Category: News

Turquía investiga caída de dron tras derribar otro días antes

ANKARA (AP) — Turquía está investigando la caída de un dron en el noroeste del país, informaron medios locales el viernes, solo días después de derribar otro que ingresó en su espacio aéreo desde el Mar Negro.

Residentes en la provincia de Kocaeli descubrieron el dron dañado en un campo, lo que provocó una investigación oficial sobre los restos, informaron medios de prensa locales, entre ellos el canal de noticias NTV.

Una evaluación inicial indica que la aeronave podría ser un dron de reconocimiento Orlan-10 de fabricación rusa, declaró el Ministerio del Interior en un comunicado, añadiendo que la investigación estaba en curso.

El lunes, aviones de combate F-16 turcos interceptaron lo que los funcionarios describieron como un dron “fuera de control” después de que violara el espacio aéreo del país.

El ministerio de defensa declaró que ese dron fue destruido en un lugar seguro para proteger a los civiles y el tráfico aéreo. Posteriormente, el gobierno de Turquía advirtió tanto a Rusia como a Ucrania que ejercieran mayor precaución sobre la seguridad en el Mar Negro.

Ese derribo se produjo después de una serie de ataques ucranianos a petroleros de la “flota clandestina” rusa frente a la costa turca, lo que generó preocupaciones en Turquía sobre el riesgo de que la guerra en Ucrania se extienda a la región.

El Ministerio de Defensa indicó que el dron que fue derribado el lunes probablemente se rompió en pequeños fragmentos que se dispersaron en un área amplia, lo que complica los esfuerzos para identificarlo. Los esfuerzos de búsqueda y análisis técnico aún estaban en curso, afirmó.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

UMich Survey Sees ‘Current Conditions’ In America As The Worst In 47 Years

UMich Survey Sees ‘Current Conditions’ In America As The Worst In 47 Years

The final print for UMich’s sentiment survey for December was a doozy…

While the headline sentiment gauge and Expectations ticked up, Current Conditions slipped further…

…to an all-time record low… yes… worse than during Oct 1987’s crash, 9/11, the GFC, and COVID…

This – as you might guess – is very unusual with stocks at record highs and as we have labored extensively this year, UMich’s survey seems rife with bias

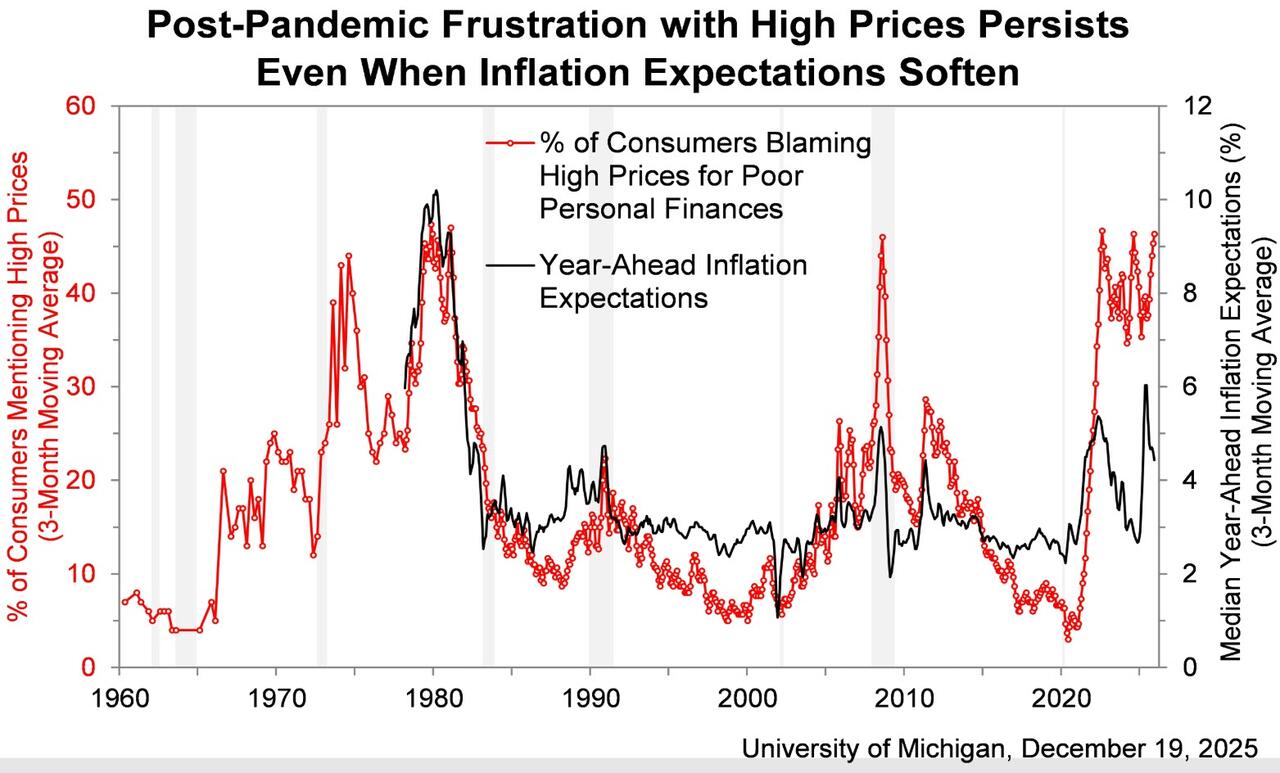

UMich claims that post-pandemic frustration with high prices persists…

Which is incredible since inflation expectations are plunging…

As Democrats realize their TDS-driven hyperinflation fears were utter bullshit after all (shame on all those MSM pundits)…

Buying conditions for durable goods fell for the fifth straight month, whereas expectations for personal finances and business conditions rose.

“Despite some signs of improvement to close out the year, sentiment remains nearly 30% below December 2024, as pocketbook issues continue to dominate consumer views of the economy,” Joanne Hsu, director of the survey, said in a statement.

Labor market expectations lifted a bit this month, though a solid majority of 63% of consumers still expects unemployment to continue rising during the next year.

Hsu concludes: “This year, we saw a spike in inflation expectations that softened very quickly, while high-price mentions have remained consistently high. It appears that consumers have yet to internalize the post-pandemic level of prices as a new normal, which influences how they view the economy.“

Tyler Durden

Fri, 12/19/2025 – 10:26

https://www.zerohedge.com/markets/umich-survey-sees-current-conditions-america-worst-47-years

El aspirante al Oscar “O Agente Secreto” aprovecha el auge del cine brasileño

Por GABRIELA SÁ PESSOA

SAO PAULO (AP) — “O Agente Secreto” (“El agente secreto”) una película brasileña preseleccionada para los Oscar, trata sobre personas comunes. Sigue a un científico modesto y padre viudo que se convierte en objetivo de la dictadura militar de Brasil en los años 1970, no porque sea un activista o revolucionario, sino porque se enfrenta a un empresario con vínculos con el régimen.

“Está en peligro simplemente por ser quien es, por mantener los valores que tiene”, afirmó su astro Wagner Moura en una entrevista reciente con The Associated Press. “Así es como funciona el autoritarismo en todas partes”.

Dirigida por Kleber Mendonça Filho, “O Agente Secreto” ha sido aclamada por los críticos como una de las mejores películas del año y llega en medio de un renovado interés internacional por el cine brasileño. Tendrá su estreno comercial en Estados Unidos el viernes y cuenta con importantes victorias en el Festival de Cine de Cannes tanto para Mendonça Filho (mejor director) como para Moura (mejor actor).

A principios de este mes, el thriller de dos horas y media obtuvo nominaciones al Globo de Oro por mejor drama, mejor película no inglesa y mejor actor en un drama. Y actualmente está en la lista de cintas preseleccionadas en la categoría de mejor película internacional para los Premios de la Academia.

Identidad y memoria

“O Agente Secreto” llega en un momento fuerte para el cine brasileño tras el éxito de : (“Ainda estou aqui” (“Aún estoy aquí”), que ganó el Oscar de este año a la mejor película internacional y un Globo de Oro para la actriz principal Fernanda Torres.

En Brasil, las expectativas para “O Agente Secreto” son altas. Moura dijo que el entusiasmo generalizado en torno a la película, y el compromiso del público con los artistas brasileños, lo ha hecho “increíblemente feliz”.

“Ningún país se desarrolla sin cultura, sin identidad”, expresó. “Estás viendo una película brasileña, viendo una parte de Brasil y su historia. Eso importa”.

Ambientada en 1977, en el apogeo de la dictadura de Brasil, “El Agente Secreto” comienza con un montaje en blanco y negro de los símbolos nacionales de la época, desde clásicos del cine hasta telenovelas exitosas.

Mendonça Filho ancla la historia en un tiempo y lugar precisos: el Carnaval en Recife, la ciudad natal del cineasta en el noreste de Brasil. Como el centro de su universo cinematográfico, la ciudad es el escenario para confrontar a un país que aún lucha por reconciliarse con su pasado.

“Hemos consumido cosas increíbles de tantos lugares, desde Akira Kurosawa en Japón hasta Elvis Presley en el sur de Estados Unidos”, dijo Mendonça Filho. “Soy brasileño, y mi película es brasileña. Si es buena, será universal.”

Una historia en tiempo real

Al vivir encubierto y bajo el alias Marcelo, Armando pasa sus días buscando en archivos pistas sobre el pasado de su madre y planeando huir del país con su hijo pequeño. A medida que se desarrolla su búsqueda, las calles explotan con la algarabía del Carnaval, una celebración tan arraigada en la vida brasileña que incluso el jefe de policía aparece desaliñado con confeti aún pegado en su cabello.

Mendonça Filho mezcla el suspense político con leyendas urbanas de la época, tocando temas que van más allá de la dictadura misma, incluyendo corrupción, violencia estatal y complicidad institucional.

Una secuencia crucial se desarrolla dentro de un cine, un guiño a la cinefilia de toda la vida del director. Mientras las audiencias ficticias salen de las proyecciones de “Jaws” (“Tiburón”) y “The Omen” (“La profecía”), sacudidas por amenazas ficticias, el país mismo vive bajo un terror real.

En la última década, el cine brasileño ha revisitado cada vez más la dictadura militar, que gobernó de 1964 a 1985. Junto a “O Agente Secreto” y “Ainda estou aqui”, los cineastas han regresado al período en obras como “Marighella”, dirigida por Moura, sobre el legendario líder guerrillero que tomó las armas contra el régimen.

Muchas de estas películas se hicieron o estrenaron en la última década, en medio del ascenso de la extrema derecha en Brasil. Su figura más prominente fue el expresidente Jair Bolsonaro, un capitán del ejército retirado que elogió a los oficiales acusados de tortura y minimizó los crímenes de estado cometidos durante la dictadura.

Mendonça Filho es uno de los cineastas que han asumido la tarea de confrontar la memoria nacional.

“La dictadura es un trauma que nunca se examinó verdaderamente”, dijo. “No puedes simplemente decir, ‘Sigue adelante, olvídalo’. Se forma una costra sobre ello. Lo mismo le pasa a toda una nación.”

Cuando “O Agente Secreto” se estrenó en cines brasileños el 6 de noviembre, la historia se estaba desarrollando en tiempo real.

Ese mismo mes, Bolsonaro fue arrestado y comenzó a cumplir una sentencia de prisión de 27 años por intentar anular las elecciones de 2022 después de perder ante el presidente Luiz Inácio Lula da Silva. Por primera vez, también se encarceló a oficiales militares de alto rango por su papel en el intento de golpe.

“Hoy, soy mucho más optimista sobre Brasil como democracia”, dijo Mendonça Filho. “Por primera vez, estamos responsabilizando a los oficiales militares y enviando a prisión a un presidente que no hizo más que dañar al país.”

Una mujer extraordinaria y ordinaria

Pocas historias en “O Agente Secreto” son tan impactantes como la de Tânia Maria, de 78 años, quien interpreta a Dona Sebastiana.

Una artesana brasileña, Maria vivió una vida ordinaria hasta los 72 años, cuando fue elegida como extra en la película de 2019 de Mendonça Filho, “Bacurau”. Desde entonces, ha actuado en seis películas que aún no se han estrenado.

El director dijo que nunca olvidó su presencia: “una postura de ave, una voz moldeada por 60 años de cigarrillos y un sentido del humor afilado como una navaja”. Más tarde escribió el papel de Dona Sebastiana específicamente para ella.

El personaje, que alberga a fugitivos políticos, incluido Armando, se destaca. Cuando camina hacia la cámara con un vestido floreado, cigarrillo en mano, la película brevemente le pertenece a ella.

“Su autenticidad lleva algo de muchas mujeres que he conocido”, dijo Mendonça Filho. “Hay algo literario en ella”.

Moura dijo que no pudo ocultar su asombro ante la autenticidad de la actriz. Señaló su primera escena juntos, en la que Dona Sebastiana muestra a Armando el apartamento en el que se está mudando.

Si los espectadores observan de cerca, dijo, verán que él está genuinamente “como un tonto orbitando a su alrededor.”

Maria vive en un pueblo rural de unas 22.000 personas en el noreste de Rio Grande do Norte. No hay cine allí. Dice que las únicas películas que ha visto son aquellas en las que actuó.

Para Maria, la autenticidad de su interpretación comienza con el guion de Mendonça Filho.

“Filmar es maravilloso, y las películas de Kleber Mendonça se sienten como si estuvieran copiando nuestras vidas”, dijo, riendo. “La vida de Dona Sebastiana es mi vida. Siempre me ha gustado acoger a la gente, y siempre me ha gustado quejarme.”

Desde el estreno de la película en Brasil, la costurera convertida en actriz se ha convertido en una sensación nacional, apareciendo en programas matutinos y ganando miles de seguidores.

También espera un reconocimiento en los Oscar, tanto para la película como, quizás, para ella misma.

“Quiero ir a los Oscar”, dijo. “Y quiero hacer mi propio vestido. Será rojo, muy brillante.”

___

Sigue la cobertura de AP sobre América Latina y el Caribe en https://apnews.com/hub/latin-america

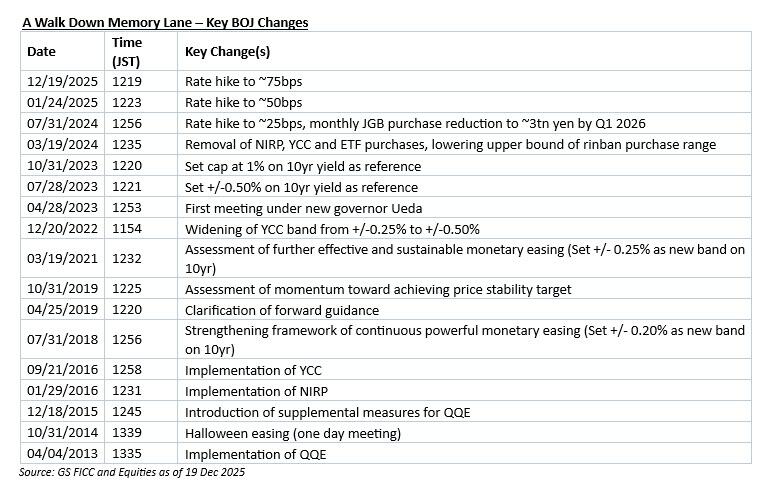

Loss Of Credibility: Yen Craters, Yields Surge After BOJ Hikes Rates To Highest Since 1999

Loss Of Credibility: Yen Craters, Yields Surge After BOJ Hikes Rates To Highest Since 1999

In the last central bank decision of 2025, the BOJ lifted its key rate to 0.75% from 0.50% in a widely anticipated and telegraphed move, taking borrowing costs to their highest level in three decades. It wasn’t enough, however, and after an initial kneejerk move, the yen plunged while yields soared as the market concluded that what Ueda did was too little, too late, and the hike was too vague to press the hawkish case.

As such, the market doves are back in control, and forcing the BOJ to either double down and puts Japan’s money where its mouth is, or lose control of either the currency or the bond market, or eventually, both.

In a recap of what the BOJ did, Bloomberg writes the following:

Ueda said risks tied to the impact of US tariffs appear to be easing and pointed to solid wage growth momentum next year year, a condition for more sustained inflation.

Both the BOJ statement and Ueda’s remarks implied there’s room to raise rates further, while offering assurance that conditions would remain accommodative. That reinforces expectations of a gradual and data-dependent tightening path.

Ueda also said the policy rate remains some distance from the lower-end of a neutral range and added he would like to recalculate that if the opportunity arises, signaling openness to further tightening but also a desire for greater confidence in the framework before moving more decisively.

As BBG notes, by lifting the policy rate to a three-decade high of 0.75% on Friday, Ueda continued his historic march toward restoring normality to Japan’s monetary policy and the economy after decades of unconventional steps and underperformance. The only problem: Japan will never survive in a world where monetary policy is even remotely “normal ” and as a result, government bond yields immediately climbed to the highest levels since the 1990s, an indication that the BOJ policy space is now narrower than ever.

And indeed, Bloomberg admits that while Ueda had telegraphed Friday’s move ahead of time, he didn’t offer similar clarity about what comes next, and that’s left yen bears chomping on the currency instead of backing away. The yen slid more than 1% against the dollar, to around 157.40, in the hours after Ueda’s press conference.

“Listening to what he said, I honestly couldn’t tell at all when the next rate hike might be,” said Teppei Ino, Tokyo head of global markets research at MUFG Bank. “He didn’t really say anything about the neutral rate — there was simply no guidance at all.”

Addressing the hawkish side, Goldman’s Kai Wen Lim writes that the statement removed language that growth and inflation will stagnate due to tariffs, coupled with hawkish voices on the board and a clear acknowledgement that real rates are still low, all leaned on the more hawkish side despite a lack of new details. The reaffirmation bolstered bearish sentiment causing futures to sell off ~4bps while BOJ pricing also inched higher across the curve from March onwards, with June and July seeing the most traction implying market expectation of the next hike being ~6 months away.

On the other hand, classic “buy the rumor, sell the fact” phenomenon was observed in USDJPY, with the pair initially weakening a touch on initial headlines before surging and swiftly breaking past the 156 handle (and then 157) with investors likely thinking interest rate differentials remain very high, coupled with the disappointment over the lack of clearer guidance on the timing of the next hike.

A rather pragmatic take was shared by Goldman Delta One head, Rich Privorotsky who pointed to the breakout in Japanese 10 year yields above 2% – rising 5bps to 2.02%, the highest since 1999 – as the market was convinced the BOJ remains behind the curve.

But the latest twist – which is what the cartoonish BOJ is so known for – was the lack of a pre-commitment to future hikes, and the continued vagueness on timing.

“The market had expected a hawkish hike from the BOJ, with the expectation of clarifying its stance on narrowing the neutral rate range and future rate hike path,” ING Bank’s Min Joo Kang and Chris Turner wrote in a note. “However, both the BOJ and Ueda remained quite vague on this matter, which likely caused disappointment in the market.”

As a result, the whole JGB curve twisted higher and bear steepening while the JPY is weakening, precisely the opposite of what the BOJ wanted to achieve! According to Privo, on the margin “the price action would suggest BOJ still behind the curve (run it hot).” Japan equities are higher led by Japan banks, momentum and construction. Keep an eye on longer dated rates for hints on whether the BOJ is about to lose control of the bond market.

Many market players had been expecting the governor to back up their consensus view that Ueda will keep raising rates every six months.

Some of them even thought he might hint at how far the BOJ wanted to hike rates, by referring to the neutral interest rate. Instead, the professor-turned-central bank governor struck a pragmatic note, saying the bank would edge closer to neutral rather than trying to pinpoint in advance where it is.

That creates a headache for Japan’s Finance Ministry, which spent some $100 billion last year to prop up the currency when it weakened to around 160 per dollar — not far from where it is now.

“The yen’s slide is likely to heighten caution about the risk of intervention,” Ino said.

The market moves point to some of the difficulties Ueda faces in the second half of his term. In his first two-and-a-half years, the governor exceeded expectations by transforming policy at the BOJ and raising rates.

Ueda now risks damaging that reputation even more – and infuriating Prime Minister Sanae Takaichi – if he hikes rates too fast and the economy collapses, while the yen craters. But moving too slowly could prolong the inflation damage for households, and leave the Finance Ministry with work to do in the currency market.

What’s more, a return to yen intervention may also prompt further blowback from President Donald Trump’s administration in the US, which sometimes appears frustrated by Japan’s cautious monetary policy.

Nobuyasu Atago, chief economist at Rakuten Securities Economic Research Institute and a former BOJ official, notes that US Treasury Secretary Scott Bessent is clearly in favor of correcting yen weakness through BOJ policy rather than intervention.

“Governor Ueda likely thinks that yen weakness will enable him to keep raising rates,” said Atago. “But that takes him further away from policy normalization that responds to the bedding-in of inflation based on domestic demand, not external shocks.”

For now, the only thing that’s clear is that rates are likely to increase again unless of course the economy collapses next.

According to Bloomberg, the question now is how far Ueda can go. Just two years ago, economists projected that the bank would only reach 0.5% in this hiking cycle. Now, if the central bank can hike every six months, Ueda would be walking out of the BOJ building in April 2028 with the rate at 1.75% and a reputation for working miracles in Japan.

“The hurdle just gets higher and higher,” Kazuo Momma, a former BOJ executive director in charge of monetary policy, told Bloomberg. Although the BOJ doesn’t know where the neutral rate is, each hike brings the bank closer to it, he said. Among 48 economists surveyed in December, the median forecast points to two more hikes. But more than 20 of them expect three or more.

Ueda has repeatedly said that he prefers to hike and monitor the impact rather than map out his endgame. And he’s reiterated time and again that he will continue to raise rates if the economy and prices play out as the bank expects.

In Friday’s policy statement, the BOJ stated that the real rate remains at a “significantly” low level.

“That suggests the next rate hike will still be an adjustment of monetary easing and that’s hugely important,” Momma said. “This implicitly says that the BOJ thinks 1% isn’t the neutral rate.”

In other words, as long as the BOJ keeps referring to rates at “significantly” low levels, the central bank remains a ways off the neutral rate. That also fits in with Ueda’s view that his rate hikes aren’t yet tightening moves, but are instead the adjustment of accommodative conditions. With inflation still way above borrowing costs, it’s hard to argue otherwise.

Commenting on the paradoxical plunge in both the yen and yields, Bloomberg FX strategist Vassilis Karamanis said that this was “not a paradox but a reflection of positioning and timing” (well, maybe it was a little bit of a paradox). He explains why:

Yen weakness after the Bank of Japan’s interest rate increase shouldn’t surprise. Neither should the risk of intervention if thin liquidity turns an orderly grind into a disorderly move.

The BoJ did what yen bulls have been long waiting to see, but it didn’t hand them a clear victory. The central bank raised its benchmark rate by a quarter point to 0.75%, the highest in 30 years, and kept the door open to further increases if the outlook holds. The message was that officials are growing more confident inflation can be sustained around target.

And yet the first price reaction looked like a reminder that FX is rarely polite. The yen weakened, with USD/JPY pushing through the 156 area even as Japanese yields rose, with the 10-year yield topping 2% for the first time since 2006. That’s not a paradox but a reflection of positioning and timing.

Above all, this was widely expected. When the market walks into a meeting already priced for 25 basis points, “hawkish BOJ” has to mean more than just delivering the hike. It needs to mean conviction on the pace, and right now, the bar for that conviction is high because the BOJ communicates gradualism given there was no upgraded assessment of the economy. Governor Kazuo Ueda said that it’s difficult to determine the neutral rate ahead of time, and that the pace of adjustment of easing depends on the economy and prices.

This gradualism matters because the yen’s core problem isn’t whether Japan can hike, but whether it can hike fast enough to overwhelm the funding-currency reflex. Carry and hedging behavior have inertia. You can tighten policy and still watch USD/JPY grind higher if the market thinks the next move is “sometime in 2026” rather than next quarter, especially while the US-Japan rate gap remains wide enough to keep the carry trade alive.

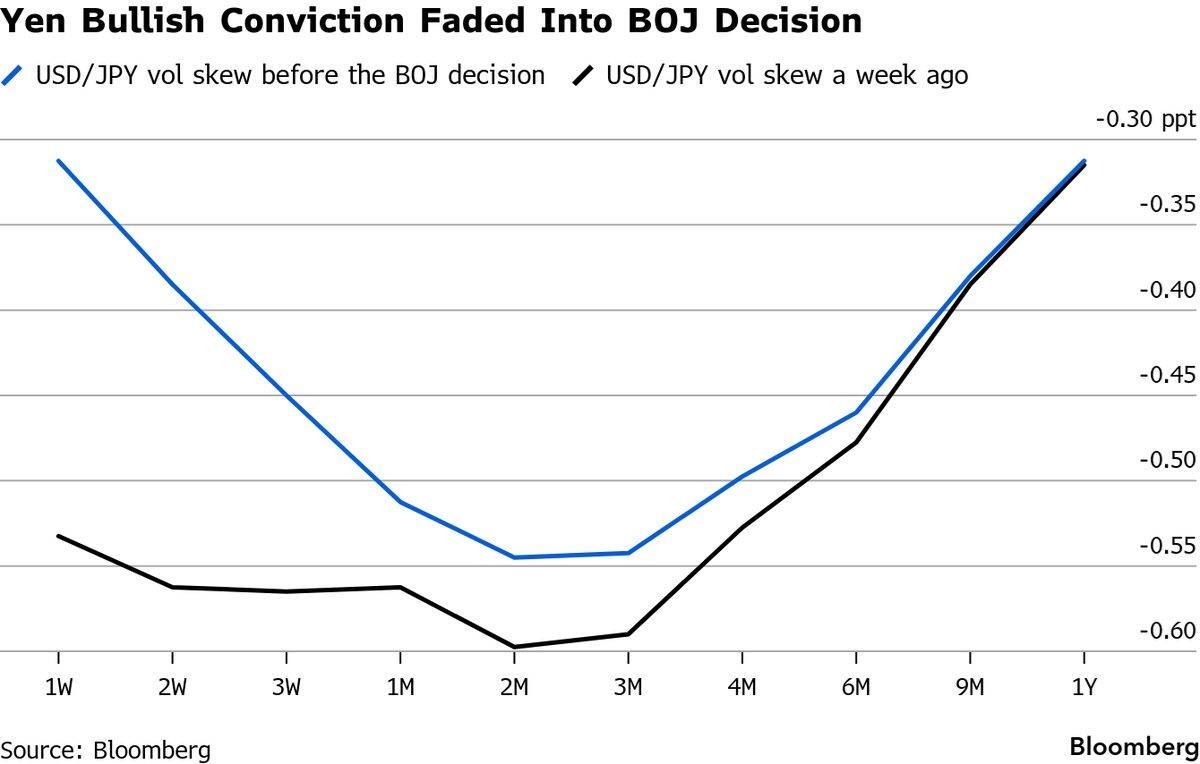

Options were flagging that risk into the meeting. The chart below shows USD/JPY skew flattening versus last week, a sign traders were less willing to pay up for yen strength protection across the front end. And CFTC positioning tells a similar story: hedge funds weren’t in a rush to cover shorts.

The macro backdrop isn’t giving the yen a clean runway either. Fiscal stimulus expectations and Japan’s heavy debt load keep the bond market sensitive, and currency weakness can still function as a release valve rather than a red line. Which brings us to the part yen traders need to respect into year end: intervention risk.

The market loves to talk about 160 as if it’s a magic number but I’m not so sure officials also do so. While in theory their framework is supposed to be about speed, disorder and volatility, and not a single level, recent episodes show thresholds can be blurry in practice. And as holiday conditions can turn a routine move into an ugly one quickly, levels and volatility may not matter much, and we could see a preemptive move from the Ministry of Finance as the one in November 2024.

Liquidity is thinning into year-end. If USD/JPY starts to gap on air pockets rather than fundamentals — remember, the rate gap has been narrowing for three years now — the theme can turn from BOJ gradualism to MOF tolerance. That’s why the post-hike yen selloff is not the shocking part. That would be assuming officials will wait patiently for 160 or above if the market hands them disorder first.

Tyler Durden

Fri, 12/19/2025 – 10:18

Loss Of Credibility: Yen Craters, Yields Surge After BOJ Hikes Rates To Highest Since 1999

Loss Of Credibility: Yen Craters, Yields Surge After BOJ Hikes Rates To Highest Since 1999

In the last central bank decision of 2025, the BOJ lifted its key rate to 0.75% from 0.50% in a widely anticipated and telegraphed move, taking borrowing costs to their highest level in three decades. It wasn’t enough, however, and after an initial kneejerk move, the yen plunged while yields soared as the market concluded that what Ueda did was too little, too late, and the hike was too vague to press the hawkish case.

As such, the market doves are back in control, and forcing the BOJ to either double down and puts Japan’s money where its mouth is, or lose control of either the currency or the bond market, or eventually, both.

In a recap of what the BOJ did, Bloomberg writes the following:

Ueda said risks tied to the impact of US tariffs appear to be easing and pointed to solid wage growth momentum next year year, a condition for more sustained inflation.

Both the BOJ statement and Ueda’s remarks implied there’s room to raise rates further, while offering assurance that conditions would remain accommodative. That reinforces expectations of a gradual and data-dependent tightening path.

Ueda also said the policy rate remains some distance from the lower-end of a neutral range and added he would like to recalculate that if the opportunity arises, signaling openness to further tightening but also a desire for greater confidence in the framework before moving more decisively.

As BBG notes, by lifting the policy rate to a three-decade high of 0.75% on Friday, Ueda continued his historic march toward restoring normality to Japan’s monetary policy and the economy after decades of unconventional steps and underperformance. The only problem: Japan will never survive in a world where monetary policy is even remotely “normal ” and as a result, government bond yields immediately climbed to the highest levels since the 1990s, an indication that the BOJ policy space is now narrower than ever.

And indeed, Bloomberg admits that while Ueda had telegraphed Friday’s move ahead of time, he didn’t offer similar clarity about what comes next, and that’s left yen bears chomping on the currency instead of backing away. The yen slid more than 1% against the dollar, to around 157.40, in the hours after Ueda’s press conference.

“Listening to what he said, I honestly couldn’t tell at all when the next rate hike might be,” said Teppei Ino, Tokyo head of global markets research at MUFG Bank. “He didn’t really say anything about the neutral rate — there was simply no guidance at all.”

Addressing the hawkish side, Goldman’s Kai Wen Lim writes that the statement removed language that growth and inflation will stagnate due to tariffs, coupled with hawkish voices on the board and a clear acknowledgement that real rates are still low, all leaned on the more hawkish side despite a lack of new details. The reaffirmation bolstered bearish sentiment causing futures to sell off ~4bps while BOJ pricing also inched higher across the curve from March onwards, with June and July seeing the most traction implying market expectation of the next hike being ~6 months away.

On the other hand, classic “buy the rumor, sell the fact” phenomenon was observed in USDJPY, with the pair initially weakening a touch on initial headlines before surging and swiftly breaking past the 156 handle (and then 157) with investors likely thinking interest rate differentials remain very high, coupled with the disappointment over the lack of clearer guidance on the timing of the next hike.

A rather pragmatic take was shared by Goldman Delta One head, Rich Privorotsky who pointed to the breakout in Japanese 10 year yields above 2% – rising 5bps to 2.02%, the highest since 1999 – as the market was convinced the BOJ remains behind the curve.

But the latest twist – which is what the cartoonish BOJ is so known for – was the lack of a pre-commitment to future hikes, and the continued vagueness on timing.

“The market had expected a hawkish hike from the BOJ, with the expectation of clarifying its stance on narrowing the neutral rate range and future rate hike path,” ING Bank’s Min Joo Kang and Chris Turner wrote in a note. “However, both the BOJ and Ueda remained quite vague on this matter, which likely caused disappointment in the market.”

As a result, the whole JGB curve twisted higher and bear steepening while the JPY is weakening, precisely the opposite of what the BOJ wanted to achieve! According to Privo, on the margin “the price action would suggest BOJ still behind the curve (run it hot).” Japan equities are higher led by Japan banks, momentum and construction. Keep an eye on longer dated rates for hints on whether the BOJ is about to lose control of the bond market.

Many market players had been expecting the governor to back up their consensus view that Ueda will keep raising rates every six months.

Some of them even thought he might hint at how far the BOJ wanted to hike rates, by referring to the neutral interest rate. Instead, the professor-turned-central bank governor struck a pragmatic note, saying the bank would edge closer to neutral rather than trying to pinpoint in advance where it is.

That creates a headache for Japan’s Finance Ministry, which spent some $100 billion last year to prop up the currency when it weakened to around 160 per dollar — not far from where it is now.

“The yen’s slide is likely to heighten caution about the risk of intervention,” Ino said.

The market moves point to some of the difficulties Ueda faces in the second half of his term. In his first two-and-a-half years, the governor exceeded expectations by transforming policy at the BOJ and raising rates.

Ueda now risks damaging that reputation even more – and infuriating Prime Minister Sanae Takaichi – if he hikes rates too fast and the economy collapses, while the yen craters. But moving too slowly could prolong the inflation damage for households, and leave the Finance Ministry with work to do in the currency market.

What’s more, a return to yen intervention may also prompt further blowback from President Donald Trump’s administration in the US, which sometimes appears frustrated by Japan’s cautious monetary policy.

Nobuyasu Atago, chief economist at Rakuten Securities Economic Research Institute and a former BOJ official, notes that US Treasury Secretary Scott Bessent is clearly in favor of correcting yen weakness through BOJ policy rather than intervention.

“Governor Ueda likely thinks that yen weakness will enable him to keep raising rates,” said Atago. “But that takes him further away from policy normalization that responds to the bedding-in of inflation based on domestic demand, not external shocks.”

For now, the only thing that’s clear is that rates are likely to increase again unless of course the economy collapses next.

According to Bloomberg, the question now is how far Ueda can go. Just two years ago, economists projected that the bank would only reach 0.5% in this hiking cycle. Now, if the central bank can hike every six months, Ueda would be walking out of the BOJ building in April 2028 with the rate at 1.75% and a reputation for working miracles in Japan.

“The hurdle just gets higher and higher,” Kazuo Momma, a former BOJ executive director in charge of monetary policy, told Bloomberg. Although the BOJ doesn’t know where the neutral rate is, each hike brings the bank closer to it, he said. Among 48 economists surveyed in December, the median forecast points to two more hikes. But more than 20 of them expect three or more.

Ueda has repeatedly said that he prefers to hike and monitor the impact rather than map out his endgame. And he’s reiterated time and again that he will continue to raise rates if the economy and prices play out as the bank expects.

In Friday’s policy statement, the BOJ stated that the real rate remains at a “significantly” low level.

“That suggests the next rate hike will still be an adjustment of monetary easing and that’s hugely important,” Momma said. “This implicitly says that the BOJ thinks 1% isn’t the neutral rate.”

In other words, as long as the BOJ keeps referring to rates at “significantly” low levels, the central bank remains a ways off the neutral rate. That also fits in with Ueda’s view that his rate hikes aren’t yet tightening moves, but are instead the adjustment of accommodative conditions. With inflation still way above borrowing costs, it’s hard to argue otherwise.

Commenting on the paradoxical plunge in both the yen and yields, Bloomberg FX strategist Vassilis Karamanis said that this was “not a paradox but a reflection of positioning and timing” (well, maybe it was a little bit of a paradox). He explains why:

Yen weakness after the Bank of Japan’s interest rate increase shouldn’t surprise. Neither should the risk of intervention if thin liquidity turns an orderly grind into a disorderly move.

The BoJ did what yen bulls have been long waiting to see, but it didn’t hand them a clear victory. The central bank raised its benchmark rate by a quarter point to 0.75%, the highest in 30 years, and kept the door open to further increases if the outlook holds. The message was that officials are growing more confident inflation can be sustained around target.

And yet the first price reaction looked like a reminder that FX is rarely polite. The yen weakened, with USD/JPY pushing through the 156 area even as Japanese yields rose, with the 10-year yield topping 2% for the first time since 2006. That’s not a paradox but a reflection of positioning and timing.

Above all, this was widely expected. When the market walks into a meeting already priced for 25 basis points, “hawkish BOJ” has to mean more than just delivering the hike. It needs to mean conviction on the pace, and right now, the bar for that conviction is high because the BOJ communicates gradualism given there was no upgraded assessment of the economy. Governor Kazuo Ueda said that it’s difficult to determine the neutral rate ahead of time, and that the pace of adjustment of easing depends on the economy and prices.

This gradualism matters because the yen’s core problem isn’t whether Japan can hike, but whether it can hike fast enough to overwhelm the funding-currency reflex. Carry and hedging behavior have inertia. You can tighten policy and still watch USD/JPY grind higher if the market thinks the next move is “sometime in 2026” rather than next quarter, especially while the US-Japan rate gap remains wide enough to keep the carry trade alive.

Options were flagging that risk into the meeting. The chart below shows USD/JPY skew flattening versus last week, a sign traders were less willing to pay up for yen strength protection across the front end. And CFTC positioning tells a similar story: hedge funds weren’t in a rush to cover shorts.

The macro backdrop isn’t giving the yen a clean runway either. Fiscal stimulus expectations and Japan’s heavy debt load keep the bond market sensitive, and currency weakness can still function as a release valve rather than a red line. Which brings us to the part yen traders need to respect into year end: intervention risk.

The market loves to talk about 160 as if it’s a magic number but I’m not so sure officials also do so. While in theory their framework is supposed to be about speed, disorder and volatility, and not a single level, recent episodes show thresholds can be blurry in practice. And as holiday conditions can turn a routine move into an ugly one quickly, levels and volatility may not matter much, and we could see a preemptive move from the Ministry of Finance as the one in November 2024.

Liquidity is thinning into year-end. If USD/JPY starts to gap on air pockets rather than fundamentals — remember, the rate gap has been narrowing for three years now — the theme can turn from BOJ gradualism to MOF tolerance. That’s why the post-hike yen selloff is not the shocking part. That would be assuming officials will wait patiently for 160 or above if the market hands them disorder first.

Tyler Durden

Fri, 12/19/2025 – 10:18

Man sets himself on fire at Damen station on CTA Blue Line

A man set himself on fire Friday morning at a CTA Blue Line stop at Damen Avenue in the Wicker Park neighborhood, causing significant Blue Line delays, officials said.

It was not immediately clear if the fire was accidental or not, Chicago Fire Department spokesman Larry Merritt said.

The man was taken in critical condition to Stroger Hospital.

Train service on the Blue Line was significantly delayed Friday, Chicago Transportation Authority officials warned.

“Forest Park- bound Blue Line trains are running w/residual delays following earlier fire department activity at Damen,” the CTA said in an alert. “Allow extra travel time.”

https://www.chicagotribune.com/2025/12/19/fire-damen-cta-blue-line/

6-foot-8 Edvardas Stasys plays a ‘huge part’ in Benet’s success. The Division I prospect does more than dunk.

Benet junior forward Edvardas Stasys traces his family’s roots across the Atlantic Ocean to Lithuania, a country with a rich basketball tradition.

Stasys’ father, Tomas, played basketball in Lithuania, came to the United States to attend college in the early 2000s and decided to stick around.

“Being Lithuanian is a big part of who I am,” Stasys said. “The first team I played on was a Lithuanian team. It’s a tight-knit community.”

The 6-foot-8 Stasys belongs to a tight-knit family that includes his older sister Gabby, who plays volleyball at Yale. He hasn’t visited Lithuania for several years, but his grandparents and other relatives still live there, and he’s in regular contact with them.

Then there is Stasys’ father.

“He’s always come to support me at all my games,” Stasys said. “He’s my biggest supporter.”

Stasys has plenty of supporters among his teammates, including one who hails from across the Pacific Ocean.

Senior guard Ethan MacDermot, who moved to the United States from Australia at the beginning of the summer, was impressed with Stasys right away.

“He’s quite mature and responsible,” MacDermot said. “He holds himself to a high standard.

“He’s just a great teammate, very engaging. He plays his role well. He has a real positive outcome on the team.”

Indeed, Stasys’ role has grown this season, as has his impact. He was the first or second player off the bench last season, when Benet won its first state championship.

Now Stasys is starting for the Redwings (10-1) and is averaging 12.0 points and 6.0 rebounds while shooting an impressive 63%.

“He’s really been a big part of our team,” Benet coach Gene Heidkamp said. “He has the ability to run and score in transition, score around the basket.

“He’s on the glass. He’s an excellent defender. Any success we’re going to have, he’s going to be one of the main reasons.”

That was the case Thursday. Stasys made 6 of 7 shots and finished with 12 points in Benet’s 49-25 nonconference victory over Lake Forest in Lisle.

Senior guard Jayden Wright, an Eastern Illinois recruit, likes what he’s seeing from the agile big man.

“He’s getting better in every single aspect on the basketball court,” Wright said. “He’s more confident. We know he can score at the basket, but he’s doing that at an even higher level, and just his energy.

“He brings a lot to the table for us. He’s definitely a huge part of our success.”

Stasys is driven to get better, and MacDermot is witnessing the results.

“Over the summer, the entire team was in the weight room, so I feel like he’s definitely worked on that aspect,” MacDermot said. “He definitely got more athletic and stronger, which has helped him be stronger in the paint.”

Stasys and 7-1 senior center Colin Stack, a North Dakota State recruit, make the Redwings particularly strong in the paint. Early in the third quarter Thursday, Stack found Stasys on a lob pass for an easy layup. Stasys scored inside again on the next possession.

“I love playing with Colin,” Stasys said. “He’s an incredible athlete. Normally, they’ve got to take the 5 man over to Colin, so then I’ve got a mismatch. So we can work with the high-low action.”

Stasys is also in the thick of the action on defense, which he knows is critical to success at the next level.

“Being able to play on both sides of the floor is huge,” he said. “I’m pretty athletic. Right now, rebounding, defensively, and getting to the rim is definitely the strongest aspects of my game. I’m trying to develop my game on the perimeter, so just expanding my game.”

Stasys has offers from Western Michigan and Grand Valley State and interest from Stanford and several Ivy League teams.

“I want to go to a high-academic school, but also I want to play basketball to the highest level I can,” he said. “I think I’ve got very good potential to be a good player. I try to work at it every single day.”

Matt Le Cren is a freelance reporter.

https://www.chicagotribune.com/2025/12/19/basketball-benet-edvardas-stasys/

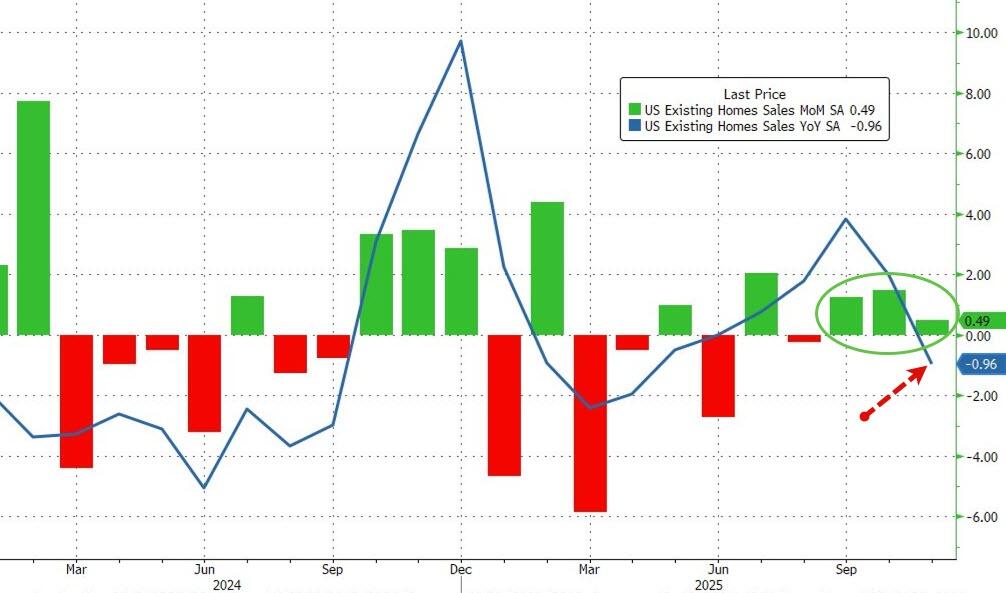

Year-Over-Year Existing Home Sales Disappoint In November, Decline Most In 6 Months

Year-Over-Year Existing Home Sales Disappoint In November, Decline Most In 6 Months

With mortgage rates tumbling, housing market participants have been disappointed by the lack of enthusiasm by homebuyers to apply for mortgages (though there was a decent bounce in refi activity)…

This morning’s existing home sales data (admittedly for November) will give us a further glimpse into the reality oh home-buying vs home-selling as the gap between current mortgage rates and the average existing mortgage rates is narrowing (but remains vast)…

But, analysts (rightfully, given the slide in mortgage rates) expected the recent trend of existing home sales growth to continue in November and it did… but only a mere +0.5% MoM (vs +1.2% MoM exp). October was revised up to +1.5% from +1.2%. More problematically, the disappointment pulled existing home sales down 1% YoY (the first negative print since May)…

Source: Bloomberg

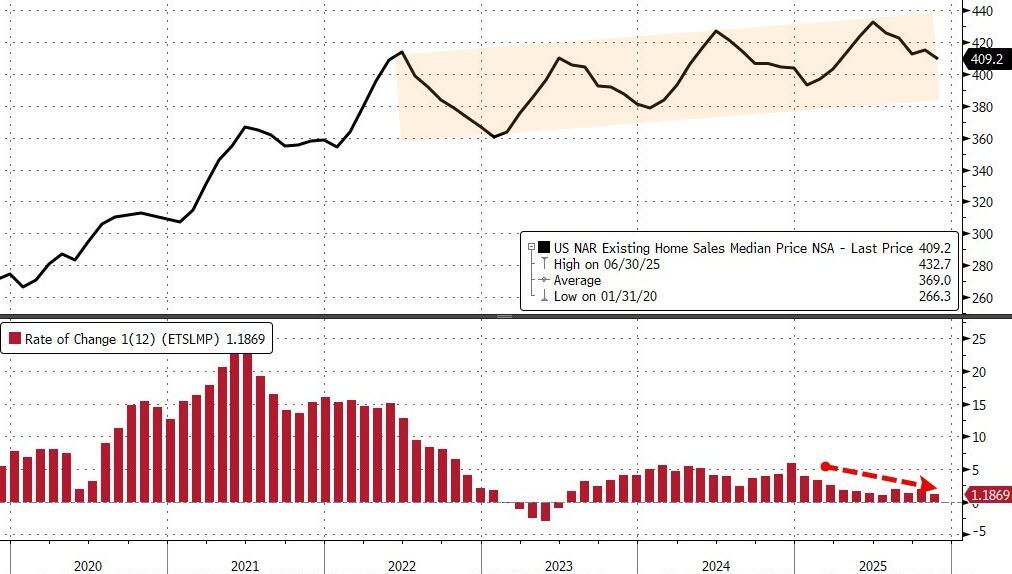

Meantime, the median sales price increased 1.2% from a year ago to $409,200. That was one of the weakest gains since mid-2023.

“Existing-home sales increased for the third straight month due to lower mortgage rates this autumn,” NAR Chief Economist Lawrence Yun said in a statement.

“However, inventory growth is beginning to stall.”

Source: Bloomberg

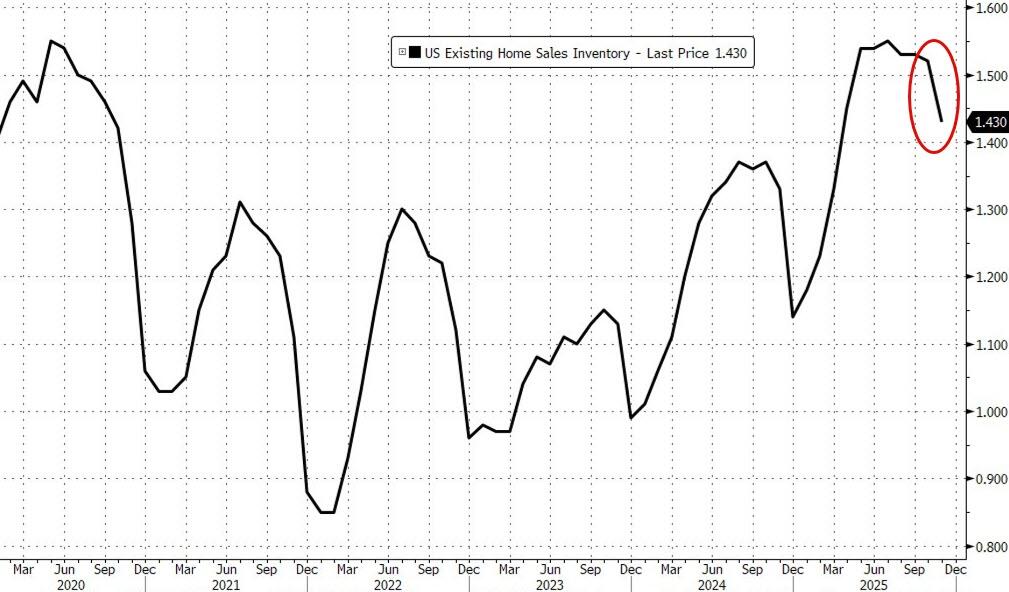

In November, the supply of previously owned homes on the market fell from the previous month to 1.43 million, roughly flat in recent months.

Source: Bloomberg

Yun said that’s because sellers aren’t desperate and are choosing to de-list and try again in the popular spring-selling season instead.

At the current sales pace, inventory is equivalent to 4.2 months’ supply, the weakest since March.

Sales rose in the Northeast and South, the nation’s biggest home-selling region. The pace of closings in those two regions were the highest since early this year. Activity was flat in the West and declined in the Midwest.

And, arguably, there is more room for existing home sales to run here as mortgage rates hit three year lows…

Source: Bloomberg

NAR sees sales rising 14% next year, higher than most other forecasts but a figure that Yun said he feels “confident” in. That assumes more inventory will come on the market, mortgage rates will hover around 6% and the Federal Reserve will cut interest rates another two times, compared to policymakers’ median projection for one.

Tyler Durden

Fri, 12/19/2025 – 10:10

TrueNorth to move ahead with reorganization: ‘This has not been an easy year’

In a reversal of fortunes from earlier this year, TrueNorth Educational Cooperative 804 will proceed with an extensive reorganization effort, with nearly all of its member districts remaining on board.

During a leadership council meeting on Wednesday, the cooperative’s members voted to memorialize their decisions regarding whether to remain, withdraw, or stay undecided in relation to TrueNorth. Just one district — Glenview School District 34 — chose to withdraw, and another — Deerfield School District 109 — remains undecided.

TrueNorth provides education services to students with special needs in southeastern Lake County, such as those with autism, anxiety, developmental delays, emotional or behavioral disabilities, and other issues.

Earlier this year, several member districts had moved to withdraw from the district, saying they had expanded their own special education programs and services and no longer needed TrueNorth. That snowballed into all 18 participating school districts submitting letters of intent to withdraw from the cooperative.

But after months of discussions and planning around potential reorganization, including a proposed overhaul of the cooperative’s funding model, the member school districts voted Wednesday to either remain or continue with withdrawal, and TrueNorth will be moving ahead with reorganization.

Since the withdrawal shakeup began earlier this year, TrueNorth has seen a change of leadership. Former Superintendent Kurt A. Schneider joined Milwaukee Public Schools as an academic superintendent in June. In his place, leading TrueNorth are Interim Superintendents Jimmy Gunnell and Jim Nelson, who have more than three decades of combined experience as executive directors at similar cooperatives.

Mike Carrol, TrueNorth faculty association president, speaks during a leadership council meeting. In a reversal from earlier this year, nearly all of the education cooperative’s member districts plan to remain as it moves ahead with reorganization. (Joe States/Pioneer Press)

During public comments on Wednesday, Mike Carroll, the TrueNorth Faculty Association president, expressed the staff’s thanks to those involved in the reorganization process that helped stave off dissolution. Carroll requested a continued “commitment to transparency and timeliness” as the process, which will include extensive staffing reductions, continues.

“This has not been an easy year. The uncertainty and anxiety surrounding the future of our cooperative has been significant for staff,” Carroll said. “Our shared goal for this school year is to support every student as we navigate this transition.”

In a letter to the public earlier this year, Nelson and Gunnell had said they anticipated about half of the current TrueNorth administration and staff positions would be eliminated. On Wednesday, Gunnell said those cuts would be spread over two years.

What exactly that process would look like still needs to be finalized, Gunnell said.

As part of restructuring, gone also will be the superintendent position, replaced by an executive director.

Reorganization

In previous interviews and a September letter to families and staff, Gunnell and Nelson laid out the broad strokes of what reorganization will look like: “Significant changes to leadership, governance and funding models,” and making the cooperative “more focused and sustainable.”

School districts had initially moved for withdrawal because, in the decades since TrueNorth’s creation, they had expanded their own special education services. Looking ahead, TrueNorth will focus on the “complex and unique learners,” Nelson said, the “1% exceptional learner, those students that need more structure and support.”

James Nelson, co-superintendent of TrueNorth Educational Cooperative, speaks during a leadership council meeting. He and James Gunnell are leading the cooperative through reorganization. (Joe States/Pioneer Press)

“We’re working directly with the district representatives for special education to determine what those needs are,” Gunnell said. “That’s been a big change, to actually listen to what they need and design programs based on their needs.”

According to the letter, funding will shift to a “usage-based” model for member districts, rather than paying the annual membership fees or operations and maintenance assessments based on total student enrollment.

Usage charges will be partially offset by funding from the Illinois State Board of Education, with administrative expenses built into tuition and service rates paid by member districts based on usage, the letter said.

The reorganization will also include the sunsetting of some current programs and services, since member districts have “developed greater internal capacity,” the letter said.

Arbor Academy, and the three North Shore Academy elementary, middle and high schools will operate as a single therapeutic day school on the TrueNorth campus, the letter said, starting next school year.

TrueNorth will continue to offer early childhood programs to member districts, as well as transition services for students at the therapeutic day school through the school year in which they turn 22.

The cooperative will also continue providing member districts with access to contracted specialized services, including assistive technology, augmentative and alternative communication, vision services, nursing coordination and one-on-one support, occupational and physical therapy, speech-language services, and psychological school-based services.

https://www.chicagotribune.com/2025/12/19/truenorth-educational-cooperative-804-2/

Indian Prairie School District 204 board OKs $360.5 million tax levy, up 4.15% from last year

The Indian Prairie School District 204 board recently approved a $360.5 million property tax levy for 2025.

The levy, which is for taxes to be paid next year, features a roughly $14.4 million increase over the 2024 levy, which property owners paid this year.

Assuming an average home value of $507,000, the increase will add about $187, an increase of about 2.9%, to the portion of the tax bill paid to the school district, according to District 204 Chief School Business Official Matt Shipley.

The total estimated payment to the district for a taxpayer with a property valued at $507,000 would be $7,318, Shipley told The Beacon-News.

The property tax levy, which represents the total amount Indian Prairie is looking to receive from all property owners in the district, was increased by the Consumer Price Index, or CPI, a measure of inflation set by the U.S. Bureau of Labor Statistics, along with an allowance for new construction. State law caps taxing bodies’ tax extensions at 5% or the previous year’s CPI, whichever is lower.

The CPI in 2024 was 2.9%, and the district is expecting an additional 1.25% increase for new property, according to Shipley, for a total operating levy increase this year of 4.15%.

The $360.5 million figure does not include, however, the district’s bond and interest levy, set at around $27.2 million — around $1.5 million higher than last year. The bond and interest levy amount is set by the county, Shipley has said.

That levy amount is consistent, Shipley said, with the district’s promise to keep the tax rate flat for residents in terms of their contribution to capital projects following the passage of a referendum in November authorizing the district to sell $420 million in bonds for facility improvements. The bonds are to be paid for using a continuation of an existing 37-cent property tax per $100 of equalized assessed value that would otherwise have expired at the end of 2026.

With the bond and interest levy, the district’s total levy amount comes to a little under $387.7 million, for an overall increase of approximately 4.28% from 2024, per Shipley’s presentation.

On Monday, Shipley said that the district is “asking for revenues only to the extent necessary to fund services,” citing rising costs outpacing the CPI for things like salaries, health insurance benefits and transportation. And he said state and federal funding the district receives “have also not kept up with inflationary challenges,” which make property tax revenue “even more critical for the district.”

At a school board meeting in November, Shipley explained that the district is expecting to see significant increases in assessed property values this year. He said that tax values tend to lag behind market values, but are expected to catch up to the post-COVID-19 pandemic market increases.

The district is also anticipating around $70 million in new property within the district, he said, which equates to an additional roughly $3 million in revenue to D204.

The majority of District 204’s revenue tends to come from property taxes. Its most recently adopted budget, passed in September, shows property taxes accounting for a little more than 77% of the district’s expected revenue. That percentage has been gradually rising over the past two decades, Shipley said on Monday when the levy was approved.

The tax burden in the district has also shifted more toward residential properties and away from commercial or industrial properties following the quadrennial reassessment in 2023, officials have said.

At Monday’s meeting, Shipley said the district is nevertheless estimating this will be its lowest tax rate since 2011, in part because of the “strong local residential property market” and the district having in past years made annual increases at or below the CPI.

The levy approved by the school board on Monday is expected to generate a tax rate of approximately 4.55%, according to Shipley, and an increase in an average property owner’s tax payment this year of 2.9%. But the levy numbers do not necessarily reflect the change individual taxpayers will see on their property tax bills, as it depends on changes in the assessed values of their properties.

Shipley, in November, explained that the district does not control the property assessment process. While the average increase in property tax bills this year is 2.9%, some taxpayers will see higher increases, and some will see lower. A more than 2.9% increase on an individual’s property tax bill would result from their property values having increased more than the average property throughout the district, he said.

Following the levy’s approval — which had to be done before the end of December, according to Shipley — the district then files it with DuPage and Will counties, which will issue the final property tax extension. The district does not expect to receive the full amount it is requesting, Shipley explained, as the counties will adjust the levy down based on the exact new property amount once it’s determined in the spring.

From there, the counties’ treasurers will bill residents, collect the property taxes and remit the district’s portion of the taxes collected to Indian Prairie.

mmorrow@chicagotribune.com

https://www.chicagotribune.com/2025/12/19/indian-prairie-approves-tax-levy-2/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}