Category: News

Parabolic Semiconductor Rally Is Pricing In 2028 Already

Parabolic Semiconductor Rally Is Pricing In 2028 Already

Authored by Lance Roberts via RealInvestmentAdvice.com,

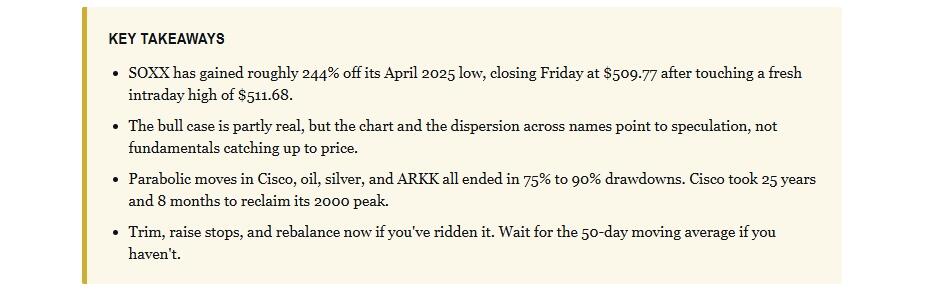

The parabolic semiconductor rally crossed a line this week. SOXX, the iShares Semiconductor ETF, closed Friday at $509.77 after touching a fresh intraday high of $511.68. That’s a gain of roughly 244% from the April 2025 low of $148.31. Most of that move has been compressed into the last two months alone. Since mid-March, SOXX has tacked on another 58%. The chart is now textbook parabolic. And parabolic charts almost never end politely.

If you wanted a real-time stress test of how fragile this move is, you got one this week. Semiconductors took a -2.86% hit on Thursday on softer Iran headlines, with Broadcom and Micron dragging. By Friday’s open, the dip was already being bought aggressively. A stronger-than-expected April jobs report (115,000 vs. 65,000 expected) and renewed peace-deal optimism sent the Nasdaq up 1.71% on the day, with SOXX printing a new intraday high before the close. That’s not a market digesting risk. That’s a market refusing to take “no” for an answer.

I’ve watched this movie before. After 30 years of cycles, the ending is rarely a surprise. The setup, however, is almost always sold as “this time is different.” It isn’t. In fact, every parabolic semiconductor rally in modern memory has ended the same way, and there’s no reason to expect a kinder math this round.

Where The Parabolic Semiconductor Rally Stands Today

Start with the math, because it’s doing the talking. SOXX is currently trading 62% above its 200-day moving average and 34% above its 50-day. Readings that stretched are the back end of a move, not the middle. The slope of the advance has steepened in each successive month. That is the signature of a momentum trade pulling in late buyers, not of fundamentals catching up to price.

Look across the complex, and the dispersion is striking. Micron is up nearly 1,000% off its April 2025 low. AMD is up roughly 450%. Nvidia, the index’s anchor, is up “only” 140%. Notably, the stocks that crashed hardest a year ago have rallied the most in the recovery. That’s exactly how late-cycle chase trades behave. The trash leads the way up because it has the largest short position to cover and the most leverage to a narrative. In other words, this parabolic semiconductor rally is now being driven by the names with the worst fundamentals, not the best.

Notice in the chart above how the slope of the advance has steepened in each successive month. The early move off the April low was a recovery. The middle was a trend. What we have now is something else.

Real Demand Or A Speculative Frenzy?

I get the bull case. AI capex is real. Hyperscaler orders are real. Foundry utilization is real. Nvidia, Broadcom, and TSMC are delivering numbers that justify premium multiples. So far, so good. The shortage narrative around HBM memory and leading-node capacity has actual data to back it up, and that’s the part of the story bulls keep pointing to.

However, here is the problem with the current setup. A real fundamental story doesn’t require a parabolic chart to validate it. In fact, fundamentals tend to drag prices up the trend line, not push them through the ceiling. When a “shortage” narrative arrives at the same moment that the worst-quality names in the sector are leading the index higher, that’s not fundamentals at work. That’s the narrative being recycled to justify a move that has already happened. Indeed, the parabolic semiconductor rally we’re seeing right now bears almost none of the hallmarks of a fundamentals-led advance.

Look at the dispersion again. If this were a shortage-driven, fundamentals-led rally, the leaders would be the names with the cleanest demand visibility. Instead, the laggards from a year ago are the runaway winners. Micron up 1,000%. AMD up 450%. Nvidia, the company that actually owns the AI capex story, up “only” 140%. Quality is being left behind because the chase is no longer about earnings. It’s about beta.

Here’s the part that should bother bulls the most. SOXX is trading at multiples that already reflect strong 2026 earnings. The current rally has likely already fully priced in 2026 earnings. From here, you are paying for 2027 and 2028 growth in a sector where the cycle has not been repealed. Semiconductors are still cyclical. Always have been. The day the AI capex cycle hiccups, even briefly, is the day this chart breaks.

Make no mistake, the rally has been spectacular. The exit will be too. Importantly, we have decades of data on what happens when speculative momentum compresses years of expected returns into months. The pattern is remarkably consistent across asset classes and across decades. As a result, the path forward for this parabolic semiconductor rally is not a mystery, even if the timing is.

The consistent thread is that parabolic charts don’t unwind through gentle rotation. They snap. The exit is faster than the entry, and the stocks that led the rally on the way up tend to lead the carnage on the way down. The investors most hurt are not the ones who avoided the move entirely. They’re the ones who showed up late, on the back of the same shortage narratives that are now circulating around semiconductors.

Recovery time is the part most investors underestimate. Cisco, the poster child of the dot-com semiconductor adjacency, only reclaimed its March 2000 peak on December 10, 2025. That’s 25 years, 8 months, and 13 days from peak to recovery. The business kept growing throughout. Earnings kept compounding. Revenues nearly quintupled. The stock simply paid forward too many years of growth at the top, and the math demanded a quarter century to absorb the excess.

Anyone who bought at the 2000 peak earned a nominal break-even after factoring in dividends, but lost meaningfully to inflation along the way. That’s not a recovery story. That’s a generational opportunity cost. ARKK, which ran +360% into its 2021 peak, still trades below it five years later. Different decades, different assets, but the pattern holds. Speculative tops resolve through painful, prolonged drawdowns, not graceful rotations.

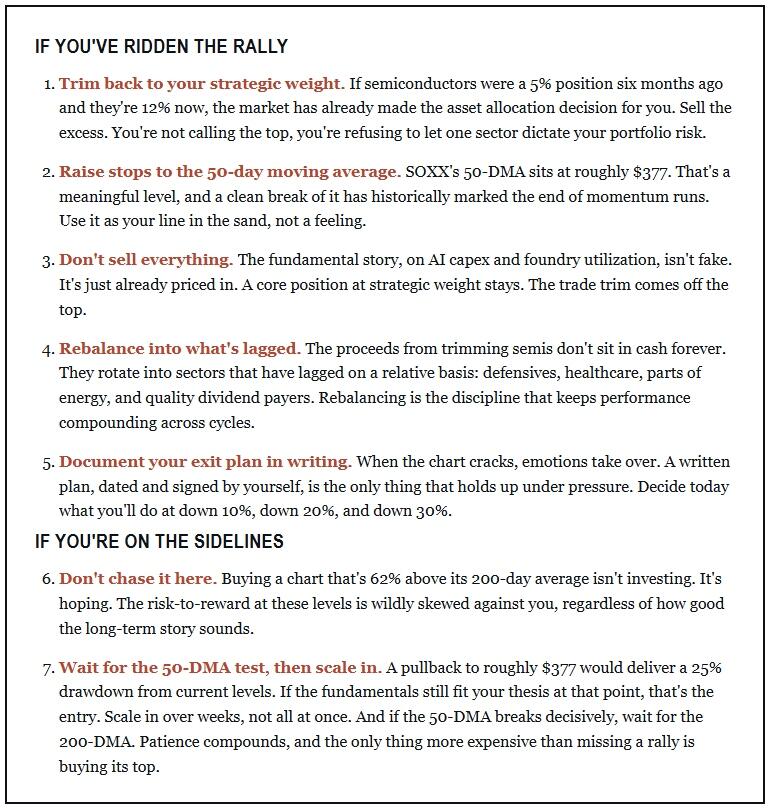

The Risk Management Playbook

So what do you actually do? Of course, the answer depends on whether you’ve ridden this rally or you’re staring at the chart wondering if it’s too late to participate. Honestly, the answer for most investors is the same in either case. You don’t have to be all-in or all-out. You just can’t let the position size make the decision for you.

Here is the playbook we’re using for clients right now. First, five points if you’re already invested. Then, two if you’re not.

The Bottom Line

The semiconductor rally has been one of the most extraordinary moves of the post-COVID era. The fundamentals supporting the early stages of the move were real. The fundamentals supporting the most recent leg are increasingly imaginary. SOXX has likely fully priced in 2026 earnings already, and the stocks leading the index higher are no longer the ones with the cleanest demand stories.

Of course, parabolic charts rarely give back gracefully. Cisco, oil, silver, and ARKK all showed that exits come faster than entries, and recovery can take years to decades. The parabolic semiconductor rally has been spectacular. The exit will be too. The question isn’t whether the chart cools off. The question is whether you’ve prepared your portfolio for it before it does.

Tyler Durden

Mon, 05/11/2026 – 11:45

https://www.zerohedge.com/markets/parabolic-semiconductor-rally-pricing-2028-already

Moderna Extends Rally After Two More Cruise Ship Passengers Test Positive For Hantavirus

Moderna Extends Rally After Two More Cruise Ship Passengers Test Positive For Hantavirus

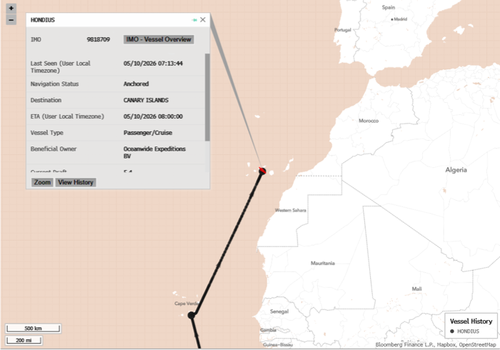

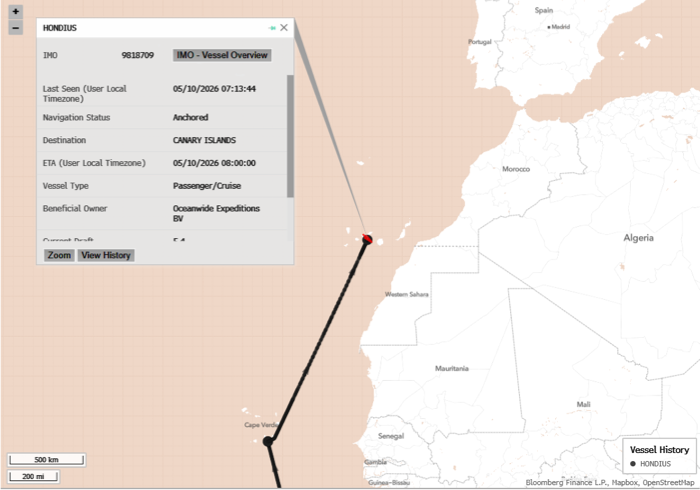

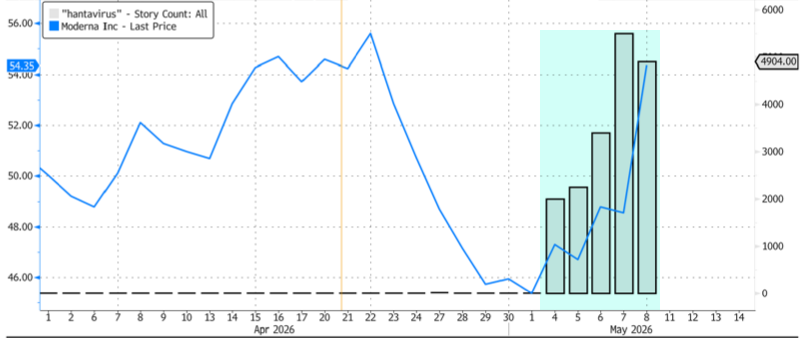

Moderna shares are up another 7% in premarket trading, as renewed alarm over the hantavirus-plagued MV Hondius cruise ship energizes investor focus on the company’s vaccine pipeline.

The latest news catalyst: Two passengers evacuated from the cruise ship on Sunday tested positive, reinforcing concerns that the outbreak remains active.

The Hondius is moored at a port in Spain’s Canary Islands.

On Sunday, passengers were escorted off by personnel in protective gear before being flown home on government and military aircraft.

Seventeen Americans were taken to the University of Nebraska Medical Center, with one sent to the Nebraska Biocontainment Unit and the others placed in the National Quarantine Unit for monitoring.

The outbreak has killed three people, with five additional infections among passengers who had already left the ship.

Last Friday, we asked whether the vaccine trade is back, given news from beleaguered Moderna that it had started work on an early-stage vaccine targeting hantaviruses.

The surge in corporate media coverage of hantavirus has sent Moderna shares up nearly 20%. The latest news on Monday sent the stock up another 7% in premarket trading in New York.

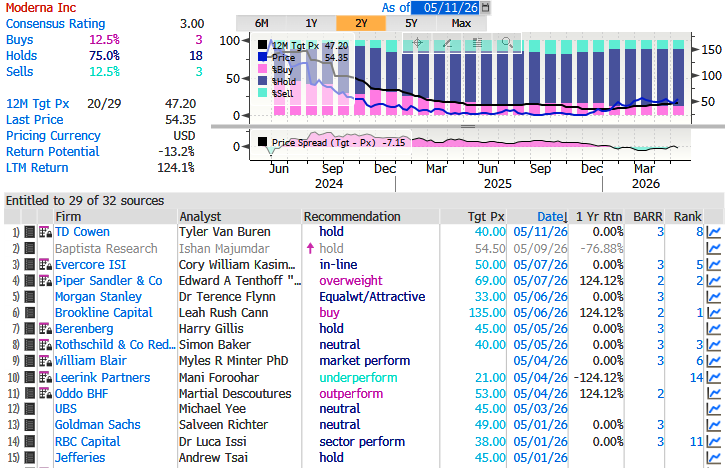

Longer timeframe for Moderna stock:

Polymarket odds of a hantavirus pandemic this year are about 8%.

Hantavirus pandemic in 2026?

Yes 8% · No 92%

View full market & trade on Polymarket

Will hantavirus be enough to change Wall Street’s neutral sentiment around the pharma stock?

Global health officials are honing in on Argentina as the likely source of the virus, since the ship departed from there on April 1. Patient zero was a Dutch man who had traveled in Argentina and South America before boarding the ship. The Dutchman and his wife have since passed.

Tyler Durden

Mon, 05/11/2026 – 11:25

Energy Secretary Open To Suspending US Gas Tax As Pump-Rage Surges

Energy Secretary Open To Suspending US Gas Tax As Pump-Rage Surges

With Americans increasingly incensed over the steadily climbing cost of refueling their vehicles, the US Energy secretary says he’s “open to all ideas” to bring down the price at the pump, to include suspending the federal gas tax.

This is bad, right? pic.twitter.com/Sw3UGcW31q

— Rothmus 🏴 (@Rothmus) May 11, 2026

“All measures that can be taken to lower the price of at the pump and lower the prices for Americans, this administration is in support of,” Chris Wright told Meet the Press on Sunday. “We’re releasing oil from our strategic petroleum reserves and getting 30 other nations to do that in coordination with us…We revised the EPA regulations on summer gasoline blend to make it easier for American refineries to produce more gasoline.”

“I think it’s a great idea,” said President Trump, “for a period of time.”

“We’re going to take off the gas tax for a period of time, and when gas goes down, we’ll let it phase back in.”

Suspending the tax may only trigger more resentment about the administration’s war of choice: Once they learn the tax only accounts for 18.4 cents per gallon of gas and 24.3 cents for diesel, Americans may view the limp gesture as merely adding insult to injury. In a recent poll, 81% of respondents said gas prices are straining their household finances. It’s a bipartisan feeling: 79% of Republicans felt that way. With the midterms now less than six months away, the political impact could be significant — 81% of independents say Trump is to blame to some extent.

Americans expressing their frustration with gas prices pic.twitter.com/Lm6ofNS9qf

— Molly Ploofkins (@Mollyploofkins) May 9, 2026

The administration has been flailing in its messaging on gas prices. In mid-March — two weeks after Trump teamed up with Israel to launch a war on Iran — Wright told Meet the Press that Americans could expect “a few more weeks” of elevated prices, with a “very good chance” they would drop under $3 by summer. In mid-April, Wright told CNN that gas may not be below $3 “until next year.” Around the same time, however, Trump told Maria Bartiromo that “gasoline is coming down very soon and very big.” Now, 10 weeks into the war, and with summer just around the bend, the national average gas price is $4.52; diesel is $5.65. That’s about a 50% increase since the US-Israeli war on Iran began.

🚨 TRUMP: “Gas prices are WAY down” https://t.co/KGnWO4WnYz pic.twitter.com/uhL18QxZXd

— NoLimit (@NoLimitGains) May 10, 2026

Prudently refusing to dig himself any deeper on Sunday, Wright told Meet the Press, “I can’t make any predictions about oil prices or gasoline prices...when we start to get free flow of traffic through the Strait of Hormuz, energy prices will come down.” With Trump rejecting the latest counter-offer from Iran, there’s little reason to think that free flow will be happening anytime soon.

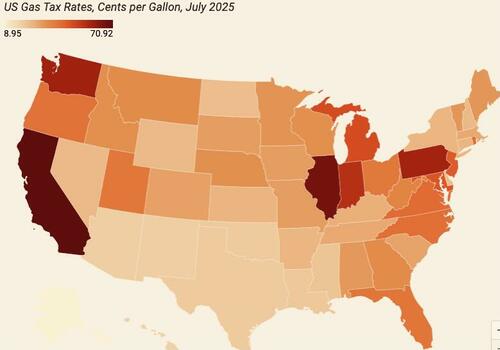

For most Americans, state fuel taxes are a bigger factor than the federal tax — particularly in those states where leftists dominate government. California’s gas tax is the worst, at 70.9 cents per gallon, followed by Illinois (66.4 cents) and Washington (59 cents).

State gas taxes vary widely: California’s 70.9-cent-per-gallon tax is a big reason why the average gas price there is $6.15 (Tax Foundation graphic)

Some states have reduced or suspended their fuel taxes to buffer their residents from that effect of the Trump-Netanyahu war on Iran. Last week, Indiana Gov. Mike Braun extended a suspension of the state sales tax on gas, and paused the gas tax too. Together, that cuts 59.3 cents per gallon from the pump price. In March, Georgia suspended its 33-cent tax, but that suspension ends on May 18, and the legislature is out of session. Utah trimmed its tax by 6 cents — but that relief doesn’t take effect until July 1. Earlier this month, Michigan Gov. Gretchen Whitmer endorsed a federal tax suspension, but (shocker!) doesn’t want to do anything with her state’s 52.4-cent tax, which is the sixth-highest in the country.

Tyler Durden

Mon, 05/11/2026 – 10:55

https://www.zerohedge.com/markets/energy-secretary-open-suspending-us-gas-tax-pump-rage-surges

“You Just Can’t Earn A Billion Dollars”: AOC Declares Billionaires To Be A Capitalist Myth

“You Just Can’t Earn A Billion Dollars”: AOC Declares Billionaires To Be A Capitalist Myth

This week, Rep. Alexandria Ocasio-Cortez (D-N.Y.) came up with the best reason to tax billionaires: They do not actually exist.

On a podcast, Ocasio-Cortez declared with all the certainty of a freshman in a Smith College political science course that the notion of a self-made billionaire is simply a fantasy, because “you just can’t earn” a billion dollars. It is only the latest in a series of socialist fables that are being dressed up as economic facts.

The difference is that this fable, if told often enough, could become true.

In suggesting that true billionaires are a capitalist myth, Ocasio-Cortez is suggesting that people like Elon Musk and Jeff Bezos really did not earn their wealth and, therefore, it is really not their money.

“There’s a certain level of wealth and accumulation that is unearned. You can’t earn a billion dollars. You just can’t earn that. You can get market power, you can break rules, you can abuse labor laws, you can pay people less than what they’re worth, but you can’t earn that.”

In other words, you can only make a billion dollars through theft and exploitation rather than actual entrepreneurial enterprise. This statement comes as support builds for the California billionaires’ tax which, even before it has a chance to pass in November, has already cost the state trillions due to an exodus of these billionaires.

In my book, “Rage and the Republic,” I discuss common myths spread by the left to fuel economic factionalism.

One common myth is that the “wealthy do not pay their fair share of taxes.” In truth, the top ten percent of taxpayers pay the vast majority of taxes in the U.S. In the book, I also dispel the claim that most millionaires inherited their wealth or came from privileged backgrounds.

These myths are designed to make redistribution schemes more palatable. And Democrats are ramping up the “eat-the-rich” rhetoric ahead of the midterms in pushing both millionaire and billionaire taxes. Democrats from Washington to Virginia are pushing millionaire taxes, and the mere conversation has already set off a stampede of high-earning taxpayers to red states like Texas and Florida, which have no state income tax.

It was also evident in this week’s California gubernatorial debate. Candidate Katie Porter (D) said she opposes the billionaire’s tax because it would not go far enough. Porter then pressed the only billionaire in the group, Tom Steyer, who has been moving to the far left to grab voters in the wake of the departure of former Rep. Eric Swalwell (D-Calif.) as a candidate. Steyer said that he supports the billionaire tax but would want to go even further.

Steyer has spent a fortune of his own money on this race, apparently to convince Democratic primary voters that he is some kind of red billionaire in the mold of a George Soros or Neville Roy Singham. Good luck with that — after spending roughly $150 million of his own money, Steyer is still languishing between 12 and 18 percent support.

Of course, Steyer was not asked if he believes that real billionaires such as himself exist. Yet he has already apologized for making considerable money on private prisons, including those used to hold undocumented immigrants.

Ironically, in finance, a “unicorn” is a company worth more than $1 billion dollars, a term coined by venture capitalist Aileen Lee to capture the rare and almost magical status of such enterprises.

Conversely, Ocasio-Cortez’s unicorn myth is part of a general denial of economic realities that has taken hold on the left. The cost of these policies is borne by workers, who are being left to eat soundbites.

Democrats have sold voters on raising minimum wages as high as $30 per hour, even though such policies cost thousands of jobs. Sen. Elizabeth Warren (D-Mass.) and former Transportation Secretary Pete Buttigieg bragged about blocking a merger of JetBlue and Spirit Airlines, claiming that it would create cheaper flights and better jobs. Spirit has now been forced to close its doors, causing the loss of thousands of flights and jobs.

A rising generation of voters is eagerly devouring soundbites and promises of the “warmth of collectivism” from figures like New York’s socialist mayor, Zohran Mamdani. From promises of free buses to state-run grocery stores, voters are buying the same threadbare socialist schtick.

That was on display this week as socialist Seattle mayor Katie Wilson laughed when asked about the millionaires fleeing the city over rising taxes and crime. She delighted the crowd by mocking the departing millionaires with two words: “Like, bye!”

The last laugh, however, rests with those fleeing a city facing a projected deficit of $114 million. As Wilson faces major cuts in the city budget, she gleefully mocks those whose tax dollars the city will desperately need to close this gap if it is to maintain public services.

Ironically, Wilson and other Democrats are quickly making their myth a reality. Soon, there will be no billionaire unicorns roaming the land.

Even millionaires may become scarce, as these wealthy citizens move to less hostile states with less delusional leaders.

The solution to this exodus is equally predictable. Rep. Ro Khanna (D-Calif.), who has campaigned for a billionaire tax in his state while representing Silicon Valley, has also joined with socialist Bernie Sanders to push for a national billionaire’s tax — an effort to guarantee that there is no place to hide. This is the same approach that tanked the French economy under François Mitterrand after the wealthy fled that nation.

This is not, however, a time for economics or history. It is the time of fables. Ocasio-Cortez has thrived in the land of socialist unicorns.

She can even attend the ultra-rich Met Gala wearing an expensive “Tax-the-Rich” gown.

Like her dress, it is fashionable to deny that billionaires created their wealth. It is your money for the taking.

The result is that billionaires and even millionaires in states like New York may go the way of unicorns, fanciful creatures that once thrived in a land of jobs and growth.

Jonathan Turley is a law professor and the best-selling author of “Rage and the Republic: The Unfinished Story of the American Revolution.“

Tyler Durden

Mon, 05/11/2026 – 10:35

Aramco CEO Says Energy Market May Not Normalize Until 2027 Amid Billion-Barrel Supply Shock

Aramco CEO Says Energy Market May Not Normalize Until 2027 Amid Billion-Barrel Supply Shock

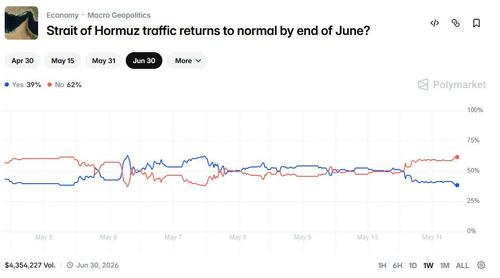

From the Trump administration’s recent Project Freedom push to mounting warnings from Wall Street analysts, security experts, energy strategists, and major oil company executives, there is a growing sense that the global energy market is quickly approaching a breaking point due to the heavily disrupted Strait of Hormuz.

There was good news over the weekend, as a Qatari LNG tanker transited the Hormuz chokepoint. However, a second tanker from the energy-rich Gulf country abruptly made a U-turn in the Strait early Monday, dashing hopes for any near-term normalization, especially since the U.S. and Iran have yet to reach a peace deal.

The countdown to global energy chaos is increasingly viewed in weeks, not months. If the maritime chokepoint remains impaired for the next several weeks, according to Frederic Lasserre, head of research at Gunvor, one of the world’s largest oil traders, then the “tipping point to something has to give is June.”

Warnings of incoming energy market turmoil continued on Monday, with the CEO of Aramco, formerly known as the Saudi Arabian Oil Company. Amin Nasser warned that the market could lose around 100 million barrels of oil each week if Hormuz remains closed.

Nasser told investors on an earnings call earlier today that if the Hormuz chokepoint is disrupted for another couple of weeks, then it would take the global energy market until 2027 to normalize.

Here are the most important comments from Nasser’s call with the analyst:

Energy Supply Shock Is Largest Ever Experienced

It’ll Take Months for Oil Market to Rebalance Even If Hormuz Reopens Today

Market to Normalize in 2027 if Hormuz Opening Is Delayed by Few More Weeks

Market Has Seen Supply Loss of About 1 Billion Barrel of Oil

Alternative Flows Bypassing Hormuz, Strategic Reserve Releases Partially offset that

Market Could Lose Around 100 Mln Barrels of Oil For Every Week

Demand Rationing to Continue As Long As Supply Remains Disrupted

Return to Demand Growth Expected to Be Robust If Trade Resumes

Demand Growth to Be Driven by Urgency to Ensure Security of Supply

Supply Chains Will Need Several Months to Return to Normal

Building on the countdown-to-energy-chaos theme, Morgan Stanley analyst Martijn Rats warned clients that the oil market is in a “race against time” as the maritime chokepoint remains heavily disrupted. He noted that global supply buffers, which have kept crude prices contained during the ten-week Iran war, are starting to come under pressure.

Rats said that nearly 1 billion barrels have already been lost, yet Brent crude futures have not exceeded 2022 levels because the market entered the crisis with spare supply buffers and because traders kept assuming Hormuz would reopen.

“The ability of the US to continue this elevated level of exports is hard to gauge but appears under more pressure,” the analyst noted, adding, “The United States’ 3.8m b/d increase in exports and China’s 5.5m b/d cut in imports have shielded the rest of the world from 9.3m b/d of tightness.”

Rats warned, “Even if the Strait reopened tomorrow, the time required to restart fields, repair refineries, and reposition tanker tonnage means the market is on track to lose another billion barrels over the balance of 2026.”

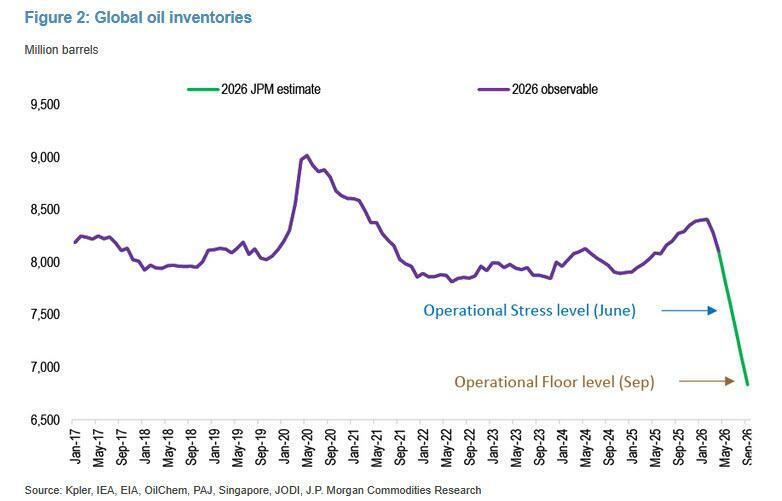

In a separate note, JPMorgan’s resident commodity expert, Natasha Kaneva, explained where the next phase of the global energy shock could unfold.

Kaneva’s chart on global oil inventories is truly shocking.

Overall, the warnings are piling up. If the maritime chokepoint remains shuttered through this month, real panic may begin then.

Tyler Durden

Mon, 05/11/2026 – 10:15

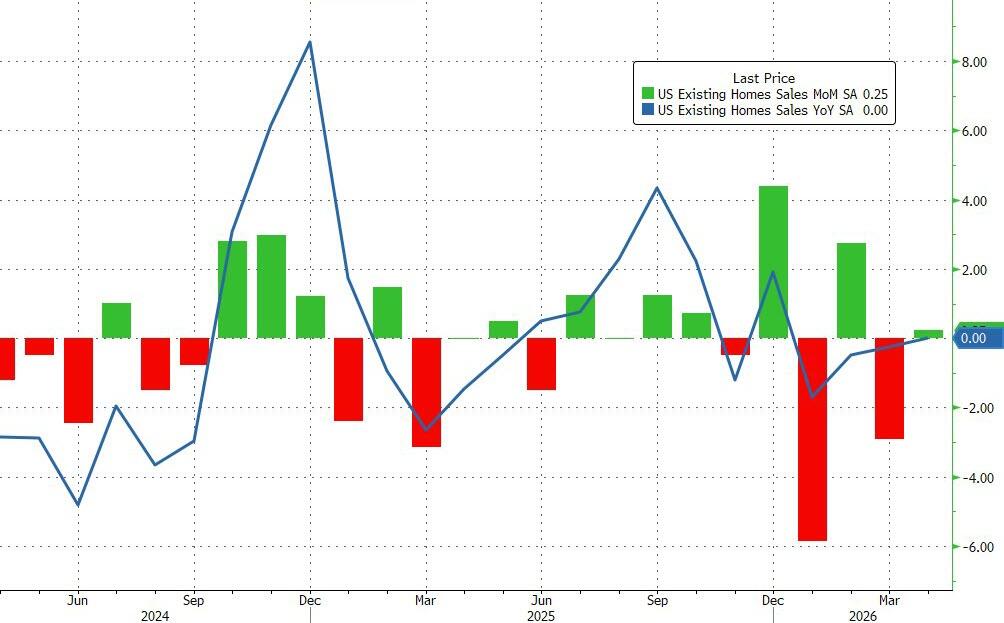

US Existing Home Sales Disappoint In April, Despite Lower Mortgage Rates

US Existing Home Sales Disappoint In April, Despite Lower Mortgage Rates

With the Spring selling season already in tatters, existing home sales were expected to rebound in April very modestly (+2.0% MoM) off recent record lows. However, the rebound was far less than expected, up just 0.2% MoM, which left sales of existing homes unchanged YoY…

Source: Bloomberg

Total existing home sales SAAR hover just above 4.00 million homes…

Source: Bloomberg

The NAR report showed the median selling price rose 0.9% from a year earlier to $417,700 last month – the highest for any April on record.

Source: Bloomberg

The inventory of previously owned homes increased from a year ago to 1.47 million – the most for any April since 2019.

Source: Bloomberg

“Even though it’s the highest inventory post-Covid, we are not close to the pre-Covid April inventory of 1.83 million,” Lawrence Yun, NAR chief economist, said on a call with reporters.

Contract closings rose in the Midwest and South, according to the NAR. They fell to a three-month low in the West.

Finally, it appears home sales are becoming less and less elastic relative to mortgage rates (which had fallen notably during the period of reporting)..

Source: Bloomberg

And, as the chart shows, mortgage rates are recently on the rise again…which will not help the situation at all.

Tyler Durden

Mon, 05/11/2026 – 10:07

“Friendly Local Assassin” Suspect In White House Correspondents’ Dinner Shooting Pleads Not Guilty

“Friendly Local Assassin” Suspect In White House Correspondents’ Dinner Shooting Pleads Not Guilty

In a federal courtroom in Washington this morning, 31-year-old Cole Tomas Allen entered a not guilty plea to charges stemming from the April 25 shooting incident at the White House Correspondents’ Association (WHCA) Dinner. The plea sets the stage for a high-profile trial that could determine whether Allen faces life in prison for what authorities describe as an attempted assassination of President Donald Trump.

Allen was tackled by Secret Service after gunfire erupted just outside the ballroom packed with roughly 2,600 attendees – including the President, First Lady Melania Trump, Vice President JD Vance, and numerous Cabinet officials and journalists.

The night of April 25…

Around 8:36 p.m. EDT, as dinner service was underway, Allen – armed with a 12-gauge Maverick shotgun, an Armscor Precision .38 semi-automatic pistol, and multiple knives – rushed past a security checkpoint on an upper level of the hotel. He fired at least one shot (reports indicate possible additional rounds) in the direction of law enforcement before being tackled by Secret Service agents and other officers.

One Secret Service agent was struck in his bulletproof vest by buckshot; he was treated and released from the hospital. Allen sustained a knee injury after tripping during the confrontation but was not shot. No bystanders or attendees were injured or killed. President Trump was quickly surrounded by agents and evacuated – 10 seconds after JD Vance, and the dinner was halted and later rescheduled.

Surveillance footage captured the rapid sequence: Allen sprinting with weapons visible, the sound of gunfire, and swift law enforcement response. Allen had checked into the hotel as a guest days earlier, traveling by Amtrak from his home in Torrance, California.

Today, we are releasing video already provided to U.S. District Court showing Cole Allen shoot a U.S. Secret Service officer during his attempt to assassinate the President at the White House Correspondents’ Dinner.

There is no evidence the shooting was the result of friendly… pic.twitter.com/a8gRXkW6BH

— US Attorney Pirro (@USAttyPirro) April 30, 2026

Born April 11, 1995, Allen is a California native with an extensive academic background – earning a bachelor’s degree in mechanical engineering from the California Institute of Technology (Caltech) in 2017 and a master’s in computer science from California State University, Dominguez Hills in 2025. He interned at NASA, worked part-time as a tutor at C2 Education in Torrance (named “Teacher of the Month” in December 2024), and developed video games, including a ‘non-violent fighting game’ (lol) called Bohrdom that was later removed from Steam following his arrest.

Acquaintances and family described him as highly intelligent, polite, inquisitive, and generally “gentle” or “super stable,” with no prior criminal history. He lived with his parents and siblings, regularly practiced at shooting ranges, and had expressed anti-Trump political views online and in person—including a small donation to Kamala Harris’s 2024 campaign and attendance at protests.

The Manifesto and Alleged Motive

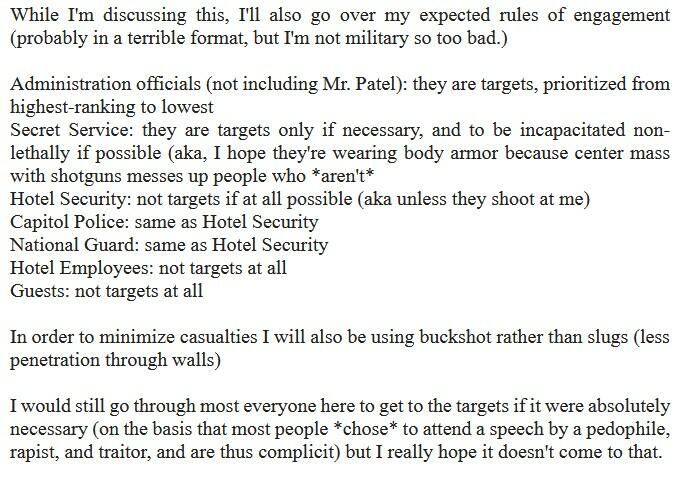

Approximately 10 minutes before the attack, Allen emailed a lengthy note titled “Apology and Explanation” to family members. In it, he apologized for “abusing” their trust and stated he did not expect forgiveness. He exhibited deep hatred of Trump, referring to himself in one passage as the “Friendly Federal Assassin” and outlining an intent to target “administration officials (not including Mr. Patel)” – widely interpreted as sparing FBI Director Kash Patel – from highest-ranking to lowest.

The document criticized specific actions such as federal operations against alleged drug boats and highlighted what Allen perceived as lax security at the hotel and event. Also for some reason FBI Director Kash Patel was not a target.

Authorities have described the note and related materials recovered from his devices and hotel room as a manifesto reflecting political grievances and a belief that it was his “duty” to act. Investigators are still examining the full scope of his radicalization, but preliminary findings point to targeted political violence rather than random or personal animus.

#WHCD #TRUMP

**Here is the full text of Cole Allen’s manifesto**, as published by the New York Post (1,052 words, signed “Cole ‘coldForce’ ‘Friendly Federal Assassin’ Allen”).

Part: 1/2

—

Hello everybody!

So I may have given a lot of people a surprise today. Let me start off… pic.twitter.com/6brCsHjHoJ

— CosMike (@C0sM1ke) April 27, 2026

Developments

Allen was charged days after the incident with attempting to assassinate the president, assaulting a federal officer with a deadly weapon, and multiple firearms violations (including interstate transportation of a firearm with intent to commit a felony and discharging a firearm during a crime of violence). A federal grand jury later returned a four-count indictment.

He has remained in federal custody in Washington. Early proceedings included concerns over his detention conditions – initially on suicide watch, later removed – prompting a federal magistrate judge to express alarm about his treatment, including reports of five-point restraints, and to demand explanations from jail officials (poor baby!). Allen’s defense team has filed motions, including one seeking the recusal of U.S. Attorney for D.C. Jeanine Pirro, and has highlighted what they describe as unusually harsh conditions compared to other high-profile detainees.

Today’s arraignment before Judge Trevor McFadden was the first formal opportunity for Allen to enter a plea on the indicted charges. With the not guilty plea entered, the case now proceeds toward trial, discovery, and potential pre-trial motions. If convicted on the lead count, Allen could face life imprisonment.

Tyler Durden

Mon, 05/11/2026 – 10:00

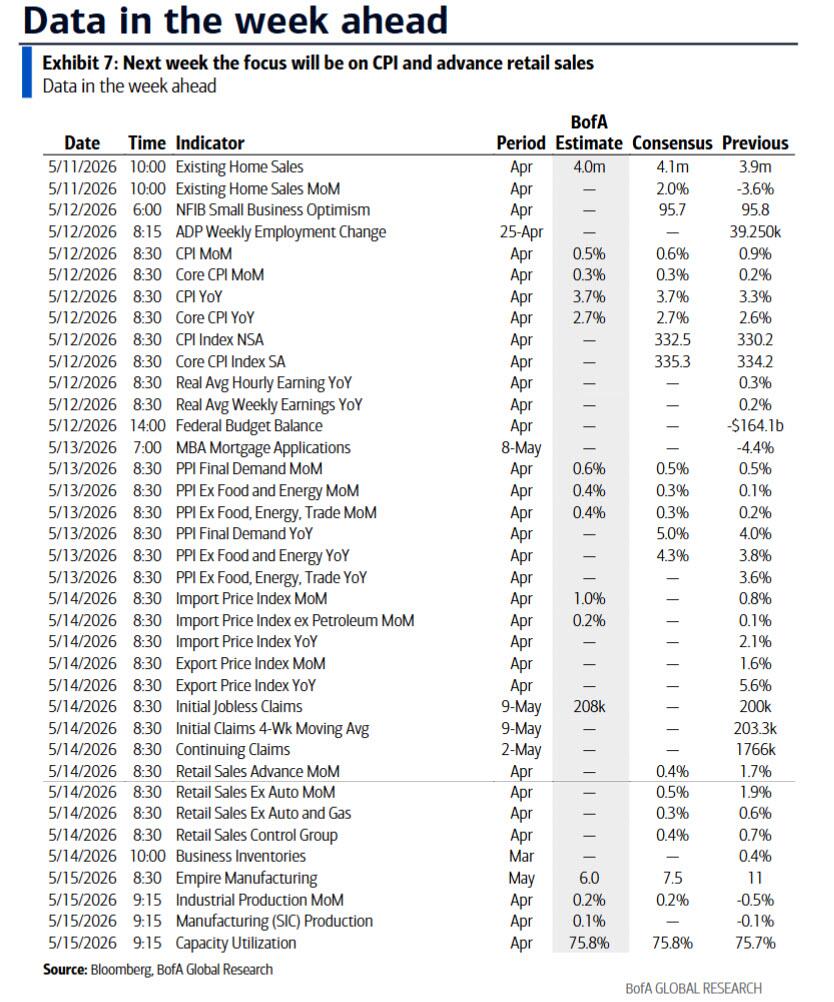

Key Events This Week: CPI, PPI, Retail Sales, Trump-Xi Summit

Key Events This Week: CPI, PPI, Retail Sales, Trump-Xi Summit

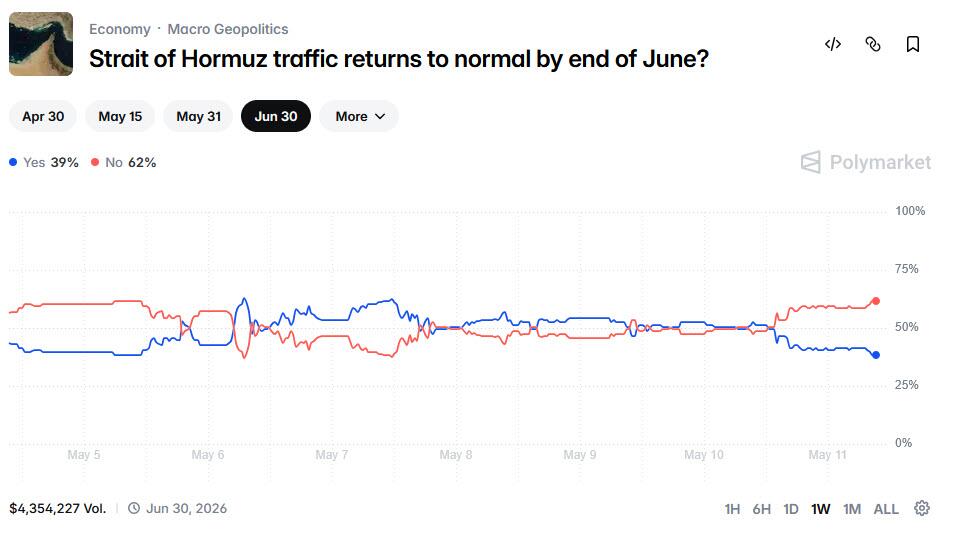

As DB’s Jim Reid tallies overnight, it has now been 73 days since the war in Iran began, with the past 32 marked by a stalemate characterized by a mix of truce and ongoing ceasefire. The absence of any meaningful kinetic activity for over a month suggests a firm US preference for reaching a deal. However, a counterpoint is that uncertainty over who holds negotiating authority in Iran may be complicating progress and delaying more difficult times ahead. It remains an unusual conflict with little action now for a month. In simple terms though, as long as the Strait of Hormuz stays closed, markets remain on a knife edge. Polymarket currently assigns a 39% probability to it fully reopening by 30 June.

The latest is that oil and yields are up again this morning as President Trump has posted that “I have just read the response from Iran’s so called ‘Representatives'” which he went on to call “TOTALLY UNACCEPTABLE”. This was based on a WSJ report that suggested Iran was offering to transfer some of highly enriched uranium to another country but wouldn’t dismantle its nuclear facilities. Iran’s official news agency has disputed the report anyway. Brent is up +4.23% and 10yr US yields are up +3.5bps. However, US and European equity futures are largely flat and Asian equities are largely higher on the AI trade. The KOSPI is on fire again with the index up +4.0% as semiconductors surge again. The index has crossed +85% YTD.

This comes ahead of the planned mid-to end week meeting between US President Donald Trump and China’s President Xi Jinping in Beijing. It’ll be interesting to see whether this meeting does anything to shape negotiations in the war. Both leaders would clearly like to show their influence on the world stage. So certainly the biggest headline event of the week (full preview here).

Before that, the new week arrives with markets still processing last Friday’s US payrolls report, which came in broadly firm and reinforced the view that labor market conditions remain resilient. While not strong enough to decisively alter the policy outlook, the release did little to ease concerns that underlying inflation pressures could persist, especially given still-solid wage dynamics. Against this backdrop, outside of the Iran War developments which will of course take center stage, the coming week will remain centered on the US, with a dense run of data and policy developments.

This week’s focal point will be tomorrow’s April CPI report. DB economists expect headline inflation to rise by +0.58% month-on-month, moderating from March’s +0.9%, but still relatively firm. In contrast, the core measure is projected to accelerate to +0.39% MoM from +0.2%, suggesting underlying price pressures remain sticky even as energy-related effects fade. The YoY rates would move from 3.3% to 3.8% for the former and from 2.6% to 2.8% for the latter.

Producer price data follows on Wednesday and then the remainder of the week shifts towards activity indicators. DB economists expect retail sales to decline by -0.3% MoM after March’s strong +1.7% increase, pointing to some payback in consumer spending. Meanwhile, industrial production is forecast to rise modestly by +0.2% MoM following a -0.5% drop previously, suggesting a tentative stabilization in manufacturing output.

Policy and politics will also be important. A Senate vote on Kevin Warsh’s nomination as Fed Chair is scheduled for today, just days before Jerome Powell’s term is set to expire at the end of the week. It’s possible the vote could get pushed back a day or so due to other Senate business but by the end of the week you would expect Warsh to have taken Miran’s seat on the board with Powell staying on the committee.

In Europe, inflation readings from Denmark and Norway today are followed with Germany’s ZEW survey tomorrow with sentiment darkening even with the nation’s extraordinary fiscal package. Later in the week, the ECB’s economic bulletin may offer additional context on the central bank’s assessment of inflation and activity trends.

In the UK, attention will be split between politics and macro. The State Opening of Parliament and the King’s Speech on Wednesday will outline the government’s legislative agenda for the year ahead. With PM Starmer under tremendous pressure following the very poor (but broadly as expected) local election results on Thursday there is talk of a leadership challenge as soon as today. Backbench MP Catherine West has said she will stand, which would be a stalking horse nomination. However, many left-wing MPs (as she is) have urged her not to as their preferred candidate Andy Burnham is not currently an MP. They fear an election now might be a bit too early and may allow a more moderate candidate like Wes Streeting to prevail. So timing tactics could prolong Starmer’s reign. A reminder that in September last year, Mr Burnham said that the UK should no longer be “in hock to the bond markets”. This caused a spike in Gilt yields and although he subsequently downplayed the remarks, this is something to watch carefully as we navigate the politics of the next few days and weeks. On the data side, Q1 UK GDP on Thursday will offer up the latest state of play growth wise.

In Asia, Japan’s schedule includes household spending data tomorrow, alongside the Economy Watchers survey and bank lending figures on Wednesday. In addition, the Bank of Japan will publish its summary of opinions from the April meeting, which should provide greater insight into policymakers’ thinking and any emerging shifts in the policy stance.

There are multiple appearances from Fed, ECB, BoE and BoJ officials throughout the week, and on the corporate front, earnings continue at a steadier pace. In the US, Cisco and Applied Materials are among the key names, while internationally the focus includes major firms such as Tencent, Alibaba, Siemens and Bayer. See the day-by-day calendar at the end as usual for a fuller week ahead preview.

Courtesy of DB, here is a day-by-day calendar of events

Monday May 11

Data: US April existing home sales, China April CPI, PPI, Denmark April CPI, Norway April CPI

Earnings: Petroleo Brasileiro, Constellation Energy, Barrick Mining, Compass, AST SpaceMobile

Auctions: US 3-yr Notes ($58bn)

Other: US Senate vote on Kevin Warsh’s nomination for Fed Chair

Tuesday May 12

Data: US April CPI, federal budget balance, NFIB small business optimism, Japan March household spending, leading index, coincident index, Germany May Zew survey, Italy March industrial production, Eurozone May Zew survey

Central banks: Fed’s Goolsbee speaks, ECB’s Dolenc speaks, BoJ Summary of Opinions April MPM

Earnings: Siemens Energy, Mitsubishi Heavy Industries, MunichRe, Bayer, Vodafone, Venture Global, On Holding, thyssenkrupp

Auctions: US 10-yr Notes ($42bn)

Wednesday May 13

Data: US April PPI, Japan April bank lending, Economy Watchers survey, March BoP current account balance, BoP trade balance, Germany April wholesale price index, March current account balance, Eurozone March industrial production, Q1 employment

Central banks: Fed’s Collins and Kashkari speak, ECB’s Lagarde, Lane and Radev speak, BoE’s Mann speaks

Earnings: Tencent, Cisco, Alibaba, Siemens, SoftBank, Allianz, Deutsche Telekom, E.ON, RWE, Alstom

Auctions: US 30-yr Bonds ($25bn)

Other: UK King’s Speech and the State Opening of Parliament

Thursday May 14

Data: US April retail sales, import price index, export price index, March business inventories, initial jobless claims, UK April RICS house price balance, Q1 GDP, Japan April M2, M3, Canada April existing home sales, March wholesale sales ex petroleum

Central banks: Fed’s Hammack and Barr speak, BoJ’s Masu speaks, BoE’s Pill speaks

Earnings: Applied Materials, National Grid, Figma

Other: US President Trump travels to China (through May 15)

Friday May 15

Data: US May Empire manufacturing index, April industrial production, capacity utilisation, Japan April PPI, April machine tool orders, Italy March general government debt, Canada April housing starts, March international securities transactions, manufacturing sales

Central banks: Fed Chair Powell’s term ends, ECB’s economic bulletin

Finally, looking at just the US, the key economic data releases this week are the CPI report on Tuesday and the retail sales report on Thursday. There are several speaking engagements by Fed officials this week, including events with Presidents Williams, Goolsbee, Collins, Kashkari, Schmid, and Hammack and Governor Barr on Thursday.

Monday, May 11

10:00 AM Existing home sales, April (GS +3.0%, consensus +2.0%, last -3.6%)

Tuesday, May 12

03:15 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will participate in a monetary policy panel at a conference jointly organized by the Swiss National Bank and the International Monetary Fund in Zurich, Switzerland. A Q&A session is expected. On May 4, Williams said, “The elevated levels of inflation, mixed signals from the labor market, and heightened uncertainty from the Middle East conflict present an unusual set of circumstances, but the current stance of monetary policy is well positioned to balance the risks to our maximum employment and price stability goals.”

08:30 AM CPI (MoM), April (GS +0.58%, consensus +0.6%, last +0.9%); Core CPI (MoM), April (GS +0.31%, consensus +0.3%, last +0.2%); CPI (YoY), April (GS +3.68%, consensus +3.7%, last +3.3%); Core CPI (YoY), April (GS +2.67%, consensus +2.7%, last +2.6%): We estimate a 0.31% increase in April core CPI (month-over-month SA), which would raise the year-over-year rate to 2.67%. We expect mixed autos inflation, reflecting a 0.4% decline in used car prices, a 0.1% increase in new car prices, and a 0.4% increase in the car insurance category. We forecast a jump in the shelter categories—a 0.50% increase in the OER category and a 0.44% increase in the rent category—reflecting the unwind of the downward bias in the index level from missed data collection during the government shutdown. The panel group that should have been sampled in October will be sampled in April and compared to prices from twelve months prior (i.e. April will effectively show two months’ worth of increases). We expect mixed readings for the travel services categories (airfares: +3%; hotels: flat), reflecting signals from alternative price data. We expect diminishing upward pressure from tariffs on categories that are particularly exposed (such as recreation) worth +0.04pp. We estimate a 0.58% rise in headline CPI—reflecting higher food prices (+0.3%) and sharply higher energy prices (+4.6%)—which would raise the year-over-year rate to +3.68% from +3.26%. Our forecast consists of a 0.26% monthly increase in the core PCE price index in April.

01:00 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will speak at the Greater Rockford Chamber of Commerce Luncheon in Rockford, Illinois. A Q&A session is expected. On May 8, during an interview in which he was asked whether inflation is the main danger now given that the labor market appears to have stabilized, Goolsbee responded, “I am optimistic that rates can go down, if we get some progress on inflation, [showing] we are headed back to the 2% inflation, [but] we just haven’t had [progress on inflation] for some time, and that makes me less optimistic.” When asked about the easing bias in the April FOMC statement, Goolsbee responded, “I was always skeptical of the value and appropriateness of using forward guidance [on things] that the committee doesn’t think it is going to do for some number of months or committing to actions well in the future.”

Wednesday, May 13

08:30 AM PPI final demand, April (GS +0.6%, consensus +0.5%, last +0.5%); PPI ex-food and energy, April (GS +0.5%, consensus +0.3%, last +0.1%); PPI ex-food, energy, and trade, April (GS +0.3%, consensus +0.3%, last +0.2%);

11:30 AM Boston Fed President Collins (FOMC non-voter) speaks: Boston Fed President Susan Collins will give remarks and participate in a fireside chat at the Boston Economic Club. Speech text and Q&A are expected. On May 7, Collins said she preferred to adjust the text of the post-meeting statement to “not be as closely aligned with language that has been associated with the presumption that the next move will be a cut.” She also added, “I do think that there are scenarios in which it would be important to strongly consider a hike.”

01:15 PM Minneapolis Fed President Kashkari (FOMC voter) speaks: Minneapolis Fed President Neel Kashkari will participate in a moderated discussion at a St. Paul Area Chamber event. A Q&A session is expected. On May 7, Kashkari said, “We voted against the forward guidance because we just didn’t want to signal that the next move was likely down.” He also added, “We cannot let elevated inflation be the new normal.”

Thursday, May 14

08:30 AM Import price index, April (consensus +1.0%, last +0.8%); Export price index, April (consensus +1.1%, last +1.6%)

08:30 AM Initial jobless claims, week ended May 9 (GS 205k, consensus 205k, last 200k); Continuing jobless claims, week ended May 2 (consensus 1,785k, last 1,766k)

08:30 AM Retail sales, April (GS +0.2%, consensus +0.6%, last +1.7%); Retail sales ex-auto, April (GS +0.3%, consensus +0.6%, last +1.9%); Retail sales ex-auto & gas, April (GS +0.1%, consensus +0.4%, last +0.6%); Core retail sales, April (GS +0.2%, consensus +0.4%, last +0.7%): We estimate core retail sales increased 0.2% in April (ex-autos, gasoline, and building materials; month-over-month SA), reflecting mixed alternative data and a headwind from potential residual seasonality. We estimate headline retail sales increased 0.2%, reflecting higher gasoline prices but lower auto and food services sales.

10:15 AM Kansas City Fed President Schmid (FOMC non-voter) speaks: Kansas City Fed President Jeff Schmid will speak on payments innovation and community banking at the Future of Banking Conference hosted by the Federal Reserve Bank of Kansas City. Speech text and Q&A are expected. On April 1, Schmid said, “With inflation already running hot, now is not the time to assume that the inflation from higher oil prices will be transitory.” He also added, “We must remain focused on our headline inflation objective, otherwise, I believe there is a real risk that inflation will get stuck closer to 3 percent than 2 percent in the long run.”

01:00 PM Cleveland Fed President Hammack (FOMC voter) speaks: Cleveland Fed President Beth Hammack will deliver opening remarks at the Cleveland Fed Conversations on Central Banking event. On May 7, Hammack said, “The statement that we put out is that interest rates were on hold, but we have the signal in there that it’s more likely that the next move will be down, [and] I thought that was a little bit misleading, just given my view of where the economy is.” She also added that her “baseline outlook is that interest rates will be on hold for quite some time.”

05:30 PM Fed Governor Barr speaks: Fed Governor Michael Barr will deliver remarks at an event organized by the Money Marketeers of New York University. Speech text and Q&A are expected. On May 5, Barr said, “The duration of the conflict matters a lot, and the longer it goes on, the greater the risk that the inflation we are seeing in these prices becomes embedded in the economy.”

05:45 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will participate in a moderated discussion at a conference organized by Moody’s. A Q&A session is expected.

Friday, May 15

08:30 AM Empire State manufacturing index, April (consensus +7.5, last +11.0)

09:15 AM Industrial production, April (GS +0.4%, consensus +0.2%, last -0.5%); Manufacturing production, April (GS +0.1%, consensus +0.2%, last -0.1%); Capacity utilization, April (GS 75.8%, consensus 75.8%, last 75.7%): We estimate industrial production increased 0.4% in April, largely reflecting strong natural gas and oil production. We estimate capacity utilization edged up to 75.8%.

Source: DB, Goldman

Tyler Durden

Mon, 05/11/2026 – 09:35

https://www.zerohedge.com/markets/key-events-week-cpi-ppi-retail-sales-trump-xi-summit

Khamenei Orders Iran’s Army To ‘Continue Decisive Operations’

Khamenei Orders Iran’s Army To ‘Continue Decisive Operations’

Iran’s Supreme Leader Mojtaba Khamenei has ordered the country’s forces to continue military operations against the US and Israel, according to a report by Iranian public broadcaster IRIB released Sunday.

The order came during a meeting between Khamenei and Major General Ali Abdollahi, the commander of the Iranian army’s Khatam al-Anbiya Headquarters. “During this meeting, the Supreme Commander-in-Chief, His Eminence Ayatollah Sayyed Mojtaba Hosseini Khamenei, while expressing appreciation for the brave and valiant fighters and the country’s powerful armed forces, issued new directives and guidance for continuing operations and confronting enemies decisively,” the report said.

Abdollahi also “presented a report on the readiness of the armed forces” during the meeting, IRIB added. The report comes after two months of speculation and unverified media claims about the Supreme Leader’s status.

Western news outlets like The Guardian and The Times had claimed earlier in the war that Khamenei was in a coma following the US-Israeli strikes that assassinated his father. Reports also claimed that he fled to Russia.

Mazaher Hosseini, head of protocol in the office of Iran’s supreme leader, recently stated that Khamenei was healing from minor injuries he sustained and “is now in complete health.”

“Thank God, he is in good health. The enemy is spreading all kinds of rumors and false claims. They want to see him and find him, but people should be patient and not rush. He will speak to you when the time is right,” the Iranian official stated.

The IRIB report came a day after CNN cited US intelligence as saying that Khamenei “is playing a critical role in shaping war strategy alongside senior Iranian officials.“

It also comes days after Iran’s President Masoud Pezeshkian said he met with the supreme leader. “What struck me most during this meeting was the vision and the humble and sincere approach of the supreme leader of the Islamic Revolution,” he said.

Tehran has sent out its response to a new US proposal for a ceasefire via Pakistan, according to state media. The US has maintained an illegal blockade of Iranian ports since the ceasefire began.

Washington violated the truce days ago by bombing Iran’s coast and attacking two vessels. Iranian forces targeted two US military vessels in response. The next day, skirmishes broke out between Iranian and US forces in the Strait of Hormuz.

Spokesperson for the Iranian parliament’s Foreign Policy and National Security Committee, Ebrahim Rezaei, said on Sunday that Tehran will strike US military bases and vessels in response to any new violations from Washington – stressing that “restraint has come to an end.”

Tyler Durden

Mon, 05/11/2026 – 09:20

https://www.zerohedge.com/geopolitical/khamenei-orders-irans-army-continue-decisive-operations

‘Starmer Out’ Odds (& Gilt Yields) Rise As Embattled UK PM Vows To ‘Prove Doubters Wrong’

‘Starmer Out’ Odds (& Gilt Yields) Rise As Embattled UK PM Vows To ‘Prove Doubters Wrong’

UK Prime Minister Keir Starmer vowed this morning to fight any bid to topple him, insisting he is “not going to walk away” and claiming that the country would never forgive Labour if it indulged in the “chaos” of a leadership contest.

“I know that people are frustrated by the state of Britain, frustrated by politics, and some people frustrated with me,” Starmer said in London on Monday.

“I know I have my doubters, and I know I need to prove them wrong.”

Starmer is fighting to stay in 10 Downing St. after a drubbing in local election results triggered a wave of Labour MPs to call for his departure.

He had a brief moment of respite on Monday when a former minister, Catherine West, withdrew her threat to force an immediate leadership contest, though she said she’d still push for a timetable for Starmer’s exit.

“I have listened to the prime minister’s speech this morning,” she told the BBC.

“I welcome the renewed energy and ideas. However, I have reluctantly concluded that this morning’s speech was too little too late.”

Starmer’s speech was light on new policy. The prime minister announced the government would legislate to take full ownership of British Steel, which is already under temporary government control. He also announced more investment in education programs like apprenticeships, technical colleges and in special educational needs.

Starmer sharpened his rhetoric against the populist parties who made strong gains at last week’s elections, warning that the country risks going down a “dark path,” as he stood behind a podium that read “Stronger Fairer Britain.”

“We are not just facing dangerous times but dangerous opponents,” he said, name-checking both Reform UK leader Nigel Farage and the Greens’ Zack Polanski.

“If we don’t get this right our country will go down a very dark path.”

Gilts fell, with the 10-year yield rising as much as 8 basis points to the day’s high of 5.00%, while the pound eased against the dollar and the euro.

Meanwhile, despite his vows, Polymarket odds of Starmer being gone by year-end are on the rise…

The call for a September leadership election, which would put it around the same time as Labour’s annual conference in Liverpool, puts pressure on Starmer’s health secretary, Wes Streeting, to decide whether to challenge his boss for the job before other candidates emerge.

Streeting, who is seen as a standard-bearer for the right of the party, is said to be weighing his options.

Starmer explicitly said he would fight to remain in office if a Labour colleague sparks a leadership contest, vowing: “I’m not going to walk away.”

Asked if he would stand if a race was triggered, he said: “Yes.”

Tyler Durden

Mon, 05/11/2026 – 09:05

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}