Category: News

Russia, Ukraine Agree To Breakthrough 32-hour Orthodox Easter Ceasefire

Russia, Ukraine Agree To Breakthrough 32-hour Orthodox Easter Ceasefire

In a huge and very positive development, Russia’s President Vladimir Putin has announced a 32-hour ceasefire for Orthodox Easter, or Pascha, which is this weekend. Ukraine’s President Volodymyr Zelensky has immediately confirmed that Ukraine will honor the holiday truce.

“We proceed on the basis that the Ukrainian side will follow the example of the Russian Federation,” the Kremlin then further confirmed in a statement.

Based on regional media reporting of the rare ceasefire, the pause in fighting will begin at 4pm Moscow time (13:00GMT) on Saturday and run until midnight on Sunday.

This will cover the whole period of Pascha celebrations in both countries, which is done according to the Julian calendar and thus typically comes a weekend or two later that Western Easter (on the Gregorian calendar). The overwhelming majorities of both countries are adherents of the Eastern Orthodox Church.

Typically in orthodox churches there is a long Saturday morning service, and then the main liturgy comes at midnight – going into the early Sunday morning hours, followed by feasting and breaking the Lenten fast. And then late Sunday morning or early after noon there is another service, after which there is more celebratory feasting.

Russian media reports that Defense Minister Andrei Belousov has instructed Chief of the General Staff Valery Gerasimov to halt Russian military operations during the period; however, just like in past short truces Russia says it will respond immediately to any ‘violations’ observed.

Zelensky meanwhile confirmed that “Ukraine has repeatedly stated that we are ready for reciprocal steps. We proposed a ceasefire during the Easter holiday this year and will act accordingly.”

“People need an Easter without threats and a real move towards peace, and Russia has a chance not to return to attacks even after Easter,” he added.

Such a holiday truce has been tried in the past, but is typically marred by frontline ‘violations’ and tit-for-tat accusations and denunciations.

But this year, after well over four years of brutal fighting which has taken likely hundreds of thousands of lives, there is a good chance the Easter truce will hold given the sheer exhaustion and war-weariness on each side.

What’s more is that if there is success, it could provide the basis for something more lasting, as both sides say they are still interested in hammering out a permanent end to the war. But for Moscow, this will require that Ukraine cede much of the east and give political recognition too, including over Crimea.

Tyler Durden

Fri, 04/10/2026 – 10:00

Trump Posts About “World’s Most Powerful Reset!!!”

Trump Posts About “World’s Most Powerful Reset!!!”

Without providing any elaboration or context, President Trump just posted the following to his social media feed:

No idea what he is talking about?

Pressure on China (multiple chokepoints on energy supply)?

Chatter on Russia-Ukraine talks?

America First, maybe?

4-D Chess or another fantastical plan?

Any ideas?

Tyler Durden

Fri, 04/10/2026 – 09:46

https://www.zerohedge.com/markets/trump-posts-about-worlds-most-powerful-reset

Apple To Close First Unionized Store, Along With Two Others, Citing “Declining Conditions”

Apple To Close First Unionized Store, Along With Two Others, Citing “Declining Conditions”

Apple is permanently closing three mall-based stores in the coming months: Apple North County in California, Apple Trumbull in Connecticut, and Apple Towson Town Center in Maryland, which is the company’s first unionized store.

“Following the departure of several retailers and declining conditions at Trumbull Mall, the Shops at North County, and Towson Town Center, we’ve made the difficult decision to close our stores at these locations,” Apple told computer blog AppleInsider in a statement.

Most workers will be transferred to nearby stores if they choose to remain with Apple, while unionized Towson employees will need to apply for open roles under the current bargaining agreement.

Apple wouldn’t provide additional color on what exactly those “declining conditions” were, such as whether they involved a slowdown in foot traffic or thefts.

Focusing on the unionized Towson location, the International Association of Machinists and Aerospace Workers reacted furiously to Apple’s decision. The move suggests that Tim Cook has little interest in bending the knee to lefty union pressure.

APPLE STORE CLOSURES | Apple announced its closing 3 locations, inside malls or shopping plazas across the country, on Thursday.

1/3 locations is Towson Town Center. The union representing the workers in Towson says they’re outraged. Doors set to close on June 11. @wbaltv11 pic.twitter.com/M9m3CZnqYQ

— Tori Yorgey WBAL (@toriyorgeytv) April 10, 2026

“The IAM Union is outraged by Apple’s decision to close its Towson, Md., store — the first unionized Apple retail location in the United States — and abandon both its workers and a community that relies on it for critical services and its unique access to public transit,” the union wrote in a statement to the outlet.

IAM continued:

Apple’s claim that the collective bargaining agreement prevents relocation is simply false and raises serious concerns that this closure is a cynical attempt to bust the union.

We are exploring all legal options and will work with elected officials and allies to hold Apple accountable. We stand with our IAM Coalition of Organized Retail Employees (IAM CORE) members and the community that depends on this store for essential access and support.”

Apple appears to be sending a very clear message to workers considering the union route: go down that path, and you may end up like the Towson store.

Tyler Durden

Fri, 04/10/2026 – 09:45

Artemis II Astronauts To Return Home Today: What To Know

Artemis II Astronauts To Return Home Today: What To Know

Authored by T.J.Muscaro via The Epoch Times,

Humanity’s first mission around the Moon in more than 50 years is coming home the way of a meteor.

NASA astronauts Reid Wiseman, Victor Glover, and Christina Koch—as well as Jeremy Hansen of the Canadian Space Agency—will reenter Earth’s atmosphere in their Orion spacecraft Integrity at approximately 7:53 p.m. on April 10.

Artemis II’s 10-day journey beyond the moon to the farthest point away from Earth that humans have traveled will end with the astronauts’ ride in a fireball through the sky and splashdown in the Pacific Ocean off the coast of San Diego at approximately 8:07 p.m.

This is the pinnacle of the adventure that Glover has been thinking about since he got assigned to the mission on April 3, 2023, and NASA officials have been thinking about it since even before that.

After Artemis I, the Orion spacecraft’s heat shield and reentry trajectory went through a drastic redesign.

NASA’s associate administrator, Amit Kshatriya, affirmed on April 9 that the crew and everyone involved were confident in Integrity’s systems.

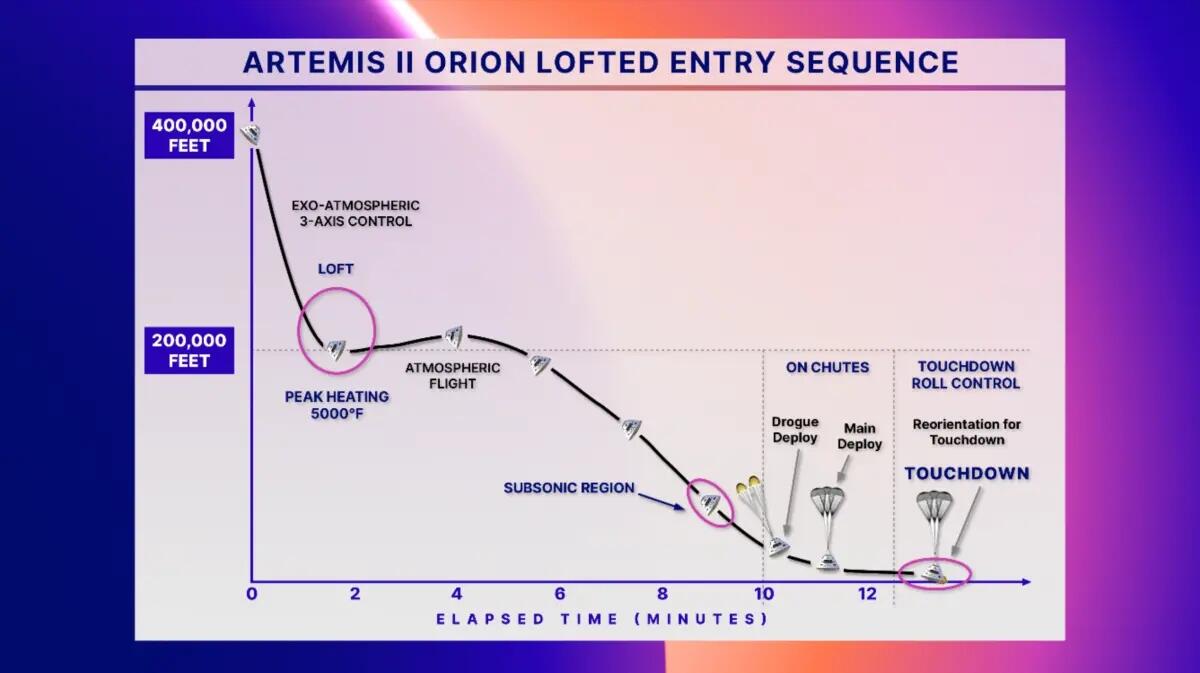

Reentry Timeline

NASA’s Rick Henfling will be the flight director at mission control during reentry and splashdown, and he outlined the course of events ahead of the mission’s dramatic conclusion.

11:35 a.m. EDT—The crew will wake up and start their day. They will make final preparations and configure the cabin for reentry as Integrity gets closer to home and travels faster and faster.

Those preparations include donning the orange-and-blue pressure suits they wore for launch and stowing all remaining loose equipment for reentry. One final course correction burn is also scheduled.

7:33 p.m.—Integrity’s Orion crew module will separate from its European Service module—the deep-space workhorse that kept Artemis II on course, provided power and life support, and offered exterior vantage points from which photographs were taken and shared with the world.

Shortly after separation, the crew capsule will fire its own thrusters to optimize its reentry angle and distance itself from the service module, which is now doomed and will burn up in the atmosphere.

7:53 p.m.—Integrity starts its reentry at an altitude of 400,000 feet, nearly 2,000 miles southwest of its landing zone in the Pacific Ocean. The astronauts will be falling backward, so the capsule’s heat shield is facing forward, and upside down, so the crew can see the horizon line.

An infographic featuring the Artemis II Orion lofted entry sequence, presented by Artemis II Flight Director Rick Henfling during the mission status briefing to the media and public at NASA’s Johnson Space Center in Houston on April 8, 2026. NASA

The spacecraft must hit the Earth’s atmosphere at the right angle to pass through safely.

Fight director Jeff Radigan told reporters on April 9 that Mission Control was continuing to review data and telemetry to ensure that Artemis II remains on course.

“We got less than a degree of angle that we need to hit,” Radigan said. “We’ve got a little bit of wiggle room. We don’t plan to use that.”

Artemis II is expected to reach a top speed of 34,965 feet per second, approximately 23,864 mph, just short of the mission’s overall top speed of approximately 24,500 mph.

This means they will fail to break Apollo 10’s record-setting speed of 36,397 feet per second, or 24,816 mph.

Radigan told The Epoch Times that Artmeis II’s return home would be very similar to the Apollo mission that came before it. They are essentially coming straight down and much faster compared with reentries from low-Earth orbit.

Integrity will essentially become a man-made meteor, engulfed in a ball of fire and plasma and facing temperatures of up to 5,000 degrees Fahrenheit as it rips through the atmosphere.

The crew inside is expected to experience g-forces of 3.9. That is 3.9 times the force of normal gravity on Earth.

However, Henfling said that type of g-force would be experienced during a nominal trajectory. If the crew had to take any of the contingency trajectories mapped out, they could experience g-forces of up to 7.5.

Their capsule will perform multiple roll reversal maneuvers to distribute heat evenly across the heat shield and help slow down.

However, they will not be piloting the capsule. Radigan confirmed that although the crew has been trained and is capable of taking control if necessary, Integrity’s computer will fly the crew home.

Mission Control expects to lose contact with Integrity 24 seconds after entry interface.

Henfling said that as plasma builds up around the spacecraft, it interferes with telemetry. That blackout is expected to last about six minutes.

7:59 p.m.—Integrity will reacquire signal with Mission Control and will be down to an altitude of about 150,000 feet and falling.

About nine minutes into reentry, Earth’s atmosphere will slow the Orion capsule to subsonic speeds.

8:03 p.m.—Integrity drops to about 22,000 feet, and drogue parachutes deploy.

At about 6,000 feet, the main parachutes will deploy.

8:07 p.m.—Artemis II splashes down in the Pacific Ocean off the coast of San Diego. In 13 minutes, Integrity will have slowed from approximately 25,000 mph to just 20 mph.

8:22 p.m.—Wiseman, Glover, Koch, and Hansen power down Integrity.

Recovery Operations

Artemis II will be recovered in a joint operation between NASA and the Department of War. The USS John P. Murtha, the recovery ship, left port in San Diego on April 7 to assume its position and await recovery.

The targeted time to extract the astronauts from the capsule is 9:06 p.m.

The USS John P. Murtha pictured with an Orion crew capsule during a recovery test in preparation for NASA’s Artemis I uncrewed test flight on March 14, 2020. NASA

Debbie Korth, Orion deputy program manager, said the goal is to have the crew out of the capsule and on the recovery ship within two hours after splashdown.

They will also have several aircraft circling the area to get eyes on the returning craft as soon as possible.

Divers will arrive on-scene first and open the hatch.

Medical personnel will then enter the capsule to assess the crew. Hansen will be reached first, followed by Wiseman, then Koch, and Glover.

Once everyone is cleared by the medics, Koch will be the first to leave the capsule, followed by Glover, then Hansen.

Wiseman, Artemis II’s commander, will be the last to step outside.

The crew will then be lifted into helicopters and transferred to the recovery ship in the same order they left Integrity.

Once aboard, they will be taken to a medical bay for further evaluation.

That whole process is expected to take at least 40 minutes.

Meanwhile, teams will remain on-site to secure Integrity, which will be towed aboard the recovery ship via its amphibious transport dock.

The crew is scheduled to fly back to Johnson Space Center in Houston between 12 and 24 hours after recovery, and their Orion capsule will be trucked across the country to Kennedy Space Center in Florida.

All of the remaining science the crew collected, including images yet to be downlinked and the biological experiments, such as the AVATAR project, which flew on board to learn how deep space affects human health, will be sent off to their respective teams for analysis.

“We have to get back,” Glover said during a call with the media on April 8. “There’s so much data that you’ve seen already, but all of the good stuff is coming back with us.”

Tyler Durden

Fri, 04/10/2026 – 09:30

https://www.zerohedge.com/technology/artemis-ii-astronauts-return-home-today-what-know

Pakistan Under Security Lockdown As Iran Delegation Arrives For US Talks – Fighting Hasn’t Ceased In Lebanon

Pakistan Under Security Lockdown As Iran Delegation Arrives For US Talks – Fighting Hasn’t Ceased In Lebanon

Summary:

Iran makes clear Lebanon fighting must end or else Pakistan talks “meaningless” – as its delegation arrives in ‘locked down’ Pakistan.

Trump ‘optimistic’ a deal within reach – also as Israel-Lebanon talks scheduled in Washington next week. US delegation headed by Vance en route to Islamabad.

Lloyd’s: “The Iranians are willing to negotiate with certain countries to secure voyages, but only on a case-by-case basis.”

After days of search and rescue, Lebanon death toll stands at over 300 following the Wednesday ‘surprise’ Israeli strikes. Sporadic IDF attacks continue on south and east.

* * *

Sporadic Fighting Persists in Lebanon

A big question remains: will Israel and Lebanon actually formally start the ceasefire negotiations that Prime Minister Netanyahu ordered his cabinet to prepare for? Negotiations are tentatively expected to begin next week at the State Department in Washington. The massive Israeli strikes from earlier this week have threatened to derail the Iran ceasefire deal before it really gets off the ground.

For now, Israel has continued attacking Lebanon on Friday, also as Hezbollah has continued firing missiles on northern Israel. Wednesday saw some 70 rockets fired from Lebanon, after the earlier massive Israeli surprise attacks which killed over 300 Lebanese and over 1,150 wounded. There may be some ground fighting in the south too, amid ongoing IDF aerial attacks on southern Lebanon. Al Jazeera says that an Israeli airstrike hit the town of al-Tayri in southern Lebanon, and another targeted the town of Sahmar in the western Bekaa region of eastern Lebanon. Heavy Israeli strikes in the Nabatieh area of southern Lebanon have also been reported Friday.

Hezbollah Secretary-General Naim Qassem has vowed in a statement carried by AI Mayadeen that the Iran-aligned group will “remain steadfast” as “resistance will continue until our last breath.” He praised Hezbollah for thwarting a ground invasion, saying “the enemy was surprised by the methods of resistance, the flexibility of the Mujahideen movement, and their defensive capabilities.” He vowed, “We will not accept a return to the previous situation, and we call on officials to stop offering free concessions,” while denouncing the “bloody criminality on Wednesday.”

Iranian Delegation Arrives in Pakistan

As the US and Iran prepare for talks in Pakistan, the Lebanon crisis is still a closely watched sticky issue which could escalate before it gets better. Pakistani media has reported that the Iranian delegation has arrived for negotiations, which are set to proceed Saturday, also pending the arrival of the US team headed by Vice President JD Vance – and including Trump envoys Steve Witkoff and Jared Kushner.

US team headed by Vance en route to Pakistan…

JD Vance departs for peace talks with Iran in Pakistan:

We’re looking forward to the negotiation. I think it’s going to be positive.

If the Iranians are willing to negotiate in good faith and extend an open hand, that’s one thing.

If they’re going to try to play us, they’re… pic.twitter.com/gBK06pia8c

— Clash Report (@clashreport) April 10, 2026

However, there’s been no official confirmed info about the arrival of Iranian Parliament Speaker and the Foreign Minister, but we can at least assume that Abbas Araghchi will be there in person. Parliament Speaker Ghalibaf is likely there too.

Meanwhile, unconfirmed/developing chatter of division within Iranian negotiating ranks:

THE IRGC COMMANDER-IN-CHIEF AHMAD VAHIDI IS SEEKING TO CURB THE AUTHORITY OF MOHAMMAD BAGHER GHALIBAF AND FOREIGN MINISTER ABBAS ARAGHCHI IN THE TALKS. || VAHIDI HAS ALSO PUSHED FOR THE INCLUSION OF MOHAMMAD BAGHER ZOLGHADR, SECRETARY OF THE SUPREME NATIONAL SECURITY COUNCIL, IN THE NEGOTIATING TEAM — A MOVE OPPOSED BY CURRENT MEMBERS, WHO CONSIDER HIM LACKING EXPERIENCE FOR STRATEGIC NEGOTIATIONS. – SOURCES

SENIOR IRANIAN OFFICIALS ARE LOCKED IN A DISPUTE OVER THE COMPOSITION AND AUTHORITY OF THE DELEGATION SET TO NEGOTIATE WITH THE UNITED STATES IN ISLAMABAD, ACCORDING TO INFORMATION RECEIVED BY IRAN INTERNATIONAL. – SOURCES

Islamabad is said to be under effective lockdown while hosting the high stakes summit. President Trump previously expressed concern over the security situation, related to sending Vance. One outlet observes, “Pakistan has ramped up security in Islamabad ahead of high-stakes direct talks between the United States and Iran, with the federal capital administration declaring a two-day public holiday on Thursday and Friday.”

⚡️Nabatieh pic.twitter.com/qarGQEKHIo

— War Monitor (@WarMonitors) April 10, 2026

A Pakistani official has told The Guardian, “Our priority is that the talks go smoothly. We don’t want to be seen as a spoiler. Our role is as a facilitator and mediator. We will leave it to both parties, Iran and the US, to share any developments with the media if they want.”

Iran’s president, Masoud Pezeshkian, has made clear Iran’s position that any peace negotiations would be “meaningless” if they took place while Israeli bombs continue to fall on Lebanon.

Hormuz Status Update: ‘No Option’ but to Negotiate Passage with Iran

As a reminder, President Trump has stated that Iran is “doing a very poor job” of allowing oil to flow through the Strait of Hormuz and warned Tehran against imposing tolls on vessels transiting the waterway. An Iranian lawmaker stated earlier that some ships are being charged as much as $2 million for passage through the strait.

Reuters highlights that the majority of ships that have sailed through the Strait of Hormuz in the past day were linked to Iran, per fresh tracking data. The majority of vessels, however, are still not risking passage with the waterway still under threat.

“Three tankers – a crude supertanker that can carry 2 million barrels of oil, a bunkering tanker and a smaller oil ship – all left Iranian waters in the past 24 hours, based on separate data analysis from Kpler and Lloyd’s List Intelligence platforms,” Reuters notes. “Four dry bulk ships – including one that loaded iron ore from Iran bound for China – also sailed in the past day, the data shows.”

📸 IRGC Navy’s destroyed Shahid Mahdavi floating base ship following U.S. airstrikes. pic.twitter.com/BsmMZ3doB4

— Clash Report (@clashreport) April 10, 2026

On the evening of Islamabad talks, Iran holds the Hormuz leverage. “The Iranians are willing to negotiate with certain countries to secure voyages, but only on a case-by-case basis,” said Bridget Diakun, a senior risk and compliance analyst at Lloyd’s List Intelligence, to the NY Times. “The Trump administration is forcing its allies to negotiate with Iran because there is no other option.”

Tyler Durden

Fri, 04/10/2026 – 09:15

Not Just ‘Death To America’, It’s ‘Death To Everyone’ When Fertilizer Supply Shock Hits

Not Just ‘Death To America’, It’s ‘Death To Everyone’ When Fertilizer Supply Shock Hits

Santiago Capital’s Brent Johnson, known for his dollar milkshake theory, had an ominous warning at last evening’s ZH debate: Even if the war is settled (and there’s no guarantee of that), baked in supply shocks could be very bad for agriculture. This comes as just yesterday, Mises Institute’s Connor O’Keefe warned of “a time bomb in global food markets”.

… and Brent is the dollar bull.

Johnson joined Marc “Dr. Doom” Faber and Thoughtful Money’s Adam Taggart to debate what comes after the tenuous ceasefire that Trump has brokered with Iran. Major win for the U.S. and the dollar or simply relative mitigation of a pointless blunder?

Below were key points by Dr. Doom and the Milkshake man, though we highly recommend the full discussion for those with time:

Inflation for thee but not for me

Marc Faber’s argument centered on a disconnect between official inflation data and lived experience… something the war, even if concluded promptly, will only exacerbate. While the legendary “shadowstats” is no longer updated, it last had May ‘23 real inflation at 8% annually, double the government’s reported figure of 4%.

Faber rejects low headline figures:

“I don’t believe that anywhere in the world the rate of inflation was like around 2% (pre-war). This is complete nonsense. Open the invoices of your insurance company! Insurance premiums are going up by something like 10%… everywhere the prices are up.”

Average households cannot sustain such strain for long. In Faber’s view, a large share of the population is financially stretched: “around 70% of Americans… live paycheck to paycheck.” Income barely covers expenses, leaving little margin for shocks. “This is sort of like a modern slavery… people are… anxiously waiting for the salaries to pay their debts.”

Faber’s slavery analogy extends to the K-shaped economy, where wealthy asset owners see massive booms in their on-paper wealth while Joe six-pack (with no assets) just sees his gas and groceries go up:

“My outlook for the economy was already, before the war in Iran, was not favorable… the financial markets have gone into the sky and the real economy of people is flat on its back.”

— ZeroHedge Debates (@zerohedgeDebate) April 9, 2026

Fertilizer > Oil

Brent Johnson framed the debate around power as opposed to market forces: “If the United States is going to lose dominance, somebody else has to take it.” He pointed to the U.S.-Israeli assassination of Iran’s head of state and the lack of global pushback as evidence that U.S. global influence remains intact for now.

“Nobody has done anything to stop it.”

He does not claim the month-long U.S. operation will be a success. “That could very well be a huge miscalculation… [but] it might work.” Outcomes are not predetermined, and states still use force to pursue objectives, “countries do use military force to get what they want… I understand why they did it… and how it could possibly work.”

Largely a dollar bull, Johnson still sees pain on the horizon for all fiat holders. ”We are going to get at least a short-term inflationary impulse… a pretty severe [one]… it may hit the United States the least… it’s going to hurt the rest of the world more.”

“We’re just now going to be in the summer driving season here pretty soon and gasoline and energy prices are already up… that could dramatically negatively affect the US economy.”

Beyond energy, the underappreciated yet vital product that must flow through the Strait of Hormuz: fertilizers and chemicals.

“The bigger impact that I worry about is the fact that fertilizers and chemicals also get transited through the Strait of Hormuz. And the timing of this happening is impacting the planting season for both the summer season in the Northern Hemisphere and the winter planting season in the Southern Hemisphere. It’s my expectation that even if the strait fully opens tomorrow, which it won’t… There’s going to be a four to six week period where most ships don’t arrive…”

The result: civil unrest.

“That is going to have a material impact on food prices. Six to nine months down the road. Once you get food price rises and food shocks, then you get social shocks. Then you get people out in the streets chanting ‘death to everyone’ not just ‘death to America’.”

— ZeroHedge Debates (@zerohedgeDebate) April 9, 2026

Listen to their full remarks and learn which cigarettes Dr. Doom smokes in the full debate below. Watch on the ZeroHedge X feed, Taggart’s Thoughtful Money YouTube channel, or listen on the ZH Spotify.

— zerohedge (@zerohedge) April 9, 2026

Tyler Durden

Fri, 04/10/2026 – 09:00

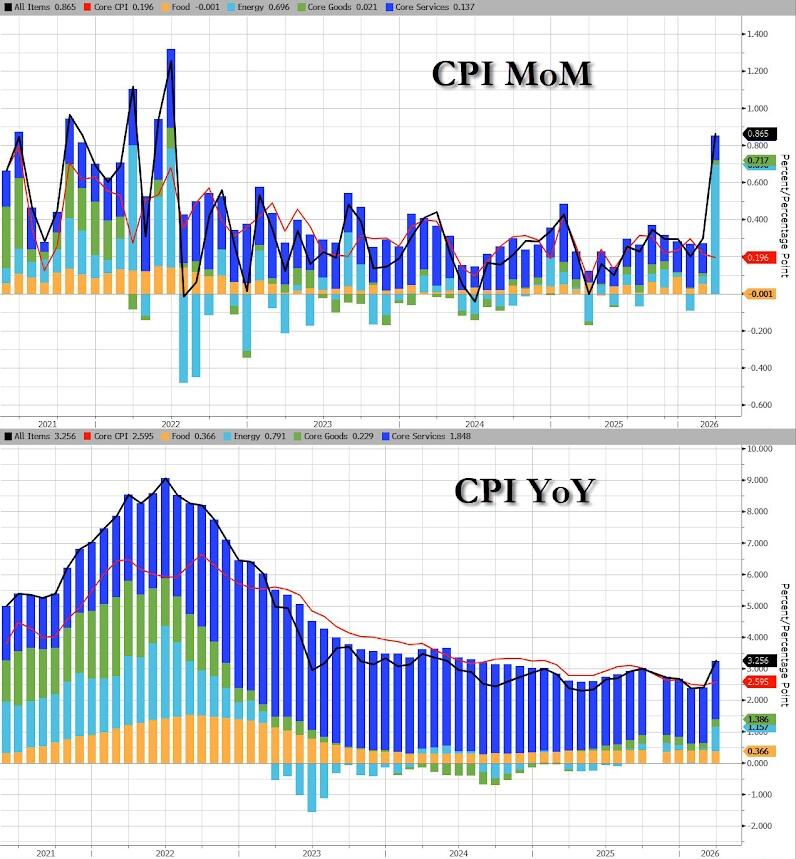

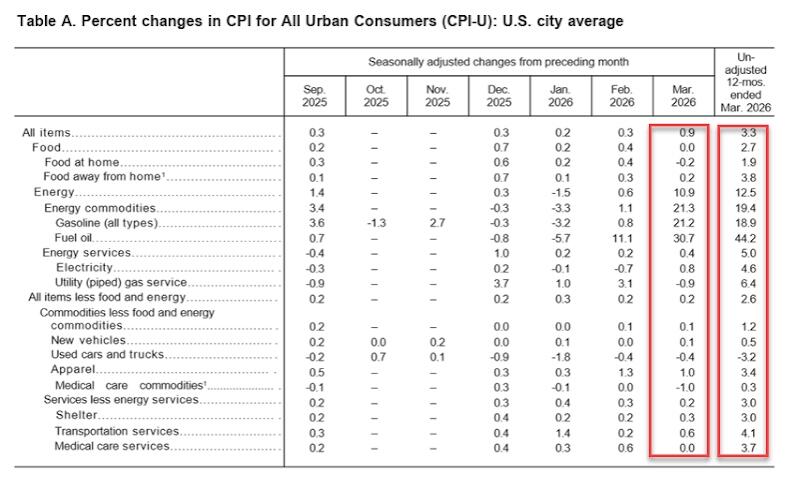

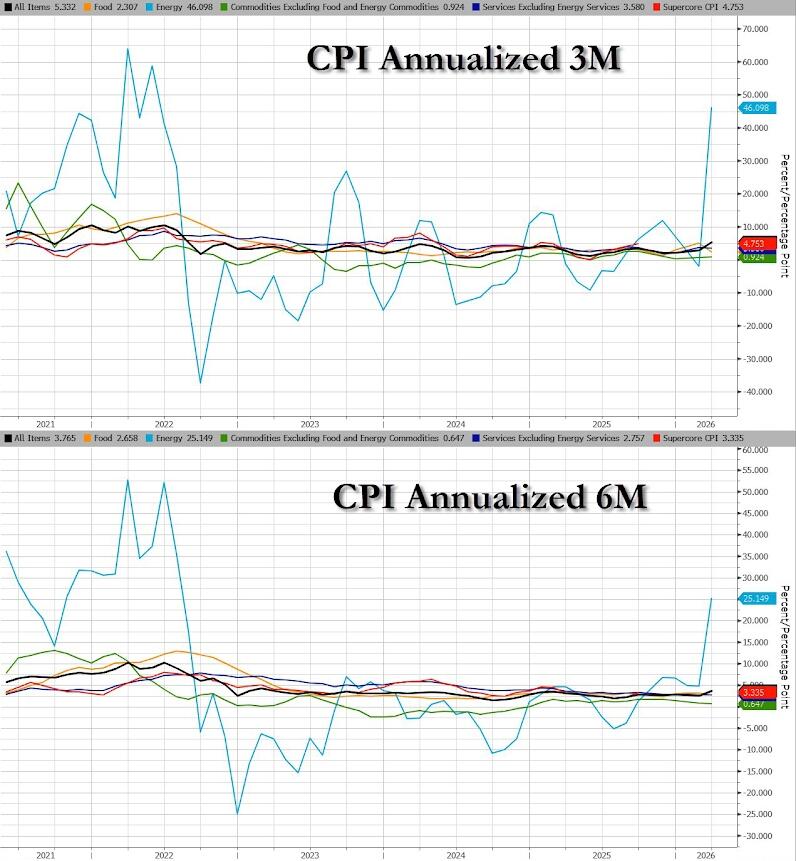

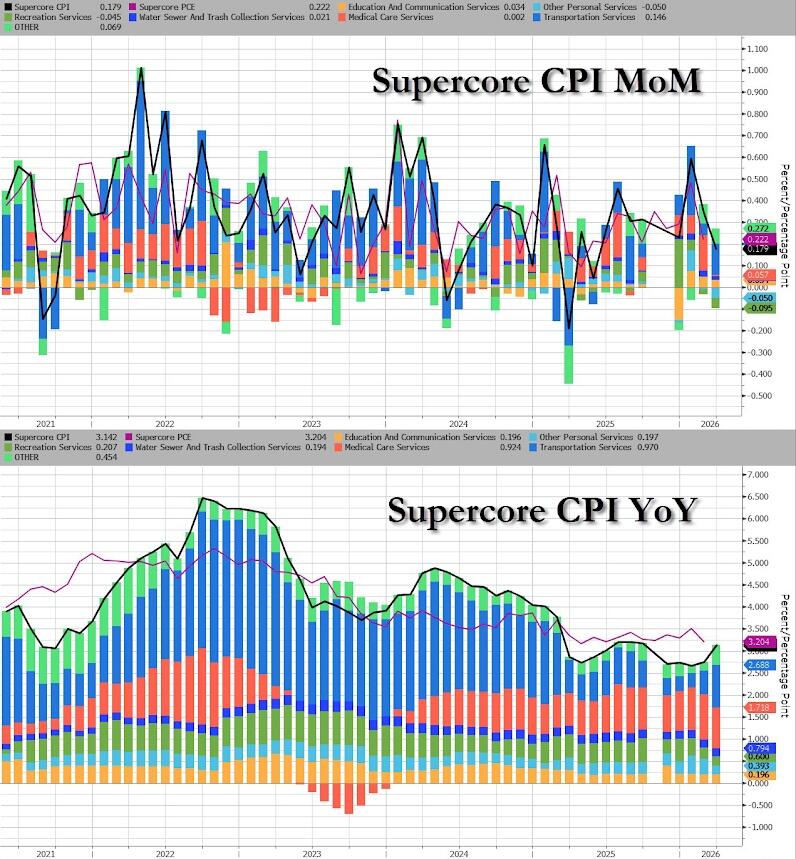

Core CPI Prints Cooler Than Expected Despite Biggest Jump In Energy Prices Since 2005

Core CPI Prints Cooler Than Expected Despite Biggest Jump In Energy Prices Since 2005

While PCE showed some signs of higher energy prices leaking into inflation prints, it was still February data. As we previewed, today’s CPI data is for March and will bear the full brunt of the Iran War’s impact on energy costs after Core CPI fell to its lowest in four years in February.

The headline CPI soared 0.9% MoM (as expected) and while it was a big MoM jump, Consumer Prices rose 3.3% YoY (up from +2.4% YoY in February), but below the 3.4% YoY exp…

Source: Bloomberg

This is the highest headline CPI YoY since April 2024 and biggest MoM jump since June 2022.

Obviously, Energy dominated the rise in headline CPI…

CPI Highlights:

CPI rose 0.9% MoM in March, up from 0.3% in February; it rose 3.3% YoY, up from 2.4% in February.

The index for energy rose 10.9% in March, led by a 21.2% increase in the index for gasoline which accounted for nearly three quarters of the monthly all items increase.

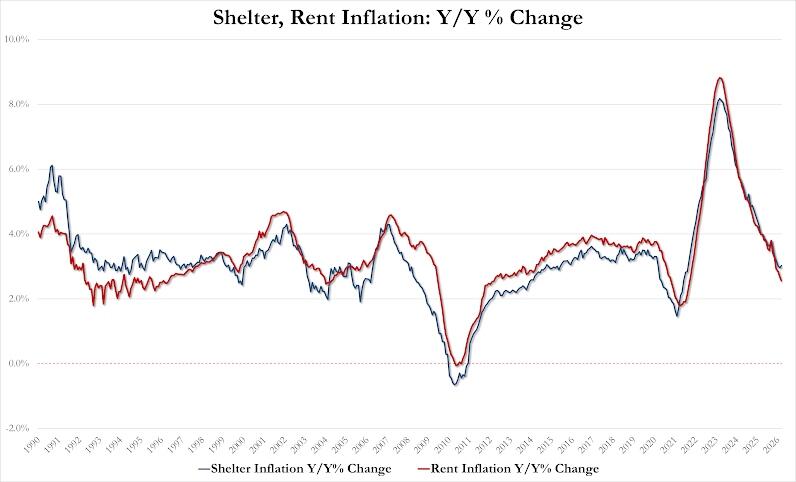

The shelter index also increased in March, rising 0.3%.

The index for food was unchanged over the month as the index for food away from home rose 0.2%, while the index for food at home fell 0.2%.

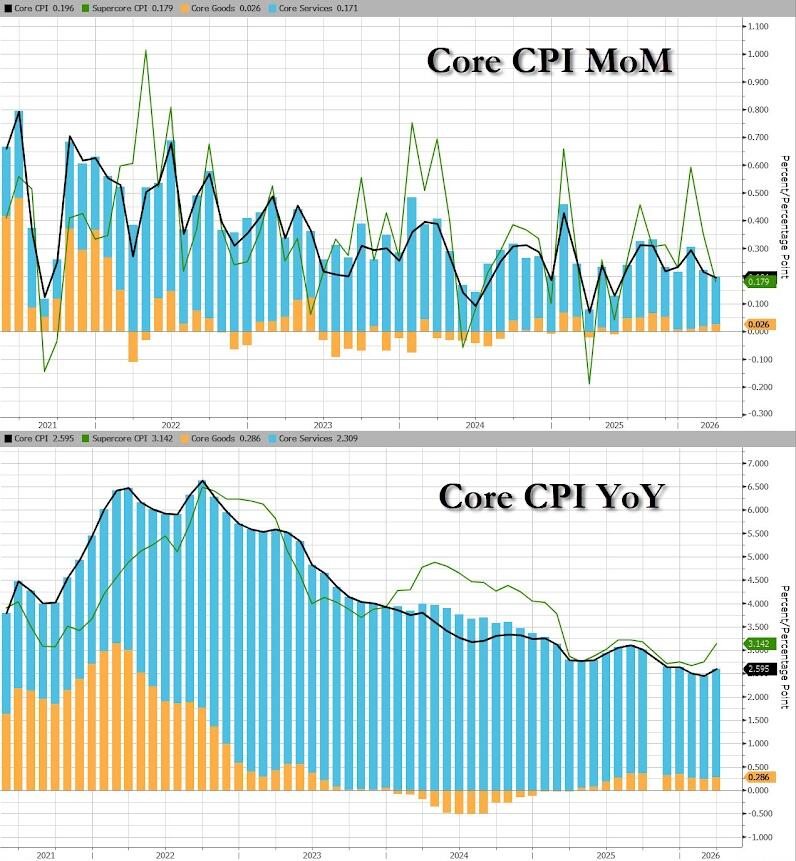

Core CPI rose 0.2% in March: Indexes that increased over the month include airline fares, apparel, household furnishings and operations, education, and new vehicles. Conversely, the indexes for medical care, personal care, and used cars and trucks were among the major indexes that decreased in March.

Core CPI rose 3.3% YoY for the 12 months ending March, after rising 2.4% in February. The all items less food and energy index rose 2.6% over the year, following a 2.5% increase over the 12 months ending February. The energy index increased 12.5% for the 12 months ending March. The food index increased 2.7% over the last year.

Food:

The index for food was unchanged in March after rising 0.4% in February.

The food at home index declined 0.2% over the month. Four of the six major grocery store food group indexes decreased in March.

The index for meats, poultry, fish, and eggs decreased 0.6% over the month as the index for eggs declined 3.4%.

The cereals and bakery products index also decreased 0.6% in March, as did the dairy and related products index.

The index for nonalcoholic beverages fell 0.3% over the month. In contrast, the fruits and vegetables index rose 1.0% in March.

The index for other food at home was unchanged over the month.

The food away from home index rose 0.2% in March. The index for full service meals rose 0.3% over the month and the index for limited service meals rose 0.2%.

Energy CPI highlights – a gas/electricity hammering thanks to Iran/Data centers:

The index for energy increased 10.9 percent in March, the largest monthly increase in the index since September 2005.

The gasoline index increased 21.2 percent over the month, the largest monthly increase since the series was first published in 1967. (Before seasonal adjustment, gasoline prices increased 24.9% in March.)

The index for electricity rose 0.8% in March.

The fuel oil index increased 30.7% over the month, the largest monthly increase in the index since February 2000. Conversely, the index for natural gas decreased 0.9% over the month.

Gasoline’s surge accounted for two-thirds of the rise in headline CPI…

Energy CPI is tracking WTI (and has room to rise further if oil remains disrupted)…

Core CPI (excluding Energy and Food prices) printed cooler than expected (+0.2% MoM vs +0.3% MoM exp) with the Core YoY rising only modestly from February…

Source: Bloomberg

Core Services costs slowed modestly…

Source: Bloomberg

All items less food and energy…

The shelter index increased 0.3% over the month as did the owners’ equivalent rent index.

The index for rent increased 0.2% in March.

The lodging away from home index rose 0.2% over the month.

The index for airline fares increased 2.7% over the month, after rising 1.4% in February.

The apparel index rose 1.0% in March and the household furnishings and operations index rose 0.2%.

The index for education rose 0.3% over the month and the index for new vehicles rose 0.1% in March.

The medical care index decreased 0.2% in March, after rising 0.5% in February.

The index for prescription drugs decreased 1.5% over the month. Conversely, the physicians’ services index increased 0.7% over the month and the hospital services index rose 0.4%. The personal care index declined 0.5% in March and the used cars and trucks index decreased 0.4% over the month.

The index for recreation and the index for motor vehicle insurance were both unchanged over the month. The index for all items less food and energy rose 2.6% over the past 12 months. The shelter index increased 3.0 percent over the last year.

Other indexes with notable increases over the last year include medical care (+3.1 percent), household furnishings and operations (+4.0 percent), airline fares (+14.9 percent), and recreation (+2.2 percent).

Obviously, short-term (annualized) CPI is exploding higher…

SuperCore CPI (Services ex-Shelter) lifted very modestly on a YoY basis with Transportation Services the biggest driver…

Source: Bloomberg

The trend for slowing cost-of-housing inflation remains lower, but March did see notable MoM jumps…

Shelter inflation up 0.4% MoM, biggest monthly increase since Jan 2025. also up 3.02% YoY, first annual increase since Sept 2025

Rent inflation up 0.2% MoM, and up 2.56% YoY, slowest annual increase since Oct 2021

Nothing too surprising here for policymakers to fret over and rate-cut odds are modestly higher since the print.

The market seems willing right now to look through the spike – let’s just hope the ’70s analog is not about to play out.

Tyler Durden

Fri, 04/10/2026 – 08:41

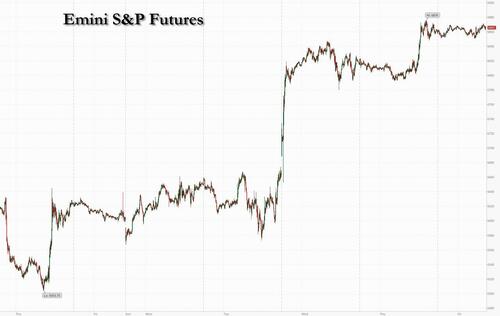

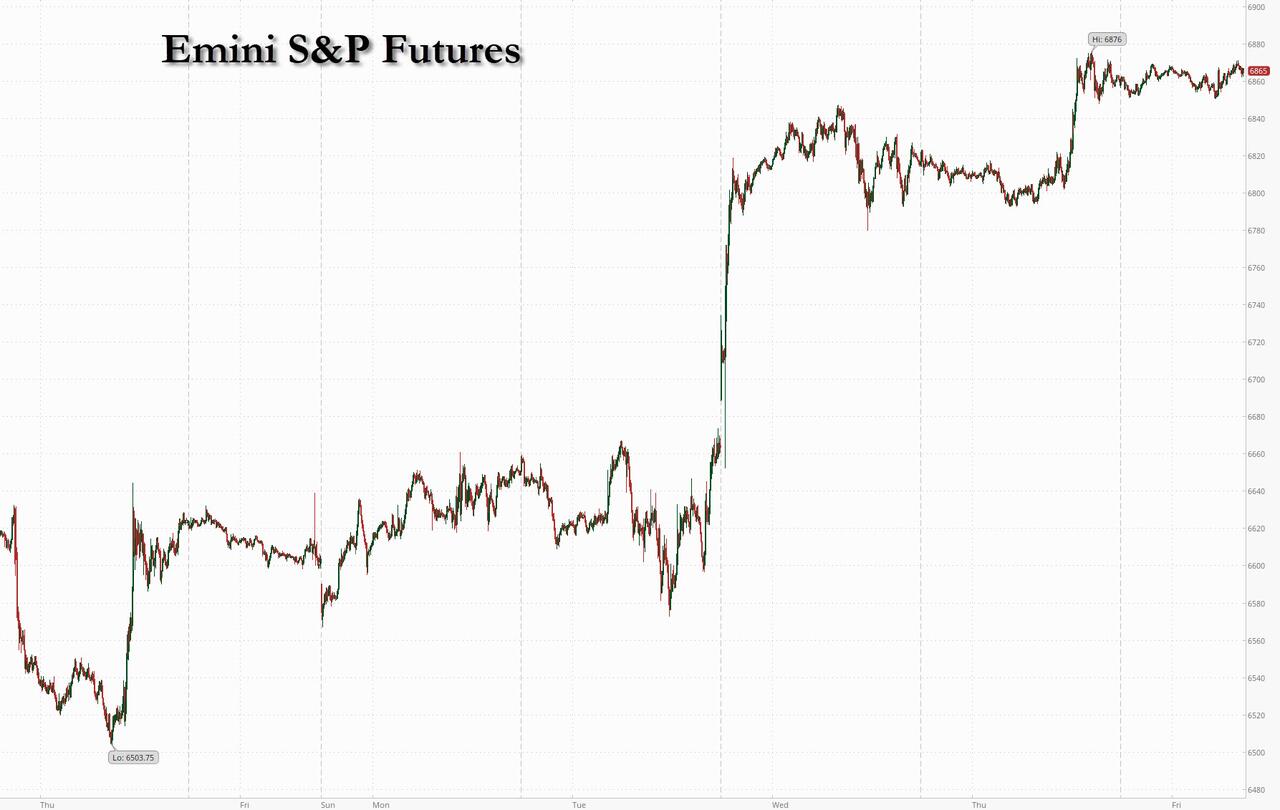

Futures Flat Ahead Of CPI, Ceasefire Negotiations

Futures Flat Ahead Of CPI, Ceasefire Negotiations

US equity futures are flat, recovering from an earlier drop, and set to extend a seven-day rally, the longest since October, as investors looked to talks between the US and Iran for signs a fragile truce can hold while bracing for a big jump in today’s CPI report (full preview here). As of 8:00am ET, S&P futures were up 0.1%,on track for their biggest weekly advance in almost a year. Nasdaq futures rose 0.2%, its winning streak is the longest since September, led once again memory stocks while Mag 7 were mixed (NVDA -0.5% and MSFT +0.5%). Europe’s Stoxx 600 gained 0.8% as Ukraine’s top negotiator with Russia expressed optimism about peace talks. Overnight, headlines were mostly quiet as investors continue assessing the negotiation progress between the US and Iran. Hormuz and Lebanon remains the two key focuses. Meanwhile, a BBG headline this morning saying that Ukraine may be near a deal with Putin drove futs modestly higher; gold trades flat around $4,765. Bond yields are unchanged to 1-2bp lower, the 10Y TSY trading at 4.29%; oil is 1% higher to $98.6; base metals are mostly lower. Brent crude was steady at near $96 a barrel but on pace for its steepest weekly loss in nine months. On today’s calendar, we have March CPI due at 8:30 a.m. ET, followed by factory orders for February and final readings for February durable/cap goods at 10 a.m. University of Michigan Sentiment also due at 10 a.m.

In premarket trading, Magnificent Seven stocks are mostly higher (Microsoft +0.2%, Meta +0.6%, Alphabet +0.2%, Amazon +0.2%, Apple -0.3%, Tesla +0.2%, Nvidia -0.1%)

CoreWeave (CRWV) gains 4% after Anthropic PBC agreed to rent data center capacity from the company.

Docusign (DOCU) slips 1.7% after Citi downgraded the company and other application software stocks to neutral, saying the group they doesn’t have any exciting 12-month catalysts. The other downgraded stocks include Autodesk (ADSK), which is down 1.4%.

Kyivstar Group (KYIV) rises 9% after Ukraine’s top negotiator with Russia said he sees progress toward a possible peace deal between the two countries.

Lumentum (LITE) climbs 5% after the firm said demand from the biggest US tech companies is accelerating. Peer Coherent (COHR) climbs 4%.

Organon & Co. (OGN) soars 21% after the Economic Times reported that Sun Pharmaceutical is set to make a $12 billion offer for debt-ridden company. Sun Pharmaceutical called the report speculative in nature.

Taiwan Semiconductor Manufacturing Co.’s ADRs (TSM) are up 2% after the company reported March sales that reinforced how the company is seeing strong AI demand.

Tecnoglass (TGLS) slips 2% after the window manufacturer lowered its full-year adjusted Ebitda outlook due to tariffs on certain aluminum-containing products and derivatives.

In other corporate news, an earnings beat by CATL may set the stage for a short squeeze, after a surge in the battery maker’s shares on bets tied to soaring energy prices. Lumentum said demand from the biggest US tech companies for its optical components is accelerating and on track to fill its order books through 2028. AI is also on traders’ radars this Friday. TSMC reported a 35% increase in quarterly revenue, suggesting ongoing global chip demand remains intact. China AI firm Sharetronic procured hundreds of Super Micro systems containing banned high-end Nvidia chips. Treasury Secretary Bessent and Fed Chair Powell summoned Wall Street bank CEOs to discuss Anthropic’s new AI to discuss cyber risks.

Anticipation of weekend talks between the US and Iran following this week’s ceasefire agreement are keeping markets on edge. The longest winning run for the S&P 500 since October looks set to be tested as traders prepare for CPI data before attention turns to US-Iran discussions in Islamabad at the weekend. The truce announced on Tuesday remains shaky, with Kuwait reporting large-scale drone attacks on “vital” facilities overnight and accusing Iran and its proxy groups of violating the terms of the agreement.

Israel continued to target towns in south Lebanon, where its parallel campaign against Tehran-backed Hezbollah threatens to undermine negotiations. “I’m not trimming into the weekend,” said Rajeev De Mello, global macro portfolio manager at Gama Asset Management SA. “The direction of travel seems to be to talk rather than to fight.”

The latest tone in markets suggests some optimism negotiators from Washington and Tehran will make progress on longer term de-escalation, despite the remaining points of tension. Whatever the outcome, there are plenty of supply chain bottlenecks and delayed consequences still to work through. Daily commercial traffic through the Strait of Hormuz remains close to zero. The “Trillion Dollar War” is weighing on global economic outlooks, note Bloomberg Economists whose global growth tracker – which uses a machine-learning algorithm to extract signals from data for 18 advanced and EM economies – points to an abrupt reversal, after a build-up in momentum at the start of the year. “Investors are hoping for fruitful negotiations,” said Guillermo Hernandez Sampere, head of trading at asset manager MPPM. Still, “a swift conclusion will be difficult to achieve, as economic interests prevail on all sides and no one wants to be disadvantaged,” he said.

Oil remains in focus. Saudi Arabia said its production capacity has been reduced by attacks on energy infrastructure. WTI could hold at $100 a barrel – or higher – for longer if disruptions to tanker traffic keep global crude flows constrained, Bloomberg notes pointing to a surge in net long crude futures amid oil’s widening risk premium.

“We believe this could be the beginning of the end, and is presenting an opportunity for investors to focus on pre-war trends and fundamentals,” Bernstein analysts Rupal Agarwal and Cheng Zhang wrote in a note.

Some investors are not convinced that the ceasefire marks the end of trouble for financial markets. Crude remains over $90 a barrel, a level that threatens to drive inflation and suppress economic growth. “I’m not very optimistic at all,” said Nick Ferres, chief investment officer of Vantage Point Asset Management in Singapore. “Overall, our sense is that the sustained premium in crude is not reflected yet in profit margins, and that ought to contribute to a higher equity risk premium.”

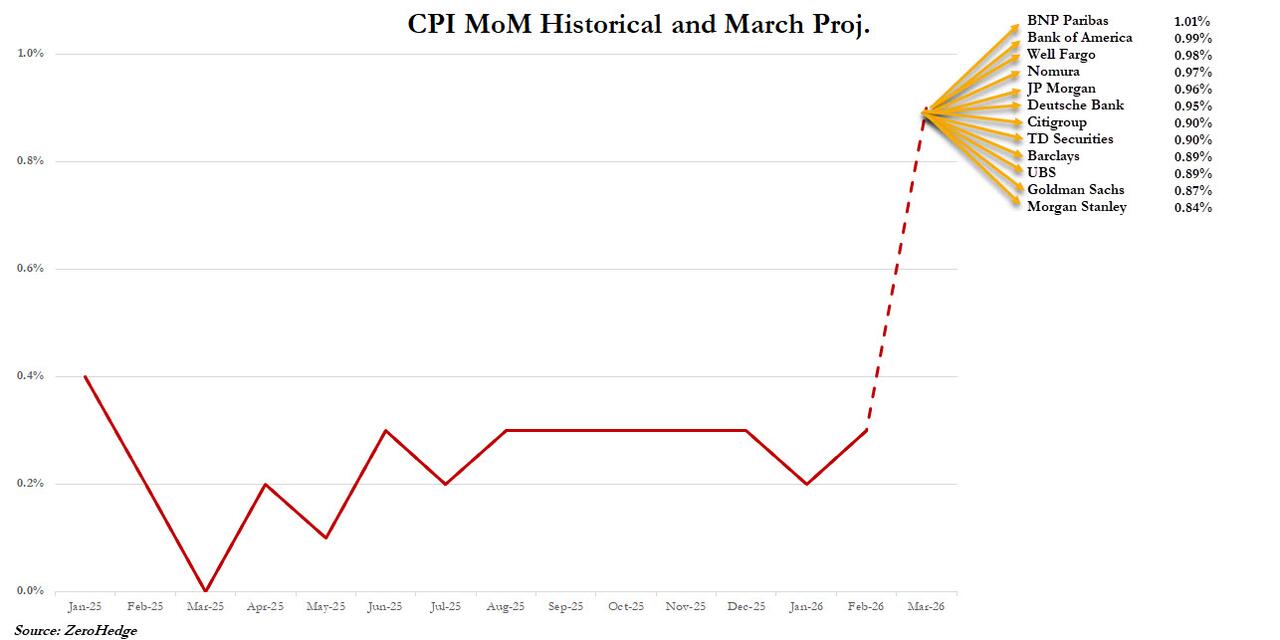

The March CPI report is expected to show gasoline prices drove the fastest monthly increase in the headline gauge in almost four years, while core CPI will likely remain tame. The Cleveland Fed nowcast point to headline CPI of around 3.25% Y/Y in March (vs an actual 2.4% in February), though core inflation should be steadier at around 2.5% Y/Y, suggesting the March strength is likely to come from fuel and other energy-related components rather than a broad-based underlying inflation surge. Wall street upside estimates are even more aggressive, with median expectations for headline CPI surging from 0.3% MoM to 0.9%, and from 2.4% to 3.4% YoY. (Our full preview is here).

“Headline risk pertaining to the war remains far and away the biggest driver of volatility,” Kyle Rodda, a senior financial market analyst at Capital.com, wrote in a note. “However, inflation data also presents meaningful event risk.”

Europe’s Stoxx 600 gained 0.8% as Ukraine’s top negotiator with Russia expressed optimism about peace talks, stocks are led by construction and media. Markets received an additional boost from news of a potential peace deal between Ukraine and Russia, though that dented defense stocks. Italian luxury brand Brunello Cucinelli jumped after impressive results, while Sodexo’s disappointing guidance weighed on its stock. Here are the biggest movers Friday:

Brunello Cucinelli gains as much as 6.6% after the Italian luxury clothing company reported solid first-quarter earnings thanks to strong retail sales, which according to analysts, confirms the company’s stand-out position in the sector

Reply shares rose as much as 8.4% in Milan trading, the most in a year, after the Italian digital services firm announced that it would buy back ordinary shares worth as much as €550m

Holcim rises as much as 3.1% after Goldman Sachs upgrades the Swiss building materials company to buy from neutral, seeing an attractive entry point following the stock’s decline this year

Tomra gains as much as 7.1% after Pareto Securities reiterated its buy recommendation on the Norwegian recycling equipment firm, saying the blue-sky scenario related to changes in the European deposit-return scheme is materializing

Instalco gains as much as 9.2%, the most since February, after both Pareto Securities and SEB raised its recommendations on the Swedish building installation and maintenance firm to buy from hold

Plejd shares gain as much as 16% to hit a fresh record high after earnings from the Swedish electrical equipment maker surpassed Bloomberg-compiled consensus expectations across all metrics, with first-quarter Ebit 49% ahead

Sodexo shares plunge as much as 20%, to the lowest level since 2011, after the French food services company issued weaker-than-expected guidance for organic revenue growth and underlying operating margin

DEME Group shares fall as much as 8.8%, the most in a year, after ING lowers its rating to hold from buy, citing headwinds it sees lying ahead for earnings at the Belgian engineering firm

Leonardo shares fall as Italy’s government picked a former executive at the aerospace and defense company, Lorenzo Mariani, to replace Roberto Cingolani as CEO. Mariani currently works for missile maker MBDA

Asian stocks advanced, posting their biggest weekly gain since November 2022, as a ceasefire between the US and Iran triggered a relief rally. The MSCI Asia Pacific Index gained 0.7%, taking its weekly increase to 6%. Chipmakers TSMC and SK Hynix were among biggest boosts to the gauge Friday. Indonesia’s benchmark jumped 2%, leading gains around the region, followed by Taiwan, mainland China and South Korea. The week’s advance signals a return of risk appetite across Asian markets after steep losses in March on concerns over the war. Still, uncertainty remains over the chances for lasting peace and the trajectory for oil prices.

In FX, the Bloomberg Dollar Spot Index gains 0.1%, snapping a four-day decline. The gauge has still dropped 1.2% this week, headed for its worst performance since January. The yen edged lower against the dollar; Japanese bonds dropped amid expectations for a near-term rate hike by the Bank of Japan. Japanese Finance Minister Satsuki Katayama says authorities are prepared to take action on all fronts in markets, considering the impact of currency moves on households and the economy.

In rates, US treasuries were on track to snap a four-day run of gains as investors await March US inflation data due later Friday to see the impact of higher oil prices from the Iran war. Treasuries are slightly cheaper across the curve, with yields off session highs in early US trading ahead of March CPI report expected to show the biggest monthly headline increase in almost four years, driven by gasoline prices. US yields are 1bp-2bp cheaper across a slightly steeper curve, 10-year by 1.8bp near 4.29%; German and UK counterparts lag by 3bp and 4bp respectively. In Europe, bonds slide as traders add to rate-hike bets again, with European and UK 10-year yields rising between four and seven basis points and German 30-year yields hitting the highest since 2011. Ahead of CPI data, Fed-dated OIS contracts price in around 6 basis points of easing by the end of the year and fully price in a quarter-point move by September 2027

In commodities, WTI crude oil futures are little changed after erasing a 2.6% increase. Brent trades close to $97/barrel and WTI around $98. Gold prices drifting lower to around $4,750/oz.

The US economic data calendar includes March CPI (8:30am), February factory orders, April preliminary University of Michigan sentiment (10am) and March federal budget balance (2pm)

Market Snapshot

S&P 500 mini little changed, Nasdaq 100 mini little changed, Russell 2000 mini -0.2%

Stoxx Europe 600 +0.4%, DAX +0.2%, CAC 40 +0.3%

10-year Treasury yield +2 basis points at 4.29%

VIX -0.1 points at 19.43

Bloomberg Dollar Index little changed at 1200.13, euro little changed at $1.1704

WTI crude +0.8% at $98.66/barrel

Top Overnight News

President Trump on Thursday demanded Iran stop charging tolls for tankers to cross the Strait of Hormuz, as Iran’s supreme leader promised the country would control the crucial waterway. Axios

The truce remained shaky, as Kuwait reported overnight drone attacks. Israel is preparing for talks with Lebanon but said it’ll continue strikes on Hezbollah, with Trump’s push for an exit straining relations. BBG

President Donald Trump told NBC News on Thursday that he was “very optimistic” a peace deal with Iran was within reach as a diplomatic delegation led by Vice President JD Vance prepared to head to Pakistan for high-stakes talks aimed at ending the nearly six-week conflict. NBC

Volodymyr Zelenskiy’s top negotiator with Russia said he sees Ukraine nearing a peace deal with Vladimir Putin. “They all understand the war needs to end,” Kyrylo Budanov said in an April 4 interview with Bloomberg. BBG

While every administration crafts its own defense strategy, Trump’s second is making the unusual move of discarding a policy that was formulated by his first. That bipartisan approach sanctioned by Trump 1.0 characterized China as the most consequential U.S. adversary. The Trump 2.0 framework is instead a seismic shift in U.S. policy, trade practices and rhetoric toward Beijing driven by a new mantra: Don’t rock the boat. WSJ

China made a rare diplomatic foray in the Iran war, nudging Tehran to agree to sit down for talks with the U.S. Beijing’s role wasn’t decisive, but Chinese leader Xi Jinping now has something valuable: diplomatic capital with President Trump. WSJ

China’s factory-gate prices rose for the first time in more than three years in March, in an early sign that the war in Iran is feeding cost pressures into the world’s second-largest economy. China’s PPI came in a bit firmer than anticipated at +0.5% Y/Y (vs. the Street +0.4% and up from -0.9% in Feb) while the CPI ran a touch cooler at +1% (vs. the Street +1.1% and down from +1.3% in Feb). RTRS

Trump administration reportedly considering a new crackdown on Chinese telecom Carriers’ US operations, according to the agency.

Artificial intelligence lab Anthropic is exploring the possibility of designing its own chips, three sources said, as the company and its rivals respond to a shortage of AI chips needed to power and develop more advanced AI systems. Also, Scott Bessent and Jerome Powell summoned Wall Street CEOs to warn of potential cyber risks from Anthropic’s new AI model and others. RTRS, BBG

CPI Preview: We expect a 0.28% increase in March core CPI (vs. +0.3% consensus), corresponding to a year-over-year rate of 2.69% (vs. +2.7% consensus). We expect a 0.87% increase in headline CPI (vs. +1.0% consensus), reflecting sharply higher energy prices. Our forecast is consistent with a 0.23% increase in core PCE in March. Goldman

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher following the gains on Wall Street, where markets extended on the ceasefire-driven momentum, although strikes continued in the region and Israel declared it will keep striking Lebanon ahead of talks next week. Furthermore, shipping through the Strait of Hormuz remained at a virtual standstill, and US President Trump criticised Iran on the Strait of Hormuz and warned it to stop charging tolls in the strait. ASX 200 was dragged lower by underperformance in tech and energy, while nearly all sectors were lacklustre, aside from the mild resilience seen in real estate and financials. Nikkei 225 rallied with index heavyweight Fast Retailing among the top gainers after its shares surged to fresh record highs following strong earnings results, while participants also reflected on PPI data, which ultimately printed mixed, but showed an acceleration for both the M/M and Y/Y figures. Hang Seng and Shanghai Comp were higher amid some strength in tech, property and auto stocks, while the latest inflation data for China was mixed as CPI printed softer-than-expected, but PPI slightly topped forecasts and showed a return to growth in factory gate prices for the first time in more than three years.

Top Asian News

Japan’s Finance Minister Katayama declines to comment on FX levels and said the government is prepared to take decisive action in markets, but will not elaborate on future potential measures. said: Speculation is intensifying in oil, futures, and currency markets.

Japanese Finance Minister Katayama say unable to gauge the effect of a food sales tax reduction on prices at this stage and not in a position to discuss steps against possible oil supply deficits. Will co-chair a session on critical minerals on the margins of the G7 meeting. Private credit will be on the G7 agenda but no significant crisis is seen and Japan has no substantial exposure. G7 finance ministers unanimously agree the Middle East situation should not be extended.

South Korean parties agree on an extra budget size of KRW 26.2tln, according to Yonhap.

European bourses (STOXX 600 +0.5%) are gaining heading into the US-Iran talks at the weekend. If indices can hold onto their gains, it would be the first Friday since the Iran war began that stocks would end in the green. The complex has been fairly choppy this morning, with some pressure seen alongside a slight bid in the crude complex, but then reversed those losses after reports suggested that Ukraine’s top aide Budanov reportedly saw Ukraine nearing a deal with Russian President Putin. European sectors are broadly in the green. Media, Health Care and Technology tops the sector pile while Basic Resources and Travel and Leisure lags. The tech sector has been given a boost after TSMC reported YTD sales that beat estimates, supporting the likes of ASML and STMicroelectronics. On the other hand, Travel and Leisure is under pressure following earnings by Sodexo, in which the Co. cut its 2026 organic revenue growth forecast, citing ongoing execution challenges. US equity futures (ES/NQ U/C, RTY -0.1%) are posting modest losses ahead of the US CPI later, in which headline inflation is expected at 3.3% Y/Y, rising from 2.4% while core inflation also expected to rise to 2.7% Y/Y from 2.5%.

Top European News

US President Trump endorses Hungarian PM Orban, reiterates that he’s a truly strong and powerful leader with a proven track record delivering phenomenal results.

UK retail footfall returned to growth in March as a number of visits to stores comprising of main street shops, retail parks and shopping centres for the five weeks to April 4th rose 2.4% Y/Y, according to the British Retail Consortium.

FX

Energy prices continue to dominate price action across G10 currencies, with USD leading. Focus remains on geopolitical updates, none of which overnight did much to spur crude benchmarks ahead of US/Iran talks scheduled this weekend. This morning, newsflow has been light, though there were reports that Iran said no talks would happen until attacks [on Lebanon] stop. US CPI is due at 13:30 London time; today’s release should not be a game-changer for the Fed unless the print significantly exceeds expectations, policy will likely be dictated after members assess the second round effects of the Middle East conflict in future months’ prints.

Do note that the USD saw some mild selling pressure to session lows of 98.79 (vs 99.00 peak), after reports suggested that Ukraine’s top aide Budanov reportedly saw Ukraine nearing a deal with Russian President Putin. But it is worth highlighting that the interview was conducted on April 4th, while recent rhetoric via Ukrainian President Zelensky suggested that Putin is not genuinely seeking peace.

EUR will look to Sunday’s Hungarian election (Full Preview), where polling suggests opposition support Tisza will take power, though still unclear whether the opposition will gain a supermajority or a simple majority. Desks suggest a supermajority sees HUF and EUR strength, while a simple majority may see initial HUF gains and potential EUR strength, “likely to be pared”. EUR/USD marginally surpassed the 1.17 level with a session high at 1.1702. Elsewhere for the single currency, German inflation was left unrevised at 1.1% on a monthly basis.

For NOK, Norwegian core inflation this morning surprised to the downside, but still remains elevated on a 3% handle, in line with the Norges Bank’s forecast. With markets shrugging off the modest gains in crude this European morning, the net energy exporter’s currency is flat/modestly lower against EUR within a 11.0839-11.1194 range.

Kiwi is the worst-performing G10 currency against a stronger buck, after the rally in the pair stalled just above 0.5870. Likely an element of profit-taking after gains over the past two days, with markets continuing to price 75bps of hikes by year end, unchanged from Thursday’s close. Additionally, key metals trade 1-2% lower – as such, AUD also underperforming against the greenback.

Fixed Income

Fixed benchmarks are flat/mixed this morning, as the complex awaits US CPI later today and heading into the weekend, where US and Iranian officials are to meet for peace talks in Pakistan. While preparations are proceeding “full steam ahead” in the Pakistani capital, both sides have issued warnings that could still derail the meeting. Heading into the confab, US President Trump said he is optimistic that an Iran peace deal is within reach, but warned that if no deal is reached, “it is going to be very painful”.

USTs are currently flat, with price action lacklustre heading into US CPI. Currently trades within a 111-05 to 111-11+ range, with the 2yr yield hovering near familiar levels at 3.795%, but still well off the extremes seen during the heights of the Iranian war. Traders are currently awaiting the US inflation report, where analysts expect consumer prices to rise by 0.9% M/M (prev. 0.3%), and the annual rate to jump to 3.3% Y/Y (prev. 2.4%); core inflation is expected to rise 0.3% M/M (prev. 0.2%). Officials say inflation remains too high, with upside risks if oil shocks spill into core prices and expectations, although expectations are still seen as well anchored at this point.

Recapping the action this week, USTs are currently higher by 16 ticks vs the Monday open, with strength facilitated by ceasefire related optimism – however, US paper has pulled back from highs given the fragile nature of the two-week pause so far. US 2s10s is near enough unchanged since the start of the week, but did experience some steepening amidst the initial ceasefire related optimism.

Bunds and Gilts are trading on either side of the unchanged mark, with both currently just off session lows. Earlier, Final German Inflation was unrevised in March, and had little impact on Bunds this morning. The action this week across Bunds is reflective of the easing tensions in the Middle East, with the 2yr yield now residing around 2.56% vs the Tuesday open at 2.65%. This has also been reflected in ECB pricing – with money markets fully pricing in an ECB rate hike in April towards the start of the week, now, only 6bps. The temporary ceasefire will allow policymakers to bide their time and assess whether second-round inflation effects filter through into the economy – markets still pricing in two hikes by year-end.

Commodities

Oil rose for a second consecutive session after Saudi Arabia said attacks on energy infrastructure had reduced its production capacity, with Brent climbing above USD 96/bbl. Despite the rebound, both benchmarks remain on course for their largest weekly loss since June, following Tuesday’s ceasefire announcement. Middle East situation aside, a piece in Bloomberg suggested that Ukraine’s top aide Budanov reportedly saw Ukraine nearing a deal with Russian President Putin – though this interview was conducted on April 4th. Nonetheless, this spurred some pressure in Brent Jun’26, falling to a session low of USD 96.03/bbl before paring back towards USD 97/bbl mark, with gains currently around USD 1/bbl.

Ahead, the focus is on weekend talks between the US and Iran in Islamabad, Pakistan. The diplomatic picture remains complicated, however. US President Trump said he was “optimistic” about a deal but threatened Tehran over reported fees being levied on tankers in the Strait of Hormuz, adding that Iran was doing a “poor job” of allowing energy supplies to flow despite ceasefire commitments. He also asked Israeli PM Netanyahu to scale back attacks on Lebanon, amid concerns the fighting could undermine negotiations – a view echoed by both Iran and ceasefire mediator Pakistan, which have described Israel’s Lebanon offensive as a truce violation.

Spot gold trades subdued on either side USD 4,750/oz (USD 4,731-4,780/oz), but on track for a third straight weekly gain, supported by central bank buying and diplomatic hopes. Critical Metals’ CEO cautioned that bullion could face pressure if oil prices rebound materially, stoking inflation concerns and rate expectations.

Copper is flat in indecisive trade with broader base metals mixed. 3M LME copper currently trades in a 12,641.00- 12,772.87/t range. In data, China’s factory deflation ended after more than three years, with PPI rising 0.5% Y/Y in March (exp. 0.4%), as surging energy costs snapped the deflationary streak.

US offers 30mln barrels in crude oil exchange from the Strategic Petroleum Reserve, as part of IEA coordinate release.

Japanese PM Takaichi said to release about 20 days of oil stockpiles in May.

China allows state oil firms to release their reserves amid US-Iran conflict.

TotalEnergies (TTE FP) said it shut down SATORP refinery in Saudi Arabia as safety precaution following processing train damage.

EU and US nearing a critical minerals deal to “combat Chinese control”, Bloomberg reported.

Venezuela passes mining law as Acting President Rodriguez courts investment, according to Bloomberg.

Central Banks

US Senate Banking panel is no longer intending to conduct a confirmation hearing for Kevin Warsh next week with the delay due to paperwork.

BoJ Deputy Governor Himino said no strict definition on what constitutes stagflation, adds must be vigilant to chance Middle East conflict, which if prolonged, could work to weigh on the economy and push up inflation. Doesn’t think Japan’s economy is in stagflation. Face dilemma if prolonged Middle East conflict pushes down growth and accelerates inflation. Will make appropriate decisions on price target and will make the appropriate decision at each meeting. Will take most appropriate policy to stably hit the inflation target, considering scale and duration of shocks and broader economic environment.

BoK maintains the Base Rate at 2.50%, as expected.

BoK said rate decision was unanimous and that Middle East conflict poses risks to growth. Growth likely to be below 2% this year. To thoroughly assess external and internal conditions including the Middle East situation. To closely monitor impact on inflation, growth and financial stability. Necessary to remain cautious about FX volatility. Inflation likely to be significantly above 2.2% this year. Raises 2026 GDP growth forecast to 2.0% from 1.8% and CPI forecast to 2.2% from 2.1%.

BoK Governor Rhee said growth path to hinge on the Middle East and trade conditions, adds board members are in wait-and-see mode as Middle East conflict situation is too volatile. It is too early to judge the direction of the Middle East shock, stating that a temporary shock does not warrant a rate response, although a prolonged shock may require a policy response. Iran war has a bigger impact on inflation and growth outlook in South Korea than the war in Ukraine. To assess the size and duration of the Middle East war impact. Too early to discuss a rate hike amid Middle East volatility. Board needs to watch the course of Middle East negotiations first. Asian economies more vulnerable to supply-side impact from Iran war compared to European economies.

Geopolitics: Iran

US President Trump posted “Iran is doing a very poor job, dishonourable some would say, of allowing Oil to go through the Strait of Hormuz. That is not the agreement we have!”.

US President Trump posted “There are reported that Iran is charging fees to tankers going through the Hormuz Strait — They better not be and, if they are, they better stop now!”.

US President Trump criticises WSJ for stating he declared premature victory in Iran, adds there is nothing premature about it, also said because of him, Iran will never have a nuclear weapon and oil will start flowing very quickly.

Iran reiterates no talks will happen until attacks stop and no delegation is heading to Pakistan. However, it was reported that the Iranian delegation arrived in the Pakistani capital of Islamabad late on Thursday for upcoming talks, with the delegation led by Iranian Foreign Minister Araghchi and Parliament Speaker Ghalibaf.

Informed source told Tasnim that news in some media about the arrival of Iranian negotiating teams to Islamabad to negotiate with Americans is completely false, adds until US fulfils commitments negotiations are suspended.

Iranian delegation has not yet reached Islamabad despite plans for the first round of negotiations today, Pakistan media report.

IRGC affirms Iran’s armed forces have absolutely not carried out any launches towards any country during the ceasefire hours up to this moment.

UK Government said UK PM Starmer and US Present Trump spoke this evening, and agreed there is a ceasefire in place, agreement to open the Strait, and we are at the next stage of finding a resolution. Discussed the need for a practical plan to get shipping moving again as quickly as possible and agreed to speak again soon.

Iranian Supreme Leader Khamenei may deliver address to the nation soon, TASS reported.

Israeli Chief of Staff Zamir said will continue the war in Lebanon, can return to the war against Iran at any moment and with greater force.

Israel is working to continue the war on Lebanon within two days and 5 more days before responding to American pressures, Al Jazeera reported citing Ma’ariv sources.

Israeli airstrike targets Habbouch town in southern Lebanon, while reported also noted that siren sound in Metula, Israel.

Iranian media reported of intense activity of hostile drones in Iranian cities Tehran, Parachin, Tabriz, and other cities.

Six rockets were fired from southern Lebanon towards Al Jalil in northern Israel.

Air raid sirens have sounded in the Mizgav Am and Metula settlements in northern Israel.

Air raid alarms were activated in Tel Aviv, while Israeli military said Hezbollah launched a missile at Israel which set off air raid alarms.

Warning sirens sound in Kiryat Shimona and surrounding areas, according to Mehr News.

Shipping traffic in Strait of Hormuz was down on Thursday as just six ships travelled through the strait with two oil tankers among the six ships, according to CBS.

Geopolitics: Ukraine

Ukrainian President Zelensky’s top aide/negotiator Budanov reportedly sees Ukraine nearing a deal with Russian President Putin, Bloomberg reports; interview conducted on April 4th.

Russia’s Kremlin confirms envoy Dmitriev’s trip to the US, says Dmitriev is not negotiating on a Ukraine settlement.

Geopolitics: Other

Chinese President Xi said China will never tolerate Taiwan independence, CCTV reported.

North Korea’s Foreign Minister tells Chinese counterpart that ties between the two countries are developing into an elevated new phase.

China’s Foreign Minister Wang Yi said it is China’s steadfast stance to strengthen China-North Korea relations, irrespective of any shift in the international landscape, according to KCNA. North Korea has achieved results despite suppression by the US and Western powers.

Cuba’s President said asked the US to engage in a dialogue without condition and not demand changes from our political system.

US Event Calendar

8:30 am: United States Mar CPI MoM, est. 0.94%, prior 0.3%

8:30 am: United States Mar Core CPI MoM, est. 0.3%, prior 0.2%

8:30 am: United States Mar CPI YoY, est. 3.4%, prior 2.4%

8:30 am: United States Mar Core CPI YoY, est. 2.7%, prior 2.5%

10:00 am: United States Feb Factory Orders, est. -0.2%, prior 0.1%

10:00 am: United States Apr P U. of Mich. Sentiment, est. 51.5, prior 53.3

10:00 am: United States Feb F Durable Goods Orders, est. -1.4%, prior -1.4%

10:00 am: United States Feb F Durables Ex Transportation, prior 0.8%

2:00 pm: United States Mar Federal Budget Balance, est. -153.25b, prior -160.53b

DB’s Jim Reid concludes the overnight wrap

The market tone has remained positive this morning, with oil prices steady and fresh gains for global equities ahead of the US-Iran talks in Islamabad tomorrow. Indeed, the S&P 500 (+0.62%) has now risen for 7 consecutive sessions, with futures on the index (+0.01%) just about pointing towards an 8th gain today. Moreover, oil prices have been steady overnight too, with Brent at $96.23/bbl currently, slightly beneath its levels 24 hours ago. And notably, the VIX index (-1.55pts) closed at just 19.49pts yesterday, falling beneath its pre-strike level of 19.86pts on February 27. So for markets at least, the financial stress has continued to ease before the weekend talks.

The main catalyst for that risk-on move was the announcement yesterday that Israel would start direct talks with Lebanon “as soon as possible”, and President Trump said shortly after that Israel was “scaling back” its operations in Lebanon. That’s significant because Lebanon has been a potential key stumbling block around the ceasefire, with Israel issuing evacuation orders in eight neighbourhoods of Beirut yesterday, whilst Iran’s President Pezeshkian said the attacks were a “clear violation” of the ceasefire agreement. So those hopes for a de-escalation in Lebanon helped ease concerns that the broader ceasefire could fall apart ahead of this weekend’s talks.

In general, the tone around the US-Iran talks has remained positive, with Trump telling NBC news yesterday that he was “very optimistic” a peace deal was within reach. He also added that Iran’s leaders “talk much differently when you’re at a meeting than they do to the press. They’re much more reasonable”. That said, he made a couple of more negative posts about Iran yesterday evening, warning that Iran “better not be” charging fees to tankers going through the Strait of Hormuz, warning that “if they are, they better stop now!” And just over an hour later, he then posted that “Iran is doing a very poor job, dishonorable some would say, of allowing Oil to go through the Strait of Hormuz. That is not the agreement we have!”

Nevertheless, markets in Asia have posted further gains overnight, with all the major indices advancing. That includes the Nikkei (+1.77%), the KOSPI (+1.81%), the CSI 300 (+1.18%), the Shanghai Comp (+0.63%) and the Hang Seng (+0.60%). There’ve also been a few stories from the region, with China’s PPI inflation moving back into positive territory in March for the first time since September 2022. The latest release showed PPI at +0.5% (vs. +0.4% expected), although CPI fell back slightly to +1.0% (vs. +1.1% expected). Meanwhile, the Bank of Korea held rates at 2.5% as expected, although their statement said that CPI this year “is expected to exceed considerably the February forecast of 2.2%”.

Against that backdrop, oil prices have been pretty steady, with Brent crude currently up +0.23% overnight at $96.23/bbl. That builds on a modest gain yesterday, when Brent had risen +1.23% ot $95.92/bbl. Even at the intraday high yesterday, shortly before the news on the Israel-Lebanon talks broke, Brent only got up to $99.50/bbl, remaining beneath the $100/bbl mark throughout. So there’s been a clear shift in sentiment since the two-week ceasefire announcement, when oil prices were back at $110/bbl, with the overall market tone still a lot more confident than it was at the start of the week. In addition, 12-month Brent futures have continued to fall, with a -0.17% decline yesterday to $76.74/bbl, and a further -0.30% decline overnight to $76.51/bbl.

Although oil prices have come down since the ceasefire announcement, inflation concerns are still pretty high right now, meaning that all eyes will be on today’s US CPI print for March. That’s an important one, because it’s the first to cover the period since the Iran war began on February 28, and we know from the Euro Area flash CPI print that the energy price spike is now clearly visible in the data. For today, our US economists are expecting a notable jump given the surge in gasoline prices, with monthly headline CPI rising to +0.95% in March. If realised, that would be the highest monthly print since June 2022, and it would also push the year-on-year rate back up to 3.4%, which we haven’t seen since early 2024. Then for core CPI, they expect a smaller uptick given it excludes energy and food prices, with the monthly core print up to +0.33%, and the year-on-year measure at +2.7%.

Ahead of that release, US markets had a volatile session yesterday as the geopolitical headlines came through. Ultimately however, the prospect of direct talks between Israel and Lebanon led to a recovery through the session, with the S&P 500 (+0.62%) closing at a one-month high. In fact, it was the index’s 7th consecutive gain, which left it less than 2.5% beneath its record high from late-January. The Magnificent 7 (+1.58%) led that advance yesterday, but there were gains across the board, while software & services (-2.18%) and energy (-1.19%) being the only industry groups in the S&P 500 to post major declines. Moreover, the geopolitical news meant investors grew more confident that the Fed might still cut rates this year, with markets pricing in a 33% likelihood of a cut by the December meeting by yesterday’s close. That’s the highest probability of a 2026 cut in the last three weeks, which helped 10yr Treasury yields (-1.7bps) to come down to 4.28%.

Earlier in Europe, markets had seen a relative underperformance, with bonds and equities paring back their very strong gains from the Wednesday session. In part, that was driven by more concerns about the European inflation outlook, given its relative exposure to higher oil prices, and the 1yr Euro inflation swap (+12.2bps) moved back up to 3.23% by the close. So that led to a pickup in yields across the board, with yields on 10yr bunds (+4.4bps), OATs (+3.3bps) and BTPs (+3.1bps) all moving higher. And there was a decent pullback for equities as well, with the STOXX 600 (-0.15%) and the DAX (-1.14%) both losing ground.

Finally, we did get a fresh batch of US data yesterday, although much of it was backward looking for the period before the Iran conflict began. The main highlight was the PCE inflation for February, which is the Fed’s target measure. That came in as expected, with headline and core PCE both at +0.4% on the month, in line with consensus. So for headline PCE, that kept the year-on-year measure at +2.8%, whilst core PCE fell back a tenth to +3.0%. Or in other words, inflation was still lingering above the Fed’s 2% target even before the latest energy shock. Otherwise, we also had the weekly initial jobless claims, which rose by more than expected to 219k in the week ending April 4 (vs. 210k expected). And looking even further back, Q4 GDP growth was revised down again in the third estimate, with the latest reading showing an annualised rate of just +0.5% (vs. +0.7% in the second estimate).

Looking at the day ahead now, US data releases include the March CPI print, the University of Michigan’s preliminary consumer sentiment index for April, and factory orders for February. Otherwise from central banks, we’ll hear from ECB Vice President de Guindos.

Tyler Durden

Fri, 04/10/2026 – 08:25

https://www.zerohedge.com/markets/futures-flat-ahead-cpi-ceasefire-negotiations

Why Rent Control Fails: Lessons From New York To Portland

Why Rent Control Fails: Lessons From New York To Portland

Authored by Tom Wilson via The Mises Institute,

Housing costs in New York City have reached a level that many people can no longer afford. The response has been to push for more control—limits on rent increases and expanded tenant protections. The intention is clear. However, housing markets respond to incentives, not intentions.

Under Zohran Mamdani, New York City is moving further in that direction.

The focus is on limiting rent increases, expanding tenant protections, and increasing the role of government in the housing market.

The policy has not fully taken effect yet. Once these rules interact with rising costs, the housing market will respond to the incentives.

Rent control keeps rents down, but it does not keep costs down for the landlord.

There is no cap on insurance premiums. Property taxes can still rise year after year. Maintenance and labor costs continue to climb as well. As those costs rise, landlords are forced to adjust. Some delay maintenance. Others see their margins get too thin to justify the risk.

Single-family rentals are often taken off the market.

The landlord notifies the tenant that the lease will not be renewed, repairs the property, and sells it to an owner-occupant. Each time this happens, the number of available rental units declines.

As supply shrinks, the market tightens.

Landlords become more selective, prioritizing tenants with strong credit, stable income, and clean rental histories. For renters with past evictions or setbacks, finding housing becomes more difficult. A second chance is harder to come by.

Rent control also removes flexibility.

If the city allows a fixed annual increase, the landlord must take it each year or lose it. There is no ability to hold a rent flat during a difficult period and recover it later. What was intended as protection begins to limit discretion.

These outcomes are not unique to one city. They follow the structure of the policy itself. When rent is constrained but costs continue to rise, the system adjusts in predictable ways.

In Portland, similar policies have already been tested. After Oregon implemented rent caps and expanded tenant protections in 2019, the number of single-family homes available for rent fell by roughly 14 percent over the following years, with thousands of units leaving the market, as shown in this analysis of Portland’s rental supply.

That decline came from the same pressures building over time. Costs were not capped, but rents were. This reduced flexibility and increased risk.

Small landlords, who often operate on small margins, were the first to respond. Many chose to exit rather than continue operating under those conditions. Properties were sold, frequently to owner-occupants, and removed from the rental market entirely.

The result was fewer available units, tighter supply, and increased competition among renters. The policy did not eliminate pressure in the system. It shifted where that pressure showed up.

To make housing more affordable, the focus must shift to supply. Rents rise when demand outpaces the number of available units. Constraining rent has been shown to reduce supply and further the imbalance. Increasing supply is what addresses that imbalance.

That means reducing the barriers that slow construction. Zoning restrictions, permitting delays, and regulatory costs all limit how quickly new units can come to the market. When those constraints are reduced, supply can expand and pressure on prices can ease.

This approach works by allowing the market to adjust. As more units become available, competition among landlords increases, and rents stabilize without the need for rigid controls.

It is not a quick fix. It does not produce immediate results that can be pointed to in the next election cycle. However, it addresses the underlying problem rather than shifting the pressure somewhere else.

Demand for housing in cities like New York remains strong. Jobs, population density, and limited space all place constant pressure on available units. When supply cannot expand to meet that demand, prices rise.

The question is not whether a politician’s intention is good. The market does not care about intentions. It responds to incentives.

Tyler Durden

Fri, 04/10/2026 – 08:05

https://www.zerohedge.com/personal-finance/why-rent-control-fails-lessons-new-york-portland

Mexico’s “Energy Sovereignty” Dos Bocas Oil Refinery Hit By Major Fire

Mexico’s “Energy Sovereignty” Dos Bocas Oil Refinery Hit By Major Fire

One of Mexico’s largest refineries, with a processing capacity of 340,000 barrels per day, appears to have suffered a fire in its coke storage area, marking the second incident in less than a month.

The Dos Bocas refinery, built by Pemex in the southeastern state of Tabasco, is the crown jewel of Mexico’s push to reduce dependence on imported gasoline and diesel, especially from U.S. exporters in the Gulf of America. It cost about $21 billion to build and was a major energy project under former President Andrés Manuel López Obrador.

20 mil millones de dólares costo esta basura de Dos Bocas, una gran parte se fue en corrupción y hoy nuevamente de incendia. Para eso quieren el ahorro de las Afores para seguirlo desperdiciando. pic.twitter.com/YluvShvCu4

— (Kizmar) (@antonioaranda_) April 10, 2026

Reuters reports that a fire broke out in the refinery’s coke storage area on Thursday afternoon. This area is where petroleum coke, a solid, carbon-rich byproduct of refining heavy crude oil, is stored. Petcoke is highly combustible, especially when fine dust accumulates.

🔴 ÚLTIMA HORA : Se incendia Dos Bocas pic.twitter.com/udFL7PACIi

— Mario Di Costanzo (@mario_dico50) April 9, 2026

By late Thursday, President Claudia Sheinbaum stated on X that the fire was under control and limited to the coke storage area.

Pemex informa. https://t.co/9HC66pnIdh

— Claudia Sheinbaum Pardo (@Claudiashein) April 10, 2026

“The director of Pemex and the manager of the Olmeca refinery have informed me the fire is confined solely to a coke storage area and is under control,” said President Claudia Sheinbaum.

El director de Pemex y el gerente de la Refinería Olmeca me informan que el incendio se encuentra localizado exclusivamente en un área de almacenamiento de coque y está controlado.