Category: News

Arizona takes No. 1 in Top 25 men’s basketball poll for the 1st time since 2023 as Purdue slides to No. 6

Arizona took over the top spot in the AP Top 25 men’s college basketball poll on Monday, a reward for a perfect start to the season that includes a quartet of wins against ranked foes, including a lopsided victory over Auburn last weekend.

Purdue, which had spent the past three weeks at No. 1, slid to sixth following its 81-58 home loss to Iowa State and the entire poll got a shakeup as only two teams remained in the same spots from last week.

The Wildcats received 33 of 60 first-place votes from a national media panel to claim No. 1 for the first time since Dec. 11, 2023, and only the third time since the 2013-14 season. They edged No. 2 Michigan, which earned 19 first-place votes, thanks in part to wins over Florida, UConn and UCLA, along with their 97-68 romp over the then-No. 20 Tigers on Saturday night.

“Obviously it’s nothing you shy away from,” Wildcats coach Tommy Lloyd said of being No. 1. “You know, you’re at Arizona. The big stage. It’s part of being at a program like this. But we have bigger things on our mind.”

The Wolverines also moved up one spot for their best ranking since March 2021. Duke claimed six first-place votes and moved up to No. 3. And the Cyclones parlayed their big win in West Lafayette, Indiana, into a six-spot climb to No. 4 and a first-place vote. Iowa State has never been ranked No. 1 in the AP poll era, which began with the 1948-49 season.

“They stole our spirit,” said Purdue coach Matt Painter, whose team tied a record for the largest margin of defeat at home as the nation’s No. 1 team. “Our reason for having a high frustration level was them. They’re damn good. They took us to the woodshed.”

UConn remained ahead of Purdue at No. 5 after beating Kansas inside Allen Fieldhouse last week.

Houston was seventh, Gonzaga climbed three spots to eighth, Michigan State was ninth and BYU rounded the top 10 following a week of high-profile matchups across college basketball.

Louisville dropped five spots to No. 11 after losing to Arkansas. Alabama remained at No. 12, followed by Illinois, North Carolina and Vanderbilt, the only unbeaten team left in the SEC and one of just eight left in Division I men’s basketball.

Texas Tech was next, followed by the Razorbacks, who jumped eight spots after also beating Fresno State last week. Florida fell to No. 18 following its 67-66 loss to the Blue Devils, while Kansas moved up to No. 19 and Tennessee finished out the top 20.

The last five in the poll were Auburn, St. John’s, Nebraska, Virginia and UCLA.

The No. 23 Huskers are 9-0 for only the third time in school history, and they have won 13 straight dating to last season, the third-longest run in school history. The ranking is their best since they were 21st the second week of the 2014-15 season.

Rising and falling

Arkansas was No. 14 in the preseason poll, nearly dropped out entirely, but made a big jump this week back to No. 17 following its two wins. Iowa State’s climb to No. 4 has been a steady one since it was ranked 16th in the preseason poll.

Tennessee tumbled seven spots to No. 20 this week following losses to Syracuse and Illinois. Purdue and Louisville each fell five spots.

In and out

Nebraska and Virginia both made their poll debuts, replacing Indiana and USC. The Cavaliers did not receive a single vote last week but earned enough to join the rankings at No. 24. UCLA also returned to the rankings while Kentucky dropped out.

Conference watch

The Big 12, Big Ten and SEC lead the way with six ranked teams apiece, but the Big 12 has the nation’s No. 1 team. It also has four in the top 10, while the Big Ten has three and the SEC none. The ACC has four ranked teams, the Big East two and the West Coast one.

https://www.chicagotribune.com/2025/12/08/arizona-mens-college-basketball-poll/

Arizona takes No. 1 in Top 25 men’s basketball poll for the 1st time since 2023 as Purdue slides to No. 6

Arizona took over the top spot in the AP Top 25 men’s college basketball poll on Monday, a reward for a perfect start to the season that includes a quartet of wins against ranked foes, including a lopsided victory over Auburn last weekend.

Purdue, which had spent the past three weeks at No. 1, slid to sixth following its 81-58 home loss to Iowa State and the entire poll got a shakeup as only two teams remained in the same spots from last week.

The Wildcats received 33 of 60 first-place votes from a national media panel to claim No. 1 for the first time since Dec. 11, 2023, and only the third time since the 2013-14 season. They edged No. 2 Michigan, which earned 19 first-place votes, thanks in part to wins over Florida, UConn and UCLA, along with their 97-68 romp over the then-No. 20 Tigers on Saturday night.

“Obviously it’s nothing you shy away from,” Wildcats coach Tommy Lloyd said of being No. 1. “You know, you’re at Arizona. The big stage. It’s part of being at a program like this. But we have bigger things on our mind.”

The Wolverines also moved up one spot for their best ranking since March 2021. Duke claimed six first-place votes and moved up to No. 3. And the Cyclones parlayed their big win in West Lafayette, Indiana, into a six-spot climb to No. 4 and a first-place vote. Iowa State has never been ranked No. 1 in the AP poll era, which began with the 1948-49 season.

“They stole our spirit,” said Purdue coach Matt Painter, whose team tied a record for the largest margin of defeat at home as the nation’s No. 1 team. “Our reason for having a high frustration level was them. They’re damn good. They took us to the woodshed.”

UConn remained ahead of Purdue at No. 5 after beating Kansas inside Allen Fieldhouse last week.

Houston was seventh, Gonzaga climbed three spots to eighth, Michigan State was ninth and BYU rounded the top 10 following a week of high-profile matchups across college basketball.

Louisville dropped five spots to No. 11 after losing to Arkansas. Alabama remained at No. 12, followed by Illinois, North Carolina and Vanderbilt, the only unbeaten team left in the SEC and one of just eight left in Division I men’s basketball.

Texas Tech was next, followed by the Razorbacks, who jumped eight spots after also beating Fresno State last week. Florida fell to No. 18 following its 67-66 loss to the Blue Devils, while Kansas moved up to No. 19 and Tennessee finished out the top 20.

The last five in the poll were Auburn, St. John’s, Nebraska, Virginia and UCLA.

The No. 23 Huskers are 9-0 for only the third time in school history, and they have won 13 straight dating to last season, the third-longest run in school history. The ranking is their best since they were 21st the second week of the 2014-15 season.

Rising and falling

Arkansas was No. 14 in the preseason poll, nearly dropped out entirely, but made a big jump this week back to No. 17 following its two wins. Iowa State’s climb to No. 4 has been a steady one since it was ranked 16th in the preseason poll.

Tennessee tumbled seven spots to No. 20 this week following losses to Syracuse and Illinois. Purdue and Louisville each fell five spots.

In and out

Nebraska and Virginia both made their poll debuts, replacing Indiana and USC. The Cavaliers did not receive a single vote last week but earned enough to join the rankings at No. 24. UCLA also returned to the rankings while Kentucky dropped out.

Conference watch

The Big 12, Big Ten and SEC lead the way with six ranked teams apiece, but the Big 12 has the nation’s No. 1 team. It also has four in the top 10, while the Big Ten has three and the SEC none. The ACC has four ranked teams, the Big East two and the West Coast one.

https://www.chicagotribune.com/2025/12/08/arizona-mens-college-basketball-poll/

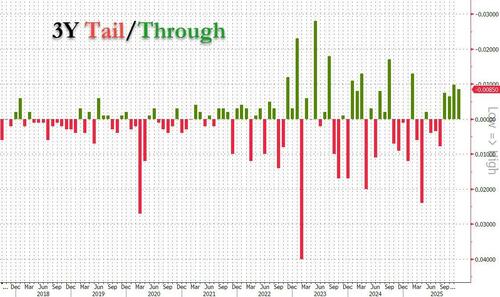

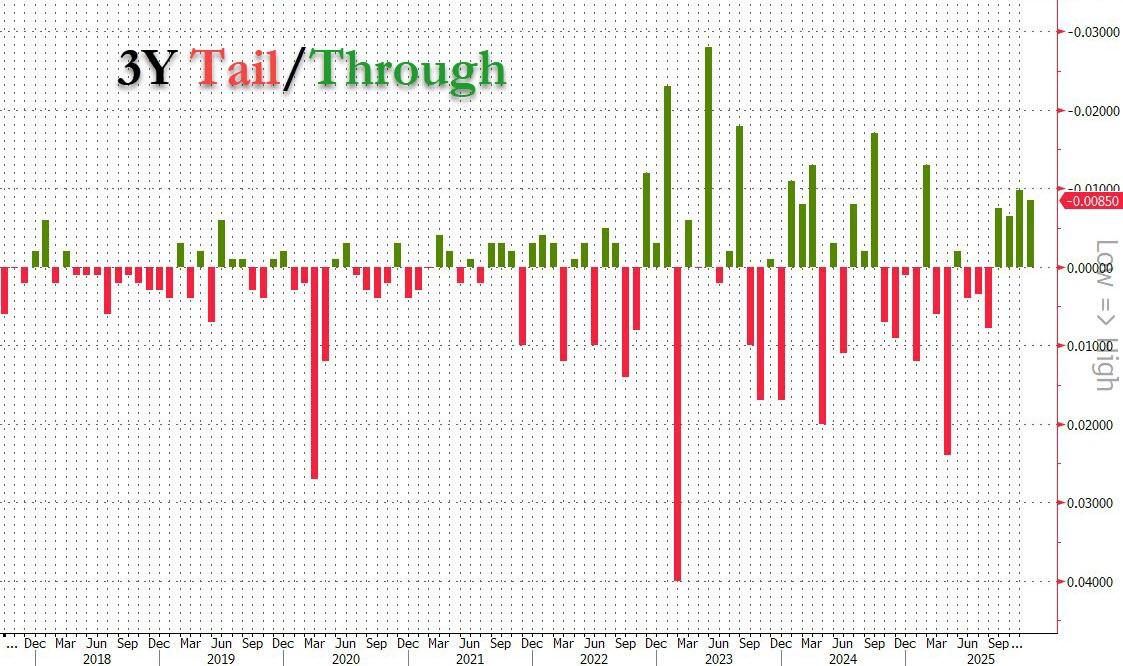

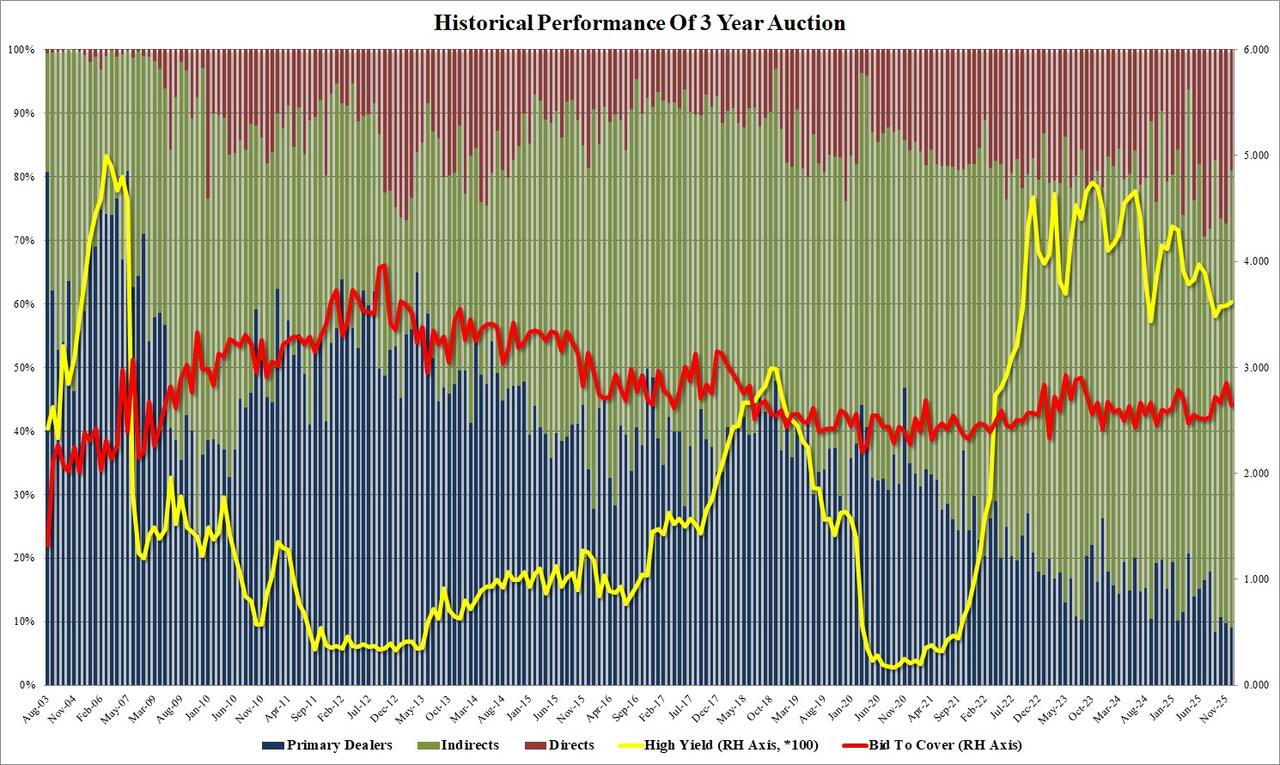

Solid, Stopping-Through 3Y Auction Boosted By Surge In Foreign Demand

Solid, Stopping-Through 3Y Auction Boosted By Surge In Foreign Demand

Due to the FOMC meeting falling on a Wednesday, the Treasury is scrambling to issue this week’s coupon auctions, starting with a $58BN 3Y auction which saw solid demand when it was offered at 1pm ET.

The sale of $58BN in 3 year paper priced at a high yield of 3.614%, up from 3.579% in November, and the highest since August. The auction also stopped through the 3.622% When Issued by 0.8bps, the 4th consecutive stopping through 3Y auction.

The bid to cover was dropped to 2.641 from 3.850 but was still just above the 2.632 six-auction average.

The internals were more solid, with Indirects awarded 72.0%, up sharply from 63.0% in November and the highest since September. It was also one of the highest foreign awards on record.

And with Directs taking down 19.0%, down from 27.32 last month, Dealers were left holding just 9.03%, the lowest since September, and below the 13.1% recent average.

Overall, this was a very solid auction, one which came at just the right time: with 10Y yields surging today just shy of 4.20% before retracing the move and dipping by about 1bp on the solid 3Y auction results.

Tyler Durden

Mon, 12/08/2025 – 13:25

https://www.zerohedge.com/markets/solid-stopping-through-3y-auction-boosted-surge-foreign-demand

Solid, Stopping-Through 3Y Auction Boosted By Surge In Foreign Demand

Solid, Stopping-Through 3Y Auction Boosted By Surge In Foreign Demand

Due to the FOMC meeting falling on a Wednesday, the Treasury is scrambling to issue this week’s coupon auctions, starting with a $58BN 3Y auction which saw solid demand when it was offered at 1pm ET.

The sale of $58BN in 3 year paper priced at a high yield of 3.614%, up from 3.579% in November, and the highest since August. The auction also stopped through the 3.622% When Issued by 0.8bps, the 4th consecutive stopping through 3Y auction.

The bid to cover was dropped to 2.641 from 3.850 but was still just above the 2.632 six-auction average.

The internals were more solid, with Indirects awarded 72.0%, up sharply from 63.0% in November and the highest since September. It was also one of the highest foreign awards on record.

And with Directs taking down 19.0%, down from 27.32 last month, Dealers were left holding just 9.03%, the lowest since September, and below the 13.1% recent average.

Overall, this was a very solid auction, one which came at just the right time: with 10Y yields surging today just shy of 4.20% before retracing the move and dipping by about 1bp on the solid 3Y auction results.

Tyler Durden

Mon, 12/08/2025 – 13:25

https://www.zerohedge.com/markets/solid-stopping-through-3y-auction-boosted-surge-foreign-demand

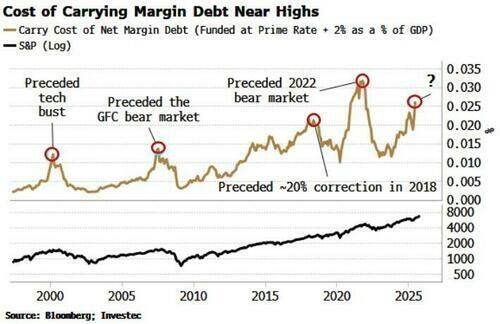

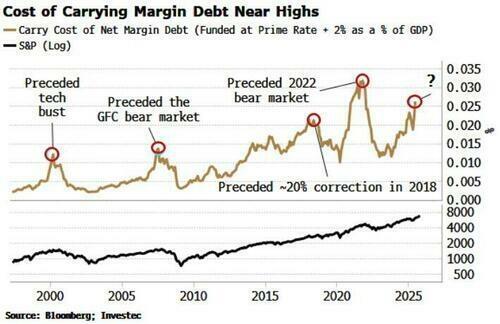

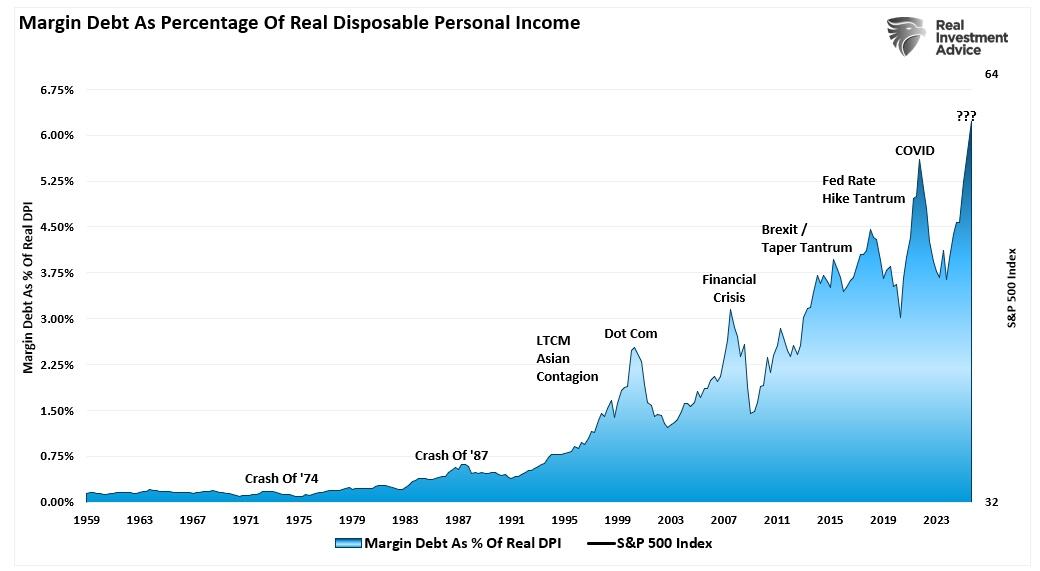

The DPI Link To Margin Debt

The DPI Link To Margin Debt

Authored by Lance Roberts via RealInvestmentAdvice.com,

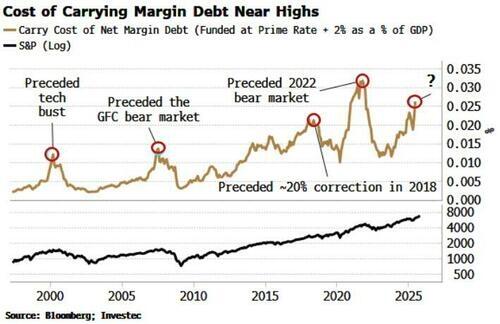

A recent article by Simon White, via Bloomberg, discussed the rising cost of margin debt for investors. While his analysis below compares the cost of debt to GDP, we will also consider a more critical comparison to disposable personal income (DPI). Here is Simon’s point.

“Yet, where history does raise a red flag is if we look at the cost of carrying the margin debt. Based on an idea from Investec Research, we can estimate the total cost of carrying margin debt versus GDP (I also adjust margin debt for credit balances). This net margin debt has only been higher in the pandemic, when savings went through the roof. As we can see, cost-of-carry peaks for net margin debt have preceded significant downward moves in stocks: the tech bust in 2000, the GFC bear market in 2008, the near 20% correction in 2018 and the 2022 bear market.“

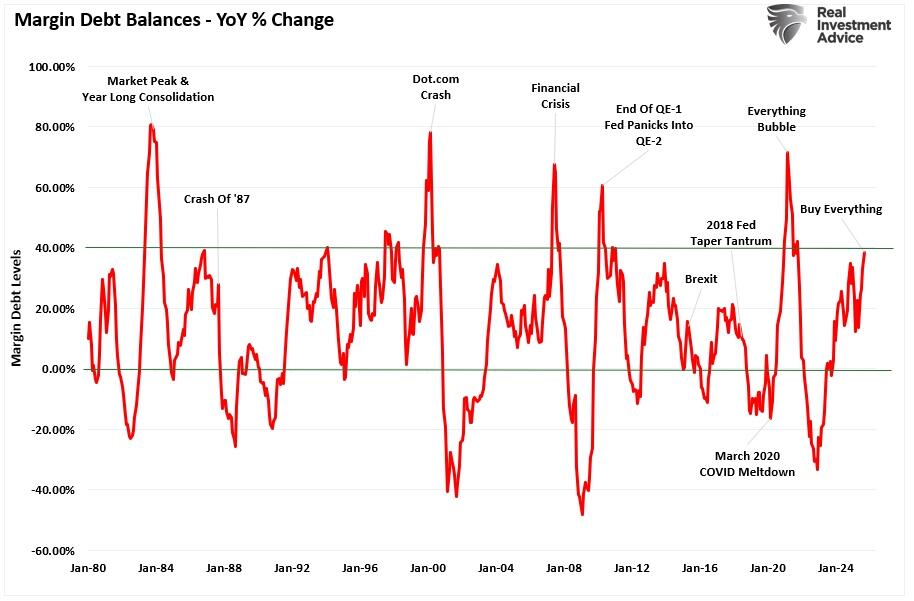

Before we proceed with our discussion, margin debt now stands at a record of more than $1.1 trillion, up nearly 40% on an annual basis.

Why is that important? It is essential to reiterate a crucial point about margin debt.

“Margin debt is not a technical indicator for trading markets. What it represents is the amount of speculation occurring in the market. In other words, margin debt is the “gasoline,” which drives markets higher as the leverage provides for the additional purchasing power of assets. However, leverage also works in reverse, as it supplies the accelerant for more significant declines as lenders “force” the sale of assets to cover credit lines without regard to the borrower’s position.

The last sentence is the most important. The issue with margin debt is that the unwinding of leverage is NOT at the investor’s discretion. That process is at the discretion of the broker-dealers that extended that leverage in the first place. (In other words, if you don’t sell to cover, the broker-dealer will do it for you.) When lenders fear they may not recoup their credit lines, they force the borrower to put in more cash or sell assets to cover the debt. The problem is that “margin calls” generally happen simultaneously, as falling asset prices impact all lenders simultaneously.“

In other words, the risk with margin debt is:

“Margin debt is a double-edged sword, and the edge that cuts you, cuts the deepest.”

So, why are we discussing this? Because margin debt levels are reaching a point where forward market returns are substantially lower.

Which brings us back to Simon White and the cost of carrying margin debt.

The Link Between Disposable Personal Income and Margin Debt

Currently, household allocations to equities are at a record. Of course, such should be unsurprising given the strong market advances over the past few years.

There is more to this story than just rising asset prices. When investors are chasing a bull market, they initially invest their savings in the financial markets. If prices continue to rise, they then turn to margin debt to continue investing. However, as noted above, that is a “bullish benefit” to the market as the leverage increases investors’ “buying power.”

However, margin debt is not “free,” and generally carries an interest rate that is two percentage points above the bank’s “prime lending” rate. Currently, the bank’s prime lending rate is around 7%, which suggests that most margin debt is carrying an interest rate of 9%. Therefore, investors must consider the interest rate risk associated with the borrowed capital to generate a profit. Over the last three years, returns of 10% or more have been relatively easy, at least so far.

But that brings us to our warning. Understanding the link between disposable personal income (DPI) and margin debt is crucial for assessing market risk. DPI is the income households have after taxes, available for saving or investing. When DPI growth slows, households have fewer fresh savings to deploy. In this context, some investors turn to margin borrowing to maintain or increase exposure.

In the second quarter of 2025, U.S. Disposable Personal Income (DPI) stood at approximately $22.858 trillion on a seasonally adjusted annual rate basis. This figure represents a nominal increase from $22.564 trillion in Q1 2025. While that growth suggests income levels are still rising, further data paint a more nuanced picture of investor capacity and market risk. Real disposable personal income (adjusted for inflation) for Q2 2025 grew by about 3.1% year‑over‑year. This growth rate remains below the long‑term average of roughly 3.44%. In practical terms, households are seeing slower growth in their “money left over” after taxes and basic costs, reducing the flow of new savings that could be invested.

Margin debt as a percentage of real DPI has been reported at around 6.23 %, the highest on record. This ratio also suggests that for every $100 of real DPI, roughly $6 of margin debt is outstanding, a non‐trivial amount.

Naturally, when fresh savings are lacking and investors turn to margin to participate in markets, two risks emerge.

The quality of the investor base weakens because borrowed money replaces savings.

The carrying cost of that borrowing becomes more salient when interest rates are elevated. If the margin debt carries higher interest and investors’ income growth is weak, servicing the debt becomes harder, reducing the buffer against loss.

In summary, weak DPI growth, combined with elevated margin borrowing, creates a vulnerability. In such an environment, the investor base is much less resilient.

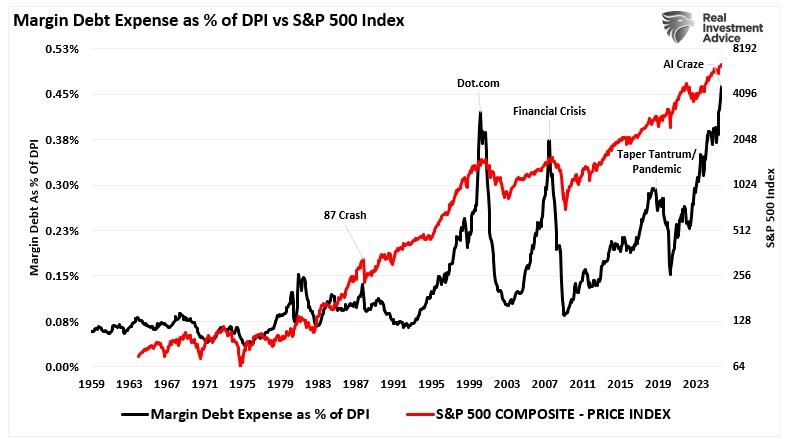

The “Cost Of Carry”

In recent years, not only has margin debt surged, but the “cost of carrying” that debt has also risen. As borrowing costs increase, the break‐even point for leveraged equity exposure rises. If an investor borrows at a higher interest rate and the market stagnates or declines, the drag from interest and margin loan costs erodes returns. Simon’s view of carrying costs as a percentage of GDP is correct. However, another salient perspective is to consider them as a function of DPI. In other words, if an investor account is fully invested, margin interest must be paid either by selling assets or from disposable income.

With margin debt expense as a percentage of DPI at the highest level on record, the risk of market reversal becomes elevated. Higher interest rates also mean that margin borrowing becomes less attractive relative to other uses of capital. If margin rates rise, investors holding prominent borrowed positions may face higher servicing costs and increased pressure in the event of a correction. In such an environment, as shown above, the historical outcome has been one of increased financial fragility.

Moreover, elevated rates can suppress earnings growth across the economy, reducing incentive returns and market momentum. For leveraged investors, slower earnings growth makes it harder to absorb the cost of borrowing. Therefore, from a market‑structure perspective, the combination of high margin debt and high borrowing costs creates a vulnerability:

Leverage is greater.

Investor income growth is weaker.

The carrying cost of debt is higher.

These three factors form a feedback loop: high costs and weak income reduce investor resilience; a market drawdown triggers margin calls, which in turn accelerate the decline through forced selling. Academic models of margin trading indicate that this type of feedback loop can transform a modest correction into a sharper decline.

Thus, rising carrying costs of margin debt amplify the risk embedded in the margin debt–DPI link.

Tyler Durden

Mon, 12/08/2025 – 13:25

The DPI Link To Margin Debt

The DPI Link To Margin Debt

Authored by Lance Roberts via RealInvestmentAdvice.com,

A recent article by Simon White, via Bloomberg, discussed the rising cost of margin debt for investors. While his analysis below compares the cost of debt to GDP, we will also consider a more critical comparison to disposable personal income (DPI). Here is Simon’s point.

“Yet, where history does raise a red flag is if we look at the cost of carrying the margin debt. Based on an idea from Investec Research, we can estimate the total cost of carrying margin debt versus GDP (I also adjust margin debt for credit balances). This net margin debt has only been higher in the pandemic, when savings went through the roof. As we can see, cost-of-carry peaks for net margin debt have preceded significant downward moves in stocks: the tech bust in 2000, the GFC bear market in 2008, the near 20% correction in 2018 and the 2022 bear market.“

Before we proceed with our discussion, margin debt now stands at a record of more than $1.1 trillion, up nearly 40% on an annual basis.

Why is that important? It is essential to reiterate a crucial point about margin debt.

“Margin debt is not a technical indicator for trading markets. What it represents is the amount of speculation occurring in the market. In other words, margin debt is the “gasoline,” which drives markets higher as the leverage provides for the additional purchasing power of assets. However, leverage also works in reverse, as it supplies the accelerant for more significant declines as lenders “force” the sale of assets to cover credit lines without regard to the borrower’s position.

The last sentence is the most important. The issue with margin debt is that the unwinding of leverage is NOT at the investor’s discretion. That process is at the discretion of the broker-dealers that extended that leverage in the first place. (In other words, if you don’t sell to cover, the broker-dealer will do it for you.) When lenders fear they may not recoup their credit lines, they force the borrower to put in more cash or sell assets to cover the debt. The problem is that “margin calls” generally happen simultaneously, as falling asset prices impact all lenders simultaneously.“

In other words, the risk with margin debt is:

“Margin debt is a double-edged sword, and the edge that cuts you, cuts the deepest.”

So, why are we discussing this? Because margin debt levels are reaching a point where forward market returns are substantially lower.

Which brings us back to Simon White and the cost of carrying margin debt.

The Link Between Disposable Personal Income and Margin Debt

Currently, household allocations to equities are at a record. Of course, such should be unsurprising given the strong market advances over the past few years.

There is more to this story than just rising asset prices. When investors are chasing a bull market, they initially invest their savings in the financial markets. If prices continue to rise, they then turn to margin debt to continue investing. However, as noted above, that is a “bullish benefit” to the market as the leverage increases investors’ “buying power.”

However, margin debt is not “free,” and generally carries an interest rate that is two percentage points above the bank’s “prime lending” rate. Currently, the bank’s prime lending rate is around 7%, which suggests that most margin debt is carrying an interest rate of 9%. Therefore, investors must consider the interest rate risk associated with the borrowed capital to generate a profit. Over the last three years, returns of 10% or more have been relatively easy, at least so far.

But that brings us to our warning. Understanding the link between disposable personal income (DPI) and margin debt is crucial for assessing market risk. DPI is the income households have after taxes, available for saving or investing. When DPI growth slows, households have fewer fresh savings to deploy. In this context, some investors turn to margin borrowing to maintain or increase exposure.

In the second quarter of 2025, U.S. Disposable Personal Income (DPI) stood at approximately $22.858 trillion on a seasonally adjusted annual rate basis. This figure represents a nominal increase from $22.564 trillion in Q1 2025. While that growth suggests income levels are still rising, further data paint a more nuanced picture of investor capacity and market risk. Real disposable personal income (adjusted for inflation) for Q2 2025 grew by about 3.1% year‑over‑year. This growth rate remains below the long‑term average of roughly 3.44%. In practical terms, households are seeing slower growth in their “money left over” after taxes and basic costs, reducing the flow of new savings that could be invested.

Margin debt as a percentage of real DPI has been reported at around 6.23 %, the highest on record. This ratio also suggests that for every $100 of real DPI, roughly $6 of margin debt is outstanding, a non‐trivial amount.

Naturally, when fresh savings are lacking and investors turn to margin to participate in markets, two risks emerge.

The quality of the investor base weakens because borrowed money replaces savings.

The carrying cost of that borrowing becomes more salient when interest rates are elevated. If the margin debt carries higher interest and investors’ income growth is weak, servicing the debt becomes harder, reducing the buffer against loss.

In summary, weak DPI growth, combined with elevated margin borrowing, creates a vulnerability. In such an environment, the investor base is much less resilient.

The “Cost Of Carry”

In recent years, not only has margin debt surged, but the “cost of carrying” that debt has also risen. As borrowing costs increase, the break‐even point for leveraged equity exposure rises. If an investor borrows at a higher interest rate and the market stagnates or declines, the drag from interest and margin loan costs erodes returns. Simon’s view of carrying costs as a percentage of GDP is correct. However, another salient perspective is to consider them as a function of DPI. In other words, if an investor account is fully invested, margin interest must be paid either by selling assets or from disposable income.

With margin debt expense as a percentage of DPI at the highest level on record, the risk of market reversal becomes elevated. Higher interest rates also mean that margin borrowing becomes less attractive relative to other uses of capital. If margin rates rise, investors holding prominent borrowed positions may face higher servicing costs and increased pressure in the event of a correction. In such an environment, as shown above, the historical outcome has been one of increased financial fragility.

Moreover, elevated rates can suppress earnings growth across the economy, reducing incentive returns and market momentum. For leveraged investors, slower earnings growth makes it harder to absorb the cost of borrowing. Therefore, from a market‑structure perspective, the combination of high margin debt and high borrowing costs creates a vulnerability:

Leverage is greater.

Investor income growth is weaker.

The carrying cost of debt is higher.

These three factors form a feedback loop: high costs and weak income reduce investor resilience; a market drawdown triggers margin calls, which in turn accelerate the decline through forced selling. Academic models of margin trading indicate that this type of feedback loop can transform a modest correction into a sharper decline.

Thus, rising carrying costs of margin debt amplify the risk embedded in the margin debt–DPI link.

Tyler Durden

Mon, 12/08/2025 – 13:25

Big Ten ties record with 9 teams in the Top 25 women’s basketball poll — including 3 in the Top 10

The Big Ten matched The Associated Press Top 25 women’s basketball record with nine ranked teams as Nebraska entered at No. 24 on Monday.

The conference set the mark last year on Dec. 2 and this week has three teams in the top 10 alone.

UConn still is No. 1, receiving 23 first-place votes from a national media panel. Texas garnered the other nine votes to remain second.

The top 10 was unchanged this week. South Carolina and UCLA stayed third and fourth with LSU and Michigan next. Maryland was seventh after rallying to beat Minnesota in double overtime Sunday.

TCU, Oklahoma and Iowa State rounded out the first 10. The Cyclones play in-state rival No. 11 Iowa on Wednesday.

Other Big Ten teams in the poll include No. 16 USC, No. 20 Washington, No. 21 Ohio State and No. 25 Michigan State. The Cornhuskers are ranked for the second consecutive season after starting 9-0.

“I’ve been honored to be a part of this league for the last 13 seasons, working on year 14, where I’ve watched the league just get better and better,” Michigan coach Kim Barnes Arico said. “And then when you have that type of improvement, and then add the four West Coast teams that are tremendous as well, I just think it added another top four teams to an already great league.”

Tennessee’s milestone ranking

The 18th-ranked Lady Vols appeared in the poll for the 800th time in the 50-year history of the rankings. Tennessee had a stretch of being in the Top 25 for 565 straight weeks, a record later surpassed by UConn.

Conference supremacy

The Big Ten took over the top spot with nine teams, while the Southeastern Conference was next with eight. The Big 12 has four and the Atlantic Coast Conference has three. The Big East has one.

Struggling ACC

The ACC had a rough week, going 3-13 against the SEC in the conference challenge. The ACC saw its run of having at least one top 10 team in every poll end earlier this season after 453 consecutive weeks.

Notre Dame fell one spot to No. 19 after blowing a 19-point lead in Thursday’s 69-62 loss to Mississippi — the largest in program history. The Irish rebounded with a 93-58 win in their ACC opener against Florida State on Sunday.

Games of the week

No. 1 UConn at No. 16 Southern California, Saturday

The Huskies head across the country for one of the few ranked games left on their schedule. The two teams have met a few times over the last couple of seasons, including in the NCAA Tournament regional final in 2024 and 2025. UConn won both of those matchups while the Trojans were victorious in Connecticut during a regular-season game.

No. 2 Texas vs No. 13 Baylor, Sunday

The two former Big 12 rivals will tip off in the Sprouts Farmers Market espnW Invitational in Fort Worth, Texas. The game will be played at the site of one of the two regionals for the NCAA Tournament.

https://www.chicagotribune.com/2025/12/08/big-ten-womens-basketball-poll/

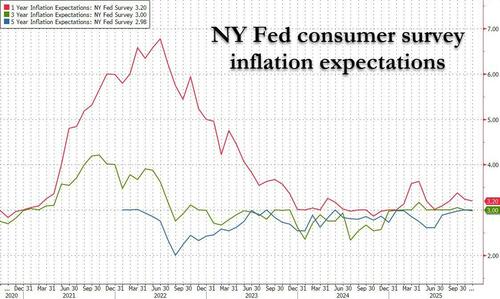

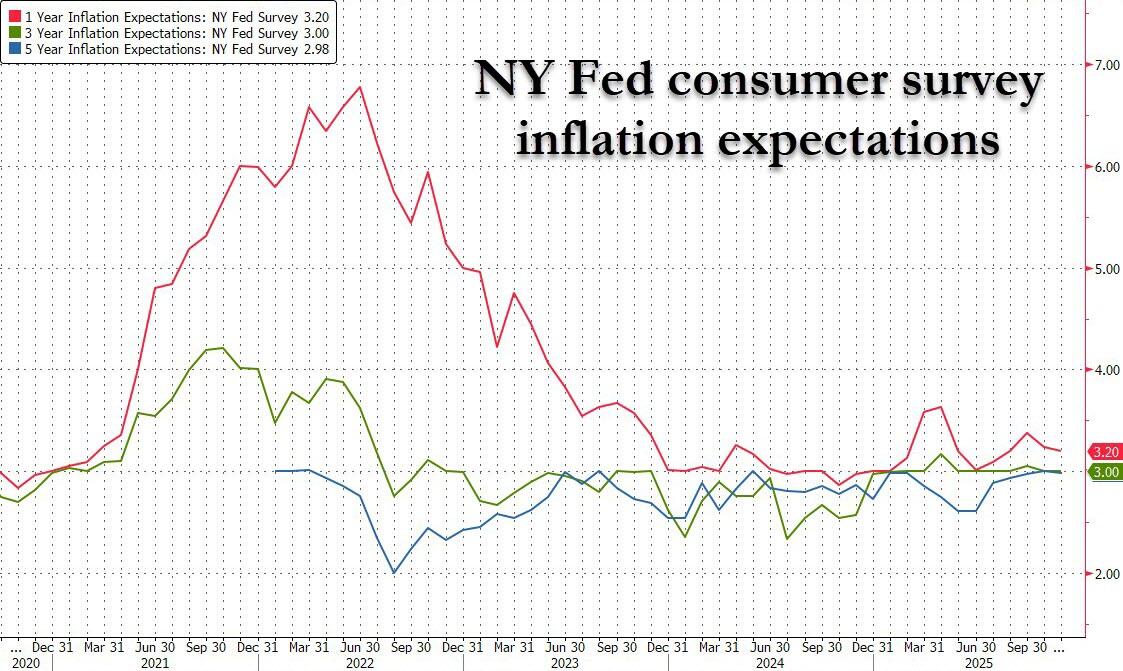

NY Fed Consumer Survey Shows Steady Inflation, Despite Soaring Expectations For Medical Care Costs

NY Fed Consumer Survey Shows Steady Inflation, Despite Soaring Expectations For Medical Care Costs

US consumer inflation expectations were stable in November while perceptions about households current financial situations deteriorated “notably” and perceptions about job prospects improved, according to the latest Survey of Consumer Expectations from the Federal Reserve Bank of New York.

Median inflation expectations a year ahead was little changed at 3.2% last month, down from 3.24% in November, while expected inflation three and five years ahead remained at 3%, according to responses in the New York Fed’s monthly Survey of Consumer Expectations, published Monday.

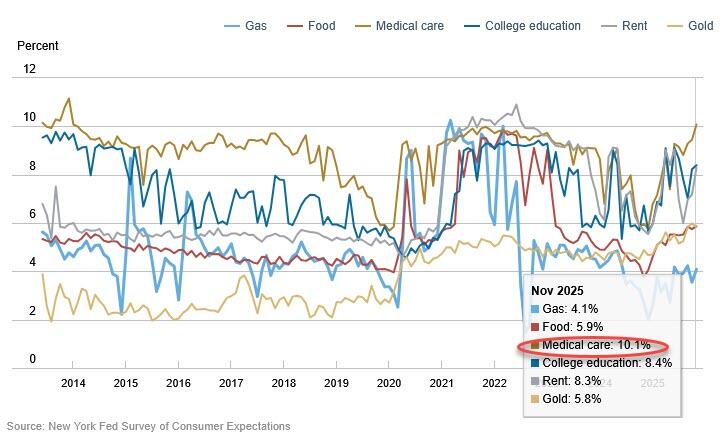

Median year-ahead commodity price change expectations increased by 0.2 percentage point for food (to 5.9%), 0.6 percentage point for gas (to 4.1%), 0.7 percentage point for the cost of medical care (to 10.1%), 0.2 percentage point for the cost of a college education (to 8.4%) and by 1.1 percentage points for rent (to 8.3%). Of note, the reading for the expected change in the cost of medical care is the highest since January 2014, shortly after the series began.

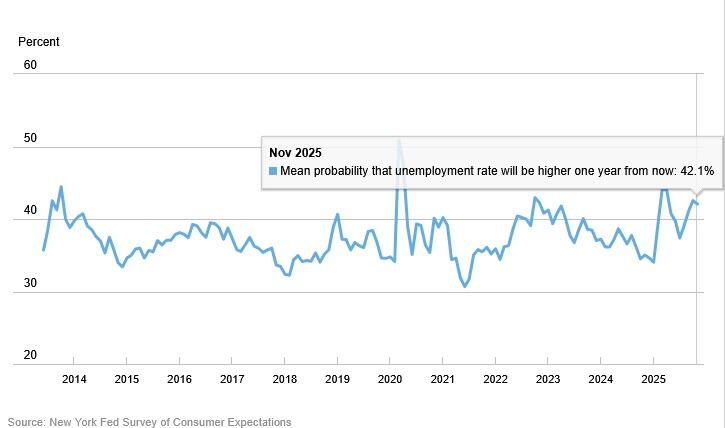

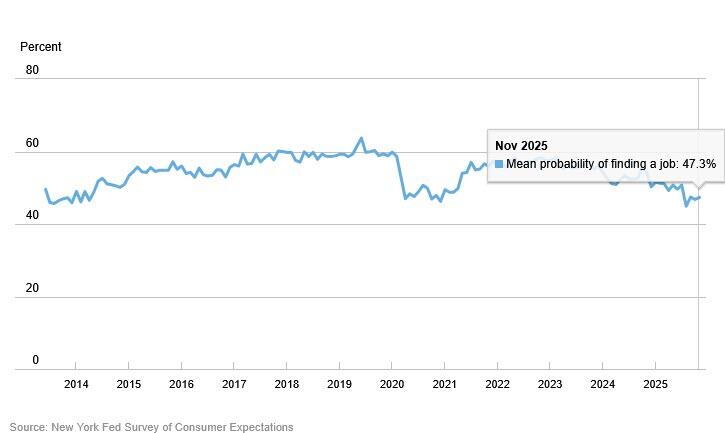

The survey showed consumers largely were more optimistic about the labor market in November than a month earlier, marking down the chances of a higher unemployment rate a year from now and reporting better odds of finding a job if they were to lose theirs.

The perceived probability of losing one’s job fell 0.2% to 13.8%, marking the lowest reading this year. At the same time, the mean probability of leaving one’s job voluntarily also slumped to 17.7%, the lowest since February.

Consumers are reduced the chances of a higher unemployment rate a year from now…

… and reporting better odds of finding a job if they were to lose theirs.

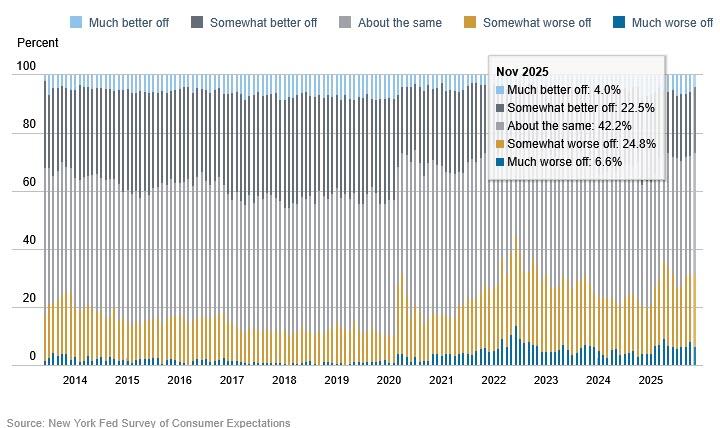

But with job prospects still worse than last year and inflation still elevated, a greater share of households reporting that their households were worse off compared to a year ago and a smaller share reporting they were better off. Expectations about year-ahead financial situations also deteriorated slightly, with a smaller share of respondents reporting that their households are expecting to be better off a year from now.

The percentage of respondents saying their current financial situation was worse than a year ago rose to 39%, the highest in two years.

Some more highlights from the report:

Median one-year-ahead earnings growth expectations remained unchanged at 2.6% in November.

Median nominal household spending growth expectations increased by 0.2 percentage point to 5.0%.

Perceptions of credit access compared to a year ago deteriorated, with the net share of respondents expecting it will be easier versus harder to obtain credit a year from now decreasing, while expectations for future credit availability were largely unchanged.

The average perceived probability of missing a minimum debt payment over the next three months increased by 0.6 percentage point to 13.7%, modestly above the trailing 12-month average of 13.3%.

The median expectation regarding a year-ahead change in taxes at current income level increased by 0.9 percentage point to 4.1%, the highest reading since June 2024. The increase was broad-based across age, education, and income groups.

Median year-ahead expected growth in government debt increased by 2.0 percentage points to 9.2%, the highest reading since July 2024.

The mean perceived probability that the average interest rate on saving accounts will be higher in 12 months decreased by 0.8 percentage point to 24.1%.

Perceptions about households’ current financial situations compared to a year ago deteriorated notably with a larger share of respondents reporting that their households were worse off compared to a year ago, and a smaller share reporting they were better off. Expectations about year-ahead financial situations also deteriorated slightly with a smaller share of respondents reporting that their households are expecting to be better off a year from now.

The mean perceived probability that U.S. stock prices will be higher 12 months from now decreased by 1.0 percentage point to 37.9%.

More in the full report.

Tyler Durden

Mon, 12/08/2025 – 13:00

Presidenta mexicana confía en que el Mundial generará un buen ambiente para la revisión del T-MEC

Associated Press

CIUDAD DE MÉXICO (AP) — La presidenta mexicana Claudia Sheinbaum se mostró el lunes confiada de que el Mundial de 2026 generará un “buen ambiente” para la revisión el próximo año del tratado comercial entre México, Estados Unidos y Canadá (el T-MEC).

Tras el primer encuentro cara a cara que sostuvo el viernes con el presidente Donald Trump en Washington en medio del sorteo de la conformación de los grupos del torneo, Sheinbaum destacó la cordialidad que predominó en la reunión, en la que también estuvo presente el primer ministro de Canadá, Mark Carney, e insistió en que el estadounidense “fue muy amable” con ella.

“Lo que se vio fue una buena relación entre los tres países”, dijo mandataria durante su conferencia matutina. Señaló — sin ofrecer detalles— que aunque no se avanzó mucho “fue muy importante” y añadió que “debemos de seguir trabajando”.

Al ser interrogada sobre si el Mundial que organizarán los tres países podría propiciar buenas condiciones para las negociaciones comerciales entre México y EEUU, que han sido muy tensas en los últimos meses tras los aranceles impuestos por Trump, la mandataria respondió que “sí, es un buen ambiente para revisión del tratado”. Recalcó además que el torneo mundialista “genera buenas condiciones” para la relación entre los tres gobiernos.

Aunque la presidenta mexicana se ha mostrado optimista sobre el futuro del T-MEC, Trump dejó entrever la semana pasada que podría no renovarlo y buscar otro acuerdo con México y Canadá. El estadounidense reiteró sus cuestionamientos contra el tratado trilateral y señaló que “México y Canadá se han aprovechado de Estados Unidos como casi todos los demás países”.

Como parte de sus políticas proteccionistas, Trump impuso en meses pasados un arancel de 25% a los bienes no cubiertos por el T-MEC y a los camiones medianos y pesados. También, acordó un gravamen de 50% al acero, el aluminio y el cobre, y una tarifa de 17% al tomate mexicano.

Desde hace meses Washington y México han mantenido negociaciones para tratar de aliviar los aranceles para el sector automotriz —que es una de las industrias claves del país latinoamericano y genera alrededor de 4,5% del producto interno bruto (PIB)— el acero, el aluminio y el cobre.

Dr. Oz Threatens To Pull Funding From Minnesota After $1 Billion In Medicaid Funding Was Stolen by Fraudsters

Dr. Oz Threatens To Pull Funding From Minnesota After $1 Billion In Medicaid Funding Was Stolen by Fraudsters

Authored by Jacki Thrapp via The Epoch Times,

The Centers for Medicare & Medicaid Services (CMS) threatened to withhold federal funding from Minnesota after fraudsters allegedly stole more than $1 billion set aside for Medicaid programs.

CMS administrator Dr. Mehmet Oz ordered Minnesota Gov. Tim Walz to follow a series of guidelines that crack down on the fraud and said that if the state does not comply, it will lose federal money.

“Either fix this in 60 days or start looking under your couch for spare change because we are done footing the bill for your incompetence,” Oz announced on Dec. 5.

CMS will require Minnesota officials to provide weekly updates for six months on the actions it is taking to stop fraud and to freeze enrollment of high-risk providers.

The Minnesota Department of Human Services was also ordered to create a corrective action plan outlining how it will prevent fraud going forward. Oz wants this plan submitted by the end of December.

“Our staff at CMS told me they’ve never seen anything like this in Medicaid—and everyone from Gov. Tim Walz on down needs to be investigated, because they’ve been asleep at the wheel,” Oz wrote in a X post on Dec. 5.

The Epoch Times reached out to Walz’s team for comment but did not hear back by publication time.

The CMS administrator blamed “bad actors” in Minnesota’s Somali community for being part of the fraudulent activity.

There are nearly 80,000 Somalis living in the state, with the majority of them in the Minneapolis–Saint Paul Twin Cities region, according to Minnesota Compass.

Oz specifically alleged fraudsters targeted a housing program that was designed to help disabled homeless people and a program that reimbursed therapy costs for families who have children with autism.

“The housing program was supposed to cost $2.6 million annually,” Oz said.

“Last year, it paid out over $100 million. The autism program ballooned from $3 million in 2018 to nearly $400 million in 2023. These scammers used stolen taxpayer money to buy flashy cars, purchase overseas real estate, and offer kickbacks to parents who enrolled their kids at fake autism treatment centers. Some of it may have even made its way to the Somalian terrorist group Al-Shebab.”

Rep. Ilhan Omar (D-Minn.) was asked about allegations that the stolen funds could be linked to terrorism during an appearance on CBS News’s “Face the Nation” on Dec. 7.

“If there was a linkage in that, the money that they had stolen going to terrorism, then that is a failure of the FBI and our court system in not figuring that out and basically charging them … with these charges,” Omar said.

“And so I do know that for many years, this sort of like alarm that there is money being transferred through the airport in bags and going to terrorism has all—that accusation has always existed. There has never been here and there in those accusations. But if that is the case, if money from U.S. tax dollars is being sent to help with terrorism in Somalia, we want to know, and we want those people prosecuted, and we want to make sure that that doesn’t ever happen again.”

Immigration and Customs Enforcement announced plans to ramp up activities in the Twin Cities region after President Donald Trump rescinded temporary protected status for Somali immigrants living in the state.

Minneapolis Mayor Jacob Frey dismissed the Trump administration’s immigration efforts and accused it of spending too much time “terrorizing certain groups within our community.”

Tyler Durden

Mon, 12/08/2025 – 12:40

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}