern Time tonight (1am London) for Iran to agree a deal as he threated to destroy Iran’s bridges and power plants. The renewed escalation threat has seen Brent crude move back above $111/bbl this morning after trading as low $107/bbl yesterday. In turn, S&P 500 futures are down -0.44% overnight after posting a fourth consecutive advance (+0.44%) yesterday that saw the index erase half of its decline since the Iran strikes began.

In terms of Trump’s latest ultimatum to Iran, the US President shared the 8pm ET Tuesday deadline on social media on Sunday and then referred to it several times yesterday as he demanded that Iran strikes a deal that “that’s acceptable to me”, while threatening intensified attacks against Iran that would destroy “every bridge” and take “every power plant” out of business. Notably, Trump said that a deal should include “free traffic of oil”, calling reopening the Strait of Hormuz “a very big priority”. So a seeming shift from previous suggestions that reopening the straits was not a core objective for the US. The President repeatedly suggested that this evening’s deadline was final, saying that he was “highly unlikely” to postpone it. Recall that Trump had issued an initial 48-hour ultimatum for striking Iran’s power plants back on March 21, first extending this by 5 days and then followed by another 10-day pause that had been due to expire yesterday.

Earlier yesterday, we had heard various reports on talks as other countries in the region have pushed for a ceasefire deal. Iran’s state-run IRNA then reported that Tehran rejected a ceasefire via Pakistani mediators, instead demanding a permanent end to the war as well as lifting of sanctions, reconstruction efforts and a protocol for safe passage through Hormuz. Meanwhile, Trump called Iran’s proposals a “very significant step” but “not good enough” as he threatened the escalatory strikes.

So that left oil markets facing crosswinds from Trump’s escalation threat to possible ceasefire talks as well as news that shipping via the Strait of Hormuz has been edging higher in recent days. Iran said on Saturday that “brotherly” Iraq would be exempt from shipping restrictions in the Strait, and AIS data showed five tankers crossing the Strait that day (possible that more did so with transponders turned off). That was the most since March 1 but still a small fraction of the roughly 60 tankers a day before the war.

Brent crude whipsawed in a relatively tight range yesterday, falling from above $111/bbl at yesterday’s open to as low as $107/bbl early in European hours before closing +0.68% on the day at $109.77/bbl. It is another +1.67% higher at $111.60/bbl as I type.

With oil markets relatively stable, risk assets had a decent start to the week, with the S&P 500 (+0.44%) advancing for a fourth session in a row yesterday, its longest run since January. That left the S&P 500 up +4.22% from last Monday’s closing low, erasing around half of the -7.78% decline it had seen since February 27. The NASDAQ (+0.54%) and the Mag-7 (+0.28%) saw similar gains, while nearly two thirds of the S&P 500 constituents moved higher on Monday with cyclical sectors outperforming. Private investment companies including Apollo (-0.87%) and Blackstone (-0.72%) underperformed amid lingering concerns about private credit. By contrast, US HY credit spreads tightened by -8bps to 291bps, their lowest level since March 5.

In Asia this morning, the Nikkei (-0.38%) is down following a +0.55% increase yesterday after softer Japan household spending data (-1.8% YoY vs -0.8% expected) which posted a third consecutive year-over-year decline in February. Meanwhile, the KOSPI (+0.30%) is continuing its upward trend after a +1.36% rise on Monday. Samsung Electronics was up as much as +4.9% at the open as it projected record quarterly profits due to strong AI chip demand, but its stock is now down -1.98% as I type. Elsewhere, the S&P/ASX 200 (+1.43%) is significantly higher this morning, while the CSI (-0.29%) and the Shanghai Composite (+0.03%) are more subdued. In the US, S&P 500 futures (-0.44%) have lost ground overnight, whereas Euro STOXX 50 (+0.13%) futures are edging higher after yesterday’s US advance.

In terms of yesterday’s other news, the March ISM services release in the US highlighted the inflationary risks stemming from the Iran war. While the headline reading retreated from a post-2022 high of 56.1 to 54.0 (vs. 54.9 expected), the prices paid component saw a stronger-than-expected rise to 70.7, its highest since October 2022. And there were contrasting signals within the details, as new orders rose to a 3-year high of 60.6, but employment fell to a 2-year low of 45.2. Amid this mixed data, the Treasury curve saw a modest flattening yesterday, with the 2yr yield up +0.8bps to 3.85% but 10yr down -1.3bps to 4.33%.

Treasury yields had seen a sizeable rise in Friday’s shortened session, with 2yr up +4.4bps and 10yr up +3.9bps following the strong March employment report. The release saw both headline (+178k vs +65k expected) and private (+186k vs. 78k expected) payrolls come in far above consensus expectations, with the unemployment rate also dropping from 4.44% to 4.29% (vs. 4.4% expected). To be sure, the rebound from strike- and weather-related weakness in February payrolls played a role, with the earlier timing of Easter also possibly bringing forward some payroll gains at the expense of April. Still, averaging through the Q1 employment reports, headline (+68k) and private (+79k) payrolls have been running above estimates of breakeven job gains and well above their subdued pace in late 2025, easing concerns on the employment side of the Fed’s dual mandate.

Turning to the week ahead, the data highlight will be the March CPI print in the US on Friday where the impact of the energy price shock will be on full display. Our economists expect a roughly 25% increase in gasoline prices to yield a 0.95% monthly gain in headline CPI, raising the annual rate from +2.4% to +3.4%, while core inflation sees a more moderate +0.33% monthly rise. The March CPI reading will also be preceded by the February core PCE inflation print on Thursday, which we expect at +0.39% MoM. That would mark the highest monthly print since last February and bring the 3- and 6-month annualised rates of the Fed’s preferred inflation metric up to 4.5% and 3.5% respectively.

Other notable US data releases this week include the March NY Fed inflation expectations survey and February durable goods orders today as well as the University of Michigan consumer sentiment on Friday. Elsewhere, we have the Euro Area final March services PMIs (today), Germany’s February factory orders (Wednesday) and industrial production (Thursday), and the March inflation reports in China (Friday). From central banks, Wednesday will see the March FOMC minutes and a rates decision in New Zealand (our economists expect a hold). See the full day-by-day rundown below.

And while Iran headlines will dominate the geopolitical news, we also have NATO Secretary General Rutte scheduled to meet with Trump in Washington tomorrow in a visit that comes amid Trump’s vocal criticism of NATO allies over their stance on the Iran war.

Tyler Durden

Tue, 04/07/2026 – 08:30

Polymarket Unveils Exchange Overhaul, Native Stablecoin As US Expansion Looms

Polymarket Unveils Exchange Overhaul, Native Stablecoin As US Expansion Looms

Authored by Micah Zimmerman via Bitcoin Magazine,

Bitcoin and crypto focused prediction market platform Polymarket is preparing its most significant infrastructure upgrade to date, rolling out a rebuilt trading system alongside a new native stablecoin designed to replace bridged collateral and streamline on-chain activity.

The overhaul, described by the company as a “full exchange upgrade,” is expected to go live over the next several weeks and includes new smart contracts, an updated central limit order book (CLOB), and a proprietary collateral token called Polymarket USD.

The token will be backed 1:1 by USDC and will replace USDC.e, a bridged version of the stablecoin currently used across the platform.

Last month, Intercontinental Exchange, the parent company of the New York Stock Exchange, made a $600 million direct cash investment in prediction market platform Polymarket as part of a broader equity fundraising round, the company announced.

The shift away from bridged assets reflects a broader effort to reduce reliance on cross-chain infrastructure, which can introduce additional risks and inefficiencies.

By moving to a natively controlled collateral token, Polymarket aims to tighten control over settlement, improve liquidity consistency, and simplify the trading experience for users.

At the core of the upgrade is a redesigned matching engine and an improved order book architecture.

The new system is intended to deliver faster execution, tighter spreads, and lower operational overhead. According to developer materials, the updated exchange stack reduces the complexity of order structures while introducing support for advanced features such as EIP-1271 signatures, enabling smart contract wallets to interact more seamlessly with the platform.

Polymarket said most users will experience a smooth transition, with the interface automatically handling the conversion of existing assets into Polymarket USD via a one-time approval. However, more advanced traders and developers will need to manually wrap their holdings using a dedicated collateral onramp contract and update integrations to align with the new system.

As part of the migration, all existing order books will be cleared during a scheduled maintenance window, with the company promising advance notice ahead of the transition. The reset is intended to ensure consistency across the upgraded infrastructure and avoid discrepancies between legacy and new systems.

Prediction markets like Polymarket are booming

The timing of the overhaul comes amid rapid growth for Polymarket, which has seen trading volumes surge in recent months. The platform reportedly surpassed $10 billion in monthly volume in March, underscoring increasing demand for event-based trading markets across crypto and traditional finance audiences.

Beyond performance improvements, the upgrade signals a strategic shift toward greater vertical integration. Polymarket has historically relied on external systems, including optimistic oracle mechanisms, to resolve market outcomes. However, the company has hinted at future plans for a native token, potentially called POLY, which could play a role in governance and dispute resolution.

If implemented, such a token could allow Polymarket to internalize key functions like market validation and outcome verification, reducing dependence on third-party protocols and giving the platform more direct control over what it defines as “truth” within its markets.

The infrastructure revamp also aligns with Polymarket’s renewed push into the U.S. market. After previously halting domestic operations, the company has since registered with the Commodity Futures Trading Commission and is positioning itself to operate within an increasingly defined regulatory framework.

With its latest upgrade, the company is attempting to evolve from a fast-growing crypto application into a fully-fledged exchange platform, combining improved execution infrastructure with tighter control over collateral, governance, and market integrity.

Tyler Durden

Tue, 04/07/2026 – 08:05

US Already Spent Over $42 Billion & Counting On Iran War

US Already Spent Over $42 Billion & Counting On Iran War

This week will see the Iran war reach 40 days of fighting, which is a far cry from the mere “four days” some US administration officials offered as a possible ‘optimistic’ timeline at the very opening of Trump’s Operation Epic Fury.

According to the Iran War Cost Tracker portal, the US military operation has cost more than $42 billion thus far. The tracker has arrived at this figure largely based on a Pentagon briefing to Congress on March 10, which disclosed that Washington spent $11.3 billion in the first six days of the new war in the Middle East.

The same briefing indicated the Pentagon planned to spend at least an additional $1 billion per day for the remainder of the conflict.

The real cost could be much, much higher given that at this point dozens of ultra-expensive aircraft and radars have been knocked out by Iran’s ongoing retaliation, and as the US has begun high risk incursions into the region and into Iranian territory itself.

Axios in a report days ago highlighted that “The U.S. is dedicating significant amounts of firepower to the Middle East as it wrestles with Iran. Some of it — billions of dollars’ worth, in fact — will not be returning.”

Describing the mounting costs in terms of blood and treasure, Axios wrote that “Hundreds of American troops have been injured and 13 killed” – and also: “Some exquisite weaponry, everything from stealth jets to radars, has been knocked out.”

Axios continues, “The high end includes costs associated with radar replacement at Al Udeid Air Base in Qatar and some fixes to the Gerald R. Ford aircraft carrier, which last month suffered an hours-long laundry fire.” The laundry room fire narrative has been subject of immense speculation and skepticism, with the supercarrier undergoing lengthy emergency repairs at its current port of Split, Croatia.

Also confirmed damaged or destroyed are the following:

One Lockheed Martin F-35A

One Boeing E-3 Sentry

One RTX AN/TPY-2 radar

Three Boeing F-15E Strike Eagles

Multiple Boeing KC-135 Stratotankers

Multiple General Atomics MQ-9 Reapers

The lost military hardware, some of which may have yet to be disclosed, itself is a loss in the billions.

Here’s what is known so far about U.S. Air Force losses during Operation Epic Fury:

Total losses are estimated to exceed $2 billion, with replacement costs potentially even higher.

— Four F-15E Strike Eagles have been lost, one over Iran and three downed by friendly fire over… pic.twitter.com/OjaR0gzdWv

— Egypt’s Intel Observer (@EGYOSINT) April 3, 2026

Despite the immense and growing expense on the American taxpayer, there’s still not been a Congressional War Powers resolution passed. As yet, there’s really not been any real or robust debate over the merits or justification of the war among the people’s representatives in Congress.

Independent journalist (formerly of The Intercept) Lee Fang writes, “We learned from the Afghan papers & SIGAR reports that everything the Pentagon and cable media told us about that occupation was a lie. The U.S. installed hated pedophile drug lords to run that country while contractors ransacked billions. The Iran war is 10x more built on lies.” And so the Iran situation could get a lot worse, and could be for potentially years to come.

Tyler Durden

Tue, 04/07/2026 – 07:45

https://www.zerohedge.com/geopolitical/us-already-spent-over-42-billion-counting-iran-war

75 Gulf Energy Assets Damaged In U.S.-Iran War As Supply Shock Intensifies

75 Gulf Energy Assets Damaged In U.S.-Iran War As Supply Shock Intensifies

International Energy Agency (IEA) Executive Director Fatih Birol was interviewed by the French newspaper Le Figaro earlier on Tuesday and warned that the Gulf energy shock “is more severe than those of 1973, 1979, and 2022 combined” because it is affecting oil, gas, food, fertilizers, petrochemicals, helium, and global trade all at once.

Birol said in the interview that more than 75 energy sites across the Gulf region have been attacked, with about a third severely damaged, suggesting tens of billions of dollars in repairs and a prolonged disruption of some energy flows, further tightening global supplies and compounding the disruption at the Strait of Hormuz chokepoint.

The newspaper asked Birol, “How quickly can Gulf production recover?”

He responded:

“We are monitoring energy infrastructure in real time—fields, refineries, terminals. Seventy-five facilities have been attacked and damaged, more than a third severely. Repairs will take a long time. Countries like Saudi Arabia may recover faster due to strong engineering capabilities and financial resources, but elsewhere, such as Iraq, the situation is far worse. About 15 million people depend on oil and gas revenues there, and the country has lost two-thirds of its oil income, approaching economic paralysis. It will take a long time for the Middle East—previously a reliable energy hub—to recover.”

Cherry-picking the most important parts of the interview:

Le Figaro asked: Who will suffer the most?

Birol responded: The global economy will suffer. Of course, European countries will struggle, as will Japan, Australia, and others. But developing countries will be the most affected due to high oil, gas, and food prices, and accelerating inflation. Their economic growth will be heavily impacted. I fear many developing countries will see their external debt rise significantly. That is why I am pessimistic—this crisis stems not from energy itself, but from geopolitics.

Le Figaro asked: Which countries are most exposed to shortages?

Birol responded: Import-dependent countries are most exposed: in Asia—South Korea, Japan, but especially Indonesia, the Philippines, Vietnam, Pakistan, and Bangladesh. African countries will also be heavily affected, as developing nations have limited financial flexibility.

Le Figaro asked: How quickly can Gulf production recover?

Birol responded: We are monitoring energy infrastructure in real time—fields, refineries, terminals. Seventy-five facilities have been attacked and damaged, more than a third severely. Repairs will take a long time. Countries like Saudi Arabia may recover faster due to strong engineering capabilities and financial resources, but elsewhere, such as Iraq, the situation is far worse. About 15 million people depend on oil and gas revenues there, and the country has lost two-thirds of its oil income, approaching economic paralysis. It will take a long time for the Middle East—previously a reliable energy hub—to recover.

Le Figaro asked: How significant is the drop in Gulf oil production?

Birol responded: Enormous. These countries are producing just over half of pre-war levels. As for natural gas, exports have stopped entirely. March was already difficult, but April will be worse. If the Strait remains closed throughout April, we will lose twice as much crude and refined products as in March. We are entering a “black April.” In the Northern Hemisphere, April usually marks spring—but now it may feel like the beginning of winter.

Birol has painted a bleak outlook for energy markets and the global economy for weeks in various interviews.

However, emerging through the fog of war, the U.S. appears poised to be a net beneficiary of the chaos across the Gulf, with energy flows expected to remain disrupted for some time.

Qatar Dethroned As ‘LNG King’ As U.S. Seizes Throne, Reshaping Future Of Gas

Wyoming’s Helium Empire Ascends As Qatar Gas Goes Flat

A reminder to readers of JPMorgan’s note last week, mapping how the energy shock dominoes begin to fall. Read it here.

Tyler Durden

Tue, 04/07/2026 – 07:20

https://www.zerohedge.com/energy/75-gulf-energy-assets-damaged-us-iran-war-supply-shock-intensifies

Marc Andreessen Calls AI Job-Loss Fears ‘Fake’, Expects Employment Gains

Marc Andreessen Calls AI Job-Loss Fears ‘Fake’, Expects Employment Gains

It is not the first time that the venture capital guru has questioned some of the fundamentally dystopian scenarios being proposition in an AI world.

In February, we noted that amid an armada of dystopian futurists, projecting linear thoughts into a future of ‘AI uber alles’, Marc Andreessen stands as a beacon of potential utopian light, seeing a future that looks very different and very positive for young and old alike.

In a brief few minutes, the co-founder of Netscape and VC firm Andreessen Horowitz (a16z) believes instead that we are living through a unique (and most incredible) time in history with the rise of AI coming right as human civilization needs it…

“we’re going to have AI and robots precisely when we actually need them [with populations shrinking] to keep the economy from actually shrinking.”

Simply put, Andreessen says that fears of AI-driven mass job loss are overly simplistic.

After decades of unusually slow technological change and low job churn, AI could restore historical productivity levels (exemplified by the period from 1870-1930), sparking opportunity, innovation, and net job growth rather than displacement.

Declining populations and reduced immigration will make human labor increasingly valuable. AI’s timing is “miraculous”, Andreessen exclaims, preventing economic shrinkage from depopulation.

In even radical scenarios, explosive productivity leads to output gluts, collapsing prices, and massive real-wealth gains – equivalent to “giant raises” for everyone – while making safety-nets more affordable.

Whether incremental or transformative, Andreessen sees the outcome as fundamentally positive economic news.

Of course, he does have a lot of skin in this game…

Building on that, CoinTelegraph’s Christina Comben reports that Andreessen said artificial intelligence will spark a “massive jobs boom,” dismissing fears of widespread job losses as “all fake” in a Sunday post on X.

His optimism contrasts with a March US jobs report showing unemployment holding steady at 4.3%, while the number of people unemployed for 27 weeks or more rose by 322,000 over the past year.

Andreesen shared a Business Insider report showing a sharp rise in tech job openings in 2026, with more than 67,000 software engineering roles, a twofold increase from 2023, and argued that employers had recovered from post-pandemic hiring corrections and the interest rate spike.

“The ‘AI job loss’ narratives are all fake,” he wrote.

“AI = massive ramp in productivity = massive ramp in demand = massive jobs boom. Watch.”

Andreessen is one of Silicon Valley’s most influential investors, a co-founder of Netscape and venture firm Andreessen Horowitz.

He is also a major backer of US crypto and AI companies.

Job losses in tech pile up

On the ground, the reality is somewhat different. On Feb. 26, Jack Dorsey’s Block cut 40% of its staff as the company accelerated its use of AI, including experiments with agents to take over parts of middle management.

On March 19, crypto exchange Crypto.com announced a 12% workforce reduction due to AI integrations, warning that companies “that do not make this pivot immediately will fail.”

Crypto.com cuts 12% of its staff. Source: Kris Marszalek

AI-driven pivots by companies are also impacting employment.

Oracle reportedly cut up to 30,000 jobs recently, citing “broader organizational change,” as it pushes to build AI data centers.

MARA, which has been repurposing its Bitcoin mining infrastructure for AI, has reportedly reduced its staff by 15%.

Andreessen’s comments meet with skepticism

That backdrop helps explain the online backlash Andreessen received.

“Tell that to the average lower middle class American who can’t find a job or the consumer who can’t get decent customer service,” crypto influencer WendyO replied.

Tory Green, co-founder at io.net argued Andreessen could be proved right on net job creation, but only if AI tools are broadly accessible and not captured by a handful of platforms.

Tyler Durden

Tue, 04/07/2026 – 06:55

https://www.zerohedge.com/ai/marc-andreessen-calls-ai-job-loss-fears-fake-expects-employment-gains

Germany’s Debt Spiral: Bundesbank Chief Breaks Silence

Germany’s Debt Spiral: Bundesbank Chief Breaks Silence

Submitted by Thomas Kolbe

It’s not every day that top officials of the German Bundesbank take an explicit stance on daily politics.

Nagel’s stark warnings about Germany’s debt and the government’s creative accounting were surely met with grim recognition in Berlin’s corridors of power. Open criticism is rare there, and when it comes from credible insiders, it stings even more.

Bundesbank President Joachim Nagel

Chancellor Friedrich Merz and his Finance Minister Lars Klingbeil apparently still believe the fairy tale that debt-fueled demand policy can create economic miracles, generate growth, and deliver real prosperity. The result: a staggering debt binge that threatens to finish Germany economically.

Of course, this is a Keynesian nursery tale, endlessly repeated by politicians. With this simplified version of economics, political power is cemented – while the anonymous masses of taxpayers are left to clean up the debt disaster.

The government assumes the taxpayer backstop—and has surrounded itself with a state-friendly media sector, like a protective membrane. This behavior is conditioned.

The truth about mounting state debt, its destructive impact on private business, inflation, and the erosion of middle-class purchasing power is rarely discussed, and only in the media’s backrooms. When criticism reaches the public eye, its proponents are aggressively attacked and their valid arguments systematically sterilized.

Since January 2022, Joachim Nagel has led the Bundesbank. Recently, he warned for the first time about the unchecked growth of public debt—breaking Berlin’s long-standing elite vow of silence. Last year, he said, national debt rose by €144 billion to €2.84 trillion, pushing the debt-to-GDP ratio to 63.5 percent.

Some may recall the Maastricht limit, which capped debt at 60 percent. Those times are long gone, and the official debt numbers are, of course, grossly misleading.

For years—especially since the banking bailouts 15 years ago—the government has operated shadow budgets. Hoping the public won’t dig into fiscal details, these rarely illuminated debt channels are declared “special funds,” off the official books. Over 20 such hidden debt pots inflate actual state debt by at least €550 billion. Germany’s real debt likely sits near 80 percent of GDP and could exceed 85 percent by the end of this fiscal year.

The most infamous of these special funds originates from the debt crisis 15 years ago. The Financial Market Stabilization Fund (FMS) provided €400 billion in government guarantees and €80 billion in potential recapitalizations. Ultimately, €168 billion in guarantees and around €30 billion in direct transfers to financial institutions were used, while roughly €50 billion in debts from that era remain.

One of the largest black funds in federal history. Only Merz’s half-trillion-euro special fund will surpass this scale. Lesson learned: state financing has become an undeniable Ponzi scheme. Bond markets will ultimately dictate when the fiat money spree ends—they are the final arbiters of decades of political chaos.

Merz and his debt-hungry, insatiable finance minister are deliberately driving state spending to dizzying heights, yet must acknowledge that the heavily damaged German “economic tanker” can no longer move forward.

To buy time, the tragicomic duo plans to tighten middle-class taxes to the limit, holding taxpayers accountable for their fiscal free-for-all.

This is irresponsible, economically destructive policy unseen in Germany since WWII—the construction of a new socialism.

Against this backdrop, the Bundesbank president urged a return to sound budget planning. Deficits must be reduced mid-term without cutting essential infrastructure. Sadly, Nagel stopped short of endorsing free-market principles outright, missing the chance to clarify that the diversion of additional debt via special funds is systemic.

Policy cannot be fiscally restrained as long as bond markets are manipulated by monetary policy. According to the ifo Institute, 95 percent of this additional debt was added to the pre-existing debt binge and diverted. Social policy with a money printer—this is how far German fiscal policy has sunk.

Those seeking the real debt picture must dig deep—including pension obligations and current retirement promises. The scale of these liabilities defies imagination.

Germany—and nearly all of the EU—is trapped in a debt spiral. Turmoil in capital markets, broad restructuring, and massive wealth and debt redistribution loom. A standalone debt haircut would be systemic death: it would shrink circulating fiat credit and trigger a deflationary shock beyond the capacity of banks to absorb—a dead-end.

When will Germany begin monetizing its treasure, its massive gold reserves? Four years ago, the government under then-Chancellor Olaf Scholz pressured the Bundesbank to sell part of its gold to fund the defense special fund.

“Top” economists at Spiegel were reportedly inflamed by this idea—in these circles, the significance of collateralized, limited-quantity assets is poorly understood, even though they may one day underpin a new monetary regime.

It is fortunate that Nagel held the firewall against political adventurers and media amateurs. The Bundesbank may one day play a decisive role in a severe currency and debt crisis.

* * *

About the author: Thomas Kolbe is a German graduate economist. For over 25 years, he has worked as a journalist and media producer for clients from various industries and business associations. As a publicist, he focuses on economic processes and observes geopolitical events from the perspective of the capital markets. His publications follow a philosophy that focuses on the individual and their right to self-determination

Tyler Durden

Tue, 04/07/2026 – 06:30

https://www.zerohedge.com/economics/germanys-debt-spiral-bundesbank-chief-breaks-silence

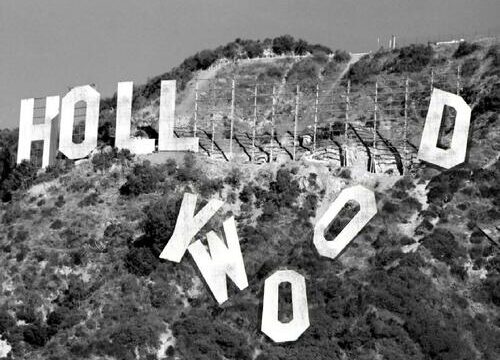

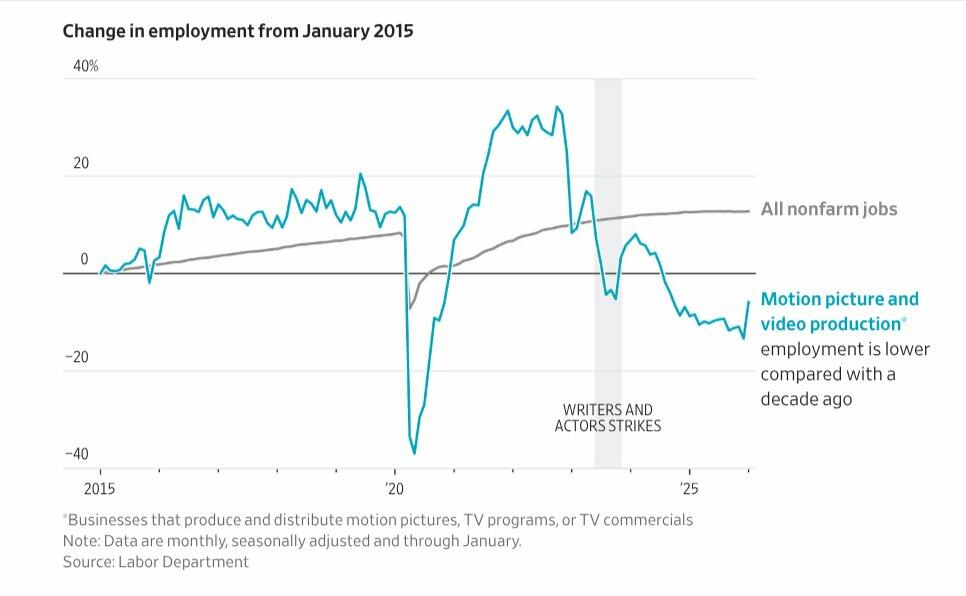

Death Of Hollywood In Two Charts

Death Of Hollywood In Two Charts

The nightmare story for Hollywood is playing out in real time for the world to see, as a century-old entertainment economy implodes and bears all the hallmarks of what happened to Detroit after the auto industry went bust.

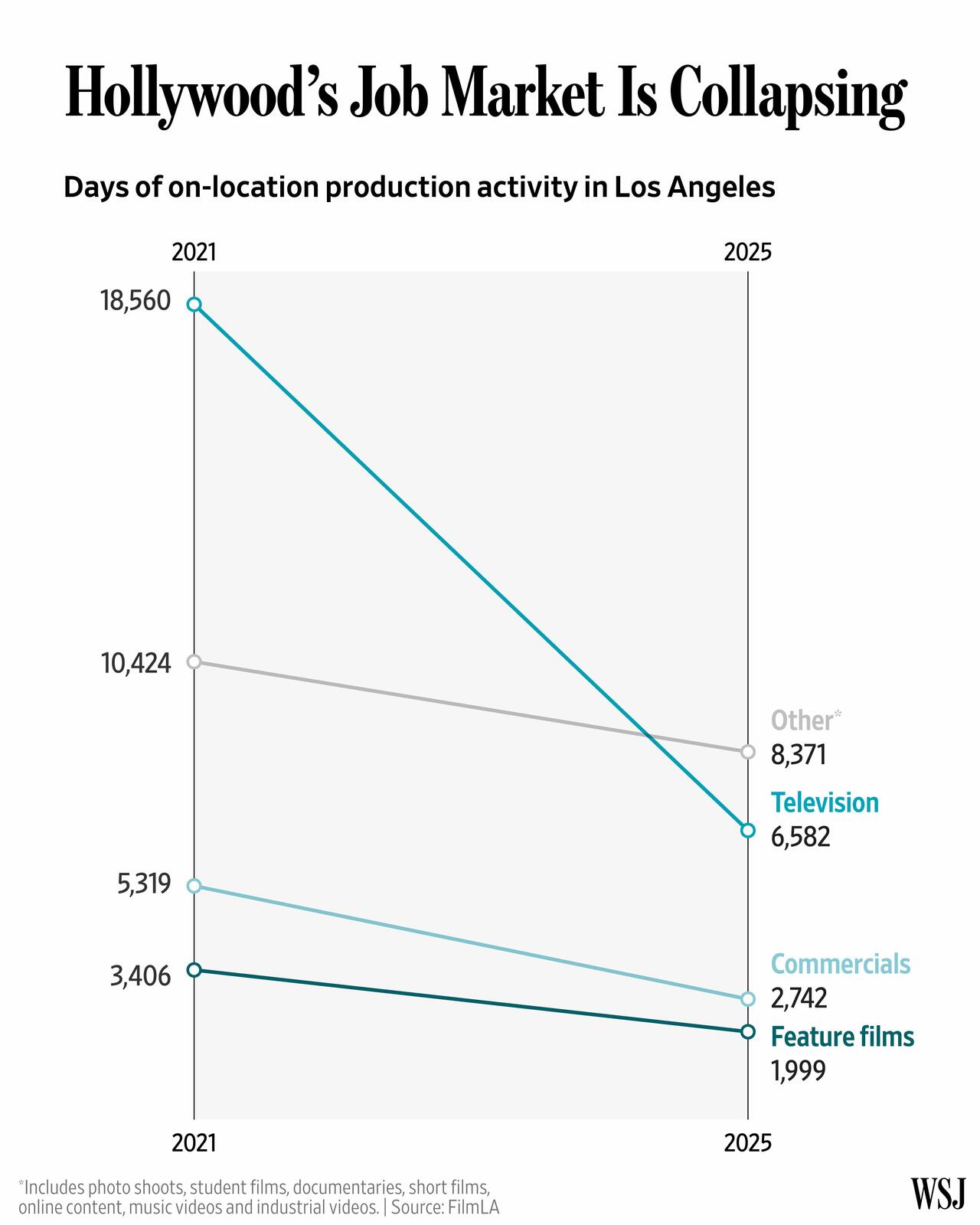

A new Wall Street Journal report describes the Hollywood job market as being in “collapse” mode, with employment in the industry down 30% from its late-2022 peak, while behind-the-scenes union workers logged 36% fewer hours last year than in 2022.

One big reason is that studios are making fewer shows and movies, and more of what they make is being filmed overseas or in other U.S. states that offer better tax incentives.

None of these overseas productions, or productions in other business-friendly states, should come as a surprise given that California is controlled by unhinged, one-party-rule Democratic Party leaders whose state-killing progressive policies have sparked a massive exodus of residents, businesses, and even billionaire tech bros.

The job market collapse in Hollywood has led to increasing calls for a federal production tax credit, with lobbyists linked to studios saying that a 15% federal incentive, on top of state subsidies (which typically range from 20% to 40%), could help break the production bust cycle and reshore more production back to the state.

But tax incentives won’t solve the job crisis on their own. With crazed liberal elites left holding the bag of studio garbage, younger audiences are spending more time on YouTube, TikTok, and Instagram for video consumption, while an increasing number of Americans have boycotted films and TV shows they consider “woke.”

The regime’s propaganda machine is collapsing under the weight of its own irrelevance. Hollywood exists solely to launder the radical leftist agenda into the minds of the youth. They despise the audience they claim to serve. This victory proves the market rejects their synthetic…

— Saggezza Eterna (@FinalTelegraph) February 1, 2026

“The biggest question now is whether the current downturn is temporary,” the WSJ report asked.

Well, in WSJ’s own words, the job bust will likely go into hyperdrive in the era of AI …

“Artificial intelligence, meanwhile, could eliminate more production jobs or spark a new production boom if the technology enables content to be made less expensively.”

Ben Horowitz says a famous Hollywood friend told him half the movie they’re making is AI.

It’s collapsing the cost of filmmaking, and when creation gets cheap enough, entirely new mediums could emerge.

Source: @bhorowitz at Columbia Business School pic.twitter.com/B2uL2S68t4

— a16z (@a16z) October 5, 2025

To sum up, Hollywood’s sphere of left-wing influence is collapsing, and it is no longer taken seriously.

Beyond studios, in the world of corporate media, job losses are mounting for white-collar liberals …

Tyler Durden

Tue, 04/07/2026 – 05:45

Iranian Kurdish Groups Deny Receiving US Arms After Trump’s ‘Guns For Protesters’ Remark

Iranian Kurdish Groups Deny Receiving US Arms After Trump’s ‘Guns For Protesters’ Remark

Several Iranian Kurdish opposition groups on Monday denied reports that the US had armed them during anti-government protests and riots that erupted in January, leaving over 3,000 Iranians dead.

Mohammed Nazif Qaderi, a senior official from the opposition Kurdistan Democratic Party of Iran (KDPI), called the reports “baseless,” saying, “We haven’t received any weapons. The weapons we have are from 47 years ago, and we obtained them on the Islamic Republic’s battlefield, and we bought some from the market.”

“Our policy is not to make demonstrations violent and use harsh methods, rather we believe we must make our demands in a peaceful and civil manner without weapons,” Qaderi said.

The protests and riots began in January after the US Treasury deliberately created a shortage of US dollars in Iran’s heavily sanctioned economy, causing the Iranian currency to collapse. The uprising began with economic-driven demonstrations in Tehran’s Grand Bazaar, which saw shopkeepers shutter their stores.

Armed groups then used the protests that erupted in response as cover to carry out attacks against Iranian security forces and paramilitary groups, known as Basij. Rioters also attacked and burned government buildings and mosques.

Israeli media reported that Mossad had agents on the ground in Iran to organize armed groups and create chaos in advance of the US-Israeli bombing campaign launched weeks later, on 28 February.

The Kurdish denial came one day after US President Donald Trump admitted for the first time during an interview with Fox News that the US attempted to ship “a lot of guns” to anti-government protesters in Iran.

Trump appears to confirm that the US pursued a Syria scenario in Iran earlier this year.

Thousands of Iranians were killed as security forces cracked down on unrest. At the time, Iranian authorities claimed many victims were either caught in crossfire or armed militants. https://t.co/ISzAXgph9N

— Mohammad Ali Shabani (@mashabani) April 5, 2026

While confirming the intent to arm the uprising that began in late 2025, Trump claimed the operation failed because the Kurds, who were used as the delivery channel, “kept the weapons” for themselves instead of passing them to the demonstrators.

This blunt disclosure not only provides the Iranian government with direct evidence of US interference but also publicly blames the US’s Kurdish allies for the missing arms.

In response to Trump’s comments, Amjad Hussein Panahi, head of communications for Komala of the Toilers of Kurdistan, stated, “We assure you we haven’t received a single bullet or weapon from any country or place, and we’re not aware of the existence of such a thing; what we have is our own.”

Reports first emerged that the CIA was working to arm Kurdish forces in an effort to foment an uprising in Iran in early March.

Trump:

We sent some guns; they were supposed to go to the people of Iran. You know what happened? The people we sent them through kept them.

I am very upset with a certain group of people, and they will pay a big price for that. pic.twitter.com/dACg5aZyMS

— Clash Report (@clashreport) April 6, 2026

Multiple people familiar with the plan told CNN that the Trump administration had been in active discussions with Iranian opposition groups and Kurdish leaders in Iraq. The CIA wished to provide weapons and air support to Kurdish militants as part of an operation to topple the Iranian government.

Tyler Durden

Tue, 04/07/2026 – 05:00

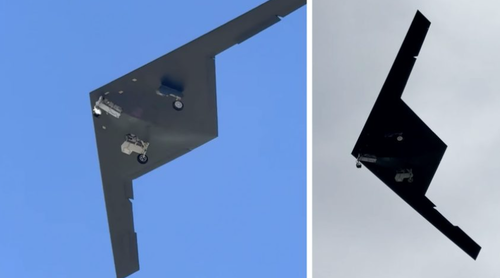

RQ-180 Spy Drone Reappears Again In Greece As Larissa Air Base Backs U.S. Recon Ops

RQ-180 Spy Drone Reappears Again In Greece As Larissa Air Base Backs U.S. Recon Ops

New footage of what appears to be the highly secretive Northrop Grumman RQ-180 stealth surveillance drone has surfaced near Larisa, Greece, according to the aviation outlet The Aviationist.

The RQ-180 apparently appeared in daylight hours on approach to landing at Larisa Air Base, home to the Hellenic Air Force’s 110 Combat Wing. The footage offers one of the clearest views yet of the flying-wing spy drone and confirms it is neither the B-2 Spirit nor the B-21 Raider.

Screenshot from videos taken by Efthymios Siakaras near Larissa, Greece. (Image credit: The Aviationist/Efthymios Siakaras)

The aircraft has never been formally acknowledged in detail by the Pentagon, but the designation has circulated in defense reporting since at least 2013. Its core mission is to collect imagery, radar, and signals intelligence in places where a non-stealth drone, such as the Global Hawk, would be too vulnerable.

The earliest video of the RQ-180, which could be among the first-ever glimpses of the drone, emerged in late March and was first reported by the local Greek news website OnLarissa.

The Aviationist pointed out this latest footage only suggests that “Larissa is in fact being used as a regular forward operating location for the RQ-180.”

Larisa Air Base has already been used for MQ-9 Reaper reconnaissance operations in the region. The base is part of the Eastern Mediterranean support network, where Reuters reported that Western militaries increased their presence last month.

The RQ-180’s most likely role in the US-Iran conflict is reconnaissance.

Tyler Durden

Tue, 04/07/2026 – 04:15

Europe’s Climate Policy Forces Industry Into Retreat; Even Its Critics Are Folding

Europe’s Climate Policy Forces Industry Into Retreat; Even Its Critics Are Folding

Submitted by Thomas Kolbe

In the media business, five months is an eternity. And it does indeed seem like an eternity has passed since Christian Kullmann, CEO of the German chemical giant Evonik, sharply criticized European climate policy at the end of October.

At the time, Kullmann gave an interview to Süddeutsche Zeitung, in which he called—if not for the outright abolition—then at least for a significant weakening of the EU-wide CO₂ emissions trading system, given the dramatic state of the economy.

Kullmann rightly pointed out that there is probably no stricter CO₂ regime anywhere in the world than in the EU. And since the climate, as we know, has no borders, he argued it makes little sense to disadvantage domestic cutting-edge technology in this way. He explicitly referred to the costly CO₂ trading system, which drained a staggering €21.4 billion from the German economy last year alone—under the banner of climate policy through this relatively new mechanism.

Five months after these remarkable statements—briefly breaking the long-standing silence of German industrial leaders—the question must be asked whether there is anywhere else in the world a comparable project to the EU’s CO₂ regime. With the United States abandoning its policy of artificial energy scarcity, its war on conventional energy production, and heavy-handed regulation of its own industrial base, the EU now stands alone in its ideological campaign against economic rationality. No one else seems willing to join the chorus of Europe’s climate apocalypticism.

This European isolationism may elsewhere be perceived as a form of late-stage counter-colonization—a return flow of capital from remorseful Europeans willing to accept self-imposed sacrifice to help other regions get back on their feet. Around the world, this selflessly naive “degrowth suicide” is welcomed, as it delivers not only so-called climate support from European funds but, more importantly, accelerated industrial investment from European companies—served on a silver platter by eco-socialist policymakers. A civilizational ingredient that, it seems, Europe itself now believes it can do without.

In China, one has learned to remain quiet when a geopolitical rival makes mistake after mistake—as is currently the case with European climate policy. Energy-intensive firms like Evonik are penalized by CO₂ pricing with an artificial competitive disadvantage. Once embedded in political and administrative structures, this amounts to a genuine stimulus program for foreign industrial locations.

At the same time, China—like the increasingly deregulated United States under President Donald Trump—is developing a powerful vacuum effect in global capital markets. The world is benefiting from German engineering and European capital.

This dynamic is particularly evident in the chemical industry. As a highly energy-intensive sector, it has suffered one of the hardest blows from European climate policy, alongside the automotive industry. Kullmann’s warning about the erosion of economic foundations was more than justified—but it came far too late and remained, for a time, a lone voice in the wilderness.

Since 2018, Germany’s chemical industry has lost roughly a quarter of its production capacity. The sector is operating at an average capacity utilization of just 70%, a level that reflects a sectoral depression not seen in Germany since the end of World War II.

Yet the worse the economic situation becomes, the more firmly German policymakers cling to their belief in the green transformation. Corporate silence is secured by a massive subsidy machine, just as the sympathetic media sector provides the shrill soundtrack to the broader economic decline.

Tactically astute from a media standpoint, Brussels—under pressure from European industry—has agreed to ease some pressure from the CO₂ cost burden. The European Commission is expected to temporarily freeze the volume of circulating certificates within the market stability reserve in order to stabilize prices.

For Evonik CEO Kullmann, the outcome presented by Brussels appears acceptable. His once sharp criticism of the CO₂ mechanism has mysteriously vanished into the media ether. The change of heart clearly follows the promise of further subsidies.

A destructive mechanism has emerged between large corporations and an eco-socialist political leadership. At the media level, corporate executives and political actors stage a kind of ping-pong game that simulates critical debate and conflicting interests at the highest levels of decision-making.

Evidently, there is no willingness to even slow down the ongoing transfer of wealth—from the productive sectors of society to politically favored extractive sectors such as the green economy—even amid prolonged economic stagnation. The economic and social consequences of this policy are, for now, being conveniently ignored in both Brussels and Berlin.

* * *

About the author: Thomas Kolbe is a German graduate economist. For over 25 years, he has worked as a journalist and media producer for clients from various industries and business associations. As a publicist, he focuses on economic processes and observes geopolitical events from the perspective of the capital markets. His publications follow a philosophy that focuses on the individual and their right to self-determination

Tyler Durden

Tue, 04/07/2026 – 03:30

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}