Category: News

Naperville Police Arrests for Nov. 30-Dec. 3

The following items were taken from Naperville police reports and press releases. An arrest does not constitute a finding of guilt:

A 33-year-old woman from Yorkville was arrested on a warrant at 2:56 p.m. Nov. 30 in the 1600 block of West Diehl Road.

A 31-year-old woman from Aurora was arrested on a warrant at 9 p.m. Nov. 30 at West Jefferson Avenue and South Route 59.

A 23-year-old man from Willowbrook was arrested on a warrant at 10:31 p.m. Nov. 30 at McCoy Drive and South Route 59 in Aurora.

A 33-year-old man from Naperville was arrested on charges of driving with expired license plates, driver’s view obstructed, driving under the influence of alcohol, attempted possession of a controlled substance, unlawful possession of cannabis by a driver, driving on a registration suspended for non-insurance, driving without insurance and improper window tinting at 1:31 a.m. Dec. 1 in the 500 block of North Sleight Street.

A 27-year-old man from Romeoville was arrested on a warrant at 2:30 p.m. Dec. 1 at the police station, 1350 Aurora Ave.

A 27-year-old man from Berkeley was arrested on a warrant at 4:11 p.m. Dec. 1 at North Columbia Street and East 5th Avenue.

A 25-year-old man from Chicago was arrested on charges of aggravated battery and aggravated battery in a public place at 10:46 p.m. Dec. 1 at the police station, 1350 Aurora Ave.

A 33-year-old man from Plainfield was arrested on a warrant at 10:47 p.m. Dec. 1 at Hobson Road and Washington Street.

A 19-year-old man from Naperville was arrested on charges of reckless driving, street racing, speeding 35 mph over the posted limit and leaving the scene of an accident at 5:51 p.m. Dec. 2 at the police station, 1350 Aurora Ave.

A 55-year-old woman from Aurora was arrested on a warrant at 6:57 p.m. Dec. 2 in the 800 block of East Ogden Avenue.

A 28-year-old man from Aurora was arrested on charges of burglary and retail theft exceeding $300 at 4:30 p.m. Dec. 3 in the 1400 block of South Route 59.

https://www.chicagotribune.com/2025/12/08/naperville-police-arrests-blotter-december/

Trump Readies “One-Rule” Executive Order Aimed At Centralizing AI Regulation

Trump Readies “One-Rule” Executive Order Aimed At Centralizing AI Regulation

President Trump continues to argue that a single, national set of rules, otherwise known as a “One Rulebook,” governing the artificial intelligence industry is essential, rather than a patchwork of state-by-state regulations that would slow development amid a superpower race with China. This comes as Trump’s national strategy to build out data centers, revitalize the industrial base, restart rare-earth mining and refining operations, and upgrade power grids becomes vital to maintaining America’s tech dominance in the years ahead.

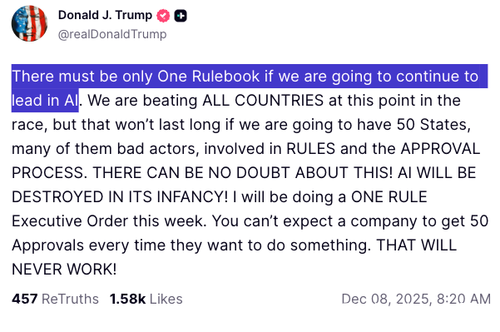

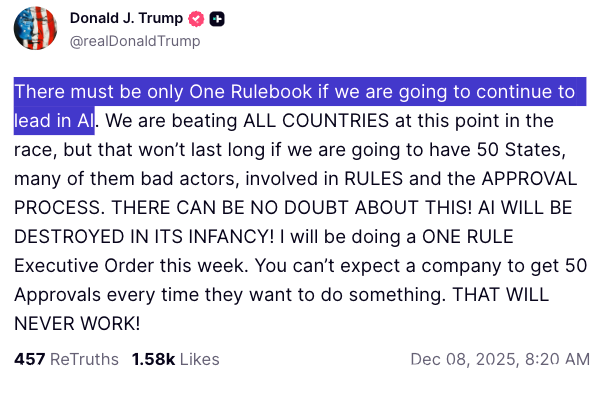

“There must be only One Rulebook if we are going to continue to lead in AI,” Trump wrote on Truth Social just moments ago.

He continued, “We are beating ALL COUNTRIES at this point in the race, but that won’t last long if we are going to have 50 States, many of them bad actors, involved in RULES and the APPROVAL PROCESS. THERE CAN BE NO DOUBT ABOUT THIS! AI WILL BE DESTROYED IN ITS INFANCY!“

Trump noted that the “One Rule Executive Order will be signed this week,” adding, “You can’t expect a company to get 50 Approvals every time they want to do something. THAT WILL NEVER WORK!“

The Trump administration believes that allowing 50 different states to create their own AI rules and approval processes would paralyze development, slow innovation, and ultimately be detrimental to the nation.

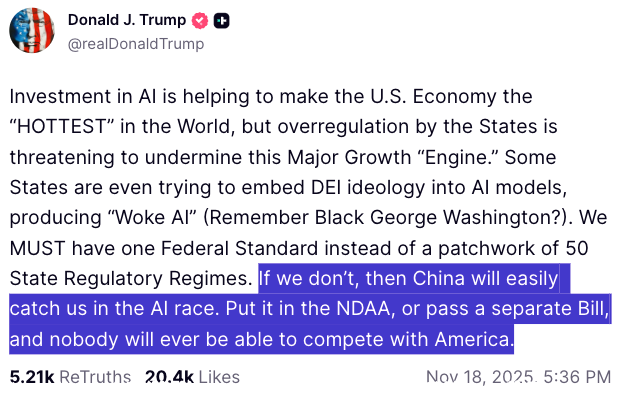

Last month, Trump wrote on Truth Social, “Some States are even trying to embed DEI ideology into AI models, producing ‘Woke AI’ (Remember Black George Washington?). We MUST have one Federal Standard instead of a patchwork of 50 State Regulatory Regimes.”

“If we don’t, then China will easily catch us in the AI race. Put it in the NDAA, or pass a separate Bill, and nobody will ever be able to compete with America,” the president warned.

Last Wednesday, Nvidia CEO Jensen Huang reiterated Trump’s points on the need for a national set of rules, noting that state-by-state AI regulation would harm the industry’s growth.

“State-by-state AI regulation would drag this industry into a halt and it would create a national security concern, as we need to make sure that the United States advances AI technology as quickly as possible,” Huang said.

Given the sheer incompetence of Democrats who have run blue states into the ground, exemplified most recently by the massive welfare fraud by Somalis under Tim Walz’s watch, the Trump administration believes a blanket federal approach to ensuring AI development is the best plan of action to secure the nation’s technological advantage over the rest of the world… and the man at the center of AI – Jensen Huang – agrees vehemently: “A federal AI regulation is the wisest.”

Tyler Durden

Mon, 12/08/2025 – 09:00

https://www.zerohedge.com/ai/trump-readies-one-rule-executive-order-aimed-centralizing-ai-regulation

Confluent Shares Erupt After Report Of $11 Billion IBM Takeover Bid

Confluent Shares Erupt After Report Of $11 Billion IBM Takeover Bid

Confluent shares skyrocketed in premarket trading in New York after a Wall Street Journal report revealed that IBM is in talks to buy the data infrastructure company for $11 billion. The deal could be announced as soon as today.

*IBM acquiring Confluent in $11 billion all-cash deal

*IBM: Confluent Deal Represents Enterprise Value of $11 Billion

— zerohedge (@zerohedge) December 8, 2025

Confluent is a data-infrastructure software company built around Apache Kafka, an open-source technology created at LinkedIn and later spun out. It offers a streaming data platform that lets companies move and process data in real time rather than in slow batches, which is vital for AI and machine-learning pipelines.

A successful deal would be IBM’s largest in years, furthering its pivot toward AI and cloud after the $6.4 billion HashiCorp purchase last year. IBM has posted increasing consulting revenue, slashed thousands of jobs to restructure its workforce, and ramped up quantum computing development.

Shares of Confluent surged 28% in premarket trading. The stock is down 17% on the year as of Friday’s close and has been range-bound since the second half of 2022.

The potential deal shows how IBM is continuing to pivot from its slow-growing legacy business and reshape itself around AI and quantum computing. It wants to be viewed as a serious player in AI infrastructure rather than just another legacy enterprise software vendor.

Tyler Durden

Mon, 12/08/2025 – 08:50

https://www.zerohedge.com/markets/confluent-shares-erupt-after-report-11-billion-ibm-takeover-bid

Futures Rise For 10th Day In Past 11 With Fed Rate Cut Looming

Futures Rise For 10th Day In Past 11 With Fed Rate Cut Looming

With just 17 trading sessions left in 2025, stock futures edge higher again and are on pace for 10 gains in the past 11 days. S&P 500 futures were up 0.2% as of 5:32 a.m. in New York, with Nasdaq 100 contracts +0.3%. Pre-market, Mag 7 are mostly unchanged except for a -1.3% decline in TSLA on a downgrade from Morgan Stanley. Most Asian markets clock firm start to the week, while European markets are mixed. Bond yields are 1-2bp higher and the USD is flat after reversing an earlier drop. Commodities are mixed: oil and most base metals are down small, while precious metals are higher. Over the weekend, there were several corporate headlines: (i) MSFT is considering shift custom chip business to Broadcom from Marvell (The Information). (ii) Trump warned the Netflix-Warner deal may post antitrust problem (BBG); (iii) IBM close to buy Confluent. A Fed cut on Wednesday looks like a done deal, but the trajectory after that is less clear. JPMorgan’s Mislav Matejka warned that the recent stock rally could stall after the decision. The Fed is also expected to restart “Reserve Management Purchases” ($45BN per month), which according to BofA’s Mark Cabana is not priced in; we also get earnings from Oracle and Broadcom, which may provide an end-of-year test for the AI narrative.

In premarket trading, Mag 7 stocks are mixed, with Tesla an outlier to the downside following a downgrade by Morgan Stanley from OW to EW (Amazon +0.3%, Nvidia +0.2%, Alphabet -0.1%, Microsoft +0.07%, Meta -0.1%, Apple -0.3%, Tesla -1.3%)

Agios Pharmaceuticals (AGIO) falls 3% after saying that the FDA has not yet issued a regulatory decision on the supplemental new drug application for mitapivat in thalassemia.

Carvana (CVNA) rises 9%, CRH (CRH) gains 7% and Comfort Systems USA (FIX) climbs 1% after S&P Dow Jones Indices said they will join the S&P 500 Index before trading opens Dec. 22.

Confluent (CFLT) is up 28% after the the Wall Street Journal reported International Business Machines Corp. is in advanced negotiations to acquire the data infrastructure firm.

CoreWeave (CRWV) drops 5% after announcing a $2 billion convertible senior notes offering.

Fluence Energy (FLNC) falls 4% after Mizuho Securities analyst Maheep Mandloi cut the recommendation to underperform, saying data-center opportunities are still early-stage.

ITT (ITT) slips 3% after plans to sell 7 million shares to help fund a portion of its SPX Flow deal.

Kymera Therapeutics (KYMR) rises 29% after the drug developer announced positive results from a Phase 1b clinical trial of KT-621.

Tesla (TSLA) shares fall 1.4% in premarket trading as Morgan Stanley downgrades the electric-car maker to equal-weight from overweight, saying non-auto catalysts priced into the stock.

In corporate news, Trump raised potential antitrust concerns around Netflix’s planned $72 billion acquisition of Warner Bros. Discovery. IBM is in advanced negotiations to acquire data infrastructure firm Confluent for around $11 billion, the WSJ reported. Robinhood is set to enter the Indonesian market after signing deals to acquire two local brokerages. Unilever spinoff The Magnum Ice Cream Co. will start trading in New York today as part of a three-location listing.

US stocks have rebounded in recent weeks after some Fed officials – and especially vice chair John Williams – signaled they intend to cut rates for a third straight time on Wednesday. Still, the advance has been jittery as uncertainty over the pace of easing in 2026 and wariness about the sustainability of an AI-driven rally temper sentiment.

Investors are now looking ahead to 2026. Over three-quarters of asset managers polled in an informal Bloomberg survey are positioning for a risk-on environment through 2026. Among strategists, Oppenheimer AM’s John Stoltzfus is calling for an 18% rally in the S&P 500 next year, becoming the most optimistic forecaster among those tracked by Bloomberg for a third year running. Still, there are some nuances. Investors are rotating out of the tech behemoths that drove virtually all of this year’s rally in the S&P 500 and are snapping up shares of risky small companies and old-economy transportation names. Yardeni Research now recommends effectively going underweight the Mag 7 versus the rest of the S&P 500, expecting a shift in earnings growth ahead.

For stocks, interviews with 39 investment managers across the US, Asia and Europe showed that a vast majority of allocators were still positioning for a risk-on environment through next year. The thrust of the bet is that resilient global growth, further developments in artificial intelligence, accommodative policy and fiscal stimulus will deliver outsize returns.

Fabien Benchetrit, head of target allocation for France and southern Europe at BNP Paribas Asset Management, said he remains bullish on 2026 but isn’t planning to increase his stock exposure before year-end. “Like other market participants, we’ve had a good year and it doesn’t make much sense to do it when liquidity typically dries up in the last two weeks of December,” he said. “In terms of AI, 2025 was all about capex, but 2026 will be about these investments delivering revenues, profits and productivity gains.”

Unease that inflation remains too high has also caused divisions among Fed officials, in a rift that’s been exacerbated by the lack of fresh data during the shutdown. After this week’s likely cut, money markets are leaning toward two more moves by the end of 2026, down from three signaled barely a week ago.

While a resilient economy, seasonal support and catch-up positioning are supporting stocks, key risks still loom for investors, said Daniel Murray, deputy chief investment officer and global head of research at EFG Asset Management. Those include “that the Fed is less dovish than investors currently assume,” Murray said, along with “a delayed tariff impact that sees inflation higher for longer and cracks starting to widen in the labor market.”

“The tone of Chair Powell’s press conference and accompanying statement will be critical,” wrote Deutsche Bank AG strategist Jim Reid. “We expect Powell to emphasize that the hurdle for further cuts in early 2026 is high, signaling a near-term pause. This guidance will be key to maintaining credibility.”

The Stoxx 600 is little changed as gains in industrial and insurance shares are offset by losses in consumer products and chemicals. Here are some of the biggest movers on Monday:

Kloeckner shares climb as much as 27% in Frankfurt, the most since 2008, after the firm said Worthington Steel was conducting due diligence with a view to a potential takeover of the German metals company.

Galderma shares rise as much as 4.5%, touching a record high, after L’Oreal announced plans to double its stake in the Swiss dermatology firm to 20%.

FlatexDEGIRO shares rise as much as 5.9% after Berenberg raised its price target on the online brokerage firm.

AUTO1 shares rally as much as 5.4% after Jefferies initiated coverage of the digital platform for buying and selling used cars with a buy recommendation.

Absa shares rise as much as 4.8% in Johannesburg, to their highest intraday level on record after the bank said it expects mid-single digit revenue growth in 2025, with stronger growth in non-interest income than net interest income.

GEA Group shares sink as much as 5%, to their lowest level since April, after Morgan Stanley downgraded the equipment supplier for the food processing industry to underweight.

Ferrari shares fall as much as 3% after Morgan Stanley downgraded the Italian luxury car maker to equal-weight on account of its decision to strictly limit volume growth until 2030.

Embracer falls as much as 33% as shares in the Swedish game company traded without rights to the upcoming spinoff of its Coffee Stain Group subsidiary.

Schott Pharma shares drop as much as 6.8% to the lowest level on record after analysts at Barclays and Deutsche Bank downgraded their ratings on the stock, saying the 2026 fiscal year will be a “transition year” for the German pharma packaging company.

Earlier in the session, Chinese indexes rally after local media reports leverage limit hike for brokerages, and the Politburo pledges more proactive macroeconomic policies. The ChiNext soars more than 3% and the CSI 300 gains about 1.2%. Topix, Taiex and Kospi are also in the green. Hang Seng slides almost 1%.

In FX, the Bloomberg Dollar Spot Index is flat. EUR/USD rose to session highs after ECB’s Schnabel said she is comfortable with investor bets that the next interest-rate move will be an increase. The yen eases back to around 155.50/USD. Offshore yuan stays marginally stronger after a strong trade report.

In rates, treasuries outperform their European counterparts but are still in the red. US 10-year borrowing costs climb 2 bps to 4.15%. Europe led declines in global bond markets after the European Central Bank’s Isabel Schnabel became the first senior official to suggest with any certainty that European rates have reached a floor, and she is comfortable with investor bets that the next interest-rate move will be an increase. German 10-year yields rise 4 bps to 2.84%. Gilts also drop, pushing UK 10-year yields up 4 bps to 4.52%. Japanese bond yields rose across the curve after data showed that the economy shrank in the three months through September, giving some justification for Prime Minister Sanae Takaichi’s stimulus package announced last month. The figures add an element of complexity to the Bank of Japan’s policy decision next week, but likely won’t derail it from its gradual hiking path. Aussie bonds remain heavy as 10-year yield hits a two-year high ahead of Tuesday’s RBA decision. JGB futures are tightly rangebound following lackluster GDP report.

In commodities, WTI crude futures fall 1% to near $59.50 a barrel. Brent crude futures pause around $63.90 and gold rises back above $4,210 an ounce. Spot gold adds $10 while Bitcoin rises 1.9% to around $92,000.

Today’s economic calendar includes November NY Fed 1-year inflation expectations at 11am

Market Snapshot

S&P 500 mini +0.1%

Nasdaq 100 mini +0.2%

Russell 2000 mini +0.4%

Stoxx Europe 600 little changed

DAX +0.2%

CAC 40 little changed

10-year Treasury yield +1 basis point at 4.15%

VIX +0.8 points at 16.22

Bloomberg Dollar Index little changed at 1211.98

euro little changed at $1.1652

WTI crude -0.9% at $59.54/barrel

Top Overnight News

Donald Trump said Netflix’s planned $72 billion acquisition of Warner Bros. Discovery may pose antitrust concerns, warning that the combined entity’s market share “could be a problem.” He confirmed he met with Netflix co-CEO Ted Sarandos recently. BBG

Trump plans to unveil a $12 billion farm aid package today, including one-time payments for crop farmers hit by low prices amid slow Chinese purchases. Advisers are also weighing measures to curb soaring beef prices, including reopening the border to Mexican cattle. WSJ

Trump signed a Presidential Memorandum directing the HHS to fast-track a comprehensive evaluation of the vaccine schedules from other countries around the world, and better align the US vaccine schedule.

White House said it will establish food supply chain security task forces to protect competition.

US Treasury Secretary Bessent said the US will finish the year with 3% GDP growth.

China’s trade surplus in goods this year topped $1 trillion for the first time, a milestone that underscores the dominance that the country has attained. For the first 11 months of the year, China’s exports increased 5.4% from the year-earlier period to $3.4 trillion, while the country’s imports declined 0.6% over that same stretch to $2.3 trillion. WSJ

China’s annual car sales dropped 8.5% in November in a second straight monthly decline, for their biggest fall in 10 months, data showed on Monday, amid a waning scramble to buy vehicles before government subsidies dwindle at year-end. RTRS

Japan’s real wages shrank for the 10th consecutive month in October, with an uptick in nominal pay falling short of taming relentless consumer inflation, government data showed on Monday.

Thailand has launched air strikes on Cambodia after border clashes that killed on Thai soldier, marking the collapse of a Trump brokered peace deal between the south east Asian neighbors. FT

Industrial production in Europe’s largest economy continued to accelerate in October, with the sector showing further signs of stabilization as it awaits large-scale government investment. October came in at +1.8% M/M (vs. the Street +0.3%). WSJ

Sen. Bill Cassidy (R-La.) said he planned to present Republican leadership with his health care plan as soon as Sunday night, predicting that the divisive proposal to put money directly in Americans’ health savings accounts could clear the 60-vote threshold needed to pass in the Senate. Politico

IBM is in advanced talks to acquire data-infrastructure company Confluent (CFLT) for around $11 billion, according to people familiar with the matter. A deal could be announced as soon as today. WSJ

Following an 11% drawdown this fall, Consumer Discretionary stocks have rebounded by 7% during the past two weeks. The combination of hawkish Fed commentary, weak labor market data, declining consumer sentiment, and downbeat corporate commentary contributed to a sell-off in Consumer Discretionary stocks between early September and mid-November. During the past two weeks, however, consumer stocks have rebounded, with the equal-weight S&P 500 Consumer Discretionary sector outperforming the equal-weight S&P 500 by 2%: Goldman

Trade/Tariffs

US President Trump said we’ll work it out, when asked if he would restart trade talks with Canada, while it was separately reported that the Canadian PM’s office said PM Carney agreed with US President Trump and Mexican President Sheinbaum to keep working together on the trade deal.

USTR said China’s trade commitments are going in the right direction and that they are seen to be in compliance so far.

French President Macron warned that the EU could hit China with tariffs if nothing is done to reduce its widening trade deficit with the EU, according to Les Echos.

EU is to expand the carbon border tax to garden tools and washing machines, as it seeks to close loopholes in the law to prevent carbon-intensive imports, according to FT.

US Embassy in India said US Under Secretary of State for Political Affairs Allison Hooker will visit New Delhi and Bengaluru, India, on December 7th-11th.

German Foreign Minister said a lot of work is still needed to persuade China to issue general export licenses for rare earths.

China’s Vice Commerce Minister said he welcomes EU automakers to continue to invest in China. Urges Germany and the EU auto association to push the EU Commission to resolve the EV anti-subsidy case. On Nexperia, he said the root cause of chaos in the global semiconductor supply chains lies in the Netherlands.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed following a lack of major macro drivers over the weekend and with markets tentative ahead of this week’s risk events, while participants also digested data, including the latest Chinese trade figures. ASX 200 was subdued amid somewhat mixed trade data from Australia’s largest trading partner and as the RBA kick-started its 2-day policy meeting. Nikkei 225 traded indecisively following a slew of mixed data from Japan, including firmer-than-expected Labour Cash Earnings and disappointing revisions to Q3 GDP, while sentiment was also clouded by geopolitical tensions after Japan accused Chinese fighter jets of aiming military radar at Japan’s Self-Defence Force jets. Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark underperforming as gains in tech were overshadowed by losses in the big banks, while participants also digested the latest Chinese trade data, which showed a stronger-than-expected recovery in Exports but Imports disappointed.

Top Asian News

China’s Politburo held a meeting on the economy and reiterated its stance that monetary policy is to be moderately loose, with fiscal policy being more proactive, while it stated that the economic operation is generally stable and it will implement more active macro policies. Furthermore, it will continue to prevent and resolve risks in key areas, as well as stabilise employment, markets, and enterprises’ expectations.

Hong Kong held its legislative election on Sunday to elect 90 Legislative Council members from the 161 government-vetted candidates.

Australia Treasurer Chalmers said they will not extend electricity rebates and that the mid-year review will not be a mini budget, while he added that the review will include savings.

BoJ Governor Ueda to attend Japan’s lower house budget committee from 05:35-06:05 GMT on Tuesday, according to a parliamentary source cited by Reuters.

Chinese President Xi held a meeting with non-party members on the economy, according to Xinhua, and said China to stabilise jobs and markets. said 2025 has been unusual and will smoothly meet the main targets. To reinforce economic growth momentum. Economic goals will be achieved this year. To drive reasonable economic growth.

China’s auto industry body CPCA said China sold 2.24mln passenger cars in November, down 8.5% Y/Y; Tesla (TSLA) exported 13,555 China-made vehicles (prev. 35,491 in October).

Indonesian Finance Minister said the nation is to impose a coal export tax near year between 1% and 5%.

European bourses (STOXX 600 +0.1%) began the morning mixed, with a slight negative bias. Since the open, indices have held an upward bias with some climbing marginally into the green. European sectors are mostly lower. Industrials and Tech hold towards the top of the pile, whilst Real Estate and Media lags a touch. In terms of a key story, BNP Paribas (+0.7%) is to sell its stake in AG insurance to Ageas (+2.2%) for EUR 1.9bln.

Top European News

UK PM Starmer said former Deputy PM Angela Rayner will return to the cabinet after resigning in September, while he described her as “hugely talented”.

Tony Blair is reportedly exploring alternative Labour leadership options amid frustration with UK PM Starmer’s direction, according to The Times.

ECB’s Schnabel said she is ‘comfortable’ on bets that next move will be a hike. Later on, she also said she would be ready to succeed President Lagarde if she were asked to, via Bloomberg. She said the euro economy is on course to grow above potential despite the headwinds, and the economic outlook has brightened and the downside risks to growth have been reduced significantly, and uncertainty has come down quite quickly, which should further support future economic activity. The global economy and global trade have proven to be more resilient. On inflation, she said it’s in a good place. It’s currently around 2%, and we also project medium-term inflation to be around 2%. Volatile energy prices and related base effects may push headline inflation temporarily below our target. Services inflation has been much stickier than expected. The downward pressure on goods inflation due to a stronger euro, lower energy prices and potential trade diversion from China has been weaker than expected. On policy, she said interest rates are in a good place. Rather comfortable with those expectations of the next move being a rate hike. A first rate hike in June 2026 remains very uncertain.

ECB’s Rehn said the ECB is concerned about central bank independence in the US, via Econostream. Adds that Fed independence is an important issue for “all of us globally”. On an insurance cut, said “we are not in the insurance business, not in December, March or June”. Inflation expectations have remained quite well anchored around the 2% target. German spending to have a “formidable positive impact” on Germany and the Euro area.

ECB’s Rehn said they must be aware of upside and downside inflation risks, while he added that inflation risk is slightly tilted to the downside in the medium-term. Furthermore, he said they should not impose unnecessary bars or floors on policy, and that the position on interest rates is not fixed.

French President Emmanuel Macron called for a change in the ECB’s approach to monetary policy to boost the single market and protect it from the risks of a financial crisis, while he commented that reasserting the value of the European internal market means it can’t let inflation be its sole objective, but also growth and employment.

European Commission may announce a package to support the auto industry on December 16th, according to industry sources.

German Chancellor Merz and French President Macron are set to discuss the fate of the Franco-German fighter jet project FCAS in the week of December 15th, according to an industry source.

Germany’s auto industry body VDA said it expects 2026 registrations to rise 2% to 2.9mln. Electric car sales in Germany to jump 17% to 979k in 2026. Expects the nation to remain the world’s second-largest EV producer in 2026.

French Socialist Party (PS) leader Faure said the party will vote for the French budget’s social security programme.

FX

DXY has now returned to flat territory after being dragged lower, but EUR strength as ECB hawk Schnabel said she is ‘comfortable’ on bets that the next move will be a hike, albeit not any time soon, according to Bloomberg. Little notable reaction was seen in ECB marking pricing throughout 2026, which remains unchanged for rates throughout the horizon, although the EUR strengthened and EZ yields rose.

The Single Currency was also supported by surprisingly upbeat German Industrial Output data. EUR/USD hit a 1.1672 peak, matching Friday’s high, before waning back towards 1.1650 levels. Subsequently, DXY fell to a 98.79 trough before trimming losses back towards near-99.00.

GBP is subdued by the EUR/GBP cross, which briefly eclipsed its 50 DMA (0.8751) from a 0.8726 low on the back of the aforementioned ECB commentary and data. GBP/USD meanwhile closed around its 200 DMA on Friday and traded below the level (1.3331) throughout most of today’s session. In terms of weekend UK newsflow, Tony Blair is reportedly exploring alternative Labour leadership options amid frustration with UK PM Starmer’s direction, according to The Times.

Other G10s are largely flat with Antipodeans mixed following the Chinese Trade Balance data, which showed a stronger-than-expected recovery in Exports but Imports disappointed. Thus, AUD is subdued ahead of the RBA decision tomorrow, whilst NZD is among the better performers as AUD/NZD falls back after meeting resistance at 1.1500.

Fixed Income

USTs are trading lower by a couple of ticks, having held a negative bias throughout the European morning. Nothing really much driving things for US paper this morning, and action appears to be following peers and in a continuation of Friday’s losses. Traders await the FOMC meeting mid-week, where a 25bps cut is widely expected – but likely to be subject to dissent from several board members. Back to price action, USTs are trading within a narrow 112-14 to 112-19 range, with today’s trough a tick below that made on Friday. Further pressure could see a retest of the trough made on 20th November at 112-10+.

Bunds are also pressured, and to a larger magnitude than USTs (but less so than UK paper). The benchmark followed US paper overnight, and held a negative bias, before taking a leg lower on comments via Schnabel. The arch-hawk, speaking on Bloomberg, said that she is ‘comfortable’ on bets that the next move will be a hike, albeit not any time soon. In an immediate reaction, Bund Mar’26 fell from 127.98 to 127.80 over the course of around 5 minutes, before then extending to a trough of 127.74; from a yield perspective, the 10-year rose 3bps to 2.83%, levels not seen since March. Elsewhere, other ECB members have not impacted assets quite so much, with Rehn suggesting that “inflation expectations have remained quite well anchored around the 2% target.”, via Econostream. And finally on the data front, German Industrial Output M/M rose more than expected; ING’s Brzeski said “there are at least tentative signs of a bottoming out” in the German economy.

Gilts underperform vs peers, and are currently down by around 40 ticks. Price action has been fairly muted this morning, gapped lower at the open and has resided at the bottom end of a 90.90 to 91.11 range. Pressure today in tandem with US/German paper, but with underperformance perhaps explained by ongoing domestic political updates. Focus has been on reports that Tony Blair is reportedly exploring alternative Labour leadership options amid frustration with UK PM Starmer’s direction, according to The Times. Moreover, perhaps some focus on political instability within the Labour Party as PM Starmer floats the return of Angela Rayner. Elsewhere, a KPMG/REC survey showed the UK labour market weakened further in November.

Commodities

WTI and Brent oscillated in a tight USD 59.98-60.27/bbl and USD 63.63-63.94/bbl, respectively, throughout the APAC session. As the European session got underway, benchmarks failed to extend the highs of the APAC session and reversed lower to dip below USD 60/bbl and USD 63.50/bbl, despite a lack of crude-specific newsflow. Currently, benchmarks are extending on session lows as progress on a potential peace deal between Ukraine and Russia remains in focus.

Spot XAU edged higher throughout the APAC session amid a weaker dollar ahead of Wednesday’s FOMC rate decision, in which the Fed is expected to cut rates by 25bps at its meeting on Wednesday. XAU hit a low of USD 4191/oz as the APAC session commenced and gradually traded higher to a peak of USD 4219/oz as the European session got underway. Data over the weekend showed that the PBoC increased its gold reserves for a 13th consecutive month.

3M LME Copper extended to a new ATH of USD 11.75k/t as China’s Politburo reiterated its stance that monetary policy is to be moderately loose, setting domestic growth as its top economic priority. This comes amid new demand, fuelled by AI infrastructure build and EVs, coming up against a tight global supply. China’s exports also rose in November to 5.9%, compared to the expected 3.8% and the October figure of -1.1%.

UAE Energy Minister said overall demand for energy will increase, fossil fuels will be “a percentage of it”. Adds that natural gas is important and they intend to not only satisfy their local demand but also grow exports of their LNG. Agrees that natural gas demand is more than the projects they are seeing.

Russia’s Kremlin said India buys energy where it is profitable to; as far as Russia understands, India will “continue to do that”.

EU to delay proposals on carbon border tariff and proposals for automotive sector, including Co2 emissions to December 16th, according to a document seen by Reuters.

Geopolitics: Middle East

Israeli PM Netanyahu said he will meet with US President Trump this month, while he said they believe there is a path to a workable peace with their Palestinian neighbours and that the sovereign power of security from the Jordan River to the Mediterranean will always remain in Israel’s hands. Furthermore, he said political annexation of the West Bank remains a subject of discussion, and the status quo in the West Bank will remain for the foreseeable future, as well as noted that they are close to the second phase of Trump’s Gaza plan.

Palestinian PM Mustafa said Israel is stepping up the ‘creeping annexation’ of the West Bank and is intensifying efforts to make the West Bank unliveable and drive people out of the occupied territory, according to FT.

Turkey’s Foreign Minister said Hamas is ready to hand over the Gaza administration to the Palestinian committee to advance the Gaza ceasefire deal. He also commented that Hamas disarmament in the first phase of the Gaza deal may not be a realistic and doable objective, while other steps are needed first.

US, Israel and Qatar were reportedly holding a trilateral meeting in New York on Sunday to rebuild relations, according to Axios.

A US official said the US is pushing Ukraine to agree “faster” to the peace plan, according to AFP.

Geopolitics: Ukraine

Ukraine’s President Zelensky says no accord so far on Ukraine’s Donbas in US talks, via Bloomberg.

Ukrainian President Zelensky said he had a substantive call with US envoy Steve Witkoff and Jared Kushner, while he stated they agreed on the next steps and format for talks with America, as well as noted that Ukraine is determined to continue working honestly with the US side in order to bring real peace. Zelensky separately commented that talks with US representatives on a peace plan were constructive but not easy.

Ukrainian military conducted a strike on Russia’s Ryazan oil refinery.

Russian Defence Ministry said Russian forces captured Kucherivka in Ukraine’s Kharkiv region and completed the capture of Rivne in Ukraine’s Donetsk region, while they carried out a group strike on Ukraine’s transport infrastructure facilities, fuel and energy complexes, and long-range drone complexes.

Russia and China held their third joint anti-missile drills on Russian territory.

Japanese Chief Cabinet Secretary Kihara said China’s claims about the Japan Self-Defence Force’s dangerous flight are inaccurate, while he added it is very important to gain an understanding of other countries, including the US, regarding Japan’s stance.

Japan is reportedly frustrated at the Trump administration’s silence over the row with China and urged the US to give PM Takaichi more public support, according to FT.

Australia’s Defence Minister Marles said they are deeply concerned about the actions of China following the air incident near Japan, while Marles discussed with Japanese Defence Minister Koizumi common serious concerns about the situation in the South China Sea and East China Sea. Furthermore, they discussed how to work together to maintain a free and open Indo-Pacific, while Marles also commented that they want the most productive relationship they can achieve with China.

Pakistan and Afghanistan exchanged heavy fire in a border region on Friday.

Thai Army spokesman said their military launched airstrikes in the disputed border area with Cambodia.

The Chinese Foreign Ministry said China believes both countries can win from cooperation on the new US defence strategy. Also said it stands ready to work with the US to improve ties and that China will firmly defend its sovereignty.

Rapid Support Forces confirms control of Heglig oil field, the largest oil field in Sudan, according to Sky News Arabia.

Russia’s Kremlin said it welcomed the removal of Russia from the list of US direct threats in the new national security strategy.

Geopolitics: Other

Japanese Defence Minister Koizumi said Chinese military planes directed radar at Japan’s self-defence forces twice. It was separately reported that Japanese PM Takaichi said the incident involving Chinese fighter jets directing radar at Japanese planes is extremely regrettable, while she said they will respond calmly and resolutely to the development.

US Event Calendar

November NY Fed 1-year inflation expectations at 11am

DB’s JIm Reid concludes the overnight wrap

All roads this week will point to Wednesday’s FOMC. Markets and DB expect the Fed to deliver a final and third 25bps rate cut for 2025, making it 6 cuts and 175bps in this easing cycle since September 2024. The decision is unlikely to be unanimous, with dissent anticipated from both hawkish and dovish members. Should four or more officials break ranks, it would mark the largest split since 1992. Beyond the headline move, the tone of Chair Powell’s press conference and the accompanying statement will be critical. We expect Powell to emphasise that the hurdle for further cuts in early 2026 is high, signalling a near-term pause. This guidance will be key to maintaining credibility ahead of likely softer labour market data due later in December.

Beyond the Fed, the global calendar features several other central bank decisions and important data releases. Maybe tech earnings from Oracle (Wednesday) and Broadcom (Thursday) will be the most interesting, with the two names diverging considerably over the last couple of months. The former is down -34% over this period with the latter only -3% off its all-time-high seen a couple of weeks ago. In terms of central banks, the Reserve Bank of Australia meets tomorrow, where policymakers are expected to hold rates steady, but with a hawkish tilt likely after recent inflation increases. The January 7th inflation data could encourage markets to price in a hike as soon as February. The Bank of Canada follows on Wednesday, with the Swiss National Bank on Thursday with both expected to stay on hold. Canada saw a +16bps rise in 2yr yields on Friday after another strong labour market release with traders now suddenly, and fully, pricing in a hike by October next year. Meanwhile, the SNB are trying to avoid negative rates next year with rates now around zero.

Elsewhere, UK monthly GDP for October will be released on Friday, alongside German industrial production today and trade figures on Tuesday. China inflation is released on Wednesday where our economists expect CPI inflation to rise by 0.5ppt to 0.7% YoY and PPI to improve by 0.2ppt to -1.9% YoY. Nordic inflation prints are also due midweek, with Denmark and Norway publishing November CPI reports. Also watch out for the BoJ Ueda who speaks in London tomorrow ahead of a fascinating BoJ meeting next Friday just as the market winds down for Xmas.

Expanding further on the FOMC now, according to our economist’s preview here, the updated Summary of Economic Projections (SEP) should show only modest revisions. Growth forecasts for 2025 and 2026 are likely to be nudged higher, consistent with the October staff update, while inflation projections should be trimmed for this year and next. The unemployment path is expected to remain broadly unchanged. The dot plot should continue to point to one cut per year over the next two years, reinforcing the message that policy is approaching the neutral range (3.5–3.75%). Our economist’s baseline remains that the Fed stays on hold through the first half of 2026, with risks skewed towards another cut in Q1 if labour market weakness persists. Under new leadership later in the year, they anticipate a September cut as disinflation resumes, taking the trough in the fed funds rate to around 3.3%.

While the Fed dominates, a handful of other releases could provide additional nuance. Tomorrow brings combined September–October JOLTS data, offering a backward-looking snapshot of hiring and quits trends. Recent figures have underscored a “low hiring/low firing” dynamic, with private hiring at multi-year lows and quits subdued. Wednesday’s Employment Cost Index for Q3 is forecast at DB to hold steady at +0.9%, keeping annual growth around 3.6%. Thursday rounds out the docket with September trade numbers (-$69.6bn expected vs. -$59.6bn prior) and initial jobless claims (225k vs. 191k), the latter likely to increase after holiday distortions.

Asian equities are relatively quiet ahead of an important week. As I check my screens, the Nikkei is flat, impacted by Japan’s revised Q3 GDP data (details below). In other markets, Chinese stocks are diverging with the Hang Seng (-1.05%) lower, while the CSI (+1.05%) and the Shanghai Composite (+0.67%) are higher, buoyed by better-than-expected China exports and a larger trade surplus compared to the previous month. Additionally, the KOSPI (+0.77%) is also rising. S&P 500 (+0.18%) and NASDAQ 100 (+0.25%) futures are both trading higher.

Returning to China, outbound shipments increased by +5.9% year-on-year in November, surpassing market expectations for +4.0% growth, marking a recovery from an unexpected -1.1% decline in October — the first contraction since March 2024. Imports rose by +1.9% last month, falling short of the anticipated +3.0% increase, as a prolonged housing downturn and rising job insecurity continued to hinder domestic consumption. This growth was an improvement compared to the 1% recorded in October. Elsewhere, in Japan, the revised annualised Q3 growth contraction was reported at -2.3%, compared to an earlier estimate of -1.8% and a market forecast of a -2.0% decline.

On a quarter-on-quarter basis, GDP decreased by -0.6%, which is steeper than the initial -0.4% contraction and exceeded the forecast of a -0.5% decline. Separately, real wages fell by -0.7% in October compared to the previous year, a slower decline than the revised -1.3% drop in September, but it extended a losing streak that began in January. Meanwhile, average nominal wages, or total cash earnings, rose by +2.6% year-on-year in October, marking a three-month high that followed a +2.1% increase in the previous month.

In bond markets, yields on the 10-year Australian government bonds are +2.2bps, reaching 4.71%, marking the highest level in two years in anticipation of the RBA meeting tomorrow. New Zealand’s 10-year government bond are +8.8bps. 10 and 30yr JGBs are +2bps and +3bps higher respectively.

Recapping last week now and markets continued to grind higher, with the S&P 500 (+0.31%; +0.19% Friday), NASDAQ (+0.91%; +0.31% Friday), and the STOXX 600 (+0.41%; -0.01% Friday) all edging higher. The Mag-7 (+1.40%; +0.35% Friday) was boosted by strong performances from Tesla (+5.77%; +0.10% Friday) and Meta (+3.93%; +1.80% Friday), the latter on a Bloomberg report of budget cuts up to 30% for its metaverse division. In contrast, Microsoft fell -1.80% (+0.48% Friday) amid a press report of lowered AI sales quotas, which the company subsequently denied. The overall risk-tone saw the VIX volatility index (-0.55pts) fall to a two-month low of 15.41, and credit spreads tighten, with both US IG (-3bps) and HY (-5bps) rallying.

On the data front, we saw mixed US labour market releases, as the ADP report showed US private payrolls falling by 32k in November (vs. +10k expected) driven by highest job losses for small businesses since the pandemic (-120k) but weekly initial jobless claims (191k vs. 220k expected) painted a more robust picture, although Thanksgiving distortion likely dominated. In terms of survey releases, ISM services was slightly stronger than anticipated at 52.6 (vs. 52.0 expected), while its prices paid component fell to a seven-month low of 65.4 (vs. 68.0 expected). And on Friday, the University of Michigan consumer sentiment (53.3 VS 51.0 expected) rebounded from its November slump as 5-10 year inflation expectations (3.2% vs 3.4% expected) fell to their lowest since January.

While a December Fed rate cut is more than 95% priced, the conflicting data drove a hawkish adjustment further out with the amount of cuts priced by end-26 declining by -9.3bps (-3.4bps Friday). This led to a rise in Treasury yields, with the 2yr yield up +7.0bps to 3.56%, while the 10yr saw its biggest weekly sell-off since April (+12.1bps to 4.14%, +3.7bps Friday). Higher yields were also driven by developments in Japan, as comments from BoJ Governor Ueda led investors to anticipate a December rate hike. 10-year JGB yields rose by +13.5bps to a post-2008 high of 1.94% and 30-year yields by +1.5bps to 3.35%, its highest since the tenor was introduced in the late-1990s.

In Europe, 10yr bunds (+10.9bps), OATs (+11.4bps), and BTPs (+8.5bps) joined the global bond sell-off. That came as the Euro Area flash CPI for November was higher than expected at +2.2% (vs. +2.1% expected), while the composite PMI was revised up to 52.8, its highest in two-and-a-half years. The data supported modest equity gains, with the DAX +0.80% higher though the CAC 40 (-0.10%) was marginally lower. European credit spreads were also tighter for both IG (-6bps) and HY (-8bps).

In commodities, Brent crude saw a modest rally of +2.20% to $63.75/bbl, as no concrete plans for a ceasefire in Ukraine emerged. Cryptocurrencies experienced a volatile week. Bitcoin ended the week down -1.88%, but that included a -5.19% move on Monday and +5.97% on Tuesday. Gold was down -0.98% to $4,198/oz following an almost 5% rally the previous week.

Tyler Durden

Mon, 12/08/2025 – 08:42

https://www.zerohedge.com/markets/futures-rise-10th-day-past-11-fed-rate-cut-looming

F1 en 2026: Fechas clave, nuevos aspirantes al título y debut de Cadillac

Por JAMES ELLINGWORTH

Momento de decirle adiós al DRS y abrirle las puertas al impulso extra de batería para facilitar los adelantamientos.

El Gran Premio de Abu Dhabi del domingo marcó la última vez que la Fórmula 1 utilizó el DRS (el sistema de ayuda de adelantamiento de reducción de arrastre, introducido en 2011. El próximo año, los pilotos tendrán que gestionar los sistemas del monoplaza más de cerca que nunca, con un papel más visible para la tecnología aerodinámica y eléctrica.

Después de una reñida temporada por el título que terminó con el primer campeonato de Lando Norris, esto es lo que se espera en 2026:

Más pequeños, ligeros y eléctricos

Los mayores cambios en el reglamento en años hacen que los coches sean más cortos, estrechos y ligeros, con “aerodinámica activa” móvil —modo X para velocidad en línea recta, modo Z para curvas— y una mayor dependencia de la energía híbrida eléctrica.

El objetivo de la FIA era que la energía eléctrica representara la mitad de la producción total junto con un motor tradicional V6 turbo. En lugar del DRS, los pilotos pueden desplegar energía eléctrica adicional en momentos clave. Eso hace que la conducción sea aún más estratégica, pero podría llevar a que los pilotos levanten el pie del acelerador y se deslicen en algunas rectas para permitir que los sistemas eléctricos recojan energía.

La FIA afirma que las reglas enfatizan la habilidad del piloto, pero ha habido opiniones mixtas de quienes han probado los diseños de 2026 en los simuladores de sus equipos.

Los monoplazas más pequeños y ágiles podrían ayudar en los adelantamientos, pero los más rápidos y más lentos podrían estar hasta cuatro segundos por vuelta de diferencia en ritmo, según ha indicado el proveedor de neumáticos Pirelli. En términos de F1, eso es una eternidad. Se espera ver más fallos de motor mientras los equipos equilibran la fiabilidad con el rendimiento.

Mercedes y Aston Martin apuntan a más

¿Podría ser este el año en que Lewis Hamilton recupere su forma en Ferrari y persiga un octavo título? Tal vez no.

Aunque nunca se llevó bien con los modelos de 2022-25, Hamilton dijo a la BBC que “no esperaba con ansias” 2026 después del Gran Premio de Las Vegas el mes pasado, otra decepción desde que se unió a Ferrari.

Mercedes ha diseñado algunos de los motores más dominantes de la F1 antes, pero su llamativo concepto aerodinámico “zero-pod” fue un fracaso cuando comenzó el último período de regulación en 2022. Si aciertan en ambos aspectos esta vez, George Russell podría ser un contendiente al título después de dos victorias en 2025. Mercedes también suministra los motores a McLaren y Alpine.

Otro equipo a observar es Aston Martin, que tendrá su primer monoplaza creado con el laureado diseñador Adrian Newey a cargo, ahora con Honda como proveedor exclusivo de motores, y confía que el español Fernando Alonso, dos veces campeón mundial, gane su primera carrera de la F1 después de 13 años.

Williams también podría dar un paso adelante después de abandonar prematuramente sus proyectos de 2025 para centrarse en 2026.

Nuevo equipo Cadillac, caras conocidas

La parrilla de F1 se expande a 22 autos por primera vez desde 2016, ya que Cadillac se convierte en el undécimo equipo con el respaldo de General Motors.

El equipo más nuevo tendrá a dos de los pilotos más experimentados, ya que el mexicano Sergio Pérez y el finlandés Valtteri Bottas regresan, con un total combinado de 16 victorias y 527 largadas entre ambos.

El equipo estadounidense ha estado tomando lecciones de los programas espaciales de la NASA y tiene un jefe británico que se compara a sí mismo con un “Ted Lasso inverso” por el choque cultural de trabajar en las carreras de autos de Estados Unidos.

Arvid Lindblad, un británico de 18 años, será el único novato en 2026 en Racing Bulls. Ocho de los diez equipos existentes han jugado a lo seguro con la misma alineación de pilotos, por lo que el único otro cambio ha sido el ascenso de Isack Hadjar a Red Bull para unirse a Max Verstappen. Yuki Tsunoda pasa a un papel de reserva.

Nuevo circuito en Madrid

El Madring es el único nuevo circuito en el calendario de 2026. El circuito urbano de Madrid toma el título del Gran Premio de España de Barcelona, que permanece en el calendario ya que España tendrá una segunda carrera por primera vez desde 2012.

Eso significa que no hay espacio para el segundo F1 de Italia, el Gran Premio de Emilia-Romaña en el circuito de Imola, que ha celebrado cinco carreras desde 2020.

El momento de la verdad

Después del espectáculo de lanzamiento de temporada con alfombra roja de 2025 en Londres, el inicio de la temporada 2026 será discreto.

Los nuevos autos saldrán a la pista por primera vez en un test privado en España a partir del 26 de enero.

Habrá dos sesiones de pruebas abiertas más en Bahréin en febrero antes del Gran Premio de Australia que inaugura la temporada en Melbourne el 8 de marzo.

___

Deportes AP: https://apnews.com/hub/deportes

AP Explica: Qué hay detrás de los nuevos enfrentamientos entre Tailandia y Camboya

Por GRANT PECK

BANGKOK (AP) — Una historia de enemistad entre Tailandia y Camboya por reclamos territoriales ha vuelto a convertirse en combate abierto, solo unos meses después de que ambas partes acordaran un alto el fuego promovido por el presidente estadounidense Donald Trump.

Las dos naciones del sudeste asiático lucharon en julio durante cinco días en y alrededor de un territorio fronterizo disputado, causando decenas de muertes civiles y militares y la evacuación de decenas de miles de aldeanos en ambos lados.

El lunes, estallaron los combates más intensos desde el alto al fuego. Aunque no está claro quién disparó primero, Tailandia lanzó ataques aéreos a lo largo de la frontera mientras también estallaban combates terrestres.

La disputa se remonta a principios del siglo XX

Tailandia y Camboya tienen una historia de enemistad de siglos y experimentan tensiones periódicas a lo largo de su frontera terrestre de más de 800 kilómetros (500 millas).

Los reclamos territoriales se derivan en gran medida de un mapa de 1907 creado mientras Camboya estaba bajo el dominio colonial francés, que Tailandia sostiene es inexacto. Muchos tailandeses todavía están molestos por un fallo de 1962 de la Corte Internacional de Justicia, que otorgó la soberanía de la tierra disputada a Camboya, una decisión reafirmada en 2013. El desacuerdo alimentó varios enfrentamientos armados entre 2008 y 2011.

El alto al fuego respaldado por Trump era frágil

Se alcanzó una paz incómoda a finales de julio, cuando Malasia impulsó conversaciones de paz y el presidente Trump llevó a las partes en conflicto a la mesa de negociaciones advirtiéndoles de la importancia del mercado de Estados Unidos para las exportaciones de ambas naciones, amenazando con retener privilegios comerciales cruciales.

Trump posteriormente afirmó que esta intervención era un ejemplo entre varios de todo el mundo donde sus acciones llevaron a la paz entre naciones en guerra.

El pacto preliminar fue seguido por un acuerdo más detallado en octubre. Sus términos exigían la coordinación de operaciones de desminado, la retirada de armas y equipos pesados de la frontera, la implementación de medidas para restaurar la confianza mutua y abstenerse de retórica dañina y la difusión de información falsa. Ninguna de estas acciones se implementó por completo.

Ambas naciones continuaron librando una amarga guerra de propaganda y ha habido ocasionales brotes menores de violencia transfronteriza.

Una queja importante de Camboya ha sido que Tailandia continúa reteniendo a 18 soldados capturados. Tailandia acusa a Camboya de colocar nuevas minas terrestres en las áreas en disputa que mutilaron a soldados tailandeses. Camboya dice que las minas quedaron de la guerra civil que terminó en 1999.

El fracaso en implementar los términos del alto el fuego fue utilizado por el lado tailandés como excusa para no liberar rápidamente a los prisioneros camboyanos, a pesar de que el acuerdo de octubre instaba a hacerlo “como una demostración del deseo de Tailandia de promover la confianza y la seguridad mutuas.”

El conflicto impacta la diplomacia, el comercio y el turismo

Tailandia es uno de los aliados más cercanos y antiguos de Washington. El país también tiene una gran ventaja militar, mejor demostrada por su capacidad mayormente incontestada de usar el poder aéreo.

Pero Camboya también ha estado tratando de fortalecer su posición diplomáticamente. Fue uno de los primeros países en apoyar firmemente una nominación al Premio Nobel de la Paz para Trump, incluso organizando manifestaciones a favor de eso.

Camboya también ha empleado una intensa campaña de propaganda en las redes sociales, retratándose como la parte débil y emitiendo frecuentes acusaciones no verificables sobre las acciones tailandesas. El nacionalismo beligerante ha sido ubicuo en ambos lados.

Washington, por su parte, parece estar tratando activamente de construir mejores relaciones con Camboya para alejarla de su estrecha relación con China, pero eso a su vez ha generado resentimiento en Tailandia.

Camboya ha avanzado más hacia la finalización de un acuerdo comercial con Washington que Tailandia, cuya economía es mucho más grande y compleja.

Las posibles consecuencias económicas van más allá del comercio. Los combates renovados llegan justo cuando la temporada turística de invierno está en su apogeo y corren el riesgo de disuadir a los turistas. El turismo es una fuente importante de ingresos para ambas naciones, que todavía están tratando de recuperarse del golpe que la industria sufrió durante la pandemia de coronavirus.

La competencia cultural también es un factor

La mala relación entre los dos vecinos no se trata solo de reclamos fronterizos superpuestos, sino también de una enemistad cultural profundamente arraigada que tiene sus raíces desde hace siglos, cuando eran grandes imperios en competencia.

En tiempos más modernos, la animosidad ha persistido, ya que el desarrollo de Camboya, obstaculizado por el colonialismo francés y, en la década de 1970, el brutal régimen del Jmer Rojo, ha quedado muy atrás de Tailandia.

Ambos han luchado por reclamos sobre productos culturales que van desde el boxeo, la danza de máscaras, la vestimenta tradicional y la comida.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

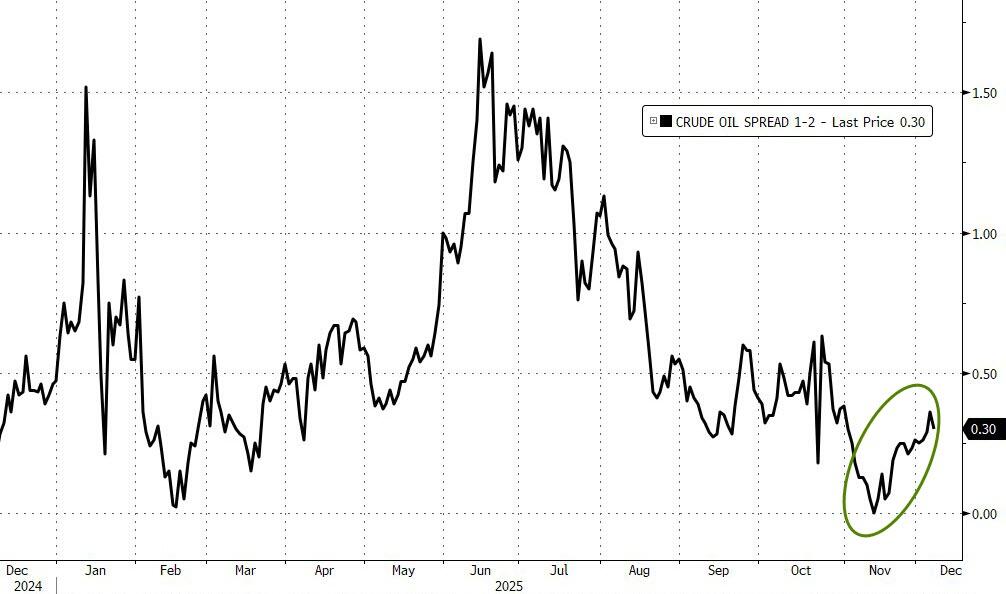

Oil Reclaims Key Levels, Forcing Shorts To Blink

Oil Reclaims Key Levels, Forcing Shorts To Blink

WTI moved back above its 50-day moving average Friday and is fighting to hold above $60 this morning.

A market that spent weeks obsessing over punishing oversupply is now being forced to respect a technical line that encourages short covering rather than fresh selling.

As Bloomberg macro strategist, Michael Ball writes, a return to a war premium is warranted as a genuine peace deal between the Ukraine and Russia remains elusive. Ukrainian negotiators are headed into another round of talks in Florida, while Russia is already objecting to parts of the US-backed plan and waiting on a fresh readout from the discussions.

Traders are watching the process for any sign of a settlement that could eventually ease sanctions and boost Russian supply as covered by colleagues Grant Smith, Alex Longley and Will Kubzansky. However, with Ukraine still striking targets like the Syzran refinery and Temryuk port and Washington lobbying Europe to tighten the screws on Moscow’s frozen assets, a deal looks far away.

At the same time, the technical picture has turned more supportive.

WTI has pushed back through its 50-day moving average, a key line that many treat as short-term support.

Meantime, low implied volatility and firmer prompt spreads signal a better balanced or slightly tighter near-term market, rather than one braced for a sudden collapse.

The longer-term anchor on oil remains that surplus story. Saudi Aramco has cut its flagship Arab Light official selling price to Asia to the lowest level since the early-2020s, admitting that refiners have plenty of choice and need an incentive to take Saudi barrels over others.

Sell-side research still leans negative on oil, with banks like Macquarie flagging oil multi-million-barrel-a-day surplus and sketching Brent-in-the-$50s scenarios as storage builds and refining margins compress.

That kind of fundamentally bearish backdrop implies positioning is still skewed short among macro funds and CTAs.

That’s why the pain trade now points higher – if WTI can hold above its 50-day moving average and the $60 level in a low-vol, firmer-spread backdrop, the current bounce may force further short covering barring fresh catalysts.

Tyler Durden

Mon, 12/08/2025 – 08:05

https://www.zerohedge.com/markets/oil-reclaims-key-levels-forcing-shorts-blink

‘One Battle After Another’ leads Golden Globe nominations

Paul Thomas Anderson’s “One Battle After Another” scored a leading nine nominations to the 83rd Golden Globe Awards on Monday, adding to the Oscar favorite’s momentum and handing Warner Bros. a victory amid its deal to be acquired by Netflix.

“One Battle After Another” landed nominations for its cast — Leonardo DiCaprio, Teyana Taylor, Sean Penn and Chase Infiniti — along with nods for Anderson’s screenplay and direction. It’s competing in the Globes’ category for comedy and musicals.

Close on its heels was Joachim Trier’s “Sentimental Value,” a Norwegian family drama about a filmmaking family. The Neon release’s eight nominations included nods for four of its actors: Stellan Skarsgård, Renate Reinsve, Elle Fanning and Inga Ibsdotter Lilleaas.

The Globe nominations, a tattered but persistent rite in Hollywood, are coming on the heels of the a potentially seismic shift in entertainment. On Friday, Netflix struck a deal to buy Warner Bros. Discovery for $72 billion. If approved, the deal would reshape Hollywood and put one of its most storied movie studios in the hands of the streaming giant.

Both companies are prominent in this year’s awards season. Along with “One Battle After Another,” Warner Bros. has “Sinners,” Ryan Coogler’s acclaimed vampire hit. It was nominated for seven awards by the Globes, including box office achievement.

Netflix’s contenders include Noah Baumbach’s “Jay Kelly,” Guillermo del Toro’s “Frankenstein” and the streaming smash hit, “KPop Demon Hunters.”

Nominations were read by Marlon Wayans and Skye P. Marshall, from Beverly Hills, California.

As the Globes continue to transition out of their scandal-plagued past, there’s one notable change this year. For the first time, the Globes are giving a best podcast trophy. The inaugural nominees are “Armchair Expert With Dax Shepard,” “Call Her Daddy,” “Good Hang With Amy Poehler,” “The Mel Robbins Podcast,” “SmartLess” and NPR’s “Up First.”

After a series of controversies for the Hollywood Foreign Press Association, the group that previously put on the ceremony, the Globes were sold in 2023 to Todd Boehly’s Eldridge Industries and Dick Clark Productions, a part of Penske Media. A new, larger voting body of more than 300 people now vote on the awards, which moved from NBC to CBS on a shorter, less expensive deal.

Nikki Glaser is returning as host to the Jan. 11 Globes, airing on CBS and streaming on Paramount+. This past January, Glaser won good reviews for her first time emceeing the ceremony. Ratings were essentially unchanged, slightly dipping to 9.3 million viewers, according to Nielsen, from 9.4 million in 2024.

In the early going in Hollywood’s awards season, Anderson’s “One Battle After Another” has dominated and is seen as the Oscar best picture front-runner. Also in the mix are Chloé Zhao’s “Hamnet,” Trier’s “Sentimental Value” and Josh Safdie’s “Marty Supreme.”

Helen Mirren will receive the Cecil B. DeMille Award in a separate prime-time special airing Jan. 8. Sarah Jessica Parker will be honored with the Carol Burnett Award.

https://www.chicagotribune.com/2025/12/08/golden-globe-nominations-2/

Miami knows CFP process isn’t perfect after Notre Dame decision: ‘Not everybody’s going to be happy’

CORAL GABLES, Fla. — Mario Cristobal spent four seasons working under Nick Saban at Alabama and learned countless lessons, some of which stand out more than others.

And when thinking about the College Football Playoff, one of Saban’s quotes from Cristobal’s time as an assistant with him stood out.

“’If you want to make everybody happy, don’t coach and get involved in football. Go sell ice cream because the ice cream man makes everybody happy,’” Cristobal said, recalling the Saban line. “In football, not everybody’s going to be happy.”

Notre Dame opts out of bowl games after being bounced from the College Football Playoff field

A year ago, at 10-2 and snubbed by the CFP committee, Miami wasn’t happy.

This year, at 10-2 and headed to Texas A&M for a playoff game, the Hurricanes are thrilled. It ultimately came down to an either-or pick for the last at-large spot, Miami or Notre Dame — and the committee had no choice but to finally recognize the Hurricanes’ 27-24 season-opening win over the Fighting Irish.

With that, Miami went to the playoff. Notre Dame’s season ended; it passed on bowl invites, telling fans it would turn its focus toward winning a national title in 2026. And yes, the Hurricanes and Irish are scheduled to play at Notre Dame next November.

“Notre Dame’s a great football team,” Cristobal said. “Processes like this … all processes need to be assessed again and remedied wherever they can, but I think everybody’s working at it. Last year we were excluded and we weren’t very happy. It’s a tough business, man. It’s a really, really tough business. I respect everybody and everyone involved in it.”

The CFP selection committee was asked to re-watch the Notre Dame-Miami game in recent days, and committee chair Hunter Yurachek said things stood out.

“There was observation from the coaches in the room where Notre Dame did a lot of chasing of some of the athletic receivers, especially on the Miami side, and it just felt like there was a little bit more athleticism on the side of Miami versus Notre Dame,” Yurachek said. “Then, the fact that Miami’s defense really stifled Notre Dame’s running game like nobody else did the entire season.”

Tweaks to the process are surely coming. Miami wound up losing a five-way tiebreaker for a berth in the Atlantic Coast Conference title game and the rules that the league operates under have been under some fire since. If that tiebreaker went Miami’s way, it’s entirely possible that the Hurricanes would have played their way in or out and Notre Dame would have had a playoff spot either way.

Also befuddling to many: How Notre Dame could be ahead of Miami in every CFP ranking, but fall behind the Hurricanes at the end — after a weekend where neither club played. In short, the CFP committee said its prisms became different when looking solely at those two clubs for one spot and not as part of a larger group. That makes some sense, yet it’s still easy to see why those on the wrong end of the decision could find it somewhere between confusing and flat-out wrong.

“It’s a hard job,” Cristobal said. “It’s a tough industry, right? I mean, where else are so many variables so influential in the outcome of a game that could send teams in a death spiral or propel others to new heights? And you have human error, and you have officiating, and you have injuries and all that stuff. There’s so much that goes into the game of football that when you also add a committee to make decisions, it’s hard on everybody.”

Had the CFP not come calling, Miami probably would have been settling for a berth in the Gator Bowl. For many players who’ll look at the 2026 NFL draft, the bowl probably would have been one to skip — and that would have conceivably meant the end of the college careers for players like Carson Beck, Rueben Bain Jr., Akheem Mesidor, CJ Daniels and more. That’s not a new concept for college football; bowl games are often very watered-down right now when teams miss the CFP.

“I know one thing: The passion behind college football is at an all-time high,” Cristobal said. “And the part I’m most happy about in terms of the process is that we didn’t compromise winning on the field. Because with all the chaos in college football right now, all the uncertainty, college football has been hurled into a different galaxy. Coaches are taking jobs, but they have to fly back to be able to coach their teams for the current job. With all this going on, I’m glad that we didn’t punish the student athletes who actually laid it on the line — on the field.”

https://www.chicagotribune.com/2025/12/08/miami-college-football-playoff-notre-dame/

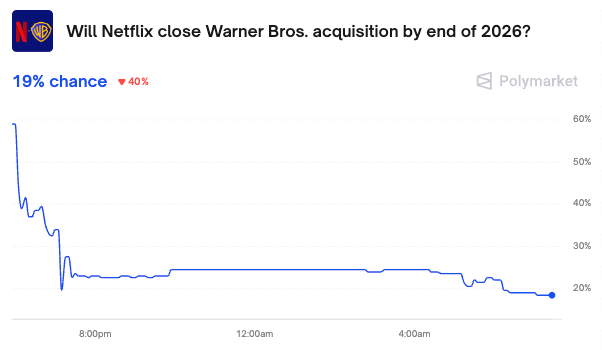

“Could Be A Problem”: Trump Weighs In On Netflix-Warner Mega Deal

“Could Be A Problem”: Trump Weighs In On Netflix-Warner Mega Deal

Beyond President Trump’s walk down the red carpet at the Kennedy Center Opera House in Washington, D.C., where he greeted actors, musicians, and entertainment industry legends on Sunday evening, he also spoke with reporters about one of the biggest developments in Hollywood: Netflix’s plan to acquire Warner Bros., including its film and television studios as well as HBO and HBO Max, in a $72 billion deal.

Trump told reporters on the red carpet that he had some skepticism about the prospects of the Netflix-WBD getting approval. He suggested that regulators could push back, noting Netflix already has a large market share that would “go up a lot” if it acquires WBD.

“Well, that’s got to go through a process, and we’ll see what happens,” the president said, adding, “They have a very big market share … when they have Warner Bros., that share goes up a lot.”

Trump said he plans to discuss the mechanics of the deal with “some economists” before giving it his approval.

“I’ll be involved in that decision, too,” he said. Normally, presidents don’t intervene directly in antitrust reviews of corporate mergers, which makes his comments stand out. It also reinforces the growing panic across Hollywood about what this deal could mean.

“But it is a big market share, there’s no question about that. It could be a problem,” he added.

President Trump says he would have a role in whether a proposed merger between Netflix and Warner Brothers should go forward, telling reporters the market share of a combined entity could raise concerns https://t.co/bIqw9EKC72 pic.twitter.com/F4bw7d6TUp

— Reuters (@Reuters) December 8, 2025

No other than the former WBD CEO summed things up succinctly:

If I was tasked with doing so, I could not think of a more effective way to reduce competition in Hollywood than selling WBD to Netflix.

And as we pointed out:

Why Netflix Buying Warner Bros Would Be A Disaster For America

Besides consolidation, Benny Johnson pointed out the marriage between the two companies may only suggest a more sinister plot: Netflix’s plan to “own a monopoly on children’s entertainment.”

Over the weekend, Barclays analysts led by Kannan Venkateshwar questioned Netflix’s deal, asking why it would spend nearly $80 billion for a studio company it already disrupted, especially with only $2 to $3 billion in expected synergies and a slow integration due to existing WBD distribution and content-licensing agreements (read the report).

Also, Trump added that Netflix’s CEO, Ted Sarandos, joined him at the White House last week. He said Sarandos was a “great person” who has done “one of the greatest jobs in the history of movies.”

The latest Polymarket odds of whether the Netflix-WBD closes by the end of 2026 stand at 19%.

Merger approvals are typically handled by independent regulatory agencies, such as the Federal Trade Commission and the Department of Justice, rather than by the president directly. That makes Trump’s stated involvement highly unusual. It’s also worth noting that Paramount–Skydance, backed by the Ellison family, recently made a bid for WBD.

Tyler Durden

Mon, 12/08/2025 – 07:45

https://www.zerohedge.com/markets/could-be-problem-trump-weighs-netflix-warner-mega-deal

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}