Category: News

Australia to tighten gun laws after Bondi Beach Hanukkah massacre

SYDNEY — Australian leaders promised Monday to immediately overhaul already-tough gun control laws after a mass shooting targeted a Hanukkah celebration on Sydney’s Bondi Beach. At least 15 people died in the attack, which has fueled criticism that authorities are not doing enough to combat a surge in antisemitic crimes.

Among the new measures proposed would be a limit on the number of guns someone can own and a review of licenses held over time. Those and other actions would represent a significant update to the landmark national firearms agreement, which virtually banned rapid-fire rifles after a gunman killed 35 people in Tasmania in 1996, galvanizing the country into action.

“The government is prepared to take whatever action is necessary. Included in that is the need for tougher gun laws,” Prime Minister Anthony Albanese said.

The violence erupted at the end of a summer day when thousands had flocked to Bondi Beach, an icon of Australia’s cultural life. They included hundreds gathered for the Chanukah by the Sea event celebrating the start of the Jewish festival with food, face painting and a petting zoo. Albanese called the massacre an act of antisemitic terrorism that struck at the heart of the nation.

Police shot the two suspected gunmen, a father and son. The 50-year-old father died at the scene. His 24-year-old son remained in a coma in hospital on Monday, Albanese said. Police won’t reveal their names.

At least 38 other people are being treated in hospitals.

Among those is a man who was captured on video appearing to tackle and disarm one apparent assailant, before pointing the man’s weapon at him, then setting the gun on the ground.

The man was identified by Home Affairs Minister Tony Burke as Ahmed al Ahmed. The 42-year-old fruit shop owner and father of two was shot in the shoulder.

Al Ahmed, an Australian citizen who migrated from Syria in 2006, underwent surgery on Monday, his family said.

Al Ahmed’s parents, who moved to Australia in recent months, said their son had a background in the Syrian security forces.

“My son has always been brave. He helps people. He’s like that,” his mother, Malakeh Hasan al Ahmed, told Australian Broadcasting Corp. through an interpreter.

Authorities had investigated one of the suspected gunman

Albanese confirmed that Australia’s main domestic spy agency, the Australian Security Intelligence Organization, had investigated the younger suspected gunman for six months in 2019.

The ABC reported that the agency had examined the son’s ties to a Sydney-based Islamic State group cell. Albanese did not describe the associates, but said the agency was interested in them rather than the son.

“He was examined on the basis of being associated with others and the assessment was made that there was no indication of any ongoing threat or threat of him engaging in violence,” Albanese said.

Australia has gun laws meant to prevent mass attacks

The horror at Australia’s most popular beach was the deadliest shooting in almost three decades since the 1996 Port Arthur massacre. The removal of rapid-fire rifles has markedly reduced the death tolls from such acts of violence since then.

Albanese’s proposals to limit the number of guns someone can own and review licenses were announced after the authorities revealed that the older suspected gunman had held a gun license for a decade and amassed his six guns legally.

Leaders of the federal and state governments on Monday also proposed restricting gun ownership to Australian citizens, a measure that would have excluded the older suspect, who came to Australia in 1998 on a student visa and became a permanent resident after marrying a local woman. Officials wouldn’t confirm what country he had migrated from.

His son, who doesn’t have a gun license, is an Australian-born citizen.

The government leaders also proposed the “additional use of criminal intelligence” in deciding who was eligible for a gun license. That could mean the son’s suspicious associates could disqualify the father from owning a gun.

Chris Minns, premier of New South Wales where Sydney is the state capital, said his state’s gun laws would change, but he could not yet detail how.

“If you’re not a farmer, you’re not involved in agriculture, why do you need these massive weapons that put the public in danger and make life dangerous and difficult for New South Wales Police?” Minns asked.

Dozens being treated in hospitals

Among those hospitalized are two police officers. Those killed included a 10-year-old girl, a rabbi and a Holocaust survivor.

While none of the dead or wounded have been formally named by the authorities, the identities of those killed, who ranged in age from 10 to 87, began to emerge in news reports Monday.

Among them was Rabbi Eli Schlanger, assistant rabbi at Chabad of Bondi and an organizer of the family Hanukkah event that was targeted, according to Chabad, an Orthodox Jewish movement that runs outreach worldwide.

Israel’s Foreign Ministry confirmed the death of an Israeli citizen, but gave no further details. French President Emmanuel Macron said a French citizen, identified as Dan Elkayam, was among those killed.

Larisa Kleytman told reporters outside St Vincent’s Hospital in Sydney that her husband, Alexander Kleytman, was among the dead. The couple were both Holocaust survivors, according to The Australian newspaper.

Jewish leaders criticize government’s response to antisemitism

Over the past year, Australia has been rocked by antisemitic attacks in Sydney and Melbourne. Synagogues and cars were torched, businesses and homes graffitied and Jews attacked in those cities, where the vast majority of the nation’s Jewish population lives. Of Australia’s 28 million people, about 117,000 are Jewish, according to official figures.

The massacre provoked questions about whether Albanese and his government had done enough to curb rising antisemitism. Jewish leaders and the massacre’s survivors expressed fear and fury as they questioned why the men hadn’t been detected before they opened fire.

“There’s been a heap of inaction,” said Lawrence Stand, a Sydney man who raced to a bar mitzvah celebration in Bondi when the violence erupted to find his 12-year-old daughter.

“I think the federal government has made a number of missteps on antisemitism,” Alex Ryvchin, spokesperson for the Australian Council of Executive Jewry, told reporters gathered on Monday near the site of the shooting. “I think when an attack such as what we saw yesterday takes place, the paramount and fundamental duty of government is the protection of its citizens, so there’s been an immense failure.”

The Australian government has enacted various measures — including appointing a special envoy to combat antisemitism, toughening laws and investing in enhanced security for Jewish schools and synagogues — to counter a surge in antisemitism since Hamas attacked Israel on Oct. 7, 2023, and Israel responded with an offensive in Gaza.

Israeli Prime Minister Benjamin Netanyahu said Sunday that he warned Australia’s leaders months ago about the dangers of failing to take action against antisemitism. He claimed Australia’s decision, in line with scores of other countries, to recognize a Palestinian state “pours fuel on the antisemitic fire.”

Albanese in August blamed Iran for two of the previous attacks and cut diplomatic ties to Tehran. Authorities have not suggested Iran was linked to Sunday’s massacre.

https://www.chicagotribune.com/2025/12/15/bondi-beach-australia-gun-laws/

Lluvias torrenciales e inundaciones repentinas dejan 37 muertos en la ciudad marroquí de Safi

Por AKRAM OUBACHIR

CASABLANCA, Marruecos (AP) — Al menos 37 personas murieron a causa de las inundaciones provocadas por lluvias torrenciales en la ciudad costera de Safi, en Marruecos, informó el lunes el Ministerio del Interior.

Las autoridades marroquíes indicaron que las fuertes lluvias y las inundaciones repentinas durante la noche causaron daños en alrededor de 70 hogares y negocios y arrastraron 10 vehículos. El Ministerio del Interior reportó que 14 personas fueron hospitalizadas.

Medios locales publicaron que las escuelas anunciaron tres días de suspensiones de clases. Las lluvias también causaron inundaciones y daños en otras partes de Marruecos, incluyendo la ciudad norteña de Tetuán y la localidad montañosa de Tinghir.

Safi, una ciudad en la costa atlántica de Marruecos a más de 320 kilómetros (200 millas) de la capital, Rabat, es un importante centro para las industrias pesquera y minera críticas del país. Ambas emplean a miles de personas para capturar, extraer y procesar los productos para la exportación. La ciudad, con una población de más de 300.000 habitantes, alberga una importante planta de procesamiento de fosfatos.

Videos compartidos en redes sociales mostraron autos varados y parcialmente sumergidos cuando las aguas de la inundación avanzaban por las calles de Safi.

El cambio climático ha hecho que los patrones climáticos sean más impredecibles en Marruecos. El norte de África ha sido azotado por varios años de sequía, endureciendo los suelos y haciendo que montañas, desiertos y llanuras sean más susceptibles a las inundaciones. El año pasado, las inundaciones en áreas montañosas y desérticas normalmente áridas causaron la muerte de casi dos docenas de personas en Marruecos y Argelia.

Las inundaciones de esta semana ocurrieron después que 22 personas murieran en el colapso de dos edificios en la ciudad marroquí de Fez. Marruecos ha invertido en iniciativas de gestión de riesgos de desastres, aunque los gobiernos locales a menudo no hacen cumplir los códigos de construcción y los sistemas de drenaje pueden ser deficientes en algunas ciudades. Las inequidades en infraestructura fueron un foco de las protestas lideradas por jóvenes que recorrieron el país a principios de este año.

__ El periodista de The Associated Press Sam Metz contribuyó a este despacho desde Rabat, Marruecos.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

Chile Turns Hard To The Right: Tough-On-Crime, Anti-Immigration Candidate Easily Wins Presidency

Chile Turns Hard To The Right: Tough-On-Crime, Anti-Immigration Candidate Easily Wins Presidency

In an election where the decisive themes echoed mounting concerns in the Americas and Europe, a conservative who’s vowed to crack down on illegal immigration and crime trounced his Communist opponent in Sunday’s presidential election in Chile. The result confirms a major political current that now has many Latin American countries embracing right-wing politics.

Jose Antonio Kast has promised to build physical barriers on the country’s northern frontier (Esteban Felix – AP via El Pais)

With 98% of the votes counted, 57-year-old José Antonio Kast was coasting to a 58%-to-42% clobbering of Jeannette Jara, a member of the Communist Party. Kast, a devout Roman Catholic and father of nine, will replace incumbent leftist President Gabriel Boric. It was Kast’s third presidential bid. Underscoring the comprehensiveness of his victory, Kast won all of Chile’s regions, including historic leftist strongholds.

“Chile will be free from crime again, free from anguish, free from fear,” said Kast in a victory speech at his campaign headquarters in the capital city of Santiago. “Chile needs order.” He assured supporters he would clamp down on criminals and “lock them up.” Supporters displayed banners with slogans like “Bye-Bye Illegals” and “Play Time is Over.”

Jose Antonio Kast embraces his wife at a rally in Chile

Crime weighed heavily in the contest, with 63% of Chileans saying it was their biggest worry. That’s about double the global average. Illegal immigration (40%) is the second-biggest concern. The two worries go hand-in-hand, as a 50% surge in murders from 2018 to 2024 is largely the work of international criminal gangs. Chile has more than 300,000 illegal immigrants, many of them Venezuelan.

At Kast’s victory rally, supporters wore red “Make Chile Great Again” hats, and confirmed that crime helped flip the country into the right-wing country. “I grew up in a peaceful Chile where you could go out in the street, you had no worry, you went out and you never had problems or fear,” 23-year-old engineering student Ignacio Segovia told Reuters. “Now you can’t go out peacefully.”

Kast will take office in March. Guiding off the inauguration date, he has repeatedly warned illegals of how many days they to self-deport, before his administration kicks them out. Self-deporation, Kast has said, will give them the opportunity to bring their possessions with them, while avoiding detention. “If you don’t leave voluntarily, we will detain you, retain you, expel you, and you’ll leave with what you have on,” said Kast. Kast’s looming victory had already had a striking effect, with wary illegal immigrants surging into Peru — so much so that Peruvian President Jose Jeri declared a state of emergency in late November. Meanwhile, authorities along Chile’s border say illegal entries have plummeted.

This is Chile as thousand celebrate the election of a right wing government. Finally defeating the Unity for Chile coalition which includes socialists & communists.

Sick of crime, immigration & ideology, the people want their country back.

— Bernie (@Artemisfornow) December 15, 2025

Writing on X, Argentinian President Javier Milei was exuberant about the “crushing victory” of Kast, whom he described as a friend, adding:

“One more step for our region in defense of life, freedom, and private property. I am certain that we will work together so that America embraces the ideas of freedom and we can free ourselves from the oppressive yoke of twenty-first century socialism…!!!”

Milei also posted a map depicting South America’s large number of right-wing governments, saying, “The left retreats, freedom advances.” Chile joins Argentina, Paraguay, Peru, Bolivia, Ecuador as countries with right or center-right governments. The Bolivian outcome earlier this year ended nearly 20 years of socialist rule.

LA IZQUIERDA RETROCEDE

LA LIBERTAD AVANZA

VLLC! pic.twitter.com/TfXucNdCJY

— Javier Milei (@JMilei) December 14, 2025

Which country will be next?

Tyler Durden

Mon, 12/15/2025 – 09:15

Authorities say they will release person of interest detained in Brown University shooting

PROVIDENCE, R.I. — A person of interest detained after a Brown University shooting that killed two students and injured nine will be released after law enforcement authorities determined there was no basis to keep the individual in custody, officials said Sunday night.

The disclosure, made at a hastily convened late night news conference, represents a dramatic setback in an investigation into killings that set off hours of chaos on the Ivy League campus and unravels progress that authorities thought they had made earlier in the day when they detained a man at a Rhode Island hotel in connection with the attack.

No current suspect in deadly shooting

The release of the lone person of interest leaves law enforcement without any known suspect, with officials pledging to redouble efforts in the investigation by canvassing for video surveillance that could help pinpoint the killer’s identity.

“We have a murderer out there,” said Attorney General Peter Neronha, while Providence Mayor Brett Smiley acknowledged that ”the news is likely to cause fresh anxiety for our community.”

Despite an enhanced police presence at Brown, officials are not recommending another shelter-in-place order like the one that followed the Saturday afternoon shooting, when hundreds of officers searched for the shooter and urged students and staff to shelter in place. The lockdown, which stretched into the night, was lifted early Sunday, but authorities had not yet released information about a potential motive.

On Sunday morning, officials took into custody a person of interest at a Hampton Inn hotel in Coventry, Rhode Island, about 20 miles (32 kilometers) from Providence. Two people familiar with the matter identified that individual as a 24-year-old man from Wisconsin, though authorities never released the individual’s name.

“I’ve been around long enough to know that sometimes you head in one direction and then you have to regroup and go in another and that’s exactly what has happened over the last 24 hours or so,” Neronha said.

He said that “certainly there was some degree of evidence that pointed to the individual” who’d been taken into custody but “that evidence needed to be corroborated and confirmed. And over the last 24 hours leading into just very, very recently, that evidence now points in a different direction.”

Shooting occurred during busy period on campus

The shooting occurred during one of the busiest moments of the academic calendar, as final exams were underway. Brown canceled all remaining classes, exams, papers and projects for the semester and told students they could leave campus, underscoring the scale of the disruption and the gravity of the attack.

As police scoured the area for the shooter, many students remained barricaded in rooms while others hid behind furniture and bookshelves. One video showed students in a library shaking and wincing as they heard loud bangs just before police entered the room to clear the building.

University President Christina Paxson teared up while describing her conversations with students both on campus and in the hospital.

“They are amazing and they’re supporting each other,” she said at a news conference. “There’s just a lot of gratitude.”

The gunman opened fire inside a classroom in the engineering building, firing more than 40 rounds from a 9 mm handgun, a law enforcement official told AP. Two handguns were recovered when the person of interest was taken into custody and authorities also found two loaded 30-round magazines, the official said. One of the firearms was equipped with a laser sight that projects a dot to aid in targeting, said the official, who was not authorized to discuss the investigation publicly and spoke to AP on the condition of anonymity.

One student of the nine wounded students had been released from the hospital, said Paxson. Seven others were in critical but stable condition, and one was in critical condition.

Durham Academy, a private K-12 school in Durham, North Carolina, confirmed that a recent graduate, Kendall Turner, was critically wounded. The school said her parents were with her.

“Our school community is rallying around Kendall, her classmates, and her loved ones, and we will continue to offer our full support in the days ahead,” the school said.

Community comes together to remember victims

On Sunday evening, city leaders, residents and others gathered at a park to honor the victims. The event originally was scheduled as a Christmas tree and Hanukkah menorah lighting.

“For those who know at least bit of the Hanukkah story, it is quite clear that if we can come together as a community to shine a little bit of light tonight, there’s nothing better that we can be doing,” Mayor Brett Smiley said at a news conference earlier in the day.

Smiley said he visited some wounded students and was inspired by their courage, hope and gratitude. One told him that active shooting drills done in high school proved helpful.

“The resilience that these survivors showed and shared with me, is frankly pretty overwhelming,” he said.

Exams were underway when the shooting began

Investigators were not immediately sure how the shooter got inside the first-floor classroom at the Barus & Holley building, a seven-story complex that houses the School of Engineering and physics department. The building includes more than 100 laboratories, dozens of classrooms and offices, according to the university’s website.

Engineering design exams were underway. Outer doors of the building were unlocked but rooms being used for final exams required badge access, Smiley said.

Emma Ferraro, a chemical engineering student, was in the lobby working on a final project when she heard loud pops. Once she realized they were gunshots, she darted for the door and into a nearby building where she waited for hours.

Surveillance video released by police showed a suspect, dressed in black, walking from the scene.

Former ‘Survivor’ contestant left the building just before shooting

Eva Erickson, a doctoral candidate who was the runner-up earlier this year on the CBS reality competition show “Survivor,” said she left her lab in the engineering building 15 minutes before shots rang out.

The engineering and thermal science student shared candid moments on “Survivor” as the show’s first openly autistic contestant. She was locked down in the campus gym following the shooting and shared on social media that the only other member of her lab who was present was safely evacuated.

Brown senior biochemistry student Alex Bruce was working on a final research project in his dorm across the street from the building when he heard sirens outside.

“I’m just in here shaking,” he said, watching through the window as officers surrounded his dorm.

Brown, the seventh-oldest higher education institution in the U.S., is one of the nation’s most prestigious colleges, with roughly 7,300 undergraduates and more than 3,000 graduate students.

https://www.chicagotribune.com/2025/12/15/brown-university-shooting/

Mandatario de Perú invita a presidente electo Kast de Chile a gabinete binacional en 2026

Associated Press

LIMA (AP) — El presidente interino de Perú, José Jerí, invitó al presidente electo de Chile, José Antonio Kast, a realizar un gabinete binacional en el segundo bimestre de 2026 y coincidió en enfrentar de manera conjunta el crimen transnacional, informaron el lunes las autoridades peruanas.

Jerí felicitó por teléfono a Kast la víspera por su victoria en la segunda vuelta presidencial de Chile “y le deseó los mayores éxitos” en su próximo gobierno que tomará posesión el 11 de marzo de 2026, dijo en un comunicado la Secretaría de Prensa del palacio presidencial peruano.

Ambos destacaron los vínculos de amistad entre Perú y Chile, y coincidieron “especialmente en la necesidad de enfrentar de manera conjunta la criminalidad y la delincuencia transnacional”.

En noviembre durante su campaña electoral Kast, un ultraderechista del Partido Republicano, prometió una política de mano dura contra la inmigración irregular y anunció que iba a expulsar a todas las personas indocumentadas de Chile una vez que asuma la presidencia.

A inicios de diciembre Chile y Perú acordaron realizar patrullajes conjuntos e incrementar la cooperación policial para enfrentar el creciente flujo migratorio en su frontera común, un día después de que militares peruanos empezaran a desplegarse a zonas limítrofes tras el estado de emergencia decretado por Perú.

Ambos países crearon un comité binacional de cooperación migratoria que busca remediar la escalada de tensión en la frontera norte de Chile, que alcanzó su ápice a fines de noviembre cuando decenas de migrantes, en su mayoría venezolanos, fueron impedidos de ingresar a Perú por no contar con los papeles necesarios.

Here’s How Markets Have Performed Since The Start Of America’s MAGA Experiment

Here’s How Markets Have Performed Since The Start Of America’s MAGA Experiment

By Eric Peters, CIO of One River Asset Management

MAGA: I remember 2017 well. It brought me to one knee. Trump had won the election in late 2016. The world braced itself for the chaos that was to come. Of course, we should all have known better. That’s not how markets work. Only rarely does an Artificial Superintelligence give investors extraordinary profits without inflicting ungodly pain. When it does give unearned gifts, it is to tempt us to foolishly bet on the obvious in some future market cycle. No ASI would ever operate in consistently predictable ways. Anyhow, over the course of 2017, the beginning of America’s MAGA experiment, here’s what happened in markets:

Dec 31 2016 – Dec 12 2017: S&P 500 +19.0% and VIX -4.12 at +9.92. Nikkei +19.6%, Shanghai +5.7%, Euro Stoxx +8.4%, Bovespa +22.6%, MSCI World +19.0%, MSCI Emerging +29.0%, Bitcoin +1711.8%, and Ethereum +8063.3%. USD rose +9.2% vs Turkey, +2.1% vs Brazil, and +0.7% vs Indonesia. USD fell -10.4% vs Euro, –7.4% vs Mexico, -7.3% vs Sterling, -5.2% vs India, -4.7% vs China, -4.6% vs Australia, -4.3% vs Canada, -3.8% vs Russia, -2.9% vs Yen. Gold +6.2%, Silver -3.9%, Oil +0.3%, Copper +19.7%, Iron Ore -20.1%, Corn -10.6%. 10yr Inflation Breakevens (EU +3bps at 1.28%, US -5bps at 1.92%, JP -12bps at 0.47%, and UK +5bps at 3.07%). 2yr Notes +64bps at 1.83% and 10yr Notes -4bps at 2.40%.

MAGA II: In 2017, the stock market grinded higher all year in an unprecedented fashion, so that by Dec 12, 2017, the VIX was below 10. Investors sold volatility aggressively, and the more they sold, the lower the VIX fell, reflexively. Which created the conditions for a series of volatility spikes that climaxed in Covid. In this first year of Trump II, we endured Independence Day, the VIX index hit 60, and we suffered so many policy flip flops that they barely affect the market at this point. Here’s how markets have done in the second stage of America’s MAGA experiment:

Dec 31 2024 – Dec 12 2025: S&P 500 +16.6% and VIX -1.67 at +15.68. Nikkei +27.4%, Shanghai +16.1%, Euro Stoxx +14.3%, Bovespa +32.8%, MSCI World +19.9%, MSCI Emerging +28.0%, Bitcoin -2.5%, and Ethereum -4.0%. USD rose +20.8% vs Turkey, +5.6% vs India, and +3.3% vs Indonesia. USD fell -29.9% vs Russia, -16.1% vs Sweden, -13.3% vs Mexico, -12.3% vs Brazil, -11.8% vs Euro, -6.8% vs Australia, -6.3% vs Sterling, -4.2% vs Canada, -3.3% vs China, and -0.9% vs Yen. Gold +55.0%, Silver +101.7%, Oil -15.6%, Copper +28.8%, Iron Ore +1.3%, Corn -2.5%. 10yr Inflation Breakevens (EU +2bps at 1.79%, US -7bps at 2.27%, JP +31bps at 1.78%, and UK -50bps at 3.01%). 2yr Notes -71bps at 3.53% and 10yr Notes -39bps at 4.19%.

MAGA III: There is so much more to America than its politics. At its core, America is the greatest business enterprise the world has ever known. Politicians fight over the fair distribution of its spoils, while engaging in international policy experiments that shift from generation to generation. It appears we’ve entered a phase that’s more focused on the Western Hemisphere than Europe and Asia. Investors will look to historical periods for parallels. Perhaps they’ll find some that prove helpful. Definitive. I’m of the mind to keep mine open, searching our Artificial Superintelligence for signals, signs. Here’s how markets have performed since the start of America’s MAGA experiment in late 2016:

Dec 31 2016 – Dec 12 2025: S&P 500 +207% and VIX +1.41 at +15.45. Nikkei +166%, Shanghai +26%, Euro Stoxx +61%, Bovespa +166%, MSCI World +154%, MSCI Emerging +60%, Bitcoin +9497%, and Ethereum +40147%. USD rose +1111% vs Turkey, +67% vs Brazil, +36% vs Chile, +33% vs Yen, +33% vs India, +29% vs Russia, +24% vs Indonesia, +23% vs South Africa, +9% vs Australia, +3% vs Canada, +2% vs Sweden, and +2% vs China. USD fell -13% vs Mexico, -10% vs Euro, and -8% vs Sterling. Gold +271%, Silver +288%, Oil +0.5%, Copper +115%, Iron Ore +21%, Corn +14.4%. 10yr Inflation Breakevens (EU +54bps at 1.79%, US +30bps at 2.27%, JP +119bps at 1.78%, and UK -1bp at 3.01%). 2yr Notes +235bps at 3.54% and 10yr Notes +174bps at 4.18%.

Tyler Durden

Mon, 12/15/2025 – 09:00

https://www.zerohedge.com/markets/heres-how-markets-have-performed-start-americas-maga-experiment

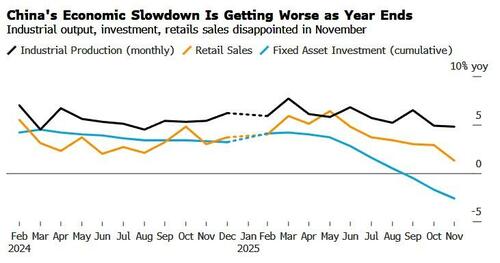

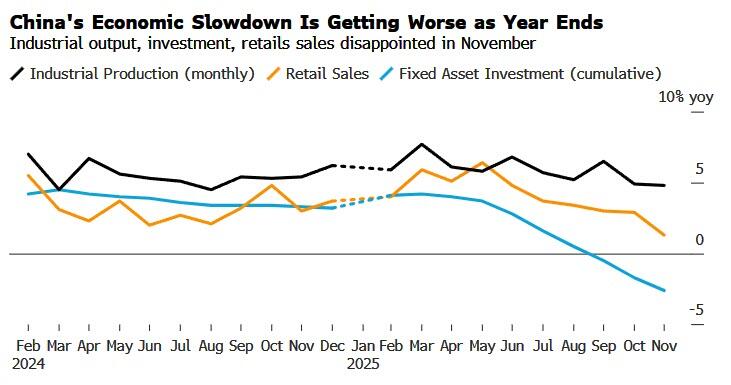

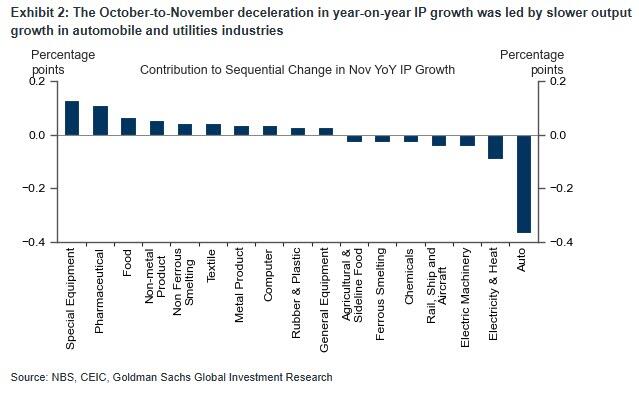

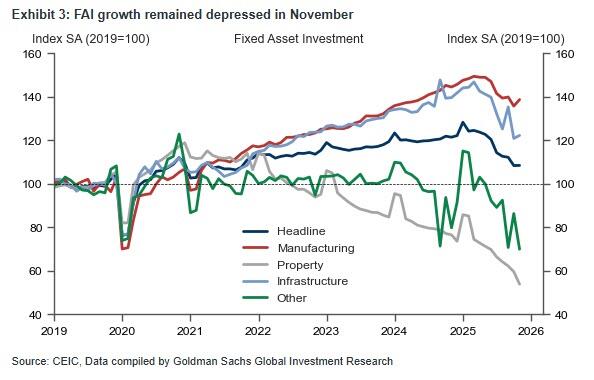

Xi Blasts “Reckless” Projects Exaggerating Growth After China Reveals Dismal Macro Data For November

Xi Blasts “Reckless” Projects Exaggerating Growth After China Reveals Dismal Macro Data For November

China’s economic momentum slowed broadly in November, with a marked weakening in consumer spending, adding pressure on Beijing to stabilize household and business demand in the world’s second-largest economy.

Industrial production (IP) growth edged down in year-on-year terms despite the notable improvement in export growth, with slower output growth in automobile and utilities industries more than offsetting faster output growth in the special equipment and pharmaceuticals industries.

Fixed asset investment (FAI) maintained its double-digit year-on-year contraction in November on a single-month basis, though we would not over-interpret its recent slump as our study suggests that the NBS statistical correction of previously over-reported data has played at least as large a role as fundamental factors (e.g., the “anti-involution” policies and a prolonged property downturn).

Retail sales growth dropped meaningfully in November despite a low base, reflecting slowing auto sales growth and the negative distortion from an earlier-than-usual start of the “Double 11” Online Shopping Festival (which had pulled forward some demand from November to October, similar to the patterns observed in June).

Year-on-year services industry output index growth – which is on a real basis and tracks tertiary (services) GDP growth closely – moderated in November.

Property sector weakness continued in November, while unemployment rates remained largely stable.

Regarding the labor market, the nationwide unemployment rate and the 31-city metric (not seasonally adjusted) both remained flat at 5.1% in November. The latest data available suggests the unemployment rate of the 16-24 age group declined to 17.3% in October from 17.7% in September, while Goldman cautions that this indicator may have underestimated the labor market challenges that younger generation is facing amid weak domestic demand, persistent deflation and fragile private sector confidence, because of the definition change.

Incorporating October-November activity data, Goldman’s GDP tracking model based on the production approach points to a small downside risk to our Q4 real GDP growth forecast of 4.5% yoy.

And with downside economic risks building, Bloomberg reports that Chinese President Xi Jinping lashed out at inflated growth numbers and vowed to crack down on the pursuit of “reckless” projects that have no purpose except showing superficial results.

“All plans must be based on facts, aiming for solid, genuine growth without exaggeration, and promoting high-quality, sustainable development,” Xi said last week, according to a report on Sunday in the People’s Daily, the Communist Party’s official newspaper.

“Those who act recklessly and aggressively without regard for reality, impose excessive demands, or deploy resources without careful consideration, must be held strictly accountable,” he said at the Central Economic Work Conference.

Xi used stark language to call for quality in economic gains and listed examples of wrongdoing such as unnecessarily huge industrial parks, disorderly expansion of local exhibitions and forums, inflated statistics and “fake construction kickoffs.”

Access to data in China can be sensitive and controlled, making it hard for observers to assess the health of the economy, but Xi’s latest remarks seem to suggest that he wants a revamp of the existing metrics used to evaluate local officials.

Finally, we note that the initial downturn in Chinese stocks was quickly bid back into positive territory after the ‘bad data’ as it appeared ‘bad news’ would be ‘good news’ from a ‘most stimmies’ perspective, but Xi’s rant dragged stocks down to end the day in the red…

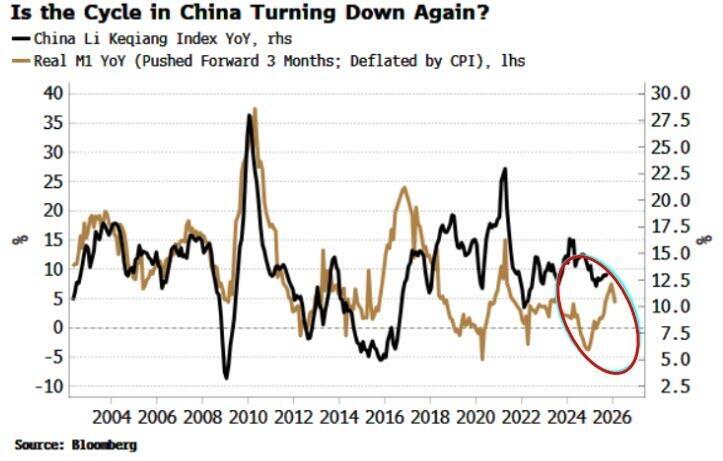

And as a reminder, we warned last week that the pace of money growth in China has slowed for a second month. If that’s sustained, global stocks could lose a hitherto supportive tailwind next year.

One snowflake doesn’t make a winter, but if M1 in China continues to pare back, that’s at least one tailwind global stocks won’t have next year.

Tyler Durden

Mon, 12/15/2025 – 08:45

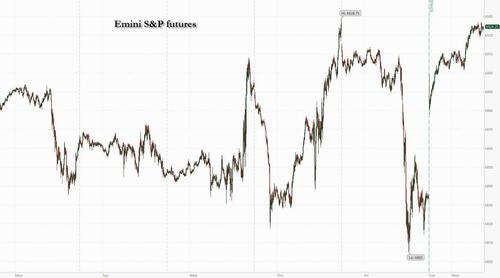

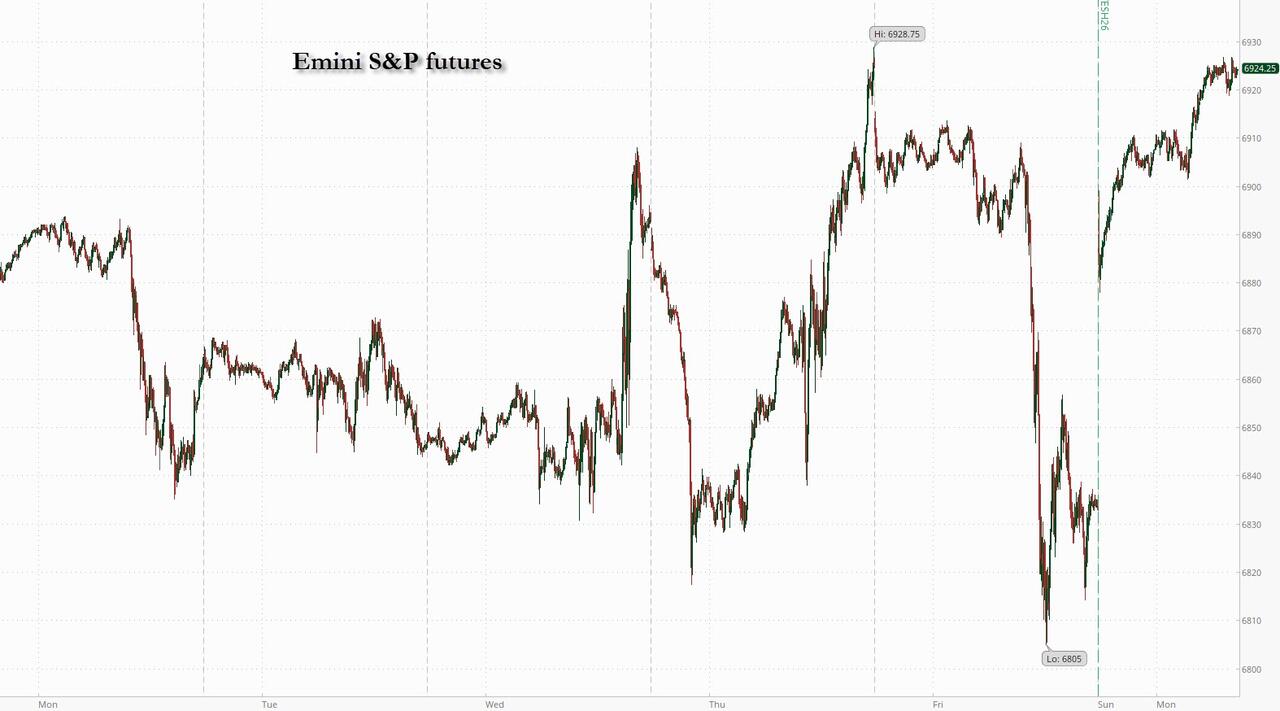

US Futures Recover Most Of Friday’s Dump As “Bad News Is Again Good News”

US Futures Recover Most Of Friday’s Dump As “Bad News Is Again Good News”

Stocks are set to recoup some of Friday’s tech-driven losses, with a big week of data releases ahead, as the last full week of 2025 comes witgh a bang. Still, sentiment seems a little shaky, with rising signs of skepticism over AI and debate about the extent of rate cuts next year. As of 8:00am ET, S&P 500 futures and Nasdaq 100 contracts both rose 0.5% after Friday’s 1.1% cash market slump in which technology sector fell 2.9%. In premarket trading, Nvidia leads Mag 7 gains, climbing 1.1% with the rest of the group largely in the green. European stocks climbed 0.8%. 10-year Treasury yields ticked lower and the dollar index traded at session lows as the yen surged on renewed bets the BOJ would hike rates this week. Bitcoin rallied 1.3% to $89,652, adding to signs that risk sentiment is steadying. Today’ key events include the December Empire manufacturing (8:30am) and NAHB housing market index (10am). Major releases later this week include November CPI Thursday. Fed speakers include Governor Miran (9:30am, 11am) and New York Fed’s Williams (10:30am).

In premarkt trading, Nvidia climbs 1.1% and is among leaders of a rebound in Magnificent Seven stocks after the group suffered a two-day drop amid concern over elevated spending and delays for projects tied to AI (Tesla +1.4%, Alphabet +0.7%, Amazon +0.4%, Apple +0.1%, Meta little changed, Microsoft is little changed).

Mining stocks are higher amid a renewed advance in metals prices.

Adobe (ADBE) slips 1.3% and ServiceNow (NOW) falls 4% after the pair were downgraded to underweight at Keybanc, which sees AI tools bringing a bigger hit to both software firms.

Dole (DOLE) climbs less than 1% on light trading after the produce company agreed to sell port and port operations in Guayaquil, Ecuador, for $75m in cash.

Entegris Inc. (ENTG) falls 2% after Goldman Sachs cut its recommendation on the semiconductor materials company to sell from neutral on slow wafer recovery.

GXO Logistics (GXO) declines 2.2% after the logistics company said Brad Jacobs will step down as non-executive chairman of the board, effective Dec. 31.

Immunome (IMNM) soars 27% after the biotech company announced positive topline results from its Phase 3 trial of varegacestat.

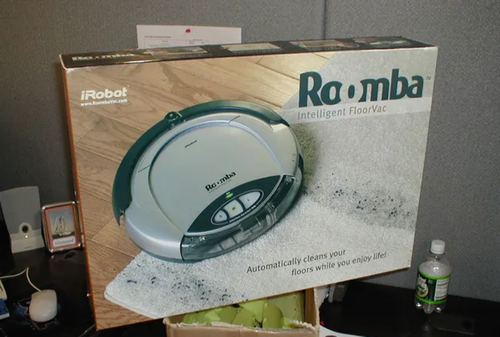

iRobot (IRBT) falls 72% after the company filed for bankruptcy and proposed handing over control to its main Chinese supplier.

Teradyne (TER) gains 3% after Goldman Sachs upgraded its recommendation to buy from sell, seeing an AI-driven demand uplift for the manufacturer of chip-testing equipment.

ZIM Integrated Shipping (ZIM) rises 4% after Calcalist reported that MSC has submitted a bid to purchase the Israeli shipping company, without saying where it got the information.

In corporate news, Roomba maker iRobot filed for bankruptcy and proposed handing over control to its main Chinese supplier. Korea Zinc plans to build a smelter in the US at an estimated cost of around $7.4 billion, backed by investments from the American government, to produce key materials used in chip-making, defense and aerospace.

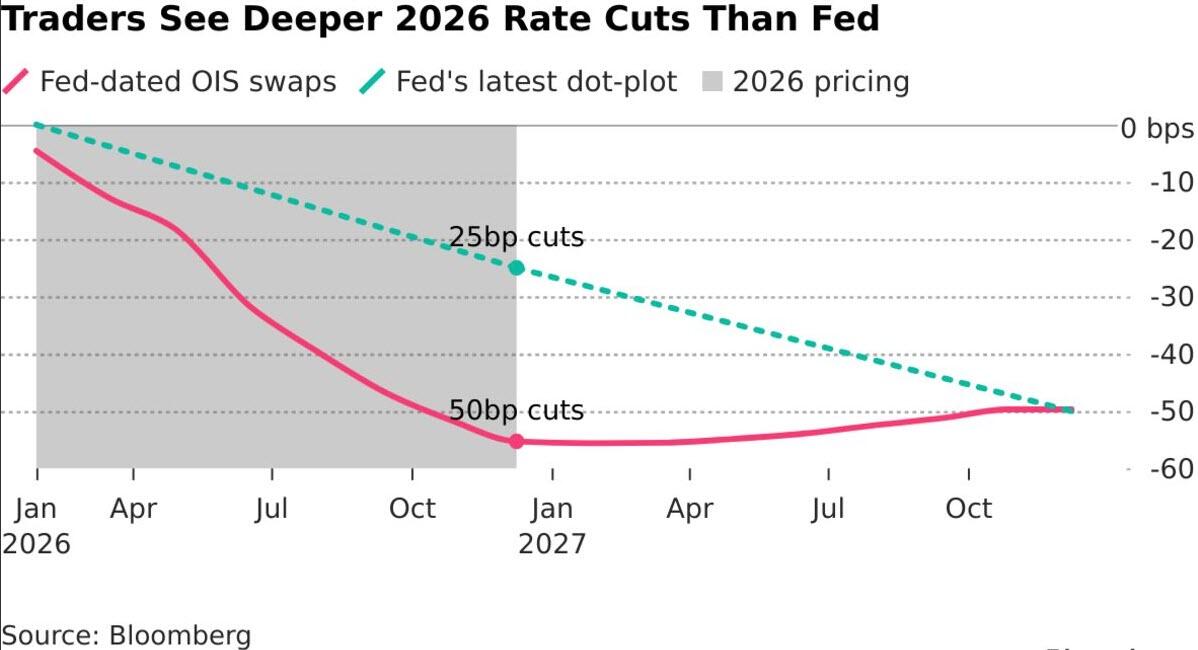

Traders are looking to delayed jobs and inflation data this week to help fill the void left by the US government shutdown as they build a picture on the economy and interest rates. Citigroup joined the upbeat chorus on the outlook for US stocks next year, while Morgan Stanley’ Michael Wilson wrote that the “good is bad/bad is good” trade is back, and weak jobs data on Tuesday could boost stocks as it would raise the probability of more rate cuts. The jobs number will also be critical for bond traders, who are betting on two rate cuts next year — one more reduction than the Fed is indicating.

“We are now firmly back into a good is bad/bad is good regime,” Morgan Stanley strategist Michael Wilson wrote in a note. “Moderate” weakness in the labor market weakness “Is likely to be received in a bullish context by equity markets,” he said.

Citi strategists led by Scott Chronert said they expect robust earnings growth will deliver a 13% rally next year for the S&P 500. That implies double-digit gains for a fourth year running, and echoes optimistic forecasts by banks including Morgan Stanley, Deutsche Bank and Goldman. “We anticipate an incremental shift from AI enablers to adopters/users in 2026, setting the stage for increased productivity improvement commentary across corporates,” Chronert wrote. “A generally supportive Fed is a key assumption in our playbook.”

Economists project a 50,000 increase in nonfarm payrolls and a 4.5% unemployment rate, consistent with a sluggish, but not rapidly deteriorating, labor market (our full preview will hit later today). The US data will help answer the question entering 2026 of whether the Fed is close to being done easing, after three straight cuts, or if it has to move more aggressively.

“We had the debate around closing our equities overweight, but we don’t believe the trend is yet ending,” said Philipp Lisibach, head of strategy and research at LGT Private Banking. “Exposure to AI continues to be rewarded, while rates and credit remain relatively unattractive. Equities still offer the most compelling risk-reward trade.”

As for the AI giants themselves, the debate among investors is whether to rein in exposure ahead of a potential bubble popping or double down on the game-changing technology. One big worry is rising depreciation expenses from the data center binge. Alphabet, Microsoft and Meta combined for about $10 billion in depreciation costs in 4Q 2023. That figure rose to nearly $22 billion in 3Q this year, and it’s expected to be about $30 billion by this time next year.

A final flurry of major central bank policy decisions is also due, with meetings at the Bank of England, the ECB and the Bank of Japan, among others. National Economic Council head Kevin Hassett said he’d consider Trump’s policy opinions if he’s picked to lead the Fed, but rate decisions would stay independent. And Ukraine and the US are due to hold a second day of talks in Berlin on Monday about a plan aimed at ending Russia’s war, with allied security guarantees for Kyiv a central focus of the negotiations.

In Europe, Stoxx 600 trades higher by 0.8%. Consumer stocks outperform on signs of better Chinese demand, while the health-care sector underperforms. Here are some of the biggest movers on Monday:

Juventus shares rise as much as 14%, the most in more than a year, after the Agnellis family’s investment vehicle Exor NV rejected an unsolicited bid by Tether Holdings to acquire the Italian football club.

Kering climbs as much as 4%, leading luxury stocks higher, after China vowed to increase financial support for key consumption areas.

Puma shares also rise as much as 4% on the news that China will strengthen coordination between the commerce and financial sectors to boost consumption.

Argenx shares fall as much as 9.7%, the most in more than seven months, after the biotechnology company discontinued its late-stage studies into thyroid eye disease.

Sanofi shares sink as much as 6.4% after its experimental multiple sclerosis drug got hit with two setbacks: a regulatory delay in the US as well as a failure in a late-stage clinical trial.

Rheinmetall leads European defense firms down, with its shares as much as 3.1% lower, after Ukrainian President Volodymyr Zelenskiy said he could accept security guarantees from the US and Europe instead of NATO membership amid ongoing peace talks.

Truecaller shares plummet as much as 29%, the most since 2023 and to a record low, after the Swedish caller ID platform guided for its 4Q ad revenues around 30% lower year-on-year.

Schweiter Technologies shares fall as much as 14%, hitting their lowest level since 2005, after the maker of composite panels issued a profit warning that Zurcher Kantonalbank says was a surprise.

Elsewhere, Chinese indexes edged lower after the latest data showed retail sales growth was the weakest since Covid, while investment slumped further. Asian shares also dropped, tracking Wall Street’s losses on Friday, with South Korea — a poster child for AI exuberance — slipping 1.8%.

In FX, the Bloomberg Dollar Index is down 0.2% with the yen top of the G-10 leaderboard ahead of an expected BOJ rate hike on Friday. Kiwi lags after RBNZ Governor Breman pushed back on investor bets over a rate hike next year.

In rates, treasury futures held small gains accumulated during European morning as the region’s bonds advanced. Global bond yields also lean lower. Gilt prices outperform 10-year equivalents from the US and Germany with the BOE set to cut rates by 25bps on Thursday. US yields are 1.5bp to 2.5bp richer across the curve with front-end tenors lagging slightly, flattening 2s10s spread by around 1bp. 10-year near 4.16% is 2.3bp lower on the day, slightly outperforming German and UK counterparts. IG dollar bond issuance slate empty, with this week expected to be the final window for any companies looking to raise capital in the debt markets before year-end. Treasury auctions this week include $13 billion 20-year bond reopening Wednesday and $24 billion 5-year TIPS Thursday. The week is packed with US economic data releases, including the delayed November jobs report on Tuesday.

In commodities, crude oil prices are now lower after failing to hold onto opening gains. Fed rate-cut bets also helped lift the price of gold on Monday. The yellow metal climbed for a fifth day to around $4,345 an ounce, approaching a record high; silver outperforms, higher by 2.9%. Bitcoin gains 1.5%.

US economic calendar includes December Empire manufacturing (8:30am) and NAHB housing market index (10am). Major releases later this week include November CPI Thursday. Fed speakers include Governor Miran (9:30am, 11am) and New York Fed’s Williams (10:30am).

Market Snapshot

S&P 500 mini +0.5%

Nasdaq 100 mini +0.5%

Russell 2000 mini +0.7%

Stoxx Europe 600 +0.8%

DAX +0.5%

CAC 40 +1%

10-year Treasury yield -2 basis points at 4.16%

VIX +0.6 points at 16.37

Bloomberg Dollar Index -0.1% at 1205.59

euro little changed at $1.1745

WTI crude -0.2% at $57.35/barrel

Top Overnight News

Affordability pressures are weighing heavily on the White House heading into next year’s midterm elections. They’re also offering cautious hope in Mexico and Canada that the U.S. won’t abandon its trilateral trade pact as the three countries enter a high-stakes review. Politico

Trump is reportedly not certain his economic policies will translate to midterm wins, while he said his US investments haven’t fully taken effect and stated that by the time they have to talk about the election, which is in another few months, he thinks their prices are in good shape: WSJ

White House economic adviser Hassett said he would consider US President Trump’s policy opinions, but added that the central bank would remain independent if he were to become the next Fed chair: BBG

Apollo Management took bets against technology companies vulnerable to AI, in which it is betting against several large loans to software makers and cutting exposure to the sector, according to FT.

SpaceX is moving forward with an insider share sale that values it at about $800 billion, setting up what could be the largest initial public offering of all time. WSJ, BBG

Volodymyr Zelenskiy signaled Ukraine may step back from its long-term goal of joining NATO if it can secure bilateral security agreements with the US, Europe and other states. It’s holding a second day of talks with the US in Berlin. BBG

Fannie and Freddie have snapped up more than $50 billion of home loans as Trump administration officials seek to drive down mortgage rates. BBG

The European Commission is expected on Tuesday to reverse the EU’s effective ban on sales of new combustion-engine cars from 2035, bowing to intense pressure from Germany, Italy and European automakers struggling against Chinese and U.S. rivals. EV makers say reneging on ban would yield more ground to China. RTRS

China’s economic momentum slowed broadly in November, with a marked weakening in consumer spending, adding pressure on Beijing to stabilize household and business demand in the world’s second-largest economy. Retail sales (+1.3% vs. the Street +2.9% and vs. +2.9% in Oct), industrial production (+4.8% vs. the Street +5% and vs. +4.9% in Oct), and investment (both fixed asset investment and property investment deteriorated in Nov). WSJ

Vanke, one of China’s largest real-estate companies, made a renewed effort to muster bondholder backing for an onshore debt repayment due this week and avoid a default after the state-backed developer’s plan was rejected, rekindling concerns about the nation’s crisis-hit property sector. RTRS

Japanese companies seem keen to raise wages again next year, despite many bracing for a tariff hit to profits, a central bank report shows days ahead of its next policy meeting. The findings will likely reinforce expectations that the central bank will raise interest rates to 0.75% from 0.5% this week. WSJ

BoJ officials are likely to start selling the central bank’s pile of exchange-traded funds as early as next month, according to people familiar with the matter, a process expected to take decades to complete. RTRS

Trade/Tariffs

US and Mexico reportedly struck a deal on Friday to settle the Rio Grande water dispute, which eases the bilateral tensions which had been stoked after US President Trump’s threat of an additional 5% tariff on Mexico if it did not provide additional water to help US farmers.

China’s Central Financial and Economic Affairs Commission Deputy Director said they will expand exports and increase imports in 2026.

China’s Customs allows dairy import products from Norway.

An Indian Trade Official said India is engaging with Mexico on higher tariffs to protect its own trade interests. Said Mexico’s primary target is not to hit Indian exports.

India has proposed a “preferential trade agreement” with Mexico.

India’s Trade Secretary said India and the US are close to a “framework” deal but won’t give a timeline.

EU plans a crackdown on very dangerous Chinese products sold on online platforms, including Alibaba (9988 HK) and Shein, according to FT.

France said conditions for an EU vote on a Mercosur deal are not yet met, despite recent progress, while France calls for the EU-Mercosur December meeting to be pushed back to continue work on mirror clauses.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly pressured at the start of a risk-packed week and following on from the tech-led declines stateside amid a rotation out of AI, while participants digested economic releases, including the BoJ Tankan and Chinese activity data. ASX 200 retreated with the declines led by mining, materials, resources and tech sectors, with the mood in Australia also sombre following a terror attack on Bondi Beach targeting a Jewish celebration. Nikkei 225 underperformed ahead of a widely anticipated BoJ rate hike later this week, while the quarterly BoJ Tankan survey showed sentiment of Large Manufacturers was at the highest in four years, which supports the case for a rate hike. Hang Seng and Shanghai Comp were subdued after the latest Chinese activity data disappointed and house prices continued to contract, with tech and biotech leading the declines in Hong Kong, while losses in the mainland were contained after reports that China is to issue ultra-long-term special government bonds in 2026 to fund major national strategies and security initiatives, as well as large-scale equipment upgrades and consumer goods trade-in programs.

Top Asian News

China is to issue ultra-long-term special government bonds in 2026 to fund major national strategies and security initiatives, as well as large-scale equipment upgrades and consumer goods trade-in programs.

China stats bureau spokesperson said China’s economy stabilised and improved in November, but the impact of changes in the external environment has deepened, and the conflict between strong domestic supply and weak demand is prominent. The spokesperson also noted that some industries and firms face difficulties, while authorities will step up counter-cyclical and cross-cyclical adjustments. Furthermore, it was stated that household consumption capability and confidence need to be further improved, with efforts to be made to stabilise jobs, boost income growth, and release consumption potential.

China Vanke’s (2202 HK) proposal for a one-year delay of repayment for a bond due December 15th was rejected by bondholders, which leaves a five-day grace period to make the CNY 2bln bond payment and avoid a potential default.

Hong Kong’s Democratic Party voted on Sunday to dissolve amid pressure from Beijing and previous alleged threats of severe consequences, including possible arrest if they did not disband, according to The Guardian.

BoJ is likely to begin selling its ETF holdings as soon as January, according to Bloomberg.

RBNZ Governor Breman said the economic outlook has evolved broadly in line with expectations, and the forward path for the Official Cash Rate published in the November monetary policy statement indicates a slight probability of another rate cut in the near term. However, she added that if economic conditions evolve as expected, the official cash rate is likely to remain at its current level of 2.25% for some time. Breman also commented that there continues to be signs that growth is recovering and financial market conditions have tightened since the November decision, beyond what is implied by the central projection for the OCR.

BoK said NPS agrees to extend its currency swap agreement for another year, with Bloomberg reporting that the NPS is to take a flexible approach to strategic FX hedging.

China NPC Standing Committee to hold a meeting between December 22-27. NPC Standing Committee to review draft revision to foreign trade law.

European bourses (STOXX 600 +0.7%) opened on a stronger footing and traded at elevated levels throughout the morning. Upside, which comes despite a broadly lower APAC session, where Chinese stocks were subdued after the latest Chinese activity data disappointed. European sectors are broadly in the green, with a cyclical bias as Autos leads whilst Healthcare underperforms; the latter has also been dragged down by losses in Sanofi (-4%) after the Co. flagged delays in an FDA decision for Tolebrutinib.

Top European News

Swiss SECO forecasts: US Tariff reduction has strengthened outlook 2025. Sees 2025 GDP (sports adj.) at +1.4% (prev. exp. +1.3%). Sees CPI +0.2% (prev. exp. +0.2%). 2026. Sees GDP (sports adj.) +1.1% (prev. exp. +0.9%). Sees CPI at +0.2% (prev. exp. +0.5%) 2027. Sees GDP (sports adj.) +1.7%. Sees CPI at +0.5%.

UK’s OFCOM launches a probe into BT (BT/ LN) and Three, following UK-wide outages in the summer

FX

G10s are mixed against the Dollar with clear outperformance in the JPY, whilst the Kiwi lags vs the USD after RBNZ’s Bremen said that the forward path for the official cash rate published in the November monetary policy statement indicates a slight probability of another rate cut in the near term.- DXY is a touch lower on the day, but likely a function of JPY strength (see below). No specific macro catalysts for the greenback as the week kicks off, but late on Friday, US President Trump said he was leaning towards Kevin Warsh or Hassett to lead the Fed. DXY trades within 98.29-98.48 parameters. The session is likely to focus on commentary from Fed’s Miran, expected to explain his dissent in last week’s FOMC meeting, while the influential Williams will speak on economic growth.

JPY is the clear outperformer in the G10 FX space, where the BoJ is set to raise rates for the first time since January 2025. Japan’s Tankan survey overnight bolstered the case for a hike in Friday’s meeting, where the reading suggested overall business sentiment improved in Q4 and inflation expectations stood pat at 2.4% for the 1, 3, and 5-year horizons. Markets currently assign a c. 80% probability that the BoJ lifts rates by 25bps on Friday. USD/JPY began trundling lower after hitting the psychological 166 level, and 21DMA at 155.96, to a session low of 154.96.

PBoC set USD/CNY mid-point at 7.0656 vs exp. 7.0569 (Prev. 7.0638)

Fixed Income

USTs are currently firmer today by a handful of ticks, and reside at the upper end of a 112-06 to 112-12 range. Overnight trade saw US paper saunter higher, but lacked a clear driver – no hints provided from a yield perspective either, with rates lower to a similar magnitude across the board. Markets now await Fed speak from Miran and Williams, and the former is expected to release an explanation of his dovish dissent last week. Then the focus will turn to key US data in the coming days, namely NFP and CPI.

Bunds are also in the green, albeit to a lesser extent than peers; currently within a 127.45 to 127.64 confine. Earlier, German Wholesale Sales M/M printed in-line with expectations, whilst Y/Y rose from the prior; the inner report pinned the rise to “higher prices of food, beverages and tobacco”. Elsewhere, focus has been on geopolitics whereby Zelensky suggested that Ukraine is willing to drop NATO membership ambitions, in favour of security guarantees. Negotiations between Ukrainian and US officials will continue in Germany later today.

Gilts also gain in today’s session, in line with peers. Nothing really much from a UK perspective this morning, aside from UK Rightmove House Prices, which continued to show contractions. An exec at the firm said, “with market conditions supporting higher levels of activity, and a hopefully more certain economic environment, we forecast a better year for price growth in 2026 with a strong rebound in activity to kickstart the year”. The docket is very thin from a UK perspective, but will pick up starting from tomorrow, where a slew of key data will precede a BoE rate decision on Thursday.

Commodities

WTI and Brent initially started the week positively following better Chinese demand, but have failed to sustain a bid higher, as US envoys meet with European and Ukrainian officials in Berlin. Benchmarks dipped to a trough of USD 57.32/bbl and USD 61.07/bbl, respectively, at the start of the APAC session, before gradually bidding higher to a high of USD 57.62/bbl and USD 61.50/bbl. Despite the improved Chinese oil demand and reports of Iran seizing a foreign tanker, benchmarks have fallen into the European open and are currently trading near session lows.

Spot XAU has started the week on the front foot as ETF flows, central bank buying, and XAG short squeeze continue to support the yellow metal. After Friday’s liquidation selloff to a trough of USD 4257/oz, XAU bounced in the latter part of last week. The yellow metal opened at USD 4304/oz and gradually trended higher throughout the APAC session and thus far, remains at session highs of USD 4350/oz with ATHs just c. USD 30/oz away.

3M LME Copper, among most markets, got caught up in the tech-led selloff on Friday but has rebounded as the European session gets underway. Despite the selloff on Friday, ANZ analysts note that “demand for the metal continues to beat expectations despite the fall in China’s economic growth”, adding that the bank is bullish with the expectation that the market will move further into a deficit in 2026.

India’s November gold imports at USD 4.02bln (prev. USD 14.7bln); oil imports at USD 14.12bln (prev. USD 14.8bln).

Russia’s Nornickel sees a global nickel surplus at more than 200KT in 2025 and 2026, sees the global Palladium market balanced in 2025, sees a deficit at 0.2 MoZ, including investments.

The US asks the EU to exempt US gas from methane law obligations until 2035.

Geopolitics: Middle East

Israel’s military conducted a strike on Gaza, which killed senior Hamas commander Raed Saed, while the Israeli military said it put a planned strike on a southern Lebanon site on hold after the Lebanese Army requested access.

Two US Army soldiers and a civilian US interpreter were killed in Syria, while the Syrian government said the attacker was a member of Syrian security forces with extremist views. It was later reported that US President Trump said they will retaliate against ISIS and that there will be a lot of damage done to the people who attacked the troops in Syria.

Geopolitics: Ukraine

US President Trump said a lot of progress is being made on Russia and Ukraine, while he responded that they don’t want it now, and it would be complex when asked about the idea of a free economic zone in the Donbas region.

Ukrainian President Zelensky said services have been working to restore electricity, heating and water supply to regions following Russian strikes on energy infrastructure. Zelensky also commented that there won’t be a peace plan that everyone will like and there will be compromises, while he also stated that US and European security guarantees, instead of NATO membership, are a compromise from Ukraine’s side and that security guarantees should be legally binding.

Ukrainian presidential adviser said Ukraine and US teams meeting on peace proposals in Berlin lasted more than five hours on Sunday and will continue on Monday, while US special envoy Witkoff said a lot of progress was made during the talks.

Ukrainian military said it struck a Russian oil refinery in the Krasnodar region and a Russian oil depot in the Volgograd region, while Ukraine’s Navy said a Russian drone attack hit a Turkish civilian vessel carrying sunflower oil to Egypt on Saturday.

Russian Defence Ministry said Russian forces captured Varvarivka in Ukraine’s Zaporizhzhia region, according to RIA.

EU’s Kallas said new sanctions on Russia’s shadow fleet will be decided today. Adds that the EU has delivered 2mln artillery rounds to Ukraine this year. Will not leave the EU summit without a decision on funding for Ukraine.

Lithuania’s Foreign Minister said he expects the EU to widen the Belarus sanctions regime to include hybrid activity. Ukraine needs something like Article 5 in terms of security guarantees, with a nuclear deterrent.

Russia’s Kremlin said Ukraine not joining NATO is a key question but subject to special discussion. Expects the US to update Russian officials on the proposals from the Berlin talks.

Washington reportedly still wants Ukraine to cede the Donbas region to Russia, via Sky News Arabia citing official familiar with the negotiations.

Geopolitics: Other

US envoy John Coale said Belarusian President Lukashenko agreed to do all he can to stop weather balloons flying into Lithuania, while Coale also stated that the US will remove sanctions on Belarusian potash and that around 1,000 remaining political prisoners in Belarus could be released in the coming months.

US President Trump said land strikes against Venezuela will start happening and don’t necessarily have to be in Venezuela.

US President Trump said on Friday that he had a very good conversation with the Thai and Cambodian PMs, while he added that they agreed to cease all shooting effective that evening and go back to the original peace accord. However, it was reported over the weekend that Thailand’s PM Charnvirakul said his country has not reached a ceasefire agreement with Cambodia and the Thai military will continue fighting on the disputed border.

Philippine Coast Guard said three Filipino fishermen were wounded and two fishing boats suffered significant damage from high-pressure water cannon blasts by Chinese Coast Guard ships in the South China Sea, while it called on China’s Coast Guard to adhere to internationally recognised standards of conduct.

China sanctioned the former chief of staff of the Japan Self-Defense Forces, in which it froze properties, prohibiting transactions with, and barring visas for former Japanese official Iwasaki.

US Event Calendar

8:30 am: Dec Empire Manufacturing, est. 10, prior 18.7

10:00 am: Dec NAHB Housing Market Index, est. 39, prior 38

Central Banks (All Times ET):

9:30 am: Fed’s Miran Delivers Talk on Inflation Outlook

10:30 am: Fed’s Williams delivers Keynote Remarks

11:00 am: Fed’s Miran Appears on CNBC

DB’s Jim Reid concludes the overnight wrap

We’ve launched our big 2026 Global Financial Market Survey with many questions on your views for the year ahead. It includes, after a two-year gap, asking you your favourite Xmas song. Where you think the S&P 500 or Mag-7 ends up creates nothing like the controversy of the announcing your favourite Xmas song. You can complete the survey here. It closes on Wednesday. All help filling in very much appreciated.

Welcome to the last full week of the year. It’s started with me sneezing, eyes watering and completely bunged up. The flu? No! Just a kids Xmas party last night where unbeknownst to me they had a cat. I’m very allergic to them. The cat actually had the right idea and had already left for the evening due to the noise. Sadly, I had to endure the noise and the cat’s airborne residue.

So not the greatest start to the week for me and just when you thought it was safe to wind down for Christmas, the coming week is shaping up to be a significant one for global markets, with a dense calendar of economic releases and major central bank decisions. The European Central Bank, the Bank of England and the Bank of Japan all have a chance to be Scrooges or Santas in their meetings this week. Alongside these announcements, the data flow will be heavy: the US will finally publish delayed employment and inflation reports, while flash PMIs for December and will provide clues on global momentum.

It’s also an interesting time for global markets with long-end yields at or around multi-month or even multi-year highs (e.g. Japan and 30yr Europe) at the same time as the weakest AI stories are increasingly being punished rather than the pre-September period when AI all went up together. If that wasn’t enough, another notable Fed story came late on Friday, as President Trump suggested that NEC Director Kevin Hassett and former Fed Governor Kevin Warsh were his two favoured candidates for the Fed Chair role. Hassett has been viewed as the frontrunner in recent weeks but following Trump’s interview his Polymarket odds fell from around 73% late on Friday to 52% this morning. Warsh has gone from 13% before the interview to 40% this morning. So, it’s fair to say there’s a lot of unfinished business going into the last full trading week of the year.

For this week specifically, in the United States, attention will centre on tomorrow’s twin employment reports for October and November, delayed by the recent government shutdown. October’s headline payrolls are expected to show a decline of around -60k (DB forecasts here and below), largely due to federal layoffs with all the early year buy-out offers coming off payroll in October. November should rebound modestly with a gain of +50k (DB). Private sector hiring is likely to remain steady in both months at around +50k (DB), slightly below the recent trend. The unemployment rate is forecast to rise to 4.5 per cent in November from 4.4 per cent in September (we will never know October), while average hourly earnings should increase by 0.3 per cent in both months, keeping year-on-year nominal compensation growth near 4.4 per cent. Hours worked are expected to stabilise at 34.3. Given the distortions caused by the shutdown, the household survey could be noisy, echoing patterns seen after the 2013 episode. For a cleaner read on labour market conditions, Thursday’s jobless claims will be important and given our economists believe this will come in at around +225k, they believe underlying hiring trends remain intact.

Inflation will also be in focus with Thursday’s US CPI release. Because October data were not collected, the report will centre on year-on-year changes. Headline CPI is expected to hold broadly steady at 3.03%, while core inflation remains at 3.02%. Monthly headline gains across October and November should average +0.24%, slightly below September’s pace with core slightly above at +0.26%. Within the details, core goods prices are likely to show modest increases in household furnishings and apparel, while used car prices continue to decline. Core services will attract particular attention, especially rents, which are expected to rebound after September’s anomalous weakness. Airline fares and lodging should soften from their recent highs, though health insurance may surprise on the upside. Beyond jobs and inflation, Tuesday’s retail sales report will offer insight into consumer spending. We anticipate a headline decline of -0.3%, driven by autos and lower fuel prices, but retail control—the component used in GDP calculations—should rise by +0.3%, signalling resilience in underlying demand. Friday’s final reading of University of Michigan consumer sentiment is expected at 54.0, with inflation expectations likely to matter more than the headline figure.

On policy, last week’s FOMC meeting delivered a 25bps rate cut and signalled a “wait and see” approach. Chair Powell struck a dovish tone, emphasising labour market risks over inflation. This week’s Fedspeak will reinforce that message, with Governor Miran and New York Fed President Williams speaking today, followed by Governor Waller and Williams again on Wednesday. Atlanta Fed President Bostic closes the week on Friday. Miran, who dissented in favour of a larger cut, is expected to reiterate his view that shelter inflation will collapse in coming quarters.

In Europe, Thursday brings a cluster of central bank decisions. The ECB is expected to keep rates unchanged at 2 per cent (see our econ preview here), while the Bank of England is forecast to deliver its sixth cut of the cycle, lowering Bank Rate to 3.75 per cent on a narrow 5-4 vote. See our economist’s preview here. The Riksbank and Norges Bank will also decide on policy on the same day with both likely to stay on hold. Ahead of the BoE meeting, UK labour market data on Tuesday and CPI on Wednesday will be closely watched. Headline inflation is forecast to ease to 3.51% year-on-year, while core ticks up slightly to 3.46% (see our economist’s preview here). Retail sales and consumer confidence on Friday will round out the UK calendar. In Germany, the Ifo survey on Wednesday and consumer confidence on Friday will provide further insight into regional conditions as fiscal spending starts to ramp up. Across the Atlantic, Canadian inflation is out today which is interesting given the sharp move from pricing in a slightly easing bias earlier this month to almost a full hike by the end of 2026 now.

Across Asia, the Bank of Japan meets on Friday and is expected to raise rates by 25bps to 0.75 per cent, with a 94% probability priced in by markets. See our economist’s thoughts here. Japan’s nationwide CPI for November will also be released on Friday, with core inflation forecast to slow to 2.9% and core-core to 3.0%. Global flash PMIs for December, covering the US, UK, Japan, Germany and France, will be published tomorrow and will offer early signals on fourth-quarter growth trends.

Asian equity markets have kicked off the week notably lower after a difficult US session on Friday. Across the region, tech-focused exchanges are the poorest performers, with the KOSPI (-1.34%) and the Nikkei (-1.36%) leading the losses, followed by the Hang Seng (-1.15%). Mainland Chinese stocks are outperforming a bit due to less AI exposure and after a series of disappointing economic indicators (details below) may be raising stimulus odds. The CSI (-0.41%) and the Shanghai Composite (-0.31%) registering minor losses due to reduced exposure to the global AI market. The S&P/ASX 200 (-0.72%) is also trading lower. S&P 500 (+0.31%) and NASDAQ 100 (+0.24%) are both bouncing back a bit though.

Returning to China, the economic slowdown intensified in November, with retail sales increasing by only +1.3% last month compared to the same period last year, significantly below Bloomberg’s forecast of +2.9% growth, and a decrease from the +2.9% rise recorded in the previous month. Industrial production rose by 4.8% in November year-on-year, falling short of the anticipated 5% increase and marking the weakest growth since August 2024. Business investment remained weak in November, with fixed asset investment declining by -2.6% year-on-year, exceeding expectations of a -2.3% drop. This decline has worsened from the -1.7% decrease observed from January to October, representing the most significant downturn since the pandemic began in 2020. A separate report indicated that new home prices in China continued to fall, decreasing by -0.39% m/m in November, compared to a -0.5% decline in the previous month, suggesting that we’re still waiting for a recovery in demand even with government assurances that they will stabilise the sector.

Recapping last week now and US equities saw a mixed week, with the S&P 500 reaching a new all-time high on Thursday but slumping by -1.07% on Friday to end the week -0.63% lower. Concerns about the sustainability of AI-related spending weighed on tech with the NASDAQ down by -1.62% (-1.69% Friday) and the Mag-7 by -1.86% (-0.75% Friday). Oracle (-12.69%, -4.47% Friday but rallying off the day’s lows) and Broadcom (-7.77%, -11.43% Friday) plunged after their earnings reports. But there was rotation towards more blue-chip stocks, with the Dow Jones (+1.05%, -0.51% Friday) holding onto a sizeable weekly gain.

The rates space saw a significant curve steepening as the FOMC delivered a third consecutive 25bp cut. While the Fed signalled a possible pause in early 2026, dovish hints supported 2026 rate cut expectations. Fed fund pricing for December 2026 was little changed over the week but down by -7.4bps from its peak on Tuesday, with 56bps of rate cuts now priced for 2026. The next cut is 54% priced by March. Front-end Treasury yields declined, with the 2yr yield falling by -3.8bps to 3.52% (-1.8bps Friday). By contrast, the 10yr yield (+4.9bps to 4.18%; +2.7bps Friday) and the 30yr yield (+5.3bps to 4.84%; +4.5bps Friday) both posted their highest levels since September, bringing the 2s10s slope to its steepest since January 2022, just before the Fed started its post-Covid hiking cycle. Meanwhile, recent money market tightness eased as the Fed also announced the commencement of reserve-management purchases of Treasury bills.

In Europe, government bonds sold off amid rising global term premia and hawkish comments by the ECB’s Isabel Schnabel. 10yr bund yields rose +5.9bps to 2.86%, their highest weekly close since March, with OATs (+5.3bps) and BTPs (+6.3bps) similarly higher. The OAT outperformance came as the French parliament approved the social security budget. In the equity space, Friday’s -0.53% decline left the STOXX 600 little changed on the week (-0.09%).

Germany’s DAX (+0.66%, -0.45% Friday) outperformed, in part helped by a Bloomberg report that German lawmakers are set to approve €52bn in defence orders next week, with Rheinmetall climbing +5.66% as a result. In the UK, the FTSE 100 (-0.19%, -0.56% Friday) wasn’t helped by a soft monthly GDP reading on Friday (-0.1% vs +0.1% expected). Meanwhile, European credit outperformed the US, with HY spreads tightening by -1bps in contrast to a +11bps widening across the Atlantic.

In commodities, Brent crude prices fell -4.13% to $61.12/bbl, to within one dollar of their 2025 lows seen back in May. In contrast, gold rose by +2.43% to $4,300/oz as investors returned to safe haven assets. Bitcoin (+1.12% on the week) managed to reclaim the $90,000 level despite a -2.89% decline on Friday.

Tyler Durden

Mon, 12/15/2025 – 08:32

https://www.zerohedge.com/markets/us-futures-recover-most-fridays-dump-bad-news-again-good-news

Philip Rivers, 44, emotional after nearly leading Indianapolis Colts to win: ‘There is doubt and it’s real’

SEATTLE — Philip Rivers fought back tears as he considered what message it would send to his sons, or the young men he has coached, that he nearly led the Indianapolis Colts to victory at age 44.

“There is doubt and it’s real,” Rivers said, choking up briefly. “The guaranteed safe bet is to go home or to not go for it, and the other one is, ‘Shoot, let’s see what happens.’ I hope in that sense that can be a positive to some young boys, or young people.”

Rivers ended a nearly five-year retirement to start Sunday against the Seattle Seahawks and played efficient football for the desperate Colts, who turned to the future Hall of Famer after Daniel Jones was lost for the season with a torn Achilles tendon.

He threw a touchdown pass in the first half, played mostly mistake-free and moved the Colts into position for Blake Grupe’s 60-yard field goal with 47 seconds left. But Jason Myers responded with a 56-yarder that gave the Seahawks an 18-16 victory.

It was a remarkable day for a grandfather who’s spent the past few years coaching high school football in his native Alabama.

Rivers took a few hard hits from the Seahawks’ stout defense, and he even enjoyed them.

“I never minded that part of it,” Rivers said. “My wife always tells me I’m crazy because there’s been times in the last three or four years I said, ‘I wish I could just throw one and get hit – hard.’”

This wasn’t a novelty act, as it may have seemed when the Colts signed the Pro Football Hall of Fame semifinalist to their practice squad less than a week ago. Coach Shane Steichen’s Colts, who began the season 7-1 but are trying to stop a second-half collapse, knew what they were getting out of the veteran.

Rivers finished 18 of 27 for 120 yards with a touchdown and an interception, with the pick coming on his final pass as he tried to force the ball down the field in the closing seconds.

“I was just thankful — grateful — that I was out there,” Rivers said. “And it was a blast — it was a blast — but obviously the emotions now are disappointment. This isn’t about me. We have a team scrapping like crazy to try and stay alive and get into the postseason.”

The Colts (8-6) have dropped four straight and five of six, and they are outside the AFC playoff picture with three games left. They trail both Jacksonville and Houston in the AFC South.

Steichen called a conservative game, relying on running the ball and controlling the clock. Rivers threw mostly short passes to the outside, checkdowns and screens.

“He went out there and gave us a chance to win it,” Steichen said.

Rivers took two sacks, and he showed his age on the first one. He stumbled while evading pressure from Boye Mafe, got up, then fell again.

Rivers pumped his right fist and let out a roar after throwing an 8-yard touchdown pass to Josh Downs with 1:33 remaining in the first half to put the Colts up 13-3.

It was Rivers’ first touchdown pass since he threw a 27-yarder to Jack Doyle in the Colts’ 27-24 loss to Buffalo in a wild-card playoff game on Jan. 9, 2021. He also became the fifth player in NFL history to throw a TD pass at age 44 or older, joining Tom Brady, George Blanda, Steve DeBerg and Vinny Testaverde.

“It’s been 1,800 days since I’ve thrown a touchdown — or interception for that matter. So we have both those (boxes) checked,” Rivers said.

Rivers was chosen last month as one of 26 semifinalists for the Hall of Fame’s class of 2026 but will now have his eligibility delayed. A player must be out of the league for at least five years before his candidacy can be considered. The earliest Rivers can be a candidate is for the class of 2031.

He ranks among the top 10 in NFL history in wins, attempts, completions, yards passing, touchdown passes and 300-yard games.

Since his retirement, he’s been coaching at St. Michael Catholic High School in Fairhope, Alabama, where the team held a watch party on Sunday. Rivers’ players were on his mind as he returned to the NFL.

“Maybe it will inspire or teach not to run or be scared of what may or may not happen,” Rivers said.

https://www.chicagotribune.com/2025/12/15/philip-rivers-emotional-nfl-return/

iRobot Crashes After Filing For Bankruptcy, Chinese Owner Emerges

iRobot Crashes After Filing For Bankruptcy, Chinese Owner Emerges

Some of us may be old enough to remember when iRobot released its first robot vacuum, the Roomba, in 2002. Nearly 25 years later, the company has ceased to exist, collapsing into bankruptcy, with its remaining assets and intellectual property set to be acquired by a Chinese competitor.

How did iRobot implode, only for a Chinese company to end up cleaning American homes?

It began when European Union competition regulators blocked Amazon’s proposed takeover of iRobot, cutting off what some Wall Street analysts saw as the company’s last realistic path to survival. It is also worth noting that the Biden administration’s FTC Chair, Lina Khan, was aligned with the EU’s position.

A prior Lina Khan special?

Encouraging the DOJ to block JetBlue from buying Spirit.

Spirit has subsequently filed for bankruptcy TWICE in the just over two years since then. https://t.co/HHLmRK7acX

— Compound248 💰 (@compound248) December 15, 2025

Founded in 1990 by MIT engineers, iRobot rose to prominence in the early 2000s with the Roomba. Now, the company has filed for Chapter 11 bankruptcy and agreed to hand control to its leading Chinese supplier, Shenzhen PICEA Robotics, under a court-supervised process in Delaware.

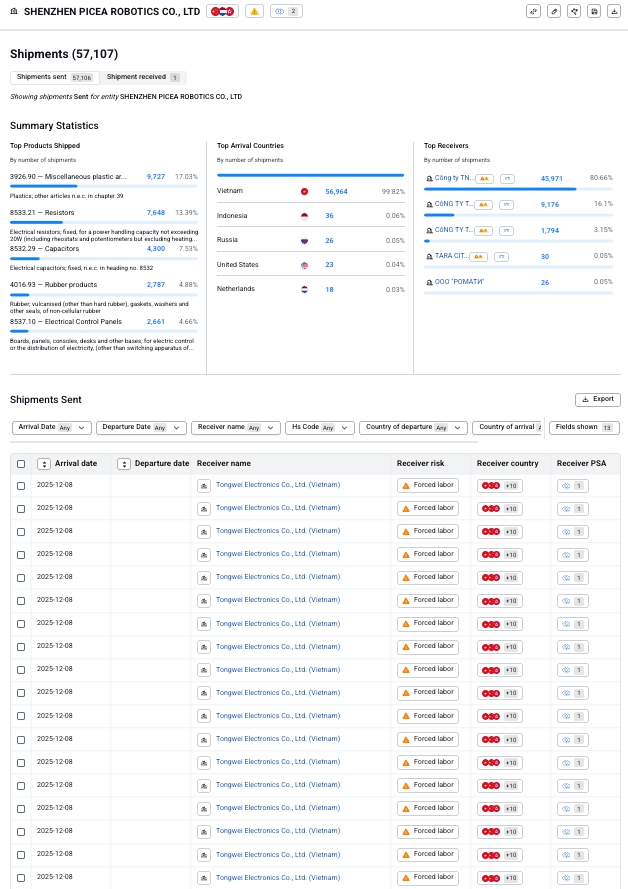

Peering into Shenzhen PICEA Robotics’ latest supply chain. By the way, it has links to companies with “forced labor” risks. This data was generated by the supply chain risk analysis company Sayari.

In New York, iRobot’s shares crashed 68% in premarket trading.

Bankruptcy filings show estimated assets of $100 million to $500 million, with liabilities in the same range.

iRobot said operations will continue without disruption, including its app, customer programs, global partners, supply chain relationships, and product support.

Thanks to the reckless EU regulators and Biden-era mismanagement, America’s iRobot will now be owned by the Chinese and likely present security risks.

Tyler Durden

Mon, 12/15/2025 – 08:05