Category: News

Pull-Forward Demand Boosts PC Shipments Amid Memory Crunch Woes

Pull-Forward Demand Boosts PC Shipments Amid Memory Crunch Woes

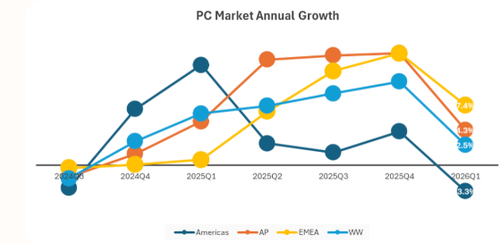

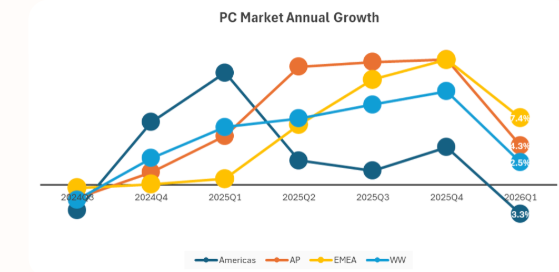

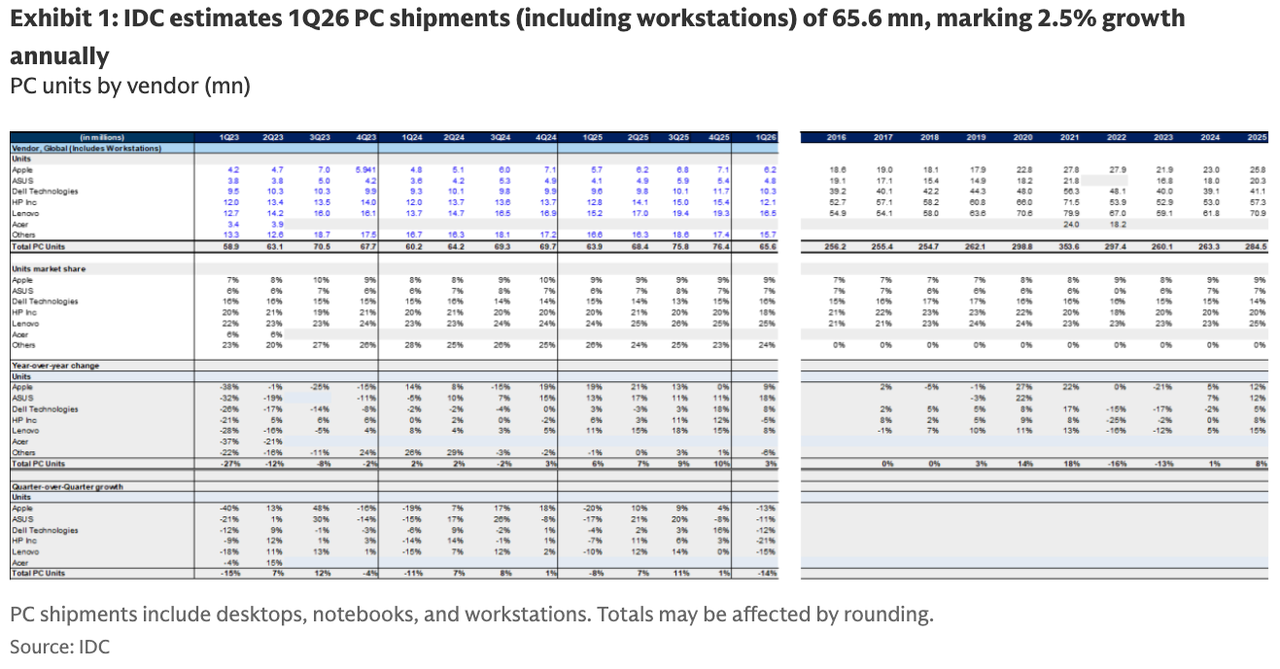

The latest snapshot of the global PC market, from International Data Corporation’s first-quarter shipment tracker, shows units rising 2.5% year over year to 65.6 million.

“Despite deteriorating macroeconomic conditions and memory shortage issues, the PC market recorded another quarter of positive growth,” IDC wrote in the report published on Thursday morning.

IDC said last quarter’s growth was “mostly fueled by the anticipation of rising component prices, Windows 10 migration, and new product introductions.”

Jean Philippe Bouchard, research vice president at IDC, noted, “The strength of every PC vendor’s supply chain and ability to access core components, such as memory, will be tested,” adding, “IDC believes that demand will be met by PC vendors who have best secured access to memory and have a device portfolio capable of addressing all price tiers of the market.”

Here are the key 1Q26 numbers on global PC shipments:

1Q26 Regional Shipments:

IDC estimates industry PC shipments of 65.6 mn grew +2.5% year over year. Global growth was driven by EMEA (+7.4% year over year) and Asia/Pacific (+4.3% year over year), while Americas was down (-3.3% year over year v. +4% in C4Q25). IDC PC unit shipments also include workstations.

1Q26 Vendor Market Share:

IDC estimates that Lenovo, Dell, Apple, and ASUS grew ahead of the market, while HP lagged. Specifically, Lenovo shipments grew 8.6% (25% share), Dell shipments grew +7.7% (16% share), Apple shipments grew +9% (9.5% share), and ASUS shipments grew 17% (7% share), while HP units declined -4.9% (18.5% share).

IDC estimates 1Q26 PC shipments (via Goldman):

Goldman analyst Katherine Murphy commented on IDC’s report and agreed that much of the PC growth in the first quarter was attributed to “a pull-forward ahead of anticipated price increases.”

The pull-forward in PC shipments comes as little surprise, given that industry insiders warned consumers in late January to buy devices heavily dependent on memory before the shortage worsened. However, in recent weeks, “Google’s DeepSeek moment” appears to have forced memory stick hoarders to dump supply onto the market, pushing prices lower.

Tyler Durden

Fri, 04/10/2026 – 13:20

https://www.zerohedge.com/technology/pull-forward-demand-boosts-pc-shipments-amid-memory-crunch-woes

Watch: Ingraham Nukes Rino Rep. For Co-Sponsoring Mass Amnesty Bill For Illegal Aliens

Watch: Ingraham Nukes Rino Rep. For Co-Sponsoring Mass Amnesty Bill For Illegal Aliens

Authored by Steve Watson via modernity.news,

Fox News host Laura Ingraham dismantled Rep. Mike Lawler (R-NY) on live television for co-sponsoring the DIGNIDAD (Dignity) Act, a bipartisan bill critics slam as mass amnesty for illegal aliens.

The heated exchange, captured in viral clips, highlights growing frustration with RINOs undermining America First priorities a little over an year into President Trump’s second term.

Ingraham pressed Lawler relentlessly over claims that the legislation would bar criminals from eligibility. Lawler stated: “[An illegal alien] can’t have committed a crime [to be eligible for the Dignity Act].” Ingraham shot back: “That’s false! FALSE! FALSE! FALSE!… You can’t come on this show and say to my audience that you can’t have committed a crime to be eligible under the, ‘Dignity Act’ because there are several crimes that are, ‘nonviolent’ that do not qualify for inadmissibility.”

MUST WATCH: Rep. Mike Lawler (R-NY): “[An illegal alien] can’t have committed a crime [to be eligible for the Dignity Act].”

Fox News’ Laura Ingraham: “That’s false! FALSE! FALSE! FALSE!… You can’t come on this show and say to my audience that you can’t have committed a crime… pic.twitter.com/f43gsRZjkw

— RedWave Press (@RedWavePress) April 9, 2026

Ingraham added: “I can’t imagine Democrat immigration officers under a Democrat president in the future, was going to hold the strict we’re not going to let any criminals in.” On gang ties, she noted: “Gang member affiliation is given wide latitude.”

The confrontation escalated further when Ingraham challenged Lawler on specific offenses. “How about multiple DUIs?” she asked. Lawler replied: “That should be included [for deportation].” Ingraham fired back: “It’s not!… They can STAY under this legislation! Unfortunately.”

Fox News’ Laura Ingraham GOES AFTER Rep. Mike Lawler (R-NY) for co-sponsoring a bill that provides MASS AMNESTY for illegal aliens.

Laura Ingraham: “How about multiple DUIs?”

Mike Lawler: “That should be included [for deportation].”

Laura Ingraham: “It’s not!… They can… pic.twitter.com/27CJqTRFgu

— RedWave Press (@RedWavePress) April 9, 2026

She also ripped into Lawler’s use of tired clichés about illegal immigrants. “You got to stop using the cliches. This ‘in the shadows’… I don’t know what shadows are you looking at? But they’re not in the shadows. They’re working in restaurants… others are engaged in widespread fraud in California.”

Fox News’ Laura Ingraham SLAPS around RINO Rep. Mike Lawler (R-NY) for co-sponsoring a bill that would provide MASS AMNESTY for illegal aliens.

Laura Ingraham “You got to stop using the cliches. This ‘in the shadows’… I don’t know what shadows are you looking at? But they’re… pic.twitter.com/CUqUFLFs3E

— RedWave Press (@RedWavePress) April 9, 2026

Ingraham emphasized: “They’re NOT already given amnesty. Why do you come on television and say that? The president has been trying to REMOVE people from this country.”

She concluded pointedly: “It’s in the read legislation. Have you read the legislation?”

The DIGNIDAD Act (H.R. 4393), introduced last year by Reps. Maria Elvira Salazar (R-FL) and Veronica Escobar (D-TX) with Lawler as a co-sponsor, offers a pathway to legal status for certain long-term illegal aliens while claiming to include border security and E-Verify mandates.

Lawler has defended it as a “bipartisan” fix, but the Ingraham segment exposed what many see as dangerous loopholes that reward lawbreakers at the expense of American citizens.

This RINO push for amnesty comes despite crystal-clear public sentiment. As we reported previously, multiple polls confirm a majority of Americans back mass deportations of all illegals:

It also directly undercuts the Biden-era failure. The former president recently made the insane claim that he had reduced illegal immigration—despite record crossings that strained communities nationwide:

Americans voted decisively for enforcement, not more pathways that erode sovereignty. Yet here we have Republicans like Lawler doing the left’s bidding, co-sponsoring legislation that critics rightly label as amnesty in disguise.

Why import chaos when the mandate is clear: secure the border, remove those here illegally, and put Americans first?

The backlash on X has been swift and brutal, with users labeling Lawler a “garbage Republican” for enabling Democrats without them even needing to lift a finger.

This episode serves as a stark reminder: true immigration reform means enforcement first—no rewards, no loopholes, no excuses.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Fri, 04/10/2026 – 13:00

FCC Set To “Supercharge” Starlink Space Internet With “Seven-Fold More Capacity”

FCC Set To “Supercharge” Starlink Space Internet With “Seven-Fold More Capacity”

Federal Communications Commission Chairman Brendan Carr wrote on X that the agency will vote late this month on an order aimed at “supercharging” internet access by scrapping outdated power limits on satellite broadband, unlocking faster speeds, greater capacity, and more reliable service.

On April 30, the FCC will vote on “Modernizing Spectrum Sharing for Satellite Broadband,” which would “promote efficient spectrum sharing between geostationary and non-geostationary satellite systems” and, in the FCC’s own words, would “unlock more than $32 billion in economic benefits for the American people and up to seven-fold more capacity for space-based broadband services.”

NEWS: On April 30th, the FCC will vote to overhaul decades-old rules to “supercharge” satellite internet speeds for SpaceX’s @Starlink and Amazon’s LEO.

If approved, capacity increases of 100% to 700% using the same number of satellites could be possible, the FCC said.… pic.twitter.com/4asX90lSXw

— Sawyer Merritt (@SawyerMerritt) April 9, 2026

FCC explained more:

Drawing from the state-of-the-art in satellite technology, the FCC’s new technical rules would revise the decades-old framework for how Geostationary Orbit (GSO) and Non-Geostationary Orbit (NGSO) systems share spectrum. That 1990s-era framework predates the revolutionary changes in spectrum sharing technology that have been developed in the decades since.

The FCC’s new framework will enable faster speeds, lower costs, and greater reliability, representing another step to ensure that consumers benefit from competitive and affordable Internet options.

The move to modernize satellite internet is a big win for consumers, as it will hopefully increase upload and download speeds while lowering access costs.

Beyond consumers, the major winner is SpaceX’s Starlink internet company, which has more than 10 million customers worldwide, nearly 4 million of whom are in North America (the US, Canada, and Mexico, with the US making up the vast majority).

The FCC is moving fast to unleash affordable, high-speed Internet. By discarding last century’s satellite regulations, we could see billions of dollars in benefits for the American economy and broadband speeds many times faster than what is available today,” Carr wrote in a statement.

He continued, “This overdue rethinking of space spectrum sharing rules will bring greater competition to the broadband marketplace and reduce the number of satellites needed to serve a given area.”

Great timing on modernizing space internet ahead of the SpaceX IPO, which is currently in nonpublic review with the SEC and slated for a public market listing in June.

Remember when the Biden-Harris regime tried to modernize broadband by spending $42 billion and connecting zero people.

* * *

Save $300 on 3-month Emergency Food Reserve with Free Shipping – Ends Tonight!

Tyler Durden

Fri, 04/10/2026 – 12:40

Only Iran “Friendly” Ships Allowed Transit Through Strait, As Tankers Pile Up Near Hormuz, Waiting To Cross

Only Iran “Friendly” Ships Allowed Transit Through Strait, As Tankers Pile Up Near Hormuz, Waiting To Cross

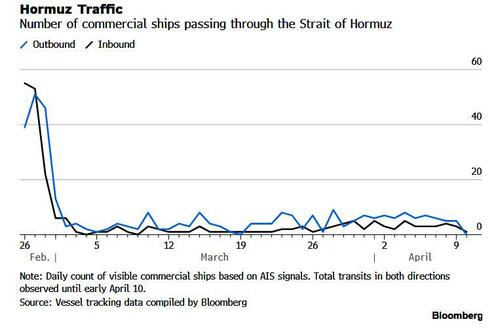

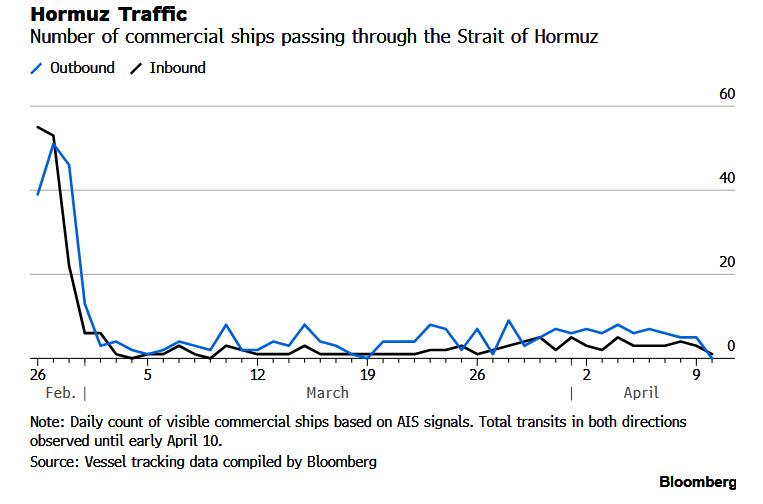

Shipping through the Strait of Hormuz remains largely limited, with transits over the past 24 hours consisting almost exclusively of ships “friendly” to Iran, including Chinese and Russian vessels. Meanwhile, those expecting the ceasefire to unblock Hormuz have actually seen the opposite: traffic through the strait, which ticked up at the weekend, has since slowed further.

Several fully-laden supertankers have moved toward the waterway in the past two days, but haven’t made the crossing out of the Persian Gulf, despite a US-Iran ceasefire taking effect this week.

Unless anything changes, this weekend’s ceasefire negotiations will be very short: the US has said the truce is conditional on Iran unblocking Hormuz. Yet since Thursday morning, just nine ships out of the roughly 800 vessels trapped in the Persian Gulf, have been observed passing through the strait, with five heading out of the gulf and four going in the opposite direction.

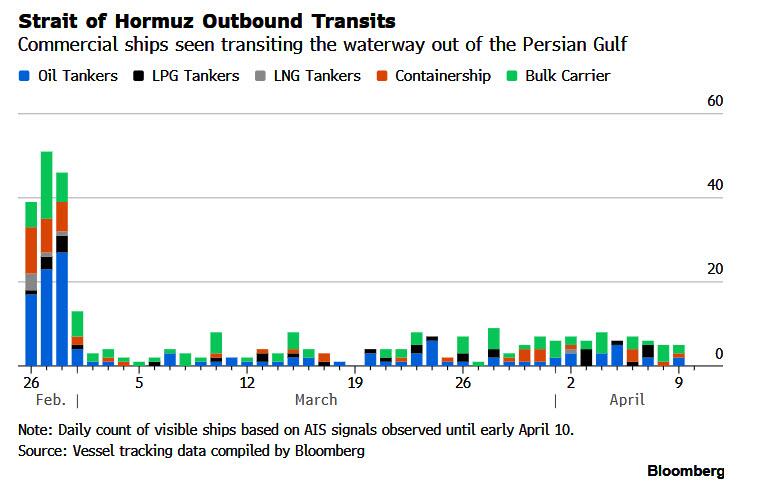

Among the most important was the Suezmax oil tanker Tour 2, hauling about 1 million barrels of Iranian crude out of the waterway. The Russian flagged supertanker Arhimeda moved in the opposite direction toward Iran’s export terminal at Kharg Island.

In a sign of some modest optimism, several oil tankers inside the Persian Gulf are anchoring near the approach to the strait, likely in order to be among the first to get underway as soon as the waterway opens up. Yet even as the ceasefire has pushed shipowners to begin considering options, most say conditions are still too unclear to attempt an exit.

Two Japanese oil tankers – itching with anticipation to get the hell out – left the waters off Saudi Arabia’s Ras Tanura on Thursday to move closer to the strait. The Mayasan and Yakumosan, both very-large carriers each hauling around 2 million barrels of crude, began sailing east late Thursday from waters off Ras Tanura in Saudi Arabia, where they have been since mid-March. The Sea Condor, a Greek-flagged products tanker that loaded in Kuwait, was also moving east in the direction of Hormuz.

Mayasan sailed into the gulf a few days before war broke out on Feb. 28, ship-tracking data show. It picked up crude from the United Arab Emirates and Saudi Arabia in late February. It is indicating Tomakomai, a port in northern Japan, as its destination. Yakumosan entered the gulf in late February, and picked up a cargo of Qatari crude from a floating storage vessel in early March. It then soon took another load from Saudi Arabia’s Juaymah, before idling for a few weeks off Ras Tanura. It is signaling a mustering point off Das Island in the United Arab Emirates as its destination.

The Japanese ships sailing east on Friday have links to Mitsui OSK Lines Ltd., a major Japanese shipowner and key energy player. While the company extracted at least one vessel from the gulf before this week’s truce, President Jotaro Tamura said on Thursday the group would now need to scrutinize details and the implementation of the ceasefire before allowing its tankers to test the Strait of Hormuz.

Mitsui owns Mayasan, while Yakumosan’s owner Phoenix Ocean Corp. shares MOL’s address. MOL said it could not comment on “the navigation status or operational measures of individual vessels,” adding its priority was the safety of seafarers, cargo, and vessels.

The Japanese tankers follow a similar move by three fully-laden Chinese ships. On Thursday, the three Chinese VLCCs clustered at a spot approaching Iran’s Qeshm, the island that now serves as a gateway for Hormuz transits. Two of the ships are linked to China’s Cosco Shipping Corp., a giant and prudent state-owned player.

The Cospearl Lake, a very-large crude carrier linked to China’s state-owned Cosco Shipping Corp., and He Rong Hai, owned by a smaller entity, appeared to be traveling east early on Thursday morning at near-top speeds, according to ship-tracking data, before coming to a virtual halt. Another Cosco-linked VLCC, the Yuan Hua Hu, began its eastward journey a few hours later. All three are signaling Chinese ownership on their tracking systems, a move typically done for safety during Iran-approved transits (and in this case they aren’t lying).

The Chinese ships are already notable for their cargoes. Two are carrying Iraqi crude, and the other Saudi. While Iran has referred to “brotherly” Iraq, most other transits have been granted to friendly nations. Iraq has told traders and refiners that vessels carrying the country’s oil are now able to transit the Strait of Hormuz thanks to an Iranian exemption.

Cospearl Lake’s and Yuan Hua Hu’s passages would also mark the first such attempt by a Cosco oil tanker in the six-week war. The company, like other large shipping firms, tends to be conservative, and its crude carriers have been trapped since US and Israeli strikes on Iran began, prompting Iran to all but close Hormuz in retaliation

Sea Condor, the Greek-flagged ship, also moved into the gulf at around the same time and picked up Kuwaiti fuels in early March. Its owner is Turandot Marine Co. which shares the same contact details as its manager, Pantheon Tankers Management, in Athens.

The tankers are part of a growing armada amassing at the entrance to the strait, off the United Arab Emirates. A Saudi Arabian-flagged VLCC, the Jaham, has moved east toward a nearby holding area off Dubai. They join other ships including two Indian-flagged, fully-laden supertankers that have been in the area since late March – the Desh Vibhor, which is off Ras Al Khaimah, and the Desh Vaibhav, which is near Dubai.

Shipowners are not only concerned about the safety of crew and cargo, but also about the need to manage Iranian demands to secure safe passage, including payments which could expose companies to sanctions risks. Trump, who announced a complete opening of Hormuz along with the ceasefire earlier this week, said on Thursday he was optimistic, only to then chastise Iran for doing a “very poor” job of allowing oil through.

Meanwhile, all transits observed in the past day passed through a narrow northern corridor of the Strait between the Iranian islands of Larak and Qeshm, which is the only passage permitted by Iran’s military.

Observed Transits

According to Bloomberg, since Thursday morning, two Iran-linked oil tankers, two bulkers and a single container ship have been observed leaving the Persian Gulf. The Greek oil tanker Serengeti, which appeared on automated tracking systems off Sri Lanka on Thursday, is estimated to have made the outbound crossing on April 1.

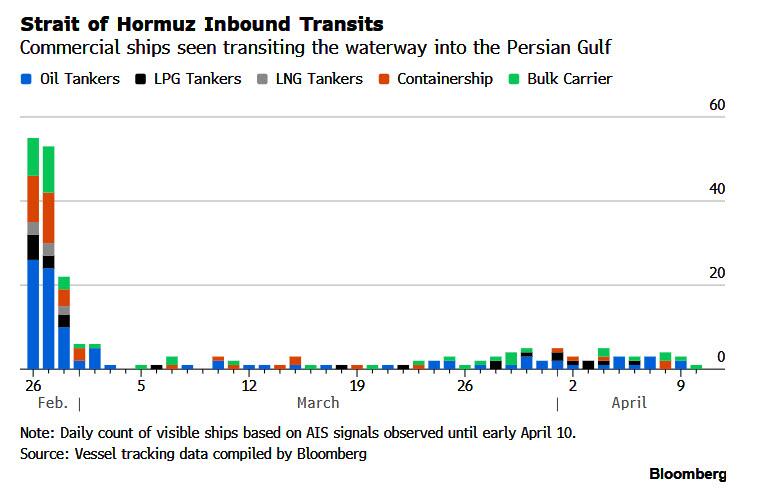

From the other side, two tankers sanctioned by the US for their involvement in the Iranian oil trade – one of which was the Arhimeda – were observed entering the Gulf on Thursday. A small bulk carrier also made the inbound transit. On Friday morning, the only vessel seen heading into the Persian Gulf was a Chinese-linked bulk carrier.

Tyler Durden

Fri, 04/10/2026 – 12:00

Think “Weekends” Rather Than “Weeks”

Think “Weekends” Rather Than “Weeks”

By Elwin de Groot, head of macro strategy

As another volatile week comes to an end, investors and market participants appear to be clinging to the hope that the two‑week ceasefire between the United States and Iran, which began on Wednesday, will not unravel entirely – at least until a direct, face‑to‑face exchange and clarification of key demands can take place during the planned talks in Islamabad this weekend. Near‑dated Brent crude edged up by $2 to $97, equity markets posted modest declines in Europe, whilst US stocks rose. European bond yields rose by 3–5 basis points, as UST yields dropped a few. This suggests that the powerful risk‑on move seen on Wednesday has been dented but not broken. Experts continue to stress the fragility of the ceasefire, but markets are showing slightly greater confidence than the underlying geopolitical reality might warrant.

Compared with the first day of the ceasefire – which saw Israel launch its largest‑ever strike on Hezbollah, the UAE carry out a large‑scale operation against Iran’s oil and petrochemical assets in the Gulf, and Iran respond with ballistic missile and drone attacks – yesterday’s developments were notably more contained. There were no confirmed direct US‑Iran strikes. That said, Hezbollah did fire rockets into northern Israel, and Iran formally accused the United States of violating the ceasefire due to Israel’s continued strikes in Lebanon. Kuwait also accused Iran and its proxies of launching drone attacks.

Crucially, shipping through the Strait of Hormuz remains severely disrupted, with only a handful of Iran‑linked and/or Chinese vessels transiting the waterway. Iran indicated that it would allow no more than 15 ships per day to pass under the ceasefire agreement – hardly meaningful given that an estimated 800-900 vessels are still waiting to exit the strait. More fundamentally, the move underscores Iran’s effective control over the waterway, a message reinforced by the publication of “two safe shipping routes” by Iran’s Ports and Maritime Organization.

As reported earlier this week, shipowners are still grappling with whether – and under what conditions – it is safe to transit the Strait of Hormuz. Insurance is only part of the equation; the security of crews is equally critical. This raises the risk that even once ships can leave the strait to deliver cargoes to Asia and Europe, owners may remain reluctant to re‑enter the area to load new shipments. This reinforces our view that even if the war were to end – a point that remains far from certain – normalisation would not be immediate. A temporary ceasefire, clearly, is not a sufficient condition for a return to business as usual.

On that note, German Chancellor Merz has told President Trump that Germany would back a mission to secure the Strait, but that such an operation would ideally be conducted under a mandate from the UN Security Council. We’ll have to see if the US administration sees any merit in this, as it would imply Russia and China will get a clear say in the matter as well.

Following his meeting with NATO Chef Rutte – which only further exposed the rift in the alliance – Trump has demanded that countries provide concrete, operational support to US military actions – specifically through access to bases, airspace, logistics, and naval participation – rather than limiting themselves to political backing or neutrality. Trump did not issue a formal ultimatum in the meeting, but officials and media reports suggest the administration is considering concrete penalties for uncooperative allies, including redeploying or withdrawing US troops from certain NATO countries, or – more extreme – reassessing US commitments to the alliance as a whole.

Tyler Durden

Fri, 04/10/2026 – 11:40

https://www.zerohedge.com/markets/think-weekends-rather-weeks

Speculation Surges That Pakistan Talks Are A Delay Tactic Ahead Of Expanded US Action On Iran

Speculation Surges That Pakistan Talks Are A Delay Tactic Ahead Of Expanded US Action On Iran

President Trump has made clear that American forces will still be “hanging around” the Persian Gulf area with an eye on Iran, while demanding that the Strait of Hormuz be opened to global energy transit once again.

Trump has vowed to keep troops positioned for a fight “until such time as the REAL AGREEMENT reached is fully complied with.” As direct US-Iran talks are set for Islamabad Saturday morning, there’s been an avalanche of speculation that the ceasefire could be ‘cover’ for a greater Pentagon force build-up and bigger impending operation.

Some pundits say that Washington needed more time to get large contingencies of Marines and Airborne units in place, possibly for some kind of risky island campaign towards reopening the strait.

This could be the case, as it’s also very evident to all that the demands of each side remain far apart, which means the chances for a breakthrough deal which finally ends the war are distant.

With a two week timeline in place to reach a deal, is this interim period merely for rearming and regrouping of forces on each side?

Clearly, the US wasn’t prepared for the fierce, sustained Iranian counter-attack on American regional bases and Gulf allies.

Open-source data of military logistics flights between the US, Europe, and the Mideast region suggests there is indeed an ongoing build-up and posturing of forces happening on the eve of the Pakistan summit.

Still, it’s clear that Trump needs an offramp, or else face the kind of endless military quagmire which would likely inevitably lead to the GOP getting decimated in next fall’s midterm Congressional elections.

Case in point: More than 70 transport planes landed in the Middle East within 24 hours of the ceasefire taking effect. That scale suggests possible preparation for a ground offensive, solidifying suspicion that Trump is using the truce to regroup: https://t.co/MHlFQjz1Tk pic.twitter.com/S3DzRMgOo2

— Bashkarma🇺🇸🌏🇷🇺 (@Karmabash) April 9, 2026

A bigger longer war, or ground conflict, would also damage the chances of a future Vance presidency.

As for Vance, the Associated Press writes, “But the arrival of Vance for negotiations marks a rare moment of high-level U.S. government engagement with the Iranian government. Since the Islamic Revolution in 1979, the most direct contact had been when President Barack Obama in September 2013 called newly elected Iranian President Hassan Rouhani to discuss Iran’s nuclear program.”

Strait of Hormuz traffic returns to normal by end of April?

Yes 19% · No 82%

View full market & trade on Polymarket

A Pentagon build-up in the region might also be Trump’s way of signaling powerful leverage for more potential major attacks on Iran to come, in order to gain more from negotiations. As yet, Iran holds the key economic leverage given its de fact Hormuz control.

Tyler Durden

Fri, 04/10/2026 – 11:20

Musk’s xAI Sues Colorado Over AI Law, Saying It Forces Developers To Back State’s Views

Musk’s xAI Sues Colorado Over AI Law, Saying It Forces Developers To Back State’s Views

Authored by Tom Gantert via The Epoch Times (emphasis ours),

Elon Musk’s artificial intelligence company, xAI, filed a lawsuit on April 9 over a Colorado law it claims makes AI developers endorse “Colorado’s views on diversity, equity, and inclusion or face significant compliance costs and civil fines.”

The chatbot Grok is the flagship product of xAI. Oleksii Pydsosonnii/The Epoch Times

The company, whose flagship product is the chatbot Grok, named Colorado Attorney General Philip Weiser as the defendant. The lawsuit states that the law’s provisions “prohibit developers of AI systems from producing speech that the State of Colorado dislikes, while compelling them to conform their speech to a State-enforced orthodoxy on controversial topics of great public concern.” The lawsuit says the Colorado law violates the First Amendment.

Weiser didn’t respond to an email seeking comment.

The lawsuit questions the use of the term “algorithmic discrimination” in the law, calling it vague.

The text of the law defines it this way: “Algorithmic discrimination means any condition in which the use of an artificial intelligence system results in unlawful differential treatment or impact that disfavors an individual or group of individuals on the basis of their actual or perceived age, color, disability, ethnicity, genetic information, limited proficiency in the English language, national origin, race, religion, reproductive health, sex, veteran status, or other classification protected under the laws of this state or federal law.”

The bill, SB24-205, was introduced in April 2024, passed the next month, and will take effect on June 30, 2026.

Colorado Senate Democrats said during debate that “algorithmic discrimination has been shown to make biased determinations in cases involving hiring practices, housing applications, financial services, and health care coverage.”

“AI systems are evolving faster than we can write and pass policy on them—which is why we need to act now,” Sen. Robert Rodriguez, a Democrat whose district spans southern Denver, said in a statement. “Many systems’ algorithms have biases baked in and can easily result in discriminatory outcomes when it comes to housing applications, hiring practices, and more.”

xAI said in its lawsuit that Grok is not biased.

“xAI has designed and developed Grok to answer to only evidence and reason, without regard to political correctness, ideological biases, or anything that might distort objective truth,” the lawsuit said.

“This unwavering commitment ensures that Grok discharges its fundamental mission—assisting humanity in understanding the universe. But the State of Colorado now seeks to force xAI to abandon its disinterested pursuit of truth and instead promote the State’s ideological views on various matters, racial justice in particular.

“It is instead an effort to embed the State’s preferred views into the very fabric of AI systems. Its provisions prohibit developers of AI systems from producing speech that the State of Colorado dislikes, while compelling them to conform their speech to a State-enforced orthodoxy on controversial topics of great public concern.”

Tyler Durden

Fri, 04/10/2026 – 11:05

Trump Touts Palantir In Post, Appearing To Counter Bears

Trump Touts Palantir In Post, Appearing To Counter Bears

U.S. software shares continued to slide on Friday, with the iShares Expanded Tech-Software Sector ETF (IGV) down 2.4%, as fears over AI-driven disruptions returned following a recent update from Anthropic.

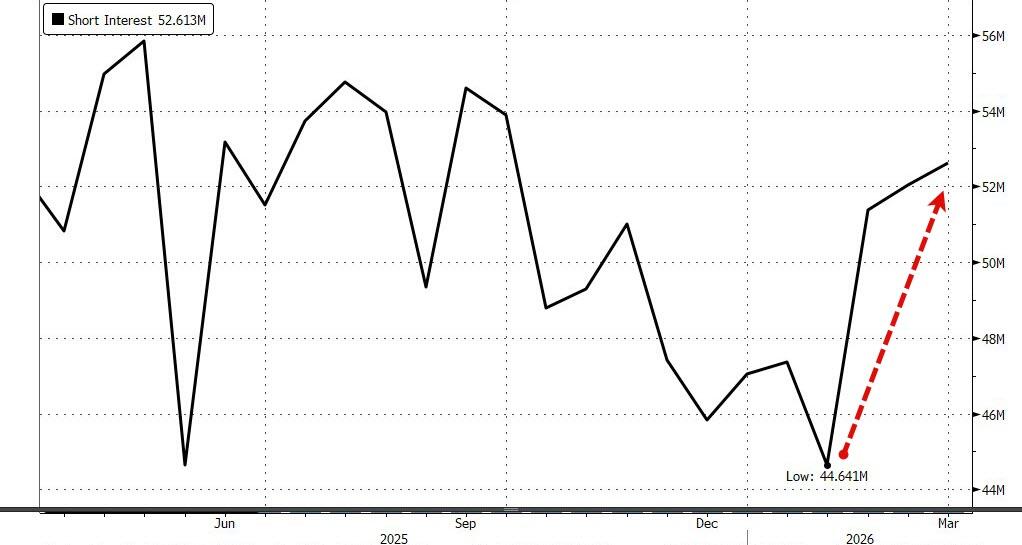

In focus is software company Palantir, which has fallen from grace and is down 40% since peaking last November.

Palantir has been in the crosshairs of “Big Short” investor Michael Burry, who claimed that AI startup Anthropic is effectively “eating Palantir’s lunch.”

Burry, the founder of Scion Asset Management, has since deleted the post, which was published on X on Thursday.

Short Interest has risen significantly in recent weeks..

Countering the Palantir bears this morning was none other than President Trump, who wrote in a Truth Social post:

“Palantir Technologies (PLTR) has proven to have great war fighting capabilities and equipment. Just ask our enemies!!! President DJT.”

PLTR shares immediately surged after the president’s comments, with the stock bottoming around $123 before moving higher to about $127. Shares are still down around 2% on the session…

Burry continued in the deleted post: “PLTR can have government, which is low margin and small,” adding that while Anthropic is scaling at lightning speed, “it took $PLTR 20 years to get to $5 Billion.”

Tyler Durden

Fri, 04/10/2026 – 11:00

https://www.zerohedge.com/markets/trump-touts-palantir-post-appearing-counter-bears

Trump Rebukes Carlson, Kelly, Owens, & Jones Over Iran Comments

Trump Rebukes Carlson, Kelly, Owens, & Jones Over Iran Comments

Authored by Luis Cornelio via HeadlineUSA,

President Donald Trump minced no words in a lengthy and fiery rebuke of podcast hosts Tucker Carlson, Megyn Kelly, Candace Owens and Alex Jones amid their criticisms over the U.S.’s military operations in Iran.

“They’re stupid people, they know it, their families know it, and everyone else knows it, too! Look at their past, look at their record. They don’t have what it takes, and they never did!” Trump wrote on Truth Social.

His comments come as part of a 482-word takedown that directly accuses Carlson, Kelly, Owens and Jones of seemingly stirring controversy for views engagement.

“They’ve all been thrown off Television, lost their Shows, and aren’t even invited on TV because nobody cares about them, they’re NUT JOBS, TROUBLEMAKERS, and will say anything necessary for some ‘free’ and cheap publicity,” Trump added.

— Rapid Response 47 (@RapidResponse47) April 9, 2026

His comments follow some of these hosts taking issue with Trump’s warning to Iran that a “whole civilization will die tonight” over Easter weekend if the Islamic regime did not reopen the Strait of Hormuz.

“Now it’s time to say no, absolutely not, and say it directly to the president, no,” Carlson said, for instance.

Trump targeted each individual with personalized criticism, saying that Carlson “couldn’t even finish college” and was a “broken man when he got fired from Fox.”

Trump also targeted Kelly, saying she “nastily asked me the now famous ‘Only Rosie O’Donnell,’” and then slammed Owens as “‘crazy.”

Trump also referenced the past controversy surrounding Owens’ dubious claims that French First Lady Brigitte Macron is transgender.

“Actually, to me, the First Lady of France is a far more beautiful woman than Candace, in fact, it’s not even close!” Trump continued.

Trump also criticized Jones, calling him “Bankrupt Alex Jones” and saying he “says some of the dumbest things, and lost his entire fortune, as he should have, for his horrendous attack on the families of the Sandy Hook shooting victims, ridiculously claiming it was a hoax.”

“These so-called ‘pundits’ are LOSERS, and they will always be!” Trump said.

* * *

Save $300 on 3-month Emergency Food Reserve with Free Shipping – Ends Tonight!

Tyler Durden

Fri, 04/10/2026 – 10:20

https://www.zerohedge.com/political/trump-rebukes-carlson-kelly-owens-and-jones-over-iran-comments

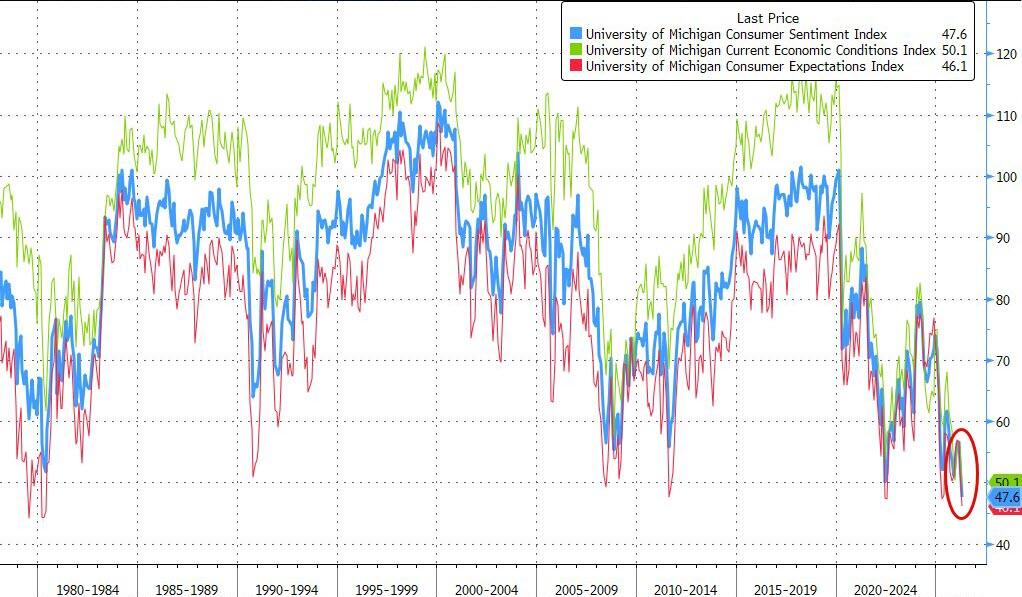

UMich Sentiment Crashes To Lowest On Record As War Sparks Inflation Panic Among Democrats

UMich Sentiment Crashes To Lowest On Record As War Sparks Inflation Panic Among Democrats

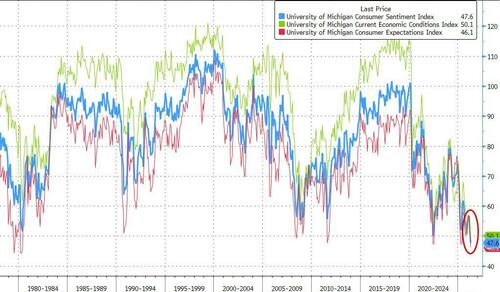

While the March UMich sentiment survey was completed before and after the start of the Iran War (with only modest impacts on sentiment and inflation expectations), today’s preliminary April data survey period was all in the war with expectations for a notable drop in sentiment and sizable jump in inflation expectations.

It turns out the expectations were right in direction but underestimated the scale as headline sentiment plunged from 53.3 to 47.6 (far worse than the 51.5 exp) with Current Conditions (50.1 vs 53.4 exp vs 55.8 prior) and Expectations (46.1 vs 50.2 exp vs 51.7 prior)…

Source: Bloomberg

That is a record low for the headline sentiment and Current Conditions and lowest print for Expectations since 1980.

Demographic groups across age, income, and political party all posted setbacks in sentiment, as did every component of the index, reflecting the widespread nature of this month’s fall.

One-year expected business conditions plunged about 20% and is now 6% below last April.

Assessments of personal finances declined about 11%, with consumers expressing a substantial increase in concerns over high prices and weaker asset values.

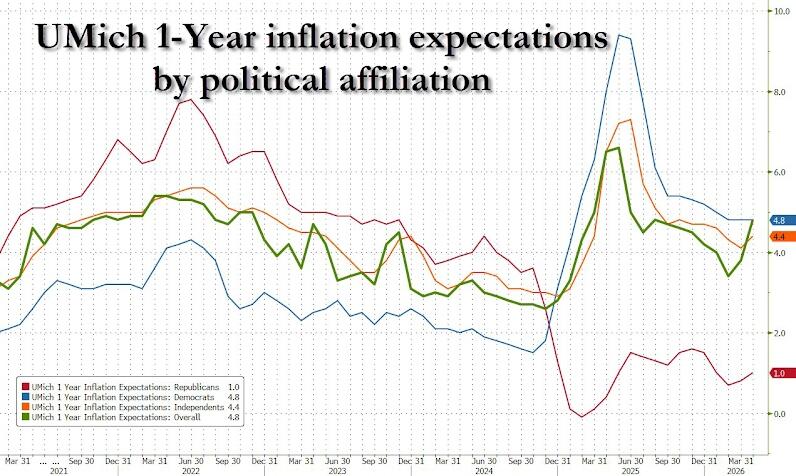

Year-ahead inflation expectations surged from 3.8% in March to 4.8% this month, the largest one-month increase since April 2025, but longer-term expectations rose only modestly…

Of course, it’s Democrats that are ‘panicans’ once again at inflation (Dems +4.8%, Reps +1.0%)…

One thing of note in that chart – how is the overall inflation expectation screaming higher (to equal Democrats’ view) with the actual breakdown by political cohort showing no huge rise?

Finally, on the potential bright side, UMich Surveys of Consumers Director Joanne Hsu notes that “98% of interviews were completed prior to the April 7th announcement of a temporary cease-fire. Economic expectations will likely improve after consumers gain confidence that the supply disruptions stemming from the Iran conflict have ended and gas prices have moderated.“

Tyler Durden

Fri, 04/10/2026 – 10:12

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}