Category: News

Futures Slide As Oil Jumps On Ceasefire Setbacks, Nasdaq In Danger Of Ending 13-Day Streak

Futures Slide As Oil Jumps On Ceasefire Setbacks, Nasdaq In Danger Of Ending 13-Day Streak

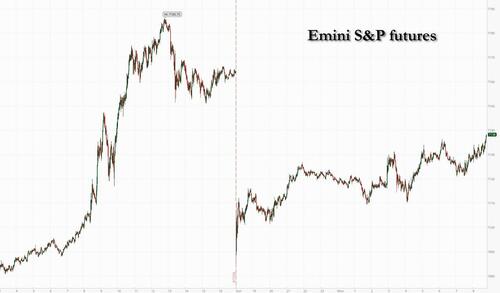

Futures are lower, but well off session lows,after a weekend of chaos in the Strait of Hormuz cast doubt over US-Iran peace talks ahead of Tuesday’s ceasefire expiration. On Saturday, Iran said the Strait will be closed until the US blockade is lifted, with ships reporting attacks. The US then fired and seized an Iranian-flagged ship on Sunday. Both headlines point to a re-escalation, as Iran military has now vowed to retaliate. It remains unclear whether the peace talks will continue ahead of the April 22nd deadline: POLITICO yesterday reported that Trump will continue peace talks with Iran in Pakistan on Monday, while Iran said in a news conference that they have “no plan” for next round of negotiation (here), although subsequent reports from AP indicated the opposite. There’s a big earnings week ahead, and top Wall Street strategists expect resilient numbers to support equities. As of 8:00am ET, S&P futures are down 0.5% following a succession of record highs; the Nasdaq is down 0.4% and set to end a near-record stretch of 13 consecutive gains. Pre-market, Mag 7 are all lower with NVDA (-1.2%), MSFT (-1.0%) and META (-1.0%) being the notable laggards. European stocks slid 1.1% while Asian stocks rose in a delayed catch up to the Friday melt up in the US. Bond yields rose sharply in Europe, whereas the moves in Treasuries were more modest. The dollar was little changed, erasing an earlier gain. WTI crude oil jumped $4.6 (or 5.5%) to $88.5; both base metals and precious metals are lower with gold briefly dropping below $4,800 an ounce, before recovering. The US session is quiet for scheduled data, while Fed’s external communications blackout period has now begun ahead of the April 29 policy announcement.

In premarket trading, Mag 7 stocks were mostly lower (Apple unchanged, Tesla -0.7%, Alphabet -1%, Amazon -1%, Meta -0.9%, Microsoft -0.8%, Nvidia -0.9%)

Airlines and cruise operators are down as the prospects of fuel prices staying at elevated levels weigh on sentiment. American Airlines (AAL) -3%, Carnival (CCL) -2%.

Energy stocks are rising as US-Iran tensions flare up over the weekend. Chevron (CVX) +1%.

Psychedelic-related stocks rally after President Donald Trump signed an executive order to expedite research and access to the substances used outside the US to treat post-traumatic stress disorder. AtaiBeckley (ATAI) +27%.

AST SpaceMobile (ASTS) drops 14% after Blue Origin’s flagship New Glenn rocket failed to correctly place a satellite made by the Texas-based company in its intended orbit.

Avis Budget (CAR) drops 2% as Barclays downgrades to underweight following the stock’s near-vertical recent rally.

Fermi Inc. (FRMI) falls 19% after the power company said its chief executive officer and chief financial officers have stepped down as the firm tries to secure its first customer.

Marvell Technology (MRVL) rises 5% after the Information reported that Google is in discussions with the semiconductor company to develop two new chips to run AI models more efficiently.

TopBuild Corp. (BLD) rises 18% after QXO Inc. said it’s acquiring the insulation company for about $17 billion. The acquisition will make QXO the second-largest publicly traded building products distributor in North America.

USA Rare Earth (USAR) gains 4% after agreeing to acquire Brazil’s Serra Verde Group in a cash-and-stock transaction, adding to a string of recent deals in the industry.

In other corporate news, regulators across Asia are stepping up scrutiny of cybersecurity risks in their financial systems, as concerns over Anthropic PBC’s latest AI model Mythos spread. Blue Origin’s flagship New Glenn rocket launched to space on its third flight, reusing a booster for the first time but failing to correctly place the satellite it was carrying into its intended orbit. In deals, American Airlines said it’s not engaged with or interested in any discussions regarding a merger with United Airlines. QXO said it’s acquiring insulation firm TopBuild for about $17 billion, making it the second-largest publicly traded building products distributor in North America. Patrick Industries and rival recreational-vehicle supplier LCI Industries are in talks to combine.

Monday’s risk-off moves are denting a rally that had erased all of the war-driven losses in US stocks. President Donald Trump and Iranian officials offered disparate views on the next stage of the war, leaving it unclear whether the sides would meet for talks on Tuesday, with a truce set to expire shortly. Sentiment was dented after oil and natural gas prices jumped as Hormuz remained closed early Monday. Iran initially said ships could pass before abruptly stopping traffic less than 24 hours later, while the US Navy fired upon and boarded an Iranian-flagged cargo ship in the Gulf of Oman. The energy crisis is rippling out in various ways. The WSJ reported that the UAE is said to be in talks with the US about a financial backstop in case the Iran war plunges the country into further crisis. The EU is planning to propose measures to “optimize” jet fuel distribution among member states, while China is becoming more dependent on the US for ethane gas. And traders are reassessing their playbooks as the war forces governments to become more self reliant.

Traders believe pressure on both parties to reach a deal remains high, even as volatility during negotiations is likely to be elevated. Iran’s state-run news agency cited President Masoud Pezeshkian as saying the war was in no one’s interest and that diplomatic avenues should be used to lower tensions.

“While the developments from the weekend certainly cooled the optimism, it did not derail it completely,” said Stephan Kemper, chief investment strategist at BNP Paribas Wealth Management. “Markets keep expecting a near-term solution which will allow energy to flow again.”

Technology stocks took a breather on Monday after the sector drove much of the rebound in US equities, with the Magnificent Seven up 20% since the US benchmark hit its 2026 bottom on March 30. Despite the re-escalation in the Middle East, top strategists say the market can keep rallying despite the turmoil. JPMorgan’s Mislav Matejka disagrees with bearish views that revolve around stagflation and expects resilient earnings to keep supporting the market. Ben Snider at Goldman Sachs says strong but narrow positive earnings revisions support a narrow market rally, while Morgan Stanley’s Mike Wilson notes that early 1Q results have been strong and the earnings recovery is intact.

The earnings season, meanwhile, has been off to a strong start. S&P 500 companies that have pusblished their results so far have seen their profits come in 11% above expectations, on aggregate, data compiled by Bloomberg Intelligence showed. Major companies releasing earnings this week include Tesla Inc. and Boeing Co. on Wednesday, followed by Intel Corp. the following day. The economic impact of seven weeks of war in the Middle East will also begin to emerge this week when purchasing manager indexes are published Thursday. “Earnings season is supportive and does matter, but the dominant driver is geopolitics. Once a deal is reached, attention will shift back to earnings,” said Patrik Lang, chief investment strategist at Global Gate Asset Management. “The strength may be somewhat concentrated, as much of the growth continues to come from the Magnificent Seven.”

While the situation in the Middle East remains in flux, traders will also focus on Kevin Warsh’s Senate confirmation hearing this week to lead the Federal Reserve. The US two-year yield is once again below the central bank’s 3.75% ceiling after trading above the level for much of the war.

Besides Warsh’s Tuesday Senate confirmation hearing, in economic data, March retail sales are due Tuesday, with economists projecting a sizable jump in overall retail sales mainly due to sharply increased spending on gasoline. PPI is due on Thursday, followed by the University of Michigan’s final consumer sentiment index for April on Fridat. The preliminary reading set a record low.

The jump in energy prices hit Europe, where the Stoxx 600 falls 1%. Airlines are the biggest losers and cyclical shares such as autos, banks and consumer products are also among notable laggards. The energy sector is outperforming. Here are some of the biggest movers on Monday:

Wacker Chemie advances as much as 2.5% after the company’s preliminary first-quarter Ebitda came in 18% ahead of consensus expectations.

Stocks related to photonics technology for AI data centers soared on Monday, with Soitec and Riber in France and UK-listed IQE up more than 10%, as a rally in the sector extended further.

Renishaw shares rise as much as 9.7% as the UK industrial instrumentation company lifts its full-year revenue and pre-tax profit guidance.

Plus500 shares rise as much as 4% after the trading platform said annual revenue and earnings should come in ahead of current expectations.

Advanced Medical Solutions shares rally as much as 19% after the maker of surgical and wound care products confirmed it is in discussions with TA Associates regarding a possible takeover offer.

Sanofi shares fall as much as 2.2% as BNP Paribas downgrades the French pharmaceutical stock to neutral from outperform on revised pipeline assumptions.

Loomis shares fall as much as 7.3% after Goldman Sachs cut its recommendation to neutral from buy, saying that while good growth and profits are expected to continue in the near term, it is mostly priced into the market.

Odfjell Drilling shares drop as much as 7.3% after the company halted production at its Deepsea Atlantic facility following an incident where the rig’s blowout preventer fell to the seabed at an approximate depth of 1,100 meters.

Earlier in the session, Asian stocks rose as investors shrugged off heightened tensions between the US and Iran to focus on prospects for further talks down the road, as well as strong local tech earnings. The MSCI Asia Pacific Index rose as much as 0.8% before paring most of its advance. SK Hynix and Tencent were among the top positive contributors. Stocks in Hong Kong led gains in the region, while South Korean shares erased their Iran war losses. While weekend hostilities cast doubt on when another round of Middle East negotiations may take place, risk sentiment has rebounded over the past couple of weeks. Earnings from Korean memory chipmaker SK Hynix due Thursday are among key upcoming catalysts for the tech trade. As global gauges rebound and touch new highs one by one, however, some investors are cautious about being too optimistic.

“The clock is ticking, and it’s still unclear whether this relief rally has legs or if it’s simply a dead‑cat bounce,” said Sophie Huynh, a portfolio manager and strategist for dynamic asset allocation at BNP Paribas Asset Management. “Since the ceasefire, there has been no increase in oil flows through the Strait of Hormuz, which makes the market’s ability to shrug off the Iran conflict hard to justify.”

In FX, the Bloomberg Dollar Spot Index adds 0.1%. The Aussie dollar and yen are the weakest of the G-10 currencies, falling 0.2% each. The Norwegian krone outperforms

In rates, treasuries are slightly cheaper across the curve, with yields partially reversing an opening gap higher after weekend developments from the Middle East cast doubt on the prospects for peace talks ahead of a looming ceasefire deadline. Meanwhile, US Navy carried out its first seizure of an Iranian vessel in the Strait of Hormuz. Oil futures are subsequently higher with Treasury yields, while S&P futures are down on the day. US yields cheaper by 1.5bp to 2.5bp across the curve with spreads broadly trading within a basis point of Friday session close. US 10-year yields traded around 4.27% with bunds and gilts lagging by 2bp and 4bp in the sector. European government bonds also underperform, with UK and German 10-year yields rising 4 bps and 3 bps respectively. US 10-year borrowing costs climb 1 bp. IG dollar issuance slate includes a couple of deals already. This week, syndicate desks anticipate sales around $20 billion to $25 billion, likely led by regional banks along with corporates coming out of their earnings blackout periods. Treasury auctions this week include $13 billion 20-year bond reopening on Wednesday and $26 billion 5-year TIPS Thursday. US economic data calendar slate empty for the session.

In commodities, Brent crude futures rise 5% to around $95 a barrel after weekend developments cast doubt on the prospects for US-Iran peace talks. Precious metals slide, with spot silver down around 2%. Bitcoin rises back above $75,000.

US session quiet for scheduled data, while Fed’s external communications blackout period has now begun ahead of the April 29 policy announcement.

Market Snapshot

S&P 500 mini -0.5%

Nasdaq 100 mini -0.5%

Russell 2000 mini -0.8%

Stoxx Europe 600 -1%

DAX -1.4%

CAC 40 -1%

10-year Treasury yield +1 basis point at 4.26%

VIX +2.1 points at 19.59

Bloomberg Dollar Index +0.1% at 1194.19

euro little changed at $1.1761

WTI crude +5.9% at $88.79/barrel

Top Overnight News

Oil climbed and equity futures dropped after the US seized an Iranian-flagged cargo vessel and Tehran again closed the Strait of Hormuz, clouding prospects for peace talks.

An Iranian delegation will arrive in Islamabad on Tuesday, despite Tehran’s statements that it had no intention of sending its negotiators while the US navy is continuing a blockade of its ports. Nikkei

US gas prices may remain at $3 per gallon or more until next year, contradicting Treasury Secretary Scott Bessent’s prediction of relief by the summer. BBG

China’s set to import a record volume of US ethane in April as petrochemical producers seek alternative feedstocks due to the Iran war. Shipments may rise to 800,000 tons, JLC said, around 60% higher than average. BBG

There is a newfound sense of anxiety amongst battleground Republicans that their Senate majority isn’t as safe as they once thought. Democrats still face steep odds in their bid to flip the chamber, but there is persistent concern that the longer the Iran war drags on and the economy sputters, the more it could complicate their path to keeping their majority in November. Politico

China sent a group of warships to hold drills in the western Pacific Ocean, a move that comes as Japan joins massive exercises with the US and the Philippines for the first time. BBG

Google is in discussions with Marvell to develop two new chips to run AI models more efficiently. The Information

A weekend hack triggered a crisis of confidence among crypto investors, with users pulling billions from DeFi’s biggest lending platform. BBG

Warsh believes AI will trigger a productivity boom that keeps growth at a healthy level and allows the Fed to cut rates, but many of his future colleagues are skeptical of this thesis. WSJ

Iran News Wrap

Iran reversed the brief reopening of the Strait of Hormuz and said the waterway had returned to “strict control” after accusing the US of not meeting its obligations and refusing to lift the blockade on Iranian ports, with at least three attacks reported on commercial ships following the re-closure, including Iranian gunboats firing on a tanker and an attack on a cargo vessel near the strait that damaged containers on board.

US President Trump said on Saturday that Iran got “a little cute” by closing the Strait again, but added there were still “very good conversations” going on.

US President Trump announced on Sunday an Iranian-flagged cargo ship named TOUSKA tried to get past the US naval blockade, but the Navy Guided Missile Destroyer USS SPRUANCE intercepted it in the Gulf of Oman and gave a warning to stop. The Iranian crew refused, after which the US Navy ship disabled the vessel by blowing a hole in the engine room. Trump added that US Marines have custody of the vessel, and they are seeing what’s on board. It was separately reported that Mehr News Agency claimed US forces fired on an Iranian merchant ship to force it to return to territorial waters, but were then forced to flee after the rapid response of IRGC naval units.

US President Trump posted on Sunday that “Iran decided to fire bullets yesterday in the Strait of Hormuz – A Total Violation of our Ceasefire Agreement!”, while Trump stated that his representatives are going to Islamabad and will be there on Monday evening for negotiations.

US President Trump said VP JD Vance, Special Envoy Witkoff and Jared Kushner will head to Islamabad, Pakistan, for fresh talks with Iran, and will arrive on Monday evening, according to a White House official.

A US senior official said that if there is no breakthrough soon, the Iran war could resume in the coming days, and that the situation with Iran is at a critical point.

Pakistan Army Chief Munir spoke to President Trump and told him that the Hormuz blockade is a hurdle to talks, according to a Pakistani security source cited by Reuters; Trump reportedly told Munir that he would consider his advice.

Iran will send a delegation to a second round of talks with the US despite the latest escalation in the Strait of Hormuz, Anadolu Agency reported, citing two Pakistani sources.

Pakistani Journalist Mallick posted “To my understanding, regardless of the statements and posturing, the second round of talks in Islamabad are to go ahead as per schedule and what is that schedule, only the parties know about the exact schedule.”

Iran parliament’s national security and foreign policy commission head said the decision has been made to continue talks with US, but this does not mean negotiation at any cost; delegation may travel to Pakistan if positive signals received from the US

Pakistan has intensified diplomatic contacts since Sunday with Washington and Tehran to ensure talks proceed as soon as Tuesday, AP reported.

Iranian Foreign Ministry Spokesperson said no decision has been made regarding participation in the new round of negotiations, Al Araby reported; the past week witnessed numerous diplomatic developments focused on negotiations to end the war. He further said that if the US or Israel launches new aggression, Iran’s armed forces will respond accordingly; Tehran has not received any serious offer regarding lifting sanctions on it.

Iranian lawmaker said he doesn’t expect any deal with the US and believes even if there is a ceasefire, it won’t last.

Iran’s Supreme Leader said Iran’s navy is ready to inflict “new bitter defeats” on its enemies.

Iranian Vice President Mohammad Reza Aref said the security of the Strait of Hormuz is not free, while he added it is impossible to restrict Iranian oil exports and, at the same time, pretend to provide free protection to others. Furthermore, he said “The choice is clear: either a free oil market for all, or risk incurring enormous costs that will affect everyone”.

Iran’s Deputy Foreign Minister said there will be no further in-person peace talks with the US until Washington changes its “maximalist” demands, while the official added Iran would not hand over its enriched uranium to the US. Furthermore, IRNA also reported that Tehran has not agreed to participate in a second round of talks.

Iran’s Security Council said it is reviewing proposals made by the US in recent days, and Iran is determined to maintain control of the Strait of Hormuz until the war ends, while it was stated that Iran will not reopen the Strait as long as the US blockade of Iranian ports is in place.

Iranian senior official said that significant differences remained between Iran and the US, including on nuclear issues and that serious talks are required, according to a report on Friday.

Iranian Harat Khatam Al-Anbiya Central HQ spokesperson said the US attack on the Iranian commercial ship violates the ceasefire, and warned Iran will soon respond and retaliate to this armed piracy.

Iranian sources told CNN that the Iranian delegation is expected to arrive in Pakistan on Tuesday, according to Al Hadath.

Iran has yet to agree to another round of talks with the US, according to Iranian press. It was also reported that Iran’s Deputy Foreign Minister said Iran will respond with full force if they return to war, while Iranian state media separately reported on Sunday evening that Tehran was not currently planning to take part in new talks with the US.

Iranian source said given US President Trump’s remarks about talks and the contradiction with what is actually unfolding between Iran and the US, they believe they are facing trickery by the adversary and are on the brink of a fresh wave of escalation, according to Al Jazeera.

Iranian senior official denied US President Trump’s claims and said that Iran did not agree to halt uranium enrichment indefinitely, while they will not accept being an exception to international law.

Pakistani media sources said gaps between the US and Iran have been narrowed in recent days, according to Al Hadath.

More than 20 vessels passed the Strait of Hormuz on Saturday, which is the highest number since March 1st, according to Kpler data. It was separately reported that an Iranian oil tanker broke through the US blockade and entered Iranian waters, according to CCTV.

N13 reported, citing an Israeli senior official, that Israel has a “red line” related to ballistic missiles; should Iran cross this red line, then Israel has no choice but to respond.

IDF confirmed it carried out the first strikes against Hezbollah since the ceasefire and that the strikes were against Hezbollah operatives who violated the ceasefire understandings.

UAE opened talks with the US about obtaining a financial backstop in case the Iran war plunges it into a deeper crisis, according to US officials cited by WSJ. Furthermore, it was reported that UAE informed Washington it will be forced to sell its oil in yuan if it is not supplied with enough dollars.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher as the region shrugged off the escalatory geopolitical headlines from over the weekend, including the re-closure of the Strait of Hormuz and attacks on several vessels by Iran, while US President Trump announced that the US Navy intercepted an Iranian-flagged vessel and blew a hole in the engine room after it attempted to get past the US blockade. This resulted in a spike in oil prices at the reopen and saw US index futures decline, although asset classes have faded the extremes as focus turns to talks in Islamabad, with President Trump sending negotiators for talks with Iran, although there is no confirmation yet on whether Iran will attend. ASX 200 traded little changed amid the mixed price action in commodity-related stocks and with financials subdued after NAB flagged a spike in impairments due to the Middle East conflict. Nikkei 225 rallied with the index briefly returning to the 59,000 level following the recent unwinding of April rate hike bets, and with the index unfazed by the rise in oil prices. Hang Seng and Shanghai Comp were higher amid earnings updates, but with further upside capped by a lack of macro catalysts, while the PBoC provided no surprises as it announced China’s benchmark LPRs were maintained at their current levels for the eleventh consecutive month.

Top Asian News

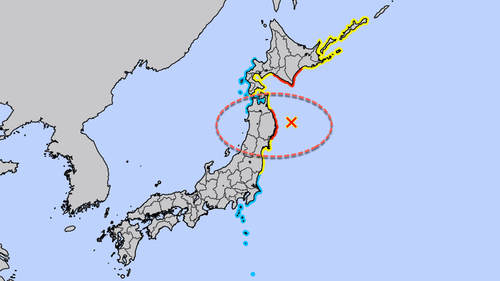

Earthquake with preliminary magnitude of 7.4 reported off the coast of Japan, with a tsunami warning issued, NHK reports

European bourses (STOXX 600 -0.9%) start the first trading week under pressure, as geopolitics continue to drive price action. Over the weekend, Iran (yet again) closed the Strait of Hormuz after accusing the US of not meeting its obligations, while an Iranian-flagged ship was struck by the US Navy. The DAX 40 is under the most pressure, while higher energy prices provide a floor for the FTSE 100. European sectors highlight the negative bias. Cyclicals such as Travel & Leisure, Autos and Banks sit at the bottom of the pile, while defensives such as Utilities outperform, with Energy also showing a strong performance amid the rise in crude prices.

Top European News

German PPI MoM (Mar) M/M 2.5% vs Exp. 1.4% (Prev. -0.5%)

German PPI YoY (Mar) Y/Y -0.2% (Prev. -3.3%)

UK Rightmove House Prices Y/Y (Apr) -0.9% (Prev. -0.2%)

Trade/Tariffs

China’s March rare earth magnet exports to the US fell 9.5% M/M and its rare earth magnet exports to Japan fell by 17.3% M/M.

FX

G10 FX are displaying a modest risk-off bias today, with DXY higher by a tenth and high beta underperforming after geopolitical escalation over the weekend (Please refer to the European opening news).

USD is the best performer as the preferred haven during this conflict, with energy prices also elevated, around USD 96/bbl for Brent. The domestic calendar is light, DXY is likely to be catalysed by Middle East Updates. Note, the Fed entered its blackout window on 18th April ahead of its 29th April confab.

GBP digests domestic political updates, with the Sun reporting that Manchester Mayor Burnham met with Former UK Deputy PM Rayner on Friday. This fuelled speculation that the two are plotting to overthrow PM Starmer, who is on a weak footing following the Mandelson revelations (PM speaks at 15:30 BST on Mandelson’s vetting). Fortunately for UK assets, few expect any movement from the Parliamentary Labour Party (PLP, the body with power to oust the PM), according to POLITICO. MUFG writes: “So far the negative impact on the pound has been limited, but UK political developments have the potential to trigger a sharper sell-off in the month ahead”. GBP prefers to focus on geopolitical developments with Brent +6-7% on the day. EURGBP trades 0.1% higher, while Cable is 0.1% lower.

JPY is one of the worst performers in the G10 space as USD/JPY continues to creep towards the critical 160 level. In a note on Sunday, Barclays said it shifted its BoJ hike forecast to June from April, following harsh (For the BoJ) repricing at the beginning of last week amid a lack of hawkish commentary from Ueda. This morning, NHK reported a preliminary 7.4 magnitude earthquake off the north-east coast of Japan. A three-meter-high wave warning was issued for the northern region; no impact on Japanese assets.

Central Banks

BoJ is reportedly likely to keep rates on hold at April’s meeting, Reuters reported citing sources.

Fixed Income

Global fixed benchmarks are broadly in the red, given the recent surge in energy prices, after Iran shut the Strait of Hormuz over the weekend and fired at three commercial vessels. (Please see the Newsquawk feed for a full geopolitical overview). Now markets await potential second round talks between US-Iran – some reports have suggested both sides will be in the region on Tuesday. As it stands, newsflow on whether the talks will actually take place is mixed; the Iranian Foreign Ministry spokesman suggested that no decision has been made on whether the talks will happen. On the yield front, a clear bear flattening is seen in the curve; a bias which has continued to play out throughout periods of escalation between US-Iran.

JGBs traded with mild gains overnight, bucking the trend seen across peers. Potentially just catching up to the considerable upside seen in fixed benchmarks on Friday (following the opening of the Strait), and also as traders price out the chance of an April hike at the BoJ. Senior rate strategist at SMBC said “the market’s main scenario appears to be that a rate hike will be put off next week”, but he highlighted that Ueda could signal a shift in stance at April’s presser.

USTs are off by around 7 ticks, and currently trade at the lower end of a 111-12+ to 111-18 range; but still holding around the mid-point of Friday’s range of 111-04 to 111-23. Essentially, markets have not entirely discounted the strength seen in US paper following Iran’s brief opening of the Strait. The US 2yr remains around 3.75%, which has proven to be a point of support for in the past week. US domestic docket ahead is particularly thin, with no US data/Fed speak scheduled.

Bunds are lower by around 40 ticks, and trading towards the bottom of a 125.66 to 125.89 range. Once again moving at the whim of geopolitical developments/higher energy prices; the GE 2s10s is a touch wider once again, but residing near the lows seen on Friday. Geopols aside, focus has been on the ECB, where a few policymakers spoke over the weekend/late-Friday. Demarco and Kazaks suggested that they were comfortable with bets of two hikes this year, whilst Kocher warned against pre-emptive ECB rate action on uncertainty. Sticking with the ECB, a recent survey of monetary policy experts by the OMFIF suggested that former ECB member de Cos is the “most qualified candidate” in the race to succeed President Lagarde.

Gilts lag vs peers. UK paper has continuously seen bouts of underperformance when oil prices rise, given its high dependence on external energy. But also adding to the downbeat narrative is domestic politics, with continued focus on PM Starmer’s future. The Sun reported that Manchester Mayor Burnham met with Former Deputy PM Rayner on Friday, which has fuelled rumours of the pair launching a leadership challenge. Gilts currently trade down by around 66 ticks and at the lower end of a 88.44 to 88.72 range.

Commodities

In geopolitics, Iran re-closed the Strait of Hormuz, stating it will remain under strict control and will not reopen while the US blockade of its ports continues, with multiple reported attacks on commercial vessels following the move. Tensions escalated after US Marines seized the Iranian-flagged cargo ship TOUSKA as it attempted to breach the blockade, while President Trump said a separate Iranian vessel was intercepted and disabled after ignoring warnings. Iran condemned the seizure as piracy and warned it would retaliate, as both sides accused each other of violating the ceasefire. Meanwhile, uncertainty persists around US-Iran talks, with Washington planning fresh negotiations in Pakistan, although Tehran has not confirmed participation and significant gaps remain, particularly over nuclear terms and control of the Strait. More recently, an Iranian Foreign Ministry spokesperson said no decision has been made regarding participation in the new round of negotiations. Elsewhere, the Pakistani Army Chief told US President Trump that the Hormuz blockade is a hurdle in talks, to which Trump responded that he would consider his advice.

Oil jumped as a result, with Brent climbing back above USD 95/bbl, reversing most of Friday’s decline (currently in a USD 94.33–97.50/bbl range) after the waterway’s brief reopening. WTI June trades in a USD 86.46–89.60/bbl range. Upside has been facilitated by the aforementioned escalation, with additional support following comments from the Iranian Foreign Ministry spokesperson indicating no decision has yet been made on talks with the US. That said, gains are somewhat capped by ongoing efforts to bring the US and Iran back to the table ahead of the ceasefire expiry on Wednesday (UK time). European natural gas prices also rose, with Dutch TTF futures briefly moving back above EUR 43/MWh after Iran shut the Strait again.

Spot gold and silver declined as the renewed disruption in Hormuz stoked inflation concerns tied to an energy supply shock and cast further doubt over efforts to end the conflict, with bullion slipping below USD 4,800/oz but currently off worst levels. Spot gold is trading in a USD 4,736–4,814/oz range.

Copper retreated from its highest close since early February. Iron ore bucked the broader trend and rose overnight, with reports noting firm Chinese demand ahead of the May Day holidays and tight near-term supply. 3M LME copper trades in a USD 13,204.90–13,375.28/t range at the time of writing.

Qatari sources say it may take up to five years to repair damaged gas facilities.

Iraq reportedly resumes Southern Oil exports after a month-long halt due to Strait of Hormuz disruption, one tanker begins loading, according to four energy sources cited by Reuters.

Geopolitics: Ukraine

Ukraine’s Drone Force Commander says Russia’s Tuapse oil refinery was struck overnight.

US Event Calendar

US session quiet for scheduled data, while Fed’s external communications blackout period has now begun ahead of the April 29 policy announcement.

DB’s Jim Reid concludes the overnight wrap

As the war in Iran enters its 8th week, recent developments can be framed in two ways: either five steps forward towards peace and three back (seems more apt than three and two), or as evidence that the two sides remain far enough apart that a lasting deal will be extremely hard to achieve and markets have become far too optimistic. I lean more towards the former, but the comparison with recent history is uncomfortable. Remember the 10%+ S&P 500 rally in the early weeks of the war in Ukraine, when hopes briefly grew of an early negotiated settlement, only to be disappointed. That episode is a clear warning sign.

That said, the political calculus around Iran may be different. According to Nate Silver’s Silver Bulletin, President Trump’s approval rating dipped notably after the war began but appears to have stabilised since the two-week ceasefire was announced on 7 April—possibly reflecting the subsequent fall in petrol prices. A renewed deterioration in negotiations would therefore be unlikely to help approval ratings if oil and gas prices were to rise again.

The headline news over the weekend was Iran stating that the Strait of Hormuz was shut less than 24 hours after indicating on Friday that it would reopen. Shipping through the strait has now again ground to a halt after picking up on Saturday. On Friday afternoon in London, Polymarket had priced the probability of Strait traffic returning to normal by the end of May as high as 84%. That has now fallen back to around 63%, close to last Thursday’s level, but still well above the 37% probability priced this time last week.

The current ceasefire is due to expire at some point on Wednesday. President Trump struck a more hawkish tone yesterday, posting that while his negotiators will be in Islamabad for talks tonight (with possible talks reported for Tuesday), if Iran does not accept the deal on the table the US will “knock out every single power plant and every single bridge in Iran”. Iran’s state TV reported last night that Iran has “no plans for now to participate” in another round of talk with the US. Meanwhile, we heard that the US Navy had intercepted and boarded an Iranian cargo vessel in the Gulf of Oman, marking the first such seizure since the US announced its blockade of Iranian shipping.

This backdrop has meant that markets this morning have reversed a good chunk of Friday’s moves. Brent crude is up +5.61% to $95.45/bbl after a -9.07% decline on Friday, leaving it at levels seen around the middle of last week. The extent of the reversal has been more partial outside of oil, with S&P 500 futures down -0.60% (+1.20% Friday), while 10yr Treasuries yield are +2.0bps higher (-6.3bps Friday).

Asian equity markets are surprisingly resilient this morning although they were long closed by the time the positive headlines came through on Friday. Across the region, the KOSPI is leading the charge with a +1.00% gain, with the the Hang Seng (+0.84%) slightly outperforming its mainland Chinese counterparts, namely the CSI (+0.54%) and the Shanghai Composite (+0.67%). The Nikkei (+0.71%) is also firm.

In terms of the week ahead, in the US, the main event in a quiet week for data and for Fedspeak given the media blackout has now started, comes tomorrow morning at 10:00am ET, when Kevin Warsh, President Trump’s nominee to become the next Chair of the Federal Reserve, appears before the Senate Banking Committee for his confirmation hearing. Although Warsh has said little publicly since being nominated, his earlier remarks offer important clues. He has previously argued that the US economy faces powerful disinflationary forces stemming from deregulation and the rapid diffusion of artificial intelligence, a mix that should ultimately allow interest rates to move lower. That narrative is likely to feature prominently in his testimony. However, the economic backdrop has shifted in recent months, making the case for near term easing less straightforward. The labour market has stabilised, inflation measures such as PCE have surprised to the upside, and the conflict in Iran has introduced renewed upside risks to prices via energy channels. See our economists’ latest forecasts here from the end of last week where they have removed the one cut in 2026 that they previously had.

While Warsh has spoken in favour of rate reductions over time, he is not generally viewed as structurally dovish. If anything, his instincts have historically leaned more hawkish than many of his peers’. The delicate balancing act on Tuesday will be how he frames a longer-term desire to lower rates while acknowledging that current conditions do not necessarily justify imminent cuts. Treasury Secretary Scott Bessent’s recent comment that he would “understand if the Fed needs to wait on rate cuts” may give Warsh some political cover, allowing him to argue that temporary inflation risks require near term vigilance before policy can ease later on.

Beyond rates, senators are likely to probe Warsh on several other fronts. He has long been critical of the Fed’s balance sheet policies, though expectations of rapid change have faded, with consensus now favouring a gradual approach that first requires regulatory adjustments to reduce banks’ demand for reserves — a view shared by several current Fed officials. He is also expected to revisit his criticism of forward guidance, particularly its detailed use outside of crisis periods, potentially signalling a desire to simplify how the Fed communicates policy intentions. Fed independence will loom large too, especially at a time when inflation has remained above target for an extended period, oil prices have surged again, and political pressure to cut rates has intensified. Even assuming Warsh ultimately secures confirmation, risks remain, with Senator Thom Tillis reiterating that he intends to block progress on Fed appointments until the Department of Justice investigation into Chair Powell is resolved.

With Fed officials in their pre meeting communications blackout, economic data will do what it can to fill the void. Tomorrow also brings the most important release of the week in the form of March retail sales. Headline sales are expected to rebound by 1.2% month on month (DB forecast), up from 0.6% previously, helped by a recovery in auto sales. Excluding autos, sales are forecast to rise by a still solid 0.8%, compared with 0.5% last month, though much of that strength is likely to reflect higher petrol prices rather than a broad resurgence in discretionary spending. The retail control group, which feeds directly into GDP calculations, is expected to grow by a more modest 0.2%, down from 0.5% previously, suggesting that underlying goods demand remains steady but unspectacular.

Later in the week, Thursday brings a handful of releases that will help round out the picture. Initial jobless claims are expected to edge up to 210,000 from 207,000, a move that will be watched closely as the data coincide with the survey window for April’s employment report. While monthly payroll numbers have been volatile, most broader measures point to a labour market that has largely stabilised over the past year and looks in better shape now than it did to many prior to the Iran War. The same day also delivers preliminary S&P Global PMIs, with manufacturing expected to ease slightly to 52.1 from 52.3, while services are forecast to recover to 51.4 from 49.8. Any commentary on supply chains or pricing pressures linked to Middle Eastern developments will be scrutinised, even if the surveys only partially capture the latest geopolitical shifts.

Across the globe, Thursday also sees the global flash April PMIs which will give a sense on how companies are viewing the current conflict, even if newsflow, net net, has improved of late. The prices paid components will be worth a watch.

There are plenty of indicators due in the UK, including labour market data tomorrow and March inflation on Wednesday. Our UK economist forecasts headline CPI to jump to 3.3% YoY, with core staying roughly steady at 3.2% (see full preview here). There will also be the March retail sales report and the April GfK consumer confidence indicator due Friday.

Sentiment data is also a theme for next week in the rest of Europe, with releases featuring the ZEW survey (tomorrow) and the Ifo survey (Friday) in Germany, as well as consumer confidence in the Eurozone (Wednesday) and France (Friday). Briefly turning to European political events, the list includes the EU leaders’ informal summit on Thursday and EU foreign affairs council meeting tomorrow. Elsewhere, March inflation will be in the spotlight in Japan on Friday when the national CPI is due. There will also be the March CPI report in Canada (today) and the Q1 CPI (tomorrow) in New Zealand. Rounding out with corporate earnings, there will be a number of companies across defence (RTX and Lockheed Martin), energy (SLB, Baker Hughes and Halliburton) and the materials (Newmont, Freeport-McMoRan) sectors reporting, whose results and outlook will be of interest amidst the Iran conflict. A number of airlines also post results. Tech names for this week will include Tesla, SK Hynix, Intel and SAP. Other highlights are Procter & Gamble, General Electric, American Express and Blackstone. See the full day-by-day week ahead at the end for more.

Recapping last week now, and markets climbed higher as prospects for a resolution between Iran and the US became more likely over the week. That was further cemented on Friday after Iran’s Foreign Minister announced that the Strait of Hormuz would now be open for the remaining period of the ceasefire. Although that was reversed less than a day later on Saturday, this helped drive Brent crude down -5.06% (-9.07% on Friday) last week to $90.38/bbl, its lowest close since March 10. In turn, multiple asset classes rallied as investors dialled back fears of a stagflation shock.

Those included equities, where multiple indices reached new records on the back of the Strait of Hormuz opening. The S&P 500 (+4.54%) saw its largely weekly rise since May 2025, closing at a new record high of 7126 (+1.20% on Friday). It had crossed above the 7,000 threshold for the first time earlier in the week on Wednesday. The Nasdaq Composite also rose +6.84% (+1.52% on Friday) to a new record, extending to a 13th day of consecutive gains for the first time since 1992. In Europe, most of the gains for equities came thanks to Friday’s jump, with the STOXX 600 (+1.91%, +1.56% Friday), CAC 40 (+2.00%, +1.97% Friday) FTSE 100 (+0.63%, +0.73% Friday) and DAX (+3.77%, +2.27% Friday) higher.

In fixed income, bonds also rallied as investors eased their concerns around the prospect of an energy-driven inflationary shock. In Europe, expectations of an April rate hike from the ECB collapsed from 34% to just 9% last week, which in turn helped yields on 2yr bunds (-19.4bps to 2.41%, -10.9bps on Friday) to see their largest weekly fall since April 2025. 10yr bund yields also declined by -9.8bps to 2.96% over the week (-7.2bps on Friday). Yields on 2yr (-8.9bps) and 10yr (-6.9bps) US Treasuries also fell over the week, as futures-implied probability that the Fed will cut by December rose to 61% compared to 26% the previous week.

Finally, the news of tensions de-escalating in the Middle East triggered other notable moves in markets, with the dollar down for the third consecutive week at -0.56% (-0.12% on Friday). In credit, spreads tightened across the board, with US IG (-1bps) and HY spreads (-12bps) both falling last week, whilst Euro IG (-4bps) and HY spreads (-4bs) also fell back.

Tyler Durden

Mon, 04/20/2026 – 08:45

Iran Says No Plans For 2nd Talks After US Seizure Of Cargo Ship, Pakistanis Contradict, Oil Prices Climb

Iran Says No Plans For 2nd Talks After US Seizure Of Cargo Ship, Pakistanis Contradict, Oil Prices Climb

Summary

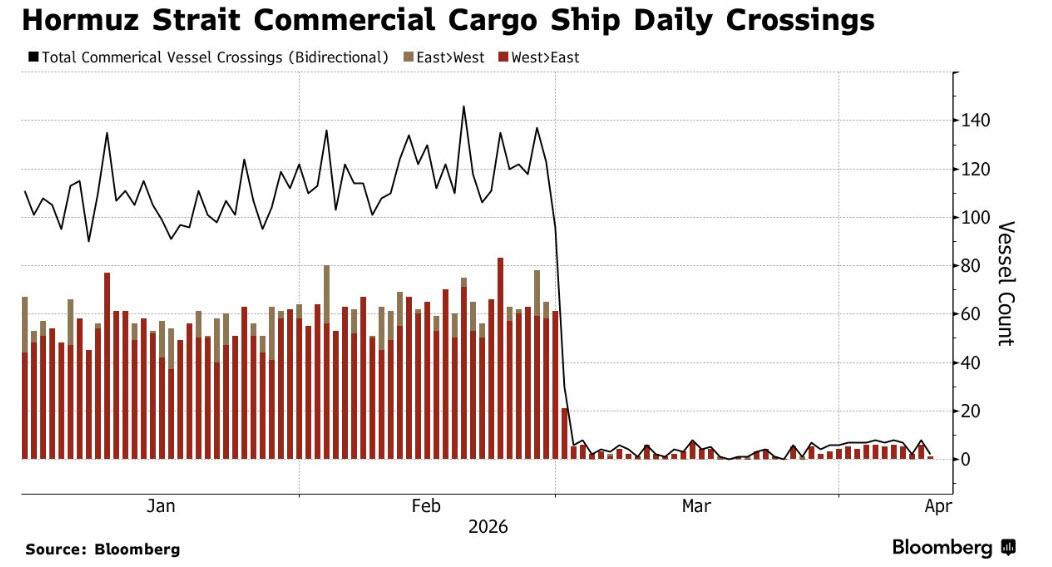

Hormuz latest: Just three ships have crossed in the past 12 hours, shipping data indicates.

Iran’s military after Sunday’s US seizure of Iran-flagged cargo ship: will “take the necessary action against the US military”

Vance will try again in Pakistan, though still unclear whether Iranians will join – Pakistanis say yes, but timeline is fluid.

Xi to Saudi crown prince important phone call: “the first time the Chinese leader had called for the reopening of the strategically vital waterway.“

Strait of Hormuz traffic returns to normal by end of April?

Yes 28% · No 72%

View full market & trade on Polymarket

* * *

Shipping Traffic Halt Latest

Al Jazeera and others have written the strait is at a virtual standstill currently, after the major Sunday incident which saw the US Navy intercept, fire upon, and board an uncooperative ship which was trying to pass the US-imposed blockade. It was an Iranian-flagged ship which was forcibly stopped in the Gulf of Oman, where some dozen US warships have been patrolling.

Just three ships have crossed in the past 12 hours, shipping data indicates. The same publication records that “Oil products tanker Nero, which is under UK sanctions, has left the Gulf and is sailing through the strait, according to satellite analysis from data analytics specialists SynMax and tracking data from the Kpler platform.” And: “Two other ships – a chemical tanker and a liquefied natural gas tanker – have also sailed into the Gulf through the critical waterway separately, the data showed.”

Reuters: Senior Iranian official says positive efforts have been started by Pakistan to end the US blockade and ensure Iran’s participation in talks.

On Monday a spokesman for Iran’s military reiterated a threat to “take the necessary action against the US military” after the Sunday US interdiction. He described that that Iran’s military exercised restraint over the incident, not taking immediate action, in order to protect the ship’s crew, but will act “once it is ensured that the lives of the families and crew of the vessel attacked by the United States are safeguarded.” Apparently the crew’s family members are accompanying them aboard the vessel, the statement suggests.

⚡️ US military releases footage of “seizure of Iranian ship Touska in Strait of Hormuz” pic.twitter.com/d7qk7G5oeC

— War Monitor (@WarMonitors) April 19, 2026

Important Xi Jinping Statement on Hormuz

China’s President Xi Jinping on Monday demanded the uninterrupted passage of vessels through the Strait of Hormuz in a phone call with Saudi Arabia’s Crown Prince Mohammed bin Salman, state news agency Xinhua reports. He urged the normalization of shipping traffic after about 50 days of disruption which obviously and significantly impacts Chinese oil imports.

“Normal navigation through the Strait of Hormuz should be maintained, this is in the shared interests of regional countries and the international community,” Xi said. He called for an immediate, comprehensive ceasefire and insisted disputes be resolved through political and diplomatic means.

South China Morning Post observes that it was “the first time the Chinese leader had called for the reopening of the strategically vital waterway, which has been repeatedly blockaded since US-Israeli strikes on Iran began on February 28.” China imported 5.86 million tons of crude oil from Saudi Arabia, down 10% from February, according to customs data released Monday.

Second Pakistan Talks Imminent?

After the Sunday dramatic US seizure of the Iranian-flagged ship, Iran’s Foreign Ministry has said the country currently no plans regarding a new round of talks, however, it also said it is reviewing the latest Washington proposal related to a second round of Pakistan-hosted talks. With that, by Monday it reasserted that the transfer of enriched uranium out of the country or into US custody has never been on the table. Tehran is insisting that it won’t be transferred anywhere.

This firm stance is after President dramatically shifted his tone over the weekend from strangely and surprisingly somewhat praising Iran’s leadership (with statements such as the US could work with them and possibly trust them) to once up again ramping up threats, posting “No more Mr. Nice Guy” on social media.

Currently there are conflicting reports on whether the Iranian side will actually be there for reported possible Tuesday talks. Pakistan officials say the timing of the talks remains fluid. According to the latest via Associated Press Iranian authorities have expressed willingness to send a delegation to Islamabad, citing two Pakistan officials. The officials reports “cautious optimism that delegations from both Iran and the United States could travel to Islamabad.”

Some confused and conflicting signaling, likely purposely so…

Iran’s Foreign Ministry spokesman Esmail Baghaei:

We have no plans for the next round of negotiations. pic.twitter.com/CFb16qt8vM

— Clash Report (@clashreport) April 20, 2026

The NY Times has declared that JD Vance will try again:

The vice president is scheduled to lead an American delegation back to Islamabad, Pakistan, this week for another round of in-person negotiations with Iran after failing to secure a deal just over a week ago.

Whether the talks even occur seems in dispute. Hours after President Trump announced the trip on Sunday, Iranian state media said that Tehran had not yet agreed to any such meeting. Later, Mr. Trump announced that a Naval destroyer had attacked an Iranian-flagged cargo ship that tried to skirt the U.S. blockade on Iranian ports in the Strait of Hormuz.

President Trump has been threatening major escalation should there be no negotiated settlement, at a moment the two sides’ position are very distant especially on the nuclear issue.

Zero Sum Positions on Nuclear Issue

The problem, according to University of Chicago Professor Robert Pape is the zero sum logic of it all. “In a matter of a day, the system snapped back to escalation,” he wrote over the weekend. “This is not a story about fragile diplomacy or poor sequencing. It is a story about zero-sum conflict, where the core issues cannot be divided, traded, or deferred without forcing one side to accept a strategic loss—a direct contest over relative power.”

“At the center of the war is a fact that cannot be negotiated away: Iran either retains a nuclear capability on the threshold of weapons, or it does not,” Pape continues. “There is no stable middle ground that satisfies both sides.”

POTUS is laying out two courses of action—a negotiated settlement, or a major escalation.

There is a third option, and he should take it: recognize there is no way to force a positive outcome and simply leave.

The region is not ours to fix. President Reagan chose this path in… pic.twitter.com/5ovi05FdwE

— Joe Kent (@joekent16jan19) April 19, 2026

And more from the analysis: “The same zero-sum logic applies—more visibly and more immediately—to the Strait of Hormuz. Before the war, Hormuz functioned as a global commons, carrying roughly one-fifth of the world’s oil supply. That assumption is now broken. Iran has demonstrated that it can shift from disruption to conditional control, allowing passage under its terms while restricting or denying access when it chooses. The United States, in response, is attempting to preserve open navigation through blockade and interdiction. But these positions cannot be reconciled.”

Tyler Durden

Mon, 04/20/2026 – 08:45

UK PM Starmer Faces “Judgment Day” Over Epstein Pal Mandelson’s Appointment

UK PM Starmer Faces “Judgment Day” Over Epstein Pal Mandelson’s Appointment

UK Prime Minister Keir Starmer is preparing for a showdown with the senior official he fired over the appointment of Peter Mandelson as US ambassador, as calls for the prime minister to resign grow.

The controversy stems from Starmer’s decision to appoint veteran Labour politician Peter Mandelson (Lord Mandelson) as Britain’s ambassador to the United States in late 2024/early 2025, despite Mandelson’s well-known past associations with the late convicted sex offender Jeffrey Epstein.

The scandal has escalated dramatically in recent days due to revelations about security vetting failures, leading to intense political pressure on Starmer.

As a reminder, Mandelson, a senior New Labour figure and former EU Trade Commissioner, has long faced questions over his friendship with sex-offender Epstein, and these ties were public knowledge when Starmer nominated him for the prestigious Washington role.

Starmer has said he was aware of the basic relationship but claims Mandelson “lied repeatedly” about the extent of contact.

He later sacked Mandelson in September 2025 after further details emerged about the depth of those links, including allegations of sharing sensitive information.

Starmer apologized to Epstein victims and accused Mandelson of betraying the country.

The appointment was always controversial, with critics questioning the judgment in placing someone with such baggage in a top diplomatic post involving close US-UK relations.

However, things have heated up recently after new reports emerged last week revealing that Mandelson failed his security vetting for the ambassador role.

Security officials recommended against clearance due to reputational and other risks, but Foreign Office officials overruled this and approved him anyway.

As The FT reports, papers published by the Cabinet Office last month include a letter from the then head of the civil service, Lord Simon Case, on November 11 2024, setting out the process before the appointment.

Case’s note, first reported by Sky News, said:

“You should give us the name of the person you would like to appoint and we will develop a plan for them to acquire the necessary security clearances and do due diligence on any potential conflicts of interest or other issues of which you should be aware before confirming your choice.”

Other papers have revealed that Jonathan Powell, Starmer’s national security adviser, found Mandelson’s appointment in December 2024 “weirdly rushed”.

Mandelson failed the vetting process by security officials, but was given security clearance nevertheless by Sir Olly Robbins, the most senior civil servant in the Foreign Office.

Starmer is facing widespread calls to resign from opposition parties and some within Labour circles.

“He is taking the public for fools,” Kemi Badenoch, leader of the Conservatives, said on Friday. “We know that No 10 was told that Mandelson had failed his vetting because journalists told them in September last year. This leaves us with two possibilities: either the Prime Minister is lying or he is so incompetent that he is unfit to run the country.”

“Either way his position is untenable,” she said.

Ed Davey, who heads the Liberal Democrats, also said on Sky News that Starmer had shown “catastrophic misjudgment and that’s why we have said he needs to go.”

Allies are standing by Starmer.. for now…

“Peter Mandelson shouldn’t have been appointed the ambassador,” Scottish Secretary Douglas Alexander said on Sky News on Monday.

“The prime minister, never mind myself, accepts that was a mistake.”

“I have absolutely no doubt at all, knowing the PM as I do, that had he known that Peter Mandelson had not passed the vetting, he would never, ever have appointed him ambassador,” Lammy, who was foreign secretary at the time, told the Guardian.

Starmer is due to make a statement and face grilling from MPs in the House of Commons today (Monday), which many are calling his “judgment day.”

Starmer has repeatedly told Parliament and the public that “full due process” and proper vetting were followed.

He now claims he was not informed that Mandelson had failed the checks – describing it as “staggering” and “unforgivable.”

He says he only learned this in the past few days and is “absolutely furious.”

Within hours of the story breaking, Starmer reportedly forced out Robbins, who is expected to appear before a parliamentary committee soon (potentially clashing with the government’s narrative).

Allies of Robbins have told British media including the Sunday Times that the former civil servant was being scapegoated.

Officials speaking to Bloomberg argue that Starmer had signaled privately that he was relaxed about Mandelson’s previously known links to Epstein, Russia and China, leading Robbins and his team to feel they were doing the prime minister’s bidding by disregarding concerns and approving his clearance regardless.

Meanwhile, Lord Gus O’Donnell, former head of the civil service, wrote in The Times newspaper that Starmer now faced “one of the worst crises in relations between ministers and mandarins of modern times”.

He added: “The dismissal of Sir Olly risks having a serious and sustained chilling effect on serving and prospective civil servants.”

The outcry over the Mandelson appointment is leaving Starmer in a vulnerable position.

Losses at the May 7 elections could open the premier up to leadership challenges, with the Sun reporting that Manchester Mayor Andy Burnham and former Deputy Prime Minister Angela Rayner held a “secret meeting” on Friday

Tyler Durden

Mon, 04/20/2026 – 08:35

Xi Urges Immediate Opening Of Hormuz Strait For First Time, In Call With Saudi Crown Prince

Xi Urges Immediate Opening Of Hormuz Strait For First Time, In Call With Saudi Crown Prince

China’s President Xi Jinping on Monday demanded the uninterrupted passage of vessels through the Strait of Hormuz in a phone call with Saudi Arabia’s Crown Prince Mohammed bin Salman, state news agency Xinhua reports. He urged the normalization of shipping traffic after about 50 days of disruption which obviously and significantly impacts Chinese oil imports.

“Normal navigation through the Strait of Hormuz should be maintained, this is in the shared interests of regional countries and the international community,” Xi said, in the statement also carried by AFP. He called for an immediate, comprehensive ceasefire and insisted disputes be resolved through political and diplomatic means.

He added that China will deepen strategic mutual trust with Saudi Arabia and expand practical cooperation.

South China Morning Post observes that it was “the first time the Chinese leader had called for the reopening of the strategically vital waterway, which has been repeatedly blockaded since US-Israeli strikes on Iran began on February 28.”

China imported 5.86 million tons of crude oil from Saudi Arabia, down 10% from February, according to customs data released Monday.

As for where things stand on the negotiations front, Iran hesitated over sending diplomats to Pakistan for a second round of peace talks after the US maintained a blockade of the Strait of Hormuz and seized an Iranian vessel, after apparently firing on it, undermining prospects for a breakthrough to end the war. Initially it appeared to shut the door on second talks, however per Associated Press Monday morning:

Iranian authorities have expressed willingness to send a delegation for a second round of talks in Islamabad this week, two Pakistani officials said Monday.

The officials, who spoke on condition of anonymity because they were not authorized to brief the media, said there is cautious optimism that delegations from both Iran and the United States could travel to Islamabad.

The US side would reportedly once again be headed up by Vice President JD Vance – who during the first round cut out early after a serious impasse was reached on the nuclear issue.

The tumultuous weekend events followed Iranian Foreign Minister Abbas Araghchi having posted on X on Friday that the Strait of Hormuz was “completely open”. By Sunday morning, Bloomberg ship tracking data had showed tanker traffic through the Strait of Hormuz was largely ground to a halt. Also, the prior 24 hours had seen multiple incidents of tankers making U-turns, and added to all this a senior Iranian official renewed threats to close the Bab al-Mandeb Strait.

According to a quick review of some other developments Monday morning and per emerging market data, China will import a record volume of US ethane this month as petrochemical producers switch feedstocks after the Middle East war disrupted critical supplies.

Recall that by mid-March Trump was actually asking for China’s help to get the blocked Strait of Hormuz reopened…

Trump said China should help reopen the Strait of Hormuz, arguing Beijing depends heavily on oil flowing through the waterway.

“I think China should help too because China gets 90 per cent of its oil from the Straits.”

He warned he wants Beijing’s position before his planned… pic.twitter.com/ZbtxAppcqO

— Clash Report (@clashreport) March 16, 2026

And in the broader region, Singapore is securing additional liquefied natural gas from outside the Middle East as the conflict in Iran constrains regional supply, according to a government body. India authorized more Russian insurers to cover vessels calling at its ports and extended permits for others as the closure of the Strait of Hormuz disrupts energy shipments from the Persian Gulf.

The International Energy Agency has meanwhile said that global power consumption rose 3% last year, driven in part by rapid demand growth from electric vehicles and data centers, according to the International Energy Agency.

Tyler Durden

Mon, 04/20/2026 – 08:05

Psychedelic Stocks Soar After Trump Order; RBC Says Commercialization Path Could Accelerate

Psychedelic Stocks Soar After Trump Order; RBC Says Commercialization Path Could Accelerate

Psychedelic drug stocks soared in premarket trading in New York after President Trump signed an executive order aimed at accelerating research and expanding access to therapies used for post-traumatic stress disorder (PTSD).

“The executive order I’m signing, we’re actually signing the executive order today, is really a moment,” Trump said at the signing event. “These treatments are currently in the advanced stages of clinical trials to ensure that they’re both safe and effective for the American patients.”

President Trump signed an executive order directing the FDA to expedite review of psychedelic drugs like ibogaine, which advocates say could treat PTSD and other mental health conditions https://t.co/vBk8EoguVF pic.twitter.com/AEW6V2merr

— Reuters (@Reuters) April 18, 2026

Trump’s order, signed on Saturday, directs the FDA to prioritize review of certain breakthrough-designated psychedelic therapies, expands potential access under the Right to Try Act, commits at least $50 million in federal funding for state partnerships, and encourages closer coordination among HHS, the FDA, the VA, and private-sector researchers.

“In many cases, these experimental treatments have shown life-changing potential for those suffering from severe mental illness and depression, including our cherished veterans,” Trump said, citing the veteran suicide rate.

The order also instructs the Justice Department to move quickly on rescheduling any psychedelic-based product that successfully completes Phase 3 trials and receives FDA approval.

Trump continued, “And the nice part is we’re actually doing this early, but it has been going on. Research has been going on for quite some time. But, you know, usually with things like this, nothing ever happens, no matter how the research ends up, but we’re changing that. This order will clear away unnecessary bureaucratic hurdles, improve data sharing among the FDA and the Department of Veterans Affairs, and facilitate fast rescheduling of any psychedelic drugs that become FDA-approved.”

Accelerating Medical Treatments for Serious Mental Illness🇺🇸@JoeRogan: “For 56 years we’ve lived under those terrible conditions. We’re free of that now. Thanks to all these people… and thanks to President Trump.” https://t.co/j1tkGACSM7 pic.twitter.com/aQmZl3z4PG

— The White House (@WhiteHouse) April 18, 2026

Oppenheimer analyst Jay Olson told clients that Trump’s weekend executive order “represents a structural inflection point for the U.S. psychedelics sector by facilitating research, regulatory timelines, and patient access, which reinforces our positive outlook.”

In response, psychedelic drug stocks in premarket trading, such as Compass Pathways jumped 24.5%, Atai Beckley gained 28%, Definium Therapeutics rose 13%, and GH Research added 17%.

“The path to commercialization could be even faster now,” RBC analyst Brian Abrahams told clients, adding that the executive order “accelerates psychedelics as the key next wave of mental health treatments.”

Abrahams’ research covers Definium Therapeutics, Compass Pathways, and GH Research. He said those stocks are likely to benefit the most.

Jefferies analyst Andrew pointed out that with the federal government increasingly aligned on psychedelics, “investor mindshare should rise meaningfully ahead of potential approvals in 2027-30.”

This marks another big win for the psychedelic space.

Tyler Durden

Mon, 04/20/2026 – 07:45

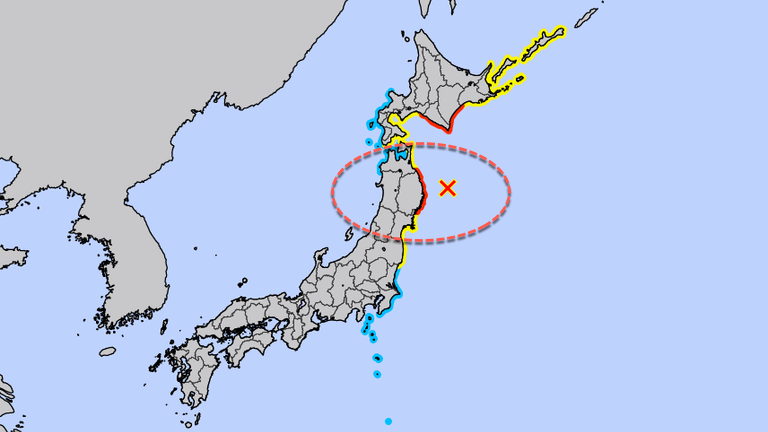

Powerful 7.5-Magnitude Quake Hits Northern Japan, Triggers Tsunami Warnings

Powerful 7.5-Magnitude Quake Hits Northern Japan, Triggers Tsunami Warnings

A powerful and shallow 7.5-magnitude earthquake struck off Japan’s northeast coast, triggering a tsunami at Kuji Port in Iwate Prefecture.

Public broadcaster NHK initially warned that a tsunami up to 10 feet high was expected to hit the Iwate area on Honshu’s main island. However, so far, it has been reported to be about 31 inches high.

The quake was reported shortly before 17:00 local time, rattled towers as far away as Tokyo, and forced the suspension of Shinkansen high-speed rail services in Iwate, NHK said.

Prime Minister Sanae Takaichi said the government had mobilized an emergency task force and urged citizens in affected areas to evacuate.

“Possible damage and casualties are now being looked into,” Takaichi told reporters in Tokyo.

Japan sits on the Pacific “Ring of Fire,” one of the world’s most seismically active zones, where multiple tectonic plates collide and generate earthquakes.

Since the 2011 Fukushima disaster, when a 9.0-magnitude quake and tsunami sparked triple reactor meltdowns, Japan has overhauled its response and evacuation systems to improve disaster readiness.

NHK cited the Tokyo Electric Power Company as saying that no issues were reported at the Fukushima Daiichi and Fukushima Daini nuclear power plants.

The Japan Meteorological Agency warned that aftershocks are possible over the next week and could be similar in size to the quake recorded earlier today.

Tyler Durden

Mon, 04/20/2026 – 06:55

From Leverage To Liability: The Hormuz Strait Is Now Iran’s Biggest Weakness

From Leverage To Liability: The Hormuz Strait Is Now Iran’s Biggest Weakness

For half a century, the Strait of Hormuz was Iran’s weapon. Today, it is its noose.

The mathematics of energy have flipped, and with them the balance of coercive power in the Persian Gulf.

Iran’s implicit deterrent was geographic, spanning from the tanker wars of the 1980s to the sanctions standoffs of the 2010s. Almost 20% of global seaborne oil, and a similar share of liquefied natural gas, passes through the Strait. The formula was simple: any military confrontation that threatened the Tehran regime risked a closure that would halt trade supplies, spike crude prices, bleed Western consumers, and, above all, inflict pain on the United States, who was the world’s largest oil importer.

The strait served as Tehran’s insurance policy and its most powerful bargaining tool. The threat was predicated on the regime’s belief that it could block everyone except its exports. The Iranian regime revealed its biggest weakness by constantly threatening to damage the global economy through a shutdown of the Strait. In reality, a total shutdown has the most severe impact on Iran.

Almost 90 per cent of Iran’s crude exports, and about 80 per cent of its total exports, depend on the transit through Hormuz. Around 25 per cent of Iranian GDP and 60 per cent of government revenues depend completely on having the Strait open.

Before the war, Iran was exporting roughly 1.7 million barrels per day, receiving around $160 million in daily revenue from exports via the Strait. Thus, Trump’s full closure of the Strait costs Tehran hundreds of millions of dollars a day in losses, not accounting for the additional fiscal and currency consequences in a country already facing an economic disaster with 40–50% inflation. The complete dependence on the Strait of Hormuz also adds to another weakness: 95% of Iranian crude at sea is sold to a single buyer, China. Tehran is not selling into a diversified and open market. Its exports are sold to a monopsony that demands large discounts, between 10 and 11 dollars per barrel.

These weaknesses were visible long before the war. Capital flight reached $15 billion in the first half of 2025 alone; the rial collapsed against the dollar, and the government’s budget, which allocates 51 per cent of oil revenues to the Islamic Revolutionary Guard Corps, became even more dependent on a single export route it could not afford to close. When the war began, Iranian crude shipments collapsed by 94%. Then, the United States’ decision to block all Iran export vessels showed that Iran’s chokepoint had become self-choking.

In the past 30 days, 80% of the essential volumes that moved through the Strait have been rerouted or offset by other oil producers, including US record exports.

The world is very different from what the Iran regime thought. In 2025, U.S. crude oil production hit a new annual record of 13.6 million barrels per day, making the United States the world’s largest producer but also the biggest exporter. The United States shipped 5.2 million barrels per day of crude and 7.2 million barrels per day of petroleum products in March 2026, both global records. For the first time, America exported more petroleum than it imported, by a net margin of almost 2.8 million barrels per day, according to the EIA. Total US liquids production now exceeds that of Saudi Arabia and Russia combined. On the natural gas side, U.S. LNG exports reached well over 15 billion cubic feet per day, surpassing Qatar and Australia to make the United States the world’s largest liquefied natural gas exporter, while U.S. dry gas production exceeds the combined output of Russia, Iran, and China. Furthermore, the United States is also the world’s largest producer of nuclear electricity, at roughly 30 per cent of global generation, and a global leader in renewable energy.

When President Trump could say in April 2026 that the United States was “clearing the Strait as a favour to countries around the world, including China, Japan, Korea, and Germany,” the framing was an accurate description of who needs Hormuz open and who does not. Only 4% of the traffic through the Strait goes to the United States, according to SP Global.

According to the International Energy Agency, throughput at Hormuz collapsed from its long-run average of about 20 million barrels per day to 3.8 million since the beginning of the war through the second week of April. Daily ship transits fell roughly 95 per cent. The Tehran regime, in a gesture more theatrical than realistic, attempted to levy a $2 million toll on each vessel crossing the strait, without understanding that the move showed desperation instead of leverage.

The US response has been the most important measure deployed against Iran in two decades of standoffs. Operation Economic Fury established a full naval blockade of Iranian ports. Iranian naval losses in the first 38 days of combat exceeded 150 vessels. The ceasefire framework under negotiation requires Iran to reopen Hormuz, but the US maintains control. Thus, negotiations revolve around Iranian dismantlement, not American concessions.

The lesson is not just that Iran miscalculated but that it massively underestimated its obvious weaknesses. The United States is not a hostage of the Gulf; it is the guarantee of its safe sea lanes. Europe is tied to U.S. LNG while keeping a substantial Russian dependence, which complicates its energy security and makes it vulnerable to fluctuations in supply and price from both sources. Asia’s largest economies, particularly China, are suffering the marginal cost of a Hormuz disruption, which has led to increased energy prices and supply chain uncertainties that further exacerbate their economic challenges. Iran’s economic nightmare has only started.

Three important factors must be considered.

First, the traditional Hormuz risk premium in Brent, which refers to the additional cost added to oil prices due to geopolitical tensions in the Strait of Hormuz, is structurally smaller than in the 2010s because U.S. supply can absorb shocks that previously had no substitute. The Brent price is lower in real and nominal terms than in the 2008, 2018, or 2022 peaks.

Second, the strength of American energy, including economics, export infrastructure, and LNG capacity, has become a key global geopolitical variable, influencing global energy prices and the strategic decisions of other nations.

Third, Iran’s economy has not only suffered damage; it has also been demolished, and its extremely weak fiscal position indicates that it cannot sustain the threat posture in Hormuz.

The Strait of Hormuz remains the world’s most important chokepoint. However, a chokepoint hurts whoever depends on it most, and Iran relies on it completely. The United States does not.

The geopolitical advantage that Tehran once held has now become its greatest weakness, likely leading to the disappearance of the regime’s effective bargaining power.

Tyler Durden

Mon, 04/20/2026 – 06:30

https://www.zerohedge.com/geopolitical/leverage-liability-hormuz-strait-now-irans-biggest-weakness

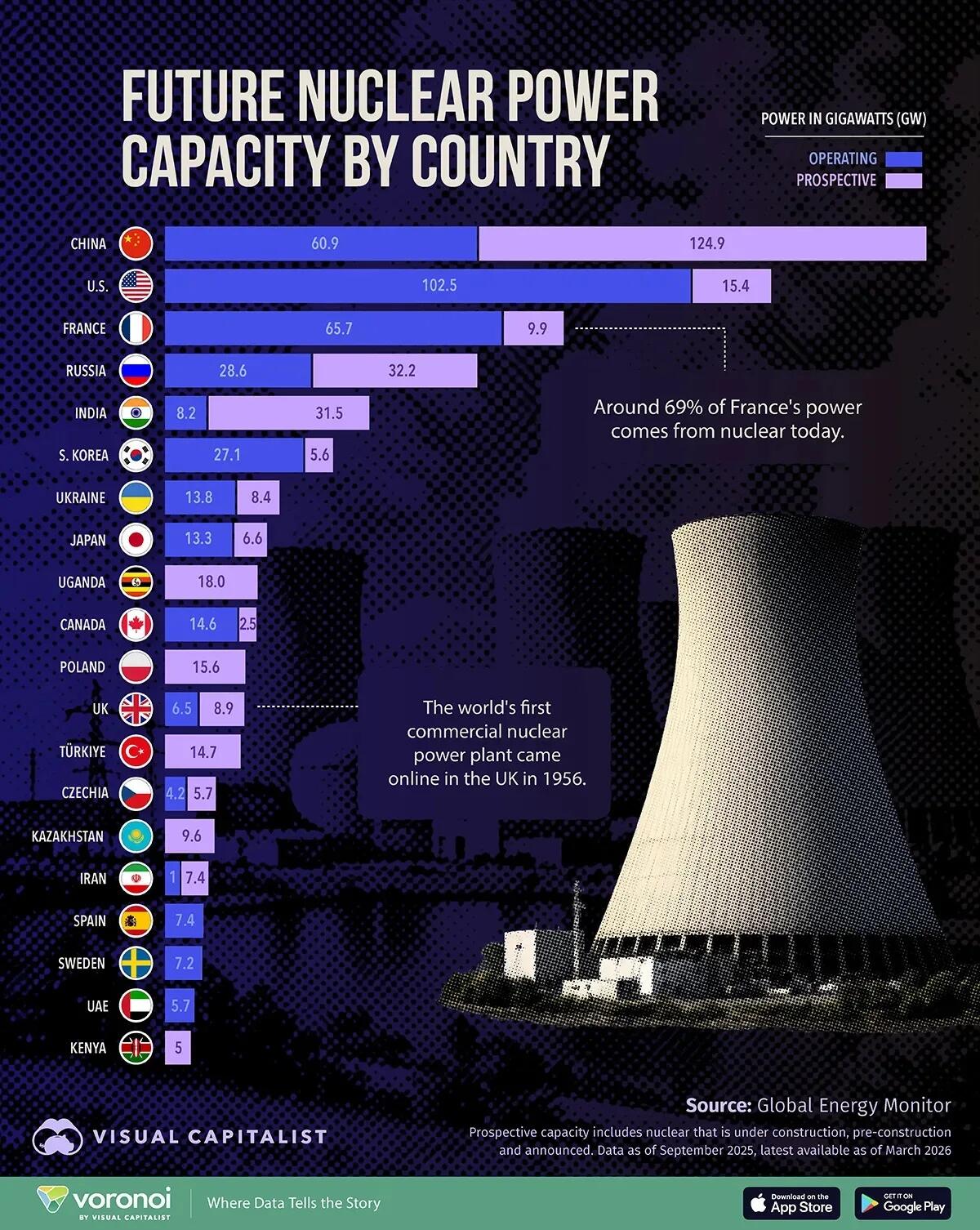

These Are The Countries Building The Most Nuclear Power

These Are The Countries Building The Most Nuclear Power

China is set to become the world’s dominant nuclear power producer.

Based on existing and planned projects, its total capacity could reach nearly 186 gigawatts, far surpassing the U.S., which currently leads globally. This shift reflects a broader push to secure reliable, low-carbon energy as electricity demand rises.

This chart, via Visual Capitalist’s Tasmin Lockwood, ranks countries by current and prospective nuclear capacity, using data from Global Energy Monitor.

How Nuclear Energy Is Set to Scale by Country

The U.S. currently leads nuclear energy production with a capacity of 102,475 megawatts, exceeding France by more than 35,000 MW.

China ranks third today at 60,898 MW, but that is set to change as new plants come online.

Dive into the data, which includes sites of any capacity as of September 2025, below:

This shift has major geopolitical implications. Countries that expand nuclear capacity can reduce reliance on imported fossil fuels while strengthening energy security and grid stability.

If all planned projects are completed, China will lead with 185,812 MW, followed by the U.S. at 117,910 MW and France at 75,590 MW.

France remains a historic leader in nuclear energy, with around 69% of its electricity generated from the technology.

The UK was home to the world’s first commercial nuclear power plant, which came online in 1956, but later scaled back its use of nuclear. The government is now aiming for a “golden age of nuclear,” though current commitments totaling 15,394 MW would rank the country just 12th globally.

Of the 17 countries with zero installed capacity today, Uganda is set to scale up the most to 18,000 MW, followed by Poland with 15,612 MW and Türkiye with 14,700 MW.

Betting on Nuclear Fusion and Fission

Today’s nuclear expansion is centered on fission, the technology that powers all existing reactors and accounts for about 10% of global electricity generation. While mature, it is evolving through smaller, modular designs that aim to reduce costs, improve safety, and speed up deployment.

This helps explain why much of the prospective capacity in the chart includes not only large-scale plants, but also a growing wave of smaller reactors backed by governments and private capital.

At the same time, nuclear fusion, the process that powers the sun, remains a long-term ambition. Despite rising investment and recent technical progress, it has yet to reach commercial scale.

For now, the global nuclear buildout is firmly rooted in fission, as countries prioritize reliable, low-carbon power that can be deployed within the next decade.

To learn more about nuclear, check out this graphic ranking the countries building the most reactors.

Tyler Durden

Mon, 04/20/2026 – 05:45

https://www.zerohedge.com/energy/these-are-countries-building-most-nuclear-power

Europe Faces Summer Jet Fuel Crisis As Iran War Slashes Supply

Europe Faces Summer Jet Fuel Crisis As Iran War Slashes Supply

Authored by Tsvetana Paraskova via OilPrice.com,

Europe faces an imminent jet fuel crisis as the Iran war and Hormuz disruption cut off key Middle Eastern supplies.

Long-term refinery closures and rising import dependence have left Europe highly exposed, with limited alternatives and growing competition from Asia.

Airlines are already cutting capacity and warning of higher fares, with potential flight cancellations looming as fuel shortages intensify.

Accelerated refinery closures in the past decade and increased dependence on kerosene from the Middle East have exposed Europe’s energy supply vulnerability once again.