Category: News

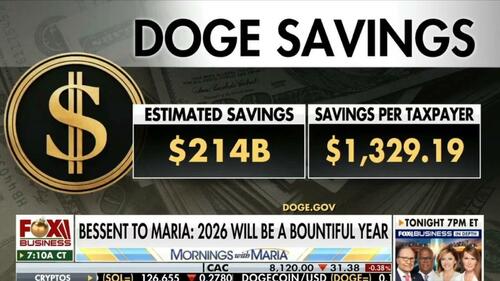

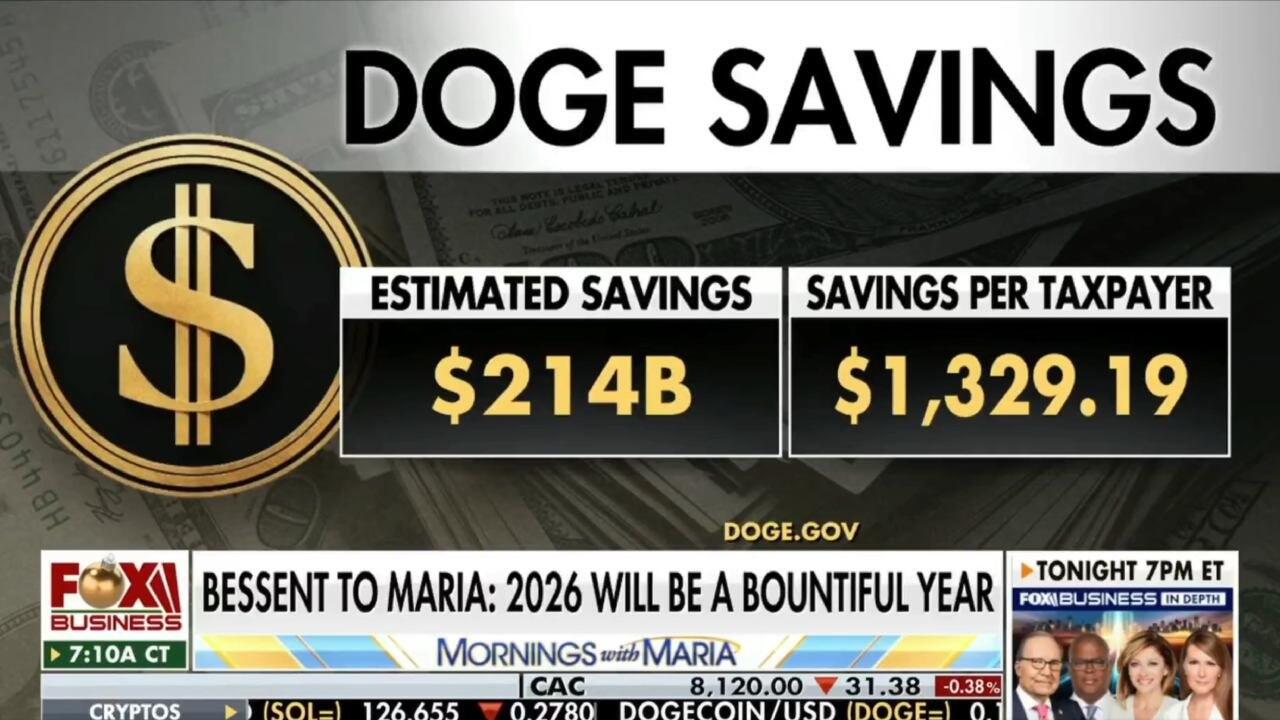

DOGE Delivers Massive $214 Billion In Taxpayer Savings… So Far

DOGE Delivers Massive $214 Billion In Taxpayer Savings… So Far

Authored by Steve Watson via Modernity.news,

In a stunning victory against bloated bureaucracy, the Department of Government Efficiency (DOGE), originally spearheaded by Elon Musk, has slashed an eye-popping $214 billion from federal spending in less than a year.

Official figures from DOGE’s own tally reveal a relentless assault on waste, including terminations of thousands of contracts, grants, and leases that were draining resources without delivering value.

From bloated defense deals to questionable health programs, the cuts are stacking up, proving that an America First approach can rein in the deep state’s excesses.

? A WIN! DOGE just hit $214,000,000,000.00 in taxpayer savings in only 11 months!

That’s $1,329 for every taxpaying American.

Elon and team delivering America a win! !pic.twitter.com/s33BjKLKJY

— Gunther Eagleman™ (@GuntherEagleman) December 22, 2025

The milestone comes amid widespread praise for Musk’s no-nonsense tactics, even as legacy media nitpicks the details. According to DOGE’s breakdown, contract cancellations alone account for around $61 billion, targeting over 13,000 agreements like a $3.9 billion aircraft maintenance boondoggle and multi-billion-dollar health service pacts that ballooned under prior administrations.

Grants saw $49 billion axed, hitting everything from foreign aid handouts to domestic epidemiology programs that critics argue fueled unnecessary spending.

Leases weren’t spared either, with $113 million clawed back from underused federal spaces across the country—think vacant offices in California and North Carolina that taxpayers were footing the bill for.

Beyond that, DOGE claims broader impacts through asset sales, fraud crackdowns, interest reductions, and workforce streamlining, pushing the total to that landmark $214 billion.

Dividing the savings by roughly 161 million U.S. taxpayers gives a saving of $1,329 for every taxpaying American, a direct hit against the endless tax hikes peddled by big-government advocates.

This triumph throws a harsh spotlight on the left’s double standards. As X user MAZE notes: “Democrats used to preach about the need to eliminate waste, fraud, and abuse from the system. Now they enable it and cover it up.”

Democrats used to preach about the need to eliminate waste, fraud, and abuse from the system.

Now they enable it and cover it up. pic.twitter.com/ocNF1DgPxw

— MAZE (@mazemoore) December 22, 2025

It’s a damning indictment—while DOGE was busy slashing redundancies, Democrats in Congress and their media allies dragged their feet, defending the very pork-barrel projects that Musk’s team eviscerated.

Recent reports confirm the context: DOGE’s efforts, though now wound down after achieving key goals, targeted sacred cows like USAID’s $1.75 billion grant to the GAVI Foundation and the Department of Energy’s half-billion-dollar handouts for dubious “decarbonization” schemes. These weren’t just cuts—they were a rejection of globalist agendas that prioritize foreign interests over American workers.

The raw impact is undeniable. Musk himself reflected that DOGE was “somewhat successful,” but the $214 billion speaks volumes, far exceeding initial lowered projections and delivering on President Trump’s promise to drain the swamp.

The ripple effects are already showing. Positive market indicators, as highlighted in recent Fox Business segments, point to a “bountiful” 2026 fueled by these efficiencies. Stock futures are climbing, cryptos are steady, and investor confidence is rebounding.

This isn’t about austerity—it’s about smart governance. By dismantling the layers of fraud and inefficiency that Democrats once railed against but now protect, DOGE has handed everyday Americans a massive return on their tax dollars.

This isn’t just numbers on a page—it’s real relief for every taxpaying American fed up with Washington’s endless money pit.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Tue, 12/23/2025 – 08:51

https://www.zerohedge.com/political/doge-delivers-massive-214-billion-taxpayer-savings-so-far

Versión ucraniana de “Bailando con las Estrellas” incluyendo a héroes de guerra

Por SAMYA KULLAB y VASILISA STEPANENKO

KIEV, Ucrania (AP) — Antes de la guerra, la versión ucraniana de “Bailando con las Estrellas” era un programa de televisión querido y popular, deslumbrando al público con actuaciones de celebridades y bailarines profesionales. El programa ahora regresa para un episodio especial, esta vez con héroes de guerra ucranianos, subrayando la resiliencia de la nación en tiempos difíciles.

Muchos aún recuerdan cómo el presidente Volodymyr Zelenskyy, entonces actor, ganó la competencia de baile en 2006, el año en que “Tantsi z zirkamy”, como se conoce al programa en ucraniano, debutó por primera vez.

En el nuevo episodio especial, los bailarines actúan con extremidades protésicas, mostrando su fortaleza para superar la adversidad. La lista de participantes incluye figuras públicas que ganaron prominencia desde que la guerra total de Rusia contra Ucrania se lanzó en febrero de 2022.

Pero al igual que la Ucrania actual, el programa, que es parte de una franquicia internacional, ha tenido que lidiar con una multitud de desafíos de guerra, incluidas frecuentes interrupciones de energía.

Todos los ingresos se destinarán al Centro para Superhumanos, una clínica especializada en el tratamiento y rehabilitación de víctimas de guerra.

Una nueva realidad

Durante una grabación previa la semana pasada, los bailarines giraron, saltaron y se deslizaron bajo el brillo de las luces, algunos integrando sin esfuerzo sus extremidades protésicas en la coreografía.

Para el productor creativo Volodymyr Zavadiuk, cada segmento del programa es valioso, creando algo especial durante tiempos difíciles.

“Se trata de nuestra resiliencia y se trata de nuestro futuro”, afirmó Zavadiuk, quien también dirige Big Brave Events y el departamento de Big Entertainment Shows en 1+1 Media.

Entre los artistas estaba Ruslana Danilkina, una veterana de guerra que perdió su pierna en combate en 2022 y ahora es reconocida en Ucrania por dedicarse a ayudar a las tropas heridas a adaptarse a la vida con prótesis.

Ella entregó una actuación apasionada centrada en reclamar su feminidad tras la lesión traumática.

También está de regreso en el programa el querido bailarín Dmytro Dikusar, esta vez como juez de la competencia. Compaginó la filmación con su servicio en el frente con su pelotón.

El músico de rock ucraniano Yevhen Halych se sentó en la silla de maquillaje antes de su número, reflexionando sobre su propia determinación de traer de vuelta el programa.

“Estamos filmando este proyecto en un país donde hay una guerra… Tenemos cortes de energía, puede haber una alerta aérea, podría haber bombardeos”, declaró. “¿Qué siento? Siento un deseo genuino de vivir una vida plena, sin importar lo que pase”.

Desafíos en tiempos de guerra

Producir el episodio especial del programa no ha sido una hazaña fácil en tiempos de guerra. Una transmisión en vivo era imposible: un ataque ruso puede ocurrir en cualquier momento. Luego estaban los obstáculos técnicos: durante la grabación de la semana pasada, un generador clave falló.

Cuando el programa se emita el domingo, el público votará por su favorito.

Danilkina, que tenía solo 18 años cuando perdió su pierna y que hoy trabaja en el Centro para Superhumanos, cautivó a todos con su apasionada actuación, su extremidad protésica artísticamente integrada en su rutina.

“Nuestro baile trata sobre la vida. Se trata de aceptar el amor”, dijo a The Associated Press después de su actuación. “Porque en realidad, cuando tu cuerpo está herido, es muy difícil amarte a ti mismo. Y permitir que alguien más te ame es aún más difícil”.

Su lesión no fue el final de su vida, indicó, y ahora quiere mostrar a “miles de chicos y chicas heridos que están comenzando sus vidas de nuevo” que no es el final de las suyas.

Para el veterano Ivan Voinov y su esposa de tres meses, Solomiia, el programa fue más que solo una actuación de baile: fue la segunda vez que bailaron juntos desde su lesión, la primera fue en su boda.

Solomiia Voinov sonrió tímidamente, recordando cómo había intentado durante mucho tiempo persuadir a Ivan de que debían bailar hasta que él cedió.

“No nos quitamos los ojos de encima mientras bailamos, y es una gran conexión”, señaló. “Estoy feliz”.

Añadió que ya estaba planeando su próximo baile: una bachata, un estilo de baile rápido y con movimientos de cadera que se originó en la República Dominicana.

“Podremos seguir bailando”, dijo. “Significa que hay futuro”.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

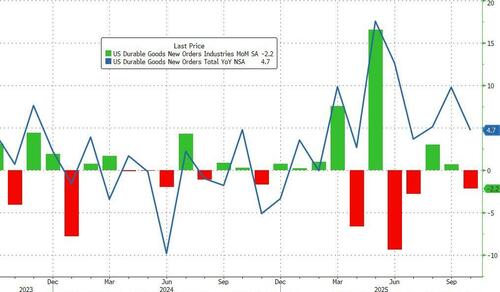

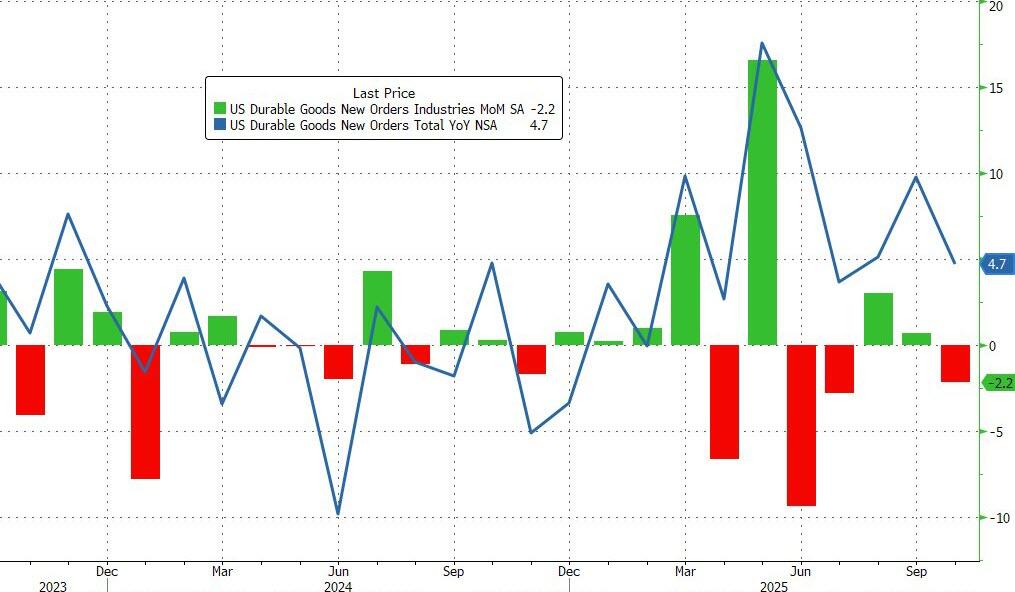

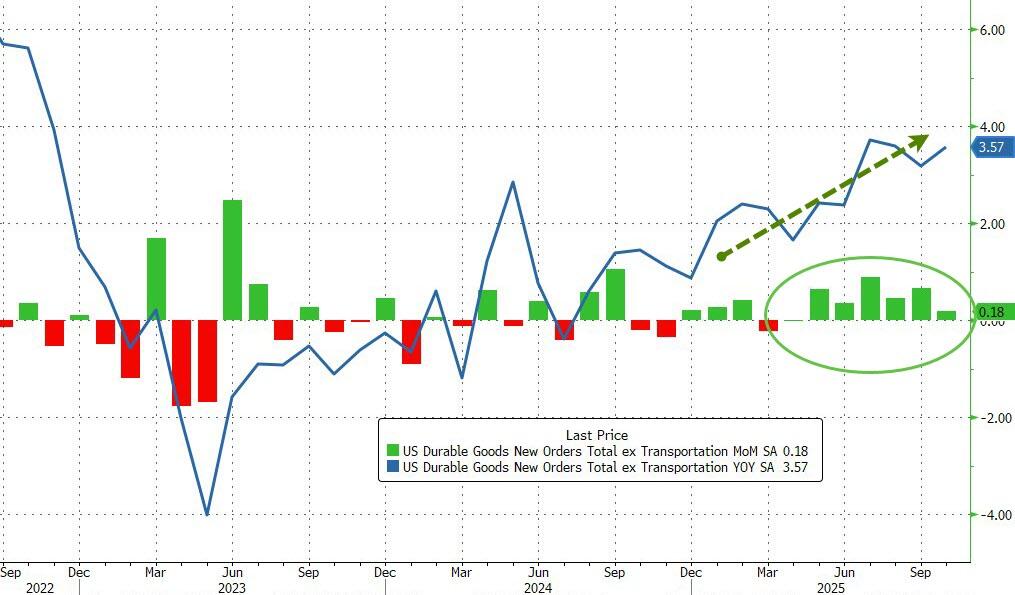

Core Durable Goods Orders Rise For 7th Straight Month

Core Durable Goods Orders Rise For 7th Straight Month

While admittedly extremely lagging, the preliminary OCTOBER durable goods orders print was a big disappointment after a rebound in the summer with the headline falling 2.2% MoM (far worse than the 1.5% MoM decline expected). However, while this disappointment dragged down the YoY growth to 4.7%, it was still well above inflation…

Source: Bloomberg

Core Orders (ex Transports) rose 0.2% MoM (notably slower than the 0.7% MoM in September and below the +0.3% MoM expected)…

Source: Bloomberg

That was the 7th straight monthly gain and lifted core durable goods orders up 3.57% YoY, near the highest since Nov 2022.

Finally, core capex remains solid with new orders ex-air up 0.5% (4th straight monthly gain) and shipments continue to significantly stronger than expected.

Tyler Durden

Tue, 12/23/2025 – 08:41

https://www.zerohedge.com/economics/core-durable-goods-orders-rise-7th-straight-month

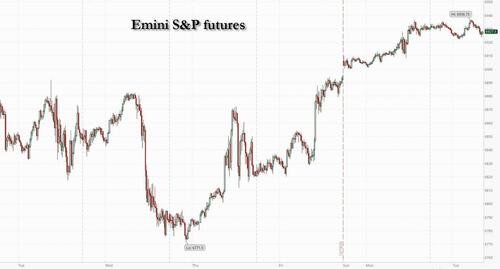

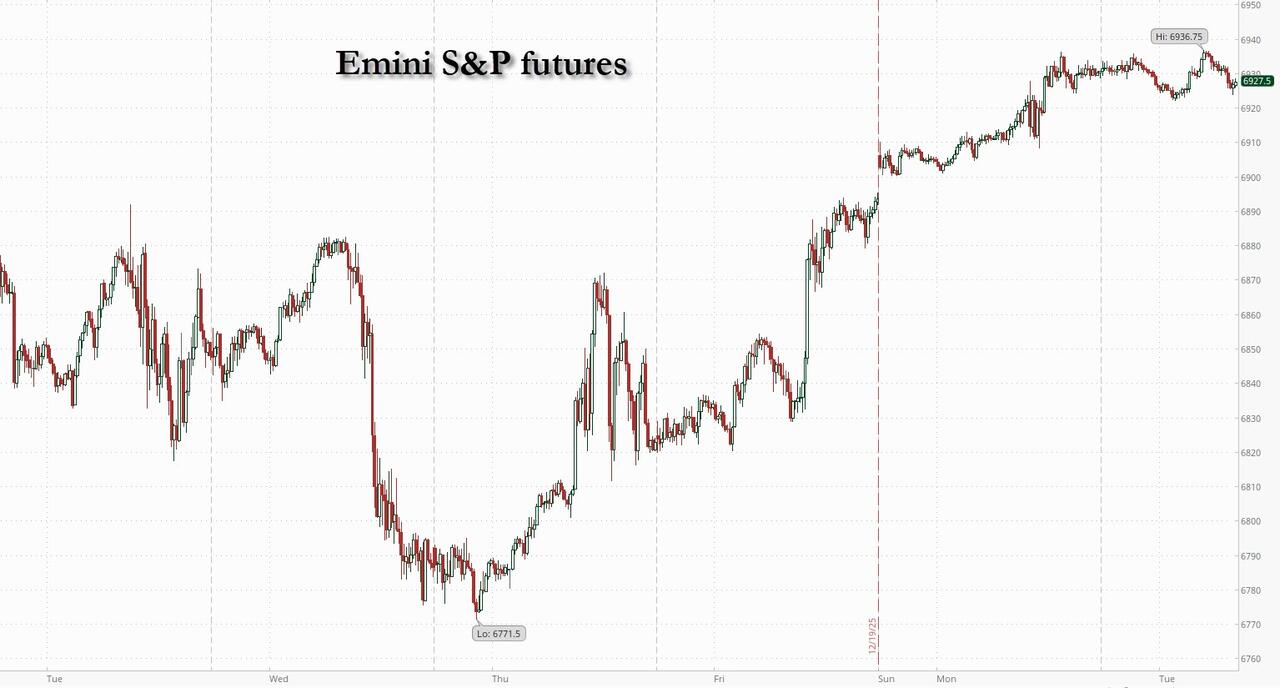

Futures Flat Ahead Of Final Macro Data Dump Of 2025

Futures Flat Ahead Of Final Macro Data Dump Of 2025

US equity futures are flat, pointing to a muted open off the overnight session highs on the last full trading session before Christmas, as traders await the last remaining data sets of 2025 to see whether they could materially change expectations for Federal Reserve interest-rate cuts. As of 8:0am ET, the S&P 500 is little changed after a three-day rally that has pushed the benchmark within reach of a new all-time high; Nasdaq futures are down 0.1% with Mag 7 names mixed. European stocks are buoyed by a 7% surge in the shares of Novo Nordisk after the Danish firm won US approval to sell a pill version of its obesity drug Wegovy. US Treasuries steadied after days of losses, with the 10-year yield declining two basis points to 4.15%. The dollar fell to the lowest level since October. Gold extended its record-breaking run, setting sights on $4,500 an ounce. Copper rose past $12,000 a ton for the first time. Bitcoin fell again, failing to stage even a modest rebound. The US calendar includes ADP weekly employment change (8:15am), 3Q GDP (8:30am), November industrial production (9:15am), December Richmond Fed manufacturing index, consumer confidence (10am).

In premarket trading, Mag 7 stocks are mixed: (Tesla +0.4%, Alphabet is little changed, Microsoft +0.07%, Apple -0.05%, Amazon -0.1%, Meta is little changed, Nvidia -0.4%)

Gold, silver and copper mining and royalty stocks climb as the metals continued to hit record highs amid rising geopolitical tensions. Barrick Mining (B) rises 1% while Hudbay Minerals (HBM) gains 1%.

Invivyd (IVVD) climbs 1% after the FDA granted a fast track designation for the biotech’s investigational vaccine-alternative monoclonal antibody candidate for Covid prevention in individuals with underlying risk factors for severe Covid.

Sable Offshore Corp. (SOC) soars 25% after the company said that the US Department of Transportation Pipeline and Hazardous Materials Safety Administration approved the firm’s Las Flores pipeline restart plan.

Zim Integrated Shipping Services (ZIM) climbs 8% after the company said it is evaluating proposals from multiple potential buyers. The review of strategic alternatives is in advanced stages.

In corporate news, department stores group Saks, facing limited options ahead of a more than $100 million debt payment due at the end of this month, is considering Chapter 11 bankruptcy as a last resort, according to people with knowledge of the situation. Johnson & Johnson was ordered to pay about $1.56 billion to a Maryland woman who blamed the company’s talc-based baby powder for causing her asbestos-linked cancer, the largest such jury verdict for an individual in 15 years of litigation. And Nvidia’s biggest Southeast Asian chip customer is facing a smuggling investigation.

The latest three-day rally pushed US stocks fractionally into positive territory for the month after a turbulent start to December. Preserving those gains until the end of December would extend this winning streak to an eighth month, the longest such run since 2018.

Meanwhile, volatility is collapsing. With the VIX index at 14.11, implied volatility for US equities over the coming 30 days is near the lowest in more than a year. That reflects enduring investor optimism around strong earnings growth, slowing inflation and a soft landing for the economy.

“Volatility is sitting at the lows of the year, while credit spreads are among the most compressed we’ve seen in decades,” said Alberto Tocchio, portfolio manager at Kairos Partners. “That dynamic is helping sustain the current market bonanza, especially in an environment where trading volumes are falling sharply and many discretionary players are already on the sidelines.”

The VIX may be snoozing around a 12-month low, but investors added new short bets across US stock futures last week, leaving net positioning near neutral levels, according to Citigroup strategists. Exposure to the Russell 2000 index of small caps is now bearish.

While Tuesday’s delayed third-quarter US gross domestic product print will likely be too dated to offer a clear read on current conditions, traders will also focus on consumer data after November showed a sharp slump in confidence.

In Europe, the Stoxx 600 edges up 0.2% to touch a new all time high with the health care sector leading gains. Novo Nordisk shares rally after the Danish drugmaker won approval to sell a pill version of its blockbuster obesity shot Wegovy in the US. Meanwhile, banks underperform. Here are some of the biggest movers on Tuesday:

Novo Nordisk shares rise as much as 7.9%, the most since August, after the Danish drugmaker won approval to sell a pill version of its blockbuster obesity shot Wegovy in the US.

SIG Group shares gain as much as 6.8%, the most in over a month, after the Swiss food packaging maker disclosed that Swedish activist investor Cevian Capital acquired a 3.1% stake.

Asian stocks were on course to advance for a third day, helped by gains in Japan amid expectations for further interest rate hikes. The MSCI Asia Pacific Index rose as much as 0.7%, with TSMC and Sony Group among the major contributors to the climb. Equities gained in Vietnam, Taiwan and Australia, while those in Indonesia fell. Speculation that the Bank of Japan may raise borrowing costs even more buoyed Japan’s financial stocks. Analysts said the yen’s continued weakness remains a tailwind for equities, even though the currency gained slightly overnight following comments by the finance minister. The onshore benchmark CSI 300 Index climbed 0.2%, despite a downgrade by Citi on Chinese equities to neutral from overweight on less favorable earnings revisions and a lackluster macro outlook.

In FX, the Bloomberg Dollar Spot Index is down 0.4%, falling for a second day and trading at the lowest since early October. The kiwi has overtaken the yen as the G-10 outperformer, rising 0.8% against the greenback. The yen is up 0.7%, dragging USD/JPY back below 156 after another round of jawboning from Japan’s Finance Minister. The Hungarian forint falls 0.2% after Economy Minister Nagy renewed his calls for lower interest rates.

Those moves came as the dollar headed for its weakest annual performance in eight years, with the options market signaling that traders are bracing for further losses. The currency is down 8.3% this year, on track for its biggest slide since 2017. Another modest dip would mark its worst year in at least two decades. Options pricing has also turned more negative, with so-called risk reversals, which track positioning and sentiment, showing options traders are the most bearish in three months.

“The structural drivers of US dollar weakness remain intact,” wrote Patrick Brenner, chief investment officer of multi-asset at Schroders Plc. “Institutional credibility continues to erode, fiscal deficits are widening, and global reserve managers remain steady buyers of gold rather than US dollar assets.”

In rates, treasuries advance, pushing US 10-year yields down 2 bps to 4.14%. European government bonds outperform.US yields richer by 1bp to 3bp across the curve in a bull flattening move, tightening 2s10s and 5s30s spreads by 1bp and 1.2bp on the day. Treasury 10-year yields trade around 4.14%, richer by 2.5bp on the day with bunds and gilts outperforming by an additional 1.5bp and 2bp in the sector. The Treasury is selling $70 billion 5-year notes at 1pm New York, with this week’s issuance concluding with $44 billion 7-year notes Wednesday. Ahead of today’s sale, the WI 5-year yield is about 3.705% which is ~14bp cheaper than the November stop-out

In commodities, gold and silver rise 0.9% each, having notched fresh record highs earlier. Copper also hits a record above $12,000 a ton. Brent was near $62 a barrel after rising about 5% over the previous four sessions as the US continued its blockade of crude shipments from Venezuela.Bitcoin falls 0.5%.

Today’s economic calendar includes ADP weekly employment change (8:15am), 3Q GDP (8:30am), November industrial production (9:15am), December Richmond Fed manufacturing index, consumer confidence (10am

Market Snapshot

S&P 500 mini little changed

Nasdaq 100 mini little changed

Russell 2000 mini little changed

Stoxx Europe 600 +0.2%

DAX +0.2%

CAC 40 -0.1%

10-year Treasury yield -2 basis points at 4.15%

VIX little changed at 14.04

Bloomberg Dollar Index -0.4% at 1201.58

euro +0.3% at $1.1796

WTI crude little changed at $58.03/barrel

Top Overnight News

Pill Version of Wegovy Is Approved for Use in the US: WSJ

Japan issues sternest intervention warning, says yen deviating from fundamentals: RTRS

China’s Sprint for Tech Dominance Can’t Hide an Economy Full of Holes: WSJ

Car Payments Now Average More Than $750 a Month. Enter the 100-Month Loan: WSJ

Copper Hits $12,000 for First Time as Tariff Trade Upends Market: BBG

Silver rises above $70/oz for the first time ever, gold rises to record $4500

Russian air attack on Ukraine kills three and sparks sweeping outages: RTRS

Ukraine’s Zelenskiy says several draft documents ready after Miami talks: RTRS

South Africans dragged into Russia’s war in Ukraine dig trenches, dodge bullets: RTRS

Russian Oil Stuck at Sea Booms as Tanker Logjams in Asia Expand: BBG

Trump is mulling giving 775 acres of federal wildlife refuge to SpaceX: NYT.

DOJ Releases Fresh Tranche of Epstein Files as Pressure Mounts: BBG

A Small Nebraska Town Is Reeling From the Exit of Meatpacking Giant Tyson: WSJ

Retail investors to have more sway over Wall Street after record year: RTRS

The AI Boom Is Making Real-Estate Investors Rich—and Exposing Them to Risk: WSJ

Trump’s First-Term Trust Buster Is Now Working to Get Paramount Its Deal: WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks eventually traded mixed after initially taking their cue from Wall Street, although volumes and news flow remained subdued as markets wound down for the holiday period. ASX 200 was underpinned by strength in gold miners after the yellow metal printed a fresh all-time high near USD 4,500/oz, supported by a softer USD and ongoing geopolitical tensions. Nikkei 225 initially saw shallower gains than peers as a firmer yen, following official jawboning, capped upside for the index, whilst further gains in the JPY later took the index into the red. KOSPI extended its tech-led rally, with Samsung Electronics shares pushing toward near all-time highs. Hang Seng and Shanghai Comp initially tracked the broader risk tone, while fresh region-specific catalysts remained scarce. Hang Seng later gave up earlier gains.

Top Asian News

Japanese Finance Minister Katayama declines to comment on forex levels or interest rates, and said Japan will take appropriate action and reiterates they have a “free hand” to respond to excessive moves in the JPY. FX moves after the BoJ press conference are speculative and not reflecting fundamentals. The market has stabilised somewhat since yesterday.

European bourses are mixed, with macro newsflow light. On the micro side, Novo Nordisk (+6.7%) said its oral Wegovy pill has been approved in the US for weight management after showing 16.6% weight loss in the OASIS 4 trial, and it plans a US launch in January 2026. European sectors have opened mixed with a slight positive bias. Health Care (+1.1%), to no surprise, leads due to gains in Novo Nordisk (+6.7%) after US approval of its weight-management drug. Utilities (+0.4%) and Food, Beverage and Tobacco (+0.4%) are also near the top, however, this is likely a rebound from yesterday’s underperformance. Banks (-0.3%), Consumer Products & Services (-0.3%) and Construction (-0.2%) lag, with little fresh newsflow driving moves.

Top European News

EU is preparing checks on imported plastics and other measures to shore up its recycling industry, according to FT.

European Car Sales +2.4% to 1.08mln vehicles in November, according to Bloomberg citing ACEA.

Novo Nordisk (NOVOB DC) said Wegovy pill is approved in the US as the first oral GLP-1 treatment for weight management after showing 16.6% weight loss in the Oasis 4 trial, and said it plans to launch the drug in the US in January 2026. US-listed NOVO shares +5% after market. Eli Lilly -1.2% after market.

US President Trump said he told French President Macron that France has to raise its drug prices.

Central Banks

RBA Minutes: Board discussed whether a rate increase might be needed at some point in 2026; holding the cash rate steady for some time could be sufficient to keep the economy in balance. October CPI suggested a risk that Q4 inflation could also be higher than forecast. The board discussed whether a rate increase might be needed at some point in 2026. Recent data suggested risks to inflation had lifted to the upside. The board judged it was too early to know whether the rise in inflation would prove persistent. The board said it would take a little longer to assess the persistence of inflation. Holding the cash rate steady for some time could be sufficient to keep the economy in balance. Policy would be assessed at future meetings, with Q4 inflation data available before the February meeting. Some board members felt conditions were no longer restrictive, while others felt they were a little restrictive. The impact of the recent rise in bond yields on financial conditions needed to be assessed. The economy was operating with excess demand and it was not clear if financial conditions were tight enough. The labour market was judged to still be a little tight, with the output gap positive. The full impact of policy easing earlier in the year was yet to be felt. Measures of capacity utilisation pointed to supply constraints. Little immediate action in AUD or ASX 200.

FX

DXY is lower and trades at the bottom end of a 97.88 to 98.23 range; really not much driving things for the USD recently, with newsflow exceptionally light, but perhaps facilitated by a strong JPY (see below). Nonetheless, traders will keep a keen eye out for Q3 GDP Advance/PCE, as well as Durable Goods (Oct), due at the same time.

JPY is amongst the outperformers, with the strength seemingly a continuation of the price action seen following fresh jawboning from Finance Minister Katayama; as a reminder, she said that they have a “free hand” to take bold action in the FX market if needed. USD/JPY drifted lower from an overnight high of 157.07, down below the 156.00 mark, where the pair currently resides.

Antipodeans also gained throughout overnight trade and into the European session, boosted by ongoing strength in metals prices (XAU now eyeing USD 4.5k/oz to the upside). Earlier, the Aussie showed little reaction to the RBA minutes, which indicated the Board debated whether a rate increase might be required at some point in 2026. Elsewhere, for the Kiwi specifically, NZD/USD breached 0.58 to the upside, which allowed the pair extend beyond the level, which can explain some of the outperformance this morning.

The GBP and EUR are steady vs the broadly weaker USD. Really not much driving things for either at the moment; the single currency really only has geopolitical updates to digest heading into the Christmas holidays. For Cable, the pair extended beyond the 1.3500 mark to make a peak of 1.3518; the next level to the upside includes the October 1 high at 1.3527.

Fixed Income

10yr JGB futures outperformed, firmer by over 40 ticks at best, while the yen simultaneously reversed its early-week weakness following verbal jawboning from Japanese Finance Minister Katayama. JGB futures then rose further after Japanese PM Takaichi said Japan’s national debt is still high, and rejected any “irresponsible bond issuance or tax cuts”, via a Nikkei interview.

USTs follow JGBs higher, with a lack of domestic newsflow helping things for the benchmark. Currently trading higher by a handful of ticks, and towards the upper end of a 112-11+ to 112-15+ range. Ahead, focus turns to some key US data points, which include US GDP Advance/PCE (Q3) and Durable Goods.

Bunds, Gilts and OATs also follow suit. For the latter, OATs remain in focus after yesterday’s cabinet meeting made the use of Article 49.3 more likely. For the near-term fiscal needs, the Assembly and Senate are set to finish debating and then adopt text to allow the government to continue financing basic public services into early-2026, despite the absence of a 2026 budget deal. A point that has contributed to OAT strength, as the benchmark marginally outmuscles Bunds, causing the OAT-Bund 10yr yield spread to probe 70bps to the downside.

China’s Finance Ministry expects aggregate government bond issuance to remain “elevated” in 2026, according to Reuters citing sources.

Commodities

WTI and Brent chop around USD 58/bbl and USD 62/bbl, respectively, in tight ranges as crude benchmarks consolidate following Monday’s bid higher. Geopolitics has resurfaced in recent sessions as the near-term driver for crude prices, with tensions between the US and Venezuela rising and a potential escalation between Israel and Iran. However, a lack of updates throughout the APAC session has led to a muted start to Tuesday’s session.

Spot XAU has followed on from Monday’s trend, peaking just shy of USD 4500/oz as the European morning gets underway, with rising geopolitical tensions acting as a new driver for the yellow metal. The recent US-Venezuela developments, specifically the blockaded oil tankers, have urged investors to look for safer places to place their investments.

3M LME Copper traded muted in a tight c. USD 60/t band throughout APAC trade, seemingly not benefiting from the further extension in gold and silver prices. As the European session gets underway, the red metal lifted as the positive risk tone in equities fed through into copper. Thus far, 3M LME Copper trades just shy of the ATH formed in Monday’s session, currently at USD 11.98k/t.

China crude steel output in November 69.6mln tonnes, -10.9% Y/Y; global crude steel output in November 140.1mln tonnes, -4.6% Y/Y, via WorldSteel.

Thai Central Bank Chief said there will be a set maximum trading volumes per major gold trader.

Thailand’s Finance Minister is looking to implement a tax on gold trading online.

Geopolitics

Russia’s Ryabkov said Russia and US held new round of talks on ‘Irritants’; main issues remain unresolved, via IFX. New round of contacts may take place in early spring.

Polish Armed Forces said they have scrambled jets following Russian strikes on Ukraine.

Russia is again attacking Ukraine’s energy infrastructure, according to Ukraine’s energy ministry.

Russia conducts airstrikes on Ukrainian capital Kyiv, according to Ukraine’s military.

Ukrainian President Zelensky said “Negotiations to end the war are “close to achieving a result”, according to Sky News Arabia.

Russia’s Kremlin states Ukraine peace talks over the weekend did not achieve breakthrough.

Russia needs to understand to what extent the US work with Ukraine and Europe on peace plan corresponds to spirit of earlier Putin-Trump Alaska summit, via TASS.

Odesa regional governor said Russian forces launch new evening drone attack on Ukraine’s Odesa, damaging port facilities and civilian ship.

“Israel’s Channel 12: Israel fears miscalculation with Iran, assures Washington that it will not take risks”, via Sky News Arabia.

US Event Calendar

8:30 am: US Oct. Durable Goods Orders, est. -1.5%, prior 0.5%

8:30 am: US 3Q GDP Annualized QoQ, est. 3.2%, prior 3.8%

8:30: US 3Q GDP Price Index, est. 2.7%, prior 2.1%

8:30 am: US 3Q Personal Consumption, est. 2.7%, prior 2.5%

10 am: US Dec. Richmond Fed Index, est. -10, prior -1

DB’s Jim Reid concludes the overnight wrap

This is the last EMR of 2025, before we resume normal service again on January 2. Many thanks for reading and for your interactions this year and wishing you all a Merry Christmas and a Happy New Year.

Markets broadly saw another risk-on move yesterday, with the S&P 500 (+0.64%) posting a third consecutive gain that left the index less than half a percent beneath its record high. However, the global bond sell-off showed few signs of relenting either, with yields reaching new milestones across several countries. The biggest story was undoubtedly the Japanese move, where the 10yr yield (+6.2bps) closed at 2.07% yesterday, the highest since 1999. But that was echoed around the world and yesterday saw 10yr bund yields (+0.2bps) inch above their March peak to close at 2.90%, marking their highest level since October 2023. That ratchet higher for yields is a significant story given that the fiscal picture is likely to remain a big theme in 2026, with many countries running budget deficits on a scale that’s rare outside of wars or major recessions.

As a reminder on Japan, yields increased sharply after the Bank of Japan’s 25bp rate hike on Friday morning, given they signalled that more rate hikes were still to come. Interestingly though, we then saw a decent bout of FX weakness, which in turn led to uncertainty about even more hikes, given the potential need to offset that inflationary impulse. However, that FX weakness began to stabilise yesterday, as finance minister Satsuki Katayama said in a Bloomberg interview yesterday that Japan had a “free hand” to take action in the FX markets, and that “The moves were clearly not in line with fundamentals but rather speculative”. So the yen strengthened after those headlines came out and was up +0.44% against the US dollar yesterday, and this morning it’s the top-performing G10 currency, strengthening a further +0.66% against the US dollar. Our FX strategist Mallika Sachdeva has written more about what happens now in Japan and she says that it makes sense for policymakers to look for measures to stabilise FX

This morning, we’ve seen some of those bond moves begin to ease as well, with yields on 10yr Japanese (-4.4bps) and Australian (-3.2bps) yields coming down, alongside those on 10yr Treasuries (-0.8bps). That comes as Japan’s PM Takaichi said in an interview today that she wouldn’t implement “irresponsible” tax cuts. Meanwhile, there’ve been further equity gains across Asia, with the CSI 300 (+0.51%), the Shanghai Comp (+0.34%) the Hang Seng (+0.18%) and the KOSPI (+0.30%) all advancing. The one exception has been the Nikkei (-0.27%) amidst an underperformance from tech stocks, but other Japanese indices like the TOPIX (+0.19%) are still higher this morning.

Otherwise yesterday, the bond sell-off was a big story outside of Japan too. For instance, in Europe 10yr bund yields (+0.2bps) hit their highest since October 2023 at 2.90%, taking them above their peak in March shortly after the fiscal stimulus announcements. They had been even higher at the intraday peak, but that was pared back after we heard from Isabel Schnabel of the ECB’s Executive Board. She said that “At the moment, no interest-rate increase is to be expected in the foreseeable future”. That was significant, because it was Ms. Schnabel who’d said earlier this month that she was “rather comfortable” with expectations about the next move being a hike, which led investors to price in a growing probability that would happen as soon as 2026. But after the latest interview, investors dialled back the likelihood of a 2026 rate hike even further, and the more policy-sensitive 2yr German yield (-0.6bps) ultimately closed slightly lower.

For US Treasuries, it was mostly a similar story of higher yields yesterday. That came as futures slightly dialled back their expectations for rate cuts next year, now pricing in 58bps by the Dec 2026 meeting, down from 60bps on Friday. In part, that was thanks to the ongoing rebound in oil prices, as that renewed concerns about inflationary pressures, with Brent crude (+2.65%) posting a 4th consecutive increase to $62.07/bbl. And we’d also heard from Cleveland Fed President Hammack over the weekend, who said her base case was that “we can stay here for some period of time until we get clearer evidence that either inflation is coming back down to target, or the employment side is weakening more materially”. So by the close, the 10yr yield (+1.6bps) was up to 4.16%, and notably, the 10yr real yield (+2.5bps) was up to 1.91%, its highest level in 4 months.

Yet despite that rise in nominal and real yields, which normally dampen investor appetite for precious metals that pay no interest, the rally for gold and silver continued to power forward yesterday. By the close, gold (+2.41%) had hit a new record of $4,444/oz, and silver (+2.80%) was also at a new peak of $69.04/oz. Moreover, both have seen further gains this morning, with gold up another +0.78% to $4,478/oz, whilst silver (+0.53%) is up to $69/40/oz. So that now brings their YTD gains to 71% and 140% respectively, which in both cases is their strongest annual performance since 1979.

In the meantime, US equities put in a decent performance as well, with the S&P 500 (+0.64%) back into positive territory for December again. So that currently leaves it on track for an 8th consecutive monthly gain for the first time since January 2018. The advance yesterday was its third consecutive move higher, and it was a broad-based move that saw over three-quarters of the index advance. Moreover, the Magnificent 7 (+0.54%) also posted a third consecutive gain to close just over 1% beneath its own record high. However, in Europe, the picture wasn’t quite as rosy, with the STOXX 600 (-0.13%) posting a modest decline.

Looking forward, today we’ll see the last batch of US data before Christmas. That includes the delayed Q3 GDP print, although that’s backward-looking and covers the period before the shutdown. However, a more recent piece of data will be the Conference Board’s consumer confidence reading for December. Remember that in November, the last reading was the lowest since the Liberation Day turmoil in April, so that will be in the spotlight given the recent downtick in sentiment indicators.

Finally on the day ahead, aside from the Q3 GDP and the Conference Board reading, today’s US data releases include industrial production for November, preliminary durable goods orders for October, and the Richmond Fed’s manufacturing index. Otherwise from central banks, the Bank of Canada will publish their summary of deliberations for the December policy decision.

Tyler Durden

Tue, 12/23/2025 – 08:29

https://www.zerohedge.com/markets/futures-flat-ahead-final-macro-data-dump-2025

ADP Weekly Employment Data Shows Labor Market Rebounding In December

ADP Weekly Employment Data Shows Labor Market Rebounding In December

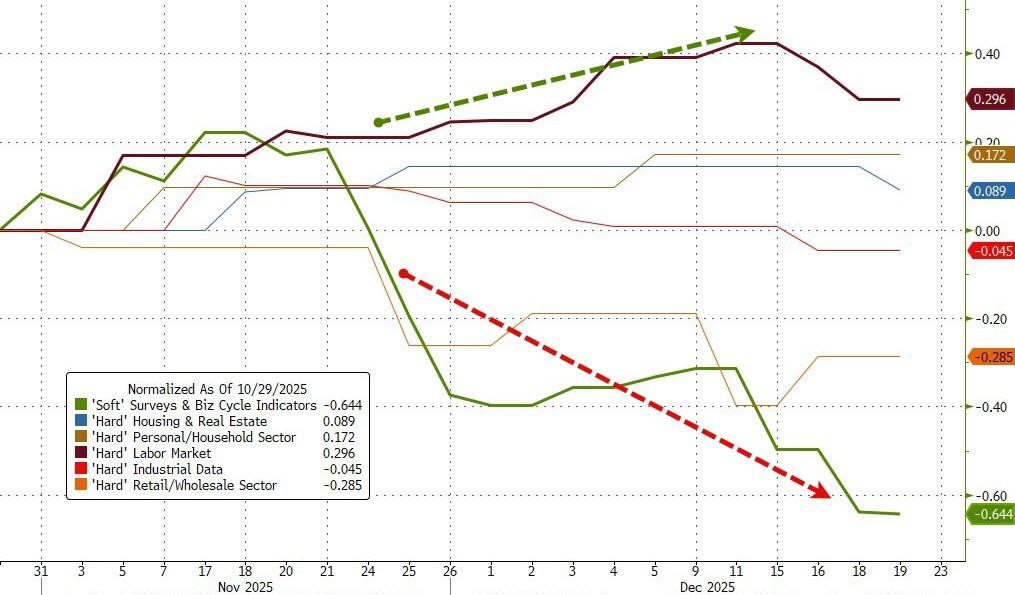

Since the start of the government shutdown, what labor market data indications we got actually surprised to the upside (while soft survey data crashed)…

…but now, as the data starts to re-emerge from its slumber, it remains mixed with jobless claims data remaining solid to say the least while JOLTS leaves questions about the low-hire, low-fire, low-quits economy. If one data set has bee noisy through the past few weeks, it’s ADP (and its new weekly updated prints). Analysts expected a 16.25k average job gain per week over the past four weeks… but the print was just +11.5k (46k on a monthly basis) for the week-ending Dec 6th, with the prior week’s average revised up strongly to +17.5k (+70k monthly).

Source: Bloomberg

That is the third straight week of month-over-month gains for the labor market after a brief slump as the government shutdown started.

Tyler Durden

Tue, 12/23/2025 – 08:22

Medicaid pagó más de $207 millones por personas fallecidas; nueva ley podría solucionarlo

Por FATIMA HUSSEIN

WASHINGTON (AP) — Programas de Medicaid realizaron más de 200 millones de dólares en pagos indebidos a proveedores de atención médica entre 2021 y 2022 para personas que ya habían fallecido, según un nuevo informe del organismo de control independiente del Departamento de Salud y Servicios Humanos.

Sin embargo, la Oficina del Inspector General del departamento expresó que una nueva disposición en el proyecto de impuestos gastos republicano, que requiere que los estados auditen sus listas de beneficiarios de Medicaid, podría ayudar a reducir estos pagos indebidos en el futuro.

Este tipo de pagos indebidos “no es exclusivo de un estado, y el problema sigue siendo persistente”, dijo a a The Associated Press Aner Sanchez, inspector general regional adjunto en la Oficina de Servicios de Auditoría. Sanchez ha estado investigando este problema durante una década.

El informe del organismo de control publicado el martes indicó que se realizaron más de 207,5 millones de dólares en pagos de atención administrada en nombre de inscritos fallecidos entre julio de 2021 y julio de 2022. La oficina recomienda que el gobierno federal comparta más información con los gobiernos estatales para recuperar los pagos incorrectos, incluyendo una base de datos de la Seguridad Social conocida como el Archivo Maestro Completo de Defunciones, que contiene más de 142 millones de registros que se remontan a 1899.

El intercambio de datos del Archivo Maestro Completo de Defunciones ha estado estrictamente restringido debido a las leyes de privacidad que protegen contra el robo de identidad y el fraude.

La ley de impuestos y gastos firmada por el presidente Donald Trump este verano amplía cómo se puede utilizar el Archivo Maestro Completo de Defunciones al exigir a las agencias de Medicaid que auditen trimestralmente sus listas de proveedores y beneficiarios en comparación con el archivo, comenzando en 2027. La intención es detener los pagos a personas fallecidas y mejorar la precisión.

El informe del martes es el primer análisis a nivel nacional de los pagos indebidos de Medicaid. Desde 2016, el inspector general del departamento ha realizado 18 auditorías sobre una selección de programas estatales y ha identificado que las agencias de Medicaid habían realizado pagos de atención administrada de manera indebida en nombre de inscritos fallecidos por un total de aproximadamente 289 millones de dólares.

El gobierno tuvo cierto éxito utilizando el Archivo Maestro Completo de Defunciones para prevenir pagos indebidos a principios de este año. En enero, el Departamento del Tesoro informó que había recuperado más de 31 millones de dólares en pagos federales que se realizaron de manera indebida a personas fallecidas como parte de un programa piloto de cinco meses después de que el Congreso otorgara al Tesoro acceso temporal al archivo por tres años como parte del proyecto de ley de asignaciones de 2021.

Mientras tanto, la agencia de seguridad social ha estado realizando actualizaciones inusuales al archivo en sí, agregando y eliminando registros, lo que complica su uso. Por ejemplo, la administración Trump en abril decidió clasificar a miles de inmigrantes vivos como fallecidos y cancelar sus números de Seguridad Social para tomar medidas contra inmigrantes que habían sido temporalmente autorizados a vivir en Estados Unidos bajo programas iniciados durante la administración Biden.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

Greta Thunberg detenida en Londres mientras apoya a activistas propalestinos en huelga de hambre

Por DANICA KIRKA

LONDRES (AP) — Greta Thunberg fue arrestada en el centro de Londres el martes mientras apoyaba a activistas propalestinos que están llevando a cabo una huelga de hambre para protestar por su encarcelamiento mientras esperan juicio por cargos relacionados con una serie de manifestaciones anteriores.

El grupo de protesta Prisoners for Palestine compartió un video que muestra a la sueca de 22 años sosteniendo un cartel en apoyo a los detenidos y su organización, conocida como Palestine Action. El gobierno británico prohibió a principios de este año a Palestine Action como una organización terrorista.

Las protestas fueron parte de una manifestación más amplia en la que otros dos activistas rociaron pintura roja frente a una compañía de seguros en el área del centro de Londres conocida como el centro de la industria de servicios financieros de Gran Bretaña. Prisoners for Palestine dice que apuntaron a la aseguradora porque apoya a Elbit Systems, una empresa de defensa vinculada a Israel.

La policía informó que un hombre y una mujer han sido arrestados bajo sospecha de daño criminal. Una tercera mujer fue arrestada posteriormente bajo sospecha de apoyar a una organización prohibida. La policía británica generalmente no identifica a los sospechosos por sus nombres antes de que se les presenten cargos.

Ocho miembros de Palestine Action han llevado a cabo una huelga de hambre para protestar por su detención sin fianza mientras esperan juicio por una variedad de cargos relacionados con protestas anteriores en todo el país.

Los dos primeros prisioneros en unirse a la protesta han estado en huelga de hambre durante 52 días y se encuentran en una “etapa crítica, donde la muerte es una posibilidad real”, dijo Prisoners for Palestine en un comunicado.

El gobierno británico se ha negado hasta ahora a intervenir en el proceso judicial, afirmando que las cuestiones sobre la fianza y la detención son asuntos que deben decidir los tribunales.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

The Challenge For 2026 Markets

The Challenge For 2026 Markets

Authored by Lance Roberts via RealInvestmentAdvice.com,

It’s that time of year when Wall Street polishes up its crystal balls and begins predicting returns for 2026. Since Wall Street never predicts a down year, which would be unwise for fee-based product revenues, these forecasts are often inaccurate and sometimes significantly wrong. Let’s review some previous years. For example, on December 7th, 2021, we wrote an article about the predictions for 2022.

“There is one thing about Goldman Sachs that is always consistent; they are ‘bullish.’ Of course, given that the market is positive more often than negative, it ‘pays’ to be bullish when your company sells products to hungry investors. It is important to remember that Goldman Sachs was wrong when it was most important, particularly in 2000 and 2008. However, in keeping with its traditional bullishness, Goldman’s chief equity strategist David Kostin forecasted the S&P 500 will climb by 9% to 5100 at year-end 2022. As he notes, such will “reflect a prospective total return of 10% including dividends.”

The problem, of course, is that the S&P 500 did NOT end the year at 5100.

Then, in 2022, Wall Street predicted a modest return of just 3.9% for 2023.

Of course, reality turned out to be markedly different.

The same trend was observed in 2023, 2024, and 2025 as Wall Street grossly underestimated the forward market return. Heading into 2025, Wall Street predicted a median return of just 8.2% with the highest estimate of nearly 15%. As we wrap up the year, the market is again closing in on a 20% return, marking the third consecutive year of such performance.

However, while analysts repeatedly fail at the guessing game, Wall Street’s annual tradition is always of higher returns. To borrow a quote:

“(Market) Predictions Are Difficult…Especially When They Are About The Future” – Niels Bohr

Okay, I took a little poetic license, but the point is that while we try, predicting the future is difficult at best and impossible at worst. If we could accurately predict the future, fortune tellers would win all the lotteries, psychics would be more prosperous than Elon Musk, and portfolio managers would always beat the index.

However, this is never the case, and as investors, we must rely on our data, analyze past events, filter out the current noise, and discern possible future outcomes. The biggest problem with Wall Street today and in the past is its consistent disregard for the unexpected and random events that inevitably occur, like the “Liberation Day” tariff event that sent the market plunging by nearly 20%. However, even when such events occur frequently, from trade wars to Brexit to Fed policy and a global pandemic, Wall Street analysts were often convinced that such things would not happen.

So what about 2026? We have some early indications of Wall Street targets for the S&P 500 index, and, as is always the case, they are primarily optimistic for the coming year. The median estimate for 2026 is for the market to rise to 7500 next year, which would be a disappointing return of just 9.3% after three years of 20% gains. However, the high estimate from Deutsche Bank suggests a 15% return, while the low estimate from BofA is just 4%. Notably, not one firm forecasts a negative return.

There are several risks to these forecasts.

The Challenge For 2026

As of this writing, the market appears poised to close the year above 6,800. That’s roughly a 17% percent gain for the year based on price appreciation. That advance was a combination of AI-fueled enthusiasm, softening inflation, and hopes of Fed rate cuts and increased liquidity. However, under the surface, the setup for 2026 looks increasingly fragile. Valuations are stretched, expectations are optimistic, and earnings have little room for error.

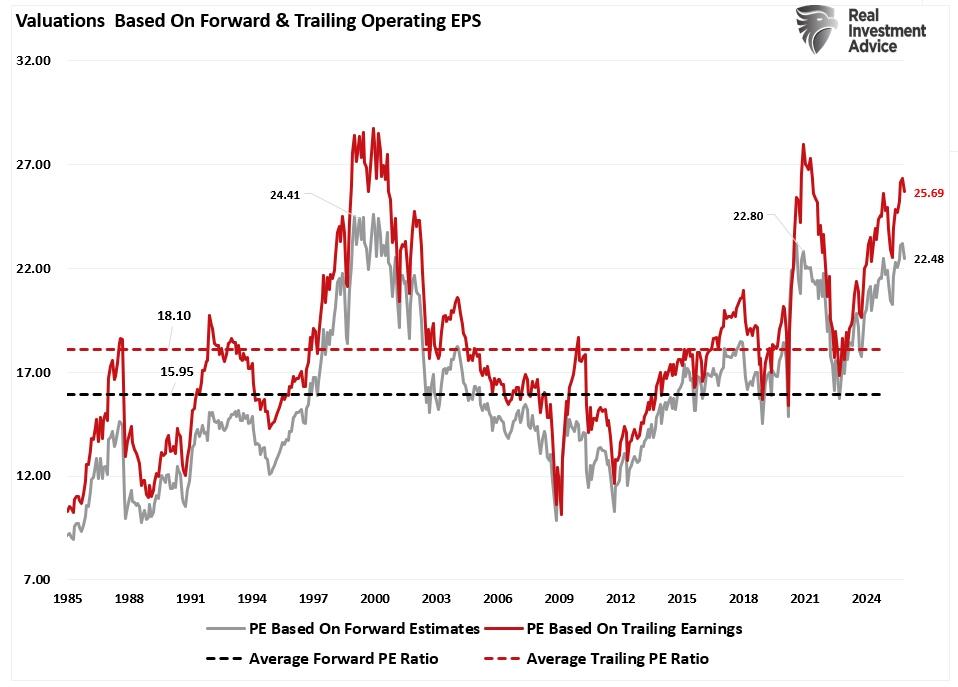

Let’s start with the data. The current trailing twelve-month price-to-earnings ratio sits at 26, near historic extremes. The Shiller CAPE ratio, which adjusts for inflation and smooths cycles over a decade, stands near 39. Forward P/E estimates for 2026 earnings are in the 23 range. By almost every measure, equities are priced at levels that historically limit future returns.

However, this also presents a risk that investors need to be prepared for. At current valuation levels, stocks don’t need a crisis to fall; they only need disappointment. If growth falls short, or if the Fed doesn’t deliver the cuts the market expects, equities face pressure. In other words, a “recession” is not the risk; it is just anything that is “less than perfect.”

Wall Street, of course, is bullish. That’s the default setting. Morgan Stanley is calling for a 14 percent gain. Goldman Sachs projects double-digit earnings growth. Deutsche Bank has a target of 8,000 for the S&P 500. But look closer. These forecasts assume strong profit growth, stable inflation, and rate cuts starting in mid-2026, which is a very tight window.

However, investors have heard this before, but have also seen what happens when markets get ahead of reality. That leaves the setup for 2026 a little less bullish, as elevated expectations and high valuations leave minimal margin for error.

Valuation Math: What the Numbers Suggest for 2026

To make sense of where the S&P 500 could go in 2026, we don’t need a prediction, just a calculator. Rather than guessing, we prefer to let “valuations do the talking.” The reason is that valuations represent investor sentiment based on the outlook for earnings growth. If forward earnings growth is strong, investors can overpay for equities today, anticipating that earnings will justify the overpayment. However, if earnings expectations start to fall, investors will reprice the markets for lower premiums.

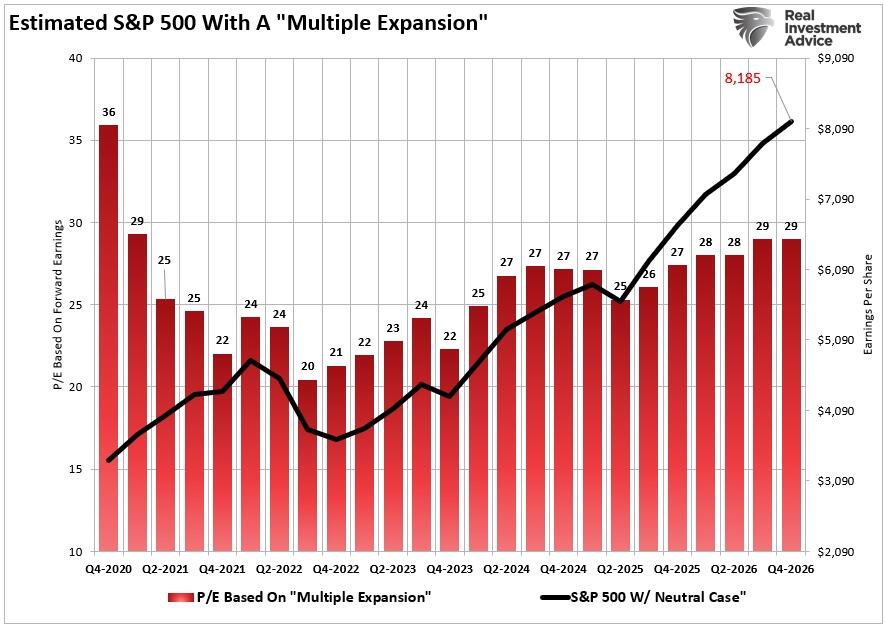

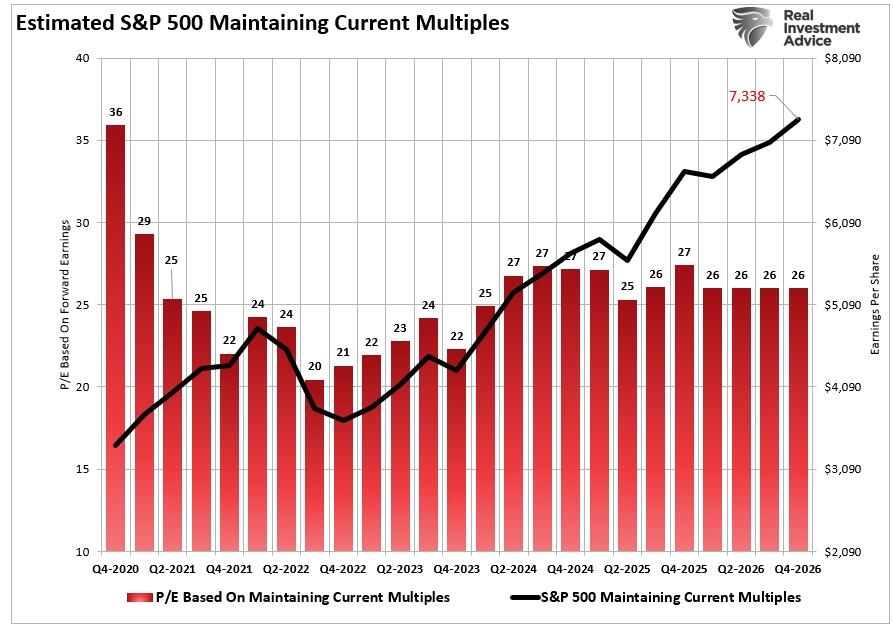

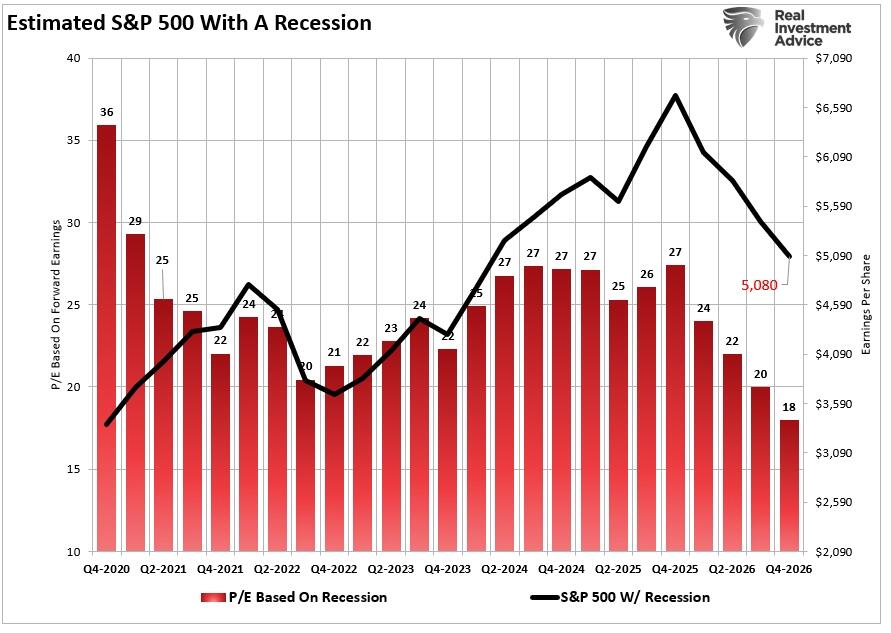

As shown below, we ran multiple scenarios based on forward earnings estimates, valuation ranges, and historical outcomes. The S&P 500 begins the year near 6,900, our base case, and from there, outcomes depend on whether multiples expand, hold, or contract. For the earnings analysis, we are using S&P Global’s forward 2026 reported earnings per share estimate of $282, which will likely be the high-water mark for 2026. Therefore, we will assume that these estimates are accurate, and we can then incorporate valuation multiples and predict forward market returns.

Here are the scenarios, based on $282 per share: (Note: There are an infinite number of possibilities that could occur in 2026. The point of the following discussion is to understand the math of valuations as it relates to market risk next year.)

Optimistic Case (Multiple Expansion): Bullish investor sentiment persists, and risk-taking intensifies, resulting in a multiple expansion to 29x. Such a prediction would suggest a figure close to Deutsche Bank’s current 2026 estimate of 8,000 as a year-end target. As shown, at 29 times earnings, the year target would be $ 8,185, or a roughly 18% gain.

Neutral Case (Maintain Current Multiples): This scenario assumes that, while the bullish market persists, concerns over monetary policy, inflation, or earnings growth rates will keep multiples stable at 26x forward earnings. Such a scenario would allow the index to rise to 7,338, representing a more historically normal 6% gain in 2026. Such a muted return will be very disappointing after three years of nearly 20% gains.

Slow-Down Case: If we assume an economic slowdown that impacts forward earnings expectations, such a scenario would potentially lead to a reversion in valuations toward its 5-year average of 22x. Such a decline would likely result in a market value of 6,209, or a negative return of approximately 10%.

Recession Case: The most likely worst-case outcome, barring a financial or credit-related event next year, is the onset of a mild recession. While such an event is likely a low-probability occurrence in 2026, a scenario like this would likely lead to more severe earnings disappointment and market repricing. If such were to occur, a valuation contraction toward 18 times earnings is possible, with a price decline in the index towards 5080, taking markets back to the 2021 peak, or a 26% correction.

Notice this: even a mild reversion in valuations creates downside. If earnings flatten and multiples fall to 20, that’s enough to limit or erase gains. If both earnings and valuations fall short, returns turn negative fast. This makes managing risk less simple in 2026. While high valuations reduce forward returns, they do not guarantee losses. However, high valuations leave “no cushion” if things go sideways.

This is not a time for aggressive positioning. It’s a time to respect the math.

Risk Factors: What Could Go Wrong in 2026

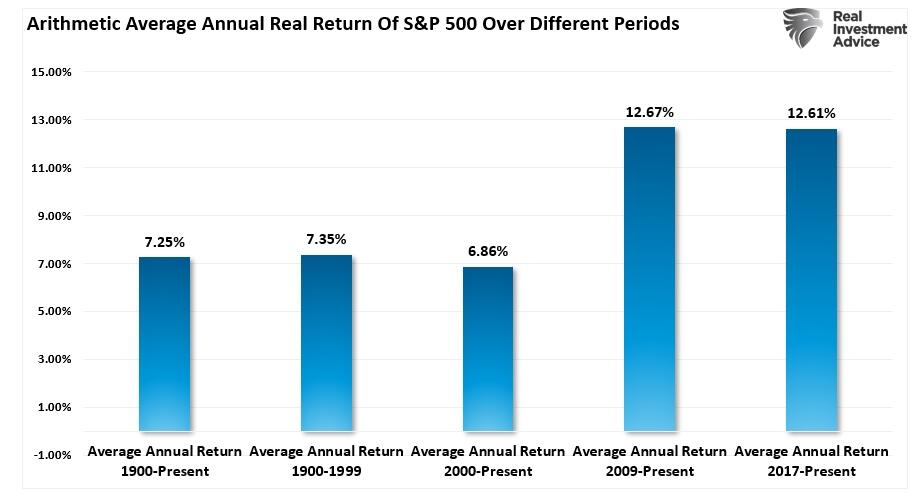

Markets don’t move in straight lines. The problem with 2026 isn’t a forecast. It’s the imbalance between expectations and risk. Everything must go right for stocks to deliver strong returns from current levels. But there’s plenty that could go wrong. As shown in the table below, since 2009, investors have enjoyed annualized real returns in the market that are 50% higher than the historic returns from 1900 to the present. Those returns were a function of near-zero interest rates, massive liquidity injections, and a valuation reversion following the 2008 crisis. None of those supports is currently available as we head into 2026.

Here is another risk. The current 3-year return is 18% above its 3-year average. While that is not the highest level on record, when the index trades significantly above its moving average, volatility tends to rise. These periods often see sharp drawdowns, and corrections become more frequent, with increased variance in returns leading to larger losses in downturns, which compounds the problem. Secondly, there are declining risk-adjusted returns. When returns deviate significantly from the trend, future returns tend to revert toward the mean. This mean reversion is driven by stretched valuations resetting. Over time, high volatility and large price swings reduce compound returns. Even if average returns remain positive, the math of compounding is compromised by losses, weakening full-cycle gains.

Secondly, the economy is forecasted to grow around 2 percent, but there are signs of slowing. With consumer debt levels rising, delinquency rates on credit cards and auto loans inching higher, and student loan repayments resuming, those factors weigh on discretionary spending.

Third, while the Fed is cutting rates, investors have already priced those cuts into the market. However, inflation remains sticky, wage growth is still elevated, and jobless claims remain near lows. As such, if the Fed hesitates or signals fewer cuts, this could pressure valuation multiples, especially for growth stocks.

Fourth, consensus earnings remain extremely optimistic in relation to expectations for economic growth and inflation. That requires strong margins, global stability, and continued AI-driven demand. If any of these falter, earnings estimates will fall, and investors will reprice markets for lower multiples.

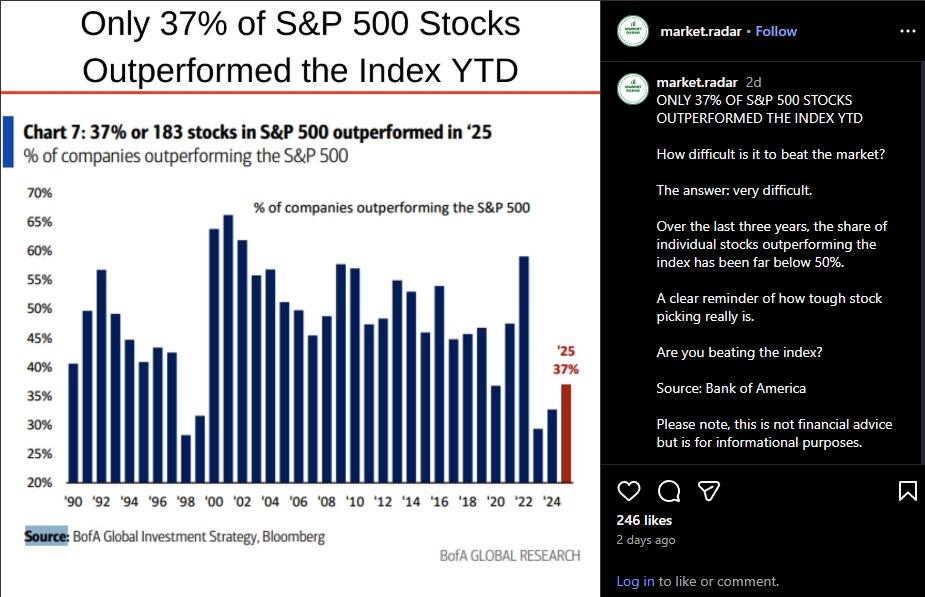

Finally, the 2025 rally was led by a small group of stocks with only about 37% of all issues outperforming the index. If leadership narrows or stalls, the index could struggle even if broader conditions remain stable.

Investors should also watch geopolitical risk. U.S. midterm elections, global conflict, or supply chain issues could disrupt assumptions; however, these are secondary concerns. The core issue remains earnings versus valuation. The higher the price you pay, the smaller the margin for error.

While this market is priced for a smooth glide path, the odds of turbulence are rising.

Strategy: What Investors Should Do Next

The playbook for 2026 isn’t about guessing market direction. It’s about managing risk, and understanding that with valuations high, earnings uncertain, and monetary policy in transition, your best move is preparation, not prediction.

The chart below combines the four potential predictions to show the possible market range for next year. Of course, you can analyze, make valuation assumptions, and derive your targets for next year based on your views. This analysis is an exercise in logic to develop a range of possibilities and probabilities over the next 12 months.

Valuations matter. At this stage of the cycle, you need to be more cautious—not more aggressive. Here’s how to position:

Lower your return expectations. If you’re assuming another 15 to 20 percent gain next year, you’re betting against the data. Valuation history suggests forward returns will be lower, especially if earnings growth slows. A more reasonable expectation is mid-single-digit returns, with higher volatility.

Reduce exposure to sectors with extreme valuations. AI might be real, but prices already assume perfection. Don’t abandon growth, but rotate toward quality. Look for companies with real cash flow, low leverage, and strong pricing power.

Focus on quality. Companies with strong cash flow, low debt, and pricing power are likely to outperform in slower-growth environments.

Increase Fixed Income. High-quality fixed income will shield portfolios against increased market volatility.

Hold some cash. Not because you’re timing the market, but because flexibility matters. If volatility spikes, you want dry powder. That also gives you a chance to buy quality at a discount if the market pulls back.

Most importantly, stop chasing narratives. AI is real, but that doesn’t make every AI stock a buy. The same goes for the “soft landing” story. Focus on the numbers. Stick with fundamentals.

In 2026, outcomes will depend on earnings, inflation, and the actions of the Fed. However, your results will vary based on your risk-management discipline, allocations, and portfolio structure. As such, it is important not to overreach, not to assume past returns will repeat, and to respect valuations.

That’s how you protect capital, and ultimately stay in the game when others can’t.

Tyler Durden

Tue, 12/23/2025 – 08:05

President Unveils ‘Trump Class’ Of Warships, Huntington Ingalls Shares Jump

President Unveils ‘Trump Class’ Of Warships, Huntington Ingalls Shares Jump

Shares of warship builder Huntington Ingalls Industries rose in premarket trading and are on track for the largest annual gain in 12 years, driven by news of President Trump’s continued push to rebuild the U.S. Navy.

HII gained 5% on Monday and another 5% in premarket trading early Tuesday after President Trump announced a plan on Monday evening to build two new “Trump-class” battleships, to acquire 20-25 of these ships in the coming years.

Here are critical details about Trump’s major announcement Monday evening (courtsey of Goldman analyst Noah Poponak):

Trump-class battleships. On December 22, 2025 President Trump announced that he had approved a plan for the U.S. Navy to build two new “Trump-class” battleships, with the goal of acquiring 20-25 of these ships in the coming years. In his address, the President noted these 30,000-40,000 ton ships will carry a large quantity of missiles, including hypersonic missiles, and will also be outfitted with electromagnetic rail guns and directed energy lasers. Trump-class battleships will also carry nuclear-armed sea launched cruise missiles (currently under development) adding an additional element of nuclear deterrence to the Navy. Trump-class destroyers appear to be designed as the center of enhanced command and control networks at sea, as the Navy looks to field more autonomous assets and traditional vessels in the coming years. The WSJ has reported that the U.S. Navy will launch a vendor competition, with plans to procure the first hull in 2030.

Poponak told clients that his 12-month price target for HII was upgraded to $384 from $356.

This year, HII shares are up a whopping 87%, the largest annual increase since the 107% increase in 2013.

Shares are at record high levels.

The S&P 500 Aerospace & Defense Index nears record highs.

Secretary of the Navy John Phelan recently said that the U.S. military will be acquiring a “new frigate class based on HII’s Legend-Class National Security Cutter design.”

Earlier this year, HII stock had one of the largest intraday gains on record as Trump touted his move to revitalize domestic shipbuilders.

All of this plays into the total reposturing of the U.S. military to focus on Western hemispheric defense and securing the hemisphere ahead of the 2030s. We’ve outlined how to profit from this (read here).

Tyler Durden

Tue, 12/23/2025 – 07:45

https://www.zerohedge.com/military/huntington-ingalls-industries-jumps-trump-class-warships

Japón supera obstáculo para reiniciar mayor planta nuclear del mundo

TOKIO (AP) — El gobernador de una provincia japonesa dio formalmente el martes su consentimiento local para reactivar dos reactores en la planta nuclear de Kashiwazaki-Kariwa, superando el último obstáculo para reiniciar la planta que ha estado inactiva durante más de una década tras los colapsos de 2011 en otra planta gestionada por la misma empresa.

Hideyo Hanazumi, gobernador de Niigata, dio formalmente su aprobación.

En su reunión con el ministro de Economía e Industria Ryosei Akazawa, transmitió el “respaldo” de la prefectura para reiniciar los reactores 6 y 7 en la planta de Kashiwazaki-Kariwa, aceptando la promesa del gobierno de garantizar la seguridad, la respuesta ante emergencias y la comprensión de los residentes.

Los preparativos para el reinicio del reactor 6 han avanzado y se espera que la empresa de servicios públicos TEPCO solicite una inspección de seguridad final por parte de la Autoridad de Seguridad Nuclear a finales de esta semana, antes de una posible reanudación en enero. El trabajo en el otro reactor tomará algunos años más.

El movimiento se produce un día después de que la asamblea prefectural de Niigata adoptara una ley de presupuesto que incluía los fondos necesarios para un reinicio, apoyando el consentimiento previo del gobernador.

“Fue una decisión pesada y difícil”, dijo Hanazumi a los periodistas.

Hanazumi también se reunió con la primera ministra Sanae Takaichi, quien también apoya la energía nuclear, y le pidió que visitara la planta para observar la seguridad.

Japón una vez planeó eliminar gradualmente la energía atómica tras el desastre en la planta de Fukushima causado por un terremoto y un tsunami. Pero ante la escasez global de combustible, el aumento de precios y la presión para reducir las emisiones de carbono, el gobierno ha revertido su política y ahora busca aumentar el uso de energía nuclear acelerando los reinicios de reactores, extendiendo su vida útil operativa y considerando la construcción de nuevos.

De los 57 reactores comerciales, 13 están actualmente en operación, 20 están fuera de servicio y otros 24 están siendo desmantelados, según las autoridades nucleares.

La planta de Kashiwazaki-Kariwa, que comprende siete reactores, es la más grande del mundo. La planta ha estado fuera de servicio desde 2012 como parte de los cierres de reactores a nivel nacional en respuesta a los colapsos de marzo de 2011 en la planta Fukushima Daiichi de TEPCO.

Los reactores 6 y 7 en Kashiwazaki-Kariwa habían superado las pruebas de seguridad en 2017, pero sus preparativos de reinicio se suspendieron después de que se encontraran una serie de problemas en 2021. La Autoridad de Regulación Nuclear levantó una prohibición operativa en la planta en 2023.

Su reanudación nuevamente enfrentó incertidumbre tras el terremoto del 1 de enero de 2024 en la cercana región de Noto, que reavivó las preocupaciones entre los residentes locales sobre la planta y la evacuación en caso de un desastre mayor. El Ministerio de Industria buscó una aprobación temprana de reanudación de Niigata dos meses después.

En Japón, el reinicio de un reactor está sujeto al consentimiento de la comunidad local.

TEPCO, fuertemente cargada con el creciente costo de décadas de desmantelamiento y compensación para los residentes afectados por el desastre de Fukushima, ha estado ansiosa por reanudar su única planta nuclear operativa para mejorar su negocio. TEPCO ha estado luchando por recuperar la confianza pública en la operación de una planta nuclear.

Además de la seguridad de la planta, los expertos dicen que la aceleración de los reinicios de reactores también genera preocupación en un país sin un reprocesamiento completo de combustible nuclear o planes para la gestión de desechos radiactivos.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}