Category: News

US Home Builders Offer ‘Elevated’ Incentives Amid Affordability Challenges

US Home Builders Offer ‘Elevated’ Incentives Amid Affordability Challenges

Authored by Mary Prenon via The Epoch Times (emphasis ours),

Faced with affordability constraints and cautious demand, and with abundant land in states such as Arizona, Utah, Texas, and Florida, many developers are offering enticing incentives to potential homebuyers.

A recent Redfin report indicates that builders are offering mortgage-rate buydowns, assistance with closing costs, and upgraded home amenities to attract buyers. In areas where supply exceeds demand, the report found builders offering up to $10,000 in closing costs, as well as top-of-the-line appliances or home finishes.

“New homes still make up a significantly higher portion of the single-family supply than before the pandemic,” the report states. As demand escalated during the COVID-19 pandemic, new home construction increased to approximately 35 percent in 2022, up from 20 percent in 2019.

While new construction has slowed to 27 percent in August, some markets are still experiencing a glut of leftover new homes on the market. As a result, the report indicates, builders may be cautious about starting new projects as they attempt to sell off existing inventory.

In its October report, the National Association of Home Builders’ (NAHB) housing market index (HMI) found that 38 percent of builders were reducing prices by as much as 6 percent, while 65 percent indicated they were offering sales incentives to prospective buyers.

Still, the NAHB noted that builder confidence for newly-constructed single-family homes was 37 in October—up by five points from September and the highest reading since April.

D.R. Horton, one of the country’s largest homebuilders, recently reported that its homebuilding revenue for the fiscal year ending Sept. 30 decreased by 7 percent to $31.5 billion, with homes closed dropping by 5 percent to 84,863.

In an Oct. 28 statement, the Arlington, Texas-based company indicated it had 29,600 homes in inventory, of which 19,600 were unsold as of the end of September.

David Auld, D.R. Horton’s executive chairman, said that affordability constraints and cautious consumer sentiment are still impacting new-home demand.

‘Incredible Deals’

Developers in Houston, Texas, are offering “incredible deals,” Houston Association of Realtors Vice Chair Kat Robinson told The Epoch Times.

“Some of them have mortgage interest rates as low as 3.99 percent—that’s unbelievable,” she said.

“So now buyers have the choice of paying around 6 percent for a resale where they may have to make some repairs, or just drive an extra 15 minutes to buy something new for a much lower rate.”

Other concessions include help with closing costs or upgrades to appliances or countertops.

“The incentive plans change about every month based on the number of units sold,” Robinson noted.

Sales of new single-family homes are comparable to last year, she said, and much better than in 2023. Pricing varies by development and location, but on average, a 1,800-square-foot new construction with three bedrooms and two baths is listed for $500,000.

Many developments offer a community center, pool, walking paths, other amenities, along with monthly homeowners association (HOA) fees.

Still, resale homes continue to draw prospective buyers.

“A lot of older neighborhoods have full-grown trees that canopy the streets and create a charming experience,” Robinson said. “A lot of people do prefer resale homes because they want trees.”

According to Robinson, the greater Houston area has more listings than ever, and buyers now have many choices and more negotiation power.

Some Areas See Higher Sales

Christy Walker, president of the Phoenix Realtors, told The Epoch Times that nearly 10 percent of the 19,200 active home listings in the greater Phoenix area are new builds, and she has seen developers offering buyer incentives.

Some of the incentives include lower interest rates of 4.5 percent on conventional loans and 4.25 percent on Federal Housing Administration (FHA) loans, according to Walker. Other incentives include assistance with closing costs or home upgrades, such as appliances or finishes.

Meanwhile, Walker has witnessed higher sales for new construction in the area.

“We have a new build that we’re selling, and appointments to see models on the new construction site were scooped up within the first hour,” she said.

“We now have over 600 on a waiting list to see them.”

Located in North Phoenix, The Ridge at Stone Butte offers single-family homes ranging from 1,600 to 4,000 square feet, featuring gourmet kitchens, spa-like bathrooms, walk-in closets, and panoramic views of the desert.

Walker noted that new construction for a 1,800-square-foot, single-family home with three bedrooms and two bathrooms typically lists in the mid-$600,000s.

“With the median sales price of about $550,000 for a similar resale home, a lot of potential homeowners are opting for a brand new home—one where they can actually save on mortgage interest costs,” she said.

Because Phoenix and its outlying regions have abundant available land, the area has traditionally been a popular place for new home development.

“We have a lot of out-of-state buyers looking for more affordable options, as well as some local move-up and first-time buyers,” Walker noted.

New Construction in 2026

In its Emerging Real Estate Trends for 2026 report, PCW and the Urban Land Institute forecast that builders are looking to the future with cautious optimism. While new homes and resale inventory are increasing, some builders are shifting to single-family rental partnerships and slowing down on major land purchases.

“Affordability remains the greatest challenge and is being addressed by constructing smaller, lower-spec homes, as most buyers are willing to sacrifice size and finishes for price relief,” the report states.

The report suggests one method builders could use to make homes more affordable is to build smaller ones. The average size of a new single-family home fell to 2,386 square feet in the second quarter from a peak of 2,692 square feet in 2016.

Other builders say they plan to lower the ceiling height, provide fewer windows, and add lower-finish countertops to save costs.

Some builders surveyed believe rising costs in labor and materials could be challenging over the next two years. Almost all stressed the need for collaboration with local municipalities to allow for increased density, thereby reducing housing costs and streamlining the permitting process and project approvals.

In an earlier report this year, the National Association of Realtors found that the South is experiencing some of the best deals in new home construction. It named the five markets with the largest declines in new home prices: Little Rock, Arkansas, with a 15.6 percent drop; Austin, Texas, 8.5 percent lower; Wichita, Kansas; Jacksonville and Cape Coral, Florida, all at more than 7 percent declines.

“We expect our sales incentives to remain elevated in fiscal 2026, the extent to which will depend on market conditions throughout the year,” he said.

Auld said that the company has expanded its new home construction into seven new states and 38 markets.

Tyler Durden

Mon, 11/17/2025 – 09:00

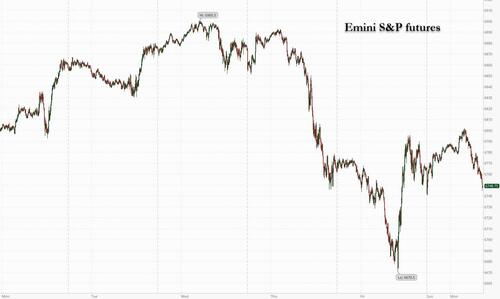

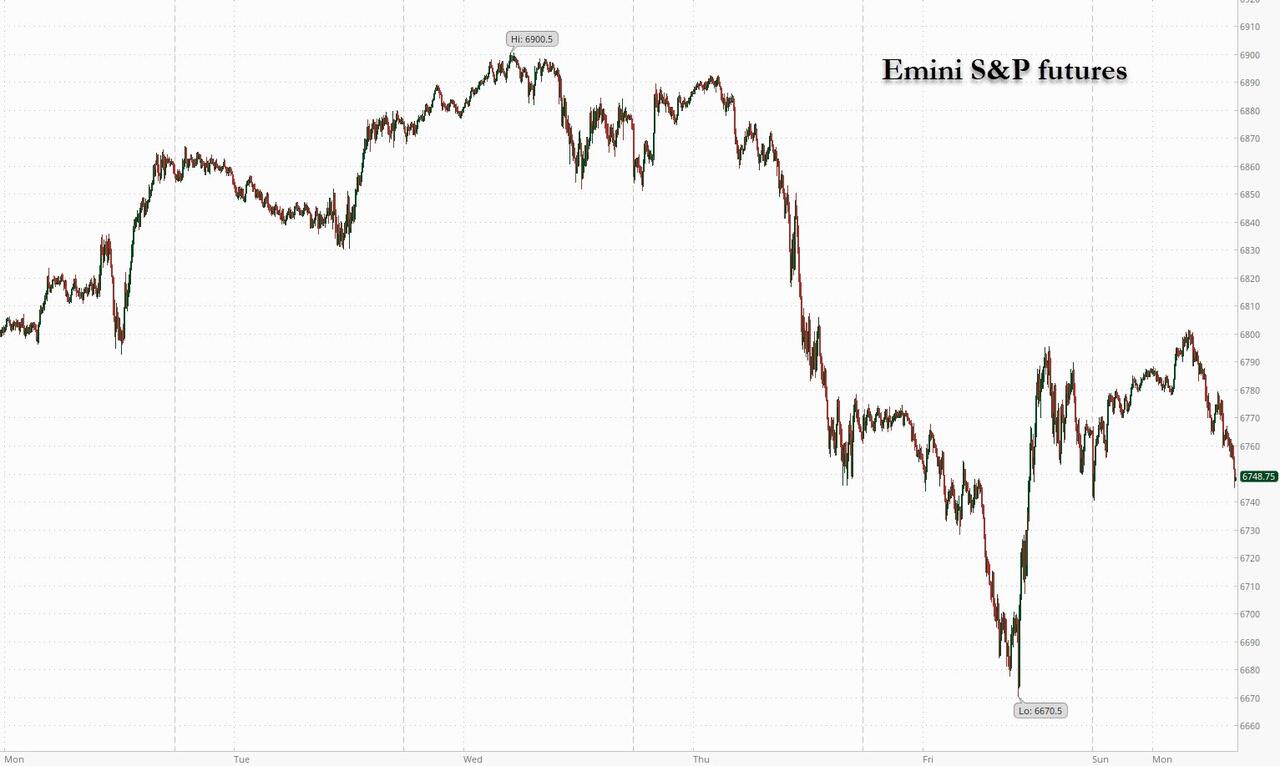

US Equity Futures Fade Overnight Gains As Global Selloff Deepens

US Equity Futures Fade Overnight Gains As Global Selloff Deepens

US equity futures are slightly higher led by Tech, but well off overnight highs, while stocks around global markets slide. As of 8:00am ET, S&P and Nasdaq futures are up 0.1%, having previously been as much as 0.6% higher, after both gauges closed above their 50-day moving averages on Friday, a key support level. In premarket trading, Mag7 names are mostly lower led by GOOG +4%, NVDA is down 1% with earnings Wednesday after the close. Bond yields are lower as the curve mostly bull steepens; USD trades near session highs. Commodities are mixed with Energy weaker, Ags stronger, and mixed performance across metals. Airlines are back to full capacity as FAA lift restrictions. Government data releases return this week with the focus on Thursday’s NFP release (Sep data). Earnings will been focused on Retailers. Some of the week’s few key events: Nvidia EPS 11/19 post close ($300bn mkt cap implied move), VIX Expiry 11/19, FOMC Minutes 11/19, Sept NFP 11/20 pre-mkt (Goldman +80k vs 50k cons), Nov Opex 11/21, HD/WMT/LOW/TGT/TJX/WSM/GAP consumer EPS, +10 Fed speakers, and a continued slew of sell-side conferences.

In premarket trading, Mag 7 stocks are mostly lower: Alphabet (GOOGL) rises 4% after a regulatory filing showed that Warren Buffett’s Berkshire Hathaway Inc. acquired 17.9 million shares of the Google parent during the third quarter. Amazon (AMZN) +0.8%, Meta Platforms (META) -0.08%, Microsoft (MSFT) -0.07%, Apple (AAPL) -0.7%, Nvidia (NVDA) -1%, Tesla (TSLA) -0.7%.

Aramark (ARMK) falls 2% after the food and facilities management company reported revenue and adjusted EPS for the fourth quarter that missed consensus estimates.

EW Scripps (SSP) rises 19% after Sinclair took an 8.2% stake.

Expeditors International of Washington (EXPD) gains 1.8% after UBS upgraded its view on the company to buy, expecting growth in the customs/other segment to offset pressure from lower ocean rates in 2026.

Gap (GAP) rises 2% as Barclays upgrades the apparel retailer’s stock to overweight, seeing “durable brand recovery” when looking past tariff pressures.

PotlatchDeltic (PCH) falls 2% after being cut by two steps at Bank of America.

Quantum Computing Inc. (QUBT) climbs 16% after the company reported third-quarter net income of $2.4 million, or 1 cent per share, versus a loss of $5.7 million, or 6 cents per share, in the quarter last year.

Sealed Air (SEE) falls 3% after Clayton Dubilier & Rice agreed to buy the packaging company that invented Bubble Wrap.

Zymeworks (ZYME) jumps 35% after the drug developer gave topline results from a late-stage trial of its experimental combination therapy for cancer of the stomach and esophagus. Shares of partner Jazz Pharmaceuticals (JAZZ) are up 21%.

In corporate news, Emirates is placing another major order for Boeing’s flagship 777X airliner, valued at $38 billion. Jeff Bezos has created an AI start-up where he will be co-CEO, according to the New York Times. Peter Thiel’s hedge fund Thiel Macro sold off its holdings in Nvidia during the third quarter, according to a 13F filing.

Stock futures have erased an earlier gain, when sentiment got a modest boost from Morgan Stanley’s Michael Wilson (whose timing has been rather atrocious in recent years), who said a new bull market and earnings cycle is powering on. Wilson predicted a 16% rally for the S&P 500 over the next year, driven by strong company earnings, making him among the most bullish strategists on the Street.

“We’re in the midst of a new bull market and earnings cycle, especially for many of the lagging areas of the index,” Wilson wrote in a note.

Others are less optimistic. Bond king Jeffrey Gundlach is worried about “garbage lending” in private credit and unhealthy valuations across asset classes, saying the US stock market is “among the least healthy in my entire career.” Among speculative assets, the steep drop in Bitcoin stabilized on Monday but smaller, riskier tokens are more fragile: A basket of the smallest digital assets fell to lows not seen since the pandemic on Sunday.

For the biggest tech stocks, Bloomberg’s analysis of 13F filings showed that hedge funds pared positions in Mag 7 stocks last quarter. Still, tech stocks accounted for the biggest weighting in portfolios, at 26%. The value of investments in consumer staples fell by the most for any industry.

“Despite being dated, the September US payrolls matter as delayed data has left uncertainty for markets and policymakers,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg. “The report will help clarify economic momentum and Fed rate-cut expectations.”

Uncertainty over the possibility of a hawkish pivot by the Fed has heightened fears that this year’s gains have gone too far. Traders have pushed the odds of a quarter-point rate cut in December below 50% after some officials signaled that further easing is far from assured. The Fed will release minutes from its Oct. 28-29 meeting on Wednesday to shed light on an unusual split among policymakers. Fed voting members including Philip Jefferson, Christopher Waller and John Williams are due to speak later on Monday.

“I do believe that the Fed still has the potential to cut in December, but that brings volatility,” Adrian Zuercher, co-head of Global Asset Allocation at UBS Global Wealth Management, told Bloomberg TV. “But overall, I do think markets are quite healthy and could actually go further up from here.”

In strategy, Deutsche Bank said that equity positioning has slipped back to neutral with discretionary investors turning underweight and positioning in mega-cap growth and tech trimmed. Meanwhile, investors are focused on ever-shortening windows of volatility to manage risks, such that the influence of contracts expiring from zero to five days away has surged, according to JPMorgan strategists. And RBC said that data shows some deterioration and slowing flows into passive investment for retail investors.

European stocks dip, tracking modest declines in Asia. Retail, travel and chemical shares are the worst performers on the Stoxx 600 while utilities and energy equities are the biggest underperformers. Here are the biggest movers Monday:

Saab surges as much as 7.1% after the Swedish defense group rounded a major week for new contracts with a keenly anticipated deal to supply Colombia with new fighter jets in a contract worth €3.1 billion ($3.6 billion)

SIG Group AG surges as much as 12% after the Swiss food packaging maker appointed Mikko Keto as CEO. Vontobel says the appointment is a first step toward boosting investor confidence

WPP shares gain as much as 6.7% as advertising agency Havas has expressed interest in the London-listed company, the Times reported over the weekend

Ninety One declines as much as 4.6% in Johannesburg, the most since June 13 after the asset management firm reported pretax profit for the first half-year that missed the average analyst estimate

Genuit Group falls as much as 14%, after the provider of water and ventilation products warned it expects the market to remain subdued for the remainder of 2025 and into next year due to the economic and political backdrop

Pluxee shares fall, after the French employee-benefits firm revised its guidance to incorporate the potential impact of changes to Brazil’s meal voucher system, news of which sent the stock tumbling last week

In rates, treasuries climb, pushing US 10-year yields down 1 bps to 4.14%. Treasury yields are richer by 1bp to 3.5bp across the curve, the 10-year around 4.12%, with 2s10s spread flatter by nearly 2bp, 5s30s by 2bp about. Gilts pare some of Friday’s slump, with UK 10-year borrowing costs falling 2 bps to 4.55%.

In FX, the Bloomberg Dollar Spot Index rises 0.1%. The Aussie dollar is the weakest of the G-10 currencies, falling 0.3% against the greenback.

In commodities, bitcoin rises over 2% and back above $95,000, erasing its weekend fall. Spot gold is steady near $4,088/oz. WTI crude futures are little changed near $60 a barrel.

Today’s US economic calendar includes November Empire Manufacturing (8:30am) and August construction spending (10am); September employment data delayed by US government shutdown is slated for Thursday. Fed speaker slate includes Williams (9am), Jefferson (9:30am), Kashkari (1pm) and Waller (3:35pm).

Key events this week include Nvidia earnings on Wednesday and the release of long-delayed economic data. Another key event this week is the release of FOMC minutes of the Oct. 28-29 meeting, when Fed Chair Powell was unusually hawkish. Markets will be looking for any details on what Powell called a “growing chorus” of officials who think the Fed should pause for at least one meeting.

Market Movers:

S&P 500 mini unch

Nasdaq 100 mini +0.1%

Russell 2000 mini little changed

Stoxx Europe 600 -0.3%

DAX -0.4%

CAC 40 -0.3%

10-year Treasury yield -3 basis points at 4.12%

VIX +0.4 points at 20.18

Bloomberg Dollar Index little changed at 1217.38

euro -0.1% at $1.1607

WTI crude -0.2% at $59.96/barrel

Top Overnight News

US President Trump posted that House Republicans should vote to release the Epstein files, via Truth Social.

Trump signaled support for Senate legislation to sanction countries doing business with Russia, potentially targeting major consumers like China and India. BBG

China slow-walks U.S. soybean purchases as stockpiles hit multi-year highs, undermining Trump’s trade deal claims. CNBC

China escalated tensions with Japan over PM Sanae Takaichi’s Taiwan remarks. The state broadcaster warned of “substantive retaliation” including sanctions and trade curbs as Beijing cautioned against travel to Japan. BBG

Japan moved on Monday to tamp down an escalating row with China over Taiwan that has prompted Beijing to urge citizens to halt travel to its East Asian neighbor. The dispute erupted after Prime Minister Sanae Takaichi told Japanese lawmakers this month that a Chinese attack on Taiwan threatening Japan’s survival could trigger a military response. RTRS

New York Federal Reserve President John Williams met with Wall Street banks this week to discuss a key short-term lending facility: Reuters.

Trump administration officials, including Health Secretary Robert F. Kennedy Jr., discussed scaling back the role of FDA Commissioner Marty Makary; RFK Jr. also considered installing a new leader to manage the agency day to day: WSJ.

Japan’s economy shrank at an annualized rate of 1.8% in the latest quarter, as US tariffs hit exports and housing investment plunged ahead of a major stimulus package expected this month to boost the struggling economy. The decline in real GDP for July to September period was less severe than economists’ median forecast of 2.5%. FT

The euro-area economy will maintain its moderate expansion, with output rising 1.3% in 2025, 1.2% in 2026 and 1.4% in 2027, European Commission forecasts showed. Inflation is seen sticking close to the ECB’s 2% target over the next two years. BBG

The UK will today unveil proposals to make it easier to remove migrants with no rights to stay in the country. BBG

The Federal Aviation Administration said it would lift its flight restrictions related to the government shutdown, clearing the way for normal operations to resume at U.S. airports after weeks of delays and cancellations. WSJ

GOOGL +430bps pre mkt after regulatory filings show Berkshire Hathaway acquired 17.9 shares during 3rd quarter and ahead of release of Gemini 3.0 AI model which may arrive as soon as this week. BBG

Trade/Tariffs

US Treasury Secretary Bessent said the China rare-earths deal will “hopefully” be done by Thanksgiving, according to Fox News. Treasury Secretary Bessent said he is confident China will honour the agreement after the upcoming meeting between Presidents Trump and Xi, and emphasised that Washington has “many levers” if Beijing does not comply.

US President Trump said he does not think more tariff rollbacks will be necessary; he said top US officials spoke with their Chinese counterparts on Friday and that he is speaking to China about soybeans, according to Reuters.

US Treasury Secretary Bessent said US President Trump’s proposal to send USD 2,000 “dividend” payments from tariffs to US citizens would require congressional approval, according to Reuters.

Tesla (TSLA) is now reportedly requiring its suppliers to exclude China-made components in the manufacturing of its cars in the US, a fresh example of the fallout from Washington–Beijing tensions, according to the WSJ.

Brazil’s Vice President Alckmin said Brazil will continue working to reduce US tariffs further; he noted that progress has been made but there is still a long way to go, expressed optimism about further progress, and said the US government has taken a step in the right direction to reduce costs for its consumers, according to Reuters.

USTR Greer has warned the EU that trade remains a “flashpoint” with Washington, according to the FT.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly lower after the mixed lead from Wall Street, with sentiment in the region subdued as US President Trump over the weekend said he does not think further tariff rollbacks will be necessary. The Nikkei 225 saw modest losses on either side of 50k, while South Korea’s KOSPI (+1.5%) stood out as a clear outperformer amid strong gains in chip names after reports that Samsung is raising chip prices, whilst China’s tourist warning to Japan was seen as a positive for South Korea. Focus remains on the tech sector this week in the run-up to NVIDIA earnings midweek. ASX 200 was subdued with sectors mixed. Telecoms, Healthcare, and Consumer Discretionary lagged, while IT and Energy outperformed. Nikkei 225 was choppy and briefly slipped under 50k following Japan’s GDP contraction — the first in six quarters, albeit shallower than feared. Rising tensions between Japan and China added pressure, with Japanese travel-related names hit after Beijing warned citizens against travelling to and studying in Japan. KOSPI was the outperformer, driven by gains in Samsung Electronics and SK Hynix after reports that Samsung raised server memory chip contract prices by up to 60% in November due to shortages – the former also plans to add a new chip production line as demand rises. Broader gains were also supported by China’s warning against travel to Japan. Hang Seng and Shanghai Comp both traded with modest losses, broadly in line with regional moves (ex-South Korea). Over the weekend, US Treasury Secretary Bessent said the China rare-earths deal will “hopefully” be completed by Thanksgiving, but stressed that Washington has “many levers” if Beijing does not comply. President Trump added he does not think further tariff rollbacks will be necessary, noting senior US officials spoke with Chinese counterparts on Friday and that discussions on soybeans continue.

Top Asian News

Samsung Electronics (005930 KS) will build a new chip production line in Pyeongtaek, South Korea, with mass production slated to begin in 2028; the company also said FläktGroup is considering building a factory in South Korea, according to Reuters.

Alibaba’s (9988 HK) Qwen has entered public beta as a direct challenge to ChatGPT.

Japan’s government is reportedly considering compiling a stimulus package of around JPY 17tln, with a supplementary budget likely to be sized around JPY 14tln, according to Nikkei.

Japan’s Key Government Panel member Kataoka says the government must compile a stimulus package of up to JPY 23tln, funded with JPY 10tln in net bond issuance and JPY 13tln with tax and non-tax revenues. Adds: BoJ should move cautiously with policy normalisation. Should wait until March or April 2026 to raise rates. Should not rule out FX intervention in addressing excessive yen weakness.

India Trade Official says India and US could soon agree to address reciprocal tariffs as part of first part of the agreement. India and USA are likely to address broader trade issues in the second part of the agreement.

Japanese PM Takaichi to meet with BoJ Governor Ueda on Tuesday at 06:30 GMT.

European bourses (STOXX 600 -0.4%) began the morning around the unchanged mark, with trade tentative, though recently sentiment has soured a touch with most European bourses slipping into the red. Nothing really behind the latest bout of pressure, but does continue the subdued mood seen overnight. European sectors also opened with a positive bias, but now holds a negative bias. Utilities and Real Estate marginally top the pile whilst Retail lags. Dassault Aviation (+6.2%) bucks the broadly lower mood in Europe, after Ukrainian President Zelensky said Ukraine had ordered 100 Rafale fighter jets.

Top European News

ECB’s Rehn said the risk of inflation slowing shouldn’t be overlooked, according to Helsingin Sanomat. He added that “low energy prices, a stronger euro, and easing wage and services inflation pose a risk that total inflation slows excessively relative to our 2% target.”

ECB’s de Guindos says expect inflation to converge towards target. Uncertainty has abated but still a defining feature of out times. FSR will focus on 3 big risks, first is about risk of financial market corrections. There’s a risk of abrupt shift in sentiment. Fiscal challenge also a key vulnerability. Banks may face deterioration of credit quality. Banks resilience is underpinned by profits and capital. Adverse economic shocks could lead to rising corporate defaults, valuation corrections and losses for private funds and their investors. Upholding the macroprudential, measures for banks implemented in recent years. Closer monitoring and strengthening the macroprudential framework for the non-bank sector. Slightly more optimistic re. growth. Wage dynamic are going in the right direction.

UK Chancellor Reeves is reportedly considering a nightly levy for British holidaymakers and foreign tourists on hotel stays and Airbnb-style rentals, via The Times.

EU Commission President von der Leyen, in a letter to member states, says the scale of Ukraine’s financing gap is significant. They have identified three main options. According to Reuters sources, the three options in the Ukraine financing are not mutually exclusive and can be combined or sequenced.

FX

DXY is flat/modestly firmer and trades in a busy 99.29 to 99.47 range, given the lack of pertinent newsflow this morning but ahead of a packed weekly docket, which includes; the release of the delayed September NFP report, FOMC Minutes and a number of Fed speakers. Today’s docket is a bit more on the quiet side with only really the NY Fed Manufacturing report and comments via Fed’s Williams, Jefferson, Kashkari and Waller.

EUR is a little lower today and trades just around the 1.1600 mark, within a 1.1596 to 1.1624 range. Newsflow for the region is relatively quiet ahead of the European Commission Autumn forecasts; there were some comments via ECB’s de Guindos who suggested that he is slightly more optimistic regarding growth, and expects inflation to converge towards target. Back to the Commission it raised its 2025 growth forecast for the bloc but cuts its view for 2026 to 1.2% (prev. 1.4%), while the inflation forecast was maintained for the year but increased in 2026. No significant EUR move seen, as such the single currency remains around the 1.16 mark.

JPY is modestly lower vs the USD, and as is the case with peers, trade has been contained within a narrow 154.41 to 154.83 range. Overnight, price action was also lacklustre, and was ultimately little moved by a less-than-feared contraction in headline GDP – largely due to weak exports and lower tourism. Analysts at OxEco write that the dip in GDP will likely prove to be temporary, suggesting that consumption should modestly improve. On the fiscal side of things, Japan’s Key Government Panel member Kataoka said that the Government must compile a stimulus package of up to JPY 23tln, funded with JPY 10tln in net bond issuance and JPY 13tln with tax and non-tax revenues.

GBP is flat/slightly lower and trades towards the midpoint of a 1.3136 to 1.3180 range. Traders remain solely focused on the Budget developments, albeit updates over the weekend have been lacking on that front. This morning, The Times reported that Reeves is considering a nightly levy for British holidaymakers and foreign tourists on hotel stays and Airbnb-style rentals.

Antipodeans are pressured, with the Aussie the marginal laggard across G10 pairs. Nothing really driving things for the currencies this morning, but follows on from subdued price action overnight, following the APAC risk tone.

Fixed Income

A contained overnight session for USTs. Meandered within a narrow 112-15 to 19 range early doors with specifics light and participants preparing for a week of delayed data to finally start hitting and a substantial amount of Fed speak; into this, the odds of a cut in December have slipped to c. 40% vs the ~50% seen last week. Thereafter, the early European morning saw a modest deterioration in the region’s risk tone (though, US futures remained strong), which provided some modest support to benchmarks generally. Lifting USTs further into the green and to a 112-22+ peak. If the move continues, we look to 112-23 from Friday before 112-31 and 113-00 from the two sessions prior. Today’s docket is dominated by Fed speak, where Williams (voter), Jefferson (voter), Kashkari (2026) and Waller (voter) are all due. From those, we expect Jefferson and Waller to provide texts, Jefferson and Kashkari to partake in Q&A’s while Williams is not expected to provide either.

Bund overnight action was contained and similar to that outlined in USTs. Until the arrival of European participants, where a bout of upside occurred as the European risk tone deteriorated. Newsflow is relatively light and the move isn’t a particularly pronounced one, with Bunds firmer by just over 10 ticks at most at a 128.79 peak. If this continues, we look to 128.97 from Friday after which there is a gap until the figure and then levels between 129.19-40 from last week.

Gilts are firmer, just about outperforming peers but the magnitude of action is also modest thus far. Gapped higher by 20 ticks to above the 92.05 mark before briefly losing the figure and then conformed to peers and lifted to a 92.29 peak, with gains of 14 ticks at most. Newsflow remains firmly focussed on the budget, and while there have been several scoops and reports around what Chancellor Reeves may do, there has not been anything of the magnitude seen last Friday. This week, the main focus point is Wednesday’s CPI, a series that provides early insight into the December deliberations, where Bailey may have to play the tie-breaking role once again.

Commodities

Crude benchmarks were muted to start the European session amid continued attacks on Russian oil infrastructure. WTI and Brent initially dipped USD 0.40/bbl on the open following the resumption of oil loading at Russia’s Novorossiysk Black Sea port. After dropping to a low of USD 59.32/bbl and 63.66/bbl respectively, benchmarks slightly rebounded, before a heftier bout of buying which sent WTI and Brent to a peak of USD 60.19/bbl and 64.48/bbl. Nothing really for it, but appeared to coincide with reports that Israeli warplanes targeted areas in southern Lebanon. This upside briefly pared, before then catching another bid back towards highs.

Spot XAU is oscillating in a tight USD 4050-4106/oz band as the European session gets underway and the market steadies itself following Friday’s selloff.

Base metals have traded rangebound throughout the APAC session and into the European session amid a lack of drivers to start the week. 3M LME Copper continues to trade well-within Friday’s range in a tight USD 10.79k-10.85k/t band as markets await fresh catalysts.

India’s October gold imports at USD 14.7bln.

Russia’s Kremlin says they have the capacity to eliminate the consequences of the Ukrainian attack on Novorossiysk in a short period of time and recommenced all export activity.

Indonesia is finalising a plan to impose export taxes of 7.5-15% on gold product shipments; designed to be effective from some point in 2026.

All operations on intake and transfer of Kazakh oil has resumed at the Novorossiysk port, via IFX.

Geopolitics: Middle East

Israeli warplanes have targeted areas in southern Lebanon, via Iran International citing Al-Mayadeen Network.

Israeli forces raided the city of Dura south of Hebron in the West Bank, according to Reuters.

Israel’s Defence Minister said the multinational force led by the US will take charge of disarming Hamas in Gaza, according to Reuters.

US Central Command said Iran’s use of military force to seize a commercial vessel in international waters is a violation of international law, according to Reuters. US Central Command said that on Friday it detected Iranian forces boarding an oil tanker flying the Marshall Islands flag in international waters, and that the tanker Talara was seized after Islamic Revolutionary Guard Corps forces boarded it via helicopter.

Iran’s foreign minister said the nation is no longer enriching uranium at any site in the country, via AP.

Israeli PM Netanyahu said there will be no Palestinian state and that Hamas will be disarmed — by force, if necessary, according to Reuters.

Iran’s Foreign Minister Araqchi said the current US approach in no way indicates readiness for equal and fair negotiations; he added that Iran will always be prepared to engage in diplomacy but not negotiations meant for dictation, according to state media.

Lebanon will file a complaint to the UN Security Council against Israel for constructing a concrete wall along Lebanon’s southern border that extends beyond the “Blue Line”, according to the Lebanese presidency.

US President Trump warned that countries doing business with Russia will face sanctions under new legislation and said Iran may be added to that list, according to Reuters.

US President Trump is reportedly considering a “bilateral security agreement pledging to defend Saudi Arabia in the event of any attack”, via Politico citing sources.

Geopolitics: Ukraine

Russia’s Novorossiysk Black Sea port resumed oil loadings on November 16, according to Reuters sources and LSEG data.

Ukraine’s military says it struck an oil refinery in Russia’s Samara region, according to Reuters.

Russia’s Defence Ministry said Russian forces took control of Yablukove in Ukraine’s Zaporizhzhia region, according to TASS.

Geopolitics: China-Japan

Japan is to send a senior diplomat to ease tensions with China, according to NHK.

China’s Coast Guard said a Chinese coastguard ship formation cruised past the Senkaku Islands and that the cruise was to protect rights and in accordance with international law, according to Reuters.

Geopolitics: Other

US aircraft carrier has arrived in the Caribbean in a major build-up near Venezuela, via AP.

US President Trump said he could have discussions with Venezuela’s President Maduro, according to Reuters.

Russian President Putin held a phone call with Israel’s PM Benjamin Netanyahu, according to the Kremlin.

US President Trump said the US will test nuclear weapons like other countries, according to Reuters.

US Event Calendar

8:30 am: Nov Empire Manufacturing, est. 5.75, prior 10.7

10:00 am: Aug Construction Spending MoM, est. -0.1%, prior -0.07%

DB’s Jim Reid concludes the overnight wrap

After the resolution of the US government shutdown, markets face a packed calendar of delayed and scheduled releases this week. Although maybe the most important event will be Nvidia’s earnings after the closing bell on Wednesday. One of the most interesting developments last week in the world of tech was the widening out of AI related CDS spreads. For example, Oracle 5yr CDS widened +18bps to 105bps and CoreWeave around +100bps to 630bps last week even as a volatile week for the Mag-7 ended in only a small -1.19% loss. The tights for the year for both were 33bps and 360bp respectively with the CoreWeave contract only starting trading in September. Some of this is concern about AI corporate bond supply over the next few quarters after a surprise surge in recent weeks. However, it seems that they are also being used as a general hedge for all sorts of positive AI positions. There aren’t many credit names to use to hedge AI lending (private and public), or general exposure, so these are bearing the brunt.

The US calendar dominates this week as agencies work through the backlog caused by the 43-day shutdown. The headline event is Thursday’s September employment report. DB’s economists expect payrolls to rebound sharply, with headline and private payrolls both forecast at +75k versus prior readings of +22k and +38k respectively, leaving unemployment steady at 4.3%. Average hourly earnings should rise 0.3%, while hours worked edge up to 34.3. If realised, these figures would lift annual nominal compensation growth to 4.9%, though quarterly growth may slow to 3.7%, its weakest pace since the pandemic.

Beyond jobs, several delayed releases will inform Q3 US GDP estimates: August construction spending (today), factory orders (Tuesday), and the trade balance (Wednesday). Earlier data suggested 2.8% annualised growth for Q3 GDP, but this week’s numbers could tilt forecasts higher. More timely indicators include the Empire State manufacturing index (today), NAHB housing market index (tomorrow), Philadelphia Fed survey and October existing home sales (both Thursday). Consumer sentiment from the University of Michigan rounds out Friday, with inflation expectations within that survey remain a key watchpoint for policymakers.

Fed communication will be another major theme. A broad slate of officials speaks throughout the week, including Vice Chair Jefferson, Governor Waller (both today), and regional presidents Williams, Kashkari (today), Barkin and Collins. Markets will scrutinise these remarks for clues on the pace of rate cuts. Jefferson may be the most interesting to see whether he continues to suggest a slowing of rate cuts as the Fed approaches neutral.

The October FOMC minutes, due Wednesday, should shed light on internal debates and the conditions for a potential December move. Recent commentary suggests a more cautious tone, with some officials signalling that a December cut is far from assured, and on Friday December futures priced in a less than a 50% chance of a cut for the first time. ECB President Lagarde also speaks on Friday, adding a European angle to the policy debate.

Globally, attention will centre on flash November PMIs due Friday. Canadian (today) and UK (Wednesday) CPI figures are released, with UK retail sales and consumer confidence rounding out Friday. In Asia, Japan reports October CPI on Thursday, while China announces lending rates the same day. Corporate earnings will also feature prominently, with Nvidia in the spotlight on Wednesday, joined by Palo Alto Networks and major US retailers such as Walmart, Home Depot and Target. Chinese tech names Baidu and Xiaomi will also report. See the day-by-day week ahead for more at the end as usual.

Asian equity markets are mixed this morning even if US futures are strong. As I check my screens, Chinese risk is soft with the Hang Seng (-0.84%) leading losses followed by the CSI (-0.70%) and the Shanghai Composite (-0.47%) amid a renewed diplomatic row between Beijing and Tokyo as relations between the two countries sour further over Taiwan. Japanese stocks are also slightly weaker with the Nikkei (-0.11%) and the Topix (-0.37%) edging lower with the rising geopolitical tensions. Elsewhere, the KOSPI (+1.80%) is rebounding sharply driven chiefly by outsized gains in chipmakers SK Hynix and Samsung Electronics. S&P 500 (+0.43%) and NASDAQ 100 (+0.67%) futures are fairly strong for this time of the day higher.

Returning to Japan, the economy shrunk at an annualised rate of -1.8% in the July-September period (v/s -2.4% expected), as US tariffs sent the nation’s exports sharply lower. On a q/q basis, GDP slipped -0.4%, the first contraction in six quarters, but smaller than the -0.6% drop the market had expected. A big decline during the quarter came in exports, which were -1.2% down from the previous quarter. Yields on the 10yr JGBs are +2.3bps higher, trading at 1.73% as we go print.

Recapping last week now and markets saw initial optimism about the end of the longest government shutdown in history reverse as hawkish Fed commentary raised doubts that the Fed will cut rates in December. In the end, the S&P 500 was little changed (+0.08% on the week; -0.05% Friday), with a +1.54% gain on Monday offset by a -1.66% fall on Thursday. The small weekly gain was led by defensive sectors such as healthcare (+3.87% on the week) as Congress passed legislation funding most government agencies through January 30, which ended the shutdown after 43 days. By contrast, tech stocks struggled with the NASDAQ down -0.45% (+0.13% Friday) and the Mag 7 -1.19% weaker (+0.17% Friday). Those declines were led by a -5.86% drop for Tesla, though Nvidia managed to bounce back +1.07% (+1.77% Friday) despite Softbank announcing that it had sold its entire stake for $5.83bn to focus on other AI investing.

Struggles in momentum trades were also visible with Bitcoin, which fell -8.53% (-3.83% Friday) and is now -24% down from its early October peak and back to levels last seen in May (it’s bounced back a couple of percent this morning). By contrast, credit had a resilient week with US IG spreads flat and HY spreads -5bps tighter respectively.

In the rates space, hawkish comments from Fed officials pushed Treasury yields higher. On Friday, Dallas Fed President Logan said “I think it would be hard to support another rate cut unless we were to get convincing evidence” from the data. Other officials had earlier also sounded sceptical about a December cut, such as Boston Fed President Collins saying that “it will likely be appropriate to keep policy rates at the current level for some time”. All the comments saw the pricing of a December rate cut decline from 67% on Tuesday to 43% by Friday’s close, with 2yr Treasury yields climbing +4.5bps to 3.61% (+1.6bps Friday) and 10yr yields +5.1bps to 4.15% (+2.9bps Friday).

Over in Europe, the French National Assembly supported the suspension of the pension age increase until after 2027 to keep the budget process on track, leading to a rally in CAC 40 of +2.77% (-0.76% Friday). The Swiss market also outperformed (+2.73%, -0.84% Friday) as the US and Switzerland reached a preliminary trade deal lowering tariffs from 39% to 15%, in exchange of $200bn direct investment in the US by the end of 2028. Both the Stoxx 600 (+1.77%, -1.01% Friday) and the DAX (+1.30%, -0.69% Friday) also saw decent gains. On the bond side, 10yr bunds (+5.4bps) and BTPs (+4.0bps) matched the weekly move in Treasuries, while OATs (-0.4bps) outperformed on the budget news.

Finally, the UK came into the spotlight after the FT reported on Thursday night that PM Keir Starmer and Chancellor Rachel Reeves ditched plans to increase income tax rates at the upcoming budget. Further reporting on Friday suggested this was in part as more optimistic projections reduced the size of the fiscal gap. Still, the news weighed on UK assets, with 10yr gilts (+13.7bps Friday, +11.3bps on the week) seeing their biggest daily sell off in four months, while the FTSE 100 fell -1.11% Friday, underperforming European peers over the week (+0.16%).

Tyler Durden

Mon, 11/17/2025 – 08:49

https://www.zerohedge.com/markets/us-equity-futures-fade-overnight-gains-global-selloff-deepens

Hombres armados secuestran a 25 alumnas de secundaria en Nigeria y matan a empleado escolar

Por DYEPKAZAH SHIBAYAN

ABUYA, Nigeria (AP) — Hombres armados atacaron una escuela secundaria en el noroeste de Nigeria antes del amanecer del lunes y secuestraron a 25 alumnas, informó la policía.

Un empleado de la escuela fue asesinado y otro resultó herido en lo que fue el último incidente de secuestros escolares en la región norte de Nigeria.

Por el momento ningún grupo se ha atribuido la autoría de los secuestros en el internado del estado de Kebbi.

Según la policía, el incidente ocurrió a las 4:00 de la mañana y las menores fueron secuestradas de sus dormitorios. El internado está en Maga, en el área de Danko-Wasagu del estado, dijo el portavoz de la policía Nafi’u Abubakar Kotarkoshi.

Los agresores estaban armados con “armas sofisticadas” e intercambiaron disparos con los guardias antes de secuestrar a las menores, comentó Kotarkoshi.

“Un equipo combinado está actualmente peinando posibles rutas de escape y bosques circundantes en una operación coordinada de búsqueda y rescate destinada a recuperar a las estudiantes secuestradas y arrestar a los perpetradores”, agregó el portavoz.

Este es el secuestro escolar más reciente registrado en la región norte de Nigeria, donde grupos armados han atacado a niños en edad escolar desde 2014, cuando el grupo miliciano Boko Haram secuestró a 276 estudiantes de Chibok en el estado de Borno.

Los secuestros se han vuelto comunes en partes del norte de Nigeria, donde docenas de grupos armados aprovechan la limitada presencia de seguridad para llevar a cabo ataques en aldeas y a lo largo de las principales carreteras. La mayoría de las víctimas son liberadas tras el pago de rescates que a veces ascienden a miles de dólares.

En marzo de 2024, más de 130 escolares fueron rescatados después de pasar más de dos semanas en cautiverio en el estado nigeriano de Kaduna.

El secuestro masivo de 276 niñas de Chibok marcó el comienzo de una nueva era de miedo, con casi 100 de las niñas aún en cautiverio en 2024.

Desde los secuestros de Chibok, al menos 1.500 estudiantes han sido plagiados, ya que los grupos armados usan cada vez más estos crímenes como una forma lucrativa de financiar otros y controlar aldeas en la región rica en minerales pero mal vigilada del país.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

Brent Initially Slides After Russia Restarts Key Novorossiysk Port After Drone Attack

Brent Initially Slides After Russia Restarts Key Novorossiysk Port After Drone Attack

Brent crude prices were initially lower, and are now flat, after operations resumed at Russia’s key Black Sea export hub, Novorossiysk. This follows last Friday’s Ukrainian drone strike on the export hub, which had sent prices soaring.

Satellite images confirm major damage to the Sheskharis oil terminal in Novorossiysk after a combined drone and missile strike. Critical loading systems and pipelines were hit. With fires raging and infrastructure crippled, the port may be out of service for a long time. pic.twitter.com/waoSfx0qxj

— NOELREPORTS 🇪🇺 🇺🇦 (@NOELreports) November 15, 2025

Brent slid to $63 per barrel in Asia and Europe after Reuters and Bloomberg reported that crude-loading operations had resumed at Novorossiysk.

Bloomberg noted that two tankers were moored at the export hub on Sunday, while Reuters reported that loading had restarted.

Much of the overnight losses were cut by the time US traders woke up, as Brent prices inched above $64. Last Friday, the drone attack sent crude oil up more than 2%.

Here’s the chart:

“People were expecting a longer outage” at Novorossiysk following the strike, said Mukesh Sahdev, the founder and chief executive officer of Xanalysts Pty. Indications of a resumption are a “bearish signal,” he added. Sahdev was quoted by Bloomberg.

Ukrainian forces have increasingly targeted Russian oil export chokepoints, including oil-refining, storage, and export infrastructure, using drones and missiles. Novorossiysk was targeted for several key reasons:

Russia’s Largest Black Sea Oil Export Terminal: Novorossiysk handles a major share of Russia’s seaborne crude exports, including Urals and CPC Blend. When it goes offline, millions of barrels per day are at risk.

Key Outlet for Sanctions-Crimped Russian Supply: With many European ports closed to Russian oil, Black Sea routes have become even more vital. Novorossiysk is one of Moscow’s few remaining large, reliable export points.

Gateway to Europe, the Mediterranean, and Global Markets: Tankers from Novorossiysk move oil toward Europe, Turkey, India, and increasingly China. Any disruption affects multiple downstream markets.

Linked to CPC Pipeline Exports: The Caspian Pipeline Consortium (CPC) routes Kazakh and Russian crude to Novorossiysk.

The broader oil market outlook heading into 2026 remains bearish (read report).

Tyler Durden

Mon, 11/17/2025 – 08:34

Column: Stalled legislation could lead to horse racing/slot machines in Richton Park

There is a bill slowly grinding its way through the Illinois General Assembly that would allow construction of harness racetrack crammed with as many as 1,200 slot machines in Richton Park.

Did I just write that?

In Richton Park?

Late last month, the Illinois Senate passed, by a vote of 49-8, a bill that would clear the path for the start of construction of such a facility, a sports palace which Richton Park Mayor Rick Reinbold thinks could be built along the Sauk Trail-Laraway Road pathway just east of Harlem Avenue.

Hold on to your wallet, sports fans. This is still Illinois and, according to state Sen. Patrick Joyce, who along with state Rep. Anthony DeLuca are two of the eight co-sponsors of the bill, there are speed bumps which could delay or even kill the plan.

The biggest obstacle is the Stickney-based Hawthorne Racetrack which is the oldest family-run racetrack in North America. It has the authority through legislation to stop the development of any other horse track within 35 miles of its location in Stickney.

For the record, the village of Richton Park is a mere 24 miles south of Stickney as the crow flies.

Last year, the Illinois Senate passed a bill eliminating that provision by January 2026, but when the House OK’d the bill this session it made some changes which now have to be approved again by the Senate.

Two key differences passed by the House were the elimination of Hawthorne’s veto power over construction of another racetrack and limiting Hawthorne to one horse race meeting a year. The House must now approve the amended bill when it meets next year before it goes to Gov. JB Pritzker for his approval.

If Hawthorne’s ban on a nearby track is eliminated, the Illinois Racing Board could issue a license for a new track with a “limit” of no more than 1,200 slots on site. As a matter of record, the Wind Creek Casino in Homewood has more than 1,400 slot machines.

Richton Park Mayor Rick Reinbold, a Navy veteran, speaks May 9, 2024 at a veterans symposium. (Mike Nolan/Daily Southtown)

There is many a slip between legislative plans and final results, but if the bill runs into opposition in the House next year “we might have to start over again,” says Joyce.

Along with the potential for a trotting track in the south suburbs there is a similar bill that the Senate must also OK for a racetrack in Macon, Illinois, some 10 miles south of Decatur.

The horse racing industry has a long checkered history in the south suburbs. For 89 years, from 1926 to 2015, Lincoln Fields, later renamed Balmoral Park, situated near Crete, was the setting for both thoroughbred and standardbred racing. Perhaps the most famous horse to run at the track was the 1941 Triple Crown winner Whirlaway who, in June 1940, won his first race as a 2-year-old at the track.

In 2015, a U.S. Court of appeals judge fined both the owners of Balmoral and Maywood Park in Melrose Park $77.8 million as restitution to casinos in Joliet, Elgin and Auroa in the aftermath of a “pay to play” scheme involving the tracks’ contributions to then Gov. Rod Blagojavich.

Both tracks quickly filed for bankruptcy.

Balmoral opened two years later as a horse show arena, held some shows but by 2020 the facility was up for sale. Price was $4 million. There were no takers.

Homewood was the site of the Washington Park racetrack from 1926 until February 1977, when a fire destroyed the grandstand and put the facility out of business. During its heyday, it was a prime midsummer stop for thoroughbreds. Perhaps its biggest event was the Aug. 31,1955, match race with Nashua defeating Swaps for a purse of $100,000, which is the equivalent of $1,208,865 in today’s world.

Meanwhile Reinbold hopes things go his village’s way these days in another plan to improve his village’s financial lot.

Some two years ago, we commented about his request to the Chicago Bears to look at his community as the site of a new stadium. Everyone knew this was a pie in the sky idea and some thought it was a pointless bit of promotion.

Considering the seeming lack of enthusiasm in Chicago for almost all things south of City Hall, I thought that instead of asking “why” we should say “why not.”

Jerry Shnay is a freelance columnist for the Daily Southtown.

https://www.chicagotribune.com/2025/11/17/column-horse-racing-slot-machines-richton-park/

Presidente de Bolivia denuncia corrupción por 15.000 millones de dólares en gobierno anterior

Associated Press

LA PAZ, Bolivia (AP) — El presidente de Bolivia, Rodrigo Paz, denunció que en su primera semana en el gobierno se detectaron casos de corrupción por unos 15.000 millones de dólares cometidos durante la anterior administración.

“Todavía estamos procesando la información y en su momento presentaremos denuncias puntuales, pero lo que hemos encontrado es una cloaca con más de 15.000 millones de dólares en corrupción. Nos han robado el futuro”, dijo el domingo en una rueda de prensa.

El mandatario mencionó como ejemplo la compra de radares para el control aéreo en la lucha contra el narcotráfico por 360 millones de euros “que no funcionan”.

Paz también acusó a su antecesor Luis Arce (2020-2025) de dejar sin recursos al Estado central. “Nos han dejado sin dinero”, sostuvo al evaluar su primera semana al frente del gobierno.

El centroderechista heredó una economía sumida en la peor crisis en 40 años con una aguda escasez de combustibles y una inflación acumulada hasta septiembre de 18,33% respecto de similar periodo del año anterior. En tanto, la cotización del dólar en el mercado paralelo más que duplicaba el cambio oficial.

Bolivia importa cerca del 60% de la gasolina y casi el 90% del diésel que consume, lo que le demanda anualmente al Estado cerca de 3.000 millones de dólares, una de las mayores causas del déficit fiscal que bordea el 10% del Producto Interno Bruto (PIB), según informes oficiales.

Paz destacó que “se está normalizando la distribución de combustibles, el precio del dólar se estabiliza y el riesgo país está bajando” pero advirtió que “todavía nos falta reordenar la casa”.

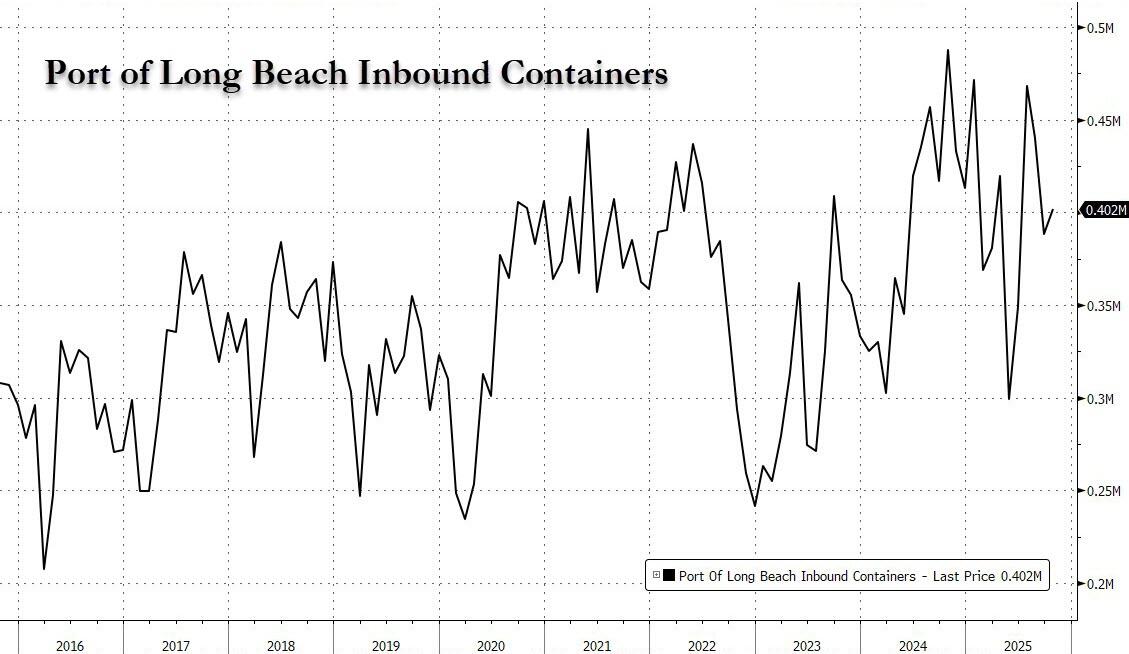

Container Imports Drop 17.6% In October At Busiest US Port

Container Imports Drop 17.6% In October At Busiest US Port

By Stuart Chrils of FreightWaves.

The Port of Long Beach is moving containerized cargo ahead of the cumulative record-setting pace achieved in 2024 despite weaker demand that saw October volumes drop by nearly 20% from a year ago.

The hub, which along with the Port of Los Angeles forms the San Pedro port complex, the nation’s busiest, moved a total 839,671 twenty foot equivalent units (TEUs) in October, down 14.9% from October 2024 – the strongest month in its 114-year history.

Imports declined 17.6% to 401,915 TEUs and exports dropped 11.5% to 99,817 TEUs. Empty containers, an indicator of future import shipments, decreased 12.6% to 337,940 TEUs.

Long Beach has moved 8,229,916 TEUs through the first 10 months of 2025, ahead 4.1% y/y and on pace to better 2024’s all-time record volume of more than 9.6 million TEUs.

The port has maintained steady operations despite an uncertain outlook amid ongoing tariff and trade policies, Port of Long Beach Chief Executive Mario Cordero and Chief Operating Officer Noel Hacegaba said in a virtual media call.

In response to a question from FreightWaves about the effect on cargo of the now-paused U.S. port fees on Chinese ships, Cordero said, “I think that the volume speaks for itself. Hopefully this pause — whether it’s ship fees or tariffs — will help the parties find a pragmatic solution that’s not going to impact the American consumer.”

“The consumer has not seen significant tariff impacts given that manufacturers, retailers, and others have shared in incurring some of these costs and mitigating price escalation to the consumer, but that may change as we approach 2026,” said Cordero, who earlier announced his retirement as port chief.

“Consumers will likely see price escalation in the coming months as shippers continue to pass along the cost of tariffs on goods and a higher percentage of these costs will be passed on to the consumer.”

Hacegaba said the port continues to work with its partners “to anticipate and mitigate issues before they arise to keep cargo and our economy moving.”

Tyler Durden

Mon, 11/17/2025 – 08:05

https://www.zerohedge.com/economics/container-imports-drop-176-october-busiest-us-port

Explosión en casa del sur de California hiere a ocho y daña viviendas cercanas

Associated Press

CHINO HILLS, California, EE.UU. (AP) — Una casa explotó en un vecindario del sur de California, hiriendo a ocho personas y dañando dos casas cercanas, un incidente en el que los bomberos evacuaron un total de 16 viviendas.

Los bomberos en Chino Hills no indicaron qué causó la explosión el domingo, pero mencionaron que detuvieron una fuga de gas. Fotos y videos del lugar mostraban la casa reducida a un montón de escombros.

“Las cuadrillas permanecerán en el lugar para continuar con la revisión y la investigación”, publicó en línea el Distrito de Bomberos de Chino Valley.

El Departamento de Bomberos informó que cuatro personas fueron llevadas de la casa a un hospital, y otras cuatro se trasladaron por sus propios medios. De momento se desconoce su estado de salud.

KABC-TV reportó que testigos dijeron haber visto a personas corriendo desde la casa que explotó, incluyendo niños pidiendo ayuda.

Las autoridades permitieron a las personas cuyas casas no resultaron dañadas regresar más tarde a sus viviendas.

Se dejó un mensaje telefónico solicitando comentarios a la Compañía de Gas del Sur de California.

Chino Hills tiene aproximadamente 78.000 habitantes y está a unos 56 kilómetros (35 millas) al sureste de Los Ángeles.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

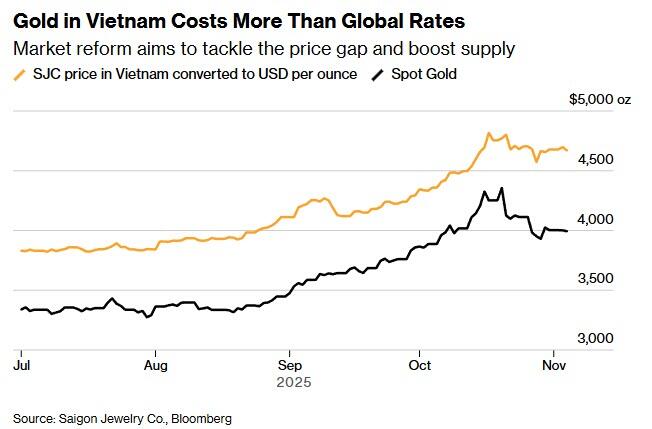

“I Feel Safer Holding Gold”: Vietnamese Govt Cracks Down On Hoarding

“I Feel Safer Holding Gold”: Vietnamese Govt Cracks Down On Hoarding

In the sweltering chaos of Hanoi, 67-year-old Le Thi Minh Tam is waging a desperate guerrilla war against vanishing stockpiles – scrambling from one gold shop to the next, only to find Soviet-style queues where the shiny salvation sells out faster than a central banker’s excuses.

“I’m getting worried, as I still don’t have enough,” she tells Bloomberg, the weight of her son’s impending nuptials crushing her, helped by the State Bank’s iron fist.

“They don’t sell gold bars anymore, only gold rings with a very limited amount for each customer.”

But as Bloomberg goes on to note, Tam’s not some outlier in this fever dream; she’s the face of a nationwide gold apocalypse triggered by the yellow metal’s moonshot to $4,380 an ounce last month.

Vietnam, where gold isn’t just bling but a cultural bunker against the fiat apocalypse – stashed under beds like contraband ammo for the next economic blitzkrieg – is in full-blown mania mode.

Weddings? Forget flowers; it’s all about gifting the one asset that laughs at inflation’s grim reaper. This isn’t optional; it’s ritual, a hedge forged in the fires of the Vietnam War when paper promises turned to ash, and even now, when bank deposits feel like IOUs from a Ponzi scheme run by Hanoi apparatchiks.

Down in Ho Chi Minh City (HCMC) – 1,700 km south, where the humidity matches the desperation – shoppers are turning into urban nomads, camping overnight like it’s the last chopper out of Saigon. Nguyen Kim Hue, a 57-year-old online food peddler scraping by in the gig economy’s underbelly, showed up at 6 a.m. thinking she’d outfox the horde.

“I thought coming at 6 a.m. was early, but it was already crowded,” she recounts, the bitter taste of empty-handed defeat still fresh from her last raid.

“The last time I came, I couldn’t buy anything because they ran out of gold.”

Cue the “sold out” signs, those scarlet letters of supply-chain sabotage.

Flashback to the glory days of communist control: Back in 2012, as inflation clawed at the dong like a rabid dog, the geniuses in Hanoi slapped a state monopoly on gold imports and production. The State Bank of Vietnam became the gatekeeper, funneling scraps through Saigon Jewelry Co.’s exclusive chokehold on bars. Result?

A yawning chasm between local premiums (10-15% over spot) and the global “free” market, birthing a black market beast that chewed up the currency and spat out volatility.

Fast-forward to October: The politburo finally cracks the door, ending the 13-year stranglehold in a half-hearted liberalization play.

But don’t pop the champagne – Hanoi’s still doling out import quotas like candy from a miser’s pocket, with the central bank playing quota czar.

“We’ll have to wait until mid-December to see how much gold import quota the central bank grants,” says Huynh Trung Khanh, vice chairman of the Vietnam Gold Traders Association, sounding like someone who has questioned his fair share of ‘five-year-plans’.

“It’ll probably be far below what the market needs to meet demand.”

Vietnam ‘demands’ 55 tons a year – a Southeast Asia heavyweight – but last year’s official imports were a measly 13.5 tons, courtesy of the same bureaucrats now pretending to “reform.”

The goal? Squeeze that premium down to 2-3%, turning Vietnam’s gold bazaar into a semi-respectable shadow of Shanghai or Mumbai. Good luck with that.

And why the frenzy? Because in a nation scarred by wars, famines, and fiat fuckery, gold is the ultimate protection against ‘the system’.

“We’ve been through wars and hard times, so people here have seen gold as the safest place for their money—a safe haven, something they can rely on when life gets tough,” Khanh remarks, echoing the global chorus from Delhi to Istanbul where central bank bids and retail panic are sending bullion to the stratosphere.

Globally, gold’s the cockroach of commodities this year – up big on ETF inflows and BRICS finger-flipping at the dollar – while wedding seasons worldwide turn jewelers into mints on steroids.

Prices have dipped from the peak, but the “sold out” apocalypse rolls on. Last week in HCMC, hordes queued for hours outside a flagship shop, tickets rationed like bread lines in the gulag. Hue dragged her husband into the fray and sweet-talked the clerk into five rings instead of one:

“At first the shopkeeper told me I could only buy one ring, but I persuaded her to sell me more,” she beamed.

“I’m so happy now.”

So what are the new rules?

As Bloomberg lays out, cash-for-gold’s dead; anything over 20 million dong ($760) demands a bank transfer, leaving grandma types fumbling for their kids’ apps like Luddites in a crypto winter.

Hue kicked off her hoard in June at 120 million dong per tael (that’s ~1.2 troy ounces for the uninitiated). Now? 147 million, a 22% gut-punch that’d make even Jamie Dimon wince.

“Before, I used to keep my savings in the bank, but now I feel safer holding gold,” she confesses.

“It’s my way of making sure my money doesn’t lose value. This is for my children’s education and my retirement.”

Translation: When the dong’s a dumpster fire and banks are just vaults for the elite’s digital funny money, you bet on the barbarous relic.

Even the kids are in on it.

Tran Thi Yen Nhi, 20 and slinging construction swag in HCMC, endured a three-hour vigil for her sister’s big day.

“My parents asked me to help, because it’s hard for them to stand in line for so long,” she says, generational torch-passing in action.

“I’ve made it a habit to buy gold whenever I can save some money, just little by little. Since I was a little girl, I saw my grandmother do the same. She bought gold whenever she saved a bit and then kept it under her bed.”

The World Gold Council pegs Vietnam’s under-mattress stash at 500 tons – pocket change next to India’s 34,600-ton elephant, but enough to make regulators sweat.

Enter the fixers

The Vietnam Association of Financial Investors is hawking a 10% tax on buys to “discourage hoarding” and shove peons toward their approved stock ponzis.

For now, it’s a measly 0.1% on bars for “data trails” and revenue grabs, plus a three-phase gold exchange rollout to drag the rings, coins, and bars out from under the bed and into the light (and sync prices with the world).

Because nothing says “trust us” like taxing the one thing folks trust more than your printing press.

But spare a thought for Tam, still grinding through the gauntlet as her son’s wedding looms like a debt collector.

“I’m so tired and worried,” she laments.

“The wedding is coming soon, and I still haven’t been able to buy enough. In Vietnam, gold isn’t just a gift. It’s how we show our love.”

In a world where governments peddle stability while inflating away your future, that’s not sentiment – it’s survival. And as Vietnam’s gold wars rage on, bet on this: The real mania’s just getting started.

Tyler Durden

Mon, 11/17/2025 – 07:45

Daywatch: Record property tax increases slam Chicago homeowners

Good morning, Chicago.

Chicago homeowners are being walloped with a record property tax hike, with some of the city’s poorest neighborhoods absorbing the steepest increases even as downtown office owners see their bills fall, according to new data from the Cook County treasurer’s office.

An analysis from Cook County Treasurer Maria Pappas’ office found the median property tax bill for a Chicago homeowner jumped 16.7% since last year, the largest percentage increase in at least 30 years. The surge follows similar spikes in Cook County’s north and south suburbs over the last two years and complicates the job of the Chicago City Council as it considers tax hikes to help close a historic budget gap.

The long-awaited second installment of Cook County property tax bills was mailed to property owners on Friday and is due Dec. 15. Across the county, residential and commercial property owners are being billed a total of $19.2 billion, a nearly 5% increase from last year. But the burden is falling unequally.

Read the full story from the Tribune’s A.D. Quig and Illinois Answers Project’s Alex Nitkin.

Here are the top stories you need to know to start your day, including: why your Thanksgiving turkey could cost more this year, 10 thoughts on the Bears’ win over the Vikings and how one musician is mashing up Beethoven and Beyoncé.

Today’s eNewspaper edition | Subscribe to more newsletters | Asking Eric | Horoscopes | Puzzles & Games | Today in History

United Airlines aircraft move from the gate at Fort Lauderdale-Hollywood International Airport, Nov. 13, 2025, in Fort Lauderdale, Fla. (AP Photo/Lynne Sladky)

FAA lifts order slashing flights, allowing commercial airlines to resume their regular schedules

The Federal Aviation Administration said yesterday it is lifting all restrictions on commercial flights that were imposed at 40 major airports during the country’s longest government shutdown.

Gov. JB Pritzker talks about recent Immigration and Customs Enforcement tactics and their effect on immigrant families at the Illinois Capitol during the legislative session on Oct. 30, 2025, in Springfield. (John J. Kim/Chicago Tribune)

Gov. JB Pritzker’s Accountability Commission still ramping up as federal immigration surge starts to subside

More than three weeks after Gov. JB Pritzker drew national attention for creating the Illinois Accountability Commission through an executive order, there is no apparent way for members of the public who have experienced or witnessed excessive force or other misconduct by federal immigration agents to report those allegations directly to the commission.

Latino US citizens racially profiled by federal immigration agents in Chicago: ‘I felt like a piece of trash’

Only 2.6% on list of 614 ‘Operation Midway Blitz’ arrestees had criminal histories, DOJ records show

Bronze turkey hens roam in a fenced grassy area after being fed on Nov. 14, 2025, at All Grass Farms in Dundee. Cliff McConville said his flock has not been affected by bird flu. (Dominic Di Palermo/Chicago Tribune)

Bird flu cases are on the rise again, including 2 million turkeys. Will that affect your Thanksgiving dinner?

Larger turkey-producing states have been hit hard in the past couple of months. Nearly 2 million turkeys have been affected by bird flu across the country since August, accounting for roughly 24% of all new cases in commercial and backyard flocks, even though turkeys only account for approximately 2% of the U.S. poultry inventory.

According to experts, the disease — combined with a drop of almost 10% in turkey meat production from last year, rising labor costs and lower overall consumer demand throughout the year — is triggering higher prices for wholesale and fresh turkeys just ahead of the holiday season.

Ross and Paula Fortini, of Libertyville, on Nov. 6, 2025. They have insurance through the Affordable Care Act exchange. If enhanced subsidies aren’t extended after the end of this year, their monthly insurance premiums will more than triple. (Stacey Wescott/Chicago Tribune)

Illinois consumers face high health insurance prices, with Obamacare subsidies still in limbo after shutdown

Selling a car. Moving homes. Cutting back on grocery spending.

They’re among the options Ross and Paula Fortini are considering if they have to pay for health insurance next year without subsidies from the federal government. The Libertyville couple’s health insurance through the Affordable Care Act exchange is set to more than triple — to more than $2,200 a month — if enhanced subsidies aren’t extended beyond the end of this year.

Bau Graves, then the executive director of the Old Town School of Folk Music, holds one of John Lennon’s guitars, a Martin D-28, on Oct. 4, 2013. (Alex Garcia/Chicago Tribune)

James ‘Bau’ Graves, former executive director of the Old Town School of Folk Music, dies at 73

James “Bau” Graves was the executive director of Chicago’s Old Town School of Folk Music for more than 11 years, steering the venerable institution in the North Side’s Lincoln Square neighborhood through a major expansion.

Graves, 73, died of heart failure on Sept. 26 at his home in Harpswell, Maine, said his wife, Phyllis O’Neill.

Valparaiso University’s first Lutheran president, William H.T. Dau, is joined by faculty members in this 1926 portrait. (Valparaiso University Archives & Special Collections/provided)

Valparaiso University marks 100 years of Lutheran control

One hundred years ago, the Lutheran University Association purchased a struggling Valparaiso University and made it what it is today.

Keith Kinzleo of Joliet stands with a sign of Ben Johnson and celebrates a Bears touchdown in the first half against the Vikings at U.S. Bank Stadium on Nov. 16, 2025, in Minneapolis. (Stacey Wescott/Chicago Tribune)

Ben Johnson’s Chicago Bears keep flipping the script in crucial moments: Brad Biggs’ 10 thoughts on Week 11

Pretty soon, even a creative screenwriter would run out of new and inventive ways for the Bears to win in dramatic fashion.

In stopping, at least for one game, a long trend of losing to NFC North foes, the Bears continued a run of pulling out victories in the final moments. Cairo Santos’ 48-yard field-goal attempt sailed through the uprights with no time remaining, lifting the Bears to a 19-17 victory over the Minnesota Vikings.

Week 11 recap: Bears beat Vikings 19-17 on Cairo Santos’ 48-yard FG as time expires

After Bears special teams had its miscues, returner Devin Duvernay found ‘a moment to make a play’

Audrey Billings, Brandon Dahlquist, Michael Mahler and Dara Cameron in “It’s a Wonderful Life: Live in Chicago!” by American Blues Theater in 2023. (Michael Brosilow)

Top 10 holiday shows in Chicago for 2025: Are you Scrooge, George Bailey or Jinkx this year?

Since it snowed, and froze, long before Thanksgiving this year, you won’t need any help to put yourself in the mood for holiday attractions. Here is our annual guide to the theater of the festive season.

Composer, conductor and producer Steve Hackman is presenting “Beethoven X Beyoncé” with the Chicago Philharmonic and guest musicians at the Harris Theater. (James Mountford)

Mashing up classical and pop with ‘Beethoven X Beyoncé’ at Harris Theater

Composer, conductor and producer Steve Hackman is breaking down barriers between the classical and pop music worlds, one orchestral reimagination at a time.

And for the first time, the Chicago-area native will return to his home city to lead the performance of his latest cross-genre work, “Beethoven X Beyoncé.” The 75-minute piece, performed by the Chicago Philharmonic and guest musicians, is a two-act fusion of Beethoven’s Symphony No. 7 with 15 Beyoncé songs.

Thanksgiving at Di Pescara. (Anjali Pinto)

Thanksgiving 2025: 70 Chicago restaurants offering dine in or take out holiday meals

Preparing Thanksgiving dinner can be an enormous hassle, involving spending all day in the kitchen keeping track of different cooking times for sides and the turkey to ensure that everything is warm and ready to go on the table. You can remove much of the stress and get to just enjoy your feast by picking up a ready-made meal from a Chicago restaurant or even a version where most of the work is done for you and you just have to roast the bird, filling the kitchen with delicious smells.

Thanksgiving 2025: 36 Chicago restaurants and bakeries offering pies and dessert

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}